Page 1

MONTHLY MARKET OVERVIEW1st — 30th September 2017

+44 (0) 203 026 5555 [email protected]

SUMMARY OF CONTENT

• Value analysis

• Total second hand S&P activity

• Newbuilding activity

• Demolition activity

• Charter rate analysis

Page 2

180k

180k

180k

180k

180k

180k

180k

180k

180k

180k

180k

180k

180k

180k

175k

175k

80k

80k

80k

80k

80k

80k

80k

80k

80k

80k

75k

75k

75k

75k

75k

75k

60k

60k

60k

60k

60k

60k

60k

55k

55k

55k

55k

55k

55k

55k

50k

50k

30k

30k

30k

30k

30k

30k

30k

30k

30k

30k

30k

30k

30k

30k

30k

30k

CAPE PMAX SUPRAYEAR

OF BUILD HANDY

DWT DWT DWT DWT

2017

2016

2010

2011

2012

2013

2014

2015

2002

2003

2004

2005

2006

2007

2008

2009

+1.3%

+2.2%

+2.8%

+3.1%

+3.1%

+2.8%

+2.4%

+1.8%

+1.3%

+0.7%

+0.3%

+0.1%

+0.2%

+0.7%

+1.9%

+3.2%

+1.5%

+1.5%

+1.6%

+1.7%

+1.8%

+1.9%

+2.0%

+2.1%

+2.2%

+2.4%

+1.7%

+1.9%

+2.0%

+2.1%

+2.3%

+2.3%

+1.5%

+1.6%

+1.8%

+2.0%

+2.2%

+2.4%

+2.5%

+2.4%

+2.6%

+2.8%

+3.1%

+3.2%

+3.3%

+3.6%

+2.6%

+2.7%

+0.1%

+0.0%

+0.0%

+0.0%

+0.0%

+0.2%

+0.3%

+0.3%

+0.1%

+0.0%

+0.0%

+0.2%

+0.3%

+0.5%

+0.6%

+0.6%

BULKER VALUES THROUGH SEPTEMBER 2017

+44 (0) 203 026 5555 [email protected]

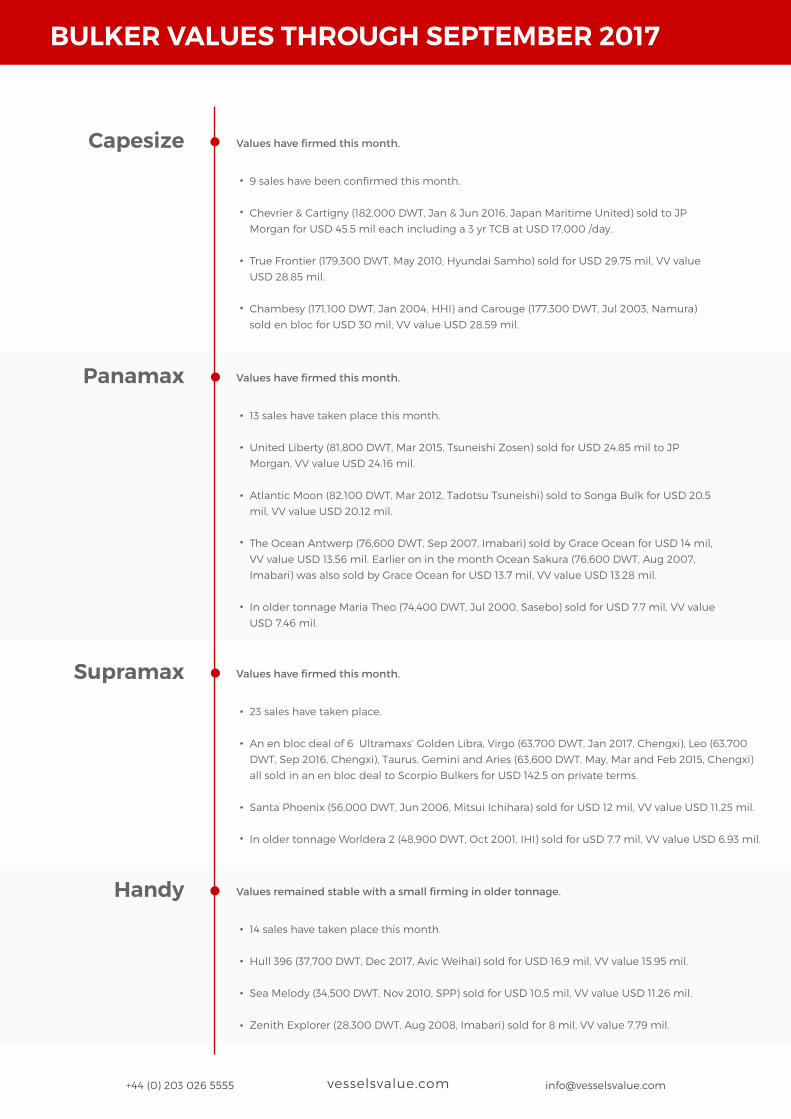

BULKERS Bulker values have firmed for all vessel types.

This table shows the monthly % change in value from 1st to the 30th September 2017for Bulker vessels, by year of build.

