DOCUMENT OF THE WORLD BANK FOR OFFICIAL USE ONLY Report No: PAD3096 PROGRAM APPRAISAL DOCUMENT ON A PROPOSED CREDIT IN THE AMOUNT OF SDR 72.3 MILLION (US$100 MILLION EQUIVALENT) TO THE PEOPLE’S REPUBLIC OF BANGLADESH FOR A STRENGTHENING PUBLIC FINANCIAL MANAGEMENT PROGRAM TO ENABLE SERVICE DELIVERY PROGRAM-FOR-RESULTS (P167491) December 29, 2018 Governance Global Practice South Asia Region This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript

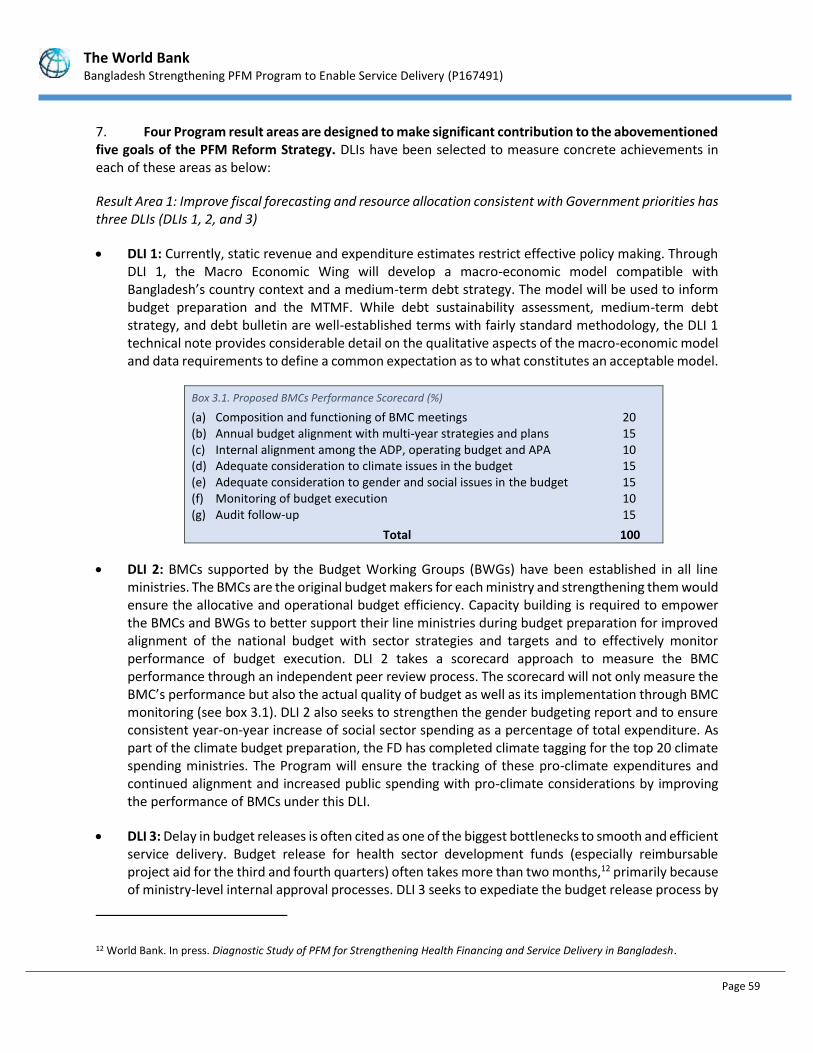

DOCUMENT OF THE WORLD BANK

FOR OFFICIAL USE ONLY

Report No: PAD3096

PROGRAM APPRAISAL DOCUMENT

ON A

PROPOSED CREDIT IN THE AMOUNT OF SDR 72.3 MILLION

(US$100 MILLION EQUIVALENT)

TO THE

PEOPLE’S REPUBLIC OF BANGLADESH

FOR A

STRENGTHENING PUBLIC FINANCIAL MANAGEMENT PROGRAM TO ENABLE SERVICE DELIVERY PROGRAM-FOR-RESULTS (P167491)

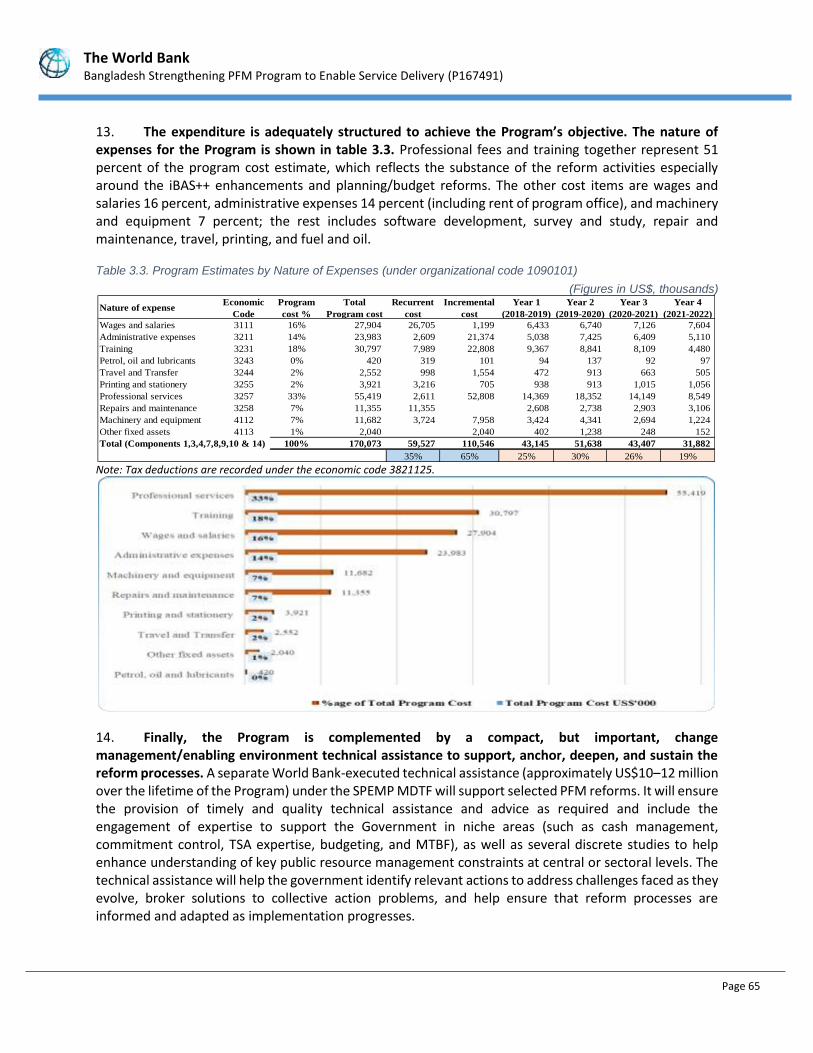

December 29, 2018

Governance Global Practice South Asia Region

This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

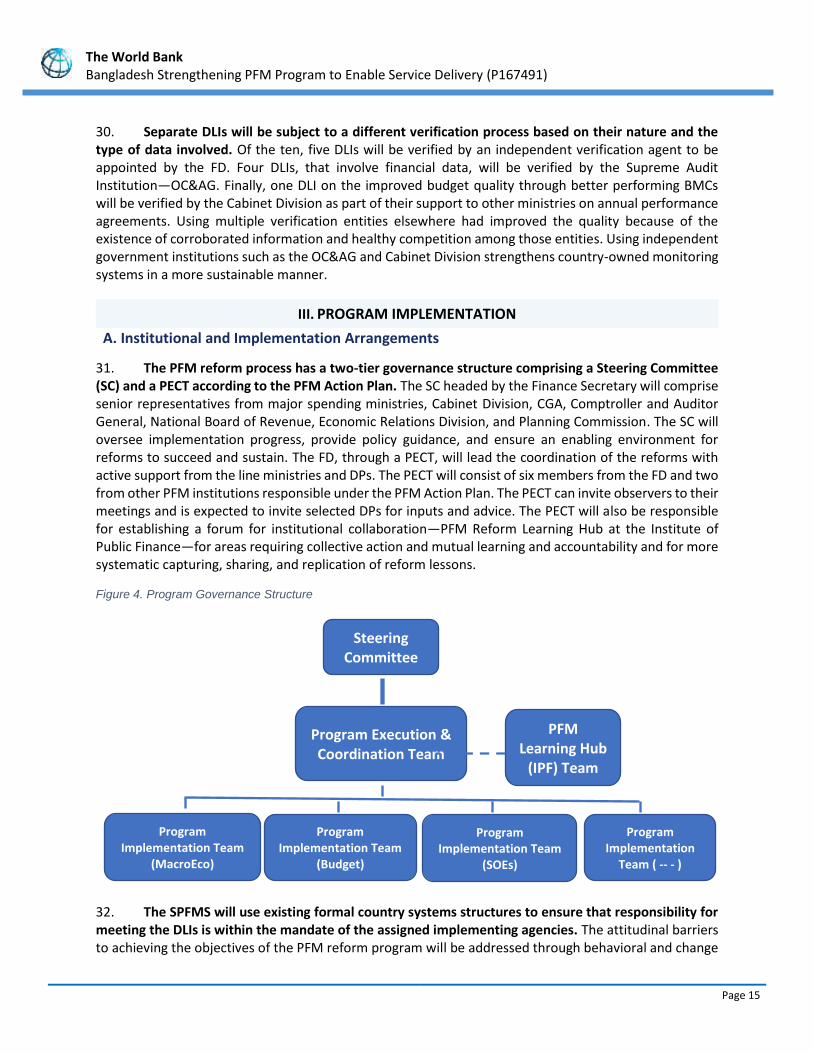

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

(Exchange Rate Effective November 30, 2018)

Currency Unit = Bangladeshi Taka (BDT)

BDT 85 = US$1

US$1 = SDR 0.723

FISCAL YEAR

July 1 – June 30

ABBREVIATIONS AND ACRONYMS

ADP Annual Development Program BACS Budget and Accounting Classification System BMC Budget Management Committee BWG Budget Working Group CAO Chief Accounts Officer CGA Controller General of Accounts CPF Country Partnership Framework CPTU Central Procurement Technical Unit DDO Drawing and Disbursing Officer DLI Disbursement-linked Indicator DLR Disbursement-linked Result DP Development Partner EFT Electronic Funds Transfer EBF Extra Budgetary Fund e-GP Electronic Government Procurement ESSA Environmental and Social Systems Assessment EU European Union FD Finance Division FSA Fiduciary Systems Assessment GDP Gross Domestic Product GHG Greenhouse Gas GPF General Provident Fund JICA Japan International Cooperation Agency iBAS++ Integrated Budget and Accounting System IFMIS Integrated Financial Management Information System IPF Investment Project Financing IMED Implementation Monitoring and Evaluation Division ISP Implementation Support Plan

The World Bank Bangladesh Strengthening PFM Program to Enable Service Delivery (P167491)

Page 3

IT Information Technology KRA Key Results Area M&E Monitoring and Evaluation MDAs Ministries, Departments, and Agencies MDTF Multi-Donor Trust Fund MoF Ministry of Finance MTBF Medium-Term Budget Framework MTMF Medium Term Macroeconomic Framework OC&AG Office of the Comptroller and Auditor General OPRC Operational Procurement Review Committee PAO Principal Accounting Officer PAP Program Action Plan PDO Program Development Objective PECT Program Execution and Coordination Team PEFA Public Expenditure and Financial Accountability PEMSP Public Expenditure Management Strengthening Program PER Public Expenditure Review PforR Program-for-Results PFM Public Financial Management PIT Program Implementation Team SAE Self-Accounting Entity SC Steering Committee SDC Swiss Agency for Development and Cooperation SEIP Skills for Employment Investment Program SOE State-Owned Enterprise SPFMS Strengthening Public Financial Management Program to Enable Service Delivery SPEMP Strengthening Public Expenditure Management Program ToR Terms of Reference TSA Treasury Single Account

Regional Vice President: Hartwig Schafer Practice Group Vice President: Ceyla Pazarbasioglu-Dutz

Practice Senior Director: Deborah L. Wetzel Country Director: Qimiao Fan

Practice Manager: George Addo Larbi Task Team Leader: Furqan Ahmad Saleem

The World Bank Bangladesh Strengthening PFM Program to Enable Service Delivery (P167491)

Page 4

BASIC INFORMATION

Is this a regionally tagged project? Financing Instrument

No Program-for-Results Financing

Bank/IFC Collaboration Does this operation have an IPF component?

No No

Proposed Program Development Objective(s) The Program Development Objective (PDO) is to improve fiscal forecasting, budget preparation and execution, financial reporting and transparency to enable better resource availability for service delivery in selected Ministries, Departments, and Agencies.

