Page 1

The Economist MBA Case Competition 2014

Muddy Waters Investment Competition

Analysis on the Zillow Trulia Merger

Authors Michael Jonas, Juan Guillermo Rintha, Philipp Soechtig

Full-Time MBA Class of 2015

WHU – Otto Beisheim School of Management

Submitted November 3, 2014

Page 2

© WHU – Otto Beisheim School of Management, www.whu.edu Page 2

Table of Contents

1. Introduction to online real estate market .............................................................................. 4

2. Case Questions ..................................................................................................................... 5

a) Which company is getting the better deal and why? ........................................................ 5

b) Does the structure of the deal make sense for each company? ......................................... 8

c) What will the futures likely be for each company on a standalone basis if the

transaction fails to close? .................................................................................................. 8

d) Based on the companies’ present combined market valuations, what assumptions

about their future would you have to make in order to buy stock in the combined

company? ........................................................................................................................ 12

e) What trades, if any, would you recommend around this transaction and why? ............. 16

3. Wrap-up .............................................................................................................................. 19

Page 3

© WHU – Otto Beisheim School of Management, www.whu.edu Page 3

Table of Exhibits

Exhibit 1: Share of visitors ......................................................................................................... 5

Exhibit 2: Future revenues/EBITDA vs. market capitalization ................................................. 6

Exhibit 3: Adj. EBITDA and synergies 2016 ............................................................................. 7

Exhibit 4: M&A deals capped to certain market share ............................................................ 11

Exhibit 5: Market position highly correlated with level of profitability .................................. 13

Exhibit 6: Share prices mainly influenced by three major drivers ........................................... 14

Exhibit 7: Significan premiums at technology M&As ............................................................. 17

Exhibit 8: Benefit from online trend ........................................................................................ 18

Page 4

© WHU – Otto Beisheim School of Management, www.whu.edu Page 4

1. Introduction to online real estate market

The fundamental structure of the American real estate market has not

radically changed in last decade, even after the housing bubble that took

place around seven years ago (CNN, Money & Main St., 2009). The

traditional and largely fragmented way has always facilitated interactions

between the agents, who personally show the properties, and the final

residents, aiming to acquire a new home. However, new virtual

mechanisms prior to those interactions are now widely used and

appreciated by the last mentioned (CNN, Zillow buys Trulia for $3.5

billion, 2014).

The online platforms in this market now store properties from diverse parts

of the country that are uploaded by the real estate agents, and display them

to thousands of people that rate them with their computers and mobile

devices. The largest ones are Zillow and Trulia, followed by others like

Realtor.com, Yahoo! Homes, Homes.com, Redfin, among others. They

provide not only information about houses to buy and to rent, but also

complementary services such as housing valuation, moving-in advice,

mortgage options, interior designer lists, and the like.

The business model of the platforms mostly relies on few streams. For

example, Trulia’s revenue largely depends on the mortgages that are

traded online, the advertisement on its site and the number of properties it

shows. The listings of properties are uploaded by the agents who pay the

platform to publish their information on its website and mobile apps.

Page 5

© WHU – Otto Beisheim School of Management, www.whu.edu Page 5

However, these payments towards Zillow and Trulia represent less than

4% of the total advertisement expenditure that the real estate market invest

(CNN, Zillow buys Trulia for $3.5 billion, 2014). On the other hand, the

platforms have relatively low fixed costs, making the marginal variable

ones (mostly the development of the platform) almost negligible (Refkin).

2. Case Questions

a) Which company is getting the better deal and why?

The merger of Zillow and Trulia seems to be the best that opportunity in

the online real estate market. It can be seen as the beginning of market

consolidation and will create the biggest player by far in the market with

market share of visitors of 24% (inman, 2014) or 3.5 times the second

largest player (see Exhibit 1). This gives market power to the combined

player and will help to negotiate higher fees with agents. On the cost side,

significant cost avoidance can be reached due to economies of scale.

Exhibit 1 Slide 7 © WHU – Otto Beisheim School of Management, www.whu.edu

This deal creates a strong market leader 1.

