60

| Date post: | 04-Jun-2018 |

| Category: |

Documents |

| Upload: | nguyentram |

| View: | 217 times |

| Download: | 0 times |

- _mM© 2017- _mM© 20172 33

Editorial

Power is one of the most critical components of

infrastructure very essential for the economic growth

envisaged by us in the days to come. The existence and

development of adequate infrastructure including Energy is

essential for sustained growth of the Indian economy.

India's Energy Sector is currently dependent more on

conventional sources such as coal, natural gas, oil, hydro and

on non-conventional sources such as wind, solar, and

agricultural waste to a lesser extent. Energy demand in the country has increased rapidly and is expected to rise

further in the years to come. In order to meet the increasing demand for energy in the country, massive addition

to the installed generating capacity is required, be it conventional or non conventional. Considering the depleting

sources of coal , oil, and even water as also the increasing cost of these sources, non conventional or renewable

energy indeed appears to be only prudent choice. We are fortunate to have natural resources such as sunlight,

wind, and bio mass in abundance which produce Renewable energy. Such energy would be very cost effective and

would make our industry more competitive. Hence the Government of India is promoting use of Renewable

Energy on a large scale .The solar energy mission of the Government of India is indeed a right initiative at the right

time. India ranks third among 40 countries in EY's Renewable Energy Country Attractiveness Index, on back of

strong focus by the Government on promoting renewable energy and implementation of projects in a time

bound manner. India's wind energy market is expected to attract investments totaling Rs 1,00,000 crore by 2020,

and wind power capacity is estimated to almost double by 2020 from over 23,000 MW in June 2015, with an

addition of about 4,000 MW per annum in the next five years. The investment scenario in the Renewable Energy

segment is looking very attractive. It has been reported that around 293 global and domestic companies have

committed to generate 266 GW of solar, wind, mini-hydel and biomass-based power in India over the next 5–10

years. This would amount to an investment of about Rs. 22 lakh crores. In the last week of February, Government

of India announced an ambitious scheme to double solar power generation capacity under the solar park scheme

to 40000 megawatts by 2020. The Government has also created a separate funding of about Rs. 8100 crores to

part finance these initiatives. We know that the nation has set a target of 100 GW of solar power by 2022. The

Government, Industry, and all of us have to work to achieve this target .

We at MCCIA are fully committed to promote the Government Policy for harnessing the Renewable Energy

and that commitment made us to take many initiatives in this rapidly developing segment of renewable energy. rd thOur National Conference on Renewable Energy held on 23 and 24 of February was one of them . We have made

it our Annual feature and the one held recently was the second in series which attracted substantial interest and

participation. A detailed report on the same appears in this March issue of Sampada. Do read it and let us know

your feedback . Happy Reading and Happy Holi too.

Dr. Anant SardeshmukhDirector General & Editor, Sampada

- _mM© 2017- _mM© 20172 33

Editorial

Power is one of the most critical components of

infrastructure very essential for the economic growth

envisaged by us in the days to come. The existence and

development of adequate infrastructure including Energy is

essential for sustained growth of the Indian economy.

India's Energy Sector is currently dependent more on

conventional sources such as coal, natural gas, oil, hydro and

on non-conventional sources such as wind, solar, and

agricultural waste to a lesser extent. Energy demand in the country has increased rapidly and is expected to rise

further in the years to come. In order to meet the increasing demand for energy in the country, massive addition

to the installed generating capacity is required, be it conventional or non conventional. Considering the depleting

sources of coal , oil, and even water as also the increasing cost of these sources, non conventional or renewable

energy indeed appears to be only prudent choice. We are fortunate to have natural resources such as sunlight,

wind, and bio mass in abundance which produce Renewable energy. Such energy would be very cost effective and

would make our industry more competitive. Hence the Government of India is promoting use of Renewable

Energy on a large scale .The solar energy mission of the Government of India is indeed a right initiative at the right

time. India ranks third among 40 countries in EY's Renewable Energy Country Attractiveness Index, on back of

strong focus by the Government on promoting renewable energy and implementation of projects in a time

bound manner. India's wind energy market is expected to attract investments totaling Rs 1,00,000 crore by 2020,

and wind power capacity is estimated to almost double by 2020 from over 23,000 MW in June 2015, with an

addition of about 4,000 MW per annum in the next five years. The investment scenario in the Renewable Energy

segment is looking very attractive. It has been reported that around 293 global and domestic companies have

committed to generate 266 GW of solar, wind, mini-hydel and biomass-based power in India over the next 5–10

years. This would amount to an investment of about Rs. 22 lakh crores. In the last week of February, Government

of India announced an ambitious scheme to double solar power generation capacity under the solar park scheme

to 40000 megawatts by 2020. The Government has also created a separate funding of about Rs. 8100 crores to

part finance these initiatives. We know that the nation has set a target of 100 GW of solar power by 2022. The

Government, Industry, and all of us have to work to achieve this target .

We at MCCIA are fully committed to promote the Government Policy for harnessing the Renewable Energy

and that commitment made us to take many initiatives in this rapidly developing segment of renewable energy. rd thOur National Conference on Renewable Energy held on 23 and 24 of February was one of them . We have made

it our Annual feature and the one held recently was the second in series which attracted substantial interest and

participation. A detailed report on the same appears in this March issue of Sampada. Do read it and let us know

your feedback . Happy Reading and Happy Holi too.

Dr. Anant SardeshmukhDirector General & Editor, Sampada

- _mM© 2017- _mM© 20174 54

C o n tFounder

Late A. R. Bhat

Editor

Dr. Anant Sardeshmukh

Content Co-ordinator

Sudhanwa Kopardekar

Content Support

Geeta Hosmane

Production & Coordination

Pramod Potbhare

Page Layout

G'tech Computers

Cover Page Design

Vivek Sahasrabudhe

Printing

Modern Printing Press

Owner/Printer/Publisher

Dr. Anant Sardeshmukh

Director General

Mahratta Chamber of Commerce,

Industries and Agriculture

Pune 411 002.

Tel. : 020-25709000 / 24440371

Vol. 72nd • Issue 12 • March 2017

CIN : U01409MH1974PLC017803

4

e n t s

5

7 MCCIA's Conference on Renewable Energyrd th

Held on 23 & 24 February 2017

9 Renewable Energy - the Need of the Hour : Bio-energy - a Sustainable Solution - Atul Mulay

11 Innovative Bio-Energy Technology by Shirke Energy

13 Maximising Returns on your Rooftop Solar Investment - Amit Rane

17 Solar Energy - A Sound Business Opportunity - Dr. Vivek Jayakumar

21 Bottlenecks Experienced in Solar Rooftop Progression - Shreya Shah

23 Every Rooftop (Solar) is Unique - Suhas Pansare

25 NABARD Financing Scheme for Solar Photovoltaic Lighting Systems

27 Solar Power Plant at Pune Railway Station A CSR initiative by Persistent Foundation

29 Let us understand GST : Taxable Person - Adv. Govind Patwardhan

33 Impact of GST on Automobile Dealers Industry - CA Madhukar Hiregange, CA Ravi Somani

39 Yellow Signal to Charity - CA Chandrashekhar Chitale

41 Ecolabels - Just a matter of compliance or an opportunity to become competitive in the markets? - Dr. Prasad Modak

43 Creating a strong B2B brand for SMEs - Nandita Khaire

45 Understanding Business Environment, Infrastructure Set up and Projects - Dr. Sachin Bhide

49 BZmoìhoeZ A±S> Q>oŠZm°bm°Or Q´>mÝñ\$a gob,

E_grgrAm`E - ZdrZ V§ÌkmZ : - n[aUm_H$maH$ CO}da AmYm[aV erVH$aU d erVJ¥h ì`dñWm - _mgirÀ`m {H$aH$moi {dH«$sgmR>r ìh°Š`w_ n°Ho$qOJ

52 Through the Looking Glass - Huned Contractor

55 MCCIA News

57 Dr. Abhay Firodia wins Entrepreneur of The Year Award

58 nwñVH$ n[aM` - Á`oð> ZmJ[aH$ Am{U ZdV§ÌkmZ - S>m°. {dH$mg BZm_Xma

13

29

52

- _mM© 2017- _mM© 20174 54

C o n tFounder

Late A. R. Bhat

Editor

Dr. Anant Sardeshmukh

Content Co-ordinator

Sudhanwa Kopardekar

Content Support

Geeta Hosmane

Production & Coordination

Pramod Potbhare

Page Layout

G'tech Computers

Cover Page Design

Vivek Sahasrabudhe

Printing

Modern Printing Press

Owner/Printer/Publisher

Dr. Anant Sardeshmukh

Director General

Mahratta Chamber of Commerce,

Industries and Agriculture

Pune 411 002.

