29

| Date post: | 21-Jan-2018 |

| Category: |

Business |

| Upload: | veda-advantage |

| View: | 284 times |

| Download: | 0 times |

Market Trends

Key indicators and trends from the past 6 months

August 2010

3

Market trend summary from Feb 2010 seminar:

Market Trends

Credit Demand is slowly recovering.

Consumer confidence is at its’ highest level for two years.

Economists generally agree that the Australian Economy is

well on the way to a speedy recovery.

So how has the outlook changed?

-3

-2

-1

0

1

2

3

Stan

dar

dis

ed

Ind

ex

Credit Card Demand Personal Loan Demand Mortgage Demand

4

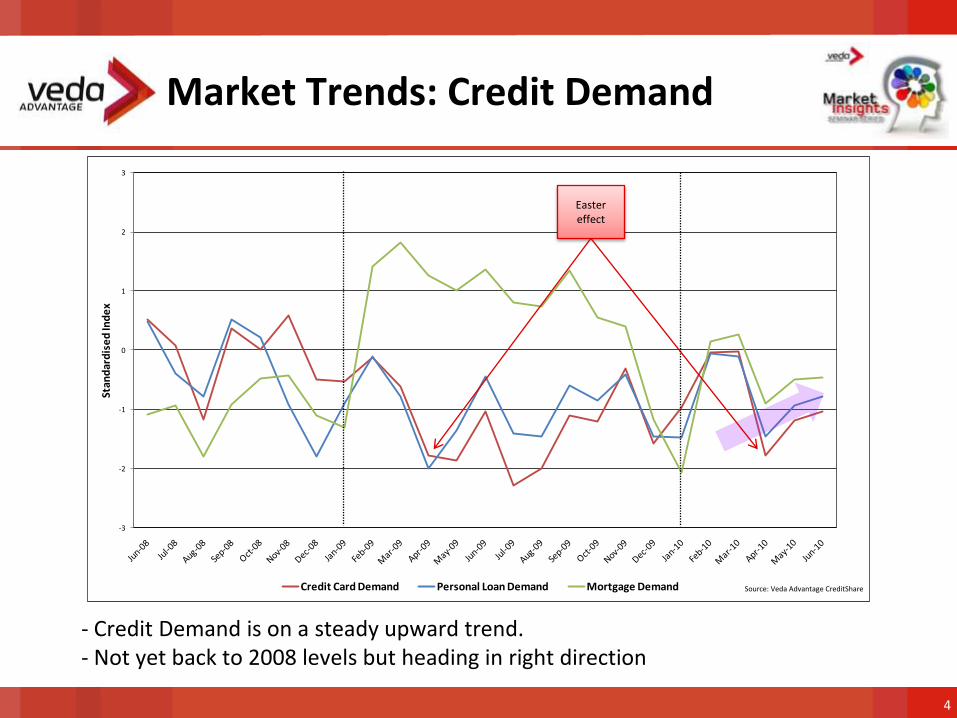

Market Trends: Credit Demand

- Credit Demand is on a steady upward trend. - Not yet back to 2008 levels but heading in right direction