Page 3

BULKER VALUES THROUGH SEPTEMBER 2017

Panamax Values have firmed this month.

13 sales have taken place this month.

United Liberty (81,800 DWT, Mar 2015, Tsuneishi Zosen) sold for USD 24.85 mil to JP

Morgan, VV value USD 24.16 mil.

Atlantic Moon (82,100 DWT, Mar 2012, Tadotsu Tsuneishi) sold to Songa Bulk for USD 20.5

mil, VV value USD 20.12 mil.

The Ocean Antwerp (76,600 DWT, Sep 2007, Imabari) sold by Grace Ocean for USD 14 mil,

VV value USD 13.56 mil. Earlier on in the month Ocean Sakura (76,600 DWT, Aug 2007,

Imabari) was also sold by Grace Ocean for USD 13.7 mil, VV value USD 13.28 mil.

In older tonnage Maria Theo (74,400 DWT, Jul 2000, Sasebo) sold for USD 7.7 mil, VV value

USD 7.46 mil.

Supramax Values have firmed this month.

23 sales have taken place.

An en bloc deal of 6 Ultramaxs’ Golden Libra, Virgo (63,700 DWT, Jan 2017, Chengxi), Leo (63,700

DWT, Sep 2016, Chengxi), Taurus, Gemini and Aries (63,600 DWT, May, Mar and Feb 2015, Chengxi)

all sold in an en bloc deal to Scorpio Bulkers for USD 142.5 on private terms.

Santa Phoenix (56,000 DWT, Jun 2006, Mitsui Ichihara) sold for USD 12 mil, VV value USD 11.25 mil.

In older tonnage Worldera 2 (48,900 DWT, Oct 2001, IHI) sold for uSD 7.7 mil, VV value USD 6.93 mil.

Handy Values remained stable with a small firming in older tonnage.

14 sales have taken place this month.

Hull 396 (37,700 DWT, Dec 2017, Avic Weihai) sold for USD 16.9 mil, VV value 15.95 mil.

Sea Melody (34,500 DWT, Nov 2010, SPP) sold for USD 10.5 mil, VV value USD 11.26 mil.

Zenith Explorer (28,300 DWT, Aug 2008, Imabari) sold for 8 mil, VV value 7.79 mil.

Capesize Values have firmed this month.

9 sales have been confirmed this month.

Chevrier & Cartigny (182,000 DWT, Jan & Jun 2016, Japan Maritime United) sold to JP

Morgan for USD 45.5 mil each including a 3 yr TCB at USD 17,000 /day.

True Frontier (179,300 DWT, May 2010, Hyundai Samho) sold for USD 29.75 mil, VV value

USD 28.85 mil.

Chambesy (171,100 DWT, Jan 2004, HHI) and Carouge (177,300 DWT, Jul 2003, Namura)

sold en bloc for USD 30 mil, VV value USD 28.59 mil.

+44 (0) 203 026 5555 [email protected]

Page 4

TANKER VALUES THROUGH SEPTEMBER 2017

+44 (0) 203 026 5555 [email protected]

All values have remained stable this month with a slight softening inolder Aframax values.

This table shows the monthly % change in value from 1st to the 30th September 2017for Tanker vessels, by year of build.

TANKERS

320k

320k

320k

320k

320k

310k

310k

310k

310k

310k

310k

310k

310k

305k

305k

305k

160k

160k

160k

160k

160k

160k

160k

160k

160k

160k

160k

160k

160k

155k

155k

155k

75k

75k

75k

75k

75k

75k

75k

75k

75k

75k

75k

70k

70k

70k

70k

70k

50k

50k

50k

50k

50k

50k

50k

50k

50k

50k

50k

45k

45k

45k

45k

45k

110k

110k

110k

110k

110k

110k

110k

110k

110k

110k

110k

110k

110k

105k

105k

105k

+0.3%

+0.2%

+0.2%

+0.1%

+0.0%

+0.0%

-0.1%

-0.1%

-0.1%

-0.2%

-0.2%

-0.3%

-0.2%

-0.3%

-0.3%

-0.3%

-0.2%

-0.3%

-0.3%

-0.4%

-0.5%

-0.6%

-0.6%

-0.7%

-0.8%

-0.8%

-0.9%

-0.9%

-1.0%

-1.0%

-1.0%

-1.1%

-0.3%

-0.4%

-0.5%

-0.6%

-0.8%

-1.0%

-1.3%

-1.7%

-2.1%

-2.6%

-3.2%

-3.8%

-4.6%

-5.4%

-6.2%

-6.9%

+0.2%

+0.1%

-0.0%

-0.1%

-0.3%

-0.5%

-0.9%

-1.2%

-1.6%

-2.2%

-2.8%

-3.3%

-4.0%

-4.7%

-5.6%

-6.4%

+0.7%

+0.7%

+0.6%

+0.5%

+0.3%

+0.2%

+0.0%

-0.2%

-0.4%

-0.6%

-0.8%

-1.1%

-1.3%

-1.6%

-1.8%

-2.0%

YEAROF BUILD VLCC SUEZ AFRA LR1 MR

DWT DWT DWT DWT DWT

2017

2016

2010

2011

2012

2013

2014

2015

2002

2003

2004

2005

2006

2007

2008

2009

Page 5

TANKER VALUES THROUGH SEPTEMBER 2017

+44 (0) 203 026 5555 [email protected]