Source: http://www.inman.com, Team analysis

Share of visitors

December 2013

Opportunity analysis

Market consolidation starts now � First mover advantage is important � Rumors about Trulia trying to acquire Move

(Realtor.com)

Zebra will be by far the biggest player � Dominate the market � Avoid competition with larger ones Other M&A opportunities were even less attractive � Highest synergy potential between Zillow

and Trulia � Acceptable range of visitors overlap

Page 6

© WHU – Otto Beisheim School of Management, www.whu.edu Page 6

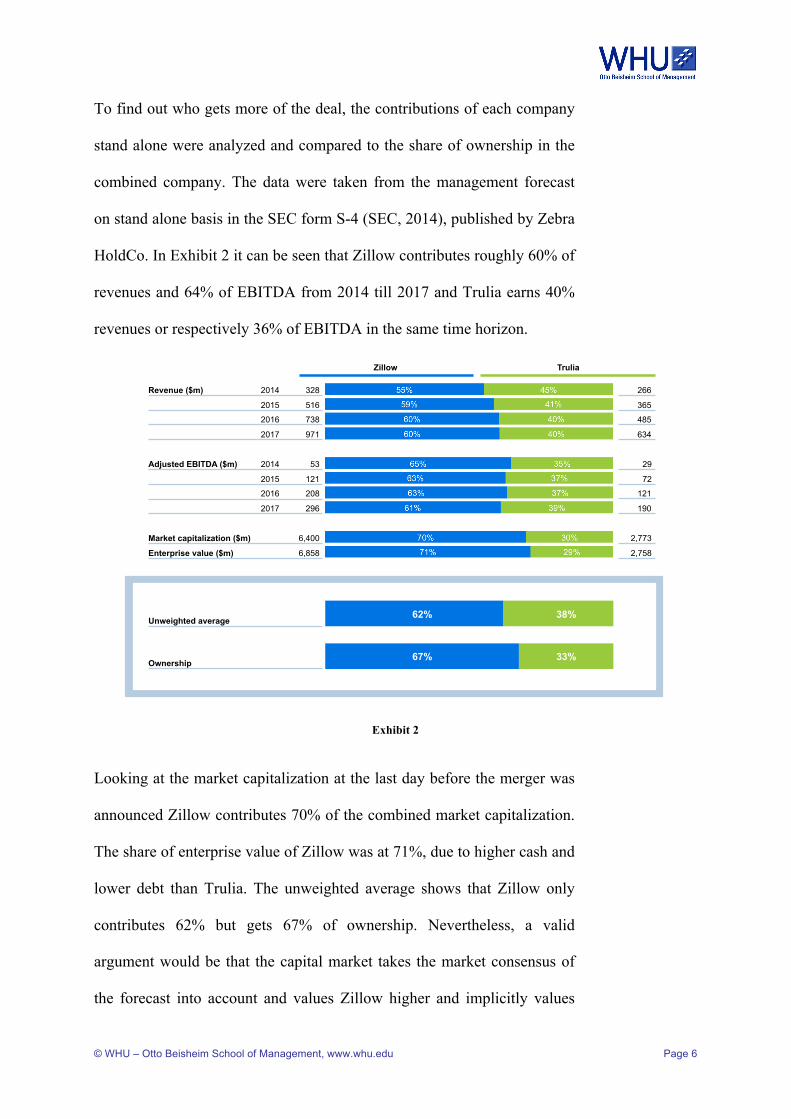

To find out who gets more of the deal, the contributions of each company

stand alone were analyzed and compared to the share of ownership in the

combined company. The data were taken from the management forecast

on stand alone basis in the SEC form S-4 (SEC, 2014), published by Zebra

HoldCo. In Exhibit 2 it can be seen that Zillow contributes roughly 60% of

revenues and 64% of EBITDA from 2014 till 2017 and Trulia earns 40%

revenues or respectively 36% of EBITDA in the same time horizon.

Exhibit 2

Looking at the market capitalization at the last day before the merger was

announced Zillow contributes 70% of the combined market capitalization.

The share of enterprise value of Zillow was at 71%, due to higher cash and

lower debt than Trulia. The unweighted average shows that Zillow only

contributes 62% but gets 67% of ownership. Nevertheless, a valid

argument would be that the capital market takes the market consensus of

the forecast into account and values Zillow higher and implicitly values

Slide 8 © WHU – Otto Beisheim School of Management, www.whu.edu

Future revenues/EBITDA vs. market capitalization

Sources: Zebra Holdco SEC form S-4, Team analysis

Revenue ($m) 2014 328

2015 516

2016 738

2017 971

Adjusted EBITDA ($m) 2014 53

2015 121

2016 208

2017 296

Market capitalization ($m) 6,400

Enterprise value ($m) 6,858

Visitors (m) 81.1

Attention on Google (index) 100.0

Number of agents (000) 56.8 Average revenue per user ($) 320.0

266

365

485

634

29

72

121

190

2,773

2,758

51.6

26.0

73.9

206.0

Zillow Trulia

Unweighted average

Ownership 67% 33%

62% 38%

1.

