SPEAKERS: Philip Simpkins, Kathy SPEAKERS: Philip Simpkins, Kathy Walker Walker

& Tom Bick& Tom Bick

The information provided in this The information provided in this

presentation is based upon complex presentation is based upon complex requirements of the IRS and Treasury requirements of the IRS and Treasury Regulations.Regulations.

Although care has been taken to Although care has been taken to present the material accurately, S&A present the material accurately, S&A disclaims any implied or actual disclaims any implied or actual warranties as to the accuracy of any warranties as to the accuracy of any material herein or completeness and material herein or completeness and any liability with respect thereto.any liability with respect thereto.

Neither S&A nor its representatives Neither S&A nor its representatives give legal, tax or financial advice.give legal, tax or financial advice.

This PowerPoint is intended to be This PowerPoint is intended to be used as an executive summary or used as an executive summary or overview.overview.

MeetingMeetingby by Philip SimpkinsPhilip Simpkins

ERISA enforcement agencies:

• DOL Department of Labor

• IRS Internal Revenue Service

• Participants can enforce fiduciary rules through lawsuits

Introduction to Fiduciary Responsibilities

• Owners, officers and directors need to be aware of their fiduciary responsibilities

• Identify possible shortcomings

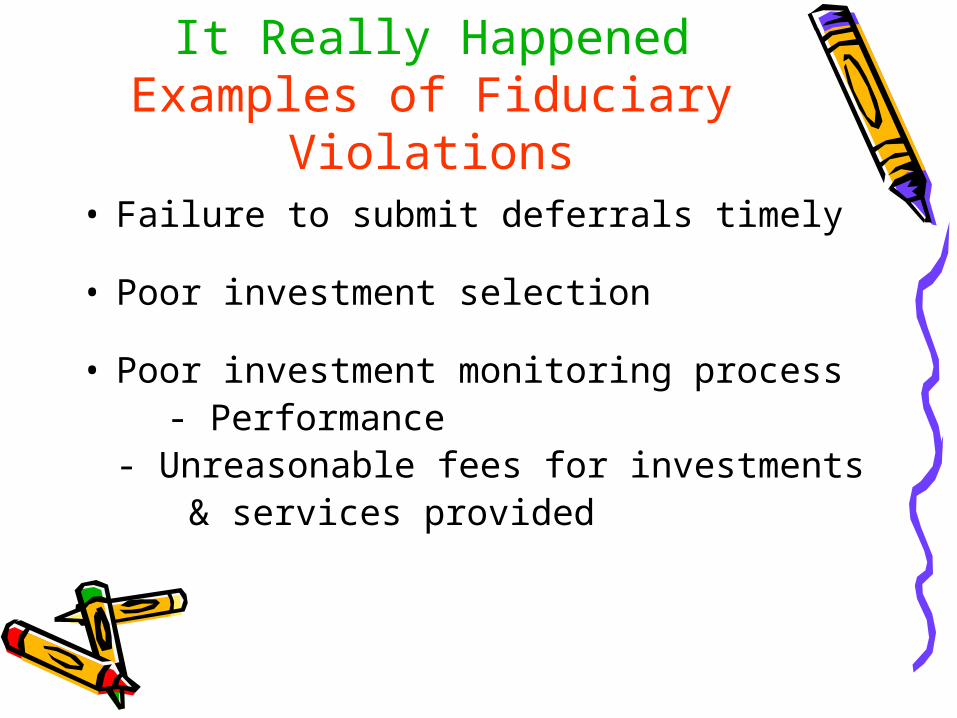

It Really HappenedExamples of Fiduciary

Violations• Failure to submit deferrals timely

• Poor investment selection

• Poor investment monitoring process - Performance

- Unreasonable fees for investments & services provided

Who is a Plan Fiduciary?

A person who:

1. Exercises any discretionary authority or control over the management or disposition of its assets

2. Renders investment advice for compensation

3. Has discretion or responsibility in the administration of the plan

Who is a Plan Fiduciary?

Key people including:

– Plan sponsor or board of directors– Plan committee members– Plan trustee– Registered Investment Advisors– Anyone if they act in a fiduciary role

(e.g. select investments or hire advisor)

Who is the Named Fiduciary?

