Making it in America: Outlook for manufacturing and automation in the United States CONFIDENTIAL AND PROPRIETARY Any use of this material without specific permission of McKinsey & Company is strictly prohibited January 2018 Rated #1 Think Tank 2016 (private sector category) by the Global Think Tank Index, University of Pennsylvania

Transcript

Making it in America:Outlook for manufacturing and automation in the United States

CONFIDENTIAL AND PROPRIETARYAny use of this material without specific permission of McKinsey & Company is strictly prohibited

January 2018

Rated #1 Think Tank 2016 (private sector category) by the Global Think Tank Index, University of Pennsylvania

2McKinsey & Company

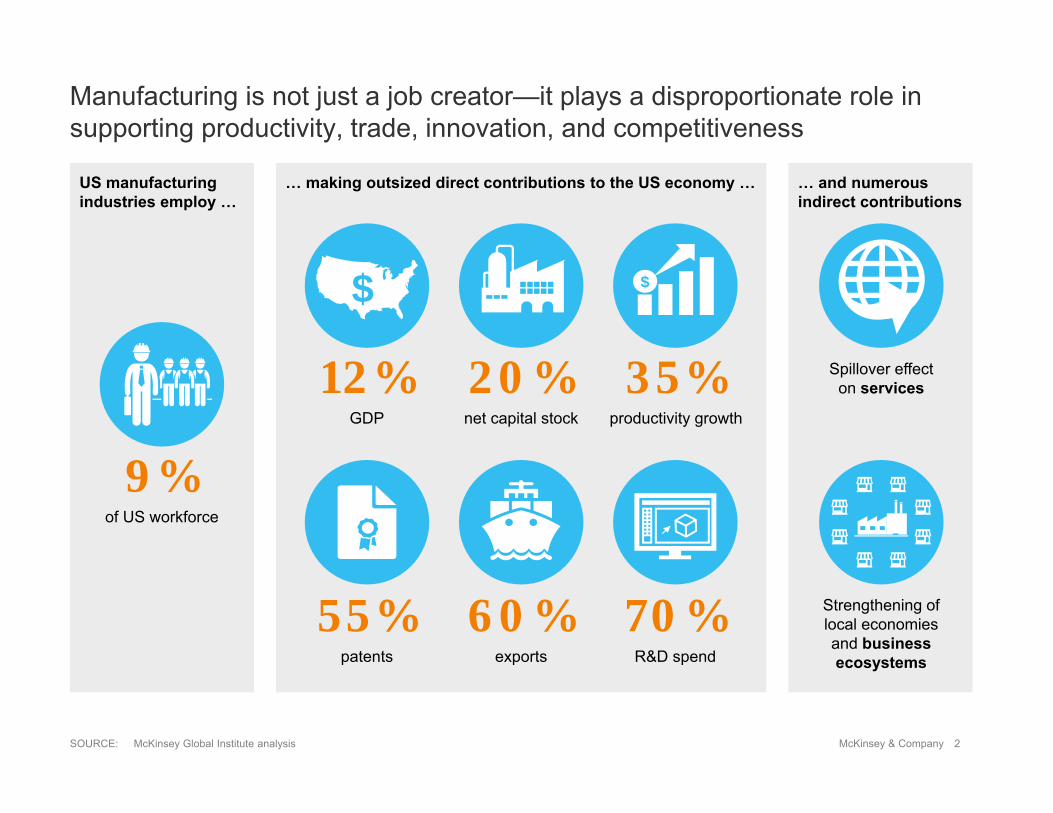

… and numerous indirect contributions

US manufacturing industries employ …

… making outsized direct contributions to the US economy …

Manufacturing is not just a job creator—it plays a disproportionate role in supporting productivity, trade, innovation, and competitiveness

