This document is for the use of the recipient only and should not be copied or distributed to any other person or entity. Please refer to important disclosures at the end of this presentation. Credit report Credit Research Norske Skog 25 November 2019 Analyst: Glenn Kringhaug +47 22 01 61 62 27 November 2019

Transcript

This document is for the use of the recipient only and should not be copied or distributed to

any other person or entity.

Please refer to important disclosures at the end of this presentation.

Credit report

Credit Research

Norske Skog

25 November 2019

Analyst: Glenn Kringhaug +47 22 01 61 62

27 November 2019

Key Terms

2

Source: ABG Sundal Collier

Issuer Norske Skog AS

GuarantorsMaterial group companies Norske Skog (Australasia) Pty Ltd, Norske Skog Bruck GmbH, Norske Skog Skogn AS, Norske Skog Saugbrugs AS, Norske Skog Golbey SAS,

Norske Skog Industries Australia Ltd., Norske Skog Tasman Ltd., Norske Skog Paper Mills (Australia) Ltd., Norske Skog Paper Mills (Albury) Pty Ltd., and Nornews A/S

Issue amount EUR 125m

Tenor 3 years, maturity 14 June 2022

Amortization 100% repayment at final maturity (bullet)

Status Senior secured (subject to the super-senior status of the RCF, guarantee facility and permitted hedging sharing security with the bonds)

Security(i) Share pledges over the Guarantors, (ii) fixed and floating charge security over (a) Saugbrugs mill, (b) the Skogn mill, the (c) the Tasman mill, the (d) Albury mill and (e) the

Boyer mill, (iii) assignment of shareholder loans and assignment of intercompany loans

Call options Make-whole first 18 months, callable thereafter (all or nothing) at par plus 50%/30%/10% of the initial Coupon after 18/24/30 months, respectively

Equity claw-back Up to 35% of issue amount may be repaid at first call price by primary proceeds raised through an IPO

Special covenants Special covenants include restrictions on shareholder distributions, negative pledge, financial support, financial indebtedness, subsidiaries distributions

Maintenance

covenants

• NIBD/EBITDA shall not exceed 2.75x

• Liquidity (free cash) shall exceed NOK 100,000,000

Incurrence tests With respect to dividend payments, NIBD / EBITDA shall not exceed 2.00x

Dividend restrictions Up to 75% of last years adjusted net profit, subject to the incurrence test being met

Permitted additional

debt

(i) RCF of maximum EUR 31m (annual clean down provisions), (ii) permitted hedging, (iii) guarantee facility, (iv) factoring facility of maximum EUR 40m, (v) financial leasing of

maximum EUR 12m, (vi) leasing in the ordinary course of business that would have been classified as an operational lease prior to the implementation of IFRS 16, (vii) Saugbrug

project facility (NOK 94m), (viii) Golbey loans of maximum EUR 8m, (ix) Bruck boiler facility of maximum EUR 58m (which is subject to the incurrence test being met at

commitment), (x) any credit facility provided by any governmental institution of maximum EUR 10m, (xi) intra-company loans, (xii) subordinated shareholder loans, (xiii) debt in

acquired entities if refinanced within 3 months and (xiv) a general basket of EUR 5m

Permitted disposal The group may freely sell or dispose (i) the Albury mill, (ii) the forest estates in Tasmania, (iii) the Bruck hydro plant, (iv) the Saugbrugs development properties

Change of control Bondholder’s put option at 101% of par value

Documentation /

TrusteeNorwegian law documentation (relevant jurisdictions for security documents) / Nordic Trustee