Person (or group) who is authorized to control and manage the operation and administration of the plan.

Named in your plan document.

Make sure your board of directors:

– Carefully considers the qualifications

– Keeps minutes on how it selected the named fiduciary

– Documents ongoing and periodic evaluation of the named fiduciary’s performance

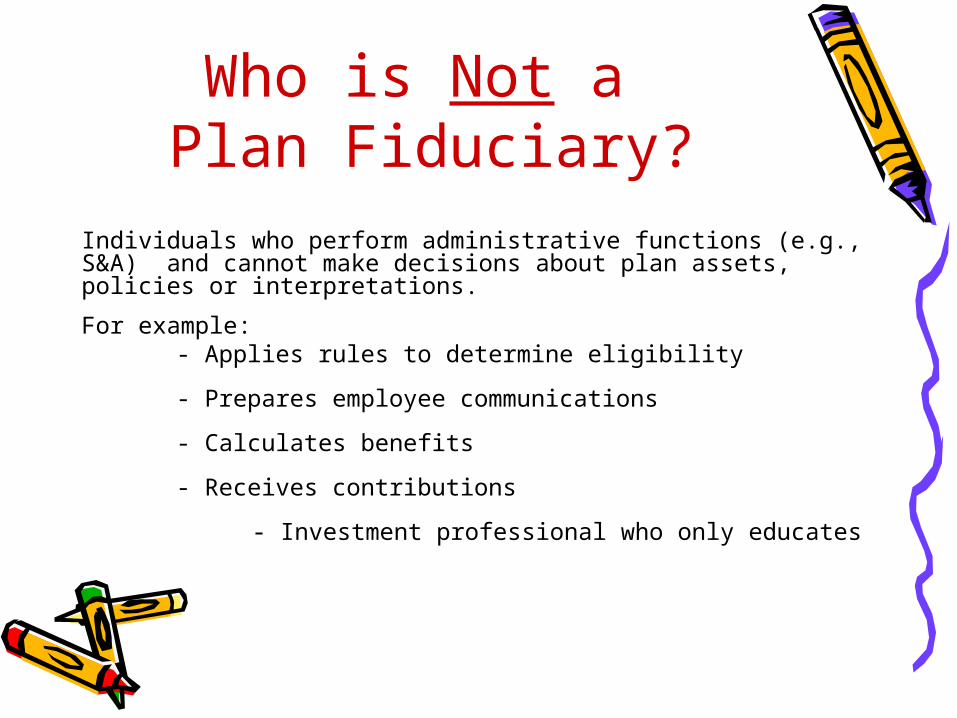

Who is Not a Plan Fiduciary?

Individuals who perform administrative functions (e.g., S&A) and cannot make decisions about plan assets, policies or interpretations.

For example:- Applies rules to determine eligibility

- Prepares employee communications

- Calculates benefits

- Receives contributions

- Investment professional who only educates

What are Your DutiesAs a Named Fiduciary?

• Manage the plan for the exclusive benefit of participants (and beneficiaries)

• Acts prudently• Select and monitor plan investments• Select and monitor plan’s services• Monitor plan’s charges• Abide by the plan’s provisions

How Are Plan Investments Selected?

Certain fiduciaries are considered investment fiduciaries and their duties include:

• Selecting the investment provider • Determining the range of investment

options and selecting the specific options• Designating the person who will make the

decisions about plan investments• Selecting the default investment (QDIA)

Investment Policy Statement (IPS)

An Important Job of the Investment Fiduciary!

• Valuable “written” tool to assist in selecting and monitoring plan investments

• ERISA does not specifically require

• Investment experts generally consider a “best practice”

• At least one court has found “was required” to satisfy ERISA’s general fiduciary standards

How can Plan Fiduciaries Limit Their Liability for Investment

Losses?

•Offer broad range of investment options

•Appropriate frequency of participant investment direction

•Provide required participant information

What are Prohibited Transactions?

• Party in interest transactions

• Acts of self-dealing

• Prohibited transaction exemptions

Other Important Guidelines!