Tel. : 020-25709000 / 24440371

Vol. 72nd • Issue 12 • March 2017

CIN : U01409MH1974PLC017803

4

e n t s

5

7 MCCIA's Conference on Renewable Energyrd th

Held on 23 & 24 February 2017

9 Renewable Energy - the Need of the Hour : Bio-energy - a Sustainable Solution - Atul Mulay

11 Innovative Bio-Energy Technology by Shirke Energy

13 Maximising Returns on your Rooftop Solar Investment - Amit Rane

17 Solar Energy - A Sound Business Opportunity - Dr. Vivek Jayakumar

21 Bottlenecks Experienced in Solar Rooftop Progression - Shreya Shah

23 Every Rooftop (Solar) is Unique - Suhas Pansare

25 NABARD Financing Scheme for Solar Photovoltaic Lighting Systems

27 Solar Power Plant at Pune Railway Station A CSR initiative by Persistent Foundation

29 Let us understand GST : Taxable Person - Adv. Govind Patwardhan

33 Impact of GST on Automobile Dealers Industry - CA Madhukar Hiregange, CA Ravi Somani

39 Yellow Signal to Charity - CA Chandrashekhar Chitale

41 Ecolabels - Just a matter of compliance or an opportunity to become competitive in the markets? - Dr. Prasad Modak

43 Creating a strong B2B brand for SMEs - Nandita Khaire

45 Understanding Business Environment, Infrastructure Set up and Projects - Dr. Sachin Bhide

49 BZmoìhoeZ A±S> Q>oŠZm°bm°Or Q´>mÝñ\$a gob,

E_grgrAm`E - ZdrZ V§ÌkmZ : - n[aUm_H$maH$ CO}da AmYm[aV erVH$aU d erVJ¥h ì`dñWm - _mgirÀ`m {H$aH$moi {dH«$sgmR>r ìh°Š`w_ n°Ho$qOJ

52 Through the Looking Glass - Huned Contractor

55 MCCIA News

57 Dr. Abhay Firodia wins Entrepreneur of The Year Award

58 nwñVH$ n[aM` - Á`oð> ZmJ[aH$ Am{U ZdV§ÌkmZ - S>m°. {dH$mg BZm_Xma

13

29

52

- _mM© 2017- _mM© 20176 7

Mahratta Chamber of Commerce Industries and Agriculture (MCCIA) had organised a two-day conference and exhibition on renewable energy. The

rd thevent was organised on the 23 and 24 February at Hotel Sheraton Grand, Pune.

The chief guest for the event was Mr. Suresh Prabhu, Hon'ble Minister for Railways, Government of India. The guest of honour was Mr. David Akov, Consul General for Israel in Mumbai.

The exhibitors at the event were companies working in the RE sector like solar power, wind and biomass. Also, there were a few banks that were endorsing exclusive finance schemes for investment in RE. The exhibition was organised for two days.

On day one, the conference started with a welcome note by Dr. Anant Sardeshmukh (Director General, MCCIA). Followed by this, Dr. R. N Kulkarni (Chief General Manager, NABARD), Dr. R. R. Sonde (Executive Director, Thermax Global) and Mr. Atul Mulay (Head Bio-energy at Praj Industries Ltd.) made presentations and shared the i r perspect ive about technologies, regulations, applications and the wish list of the renewable energy sector.

Shirke Energy, the title sponsor of the conference, launched its innovative product, converting waste biomass energy into bio-diesel. Apart from this, there were speakers from the industry speaking about transition from fossil to renewable energy economy on the back o f d i s r u p t i v e t e c h n o l o g i c a l developments. They also displayed various innovative implementation models.

M r . P r a d e e p B h a r g a v a (Independent Director at Persistent Sys tems L im i ted ) spoke abou t renewable energy and CSR. He spoke about the various CSR initiatives taken up by Persistent Foundation. He also mentioned about the 160 kWp solar power plant installed at Pune railway station that has been implemented as a CSR initiative of Persistent. Sunshot Technologies have done the EPC for solar power plant. Mr. Pradeep Bhargava, who is also a Director at Cummins India, presented the initiatives of Cummins Foundation in converting the Katraj and Balewadi wards within Pune Municipal Corporation to Zero Garbage wards. The waste generated there is processed in the respective wards itself. As a result, PMC is able to save over Rs 25 lac annually on account of power through bio gas obtained from processing wet garbage. This power is utilised to provide electricity for street lights and the toy train at Rajiv Gandhi Park in Katraj. He advised companies to undertake such initiatives under CSR so that Pune city tackles the problem of garbage more effectively.

The Conference also had sessions on solar water pumps, solar thermal technologies, utility scale solar power generation, and integration of wind energy with the grid and open access systems.

Mr. Suresh Prabhu joined the event through video conference call. He said that the railways have set up proper strategy to make the stations cleaner and greener. For the same, they plan to i n s t a l l r a i n w a t e r h a r v e s t i n g arrangements, use LED lighting at stations, etc. apart from installing rooftop solar power plants. He also mentioned that the detailed plan is available.

On day two, the first half of the event was focused on harnessing rooftop solar power to achieve the 40 GW target. There was a panel discussion of industry experts and government officials from MEDA for the same. Also, there were sessions on rooftop solar financing, technology and O&M of rooftop solar and strategy insights about defining approaches to tackle the high cost capital in renewable energy financing.

In the second half of the day, there was a panel discussion with industry experts and government officials on 'Smart City: Making Pune maximum solar city'. This was followed by a session on green buildings. In this, industry experts who have implemented green initiatives at their work place shared their perspective. We had speakers from Whirlpool India and Bharat Forge Limited. Both the companies are actively propagating reduction in power consumption and shifting to green sources of power like rooftop solar.

The last session of the day was a comparison of RE policy across states. The speaker for this session was Mr Narasimhan Santhanam, CEO of Solar Mango. He made a presentation on the various policies that are prevailing in var ious states and presented a comparative analysis of Maharashtra state, which is aggressively looking to installing solar power plants.

The master of ceremony (MC) of the event was Mr. Rahul Dasari.

----------------------------------------------------Compiled by Mohit Neve ([email protected])

MCCIA's Conference on Renewable Energy held on

rd th23 and 24 February 2017

- _mM© 2017- _mM© 20176 7

Mahratta Chamber of Commerce Industries and Agriculture (MCCIA) had organised a two-day conference and exhibition on renewable energy. The

rd thevent was organised on the 23 and 24 February at Hotel Sheraton Grand, Pune.

The chief guest for the event was Mr. Suresh Prabhu, Hon'ble Minister for Railways, Government of India. The guest of honour was Mr. David Akov, Consul General for Israel in Mumbai.

The exhibitors at the event were companies working in the RE sector like solar power, wind and biomass. Also, there were a few banks that were endorsing exclusive finance schemes for investment in RE. The exhibition was organised for two days.

On day one, the conference started with a welcome note by Dr. Anant Sardeshmukh (Director General, MCCIA). Followed by this, Dr. R. N Kulkarni (Chief General Manager, NABARD), Dr. R. R. Sonde (Executive Director, Thermax Global) and Mr. Atul Mulay (Head Bio-energy at Praj Industries Ltd.) made presentations and shared the i r perspect ive about technologies, regulations, applications and the wish list of the renewable energy sector.

Shirke Energy, the title sponsor of the conference, launched its innovative product, converting waste biomass energy into bio-diesel. Apart from this, there were speakers from the industry speaking about transition from fossil to renewable energy economy on the back o f d i s r u p t i v e t e c h n o l o g i c a l developments. They also displayed various innovative implementation models.

M r . P r a d e e p B h a r g a v a (Independent Director at Persistent Sys tems L im i ted ) spoke abou t renewable energy and CSR. He spoke about the various CSR initiatives taken up by Persistent Foundation. He also mentioned about the 160 kWp solar power plant installed at Pune railway station that has been implemented as a CSR initiative of Persistent. Sunshot Technologies have done the EPC for solar power plant. Mr. Pradeep Bhargava, who is also a Director at Cummins India, presented the initiatives of Cummins Foundation in converting the Katraj and Balewadi wards within Pune Municipal Corporation to Zero Garbage wards. The waste generated there is processed in the respective wards itself. As a result, PMC is able to save over Rs 25 lac annually on account of power through bio gas obtained from processing wet garbage. This power is utilised to provide electricity for street lights and the toy train at Rajiv Gandhi Park in Katraj. He advised companies to undertake such initiatives under CSR so that Pune city tackles the problem of garbage more effectively.

The Conference also had sessions on solar water pumps, solar thermal technologies, utility scale solar power generation, and integration of wind energy with the grid and open access systems.