International Development Association (IDA) 100.00

IDA Credit 100.00

The World Bank Bangladesh Strengthening PFM Program to Enable Service Delivery (P167491)

Page 5

Expected Disbursements (US$ Millions)

Fiscal Year 2019 2020 2021 2022 2023 2024

Absolute 20.00 12.00 15.00 15.00 18.00 20.00

Cumulative 20.00 32.00 47.00 62.00 80.00 100.00

INSTITUTIONAL DATA

Practice Area (Lead)

Governance

Contributing Practice Areas

Macroeconomics, Trade and Investment

Climate Change and Disaster Screening

Yes

PRI_PUB_DATA_TBL Private Capital Mobilized

No

Gender Tag Does the program plan to undertake any of the following? a. Analysis to identify Project-relevant gaps between males and females, especially in light of country gaps identified through SCD and CPF Yes b. Specific action(s) to address the gender gaps identified in (a) and/or to improve women or men's empowerment Yes c. Include Indicators in results framework to monitor outcomes from actions identified in (b) Yes

The World Bank Bangladesh Strengthening PFM Program to Enable Service Delivery (P167491)

Page 6

SYSTEMATIC OPERATIONS RISK-RATING TOOL (SORT)

Risk Category Rating

1. Political and Governance Substantial

2. Macroeconomic Moderate

3. Sector Strategies and Policies Moderate

4. Technical Design of Project or Program Moderate

5. Institutional Capacity for Implementation and Sustainability Moderate

6. Fiduciary Fiduciary rating from IRT:

Substantial as of 19-Jun-2018

Substantial

7. Environment and Social Environmental Risk rating from Specialist:

Low as of 19-Jun-2018 Social Risk rating from Specialist:

Low as of 08-Oct-2018

Low

8. Stakeholders Moderate

9. Other

10. Overall Moderate

COMPLIANCE

Policy

Does the program depart from the CPF in content or in other significant respects?

[ ] Yes [✔] No

Does the program require any waivers of Bank policies?

[ ] Yes [✔] No

Safeguard Policies Triggered

Safeguard Policies Yes No

Projects on International Waterways OP/BP 7.50 ✔

Projects in Disputed Areas OP/BP 7.60 ✔

Legal Covenants

By no later than one (1) month after the Effective Date, the Recipient shall establish and thereafter maintain,

The World Bank Bangladesh Strengthening PFM Program to Enable Service Delivery (P167491)

Page 7

throughout Program implementation, a steering committee, responsible for providing policy guidance and strategic oversight, monitoring Program implementation, and serving as the highest-level coordinating entity participating ministries and implementing entities under the Program. By no later than three (3) months after the Effective Date, the Recipient (through MoF) shall establish and thereafter maintain throughout Program implementation, a Program execution and coordination team, as the leading implementing directorate. By no later than three (3) months after the Effective Date, the Recipient (through MoF) shall and thereafter maintain throughout Program implementation, Program implementation teams within the relevant divisions of MoF leading the implementation of the Program. By no later than three (3) months after the Effective Date, the Recipient shall appoint and enter into verification agreements or other appropriate arrangements with the Independent Verification Agencies.

Luiza A. Nora Team Member Citizens Engagement GSU06

Nazmus Sadat Khan Team Member Economist GMTSA

Nikeisha Anthonett Russell Team Member Program Coordination GGOES

Nusrat Mehzabeen Team Member Program Coordination SACBD

The World Bank Bangladesh Strengthening PFM Program to Enable Service Delivery (P167491)

Page 8

Rizwana Tabassum Team Member Data Analysis GGOES

Robertus Cornelis Johannes Van Kippersluis

Team Member Change Management GGOES

Satish Kumar Shivakumar Team Member Loans WFACS

Saw Young Min Team Member SOEs GGOES

Suraiya Zannath Team Member Pensions GGOES

Talajeh Livani Team Member Gender GSU06

Winston Percy Onipede Cole

Team Member IFMIS & Financial Reporting GGOES

The World Bank Bangladesh Strengthening PFM Program to Enable Service Delivery (P167491)

BANGLADESH

BANGLADESH STRENGTHENING PFM PROGRAM TO ENABLE SERVICE DELIVERY

TABLE OF CONTENTS I. STRATEGIC CONTEXT ...................................................................................................... 1

A. Country Context .................................................................................................................. 1

B. Sectoral (or Multi-Sectoral) and Institutional Context ........................................................ 2

C. Relationship to the Country Partnership Framework (CPF) and Rationale for Use of Instrument ............................................................................................................................. 5

II. PROGRAM DESCRIPTION................................................................................................. 7

A. Government Program ......................................................................................................... 7

B. The Program Scope ............................................................................................................. 8

C. Program Development Objective(s) (PDO) and PDO Level Results Indicators ................. 12

D. Disbursement Linked Indicators and Verification Protocols ............................................ 12

III. PROGRAM IMPLEMENTATION ...................................................................................... 15

A. Institutional and Implementation Arrangements ............................................................. 15

B. Results Monitoring and Evaluation ................................................................................... 16

C. Disbursement Arrangements ............................................................................................ 17

D. Capacity Building ............................................................................................................... 18

IV. ASSESSMENT SUMMARY .............................................................................................. 19

A. Technical (including program economic evaluation) ........................................................ 19

B. Fiduciary ............................................................................................................................ 23

C. Environmental and Social .................................................................................................. 26

D. Risk Assessment ................................................................................................................ 27

ANNEX 4. SUMMARY FIDUCIARY SYSTEMS ASSESSMENT ..................................................... 77

ANNEX 5. SUMMARY ENVIRONMENTAL AND SOCIAL SYSTEMS ASSESSMENT ....................... 85

ANNEX 6. PROGRAM ACTION PLAN ..................................................................................... 89

ANNEX 7. IMPLEMENTATION SUPPORT PLAN ...................................................................... 92

The World Bank Bangladesh Strengthening PFM Program to Enable Service Delivery (P167491)

Page 1

I. STRATEGIC CONTEXT

Introduction

1. This Program Appraisal Document describes the context, rationale, and objectives of the World Bank’s support to a new government program for strengthening public financial management (PFM) in Bangladesh. A PFM Action Plan (2018–23) has recently been approved by the Finance Minister for effective implementation of the Bangladesh PFM Reform Strategy, 2016. This PFM Action Plan provides the implementation road map for priority actions. The Government has requested the proposed IDA Program-for-Results (PforR) operation (US$100 million) to support the Ministry of Finance (MoF) in implementing selected components of the PFM Action Plan. The Program Appraisal Document also summarizes the relevant assessments, including the technical aspects such as the best-fit, program Results Framework, cost-benefit, and fiduciary and social and environmental safeguard risks.

A. Country Context

2. Bangladesh is one of the world’s most populous countries, with an estimated 165 million people in a geographical area of about 144,415 km2 and per capita income of US$1,670 (World Bank Atlas method) in 2018, well above the lower-middle-income country category threshold which it crossed in FY14. During recent years, economic conditions have improved in the country. However, headline inflation increased to 5.8 percent in FY18, from 5.4 percent in FY17, reflecting increases in food prices because of supply shocks. Fiscal deficit was contained at around 4.5 percent of gross domestic product (GDP) in FY18. The FY18 budget targets 5 percent deficit with 26.2 percent growth in expenditures. The current account deficit increased to 3.5 percent of GDP in FY18. The GDP grew well above the average for developing countries in recent years, averaging 6.5 percent since 2010, with an officially estimated growth of 7.86 percent in FY18, driven by manufacturing and construction. Progress on reducing extreme poverty and boosting shared prosperity through human development and employment generation has continued. The poverty incidence based on the international poverty line of US$ 1.90 per capita per day (measured based on the purchasing power parity exchange rate) declined from 44.2 percent in 1991 to 14.8 percent in 2016 (latest available poverty data). In the World Bank’s Human Capital Index 2018, Bangladesh performed better than the South Asian average and the lower-middle-income average in all criteria except stunting. With the current education and health conditions, a child born today in Bangladesh will be 48 percent as productive as s/he could have been. Bangladesh’s performance against the Millennium Development Goals was impressive relative to the South Asia region average for most of the indicators. Such progress notwithstanding, the pace of poverty reduction and the rate of job creation has slowed since 2010. Bangladesh needs stronger efforts in making growth more inclusive and sustainable to meet its target of eliminating poverty by 2030 and attaining the upper-middle-income status by 2031. For accelerating private sector-led growth with improved investment climate, the key challenges are addressing deficits in infrastructure and power, with much improved quality in spending public resources, better regulations, and enhanced skills of its vast and rapidly increasing labor force.

3. Bangladesh’s vulnerability to climate change represents a growing economic and fiscal risk. Bangladesh is one of the most climate-vulnerable countries in the world. The country’s emissions are less

The World Bank Bangladesh Strengthening PFM Program to Enable Service Delivery (P167491)

Page 2

than 0.35 percent of global emissions.1 The economic losses because of climate change over the past 40 years were estimated at US$12 billion.2 Growth and stability in Bangladesh is subject to extreme forms of climate risks through both ex post and ex ante channels. Ex post macro effects include the direct effects of climate impacts such as sea-level rise, changes in crop yields, and floods after they occur. Over the next decade, growth could be lower, depending on the frequency and magnitude of flooding.3 Ex post impacts include depression of labor demand, particularly for low-skilled workers. Ex ante impacts derive from households altering their behavior in anticipation of a climate risk, which affects productivity and growth.

B. Sectoral and Institutional Context

4. Bangladesh has improved on most governance indicators in the past 10 years; however, the overall scores are still lower than the regional averages. The world governance indicators show steady improvement on most accounts (see figure 1) that indicates the success of earlier reforms to strengthen PFM, transparency, anticorruption, and rule of law. The biggest achievement has been to maintain tight fiscal management for stable economic growth. A lean public sector (roughly a million public servants including those in state-owned enterprises [SOEs]) has helped the country keep the establishment cost below 25 percent of budget, leaving sufficient space for development expenditures. The Right to Information Act (2009) provides the Government an opportunity to facilitate greater disclosure of information and become more open and accountable. However, more work is needed both on the supply side, to strengthen its ability to effectively implement the act, and on the demand side, to raise public awareness. Key public oversight institutions—audit, judiciary, anticorruption, parliamentary committees, and election commission—also need further strengthening. Finally, domestic resources mobilization needs to be significantly improved to achieve the broad development goals.

Figure 1. World Governance Indicators

Source: The World Bank - World Governance Indicators.

1 Bangladesh’s Intended Nationally Determined Contributions, page 2. 2 Nationally Determined Contribution of Bangladesh Implementation Roadmap, page 1. 3 World Bank. 2016. Helping Bangladesh Become Resilient to Climate Change Threats. Available at http://www.worldbank.org/en/news/feature/2016/10/10/helping-bangladesh-become-resilient-climate-change-threats; Germanwatch e.V. 2017. Global Climate Risk Index 2017. Available at: https://germanwatch.org/en/12978; and World Bank. 2009. Bangladesh - Policy Note on Climate Change. Available at: http://documents.worldbank.org/curated/en/691511468208161047/Bangladesh-Policy-note-on-climate-change.