• Making timely contributions

• Paying expenses from plan assets

• Selecting and monitoring service providers

• ERISA bonding

• Fiduciary protection and insurance (purchase of fiduciary liability insurance)

• Timely government filing

Plan Fiduciary Meeting and Due Diligence ChecklistPlan fiduciaries must carefully document the processes they have followed in fulfilling their duties. A complete and detailed due diligence file will help illustrate the prudent steps you have taken in fulfilling your fiduciary responsibilities.

This checklist will assist you not only in selecting and monitoring service providers, but will also assist you with the ongoing task of monitoring the plan investments, operation and administration.

[ ] Read minutes from previous plan fiduciary meeting

[ ] Conduct a plan review:

[ ] Review recent changes in the law that may affect the plan since the last review

[ ] Review Internal Revenue Service, Department of Labor or other government agency regulations or proposals that

may affect the plan

[ ] Consider potential changes in plan design

[ ] Review recent plan amendments

[ ] Review participant education and communication:

[ ] Review the results of any enrollment/educational meetings held since the last review and discuss changes for future

meetings

[ ] Schedule the next enrollment/educational meeting

[ ] Distribute Summary Annual Report (SAR)

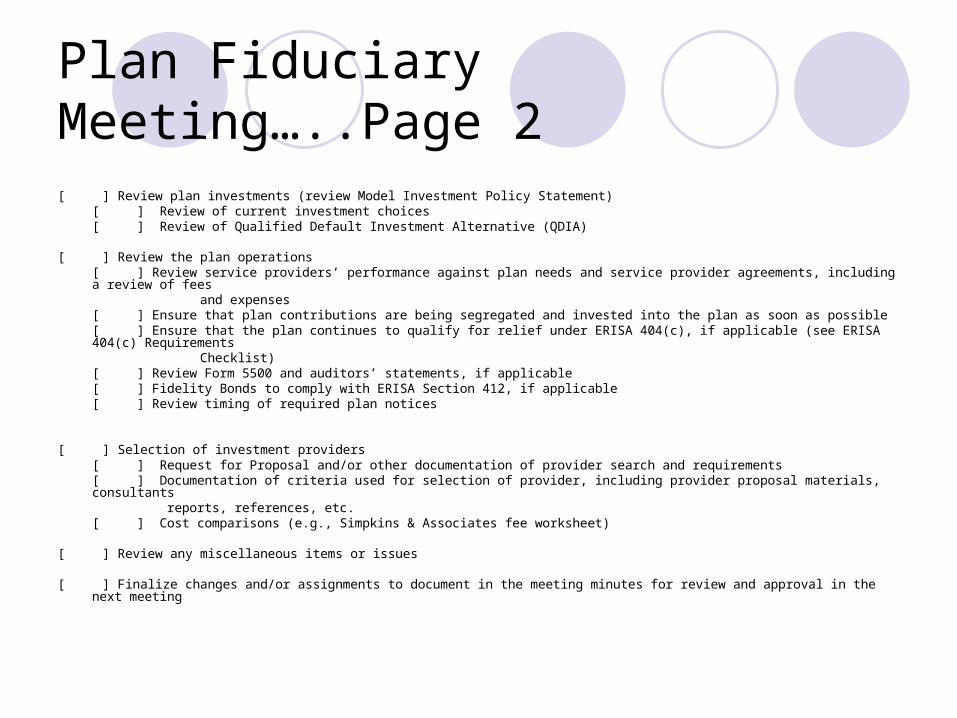

Plan Fiduciary Meeting…..Page 2

[ ] Review plan investments (review Model Investment Policy Statement)[ ] Review of current investment choices[ ] Review of Qualified Default Investment Alternative (QDIA)

[ ] Review the plan operations [ ] Review service providers’ performance against plan needs and service provider agreements, including a review of

fees and expenses

[ ] Ensure that plan contributions are being segregated and invested into the plan as soon as possible [ ] Ensure that the plan continues to qualify for relief under ERISA 404(c), if applicable (see ERISA 404(c) Requirements

Checklist) [ ] Review Form 5500 and auditors’ statements, if applicable[ ] Fidelity Bonds to comply with ERISA Section 412, if applicable [ ] Review timing of required plan notices

