Page 1

PTDConsulta-veWorkshopon

UniversalServiceStrategy,EstablishingtheUniversalServiceFund,Design&Implementa-onofpilotprojects

SonjaOestmann&AndrewDymond

NOVOTELHOTELYANGON

16February2017

Page 2

2

Content

PART1

• BriefintroducJontoUniversalService• Marketupdate

• Unservedtownships:GISanalysisandresultsPART2

• OpJonsforUSFestablishment

• Universalservicestrategy:IniJalideasforUSFprograms

Page 3

3

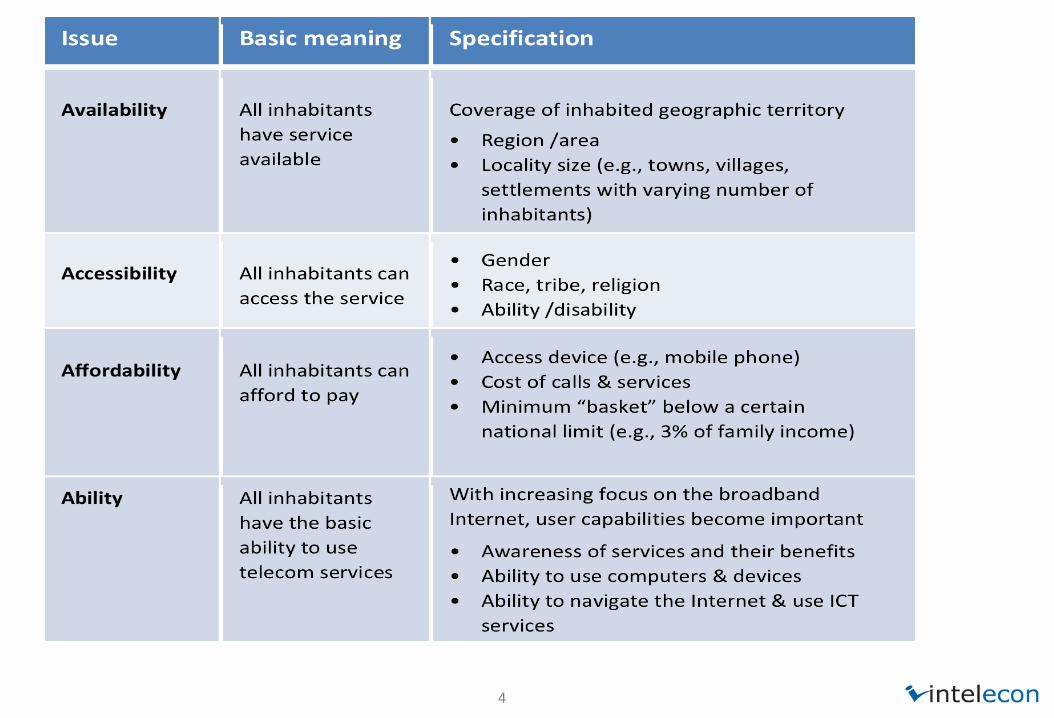

WhatisaUniversalService?

UniversalServiceisapolicygoalthatintendstoensurethat

allpeopleinacountryhaveaccess

andareabletousetelecommunicaJonsservices,

inparJcularforpeoplelivinginruralandremotepartsofthecountryandpoorerhouseholds

Page 5

5

Generallydigitalskillsusingsmartphonesarelow,forexampleonly22%cansearchforinformaJonorothercontentontheInternet(LirneAsia/MIDO2016)

Access Usage Benefits

Infrastructure Capacity Content&applicaJons

Page 6

6

SpecificscopeofUniversalService

• ChapterXVoftheTelecommunicaJonsLaw

• ProvidingbasictelecommunicaJonsnecessiJesanywhereforpublicinterest

• EnablingavailabilityandwideruseoftelecommunicaJonsservices

• UniversalServicedefinitonandbasictelecom§ Mobilevoiceservices§ WirelessbroadbandInternetserviceswithmin.speed(e.g.,3-5MBps)§ Enablingwiderusethroughawarenessraising&capacitybuilding

Page 7

7

WhyisaUniversalServicestrategyneeded?

• Commercialtelecomoperatorscannotreachallpeopleinacountry–typicallybetween5-10%willbeleewithoutservice

• AUniversalServicepolicyensuresthesepeoplegetserved,bothwithvoiceandbroadbandInternet

Page 8

8

Increasing&acceleraJngVoiceandInternetbroadbandprovision

Morepeoplehaveaccesstoservices&applicaJons,aswellasthecapacitytousethem

CreaJngopportuniJesforbotheconomic&socialgrowth

UniversalServiceStrategyoutcomes

Page 9

9

KeyObjecJvesofassignment

1. DesigningMyanmar’sUniversalServiceStrategy

2. DevelopingguidelinesforestablishingUniversalServiceFund(USF)anditsgovernanceandoperaJngprocedures

3. ImplemenJngthestrategyinanumberofpilotareas

4. Monitoring&evaluaJon

Page 10

10

Universalserviceproject–expectedJmeline

UniversalServiceStrategy

GuidetoestablishUSFUSFOperaJngManual

• DraeApril2017• ConsultaJoninMay• FinalJune2017

Pilotprojects

• DraeDesignAugust2017• FinalDesignSeptember2017• BiddingperiodOct&Nov2017• BidEvaluaJonDecember2017• ContractnegoJaJonJan2018• Startofimplementa-onFeb2018

ImplementaJonMonitoringEvaluaJon

• ApproximatelyunJlJune2019

Page 11

MARKETOVERVIEW&RESULTSFROMGISANALYSIS

Page 12

12

Thetelecommarket• Threemainmobileoperators

• MPT,Telenor,Ooredoo• 4thentrantMNTC(Mytel)expectedsoon

• TotalsubscriberSIMs49.7millioninNov2016• Around95%penetraJonbutuniquesubscribers61%+• 53%+amongstruralusers• 83%householdswithatleastonephone

• FastgrowthconJnuedfrom2015to2017• Majorrolebythetowercompanies–almost13,000

towersnowinexistence• Fibrecompaniesbuildingmajornetworks-currently

over18,000Kms*• Highpercentageofsmartphones(78%)

