41

Paying the Employee Payroll Source Review Course Fall 2013 Presented by: Carmela Miller, CPP [email protected] om

| Date post: | 16-Dec-2015 |

| Category: |

Documents |

| Upload: | jocelyn-lesley-doyle |

| View: | 228 times |

| Download: | 3 times |

Paying the Employee

Payroll SourceReview Course Fall 2013

Presented by:Carmela Miller, [email protected]

Chapter 5 ------ Objectives

• Pay Frequency• Payment on Termination• Payment Methods– Cash or Check– Direct Deposit– Electronic Paycards• Branded vs. Non-Branded

Objectives cont.

• Pay Statements• Unclaimed Paychecks (Escheatment)• Wages owed to deceased Employees• Extra Pay Periods (53rd pay period in a year)

Certification is based on Federal not State LawsContent of Chapter 5 is a great resource for State Regulations on Employee Payment. Always check for Updates on States• State Reference Charts• State by State Pay Frequency• State by State Payment upon Termination (Another good

source for this is the APA book on States)• State by State rules on Direct Deposit (this could always

change)• Paycard State Compliance issues, Pay Stub Information • Escheatment• State by State wages to deceased employees

Chapter 5- Paying the Employee

Payroll Frequency & Payment on Termination

5.1 Pay Frequency

• States Regulate how often employees must be paid.

• Table 5.1 gives us a quick look at state rules– Another great source is the State Book by APA

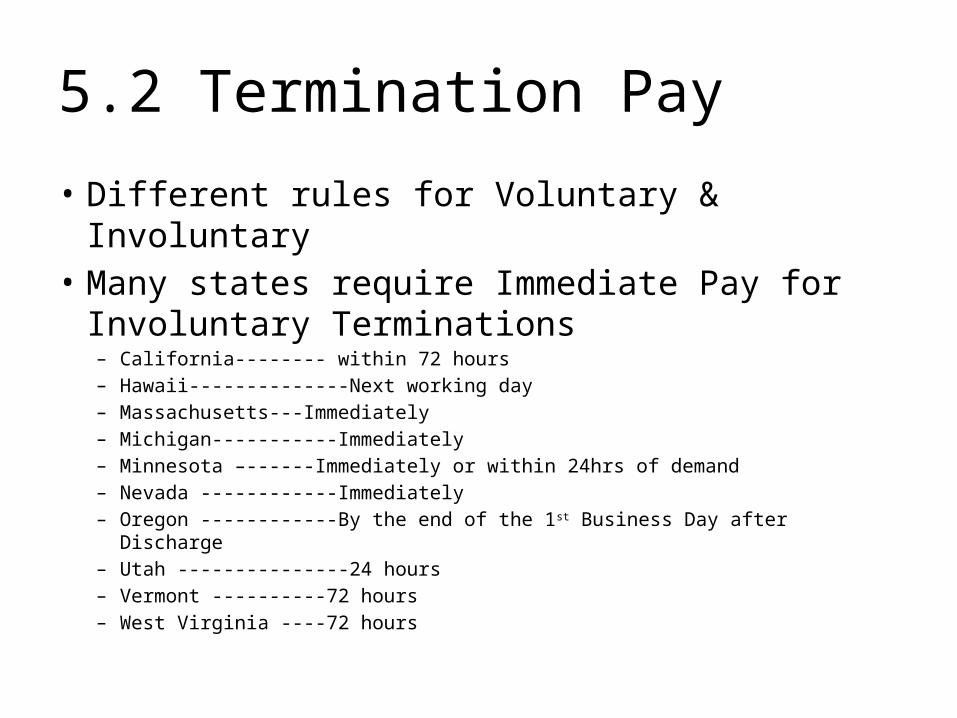

5.2 Termination Pay

• Different rules for Voluntary & Involuntary• Many states require Immediate Pay for

Involuntary Terminations– California-------- within 72 hours– Hawaii--------------Next working day– Massachusetts---Immediately– Michigan-----------Immediately– Minnesota –------Immediately or within 24hrs of demand– Nevada ------------Immediately– Oregon ------------By the end of the 1st Business Day after Discharge– Utah ---------------24 hours– Vermont ----------72 hours– West Virginia ----72 hours