Mr. Suresh Prabhu joined the event through video conference call. He said that the railways have set up proper strategy to make the stations cleaner and greener. For the same, they plan to i n s t a l l r a i n w a t e r h a r v e s t i n g arrangements, use LED lighting at stations, etc. apart from installing rooftop solar power plants. He also mentioned that the detailed plan is available.

On day two, the first half of the event was focused on harnessing rooftop solar power to achieve the 40 GW target. There was a panel discussion of industry experts and government officials from MEDA for the same. Also, there were sessions on rooftop solar financing, technology and O&M of rooftop solar and strategy insights about defining approaches to tackle the high cost capital in renewable energy financing.

In the second half of the day, there was a panel discussion with industry experts and government officials on 'Smart City: Making Pune maximum solar city'. This was followed by a session on green buildings. In this, industry experts who have implemented green initiatives at their work place shared their perspective. We had speakers from Whirlpool India and Bharat Forge Limited. Both the companies are actively propagating reduction in power consumption and shifting to green sources of power like rooftop solar.

The last session of the day was a comparison of RE policy across states. The speaker for this session was Mr Narasimhan Santhanam, CEO of Solar Mango. He made a presentation on the various policies that are prevailing in var ious states and presented a comparative analysis of Maharashtra state, which is aggressively looking to installing solar power plants.

The master of ceremony (MC) of the event was Mr. Rahul Dasari.

----------------------------------------------------Compiled by Mohit Neve ([email protected])

MCCIA's Conference on Renewable Energy held on

rd th23 and 24 February 2017

- _mM© 2017- _mM© 20178 9

Renewable Energy - the Need of the Hour : Bio-energy - a Sustainable Solution

Today, renewable energy is a critical par t o f reduc ing g loba l carbon emissions and is the need of the hour. However, the benefits of renewable energy go beyond just reducing carbon emissions; there are numerous benefits to be availed for the world. Climate change and the need to manage diminishing fossil fuel reserves are, today, two of the biggest challenges in front of us.

There is no way to protect the climate without dramatically changing how we produce and use electricity: the majority of pollution comes from power plants burning fossil fuels, especially coal in India. As an initiative toward creating sustainable environment, the Govt. is actively working to shut-down several old power plants to reduce carbon footprint in the country. On the other hand, nowadays, pollution from vehicles and burning of agricultural residue has emerged as a significant factor for increasing pollution. The traffic and number of vehicles are increasing day by day in the country, and it has become a tough challenge to control either the increasing number of vehicles or the pollution coming out from it.

Ethanol is more common in our lives than you may think. After all, any alcoholic beverage you can drink

consists ethanol. It is known by many different names such as ethyl alcohol, pure alcohol and grain alcohol. It is regarded as an alternative form of fuel that has gained much popularity for a number of reasons.

In case you were wondering, ethanol does not occur naturally in any eco-system. It is produced through the processes o f fe rmenta t ion and distillation. While the energy based use of ethanol fuel is new, it has been part of our l ives for a very long t ime. Fermenting sugar creates ethanol – knowledge used by our forefathers. These days, it comes from crops and plants that are rich in sugar or have the ability to be converted into cellulose and starch. Sugarcane, barley, sugar beets, wheat and corn are commonly used for ethanol production.

The Govt. is taking strong steps to reduce the import of crude oil by allowing use of ethanol blending in petrol. The Ministry of Petroleum & Natural Gas has given a big push for the ethanol blending programme, and is close to achieving 5% blending at national level. Sugar mills have been a v i t a l s o u r c e o f e t h a n o l t o o i l manufacturing companies in India; however, there is still a demand and supply gap for ethanol due to several

reasons. The cost of sugar and ethanol plays an important role in the overall fluctuations for ethanol production and supply.

It is estimated that the maximum available quantity of ethanol through molasses route that could be made available to OMCs stands at around 163 crore litres, which will be sufficient for only 6-7% of current ethanol blending requirement. Further, the expected available quantity of ethanol through molasses route in 2020 would not be able to even suffice 5% of ethanol blending requirement.

Surplus lignocellulosic biomass reserves across the country that are either lying idle or being wasted/burnt in many cases are a boon for biomass to ethanol program. Therefore, modern bio-refinery technical solutions have an ability to provide a sustainable solution to cater to our energy, social & environmental needs.

Praj has developed a technology to convert agricultural residue into fuel grade ethanol. This technology is a long term solution to the farmers' challenge of disposing off lignocellulosic waste – agri residue in this case – and turning it

ndinto 2 generation “bio” ethanol. This is an efficient technology indigenously

Atul Mulay

- _mM© 2017- _mM© 20178 9

Renewable Energy - the Need of the Hour : Bio-energy - a Sustainable Solution

Today, renewable energy is a critical par t o f reduc ing g loba l carbon emissions and is the need of the hour. However, the benefits of renewable energy go beyond just reducing carbon emissions; there are numerous benefits to be availed for the world. Climate change and the need to manage diminishing fossil fuel reserves are, today, two of the biggest challenges in front of us.

There is no way to protect the climate without dramatically changing how we produce and use electricity: the majority of pollution comes from power plants burning fossil fuels, especially coal in India. As an initiative toward creating sustainable environment, the Govt. is actively working to shut-down several old power plants to reduce carbon footprint in the country. On the other hand, nowadays, pollution from vehicles and burning of agricultural residue has emerged as a significant factor for increasing pollution. The traffic and number of vehicles are increasing day by day in the country, and it has become a tough challenge to control either the increasing number of vehicles or the pollution coming out from it.

Ethanol is more common in our lives than you may think. After all, any alcoholic beverage you can drink

consists ethanol. It is known by many different names such as ethyl alcohol, pure alcohol and grain alcohol. It is regarded as an alternative form of fuel that has gained much popularity for a number of reasons.

In case you were wondering, ethanol does not occur naturally in any eco-system. It is produced through the processes o f fe rmenta t ion and distillation. While the energy based use of ethanol fuel is new, it has been part of our l ives for a very long t ime. Fermenting sugar creates ethanol – knowledge used by our forefathers. These days, it comes from crops and plants that are rich in sugar or have the ability to be converted into cellulose and starch. Sugarcane, barley, sugar beets, wheat and corn are commonly used for ethanol production.

The Govt. is taking strong steps to reduce the import of crude oil by allowing use of ethanol blending in petrol. The Ministry of Petroleum & Natural Gas has given a big push for the ethanol blending programme, and is close to achieving 5% blending at national level. Sugar mills have been a v i t a l s o u r c e o f e t h a n o l t o o i l manufacturing companies in India; however, there is still a demand and supply gap for ethanol due to several

reasons. The cost of sugar and ethanol plays an important role in the overall fluctuations for ethanol production and supply.

It is estimated that the maximum available quantity of ethanol through molasses route that could be made available to OMCs stands at around 163 crore litres, which will be sufficient for only 6-7% of current ethanol blending requirement. Further, the expected available quantity of ethanol through molasses route in 2020 would not be able to even suffice 5% of ethanol blending requirement.

Surplus lignocellulosic biomass reserves across the country that are either lying idle or being wasted/burnt in many cases are a boon for biomass to ethanol program. Therefore, modern bio-refinery technical solutions have an ability to provide a sustainable solution to cater to our energy, social & environmental needs.

Praj has developed a technology to convert agricultural residue into fuel grade ethanol. This technology is a long term solution to the farmers' challenge of disposing off lignocellulosic waste – agri residue in this case – and turning it

ndinto 2 generation “bio” ethanol. This is an efficient technology indigenously

Atul Mulay

- _mM© 2017- _mM© 201710 11

developed by Praj for converting agri waste into fuel grade ethanol and is a permanent solution to an age old agri residue burning challenge.

In November 2016, Prime Minister, Mr. Narendra Modi said that the use of ethanol can reduce India's fuel imports a n d c i t e d B r a z i l ' s e x a m p l e i n successfully replacing gasoline to a large extent. “India's biggest import is petrol, diesel and oil. We can reduce this through use of ethanol. Brazil has made good use of ethanol,” Modi said. He was speaking af ter inaugurat ing the 'Sugarcane Value Chain - Vision 2025 Sugar' International Conference and Exhibition. “Ethanol production and sale has tripled in the last two years,” Modi said, adding that “ethanol can be a balancing power in the economy.” Ethanol is a renewable fuel made from corn and other plant materials.

Ethanol has a great potential as a biofuel and can contribute largely to the Govt. 's mission to achieve 10% blending ratio of ethanol in petrol by 2020.

Multiple Advantages of ethanol as a fuel :1. Renewable Resource: One of the

first benefits of ethanol is that in comparison to gasoline, it can be renewed. With the increased use of gas in our industries, many of the viable reservoirs are depleting. However, ethanol can be produced as long as the raw material needed for it can be grown. It is an eco-friendly fuel.