• CurrentpopulaJoncoverageover80%andwillreacharound94%+byMarch2019

Combinedoperator900MHzcoveragecommiXedbyQ12019

Page 13

13

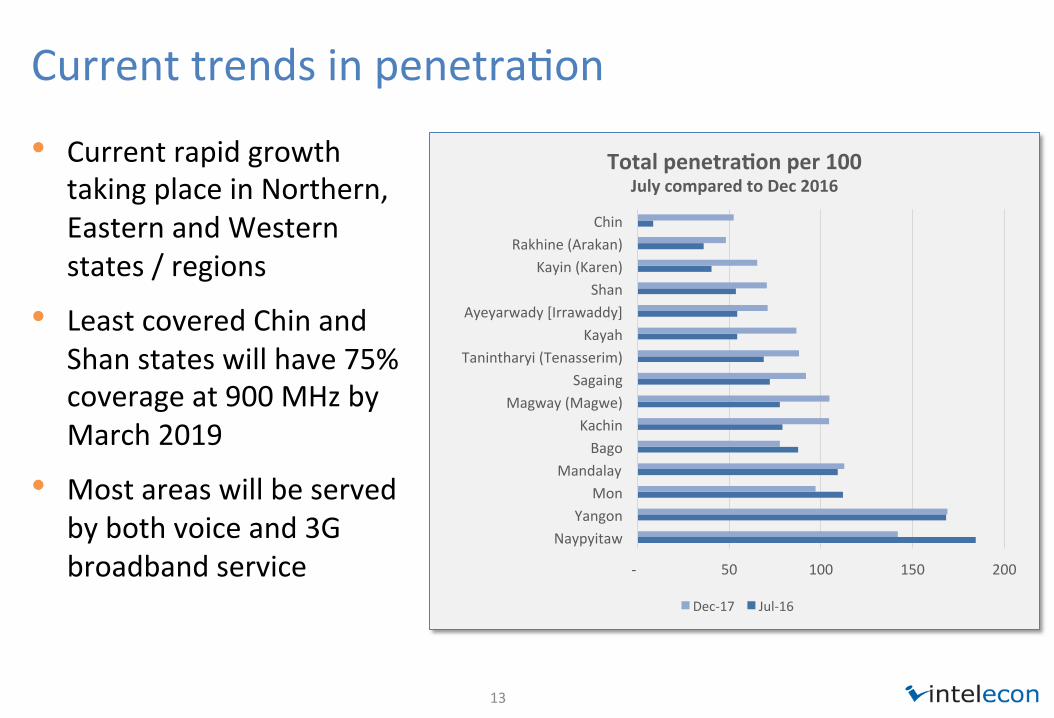

CurrenttrendsinpenetraJon

• CurrentrapidgrowthtakingplaceinNorthern,EasternandWesternstates/regions

• LeastcoveredChinandShanstateswillhave75%coverageat900MHzbyMarch2019

• Mostareaswillbeservedbybothvoiceand3Gbroadbandservice - 50 100 150 200

NaypyitawYangon

MonMandalay

BagoKachin

Magway(Magwe)Sagaing

Tanintharyi(Tenasserim)Kayah

Ayeyarwady[Irrawaddy]Shan

Kayin(Karen)Rakhine(Arakan)

Chin

Totalpenetra-onper100JulycomparedtoDec2016

Dec-17 Jul-16

Page 14

14

Thetowermarket• Towerco'sareasignificantfactorinmarketgrowthtodateandexpectedtoextendtheirpresence

asoperatorsfulfilltheirexpansioncommitments

• NeedformulJ-tenancywillbeanissueasthenetworksreachdeeperintorural,smallercommuniJesandlessdenselypopulatedareas

§ Greaterlevelofplannedpassiveand/oracJveRANsharingispredicted

• SatelliteVSATtrunkedmicro-cellsandsmalllow-costtowerswillincreaseinnumberforremotemountainousareas

2500

1800

1250 1250300 100 [VALUE] 200 200 1000

3600

05001000150020002500300035004000

Towerownership2017

Page 15

15

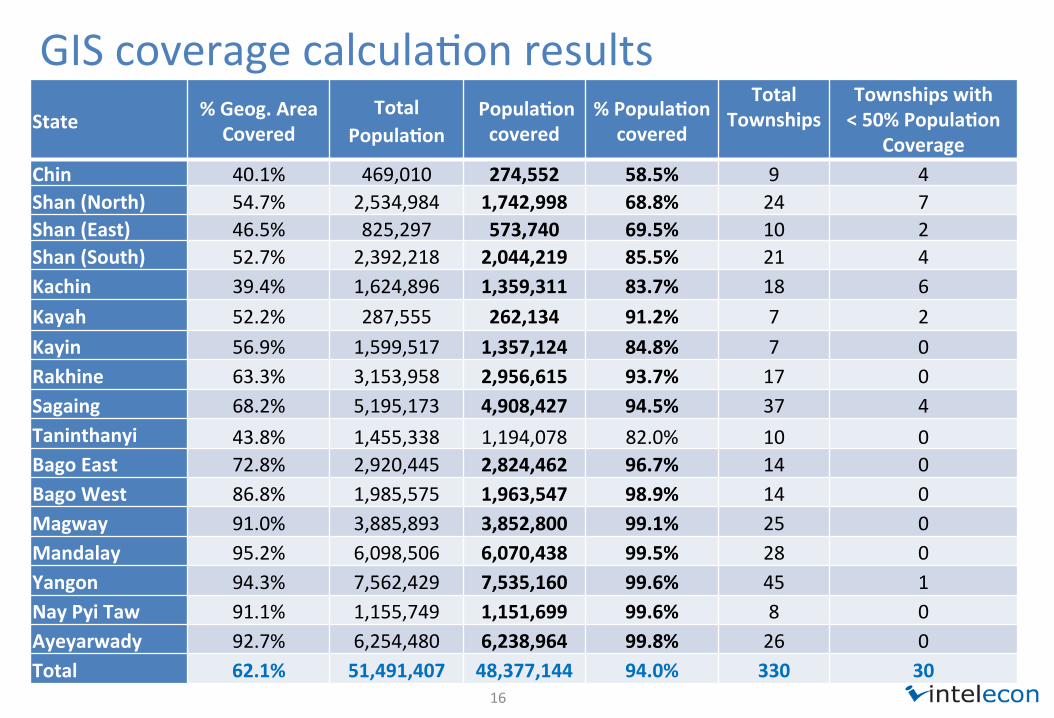

TheGISAnalysisandUSFprojectplanning

1. SuperimposecombinedoperatorcoverageoveraccuratepopulaJonmapthataccountsforallvillagetracts

2. Calculateoperatorcoverage,GapareasandunservedpopulaJons

3. CreateGeo-referencedExcelbasedbusinessplanningtoolforeachTownship

4. ResultisahighlevelcalculaJonofpercentagepopulaJoncoveredineachtownship

Combined900MHzCoverage

Page 16

16

GIScoveragecalculaJonresultsState %Geog.Area

CoveredTotal

Popula-onPopula-oncovered

%Popula-oncovered

TotalTownships

Townshipswith<50%Popula-on

CoverageChin 40.1% 469,010 274,552 58.5% 9 4Shan(North) 54.7% 2,534,984 1,742,998 68.8% 24 7Shan(East) 46.5% 825,297 573,740 69.5% 10 2Shan(South) 52.7% 2,392,218 2,044,219 85.5% 21 4Kachin 39.4% 1,624,896 1,359,311 83.7% 18 6Kayah 52.2% 287,555 262,134 91.2% 7 2Kayin 56.9% 1,599,517 1,357,124 84.8% 7 0Rakhine 63.3% 3,153,958 2,956,615 93.7% 17 0Sagaing 68.2% 5,195,173 4,908,427 94.5% 37 4Taninthanyi 43.8% 1,455,338 1,194,078 82.0% 10 0BagoEast 72.8% 2,920,445 2,824,462 96.7% 14 0BagoWest 86.8% 1,985,575 1,963,547 98.9% 14 0Magway 91.0% 3,885,893 3,852,800 99.1% 25 0Mandalay 95.2% 6,098,506 6,070,438 99.5% 28 0Yangon 94.3% 7,562,429 7,535,160 99.6% 45 1NayPyiTaw 91.1% 1,155,749 1,151,699 99.6% 8 0Ayeyarwady 92.7% 6,254,480 6,238,964 99.8% 26 0Total 62.1% 51,491,407 48,377,144 94.0% 330 30

Page 17

17

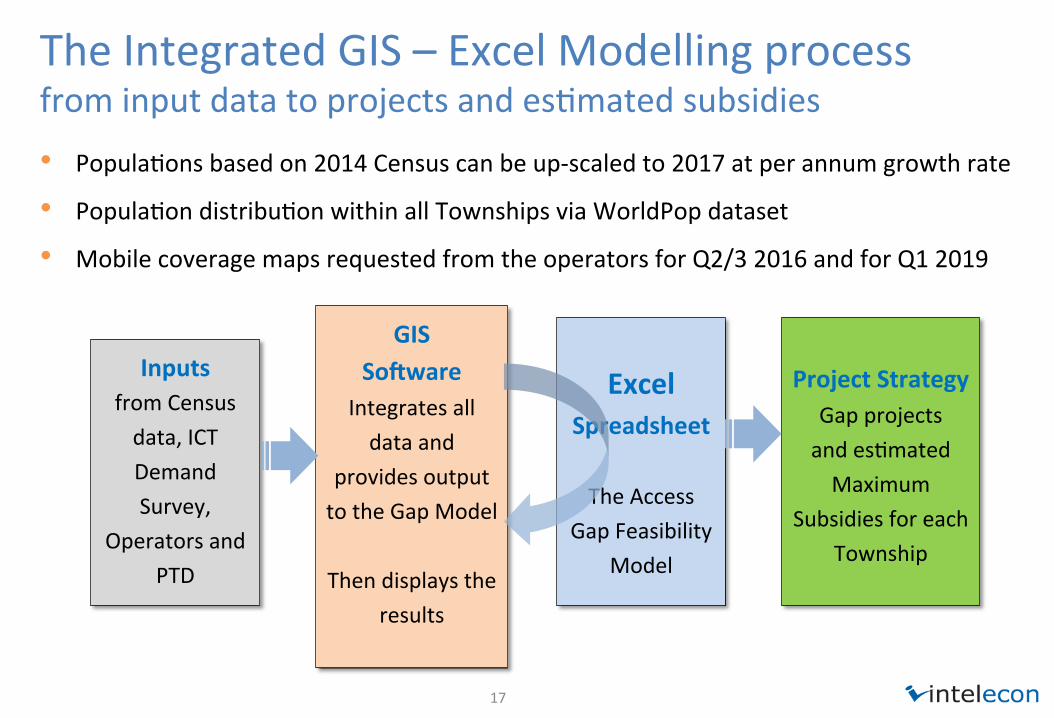

TheIntegratedGIS–ExcelModellingprocessfrominputdatatoprojectsandesJmatedsubsidies• PopulaJonsbasedon2014Censuscanbeup-scaledto2017atperannumgrowthrate

