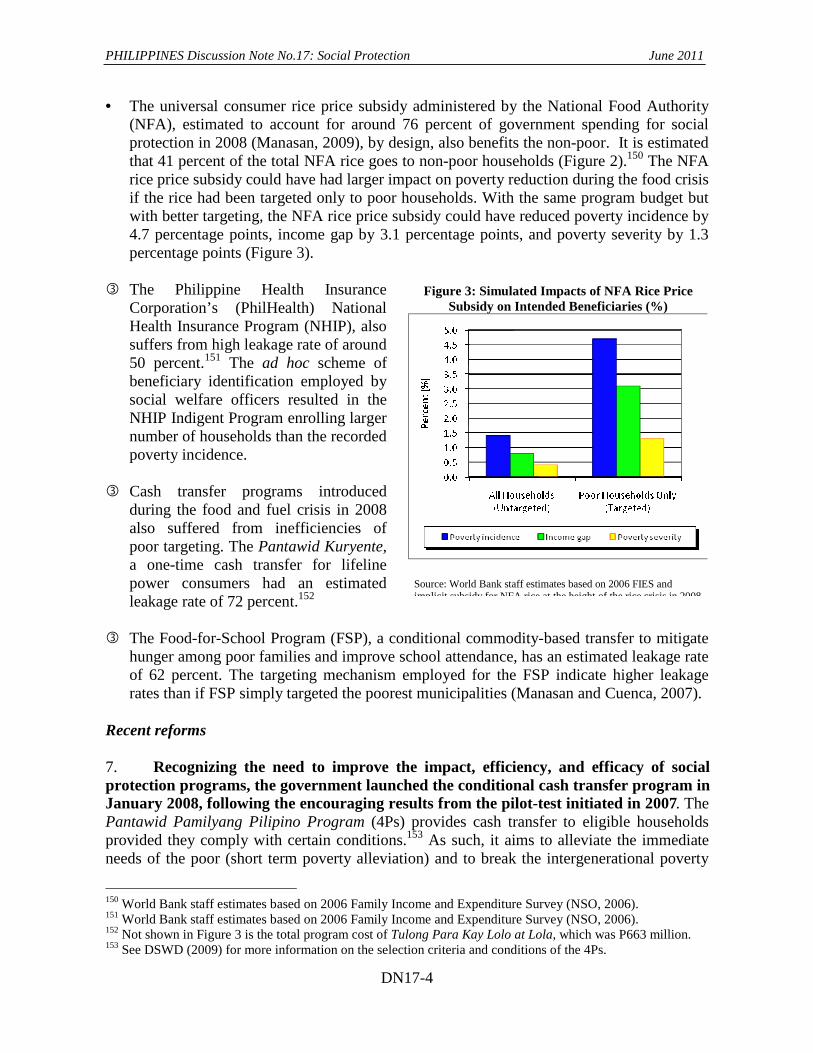

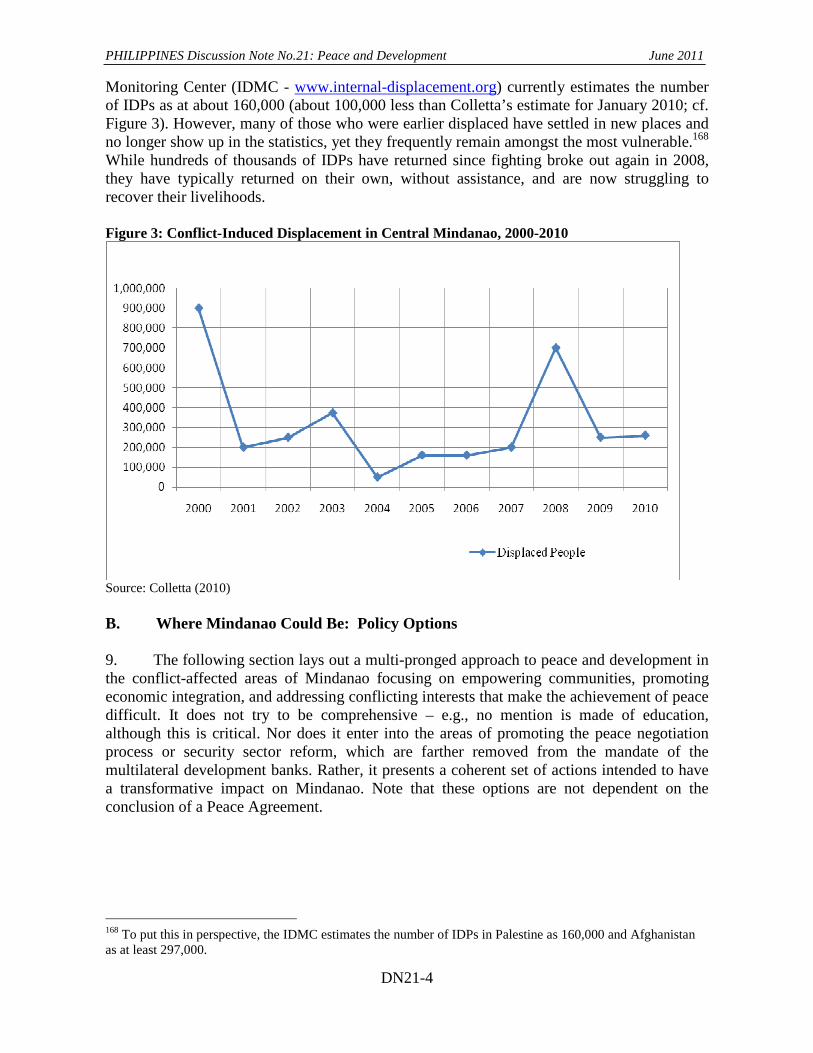

Report No. 55655 - PH Philippines Discussion Notes Challenges and Options for 2010 and Beyond June 2011 Philippines Country Team, World Bank East Asia and Pacific Region The International Finance Corporation East Asia and Pacific Department Document of the World Bank This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