Page 7

© WHU – Otto Beisheim School of Management, www.whu.edu Page 7

the risk of Trulia’s future revenues and profits higher. Therefore, only

based on this analysis it cannot be said who made the better deal.

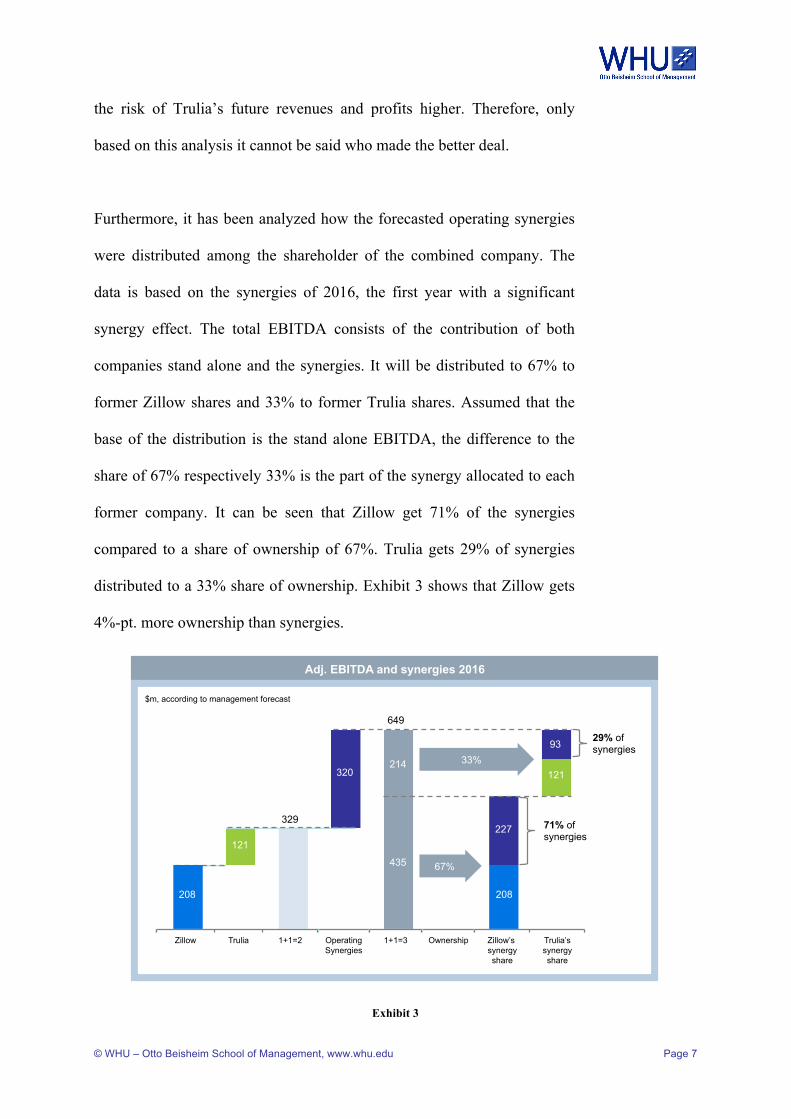

Furthermore, it has been analyzed how the forecasted operating synergies

were distributed among the shareholder of the combined company. The

data is based on the synergies of 2016, the first year with a significant

synergy effect. The total EBITDA consists of the contribution of both

companies stand alone and the synergies. It will be distributed to 67% to

former Zillow shares and 33% to former Trulia shares. Assumed that the

base of the distribution is the stand alone EBITDA, the difference to the

share of 67% respectively 33% is the part of the synergy allocated to each

former company. It can be seen that Zillow get 71% of the synergies

compared to a share of ownership of 67%. Trulia gets 29% of synergies

distributed to a 33% share of ownership. Exhibit 3 shows that Zillow gets

4%-pt. more ownership than synergies.

Exhibit 3 Slide 9 © WHU – Otto Beisheim School of Management, www.whu.edu

Zillow gets slightly higher share of synergies

Sources: Zebra Holdco SEC form S-4, Team analysis

Adj. EBITDA and synergies 2016

$m, according to management forecast

Zillow Trulia 1+1=2 Operating Synergies

1+1=3 Zillow’s synergy share

Trulia’s synergy share

29% of synergies

71% of synergies

208

121

329

320

649

435

214

227

208

121

93 33%

67%

Ownership

1.

Page 8

© WHU – Otto Beisheim School of Management, www.whu.edu Page 8

Taking that into account it seems that Zillow gets a slightly better deal

than Trulia.

b) Does the structure of the deal make sense for each

company?