Payment Methods

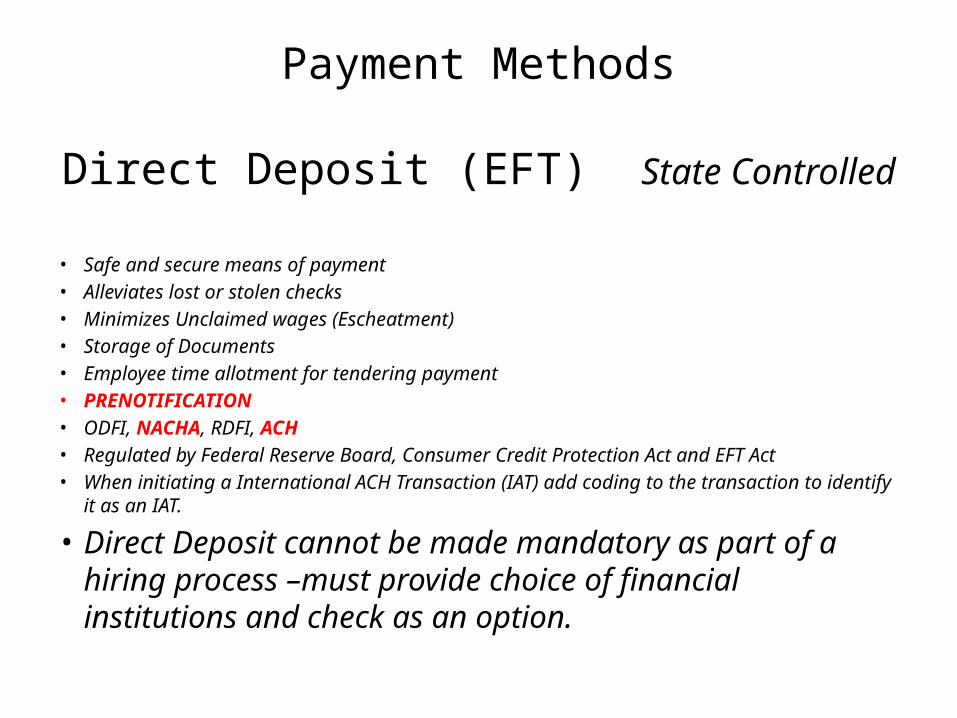

Direct Deposit (EFT) State Controlled

• Safe and secure means of payment• Alleviates lost or stolen checks• Minimizes Unclaimed wages (Escheatment)• Storage of Documents• Employee time allotment for tendering payment• PRENOTIFICATION• ODFI, NACHA, RDFI, ACH• Regulated by Federal Reserve Board, Consumer Credit Protection Act and EFT Act• When initiating a International ACH Transaction (IAT) add coding to the transaction to identify it as

an IAT.

• Direct Deposit cannot be made mandatory as part of a hiring process –must provide choice of financial institutions and check as an option.