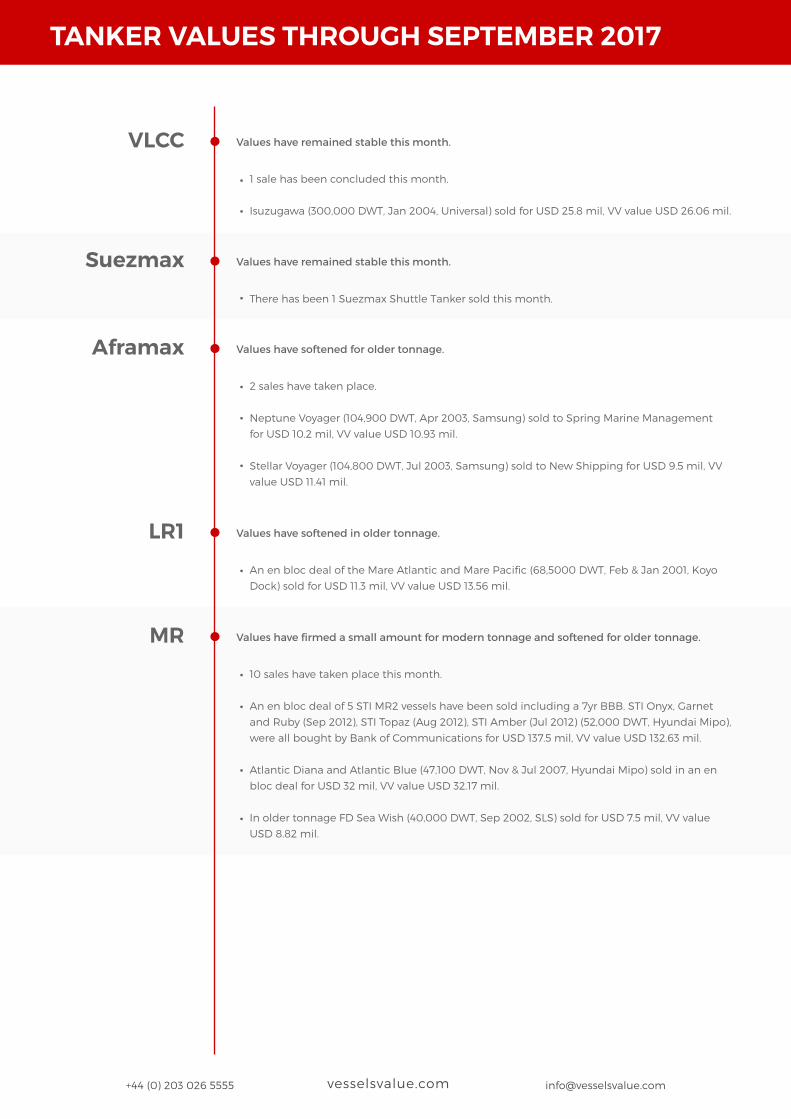

VLCC Values have remained stable this month.

1 sale has been concluded this month.

Isuzugawa (300,000 DWT, Jan 2004, Universal) sold for USD 25.8 mil, VV value USD 26.06 mil.

Suezmax Values have remained stable this month.

There has been 1 Suezmax Shuttle Tanker sold this month.

Aframax Values have softened for older tonnage.

2 sales have taken place.

Neptune Voyager (104,900 DWT, Apr 2003, Samsung) sold to Spring Marine Management

for USD 10.2 mil, VV value USD 10.93 mil.

Stellar Voyager (104,800 DWT, Jul 2003, Samsung) sold to New Shipping for USD 9.5 mil, VV

value USD 11.41 mil.

LR1 Values have softened in older tonnage.

An en bloc deal of the Mare Atlantic and Mare Pacific (68,5000 DWT, Feb & Jan 2001, Koyo

Dock) sold for USD 11.3 mil, VV value USD 13.56 mil.

MR Values have firmed a small amount for modern tonnage and softened for older tonnage.

10 sales have taken place this month.

An en bloc deal of 5 STI MR2 vessels have been sold including a 7yr BBB. STI Onyx, Garnet

and Ruby (Sep 2012), STI Topaz (Aug 2012), STI Amber (Jul 2012) (52,000 DWT, Hyundai Mipo),

were all bought by Bank of Communications for USD 137.5 mil, VV value USD 132.63 mil.

Atlantic Diana and Atlantic Blue (47,100 DWT, Nov & Jul 2007, Hyundai Mipo) sold in an en

bloc deal for USD 32 mil, VV value USD 32.17 mil.

In older tonnage FD Sea Wish (40,000 DWT, Sep 2002, SLS) sold for USD 7.5 mil, VV value

USD 8.82 mil.

Page 6

CONTAINER VALUES THROUGH SEPTEMBER 2017

+44 (0) 203 026 5555 [email protected]

CONTAINERS Container values have been variable this month. Modern Panamax valueshave softened whilst older Feedermax values have softened.