SOURCE: McKinsey Global Institute analysis

55%patents

60%exports

70%R&D spend

9%of US workforce

Spillover effect on services

Strengthening of local economies and business ecosystems

35%productivity growth

$

20%net capital stock

12%GDP

$

3McKinsey & Company

180

100

120

0

160

140

260

240

220

200

Total US manufacturing

10

Total manufacturing less computers,pharmaceuticals, and medical devices

05 201695 2000901980 85

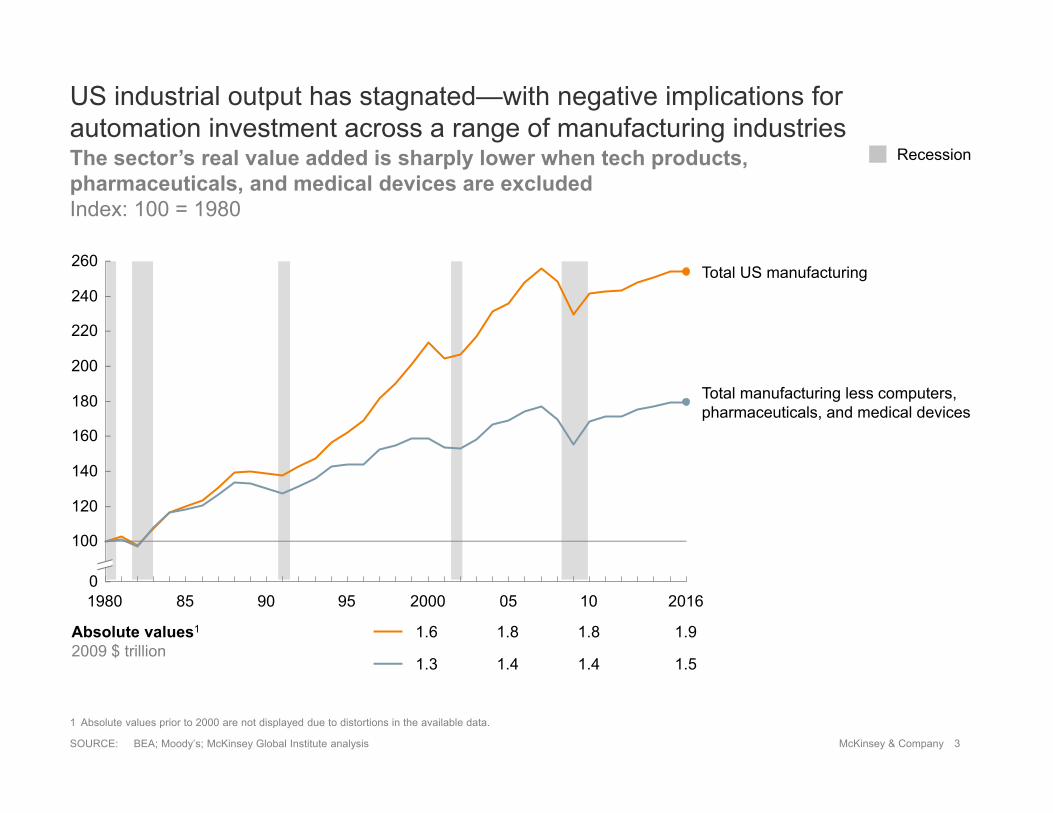

The sector’s real value added is sharply lower when tech products, pharmaceuticals, and medical devices are excludedIndex: 100 = 1980

SOURCE: BEA; Moody’s; McKinsey Global Institute analysis

1 Absolute values prior to 2000 are not displayed due to distortions in the available data.

US industrial output has stagnated—with negative implications for automation investment across a range of manufacturing industries

Recession

Absolute values1

2009 $ trillion1.6 1.8 1.8 1.9

1.3 1.4 1.4 1.5

4McKinsey & CompanySOURCE: US Census Bureau; BEA; McKinsey Global Institute analysis

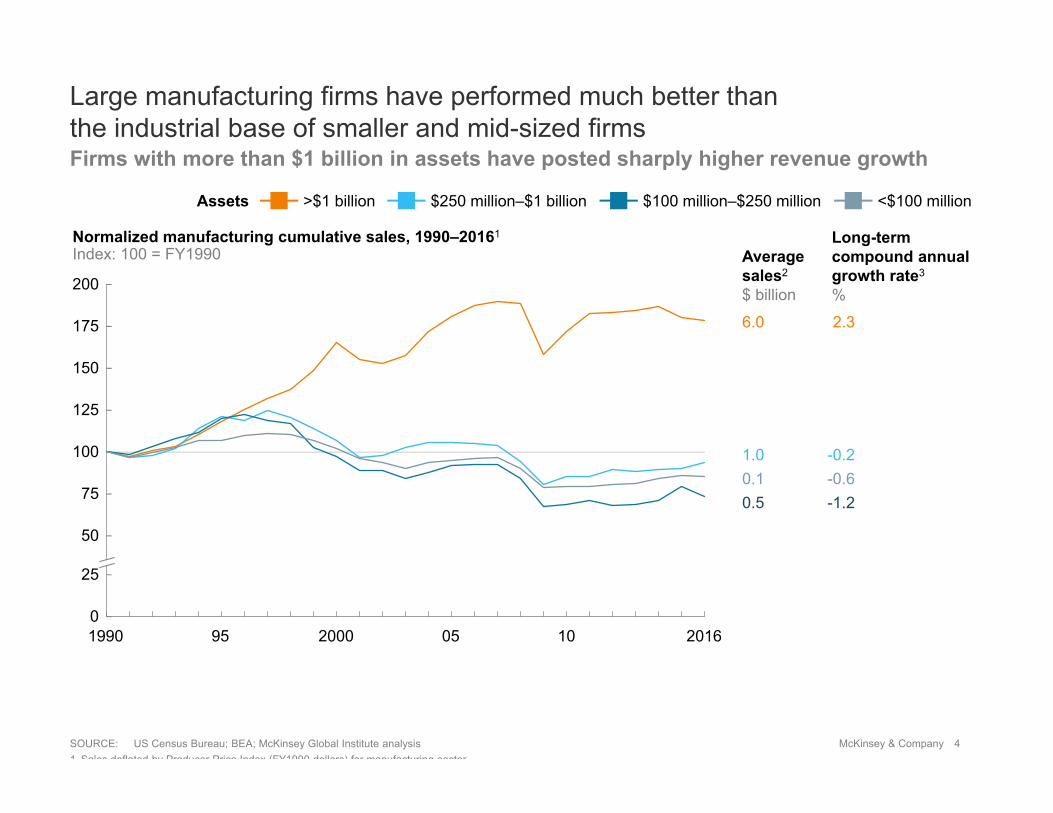

Large manufacturing firms have performed much better than the industrial base of smaller and mid-sized firms