Credit summary

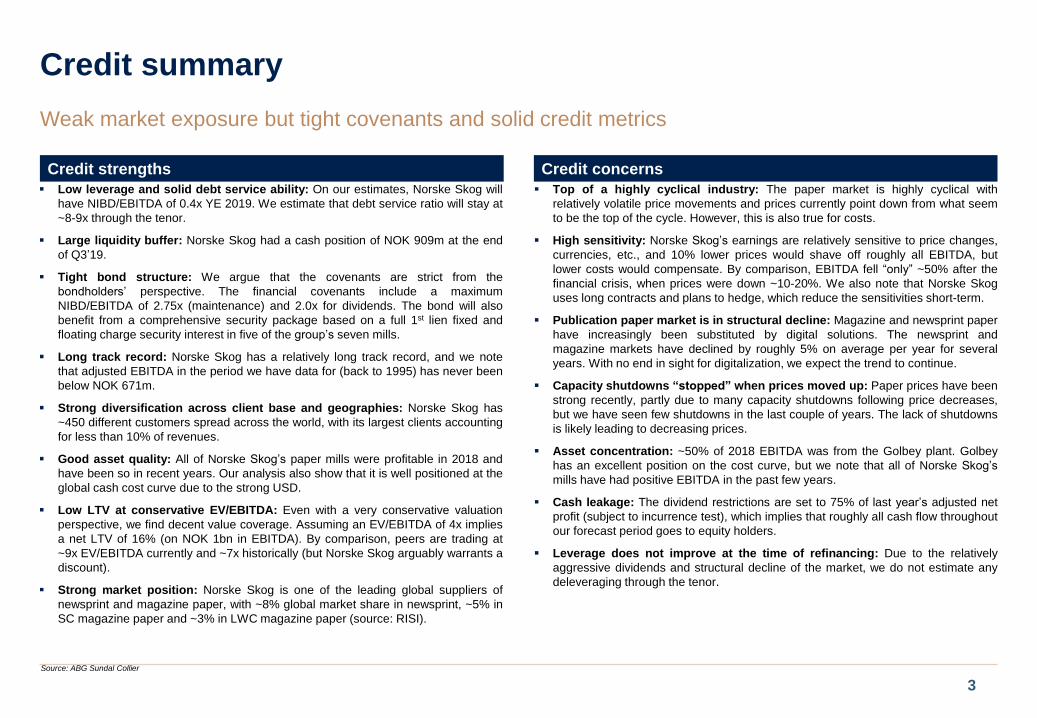

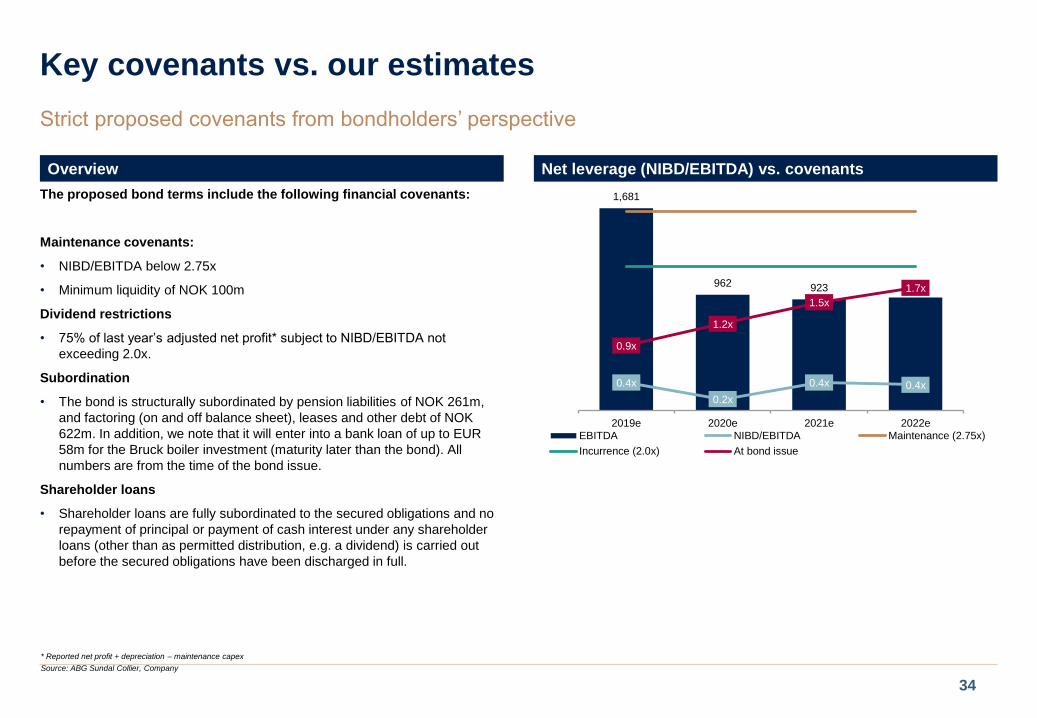

Low leverage and solid debt service ability: On our estimates, Norske Skog will

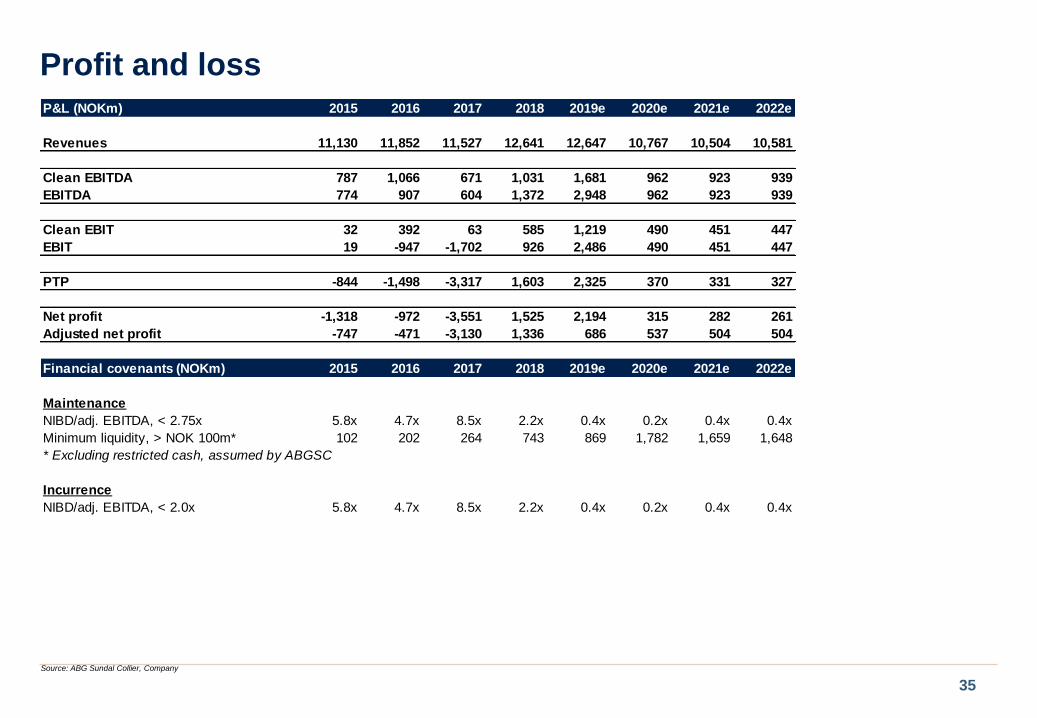

have NIBD/EBITDA of 0.4x YE 2019. We estimate that debt service ratio will stay at

~8-9x through the tenor.

Large liquidity buffer: Norske Skog had a cash position of NOK 909m at the end

of Q3’19.

Tight bond structure: We argue that the covenants are strict from the

bondholders’ perspective. The financial covenants include a maximum

NIBD/EBITDA of 2.75x (maintenance) and 2.0x for dividends. The bond will also

benefit from a comprehensive security package based on a full 1st lien fixed and

floating charge security interest in five of the group’s seven mills.

Long track record: Norske Skog has a relatively long track record, and we note

that adjusted EBITDA in the period we have data for (back to 1995) has never been

below NOK 671m.

Strong diversification across client base and geographies: Norske Skog has

~450 different customers spread across the world, with its largest clients accounting

for less than 10% of revenues.

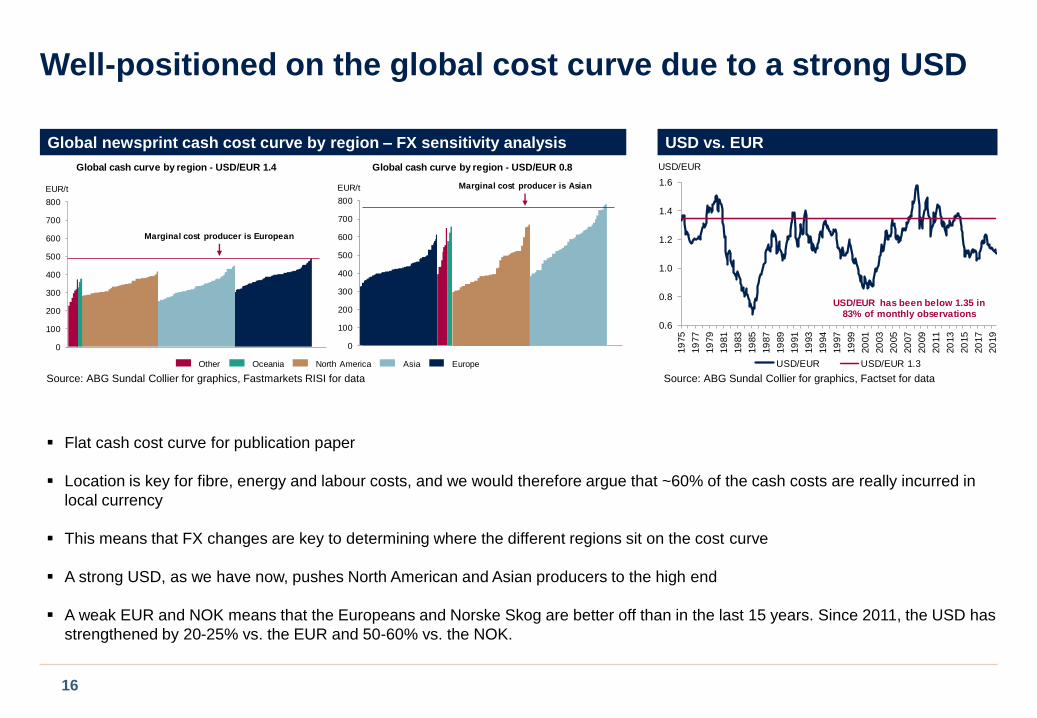

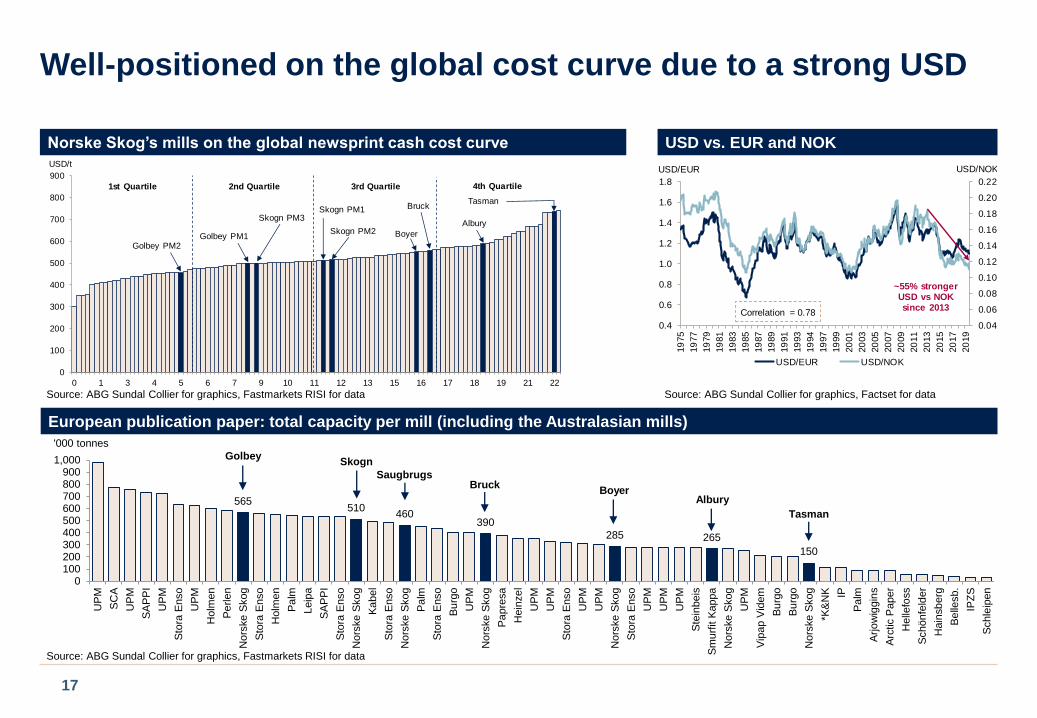

Good asset quality: All of Norske Skog’s paper mills were profitable in 2018 and

have been so in recent years. Our analysis also show that it is well positioned at the

global cash cost curve due to the strong USD.