This table shows the monthly % change in value from 1st to the 30th September 2017for Container vessels, by year of build.

2017

2016

2010

2011

2012

2013

2014

2015

2002

2003

2004

2005

2006

2007

2008

2009

7000

7000

7000

7000

7000

7000

7000

7000

7000

7000

7000

7000

7000

7000

6500

6500

4250

4250

4250

4250

4250

4250

4250

4250

4250

4250

4250

4250

4250

4250

4000

4000

1750

1750

1750

1750

1750

1750

1750

1750

1750

1750

1750

1750

1750

1750

1750

1750

1100

1100

1100

1100

1100

1100

1100

1100

1100

1100

1100

1100

1100

1100

1100

1100

YEAROF BUILD POST PMAX PMAX HANDY FMAX

TEU TEU TEU TEU

-0.6%

-0.7%

-0.8%

-1.0%

-1.1%

-1.2%

-1.3%

-1.4%

-1.6%

-1.7%

-1.8%

-2.0%

-2.0%

+1.4%

+1.4%

+1.4%

-2.3%

-2.5%

-2.5%

-2.6%

-2.8%

-2.9%

-3.0%

-3.1%

-3.3%

-3.4%

+1.4%

+1.4%

+1.4%

+1.4%

+1.3%

+1.3%

+0.4%

+0.3%

+0.2%

+0.1%

+0.0%

-0.1%

-0.1%

-0.2%

-0.2%

-0.3%

-0.3%

+4.3%

+3.6%

+3.0%

+2.6%

+1.8%

+0.4%

+0.4%

+0.3%

+0.2%

+0.1%

+0.0%

-0.1%

-0.3%

-0.4%

-0.4%

-0.6%

-3.0%

-4.7%

-6.0%

-8.0%

-9.5%

Page 7

+44 (0) 203 026 5555 [email protected]

CONTAINER VALUES THROUGH SEPTEMBER 2017

Post PMax Values have remained relatively stable this month.

There have been no Post Panamax sales this month.

A firming in older tonnage is due to scrap rates firming.

Panamax Values have softened for mid age tonnage.

2 sales have taken place this month.

CPO Savannah (4,255 TEU, Aug 2009, HHI) sold for USD 10.4 mil, VV value USD 10.68 mil.

Kaethe P (5,040 TEU, Nov 2006, HHI) was bought by MPC Container Ships for USD 9.5 mil, VV

value USD 9.96 mil.

Handy Values have remained stable this month.

2 Handy and 5 Sub Panamax sales have taken place this month.

Wehr Havel (2,524 TEU, Sep 2002, Kvaerner) sold for USD 5.3 mil, VV value USD 5.76 mil.

Feedermax Values have remained stable this month.

1 sale have been confirmed this month.

Suzanne (841 TEU, Oct 1994, Miho Zosensho) sold for USD 2 mil, VV value 1.89 mil.

Page 8

LPG VALUES THROUGH SEPTEMBER 2017

+44 (0) 203 026 5555 [email protected]

LPG LPG values have remained stable across all vessel types.

This table shows the monthly % change in value from 1st to the 30th September 2017for LPG vessels, by year of build.