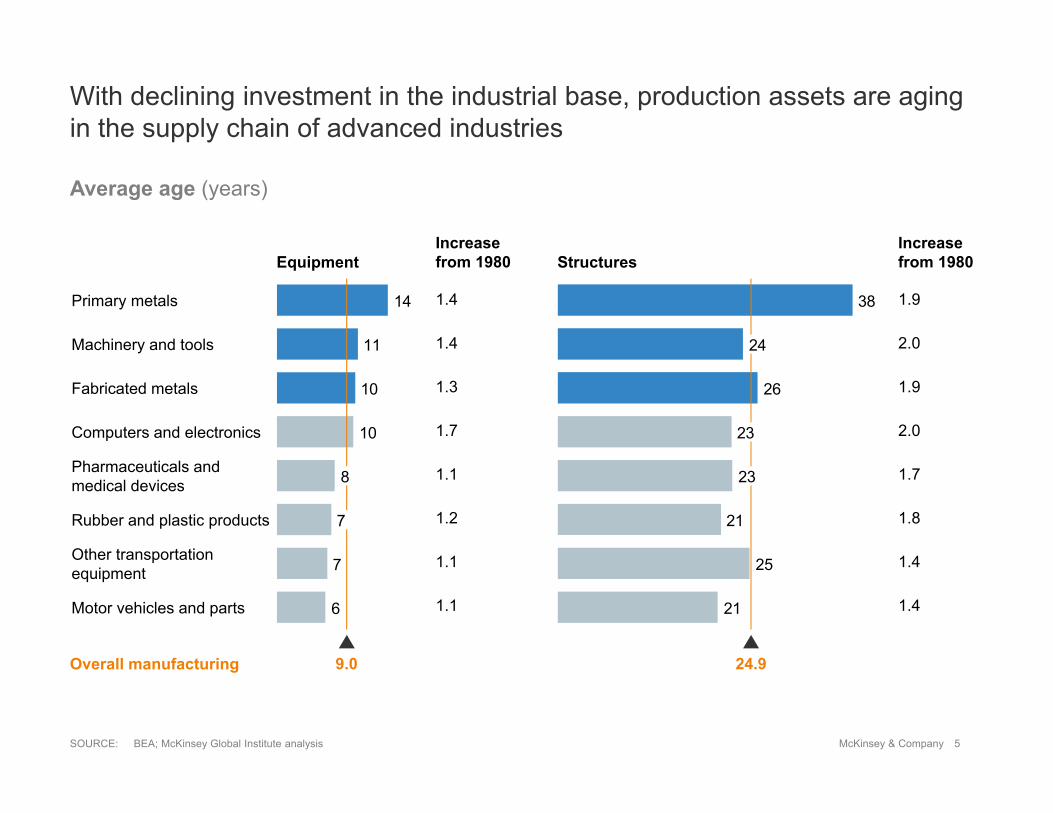

With declining investment in the industrial base, production assets are aging in the supply chain of advanced industries