2. Use of co-products: Another benefit derived from the use of ethanol fuel is that the co-products can be used in an efficient manner. Co-product carbon dioxide can be fed to the plants that are being grown for the purpose of being fermented. This cycle has the potential to become self-sustaining and reducing air pollution. Bio-CNG can also be produced as a co-product, which can be used as fuel for automobiles, power plants, etc.

3. Lower Emissions: When ethanol is added to fuel, it burns in a cleaner manner and re leases fewer

emissions in comparison to pure gasoline. While most car engines are not equipped to work without gasoline, technology is attempting to alter that. Many new car models are being fitted with engines that can work through alternate means of energy. In the future, it is quite possible to have vehicles that can depend on the use of ethanol fuel alone.

4. Reduces Dependence on Foreign Oil: Since ethanol is domestically produced, from domestically grown crops, it helps reduce dependence on foreign oil.

5. Support to Farming Industry: Ethanol production can create more jobs in rural areas and will act as an addit ional income source for farmers, through the sale of agricultural residue.

---------------------------------------------------Atul MulayPresident and Strategic Business Unit Head for Bio Energy Division at PRAJ Industries Limited, and heads Global operations

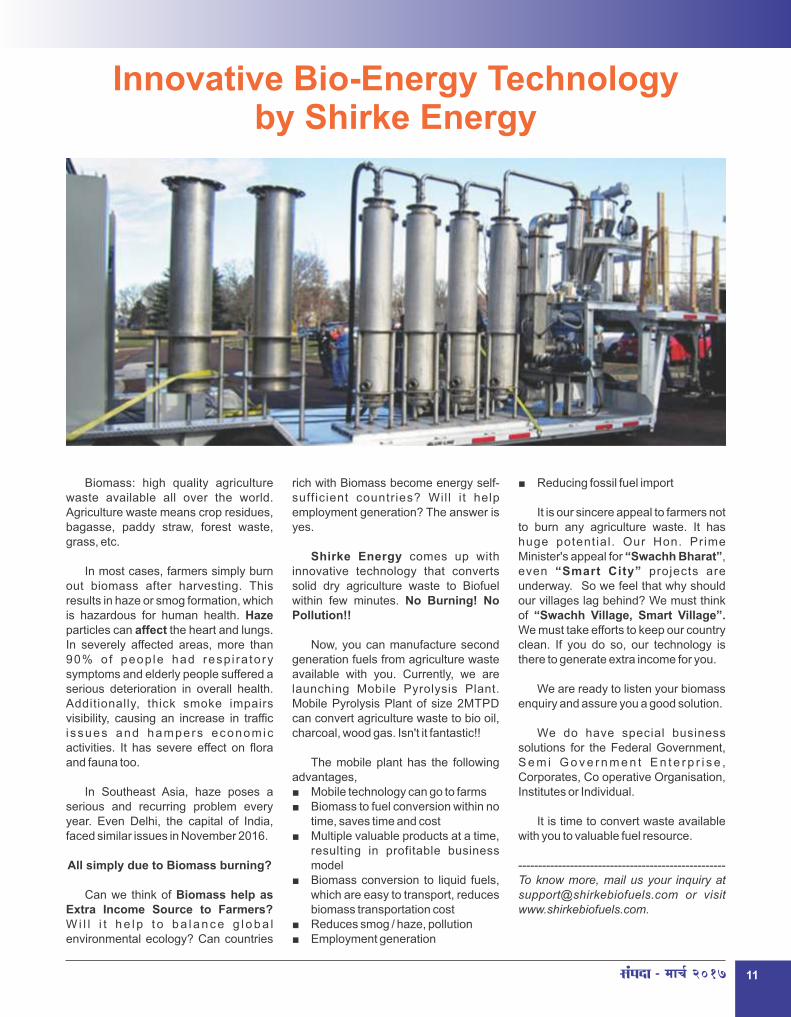

Biomass: high quality agriculture waste available all over the world. Agriculture waste means crop residues, bagasse, paddy straw, forest waste, grass, etc.

In most cases, farmers simply burn out biomass after harvesting. This results in haze or smog formation, which is hazardous for human health. Haze particles can affect the heart and lungs. In severely affected areas, more than 90% of peop le had resp i ra tory symptoms and elderly people suffered a serious deterioration in overall health. Additionally, thick smoke impairs visibility, causing an increase in traffic i ssues and hampers economic activities. It has severe effect on flora and fauna too.

In Southeast Asia, haze poses a serious and recurring problem every year. Even Delhi, the capital of India, faced similar issues in November 2016.

All simply due to Biomass burning?

Can we think of Biomass help as Extra Income Source to Farmers? W i l l i t h e l p t o b a l a n c e g l o b a l environmental ecology? Can countries

rich with Biomass become energy self-suff icient countries? Wil l i t help employment generation? The answer is yes.

Shirke Energy comes up with innovative technology that converts solid dry agriculture waste to Biofuel within few minutes. No Burning! No Pollution!!

Now, you can manufacture second generation fuels from agriculture waste available with you. Currently, we are launching Mobile Pyrolysis Plant. Mobile Pyrolysis Plant of size 2MTPD can convert agriculture waste to bio oil, charcoal, wood gas. Isn't it fantastic!!

The mobile plant has the following advantages,■ Mobile technology can go to farms■ Biomass to fuel conversion within no

time, saves time and cost■ Multiple valuable products at a time,

resulting in profitable business model

■ Biomass conversion to liquid fuels, which are easy to transport, reduces biomass transportation cost

■ Reduces smog / haze, pollution■ Employment generation

■ Reducing fossil fuel import

It is our sincere appeal to farmers not to burn any agriculture waste. It has huge potential . Our Hon. Prime Minister's appeal for “Swachh Bharat”, even “Smart City” projects are underway. So we feel that why should our villages lag behind? We must think of “Swachh Village, Smart Village”. We must take efforts to keep our country clean. If you do so, our technology is there to generate extra income for you.

We are ready to listen your biomass enquiry and assure you a good solution.

We do have special business solutions for the Federal Government, S e m i G o v e r n m e n t E n t e r p r i s e , Corporates, Co operative Organisation, Institutes or Individual.

It is time to convert waste available with you to valuable fuel resource.

----------------------------------------------------To know more, mail us your inquiry at [email protected] or visit www.shirkebiofuels.com.

Innovative Bio-Energy Technologyby Shirke Energy

- _mM© 2017- _mM© 201710 11

developed by Praj for converting agri waste into fuel grade ethanol and is a permanent solution to an age old agri residue burning challenge.

In November 2016, Prime Minister, Mr. Narendra Modi said that the use of ethanol can reduce India's fuel imports a n d c i t e d B r a z i l ' s e x a m p l e i n successfully replacing gasoline to a large extent. “India's biggest import is petrol, diesel and oil. We can reduce this through use of ethanol. Brazil has made good use of ethanol,” Modi said. He was speaking af ter inaugurat ing the 'Sugarcane Value Chain - Vision 2025 Sugar' International Conference and Exhibition. “Ethanol production and sale has tripled in the last two years,” Modi said, adding that “ethanol can be a balancing power in the economy.” Ethanol is a renewable fuel made from corn and other plant materials.

Ethanol has a great potential as a biofuel and can contribute largely to the Govt. 's mission to achieve 10% blending ratio of ethanol in petrol by 2020.

Multiple Advantages of ethanol as a fuel :1. Renewable Resource: One of the

first benefits of ethanol is that in comparison to gasoline, it can be renewed. With the increased use of gas in our industries, many of the viable reservoirs are depleting. However, ethanol can be produced as long as the raw material needed for it can be grown. It is an eco-friendly fuel.

2. Use of co-products: Another benefit derived from the use of ethanol fuel is that the co-products can be used in an efficient manner. Co-product carbon dioxide can be fed to the plants that are being grown for the purpose of being fermented. This cycle has the potential to become self-sustaining and reducing air pollution. Bio-CNG can also be produced as a co-product, which can be used as fuel for automobiles, power plants, etc.

3. Lower Emissions: When ethanol is added to fuel, it burns in a cleaner manner and re leases fewer

emissions in comparison to pure gasoline. While most car engines are not equipped to work without gasoline, technology is attempting to alter that. Many new car models are being fitted with engines that can work through alternate means of energy. In the future, it is quite possible to have vehicles that can depend on the use of ethanol fuel alone.

4. Reduces Dependence on Foreign Oil: Since ethanol is domestically produced, from domestically grown crops, it helps reduce dependence on foreign oil.

5. Support to Farming Industry: Ethanol production can create more jobs in rural areas and will act as an addit ional income source for farmers, through the sale of agricultural residue.

---------------------------------------------------Atul MulayPresident and Strategic Business Unit Head for Bio Energy Division at PRAJ Industries Limited, and heads Global operations

Biomass: high quality agriculture waste available all over the world. Agriculture waste means crop residues, bagasse, paddy straw, forest waste, grass, etc.