Source: Veda Advantage CreditShare

Easter effect

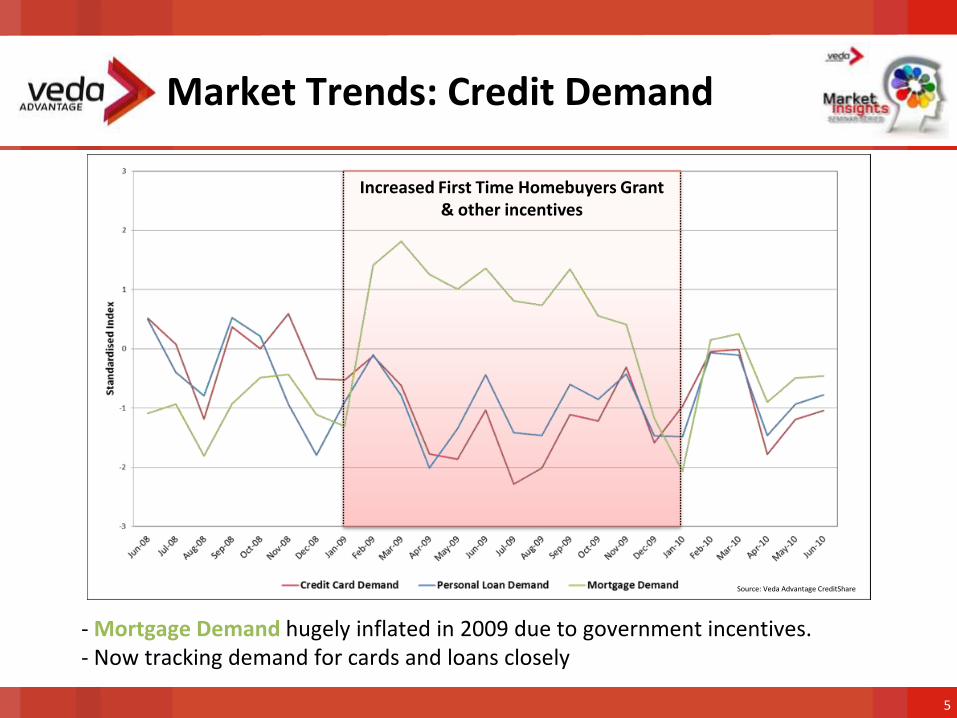

Increased First Time Homebuyers Grant & other incentives

5

Market Trends: Credit Demand

- Mortgage Demand hugely inflated in 2009 due to government incentives.- Now tracking demand for cards and loans closely

Source: Veda Advantage CreditShare

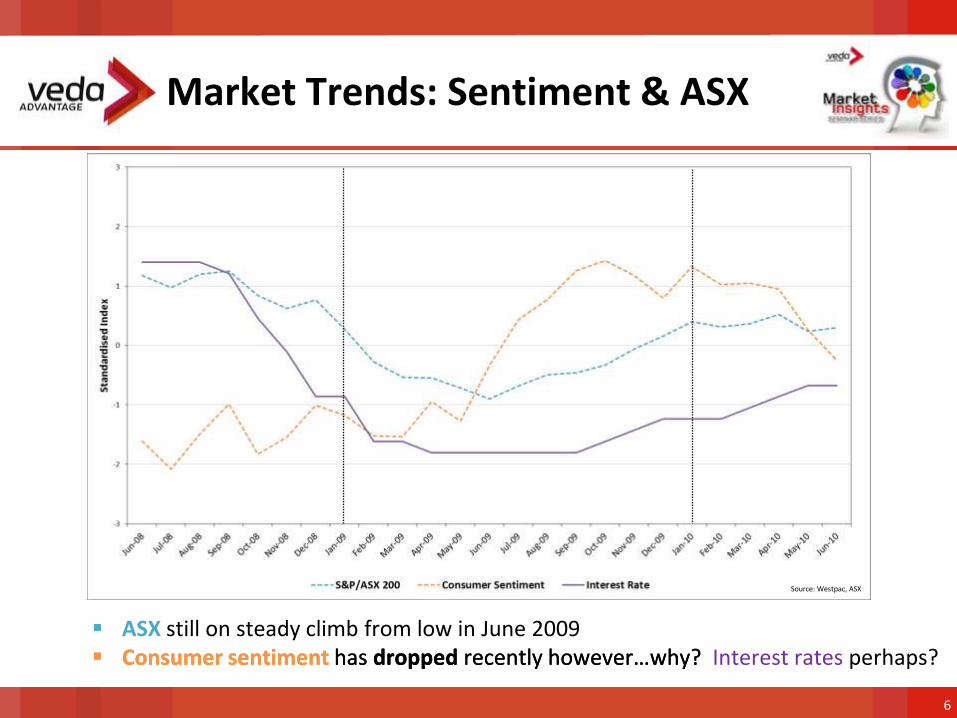

Consumer sentiment has dropped recently however…why? Interest rates perhaps?

6

Market Trends: Sentiment & ASX

ASX still on steady climb from low in June 2009 Consumer sentiment has dropped recently however…why?

