29

Copyright 2014 Market Data Retrieval Parthenon Perspectives Trends in K-12 Education September 30, 2014

Copyright 2014 Market Data Retrieval

Parthenon Perspectives

Trends in K-12 Education

September 30, 2014

Copyright 2014 Market Data Retrieval

Agenda

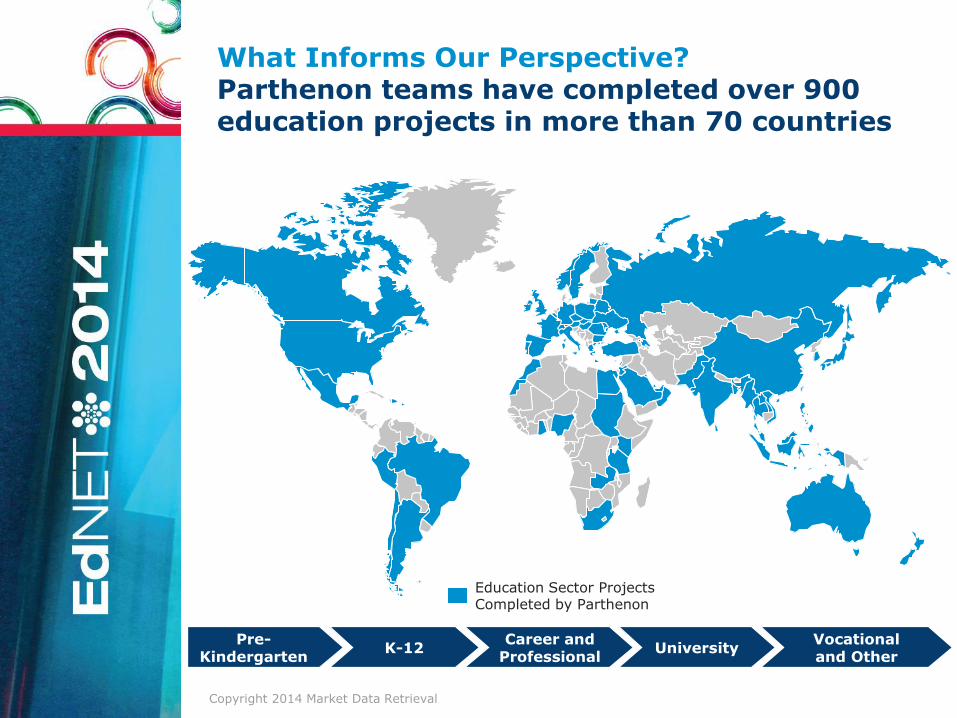

What Informs Our Perspective?

Parthenon Perspectives on U.S. K-12 Market Trends

Copyright 2014 Market Data Retrieval

What Informs Our Perspective? Parthenon teams have completed over 900 education projects in more than 70 countries

Pre-Kindergarten

K-12 University Vocational and Other

Career and Professional

Education Sector Projects Completed by Parthenon

Copyright 2014 Market Data Retrieval

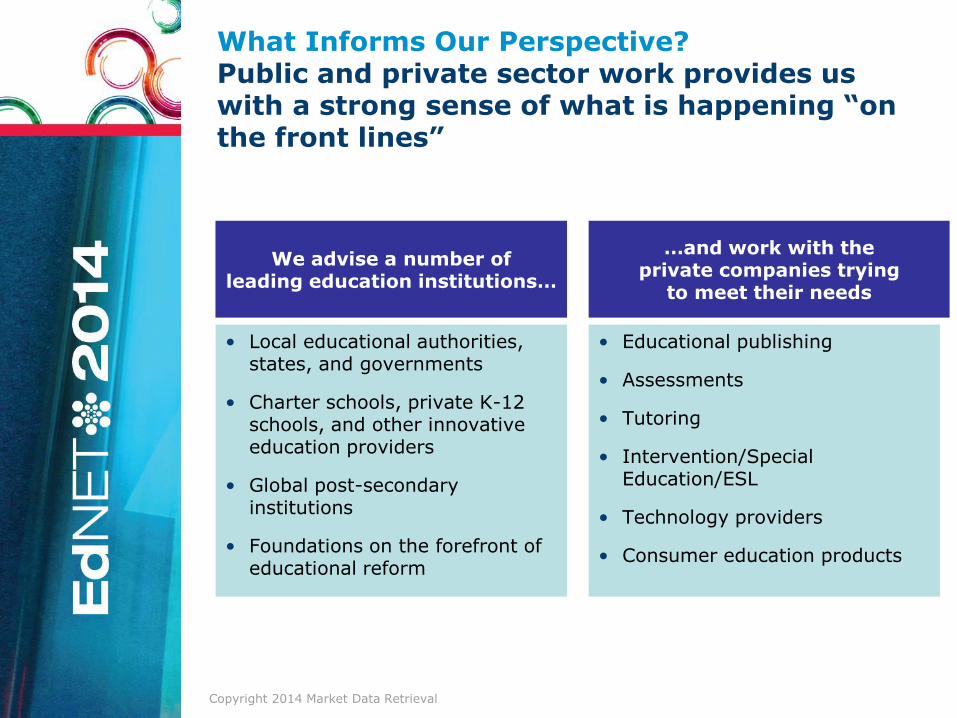

• Educational publishing

• Assessments

• Tutoring

• Intervention/Special Education/ESL

• Technology providers

• Consumer education products

• Local educational authorities, states, and governments

• Charter schools, private K-12 schools, and other innovative education providers

• Global post-secondary institutions

• Foundations on the forefront of educational reform

What Informs Our Perspective? Public and private sector work provides us with a strong sense of what is happening “on the front lines”

We advise a number of leading education institutions…

…and work with the private companies trying

to meet their needs

Copyright 2014 Market Data Retrieval

Agenda

What Informs our Perspective?

Parthenon Perspectives on U.S. K-12 Market Trends

Copyright 2014 Market Data Retrieval

A Macro View A lot is happening in the K-12 landscape

• A recovering economy…

• Rising acceptance of digital products and services…

• Wide ranging impacts as the Common Core is implemented…

• Evolving points of view on long-term policy issues:

– Managing Human Capital

– Role of “Choice” in districts

– Definitions of accountability

Provide some perspective on “what is happening” and how these trends will shape district leader

and consumer needs and the conversations you are likely to have with them

Copyright 2014 Market Data Retrieval

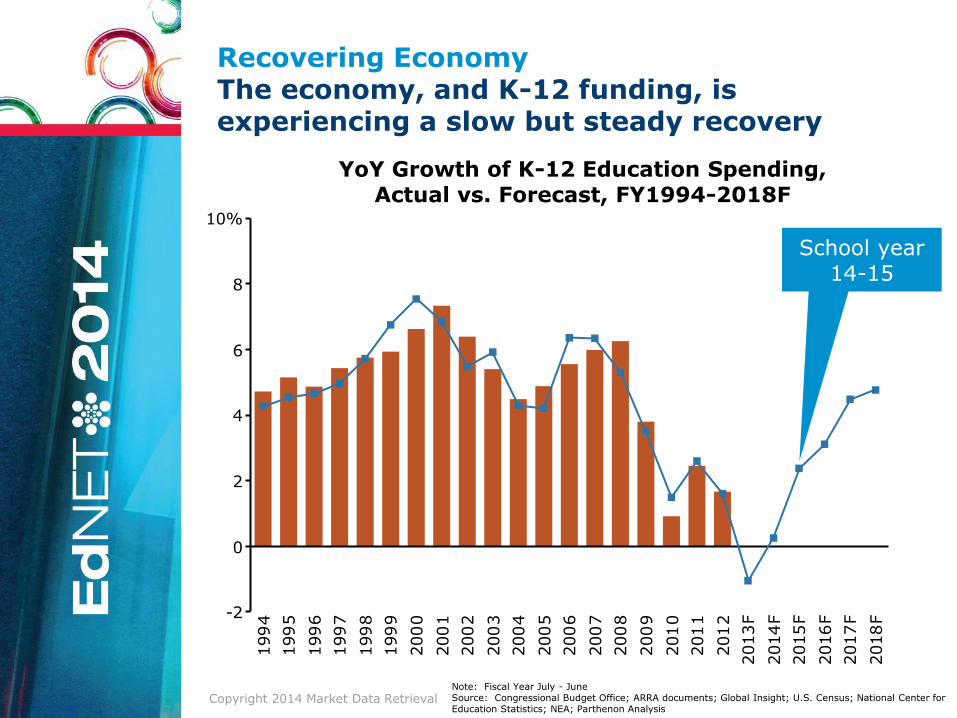

Recovering Economy The economy, and K-12 funding, is experiencing a slow but steady recovery