• PopulaJondistribuJonwithinallTownshipsviaWorldPopdataset

• MobilecoveragemapsrequestedfromtheoperatorsforQ2/32016andforQ12019

GISSogware

Integratesalldataand

providesoutputtotheGapModel

Thendisplaysthe

results

ExcelSpreadsheet

TheAccess

GapFeasibilityModel

InputsfromCensusdata,ICTDemandSurvey,

OperatorsandPTD

ProjectStrategy

GapprojectsandesJmatedMaximum

SubsidiesforeachTownship

Page 18

18

Thegeo-referencedsubsidyesJmaJonModel

DemandSide • UnservedPopulaJonsfromtheGISanalysis

• Affordability&Revenues• BasedonCensusandICTdemanddata

Costside • Distancesfromnearest

accesspointsandexisJngcoverage

• Backbone&accesssystemunitcosts

• Terrainfactorstoreflectlevelsofdifficulty

Financial/BusinessViability • Commercialviabilityor

losspertownship• Financialgap&subsidy

requirementtoachieveviability

• Cost/benefitindicatorsperarea

Strategicanalysis • Totalsubsidycosts• PrioriJzehighneedand

“smartsubsidy”areas• Targetareasbasedon

knownvillageclusters• Developprogram&

project(s)• RecommendfirstPilot

projectandsequencedprogram

Page 19

19

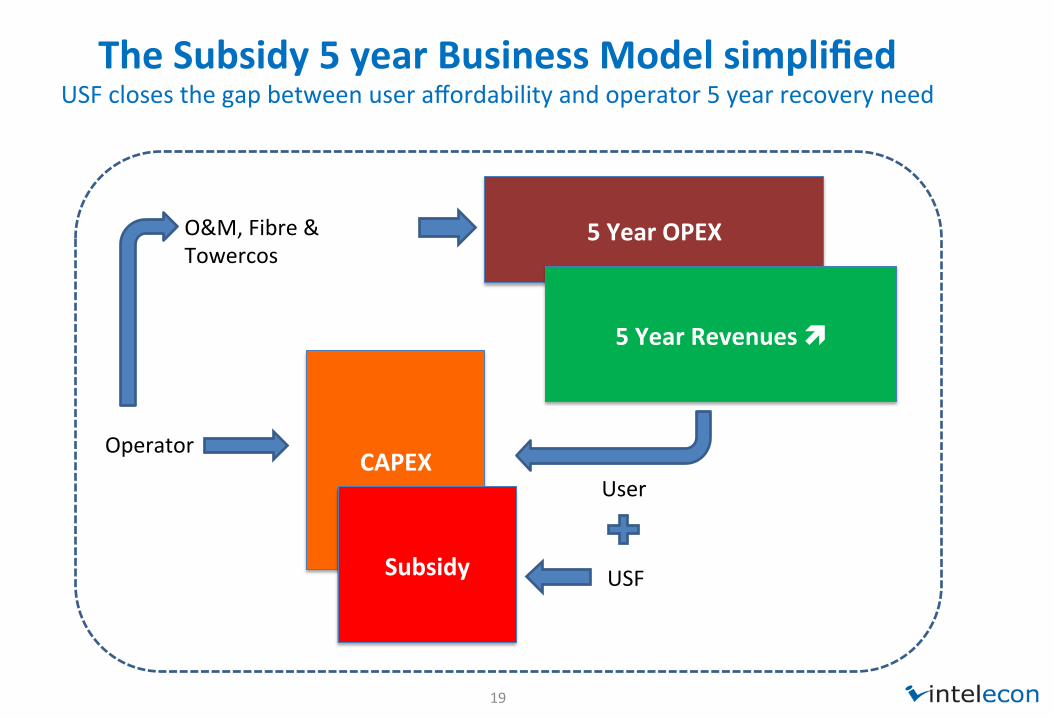

TheSubsidy5yearBusinessModelsimplifiedUSFclosesthegapbetweenuseraffordabilityandoperator5yearrecoveryneed

5YearOPEX

5YearRevenuesì

CAPEX

Subsidy

Operator

USF

User

O&M,Fibre&Towercos

Page 20

20

Marketgapsmodel:TheoreJcalframeworkforUniversalService

Hig

h in

com

e

hous

ehol

ds

Lo

w in

com

e

hous

ehol

ds

Current network reach

& access

100%

Geographical reach

USF Smart subsidy zone

True access gap

80%+

Commercialviable

95% Efficientmarket&licenceobliga-on

gap

85-90%

99%

62% 70%

RequiresongoingOPEXsupport

Viableaeersmartsubsidy

To2019

USFTarget

Page 21

21

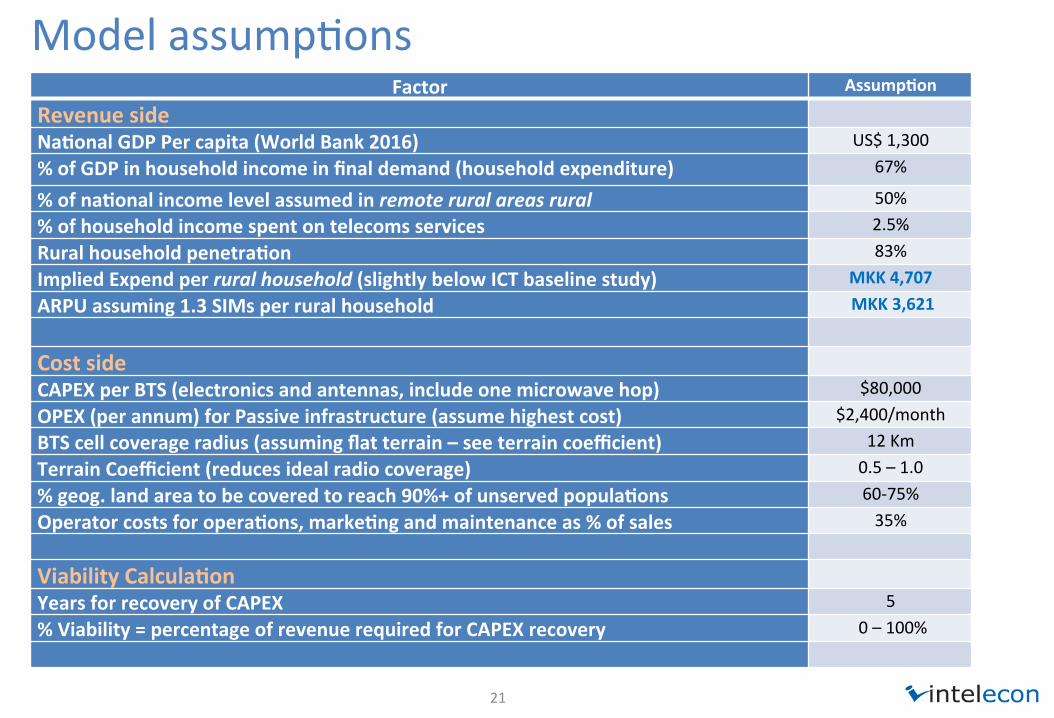

ModelassumpJonsFactor Assump-on

Revenueside

Na-onalGDPPercapita(WorldBank2016) US$1,300%ofGDPinhouseholdincomeinfinaldemand(householdexpenditure) 67%