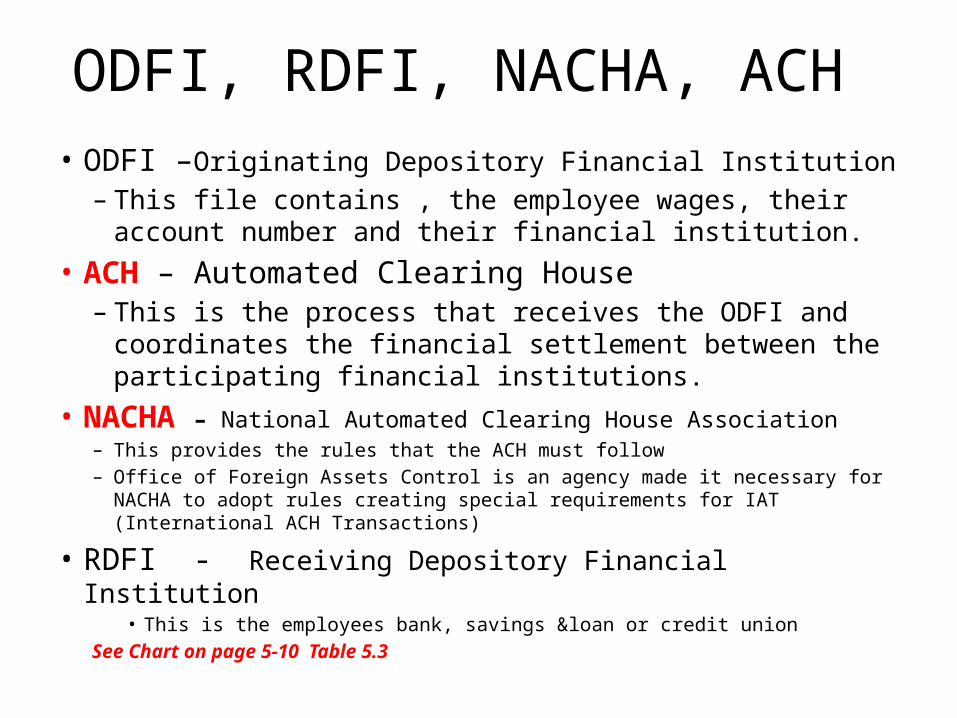

ODFI, RDFI, NACHA, ACH• ODFI –Originating Depository Financial Institution– This file contains , the employee wages, their account

number and their financial institution.• ACH – Automated Clearing House– This is the process that receives the ODFI and coordinates

the financial settlement between the participating financial institutions.

• NACHA – National Automated Clearing House Association– This provides the rules that the ACH must follow– Office of Foreign Assets Control is an agency made it necessary for NACHA to adopt

rules creating special requirements for IAT (International ACH Transactions)

• RDFI - Receiving Depository Financial Institution• This is the employees bank, savings &loan or credit union

See Chart on page 5-10 Table 5.3

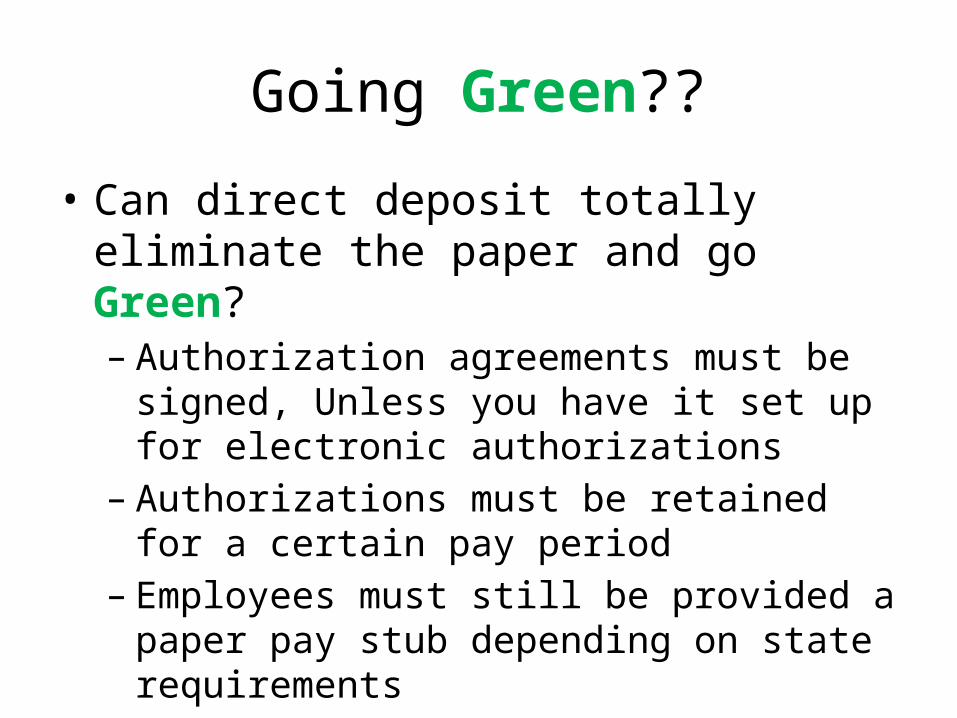

Going Green??