The deal was structured as a 100% share deal. Trulia’s shareholder will get

0.444 shares of the combined company for each share. No further cash

premium will be paid. Based on the share prices of the last day before the

public announcement of the merger agreement Trulia’s shareholder will

receive a premium of 25%. The volume of the total deal amounts to

$3.5bn. The debt of Trulia will not be repaid.

Looking at the structure of the deal, it stands out that there is no cash

involved and the combined company is not levered any further. Looking

ahead that seems to be reasonable for two reasons. Firstly, cash is needed

to facilitate the organic growth of each company. In particular, building

stronger brands, develop the US online real estate market in terms of better

service to agents and buyer/renters as well as realizing the operating

synergies and do successful post merger integration. The second reason is

the ongoing market consolidation. The combined company will need to

take an active part in that and needs firepower to execute M&A deals

quickly. The process of issuing new shares can be too long to succeed in

acquiring companies, which are interesting to more than one player of the

market, especially when cash premiums come into play after the first offer

and another capital raise is needed.

Page 9

© WHU – Otto Beisheim School of Management, www.whu.edu Page 9

Both companies will operate under a holding company called Zebra

Holdco Inc. Both trademarks will remain in the market. That makes sense

to not lose the visitors visiting both sites. Nevertheless, it is likely that

certain departments will be shared to realize the estimated cost synergies.

Especially in the IT development and maintenance economies of scale can

be gained. The back-end of both platforms can be joined. Furthermore, all

administrative functions like HR or Investors Relations can be merged.

Looking it marketing costs, it can be argued, that both trademarks will

remain and there are no advantages of the merger. However, due to the

fact that the biggest competitor is gone, there is less need to advertise

against each other. Zillow and Trulia will focus und slightly different

market segments and thereby use their resources more efficient.

Considering the no cash deal and the organizational structure of both

companies, the overall deal structure makes sense and fits to the strategy

of the combined company.

c) What will the futures likely be for each company on a

standalone basis if the transaction fails to close?

Both companies, Zillow and Trulia have already entered into an

Agreement and Plan of Merger (“Merger Agreement”) (Zillow, 2014) and

thereby committed to pursue the merger of both companies. Considering

the termination regulations of this Merger Agreement, there is still the

possibility that the planned merger will fail to close.

Page 10

© WHU – Otto Beisheim School of Management, www.whu.edu Page 10

Analyzing all termination options in the Merger Agreement, such as

“mutual written consent (…)”, “if the Initial Effective Time shall not have

occurred (…)”, the case of the other’s companies’ “Board

Recommendation Change (…)”, the main risks can be seen in external

influences. There are chances that Trulia’s stakeholders do not approve the

deal and that an US Governmental Authority classifies this merger as

illegal. While the risk of a lack in Trulia’s stakeholder approval can be

assumed to be low due to the win-win situation both companies get as a

result of this merger, there is a realistic probability that the deal will fail as

antitrust authorities may state objections.