-2

0

2

4

6

8

10%

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013F

2014F

2015F

2016F

2017F

2018F

Note: Fiscal Year July - June Source: Congressional Budget Office; ARRA documents; Global Insight; U.S. Census; National Center for Education Statistics; NEA; Parthenon Analysis

YoY Growth of K-12 Education Spending, Actual vs. Forecast, FY1994-2018F

School year 14-15

Copyright 2014 Market Data Retrieval

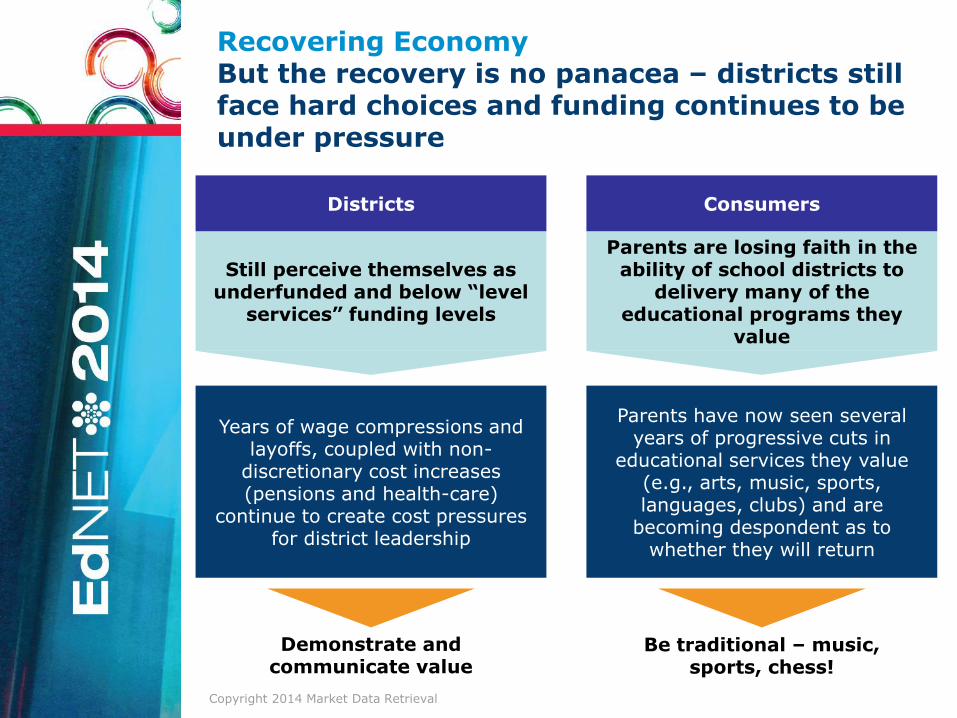

Recovering Economy But the recovery is no panacea – districts still face hard choices and funding continues to be under pressure

Still perceive themselves as underfunded and below “level

services” funding levels

Parents are losing faith in the ability of school districts to

delivery many of the educational programs they

value

Districts Consumers

Years of wage compressions and layoffs, coupled with non-

discretionary cost increases (pensions and health-care)

continue to create cost pressures for district leadership

Parents have now seen several years of progressive cuts in

educational services they value (e.g., arts, music, sports, languages, clubs) and are

becoming despondent as to whether they will return

Demonstrate and communicate value

Be traditional – music, sports, chess!

Copyright 2014 Market Data Retrieval

0

20

40

60

80

100%

Childcare

Childcare

$16B

Instructional

Materials

Non-DigitalSupplemental

Basal

Intervention

Other DigitalSupplemental

Online Courses

$8B

Form

ative

Sum

mative

$2B

General

Technology

IT Services

Software

Telecom

General Support

Hardware

$9B

SIS

LM

SS

tudent

Support

Serv

ices

Outs

ourc

ed

SES/

Tuto

ring

In-H

ouse

VirtualSchools

EMO

$4B

Prof.

Development

Outs

ourc

ed

-N

on-P

rofit

Outs

ourc

ed

-In

div

iduals

Outsourced- For-Profit

$4B

Consumer

Private Tutoring

Software/Apps

Courseware

$10B

Testing &

Assessments Stu

dent

&LM

S

$1B$1B

Outsourced

SchoolMgmt

Total = $54B

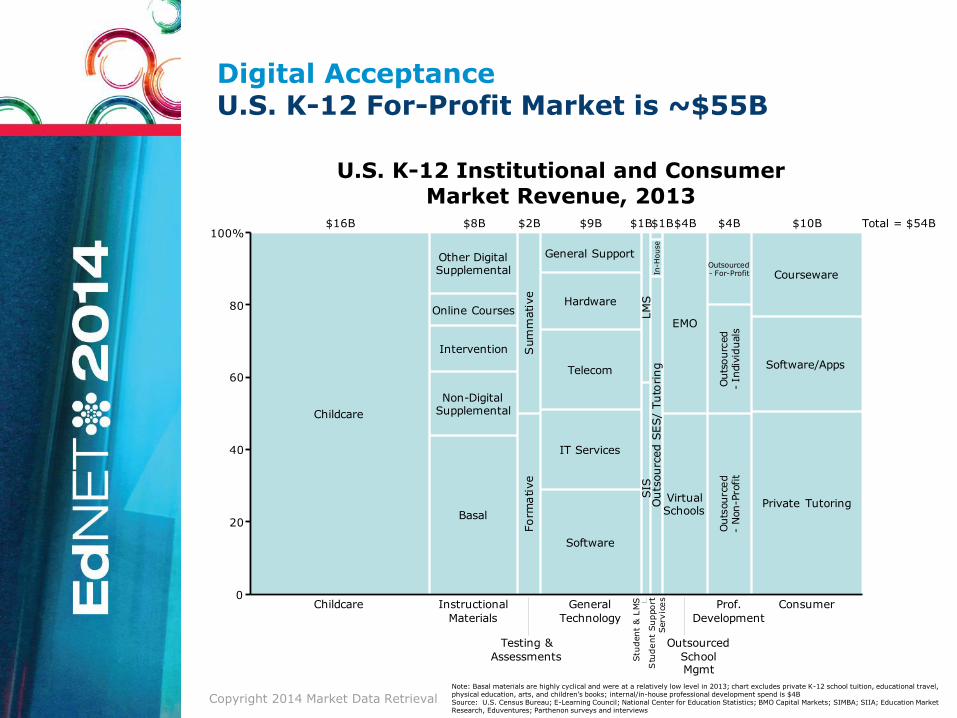

Digital Acceptance U.S. K-12 For-Profit Market is ~$55B

U.S. K-12 Institutional and Consumer Market Revenue, 2013

Note: Basal materials are highly cyclical and were at a relatively low level in 2013; chart excludes private K-12 school tuition, educational travel, physical education, arts, and children’s books; internal/in-house professional development spend is $4B Source: U.S. Census Bureau; E-Learning Council; National Center for Education Statistics; BMO Capital Markets; SIMBA; SIIA; Education Market Research, Eduventures; Parthenon surveys and interviews

Copyright 2014 Market Data Retrieval

Digital Acceptance The future of education is just around the corner, about to revolutionize the system…

Source: Online news articles and archives

Recently…

Copyright 2014 Market Data Retrieval

Digital Acceptance The future of education is just around the corner, about to revolutionize the system…