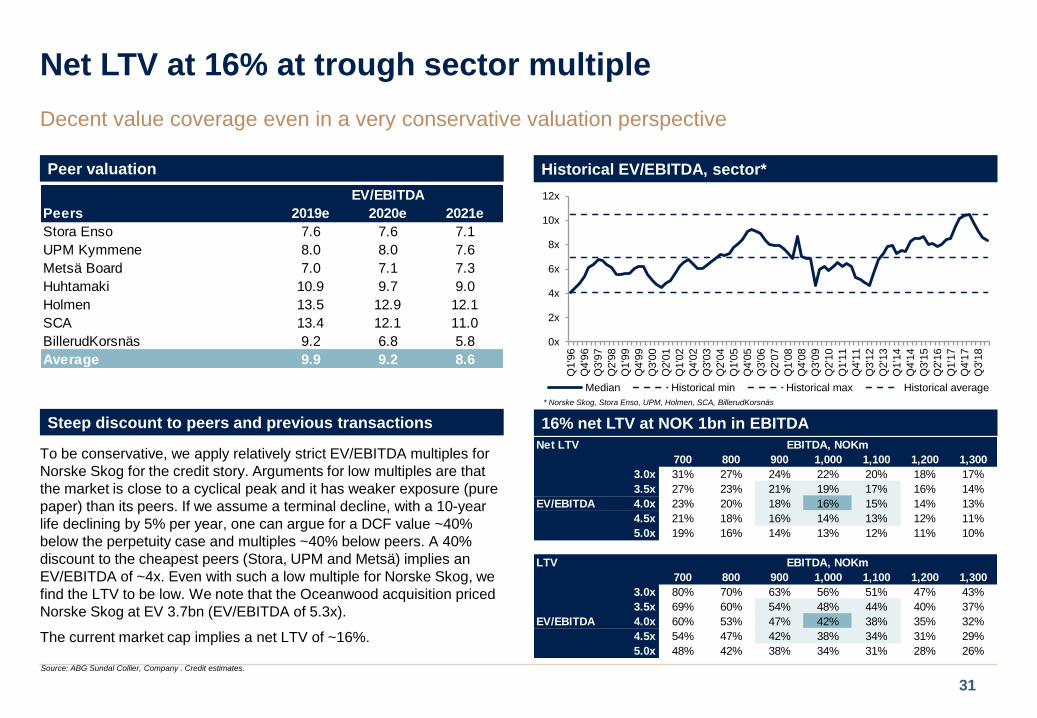

Low LTV at conservative EV/EBITDA: Even with a very conservative valuation

perspective, we find decent value coverage. Assuming an EV/EBITDA of 4x implies

a net LTV of 16% (on NOK 1bn in EBITDA). By comparison, peers are trading at

~9x EV/EBITDA currently and ~7x historically (but Norske Skog arguably warrants a

discount).

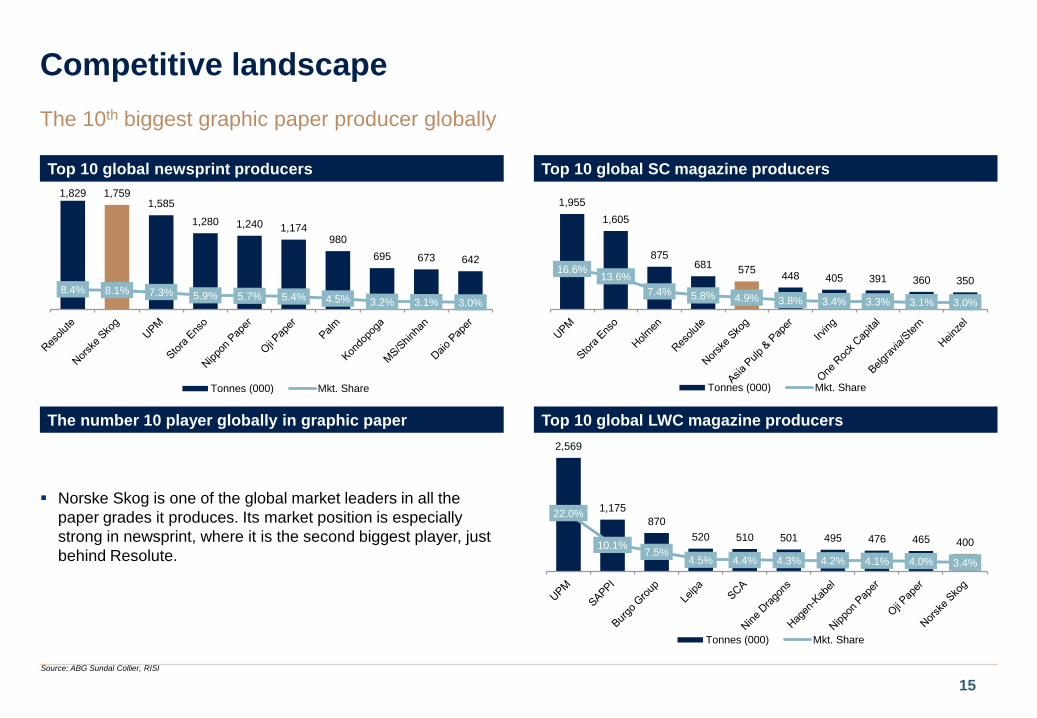

Strong market position: Norske Skog is one of the leading global suppliers of

newsprint and magazine paper, with ~8% global market share in newsprint, ~5% in

SC magazine paper and ~3% in LWC magazine paper (source: RISI).