2.0

1.7

1.9

1.9

2.0

1.8

1.4

1.4

1.7

1.2

1.3

1.4

1.1

1.1

1.1

Overall manufacturing

Equipment StructuresIncrease from 1980

Increase from 1980

1.4

SOURCE: BEA; McKinsey Global Institute analysis

6McKinsey & Company

0

160

14

60

2016

140

120

240

220

200

180

100

08069692

80

1094 02 1204981990 2000

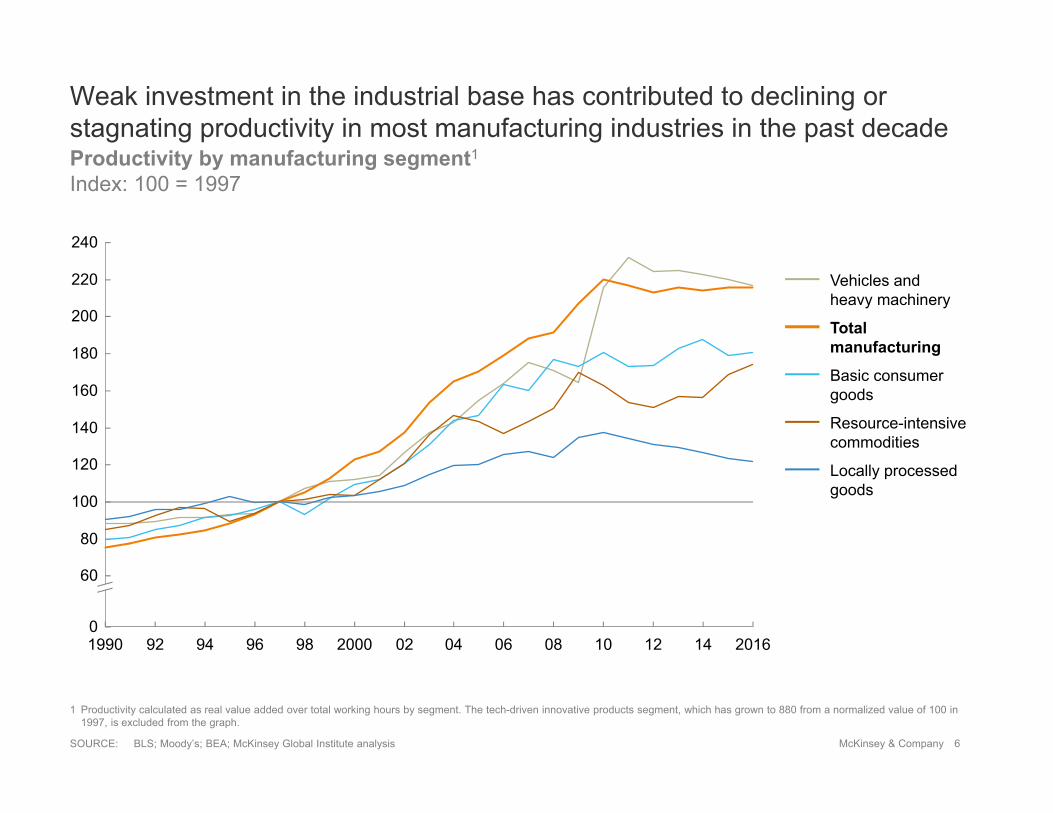

Weak investment in the industrial base has contributed to declining or stagnating productivity in most manufacturing industries in the past decade

Basic consumergoods

Totalmanufacturing

Resource-intensivecommodities

Vehicles andheavy machinery

Locally processedgoods

Productivity by manufacturing segment1

Index: 100 = 1997

1 Productivity calculated as real value added over total working hours by segment. The tech-driven innovative products segment, which has grown to 880 from a normalized value of 100 in 1997, is excluded from the graph.

SOURCE: BLS; Moody’s; BEA; McKinsey Global Institute analysis

7McKinsey & Company

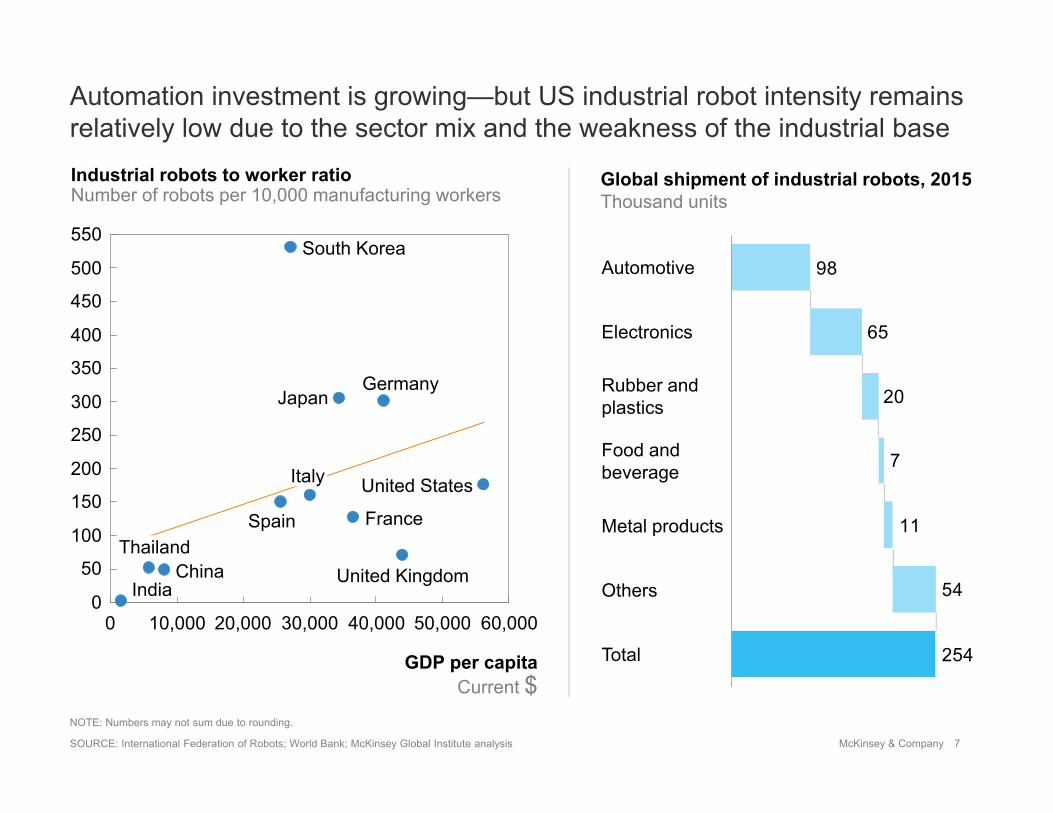

Automation investment is growing—but US industrial robot intensity remains relatively low due to the sector mix and the weakness of the industrial base

254

54

11

7

20

65

98Automotive

Total

Others

Metal products

Food andbeverage

Electronics

Rubber andplastics

SOURCE: International Federation of Robots; World Bank; McKinsey Global Institute analysis

0

300

550

450

500

350

200

400

50

60,00050,000

100

150

250

30,0000

20,000 40,00010,000

United States

India

France

United Kingdom

South Korea

GDP per capitaCurrent $

Italy

ThailandSpain

Industrial robots to worker ratioNumber of robots per 10,000 manufacturing workers

GermanyJapan

China

Global shipment of industrial robots, 2015Thousand units

NOTE: Numbers may not sum due to rounding.

