SUMMER TRAINING REPORT ON SALES & Working Capital Management Submitted in partial fulfillment of the requirement for the award of the degree’s Master's of Business Administration Kurukshetra University,Kurukshetra (Haryana) (2009-2011) UNDER THE GUIDANCE OF: SUBMITTED BY: MISS GARIMA GOUTAM MR. PUNEET ARYA

Transcript

SUMMER TRAINING REPORT

ONSALES

& Working Capital Management

Submitted in partial fulfillment of the requirement for the award of the degree’s

MILLS CO. LTD. IQBALPUR for giving me an opportunity to work in this esteemed organization

and for the help they provided wherever needed.

I am also grateful to my all staff members of company for their individually guidance and willing

cooperation throughout my project.

Puneet Arya

M.B.A

3

CONTENT

Sr. No. Topic Page No.

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

11.

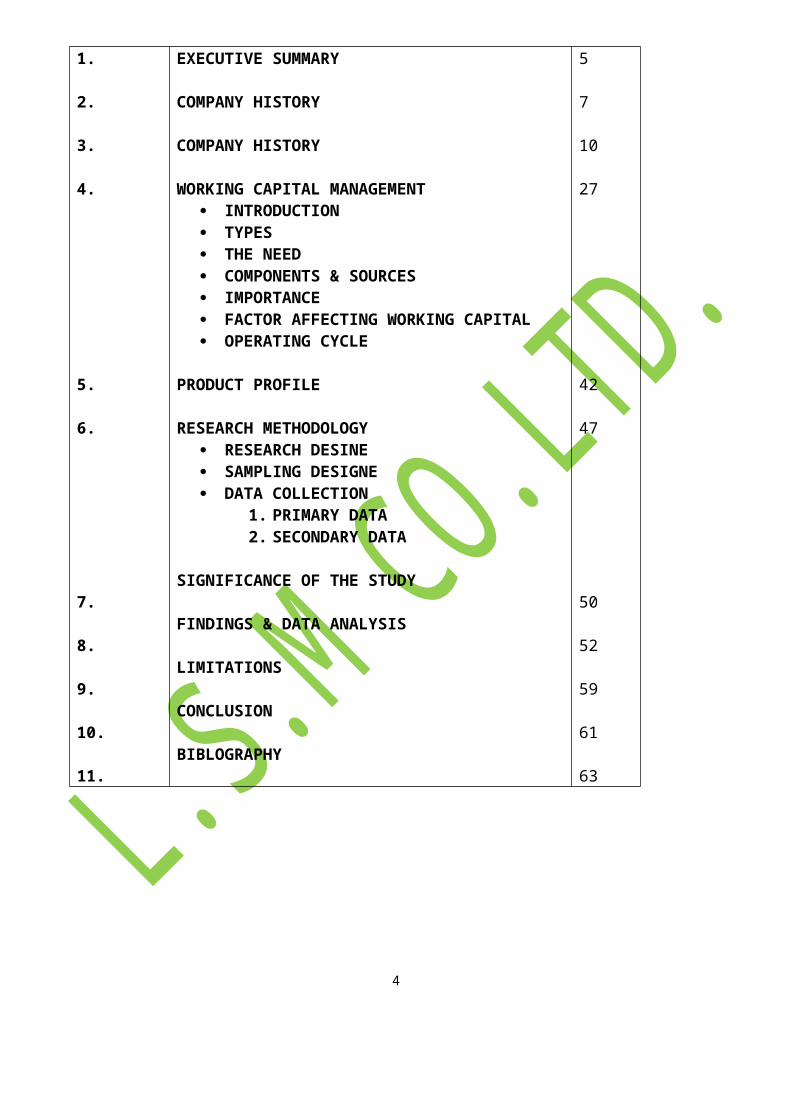

EXECUTIVE SUMMARY

COMPANY HISTORY

COMPANY HISTORY

WORKING CAPITAL MANAGEMENT INTRODUCTION TYPES THE NEED COMPONENTS & SOURCES IMPORTANCE FACTOR AFFECTING WORKING CAPITAL OPERATING CYCLE