The World Bank Bangladesh Strengthening PFM Program to Enable Service Delivery (P167491)

Page 3

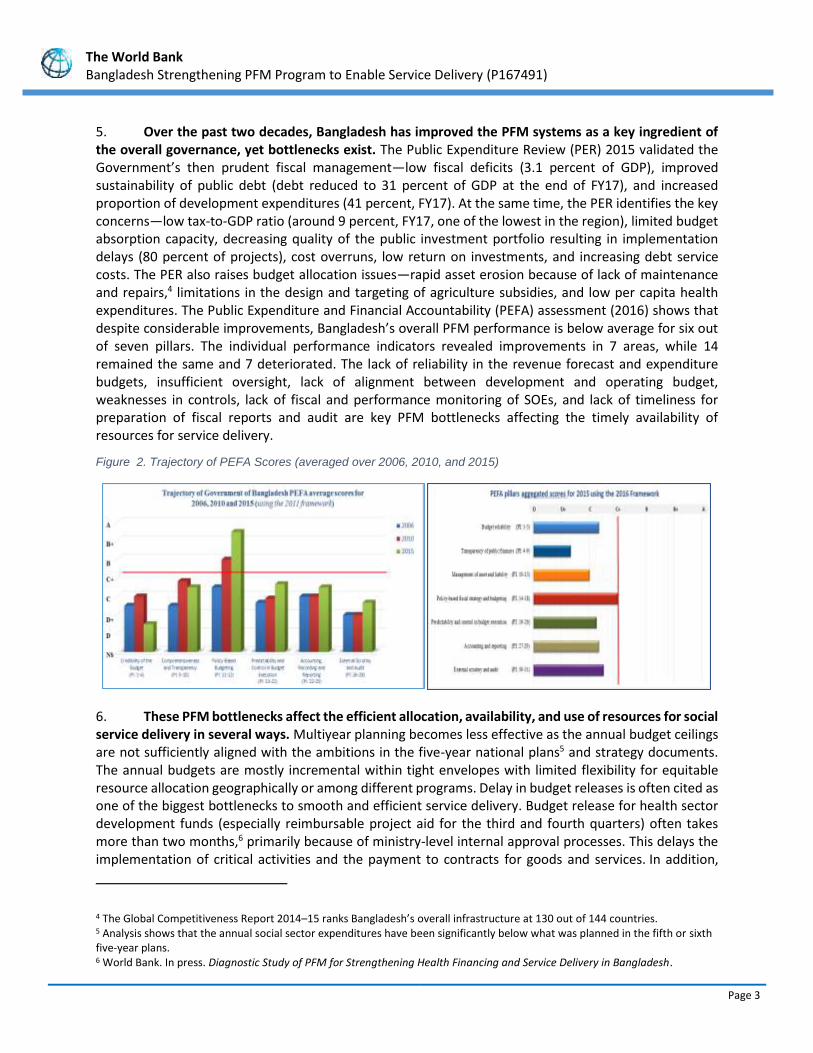

5. Over the past two decades, Bangladesh has improved the PFM systems as a key ingredient of the overall governance, yet bottlenecks exist. The Public Expenditure Review (PER) 2015 validated the Government’s then prudent fiscal management—low fiscal deficits (3.1 percent of GDP), improved sustainability of public debt (debt reduced to 31 percent of GDP at the end of FY17), and increased proportion of development expenditures (41 percent, FY17). At the same time, the PER identifies the key concerns—low tax-to-GDP ratio (around 9 percent, FY17, one of the lowest in the region), limited budget absorption capacity, decreasing quality of the public investment portfolio resulting in implementation delays (80 percent of projects), cost overruns, low return on investments, and increasing debt service costs. The PER also raises budget allocation issues—rapid asset erosion because of lack of maintenance and repairs,4 limitations in the design and targeting of agriculture subsidies, and low per capita health expenditures. The Public Expenditure and Financial Accountability (PEFA) assessment (2016) shows that despite considerable improvements, Bangladesh’s overall PFM performance is below average for six out of seven pillars. The individual performance indicators revealed improvements in 7 areas, while 14 remained the same and 7 deteriorated. The lack of reliability in the revenue forecast and expenditure budgets, insufficient oversight, lack of alignment between development and operating budget, weaknesses in controls, lack of fiscal and performance monitoring of SOEs, and lack of timeliness for preparation of fiscal reports and audit are key PFM bottlenecks affecting the timely availability of resources for service delivery.

Figure 2. Trajectory of PEFA Scores (averaged over 2006, 2010, and 2015)

6. These PFM bottlenecks affect the efficient allocation, availability, and use of resources for social service delivery in several ways. Multiyear planning becomes less effective as the annual budget ceilings are not sufficiently aligned with the ambitions in the five-year national plans5 and strategy documents. The annual budgets are mostly incremental within tight envelopes with limited flexibility for equitable resource allocation geographically or among different programs. Delay in budget releases is often cited as one of the biggest bottlenecks to smooth and efficient service delivery. Budget release for health sector development funds (especially reimbursable project aid for the third and fourth quarters) often takes more than two months,6 primarily because of ministry-level internal approval processes. This delays the implementation of critical activities and the payment to contracts for goods and services. In addition,

4 The Global Competitiveness Report 2014–15 ranks Bangladesh’s overall infrastructure at 130 out of 144 countries. 5 Analysis shows that the annual social sector expenditures have been significantly below what was planned in the fifth or sixth five-year plans. 6 World Bank. In press. Diagnostic Study of PFM for Strengthening Health Financing and Service Delivery in Bangladesh.

The World Bank Bangladesh Strengthening PFM Program to Enable Service Delivery (P167491)

Page 4

social sector budgets are fragmented because of the vertical programs and externally financed interventions that pose several management challenges at the level of the budget holders and frontline service providers. Slow procurement processes delay the provision of necessary goods and services. For example, it takes an average of 15–18 months for drugs to reach the Upazila Health Complex and below, while it should not take more than 9 months in procuring and distributing these. Sector ministries often advocate for the need for flexible cash resources at the health and education facilities. While cash handling is not considered a good practice and is risky, there is sufficient evidence from the field of how public service delivery suffers because of the lack of resources for minor repairs, petty purchases, or paying the travel allowance for maternity patients. In some health sector programs, the issue has been addressed on an ad hoc basis. Finally, inadequate audit follow-up and delayed resolution of audit queries could affect aid disbursement and civil servants’ terminal benefits, thereby negatively affecting the motivation of service providers.

7. The Government of Bangladesh has been a pioneer in introducing a climate-responsive PFM system. In 2014, the Government adopted a Climate Fiscal Framework, providing a road map to link national climate strategies with the resource allocation system. The Climate Fiscal Framework prompted more specific interventions to make the budgeting exercise under the medium-term budget framework (MTBF) climate inclusive. This was first initiated in a pilot of six ministries in the FY17–18 budget. In June 2018, the Bangladesh Climate Financing for Sustainable Development: Budget Report 2018–19 was rolled out, covering all 20 line ministries that have programs and projects of significant climate relevance. The assessment shows that 8.82 percent of the FY19 budget of the 20 ministries (covering around half of the total national budget) was targeted to climate mitigation or adaptation. It also illustrates the evolution of the Government’s financing response over time through the national budget and the growing importance of this response. Complementing this technical report, the Government—with support from United Nations Development Programme—published, for the first time, in August 2018, a Citizen’s Climate Budget, which translates the technical report into a set of simplified infographics for the general public. Together, these reports enhance transparency and help stakeholders identify areas of opportunity to leverage public expenditure to strengthen climate resilience.

8. A PFM Action Plan (2018–23) has been recently approved to support effective implementation of the PFM Reform Strategy (2016–21).7 The strategic goals of PFM reforms are to (a) maintain aggregate fiscal discipline compatible with macroeconomic stability and pro-poor growth, (b) allocate resources consistent with Government priorities as reflected in the National Plan, (c) promote the efficient use of public resources and delivery of services through better budget execution, (d) promote accountability through external scrutiny and transparency of the budget, and (e) enhance the enabling environment for improved PFM outcomes. Within these goals, the PFM Action Plan provides the implementation road map for some priority actions with clear institutional responsibilities among 13 thematic reform components, cost-benefit analysis of sub-activities, and results indicators to monitor the successful implementation. The PFM Action Plan also elaborates on the governance structure for reforms and the change management approach through a specific component devoted to these nontechnical issues. As a cross-cutting issue, climate change financing has been addressed in several components of the PFM Action Plan. In addition, the Prime Minister has approved the road map for merger of the administrative and economic cadres, which will enable better alignment between the development and recurrent budgets.

7 The PFM Action Plan has been approved by the Minister of Finance.

The World Bank Bangladesh Strengthening PFM Program to Enable Service Delivery (P167491)

Page 5

9. With the proposed IDA financing, the Strengthening Public Financial Management Program to Enable Service Delivery (SPFMS), will support implementation of part of the PFM Action Plan. The Government’s internal Program Document for the SPFMS received the approval of the Honorable Prime Minister on November 12, 2018. The SPFMS includes components directly led by the Finance Division (FD), including the macro-fiscal forecasting, debt management, budget preparation and execution, integrated financial management information system (IFMIS), treasury single account (TSA), SOE monitoring, pensions, internal audit, and financial reporting. The program boundaries are further clarified in section 2-A and 2-B of this document.

10. The SPFMS builds on the Government’s efforts to establish a climate-responsive PFM system, partly supported by the First Bangladesh Jobs Programmatic Development Policy Credit.8 A prior action under the jobs program was the rollout of climate budgeting across 20 ministries with climate-relevant expenditures and the approval by the Cabinet of the National Environmental Policy 2018, which will enable leveraging public expenditure for investments in climate resilience and climate change mitigation. This PforR operation will aim at ensuring the effective operation of this climate-responsive PFM system and ensure that climate considerations are adequately taken into account during (ex ante) budget preparation that leads to a higher spending on climate mitigation and adaptation.

C. Relationship to the Country Partnership Framework (CPF) and Rationale for Use of Instrument

11. Promoting good governance and curbing corruption are among the development goals of the Government’s Seventh Five-Year Plan (2016–20). The plan describes an approach to good governance that has a key pillar on reforming budgetary processes and further elaborates the key priorities for PFM reforms in the areas of public investment management, revenue mobilization, accounting classification and IFMIS, financial reporting, TSA, pensions, SOEs, debt management, MTBF, budget transparency, and audit and accountability. Building on the Five-Year Plan, a PFM Reform Strategy (2016–21) was approved. The strategy is being operationalized through the recently approved PFM Action Plan 2018–23.

12. The CPF (2016–20) also highlights the importance of supporting Government efforts to strengthen governance systems. It recognizes that it is a long-term agenda that demands sustained effort through upstream and downstream interventions. The CPF states that the World Bank will continue to provide lending and technical assistance to support policies and systems aimed at improving transparency and efficiency in service delivery, including on PFM. Both the Seventh Five-Year Plan and the CPF have opened opportunities for the World Bank’s engagement in PFM reforms.

13. The current context provides a unique window of opportunity to strengthen Bangladesh’s PFM institutions and systems. The World Bank has a well-recognized comparative advantage among development partners (DPs) in improving PFM systems, given its broad international experience. This is also a critical time to intervene in Bangladesh, given the heightened need for prudent use of resources under the current fiscal pressures, the call from DPs for the World Bank to take a leadership role and the greater appetite among authorities for committing to difficult reforms toward achieving upper-middle-income status.

8 Expected to be approved by the World Bank in December 2018.

The World Bank Bangladesh Strengthening PFM Program to Enable Service Delivery (P167491)

Page 6

14. The PforR is the most suitable World Bank instrument to advance key systems reforms and build institutional capacity. The proposed PforR draws from recent experience with results-based financing in Bangladesh and those supporting the PFM reforms in other countries. The observed advantages of the PforR include the following:

(a) Focus on results. The PforR focuses attention on results which reflect genuine change to the strengthening and functioning of PFM systems developed in the past and making the relevant connections to support service delivery outcomes through better functioning systems. The long iterative consultations on disbursement-linked indicators (DLIs) with the Government has allowed a more active questioning of paper commitments and enabled realism of reform goals.

(b) Ownership. PforR would transform the generalized high-level support for PFM reforms into specific actions with ownership required to achieve these results. The PforR has supported a framework for monitoring, reporting, and accountability, especially to avoid significant investments primarily driven by information technology (IT) ambitions but with insufficient utility. As part of the preparation, technical assessments conducted with client counterparts have identified key challenges and opportunities for change that could be addressed through DLIs and steps toward achieving these DLIs have been documented in a detailed technical note for each DLI.

(c) Country systems. The Government will follow its own rules and experience of the PFM processes and systems, thus bringing an additional impetus for these reforms. This will also ensure that work processes are suitable for the local context while providing adequate fiduciary oversight, for example, smaller output-based contracts instead of time-based contracts sourced under an overall management contract. Finally, it will allow the necessary flexibility to course-correct as needed to achieve the reform targets.

15. Other instruments such as Investment Project Financing (IPF), Development Policy Operation,

and Technical Assistance and Advisory Services have been considered not to be as good a fit to the

current challenges, relative to the PforR instrument, for the following reasons:

• Many PFM and governance challenges go significantly deeper than a need for policy changes and require a multiyear, more granular engagement. This makes a Development Policy Operation a less suitable instrument than a PforR.

• The need is not so much for outside technical assistance as for structuring and focusing organizational and leadership attention on key reforms. An IPF would therefore be a less perfect fit than a PforR. As the Government has been implementing the Public Expenditure Management Strengthening Program (PEMSP) since 2015 through its own funds as a recurrent budget scheme, it has built significant capacity of using mainstream country systems to undertake PFM reforms and demonstrated a prudent use of public funds. Hence, an IPF with DLIs does not seem to be good option to continue the mainstream use of country systems.

• Related to the above, small-scale technical advice alone will not deliver the incentives needed to bring forward reforms. In addition, such support has been provided by the DPs in recent years and will be available to complement the implementation of the Government PFM Program, as mentioned earlier.