[ ] Selection of investment providers[ ] Request for Proposal and/or other documentation of provider search and requirements[ ] Documentation of criteria used for selection of provider, including provider proposal materials, consultants reports, references, etc.[ ] Cost comparisons (e.g., Simpkins & Associates fee worksheet)

[ ] Review any miscellaneous items or issues

[ ] Finalize changes and/or assignments to document in the meeting minutes for review and approval in the next meeting

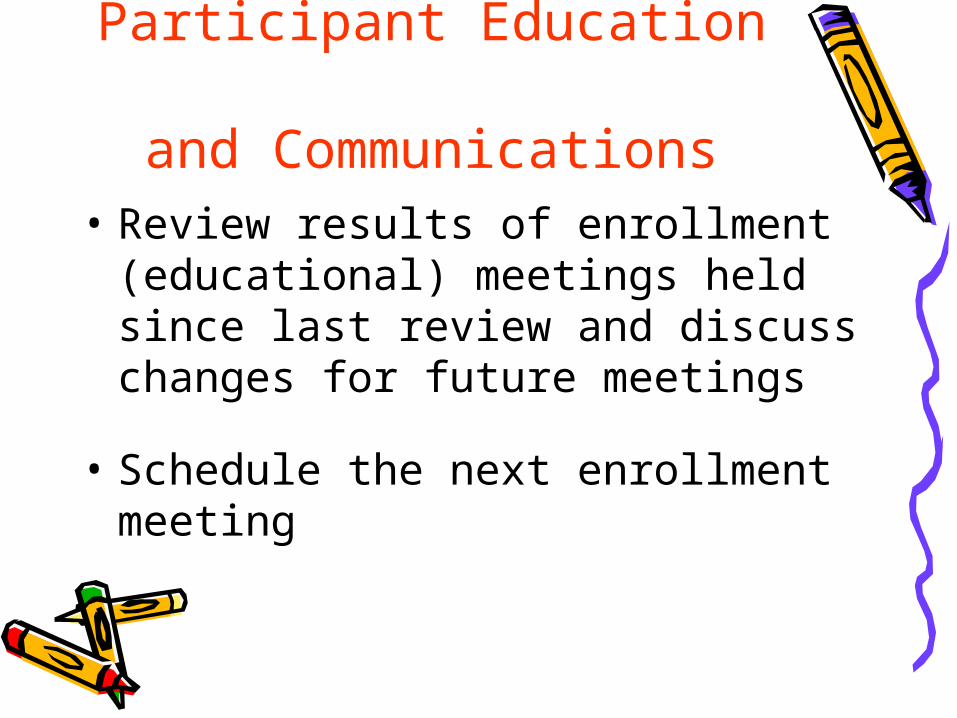

Participant Education and Communications

• Review results of enrollment (educational) meetings held since last review and discuss changes for future meetings

• Schedule the next enrollment meeting

Plan Operations Review• Review service providers’ performance, including a

review of fees and expenses

• Ensure plan contributions are being invested ASAP

• Ensure the plan continues to qualify for relief under ERISA 404(c)

• Review Safe Harbor 401(k) rules

• Fiduciary Responsibility Checklist

REMEMBER!•Document your due diligence

•Have a process that is followed

20122012 Benefits BULLETINBenefits BULLETINBy By Kathy WalkerKathy Walker

I M P O R T A N T! READ CAREFULLY

Contains IRS & DOL Compliance Requirements

2012 Benefits B U L L E T I N

The end of the year is rapidly approaching. S&A delivers participant distribution information and forms to our plan sponsors each Fall. We have also included an executive summary or overview of general issues and IRS/DOL compliance requirements. The information in this B U L L E T I N may not affect the plans of all clients. Please see 2012 IRS DISTRIBUTION GUIDELINES for more information on your distribution responsibilities.