Source: Westpac, ASX

7

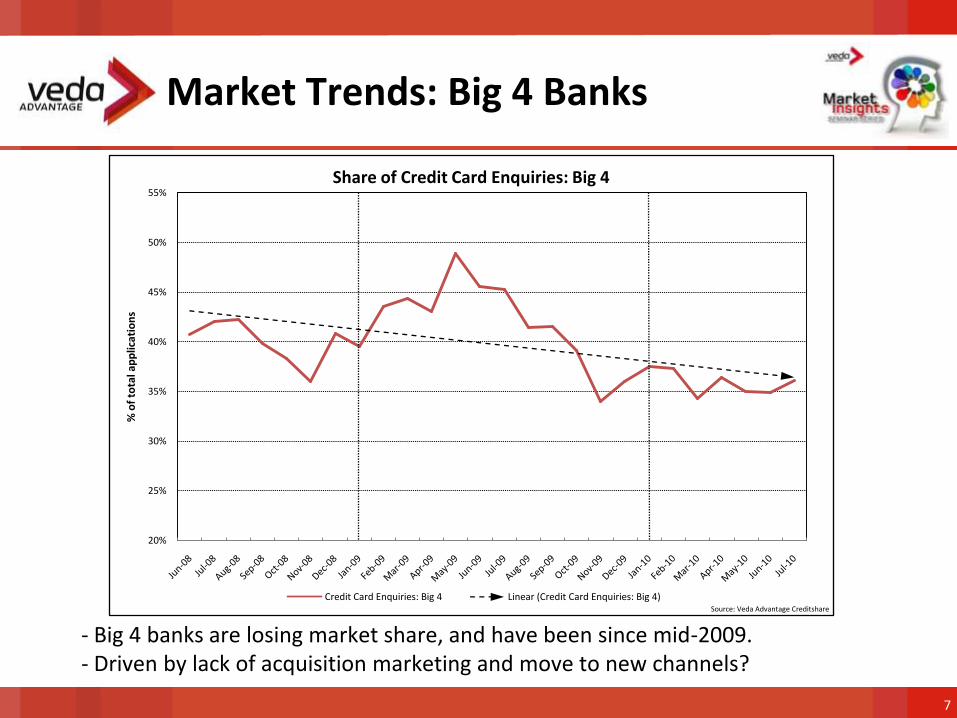

Market Trends: Big 4 Banks

- Big 4 banks are losing market share, and have been since mid-2009.- Driven by lack of acquisition marketing and move to new channels?

Source: Veda Advantage Creditshare

20%

25%

30%

35%

40%

45%

50%

55%

% o

f to

tal a

pp

licat

ion

s

Share of Credit Card Enquiries: Big 4

Credit Card Enquiries: Big 4 Linear (Credit Card Enquiries: Big 4)