10-30 years ago…

Source: Online news articles and archives

Copyright 2014 Market Data Retrieval

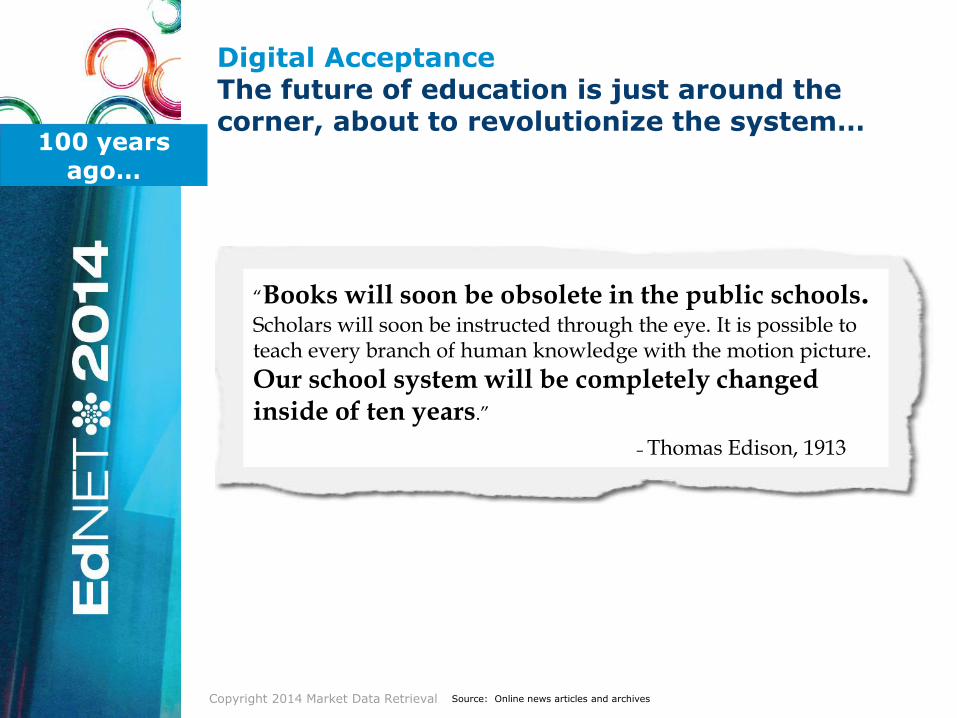

Digital Acceptance The future of education is just around the corner, about to revolutionize the system…

“Books will soon be obsolete in the public schools. Scholars will soon be instructed through the eye. It is possible to teach every branch of human knowledge with the motion picture.

Our school system will be completely changed inside of ten years.”

– Thomas Edison, 1913

100 years ago…

Source: Online news articles and archives

Copyright 2014 Market Data Retrieval

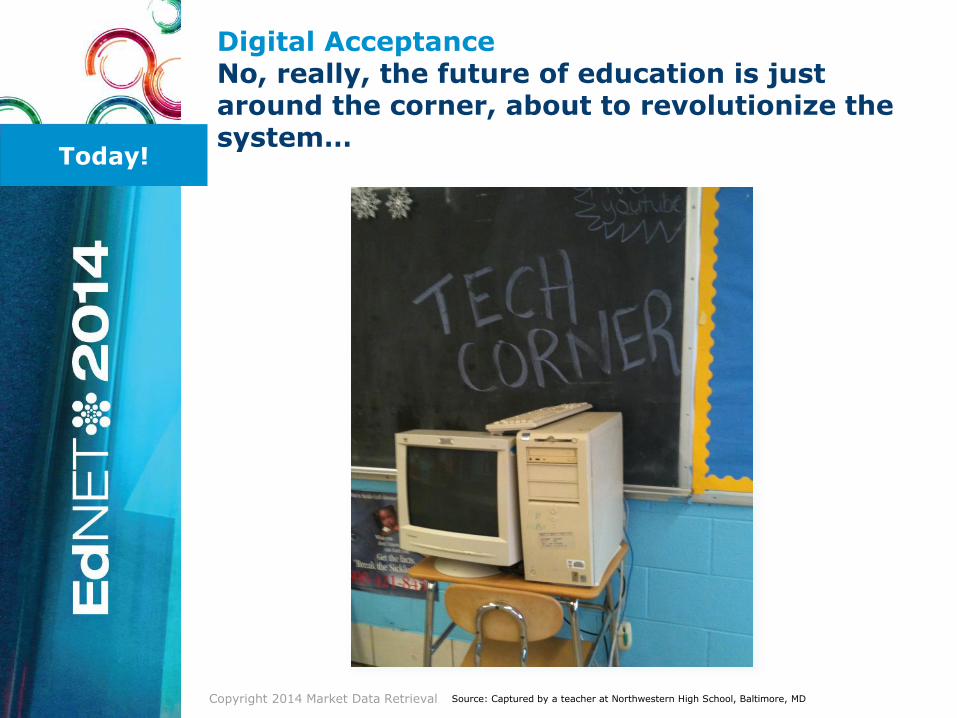

Digital Acceptance No, really, the future of education is just around the corner, about to revolutionize the system…

Today!

Source: Captured by a teacher at Northwestern High School, Baltimore, MD

Copyright 2014 Market Data Retrieval

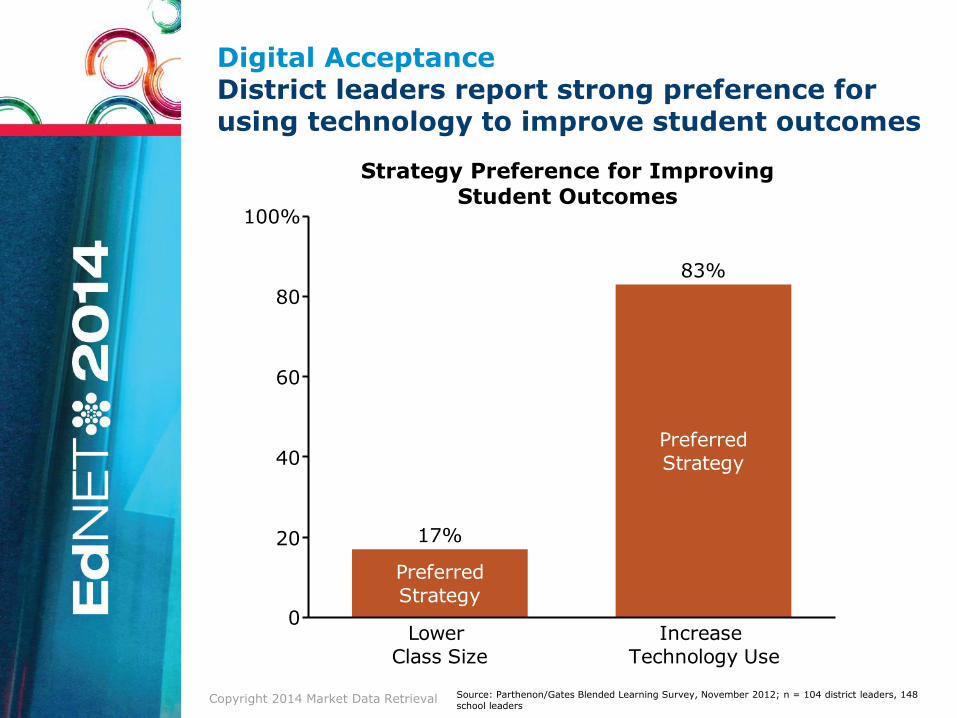

Digital Acceptance District leaders report strong preference for using technology to improve student outcomes

Source: Parthenon/Gates Blended Learning Survey, November 2012; n = 104 district leaders, 148 school leaders