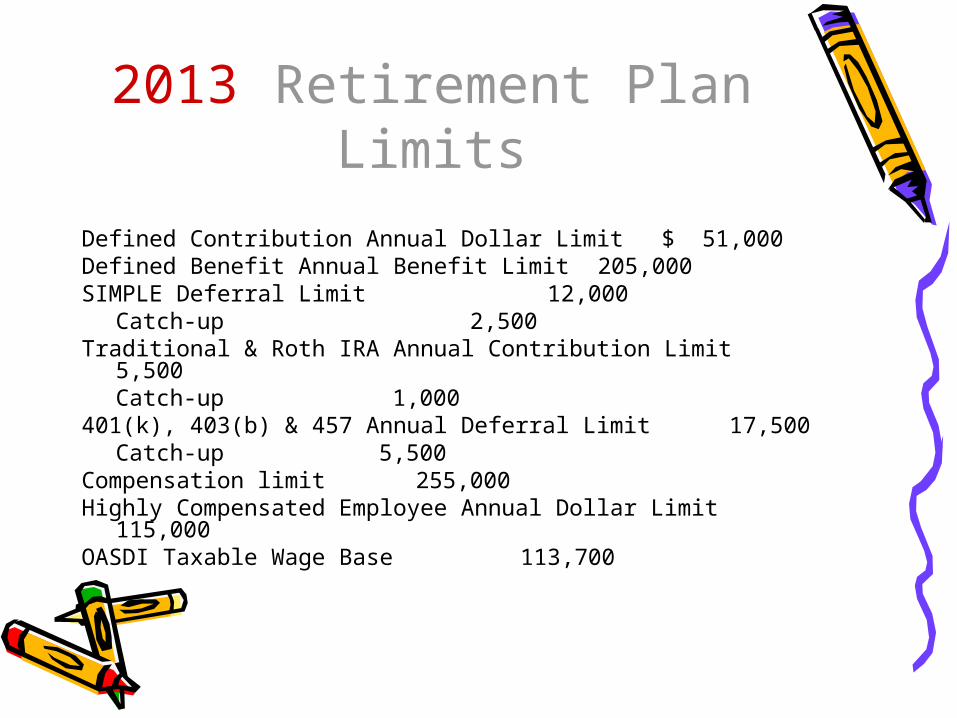

2013 Retirement Plan Limits

Defined Contribution Annual Dollar Limit $ 51,000Defined Benefit Annual Benefit Limit 205,000SIMPLE Deferral Limit 12,000

Catch-up 2,500Traditional & Roth IRA Annual Contribution Limit 5,500

Catch-up 5,500Compensation limit 255,000Highly Compensated Employee Annual Dollar Limit 115,000OASDI Taxable Wage Base 113,700

The Accountants Role in Administering a Qualified Retirement Plan!

The accountant’s role may entail preparing statements of plan assets, auditing the plan’s books and records, and preparing reports to government agencies. A plan with 100 or more participants requires special reports by an independent qualified public accountant. CPA Recommendations! We have worked with a number of excellent CPA firms in this area.

Cafeteria Plan Sponsors ~ do you offer your employees a debit card?

Some of our clients do not know that Cafeteria Plan Administration ~ Section 125 ~ has long been an integral part of the administrative services offered by Simpkins & Associates. Call Holly Simpkins at 830.980.3334 ext. 11 for more information about debit cards ~ the latest Cafeteria Plan development!

DEPOSITING 401(k) MATCHING CONTRIBUTIONS!

Normally, matching contributions made to a 401(k) plan must be deposited by the due date of the tax return for the tax year. However, if you have a safe harbor matching 401(k) plan and you use anything other than the entire plan year (e.g., each payroll period), the match for elective deferrals made during a plan year quarter must be deposited no later than the last day of the next quarter. For example, suppose you determine the matching separately for each payroll period and the plan year is the calendar year. For elective deferrals made during the third quarter of the year (July 1st – September 30th), the matching contributions would have to be deposited by December 31st.

VERY IMPORTANT ~ Fee Disclosure!

Reporting requirements, for the over 70 million US workers enrolled in a qualified retirement plan, just got more complex.

The DOL announced new rules that were effective July 1, 2012. Plan sponsors are now required to lay out administrative expenses and other charges that can be imposed on retirement plans. These rules are VERY important. Ask us or your investment professional for up to date information. You must make sure you are fully incompliance.

Highlights Administration

Please read the 2013 Highlights –Administration- These Highlights are intended to be used as an executive summary or overview. Please call us with your questions.Some of the topics include:Plan Document and DesignYour plan must have an IRS-approved document in place including a document that is up-to-date for recent law changes; remember that you do not have an approved plan until all documents have been executed and appropriately dated

Distribution Information & Forms.