%ofna-onalincomelevelassumedinremoteruralareasrural 50%%ofhouseholdincomespentontelecomsservices 2.5%Ruralhouseholdpenetra-on 83%ImpliedExpendperruralhousehold(slightlybelowICTbaselinestudy) MKK4,707ARPUassuming1.3SIMsperruralhousehold MKK3,621

Costside

CAPEXperBTS(electronicsandantennas,includeonemicrowavehop) $80,000OPEX(perannum)forPassiveinfrastructure(assumehighestcost) $2,400/monthBTScellcoverageradius(assumingflatterrain–seeterraincoefficient) 12KmTerrainCoefficient(reducesidealradiocoverage) 0.5–1.0%geog.landareatobecoveredtoreach90%+ofunservedpopula-ons 60-75%Operatorcostsforopera-ons,marke-ngandmaintenanceas%ofsales 35%

ViabilityCalcula-on

YearsforrecoveryofCAPEX 5%Viability=percentageofrevenuerequiredforCAPEXrecovery 0–100%

Page 22

22

TerrainconsideraJonsonBTSrangeandtechnology

• BTStypicalrange12Kmonflatterrain

• Terraincoefficientreducesassumedcoverageradiusbyupto50%forhillyandmountainousareas

• Increasesthecostofexpandingcoverageinmountainoustownships

• Butmayalsoleadtouniquedesign,towerandnetworkdesignorsharingarrangements

• InteleconesJmatesalsotookpopulaJonpocketsintoconsideraJon

Page 23

23

ViabilityandsubsidyconsideraJonsCategory Viabil ity

FactorProjectDescrip-onandPriorityImplica-on

Category1 >100% • Commerciallyviable.WillbeservedbyexisJngserviceproviderssoon.• Nosubsidyneeded

Category2 75-100% • Close to viable. Targeted commercially by operators soon without financialincenJve.

• Maxsubsidylessthan25%ofCapex.• USFProgramcouldaccelerateinvestment

Category3 50-75% • Commerciallyunviablewithoutasubsidyintherangeof25-50%.• GoodtargetforUSFProgram.

Category4 25-50% • Unviable.Unlikelytobeservedwithoutsubsidyintherange50-75%.• ShouldbetargetedforUSAFProgramsubsidy

Category5 0-25% • Typically unviable without major subsidy, requiring more than 75% ofinvestment(Absolutecut-offforUSF15%).

• MayalsorequireongoingoperaJngcostsubsidy.

Page 24

24

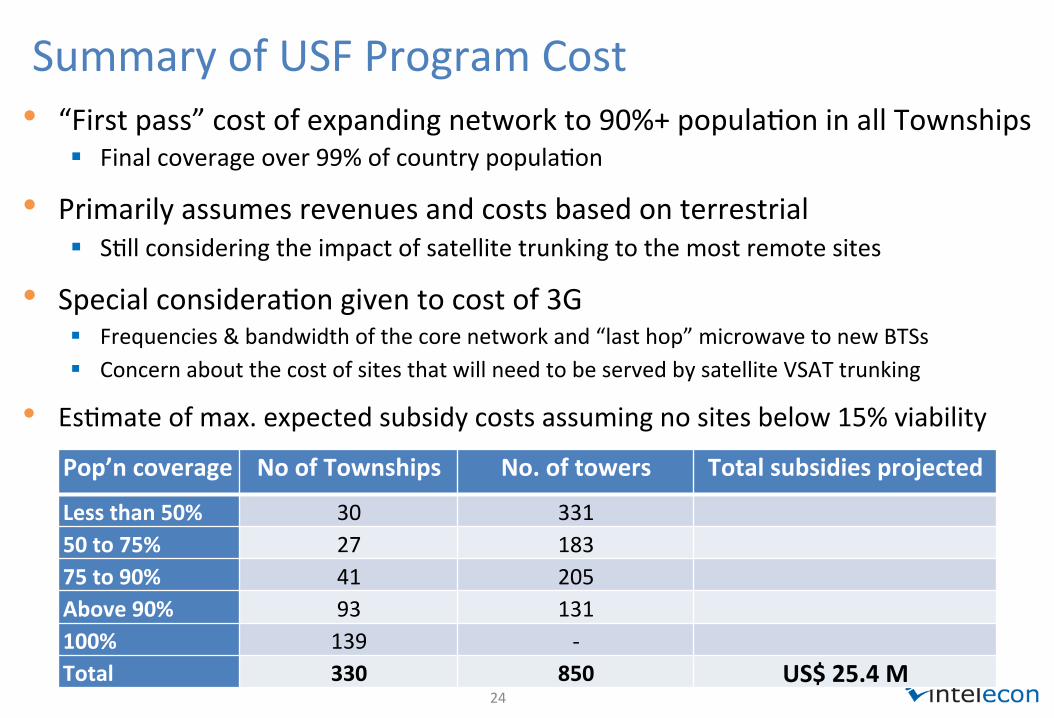

SummaryofUSFProgramCost• “Firstpass”costofexpandingnetworkto90%+populaJoninallTownships

§ Finalcoverageover99%ofcountrypopulaJon

• Primarilyassumesrevenuesandcostsbasedonterrestrial§ SJllconsideringtheimpactofsatellitetrunkingtothemostremotesites

• SpecialconsideraJongiventocostof3G§ Frequencies&bandwidthofthecorenetworkand“lasthop”microwavetonewBTSs§ ConcernaboutthecostofsitesthatwillneedtobeservedbysatelliteVSATtrunking

• EsJmateofmax.expectedsubsidycostsassumingnositesbelow15%viability

Pop’ncoverage NoofTownships No.oftowers Totalsubsidiesprojected

Lessthan50% 30 33150to75% 27 18375to90% 41 205Above90% 93 131100% 139 -Total 330 850 US$25.4M

Page 25

25

PilotAreas-interim

• 44areasbeyondQ12019commitments

• PrioritytotownshipswithsubstanJaluncoveredpopulaJons

• Mustalsobeviablewithsmartsubsidytocreateoperatorinterest§ Mostincategories3and4

• RangeofsituaJons:testassumpJons§ Someoflowercoverageareasarenot

viableforanearlywin-win§ FurtherconsideraJonofassumpJons

and%subsidypriortofinalisaJon§ ReviewforpracJcality

• ExpectreducJoninnumber

Page 26

26

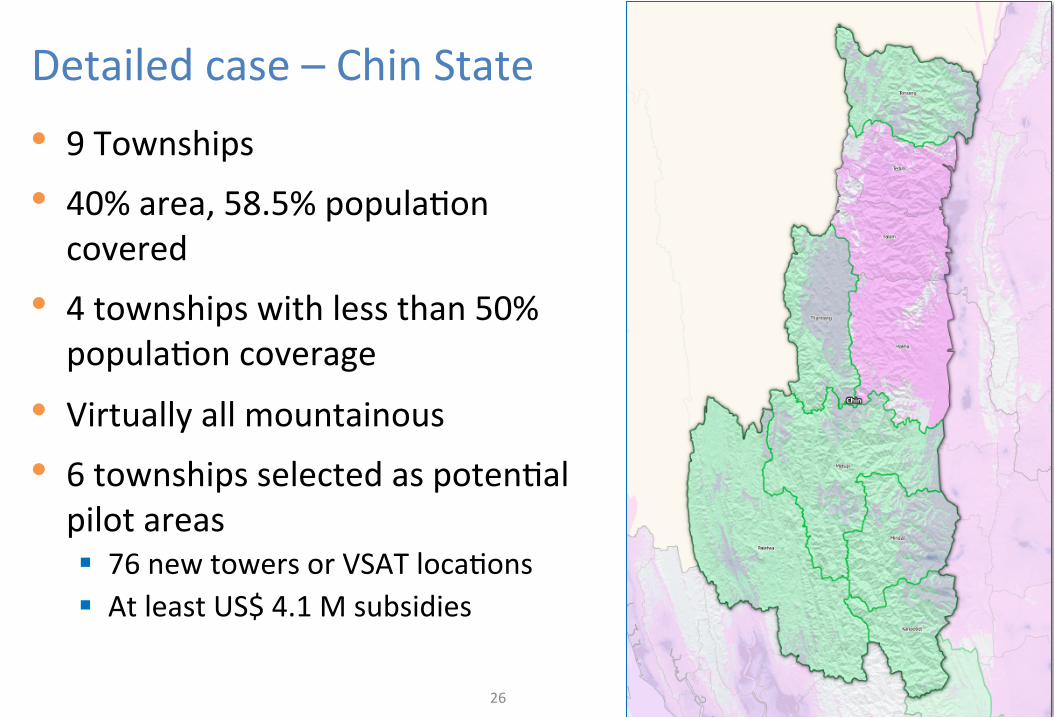

Detailedcase–ChinState• 9Townships• 40%area,58.5%populaJoncovered

• 4townshipswithlessthan50%populaJoncoverage

• Virtuallyallmountainous

• 6townshipsselectedaspotenJalpilotareas§ 76newtowersorVSATlocaJons§ AtleastUS$4.1Msubsidies