0

20

40

60

80

100%

LowerClass Size

PreferredStrategy

17%

IncreaseTechnology Use

PreferredStrategy

83%

Strategy Preference for Improving Student Outcomes

Copyright 2014 Market Data Retrieval

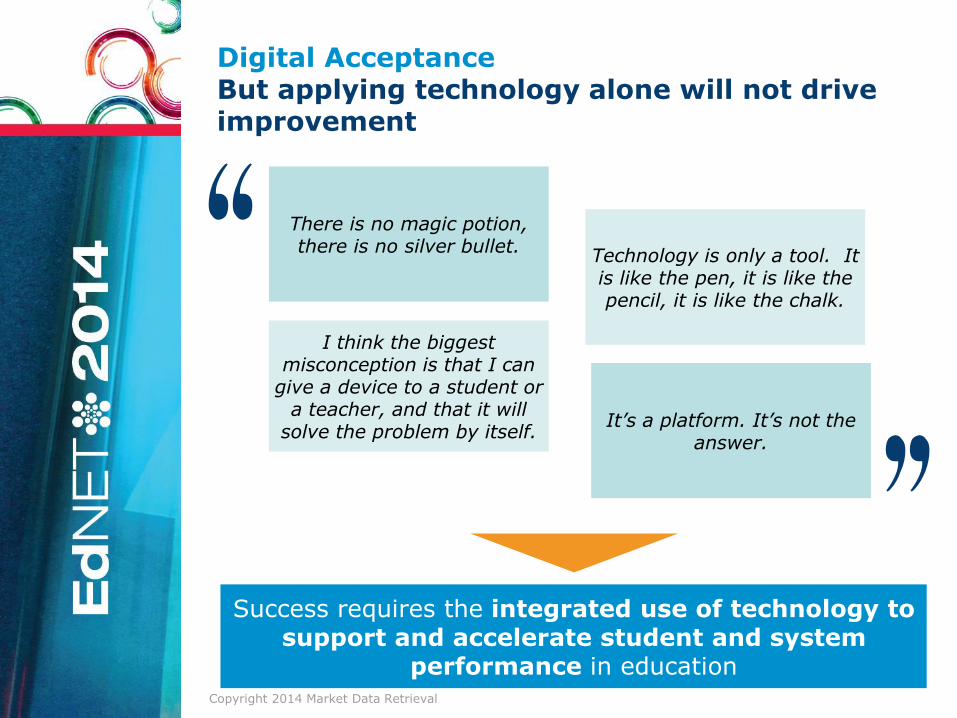

It’s a platform. It’s not the answer.

Digital Acceptance But applying technology alone will not drive improvement

Success requires the integrated use of technology to support and accelerate student and system

performance in education

Technology is only a tool. It is like the pen, it is like the pencil, it is like the chalk.

There is no magic potion, there is no silver bullet.

I think the biggest misconception is that I can

give a device to a student or a teacher, and that it will

solve the problem by itself.

Copyright 2014 Market Data Retrieval

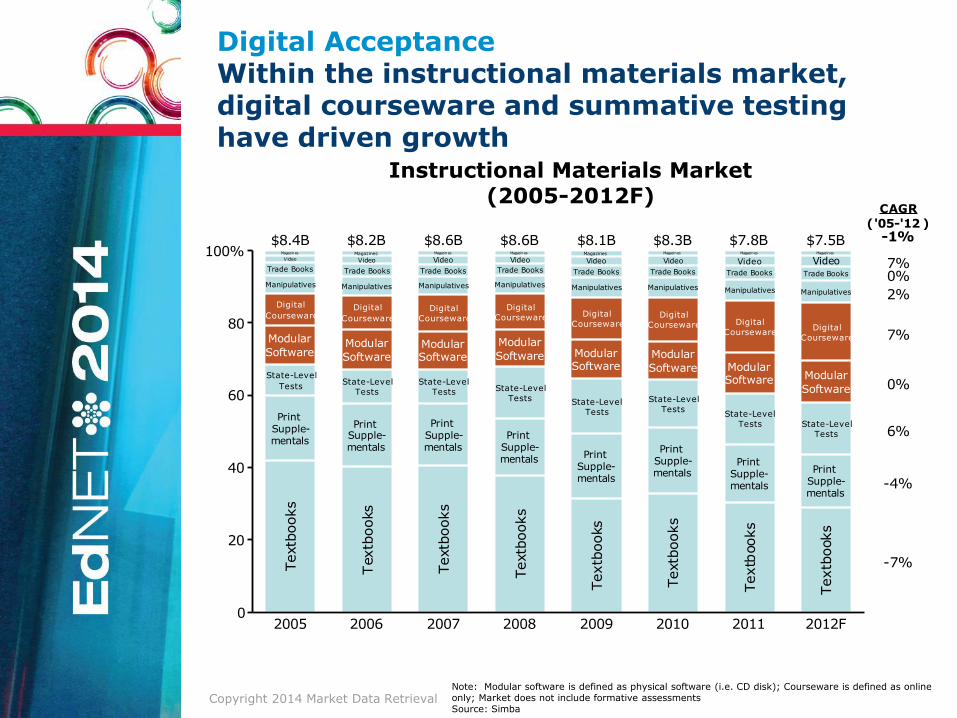

Digital Acceptance Within the instructional materials market, digital courseware and summative testing have driven growth

0

20

40

60

80

100%

2005

State-Level

Tests

Modular

Software

Textb

ooks

PrintSupple-mentals

Digital

Courseware

Video

Magazines

Manipulatives

Trade Books

$8.4B

2006

State-Level

Tests

Modular

SoftwareTextb

ooks

PrintSupple-mentals

Digital

Courseware

VideoMagazines

Manipulatives

Trade Books

$8.2B

2007

State-Level

Tests

ModularSoftware

Textb

ooks

PrintSupple-mentals

Digital

Courseware

VideoMagazines

Manipulatives

Trade Books

$8.6B

2008

State-Level

Tests

Modular

Software

Textb

ooks

PrintSupple-mentals

Digital

Courseware

VideoMagazines

Manipulatives

Trade Books

$8.6B

2009

State-Level

Tests

ModularSoftware

Textb

ooks

PrintSupple-mentals

Digital

Courseware

VideoMagazines

Manipulatives

Trade Books

$8.1B

2010

State-Level

Tests

Modular

Software

Textb

ooks

PrintSupple-mentals

Digital

Courseware

Video

Magazines

Manipulatives

Trade Books

$8.3B

2011

State-Level

Tests

ModularSoftware

Textb

ooks

PrintSupple-mentals

Digital

Courseware

Video

Magazines

Manipulatives

Trade Books

$7.8B

2012F

State-Level

Tests

Modular

Software

Textb

ooks

PrintSupple-mentals

Digital

Courseware

VideoMagazines

Manipulatives

Trade Books

$7.5B

-7%

-4%

6%

0%

7%

2%

0%7%

('05-'12 )-1%

CAGR

Instructional Materials Market (2005-2012F)

Note: Modular software is defined as physical software (i.e. CD disk); Courseware is defined as online only; Market does not include formative assessments Source: Simba