The World Bank Bangladesh Strengthening PFM Program to Enable Service Delivery (P167491)

Page 7

II. PROGRAM DESCRIPTION

A. Government Program

16. The Government’s PFM Action Plan (2018–23) includes 14 reform components, of which the new SPFMS will support 8. The Government has requested World Bank support for the PFM Action Plan components directly led by the FD—including the macro fiscal forecasting, debt management, budget preparation and execution, IFMIS, TSA, SOE monitoring, pensions, internal audit, and financial reporting. Government resources have not been sufficient to maintain the reforms’ momentum in these areas after the closure of the Strengthening Public Expenditure Management Program, package A (SPEMP-A) in 2014. This also impeded the FD’s ability to lead the overall PFM reforms in Bangladesh.

Figure 3. Program Boundary

17. The selection of eight PFM Action Plan components for the Program is driven by several factors:

(a) They are closely related to the PFM bottlenecks to service delivery, as explained in box 1.

(b) These components are closely interconnected: (i) the use of improved fiscal projections for budgeting binds the multiyear perspective with annual allocations and ensures improved budget quality and enhanced social sector allocations, (ii) improving IFMIS will lead to timely financial reporting and better use of financial information by the budget holders, (iii) improving IFMIS also entails automating and speeding up pensions and other payments through electronic funds transfer (EFT) and online bill submission, (iv) an effective internal audit and SOEs monitoring are important for efficient expenditure control (including subsidies to SOEs), and (v) government debt management and information on SOE debt and contingent liabilities are an integral part of risk analysis for fiscal projections.

(c) These components are primarily under the control of the FD that will facilitate coherent implementation of the Program.

(d) This block of PFM reforms is unfunded while other components are already supported by the World Bank and DPs—public investments (Japan International Cooperation Agency [JICA], US$5 million); procurement (IDA, US$55 million); revenue mobilization (IDA, US$60 million and European Union [EU] EUR 4 million); and external audit (EU, EUR 6 million).

The World Bank Bangladesh Strengthening PFM Program to Enable Service Delivery (P167491)

Page 8

18. The total cost of PFM reforms laid out in the PFM Action Plan exceeds US$350 million for the next five years (table 1). This includes reform activities led by the National Board of Revenue (US$49.6 million), Planning Commission (US$20.1 million), Cabinet Division (US$40.2 million), Comptroller and Auditor General (US$10.2 million), Parliament Secretariat (US$6.4 million), and Central Procurement Technical Unit (CPTU) (US$60 million), in addition to the components led by the FD (US$170 million). Out of this, US$115 million is already provided by the World Bank and other DPs. The proposed IDA PforR is financing US$100 million, or 28.1 percent of the total. Table 1. Overall PFM Action Plan Program: 2018–23a

Component Institution Amount (US$, millions)

% of Total

PFM Action Plan Components 1, 3, 4, 7–10, and 14 (the Program)

Finance Division and Controller General of Accounts (CGA)

170.0 47.7 (IDA 28.1)

C-2: Revenue Mobilization National Board of Revenue 49.6 13.9

C-5: Public Investments Planning Ministry 20.1 5.6

Note: a. Estimates for C-2, 5, 6, 11, 12, and 13 from PFM Action Plan approved by the Minister of Finance.

B. The Program Scope

19. As described earlier, the Program supported by the PforR comprises eight components of the PFM Action Plan to strengthen fiscal forecasting, budget preparation and execution, financial reporting, and transparency. This will make significant contributions for improved fiscal discipline, budget credibility, and accountability. Specific reform activities will include improving fiscal forecasting supported by better IFMIS data and reduced SOE fiscal risks, strengthening the budget management committees (BMCs) for budget credibility, ensuring timely budget releases to support improved budget out-turn, and enhancing use of the TSA. The accountability reforms will include strengthening the monitoring of the performance of SOEs, ensuring the timely submission of central government financial statements for auditing, and strengthening the internal audit function and audit committees.

20. The Program is aimed at ensuring that the improved PFM performance enables better resource availability for social service delivery in selected Ministries, Departments, and Agencies (MDAs). While the SPFMS will gradually cover all the key sectors in Bangladesh, social sectors are prioritized to pilot the PFM improvements. Examples include (a) improving the functioning of BMCs in the line ministries, (b) reducing the current 2.3 months taken to 1 month for the release of budget from departments to frontline service delivery units, (c) using financial information by the budget controlling officers, (d) monitoring performance of SOEs, (e) user group endorsing the Integrated Budget and Accounting System (iBAS++) improvement plan, (f) budget holders submitting payment bills online, (g) connecting iBAS++ with other applications/systems for direct bank transfer to pensioners or beneficiaries, (h) launching a portal to push the boundaries for fiscal transparency by disseminating key fiscal datasets (disaggregated revenue/expenditure and output) in user-friendly accessible formats, and (i) using smartphones to access

The World Bank Bangladesh Strengthening PFM Program to Enable Service Delivery (P167491)

Page 9

real-time budget information for decision making to enhance service delivery. Box 1 elaborates how these Program interventions will help to solve the PFM bottlenecks to service delivery.

Box 1. PFM Bottlenecks and Program Interventions to Enable Service Delivery (a) Ambitious five-year national plan, other strategic planning documents, and MTBF

• Improving the realism of the fiscal projections through an improved forecasting model and with due regard to fiscal risks.

• Allowing a steady growth of the social sector spending as a percentage of the total public sector spending. These resources will partly come from improving the performance of the SOE sector.

• Improving, over time, the alignment of the annual budgets with the multiyear plans and enabling quicker completion of the new development schemes and provision of additional resources for service delivery to existing facilities.

(b) Allocation of health and education resources with inadequate consideration of the need

• Improving the performance of the BMCs to lead consultations in each ministry to improve the quality of the annual budget and its execution over time.

• Annual budget allocations will be made after due regard to the fiscal need (to be separately worked out for development and operating expenditures) and better aligned to prioritize the programs and cost categories in accordance with the sector strategy.

• Better budget allocation could only be achieved over time by making incremental changes each year. This requires significant deliberation and stakeholder consultations.

(c) Fragmentation of budget primarily because of externally financed programs

• Strengthening the BMCs to progressively consolidate various programs into the annual budget and bring them in to the TSA to avoid the use of any exceptional procedures

• Discouraging the use of the special project bank accounts outside of treasury

• Ensuring timely budget releases to the drawing and disbursing officers (DDOs) to remove one key obstacle often cited

(d) Long time taken in procurement

• This PFM Program does not directly attempt to improve procurement as there is a separate World Bank project dealing with the public procurement (on e-Government Procurement [e-GP]). Nevertheless, the interface between iBAS++ and e-GP, improved payment mechanisms of the EFT, and online bill submission will expedite the payment for procurements and make them more transparent, thereby enhancing the market confidence.

(e) Delayed budget releases of development expenditures to the budget holders (especially for third and fourth quarters)

• Addressing the issue of timely budget releases through two key actions. First, this Program seeks to delink the budget releases from the need to submit a statement of expenditures as the budget execution data are now in iBAS++. Second, it seeks to ensure timely distribution of budget to the DDOs by the budget holders by establishing a monitoring mechanism through iBAS++.

(f) Lack of flexible resources at health and education facilities

• Conduct quarterly PFM field inspections by multi-institution teams to identify such challenges and then devise exceptional regulations and procedures for specific circumstances. For example, in case of the health sector, such consultations could lead to allowing the facilities to retain user fees as flexible cash and complement this with what could be collected through community support committees, and if and how a part of these resources could be used for bonuses.

(g) Inadequate audit follow-up affecting DP disbursements • Expediting the audit follow-up by establishing well-functioning audit committees. Well-functioning audit

committees on the one hand resolve the pending audit observations, and on the other hand, they provide useful feedback to auditors to improve audit quality.

The World Bank Bangladesh Strengthening PFM Program to Enable Service Delivery (P167491)

Page 10

21. This Program complements other ongoing World Bank-financed social sector operations which aim to improve service delivery outcomes directly (table 2).

Table 2. World Bank-financed Projects in Social Sectors

Project Name PDO Key Results Area (KRA)

1. Transforming Secondary Education for Results Operation (P160943) US$510 million - FY18–23

The PDO is to improve student outcomes in secondary education and the effectiveness of the secondary education system.

• Enhanced quality and relevance of secondary education

• Increased equitable access and retention to secondary education

• Strengthened Governance, Management, and Administration

2. Quality Learning for All Program (P162619) US$700 million - FY18–23

The PDO is to improve the quality of and enhance equitable access to education from pre-primary to grade 5.

• Learning outcomes in Grades 3

• Number of contact hours

• Primary cycle completion rate (up to grade 5 and grade 8)

• Primary net enrollment rate

• Percent of out of school children aged 6–14

3. Health Sector Support Project (P160846) US$565 million - FY18–23

The PDO is to strengthen the health, nutrition, and population (HNP) sector's core management systems and delivery of essential HNP services with a focus on selected geographical areas.

• Planning, budgeting, financing flows, and resource allocation

• Improving sector governance

• Procurement, supply chain management, and asset management

• Human resource management - Health management information system

• Underserved areas

• Adolescent health and nutrition

• Maternal and child nutrition

• Communicable disease control including tuberculosis

• Urban primary healthcare

4. Cash Transfer Modernization Project (P160819) US$300 million - FY19–24

The PDO is to improve the transparency and efficiency of selected cash transfer programs for vulnerable populations by modernizing service delivery.

Cash transfer programs coverage

• Lowest two quintiles based on poverty score

• Vulnerable persons in lowest two quintiles Modernizing service

• Payment using digital payments

• Efficient withdrawals

5. Income Support Program for the Poorest (P146520) US$300 million - FY16–21

The PDO is to provide income support to the poorest mothers in selected Upazilas, while (i) increasing the mothers’ use of child nutrition and cognitive development services, and (ii) enhancing local level government capacity to deliver safety nets.

• Cash transfers to bottom two quintiles with pregnant women and/or mothers of children below the age of 60 months/conditioned on maternal and child health services

• Capacity building

• Monitoring and evaluation (M&E)

Total: US$2.375 billion

The World Bank Bangladesh Strengthening PFM Program to Enable Service Delivery (P167491)

Page 11

22. The total SPFMS expenditures are estimated at US$170 million, out of which IDA will finance US$100 million (table 3). The PforR will be implemented over five years. Tables 4 and 5 provide a breakdown of the SPFMS expenditures by PFM Action Plan components and economic budget codes, respectively. The SPFMS incremental expenditures are estimated to be around US$110 million. An additional US$60 million of recurrent expenses of the FD are closely related to the implementation of these reforms, taking the total estimated cost to US$170 million.

Table 3. SPFMS Financing

Source Amount (US$, millions)

% of Total

Counterpart Funding 70.00 41.18

Borrower 70.00 41.18

International Development Association (IDA) 100.00 58.82

IDA Credit 100.00 58.82

Total SPFMS Financing 170

Table 4. SPFMS Program Expenditures

PFM Reform Action Plan

Expenditures (US$, millions)

C-1 Revenue and Expenditure Forecasting 7.15

C-3 Debt Management 5.85

C-4 Planning and Budget Preparation 28.23

C-7 iBAS++ /Budget and Accounting Classification System (BACS) 44.85

C-8 Pension Management 15.08

C-9 SOE Governance 25.23

C-10 Financial Reporting 19.23

C-14 PFM Reforms Leadership, Coordination, and Monitoring 24.38

Total SPFMS Program Expenditures 170.00 Table 5. SPFMS Expenditure Framework (under organizational code 1090101)

(Figures in US$, Thousands)

Note: Tax deductions are recorded under the economic code 3821125.

23. Finally, the Program is complemented by a compact, but important, change management/enabling environment technical assistance to support, anchor, deepen, and sustain the reform processes. A separate World Bank-executed technical assistance (approximately US$10–12 million

The World Bank Bangladesh Strengthening PFM Program to Enable Service Delivery (P167491)

Page 12

over the lifetime of the Program) under the SPEMP Multi-Donor Trust Fund (MDTF) will support selected PFM reforms. It will ensure the provision of timely and quality technical assistance and advice in cash management, commitment control, TSA expertise, budgeting, and MTBF, as well as produce several discrete studies to help enhance understanding of key public resource management constraints at the central or sectoral levels. The technical assistance will help the Government identify relevant actions to address challenges faced as they evolve, broker solutions to collective action problems, and help ensure that reform processes are informed and adapted as implementation progresses.

C. Program Development Objective(s) (PDO) and PDO Level Results Indicators

24. The PDO is to improve fiscal forecasting, budget preparation and execution, financial reporting, and transparency to enable better resource availability for service delivery in selected Ministries, Departments, and Agencies.