Page 27

27

Detailedcase:ShanState

• 55townships• Approx.50%area

covered• PopulaJoncovered

§ 68-69%inE&N§ 85%inSouth

• 13townshipswithlessthan50%coverage

• 22PotenJalpilotareas§ Newtowers§ US$4.5Msubsidies§ Expecttoreducethenumberconsiderably

Page 28

28

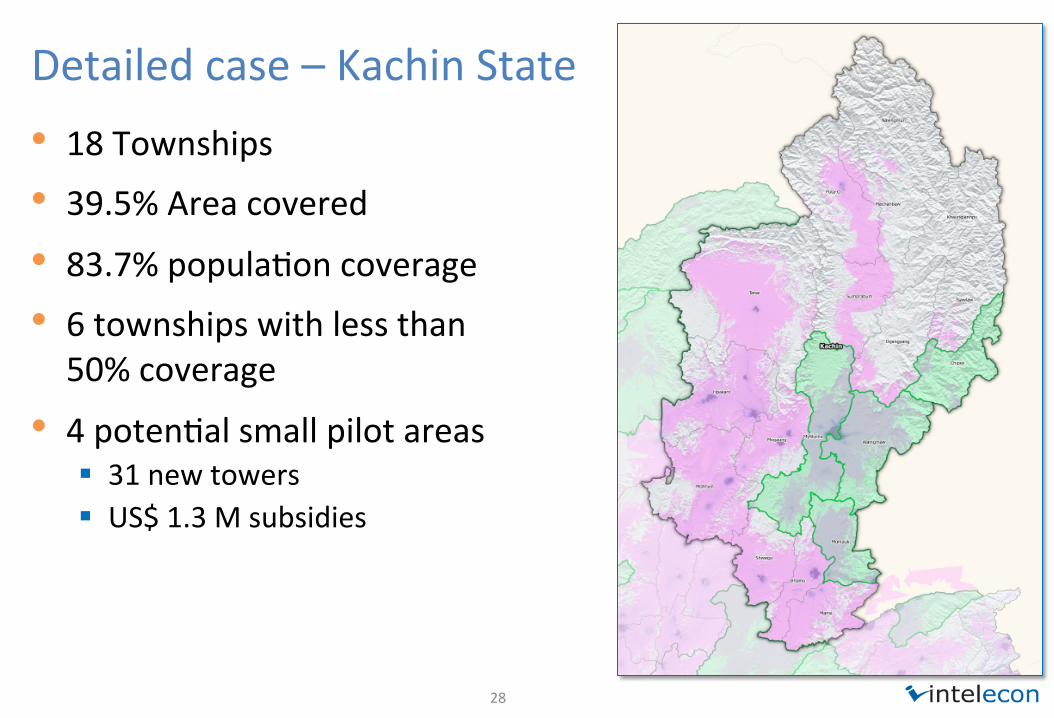

Detailedcase–KachinState• 18Townships• 39.5%Areacovered• 83.7%populaJoncoverage• 6townshipswithlessthan50%coverage

• 4potenJalsmallpilotareas§ 31newtowers§ US$1.3Msubsidies

Page 29

29

Detailedcase–TaninthanyiRegion

• 10townships• Nonewithlessthan50%populaJoncoverage§ Butsomeveryremoteareas

• 43.8%areacovered• 82%populaJoncovered• 3potenJalpilotareas

§ 88newtowers§ AlmostUS$3.0M§ Verychallengingaccess–noroads

Page 30

OPTIONSFORUSFESTABLISHMENT

Page 31

31

WhatisaUniversalServiceFund(USF)?

• Thereareover90countrieswithUSFs• TheUSFprovidesthefinanceforprovidingservicetouncovered

areasandpeople

• AUSFgetsmostlyfinancedfromasmallpercentageoftherevenueoftheoperatorsonanannualbasis.Butfundscanalsobereceivedfrom• Government• Donors• SpectrumaucJons

• AUSFisalsoaninsJtuJonalstructure–aspecialunitthatimplementstheuniversalservicestrategy

Page 32

32

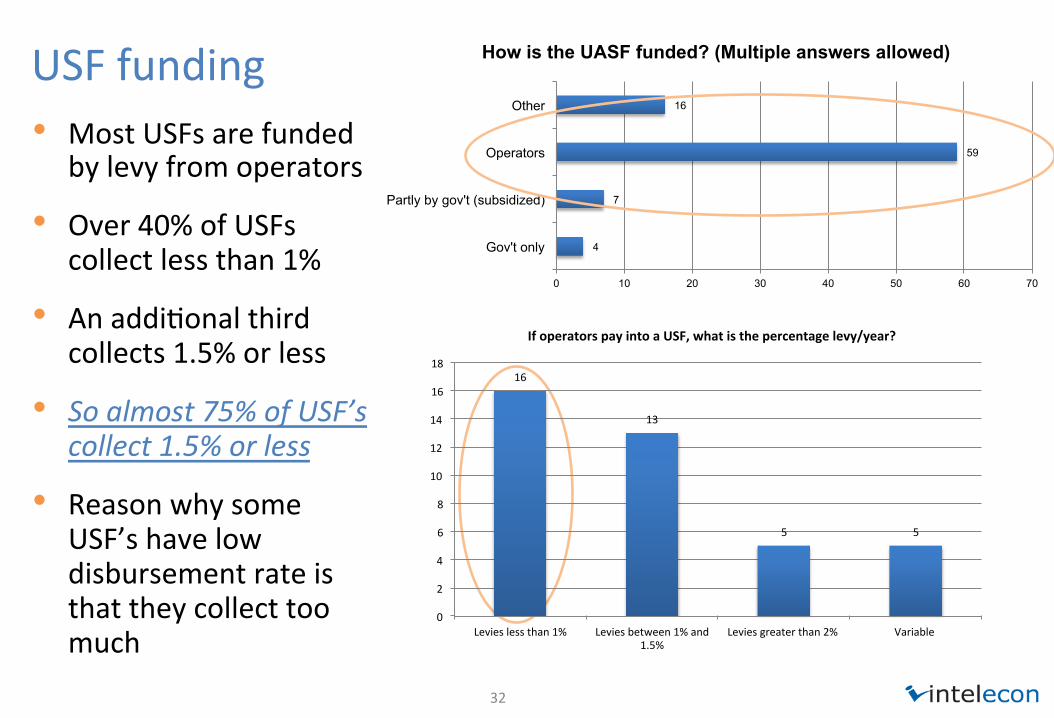

USFfunding• MostUSFsarefunded

bylevyfromoperators

• Over40%ofUSFscollectlessthan1%

• AnaddiJonalthirdcollects1.5%orless

• Soalmost75%ofUSF’scollect1.5%orless

• ReasonwhysomeUSF’shavelowdisbursementrateisthattheycollecttoomuch

4

7

59

16

0 10 20 30 40 50 60 70

Gov't only

Partly by gov't (subsidized)

Operators

Other

How is the UASF funded? (Multiple answers allowed)

16

13

5 5

0

2

4

6

8

10

12

14

16

18

Levieslessthan1% Leviesbetween1%and1.5%

Leviesgreaterthan2% Variable

IfoperatorspayintoaUSF,whatisthepercentagelevy/year?