Under Zebra Holdco, Inc. both platforms are supposed to operate as

independent brands because “two brand appeal to a larger audience”, as

Spencer Rascoff, CEO of Zillow states. Fewer than half of Trulia’s

audience visits Zillow and two third of Zillow’s visitors visit Trulia (NBR,

2014). This supports the decision to keep the brands separated. However,

both players already are the biggest companies on the online real estate

market and Zebra Holdco would then cover 24% (inman, 2014) of all US

real estate website visitors as a sum of both independent platforms as

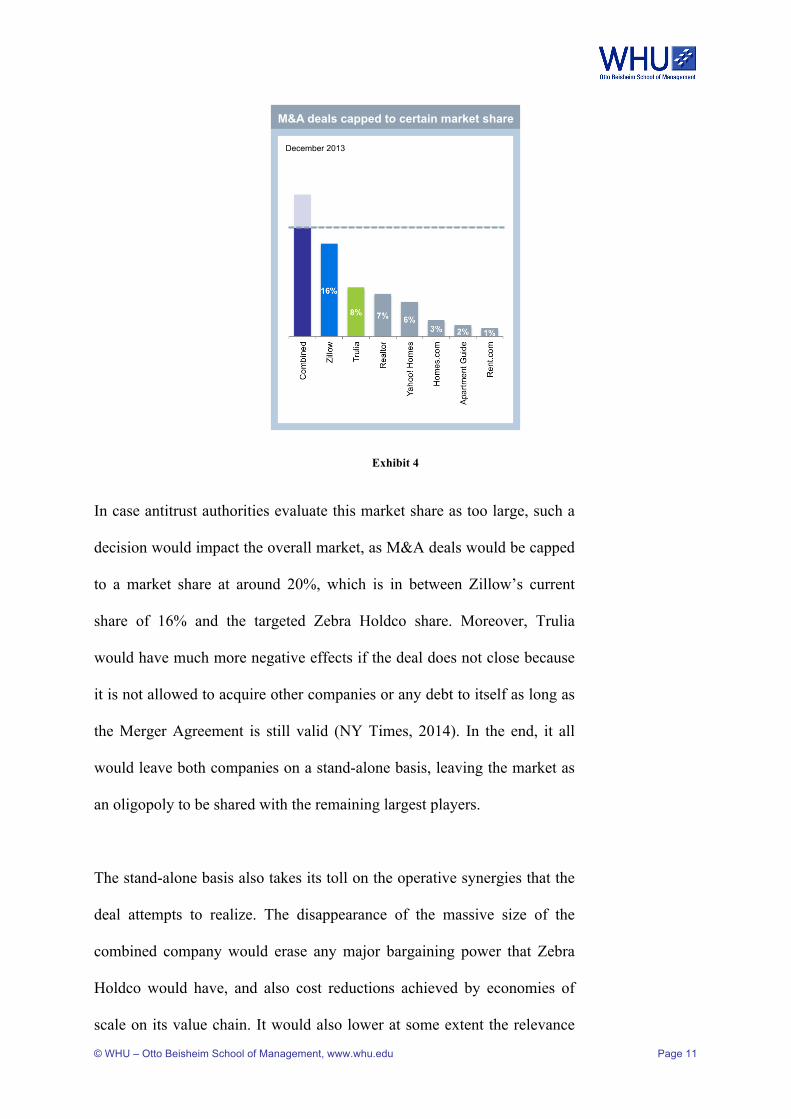

shown in Exhibit 4.

Page 11

© WHU – Otto Beisheim School of Management, www.whu.edu Page 11

Exhibit 4

In case antitrust authorities evaluate this market share as too large, such a

decision would impact the overall market, as M&A deals would be capped

to a market share at around 20%, which is in between Zillow’s current

share of 16% and the targeted Zebra Holdco share. Moreover, Trulia

would have much more negative effects if the deal does not close because

it is not allowed to acquire other companies or any debt to itself as long as

the Merger Agreement is still valid (NY Times, 2014). In the end, it all

would leave both companies on a stand-alone basis, leaving the market as

an oligopoly to be shared with the remaining largest players.

The stand-alone basis also takes its toll on the operative synergies that the

deal attempts to realize. The disappearance of the massive size of the

combined company would erase any major bargaining power that Zebra

Holdco would have, and also cost reductions achieved by economies of

scale on its value chain. It would also lower at some extent the relevance

Slide 11 © WHU – Otto Beisheim School of Management, www.whu.edu

Antitrust issues would impact the overall market

Source: http://www.inman.com, Team analysis

M&A deals capped to certain market share

December 2013

“Living apart together”

Antitrust issues on Zillow and Trulia Merger limit share of visits at ca. 20% � Oligopoly with 3-5 large players � Organic growth more important than

market consolidation � Economies of scale limited Adverse effect on Zillow’s and Trulia’s market valuation � Less operating synergies � Remaining big players � KPIs: Monetization of revenues due to

brand and service quality and management of cost basis

3.

Page 12

© WHU – Otto Beisheim School of Management, www.whu.edu Page 12

of further acquisitions that both companies may pursue and will leave

them with organic growth as the best alternative to increase their own

market share.

A further consequence of this scenario would be the necessity from the

companies to rely on the past perceptions the customers and agents already

had about them. This means that their brands and quality of service would

be the first most influential assets they will rely on after the merge attempt

to keep as the largest players in the market. Overall, a deal failure would

have adverse effect on Zillow’s and Trulia’s market valuation.

d) Based on the companies’ present combined market

valuations, what assumptions about their future

would you have to make in order to buy stock in the

combined company?

The combined market valuation of Zebra Holdco adds up to 9,173 m$ and

can is estimated by combining both the market capitalization of Zillow

(6,400 m$) and Trulia (2,773 m$). In order to buy stock in the combined

company, an increase in the share price must be expected. While there is

the argument that Zillow’s market capitalization alone with a price-to-

share ratio of 20 is already significantly higher compared to other internet

companies such as LinkedIn with a price-to-share ratio of 12, TripAdvisor

(12) and Yelp (16) (Barron's, 2014), there is the possibility of Zebra

Holdco’s share price increase under the following assumptions:

Page 13

© WHU – Otto Beisheim School of Management, www.whu.edu Page 13

Assumption 1:

An increase in market size of the combined company will lead to

an increased EBITDA margin compared to Zillow and Trulia on

a standalone basis.