8

Market Trends: Big 4 Banks

Source: Veda Advantage Creditshare

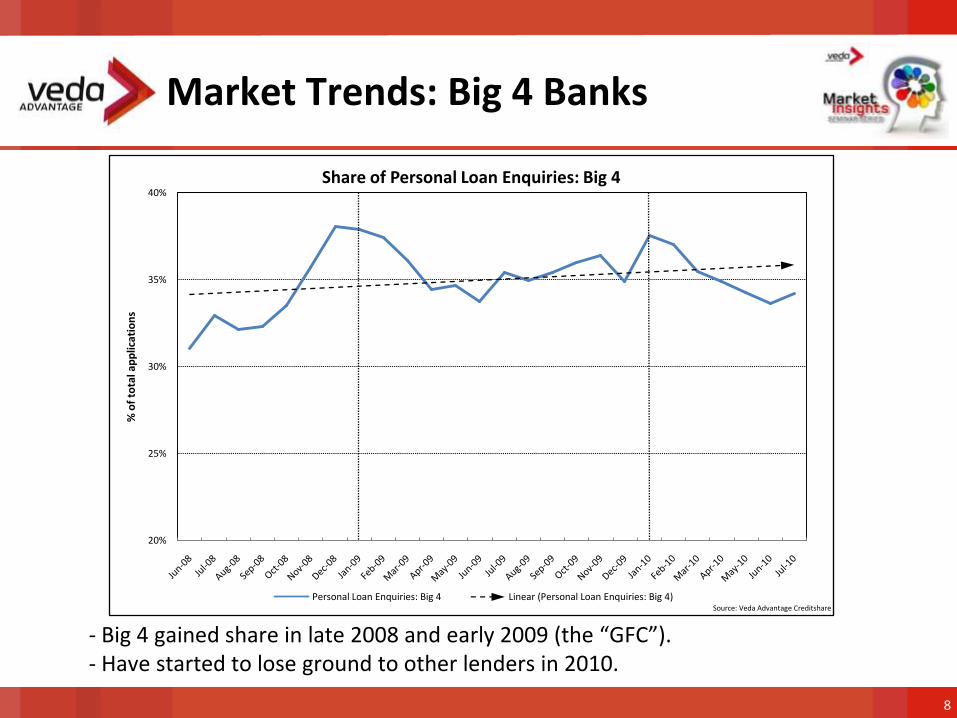

- Big 4 gained share in late 2008 and early 2009 (the “GFC”).- Have started to lose ground to other lenders in 2010.

20%

25%

30%

35%

40%

% o

f to

tal a

pp

licat

ion

s

Share of Personal Loan Enquiries: Big 4

Personal Loan Enquiries: Big 4 Linear (Personal Loan Enquiries: Big 4)

9

Market Trends: Big 4 Banks

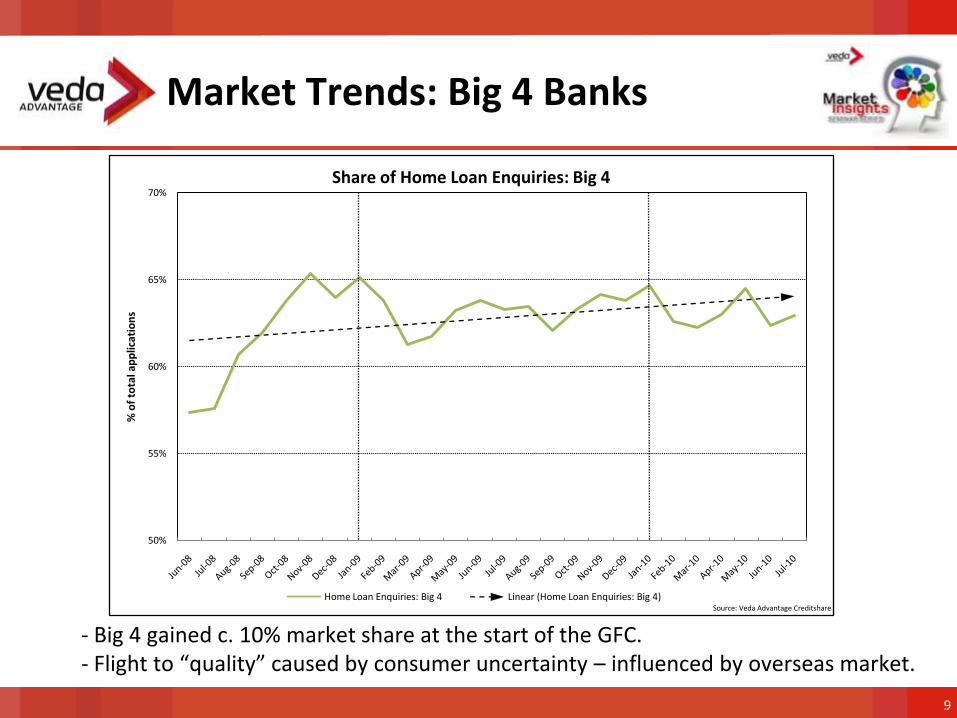

- Big 4 gained c. 10% market share at the start of the GFC.- Flight to “quality” caused by consumer uncertainty – influenced by overseas market.