Page 33

33

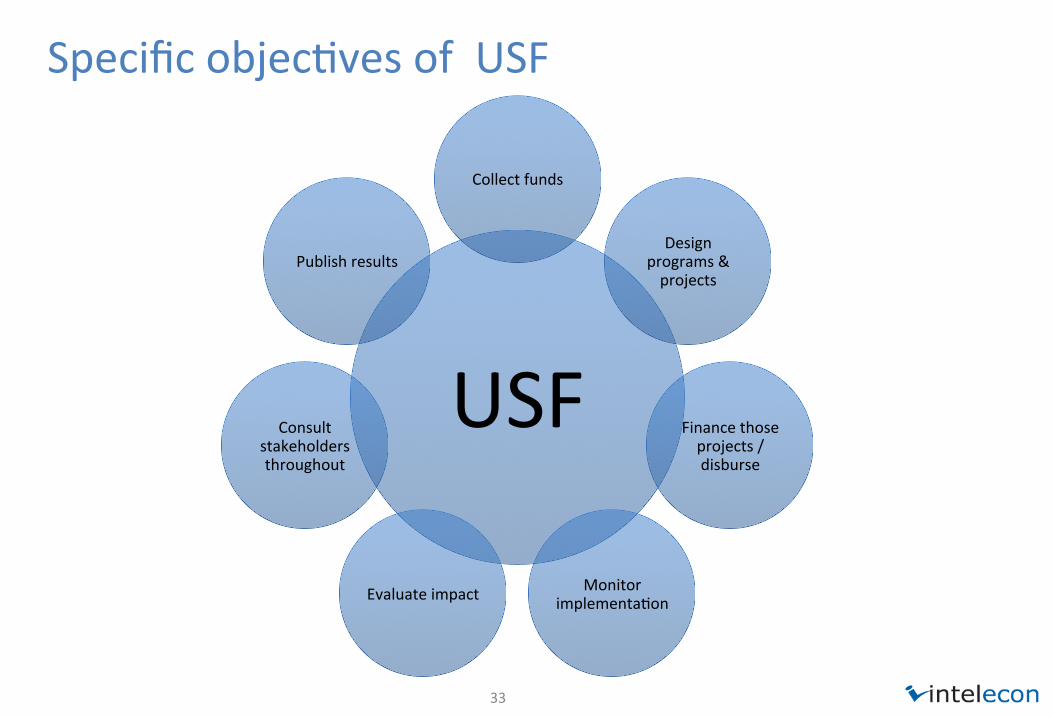

SpecificobjecJvesofUSF

USF

Collectfunds

Designprograms&projects

Financethoseprojects/disburse

MonitorimplementaJonEvaluateimpact

Consultstakeholdersthroughout

Publishresults

Page 34

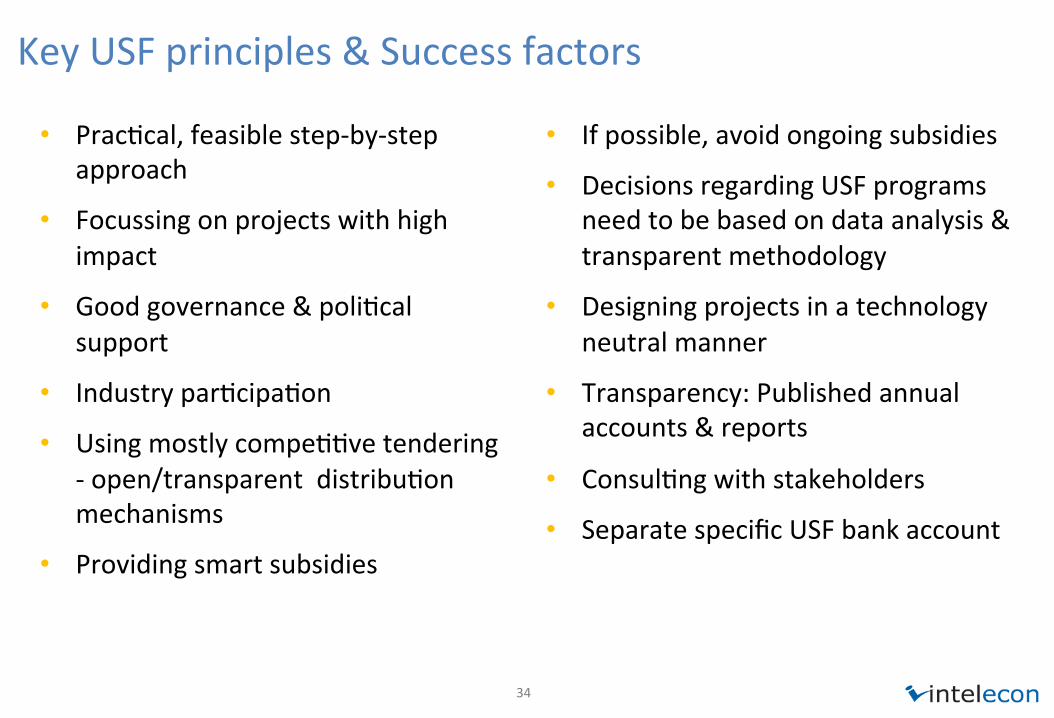

34

KeyUSFprinciples&Successfactors

• PracJcal,feasiblestep-by-stepapproach

• Focussingonprojectswithhighimpact

• Goodgovernance&poliJcalsupport

• IndustryparJcipaJon

• UsingmostlycompeJJvetendering-open/transparentdistribuJonmechanisms

• Providingsmartsubsidies

• Ifpossible,avoidongoingsubsidies

• DecisionsregardingUSFprogramsneedtobebasedondataanalysis&transparentmethodology

• Designingprojectsinatechnologyneutralmanner

• Transparency:Publishedannualaccounts&reports

• ConsulJngwithstakeholders

• SeparatespecificUSFbankaccount

Page 35

35

CompeJJvebidding

• InternaJonalbestpracJceisviacompeJJvetender

• LargemajorityofUSFsusethismethod

• RecentexamplesadvisedbyInteleconinclude:§ Uganda(since2001topresent)§ Malawi,Mozambique,BurkinaFaso§ Zambia§ Kenya(currently)§ Mongolia§ SaudiArabia§ Pakistan(broadbandmonitoring)

61%

26%

13%

0%

10%

20%

30%

40%

50%

60%

70%

Competitive tender NO competitive tender Combination

Mechanism of disbursing USF funds

[Usuallyadvancedcountrieswithhighlypenetratedmarket]