In most cases, farmers simply burn out biomass after harvesting. This results in haze or smog formation, which is hazardous for human health. Haze particles can affect the heart and lungs. In severely affected areas, more than 90% of peop le had resp i ra tory symptoms and elderly people suffered a serious deterioration in overall health. Additionally, thick smoke impairs visibility, causing an increase in traffic i ssues and hampers economic activities. It has severe effect on flora and fauna too.

In Southeast Asia, haze poses a serious and recurring problem every year. Even Delhi, the capital of India, faced similar issues in November 2016.

All simply due to Biomass burning?

Can we think of Biomass help as Extra Income Source to Farmers? W i l l i t h e l p t o b a l a n c e g l o b a l environmental ecology? Can countries

rich with Biomass become energy self-suff icient countries? Wil l i t help employment generation? The answer is yes.

Shirke Energy comes up with innovative technology that converts solid dry agriculture waste to Biofuel within few minutes. No Burning! No Pollution!!

Now, you can manufacture second generation fuels from agriculture waste available with you. Currently, we are launching Mobile Pyrolysis Plant. Mobile Pyrolysis Plant of size 2MTPD can convert agriculture waste to bio oil, charcoal, wood gas. Isn't it fantastic!!

The mobile plant has the following advantages,■ Mobile technology can go to farms■ Biomass to fuel conversion within no

time, saves time and cost■ Multiple valuable products at a time,

resulting in profitable business model

■ Biomass conversion to liquid fuels, which are easy to transport, reduces biomass transportation cost

■ Reduces smog / haze, pollution■ Employment generation

■ Reducing fossil fuel import

It is our sincere appeal to farmers not to burn any agriculture waste. It has huge potential . Our Hon. Prime Minister's appeal for “Swachh Bharat”, even “Smart City” projects are underway. So we feel that why should our villages lag behind? We must think of “Swachh Village, Smart Village”. We must take efforts to keep our country clean. If you do so, our technology is there to generate extra income for you.

We are ready to listen your biomass enquiry and assure you a good solution.

We do have special business solutions for the Federal Government, S e m i G o v e r n m e n t E n t e r p r i s e , Corporates, Co operative Organisation, Institutes or Individual.

It is time to convert waste available with you to valuable fuel resource.

----------------------------------------------------To know more, mail us your inquiry at [email protected] or visit www.shirkebiofuels.com.

Innovative Bio-Energy Technologyby Shirke Energy

- _mM© 2017- _mM© 201712 13

Amit Rane

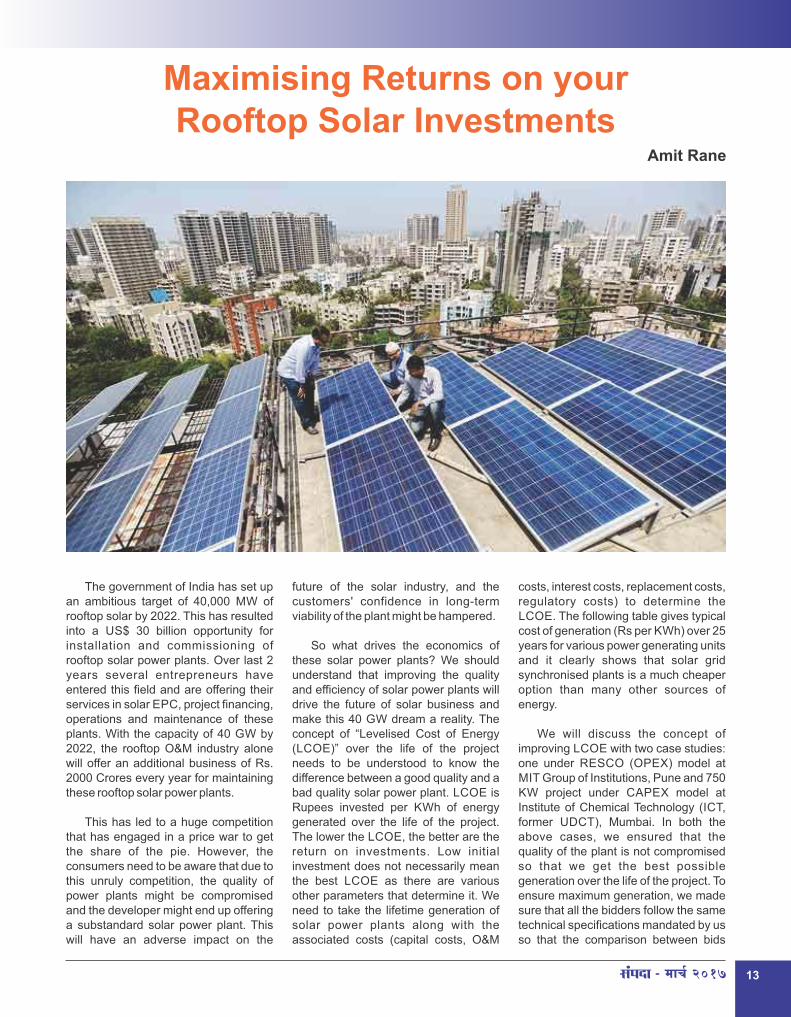

Maximising Returns on your Rooftop Solar Investments

The government of India has set up an ambitious target of 40,000 MW of rooftop solar by 2022. This has resulted into a US$ 30 billion opportunity for installation and commissioning of rooftop solar power plants. Over last 2 years several entrepreneurs have entered this field and are offering their services in solar EPC, project financing, operations and maintenance of these plants. With the capacity of 40 GW by 2022, the rooftop O&M industry alone will offer an additional business of Rs. 2000 Crores every year for maintaining these rooftop solar power plants.

This has led to a huge competition that has engaged in a price war to get the share of the pie. However, the consumers need to be aware that due to this unruly competition, the quality of power plants might be compromised and the developer might end up offering a substandard solar power plant. This will have an adverse impact on the

future of the solar industry, and the customers' confidence in long-term viability of the plant might be hampered.

So what drives the economics of these solar power plants? We should understand that improving the quality and efficiency of solar power plants will drive the future of solar business and make this 40 GW dream a reality. The concept of “Levelised Cost of Energy (LCOE)” over the life of the project needs to be understood to know the difference between a good quality and a bad quality solar power plant. LCOE is Rupees invested per KWh of energy generated over the life of the project. The lower the LCOE, the better are the return on investments. Low initial investment does not necessarily mean the best LCOE as there are various other parameters that determine it. We need to take the lifetime generation of solar power plants along with the associated costs (capital costs, O&M

costs, interest costs, replacement costs, regulatory costs) to determine the LCOE. The following table gives typical cost of generation (Rs per KWh) over 25 years for various power generating units and it clearly shows that solar grid synchronised plants is a much cheaper option than many other sources of energy.

We will discuss the concept of improving LCOE with two case studies: one under RESCO (OPEX) model at MIT Group of Institutions, Pune and 750 KW project under CAPEX model at Institute of Chemical Technology (ICT, former UDCT), Mumbai. In both the above cases, we ensured that the quality of the plant is not compromised so that we get the best possible generation over the life of the project. To ensure maximum generation, we made sure that all the bidders follow the same technical specifications mandated by us so that the comparison between bids

- _mM© 2017- _mM© 201712 13

Amit Rane

Maximising Returns on your Rooftop Solar Investments

The government of India has set up an ambitious target of 40,000 MW of rooftop solar by 2022. This has resulted into a US$ 30 billion opportunity for installation and commissioning of rooftop solar power plants. Over last 2 years several entrepreneurs have entered this field and are offering their services in solar EPC, project financing, operations and maintenance of these plants. With the capacity of 40 GW by 2022, the rooftop O&M industry alone will offer an additional business of Rs. 2000 Crores every year for maintaining these rooftop solar power plants.

This has led to a huge competition that has engaged in a price war to get the share of the pie. However, the consumers need to be aware that due to this unruly competition, the quality of power plants might be compromised and the developer might end up offering a substandard solar power plant. This will have an adverse impact on the

future of the solar industry, and the customers' confidence in long-term viability of the plant might be hampered.

So what drives the economics of these solar power plants? We should understand that improving the quality and efficiency of solar power plants will drive the future of solar business and make this 40 GW dream a reality. The concept of “Levelised Cost of Energy (LCOE)” over the life of the project needs to be understood to know the difference between a good quality and a bad quality solar power plant. LCOE is Rupees invested per KWh of energy generated over the life of the project. The lower the LCOE, the better are the return on investments. Low initial investment does not necessarily mean the best LCOE as there are various other parameters that determine it. We need to take the lifetime generation of solar power plants along with the associated costs (capital costs, O&M

costs, interest costs, replacement costs, regulatory costs) to determine the LCOE. The following table gives typical cost of generation (Rs per KWh) over 25 years for various power generating units and it clearly shows that solar grid synchronised plants is a much cheaper option than many other sources of energy.