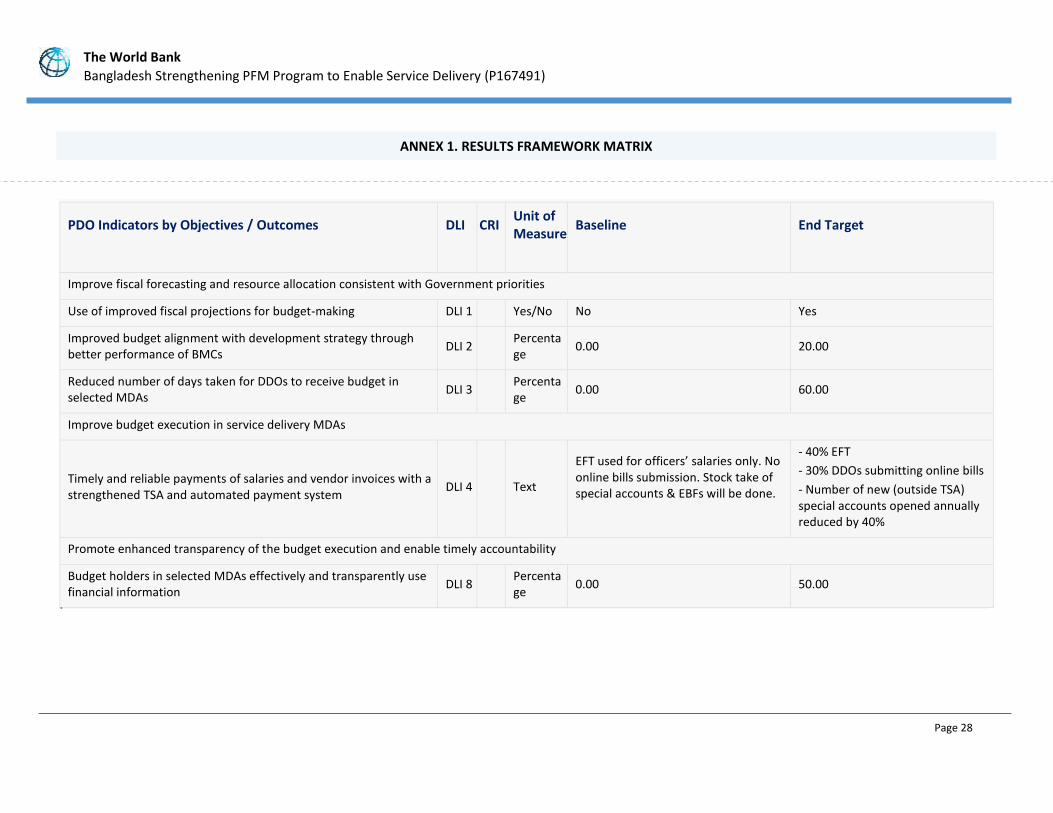

25. PDO-level results indicators are:

• Use of improved fiscal projections for budget making;

• Improved budget alignment with development strategy through better performance of BMCs (average BMC’s performance improves by 20 percent);

• Reduced number of days for DDOs to receive budget in selected Ministries, Departments, and Agencies (MDAs) (60 percent of DDOs receive budget by July 31);

• Timely, reliable payments of salaries and vendor invoices with strengthened treasury single account and automated payment system in selected MDAs (40 percent EFT and 30 percent DDOs submitting online bills and 40 percent reduction in new special accounts outside TSA); and

• Budget holders effectively use financial information (50 percent budget holders).

D. Disbursement Linked Indicators and Verification Protocols

26. The Program will remove PFM bottlenecks and enable efficient availability of resources to frontline service providers. The Program is composed of four mutually reinforcing KRAs that are priorities of the government program (PFM Action Plan) and contribute to achieving the PDO. The link of KRAs is shown with the five strategic goals of PFM reforms in table 6.

Table 6. PforR KRAs and DLIs

PforR KRAs DLIs Amount

(US$, millions)

Type Responsible Entity

KRA 1: Improve fiscal forecasting and resource allocation consistent with Government priorities for spending in service delivery

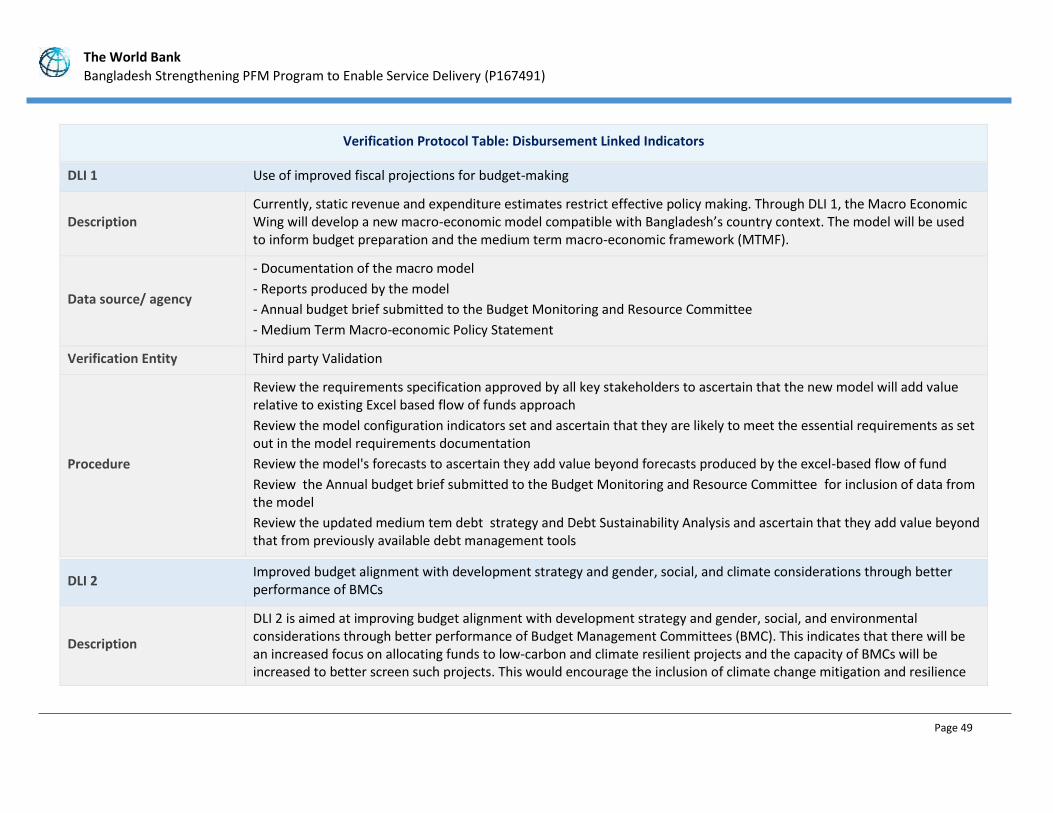

DLI 1: Use of improved fiscal projections for budget making

• Fiscal forecasting (US$8 million)

• Debt management (US$2 million)

DLI 2: Improved budget alignment with development strategy and

10

14

Outcome Outcome

• MacroEconomic Wing, FD

• Treasury and Debt Management Wing, FD, ERD

• Budget Wing, FD

The World Bank Bangladesh Strengthening PFM Program to Enable Service Delivery (P167491)

Page 13

sectors (Contribution to the PFM Strategy Goal 1 and 2)

gender, social, and climate considerations through better performance of BMCs

• Budget quality and BMC performance (US$8.5 million)

• Increased social sectors’ spending (US$5.5 million)

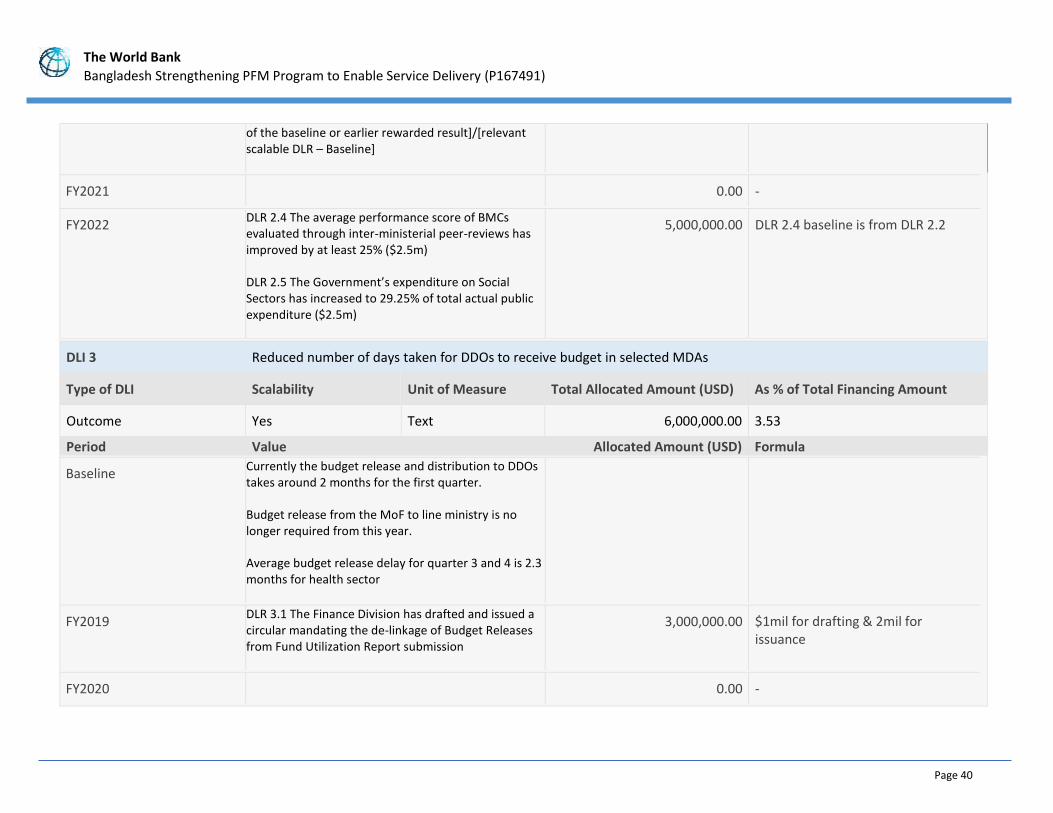

DLI 3: Reduced number of days for DDOs to receive budget in selected MDAs

6

Outcome

• FD, CGA, line ministries

KRA 2: Improve budget execution in service delivery MDAs (Contribution to PFM Strategy Goal 3)

DLI 4: Timely and reliable payments of salaries and vendor invoices with a strengthened TSA and automated payment system

• TSA (US$4 million)

• EFT (US$3 million)

• Online bill submission (US$2 million)

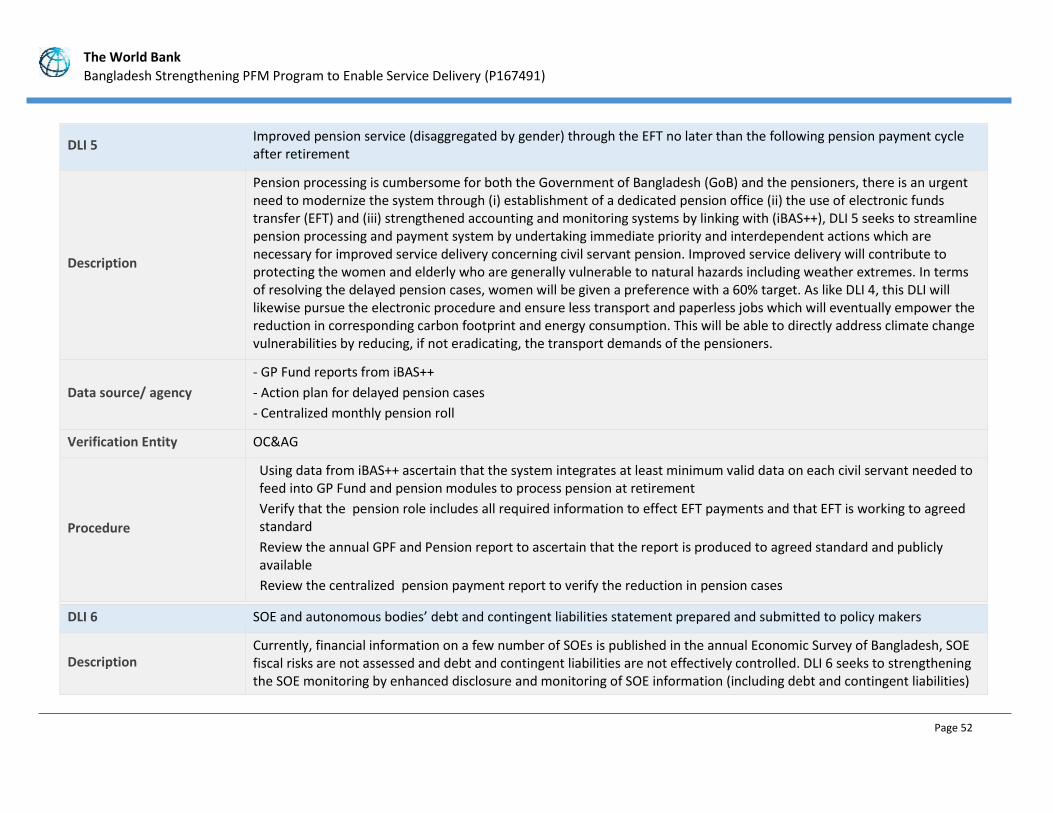

DLI 5: Improved pension service (disaggregated by gender) through facilitation of payments through EFT no later than the following pension payment cycle after retirement