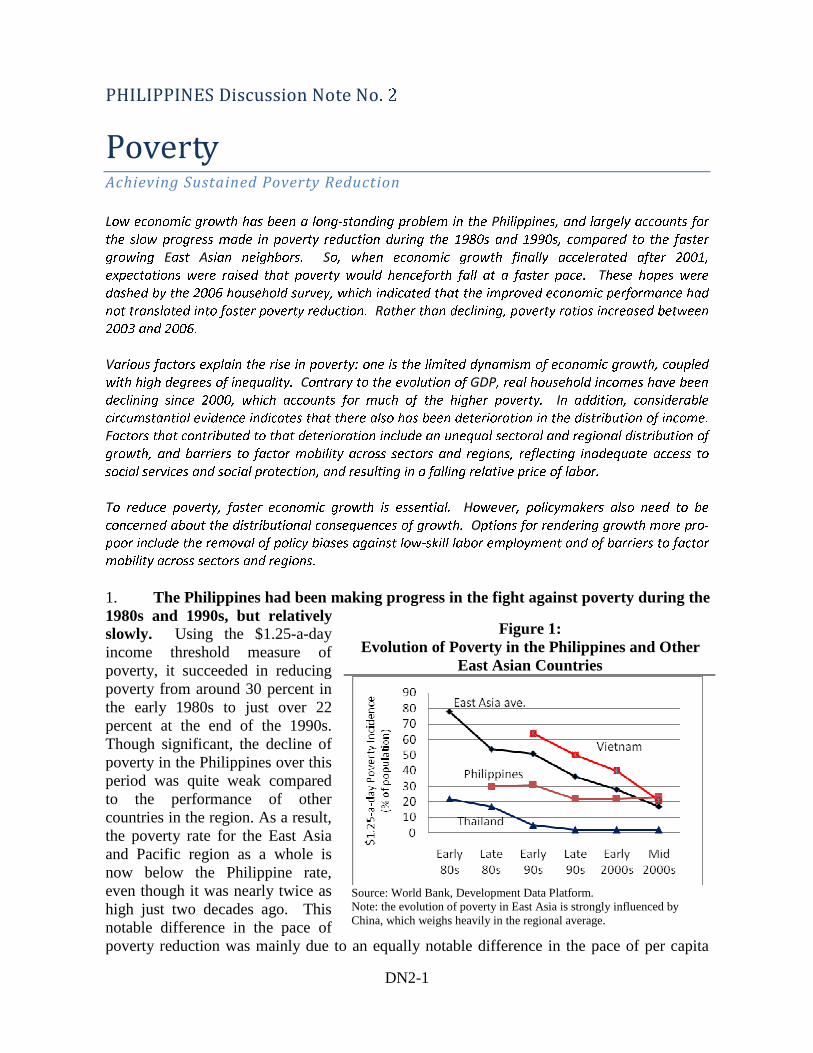

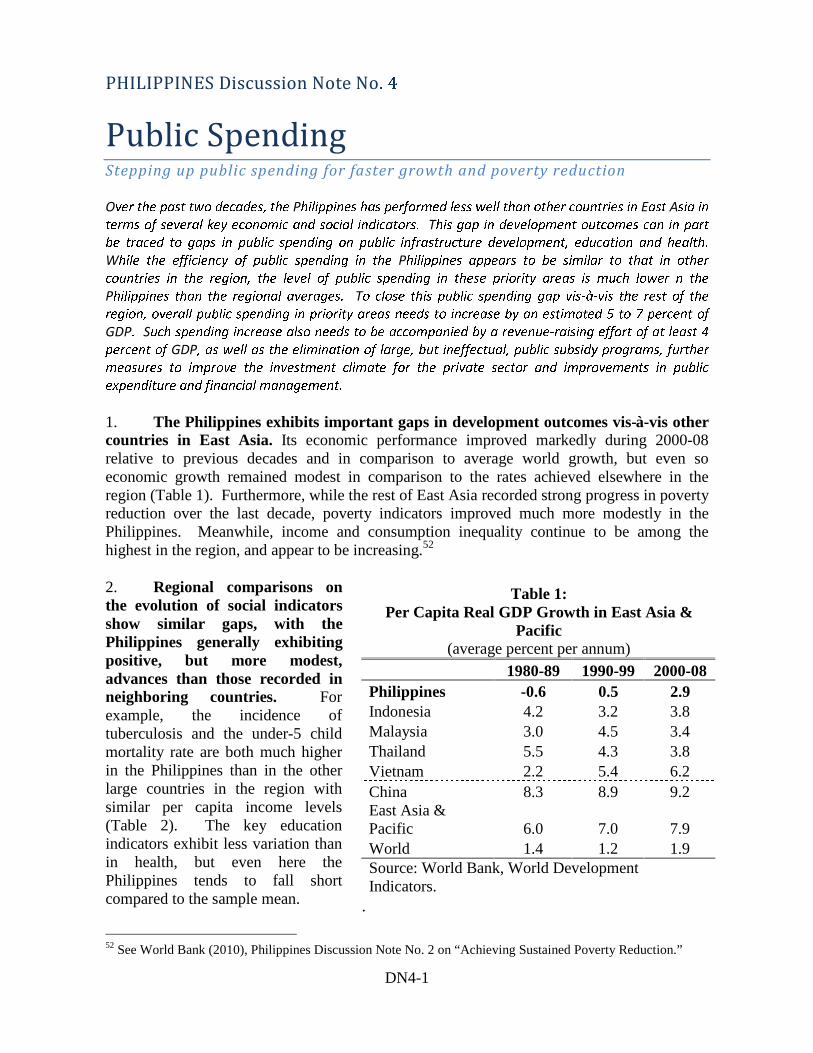

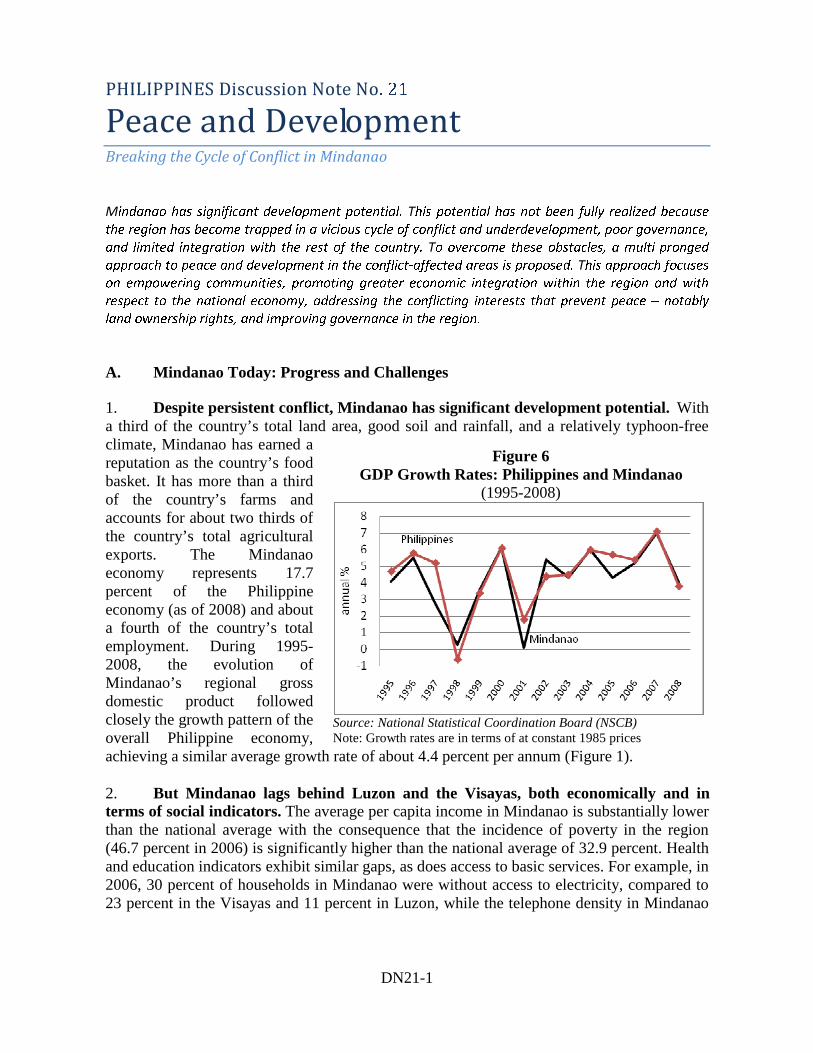

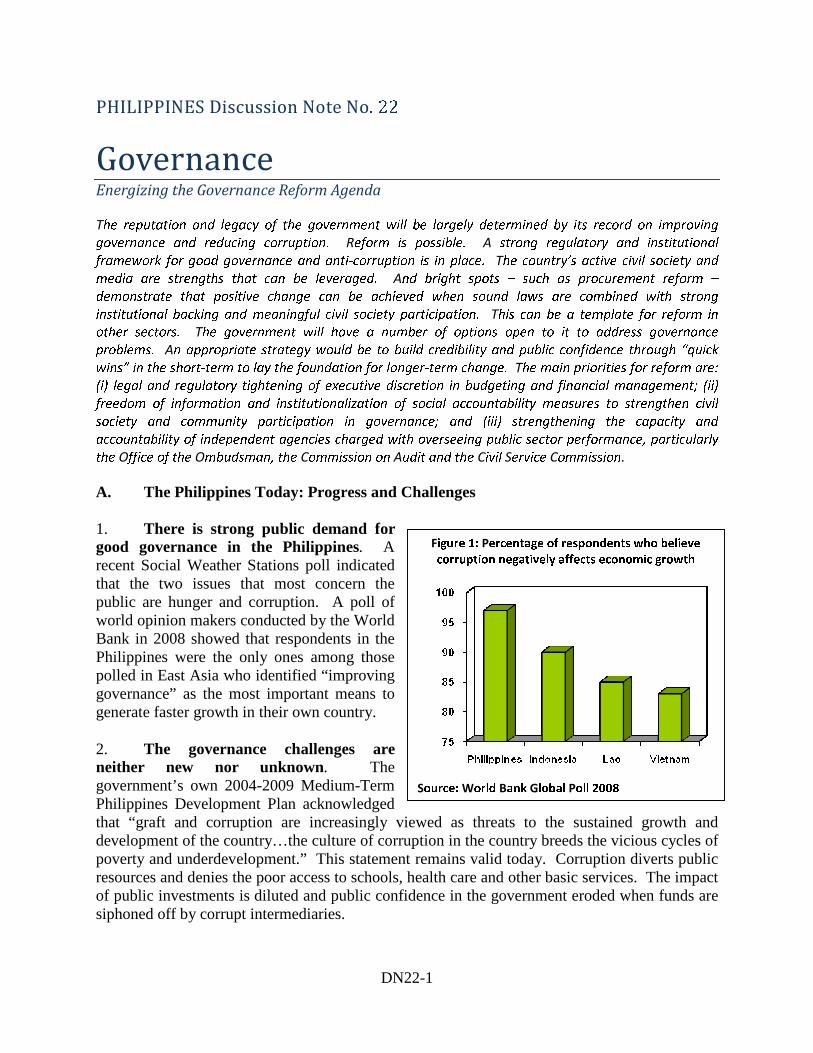

Transcript

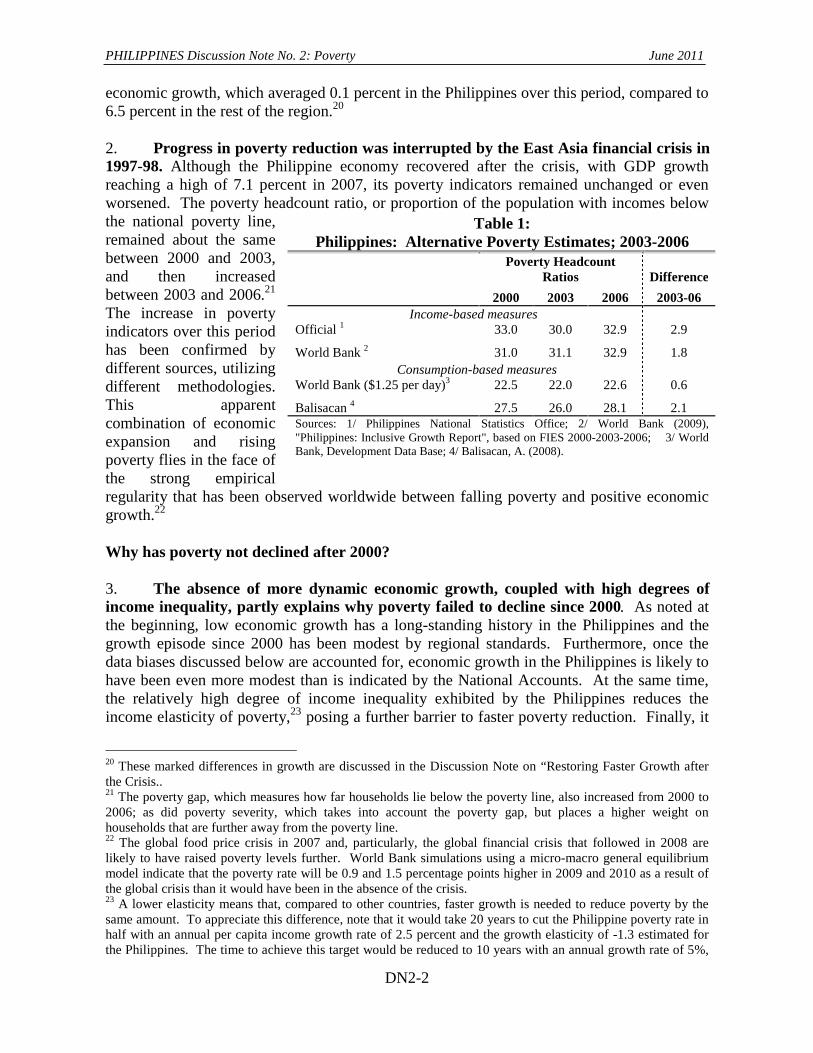

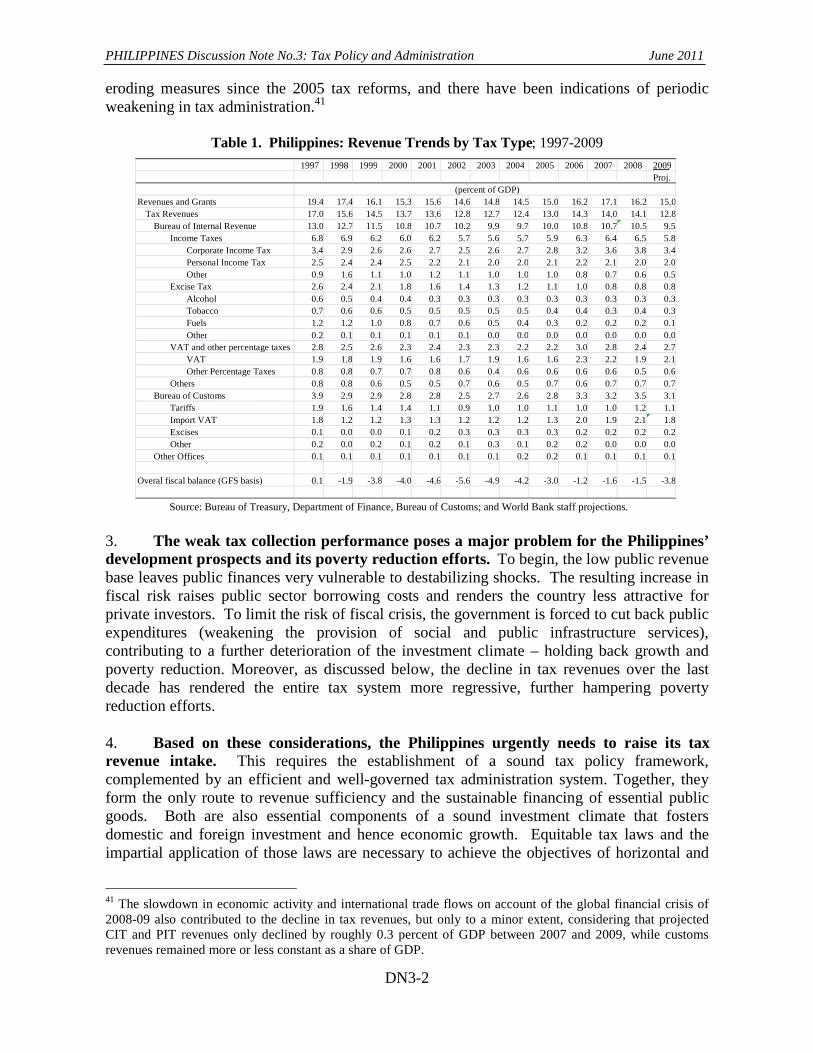

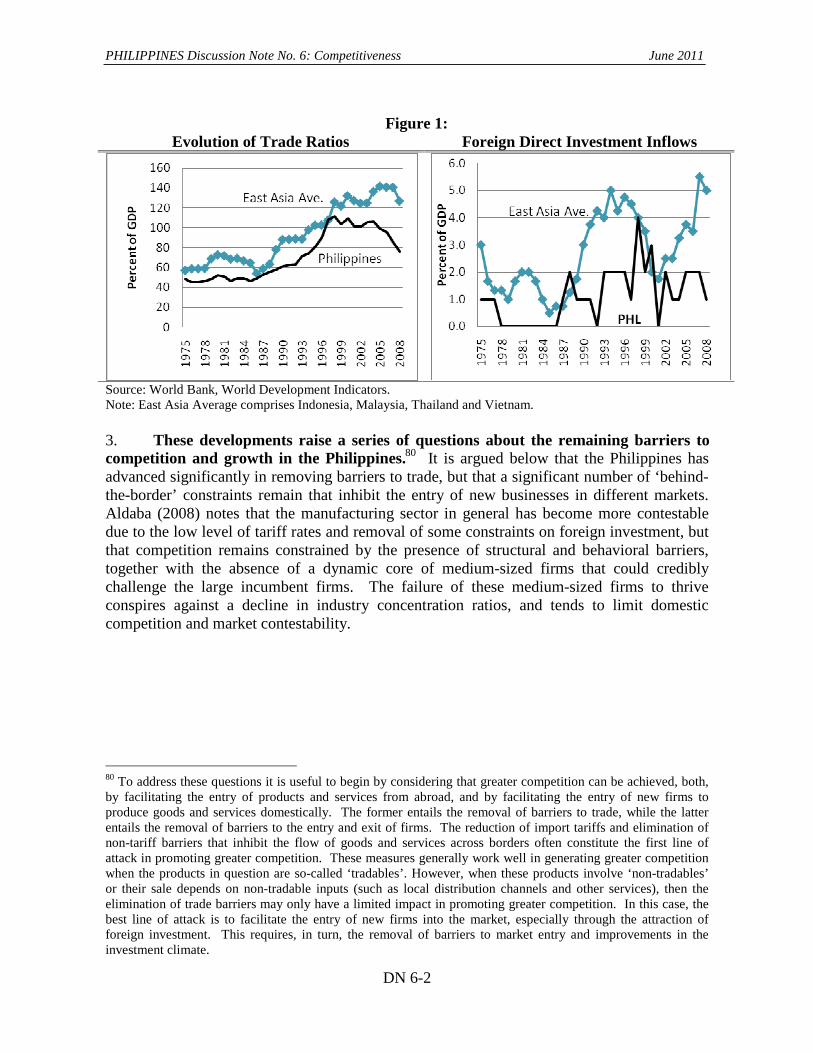

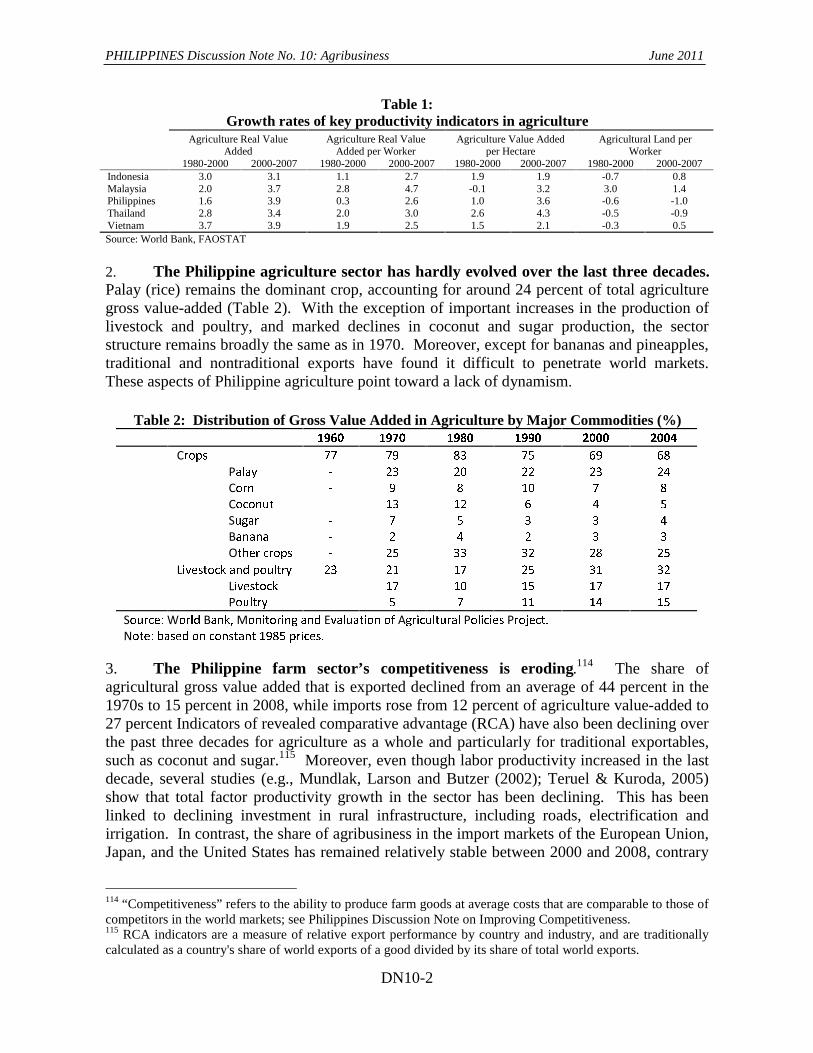

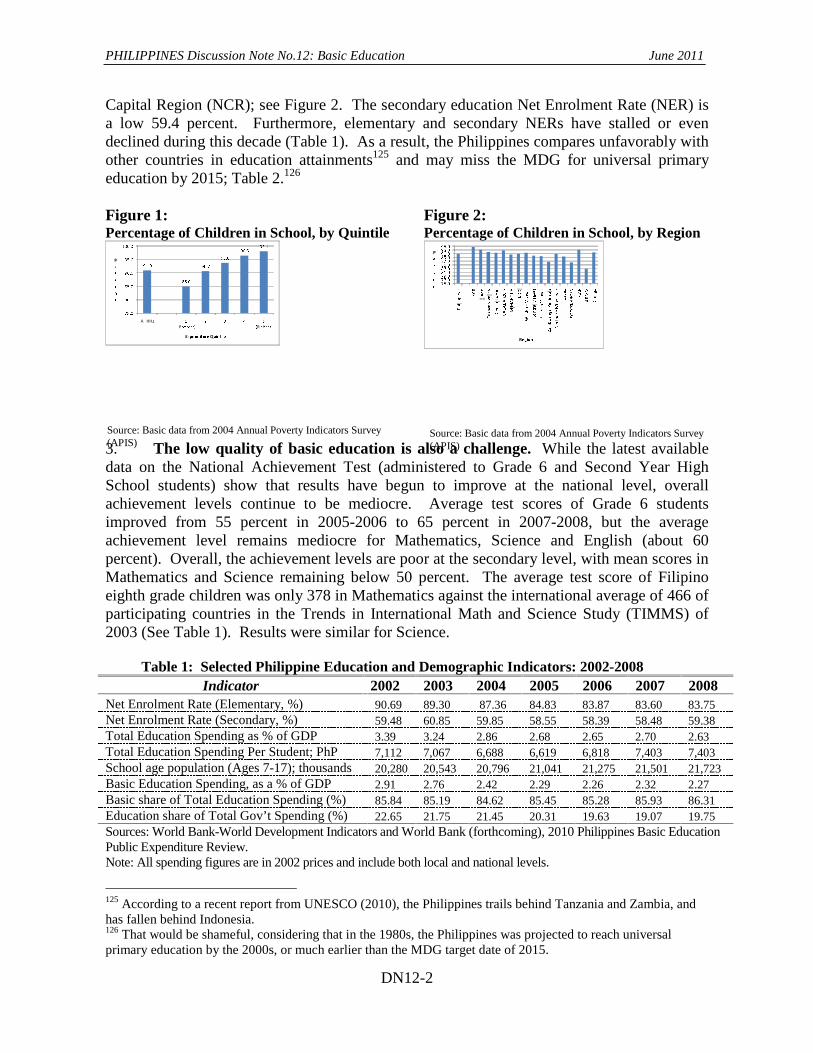

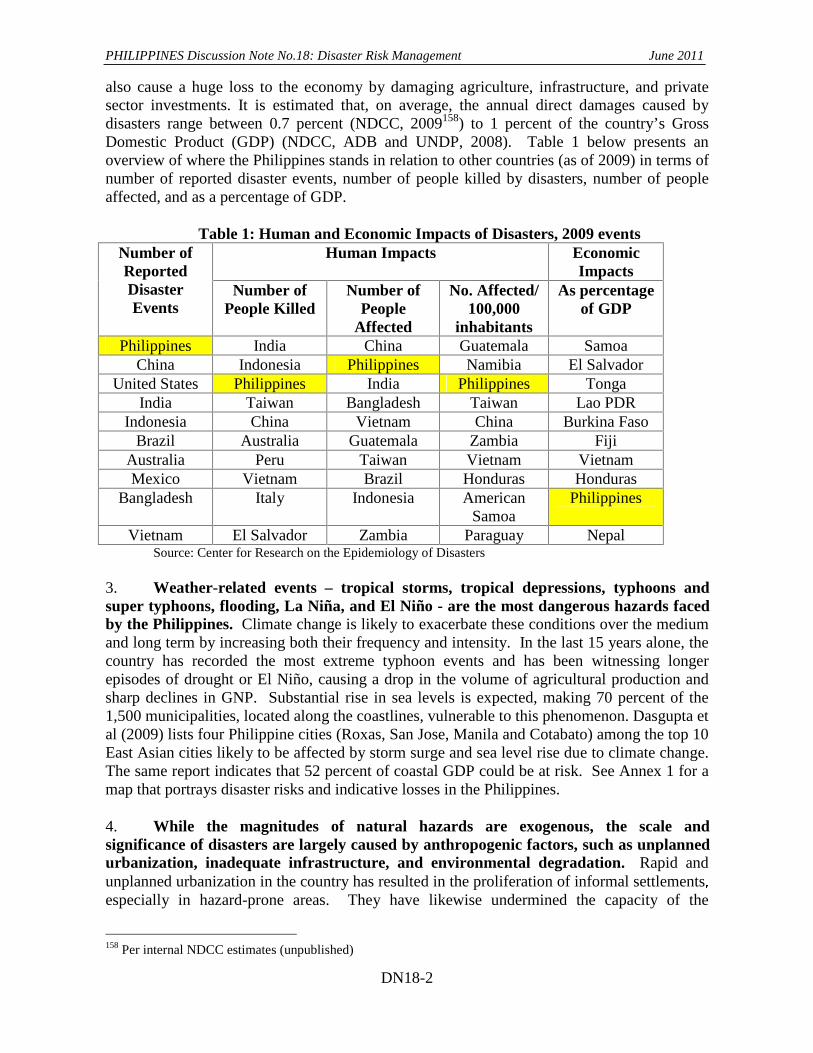

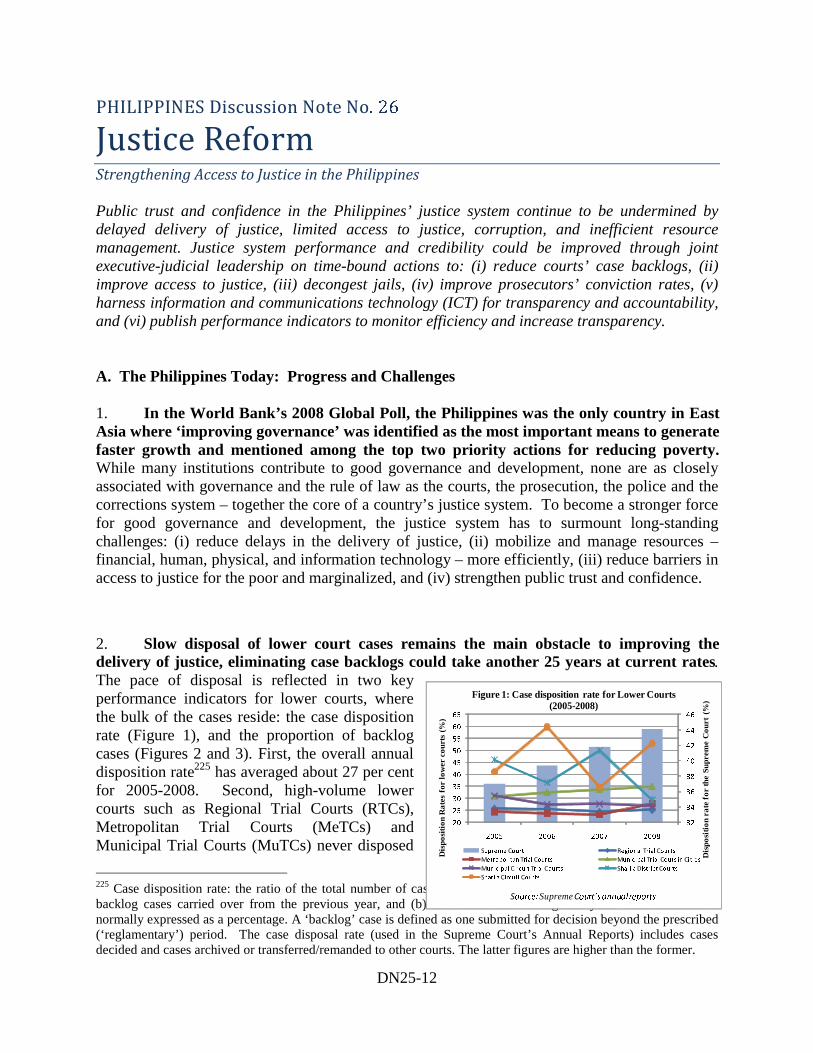

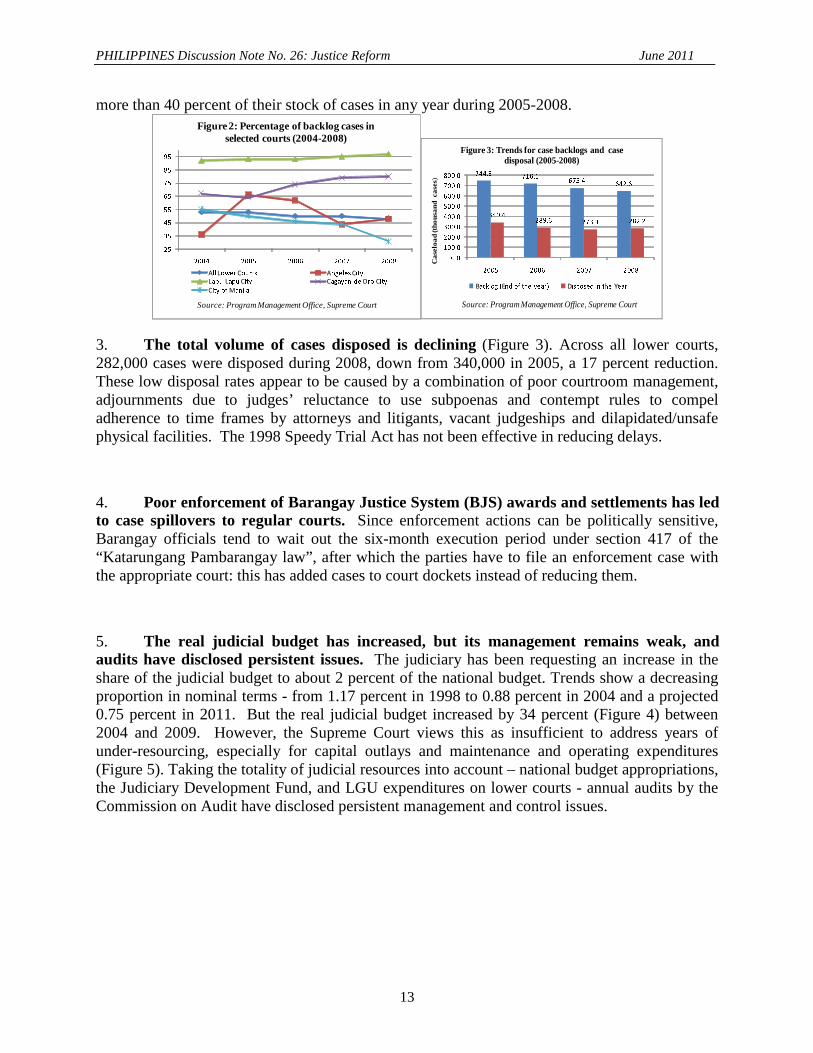

Report No. 55655 - PH

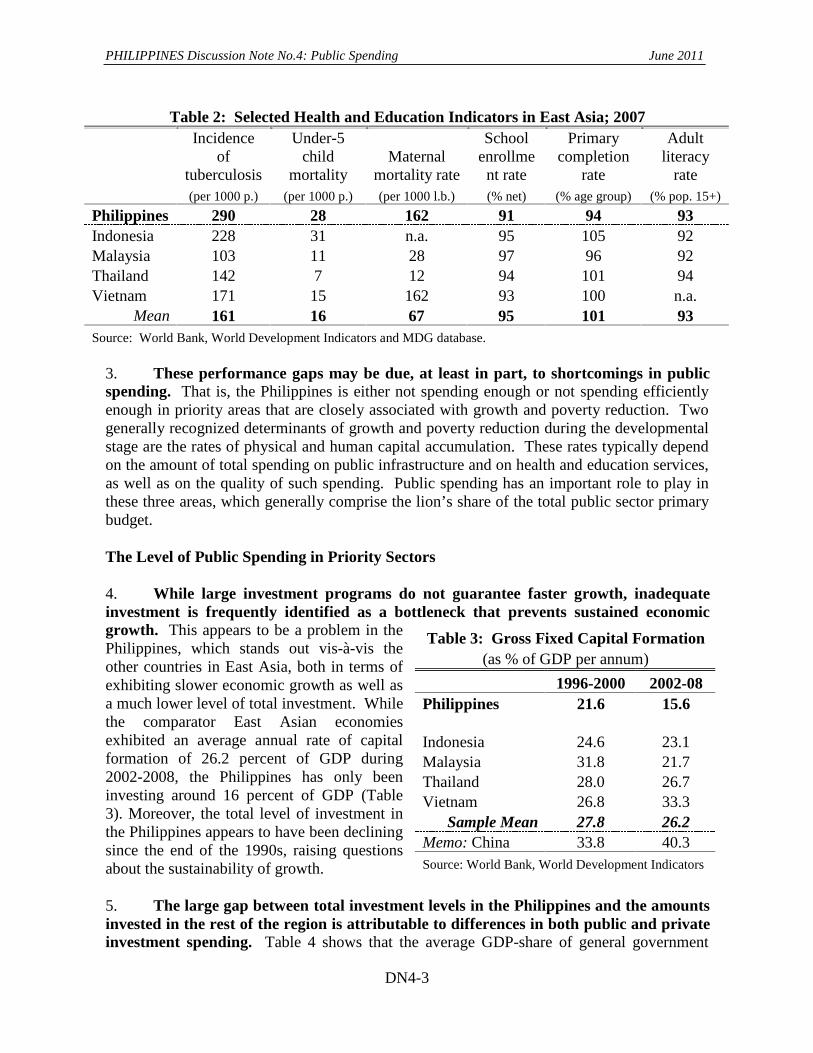

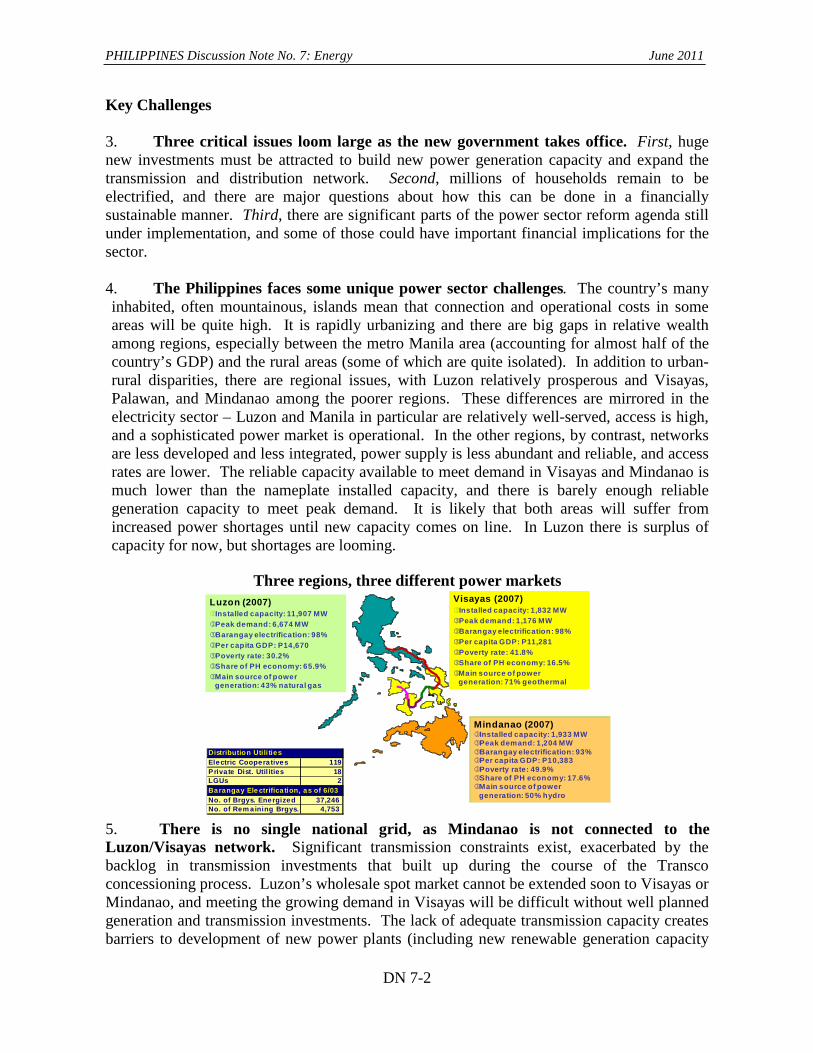

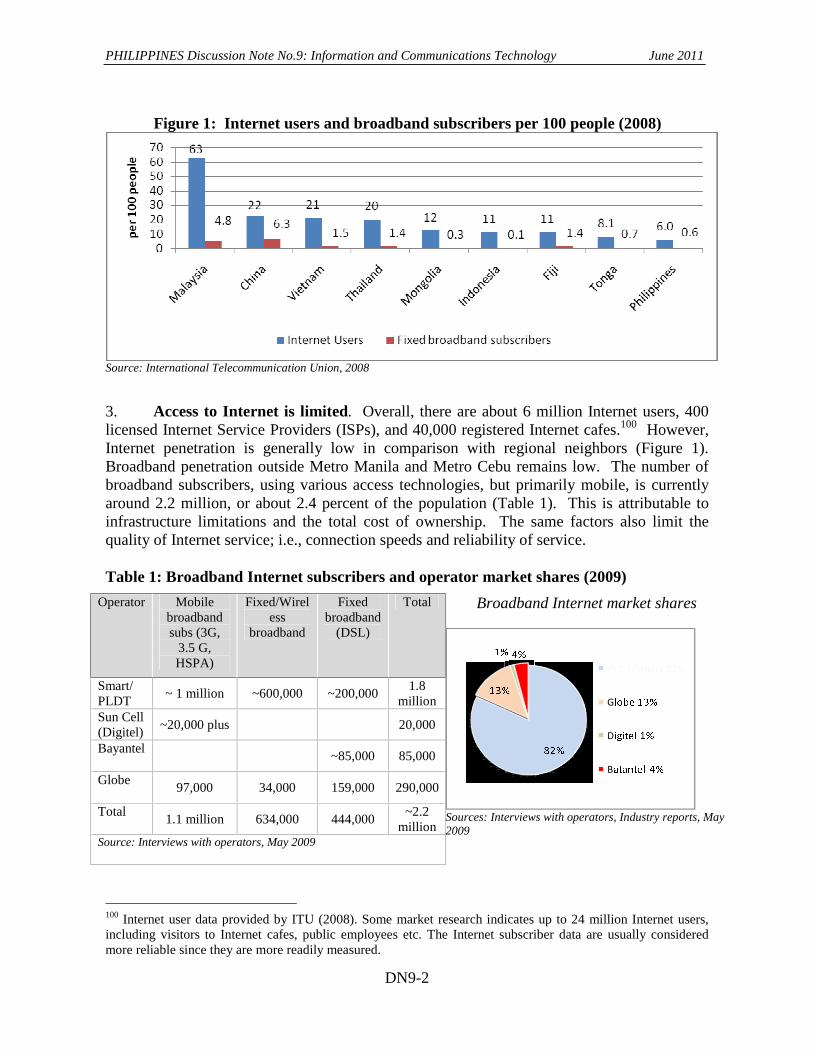

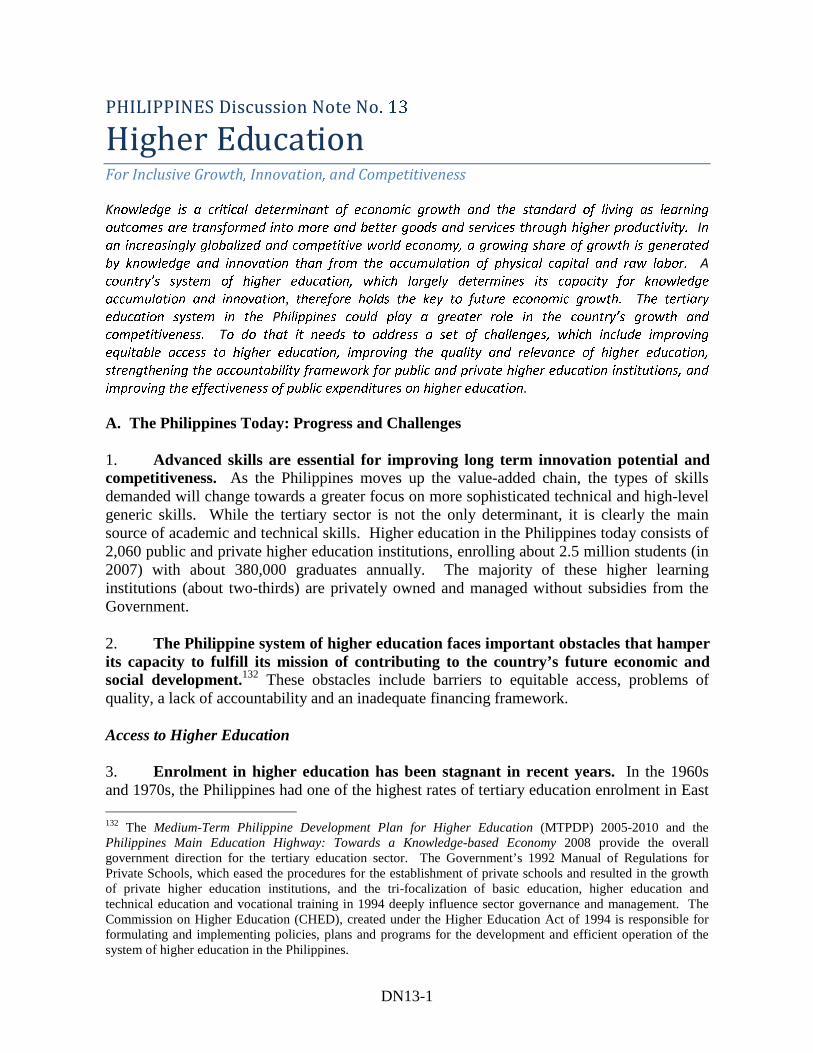

Philippines Discussion Notes Challenges and Options for 2010 and Beyond

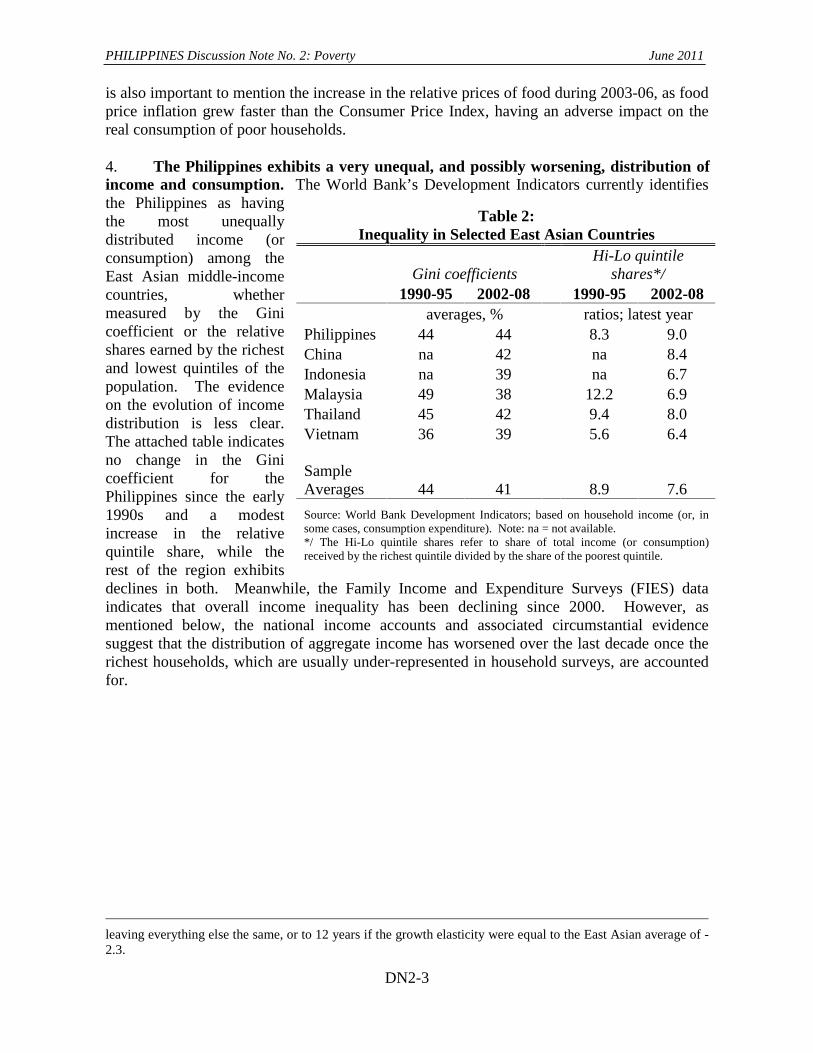

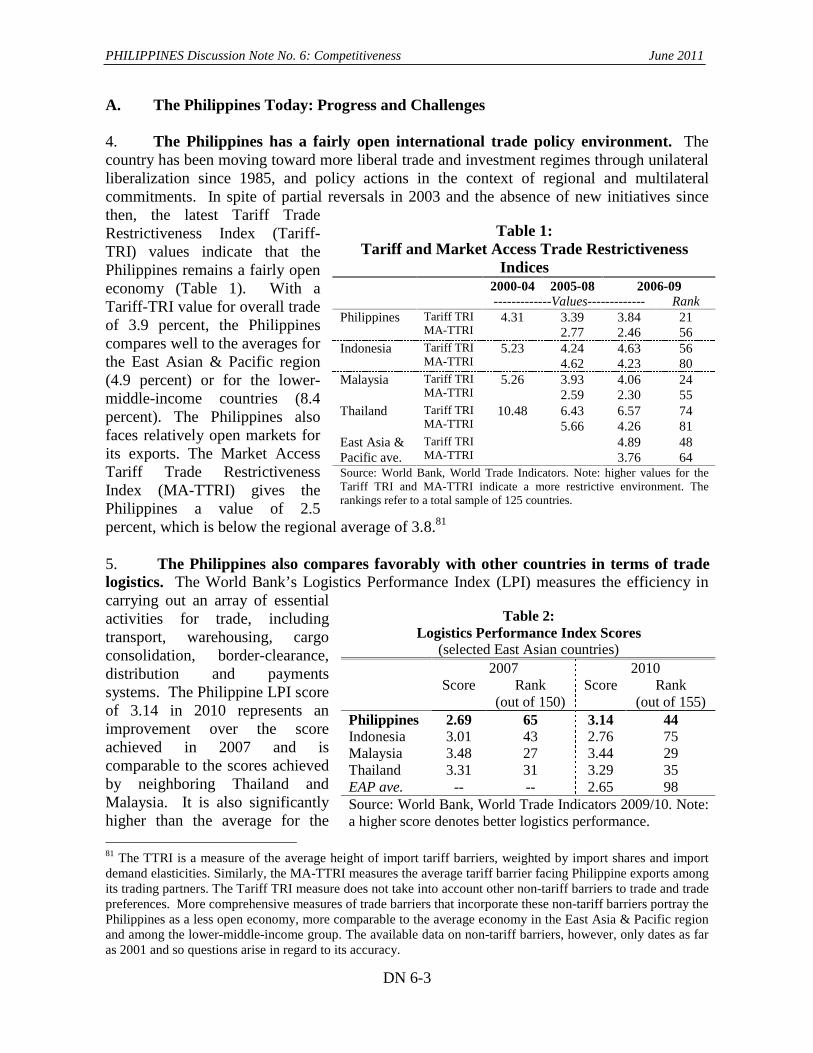

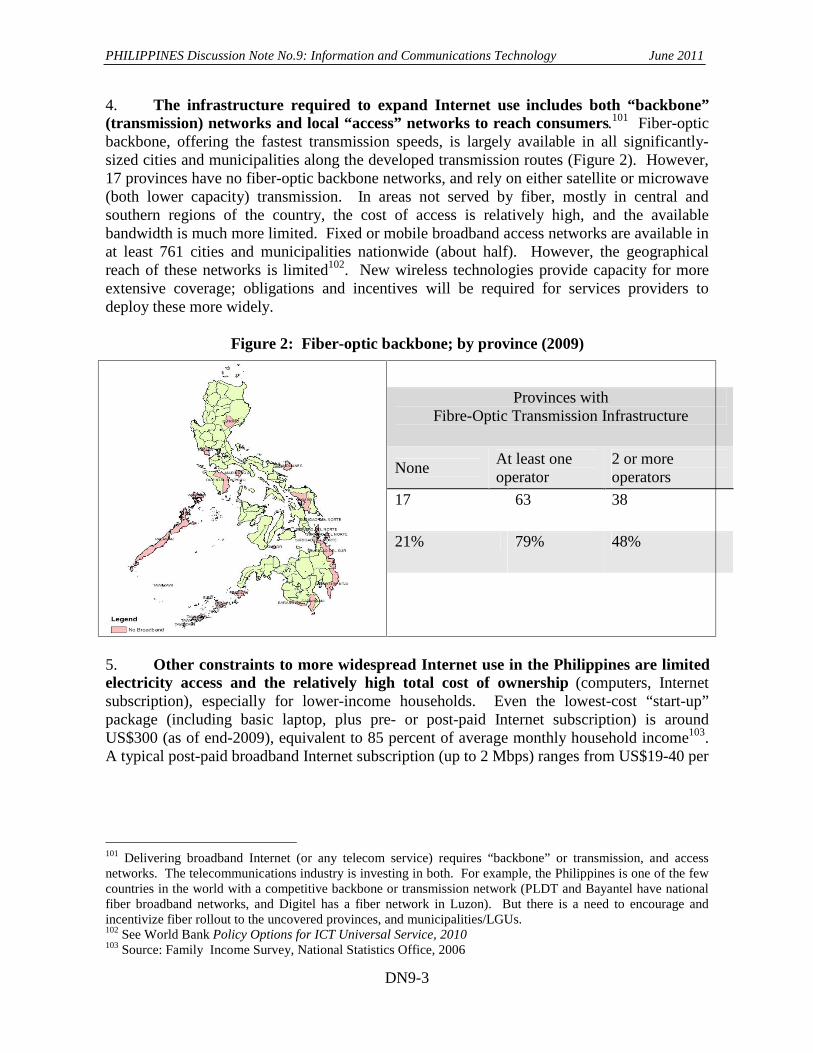

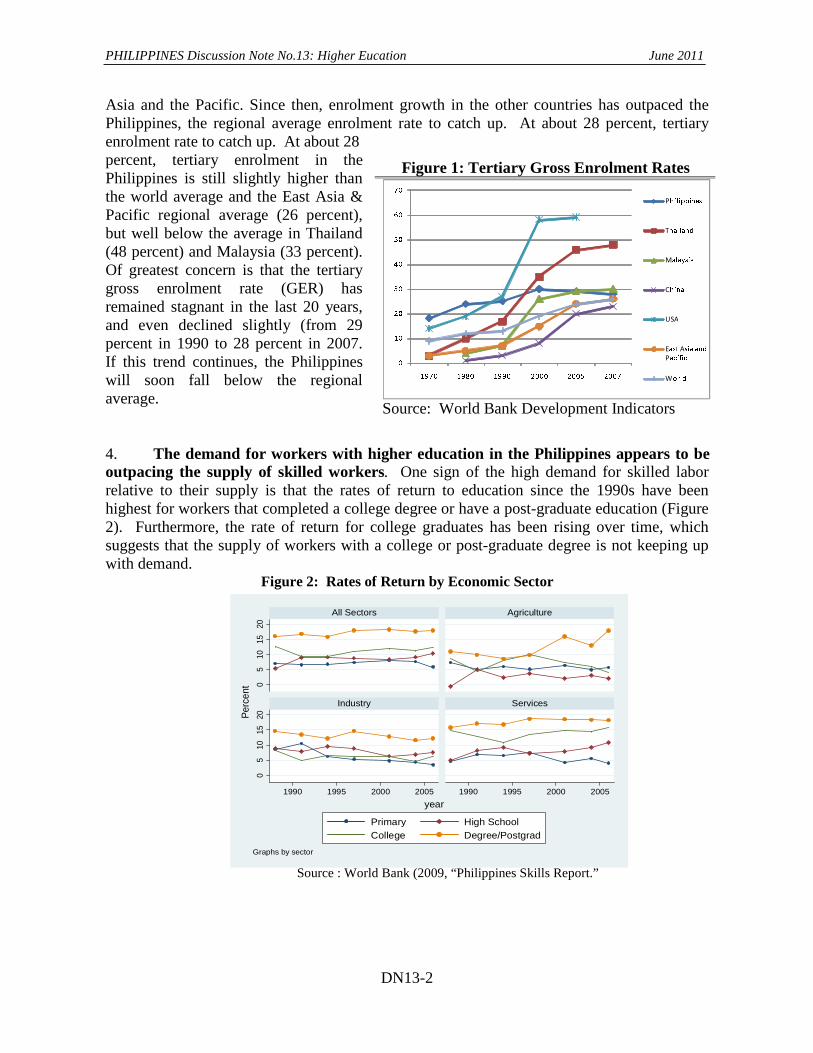

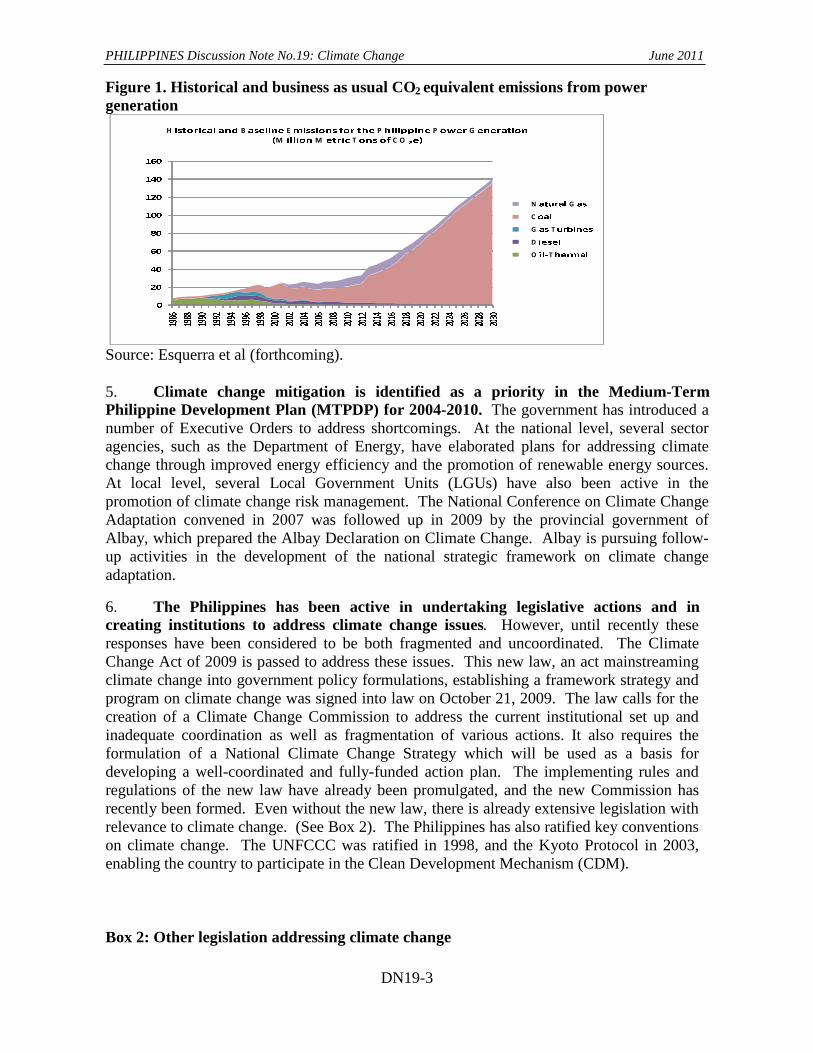

June 2011

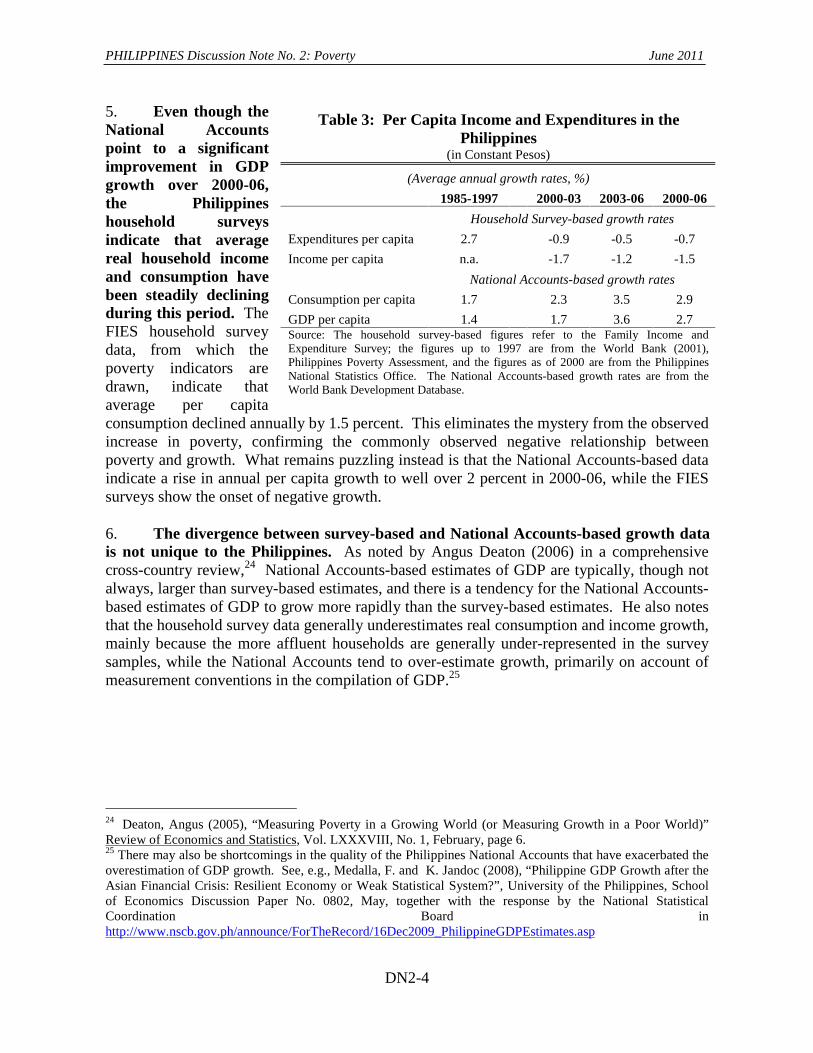

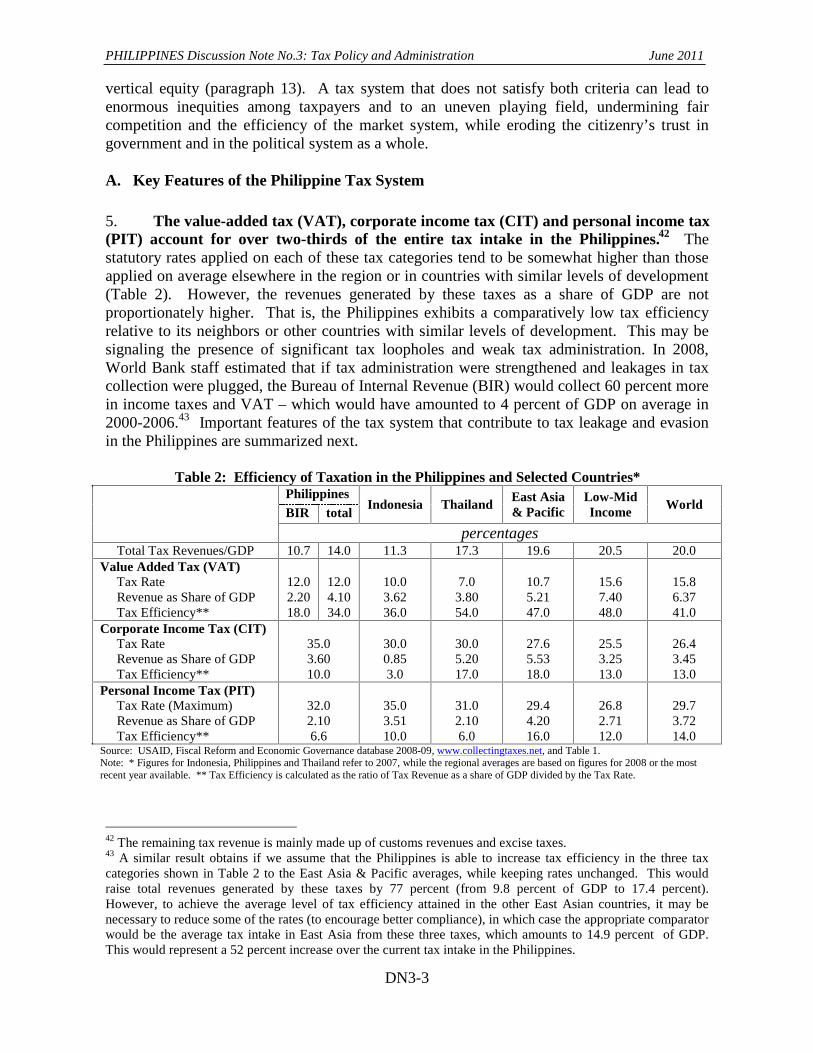

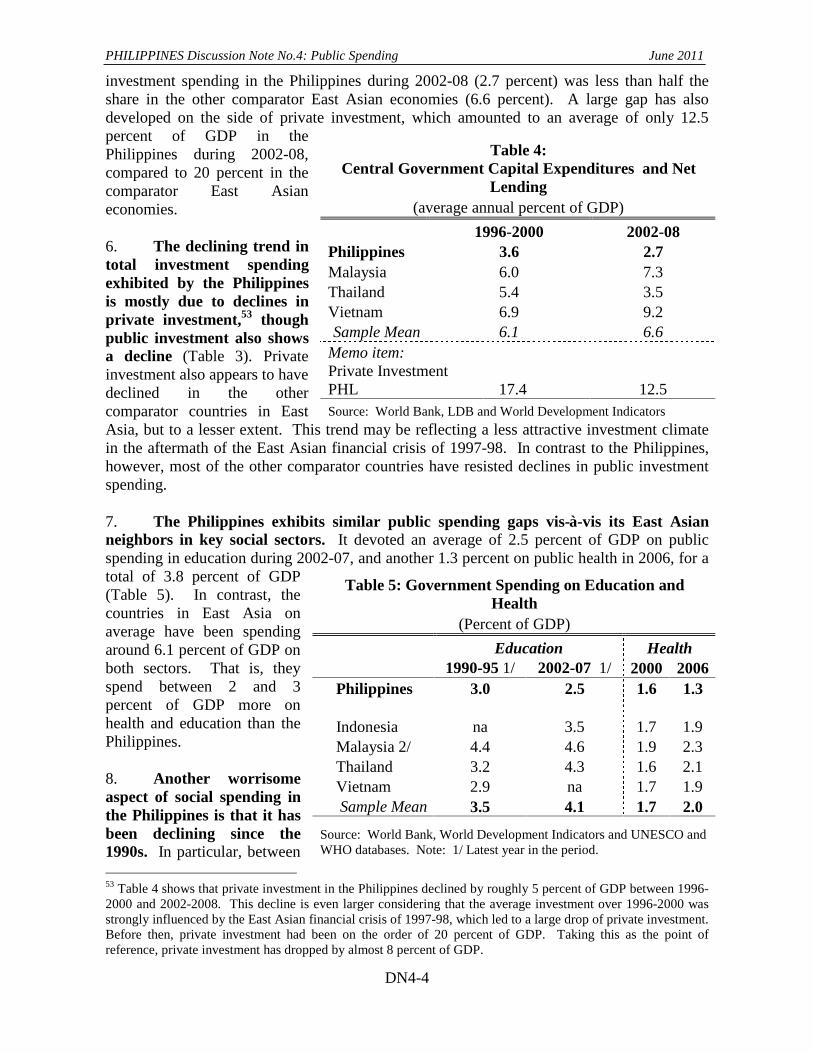

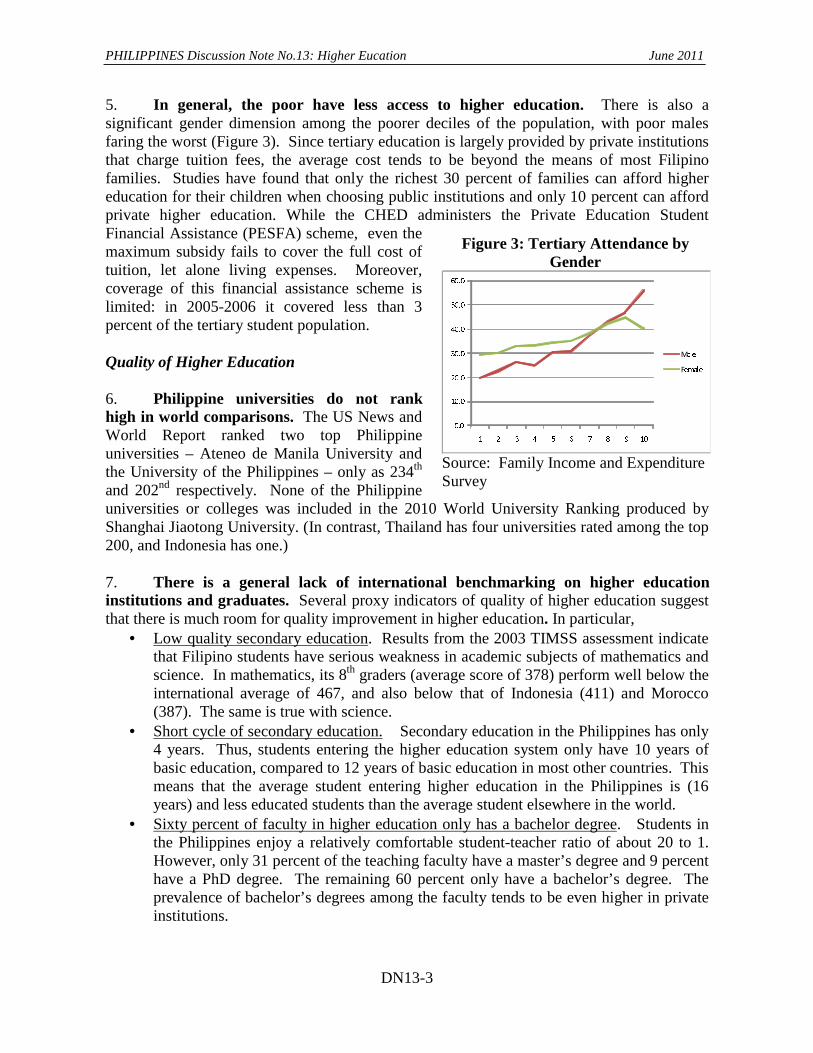

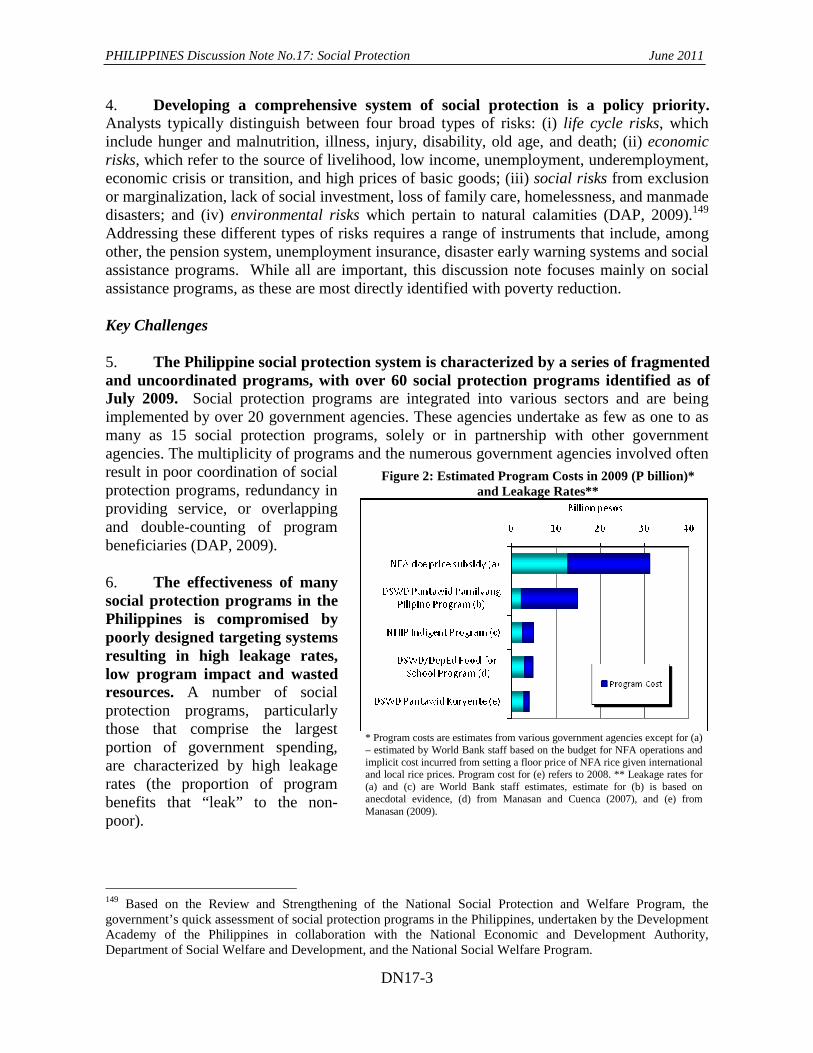

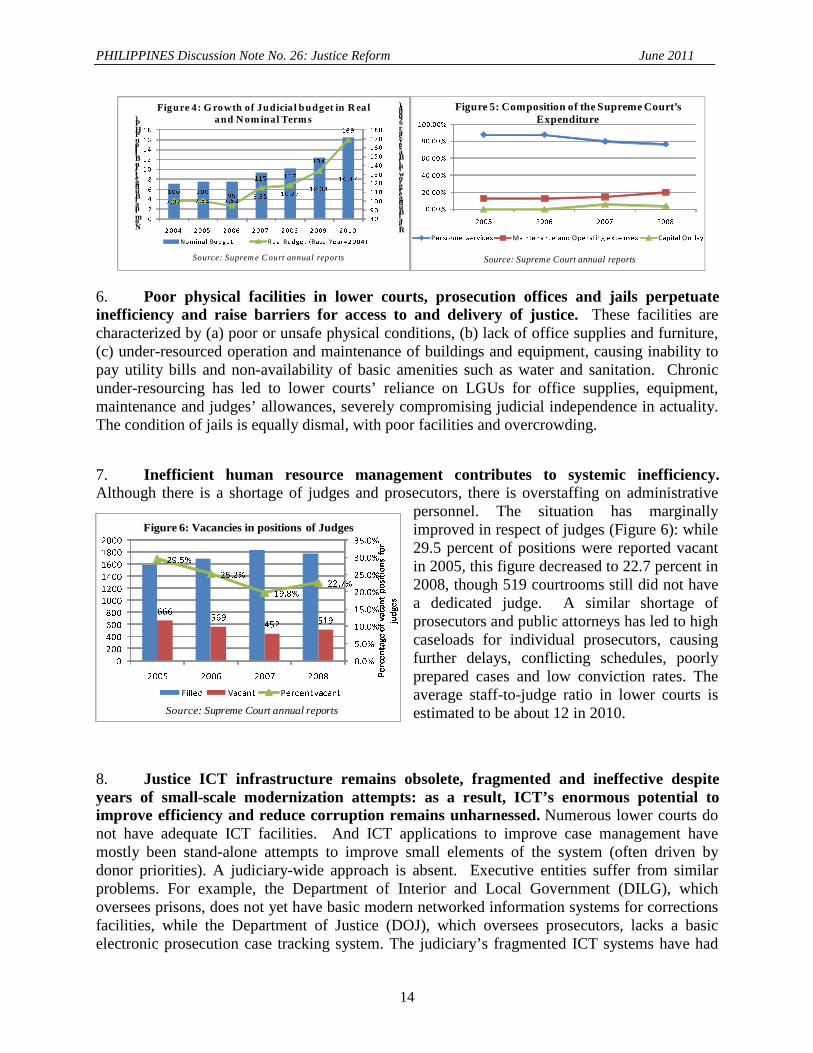

Philippines Country Team, World Bank East Asia and Pacific Region The International Finance Corporation East Asia and Pacific Department