We will discuss the concept of improving LCOE with two case studies: one under RESCO (OPEX) model at MIT Group of Institutions, Pune and 750 KW project under CAPEX model at Institute of Chemical Technology (ICT, former UDCT), Mumbai. In both the above cases, we ensured that the quality of the plant is not compromised so that we get the best possible generation over the life of the project. To ensure maximum generation, we made sure that all the bidders follow the same technical specifications mandated by us so that the comparison between bids

- _mM© 2017- _mM© 201714 15

a r e m a d e o n t h e b e s t q u a l i t y parameters. Technology selection was the key criteria to ensure that both these organisations work with most reliable technical partners for the term of the project. Our analyses show that higher investment cost with better generation over 25 years brings down LCOE drastically as compared to lower initial costs and poor generation over life of the project. Similarly, a lower solar tariff from one bidder under Power Purchase Agreement (PPA) did not offer more guaranteed savings compared to higher

solar tariff at MIT due to a huge difference in generation guarantees.

Selecting the right technology is the key to reduce LCOE. As solar modules account for more than 50% of the project cost, failure of solar modules is detrimental to the economics of the project. We have seen cases in field where solar output has reduced by more than 30% in first three years due to improper selection of solar modules. We insisted various test procedures to be carried out on modules for true linear

output over the life of the project. Understanding the module procurement process of various bidders was the key to ensure minimum degradation and maximum generation over the project life. Make of inverter and its field performance was checked as we have found out that make of inverters is compromised to reduce cost of the project. In many cases a cheaper make of inverter has resulted into 10-12% loss in generation. Shadow analysis report of each bidder was checked to see whether the estimated capacity was rightly designed or just done to show maximum savings to management. We also visited the plants installed by various bidders to check the quality of installation and verify whether the bidder was able to demonstrate the guaranteed generation at similar locations.

Care needs to be taken to ensure that during power cuts the system should be properly synchronized with the DG set. For the DG set to work optimally, a smart controller is needed that allows the DG Set to work at its spinning reserve and ensure that the solar output varies as per the load requirements. The controller should

Chart 1 also ensure that in case of low loads, the reverse flow of current from solar power system does not trip the DG set. Proper management of solar power will also contribute towards improving LCOE. We compared various controllers in market and recommended the two best control lers that meet the above requirements to be incorporated in the standard bill of supply.

Cleaning of solar modules and scheduled Operations & Maintenance (O&M) to reduce breakdown will improve the generation of solar power plants. Thus, O&M needs to be taken into consideration before arriving at LCOE, as it will have an impact on generation and the overall cost of the project. The operations and O&M cost over the life of the project are difficult to determine as the future cost of labour and water are unknown. However, the EPC partner should be ready to work out on providing PR based generation guarantees and the associated O&M costs to maintain the PR guarantee. The cost of labor and water should be worked as per the market conditions at that particular time. It is advisable to work with an EPC partner who is ready to take the O&M for the life of the project and commit to the PR based generation guarantees.

F u r t h e r m o r e , l o a d a n a l y s i s becomes an important part to maximise savings as the solar power system needs to be designed after considering the annual load pattern. The system should be designed in a manner in which there is no wastage of electricity

and all the generated energy gets consumed by the load. Unfortunately, due to unavailability of consumption data or due to lack of analytical skills of the EPC players, the load analysis is often a neglected area in the solar design process. We have seen cases where the project viability has suffered and savings have been reduced due to improper load analysis. Both MIT and ICT being educational institutes have low load days due to holidays. A substantial investment of time in load analysis helped us to understand the consumption pattern during holidays and helped us design a system that took care of the annual load with minimum wastage of generated energy.

As a takeaway from our experiences on the field, in order to get the best return on investment over the life of the

project, generation should be optimised as much as possible. A reliable EPC pa r t ne r w i t h a good t echn i ca l understanding of the solar power system will help you to improve LCOE. Also, safety measures should not be compromised to improve LCOE. While selecting technical partners, one should understand low initial cost does not necessarily offer highest return over the life of the project. The following checklist will help you to make a decision on whether a solar bid is offering a reliable solut ion and the best return on investment.

----------------------------------------------------Amit RaneFounder & Managing DirectorWudmin Energy Private [email protected]

- _mM© 2017- _mM© 201714 15

a r e m a d e o n t h e b e s t q u a l i t y parameters. Technology selection was the key criteria to ensure that both these organisations work with most reliable technical partners for the term of the project. Our analyses show that higher investment cost with better generation over 25 years brings down LCOE drastically as compared to lower initial costs and poor generation over life of the project. Similarly, a lower solar tariff from one bidder under Power Purchase Agreement (PPA) did not offer more guaranteed savings compared to higher

solar tariff at MIT due to a huge difference in generation guarantees.

Selecting the right technology is the key to reduce LCOE. As solar modules account for more than 50% of the project cost, failure of solar modules is detrimental to the economics of the project. We have seen cases in field where solar output has reduced by more than 30% in first three years due to improper selection of solar modules. We insisted various test procedures to be carried out on modules for true linear

output over the life of the project. Understanding the module procurement process of various bidders was the key to ensure minimum degradation and maximum generation over the project life. Make of inverter and its field performance was checked as we have found out that make of inverters is compromised to reduce cost of the project. In many cases a cheaper make of inverter has resulted into 10-12% loss in generation. Shadow analysis report of each bidder was checked to see whether the estimated capacity was rightly designed or just done to show maximum savings to management. We also visited the plants installed by various bidders to check the quality of installation and verify whether the bidder was able to demonstrate the guaranteed generation at similar locations.

Care needs to be taken to ensure that during power cuts the system should be properly synchronized with the DG set. For the DG set to work optimally, a smart controller is needed that allows the DG Set to work at its spinning reserve and ensure that the solar output varies as per the load requirements. The controller should

Chart 1 also ensure that in case of low loads, the reverse flow of current from solar power system does not trip the DG set. Proper management of solar power will also contribute towards improving LCOE. We compared various controllers in market and recommended the two best control lers that meet the above requirements to be incorporated in the standard bill of supply.

Cleaning of solar modules and scheduled Operations & Maintenance (O&M) to reduce breakdown will improve the generation of solar power plants. Thus, O&M needs to be taken into consideration before arriving at LCOE, as it will have an impact on generation and the overall cost of the project. The operations and O&M cost over the life of the project are difficult to determine as the future cost of labour and water are unknown. However, the EPC partner should be ready to work out on providing PR based generation guarantees and the associated O&M costs to maintain the PR guarantee. The cost of labor and water should be worked as per the market conditions at that particular time. It is advisable to work with an EPC partner who is ready to take the O&M for the life of the project and commit to the PR based generation guarantees.

F u r t h e r m o r e , l o a d a n a l y s i s becomes an important part to maximise savings as the solar power system needs to be designed after considering the annual load pattern. The system should be designed in a manner in which there is no wastage of electricity

and all the generated energy gets consumed by the load. Unfortunately, due to unavailability of consumption data or due to lack of analytical skills of the EPC players, the load analysis is often a neglected area in the solar design process. We have seen cases where the project viability has suffered and savings have been reduced due to improper load analysis. Both MIT and ICT being educational institutes have low load days due to holidays. A substantial investment of time in load analysis helped us to understand the consumption pattern during holidays and helped us design a system that took care of the annual load with minimum wastage of generated energy.

As a takeaway from our experiences on the field, in order to get the best return on investment over the life of the

project, generation should be optimised as much as possible. A reliable EPC pa r t ne r w i t h a good t echn i ca l understanding of the solar power system will help you to improve LCOE. Also, safety measures should not be compromised to improve LCOE. While selecting technical partners, one should understand low initial cost does not necessarily offer highest return over the life of the project. The following checklist will help you to make a decision on whether a solar bid is offering a reliable solut ion and the best return on investment.

----------------------------------------------------Amit RaneFounder & Managing DirectorWudmin Energy Private [email protected]

- _mM© 2017- _mM© 201716 17

Solar Energy – A Sound Business OpportunityDr. Vivek Jayakumar

2015 was a watershed year for renewable energy in the world. According to International Energy Agency (IEA), renewables, led by solar ( 4 9 G W ) a n d w i n d ( 6 6 G W ) , represented more than half the new power capacity around the world reaching 153 GW which was 15% more than previous year. This rapid growth has been driven largely by declining costs making electricity generated from r e n e w a b l e s c o m p e t i t i v e w h e n compared to conventional power. India expects to move from a renewable capacity of 50 GW (end 2016) to 175 GW (by 2022). A bulk of this capacity addition is likely to be in solar power (100 GW of which 60 GW is planned to be added through ground-mounted systems and 40 GW through rooftop systems).