3

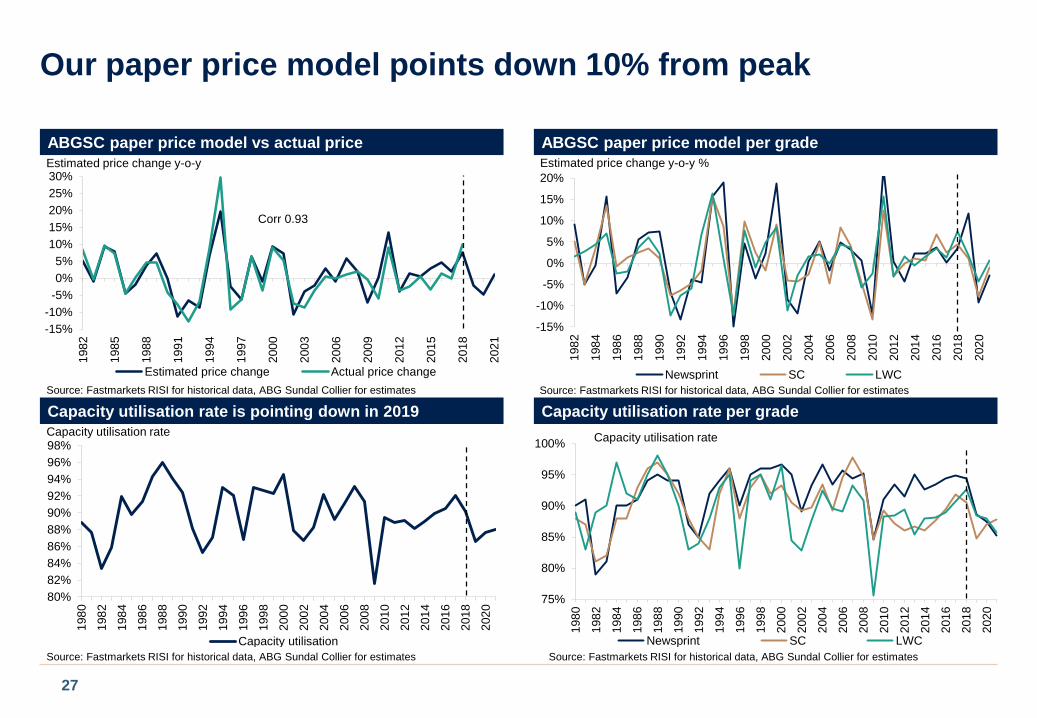

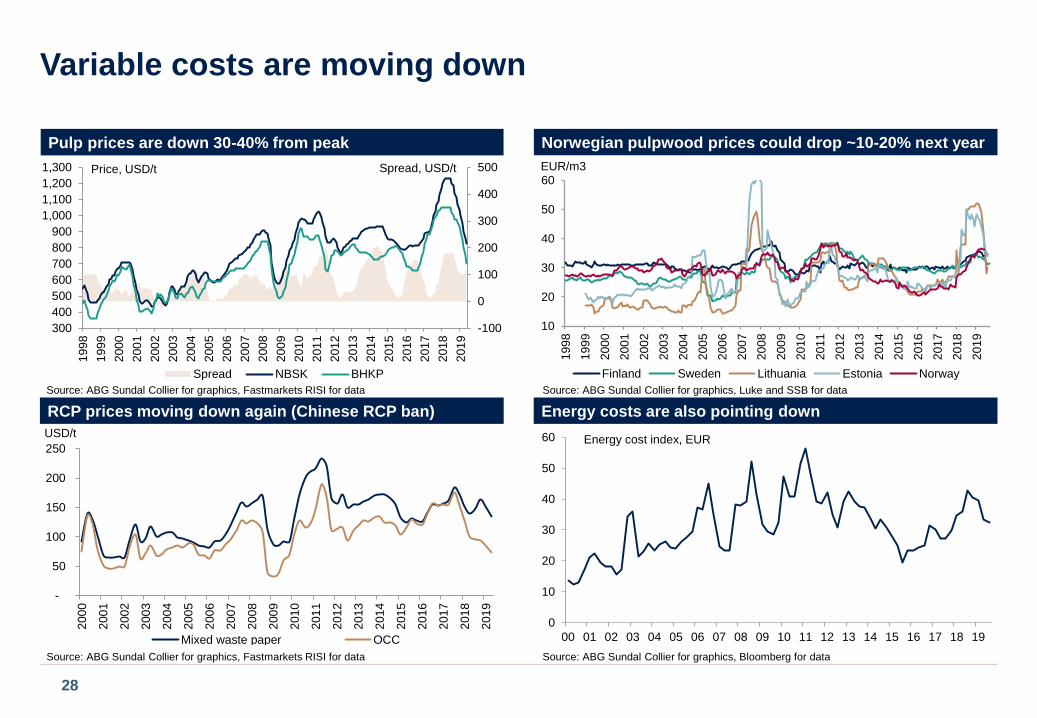

Top of a highly cyclical industry: The paper market is highly cyclical with

relatively volatile price movements and prices currently point down from what seem

to be the top of the cycle. However, this is also true for costs.

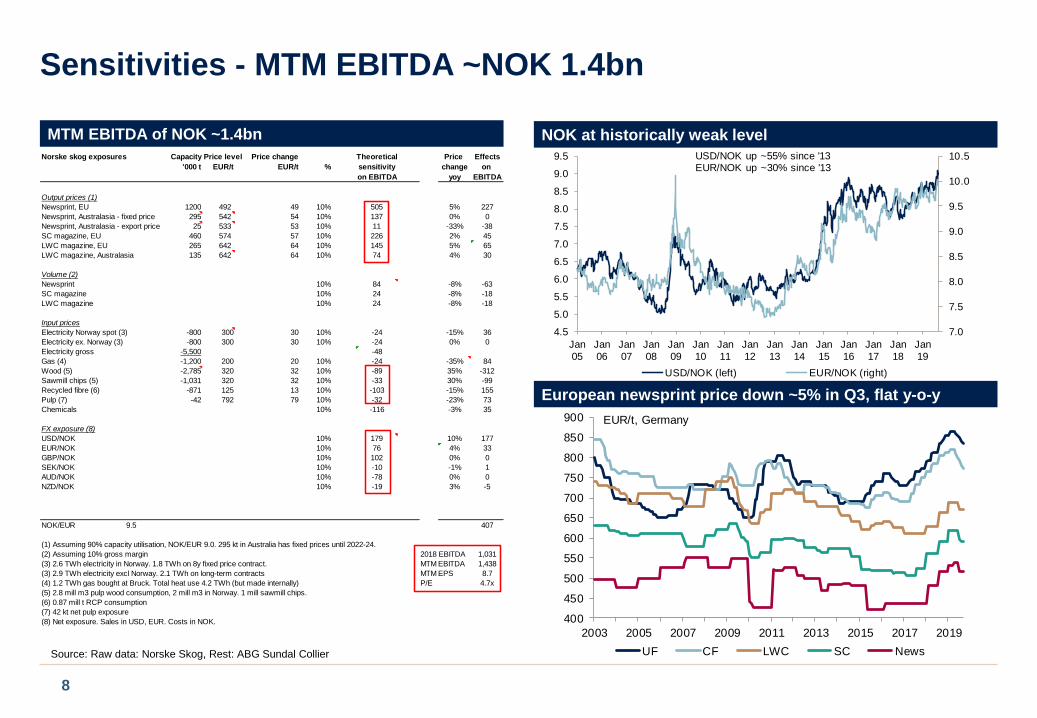

High sensitivity: Norske Skog’s earnings are relatively sensitive to price changes,

currencies, etc., and 10% lower prices would shave off roughly all EBITDA, but

lower costs would compensate. By comparison, EBITDA fell “only” ~50% after the

financial crisis, when prices were down ~10-20%. We also note that Norske Skog

uses long contracts and plans to hedge, which reduce the sensitivities short-term.

Publication paper market is in structural decline: Magazine and newsprint paper

have increasingly been substituted by digital solutions. The newsprint and

magazine markets have declined by roughly 5% on average per year for several

years. With no end in sight for digitalization, we expect the trend to continue.

Capacity shutdowns “stopped” when prices moved up: Paper prices have been

strong recently, partly due to many capacity shutdowns following price decreases,

but we have seen few shutdowns in the last couple of years. The lack of shutdowns

is likely leading to decreasing prices.

Asset concentration: ~50% of 2018 EBITDA was from the Golbey plant. Golbey

has an excellent position on the cost curve, but we note that all of Norske Skog’s

mills have had positive EBITDA in the past few years.

Cash leakage: The dividend restrictions are set to 75% of last year’s adjusted net

profit (subject to incurrence test), which implies that roughly all cash flow throughout

our forecast period goes to equity holders.

Leverage does not improve at the time of refinancing: Due to the relatively

aggressive dividends and structural decline of the market, we do not estimate any

deleveraging through the tenor.