• Pensions (US$6.5 million)

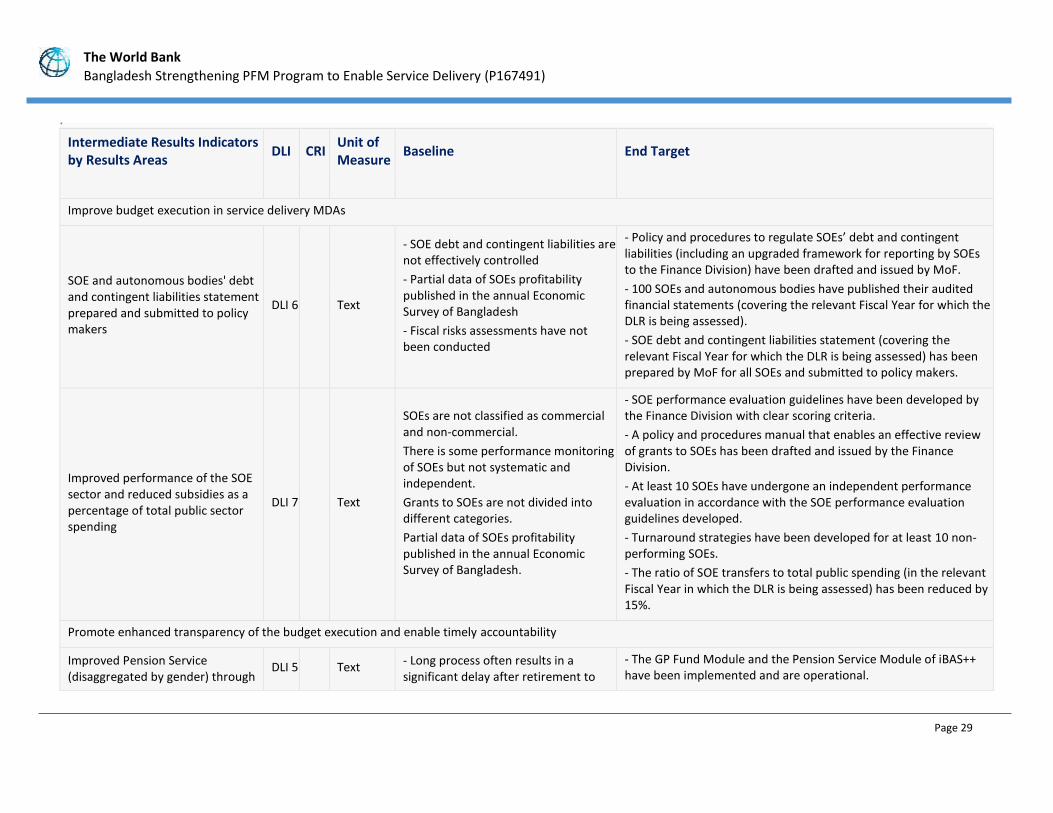

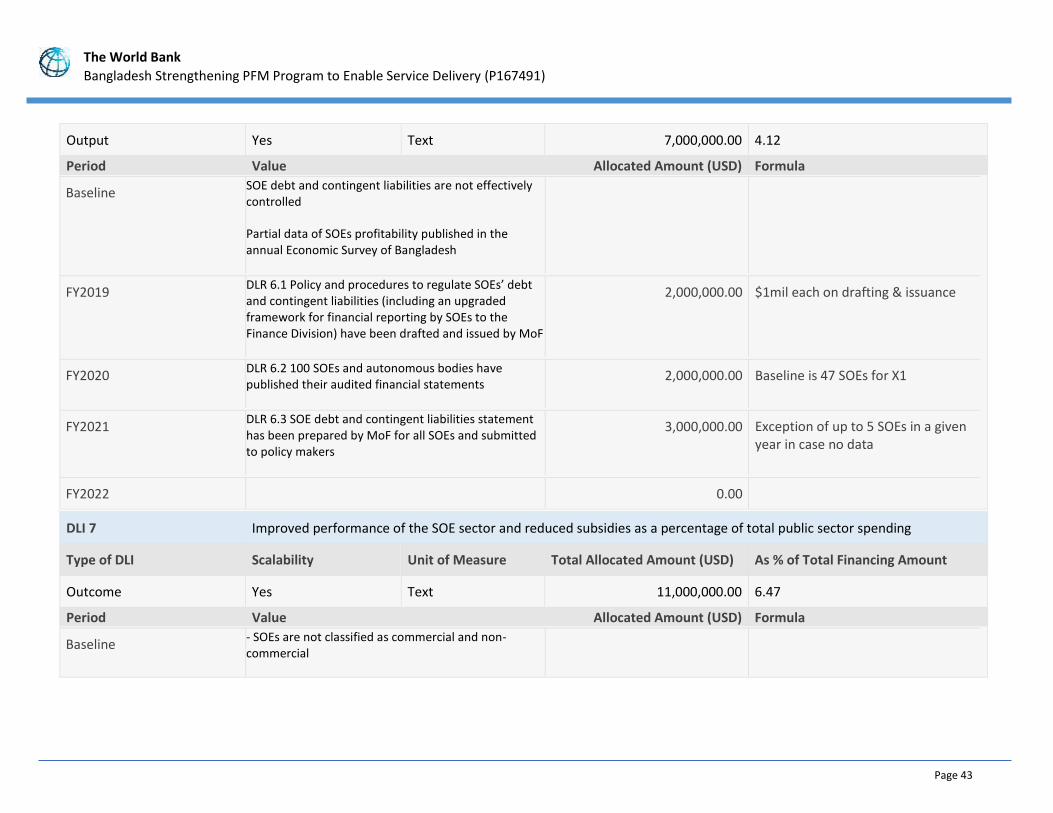

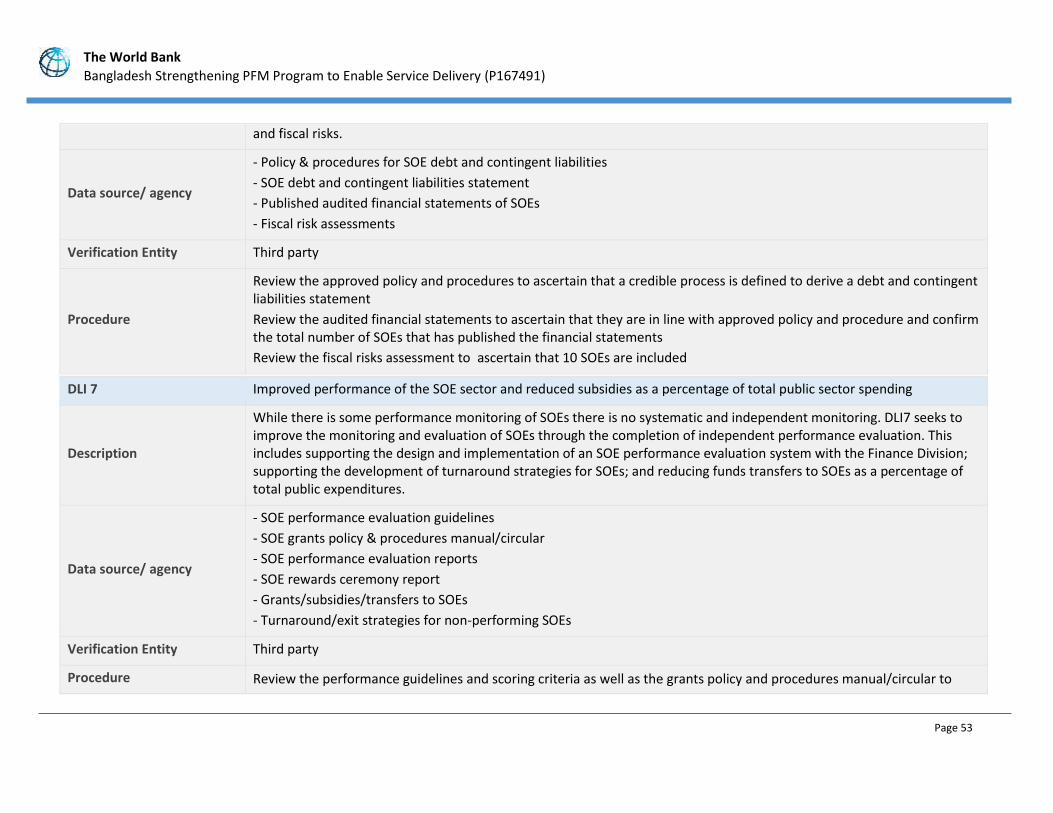

• GP Fund (US$3.5 million) DLI 6: SOE and autonomous bodies’ debt and contingent liabilities statement prepared and submitted to policy makers DLI 7: Improved performance of the SOE sector and reduced subsidies as a percentage of total public sector spending

• SOE Performance monitoring (US$6 million)

• Reduced subsidies (US$5 million)

9

10

7

11

Outcome Outcome Output Output/outcome

• iBAS++ program office

• CGA, FD

• SOE Wing, SOE Monitoring Cell FD

• SOE Wing, SOE Monitoring Cell FD

KRA 3: Promote enhanced transparency of the budget execution and enable timely accountability (Contribution to the PFM Strategy Goal 4)

DLI 8: Budget holders in selected MDAs effectively and transparently use financial information

• iBAS++ (US$6 million)

• Financial reporting, public disclosure, and use of information (US$6 million)

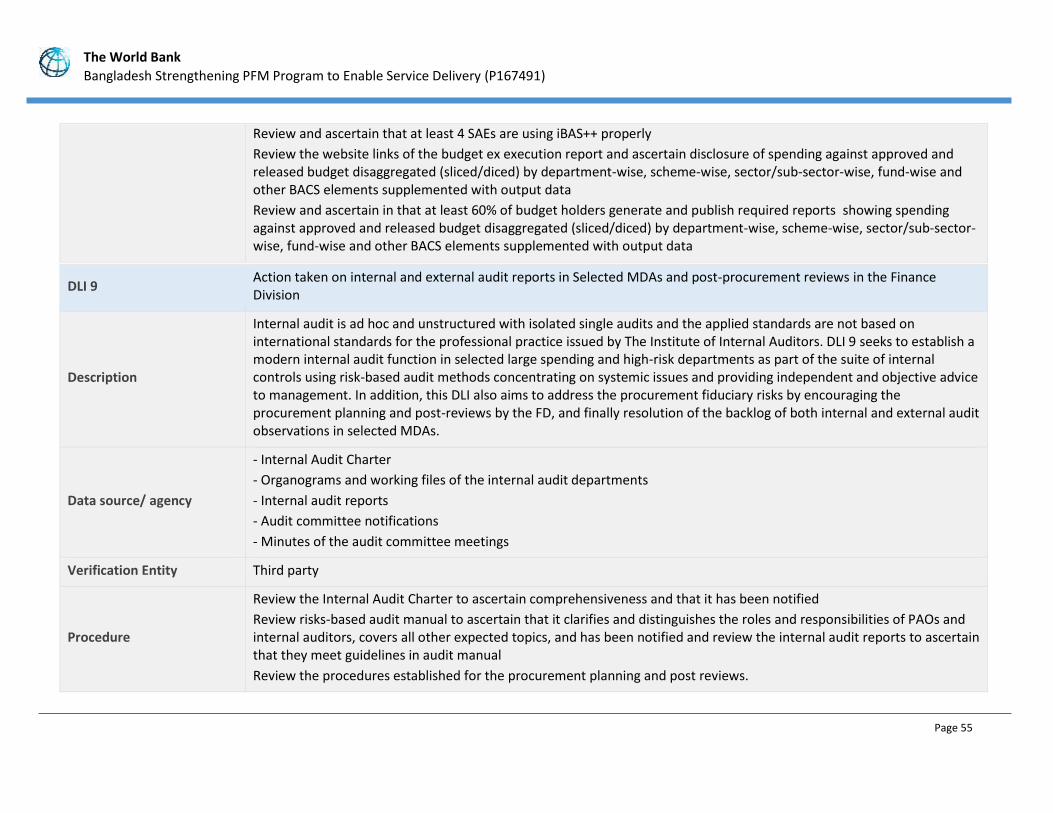

DLI 9: Action taken on internal and external audit reports in selected MDAs and procurement post reviews in Finance Division

• Internal audit (US$2.5

12

7

Outcome Output

• iBAS++ program office, Budget Wing, line ministries

• Expenditure Management Wing FD, line ministries

The World Bank Bangladesh Strengthening PFM Program to Enable Service Delivery (P167491)

Page 14

27. Each of the abovementioned 10 DLIs involve one or more actions to remove PFM bottlenecks and have been jointly selected from the PFM Action Plan. All DLIs represent critical milestones to achieve the PDO, provide adequate financial incentives to support underlying reform activities, and facilitate measurability and ease of verification. There are additional (non-DLI) indicators in the Government-owned Program Document and DLI technical notes and program action plan to ensure continued momentum of reform activities toward achievement of the DLIs and PDO.