Copyright 2014 Market Data Retrieval

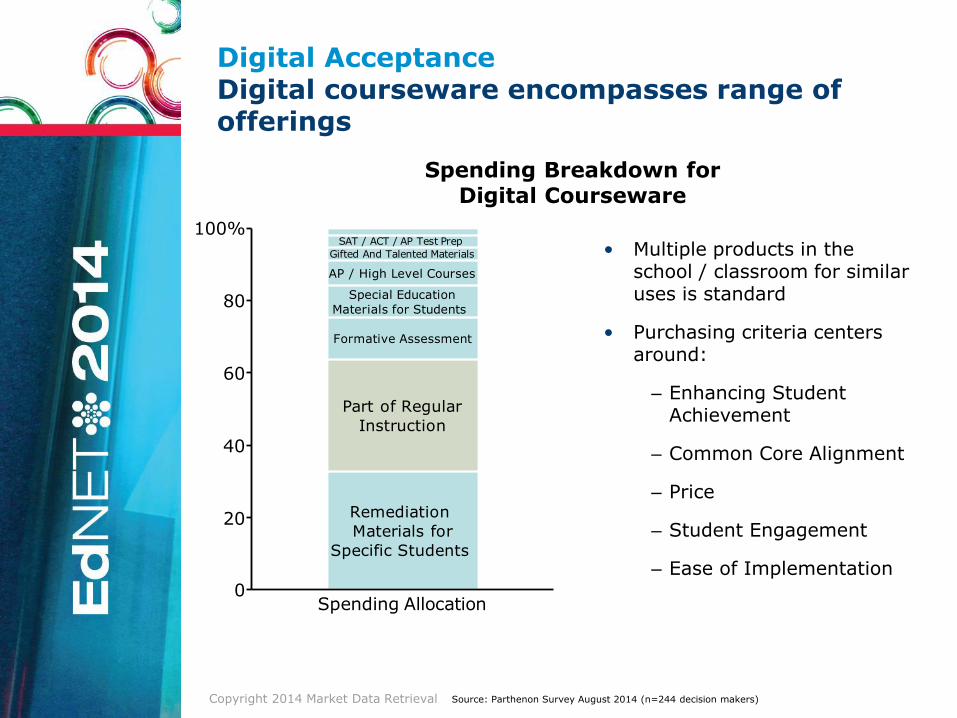

Digital Acceptance Digital courseware encompasses range of offerings

0

20

40

60

80

100%

Spending Allocation

SAT / ACT / AP Test Prep

Gifted And Talented Materials

AP / High Level Courses

Special Education

Materials for Students

Formative Assessment

Part of Regular

Instruction

Remediation

Materials for

Specific Students

• Multiple products in the school / classroom for similar uses is standard

• Purchasing criteria centers around:

‒ Enhancing Student Achievement

‒ Common Core Alignment

‒ Price

‒ Student Engagement

‒ Ease of Implementation

Spending Breakdown for Digital Courseware

Source: Parthenon Survey August 2014 (n=244 decision makers)

Copyright 2014 Market Data Retrieval

-50

0

50

100%

Significantly

Decrease

SlightlyDecrease

Slightly Increase

Significantly

Increase

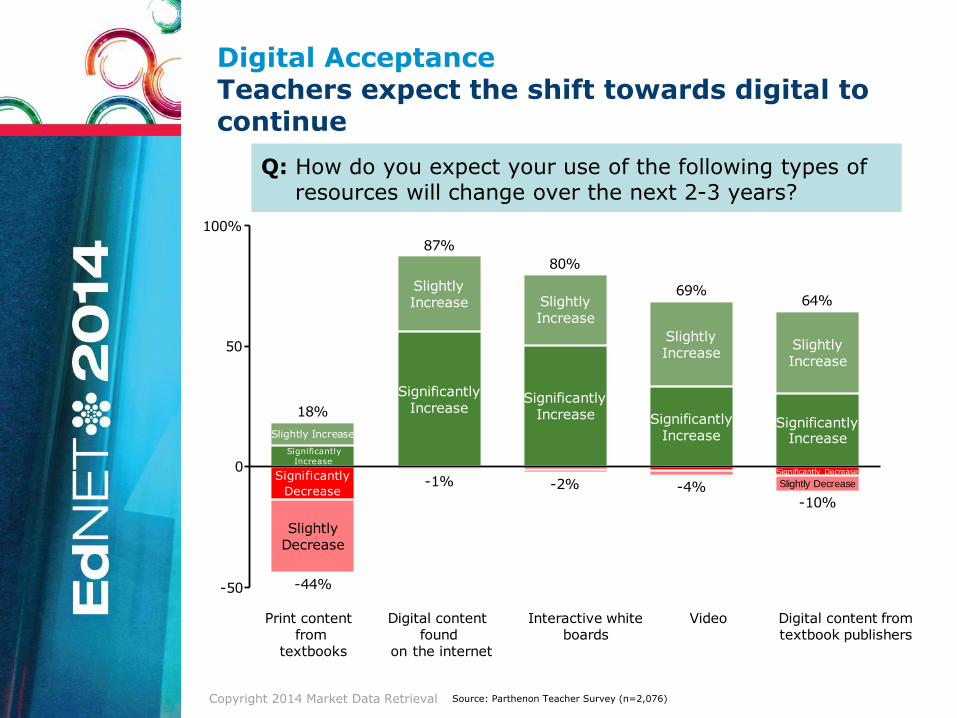

18%

-44%

SlightlyIncrease

SignificantlyIncrease

87%

-1%

SlightlyIncrease

SignificantlyIncrease

80%

-2%

SlightlyIncrease

SignificantlyIncrease

69%

-4%

Significantly Decrease

Slightly Decrease

SlightlyIncrease

SignificantlyIncrease

64%

-10%

Print contentfrom

textbooks

Digital contentfound

on the internet

Interactive whiteboards

Video Digital content fromtextbook publishers

Digital Acceptance Teachers expect the shift towards digital to continue

Q: How do you expect your use of the following types of resources will change over the next 2-3 years?

Source: Parthenon Teacher Survey (n=2,076)

Copyright 2014 Market Data Retrieval

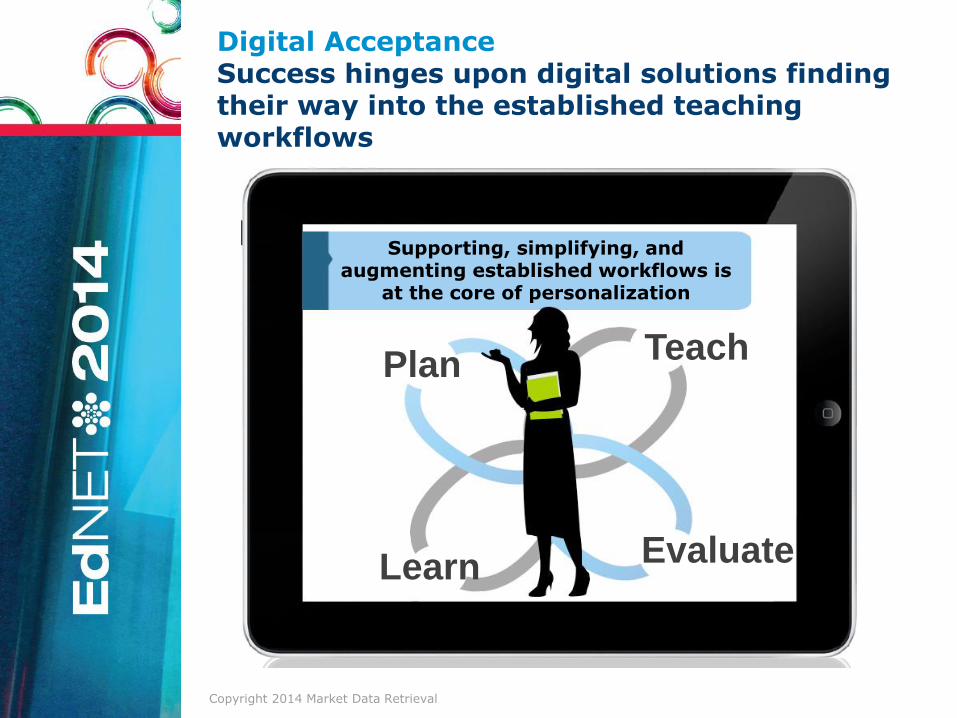

How do these digital

products integrate into the workflow?