Source: Veda Advantage Creditshare

50%

55%

60%

65%

70%

% o

f to

tal a

pp

licat

ion

s

Share of Home Loan Enquiries: Big 4

Home Loan Enquiries: Big 4 Linear (Home Loan Enquiries: Big 4)

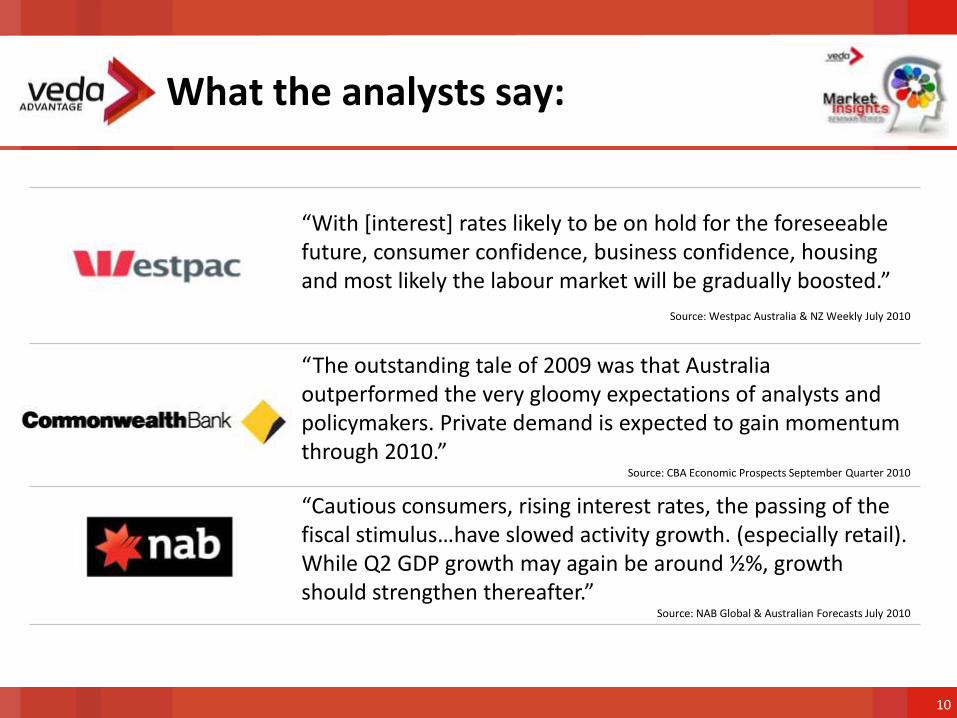

“With *interest+ rates likely to be on hold for the foreseeable future, consumer confidence, business confidence, housing and most likely the labour market will be gradually boosted.”

Source: Westpac Australia & NZ Weekly July 2010

“The outstanding tale of 2009 was that Australia outperformed the very gloomy expectations of analysts and policymakers. Private demand is expected to gain momentum through 2010.”

Source: CBA Economic Prospects September Quarter 2010

“Cautious consumers, rising interest rates, the passing of the fiscal stimulus…have slowed activity growth. (especially retail). While Q2 GDP growth may again be around ½%, growth should strengthen thereafter.”

Source: NAB Global & Australian Forecasts July 2010

What the analysts say:

10

11

Market Trends: Conclusions

Credit Demand is still recovering.

Mortgage demand is back to normal levels after

government incentives lapsed.

Interest rates seem to be affecting consumer confidence.

Big 4 banks have lost ground to other lenders in the credit

card market.

Economists generally agree that the Australian economy is

still on the way to recovery.

Questions?

Centralised Data Solutions

How to make them work in a marketing environment.

August 2010

Introduction

Many organisations are in the process of, or have already

established a single source of truth that can be leveraged by

their marketing teams

Agenda

The principles of a marketing data mart

The benefits

How to move forwards

Summary

Data Based Marketing

Problems traditionally faced by marketers

Limited customer understanding

Inability to communicate effectively

Expensive/ difficult to test ideas

Need to be ‘first’ in the market

Measuring/ demonstrating effectiveness

Marketing Data Marts

Data marts – the principle

Customer base ‘snapshot’

Typified by the term ‘Single Customer View’

Provide greater control

Remove reliance from IT

Provide greater understanding

Increase marketing effectiveness

Marketing Data Marts

Data marts – the barriers

Organic data growth

Limited IT resource

Cost (upfront)