• Can direct deposit totally eliminate the paper and go Green?– Authorization agreements must be signed, Unless

you have it set up for electronic authorizations– Authorizations must be retained for a certain pay

period– Employees must still be provided a paper pay stub

depending on state requirements

Chapter 5 – Paying the Employee

Payment Methods

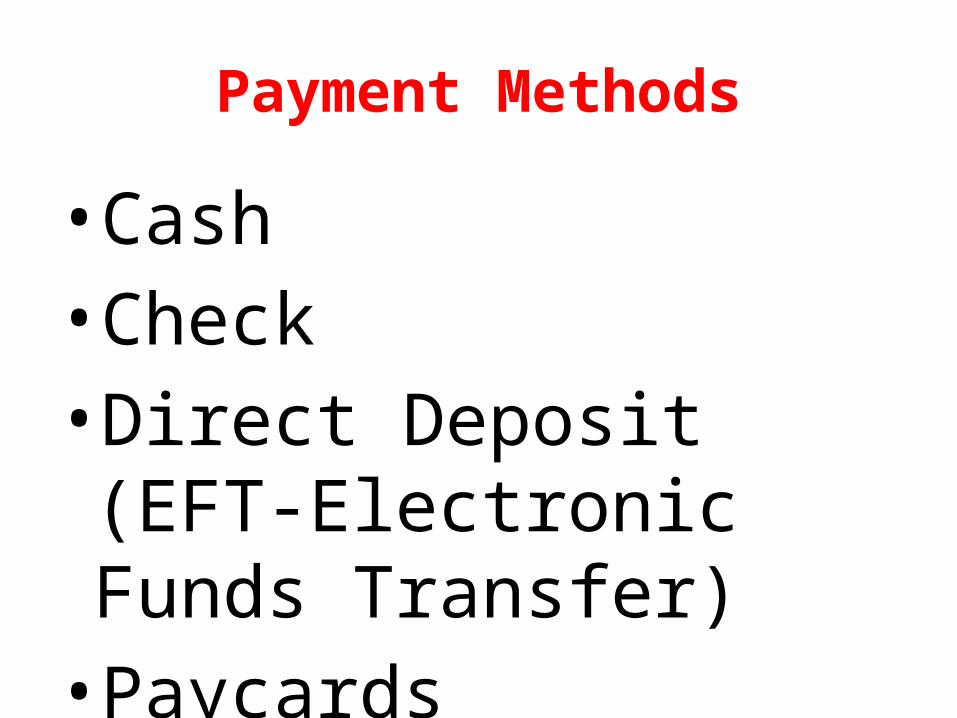

Payment Methods

•Cash•Check•Direct Deposit (EFT-

Electronic Funds Transfer)•Paycards

Cash or Check ???• Generally all 50 states allow payments by cash or check without

additional law or regulations regarding this payment option.– Ease of tendering the negotiable payments by:

• Financial Institutions must be convenient/or even located in state of company’s operations

• No additional fees are imposed for tendering the payment option(unless it is a check and the employee does not have a checking account)

– Security• Signatures required• Internal Audit and need checks and balances

Be mindful of the impact that a voided or manual check issuance causes to other departments process