28. The pricing of the DLIs was based on the following principles:

• Front-loading. DLIs have higher prices in the first two years to provide strong incentives, stimulate the program interventions and build up momentum for reforms. The experience of other results-based programs suggests that even the difficult results are achieved in outer years once the reform momentum is attained.

• Effort intensity. DLIs which are considered more difficult because of the adaptive challenge involved or would require more effort to complete the activities have higher price allocations. Within DLIs, a combination of process-, output-, and outcome-level disbursement-linked results (DLRs) enable incentivizing reform achievements as soon as they occur. Reform experience has been that the initial process-level results (when incentivized) enhance stakeholders’ confidence to achieve more difficult output-level targets.

• Scalability. DLIs are formulated as ‘scalable’ whenever possible (instead of ‘all-or-nothing’) to reward partial achievement proportionately, subject to a minimum threshold of 30 percent.

• Rollover. Because the DLI annual targets are ambitious, undisbursed amounts of financing for a DLI not achieved or partially achieved in a given year will be rolled over for use in the next year and so on up till the Program closing on June 30, 2024.

29. The combination of frontloading, scalability, and rollover has enabled limiting the total number of DLRs. While assigning DLRs to a particular year of the Program implementation is merely indicative, frontloading has enabled setting ambitious targets for earlier years, scalability allows rewarding partial performance, and rollover allows continued pursuit of achieving the higher target next year. In this way some DLRs will take more than a year to be fully achieved. Hence, for those DLRs there was no need to have progressive targets. The DLR prices and target years have been carefully calibrated through several rounds of consultations based on the assessed level of ambition involved.

million)

• Audit and procurement post-review follow-up (US$4.5 million)

KRA 4: Establish an enabling environment for improved PFM outcomes (PFM Strategy Goal 5)

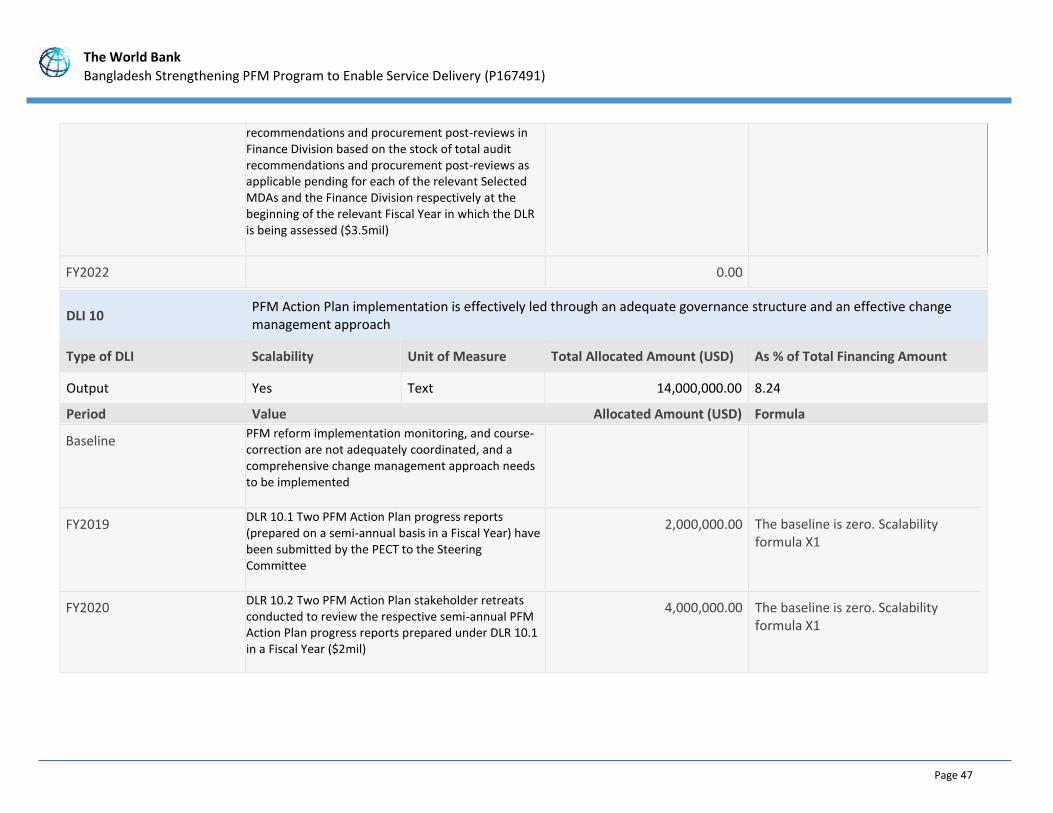

DLI 10: PFM Action Plan implementation is effectively led through an adequate governance structure and an effective change management approach

14 Process/output • Program execution and coordination team (PECT), Budget Wing, FD

100

The World Bank Bangladesh Strengthening PFM Program to Enable Service Delivery (P167491)

Page 15

30. Separate DLIs will be subject to a different verification process based on their nature and the type of data involved. Of the ten, five DLIs will be verified by an independent verification agent to be appointed by the FD. Four DLIs, that involve financial data, will be verified by the Supreme Audit Institution—OC&AG. Finally, one DLI on the improved budget quality through better performing BMCs will be verified by the Cabinet Division as part of their support to other ministries on annual performance agreements. Using multiple verification entities elsewhere had improved the quality because of the existence of corroborated information and healthy competition among those entities. Using independent government institutions such as the OC&AG and Cabinet Division strengthens country-owned monitoring systems in a more sustainable manner.

III. PROGRAM IMPLEMENTATION

A. Institutional and Implementation Arrangements

31. The PFM reform process has a two-tier governance structure comprising a Steering Committee (SC) and a PECT according to the PFM Action Plan. The SC headed by the Finance Secretary will comprise senior representatives from major spending ministries, Cabinet Division, CGA, Comptroller and Auditor General, National Board of Revenue, Economic Relations Division, and Planning Commission. The SC will oversee implementation progress, provide policy guidance, and ensure an enabling environment for reforms to succeed and sustain. The FD, through a PECT, will lead the coordination of the reforms with active support from the line ministries and DPs. The PECT will consist of six members from the FD and two from other PFM institutions responsible under the PFM Action Plan. The PECT can invite observers to their meetings and is expected to invite selected DPs for inputs and advice. The PECT will also be responsible for establishing a forum for institutional collaboration—PFM Reform Learning Hub at the Institute of Public Finance—for areas requiring collective action and mutual learning and accountability and for more systematic capturing, sharing, and replication of reform lessons.

Figure 4. Program Governance Structure

32. The SPFMS will use existing formal country systems structures to ensure that responsibility for meeting the DLIs is within the mandate of the assigned implementing agencies. The attitudinal barriers to achieving the objectives of the PFM reform program will be addressed through behavioral and change

Steering Committee

Program Execution & Coordination Team

Program Implementation Team

(MacroEco)

Program Implementation Team

(Budget)

Program Implementation Team

(SOEs)

Program Implementation

Team ( -- - )

PFM Learning Hub

(IPF) Team

The World Bank Bangladesh Strengthening PFM Program to Enable Service Delivery (P167491)

Page 16

management interventions. These will include strategic communication about the reform benefits with the political leadership to solicit commitment and ‘buy-in’ to better manage resistance; participatory engagement with stakeholders—citizens, beneficiaries, and DPs; and recognizing and rewarding of agencies and individuals for good PFM performance. This will help provide a conducive authorizing environment for sustaining the deep institutional reforms that require ownership and support by multiple stakeholders.

33. The Program implementation structure will be as follows:

(a) SC. The SC will be chaired by the Finance Secretary and will provide general strategic oversight and direction to program implementation. The SC will also monitor the program’s implementation.

(b) PECT. The PECT will be anchored at the Budget Wing, FD. The PECT will consist of eight members, while the head of the Budget Wing will be ex officio Program Director. To ensure a broad-based representation and coordination for the overall PFM reforms, at least two members of the PECT will represent PFM institutions other than the FD.

(c) PITs. Every lead institution for each of the seven components of the PFM Action Plan will nominate a three- to five-member PIT from among their staff. There will be a total of seven PITs. The PIT will be accountable for implementation of the respective reform interventions and achieve the relevant performance targets and DLIs.

(d) Focal points in counterpart institutions. The lead institution for each component has identified around three to four focal points in their counterpart institutions to ensure smooth institutional collaboration for the implementation of respective PFM reform activities. These counterpart institutions include the Bureau of Statistics, Planning Ministry, OC&AG, Cabinet Division, line ministries, and so on.

B. Results Monitoring and Evaluation

34. The SPFMS will use existing systems within the Government whenever possible to carry out results-based monitoring. The monitoring will be a continuous process of gathering data and comparing actual results of DLRs and other key indicators with expected results. The goal will be to measure how well the Program is being implemented and to ascertain when specific targets have been met. The monitoring will also provide feedback on progress achieved so that decision makers can make necessary changes to improve performance. The change management and M&E activities described in this section would complement the independent DLI verification arrangements described above in paragraph 30.

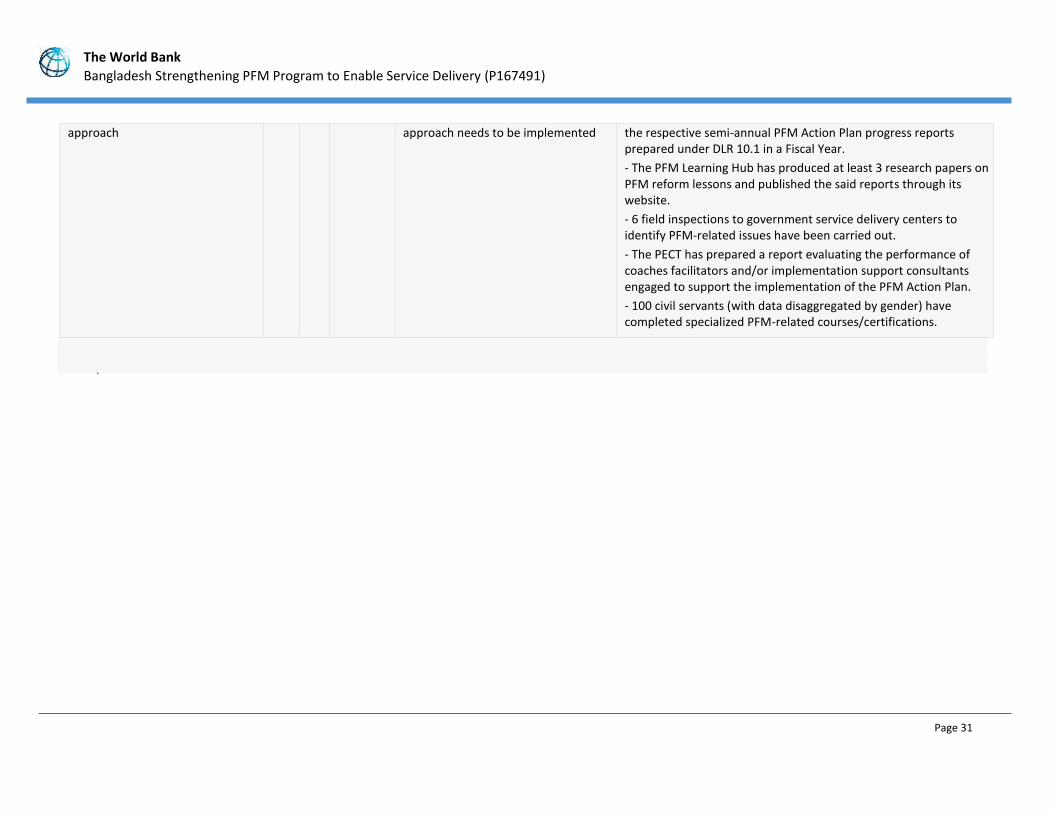

35. Technical assistance for coordination, capacity development, and M&E have been built into the implementation arrangements of the PFM Action Plan, supported through DLI 10. This will include capacity strengthening of the governance arrangement for PFM reforms and adequate enabling environment, including the establishment of the PECT that will function as a secretariat to coordinate implementation and provide technical oversight of the Program. The PECT will be led by a program coordinator who will provide technical guidance and overall management and will also include specialists in the areas of monitoring and evaluation. Besides establishing a clear governance structure, DLI 10 also includes specific M&E and change management activities to be performed as DLRs. These include establishing and functioning of a Learning Hub in the Institute of Public Finance which will produce at least three research papers on PFM reforms in Bangladesh. In addition, preparation and review of semiannual

The World Bank Bangladesh Strengthening PFM Program to Enable Service Delivery (P167491)

Page 17

program performance reports in broad-based program retreats is a key trigger for mutual accountability. The engagement of implementation facilitators and PFM innovation awards will also catalyze the Program’s performance. Finally, it is intended that the Government will adopt the same arrangements used by the SPFMS to carry out capacity building and monitoring of other components of the PFM Action Plan that are outside of the SPFMS.