This article focuses on business

opportunities in the field of electricity

generation from solar photovoltaics in India. There are certain underlying a s s u m p t i o n s t o s i m p l i f y t h e quantification of business potential in this sector.

India currently has an installed capacity of 9 GW of grid-interactive solar power of which over 8 GW have been set up as ground-mounted systems. The cost of setting up a ground-mounted, utility-scale (> 10MW) solar PV power plant has dropped from a high of INR 10 crores / MWp in 2010 to INR 4.5 crores / MWp in 2016. Being largely driven by reverse auctions, the tariffs have dropped from a high of INR 17.91/kWh in 2010 to INR 4.34/kWh in 2016. The drop in cost of setting up a utility-scale PV power plant has been driven mainly by a significant drop in PV module prices globally that dropped about 25% in 2016 alone.

The industry is confident of adding capacities in excess of 14 GW annually from 2017 onwards thus pushing India closer to the 100 GW mark. This has opened up business opportunities to the tune of INR 360,000 crores across the PV value chain.

Business opportunities may be e x p l o i t e d e i t h e r d o w n s t r e a m (generation and sale of power) or upstream (manufacturing).

IPPsIndependent power producers earn

revenue from sale of energy. While IPPs are generally technology agnostic, there is an increasing preference for solar power projects given the shorter gestation times and relatively easier project development. Energy tariff drops have however been steep with the current lowest tariff discovered in India being INR 3.3/kWh (levelised over 25

- _mM© 2017- _mM© 201716 17

Solar Energy – A Sound Business OpportunityDr. Vivek Jayakumar

2015 was a watershed year for renewable energy in the world. According to International Energy Agency (IEA), renewables, led by solar ( 4 9 G W ) a n d w i n d ( 6 6 G W ) , represented more than half the new power capacity around the world reaching 153 GW which was 15% more than previous year. This rapid growth has been driven largely by declining costs making electricity generated from r e n e w a b l e s c o m p e t i t i v e w h e n compared to conventional power. India expects to move from a renewable capacity of 50 GW (end 2016) to 175 GW (by 2022). A bulk of this capacity addition is likely to be in solar power (100 GW of which 60 GW is planned to be added through ground-mounted systems and 40 GW through rooftop systems).

This article focuses on business

opportunities in the field of electricity

generation from solar photovoltaics in India. There are certain underlying a s s u m p t i o n s t o s i m p l i f y t h e quantification of business potential in this sector.

India currently has an installed capacity of 9 GW of grid-interactive solar power of which over 8 GW have been set up as ground-mounted systems. The cost of setting up a ground-mounted, utility-scale (> 10MW) solar PV power plant has dropped from a high of INR 10 crores / MWp in 2010 to INR 4.5 crores / MWp in 2016. Being largely driven by reverse auctions, the tariffs have dropped from a high of INR 17.91/kWh in 2010 to INR 4.34/kWh in 2016. The drop in cost of setting up a utility-scale PV power plant has been driven mainly by a significant drop in PV module prices globally that dropped about 25% in 2016 alone.

The industry is confident of adding capacities in excess of 14 GW annually from 2017 onwards thus pushing India closer to the 100 GW mark. This has opened up business opportunities to the tune of INR 360,000 crores across the PV value chain.

Business opportunities may be e x p l o i t e d e i t h e r d o w n s t r e a m (generation and sale of power) or upstream (manufacturing).

IPPsIndependent power producers earn

revenue from sale of energy. While IPPs are generally technology agnostic, there is an increasing preference for solar power projects given the shorter gestation times and relatively easier project development. Energy tariff drops have however been steep with the current lowest tariff discovered in India being INR 3.3/kWh (levelised over 25

- _mM© 2017- _mM© 201718 19

years). IPPs may choose to develop green f ie ld pro jects or acqui re operational assets from other IPPs or developers. Payment security and curtailment risk are important factors to be considered. There is estimated revenue potential from energy sale to the tune of INR 133,650 crores in the next six years.

DevelopersDevelopers earn revenue generally

through sale of operational assets to IPPs and other investors. Developers leverage their strengths in land acquisition, permitting and project development. The government of India has increased the target capacity from solar parks to 40 GW. Solar parks mit igate the three r isks of land acquisition, power evacuation and permitting. Assuming that at least 50% of the new capacity is added by developers, this translates to a business opportunity of INR 180,000 crores. The sale of an operational asset will not just be based on the cost but will also consider other aspects like the tariff secured, power purchase agreement, off-taker risk, development risk in the region etc.

EPC companies / system integratorsSolar PV plants need sound EPC

i.e. engineering, procurement and construction to ensure that the plants are constructed on time, generate power reliably and perform well over the duration of the power sale agreement. While turnkey EPC costs are largely influenced by the price of PV modules, aspects like terrain, accessibility, project location (whether inside a solar park) etc. also govern. Similarly, for roof-top projects, good design and system integration is a must. The roof and surrounding conditions and existing electrical design of the buildings play a major role in the system integration cost. EPC companies and system integrators must develop procurement, project management and execution capabilities while working in an environment of intermittent cash flows and delays. Some of the IPPs and developers rely on in-house teams to undertake EPC and system integration. Discounting for this fact and assuming that 60% of the new capacity addition is done with support of a specialist EPC company or s y s t e m i n t e g r a t o r a b u s i n e s s opportunity of INR 162,000 crores exists over the next six years.

LendersA pertinent question doing the

rounds is the availability of equity capital and debt finance to help India achieve its target of 100 GW. Lenders stand exposed to over typically 70% of a project's cost over the tenor of the loan. India thus requires debt of around INR 252,000 crores over the next six years. Lenders need to be competitive in light of finance available internationally. As most of project financing is non-recourse, in addition to offtake risk and curtailment risk, lenders also need to assess credit worthiness of the owner / developer, technology and equipment proposed, energy yield predictions, execut ion par tners and pro jec t schedules. Climate Policy Initiative, one of the independent th ink-tanks, anticipates a shortfall of about 25% in the debt availability to meet India's renewable energy target of 175 GW.

Operation & MaintenanceIn a PV plant context , GTM

Research defines operations and maintenance (O&M) as a set of activities, most of them technical in nature, which enable PV power plants to optimally produce energy. Operations

and maintenance encompass a suite of activities like performance monitoring, issue detection, security, module cleaning, preventive and routine maintenance, maintaining performance guarantee ratios etc. O&M, though not complicated, is crucial for a solar PV power plant to perform reliably over its life time. Specialist O&M service providers are mushrooming across the country. While there is an increase in capacities of ground-mounted systems requiring dedicated O&M teams to be located onsite, the rooftop segment is attractive in terms of the number of systems that are likely to be deployed across the country. O&M is estimated to grow to an annual business of around INR 3000-4000 crores in 2022.

ManufacturingPV modules constitute over 55% of

a p r o j e c t ' s c o s t . T h e m o d u l e manufacturing capacity in India, as per MNRE, is around 7 GW with about 5 GW being currently operational. Indian module manufacturers are working towards cost competitiveness with less expensive options from other countries. The domestic content requirement (DCR) is not adequate to ensure full capacity utilisation and growth of the module manufacturing sector. There may be an opportunity for existing p l a y e r s t o u n d e r t a k e c o n t r a c t manufacturing for more competitive international players. It is, however, important that a vertically integrated fabrication industry is developed to ensure energy security in the long term. The manufacturing of module mounting structures (~12% of project cost) is still q u i t e u n o r g a n i s e d . N u m e r o u s opportunities exist in this segment with the proliferation of rooftop systems and the requirement of specialist mounting options. Some of the leading suppliers of inverters (~10% of project cost) have already established their manufacturing facilities in India. Opportunities exist in supp ly ing components to such suppliers. India has a well-established manu fac tu r i ng base fo r power evacuation equipment. Opportunities exist in analytics and SCADA systems.

TradingSolar has potential to reach areas

deep in India's hinterland. Trading in equipment in far flung areas will allow

leading manufacturers cater to the needs of a market hitherto ignored. The growth of rooftop solar through net-metering and decentralised applications will drive the sale of smaller power systems and equipment. Innovative trading mechanisms like online trading portals with convenient logistics have started.

ServicesA slew of service opportunities are

available for India's growing solar sector. Technical advisory, policy advisory, engineering support, project management , l i a i son and land acquisition, financial syndication etc. are some of the services that are currently being offered to the sector.

EducationThe Indian solar sector is estimated

to need over 650,000 professionals in the next 8-9 years. Training courses on design, installation, commissioning, operation and maintenance of solar systems are required to prepare an industry ready workforce. There are online educational courses certified by the government of India. Summits, conferences and workshops also add to increasing the knowledge base of the solar community. Academia could integrate solar-related capacity building programmes as part of their regular courses.