8McKinsey & Company

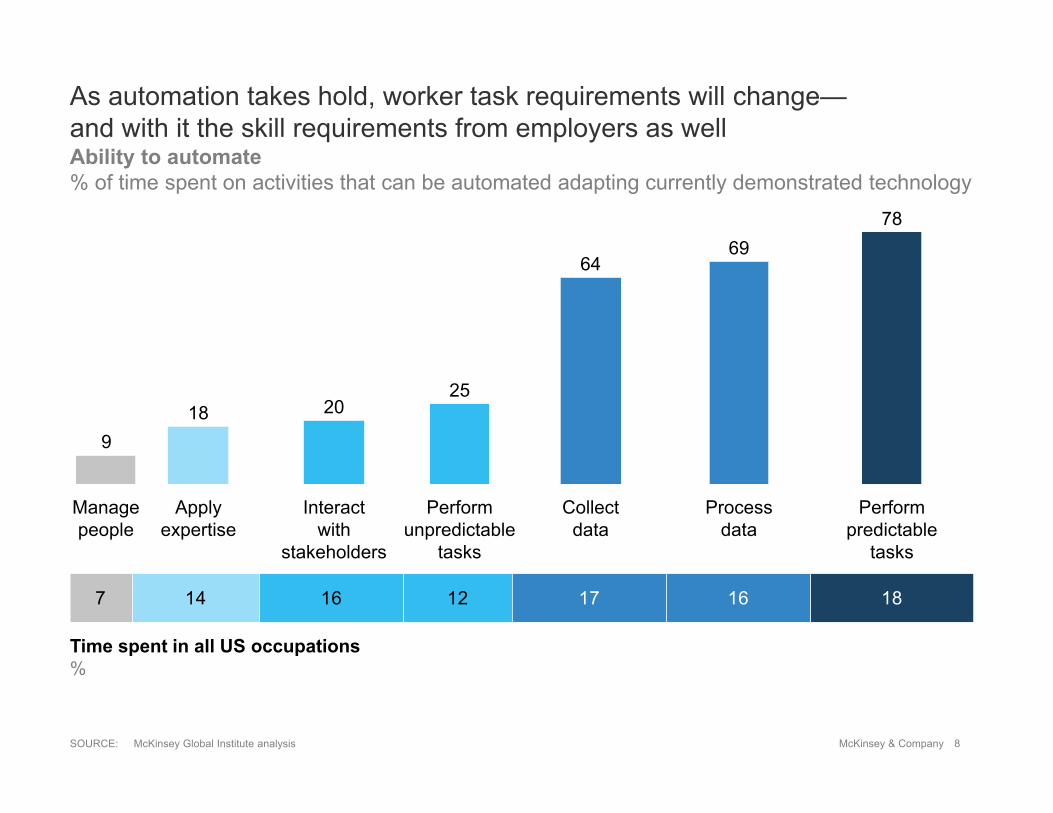

As automation takes hold, worker task requirements will change—and with it the skill requirements from employers as well

7 14 16 12 17 16 18

Perform predictable

tasks

78

Time spent in all US occupations %

SOURCE: McKinsey Global Institute analysis

9

Manage people

18

Apply expertise

Interactwith

stakeholders

2025

Perform unpredictable

tasks

64

Collectdata

69

Processdata

Ability to automate % of time spent on activities that can be automated adapting currently demonstrated technology