2017

2016

2010

2011

2012

2013

2014

2015

2002

2003

2004

2005

2006

2007

2008

2009

84k

84k

84k

84k

82k

82k

82k

82k

82k

82k

82k

82k

78k

78k

78k

78k

60k

60k

60k

60k

60k

60k

60k

60k

60k

60k

60k

60k

60k

60k

60k

57k

38k

38k

38k

38k

35k

35k

35k

35k

35k

35k

35k

35k

35k

35k

35k

35k

20k

20k

20k

20k

20k

20k

20k

20k

20k

20k

20k

20k

20k

20k

20k

20k

6.5k

6.5k

6.5k

6.5k

6.5k

6.5k

6.5k

6.5k

6.5k

6.5k

6.5k

6.5k

6.5k

6.5k

6.5k

6.5k

3.5k

3.5k

3.5k

3.5k

3.5k

3.5k

3.5k

3.5k

3.5k

3.5k

3.5k

3.5k

3.5k

3.5k

3.5k

3.5k

12k

12k

12k

12k

9k

9k

9k

9k

9k

8k

8k

8k

8k

8k

8k

12k

YEAROF BUILD VLGC LGC MGC

SP FRLARGE

SP FRSMALL

FULLPRESS LEG

CBM CBM CBM CBM CBM CBM CBM

+0.8%

+0.5%

+0.1%

+0.6%

-1.0%

-0.7%

-1.0%

-0.0%

-0.0%

-0.6%

-1.3%

-1.2%

-1.3%

-1.4%

-1.5%

-1.6%

+1.3%

+0.9%

+0.5%

+0.6%

+0.6%

+0.1%

-0.8%

-0.0%

-0.0%

-0.2%

-0.9%

-1.6%

-1.6%

-2.1%

-1.8%

-1.5%

-1.5%

-1.5%

-1.5%

-1.6%

-1.6%

-1.6%

-1.6%

-1.6%

-1.6%

-1.7%

-1.7%

-0.8%

-1.6%

-1.7%

-1.8%

-1.9%

-3.9%

-3.9%

-3.8%

-3.6%

-3.3%

-3.0%

-2.6%

-2.2%

-1.7%

-1.2%

-0.7%

-0.3%

+0.1%

+0.4%

+0.6%

+0.7%

-3.5%

-3.5%

-3.4%

-3.2%

-3.0%

-2.6%

-2.2%

-1.8%

-1.4%

-0.8%

-0.4%

+0.1%

+0.5%

+0.8%

+1.0%

+1.0%

-1.5%

-1.5%

-1.4%

-1.6%

-1.5%

-1.6%

-1.6%

-1.7%

-1.8%

-1.7%

-1.7%

+0.2%

+0.6%

+0.9%

+1.2%

+1.0%

-1.4%

-1.5%

-1.5%

-1.5%

-1.6%

-1.6%

-1.6%

-1.7%

-1.7%

-1.7%

-1.7%

+0.0%

+0.5%

+0.7%

+1.0%

+1.0%

Page 9

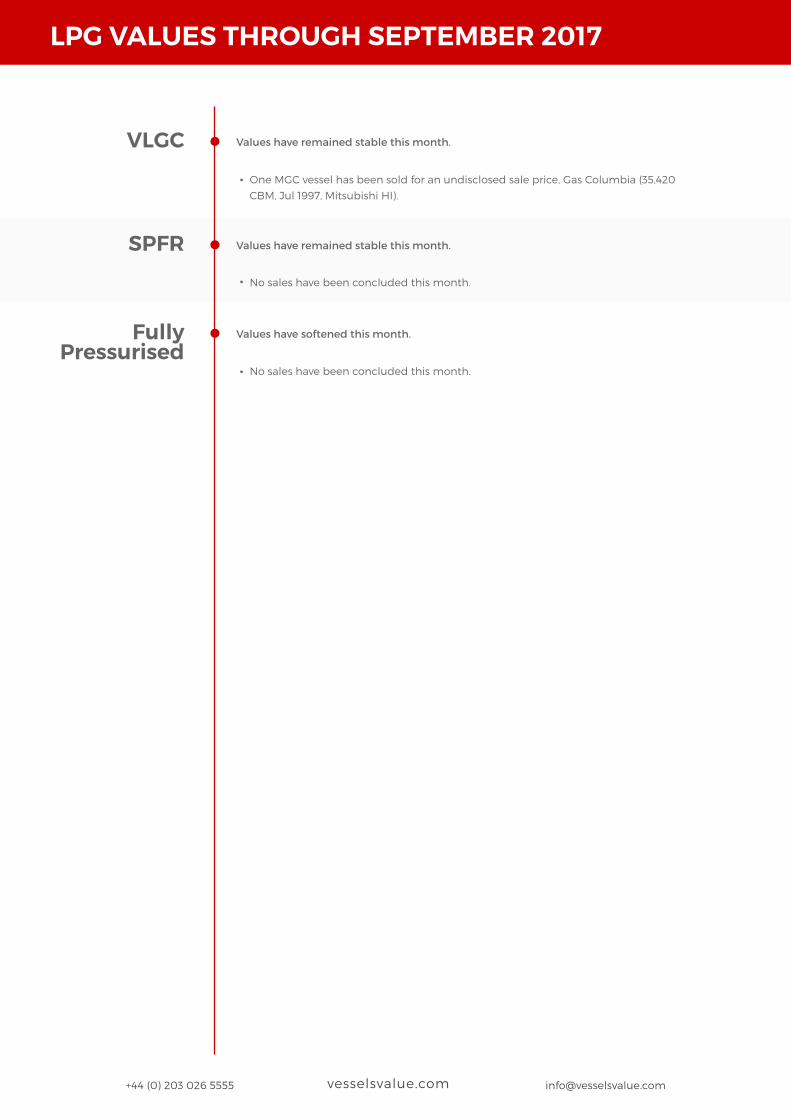

SPFR Values have remained stable this month.

No sales have been concluded this month.

+44 (0) 203 026 5555 [email protected]

LPG VALUES THROUGH SEPTEMBER 2017

VLGC Values have remained stable this month.

One MGC vessel has been sold for an undisclosed sale price, Gas Columbia (35,420

CBM, Jul 1997, Mitsubishi HI).

FullyPressurised

Values have softened this month.

No sales have been concluded this month.