PRODUCT PROFILE

RESEARCH METHODOLOGY RESEARCH DESINE SAMPLING DESIGNE DATA COLLECTION

1. PRIMARY DATA2. SECONDARY DATA

SIGNIFICANCE OF THE STUDY

FINDINGS & DATA ANALYSIS

LIMITATIONS

CONCLUSION

BIBLOGRAPHY

5

7

10

27

42

47

50

52

59

61

63

4

5

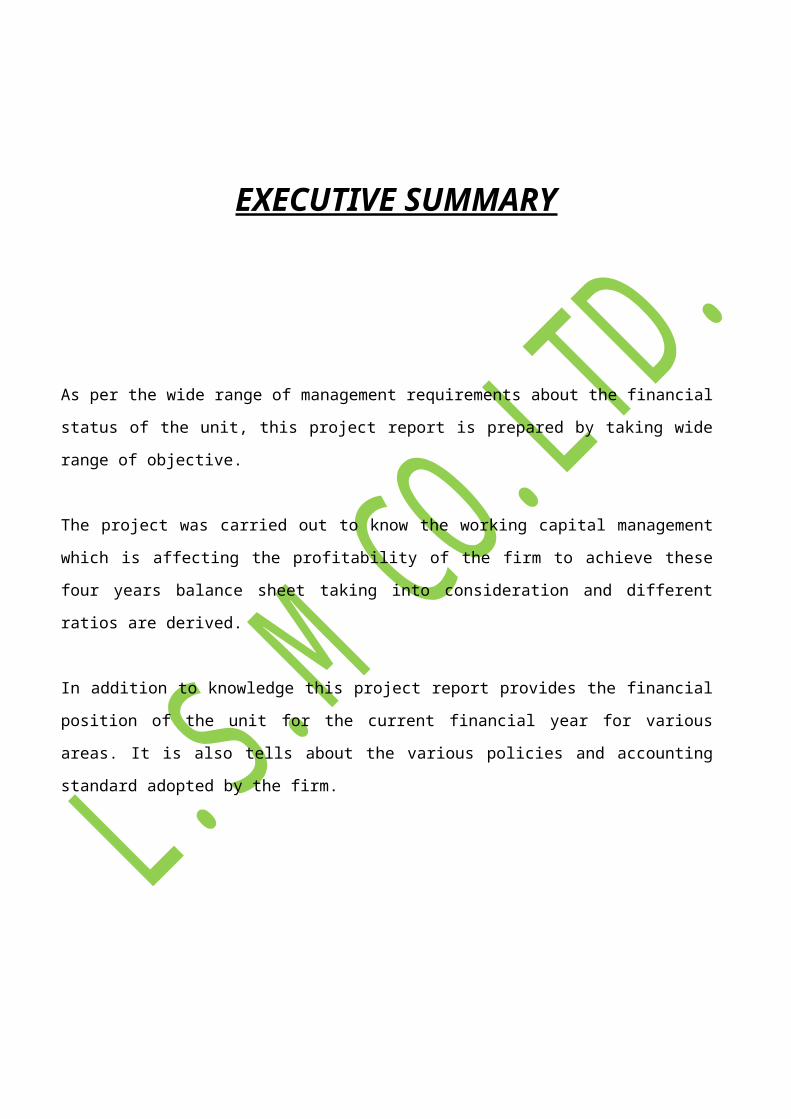

EXECUTIVE SUMMARY

As per the wide range of management requirements about the financial status of the unit, this project

report is prepared by taking wide range of objective.

The project was carried out to know the working capital management which is affecting the

profitability of the firm to achieve these four years balance sheet taking into consideration and

different ratios are derived.

In addition to knowledge this project report provides the financial position of the unit for the current

financial year for various areas. It is also tells about the various policies and accounting standard

adopted by the firm.