Credit strengths Credit concerns

Source: ABG Sundal Collier

Weak market exposure but tight covenants and solid credit metrics

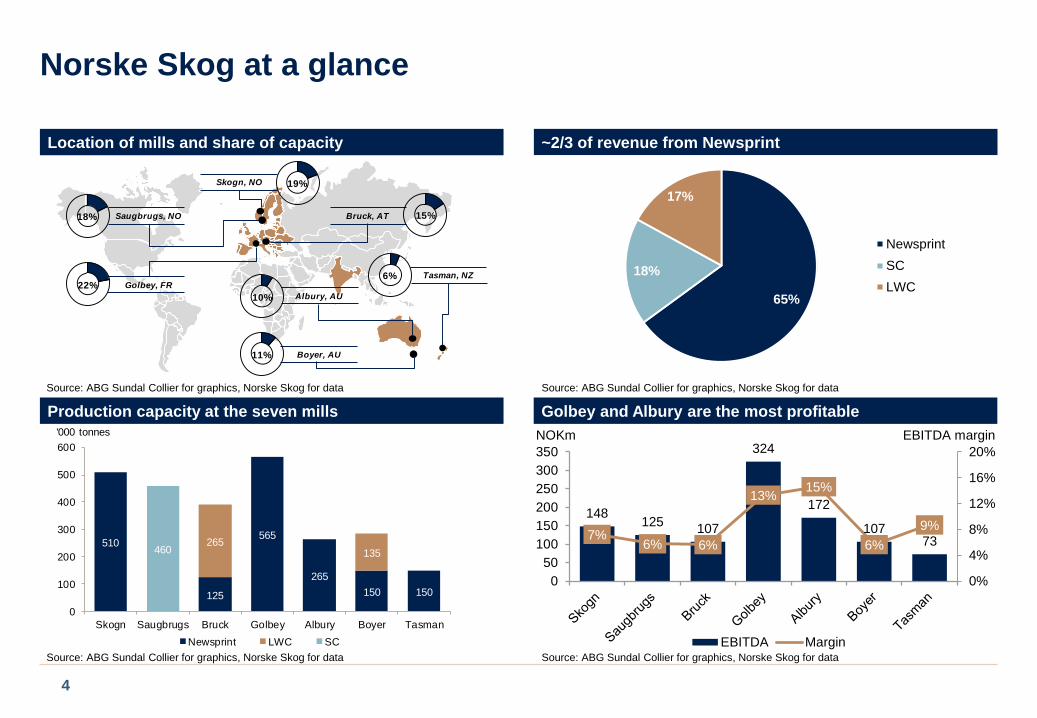

Albury, AU

Tasman, NZ

Boyer, AU

Golbey, FR

Bruck, AT

Skogn, NO

Saugbrugs, NO18%

22%

10%

15%

11%

6%

19%

510

125

565

265

150 150

265135460

0

100

200

300

400

500

600

Skogn Saugbrugs Bruck Golbey Albury Boyer Tasman

Newsprint LWC SC

'000 tonnes

Norske Skog at a glance

4

Location of mills and share of capacity ~2/3 of revenue from Newsprint

Golbey and Albury are the most profitable

148125

107

324

172

10773

7%6% 6%

13%15%

6%

9%

0%

4%

8%

12%

16%

20%

0

50

100

150

200

250

300

350

EBITDA Margin

NOKm EBITDA margin

Source: ABG Sundal Collier for graphics, Norske Skog for data

Production capacity at the seven mills

65%

18%

17%

Newsprint

SC

LWC

Source: ABG Sundal Collier for graphics, Norske Skog for data

Source: ABG Sundal Collier for graphics, Norske Skog for dataSource: ABG Sundal Collier for graphics, Norske Skog for data

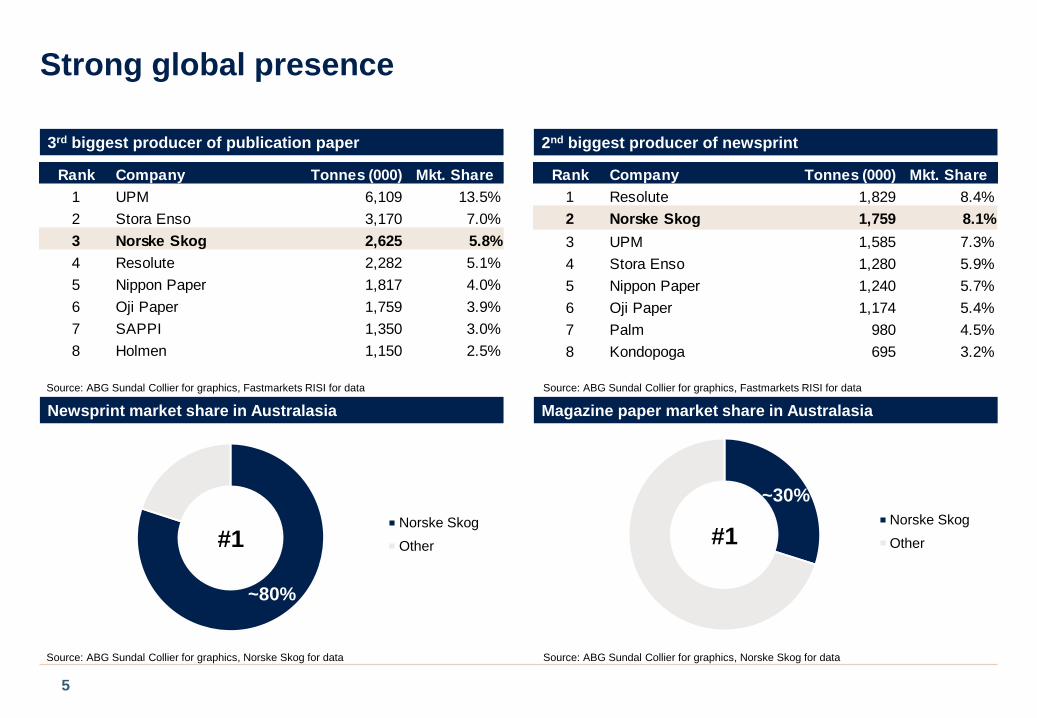

Norske Skog

Other#1

~80%

Norske Skog

Other#1

~30%

Strong global presence

5

3rd biggest producer of publication paper 2nd biggest producer of newsprint

Newsprint market share in Australasia Magazine paper market share in Australasia

Source: ABG Sundal Collier for graphics, Norske Skog for dataSource: ABG Sundal Collier for graphics, Norske Skog for data

Source: ABG Sundal Collier for graphics, Fastmarkets RISI for dataSource: ABG Sundal Collier for graphics, Fastmarkets RISI for data

Rank Company Tonnes (000) Mkt. Share

1 UPM 6,109 13.5%

2 Stora Enso 3,170 7.0%

3 Norske Skog 2,625 5.8%

4 Resolute 2,282 5.1%

5 Nippon Paper 1,817 4.0%

6 Oji Paper 1,759 3.9%

7 SAPPI 1,350 3.0%

8 Holmen 1,150 2.5%

Rank Company Tonnes (000) Mkt. Share

1 Resolute 1,829 8.4%

2 Norske Skog 1,759 8.1%

3 UPM 1,585 7.3%

4 Stora Enso 1,280 5.9%

5 Nippon Paper 1,240 5.7%

6 Oji Paper 1,174 5.4%

7 Palm 980 4.5%

8 Kondopoga 695 3.2%

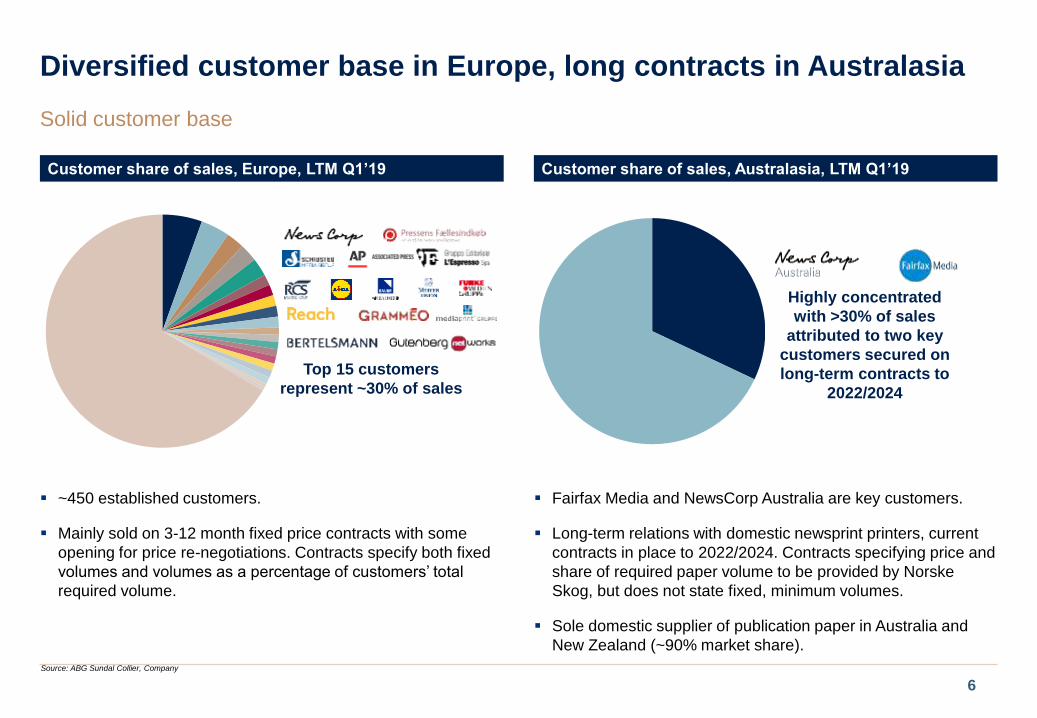

~450 established customers.