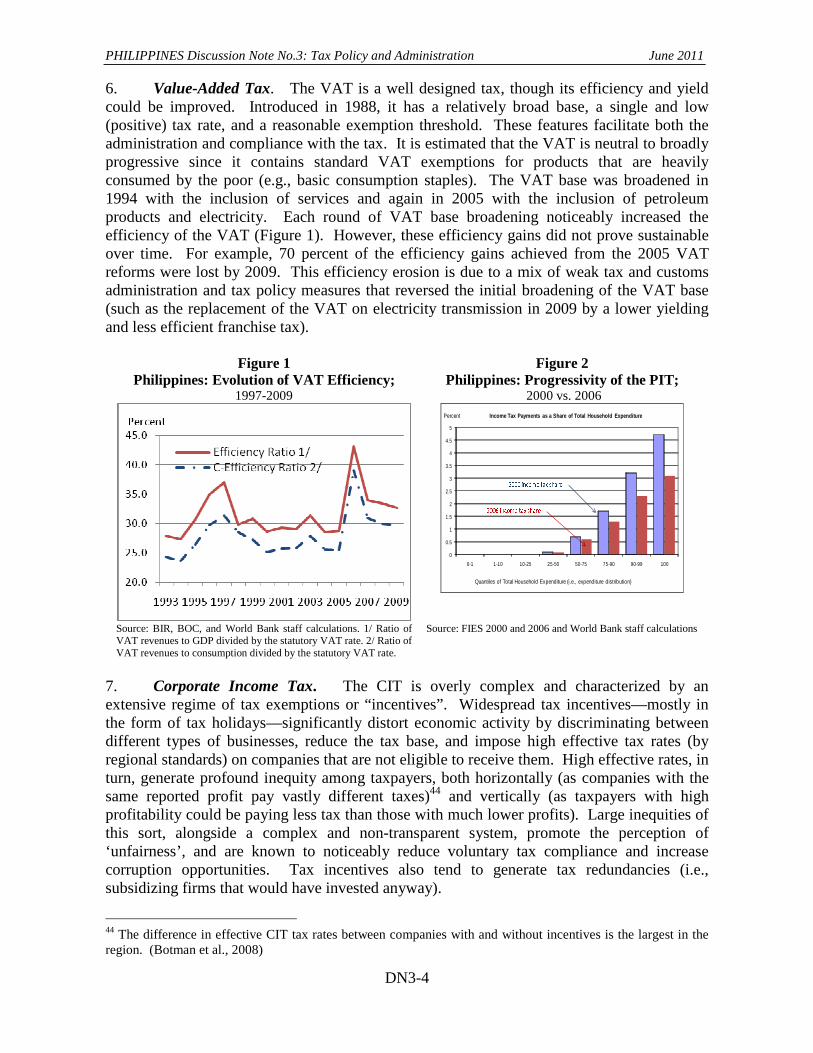

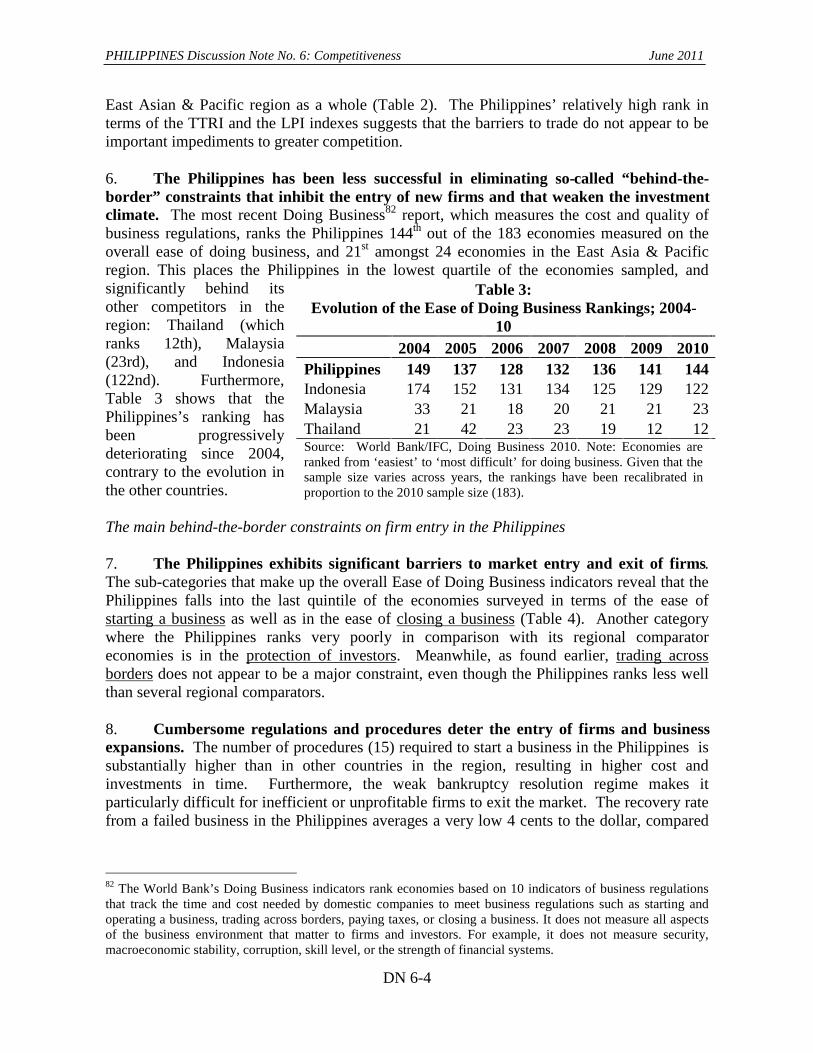

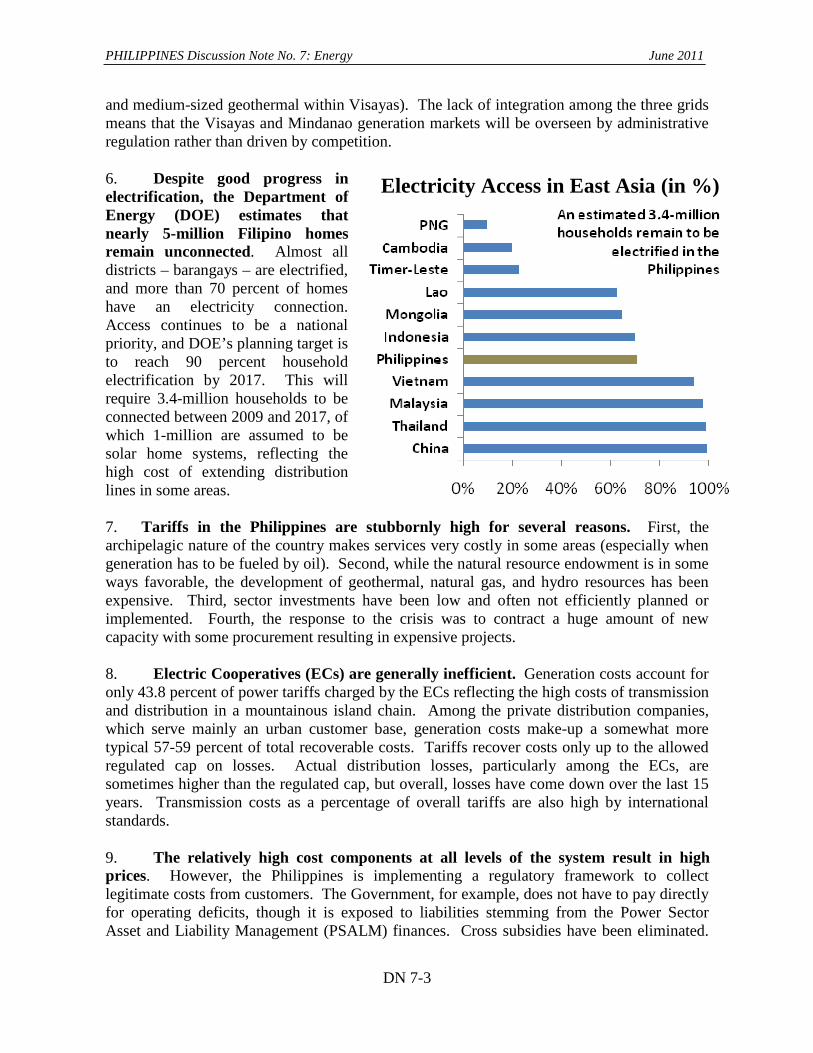

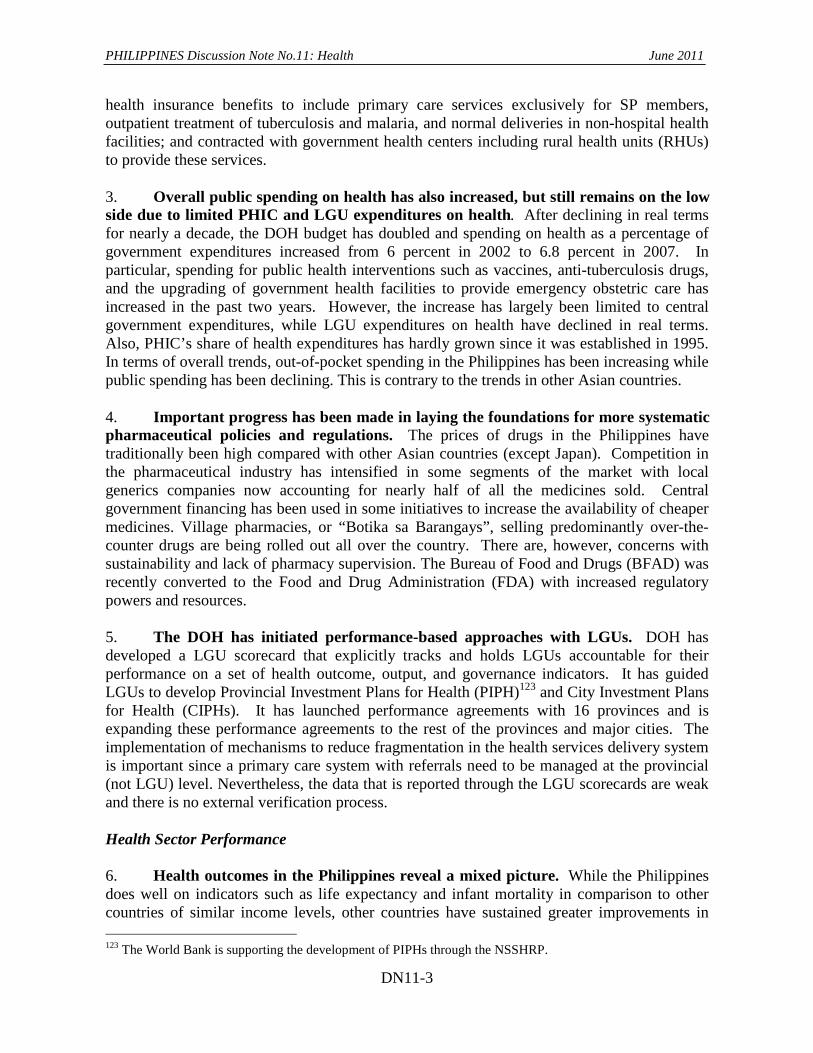

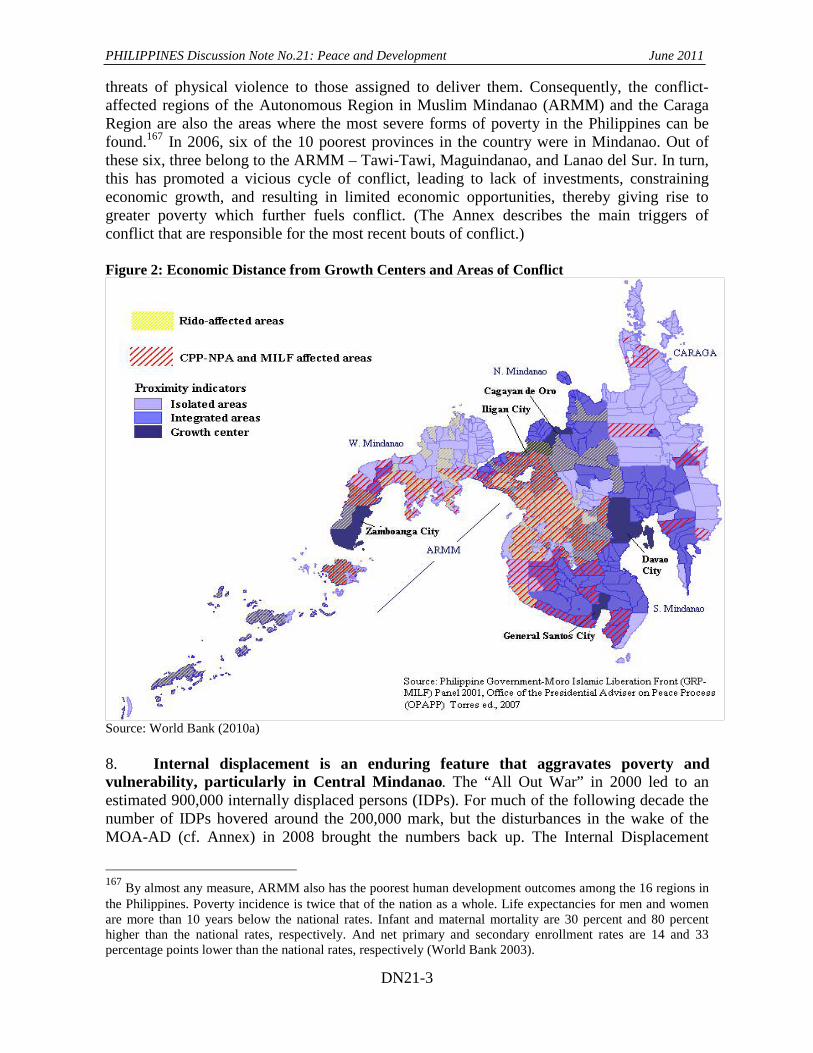

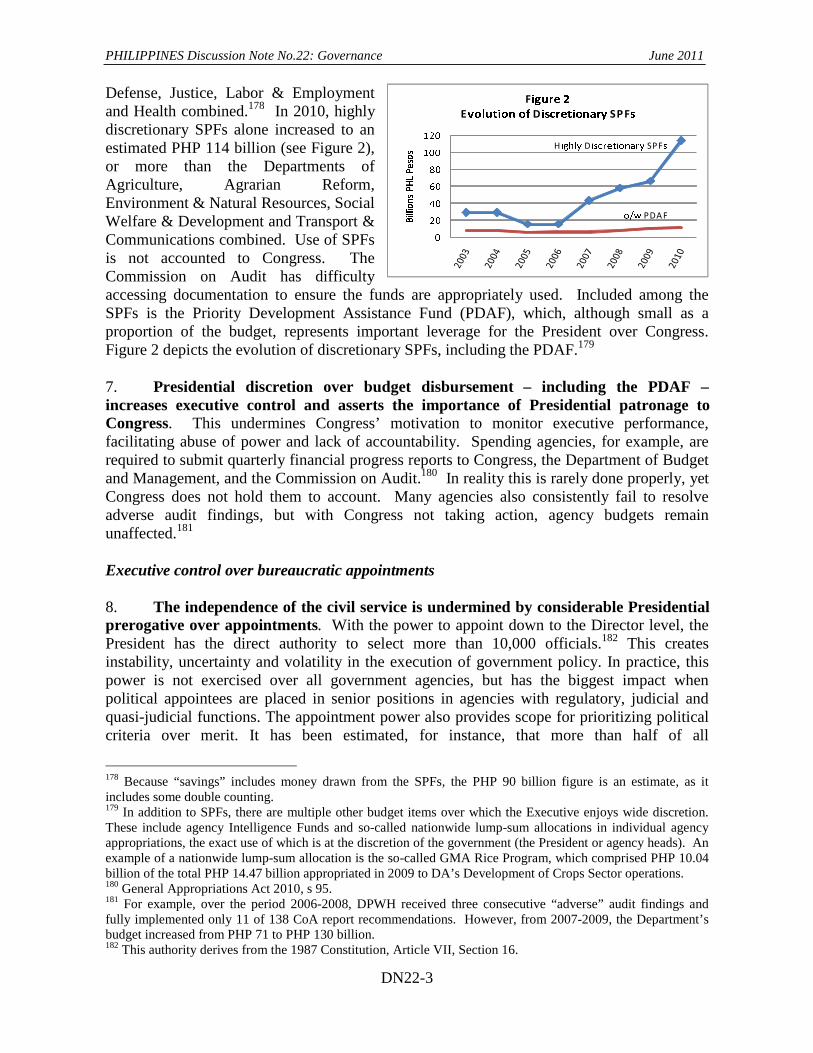

Document of the World Bank This document has a restricted distribution and may be used by recipients only in the performance of their official duties.