6

7

BRIEF HISTORY OF THE COMPANY

INTRODUCTION

Lakshmi sugar mills co. ltd, having its unit 7 registered offices at Iqbalpur, Distt. Haridwar (UK) & head office at 704, Siddhartha building, 96, Nehru place, New Delhi, was incorporated on 16th September 1940 and the company was awarded certificate for commencement of business on 20th September 1940. The company started cane crushing operation at Hamira, in the erstwhile kapurthala state in 1942 and continued its operation there till 1952. as a result of partition of the country, the area under cane cultivation decreased considerably in Hamira and therefore the company shifted its site to the present location at Iqbalpur in district Haridwar- Uttaranchal in 1953.

Initially the unit had an installed capacity of approximately 1600 TCD, while shifting the unit its capacity was marginally expanded to 1800 TCD. Later, it expanded to 2500 TCD in 1987 and subsequently to 3000 TCD in 1990-91. The company adopted double carbonation double sulphitation process till 1992-93 seasons. It switched over to the double sulphitation process in 1993-94 season and expanded plant capacity of 3500 TCD from the 1997-98 seasons onwards, thereby effecting considerable saving in the cost of production. In season 2005-06, company has expanded its installed capacity from 3500 TCD to 4500 TCD i.e. by more than 25% of existing installed capacity.

PROMOTERS/MANAGEMENT The company is being totally managed by its board of directors consisting chairperson-cum-managing director Mrs. Anjali Birla Sawhney (Promoter- Director) Miss. Shreya Sawhney, (Promoter- Director) and two other professional directors. Earlier the company was chaired by its main promoter Mr. Pawan c. sawhney who unfortunate went to his heavenly abode on 13.01.2002.

After said demise of her husband Mr. Pawan c. sawhney, Mrs. Anjali Birla sawhney took over the control of company’s whole affairs with the complete support of professionals. Mrs. Anjali Birla sawhney is having experience of industries as she is born & belongs to very eminent industrial house i.e. Birla group. She & her daughter Miss. Shreya sawhney are possessing the qualities and knowledge of sugar industry as both belongs to the renowned sugar industrialist families were associated with her husband and father-in-law being the famed sugar industrialist for last more than 30 years.

8

Both the promoter directors are well capable of controlling & managing complete affairs of Sugar Company. Other two directors Mr. Mohan.P.Patel & Sh. M.M. Sharma is also possessing experience of more than 15 years in sugar industry and are professionally qualified being chartered accountants.