GL, Taxes, Benefits

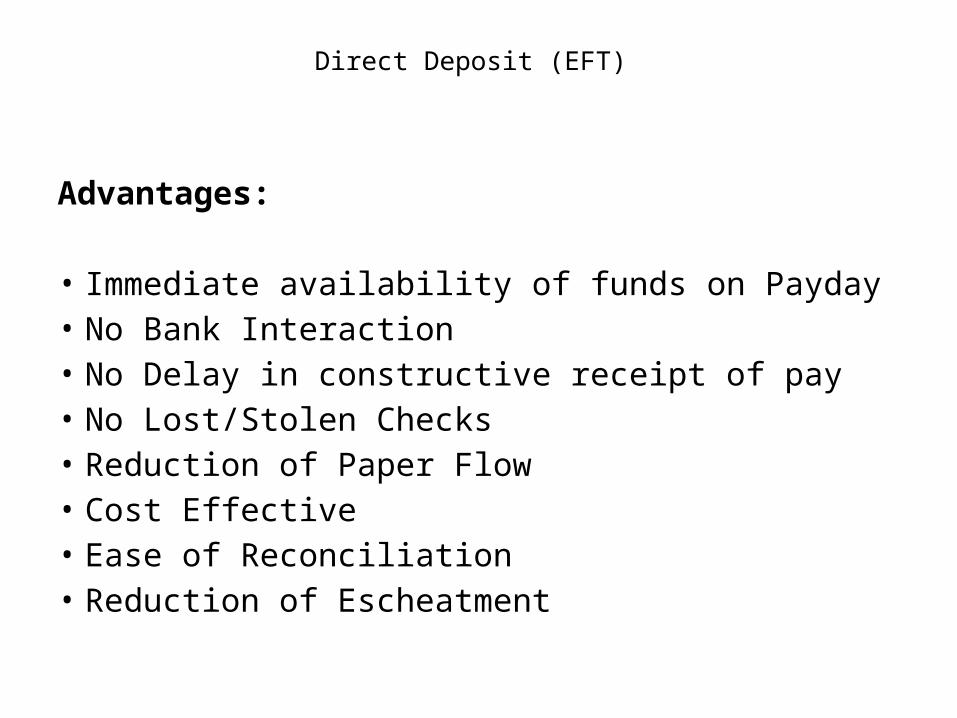

Direct Deposit (EFT)

Advantages:

• Immediate availability of funds on Payday• No Bank Interaction• No Delay in constructive receipt of pay• No Lost/Stolen Checks• Reduction of Paper Flow• Cost Effective• Ease of Reconciliation• Reduction of Escheatment

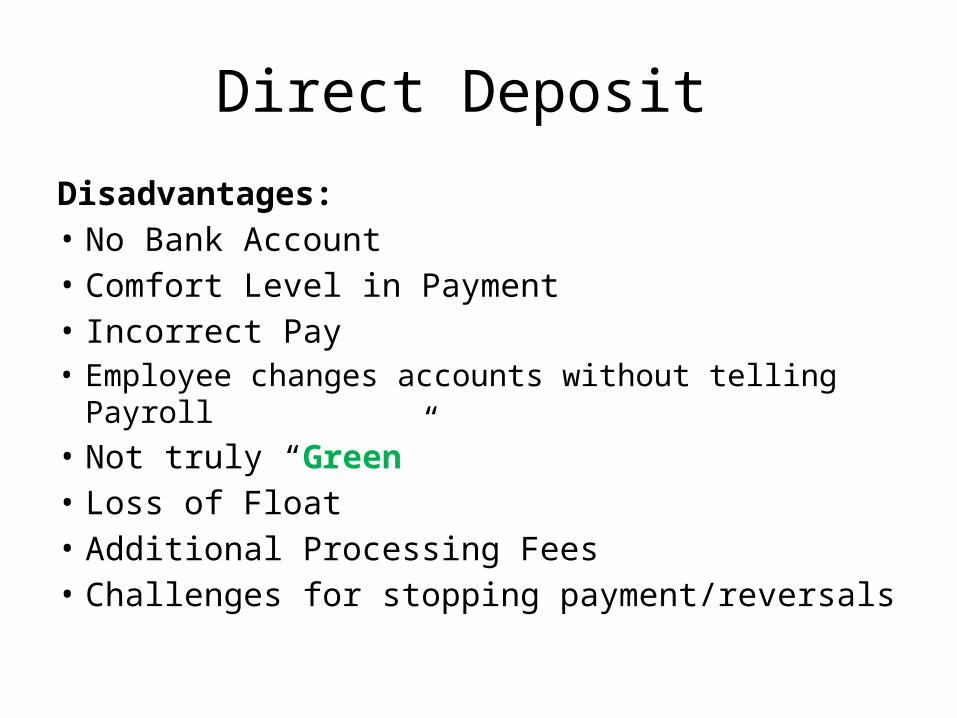

Direct Deposit

Disadvantages:• No Bank Account• Comfort Level in Payment• Incorrect Pay• Employee changes accounts without telling Payroll• Not truly “Green”• Loss of Float• Additional Processing Fees• Challenges for stopping payment/reversals