Page 10

2ND HAND S&P ACTIVITY SEPTEMBER 2017

+44 (0) 203 026 5555 [email protected]

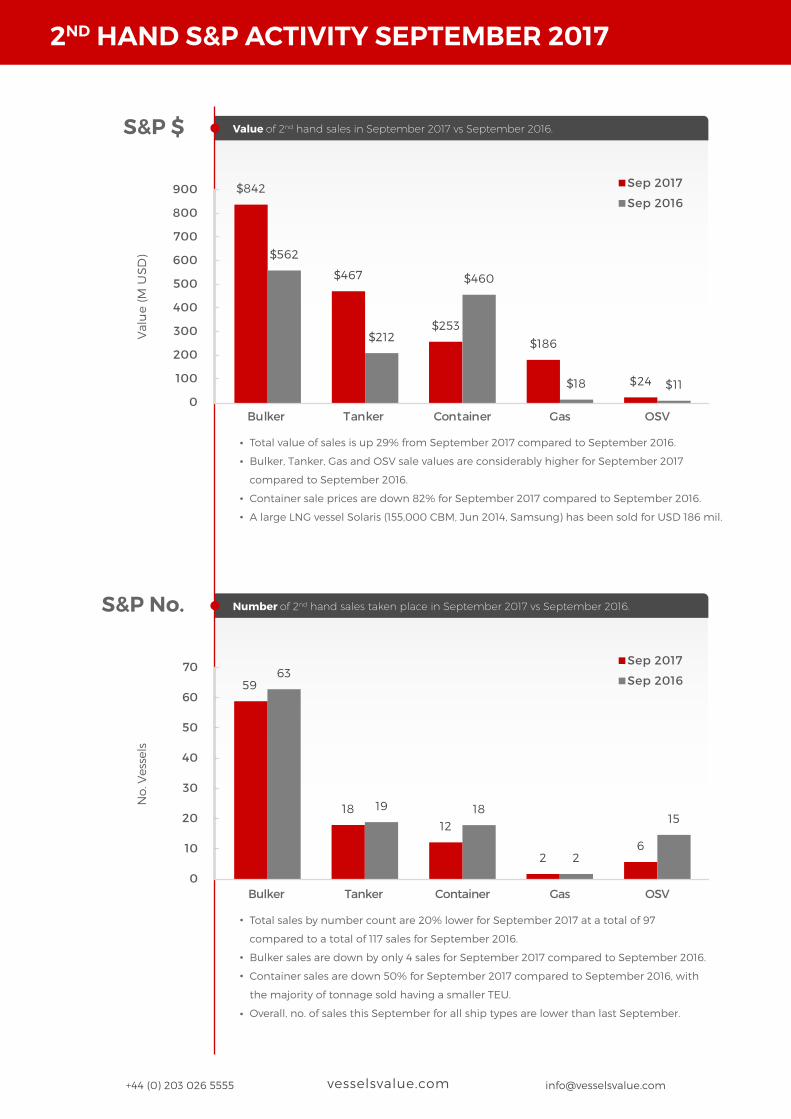

Total value of sales is up 29% from September 2017 compared to September 2016.

Bulker, Tanker, Gas and OSV sale values are considerably higher for September 2017

compared to September 2016.

Container sale prices are down 82% for September 2017 compared to September 2016.

A large LNG vessel Solaris (155,000 CBM, Jun 2014, Samsung) has been sold for USD 186 mil.

Total sales by number count are 20% lower for September 2017 at a total of 97

compared to a total of 117 sales for September 2016.

Bulker sales are down by only 4 sales for September 2017 compared to September 2016.

Container sales are down 50% for September 2017 compared to September 2016, with

the majority of tonnage sold having a smaller TEU.

Overall, no. of sales this September for all ship types are lower than last September.

No

. Ves

sels

Sep 2016

Sep 2017

Number of 2nd hand sales taken place in September 2017 vs September 2016.S&P No.

Bulker Tanker Container Gas OSV

59

1812

26

63

19 18

2

15

0

10

20

30

40

50

60

70

Val

ue

(M U

SD

)