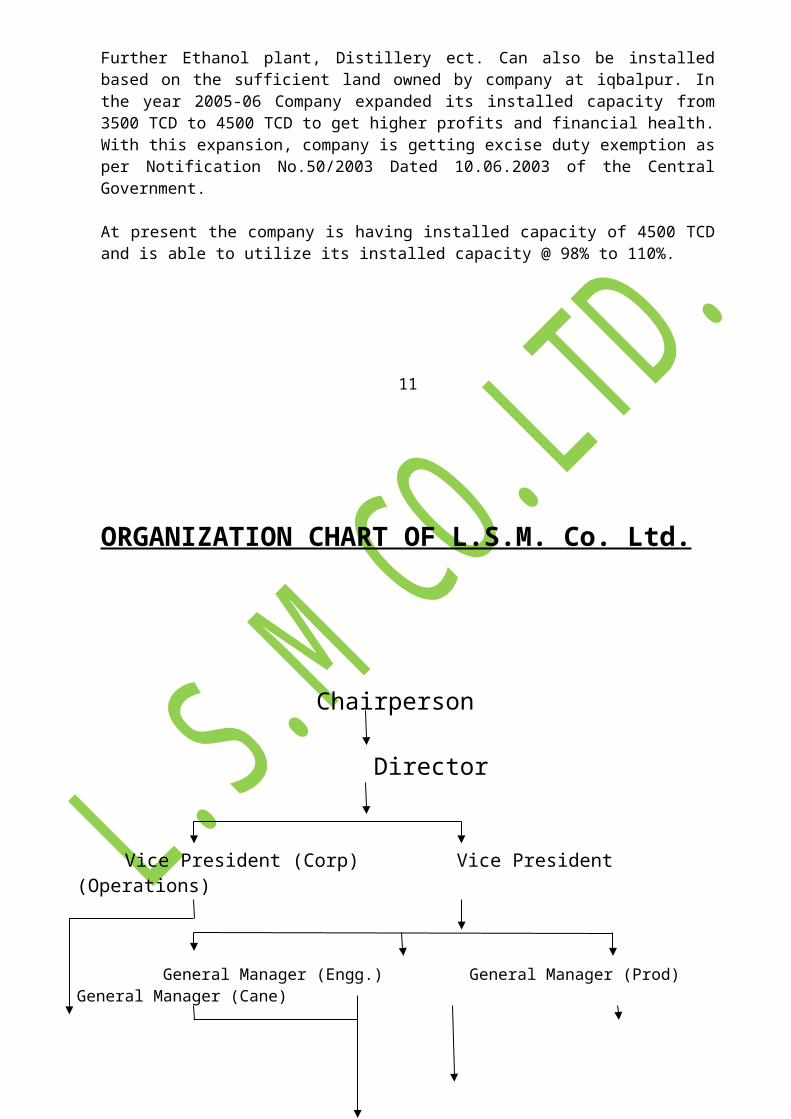

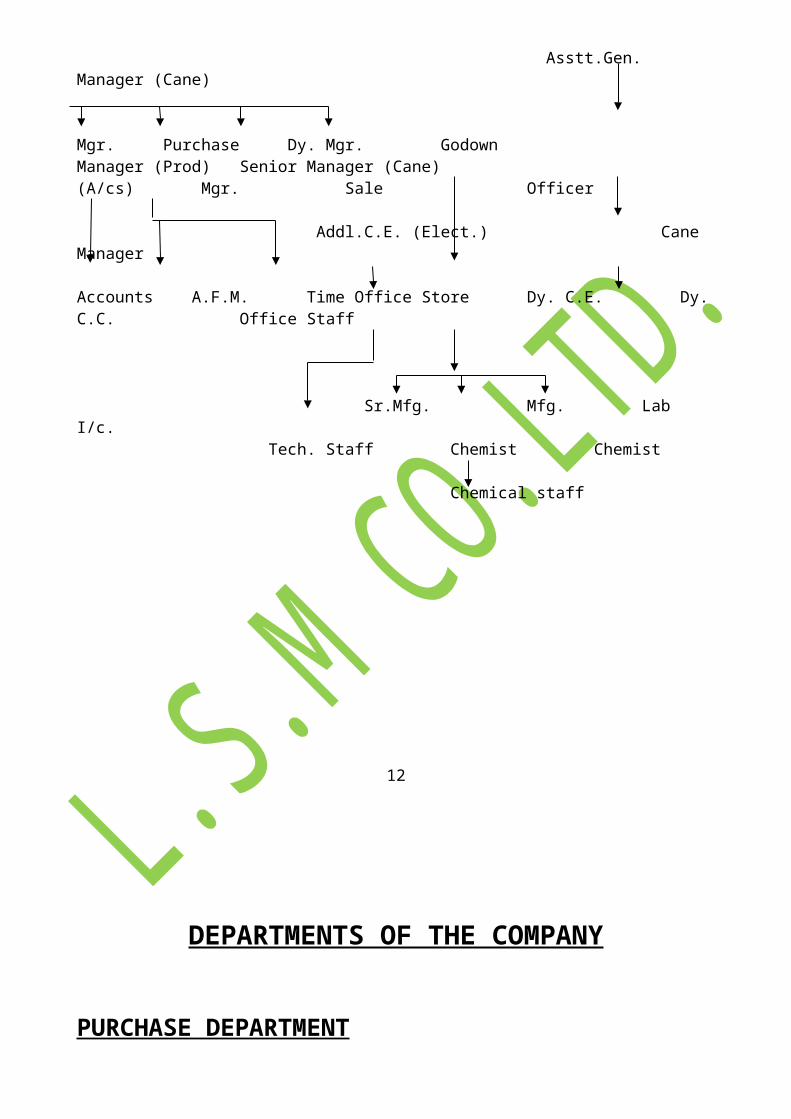

Further the company is being managed through other qualified professionals also who are directly reporting to Chairperson and Directors of the company. The technical managerial team consists of Vice President (O), General Manager (E), General Manager (P), Manager (P), Accounts, Cane & Administrative departments are managed by Manager (A/cs), General Manager (cane), and Factory Manager respectively who are also well qualified & experienced in their own field.