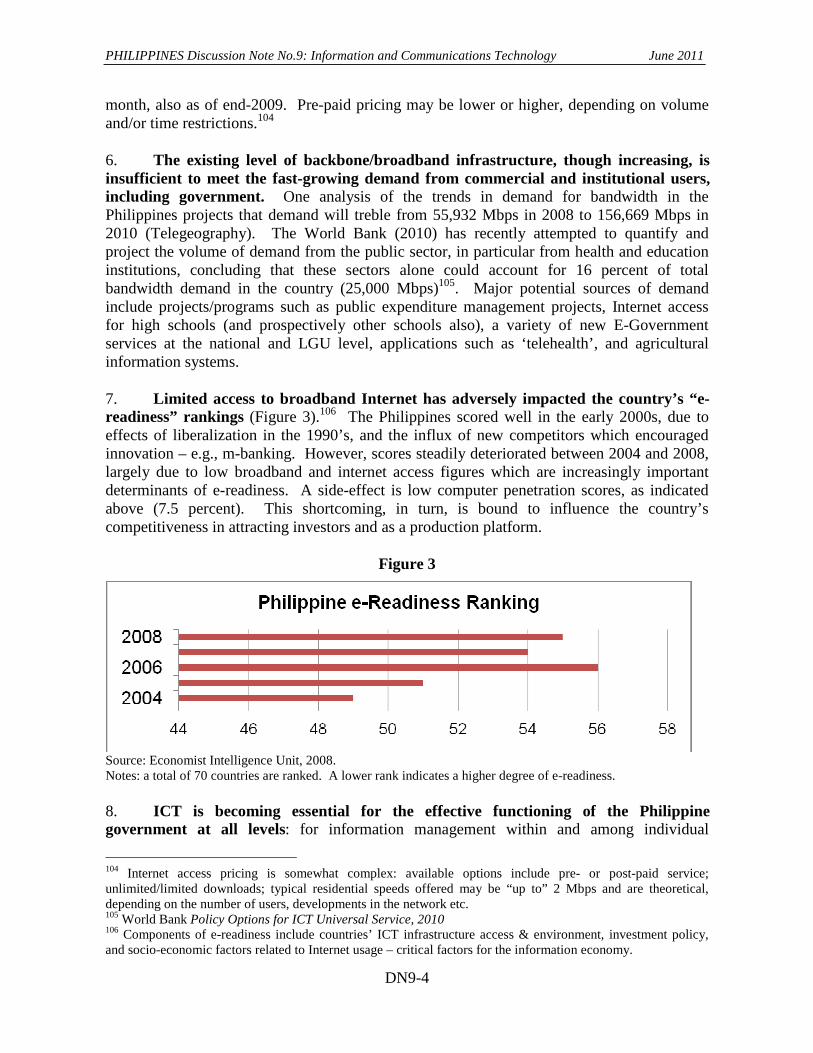

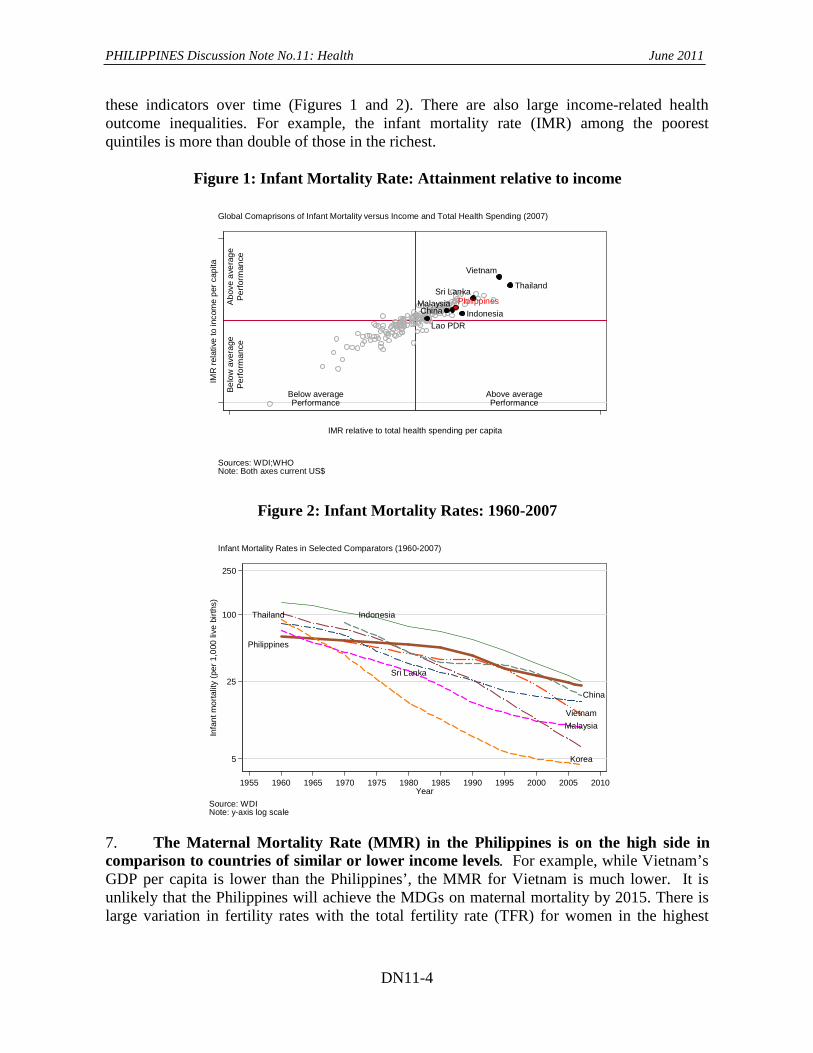

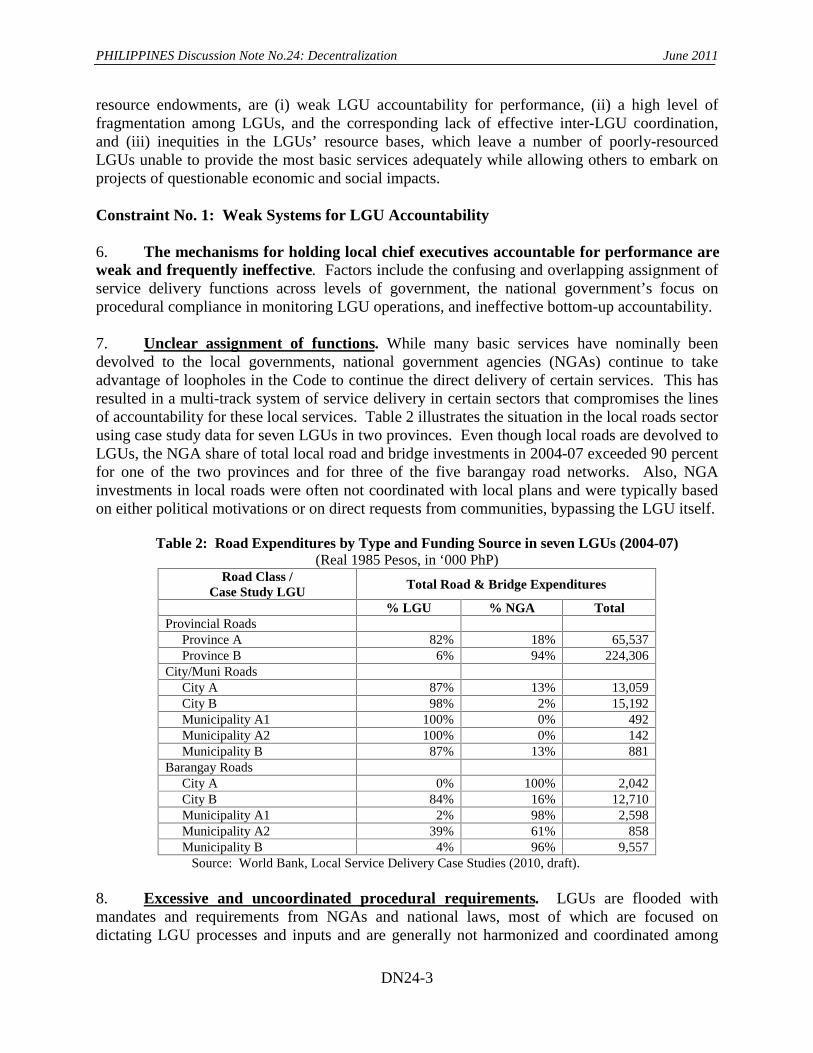

World Bank IFC Vice President James W. Adams Rashad-R. Kaldany

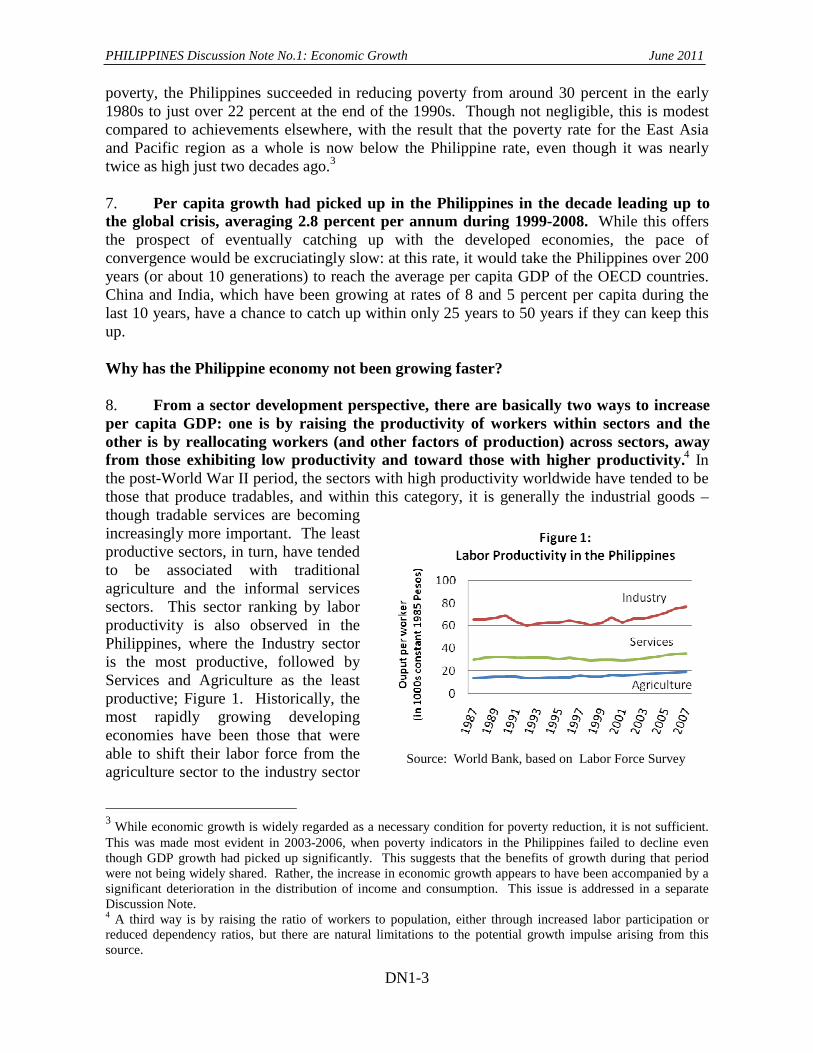

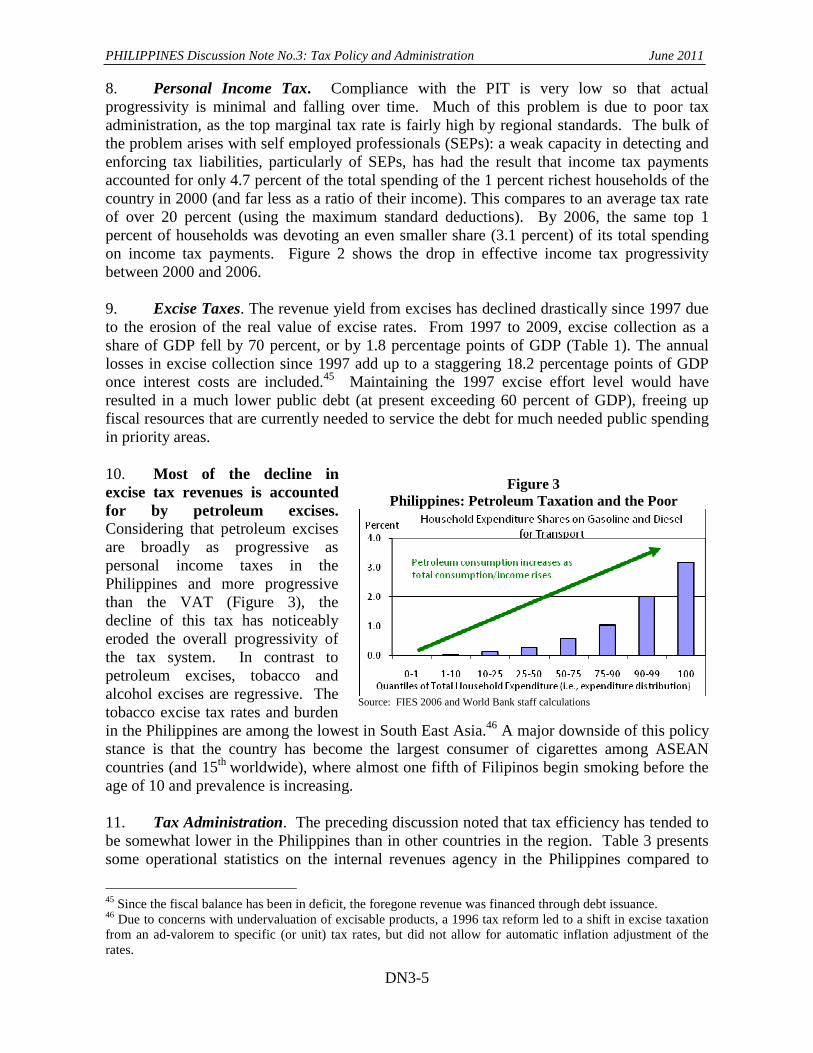

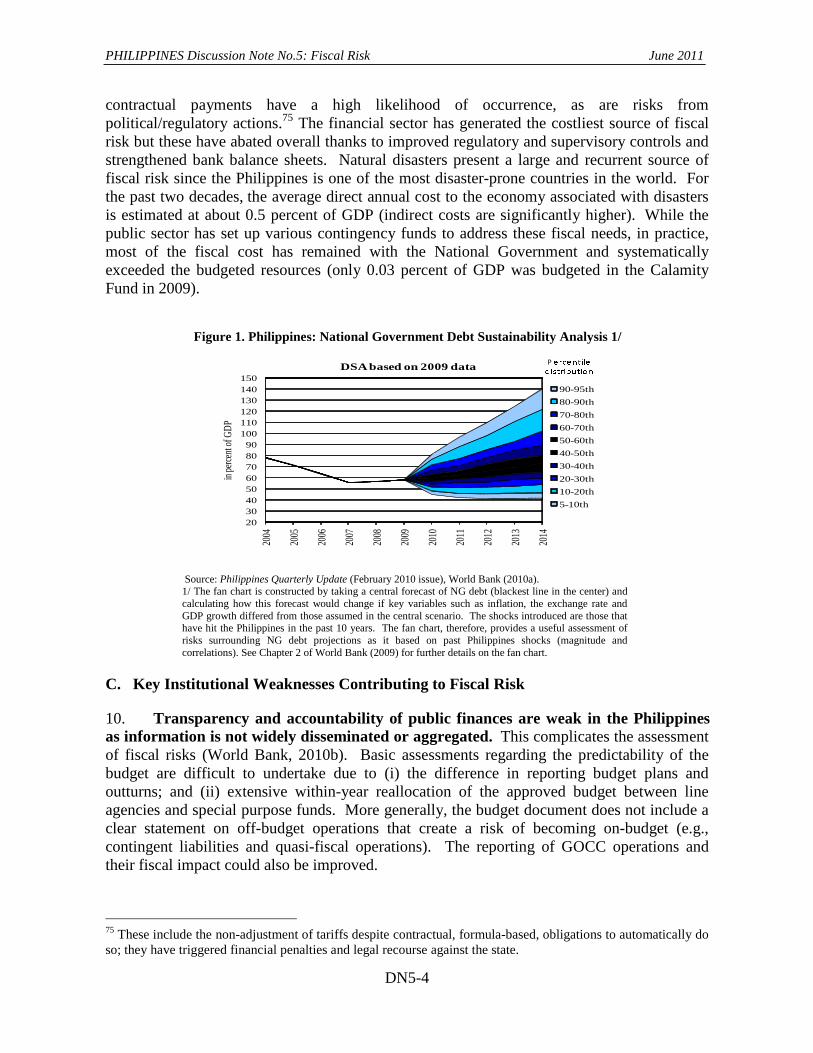

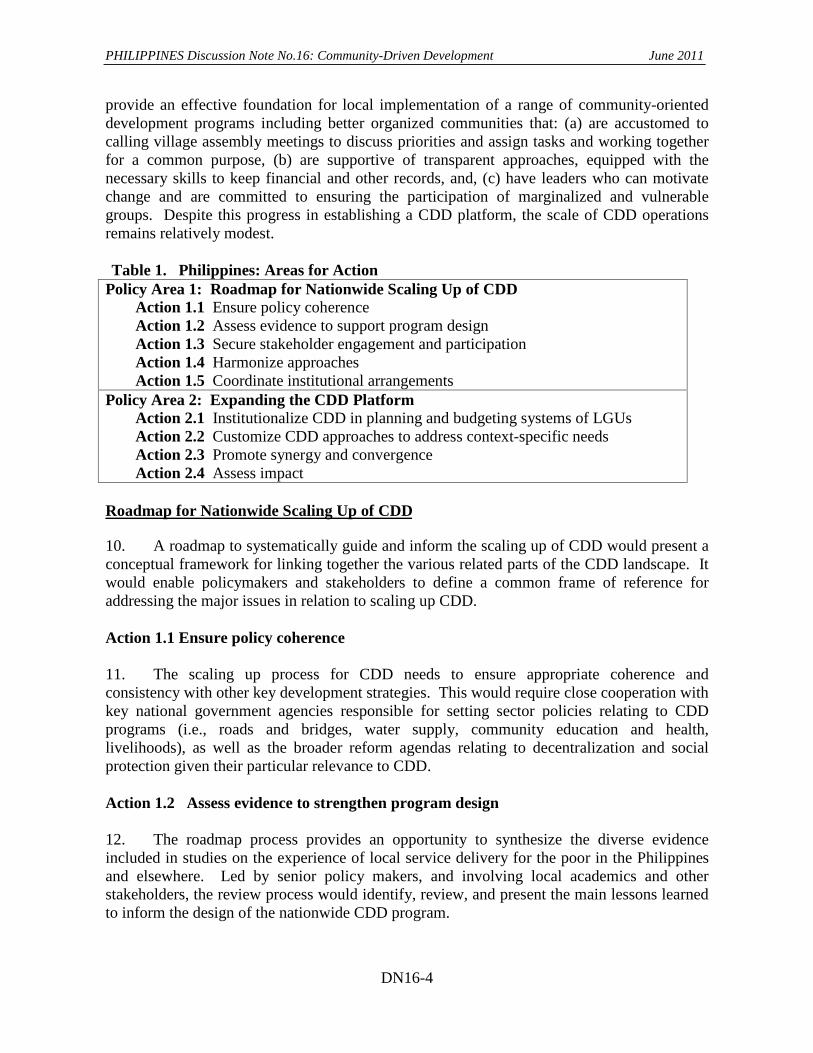

Karin Finkelston Country Director/ Resident Representative

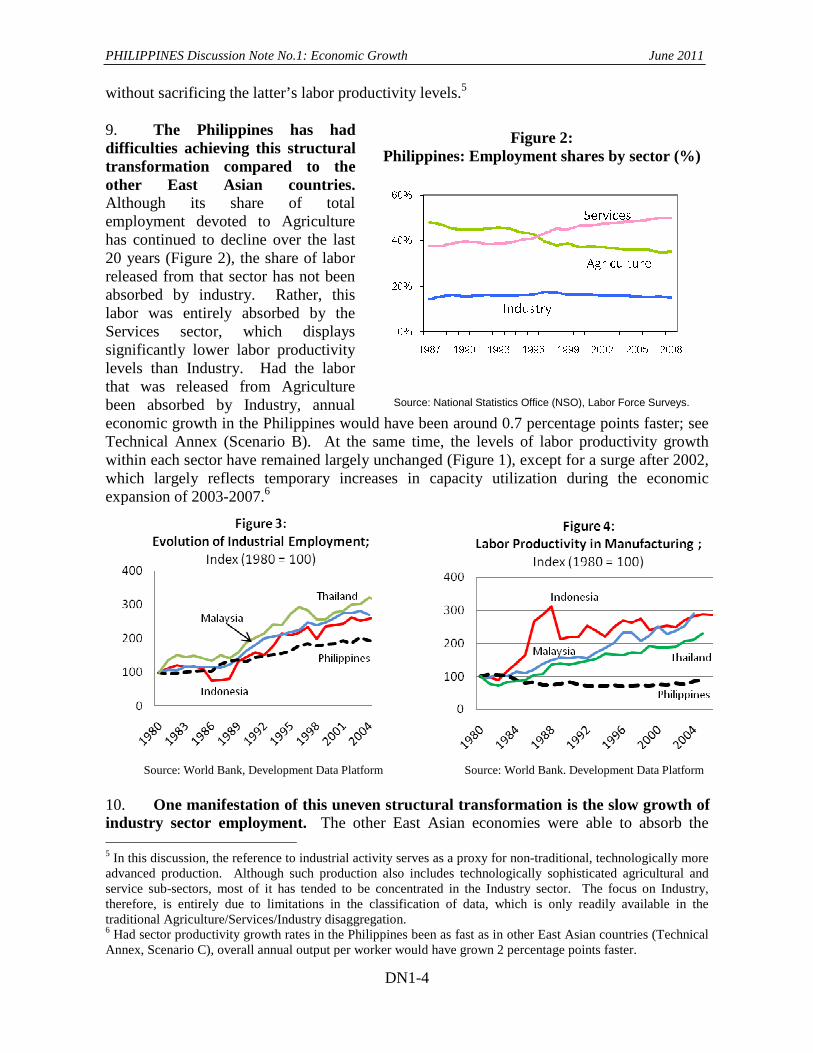

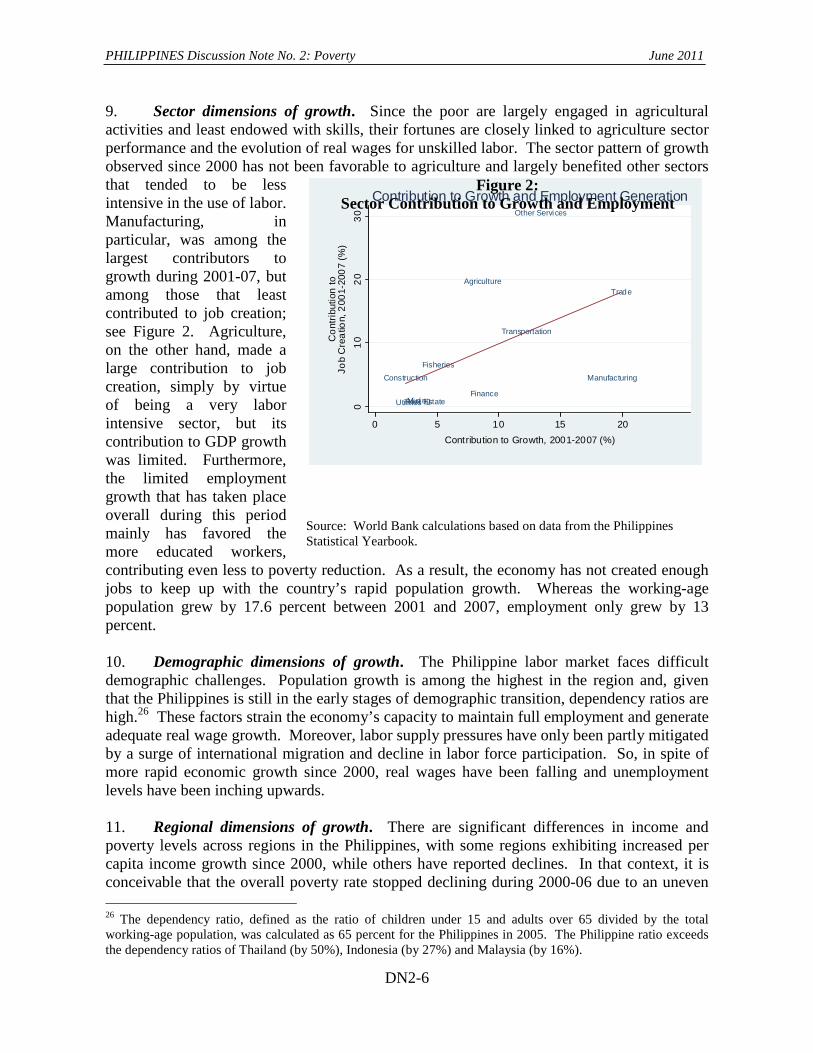

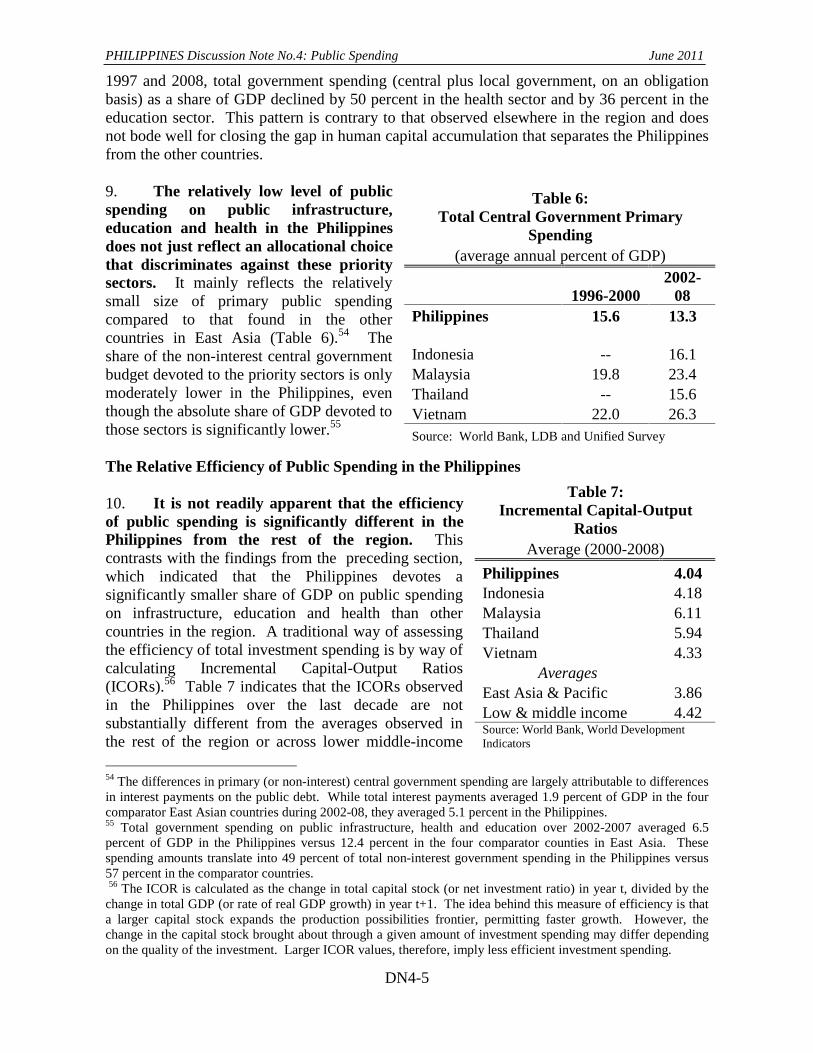

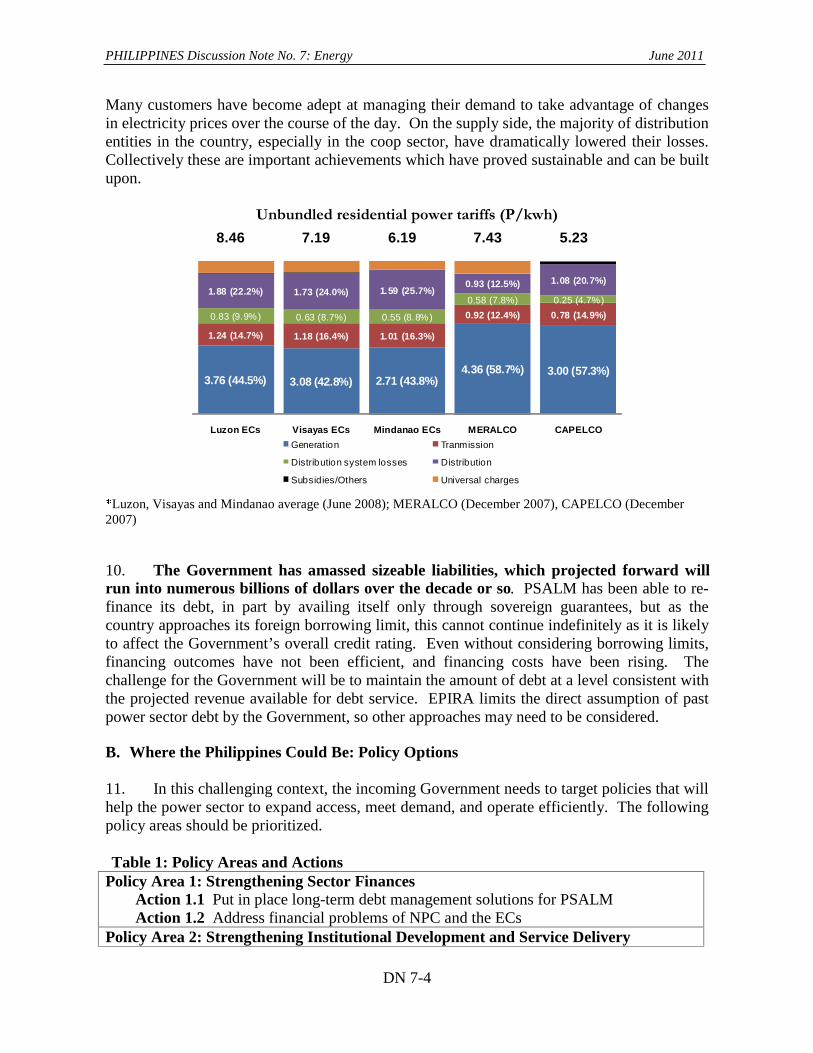

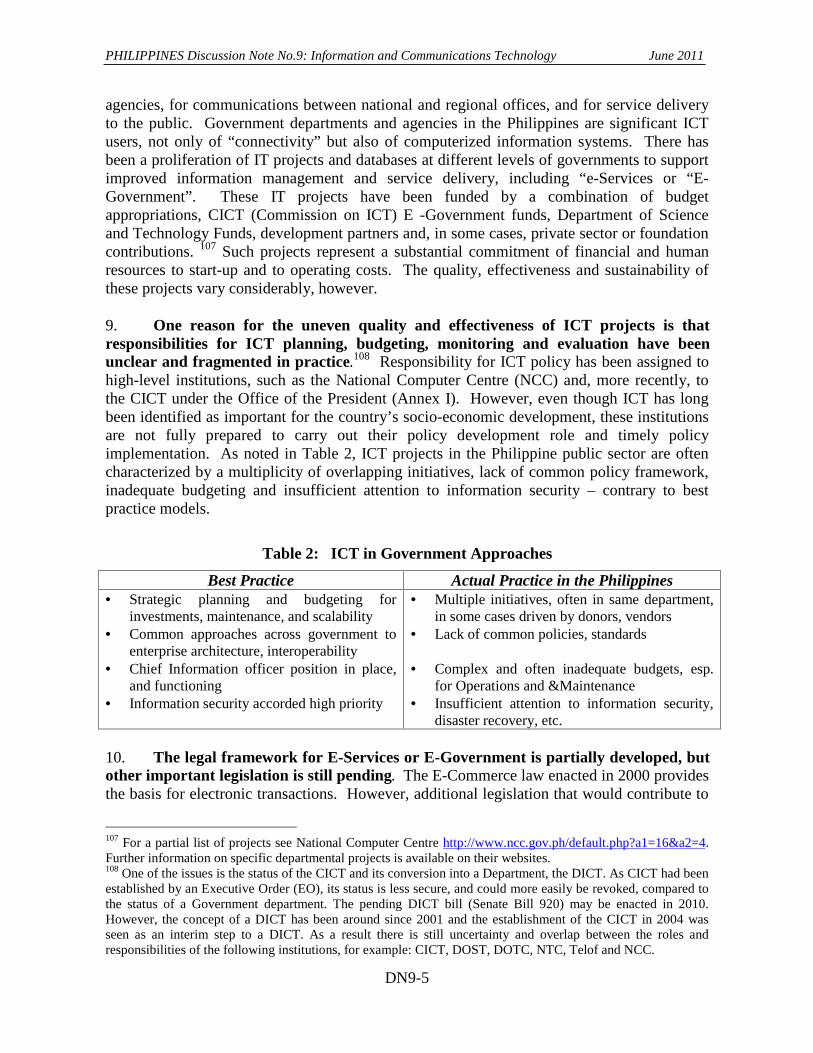

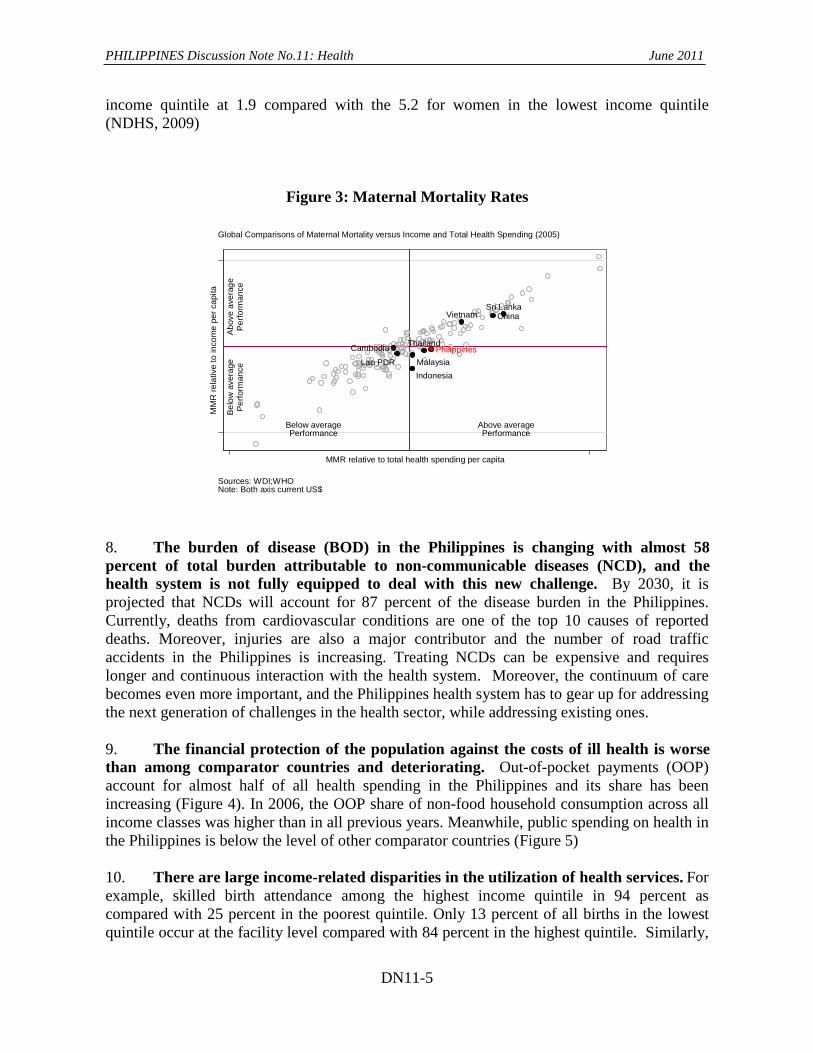

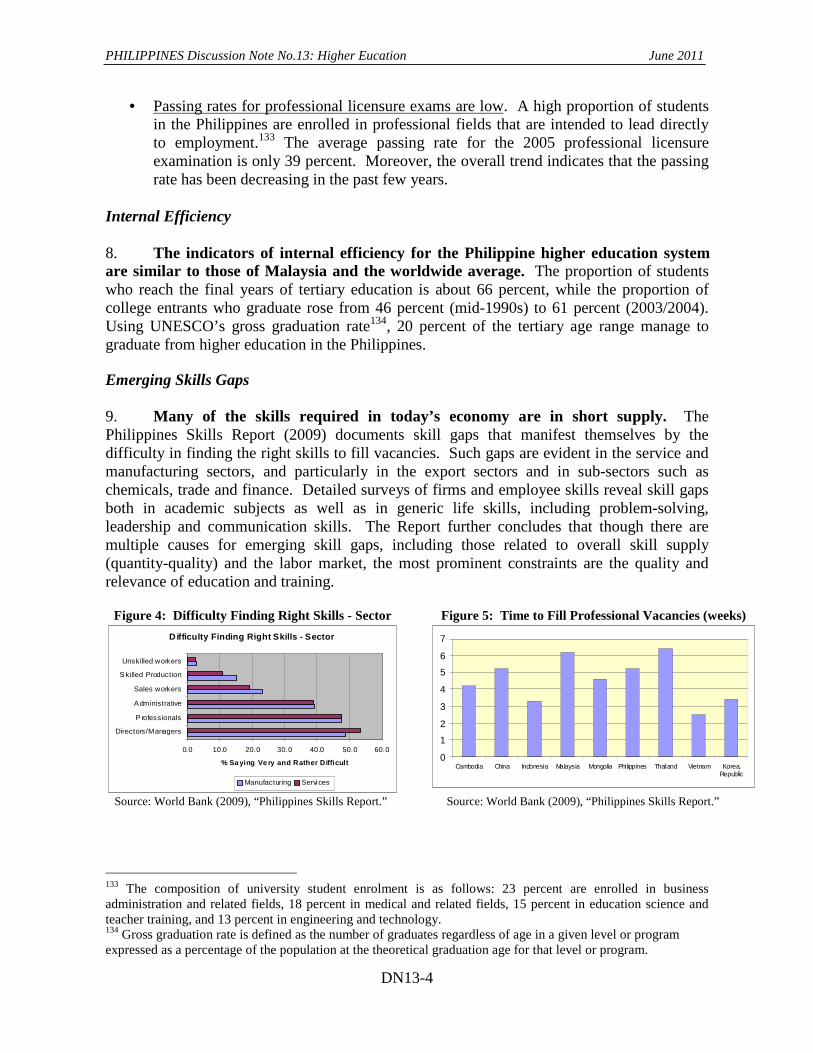

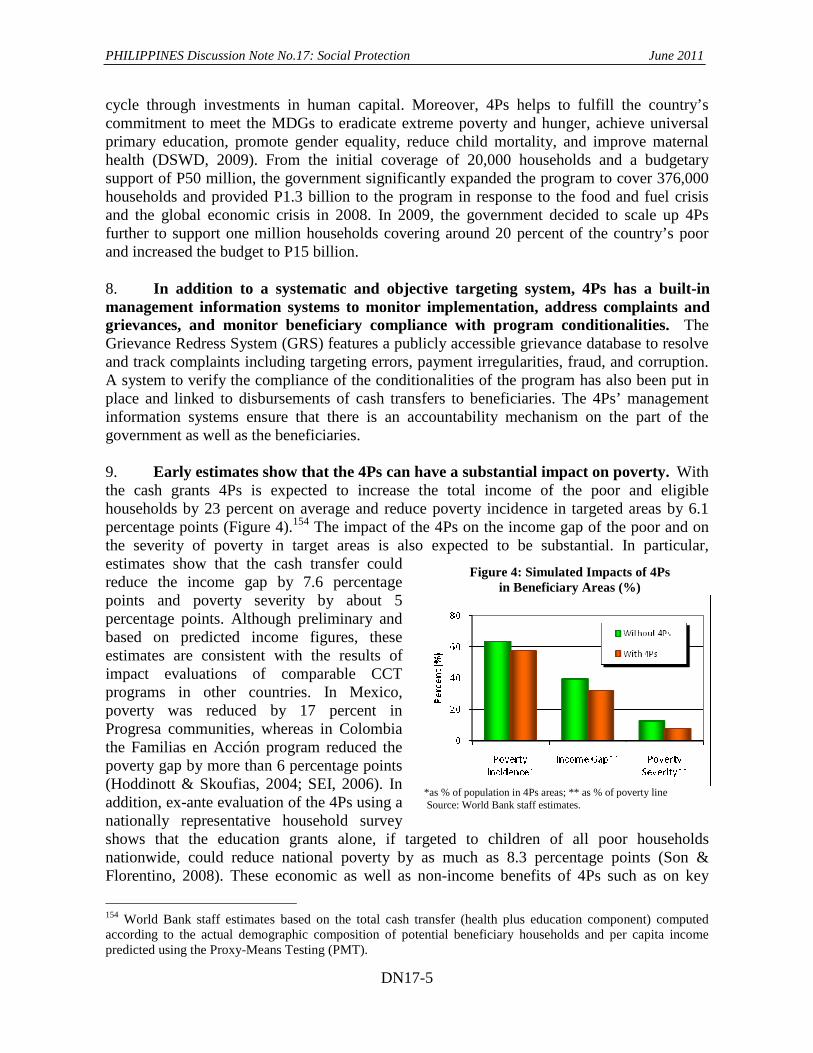

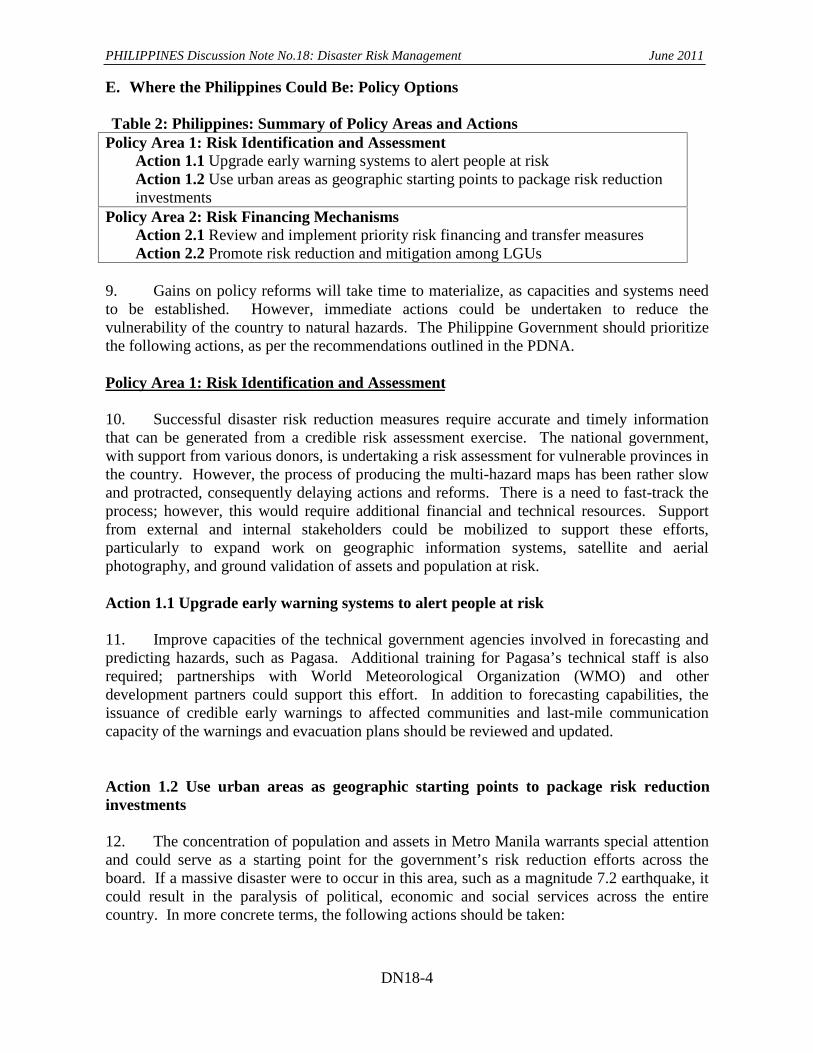

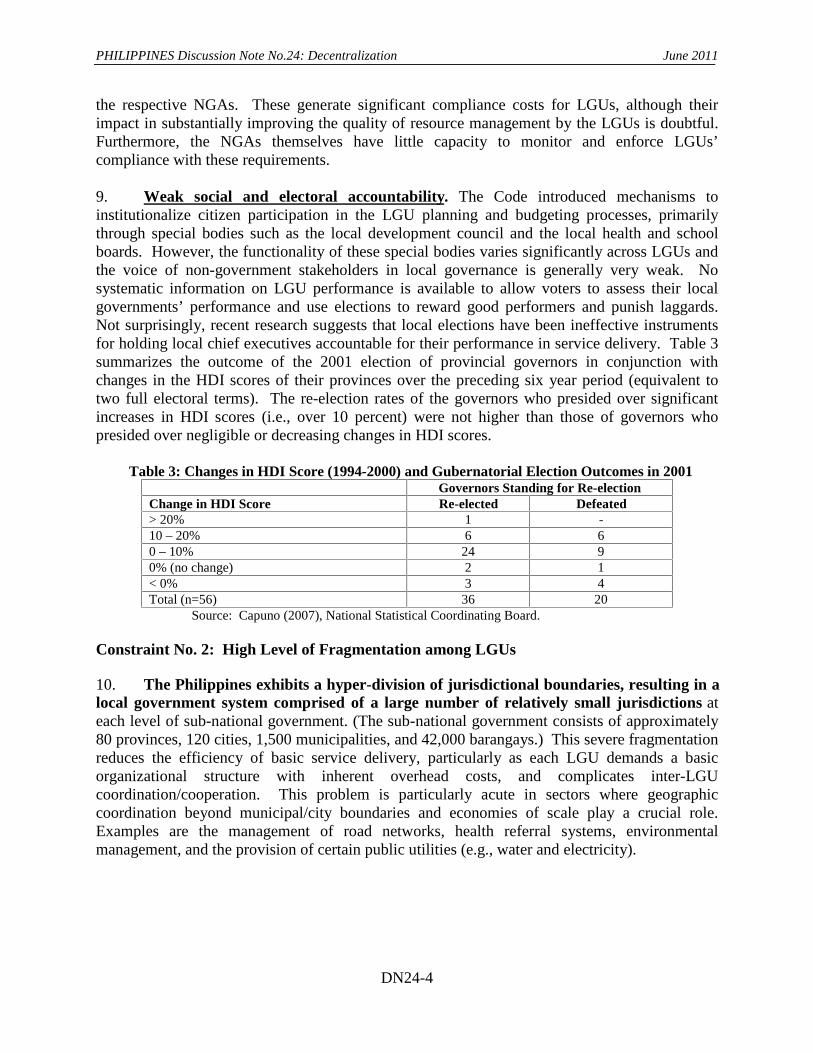

Bert Hofman Jesse Ang

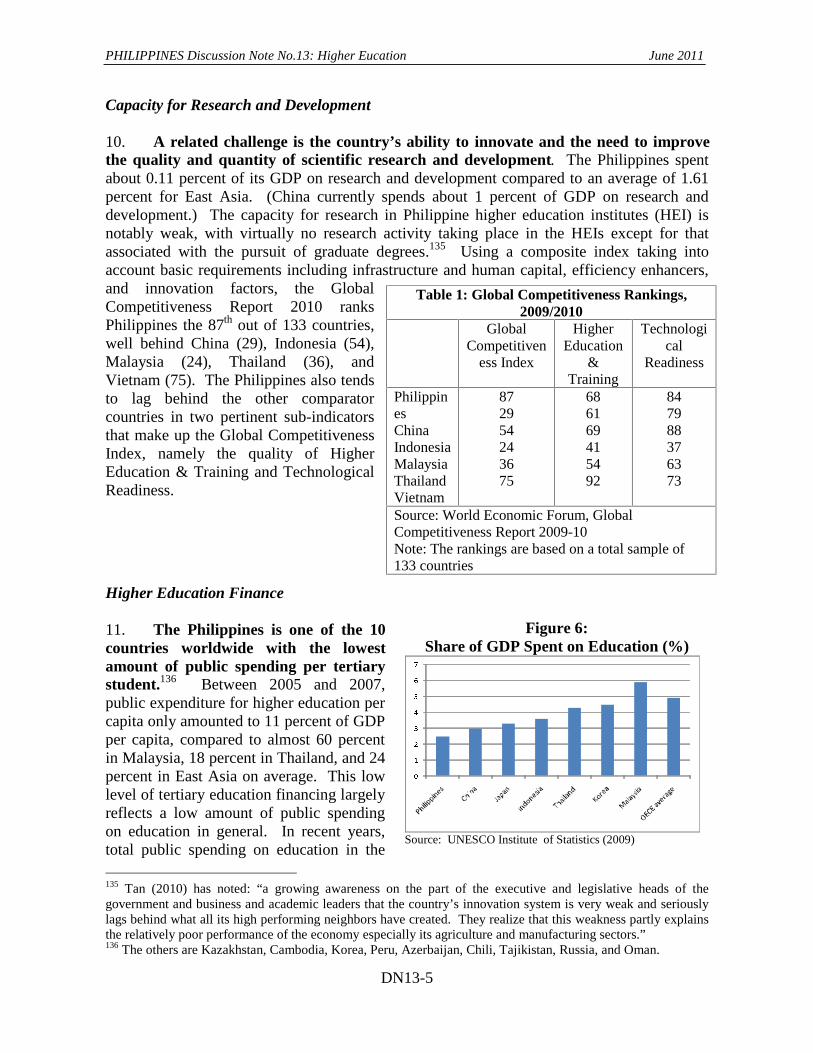

Task Team Leaders

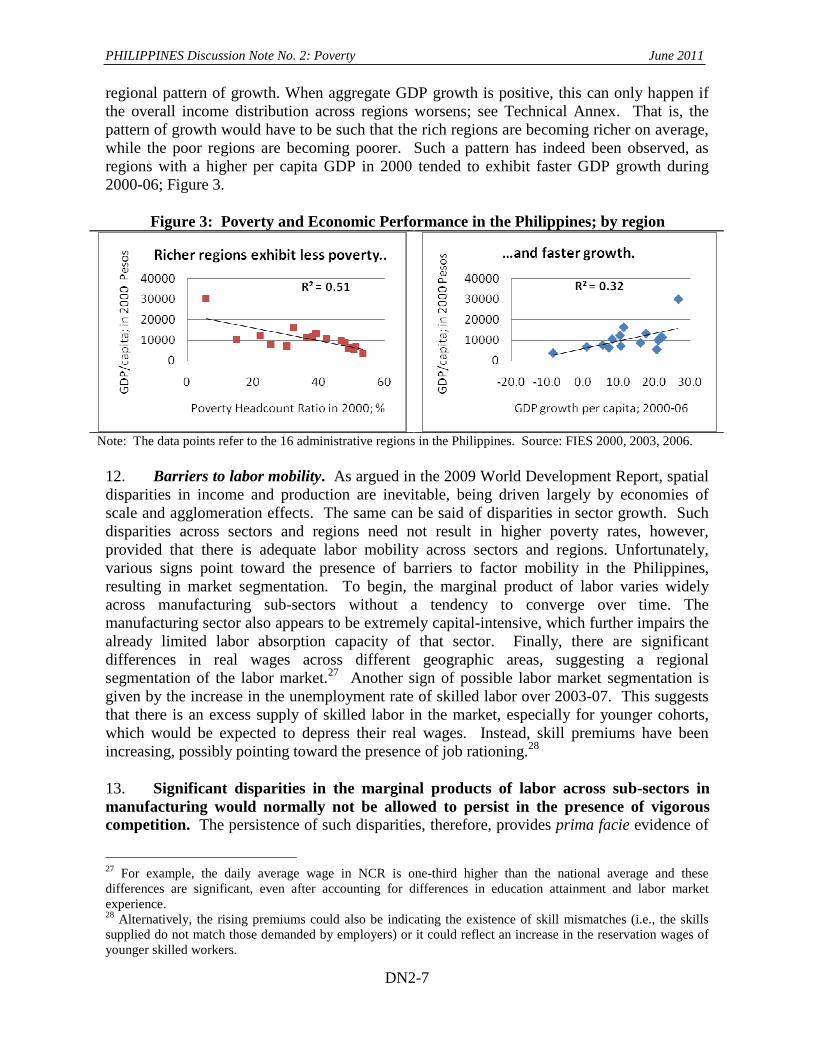