Direct Deposits

Late Direct Deposits:• Troubleshooting Funds must be posted by 9:00 am on pay date

• Verify Routing and Account Numbers Prenote?

• RDFI posting schedule• Federal Holiday Impact on processingAdditional resources can be found in communications with the ODFI for internal challenges.Regardless of delay – funds should be honored without penalty to employee. Based on voucher verification.

Employers must keep the authorization agreement for at least 2 yrs after revocation,

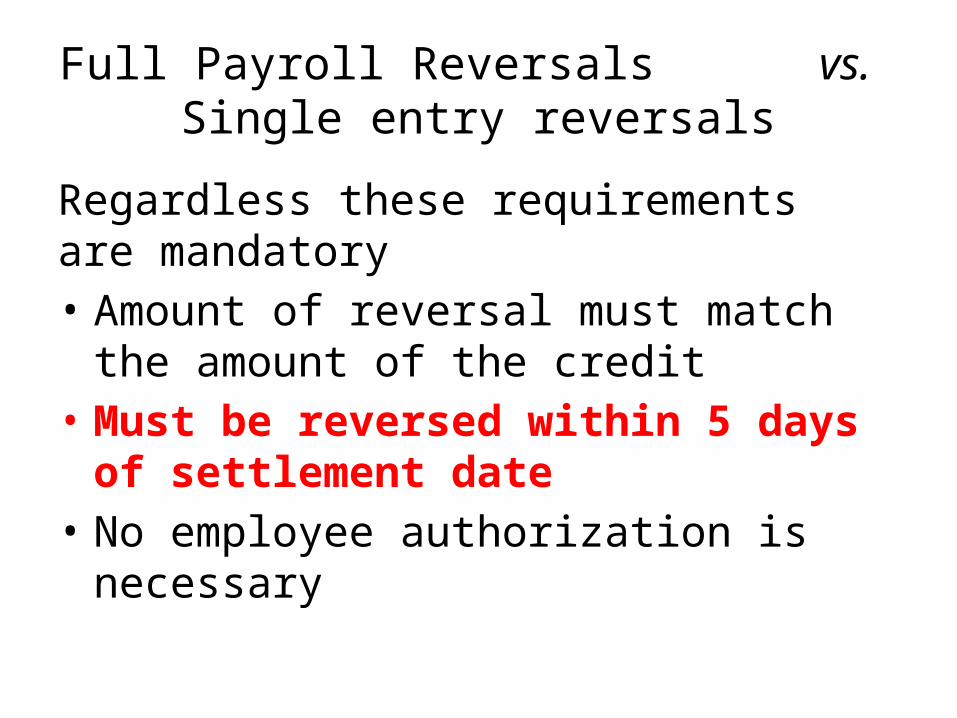

Full Payroll Reversals vs. Single entry reversals

Regardless these requirements are mandatory• Amount of reversal must match the amount of

the credit• Must be reversed within 5 days of settlement

date• No employee authorization is necessary

Chapter 5 – Paying the Employee

Pay Cards

Paycards

• Paycards are similar to debit cards• Prefunded, host based cards providing

employees access to their net pay via bank, ATM (Automatic Teller Machine) or POS( Point of Sale) purchase.

• Paycards are similar to direct deposit• Funding process for the employer is same as for

direct deposit• Process subject to the same NACHA regulations.

Paycards cont.