Required Distributions! The payment of benefits cannot be postponed indefinitely. The required beginning date for a participant who is not a 5% owner is the April 1st of the calendar year following the later of the calendar year in which he or she reaches age 70-½ or the calendar year in which the participant retires. A 5% owner must have begun receiving distributions from a qualified plan by April 1st of the calendar year after reaching age 70-½.

Roth! If your plan contains a Roth provision, please contact S&A for special assistance.

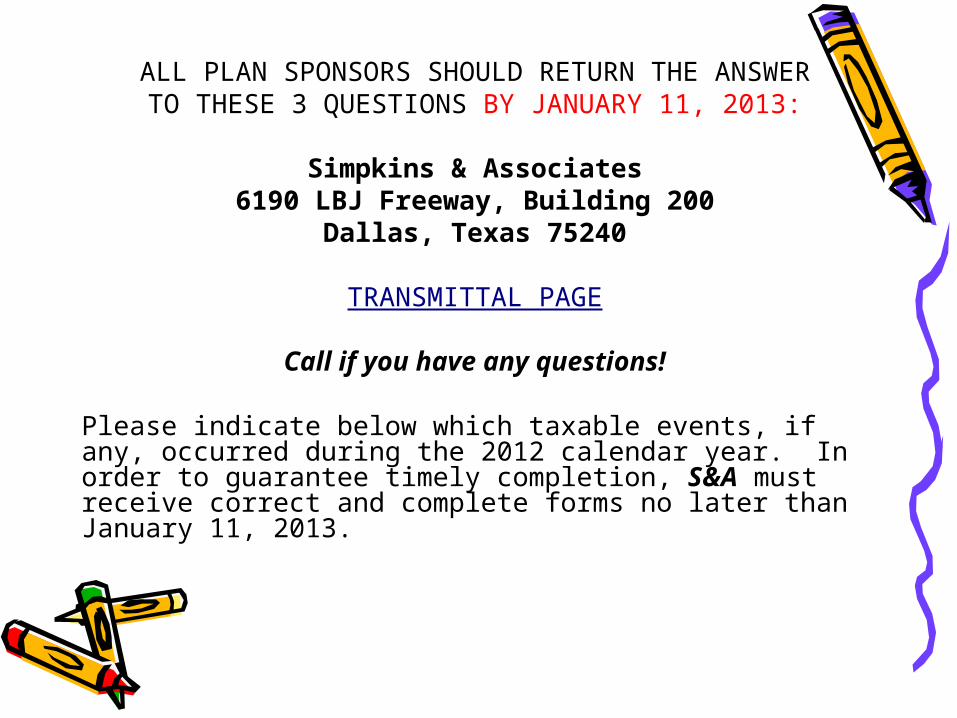

ALL PLAN SPONSORS SHOULD RETURN THE ANSWERTO THESE 3 QUESTIONS BY JANUARY 11, 2013:

Simpkins & Associates6190 LBJ Freeway, Building 200

Dallas, Texas 75240

TRANSMITTAL PAGE

Call if you have any questions!

Please indicate below which taxable events, if any, occurred during the 2012 calendar year. In order to guarantee timely completion, S&A must receive correct and complete forms no later than January 11, 2013.

Does our plan contain life insurance?

[ ] YES [ ] NO

If YES, do you want S&A to prepare PS-58 cost? [ ] Yes [ ] No

Were there any distributions from our Plan? Were there any distributions from our Plan? [ ] YES [ ] NO

If YES, do you want S&A to prepare Form 1099-Rs? [ ] Yes [ ] No If YES, do you want S&A to prepare Form 945? [ ] Yes [ ] No

Were there any loans in default or that exceeded the current loan limitations? W. Were there any loans in default or that exceeded the current• loan limitations? [ ] YES [ ] NO