Technical know how

Slow Implementation

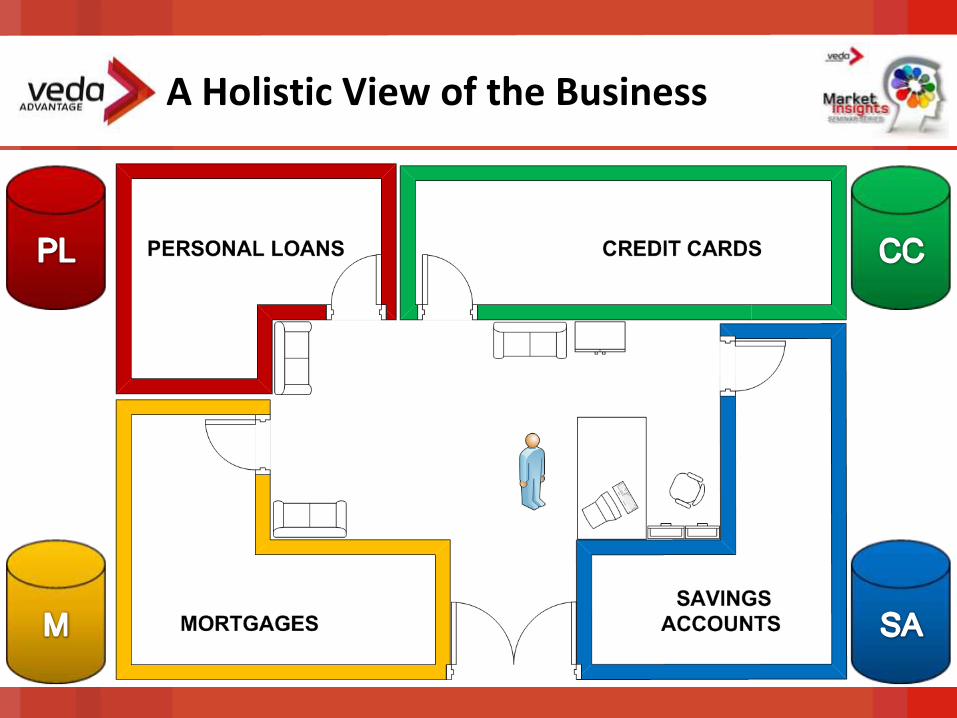

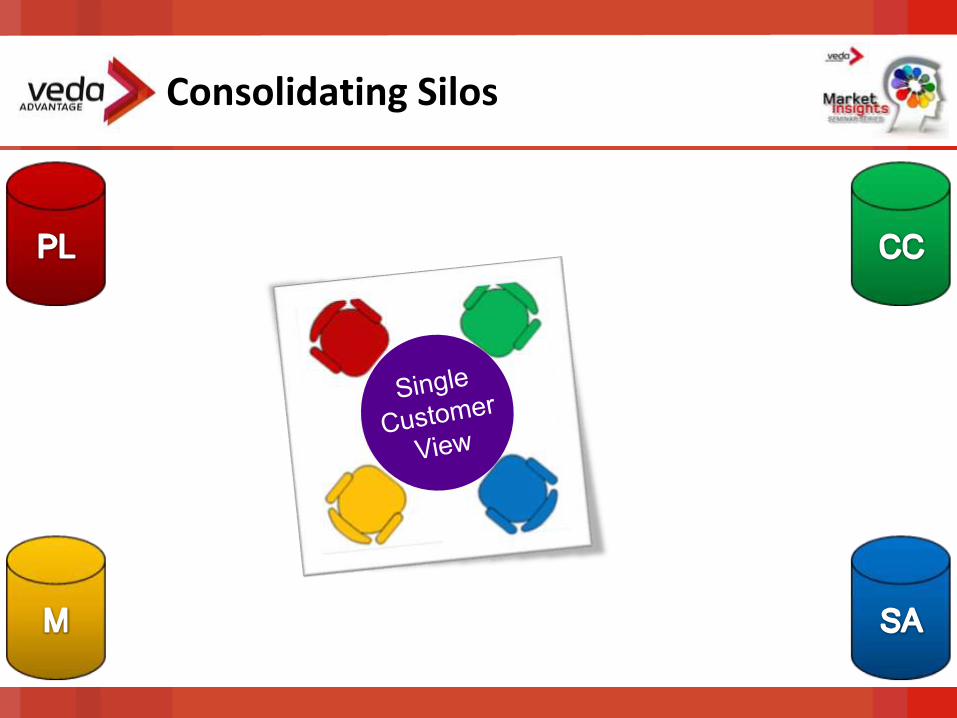

A Holistic View of the Business

Consolidating Silos

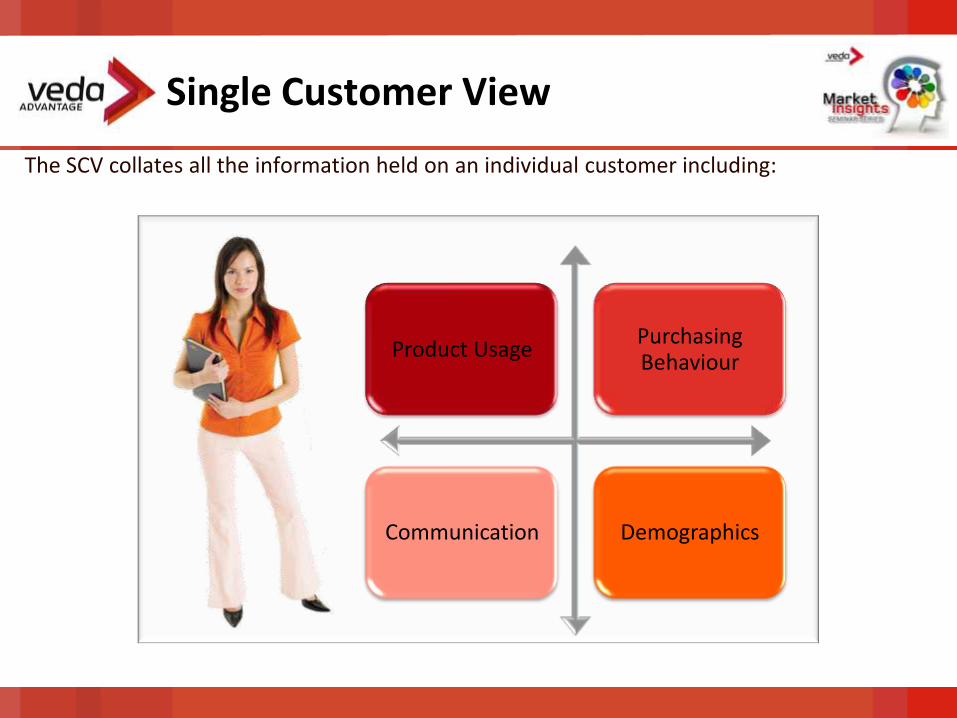

The SCV collates all the information held on an individual customer including:

Product UsagePurchasing Behaviour

Communication Demographics

Single Customer View

Ideally it also provides a more

comprehensive environment

by including generic

information for the whole

population.

Extended View

In addition to the more traditional individual level, an additional benefit to the

SCV is the ability to understand behavioural patterns at a family and household

unit level.

Family / HouseholdHouseholdIndividual

The Customer Hierarchy

The Benefits

Customer understanding

Benchmarking (internal & external)

Improves data quality

Test platform for impact analysis

Strategic planning

Speed to market

Platform for on-line marketing

Moving Forwards

Technology has advanced to allow more data to be stored

and processed cheaper and more effectively

Software has advanced and been adapted to better fit the

marketers requirements

Data has become cheaper and more readily accessible

In recent years the technical and data landscape has changed

considerably

Moving Forwards

Example ‘Affordable’ Systems

How to move forwards

In-House vs. Outsource

Greater control

Develop know how

Cost effective?

IT impact?

Speed to market

Leverage expert

knowledge

Access ‘market’ data

Cost effective (incl. no

head count & CAPEX)

Summary

The environment is different from the ‘90’s when 1 to 1

marketing was the word – it’s now a reality

Operational data marts are extremely beneficial for

effective one-line marketing

Many organisations are embracing this approach

The world has changed:

August 2010

Questions