Mainly sold on 3-12 month fixed price contracts with some

opening for price re-negotiations. Contracts specify both fixed

volumes and volumes as a percentage of customers’ total

required volume.

Diversified customer base in Europe, long contracts in Australasia

Customer share of sales, Europe, LTM Q1’19 Customer share of sales, Australasia, LTM Q1’19

Solid customer base

6

Source: ABG Sundal Collier, Company

Top 15 customers

represent ~30% of sales

Highly concentrated

with >30% of sales

attributed to two key

customers secured on

long-term contracts to

2022/2024

Fairfax Media and NewsCorp Australia are key customers.

Long-term relations with domestic newsprint printers, current

contracts in place to 2022/2024. Contracts specifying price and

share of required paper volume to be provided by Norske

Skog, but does not state fixed, minimum volumes.

Sole domestic supplier of publication paper in Australia and

New Zealand (~90% market share).

Complex business model made simple: all about prices and FX

7

Estimated EBITDA using regression model …and estimated EBITDA margin

0

500

1,000

1,500

2,000

2,500

Q1

'96

Q1

'97

Q1

'98

Q1

'99

Q1

'00

Q1

'01

Q1

'02

Q1

'03

Q1

'04

Q1

'05

Q1

'06

Q1

'07

Q1

'08

Q1

'09

Q1

'10

Q1

'11

Q1

'12

Q1

'13

Q1

'14

Q1

'15

Q1

'16

Q1

'17

Q1

'18

Q1

'19

Reported clean EBITDA Estimated EBITDA

NOKm

Correlation = 0.91

Complex business model broken down to four parameters to

estimate EBITDA.

The parameters:

Publication paper prices

Delivery volumes

Cost of fibre (pulpwood)

FX (USD/NOK)

Looking at EBITDA margins instead, we can reduce the

model to two parameters

The parameters:

Publication paper prices

FX (USD/EUR)

Source: Norske Skog, Fastmarkets RISI, LUKE and Bloomberg for historical data, ABG Sundal Collier for estimates

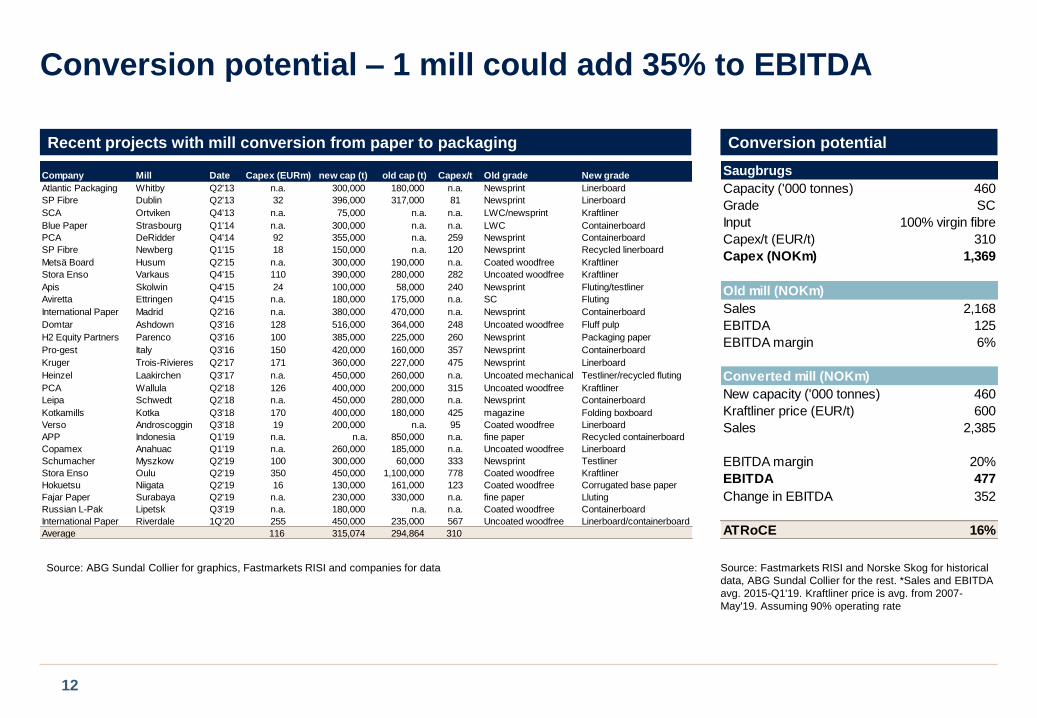

International Paper Riverdale 1Q'20 255 450,000 235,000 567 Uncoated woodfree Linerboard/containerboard

Average 116 315,074 294,864 310

Saugbrugs

Capacity ('000 tonnes) 460

Grade SC

Input 100% virgin fibre

Capex/t (EUR/t) 310

Capex (NOKm) 1,369

Old mill (NOKm)

Sales 2,168

EBITDA 125

EBITDA margin 6%

Converted mill (NOKm)