With the above team of qualified & experienced management, chairperson is carrying the affairs of the company on the progressive path & better performance from year to year basis.

9

COMPANY PROFILE

PERSENT SITUATION

The factory is suitably located with respect to availability of raw material (sugar cane), water, electricity, unskilled, skilled and professional men-power etc. the plant is located in one of the good cane growing area in the state of Uttaranchal.. The factory is located 6 kms from state highway leading to Dehradun which is well connected by road. Iqbalpur railway station is 1 kms from factory. Nearest broad gauge major railway station is situated at Roorkee which is about 12 kms from the factory. The major cities near the vicinity are Dehradun, Hardwar, and Saharanpur at a distance of about 50 to 70 kms and Delhi at a distance of about 165 kms from the factory.

The neighboring sugar factories and the competitors in the present market are:-

R.B.N.S. Sugar mill Laksar, Distt. Haridwar

Uttam Sugar mill co. Ltd, Distt. Haridwar

Triveni Sugar mill, Deoband, Distt. Saharanpur

Daya sugar mill, Distt. Saharanpur

The factory has continued to augment its performance, through various addition and modifications in plant and equipment.

The layout of plant and machinery is satisfactory. However, sufficient space can be made available for future technology Up-gradation and expansion of the factory through re-arrangement. Further Ethanol plant, Distillery ect. Can also be installed based on the sufficient land owned by company at iqbalpur. In the year 2005-06 Company expanded its installed capacity from 3500 TCD to 4500 TCD to get higher profits and financial health. With this expansion, company is getting excise duty exemption as per Notification No.50/2003 Dated 10.06.2003 of the Central Government.

At present the company is having installed capacity of 4500 TCD and is able to utilize its installed capacity @ 98% to 110%.

11

ORGANIZATION CHART OF L.S.M. Co. Ltd.

Chairperson

Director

Vice President (Corp) Vice President (Operations)

General Manager (Engg.) General Manager (Prod) General Manager (Cane)