Page 36

36

TypicalchallengesofUSFs&programs

• Capacity&stafftodesignUSFprojectsandmonitorimplementaJon

• Disbursementoffunds–risksofcollecJngtoomuchandnotdisbursingit

• Properplanning&JmelyimplementaJon–telecommarketmovesfast

• Transparency–publishingannualreports,biddingresults,spendingandprojectoutcomes

Page 37

37

USFGovernanceModels

Ministry

SingleDecision-maker

USFrisksbeingpoliJcized

Examples:India,Colombia

Inter-ministerialCouncil

Presidentappointed;includingRegulator&experts

“Topheavy”,possiblyslow

Examples:Chile,Morocco

Newagencyoroutsourced/Separatefund

manager

AlsohasBoard,incl.industry

representaJves

Highercost/efforttoestablish

Examples:Ghana,Canada,Pakistan

Regulatoryauthority

UsuallycombinedwithBoard

Usedmostoeen&canworkwell

Examples:Uganda,Peru,Kenya

Page 38

38

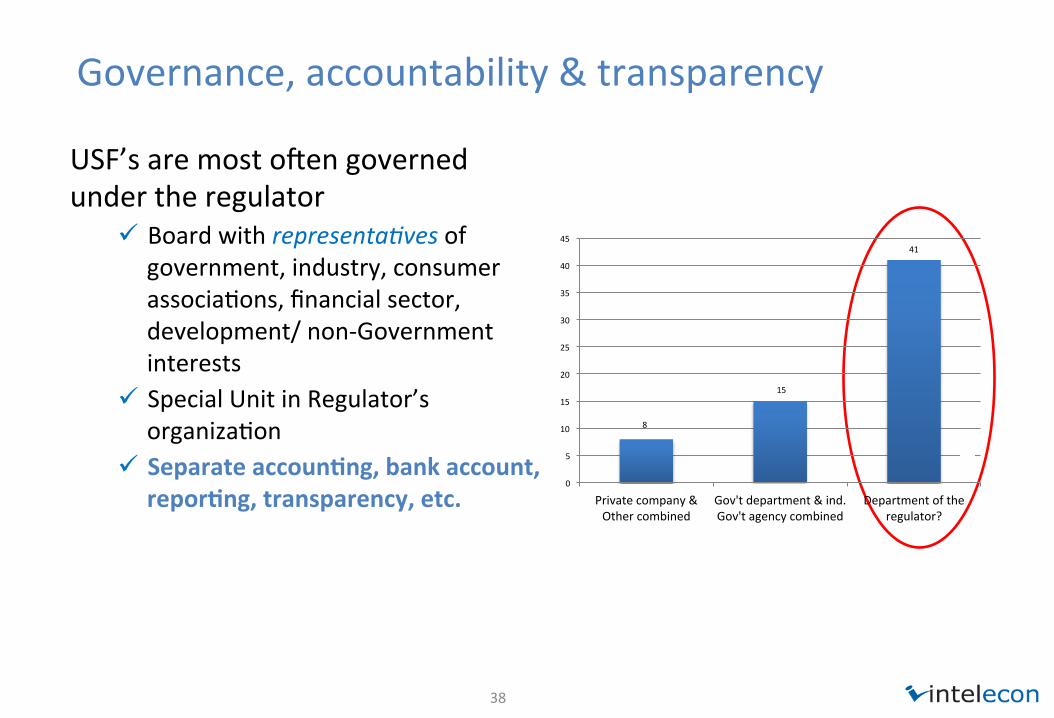

Governance,accountability&transparency

USF’saremostoeengovernedundertheregulator

ü Boardwithrepresenta7vesofgovernment,industry,consumerassociaJons,financialsector,development/non-Governmentinterests

ü SpecialUnitinRegulator’sorganizaJon

ü Separateaccoun-ng,bankaccount,repor-ng,transparency,etc.

8

15

41

0

5

10

15

20

25

30

35

40

45

Privatecompany&Othercombined

Gov'tdepartment&ind.Gov'tagencycombined

Departmentoftheregulator?

Page 39

39

USFgovernancestructure

Of49responsesinthebenchmarksurvey:• 35(73%)countrieshavetheir

USFsgovernedbyeitheraBoardoraCommi}ee/groupofMemberswiththepowertomakedecisions

• 14countries(27%)havetheirdecisionsmadethroughasinglepersononly,commonlyaDirector,ExecuJveOfficerorMinister

35

14

0

20

40

Board Director

Num

ber

of c

ount

ries

Mechanism

Mechanism to govern the USF

Page 40

40

VarioustypesofUSFBoards

USF

ExecuJveBoards–focusonstrategicvision&approvalpowers

AdvisoryBoards-increasingstakeholder

input

Oversight&MonitoringBoards–increasing

accountability

Page 41

41

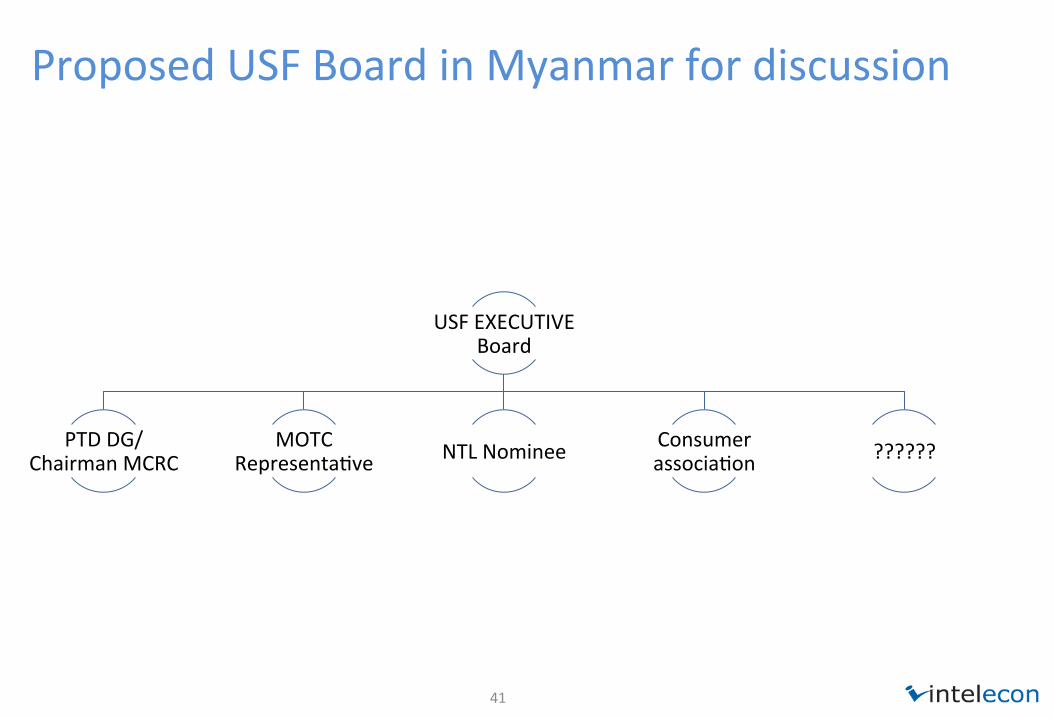

ProposedUSFBoardinMyanmarfordiscussion

USFEXECUTIVEBoard

PTDDG/ChairmanMCRC

MOTCRepresentaJve NTLNominee Consumer

associaJon ??????

Page 42

42

PrecedentselsewhereforindustryrepresentaJon

• Pakistan:OperatorsareontheUSFCompany’sBoard

• Mongolia:SeveraloperatorsrepresentedontheMonitoringCommi}ee

• Ghana:USFBoardofTrusteesincludesarepresentaJvefromeachmajortelecomoperator

• Canada:USFoversightcommi}eeincludesrepresentaJonfromoperators

Page 43

43

Financialmanagement

• USFmoniesseparatedfromMOTCorregulatoryauthorityfinances

• USFtohaveownbankaccountwithreputablebank• SeparateUSFaccountsandindependentaudits• AdministraJve&operaJonalexpensesshallrequireUSFBoard

approval–throughannualbudgetplans

• USFfinances(payments,withdrawals&othertransacJons)shallsaJsfycountry’sfinancialpoliciesandregulaJons

Page 44

44

Summary–whatisneededfromagoodinsJtuJonalUSFstructure??

ü Ensuringunbiaseddecisionsbasedonapproveddataanalysisandmethodology,andapprovedUSFscopeandstrategy

ü Ensuringpublictransparency–audiJng&annualreporJngü AccountabilityoffundcollecJon,disbursementsandprojects

ü EnsuringstakeholderconsultaJon(industry,government,civilssociety)andsupport

ü Ensuringthatfundsarewell-spentandhaveposiJveimpact

Page 45

45

Lessonslearnedregardingroles

Ministry:Policy&supervision• High-levelUniversalServicepolicyse~ng• ApprovalofoperaJngmethodologyandhigh-levelstrategy,inconsultaJonwithPTD/regulator

• ApprovalofauditedannualUSFaccounts• Reviewandupdateofuniversalservicepolicy

USFmanagementunit:Freetoexecute• ExecuJonofapprovedstrategy,designdetailsofprogramsandprojects

• MonitoringofimplementaJon

Page 46

INITIALUSFPROGRAMS/STRATEGY

Page 47

47

PotenJalUniversalServicestrategy

47

Basedon• DataandGISanalysis• StakeholdersmeeJngs(industry,government,CSOs/NGOs)andconsultaJon