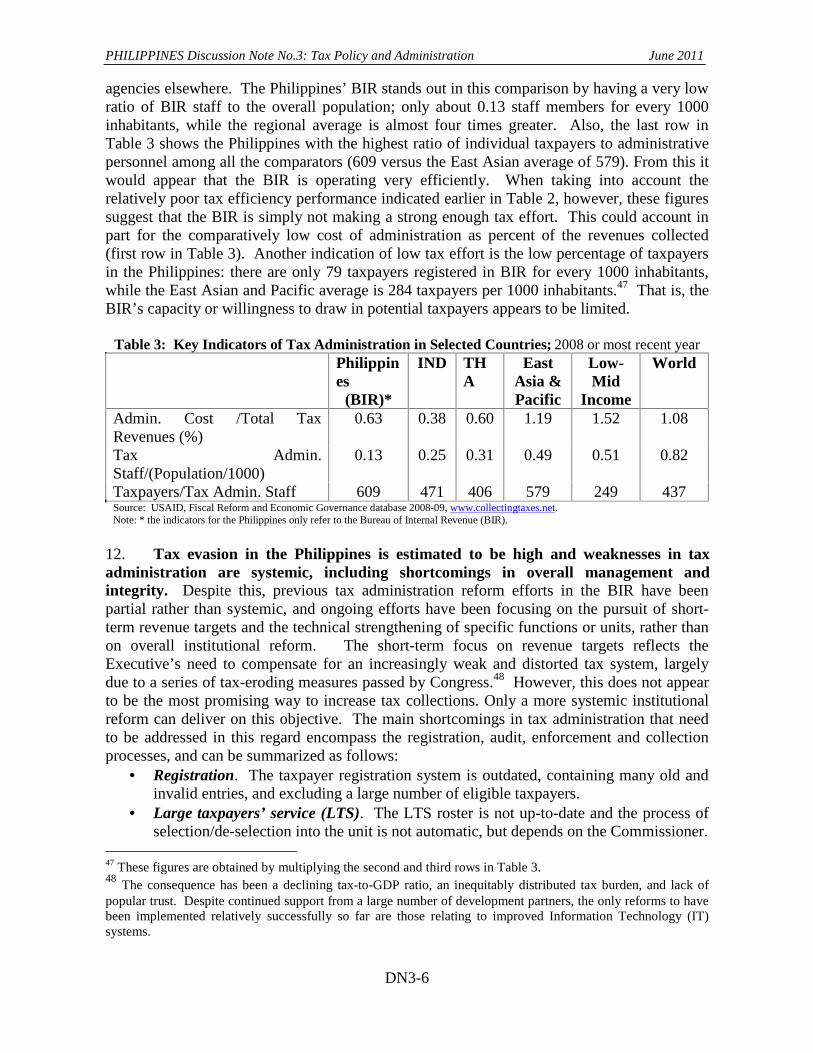

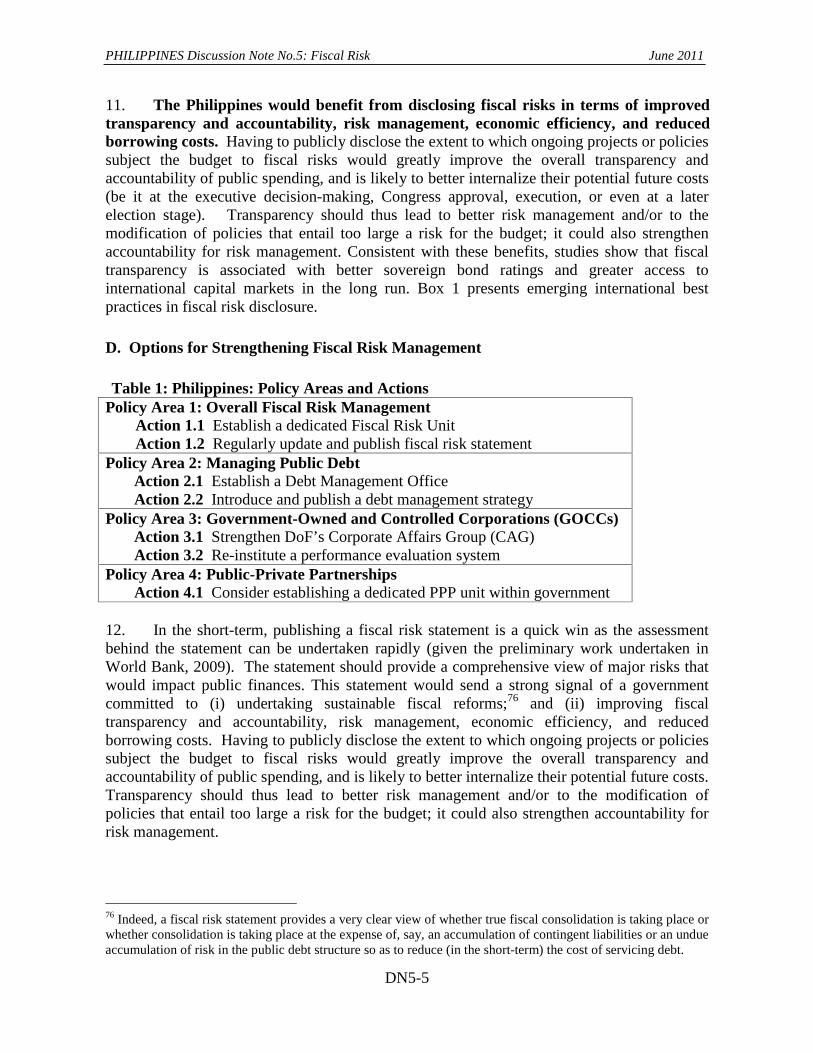

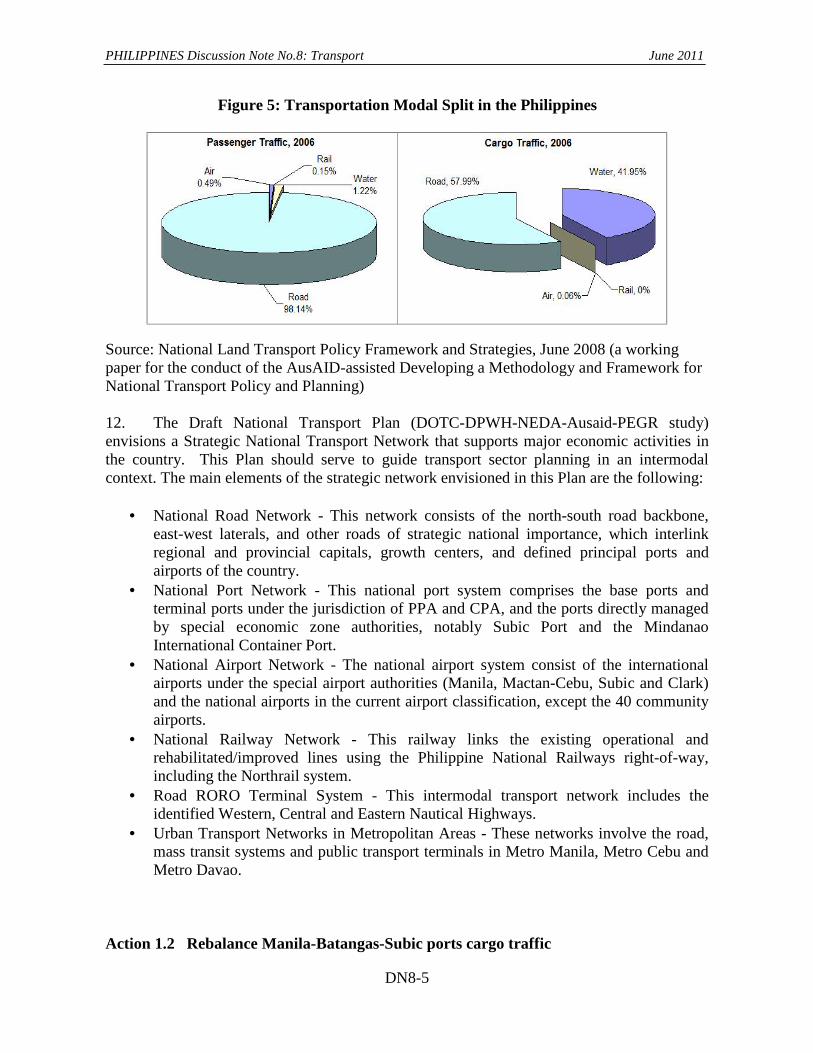

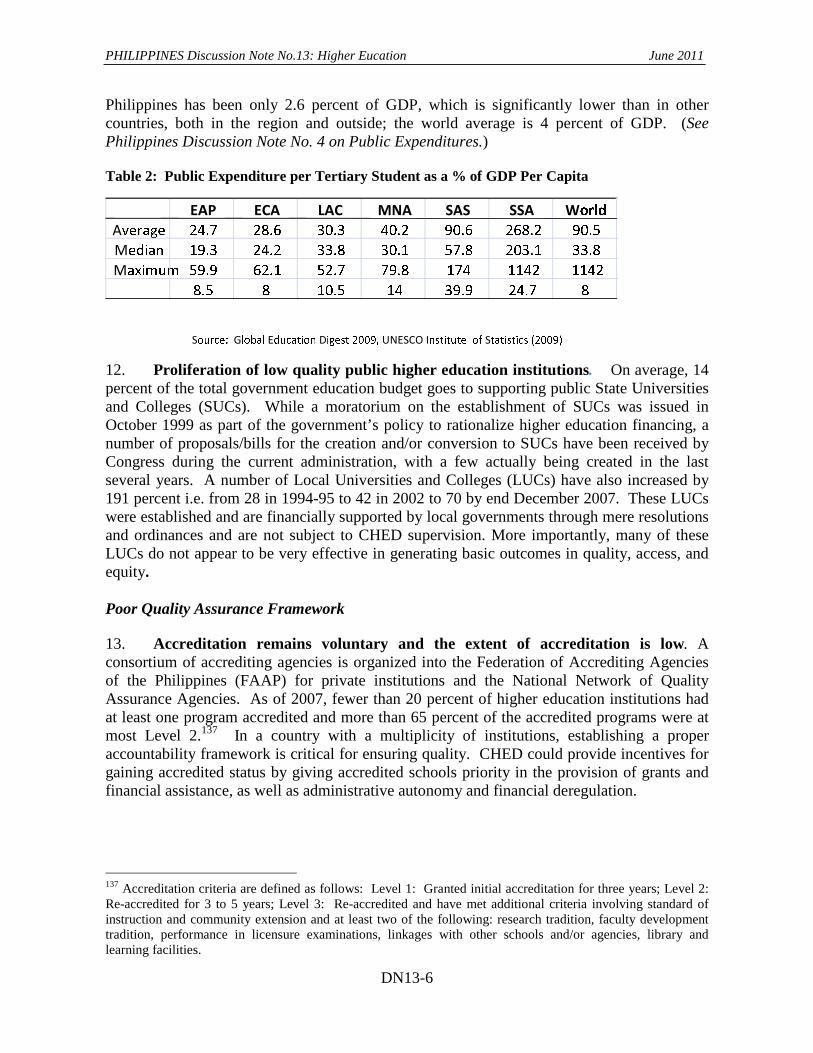

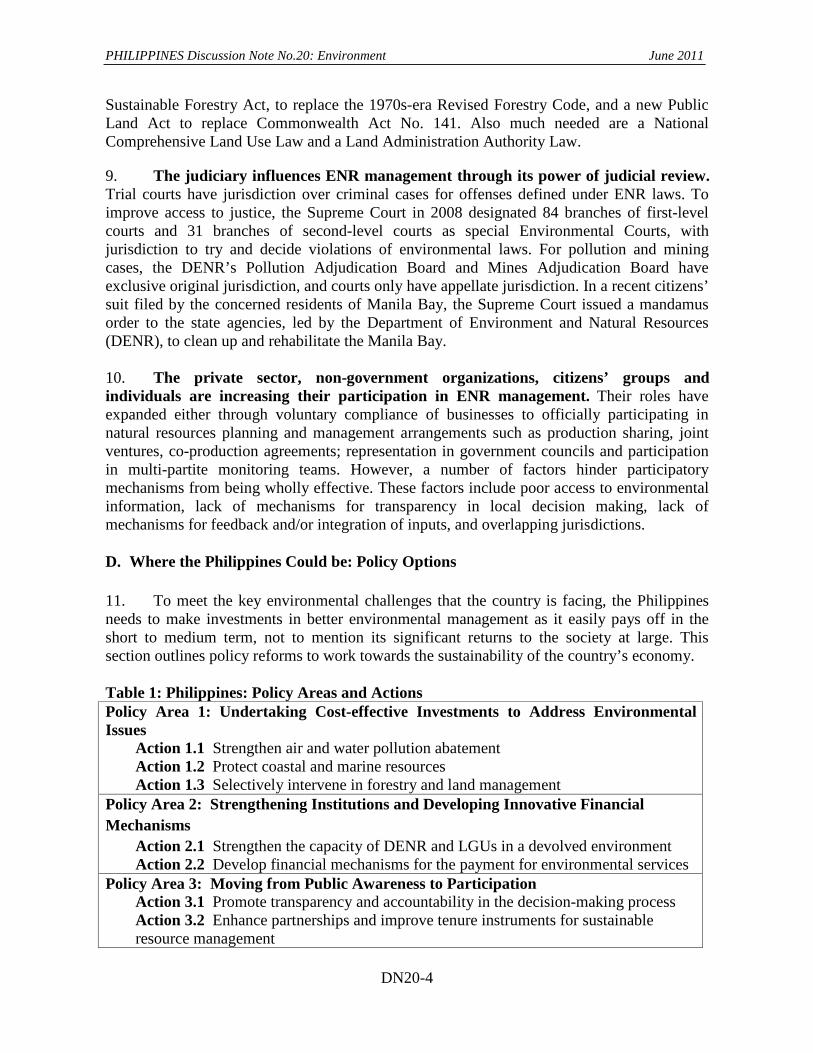

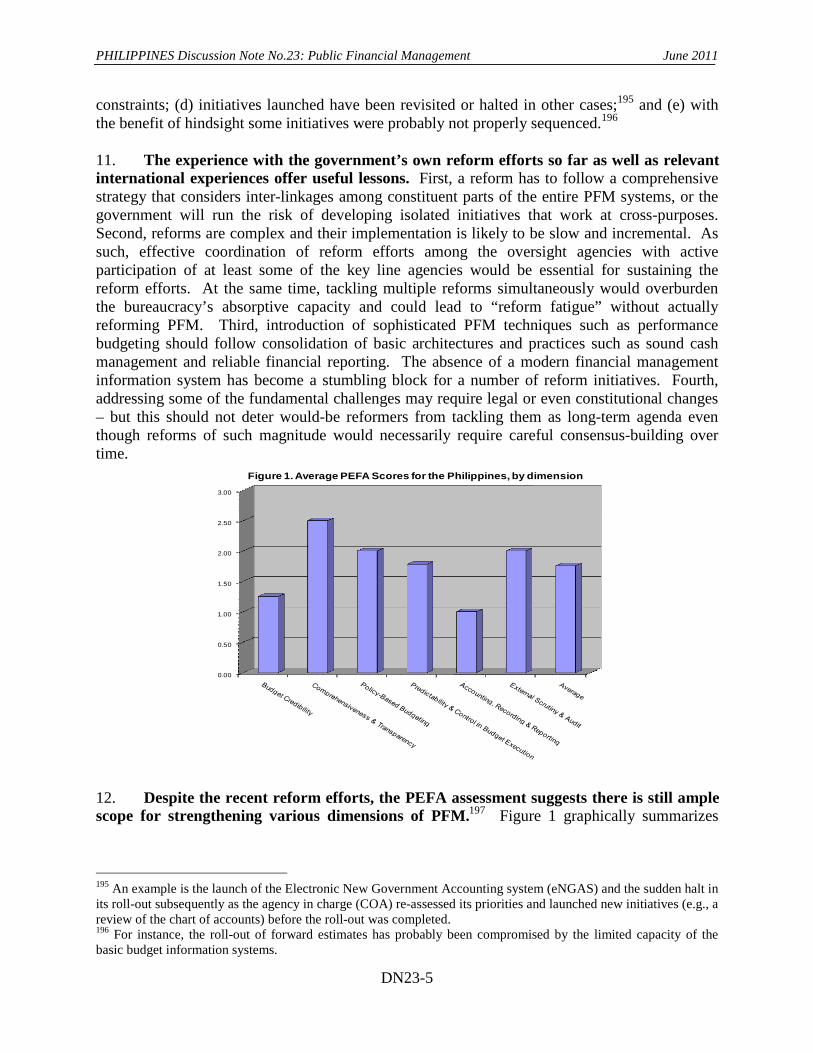

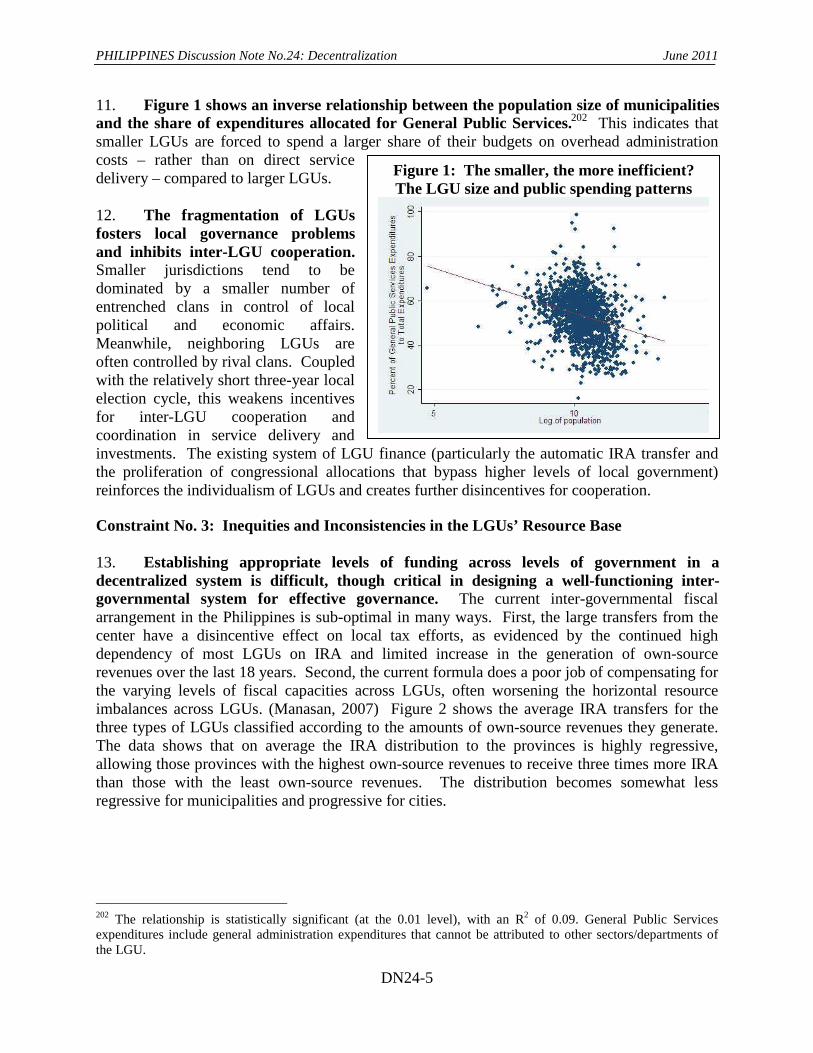

Lada Strelkova Ulrich Lachler Mark Woodward Jehan Arulpragasam

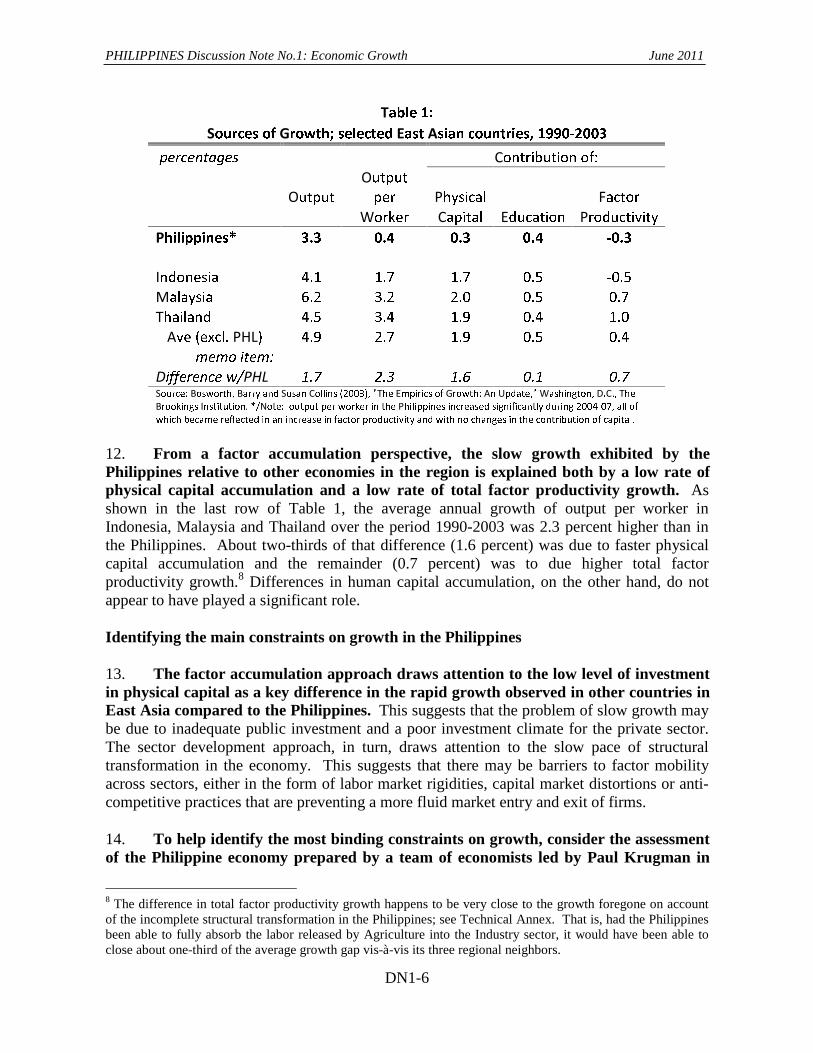

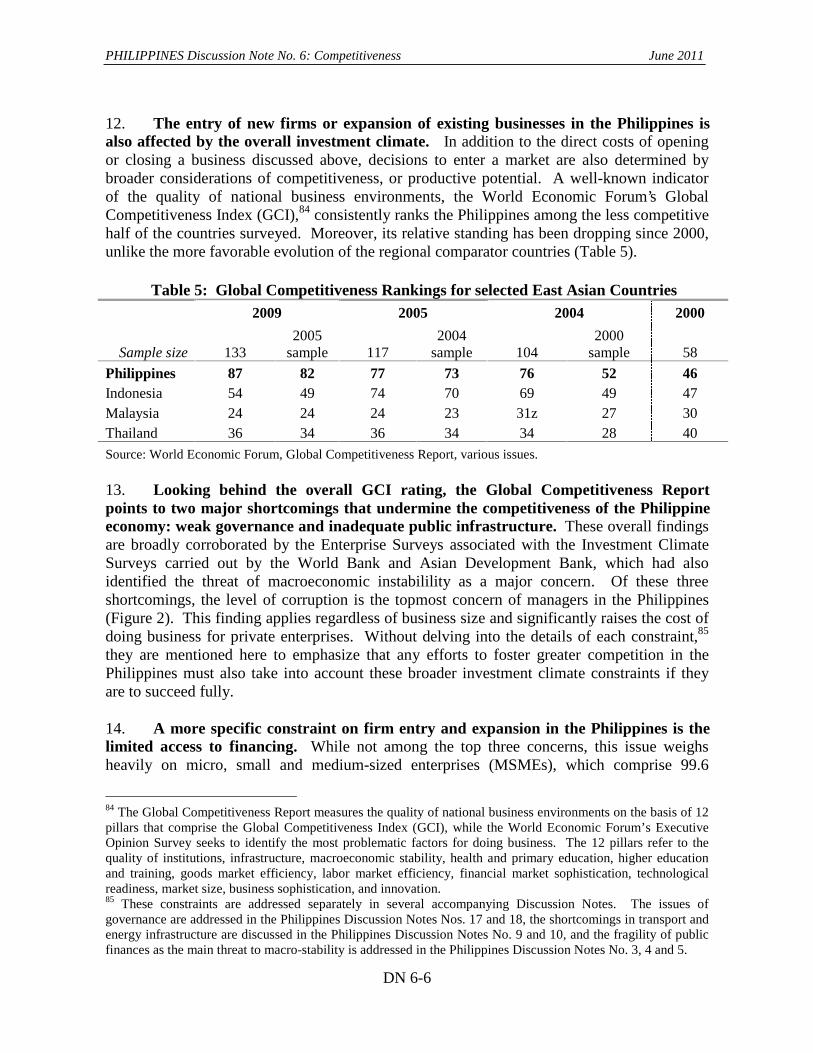

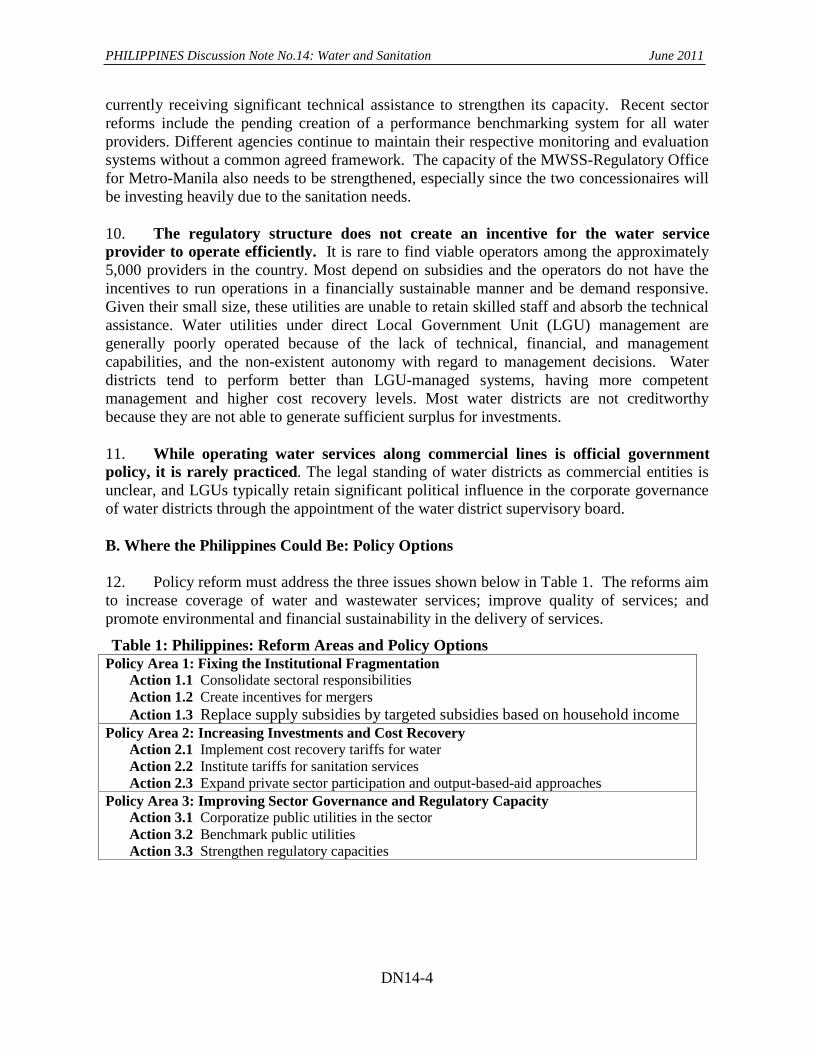

Magdi Amin

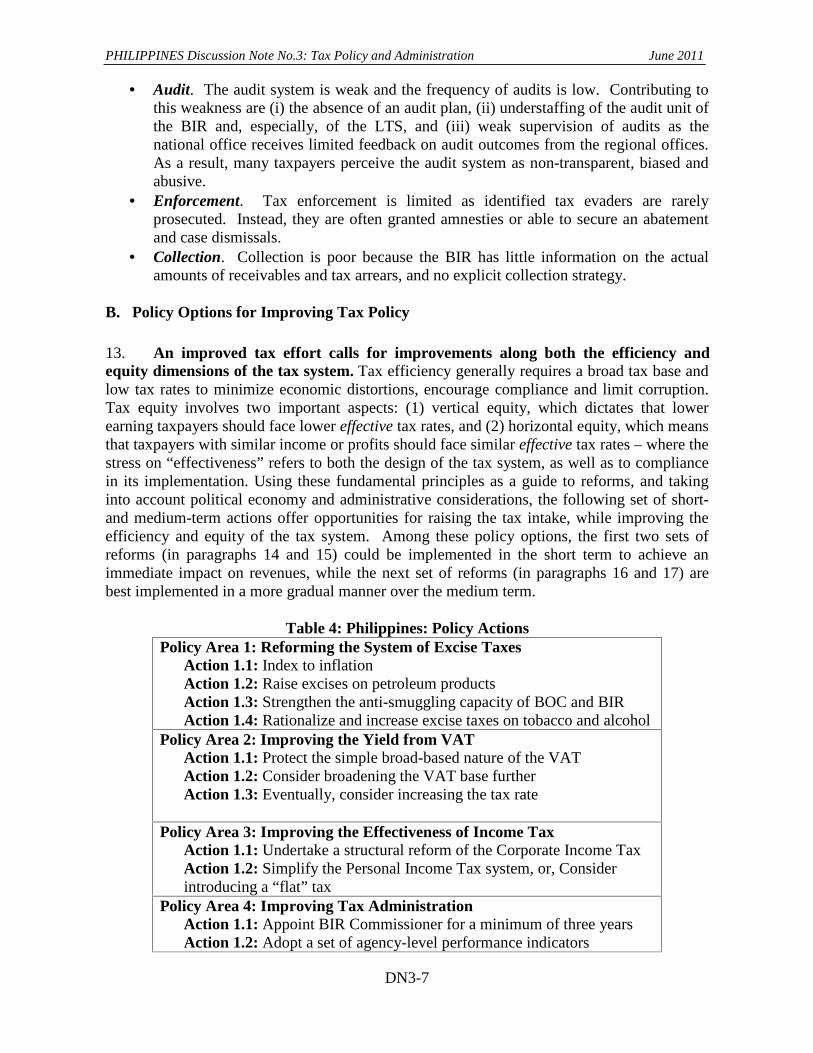

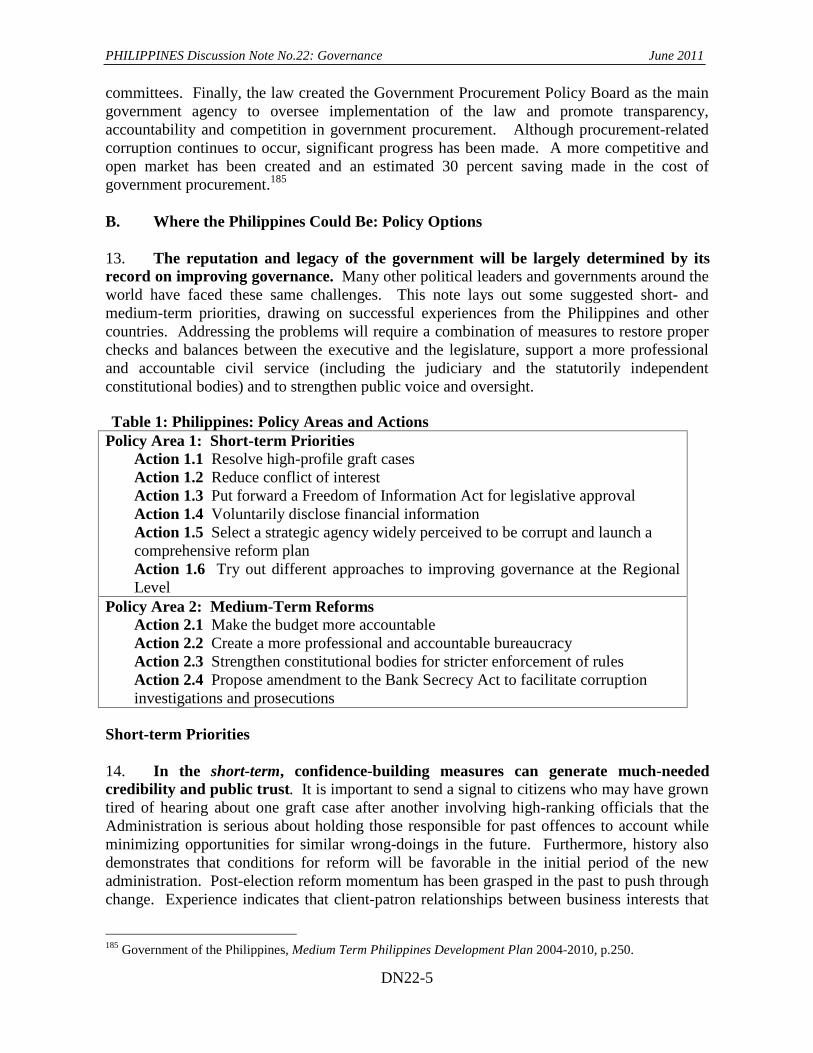

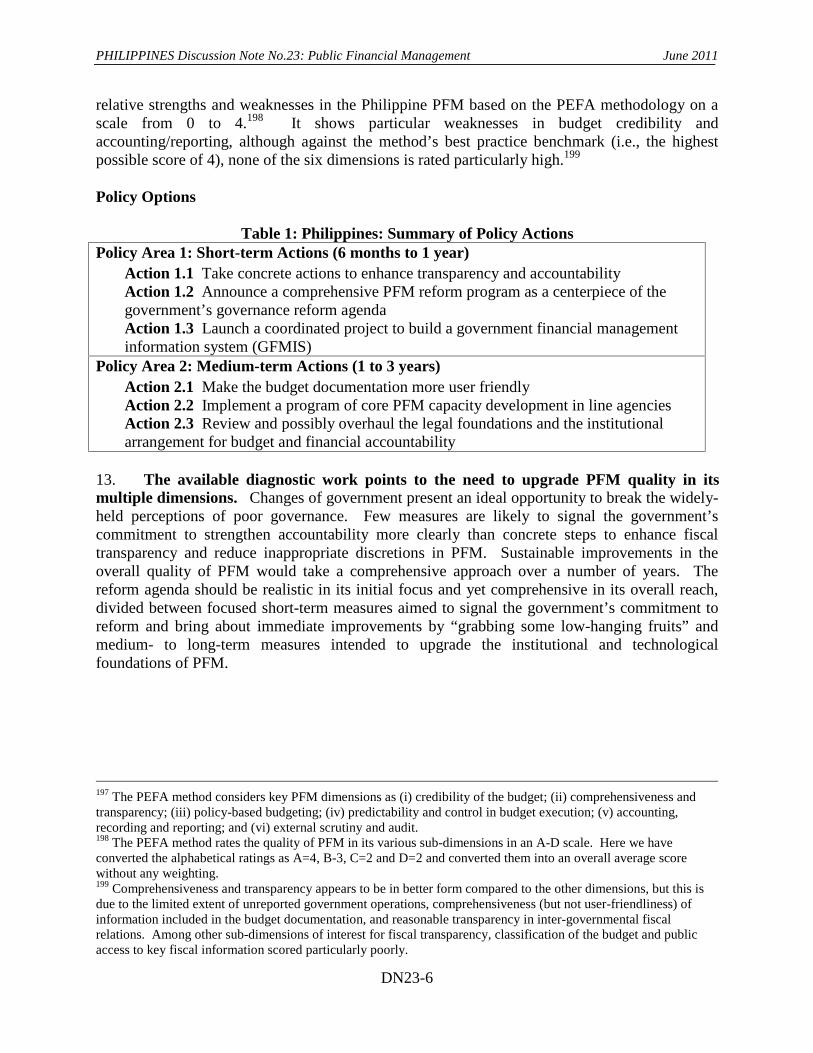

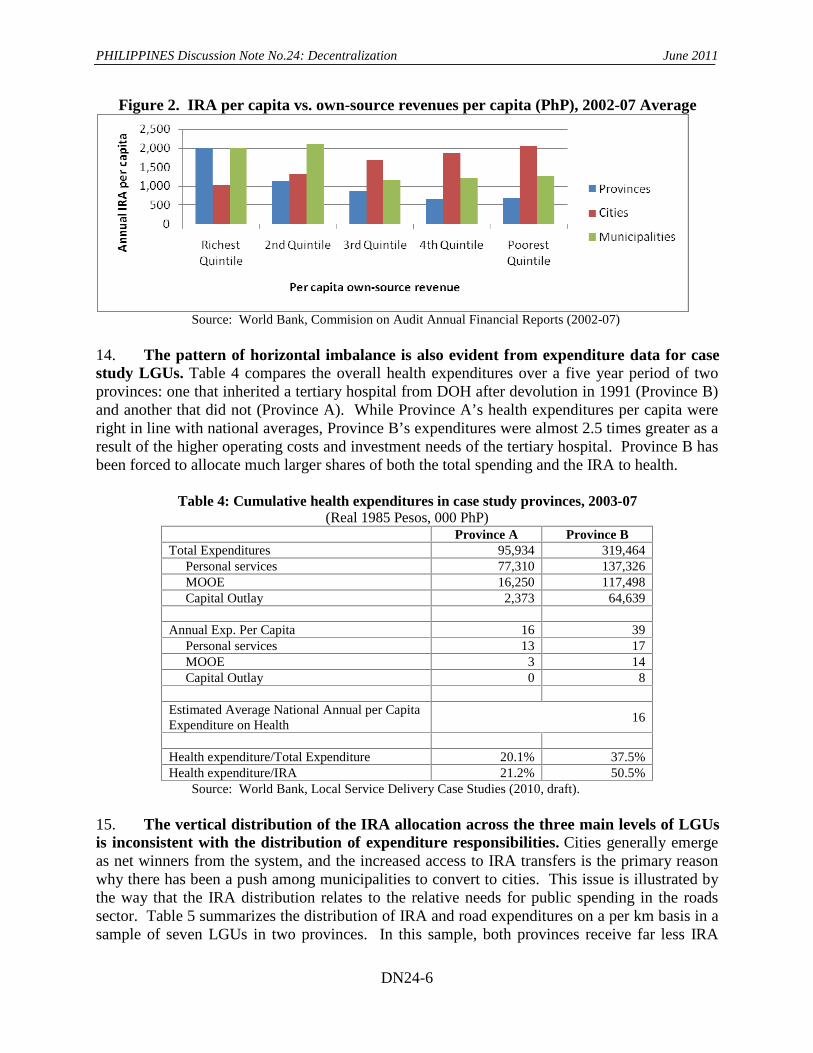

This report was prepared under the guidance of Bert Hofman, IBRD Country Director, and Jesse Ang, IFC Resident Representative, by a team led by: Lada Strelkova, Ulrich Lachler, Mark Woodward, and Jehan Arulpragasam. Daniella Gressani and Carlos Felipe Jaramillo served as peer reviewers.