Plan

Teach

Learn

Evaluate

Supporting, simplifying, and augmenting established workflows is

at the core of personalization

Digital Acceptance Success hinges upon digital solutions finding their way into the established teaching workflows

Copyright 2014 Market Data Retrieval

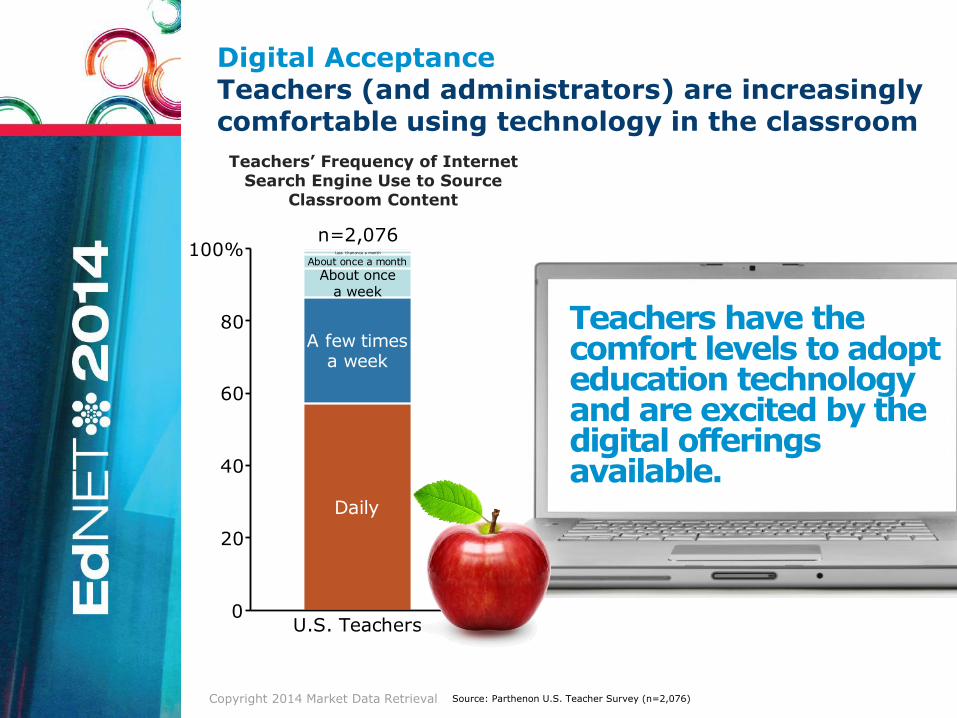

0

20

40

60

80

100%

U.S. Teachers

About oncea week

A few timesa week

Daily

Less thanonce a month

About once a month

n=2,076

Teachers have the comfort levels to adopt education technology and are excited by the digital offerings available.

Teachers’ Frequency of Internet Search Engine Use to Source

Classroom Content

Digital Acceptance Teachers (and administrators) are increasingly comfortable using technology in the classroom

Source: Parthenon U.S. Teacher Survey (n=2,076)

Copyright 2014 Market Data Retrieval

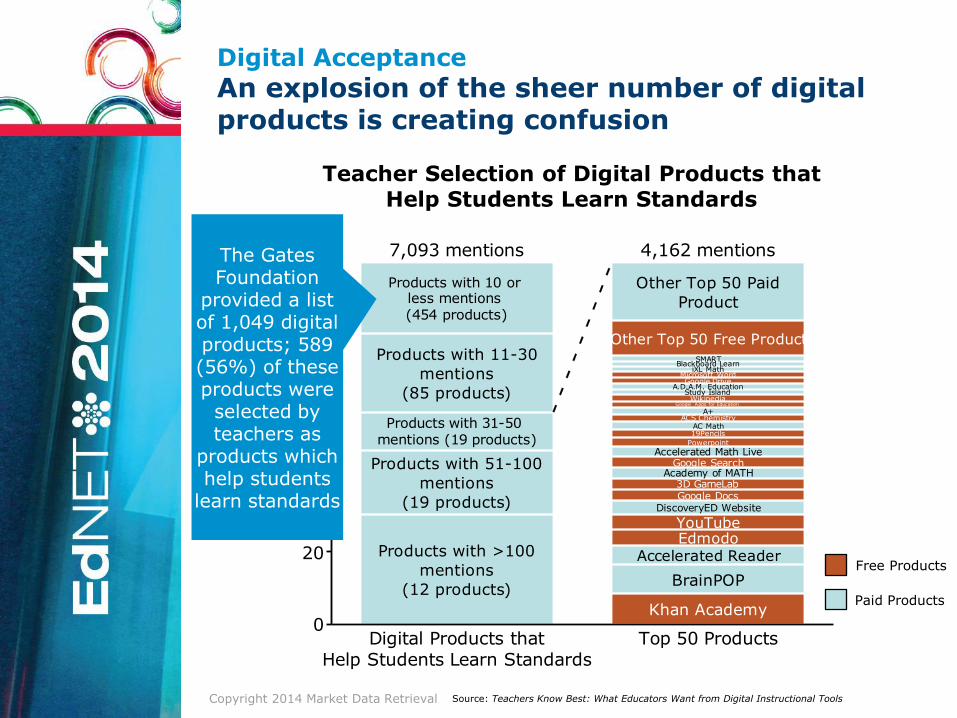

Where are the pain points?

Digital Acceptance Surprise, digital adoption is not always smooth and painless!

Copyright 2014 Market Data Retrieval

0

20

40

60

80

100%

Digital Products thatHelp Students Learn Standards

Products with 10 orless mentions(454 products)

Products with 11-30

mentions

(85 products)

Products with 31-50mentions (19 products)

Products with 51-100

mentions

(19 products)

Products with >100

mentions

(12 products)

7,093 mentions

Top 50 Products

Other Top 50 Paid

Product

Other Top 50 Free ProductSMART

Blackboard LearniXL Math

Microsoft WordGoogle Drive

A.D.A.M. EducationStudy Island

WikipediaGoogle Apps for Education

A+ACS Chemistry

AC Math19Pencils

Powerpoint

Accelerated Math LiveGoogle Search

Academy of MATH3D GameLabGoogle Docs

DiscoveryED Website

YouTubeEdmodo

Accelerated Reader

BrainPOP

Khan Academy

4,162 mentions

Digital Acceptance

An explosion of the sheer number of digital products is creating confusion

Teacher Selection of Digital Products that Help Students Learn Standards

The Gates Foundation

provided a list of 1,049 digital products; 589 (56%) of these products were

selected by teachers as

products which help students

learn standards

Free Products

Paid Products

Source: Teachers Know Best: What Educators Want from Digital Instructional Tools

Copyright 2014 Market Data Retrieval

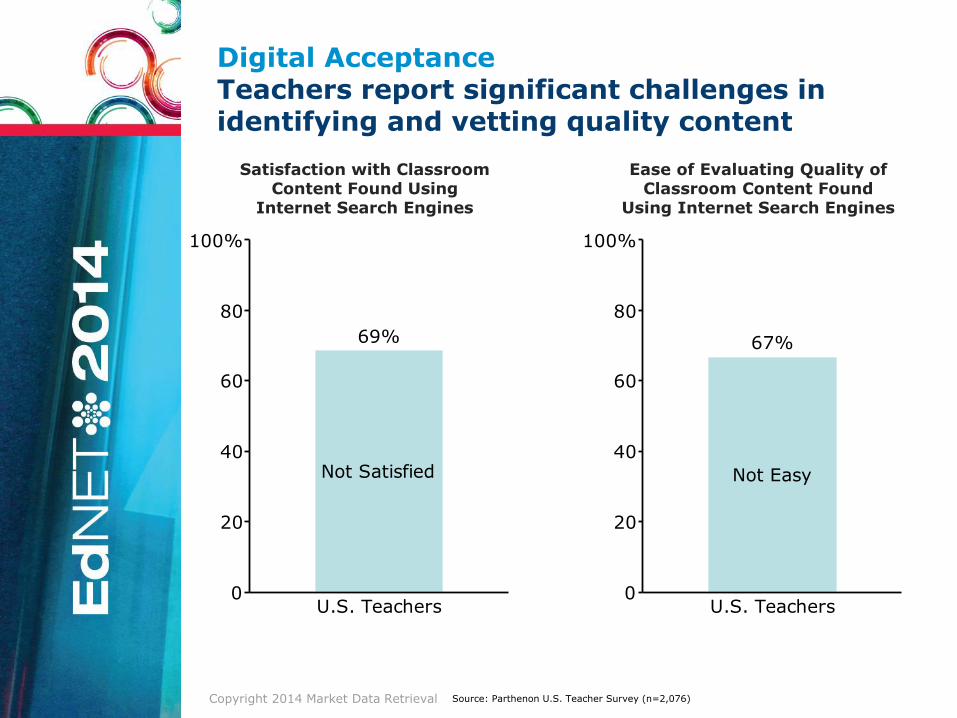

Digital Acceptance Teachers report significant challenges in identifying and vetting quality content