With the combined visitor share of 24%, Zillow and Trulia are 3.5 times

bigger than the then second largest competitor Realtor.com. Considering

the correlation between market position and the level of profitability of

other internet firms there is a high probability that Zebra Holdco’s share

price will positively influenced by an increased EBITDA margin as shown

in Exhibit 5.

Exhibit 5

Slide 12 © WHU – Otto Beisheim School of Management, www.whu.edu

Market position highly correlated with level of profitability

EBITDA margins up to 70%

Sources: capital IQ, company information, ZU analysis, Bertelsmann SE

4.

1x 3-5x 8-10x

5-30

30-50

50-70

100

Zillow

Immobilien Scout 24

rightmove.uk

REA Group

leboncoin.fr blocket

bytbil.com carsales.com.au

FINN seek

Jobindex

seloger.com

Auto Trader

Auto Scout 24

monster.com

Size versus second player

EB

ITD

A m

argi

n (%

)

Trulia

Zebra

Real estate platforms

Page 14

© WHU – Otto Beisheim School of Management, www.whu.edu Page 14

The higher profitability is a likely result of higher synergies of scale and

operating synergies of 320 m$ as introduced above. It gives the combined

companies further growth potential, which potentially leads to investors’

phantasies about the optimistic future development of Zebra Holdco.

Assumption 2:

Three major drivers mainly influence share prices: Revenue,

numbers of visitors, number of agents registered

Exhibit 6 shows that both Zillow’s and Trulia’s share price development

was highly correlated to financial and operational figures from the

respective past quarters:

• Revenue

• Number of visitors

• Number of agents registered

Exhibit 6

It can be assumed that due to a stronger market position of both companies

all three parameters will increase leading to an increased stock price. This

development is supported, as both platform brands are to operate Slide 13 © WHU – Otto Beisheim School of Management, www.whu.edu

Online and mobile trend will help Zebra to realize synergies

98%

0

40

80

01.10.12 01.10.13 01.10.14 Q3/12 Q3/13 Q3/14

0

60

120

180

01.10.12% 01.10.13% 01.10.14%Q3/12 Q3/13 Q3/14

Zillow Trulia

98%

97%

Revenue (m$) 78%

90%

73%

Visitors (m)

Agents (000)

Share prices mainly influenced by three major drivers (correlations in %)

Sources: Zillow, Trulia, Bloomberg, Morgan Stanley, UBS

4.

Page 15

© WHU – Otto Beisheim School of Management, www.whu.edu Page 15

separately which reduces the risk of agent/visitor overlap elimination.

Furthermore, both platforms can introduce volume discounts for agents,

which motivate to place real estate listings on both platforms. This again

raises revenues. As further visitors are attracted by more comprehensive

real estate databases, this figure will most probably increase as well and

also drive revenues from third party advertisements on the Zillow’s and

Trulia’s websites.

Assumption 3:

There is a significant growth potential in the online real estate

market, from which Zebra Holco’s share price will very likely

benefit.

90% of US Americans begin their home searches online. In addition to

this, Zillow and Trulia currently cover only 4% of all US American real

estate agencies’ marketing spend, which is estimated at 12 bn$ per year

(CNN, Zillow buys Trulia for $3.5 billion, 2014).

The real estate market can be described as stable and the clear trend

towards online and mobile real estate search gives rise to further growth

opportunities for the combined company. In this context, Zebra Holdco’s

growth is strongly supported by the synergy advantages, e.g. when it

comes to the joint development of new smartphone apps and the marketing

of both platforms. This cost optimized approach in a growing market will

most likely result in a favorable stock price development.

Page 16

© WHU – Otto Beisheim School of Management, www.whu.edu Page 16

e) What trades, if any, would you recommend around

this transaction and why?

The merger transaction of Zillow and Trulia can be seen as the starting

point in the US American online real estate market consolidation. In order

to further exist on a competitive level, other real estate platforms are

forced to grow. As such a growth is organically not possible at the high

speed required, it can be assumed that other players will merge as well in

order to gain size from acquisitions.

Trading recommendation 1: Buy shares of Move, Inc.