New capacity ('000 tonnes) 460

Kraftliner price (EUR/t) 600

Sales 2,385

EBITDA margin 20%

EBITDA 477

Change in EBITDA 352

ATRoCE 16%

Source: Fastmarkets RISI and Norske Skog for historical

data, ABG Sundal Collier for the rest. *Sales and EBITDA

avg. 2015-Q1'19. Kraftliner price is avg. from 2007-

May'19. Assuming 90% operating rate

Source: ABG Sundal Collier for graphics, Fastmarkets RISI and companies for data

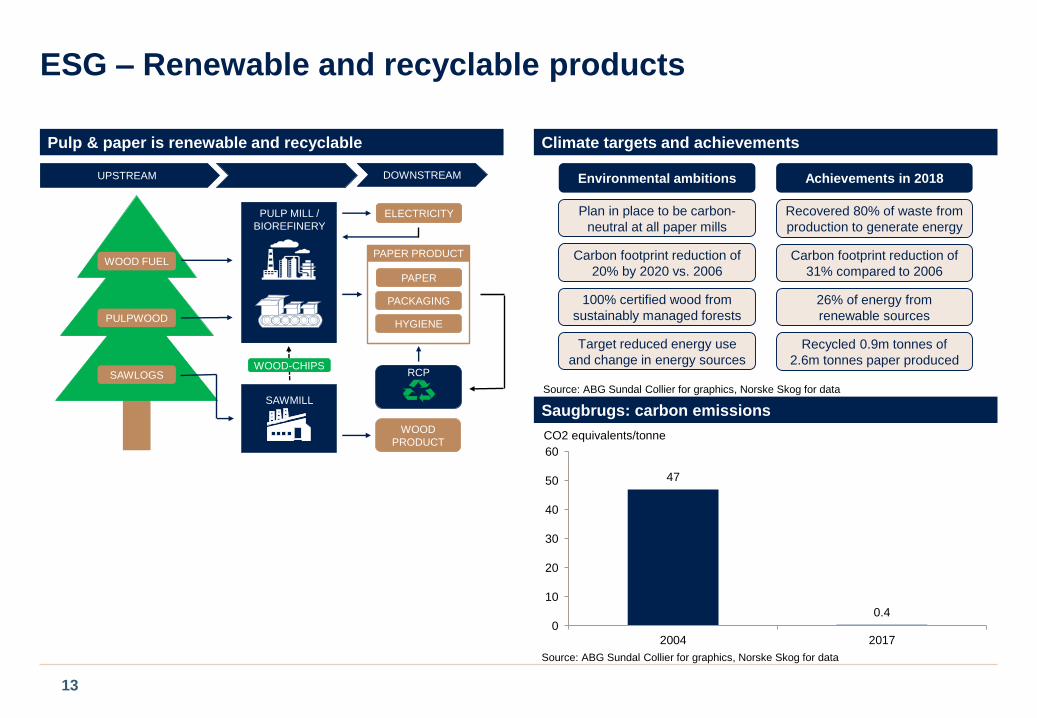

ESG – Renewable and recyclable products

13

Pulp & paper is renewable and recyclable Climate targets and achievements

PAPER PRODUCT

PAPER

PACKAGING

HYGIENE

SAWMILL

WOOD-CHIPS

ELECTRICITYPULP MILL /

BIOREFINERY

RCPSAWLOGS

PULPWOOD

WOOD FUEL

UPSTREAM DOWNSTREAM

WOOD

PRODUCT

Saugbrugs: carbon emissions

47

0.40

10

20

30

40

50

60

2004 2017

CO2 equivalents/tonne

Source: ABG Sundal Collier for graphics, Norske Skog for data

Source: ABG Sundal Collier for graphics, Norske Skog for data

26% of energy from

renewable sources

Environmental ambitions

Recovered 80% of waste from

production to generate energy

Plan in place to be carbon-

neutral at all paper mills

Recycled 0.9m tonnes of

2.6m tonnes paper produced

Achievements in 2018

Carbon footprint reduction of

20% by 2020 vs. 2006

100% certified wood from

sustainably managed forests

Carbon footprint reduction of

31% compared to 2006

Target reduced energy use

and change in energy sources

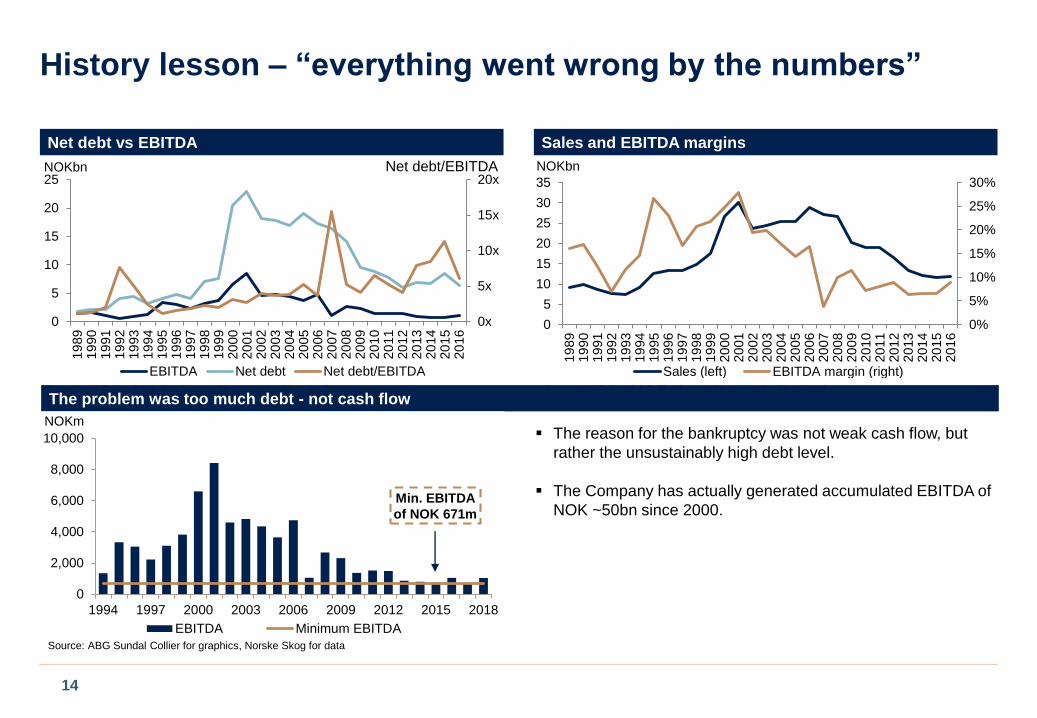

History lesson – “everything went wrong by the numbers”

14

Net debt vs EBITDA Sales and EBITDA margins

0x

5x

10x

15x

20x

0

5

10

15

20

25

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

NOKbn

EBITDA Net debt Net debt/EBITDA

Net debt/EBITDA

0%

5%

10%

15%

20%

25%

30%

0

5

10

15

20

25

30

35

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Sales (left) EBITDA margin (right)

NOKbn

Source: ABG Sundal Collier for graphics, Norske Skog for dataSource: ABG Sundal Collier for graphics, Norske Skog for dataThe problem was too much debt - not cash flow

0

2,000

4,000

6,000

8,000

10,000

1994 1997 2000 2003 2006 2009 2012 2015 2018

EBITDA Minimum EBITDA

NOKm

Min. EBITDA

of NOK 671m

The reason for the bankruptcy was not weak cash flow, but

rather the unsustainably high debt level.

The Company has actually generated accumulated EBITDA of

NOK ~50bn since 2000.

Source: ABG Sundal Collier for graphics, Norske Skog for data

Competitive landscape

Top 10 global newsprint producers Top 10 global SC magazine producers

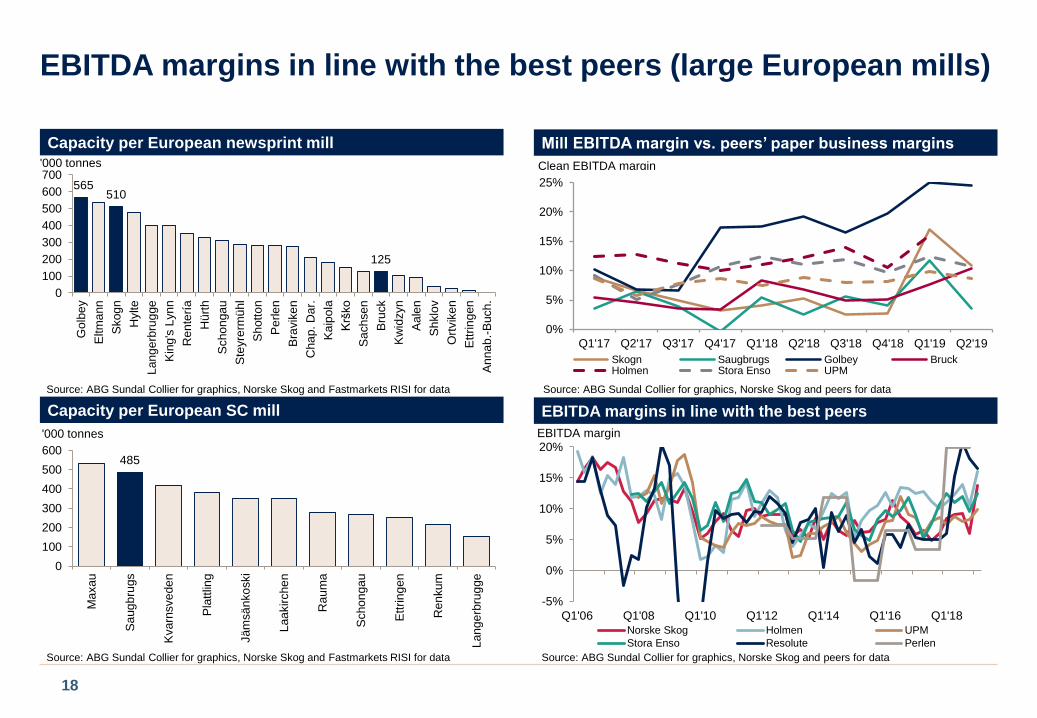

EBITDA margins in line with the best peers (large European mills)

18

Capacity per European newsprint mill

Capacity per European SC mill

Mill EBITDA margin vs. peers’ paper business margins

Source: ABG Sundal Collier for graphics, Norske Skog and peers for dataSource: ABG Sundal Collier for graphics, Norske Skog and Fastmarkets RISI for data

Source: ABG Sundal Collier for graphics, Norske Skog and peers for dataSource: ABG Sundal Collier for graphics, Norske Skog and Fastmarkets RISI for data