Sep 2016

Sep 2017

Value of 2nd hand sales in September 2017 vs September 2016.S&P $

Bulker Tanker Container Gas OSV

$842

$467

$253

$186

$562

$212

$460

$18 $11$24

0

200

400

100

300

500

600

900

800

700

Page 11

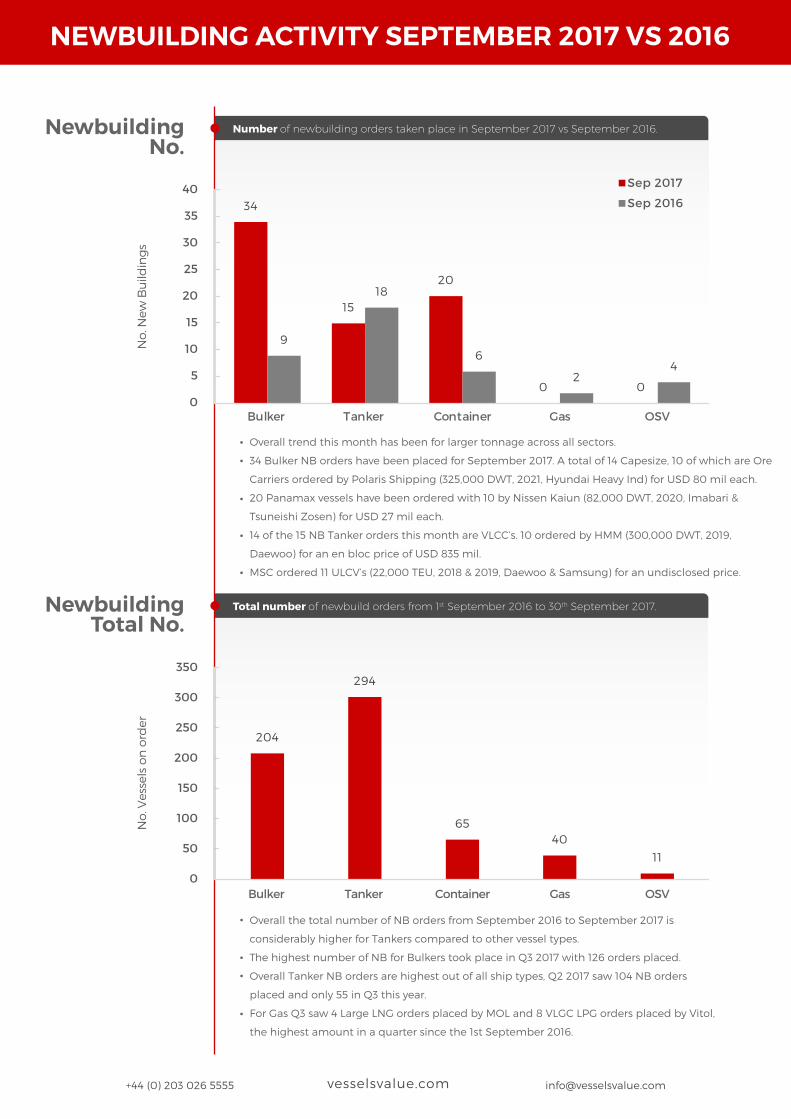

Overall the total number of NB orders from September 2016 to September 2017 is

considerably higher for Tankers compared to other vessel types.

The highest number of NB for Bulkers took place in Q3 2017 with 126 orders placed.

Overall Tanker NB orders are highest out of all ship types, Q2 2017 saw 104 NB orders

placed and only 55 in Q3 this year.

For Gas Q3 saw 4 Large LNG orders placed by MOL and 8 VLGC LPG orders placed by Vitol,

the highest amount in a quarter since the 1st September 2016.

No

. Ves

sels

on

ord

er

Total number of newbuild orders from 1st September 2016 to 30th September 2017.NewbuildingTotal No.

Bulker Tanker Container Gas OSV

204

294

6540

11

0

100

50

150

200

250

300

350

NEWBUILDING ACTIVITY SEPTEMBER 2017 VS 2016

Number of newbuilding orders taken place in September 2017 vs September 2016.NewbuildingNo.

No

. New

Bu

ildin

gs

Sep 2016

Sep 2017

Bulker Tanker Container Gas OSV

34

15

0

20

4

9

18

6

20

0

5

10

15

20

25

40

30

35

+44 (0) 203 026 5555 [email protected]

Overall trend this month has been for larger tonnage across all sectors.

34 Bulker NB orders have been placed for September 2017. A total of 14 Capesize, 10 of which are Ore

Carriers ordered by Polaris Shipping (325,000 DWT, 2021, Hyundai Heavy Ind) for USD 80 mil each.

20 Panamax vessels have been ordered with 10 by Nissen Kaiun (82,000 DWT, 2020, Imabari &

Tsuneishi Zosen) for USD 27 mil each.

14 of the 15 NB Tanker orders this month are VLCC’s. 10 ordered by HMM (300,000 DWT, 2019,

Daewoo) for an en bloc price of USD 835 mil.

MSC ordered 11 ULCV’s (22,000 TEU, 2018 & 2019, Daewoo & Samsung) for an undisclosed price.