• New way to pay employees• Many variable options in the plans• Many competitors trying for business – ensure

reputability• Verify with legal for implications from plan• Cardholder security• Employee age (18 yrs)and turnover consideration• Understand the difference between branded vs.

non-branded

Paycards Branded vs. Non-Branded

Branded:

• Visa MC Discover• Employee Signature only, easily used if stolen• ATM – PIN• Personalized• Parental Approval < 18 yrs old

PaycardsBranded vs. Non-Branded

Non-Branded• Network Logo• PIN required for ALL transactions, Stolen card

only needs pin to purchase• Most reliable – Safer• Host computer authorizes funds are there

PaycardsEmployee & Employer Benefits

Employee:

• Reduced costs• Increased independence• Improved credit status (not true with all cards)• Financial Safety• Ease of use• Replenishment if lost• No time or geographical limitations

PaycardsEmployee & Employer Benefits

Employer:

• Reduced Costs• Enhanced efficiency• All employees eligible• Increases employee productivity time• Escheatment reduction

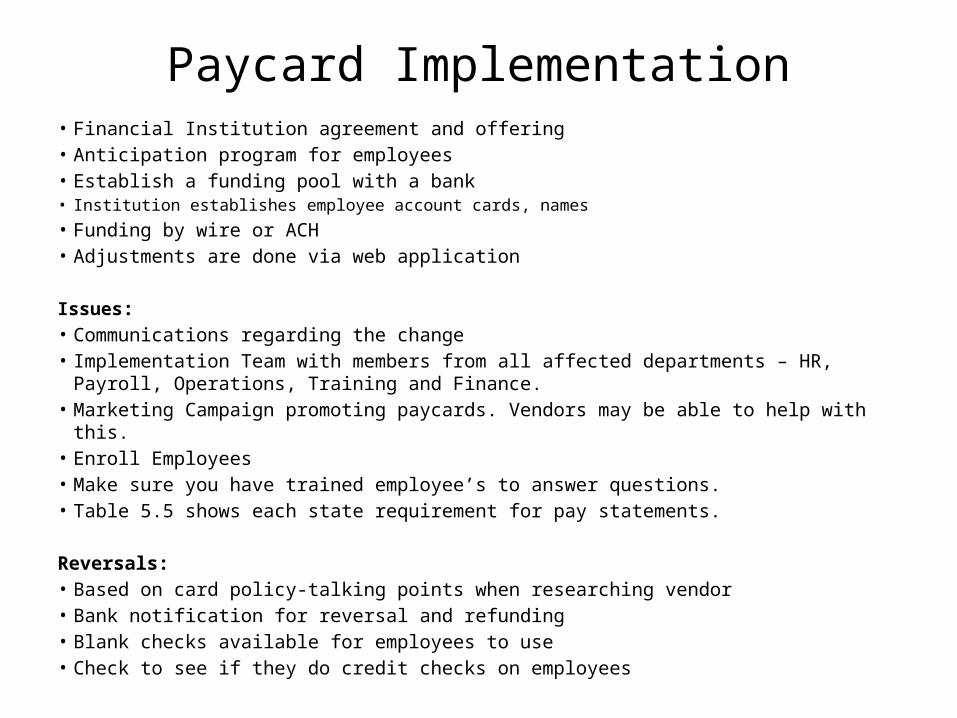

Paycard Implementation• Financial Institution agreement and offering• Anticipation program for employees• Establish a funding pool with a bank• Institution establishes employee account cards, names• Funding by wire or ACH• Adjustments are done via web application

Issues:• Communications regarding the change• Implementation Team with members from all affected departments – HR, Payroll, Operations,

Training and Finance.• Marketing Campaign promoting paycards. Vendors may be able to help with this.• Enroll Employees• Make sure you have trained employee’s to answer questions.• Table 5.5 shows each state requirement for pay statements.

Reversals:• Based on card policy-talking points when researching vendor• Bank notification for reversal and refunding• Blank checks available for employees to use• Check to see if they do credit checks on employees

Escheatment

Escheatment is the unclaimed wages (form of abandoned property) process governed by State Laws• State regulated (See table 5.6)• Length of time payment held (generally 1 yr)

– New York/Oregon – 3 yrs– North Dakota/Pennsylvania – 2 yrs.