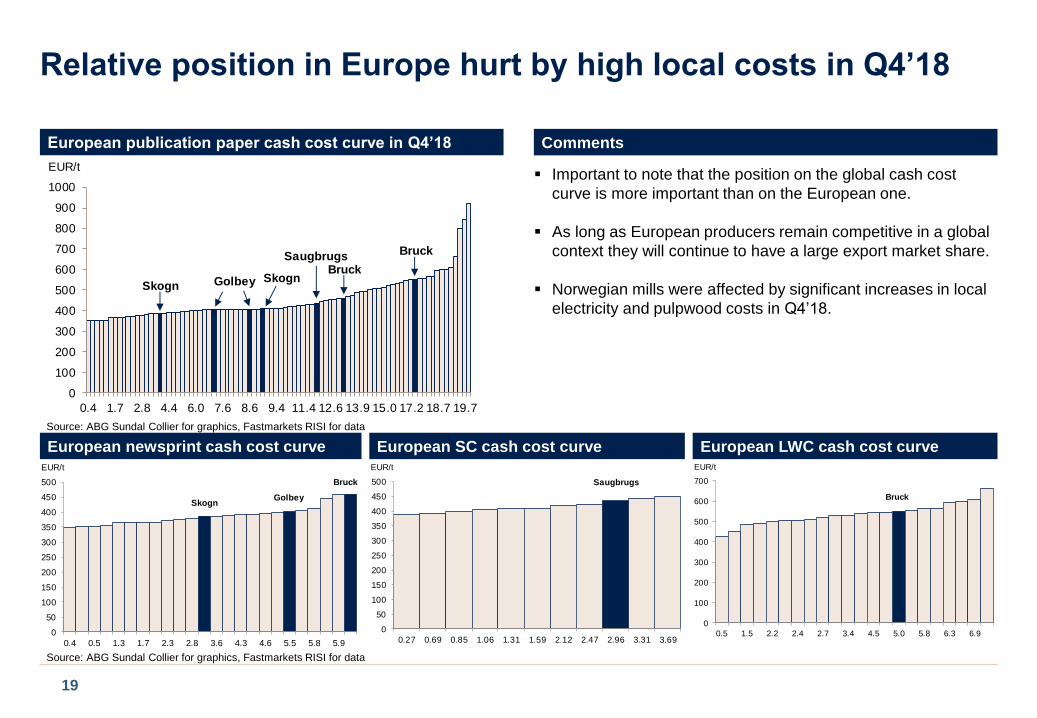

Relative position in Europe hurt by high local costs in Q4’18

19

European publication paper cash cost curve in Q4’18 Comments

European newsprint cash cost curve European SC cash cost curve European LWC cash cost curve

Important to note that the position on the global cash cost

curve is more important than on the European one.

As long as European producers remain competitive in a global

context they will continue to have a large export market share.

Norwegian mills were affected by significant increases in local

electricity and pulpwood costs in Q4’18.

Source: ABG Sundal Collier for graphics, Fastmarkets RISI for data

Source: ABG Sundal Collier for graphics, Fastmarkets RISI for data

23

0

10

20

30

40

50

60

70

80

90

Mill

#1

Mill

#2

Go

lbe

y

Mill

#3

Mill

#4

Mill

#5

Mill

#6

Mill

#7

Mill

#8

Mill

#9

Mill

#1

0

Mill

#1

1

Mill

#1

2

Mill

#1

3

Mill

#1

4

Mill

#1

5

Mill

#1

6

Mill

#1

7

Mill

#1

8

Mill

#1

9

Mill

#2

0

Mill

#2

1

Mill

#2

2

Mill

#2

3

EUR/t

Average delivery cost of EUR 39/t

38

0

10

20

30

40

50

60

70

80

90

100

Mill

#1

Mill

#2

Skogn

Mill

#3

Mill

#4

Mill

#5

Mill

#6

Mill

#7

Mill

#8

Mill

#9

Mill

#1

0

Mill

#1

1

Mill

#1

2

Mill

#1

3

Mill

#1

4

Mill

#1

5

Mill

#1

6

Mill

#1

7

Mill

#1

8

Mill

#1

9

Mill

#2

0

Mill

#2

1

Mill

#2

2

Mill

#2

3

EUR/t

Average delivery cost of EUR 56/t

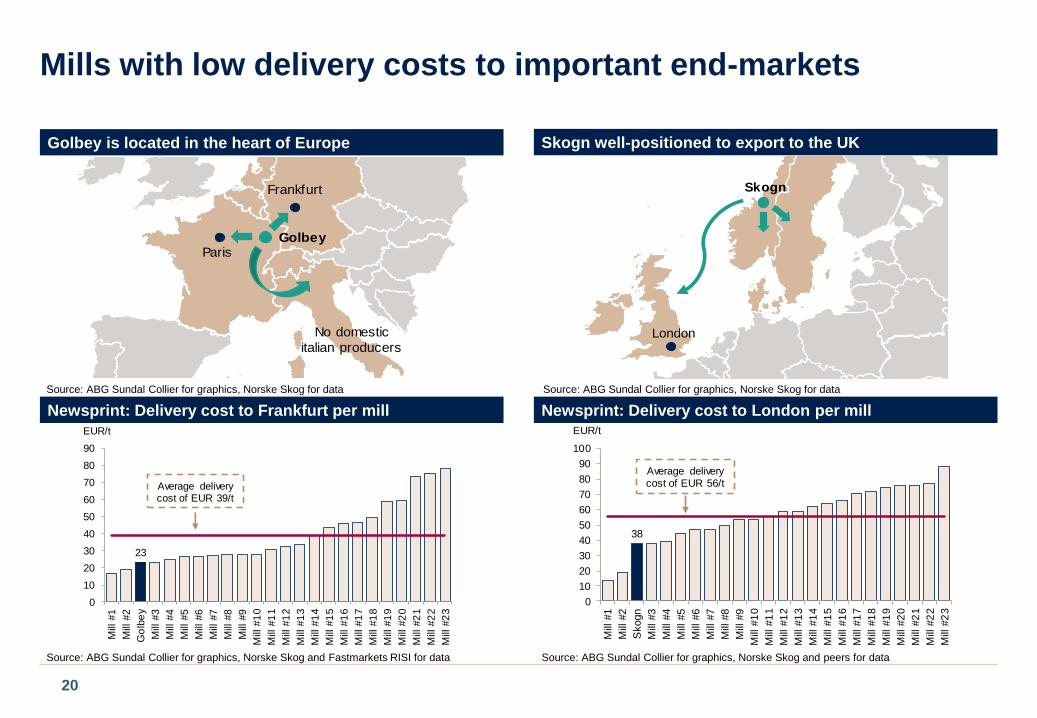

Mills with low delivery costs to important end-markets

20

Skogn well-positioned to export to the UKGolbey is located in the heart of Europe

Paris

Frankfurt

Golbey

No domestic

italian producers

Newsprint: Delivery cost to Frankfurt per mill

Source: ABG Sundal Collier for graphics, Norske Skog for dataSource: ABG Sundal Collier for graphics, Norske Skog for data

Source: ABG Sundal Collier for graphics, Norske Skog and peers for dataSource: ABG Sundal Collier for graphics, Norske Skog and Fastmarkets RISI for data

This material has been prepared by ABG Sundal Collier ASA, or an affiliate thereof ("ABGSC").

This material is for distribution only under such circumstances as may be permitted by applicable law. It has no regard to the specific investment objectives, financial

situation or particular needs of any recipient. It is published solely for informational purposes and is not to be construed as a solicitation or an offer to buy or sell any

securities or related financial instruments. No representation or warranty, either expressed or implied, is provided in relat ion to the accuracy, completeness or

reliability of the information contained herein, nor is it intended to be a complete statement or summary of the securities, markets or developments referred to in the

materials. It should not be regarded by recipients as a substitute for the exercise of their own judgement. Any opinions expressed in this material are subject to

change without notice and may differ or be contrary to opinions expressed by other business areas or groups of ABGSC as a result of using different assumptions

and criteria. ABGSC is under no obligation to update or keep current the information contained herein. ABGSC, its directors, officers and employees' or clients may

have or have had interests or long or short positions in the securities or other financial instruments referred to herein and may at any time make purchases and/or

sales in them as principal or agent. ABGSC may act or have acted as market-maker in the securities or other financial instruments discussed in this material.

Furthermore, ABGSC may have or have had a relationship with or may provide or has provided investment banking, capital markets and/or other financial services to

the relevant companies. Neither ABGSC nor any of its affiliates, nor any of ABGSC' or any of its affiliates, directors, employees or agents accepts any liability for any

loss or damage arising out of the use of all or any part of this material.