36. In addition, annual performance assessments of the PFM Action Plan will be carried out. The assessment will review, among others, whether the targets and expected outcomes are still relevant, how effectively and efficiently they are being achieved, what unanticipated effects are evident, and whether the program represents the most sustainable and cost-effective means for achieving the intended outcomes. It will also look at the continuing relevance of the Program’s theory of change, including the extent to which the performance-based allocations and capacity development supported by the program is helping to successfully drive the reforms. The DPs are requested to join the annual performance assessments of the PFM Action Plan and make a positive contribution in a more harmonized manner.

C. Disbursement Arrangements

37. Disbursement will be based on achievement of the DLIs. Annex 3 shows the proposed annual financial allocations across DLIs. On verification, the FD will communicate the achievement of the DLIs to IDA and, on the basis of IDA’s approval letter, disbursement requests will be processed using IDA’s e-Business platform. An advance limit of 20 percent of the Credit will apply, which is needed to finance program activities for first year’s results. Disbursement is expected to happen twice in a fiscal year.

38. The IDA funds in US$ will be disbursed to the TSA (consolidated fund) and the Program expenditures will be through the Government’s operating budget schemes. The Government would ensure timely budget allocation for the program expenditures to be made from the TSA. Each component of the Program will be established as a budgetary scheme in the Government’s operating budget. This is similar and, to an extent, an expansion of the ongoing PEMSP.9 Table 7 provides the indicative disbursement schedule for IDA funding.

Table 7. Bangladesh SPFMS – Disbursement Schedule

No. Estimated Date

Estimated Amount

(US$, millions)

Disbursement Basis

FY19

1. February 15, 2019 20 • Advance against DLRs to be met by June 2019 (20% of credit amount)

FY20

2. August 15, 2019 12 • Price of FY19 DLRs met netted with February advance

• Advance against DLRs to be met by June 2020

FY21

3. August 15, 2020 15 • Price of FY19 DLRs met after August 15, 2019

9 After the closure of the SPEMP-A in 2014, the Government continued to sponsor the IBAS++ development through its own resources provided through a recurrent (non-Annual Development Program [ADP]) scheme—PEMSP. This has led to several successes, including the development of several new functionalities, managing the rollout of budget preparation module to the budget-holder levels, capturing all government expenditure data in IBAS++, and designing and using the new BACS. In addition, the PEMSP has been closely supporting the FD in the preparation of annual budget each year.

The World Bank Bangladesh Strengthening PFM Program to Enable Service Delivery (P167491)

Page 18

No. Estimated Date

Estimated Amount

(US$, millions)

Disbursement Basis

• Price of FY20 DLRs met netted with August 2019 advance

• Advance against DLRs to be met by June 2021

FY22

4. August 15, 2021 15 • Price of FY20 DLRs met after August 15, 2020

• Price of FY21 DLRs met netted with August 2020 advance

• Advance against DLRs to be met by June 2022

FY23

5. August 15, 2022 18 • Price of FY21 DLRs met after August 15, 2021

• Price of FY22 DLRs met netted with August 2021 advance

• Advance against DLRs to be met by June 2023

FY24

6. August 15, 2023 10 • Price of FY22 DLRs met after August 15, 2022

• Price of FY23 DLRs met netted with August 2022 advance

7. June 30, 2024 10 • Final settlement based on Program expenditures (the World Bank disbursement cannot be more than Program expenditures)

100

D. Capacity Building

39. The interventions of this Program (systems, processes, and human) will build on the capacity of key PFM institutions and line ministries. Each component of the PFM Action Plan has built in capacity-building activities ranging from the upgrading of systems and processes to several types of individual trainings, certification, and education. Establishment of a Learning Hub at the Institute of Public Finance and engagement of implementation facilitators are some of the innovative capacity-building and change management interventions planned under the Program based on the initial understanding of the political economy context (see box 2).

40. In addition, the Program is also complemented by a compact, but important, change management/enabling environment technical assistance to support, anchor, deepen, and sustain the reform processes. A separate World Bank-executed technical assistance of approximately US$10–12 million over the lifetime of the Program under the SPEMP MDTF (financed by the Governments of Canada and the United Kingdom, and the EU) will support selected PFM reforms. It will ensure the provision of timely and quality technical assistance and advice as required and include the engagement of expertise to support the Government in niche areas (such as cash management, commitment control, TSA expertise, budgeting, and MTBF), as well as several discrete studies to help enhance the understanding of key public resource management constraints at the central or sectoral levels. The technical assistance will help the Government identify relevant actions to address challenges faced as they evolve, broker solutions to collective action problems, and help ensure that reform processes are informed and adapted as implementation progresses. This is a continuation of the ongoing engagement, for example, the development of the PFM Action Plan. This included DPs’ provision of time, comments on the PFM Action Plan, and contributions on specific analytical inputs, as well as financing for engagement of technical and secretarial assistance through the SPEMP. DPs will continue to support the technical assistance required for the SPFMS’ success.

The World Bank Bangladesh Strengthening PFM Program to Enable Service Delivery (P167491)

Page 19

Box 2. Political Economy and PFM Reform Political economy provides the perspective that powerful groups in society may seek to achieve degrees of influence or control over the state, often using its systems for some form of personal advantage. People in Government can, therefore, be gatekeepers preventing change because the status quo of the system they have developed in their own interest suits them well. Understanding the specific relationships of power between relevant stakeholders, as well as the incentives and disincentives for behaviors that are influencing (driving or hindering) the reform agenda implementation are, therefore, vital for PFM reform. As PFM focuses on the management and use of resources and increasing the transparency of decisions and resource utilization, PFM reform programs intervene directly in the distribution of power and benefits within a system. Interest groups likely to lose out following reforms, either through loss of access to influence or resources, or reduced opportunity to act in self-interest (because of improved control and transparency), may seek to block or delay reforms or subvert their implementation. The Bangladesh SPFMS addresses political economy challenges in different ways:

• First, the Program has a transparent governance structure with strong government ownership. While the lead is with the MoF, coordination and communication with major spending ministries and other government agencies, divisions, and stakeholders are well anchored through an SC at high level and through a PECT at the technical level. This will provide the authorizing environment for change to happen and for stakeholders to align and inform.

• Second, a political economy assessment study was commissioned by the World Bank during the finalization of the PFM Action Plan, providing additional insight in (a) predominantly technical versus political economy related challenges, (b) specific activities of high impact change that can create momentum, and (c) most significant (other) stakeholders involved and potential interests. Reform coordination between stakeholders will be a key attention point for the PFM SC, as reform coordination is not just across ministries but also across divisions within the same ministries. Further, the Cabinet, Prime Minister’s Office, and the Parliament and its standing committees are to be key alignment partners. The study, which looked at these stakeholders and at the reform actions proposed, confirmed the value of the suggested change management approach and led to various refinements in the approved version of the action plan and agreed technical notes. It also includes specific recommendations for involving stakeholders in relation to the particular political economy context of certain reform issues.

• Third, course-correction, reflection, and adaptation during implementation are key parts of the program design and will help surface and address political economy challenges during implementation. Facilitation/coaching of implementation teams will include, for example, simple stakeholder analysis and force field analysis exercises and create further ownership for finding solutions to issues that may come up and involve different stakeholders. The addition of the Institute of Public Finance to the governance structure further confirms this ambition to systematically learn during implementation.

• Finally, the results-based financing mechanism through which the World Bank will disburse to the Government—based on achieving pre-agreed targets for DLIs—shares risk between the World Bank and the client and shifts responsibility for access to resources to the latter. The specific DLI (DLI 10) on governance and change management (and its weight in pricing) further emphasizes the importance of the Program for effective governance and change management attention throughout the implementation.

IV. ASSESSMENT SUMMARY

A. Technical (including program economic evaluation)

41. The technical risk of the PforR is rated ‘Moderate’ considering the context and technical preparations. The Government has the readiness to implement the approved PFM Action Plan that has been prepared with the required analytical underpinning. The Program design, as outlined in the Program

The World Bank Bangladesh Strengthening PFM Program to Enable Service Delivery (P167491)

Page 20

Document and approved by the Honorable Prime Minister, provides the institutional framework and incentives for continued focus and prioritization of PFM reforms to have a clear impact on social service delivery. There is strong technical preparation with the DLI technical notes prepared by the relevant government teams. Finally, the appropriate attention given to adaptive challenges has raised stakeholders’ understanding of the PFM challenges and thereby procured the necessary appetite for the changes needed.

42. The Program is strategically relevant and technically sound for the following reasons: (a) it is directly aligned with the Bangladesh PFM Reform Strategy and PFM Action Plan, (b) it builds on previous PFM reform efforts and is selective by focusing on a subset of critical foundational reforms that are directly under the FD’s control, and (c) it considers the implementation capacity and adaptive behavioral change management needs for the reforms to be successful.

43. The PFM Action Plan provides a robust evidence base and operational framework to advance key PFM reform priorities for strengthening PFM institutions and systems. The PFM Action Plan was formulated to operationalize the Government’s PFM Reform Strategy. Both the PFM Reform Strategy and PFM Action Plan build on the lessons learned from the long reform history in the country. The PFM Action Plan was produced through a consultative process led by the FD, involving other PFM institutions and DPs. The development of the PFM Action Plan also benefited from the knowledge exchanges with other countries and expert advice on technical and adaptive aspects.

44. Within the boundaries of the PFM Action Plan, the Program focuses on key priority activities led by the FD itself and aims to scale up already tested interventions. Both the Program interventions and DLIs focus heavily on the aforementioned PFM challenges. These include interventions to support improvements in both process and service delivery. Many of these interventions have been piloted and proven successful with a promise for progressive scale-up, such as expansion of the iBAS++ and use of the EFT. Because these are proven interventions building on the ongoing reform activities with a high level of stakeholder ownership, the technical risk is not considered significant.

45. There is a logical connection linking KRAs to DLIs and in turn to intermediate objectives, elements of the PDO, and the overall outcome of enabling better resource availability for the service delivery. DLI 1 supports the adoption of an improved macroeconomic model leading to improved fiscal forecasting. DLI 2 supports improved budget alignment with development strategy, leading to better budget preparation and execution in line ministries. DLI 3 supports timely budget releases. DLI 4 supports automation to enable timely payments of salaries and invoices. DLI 5 supports improved pension service, including timely payments to pensioners. DLIs 6 and 7 support improved M&E of and reporting by SOEs. DLI 8 supports better reporting on budget execution linked to BACS and IBAS++. DLI 9 supports improved audit procedures, reporting, and resolution of audit recommendations. DLI 10 supports appropriate governance and change management processes for the Program. The DLIs and intermediate objectives feed into the PDO elements of improved fiscal forecasting, improved budget preparation and execution, enabling of better resource availability for service delivery, and improved financial reporting and transparency. In turn, these elements contribute to the intended outcome of improved service delivery.

46. The Program has an adequate governance structure and implementation arrangements. Learning from the experience of PFM reforms in Bangladesh and globally, a sound institutional setup has been devised that leverages the existing structures and capacity. This has led to effective stakeholder engagements as stakeholders can understand how the reforms are going to benefit them in performing

The World Bank Bangladesh Strengthening PFM Program to Enable Service Delivery (P167491)

Page 21

their day-to-day responsibilities with greater efficiency and effectiveness. This has led to the elaboration of the DLI technical notes indicating the high degree of readiness for implementation. For each DLI, an elaborate technical note describes how to surmount the anticipated challenges through the reform sub-activities. These technical notes are prepared by formally notified teams within the government institutions through an iterative process facilitated by experts. The preparation of the technical notes also validated the political feasibility of the reforms through the tacit knowledge of the participants.