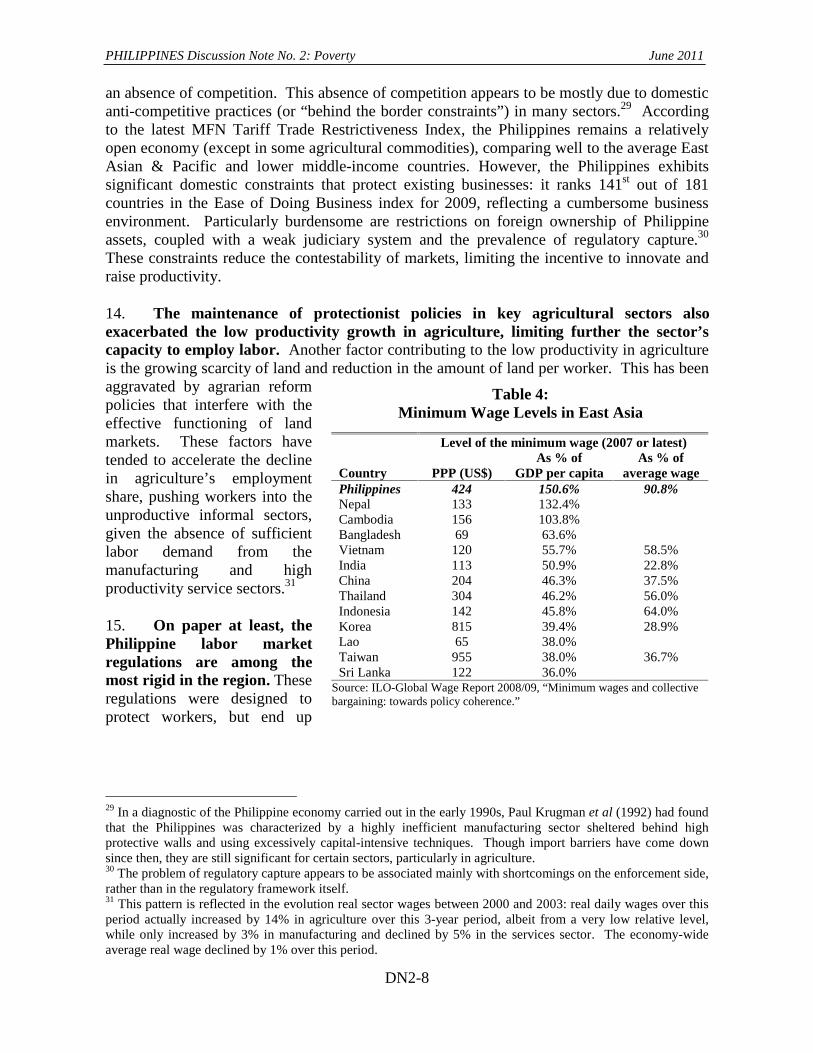

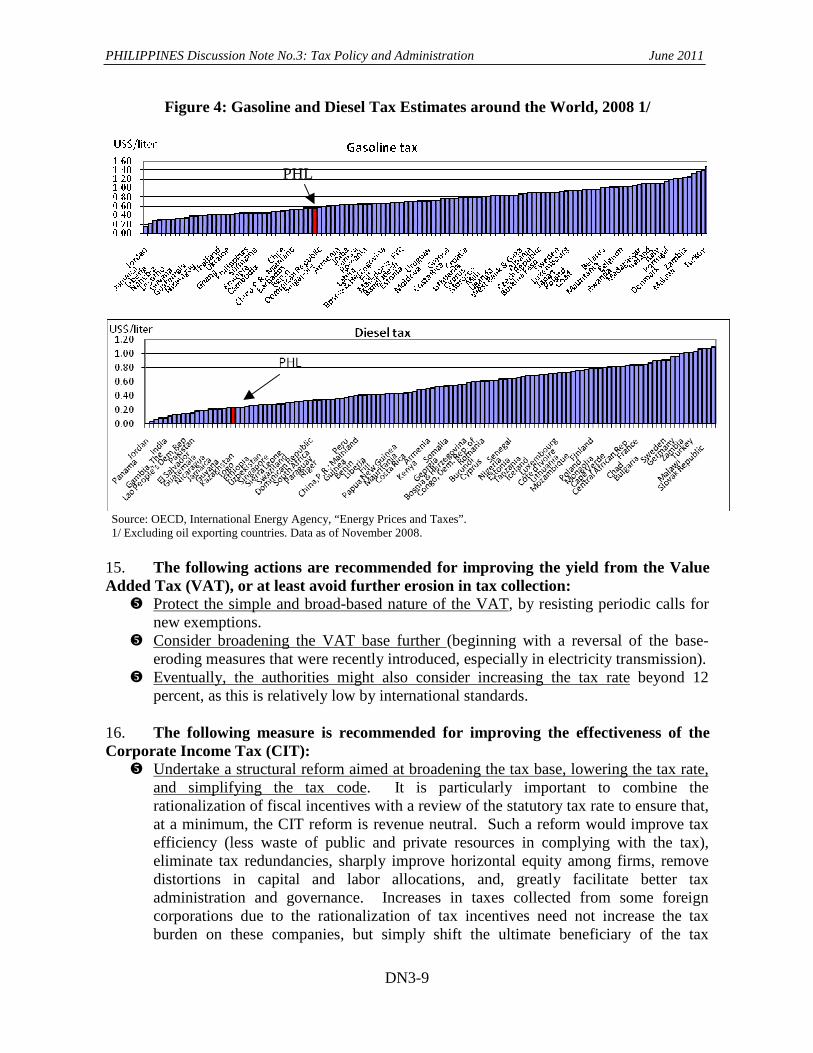

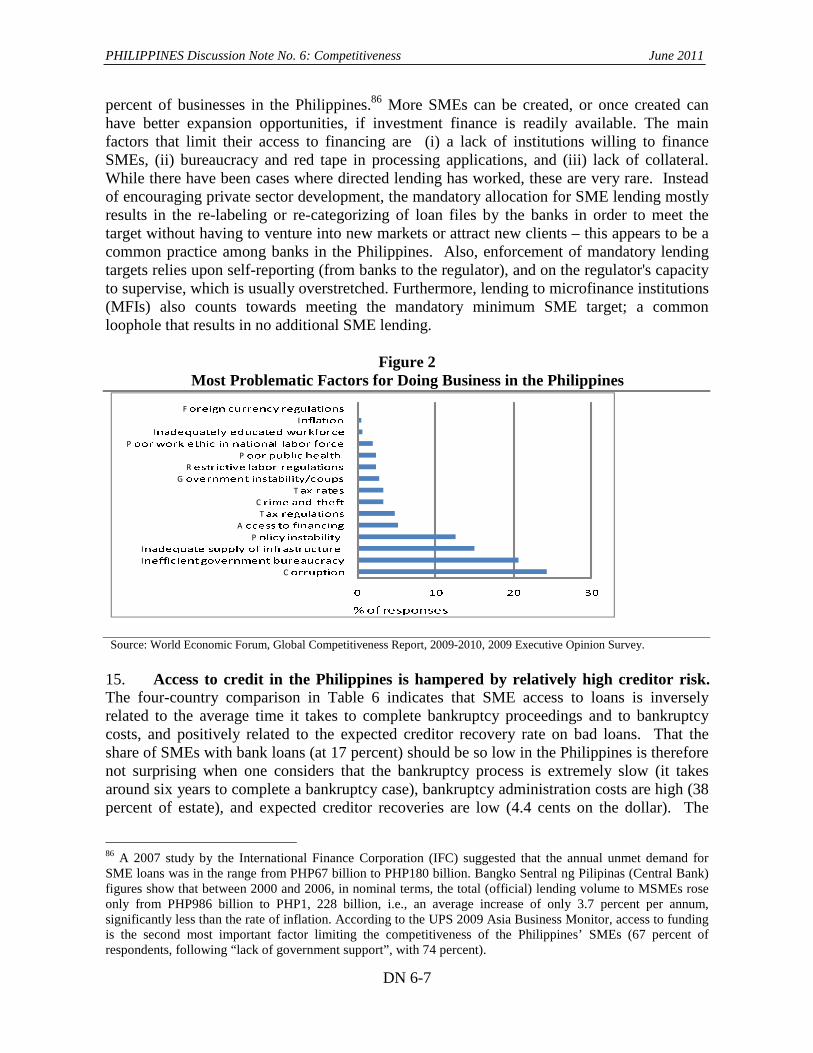

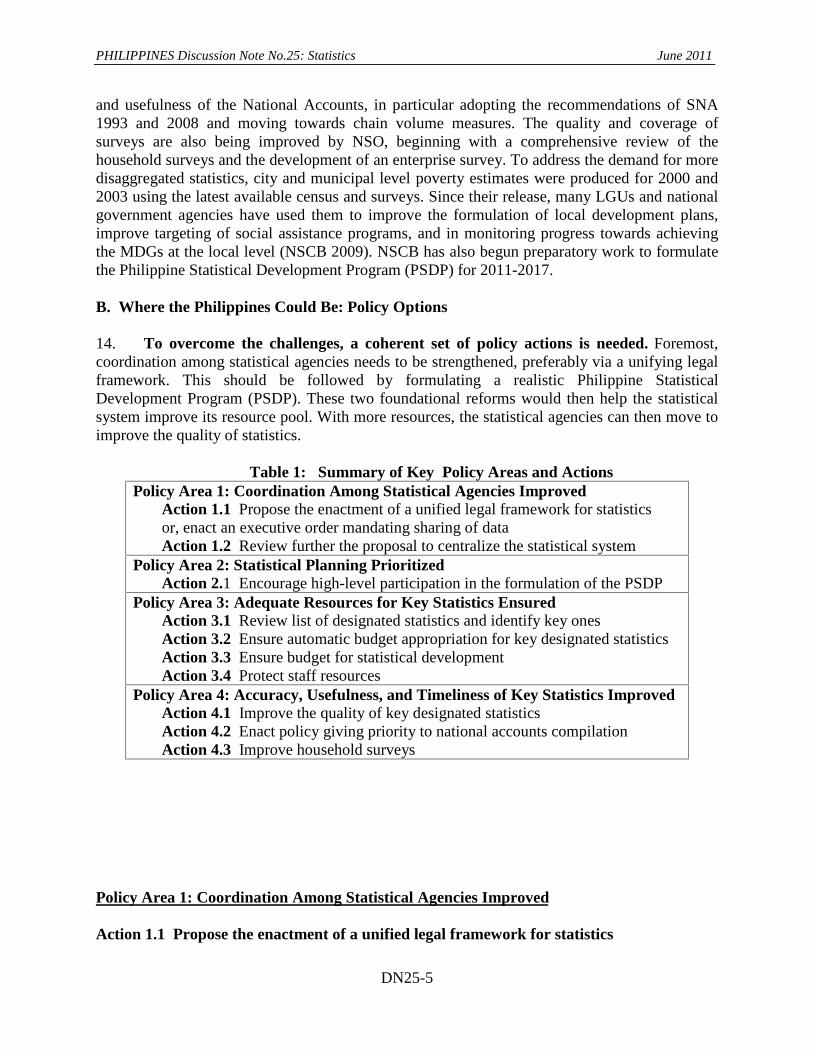

The following World Bank Group staff have made important contributions to the Philippines Discussion Notes: Ajay Tandon, Alan Townsend, Amitabha Mukherjee, Andrew Parker, Anne Sevilla, Baher El-Hifnawi, Ben Gericke, Carol Figueroa-Geron, Catherine Vidar, Christopher Ancheta, Christopher Pablo, David Llorito, Dennis Streveler, Douglas Forno, Eduardo Banzon, Eric Le Borgne, Fabrizio Bresciani, Felizardo Virtucio, Fermin Adriano, George Shieber, Gerardo Parco, Gerlin May U. Catangui, Iain Shuker, Jan Bojo, Josefo Tuyor, Junko Onishi, Karl Kendrick Chua, Lawrence Tang, Leonora Gonzales, Loraine Hawkins, Luisa Patricia Fernandez Delgado, Lynnette Dela Cruz Perez, Maribelle Zonaga, Maryse Gautier, Matthew Stephens, Maya Villaluz, Natasha Beschorner, Nora Moreno, Oscar Picazo, Patrick Labaste, Rajesh Pandey, Ramesh Siva, Rashiel Velarde, Roberto Rosadia, Rosa Alonso I. Terme, Rosechin Olfindo, Rozanno Rufino, Sarbani Chakraborty, Sheryll Namingit, Soonhwa Yi, Sudipto Sarkar, Victor Dato, Victor Dumas, Victor Vergara, Xiaoyan Liang, Yasuhiko Matsuda, and Zoe Elena Trohanis. Core team support was provided by: Maria Liberty Cardenas and Necitas Garcia; and Zafar Ahmed and Jayasankar Shivakumar (consultants).

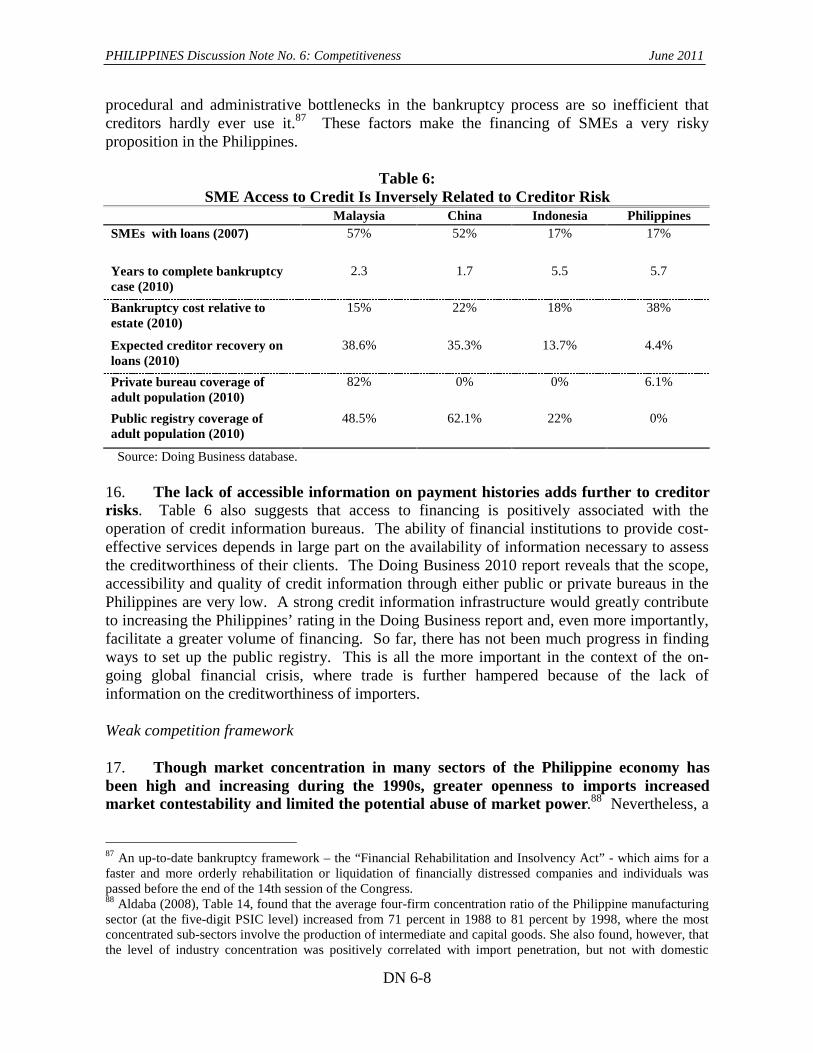

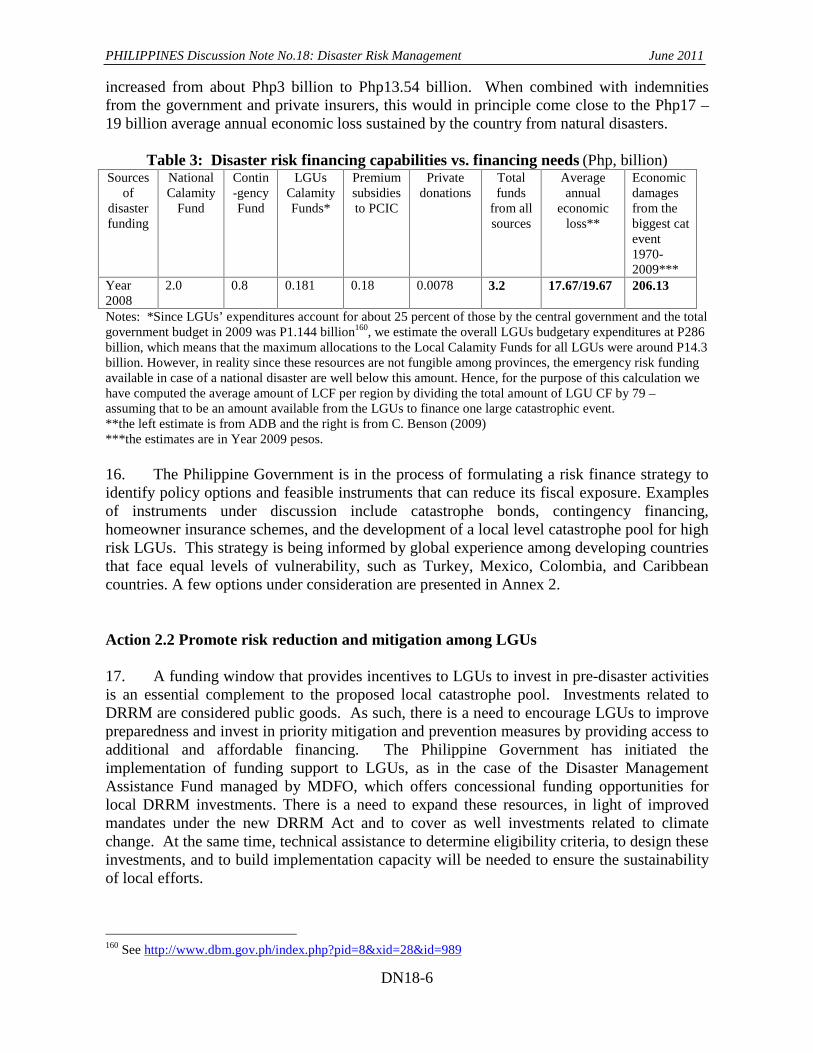

Special thanks are extended to the Australian Agency for International Development (AusAID) for supporting the preparation of this report, and to Andrew Cumpston and Ken Vine of AusAID for their contribution to individual discussion notes.