• Notification process• Wage turnover process

Best practice is to utilize direct deposit and paycards as wage payment methods.

Wages Owed to Deceased EmployeesPayments, Payee and Taxation are based on when the employee passes. (See Table 5.7)

• Federal Regulates Taxation• State Laws Regulates the payee and payment amount in

accordance with the current situation.

Illinois: Maximum Payable: All unpaid wages To Whom: Person owed for funeral expenses, spouse or child. Allowed Conditions to Pay: Small estate affidavit: estate not over $15,000

Extra Pay DaysEach year we have extra pay days caused by the calendar.• Years affected with the 53rd pay period.

2012, 2013, 2014 (Wednesday),2015, 2016• Payroll must anticipate and plan for proper processing and compliance.

– Holidays– Weekend pay date

• Salaried employees can be adjusted. Most employers don’t bother• Hourly employees must be paid all wages. No different

Best practice is to maintain pay structure and schedule without deviation…Keep good relations with employees.Verify contracts if applicable.

Review Questions

1. What laws govern how often employers must pay employees?

2. Who governs the treatment of Escheat laws?

3. What is a branded pay card?

Review Cont.

True or False1. The Fair Labor Standards Act regulates how often employees

must be paid by their employer or how soon they must be paid after performing services.

2. Direct Deposit is one area where the federal and state governments share regulatory responsibility.

3. All States regulate the payment of wages owed to deceased employees.

4. A bi-weekly salary is paid twice a month, usually the 15 th and last day of the month.

5. If 250 employees consent to direct deposit, then all employees must comply.

Review Cont.

Multiple Choices:1. The employer prepares a automated file of direct

deposit records that indicates where its employee’s pay is to be deposited. What is the name of the financial institution where this file is then sent?

a) Automated Clearing Houseb) Originating Depository Financial Institutionc) NACHAd) Receiving Depository Financial Institution

Review Cont.

2. How many years must an employee keep the authorization agreement for direct deposit after revocation by the employee?a) At least two yearsb) At least one yearc) There is no retention requirementd) At least three years

Review Cont.

3. What are “escheat” laws?a) Federal laws governing the treatment of

unclaimed wages as abandoned property.b) State laws governing the treatment of

unclaimed wages as abandoned property.c) State laws protecting employees from their

employerd) State laws outlining the frequency with which

employees are paid.

Review Cont.

4. Once an employee has given authorization for EFT and the employer creates electronic pay transactions for deposit, where does the employer send them?a) ACHb) RDFIc) ODFId) NACHA

Review Cont.

5. Under the EFT system, what participating party receives the individual transactions and posts them to the customers’/employees’ accounts?

a) ODFIb) ACHc) RDFId) NACHA

Review Cont.

6. Which of the following laws and regulations does not regulate EFT?

a) Federal Reserve Board Regulation Eb) Title IX of the Consumer Credit Protection Actc) Fair Labor Standards Actd) Electronic Fund Transfer Act

Review Cont.

7. Which of the following agencies made it necessary for NACHA to adopt rules creating special requirements for International ACH Transactions?a) Internal Revenue Serviceb) Federal Reserve Boardc) Department of Stated) Office of Foreign Assets Control

Review Cont.

8. Which of the following participants in the direct deposit process distributes EFT payments to the receiving financial institutions?

a) ODFIb) ACHc) RDFId) FRB

Review Cont.

9. Which of the following is not an employee benefit of using paycards to pay employee wages?a) Eliminating check cashing feesb) Increased risk of paycheck theftc) Protection from loss because paycard can be

replacedd) No time or geographic limitations on funds

access

Review Cont.

10.If an employer uses pre-notification to test the employee’s banking information before initiating direct deposit, how long before any actual pay is sent through the ACH network must be pre-notification be sent?

a) 6 Banking Daysb) 2 weeksc) 3 Banking Daysd) 6 Calendar Days

Paying the Employees

QuestionsComments

Read the chapter, do the quizzes, know the difference between ACH, ODFI, RDFI, NACHA and IAT

Read Questions twice, know what they are asking!