Page 12

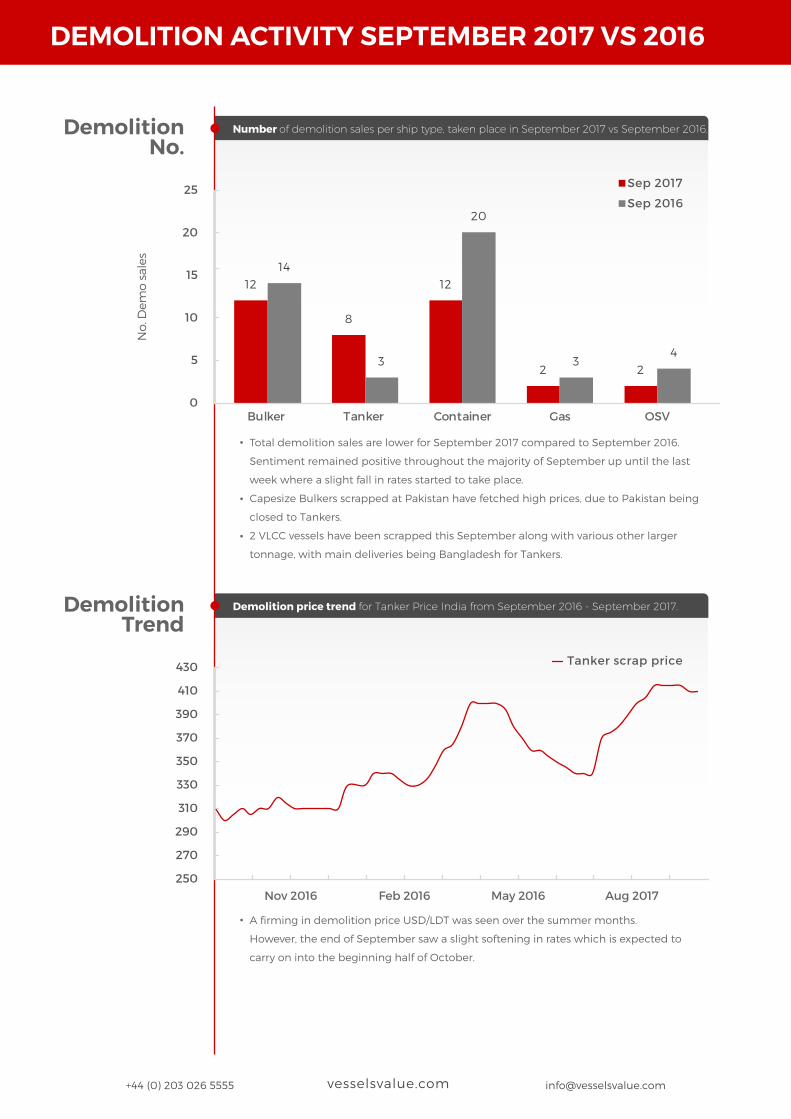

A firming in demolition price USD/LDT was seen over the summer months.

However, the end of September saw a slight softening in rates which is expected to

carry on into the beginning half of October.

Tanker scrap price

Demolition price trend for Tanker Price India from September 2016 - September 2017. DemolitionTrend

250

290

270

350

330

310

410

390

370

430

Aug 2017May 2016Feb 2016Nov 2016

DEMOLITION ACTIVITY SEPTEMBER 2017 VS 2016

+44 (0) 203 026 5555 [email protected]

Number of demolition sales per ship type, taken place in September 2017 vs September 2016.DemolitionNo.

No

. Dem

o s

ales

Sep 2016

Sep 2017

Total demolition sales are lower for September 2017 compared to September 2016.

Sentiment remained positive throughout the majority of September up until the last

week where a slight fall in rates started to take place.

Capesize Bulkers scrapped at Pakistan have fetched high prices, due to Pakistan being

closed to Tankers.

2 VLCC vessels have been scrapped this September along with various other larger

tonnage, with main deliveries being Bangladesh for Tankers.

0

5

10

15

20

25

Bulker Tanker Container Gas OSV

12

8

12

2 2

14

3

20

34

Page 13

Baltic Exchange daily market spot rates for Capesize, Panamax, Supramax andHandy Bulkers from 1st September 2016 - 30th September 2017. Source: Baltic Exchange

(US

D p

er d

ay)

Dry

Continued over supply in the VLCC sector shows a negative market sentiment mid

September putting owners under pressure with a substantial amount of tonnage available

for September. However rates have firmed towards the end of the month in the VLCC sector.

Suezmax rates softened mid September to USD 6,112/day, increasing to USD 10,830/day at

the end of the month.

Aframax rates began to soften towards the end of the month.

Capesize rates have fluctuated this month however have stayed high. Rates reached

levels of USD 21,386/day, the highest number we have seen all year.

Panamax bulkers this month have been slow with a lack of fresh cargo, confirmed by

softening rates towards the end of the month.

Supramax and Handysize rates have also seen reduced activity however rates stayed

stable throughout September.

CapesizePanamaxSupramaxHandy

0

5,000

10,000

15,000

20,000

25,000

CHARTER RATES

+44 (0) 203 026 5555 [email protected]

Baltic Exchange daily market spot rates for VLCC, Suezmax and Aframax Tankersfrom 1st September 2016 - 30th September 2017. Source: Baltic Exchange

(US

D p

er d

ay)

Wet

0

10,000

20,000

30,000

40,000

50,000

60,000

Aug 2017May 2016Feb 2016Nov 2016

VLCCSuezmaxAframax

Aug 2017May 2016Feb 2016Nov 2016

Page 14

Aug 2017May 2016Feb 2016Nov 2016

Aug 2017May 2016Feb 2016Nov 2016

Contex daily time charter rates for Panamax, Handysize and Feedermax Containersfrom 1st September 2016 - 30th September 2017. Source: Contex, VHSS

(US

D p

er d

ay)

Container

VLGC rates have remained stable this month with little variation in rates. Very few fixtures have

taken place this month with a quiet market.

MGC and LEG rates remain stable throughout September, with MGC rates now dropping

below LEG to USD 420,000/month.

Panamax rates have begun to soften again over the past few months.

Handy and Feedermax rates have remained stable throughout the month with a slight

firming in value.

PanamaxHandyFeedermax

4,000

8,000

10,000

6,000

2,000

12,000

CHARTER RATES

+44 (0) 203 026 5555 [email protected]

0

Fearnleys weekly market spot rates for VLGC, MGC and LEG Gas shipsfrom 1st September 2016 - 30th September 2017. Source: Fearnleys

(Th

ou

san

d U

SD

per

mo

nth

)

LPG

VLGCMGCLEG

100

200

300

400

500

600

700

800

900

0