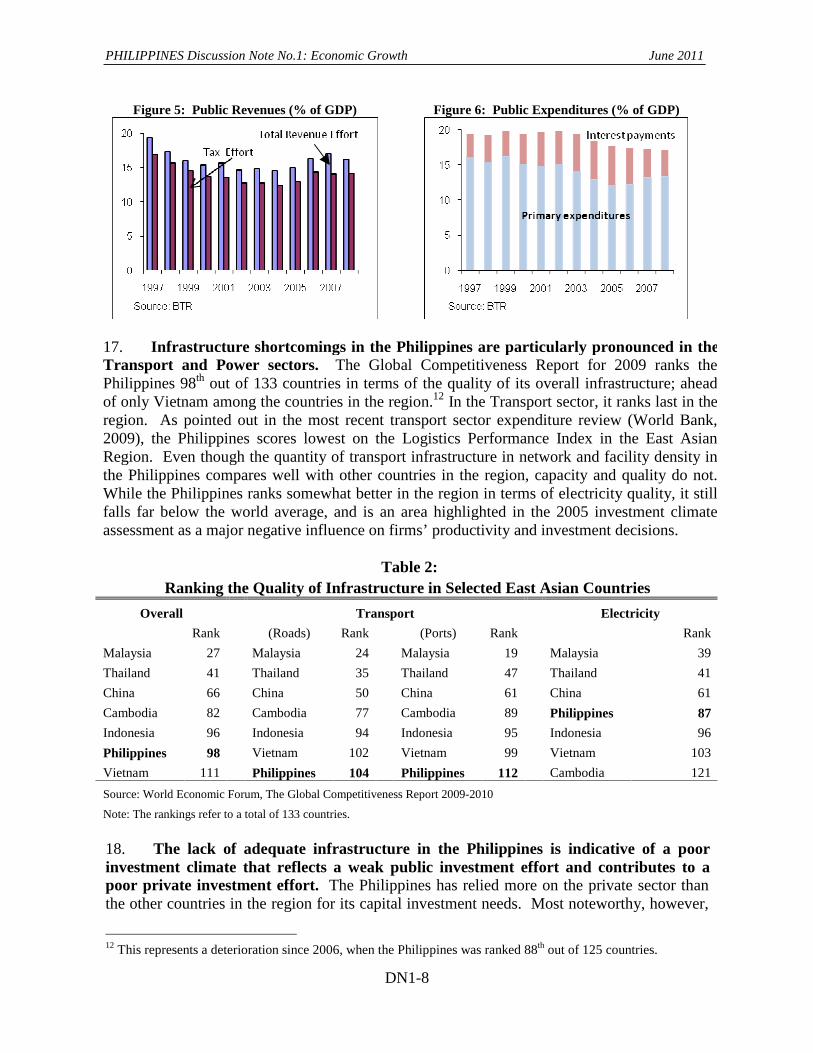

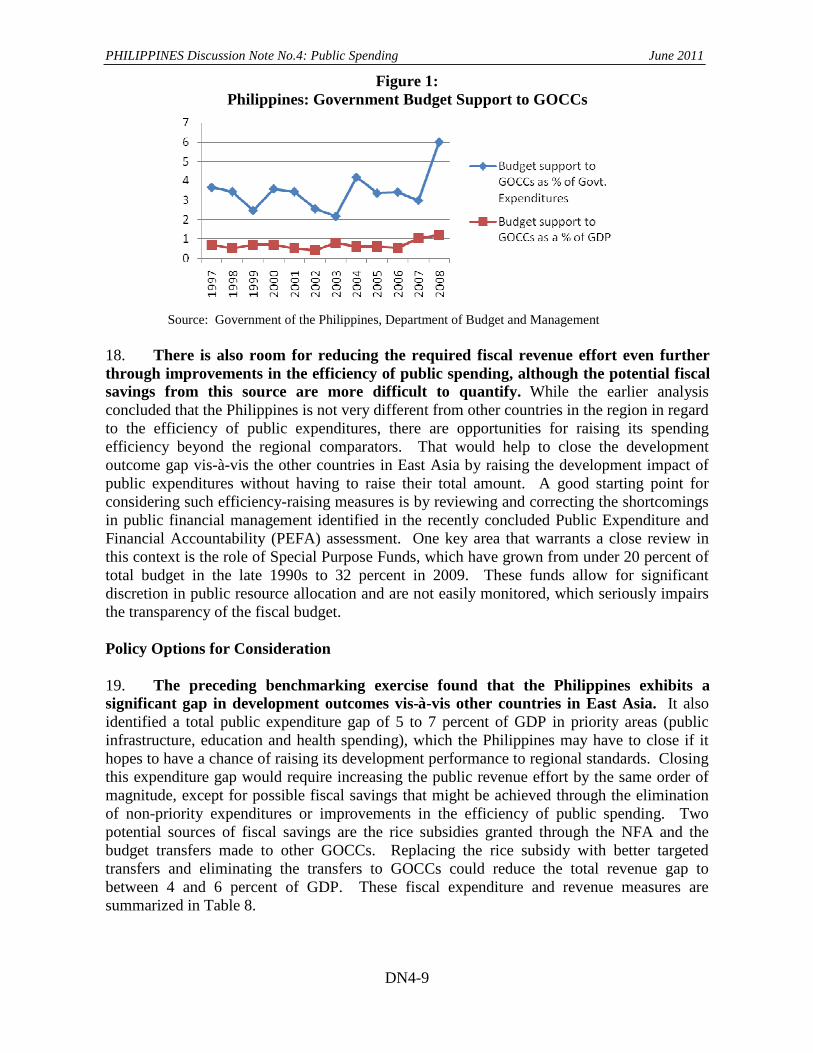

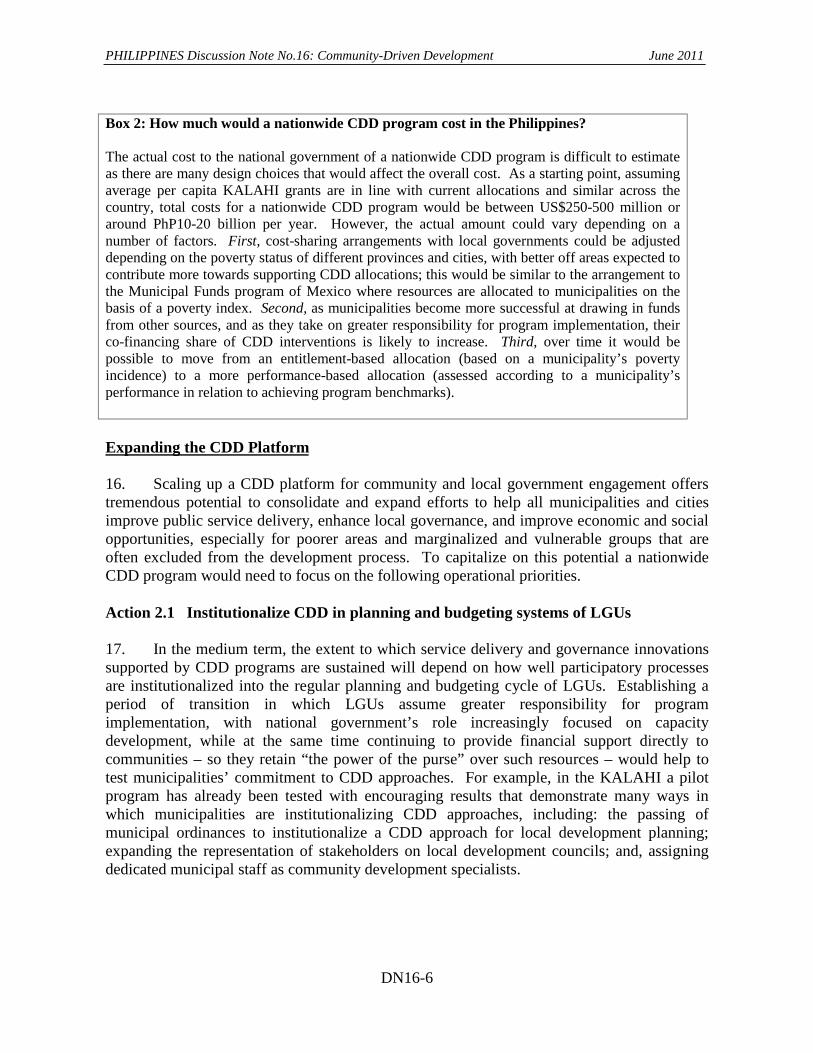

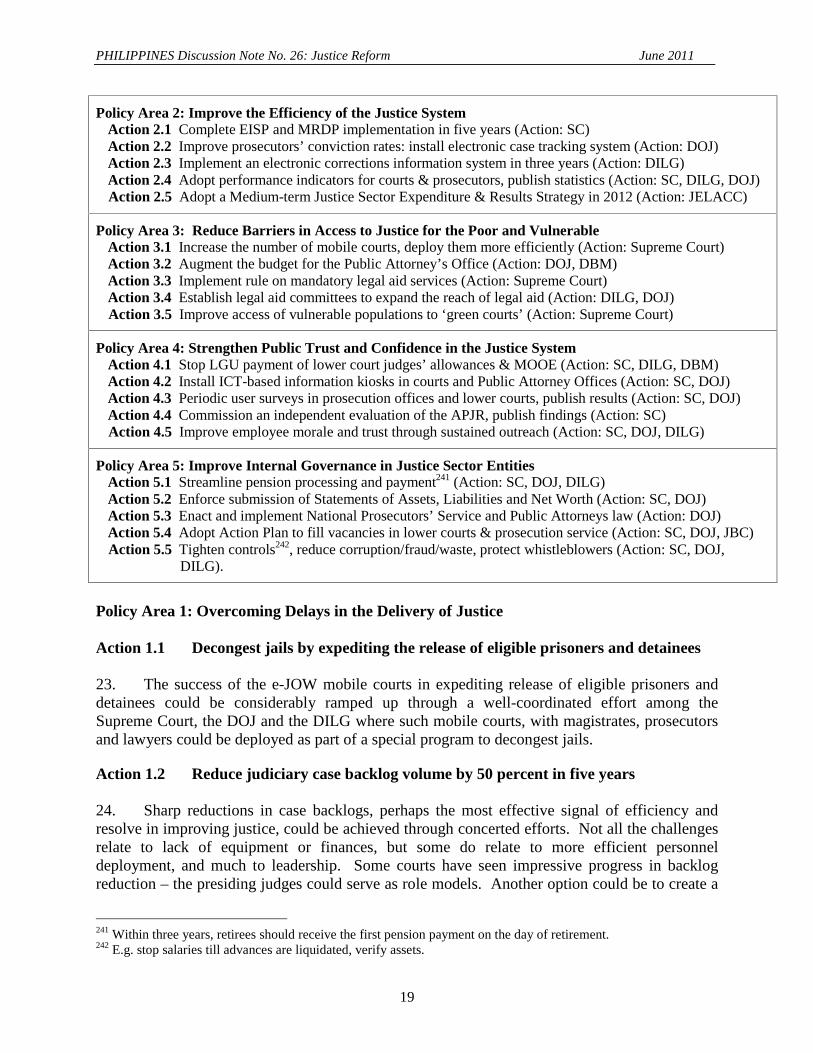

ACRONYMS AND ABBREVIATIONS

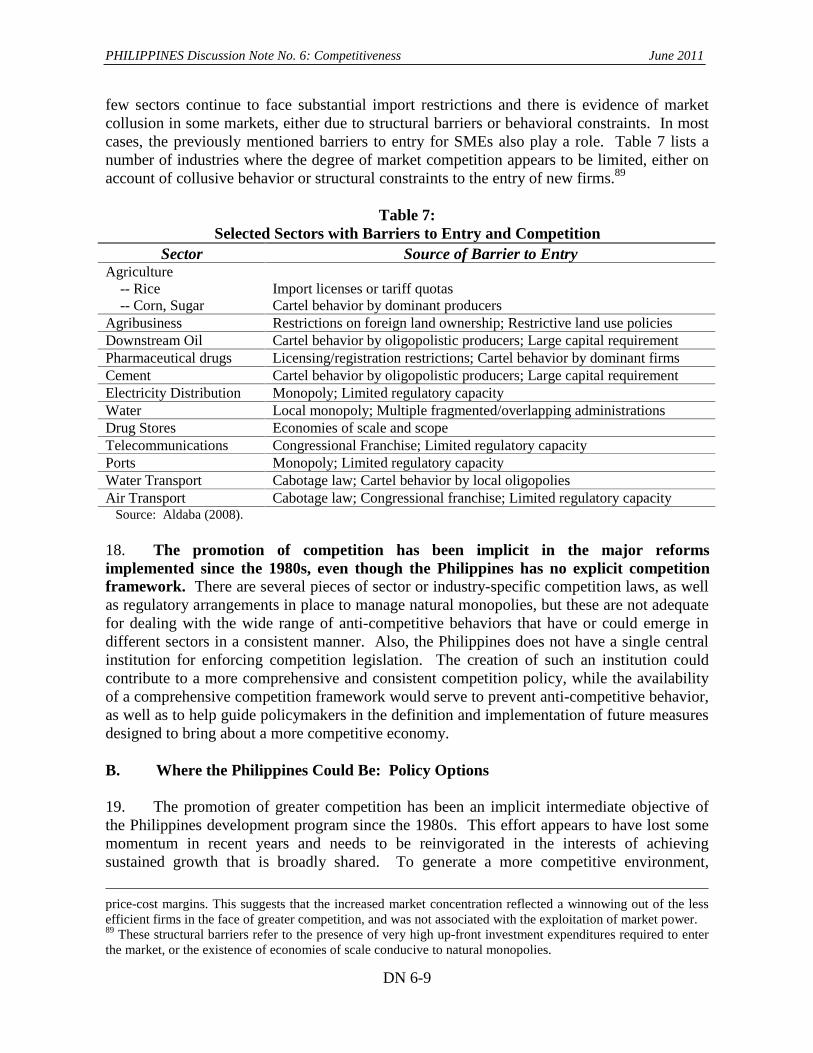

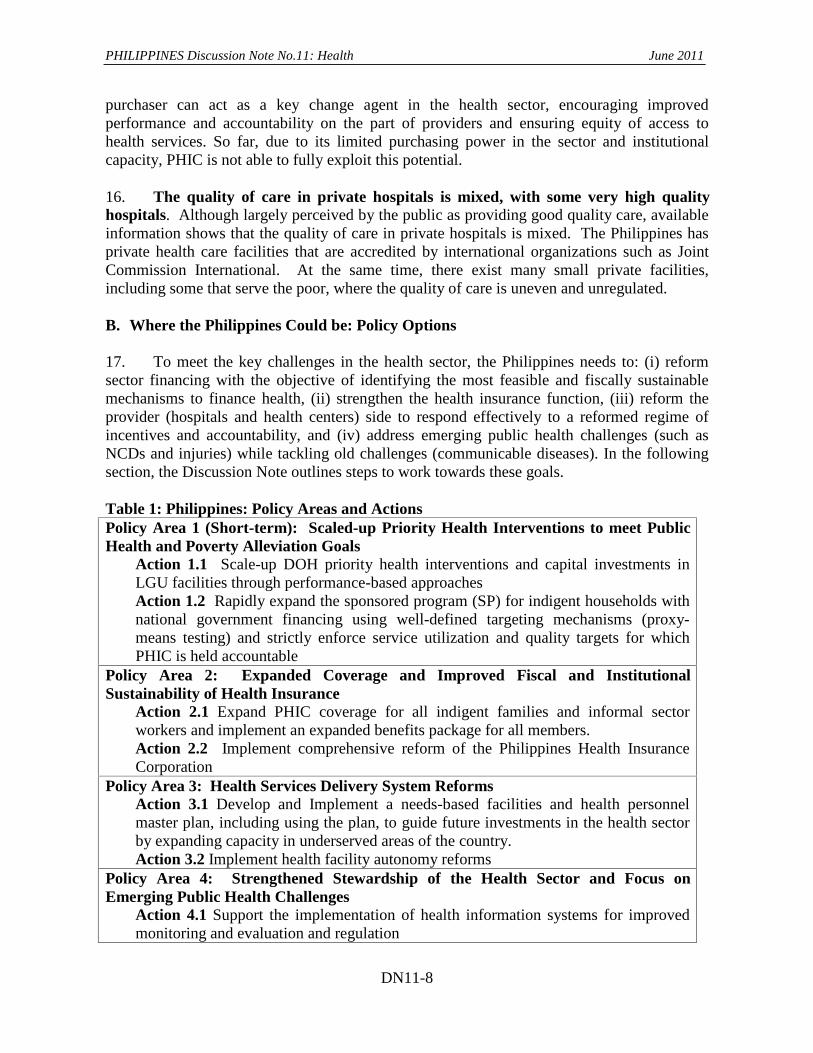

ABA-ROLI American Bar Association’s Rule of Law Initiative

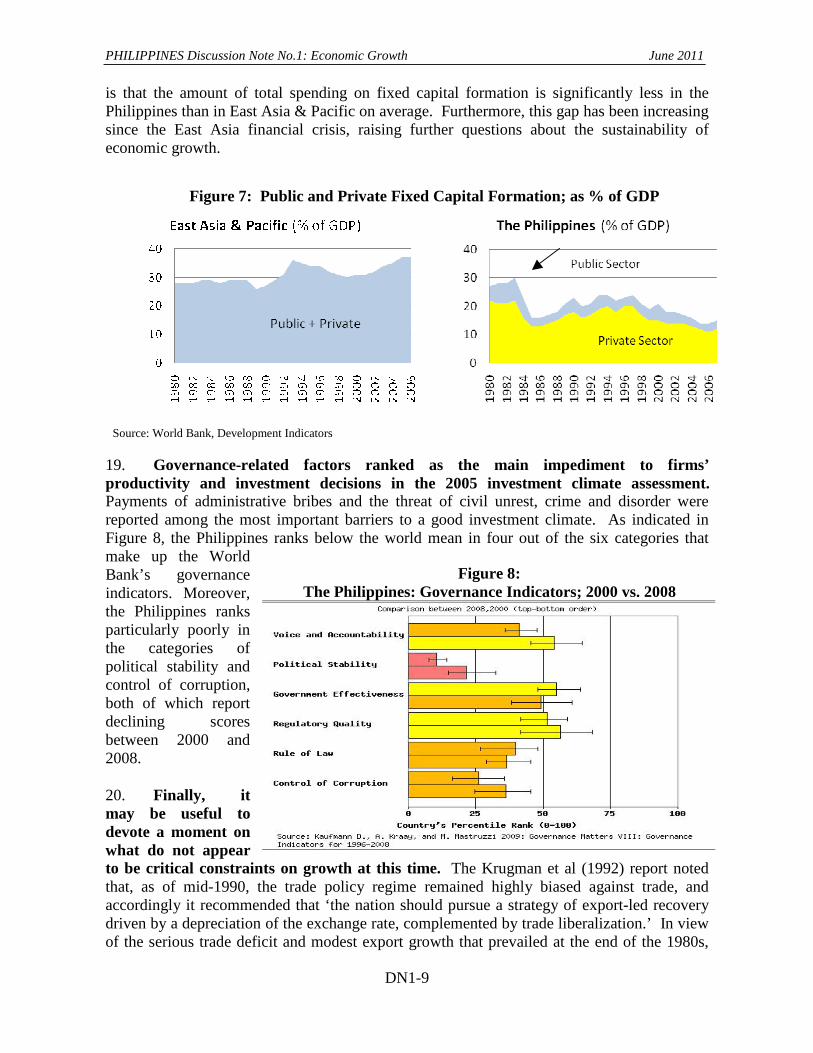

ACEF Agriculture Competitiveness Enhancement Fund

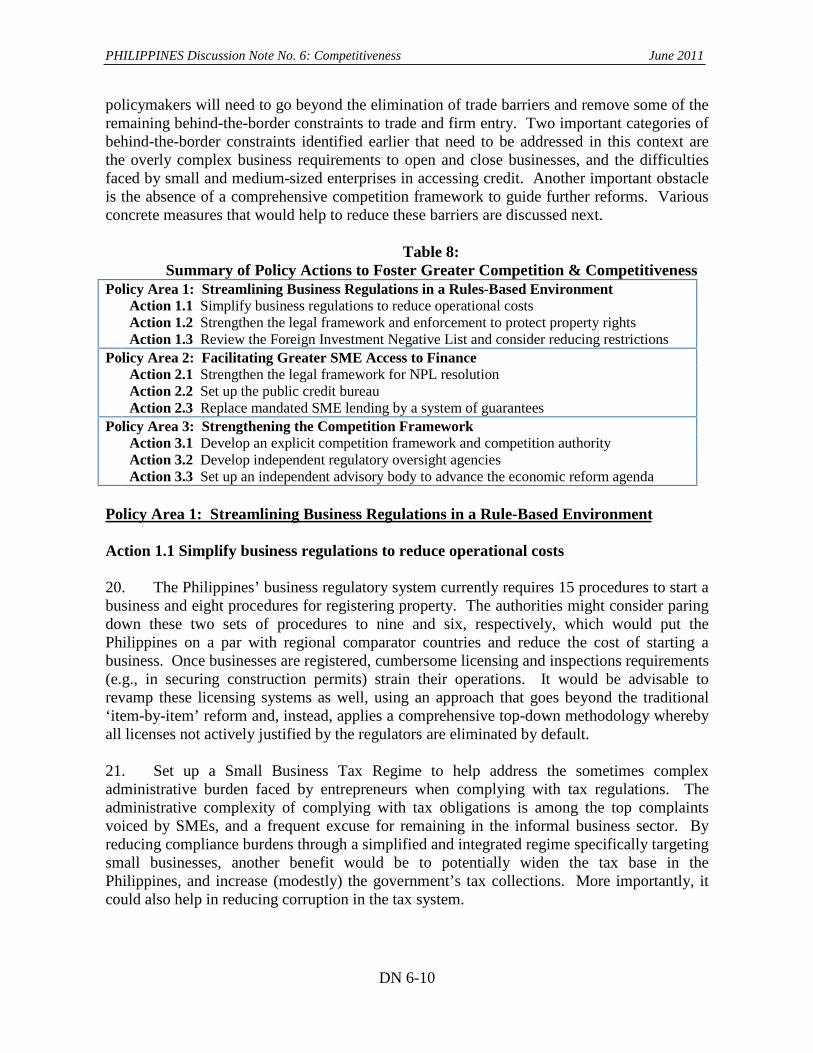

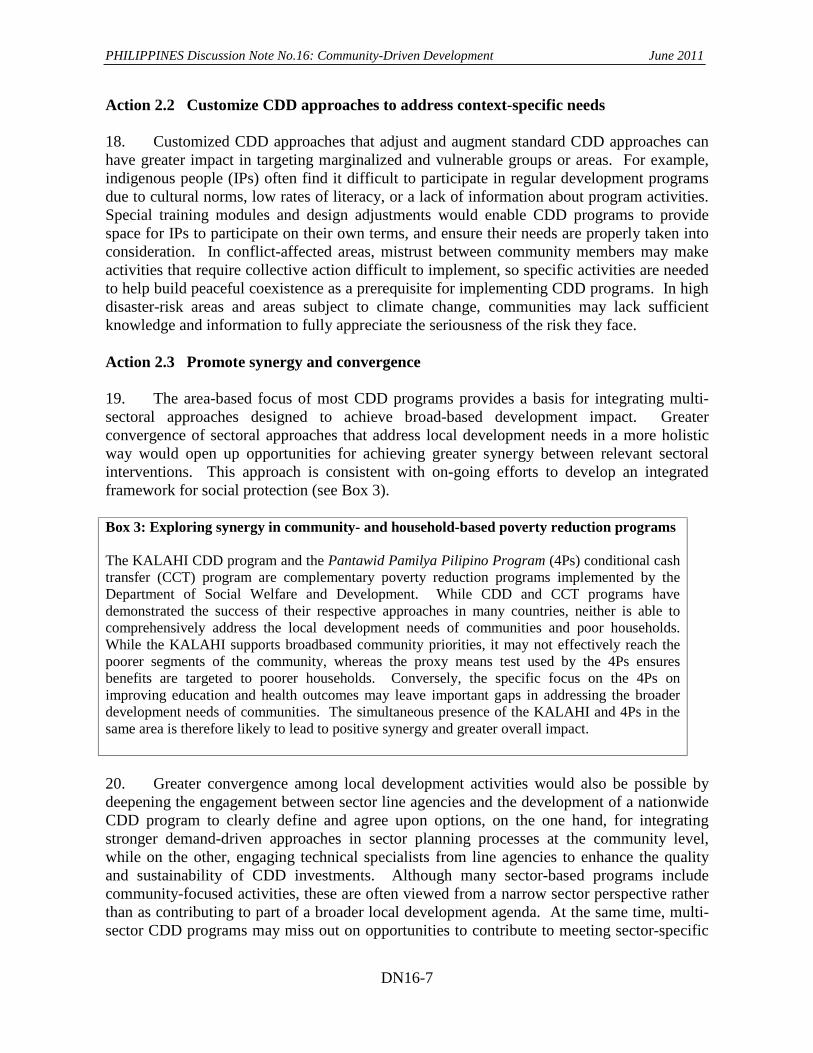

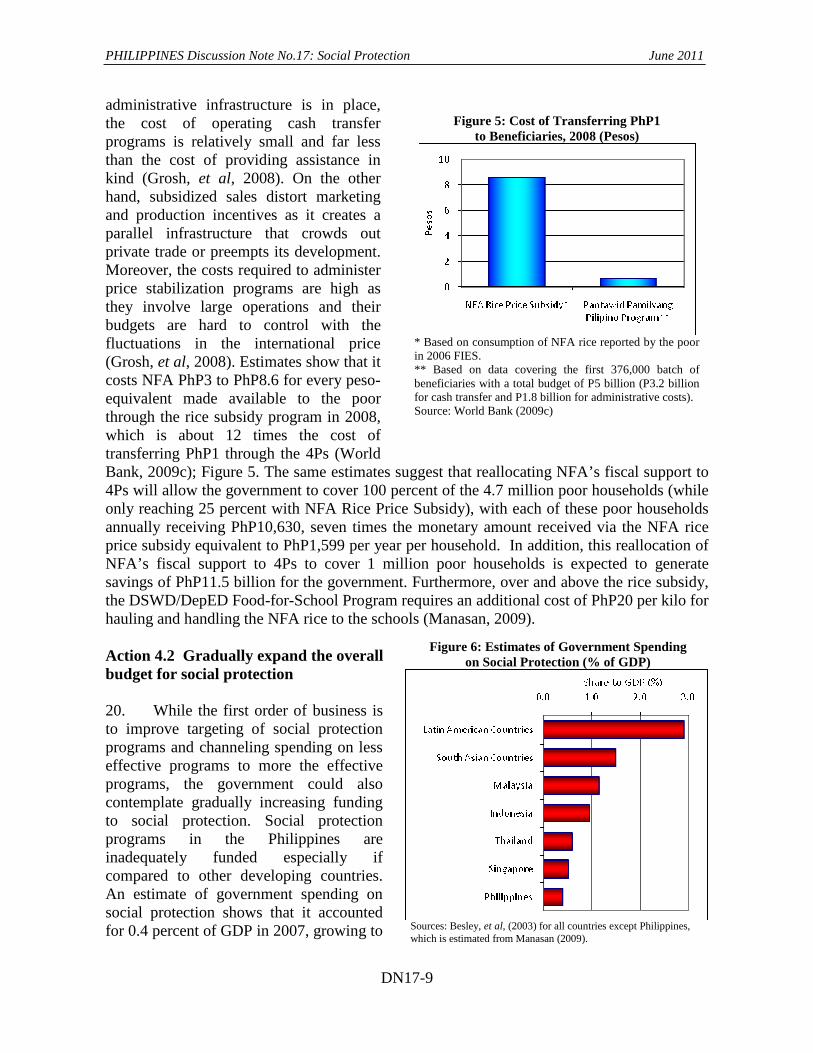

AFMA Agriculture and Fishery Modernization Act

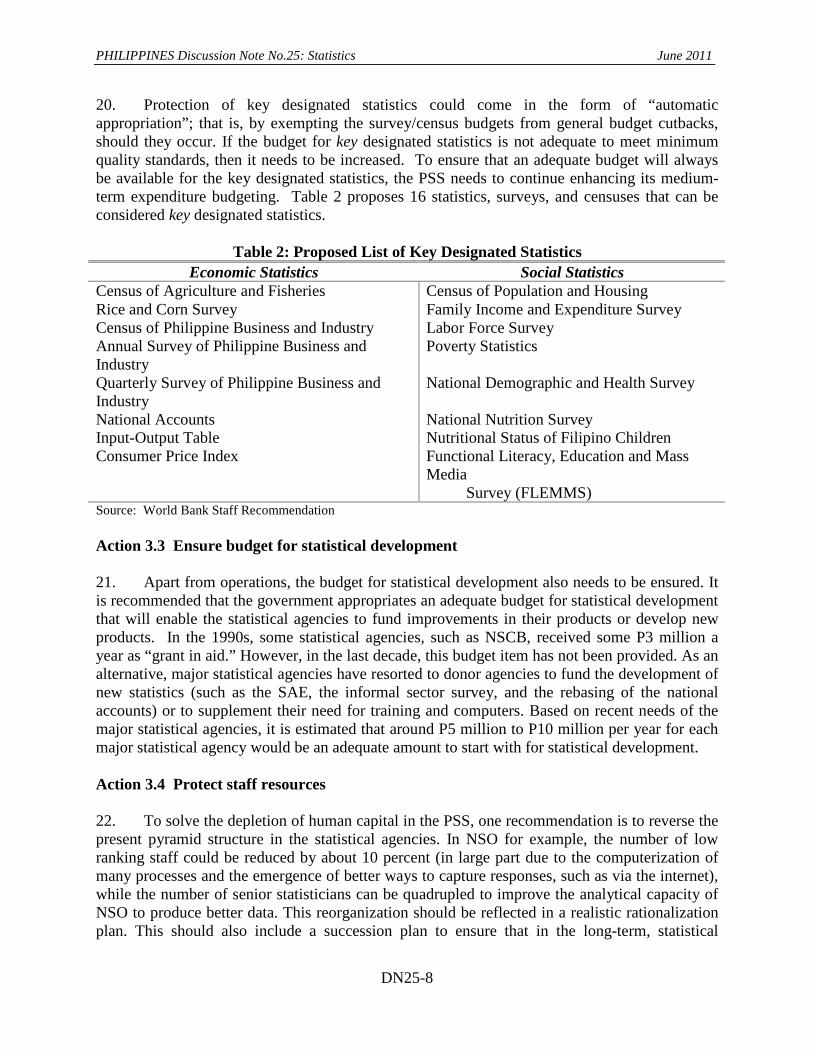

APIS Annual Poverty Indicator Survey APJR Action Program for Judicial Reform ARMM Autonomous Region in Muslim

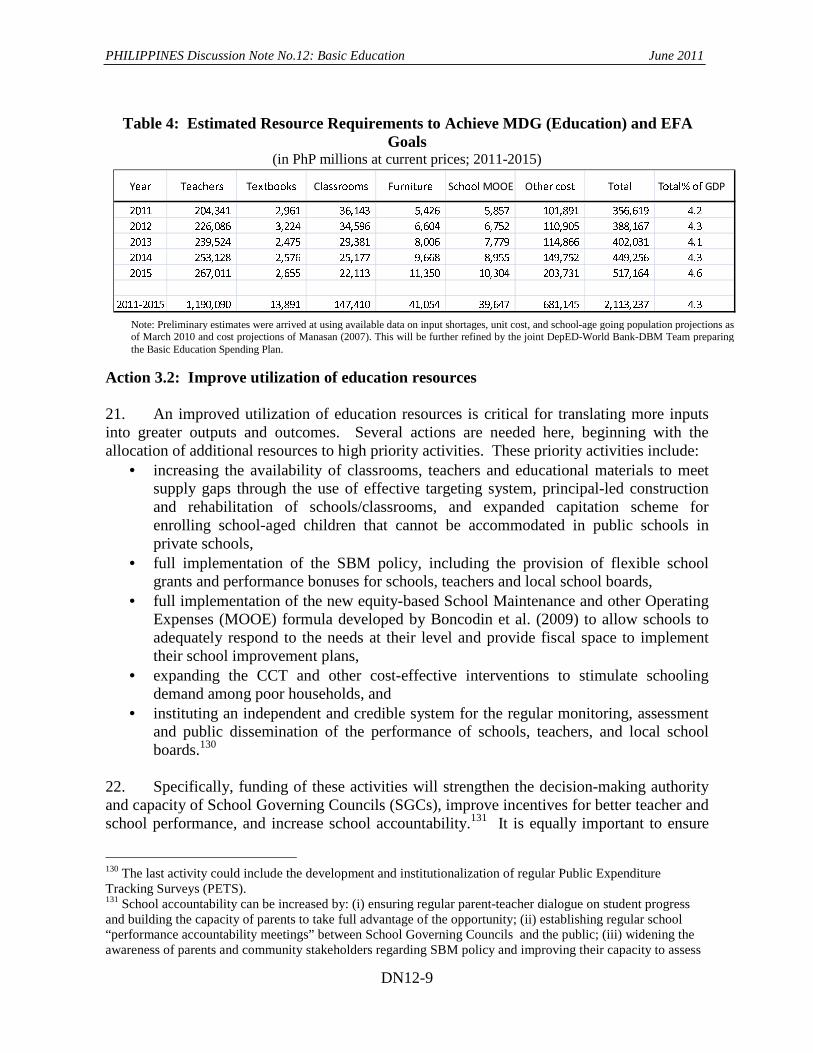

Mindanao BAS Bureau of Agricultural Statistics BEAM Basic Education Assistance for

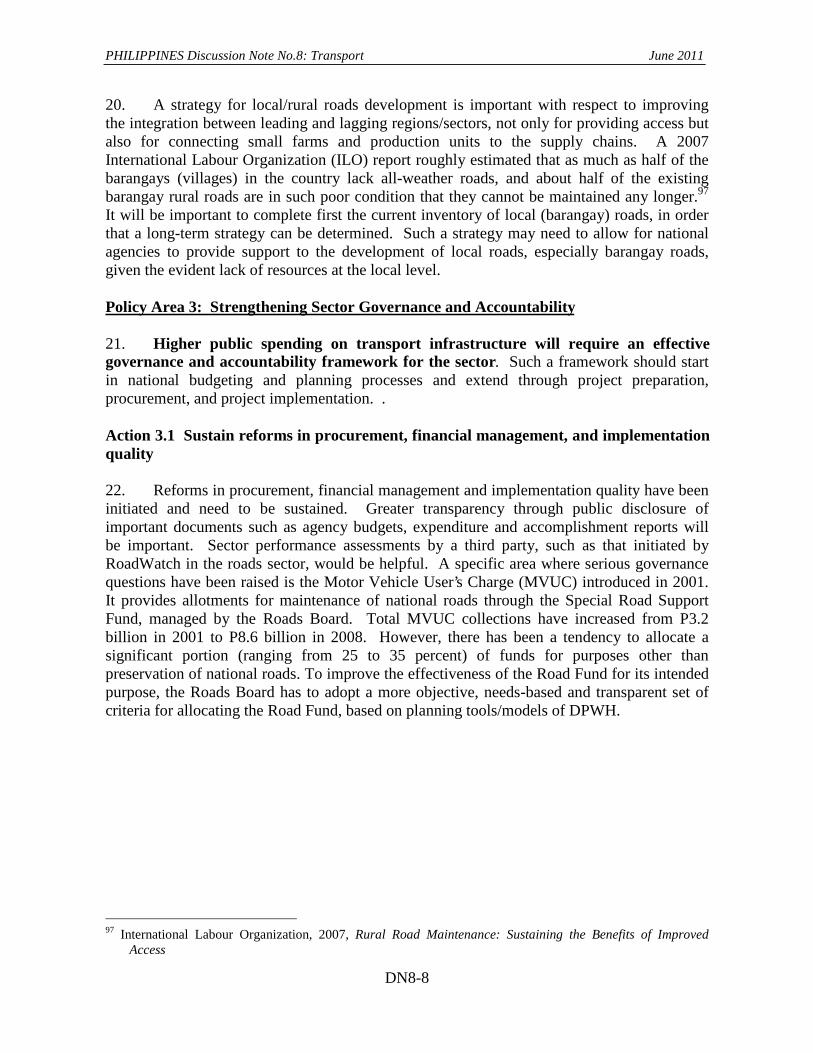

Mindanao BESF Budget of Expenditures and Sources

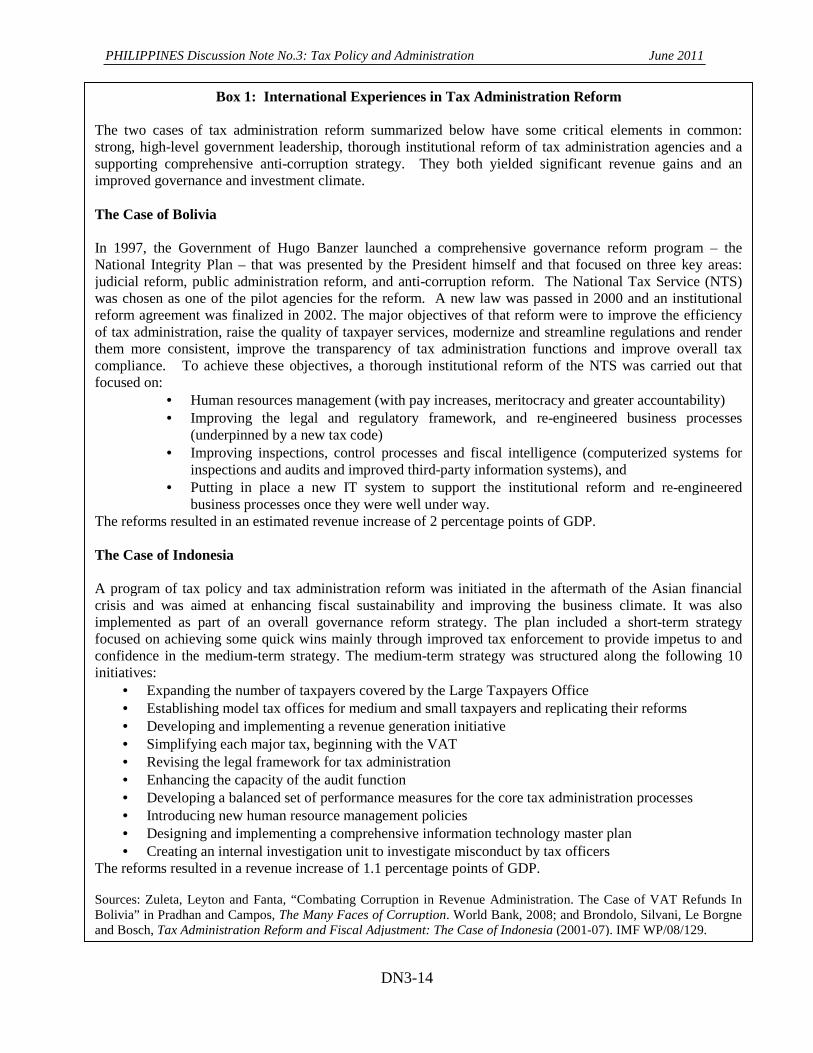

of Financing BIR Bureau of Internal Revenue BFAD Bureau of Food and Drugs BFAR Bureau of Fisheries and Aquatic

Resources BJE Bangsamoro Juridical Entity BLES Bureau of Labor and Employment

Statistics BOC Bureau of Customs BOD Burden of Disease BOT Build-Operate-Transfer BPAP Business Processing Association of

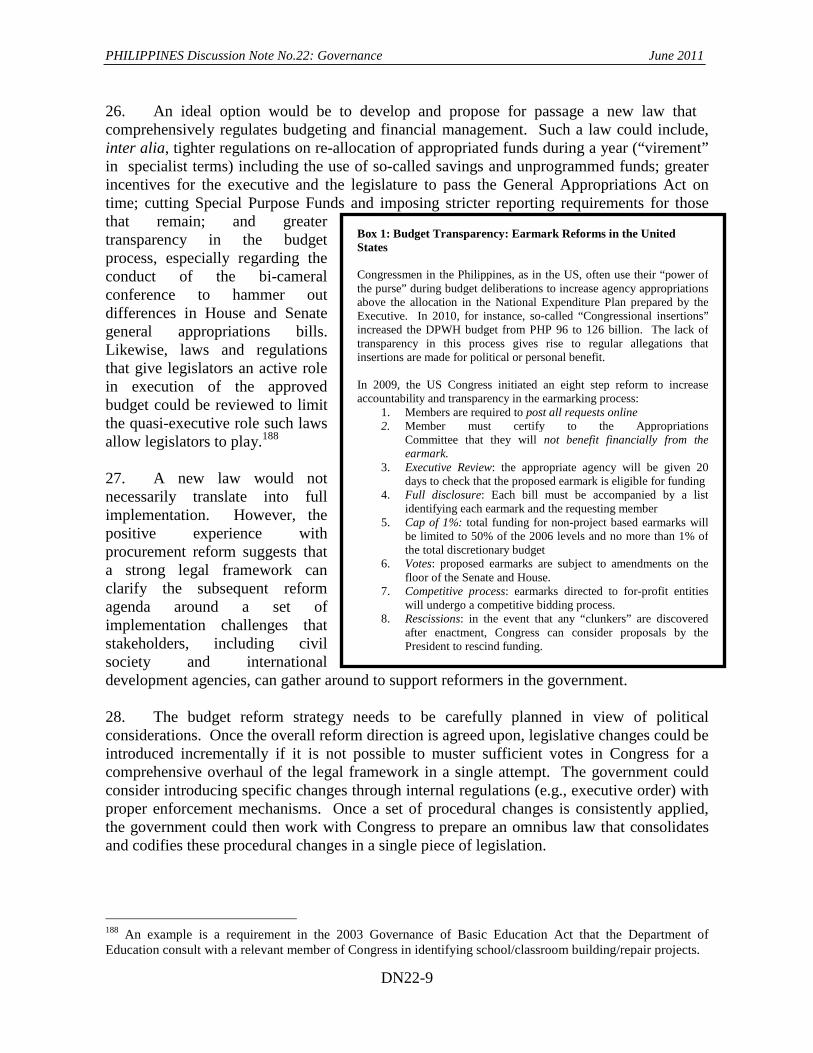

the Philippines BPO Business Process Outsourcing BSP Bangko Sentral ng Pilipinas CAAP Civil Aviation Authority of the

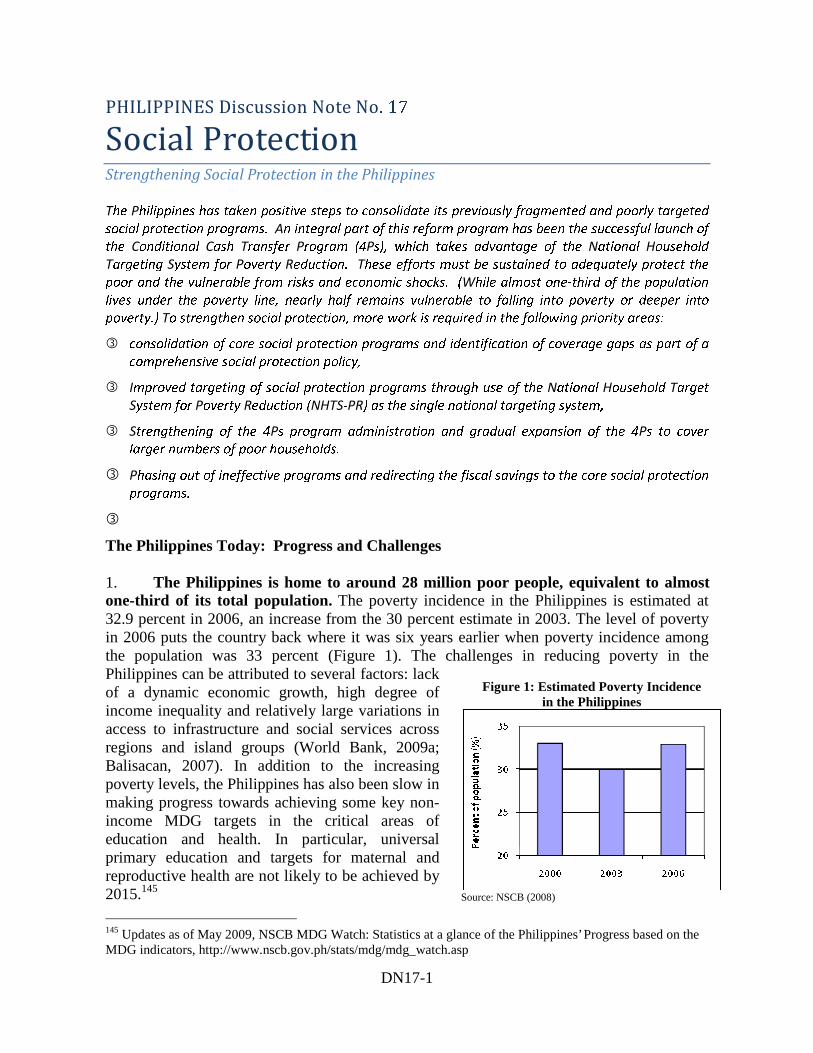

Information System CARP Comprehensive Agricultural Reform

Program CBA Cost-benefit analysis CBFM Community-Based Forest

Management CIT Corporate income tax CC Climate Change CCL Committee on Computerization and

Library CCT Conditional Cash Transfer CDD Community-driven development CDM Clean Development Mechanism CDS City Development Strategies CER Certified emission reduction CHED Commission on Higher Education CICT Commission on ICT CIIP Comprehensive and Integrated

Infrastructure Program

CIPHs City Investment Plans for Health CLUPs Comprehensive land use plans CMIS Case Management Information

System CO2 Carbon dioxide COA Commission on Audit CoST Construction Sector Transparency CPF Carbon Partnership Facility CSC Civil Service Commission CTF Clean Technology Fund CVOs Civilian Volunteer Organizations DA Department of Agriculture DAP Development Academy of the

Philippines DAR Department of Agrarian Reform DBM Department of Budget Management DENR Department of Environment and

Natural Resources DepED Department of Education DICT Department ICT DILG Department of Interior and Local

Government DMIA Diosdado Macapagal International

Airport DOE Department of Energy DOF Department of Finance DOH Department of Health DOJ Department of Justice DOLE Department of Labor and

Employment DOST Department of Science and

Technology DOTC Department of Transportation and

Communications DPWH Department of Public Works and

Highways DRRM Disaster Risk Reduction and

Management DSWD Department of Social Welfare and

Development EAP East Asia and Pacific EC Electric Cooperative e-CFM Enhanced Case Flow management ECPC Electronic Commerce Promotion

Council EFA Education-for-All EISP Enterprise Information Systems Plan EITI Extractive Industries Transparency

Initiative e-JOW Enhanced Justice on Wheels EMOC Emergency and Obstetric Care ENR Environment and Natural Resources EPIRA Electric Power Industry

Restructuring Act ERC Electricity Regulatory Commission ERR Economic rate of return ESC Education Service Contracting FAAP Federation of Accrediting Agencies

of the Philippines FAC Family Access Cards FDA Food and Drug Administration FIES Family Income and Expenditure

Surveys FLEMMS Functional Literacy, Education and

Mass Media Survey FMBO Financial Management and Budget

Office FOI Freedom of Information FSP Food-for-School Program FPA Final Peace Agreement FRI Financial Rehabilitation and

Insolvency FSI Floor-surface-index FSP Food-for-School Program GAA General Appropriations Act GCI Global Competitiveness Index GDP Gross Domestic Product GEF Global Environment Facility GER Gross enrolment rate GFDRR Global Facility for Disaster

Reduction and Recovery GFMIS Government financial management

information system GHGs Greenhouse gases GISP Government Information Systems

Plan GNP Gross National Product GOCCs Government-Owned and Controlled

Corporations GRS Grievance Redress System HEI Higher education institutes HDI Human Development Index HRH Human Resources for Health HSRA Health Sector Reform Agenda HUDCC Housing and Urban Development

Coordinating Council IBP Integrated Bar of the Philippines ICC Interagency Coordination

Committee ICOR Incremental Capital-Output Ratio ICG International Contact Group ICT Information and Communications

Technology IDPs Internally displaced persons IFC International Finance Corporation ILO International Labour Organization IMF International Monetary Fund IMR Infant Mortality Rate IMT International Monitoring Team

IP Indigenous people IPPUC Institute of Research and Urban

Planning of Curitiba IRA Individual Retirement Arrangement IRA Internal Revenue Allotment IRR Implementing rules and regulations IRRI International Rice Research Institute ISCED International Standard Classification

of Education ISPs Internet Service Providers ITES IT-enabled services ITU Internet User JCMS Judiciary Case Management System JRI Judicial Reform index JURIS Justice Reform Initiatives Support KALAHI-CIDSS

Kapitbisig Laban sa Kahirapan –Comprehensive and Integrated Delivery of Social Services

KDP Kecamatan Development Program KFR Kidnap-for-ransom LDF Local Development Fund LFS Labor Force Survey LGC Local Government Code LGU Local Government Unit LPI Logistics Performance Index LRT Light Rail Transport LRTA Light Rail Transport Authority LSMS Living Standard Measurement

Survey LTS Large taxpayers’ service LTFRB Land Transportation and Franchise

Regulatory Board LUCs Local Universities and Colleges LWUA Local Water Utilities Administration MA-TTRI Market Access Tariff Trade

Restrictiveness Index MDGs Millennium Development Goals MERALCO Manila Electric Company MeTCs Metropolitan Trial Courts MFIs Microfinance Institutions MILF Moro Islamic Liberation Front MISO Management Systems Information

Office MMR Maternal Mortality Rate MNLF Moro National Liberation Front MOA-AD Memorandum of Agreement on

Ancestral Domain MOOE Maintenance and other Operating

Expenses MPAs Marine protected areas MuTCs Municipal Trial Courts MVUC Motor Vehicle User’s Charge MRT Mass Rail Transit MRDP MISO Re-engineering and

Development Plan MSAs Major Statistical Agencies

MSME Micro small and medium-sized enterprises

MTEF Medium-Term Expenditure Framework

MTPDP Medium Term Philippine Development Plan

MT Metric Tons MWCI Manila Water Company, Inc. MWSS Metropolitan Waterworks and

Sewerage System NAIA3 Ninoy Aquino International Airport

Terminal 3 NAPC National Anti-Poverty Commission NAT National Achievement Test NCC National Computer Centre NCD Non-Communicable Diseases NCR National Capital Region NCBTS National Competency-Based

Teacher Standards NDCC National Disaster Coordinating

Council NDHS National Demographic and Health

Survey NEA National Electrification

Administration NEDA National Economic and

Development Authority NER Net Enrollment Rate NESTS National Environmentally

Sustainable Transport Strategy NFA National Food Authority NGAs National Government Agencies NGICS National Guidelines on Internal

Control Systems NGO Non-governmental organizations NGPC National Grid Company of the

Philippines NHIP National Health Insurance Program NHTS-PR National Household Target System

for Poverty Reduction NITC National Information Technology

Council NTS National Tax Services NPC National Power Company NPC-SPUG National Power Company Small

Power Utilities Group NPL Non-Performing Loans NSCB National Statistical Coordination

Board NSO National Statistics Office NSSHRP National Sector Support for Health

Reform Project NTC National Telecommunications

Commission NWRD National Water Regulatory Board OECD Organization for Economic Co-

operation and Development OFW Overseas workers OJTs On-the-job trainings OMB Office of the Ombudsman OOP Out-of-pocket payments OPIF Organizational Performance

Indicator Framework OPRCs Output and performance-based road

contracts 4Ps Pantawid Pamilyang Pilipino

Program PAGC Presidential Anti-Graft Commission PAMBs Protected Area Management Boards PCIC Philippine Crop Insurance

Corporation PDAF Priority Development Assistance

Fund PDP Philippine Development Plan PEFA Public Expenditure and Financial

Accountability PEP Philippine Environmental Policy PER Public Expenditure Review PESFA Private Education Student Financial

Assistance PETS Public Expenditure Tracking

Surveys PDNA Post-Disaster Needs Assessment PFM Public Financial Management PhilHealth Philippine Health Insurance

Corporation’s PHILJA Philippines Judicial Academy PHIC Philippines Health insurance

Corporation PIPH Provincial Investment Plans for

Health PIT Personal Income tax PLDT Philippine Long Distance Telephone

Company PMCO Philippines Mediation Centre office PMT Proxy-Means Testing PPA Philippine Ports Authority PPP Public-Private Partnerships PSALM Power Sector Asset and Liability

Management PSDP Philippine Statistical Development

Program PSNA Philippine System of National

Accounts PSS Philippine Statistical System QAAF Quality Assurance and

RHUs Rural Health Units RORO Roll-on-roll-off RTCs Regional Trial Courts SAE Small Area Estimates SALN Statements of Assets, Liabilities and

Net Worth SAOBs Statements of Allotments and

Obligations Balances SBM School-Based Management SBMA Subic Bay Metropolitan Authority SCC Small Claims Courts SCM Subsidies and Countervailing

Measures SC-MISO Supreme Court’s Management

Information System SDC Social Development Committee SDDS Special Data Dissemination System SEC Securities and Exchange

Commission SEP Self-employed professionals SGCs School Governing Councils SHI Social Health Insurance SIJ Strengthening the Integrity of

Judiciary SMEs Small and Medium-sized Enterprises SNAP Strategic National Action Plan SNITS Simplified Net Income Taxation

Scheme SP Sponsored Program SPFs Special Purpose Funds

SPSC Social Protection Sub-Committee SRTC Statistical Research and Training

Center SUCs State Universities and Colleges SWS Social Weather Station SZOPAD Special Zones for Peace and

Development Tariff-TRI Tariff Trade Restrictiveness Index TEEP Third Elementary Education Project TESDA Technical Education and Skills

Development Authority Telof Telecommunications Office TDRs Transferable Development Rights TFR Total Fertility Rate TIMMS Trends in International Math and

Science Study TRB Toll Regulatory Board TRO Temporary Restraining Order UMID Unified Multipurpose Identification UNESCO United Nations Educational,

Scientific and Cultural Organization UNFCCC United Nations Framework

Convention on Climate Change UPP Urban Poverty Program VAT Value-added Tax WESM Wholesale Electricity Spot Market WHSMP Women’s Health and Safe

Motherhood Project WMO World Meteorological Organization WTO World Trade Organization

Philippines Discussion Notes Challenges and Options for 2010 and Beyond

Table of Contents

DN No. OVERVIEW …………………………………………………………………..….….. i Economic Growth ...…………………..………………………………………..... DN 1 Poverty …………………………………………………………………………… DN 2 I. STABLE MACRO ECONOMY

Tax Policy and Administration …………………………………………….……. DN 3 Public Spending ……………..……………………………………..………….... DN 4 Fiscal Risk ………………………………………………………………………. DN 5

II. IMPROVED INVESTMENT CLIMATE

Competitiveness …………………………………………………………..…….. DN 6 Energy …………………………………………………………………………… DN 7 Transport ………………………………………………………………………… DN 8 Information and Communications Technology …………………………..….…. DN 9 Agribusiness …………..…………………………………….………………….. DN 10

III. BETTER PUBLIC SERVICE DELIVERY

Health …………………………………………………….…………………….. DN 11 Basic Education …..…………………........…………….……………………… DN 12 Higher Education ………………………....………………….………………… DN 13 Water and Sanitation ……………………………………………………..…….. DN 14 Urbanization ...…………………………………..……………………………… DN 15 Community-Driven Development. …………………………………………….. DN 16

IV. REDUCED VULNERABILITIES

Social Protection ………………………………………………………………… DN 17 Disaster Risk Management ……………………………………………………… DN 18 Climate Change …………………………………………………………….…… DN 19 Environment …………………………………………………………………….. DN 20 Peace and Development ……………………………………..…………………... DN 21

Philippines Discussion Notes Challenges and Options for 2010 and Beyond

OVERVIEW

INTRODUCTION 1. With the global economy on the way to recovery from the financial crisis, the Asian economies appear poised to bounce back strongly. For most people in the Philippines, however, a return to the status quo ante would offer little consolation. That is because when economic growth accelerated during 2002-08, poverty did not decline as hoped. With a third of the population currently below the poverty line, and high and rising inequality in incomes, the country’s main development challenge is to achieve growth that is much more widely shared—to make growth work for the poor. 2. The new administration that assumed office on June 30, 2010 faces significant opportunities as well as considerable challenges: an opportunity for new policy directions and new coalitions to push the development agenda forward with renewed vigor, but a need to overcome the inertial forces that slow down decision making and program implementation during a transition. These Discussion Notes have been prepared to help inform policy discussions in the period leading up to and following the 2010 elections. Their aim is to support the creating of a shared focus among government, civil society, business groups, and development partners on the key elements of a long-term development strategy focused on inclusive growth. Deliberately selective in their coverage, the Notes offer sectoral and thematic analyses to identify key challenges, and recommend a prioritized set of actions for consideration by the new government. The actions are consistent with the long-term strategy envisaged in the Notes and can in most cases be implemented immediately, building on successes. The analysis draws on extensive international experience and worldwide best practices, as well as past experience with what works well in the Philippines and what does not. 3. The vision underlying the Notes is one of inclusive growth, characterized by improved income opportunities and enhanced abilities of households and communities, especially the poor, to participate in markets through strengthened human capital, reduced vulnerability to shocks, and increased economic empowerment. While there are difficult choices to be made, the proposed actions could evoke strong support from key stakeholders, particularly from beneficiaries and front-line implementing agencies, as well as from development partners. KEY MESSAGES 4. For the Philippines, the main building blocks for achieving more inclusive growth are continued macroeconomic stability, an improved investment climate, better public services for the poor, and stronger protection against income shocks. An overarching challenge in the pursuit of development in the Philippines is to achieve better governance. The quality of

PHILIPPINES Discussion Notes: Overview June 2011

ii

governance is a recognized constraint on sustained growth and poverty reduction, and its improvement is a development goal aspired to by Filipinos in its own right. ¾ To maintain macroeconomic stability and cope with increased macroeconomic

uncertainty, special attention is needed to: • Strengthen the fiscal revenue base, • Improve public expenditure efficiency and targeting, and • Develop institutions for better fiscal risk management.

¾ To improve the investment climate it will be important to create an enabling business

environment by: • Promoting competitiveness, • Developing better models of infrastructure finance and management, particularly in

energy, transport, and information and communications technology (ICT) in unserved and under-served areas of the country, and

• Enhancing productivity and employment, especially in sectors of particular importance to the poor, such as agriculture.

¾ To increase the poor’s access to better public services it is important to:

• Deepen the reform agendas in key public services sectors such as basic education, health, and early childhood development, and

• Expand delivery of basic services such as water and sanitation, and urban services. ¾ To reduce vulnerabilities, actions are needed to:

• Expand and rationalize the country’s social safety net, • Engage in pro-active disaster risk reduction and management actions, and • Mainstream climate-change adaptation measures in policies, plans and programs and

expand climate-change mitigation programs in key sectors where emissions are on the rise.

¾ Good governance requires more capable and accountable government institutions at the

national, local, and agency levels. To develop such institutions requires actions to: • Strengthen core governance systems in public financial management, • Mitigate binding constraints that weaken LGU performance, including addressing

weak systems for LGU accountability, addressing hyper-fragmentation among LGUs, and improving LGUs’ resource bases, and

• Improve statistics and strengthen capacity of statistical agencies. PRIORITY POLICY ACTIONS 5. The 2006 household survey showed that though economic performance had improved since 2000, poverty reduction had not. Various factors explain the persistence of poverty, including slow economic growth and high inequality. Even though per capita GDP has been rising since 2000, real household incomes have been declining and considerable circumstantial evidence shows that income distribution has deteriorated, partly because of an

PHILIPPINES Discussion Notes: Overview June 2011

iii

unequal sectoral and regional distribution of growth, and partly because of barriers to factor mobility across sectors and regions. 6. To reduce poverty, faster economic growth is essential. Recent diagnostic studies point to three key constraints on growth in the Philippines: (i) a vulnerable fiscal situation, due largely to weaknesses in tax collection, (ii) inadequate infrastructure, particularly in transport and energy, and (iii) a weak investment climate, largely because of governance concerns. Reforms in these areas have been pending for a long time and it is difficult to envisage a sustained resumption of growth without major improvements in all three. 7. Eliminating these constraints is essential for restoring growth, but may not be enough for accelerating poverty reduction. Policymakers also need to be concerned about the distributional consequences of growth and ensure that it is sufficiently broad-based. This requires the removal of policy biases against low-skill labor employment and of barriers to factor mobility across regions and sectors. Such actions are needed to encourage the fastest growing sectors in the economy (such as manufacturing) to absorb more low-skilled labor (the poor’s main asset) and to encourage the most labor intensive sectors (such as agriculture) to grow faster and, thereby, generate more employment opportunities. These actions also are needed to allow workers to migrate from the slowest growing regions and sectors to the faster growing ones, thus maximizing their income earning opportunities. At the same time, actions are needed to upgrade workers’ human capital, enabling their participation in more productive activities.

I. Maintaining Macroeconomic Stability 8. The Philippines succeeded in maintaining macroeconomic stability despite the recent adverse developments associated with the global financial crisis. In 2009, as world GDP contracted, the Philippines’ GDP continued to grow by 0.9 percent, supported by private consumption spending that was partly fueled by remittance inflows and expansionary fiscal spending. Thanks to previous fiscal consolidation efforts, the government was able to undertake a countercyclical fiscal policy to address the economic slowdown. This has resulted in the largest fiscal easing in more than two decades. Meanwhile, prices have been stable and the balance of payments has remained strong throughout the past two years, also in large part due to the steady inflow of workers’ remittances. The economy is now recovering from the 2008-09 global recession, and the challenge will be to keep this recovery on track while the government mends its structural fiscal balance, which was weakened by the earlier countercyclical measures (a large part of which are permanent in nature), and while the central bank implements an exit strategy from its extraordinary crisis-related liquidity-support and easy monetary stance.

9. Aside from maintaining good macroeconomic management, the government also needs to address issues of medium and longer-term fiscal sustainability. To achieve sustained poverty reduction, access to essential public services needs to be expanded without jeopardizing fiscal stability. Policy actions to speed up economic growth will need to focus on strengthening tax policy and administration, significantly raising the public investment effort over the next five years, and improving governance to create a better climate for private investment.

PHILIPPINES Discussion Notes: Overview June 2011

iv

Improving public expenditure efficiency and targeting

10. The Philippines lags behind other East Asian countries in several key areas of economic and social development, largely because of its lower public spending on infrastructure development, education, and health. To achieve regional spending parity, the Philippines would have to increase public spending in these priority sectors by a combined 5 to 7 percent of GDP. In particular, public investment spending on infrastructure falls short of the regional average by 3 to 4 percent of GDP, while public spending on education and health falls short by 2 to 3 percent of GDP. This combined spending gap can be financed partly by strengthening public financial management and by eliminating large, ineffectual public subsidy programs. In this last regard, it is advisable to phase out the National Food Authority (NFA) rice subsidy and transfer part of the fiscal savings to the Conditional Cash Transfer (CCT) program. The fiscal savings achieved through these measures, however, will not suffice to close the entire spending gap. Moreover, since NFA is off-budget, the replacement of NFA spending by CCT spending would increase the central government deficit, even though it leaves the overall non-financial public sector deficit unchanged. Therefore, additional revenues on the order of 4 percent of GDP will also be needed to close this spending gap.