If YES, do you want S&A to prepare Form 1099-Rs?[ ] Yes [ ] No

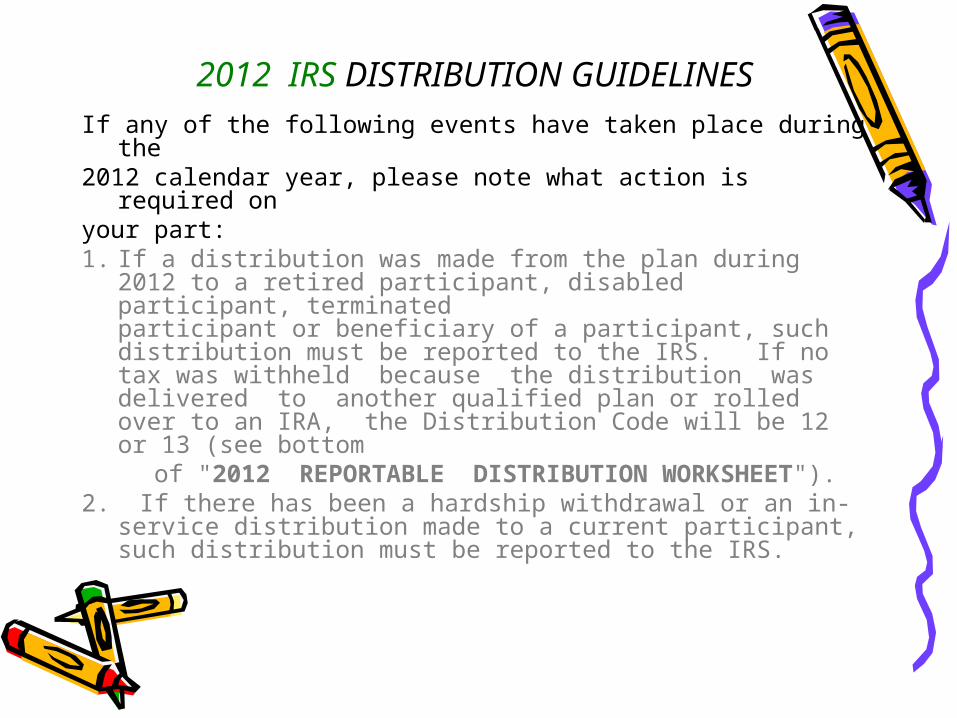

2012 IRS DISTRIBUTION GUIDELINESIf any of the following events have taken place during the2012 calendar year, please note what action is required

onyour part:1. If a distribution was made from the plan during 2012 to

a retired participant, disabled participant, terminated participant or beneficiary of a participant, such distribution must be reported to the IRS. If no tax was withheld because the distribution was delivered to another qualified plan or rolled over to an IRA, the Distribution Code will be 12 or 13 (see bottom

of "2012 REPORTABLE DISTRIBUTION WORKSHEET").

2. If there has been a hardship withdrawal or an in-service distribution made to a current participant, such distribution must be reported to the IRS.

REQUIRED NOTICESBy: Tom Bick

Required NoticesQualified Default Investment Alternative (QDIA)

– Annual notice 30 days prior to beginning of year– New Participants must receive 30 days prior to entry

date– Notice updates and reminders sent in November

Automatic Enrollment – Annual notice 30 days prior to beginning of year– New Participants must receive 30 days prior to entry

date– Notice updates and reminders sent in November

Required NoticesSafe Harbor Contribution

– Remember to pass out your notice ~ currently available on S&A website

– Execute / download amendments previously posted to S&A website

– Annual notice 30 days prior to beginning of year

– New Participants must receive 30 days prior to entry date

408(b)(2)FEE DISCLOSUREBy Kathy Walker

408(b)(2) Fee Disclosure

• Effective July 1, 2012

408(b)(2)FEE DISCLOSURE

• Must be in writing and include a description of the following:– Services to be provided– All compensation

408(b)(2)FEE DISCLOSURE

• Exemption for Plan Fiduciary• Prohibited Transaction• Failure to comply

PARTICIPANTFEE DISCLOSURE

• Effective August 30, 2012

Participant Fee Disclosure

• Final Rule Overview– Fiduciary Act– Participant Directed Accounts– Notices

Participant Fee Disclosure

• Plan Related Information– General– Administrative Expenses– Individual Expenses

Participant Fee Disclosure

• Investment Related Information - Identifying Information

– Performance Data- Benchmarks– Fee and Expense Information– Internet website