• ReviewingexisJngICTiniJaJves• InternaJonalexperience• RuralfieldvisitsandinterviewsinChinandKachin

Page 48

48

ElementsofpotenJalUniversalServicestrategy

69%

15%

10%

3%

1%

2%

Mobilevoice&broadbandservice

AssistschoolswithInternetconnecJvity

Internettraininge.g.,incommunitylibraries

Connectruralhospitals

SupportsoluJonsredisabiliJes

RelevantruralcontentpromoJon

Page 49

49

KeyreasonsforschoolconnecJvityprogram

Ø ICTcapacitybuildinginschools–starJngyoung–hasthebiggestlong-termimpactoncountry’seconomy

Ø Intoday’sdigitalage&knowledgesociety,schoolconnecJvity&integraJngICTintoeducaJoncannotwaitanylonger

Ø AssistwithdemandsJmulaJonamongfutureusersofICT

Page 50

50

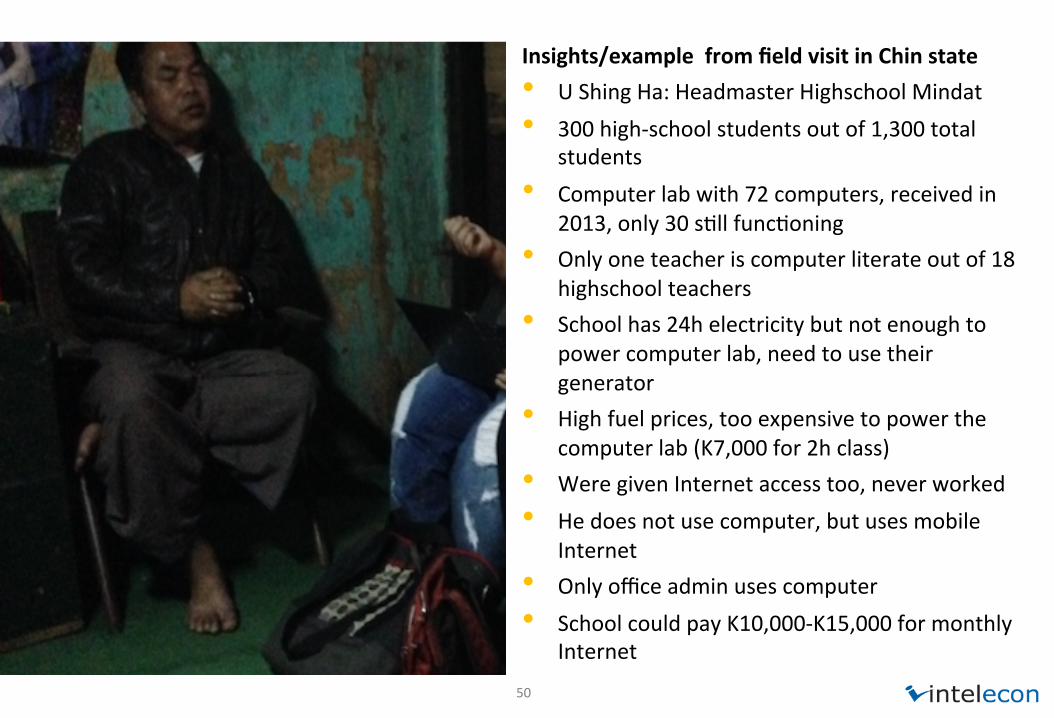

Insights/examplefromfieldvisitinChinstate• UShingHa:HeadmasterHighschoolMindat• 300high-schoolstudentsoutof1,300total

students• Computerlabwith72computers,receivedin

2013,only30sJllfuncJoning• Onlyoneteacheriscomputerliterateoutof18

highschoolteachers• Schoolhas24helectricitybutnotenoughto

powercomputerlab,needtousetheirgenerator

• Highfuelprices,tooexpensivetopowerthecomputerlab(K7,000for2hclass)

• WeregivenInternetaccesstoo,neverworked• Hedoesnotusecomputer,butusesmobile

Internet• Onlyofficeadminusescomputer• SchoolcouldpayK10,000-K15,000formonthly

Internet

Page 51

51

FocusonInternet-readyhighschools

• Sufficientpower

• Computerlabortabletsforstudents/teachers

• Trainedteachers• Ongoingsupport• ICTTeachingmaterial&plan

Page 52

Internetbandwidth

Educa-onportal

Computerlab&

upgrades

ICTTeachertraining

ITHelpdesk

Lastmileconnec-vity

Keyelementsforsuccess• Ecosystemfor

schoolconnecJvity

• PartnershipwithMinistryofEducaJon

USF

Educa-onMinistry&thirdpar-es

Page 53

53

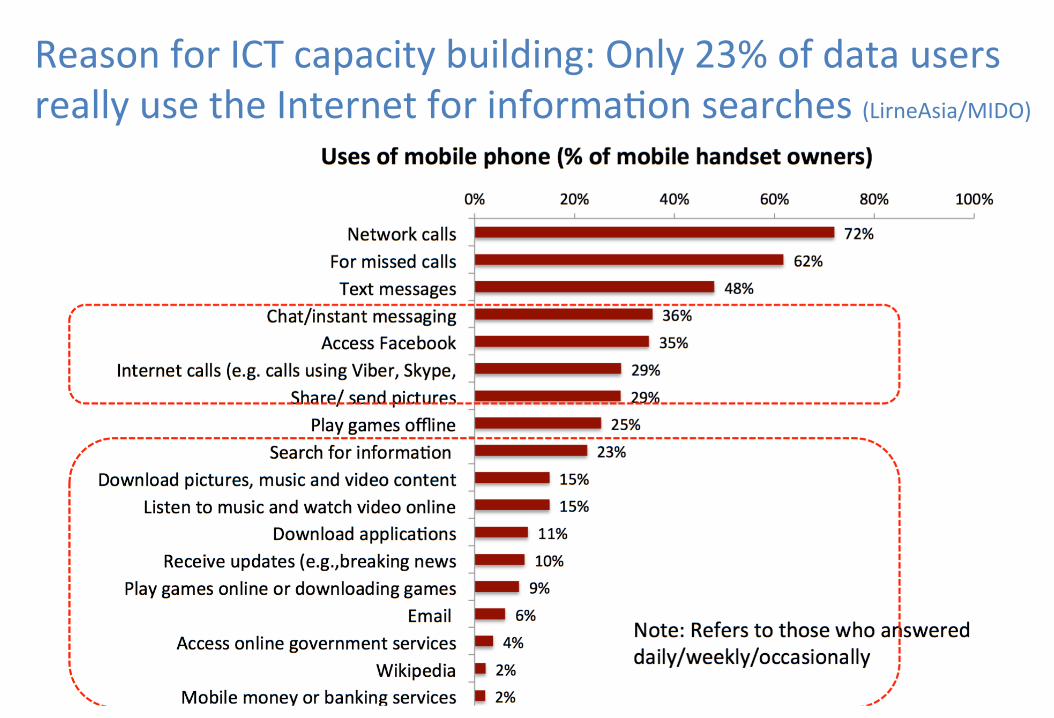

ReasonforICTcapacitybuilding:Only23%ofdatausersreallyusetheInternetforinformaJonsearches(LirneAsia/MIDO)

Page 54

54

• TownshiphospitalinMatupi• 1doctorand1denJst,27healthcarestaff,

50beds• Have2donateddesktopcomputers,both

notworking• 1laptopthatworks,thedoctorusesit• HospitalhasnoInternet• Have2landlinephonesbuttheydon’twork

forcallsoutsideofMatupi–hegoestotheWiFiInternetcaféintown

• UsesVibertocommunicatewithChinstateadministraJonandMinistryofHealth

• Sendstextandaphotooftypedreport• Heuseshisownmoneyforthese

communicaJons,nobudget• DepartmentofHealthInformaJonSystem

–2personsa}endedatraining,butcan’tuse

Page 55

55

Nextsteps

ByApril:

• DraeUniversalServiceStrategy• DraeGuideforestablishingUSF• DraeOperaJngManualforUSF

InMay:

• NextconsultaJonInJune:

• Finalizeallthreedocuments

Page 56

56

Thank you

Contact:[email protected]