9McKinsey & Company

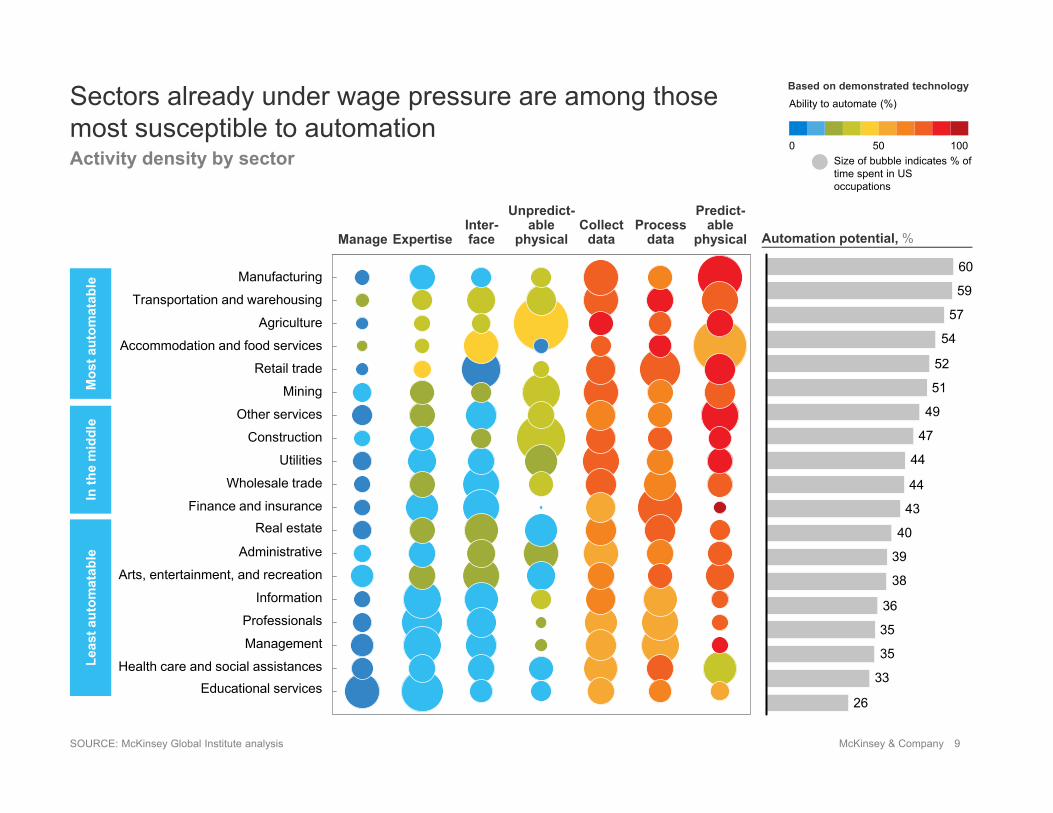

Agriculture

Transportation and warehousing

Retail trade

Accommodation and food services

Manufacturing

Mining

Construction

Utilities

Wholesale trade

Other services

Finance and insurance

Administrative

Health care and social assistances

Information

Professionals

Management

Arts, entertainment, and recreation

Real estate

Educational services

Size of bubble indicates % of time spent in US occupations

Mos

t aut

omat

able

Leas

t aut

omat

able

In th

e m

iddl

eBased on demonstrated technology

Automation potential, %Collect

data

Predict-able

physicalProcess

data

Unpredict-able

physicalInter-faceExpertiseManage

26

33

35

35

36

38

39

40

43

44

44

47

49

51

52

54

57

59

60

Sectors already under wage pressure are among thosemost susceptible to automationActivity density by sector

0 50 100

Ability to automate (%)

SOURCE: McKinsey Global Institute analysis

10McKinsey & Company

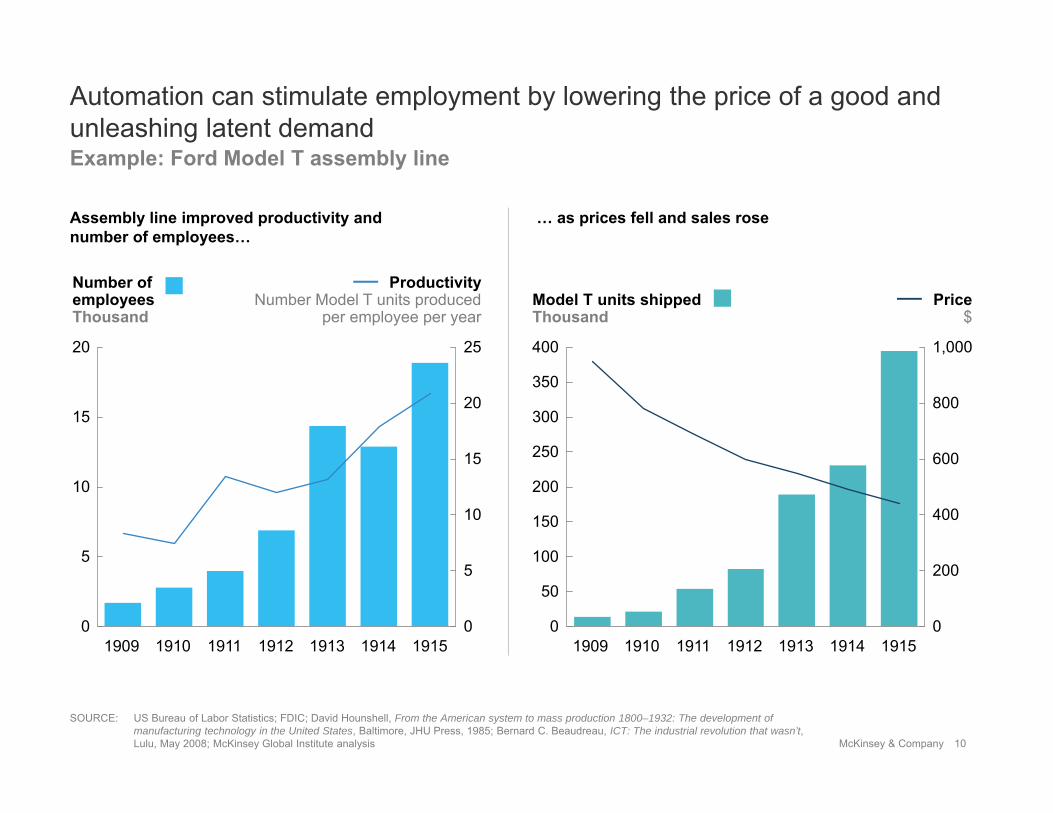

Example: Ford Model T assembly line

50

150

250

350

200

0

400

100

300

0

600

1,000

800

400

200

Model T units shippedThousand

1914 191519111910 1912 19131909

Price$

25

10

20

5

15

20

15

0

5

0

10

ProductivityNumber Model T units produced

per employee per year

1909 19111910 1912

Number of employeesThousand

19141913 1915

Automation can stimulate employment by lowering the price of a good and unleashing latent demand

Assembly line improved productivity and number of employees…

… as prices fell and sales rose

SOURCE: US Bureau of Labor Statistics; FDIC; David Hounshell, From the American system to mass production 1800–1932: The development of manufacturing technology in the United States, Baltimore, JHU Press, 1985; Bernard C. Beaudreau, ICT: The industrial revolution that wasn’t, Lulu, May 2008; McKinsey Global Institute analysis