Strengthening the fiscal revenue base

11. The government will face an increased likelihood of a fiscal crisis if public expenditures are expanded without adequate increases in public revenues that reverse the decline in tax collection that has taken place since 2007. To raise revenues in the amount indicated above, the government has various options for improving tax administration and tax policies. There are some immediate actions that the government can take to raise revenues through improved governance in tax administration, such as (i) the adoption of performance indicators in the Bureau of Internal Revenues (BIR) and approval of the BIR’s rationalization plan, and (ii) obligating the public disclosure of all assets and net worth of BIR managers, accompanied by random audits. Other important reforms include actions to strengthen the BIR’s and BOC’s capacity to prevent smuggling and detect tax evasion. In this connection, the partial lifting of the bank secrecy law and outsourcing of key customs tasks to external contractors could yield major improvements in tax collection. Such tax administrative reforms, however, would not be expected to generate more than 1 to 2 percent of GDP in the best of circumstances. To close the spending gap identified earlier, therefore, some reliance on tax policy reforms is also likely to be needed. Reforms of the excise tax and VAT systems to increase yields offer “quick win” solutions because they could be introduced quite rapidly, raising revenues immediately and, on aggregate, equitably. Specific short-term measures that can be considered include: (i) raising excises on petroleum products, (ii) rationalizing and increasing excise taxes on tobacco and alcohol, (iii) broadening of the VAT base, reversing the progressive proliferation of exemptions that took place in recent years, and (iv) indexing all excise taxes to inflation. Beyond that, it is advisable to adopt more fundamental tax reforms, including reforms of the personal and corporate tax to improve their effectiveness and progressivity.

PHILIPPINES Discussion Notes: Overview June 2011

v

Developing institutions for better fiscal risk management

12. Macroeconomic stability is critical for poverty reduction, but easily undermined by external and internal shocks. To be sure, fiscal risks are large and diverse in the Philippines, but their poor assessment and management needlessly expose the country to immiserizing fiscal crises. Effective measures to mitigate these risks could be rapidly implemented. They include strengthening the legal and institutional framework for risk management, improving the management of public debt, and improving the analysis and dissemination of data on fiscal risks. Suggested policy actions include (i) establishing a dedicated Fiscal Risk Unit and a Debt Management Office in the Department of Finance (DOF), (ii) developing and publishing an explicit debt management strategy, and (iii) strengthening the Department of Finance’s Corporate Affairs Group.

II. Improving the Investment Climate 13. Strengthening the investment climate for more vigorous private sector development remains a key challenge in the Philippines. Policy reforms and programs are needed to increase competitiveness and improve governance in order to attract more investment and thereby raise labor productivity and employment. Major constraints on improving the investment climate include the lack of infrastructure, a weak regulatory framework and limited access to finance.

Promoting competitiveness

14. The Philippines can achieve much higher growth if it can tackle the long-standing bottlenecks that discourage private investment. While much progress has been made in eliminating trade barriers and improving trade logistics, the country has been less successful in reducing behind-the-border constraints, including the cumbersome procedures required to open and close a business, inadequate investor protection, and poor access to credit among small and medium-sized enterprises (SMEs). Consideration may be given to developing an explicit competition framework policy and implementing a series of measures designed to simplify business regulations within a transparent, rules-based business operating environment and facilitate greater access to credit for SMEs. Such measures include (i) expanding the scope, quality, and accessibility of credit information by setting up the public credit bureau, (ii) strengthening the legal framework for resolving non-performing loans, (iii) simplifying business regulations to reduce operational costs, (iv) developing an explicit competition framework and competition authority, and (v) strengthening the legal framework and enforcement mechanisms to protect property rights.

Developing better models of infrastructure finance and management

15. Expanding access to energy. Reliable availability of energy, including the elimination of brown-outs, is crucial to achieving a better investment climate in the Philippines. In the power sector the restructuring and liberalization of the electricity market sparked by passage of the Electric Power Industry Restructuring Act of 2001 has progressed well, but remains incomplete in several critical areas. This process needs to be brought to completion and a long-term debt management solution put in place to deal with the government’s sizeable

PHILIPPINES Discussion Notes: Overview June 2011

vi

contingent liabilities stemming from the Power Sector Asset and Liability Management (PSALM) finances. Meanwhile, the goal of universal electrification entails connecting over four million new customers. To achieve these goals, the authorities will need to (i) advance the private ownership/administration of power plants and manage the privatization of remaining National Power Corporation assets, (ii) accelerate transmission investment, (iii) reform the electric cooperative sector and address the issue of non-bankable electric cooperatives, (iv) take measures to lower operating costs, and (v) accelerate the development of renewable energy. 16. Improving transport infrastructure. Adequate transport infrastructure is another vital element for improving the investment climate and therefore economic growth, especially in an archipelago like the Philippines. Inland transport is deteriorating due to poor road conditions and weak intermodal integration. To meet these challenges does not simply require more public spending; it calls for greatly strengthened transport development planning, approached in an intermodal context, with a joint focus on trunk highways, ports, and airport development in relation to economic activity hubs and population centers. Much more attention also needs to be given to highway maintenance. Both sets of actions require a stronger policy presence at the national level to overcome the parochial interests at the local level, and a determined focus on strengthening governance and anti-corruption mechanisms in the sector. 17. Promoting ICT. Further development of the ICT potential in the Philippines can provide additional income-generating opportunities and help improve public service delivery. The ICT sector, including business process outsourcing, is already a significant and growing segment of the economy and policies can build on its strengths. Key policy areas for consideration include the establishment of clear sector leadership, reducing skills shortages to stimulate further development of IT-enabled services, improving access to broadband Internet particularly outside major cities, and using ICT to deliver public services in a more coordinated and cost-effective manner. Policy actions to consider are the (i) assignment of clear and accountable leadership for government-ICT/e-government, (ii) partial financing of ICT infrastructure through “smart subsidies”, (iii) leveraging of the government’s role as a major user of broadband Internet, and (iv) support of fast-track skills development programs in partnership with the private sector.

Enhancing productivity and employment

18. Because most of the country’s poor live in rural areas, robust agricultural growth and productivity increases will continue to be crucial to poverty reduction. There is much room for improving agricultural performance, and the sector has significant potential for income generation, job creation, and agro-business linkages. Critical constraints include a public policy and expenditure framework centered on the pursuit of food security with a particular bias in favor of rice, and the underdevelopment of land markets. Product diversification and improved competiveness are needed to support long-term growth in the agriculture sector and strengthen its linkages to agri-business activities. Policy areas for attention include reforming the rice-focused sector policy, ensuring more equitable access to land and addressing the barriers to competitiveness. Measures recommended for early action include (i) redirecting public expenditures away from subsidies (such as rice production support programs based on fertilizer and hybrid seed subsidies) to support services enhancing agribusiness

PHILIPPINES Discussion Notes: Overview June 2011

vii

competitiveness (e.g., market access and information, regulatory and supervision functions, extension services and research and development), (ii) developing a decentralized and participatory approach to agrarian reform, and (iii) ensuring security of land tenure.

III. Increasing the Poor’s Access to Better Public Services 19. The Philippines is lagging behind in several social sector Millennium Development Goals (MDGs), and improving access to and quality of public services for the poor remains a major challenge. The achievement of the MDGs is a shared responsibility of the national and local governments, and an improved coordination of activities is essential. Strengthened transparency, coordination and cooperation, and promotion of social inclusion and empowerment can lead to improved service delivery and outcomes for the poor. Better inter-agency coordination and institutional strengthening are also needed to realize greater synergy between anti-poverty initiatives in rural and urban areas.

Deepening the reform agendas in key public services sectors

20. Improving health outcomes. The ratio of health spending to GDP in the Philippines is one of the lowest in the region. Maternal and reproductive health indicators are among the worst in the region, and without concerted action, achievement of this MDG is at risk. The Philippines also has large income-related inequalities in health outcomes; for example, the infant mortality rate among the poorest quintiles is more than double that among the richest. Poor households rely most heavily on public health facilities, where the quality of care needs improvement and access in rural areas remains difficult. The problems in the health sector largely stem from excessive fragmentation in health financing and delivery, and a lack of clarity in stewardship responsibilities. Quick actions are needed to (i) scale up priority health interventions and capital investments in LGU facilities through performance-based approaches, (ii) rapidly expand the sponsored program for indigent households with national government financing using well-defined targeting mechanisms particularly the National Household Targeting System for Poverty Reduction-proxy means test, (iii) expand Philippines Health Insurance Corporation coverage for all informal sector workers and implement an expanded benefits package for all members, (iv) develop and implement a needs-based facilities and health personnel master plan, including using the plan to guide future investments in the health sector by expanding capacity in underserved areas of the country, (v) support the implementation of integrated health information systems for improved monitoring and evaluation and regulation, and (vi) integrate the prevention and control of non-communicable diseases in public health and primary care programs. 21. Delivering better education. For the poor, education is the single most important means of escaping poverty. The quality of education in the Philippines now trails behind a number of countries with substantially lower per capita income levels, and its poor net enrolment indicators jeopardize its chances of attaining the MDG in education by 2015. Increasing access to education for poor and marginalized groups will require better targeted programs and a greater reliance on partnerships with the private sector, while improving the quality of basic education will depend on a concerted implementation of critical reforms. In both cases, additional resources for basic education will be needed. In 2005, the government introduced a sector-wide program in basic education that seeks to improve the quality of

PHILIPPINES Discussion Notes: Overview June 2011

viii

schools in a decentralized environment. This program has yielded promising results and can be further strengthened. The most strategically urgent actions in this context are to (i) allocate the necessary budget to achieve universal primary education by 2015 and to expand secondary education enrolment, particularly for children from poor families, (ii) provide complementary support for the CCT program, (iii) expand private education, (iv) build public schools in areas with no nearby private schools, (v) improve the curriculum, and (vi) revise the system of performance incentives for teachers/principals. 22. Expanding early childhood interventions. Young children who participate in early childhood development programs that prepare them for school and address their health needs have lower school dropout rates and higher achievements from primary grades to adulthood. Currently, only 20 percent of eligible children are enrolled in pre-schools, which are severely constrained by a lack of facilities. Moreover, the inadequate financial protection against illness of most Filipinos also affects pre-school children. Measures need to be taken quickly to (i) facilitate public-private partnerships in pre-school education, (ii) expand national government-local government cost-sharing arrangements, (iii) provide universal health insurance coverage for children by mandating enrolment/coverage of all children under the age of six and ensuring zero or minimal co-payments for inpatient and outpatient care of these children, and (iv) enlarge the expanded program of immunization by providing government-subsidized vaccines, including the new vaccines of HiB and MMR, for all children.

Expanding basic service delivery

23. Expanding drinking water supply and sanitation. Although the Philippines remains on track to meet the MDG for access to improved water sources (94 percent) and improved sanitation (79 percent) in 2015, significant challenges remain in broadening access to continuous piped water supply while meeting national quality norms. After the successful privatization of Metro Manila water and sanitation services in 1997, progress has been slow in implementing a second round of reforms. These need to focus on the financing of water service providers and on streamlining institutional and financial arrangements to allow investments for improvements in services and expansion by local governments, water districts, and the private sector. Short-term actions to further these goals include (i) addressing the institutional fragmentation through consolidation of sectoral responsibilities at the central and local levels (ii) improving cost recovery for the water and sanitation services, and (iii) strengthening the regulatory capacity to ensure that the service providers are providing efficient and quality services. 24. Improving urban services. The Philippines is among the fastest urbanizing countries in East Asia. By 2009, urban centers accounted for 75 percent of economic output and 67 percent of households reside in urban areas. In Metro Manila and other large cities, the proliferation of slums, congestion, and exposure to man-made and natural risks reinforces a low level equilibrium that will prevent sustained economic growth. At the same time, the economies of agglomeration offer important opportunities to increase incomes, improve access to services and uplift the poor. Better urban development is needed, however, before these opportunities can be exploited. Four sets of actions that could advance the urban agenda in that direction are (i) establishing a forward-looking and ambitious national urban policy framework, (ii) developing and implementing a national slum upgrading program, (iii)

PHILIPPINES Discussion Notes: Overview June 2011

ix

revamping national and local systems and tools for urban development planning, and (iv) improving the human resource management frameworks for cities and metropolitan areas.

25. Addressing bottlenecks in local service delivery. Community-driven development (CDD) approaches are being successfully applied in the Philippines as part of efforts to enhance decentralized service delivery and improve local-level governance and performance, especially in poorer areas. The objective now is to expand the program coverage nationally, but there are challenges such as the possible duplication of approaches, the need to harmonize institutional arrangements, as well as ensuring adequate financing. The key action areas are the development of a roadmap based on an assessment of experience to scale up the CDD program nationwide, and the consolidation and rationalization of the “CDD platform” to achieve synergy and convergence for maximum impact.

IV. Reducing Vulnerabilities 26. A large proportion of the population in the Philippines is vulnerable to falling into poverty even as efforts continue to reduce the number of poor. In addition to the economic shocks that can affect income and employment, vulnerabilities are worsened by the risks stemming from climate-induced natural disasters and related impacts which disproportionately affect the poor. The sustainable management of environment and natural resources to safeguard livelihoods is critically important.

Expanding and rationalizing the social safety net

27. An estimated 33 percent of the population lives under the poverty line, up from 30 percent in 2003, and nearly half remain highly vulnerable to falling into poverty or deeper into poverty. To address these mounting challenges, programs and resources must be better aligned, targeted, and coordinated. The Philippines has begun to improve its previously fragmented and poorly targeted social protection programs. To sustain these efforts, speedy actions are required to (i) accelerate and enhance social welfare reform to develop an operational social protection strategy, (ii) improve targeting of social protection programs by adopting the National Household Targeting System for Poverty Reduction as the single national targeting system, (iii) further strengthen the operations of the CCT program, particularly through institutional strengthening of program administration, and broaden its coverage of poor households, (iv) eliminate ineffective programs and redirect resources to core programs to create fiscal space and to strengthen the social protection system, and (v) implement a secure unique identification system to facilitate better targeting of social programs. This can be achieved by reallocating funds to efficient programs from less efficient programs such as the NFA rice price subsidy program and the Food-for-School Program.

Engage in pro-active disaster risk reduction and management actions

28. For countries as vulnerable as the Philippines, natural disasters perpetuate many of their development challenges, including the proliferation of slums and heavy congestion in urban areas, inadequate infrastructure, and environmental degradation. The government has introduced a policy framework for dealing with natural disasters that emphasizes prevention and mitigation measures, but it needs a strategy that will expand the cost-sharing role of the

PHILIPPINES Discussion Notes: Overview June 2011

x

private sector, particularly the insurance industry. Priority actions include the (i) fast-track completion of risk assessments to determine which areas are most at risk from natural disasters so that future interventions can be well targeted, (ii) review of the capacity and upgrading of the weather forecasting and early warning systems for highly exposed localities, (iii) use of urban areas (such as Metro Manila and other economic centers) as geographic starting points to package risk reduction investments, (iv) adoption of a catastrophe risk finance strategy that will reduce fiscal exposure, and (v) empowerment and encouragement of LGUs to undertake priority disaster risk reduction investments by providing them with affordable and accessible financing options.

Mainstreaming climate change adaptation measures and expanding mitigation programs

29. Adaptation to climate change is particularly critical for the Philippines, given the country’s high vulnerability to impacts including sea-level rise and extreme weather events such as intense typhoons and changes in rainfall patterns that exacerbate floods and droughts. The Philippines has adopted active legislative and institutional responses to climate change issues, but is still building up its organizational structure and capacity in this area and lacks an operational strategy to respond to climate change. With the Climate Change Act of 2009 as the legal basis, the new administration is in a good position to strengthen the Philippines response to climate change by (i) implementing the new Climate Change Act and strengthening institutions and coordination, (ii) mainstreaming adaptation and disaster preparedness activities in policies, plans, and programs at the national, sub-national and sectoral levels, (iii) developing financing facilities for adaptation and disaster response, and (iv) selectively implementing mitigation programs in key sectors (energy, transport, waste management) where emissions are on the rise.

V. Good Governance 30. The new government’s reputation and legacy will be largely determined by its record in improving governance and reducing corruption. For the most part, strong regulatory and institutional frameworks for good governance and anti-corruption are already in place. The country’s active civil society and media are strengths that can be leveraged. And bright spots such as procurement reform show that positive change can be achieved when sound laws are combined with strong institutional backing and meaningful civil society participation. For the new government, an appropriate strategy would be to build credibility and public confidence through “quick wins” in order to lay the foundation for longer-term change. Short-term actions that could achieve this objective are the (i) resolution of high-profile graft cases, (ii) putting forward a Freedom of Information Act for legislative approval, (iii) voluntary disclosure of financial information by high level policymakers, and (iv) the launch of a comprehensive reform plan in a strategically selected agency that is widely perceived to be corrupt. These short-term measures would build political capital for the government to tackle more fundamental longer-term reforms.

PHILIPPINES Discussion Notes: Overview June 2011

xi

Strengthening core governance systems in public financial management

31. Improving public financial management (PFM) is critical for making progress towards the Philippines’ development goals and is also a core element of the governance reform agenda. For both these reasons, a fundamental reform of PFM should be a high priority for the government. Although the PFM system in the Philippines is reasonably capable of maintaining overall fiscal balance, it is not a good tool for efficient execution of priority policy programs and is particularly weak in transparently accounting for how taxpayers’ money has been spent for public purposes. By launching a comprehensive PFM reform program to enhance transparency, accountability, and efficiency in budget and financial management, the government could immediately signal its commitment to strengthen governance as a decisive step away from “business as usual.” Two important steps that can be taken immediately in this direction are to (i) announce a comprehensive PFM reform program as a centerpiece of the government’s governance reform agenda, and (ii) launch a coordinated project to build a government financial management information system. If sustained over time, the reform would build institutional capacities to implement priority programs efficiently and accelerate development.

Improving decentralization

32. The pace of progress on decentralization—in particular, strengthening local governance—needs to be hastened to address the enormous challenge of poverty reduction in the country. All LGUs, regardless of level or size, need to be able to provide minimum basic services to their citizens, while major cities and metropolitan areas need to assume more ambitious roles as engines of economic growth and development. Local government performance is held back by several binding constraints, among them weak systems for LGU accountability, a high level of fragmentation among LGUs, and inequities in the LGUs’ resource base. Several intermediate policy options could help make decentralization work better in the Philippines: (i) strengthening LGU accountability by clarifying service delivery responsibilities and by improving budget transparency and performance reporting, (ii) mitigating the excessive fragmentation by optimizing the role of provinces in inter-LGU coordination and by integrating barangays into the local councils, and (iii) improving LGUs’ resource base by considering options for utilizing additional fiscal transfers allocated based on objective criteria, such as LGU performance and equalization factors. CONCLUSION 33. Making growth work for the poor in the Philippines is a significant development challenge, but one that is worth pursuing vigorously. The new administration not only has the mandate but the historic opportunity to deliver on this goal as well as other election platforms on which it was voted to power. These include “the organized and widely-shared rapid expansion of the economy through a government dedicated to honing and mobilizing the people’s skills and energies as well as the responsible harnessing of natural resources; moving to well-considered programs that build capacity and create opportunity among the poor and the marginalized in the country; policies that create conditions conducive to the growth and

PHILIPPINES Discussion Notes: Overview June 2011

xii

competitiveness of private businesses, big, medium and small; and making education the central strategy for investing in people, reducing poverty and building national competitiveness.” In addition, the new administration is committed to fight corruption. These goals are fully echoed in the strategy and policy actions identified above and elaborated in the accompanying Discussion Notes.

DN1-1

���������������������������������������������Restoring Faster Growth after the Crisis

T AA

PT

T P

T P

R

R

MT

WTO HI

1. The global financial and economic crisis that erupted in 2008 paralyzed the world’s financial markets, triggered a dramatic deceleration of international trade and resulted in the greatest contraction in world GDP since the 1930s. Although the crisis had its epicenter in the developed economies, its tremors reverberated deeply across the developing world. The Philippines was not spared. Its exports dropped by almost 20 percent in 2009 and real GDP growth fell from 7 percent in 2007 to an estimated 1.0 percent in 2009; that is, growth became negative once again in per capita terms. 2. The world economy has begun to recover and Asia appears poised to emerge from the recession both faster and stronger than other regions. Reestablishing the status quo ante, however, would provide little consolation for the Philippines. Even before the onset of the crisis, its per capita GDP had only been growing at a modest pace compared to the rapid expansion observed in neighboring countries, indicating the existence of important barriers to growth. 3. There is also a risk that the post-crisis external environment facing the developing countries may be less hospitable than before. One major difference is that the general revaluation of financial risks triggered by the crisis will result in a reduction in the total amount of cross-border lending and costlier terms, even after financial markets have

PHILIPPINES Discussion Note No.1: Economic Growth June 2011

DN1-2

fully stabilized. The crisis also laid bare important imbalances in the world economy –epitomized by the huge trade deficits incurred by the United States, financed by equally huge trade surpluses in China and Germany – that no longer appear sustainable. Eliminating these imbalances will slow down the growth of world trade, as consumers in the United States begin to save more and governments everywhere phase out their countercyclical stimulus packages to prevent inflationary pressures from building.1 Although the shape of the recovery from the global crisis (be it U, V, W or L) is still being debated, a consensus is emerging that the post-crisis world GDP will evolve along a more moderate trend line than before. 4. The new post-crisis external environment poses a particular challenge for the Philippines, where the low economic growth has been a long-standing problem. The rate at which economies grow largely depends on their capacity to structurally transform themselves away from engaging in traditional, less productive activities toward modern, more productive activities, which largely involve tradable products. As discussed below, the Philippines already had been having difficulties in achieving this transformation long before the onset of the global crisis. The challenge facing Philippine policymakers now is to accelerate this transformation at a time when the world economy may be less capable or willing to absorb the increase in tradable products that would result from this transformation. The outward-oriented development model that has characterized the fastest-growing developing economies since the 1960s still offers the best prospects for faster development in the Philippines, even though the rewards from applying that approach may not be as high as before. Why is growth so important? 5. In 1960, the Philippines was one of the most developed economies in Asia, with a per capita GDP that was roughly twice the per capita GDP of Thailand at the time.2

Today this relation is reversed, with Philippine per capita GDP only one-half that of Thailand’s. Similar reversals also emerge in comparisons with other middle-income economies in East Asia, such as Indonesia, Malaysia and most notably, China. This pattern is explained, of course, by the differences in the speed of economic growth, which permitted per-capita GDP to increase since 1960 by a factor of 19 times in China, 8 times in Thailand, and 6 times in Malaysia and Indonesia, but only by 2 times in the Philippines. While the other East Asian economies were growing at annual rates between 3.6 and 6 percent in per capita terms over 1960-2008, the Philippines only managed to grow at an average rate of 1.4 percent over this period. This meant that living standards in the other large East Asian economies have been rapidly catching up with the living standards in the industrialized OECD economies (whose per capita GDP growth averaged 2 percent), while the Philippines was progressively falling further behind. 6. This is also the main reason why the progress made in poverty reduction has been so slow in the Philippines. Using the $1.25-a-day income threshold measure of

1 Another widely feared consequence of the crisis had been the possible decline in foreign remittances, which are particularly important for the Philippine economy. Though remittance inflows have not declined in 2008 and 2009, their growth has decelerated significantly and is projected to remain at more moderate rates than before. 2 All GDP figures are measured in constant (2000) US Dollars as reported in the World Bank’s Development Data Platform.

PHILIPPINES Discussion Note No.1: Economic Growth June 2011

DN1-3

poverty, the Philippines succeeded in reducing poverty from around 30 percent in the early 1980s to just over 22 percent at the end of the 1990s. Though not negligible, this is modest compared to achievements elsewhere, with the result that the poverty rate for the East Asia and Pacific region as a whole is now below the Philippine rate, even though it was nearly twice as high just two decades ago.3

7. Per capita growth had picked up in the Philippines in the decade leading up to the global crisis, averaging 2.8 percent per annum during 1999-2008. While this offers the prospect of eventually catching up with the developed economies, the pace of convergence would be excruciatingly slow: at this rate, it would take the Philippines over 200 years (or about 10 generations) to reach the average per capita GDP of the OECD countries. China and India, which have been growing at rates of 8 and 5 percent per capita during the last 10 years, have a chance to catch up within only 25 years to 50 years if they can keep this up. Why has the Philippine economy not been growing faster? 8. From a sector development perspective, there are basically two ways to increase per capita GDP: one is by raising the productivity of workers within sectors and the other is by reallocating workers (and other factors of production) across sectors, away from those exhibiting low productivity and toward those with higher productivity.4 In the post-World War II period, the sectors with high productivity worldwide have tended to be those that produce tradables, and within this category, it is generally the industrial goods –though tradable services are becoming increasingly more important. The least productive sectors, in turn, have tended to be associated with traditional agriculture and the informal services sectors. This sector ranking by labor productivity is also observed in the Philippines, where the Industry sector is the most productive, followed by Services and Agriculture as the least productive; Figure 1. Historically, the most rapidly growing developing economies have been those that were able to shift their labor force from the agriculture sector to the industry sector

3 While economic growth is widely regarded as a necessary condition for poverty reduction, it is not sufficient. This was made most evident in 2003-2006, when poverty indicators in the Philippines failed to decline even though GDP growth had picked up significantly. This suggests that the benefits of growth during that period were not being widely shared. Rather, the increase in economic growth appears to have been accompanied by a significant deterioration in the distribution of income and consumption. This issue is addressed in a separate Discussion Note. 4 A third way is by raising the ratio of workers to population, either through increased labor participation or reduced dependency ratios, but there are natural limitations to the potential growth impulse arising from this source.

Source: World Bank, based on Labor Force Survey

PHILIPPINES Discussion Note No.1: Economic Growth June 2011

DN1-4

without sacrificing the latter’s labor productivity levels.5

9. The Philippines has had difficulties achieving this structural transformation compared to the other East Asian countries. Although its share of total employment devoted to Agriculture has continued to decline over the last 20 years (Figure 2), the share of labor released from that sector has not been absorbed by industry. Rather, this labor was entirely absorbed by the Services sector, which displays significantly lower labor productivity levels than Industry. Had the labor that was released from Agriculture been absorbed by Industry, annual economic growth in the Philippines would have been around 0.7 percentage points faster; see Technical Annex (Scenario B). At the same time, the levels of labor productivity growth within each sector have remained largely unchanged (Figure 1), except for a surge after 2002, which largely reflects temporary increases in capacity utilization during the economic expansion of 2003-2007.6

Source: World Bank, Development Data Platform Source: World Bank. Development Data Platform

10. One manifestation of this uneven structural transformation is the slow growth of industry sector employment. The other East Asian economies were able to absorb the

5 In this discussion, the reference to industrial activity serves as a proxy for non-traditional, technologically more advanced production. Although such production also includes technologically sophisticated agricultural and service sub-sectors, most of it has tended to be concentrated in the Industry sector. The focus on Industry, therefore, is entirely due to limitations in the classification of data, which is only readily available in the traditional Agriculture/Services/Industry disaggregation. 6 Had sector productivity growth rates in the Philippines been as fast as in other East Asian countries (Technical Annex, Scenario C), overall annual output per worker would have grown 2 percentage points faster.

Figure 2: Philippines: Employment shares by sector (%)

Source: National Statistics Office (NSO), Labor Force Surveys.

PHILIPPINES Discussion Note No.1: Economic Growth June 2011

DN1-5

workers released from their primary sectors at a much faster pace than the Philippines; Figure 3. Between 1980 and 2005, the Philippines managed to double the size of its industrial labor force, but the other middle-income economies in the region almost tripled theirs. At the same time, the other economies were also able to increase labor productivity within manufacturing at a much faster pace than the Philippines; Figure 4. That is, they succeeded, both, in transferring more workers into the industry sector and in continually raising the level of productivity within the sector. In doing so, they have been able to achieve significantly higher rates of economic growth. 11. What makes tradables or industrial production, in particular, so special for growth? Empirically, the expansion of such activities is closely associated with faster economic growth; see, e.g., Rodrik (2009). There are at least two schools of thought on why tradables are important for growth: one focuses on the act of trading and the other focuses on the act of producing tradable goods and services. The first viewpoint holds that there are learning or other spill-over effects from exporting because of technological or marketing externalities that are created when exporters have to compete abroad. This makes tradables special, of course, since non-tradables cannot be exported. The second viewpoint holds that the production of tradables is special, independent of whether the products are exported or displace imports. The starting premise here is that a number of different activities with different marginal productivities coexist within developing economies at any given time. In this context, as more workers shift from low-productivity to high-productivity activities, GDP increases independent of whether the goods produced are sold domestically or abroad.7 Even in the absence of technological externalities from export activities, however, it is difficult to envisage a significant expansion of tradables production in the absence of export markets, given the limited size of the Philippine domestic market for achieving economies of scale.

7 A recent empirical study (Rodrik, 2009) finds that while economic growth is positively correlated both with the GDP-share of industry and the share of exports, the former relationship is stronger and more robust that the latter. Insofar as the post-crisis external environment is less accommodating of trade surpluses, this is good news for the growth prospects of newly industrializing economies. It does not, however, provide support for pursuing an inward-oriented industrialization strategy.

PHILIPPINES Discussion Note No.1: Economic Growth June 2011

DN1-6

TS G E A

C

OO

P FW C E P

P

IMTA PHL

D PHL S B B S C T E G A U W D C T B I N P

12. From a factor accumulation perspective, the slow growth exhibited by the Philippines relative to other economies in the region is explained both by a low rate of physical capital accumulation and a low rate of total factor productivity growth. As shown in the last row of Table 1, the average annual growth of output per worker in Indonesia, Malaysia and Thailand over the period 1990-2003 was 2.3 percent higher than in the Philippines. About two-thirds of that difference (1.6 percent) was due to faster physical capital accumulation and the remainder (0.7 percent) was to due higher total factor productivity growth.8 Differences in human capital accumulation, on the other hand, do not appear to have played a significant role. Identifying the main constraints on growth in the Philippines 13. The factor accumulation approach draws attention to the low level of investment in physical capital as a key difference in the rapid growth observed in other countries in East Asia compared to the Philippines. This suggests that the problem of slow growth may be due to inadequate public investment and a poor investment climate for the private sector. The sector development approach, in turn, draws attention to the slow pace of structural transformation in the economy. This suggests that there may be barriers to factor mobility across sectors, either in the form of labor market rigidities, capital market distortions or anti-competitive practices that are preventing a more fluid market entry and exit of firms. 14. To help identify the most binding constraints on growth, consider the assessment of the Philippine economy prepared by a team of economists led by Paul Krugman in

8 The difference in total factor productivity growth happens to be very close to the growth foregone on account of the incomplete structural transformation in the Philippines; see Technical Annex. That is, had the Philippines been able to fully absorb the labor released by Agriculture into the Industry sector, it would have been able to close about one-third of the average growth gap vis-à-vis its three regional neighbors.

PHILIPPINES Discussion Note No.1: Economic Growth June 2011

DN1-7

the early 1990s; Krugman et al (1992). It noted significant problems in several areas, especially the presence of high protectionist barriers in manufacturing, a low public revenue base and inadequate investment in public infrastructure.9 Such an economy, the Krugman team concluded, could only count on a very low growth rate – perhaps as low as three percent – barely keeping up with population growth. This turned out to be a prescient observation, as annual GDP growth averaged 3.3 percent over the decade that followed; Table 1. 15. A review of economic developments in the Philippines since the early 1990s reveals that some progress has been made in a few problem areas identified by the Krugman et al (1992) report, but many others remain as relevant today as they were two decades ago. A number of recent diagnostic studies10 have identified the following key constraints on growth in the Philippines: (i) a very vulnerable fiscal situation due largely to a very low public revenue base, (ii) inadequate infrastructure, particularly in transport and electricity, and (iii) a weak investment climate due largely to governance concerns. A number of other constraints also have been variously mentioned as potentially serious obstacles, including shortcomings in the financial sector, labor market rigidities, market failures in certain sectors and an inadequate composition of skills. But there appears to be a broad consensus that the first three constraints mentioned above are the most critical. 16. The vulnerable fiscal situation constitutes a threat to macroeconomic stability and undercuts the government’s capacity to intervene in the economy and provide essential public services. The East Asian Crisis triggered a precipitous decline in public revenues, particularly tax revenues, resulting in widening fiscal deficits and a rapidly rising public debt ratio; Figure 5. A series of tax reforms in 2004-05 succeeded in temporarily reversing the decline in tax revenues and halting the rise in the public debt ratio, but these efforts began to weaken again in 2007, putting renewed pressure on the fiscal balances. The government was able to maintain macroeconomic stability in the face of weakening revenues, in part through prudent monetary management, but also in part through a decline in public expenditures on account of falling interest payments on the public debt (Figure 6). The economic slowdown associated with the current global crisis and various tax-eroding legislative responses11 have exacerbated the decline in the taxation ratio and resulted in a renewed build-up of public debt. Restoring the stability and integrity of the tax system in the Philippines is essential for removing the fears of macroeconomic instability that periodically impair the investment climate and for providing a sustainable basis for public services.

9 The Krugman team found that the essential structure of the Philippine economy was characterized by a highly inefficient manufacturing sector sheltered behind high protective walls and using excessively capital-intensive techniques, where the rapidly growing labor force was being absorbed, not into industrial jobs, but into subsistence agriculture and marginal service-sector employment. Although the government was found to have done a reasonable job of maintaining macroeconomic stability, its limited revenue base constrained its ability to undertake socially necessary spending, especially on infrastructure, which was very low by regional standards. 10 See World Bank 2005, 2007; and Asian Development Bank, 2007. 11 These tax-eroding responses refer to the passage of tax eroding measures (such as VAT exemptions for senior citizens) as well as delays in the passage of fiscal measures that were needed to preserve the gains from earlier tax policy reforms (e.g., the Rationalization of Fiscal Incentives, Simplified Net Income Taxations Scheme, SNITS, and the Restructuring of Excise Taxes on Sin Products. Moreover, the falling taxation ratio also reflects administrative inefficiencies in BIR and BOC.

PHILIPPINES Discussion Note No.1: Economic Growth June 2011

DN1-8

Figure 5: Public Revenues (% of GDP) Figure 6: Public Expenditures (% of GDP)

17. Infrastructure shortcomings in the Philippines are particularly pronounced in the Transport and Power sectors. The Global Competitiveness Report for 2009 ranks the Philippines 98th out of 133 countries in terms of the quality of its overall infrastructure; ahead of only Vietnam among the countries in the region.12 In the Transport sector, it ranks last in the region. As pointed out in the most recent transport sector expenditure review (World Bank, 2009), the Philippines scores lowest on the Logistics Performance Index in the East Asian Region. Even though the quantity of transport infrastructure in network and facility density in the Philippines compares well with other countries in the region, capacity and quality do not. While the Philippines ranks somewhat better in the region in terms of electricity quality, it still falls far below the world average, and is an area highlighted in the 2005 investment climate assessment as a major negative influence on firms’ productivity and investment decisions.

Table 2: Ranking the Quality of Infrastructure in Selected East Asian Countries

Source: World Economic Forum, The Global Competitiveness Report 2009-2010

Note: The rankings refer to a total of 133 countries.

18. The lack of adequate infrastructure in the Philippines is indicative of a poor investment climate that reflects a weak public investment effort and contributes to a poor private investment effort. The Philippines has relied more on the private sector than the other countries in the region for its capital investment needs. Most noteworthy, however,

12 This represents a deterioration since 2006, when the Philippines was ranked 88th out of 125 countries.

PHILIPPINES Discussion Note No.1: Economic Growth June 2011

DN1-9

is that the amount of total spending on fixed capital formation is significantly less in the Philippines than in East Asia & Pacific on average. Furthermore, this gap has been increasing since the East Asia financial crisis, raising further questions about the sustainability of economic growth.

19. Governance-related factors ranked as the main impediment to firms’ productivity and investment decisions in the 2005 investment climate assessment. Payments of administrative bribes and the threat of civil unrest, crime and disorder were reported among the most important barriers to a good investment climate. As indicated in Figure 8, the Philippines ranks below the world mean in four out of the six categories that make up the World Bank’s governance indicators. Moreover, the Philippines ranks particularly poorly in the categories of political stability and control of corruption, both of which report declining scores between 2000 and 2008. 20. Finally, it may be useful to devote a moment on what do not appear to be critical constraints on growth at this time. The Krugman et al (1992) report noted that, as of mid-1990, the trade policy regime remained highly biased against trade, and accordingly it recommended that ‘the nation should pursue a strategy of export-led recovery driven by a depreciation of the exchange rate, complemented by trade liberalization.’ In view of the serious trade deficit and modest export growth that prevailed at the end of the 1980s,

Figure 7: Public and Private Fixed Capital Formation; as % of GDP

Source: World Bank, Development Indicators

Figure 8: The Philippines: Governance Indicators; 2000 vs. 2008

PHILIPPINES Discussion Note No.1: Economic Growth June 2011

DN1-10

the challenging part of such a strategy was how to introduce trade liberalization without immediately generating unsustainable trade deficits. The situation in the late 2000s is significantly different in at least two respects: namely, trade barriers are significantly lower than in the early 1990s and the current account balance is in surplus. The main factor responsible for this difference is the tremendous growth in workers’ remittances. The presence of a current account surplus driven by remittances growth means that the Philippines is exporting capital and labor, which raises questions about the country’s long-run growth prospects. The binding constraint on growth does not appear to be the availability of capital or labor, however, but the lack of adequate domestic incentives to employ that capital and labor at home, rather than abroad. It is not evident, therefore, that a more depreciated exchange rate coupled with trade liberalization – as recommended by Krugman et al (1992) – would make much difference as long as the key constraints described earlier that depress the investment climate continue to persist.13

What can be done to speed up growth?

21. It is difficult to envision a sustained resumption of economic growth in the Philippines without major improvements in the tax collection effort, infrastructure investment and governance.14 Correcting these shortcomings, therefore, is bound to rank high on the agenda of policymakers intent on implementing “sound fundamentals” to restore faster growth in the Philippines. Specific measures and options for achieving these corrections are discussed in greater detail in separate Discussion Notes.15 The main channel through which these measures affect growth is through improvements in the investment climate and in public finances, which together help to close the gap in physical capital accumulation that separates the Philippines from the faster growing countries in the region. 22. What can be done beyond the implementation of “sound fundamentals” to accelerate the structural transformation of the Philippines? The elimination of barriers to factor mobility may play an important role in this regard, especially in regard to labor. Barriers to financial capital mobility do not appear to constitute a critical bottleneck at this