Demand response and energy storage

India will eventually evolve to a mature electricity market. Solar energy is intermittent or can be categorised as variable renewable energy. As solar increases it's penetration, India requires a flexible grid that can balance the alignment between renewable energy generation and demand. This can be achieved through demand response mechanisms and energy storage solutions. These are solutions that may, at this moment of time, be ahead of time in India but certainly have a major role to play in integrating large quantities of intermittent solar generation into the grid.

Solar energy has become cost competitive; the drivers of growth are shifting from policy-based support to market considerations. The sector offers tremendous opportunities across the value chain. The pie is big enough and so are the slices to attract a number of new entrepreneurs.

----------------------------------------------------Dr. Vivek Jayakumar is the executive director of Arbutus Consultants Pvt Ltd, providers of consulting, engineering and training services in the field of solar energy in India. Email : [email protected]

- _mM© 2017- _mM© 201718 19

years). IPPs may choose to develop green f ie ld pro jects or acqui re operational assets from other IPPs or developers. Payment security and curtailment risk are important factors to be considered. There is estimated revenue potential from energy sale to the tune of INR 133,650 crores in the next six years.

DevelopersDevelopers earn revenue generally

through sale of operational assets to IPPs and other investors. Developers leverage their strengths in land acquisition, permitting and project development. The government of India has increased the target capacity from solar parks to 40 GW. Solar parks mit igate the three r isks of land acquisition, power evacuation and permitting. Assuming that at least 50% of the new capacity is added by developers, this translates to a business opportunity of INR 180,000 crores. The sale of an operational asset will not just be based on the cost but will also consider other aspects like the tariff secured, power purchase agreement, off-taker risk, development risk in the region etc.

EPC companies / system integratorsSolar PV plants need sound EPC

i.e. engineering, procurement and construction to ensure that the plants are constructed on time, generate power reliably and perform well over the duration of the power sale agreement. While turnkey EPC costs are largely influenced by the price of PV modules, aspects like terrain, accessibility, project location (whether inside a solar park) etc. also govern. Similarly, for roof-top projects, good design and system integration is a must. The roof and surrounding conditions and existing electrical design of the buildings play a major role in the system integration cost. EPC companies and system integrators must develop procurement, project management and execution capabilities while working in an environment of intermittent cash flows and delays. Some of the IPPs and developers rely on in-house teams to undertake EPC and system integration. Discounting for this fact and assuming that 60% of the new capacity addition is done with support of a specialist EPC company or s y s t e m i n t e g r a t o r a b u s i n e s s opportunity of INR 162,000 crores exists over the next six years.

LendersA pertinent question doing the

rounds is the availability of equity capital and debt finance to help India achieve its target of 100 GW. Lenders stand exposed to over typically 70% of a project's cost over the tenor of the loan. India thus requires debt of around INR 252,000 crores over the next six years. Lenders need to be competitive in light of finance available internationally. As most of project financing is non-recourse, in addition to offtake risk and curtailment risk, lenders also need to assess credit worthiness of the owner / developer, technology and equipment proposed, energy yield predictions, execut ion par tners and pro jec t schedules. Climate Policy Initiative, one of the independent th ink-tanks, anticipates a shortfall of about 25% in the debt availability to meet India's renewable energy target of 175 GW.

Operation & MaintenanceIn a PV plant context , GTM

Research defines operations and maintenance (O&M) as a set of activities, most of them technical in nature, which enable PV power plants to optimally produce energy. Operations

and maintenance encompass a suite of activities like performance monitoring, issue detection, security, module cleaning, preventive and routine maintenance, maintaining performance guarantee ratios etc. O&M, though not complicated, is crucial for a solar PV power plant to perform reliably over its life time. Specialist O&M service providers are mushrooming across the country. While there is an increase in capacities of ground-mounted systems requiring dedicated O&M teams to be located onsite, the rooftop segment is attractive in terms of the number of systems that are likely to be deployed across the country. O&M is estimated to grow to an annual business of around INR 3000-4000 crores in 2022.

ManufacturingPV modules constitute over 55% of

a p r o j e c t ' s c o s t . T h e m o d u l e manufacturing capacity in India, as per MNRE, is around 7 GW with about 5 GW being currently operational. Indian module manufacturers are working towards cost competitiveness with less expensive options from other countries. The domestic content requirement (DCR) is not adequate to ensure full capacity utilisation and growth of the module manufacturing sector. There may be an opportunity for existing p l a y e r s t o u n d e r t a k e c o n t r a c t manufacturing for more competitive international players. It is, however, important that a vertically integrated fabrication industry is developed to ensure energy security in the long term. The manufacturing of module mounting structures (~12% of project cost) is still q u i t e u n o r g a n i s e d . N u m e r o u s opportunities exist in this segment with the proliferation of rooftop systems and the requirement of specialist mounting options. Some of the leading suppliers of inverters (~10% of project cost) have already established their manufacturing facilities in India. Opportunities exist in supp ly ing components to such suppliers. India has a well-established manu fac tu r i ng base fo r power evacuation equipment. Opportunities exist in analytics and SCADA systems.

TradingSolar has potential to reach areas

deep in India's hinterland. Trading in equipment in far flung areas will allow

leading manufacturers cater to the needs of a market hitherto ignored. The growth of rooftop solar through net-metering and decentralised applications will drive the sale of smaller power systems and equipment. Innovative trading mechanisms like online trading portals with convenient logistics have started.

ServicesA slew of service opportunities are

available for India's growing solar sector. Technical advisory, policy advisory, engineering support, project management , l i a i son and land acquisition, financial syndication etc. are some of the services that are currently being offered to the sector.

EducationThe Indian solar sector is estimated

to need over 650,000 professionals in the next 8-9 years. Training courses on design, installation, commissioning, operation and maintenance of solar systems are required to prepare an industry ready workforce. There are online educational courses certified by the government of India. Summits, conferences and workshops also add to increasing the knowledge base of the solar community. Academia could integrate solar-related capacity building programmes as part of their regular courses.

Demand response and energy storage

India will eventually evolve to a mature electricity market. Solar energy is intermittent or can be categorised as variable renewable energy. As solar increases it's penetration, India requires a flexible grid that can balance the alignment between renewable energy generation and demand. This can be achieved through demand response mechanisms and energy storage solutions. These are solutions that may, at this moment of time, be ahead of time in India but certainly have a major role to play in integrating large quantities of intermittent solar generation into the grid.

Solar energy has become cost competitive; the drivers of growth are shifting from policy-based support to market considerations. The sector offers tremendous opportunities across the value chain. The pie is big enough and so are the slices to attract a number of new entrepreneurs.

----------------------------------------------------Dr. Vivek Jayakumar is the executive director of Arbutus Consultants Pvt Ltd, providers of consulting, engineering and training services in the field of solar energy in India. Email : [email protected]

- _mM© 2017- _mM© 201720 21

India will find it difficult to achieve its ambitious target of 40 GW of installed solar rooftop capacity by 2022, if it continues to rely solely on policy and incentives. Till date, the solar rooftop capacity stands at 1.1 GW. In order to achieve the 40 GW target, an 86% growth/year is needed which is even faster than the growth in mobile phone connections. One of the major factors affecting the purchase decision for a solar rooftop plant is the quantum of investment involved. To facilitate this investment, the Government of India had announced various incentives and policies. These incentives included accelerated depreciation benefit, 10 year tax holiday, capital and interest subsidies, net metering policies, etc.

Even with presence of such policies, the solar power sector is expected to find it difficult to achieve the desired target. This can be attributed to various reasons as cited below :

Accelerated depreciation : Till date, accelerated depreciation had been crucial for the growth of solar rooftop industry, wherein the major buyers, which include profit making companies, are interested in claiming 80% tax benefit due to accelerated depreciation. As per Union Budget 2017, this benefit has been scaled down to 40%, which will surely dampen growth in this sector.

Sunset clause (10 year tax holiday) : Sunset clause under section 80 IA (10 year tax holiday for power generation, transmission and distribution investments) until March 2017 has also been maintained. Removal of this benefit will impact the private PPA based market and cause a shift of solar power sector from non-traditional investors to pure power companies.

Central financial assistance : Capital subsidies in terms of 30% central financial assistance have failed to create an impact on the market due to limitation of funds at disposal. Procedural hurdles due to presence of multiple agencies like MNRE, State nodal agency, electrical inspector, DISCOM have slowed the subsidy disbursal mechanism.

Net metering : Net metering has been a promising development for the rooftop solar market. However, the implementation of this policy has been rather slow with no standardisation of policy among various states. Many states have arbitrary restrictions based on offtake voltage or transformer capacity or unreasonable rules about meter locations that prevent simplest of solar power plants from availing the net metering policy.