The real estate website Realtor.com will become the second largest

platform visitor-wise in case the Zillow/Trulia merger succeeds. A clear

buying recommendation for the shares of Move, Inc., the operator of

Realtor.com can be formulated, as two scenarios seem likely:

(1) Zebra Holdco or another participant in the online real estate

market, such as Yahoo! Homes, acquires Move. In this case

Move’s share prices potentially increase due to a premium paid on

the share price by the acquiring company. Exhibit 7 shows

premiums, which have been paid on 638 technology M&A

transactions with a deal volume of >100 m$ and change of control

considered since 2004.

Page 17

© WHU – Otto Beisheim School of Management, www.whu.edu Page 17

Exhibit 7

(2) Move acquires another market participant. In this case, Move’s

share prices are likely to increase because of the company’s growth

potential with regards to increased revenues, visitors and agents

registered analogue to the correlations discussed above.

Trading recommendation 2: Buy shares of Wayfair LLC.

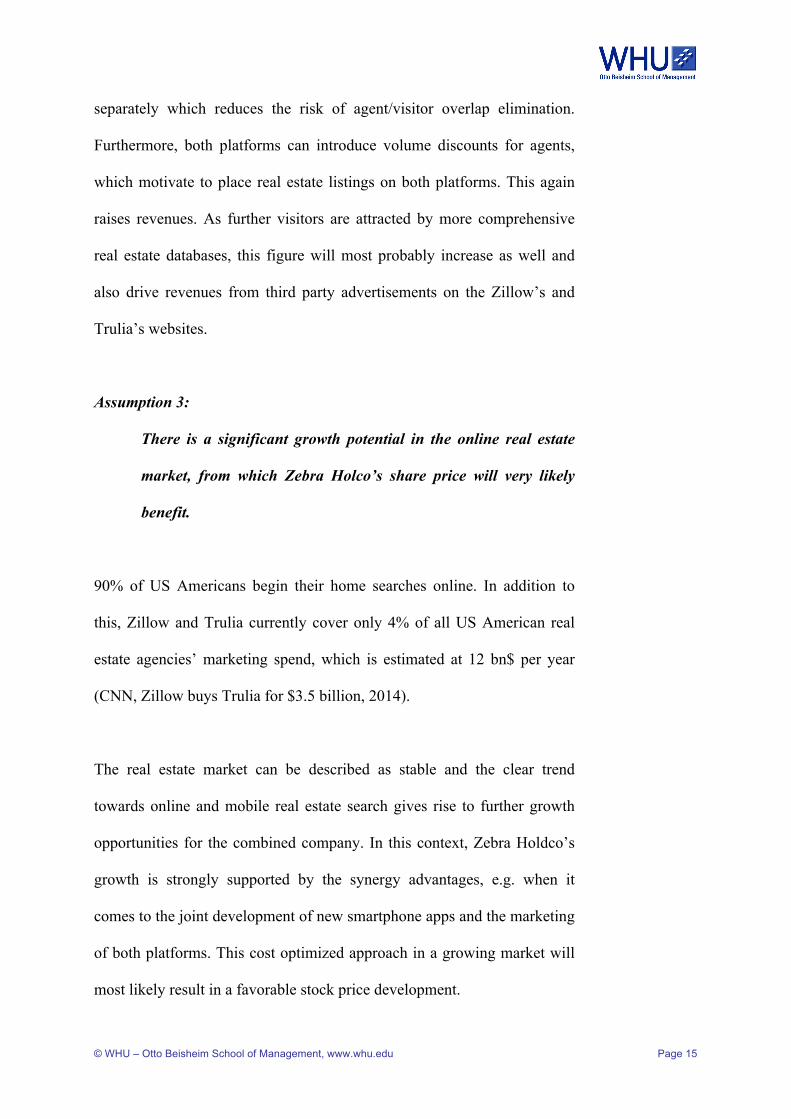

There are companies that might benefit from the online trend for real estate

searches. Exhibit 8 shows potential real estate buyers/renters needs along

the process chain. While Zillow and Trulia already cover the home search

process and act as a broker for mortgages, both can furthermore direct

customers to insurance companies and remover agencies or craftsmen

platforms, which are related to the process steps “close the deal” and

“move to new home”. These companies have the opportunity to advertise

Slide 14 © WHU – Otto Beisheim School of Management, www.whu.edu

Trading recommendation around the Zillow and Trulia Merger

Source: Zebra Holdco SEC form S-4, Team analysis

Significant premiums at technology M&As Benefit from online trend

Deal volume >$100m and change of control transactions considered

638 transactions since 2004

Home search

� Core business � Starting point for customer

Close the deal

� Act as mortgage broker � Offer insurance for new

home

Move to new home

� Remover agency service � Offer craftsmen platform

Home search

� Home improvement � Interior design � Online furniture shop

Trading recommendation: Move, Inc. Trading recommendation: Wayfair LLC.