0

20

40

60

80

100%

U.S. Teachers

Not Satisfied

69%

Satisfaction with Classroom Content Found Using

Internet Search Engines

Ease of Evaluating Quality of Classroom Content Found

Using Internet Search Engines

0

20

40

60

80

100%

U.S. Teachers

Not Easy

67%

Source: Parthenon U.S. Teacher Survey (n=2,076)

Copyright 2014 Market Data Retrieval

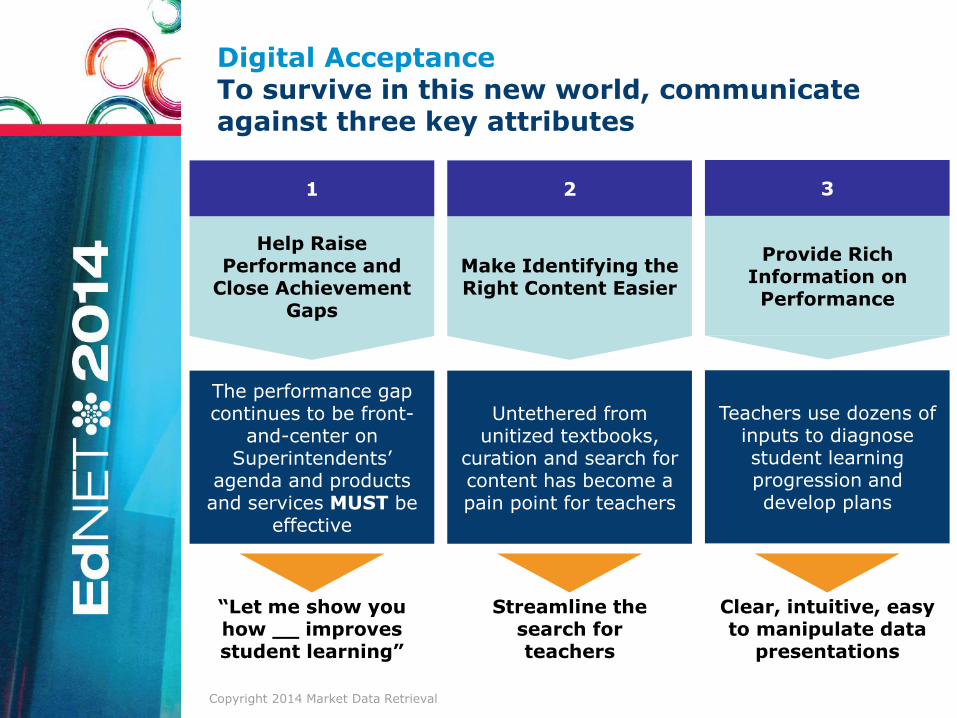

Digital Acceptance To survive in this new world, communicate against three key attributes

Help Raise Performance and

Close Achievement Gaps

1

The performance gap continues to be front-

and-center on Superintendents’

agenda and products and services MUST be

effective

“Let me show you how __ improves student learning”

Make Identifying the Right Content Easier

2

Untethered from unitized textbooks,

curation and search for content has become a pain point for teachers

Streamline the search for teachers

Provide Rich Information on Performance

3

Teachers use dozens of inputs to diagnose student learning progression and develop plans

Clear, intuitive, easy to manipulate data

presentations

Copyright 2014 Market Data Retrieval

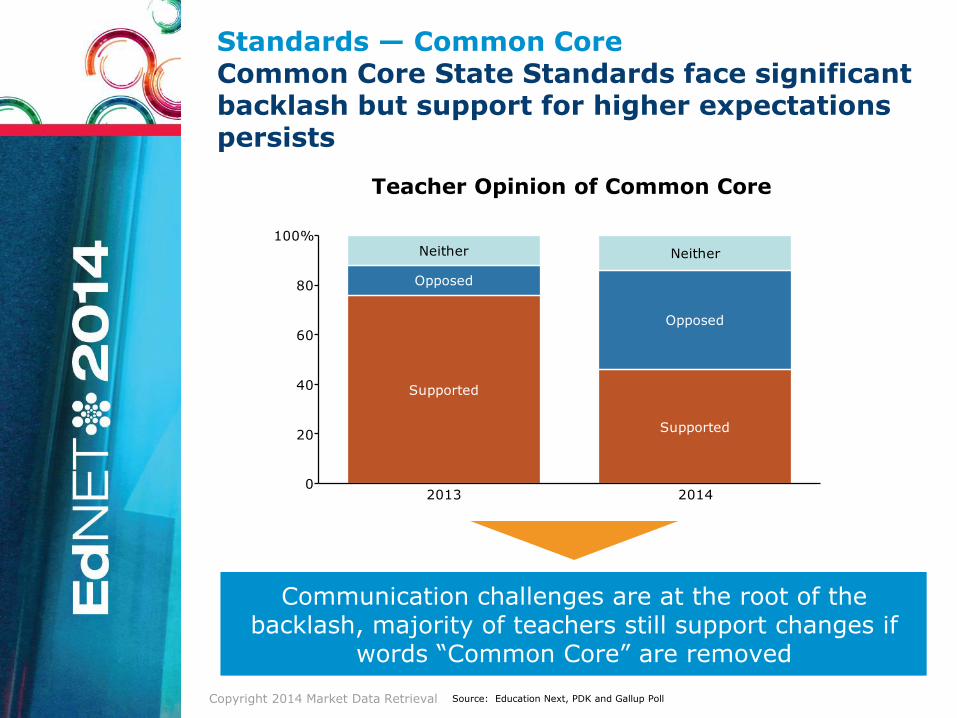

Standards — Common Core Common Core State Standards face significant backlash but support for higher expectations persists

Source: Education Next, PDK and Gallup Poll

Communication challenges are at the root of the backlash, majority of teachers still support changes if

words “Common Core” are removed

0

20

40

60

80

100%

2013

Neither

Opposed

Supported

2014

Neither

Opposed

Supported

Teacher Opinion of Common Core

Copyright 2014 Market Data Retrieval

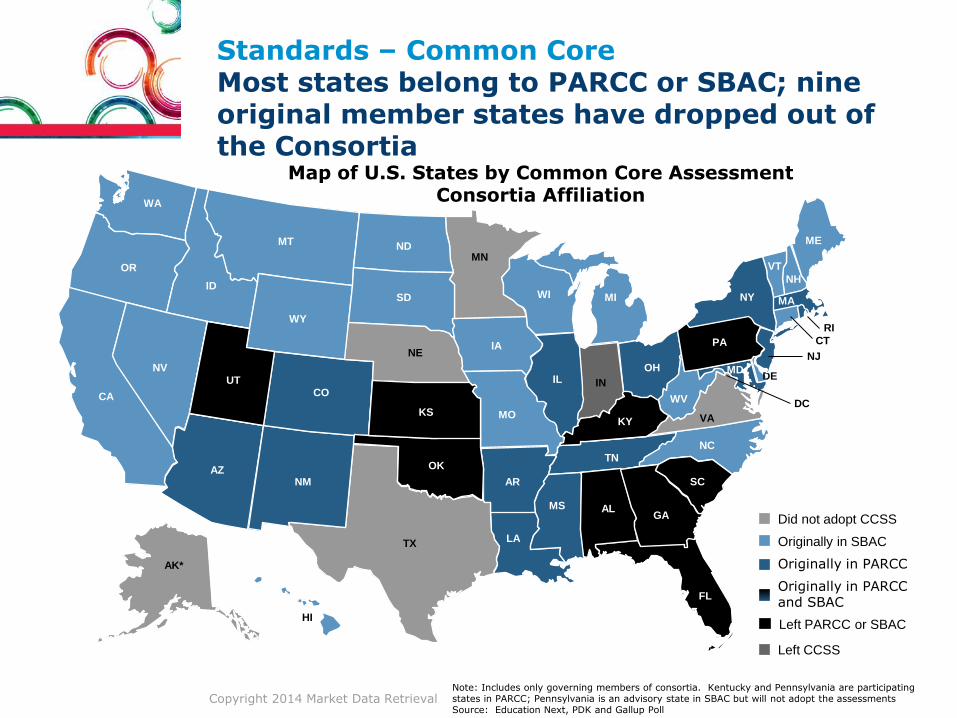

Standards – Common Core Most states belong to PARCC or SBAC; nine original member states have dropped out of the Consortia