11McKinsey & Company

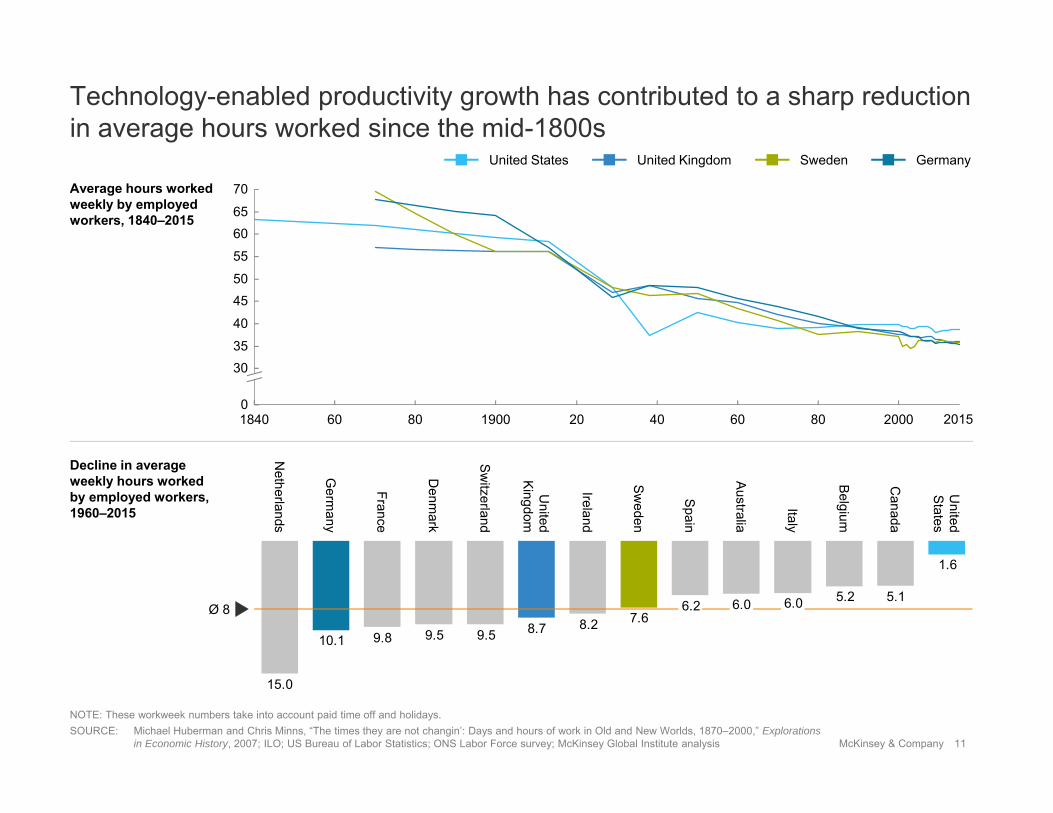

20

40

801840 1900 60

70

80

65

5055

45

60

2000

35

0

30

60 40

Average hours worked weekly by employed workers, 1840–2015

1.6

5.15.26.06.06.27.68.28.79.59.59.810.1

15.0

United

Kingdom

Netherlands

Denm

ark

France

Germ

any

Switzerland

Canada

Ireland

United

States

Australia

Spain

Ø 8

Belgium

Italy

Sweden

Decline in average weekly hours worked by employed workers, 1960–2015

Technology-enabled productivity growth has contributed to a sharp reduction in average hours worked since the mid-1800s

2015

United States United Kingdom Sweden Germany

NOTE: These workweek numbers take into account paid time off and holidays.SOURCE: Michael Huberman and Chris Minns, “The times they are not changin’: Days and hours of work in Old and New Worlds, 1870–2000,” Explorations

in Economic History, 2007; ILO; US Bureau of Labor Statistics; ONS Labor Force survey; McKinsey Global Institute analysis