5.

Page 18

© WHU – Otto Beisheim School of Management, www.whu.edu Page 18

on online real estate platforms and benefit from an increased marketing

coverage, as their target group, the home buyers/renters, can increasingly

be addressed on the real estate websites. This at the end might positively

influence revenues and growth of the third parties and lead to a share price

increase.

Exhibit 8

Wayfair LLC. covers a wide range of services in the process step “make it

your home”. The website Wayfair.com offers home improvement advices

and suggests interior designs. Furniture can be purchased online on this

website. Besides advertising on Zillow and Trulia, Wayfair LLC. could

enter into a cooperation with Zebra Holdco and e.g. offer a 5% welcome

discount to customers who contacted the real estate agent via Zillow or

Trulia. By doing so, Wayfair LLC. would also benefit from increased

growth potential and consequently rising share prices as discussed above.

Slide 14 © WHU – Otto Beisheim School of Management, www.whu.edu

Trading recommendation around the Zillow and Trulia Merger

Source: Zebra Holdco SEC form S-4, Team analysis

Significant premiums at technology M&As Benefit from online trend

Deal volume >$100m and change of control transactions considered

638 transactions since 2004

Home search

� Core business � Starting point for customer

Close the deal

� Act as mortgage broker � Offer insurance for new

home

Move to new home

� Remover agency service � Offer craftsmen platform

Make it your home

� Home improvement � Interior design � Online furniture shop

Trading recommendation: Move, Inc. Trading recommendation: Wayfair LLC.

5.

Page 19

© WHU – Otto Beisheim School of Management, www.whu.edu Page 19

3. Wrap-up

Recapitulatory, the merger of Zillow and Trulia will change the online real

estate market quite a lot. The strong combined company will use its

bargaining power and exploit economies of scales. Further consolidation is

likely will affect other companies significantly.

1. Which company is getting the better deal and why?

Zillow gets a slightly better deal based on market capitalization and share

of synergies.

2. Does the structure of the deal make sense for each company?

The structure makes sense because it facilitates further organic and

inorganic growth for both.

3. What will the futures likely be for each company on a standalone

basis if the transaction fails to close?

Antitrust issues may cause a failure and will lead to a living apart together

scenario with lower valuations.

4. What assumptions about their future would you have to make in

order to buy stock in the combined company?

Online and mobile trends remain strong and monetize; operating synergies

will be exploited as planed.

Page 20

© WHU – Otto Beisheim School of Management, www.whu.edu Page 20

5. What trades, if any, would you recommend around this transaction

and why?

Participate in further M&A deals and benefit from online trend in real

estate and related markets.

Page 21

© WHU – Otto Beisheim School of Management, www.whu.edu Page 21

List of References

Barron's. (August 09, 2014). Zillow Shares Could Fall By Half. Retrieved October 28, 2014, from http://online.barrons.com/articles/SB50001424053111904329504580071503076700616

CNN. (January 29, 2009). Money & Main St. Retrieved October 26, 2014, from How a 'perfect storm' led to the economic crisis: http://www.cnn.com/2009/US/01/29/economic.crisis.explainer/index.html?_s=PM:US

CNN. (July 28, 2014). Zillow buys Trulia for $3.5 billion. Retrieved October 27, 2014, from http://money.cnn.com/2014/07/28/real_estate/zillow-buys-trulia-for-3-5-billion/

CNN. (July 28, 2014). Zillow CEO: Why Trulia is worth it. Retrieved October 28, 2014, from http://money.cnn.com/video/news/2014/07/28/zillow-ceo-trulia-deal.cnnmoney/

inman. (February 04, 2014). Visits to real estate websites surge 25 percent from December to January. Retrieved October 21, 2014, from http://www.inman.com/2014/02/04/visits-to-real-estate-websites-surge-25-percent-from-december-to-january/

NBR. (July 28, 2014). Why Trulia deal won’t fix Zillow’s stock for long. Retrieved October 29, 2014, from http://nbr.com/2014/07/28/why-trulia-deal-wont-fix-zillows-stock-for-long/

NY Times. (July 31, 2014). Deal Book. Retrieved October 26, 2014, from http://dealbook.nytimes.com/2014/07/31/in-deal-for-real-estate-listing-trulia-zillow-comes-out-on-top/?_r=0

Refkin, J. The zero marginal cost society.

Zillow, I. (July 28, 2014). Form 8-K. Retrieved October 21, 2014, from http://investors.zillow.com/secfiling.cfm?filingID=1193125-14-284607&CIK=1334814