Map of U.S. States by Common Core Assessment Consortia Affiliation

Review/Revision

Adopted

Never Adopted

Repealed

MA

FL

IA

AR

LA

MN

WI

MO

NH

VT

MI

PA

NY

ME

TN

KY

IN

OH

AL MS

IL

NC

SC

GA

WV

MD

VA

DE

CA

WA

OR

ID

NV

AZ

TX

UT

NM

CO

MT

WY

OK

KS

ND

SD

NE

AK*

HI

CT

RI

NJ

DC

Left PARCC or SBAC

Originally in SBAC

Originally in PARCC

Did not adopt CCSS

IN

Left CCSS

Originally in PARCC and SBAC

FL

PA

KY

AL GA

UT

OK

KS

SC

Note: Includes only governing members of consortia. Kentucky and Pennsylvania are participating states in PARCC; Pennsylvania is an advisory state in SBAC but will not adopt the assessments Source: Education Next, PDK and Gallup Poll

Copyright 2014 Market Data Retrieval

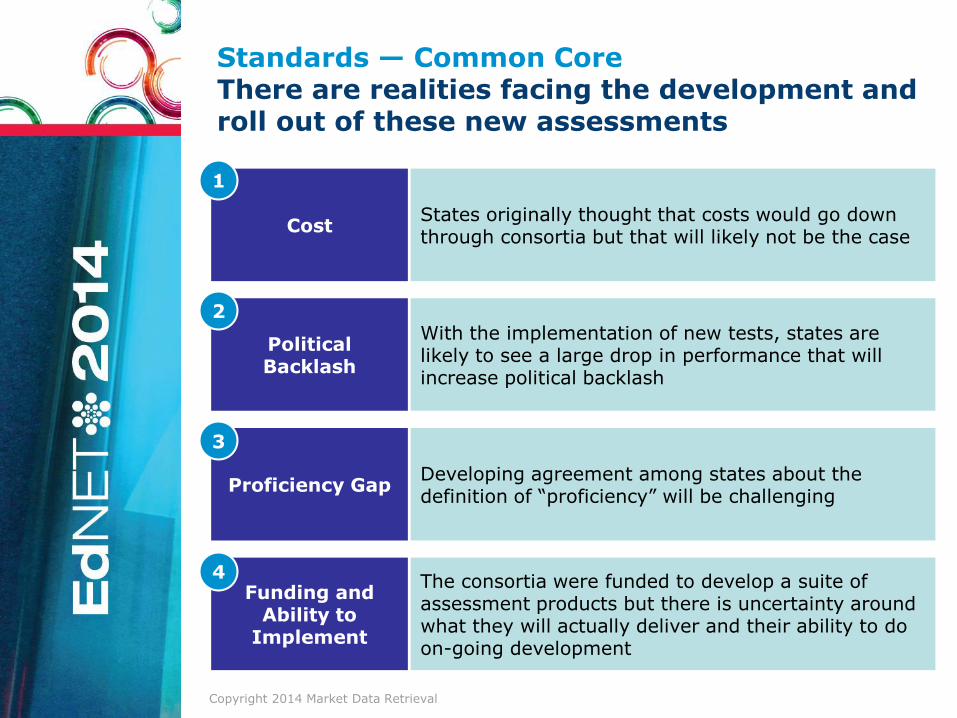

Standards — Common Core There are realities facing the development and roll out of these new assessments

With the implementation of new tests, states are likely to see a large drop in performance that will increase political backlash

Developing agreement among states about the definition of “proficiency” will be challenging

The consortia were funded to develop a suite of assessment products but there is uncertainty around what they will actually deliver and their ability to do on-going development

States originally thought that costs would go down through consortia but that will likely not be the case

Cost

1

Political Backlash

2

Proficiency Gap

3

Funding and Ability to

Implement

4

Copyright 2014 Market Data Retrieval

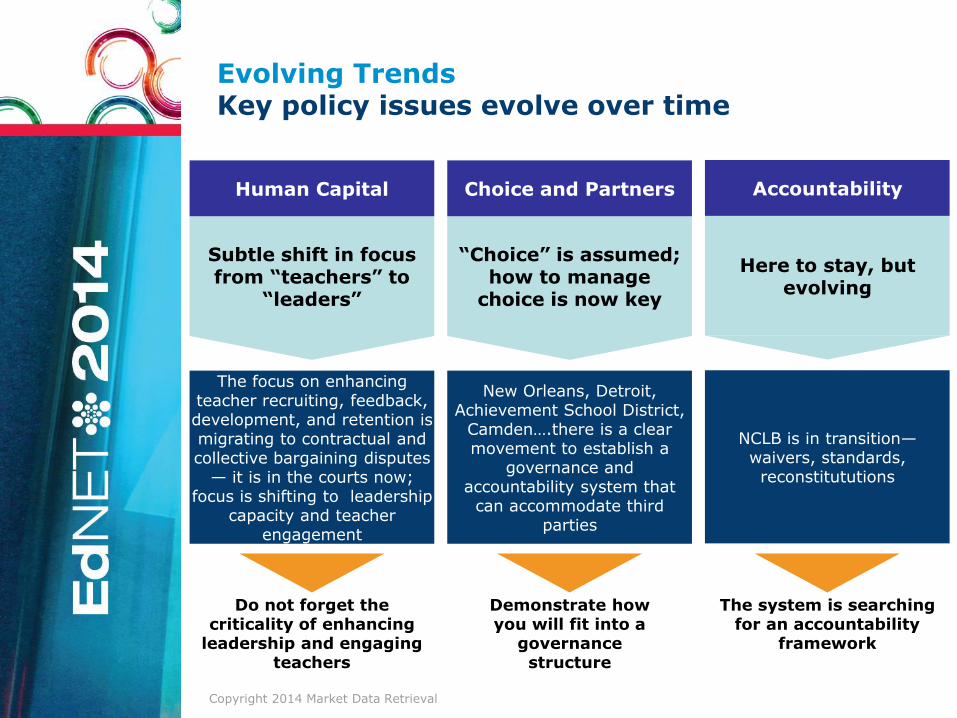

Evolving Trends Key policy issues evolve over time

Subtle shift in focus from “teachers” to

“leaders”

Human Capital

The focus on enhancing teacher recruiting, feedback, development, and retention is migrating to contractual and collective bargaining disputes

— it is in the courts now; focus is shifting to leadership

capacity and teacher engagement

Do not forget the criticality of enhancing

leadership and engaging teachers

“Choice” is assumed; how to manage

choice is now key

Choice and Partners

New Orleans, Detroit, Achievement School District,

Camden….there is a clear movement to establish a

governance and accountability system that

can accommodate third parties

Demonstrate how you will fit into a

governance structure

Here to stay, but evolving

Accountability

NCLB is in transition—waivers, standards, reconstitututions

The system is searching for an accountability

framework

Copyright 2014 Market Data Retrieval

About Parthenon

About Parthenon

Parthenon has served as an advisor to the education sector since our inception in 1991. Our Education Practice – the first of its

kind across management consulting firms – has an explicit mission and vision to be the leading strategy advisor to the global

education industry. To achieve this, we invest significantly in dedicated management and team resources to ensure that our

global expertise extends across public sector and non-profit education providers, foundations, for-profit companies and service

providers, and investors. Parthenon has deep experience and a track record of consistent success in working closely with

universities, colleges, states, districts, and leading educational reform and service organizations across the globe.

Learn more about us at www.parthenon.com.

Twitter | @Parthenon_Group

Facebook | www.facebook.com/ParthenonGroup

LinkedIn | www.linkedin.com/company/the-parthenon-group

Follow Us

for Regular

Updates

Robert Lytle

Partner, Co-Head of Education Practice

617.478.7096

Executive Assistant:

Deb Spitzley

617.478.6312

Twitter | @Robert_S_Lytle