12McKinsey & Company

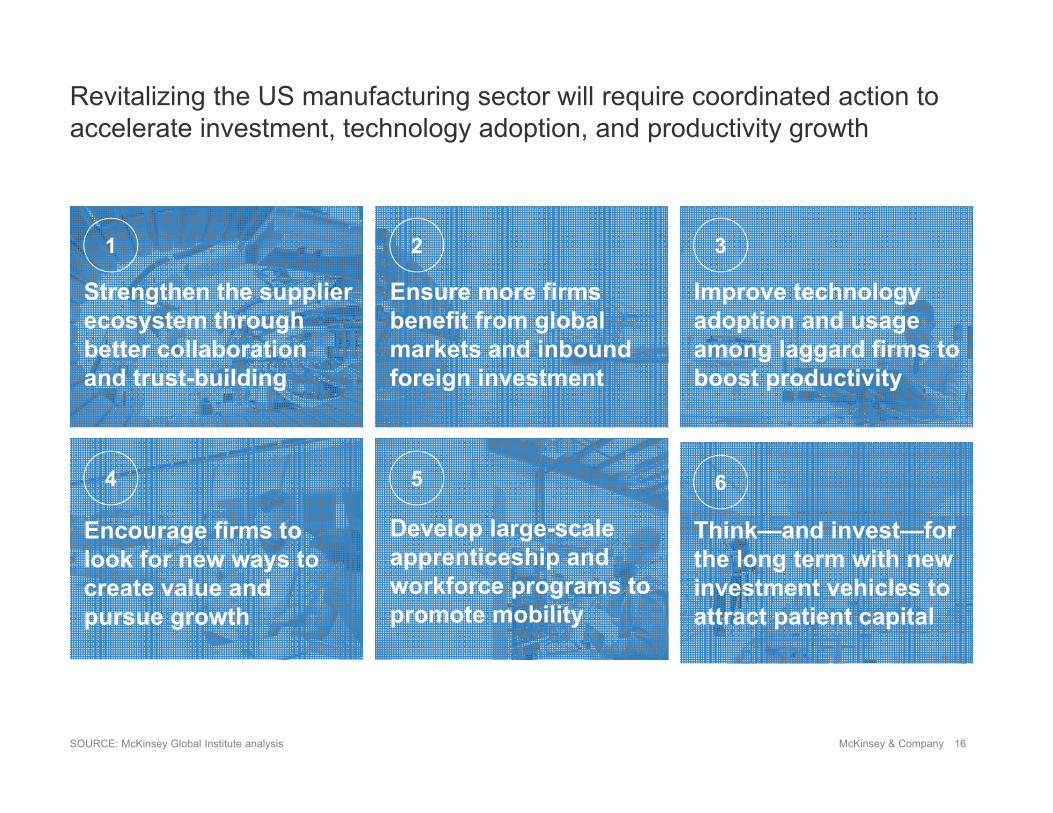

Closing thoughts:Implications for the industry

Accelerating investmentMatching companies with long-term capital for plant upgrades and automation investments

Translating investment to productivityHelping firms identify the business cases and workflow changes to benefit from automation

Building skills in the workforceMaking worker training more responsive and portable across firm and industry boundaries

Getting ahead of societal changeHelping prepare communities for the impact on job creation and income growth

Download MGI research atwww.mckinsey.com/

@McKinsey_MGI

McKinseyGlobalInstitute

@SreeRamaswamy

14McKinsey & Company

The transition needs to be actively managed—worker dislocation, income concentration, regional divergences can weaken the economic growth cycle

Increases through productivity and employment

Economic growth

Distributed as wages, profits, and taxes (or lower prices)

Consumption and investment by private, public, and inbound foreign spenders

SOURCE: McKinsey Global Institute

15McKinsey & Company

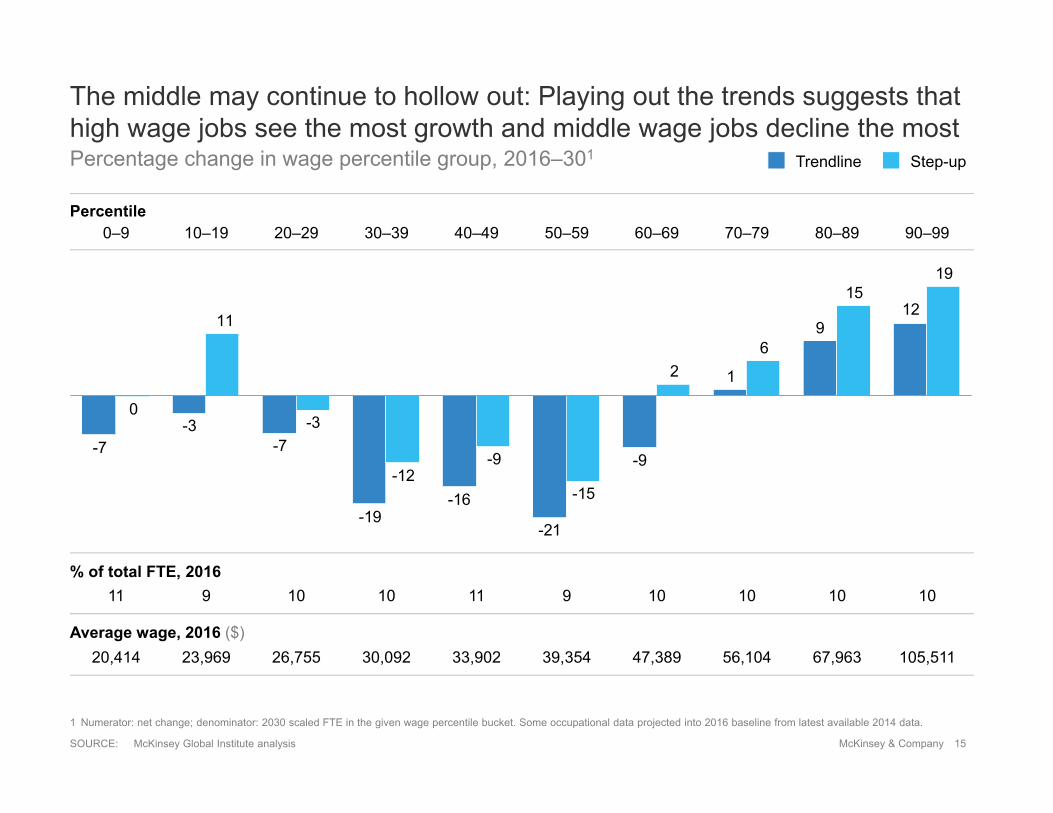

129

1

-9

-21

-16-19

-7-3

-7

1915

62

-15

-9-12

-3

11

0

Percentage change in wage percentile group, 2016–301

The middle may continue to hollow out: Playing out the trends suggests that high wage jobs see the most growth and middle wage jobs decline the most

1 Numerator: net change; denominator: 2030 scaled FTE in the given wage percentile bucket. Some occupational data projected into 2016 baseline from latest available 2014 data.