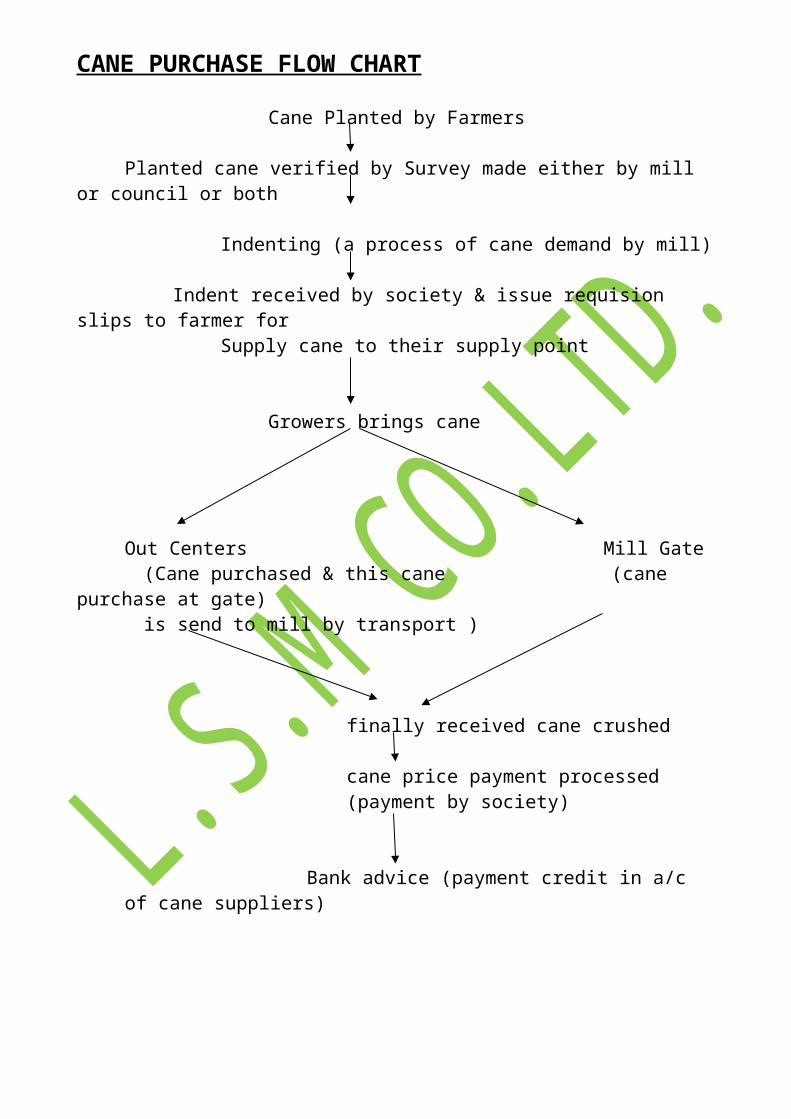

V. R.G. 23A PART I & II 9QUANTITY & VALUE OF EXCISE) FOR PROCESS VI. R.G. 23C PART I 7 II (QUANTITY &VALUE OF EXCISE) FOR CAPITAL

GOODS.

VII. PERFORMA II FOR DIRECTORATE MONTHLY

VIII. WEEKLY REPORT & TELEGRAM

IX. ER1 MONTHALY FOR CENTRAL EXCISE

X. WEEKLY REPORT THROUGH E. MAIL TO CENTRAL EXCISE

XI. SALES DAY BOOK

19

BAGASSE:-

i. ORDER FOR SALE PRICE

ii. INVOICE

iii. TRADE TAX 4% ON SALE VALUE

iv. MANI SAMITI 2% SALE VALUE

v. CESS ON MANDI SAMITI 0.50% SALE VALUE

vi. SALES DAY BOOK

PRESS MUD:-

i. ORDER FOR SALE PRICE

ii. FLAT RATE NO ANY TAX

iii. SALES DAY BOOK

20

MOLASSES:-

i. ORDER FOR SALE PRICE ii. R.G.1 FOR CENTRAL EXCISE

10% COUNTRYLIQUOR20% EXPORT70% CHEMICALS

iii. M.F. 5 FOR STATE EXCISE PART Iiv. M.F. 5 FOR STATE EXCISE PART IIv. PERSONAL LEDGER ACCOUNT (P.L.A.)vi. ADMN. CHARGES REGISTER STATE EXCISE TAX

8/- PER QLT. IN STATE20/- PER QLT. OUT STATE

vii. DAILY DESPATCH REGISTER (STATE EXCISE)viii. M.F. 4 GATE PASS RETURN FEGISTERix. CUSTOMERS REGISTERx. STOCK REGISTER xi. MOLASSES STORAGE FUND REGISTER

RS. 1.50 BELOW PER QLT. STORAGE CAPACITY ON SALESRS. 0.50 PER QLT. ON REQUIRED CAPACITY ON SALES

xii. TRADE TAX 4% ON SALES VALUExiii. EXCISE 75/- PER QLT. & 2%/- EDUCATION CESS ON EXCISE DUTYxiv. ERI MONTHLY FOR CENTRAL EXCISExv. FORTNIGHTLY STATEMENT SHEERA PRAPETRAK ONLY STATE EXCISE D.

DUNxvi. M.F. 1 FOR CURRENT YEAR PRODUVTION & DESPATCHES xvii. M.F. 2 FOR PREVIOUS YEAR PRODUCTION & DESPATCHES xviii. M.F. 7 FOR STOCK & DIPxix. SALES DAY BOOK

21

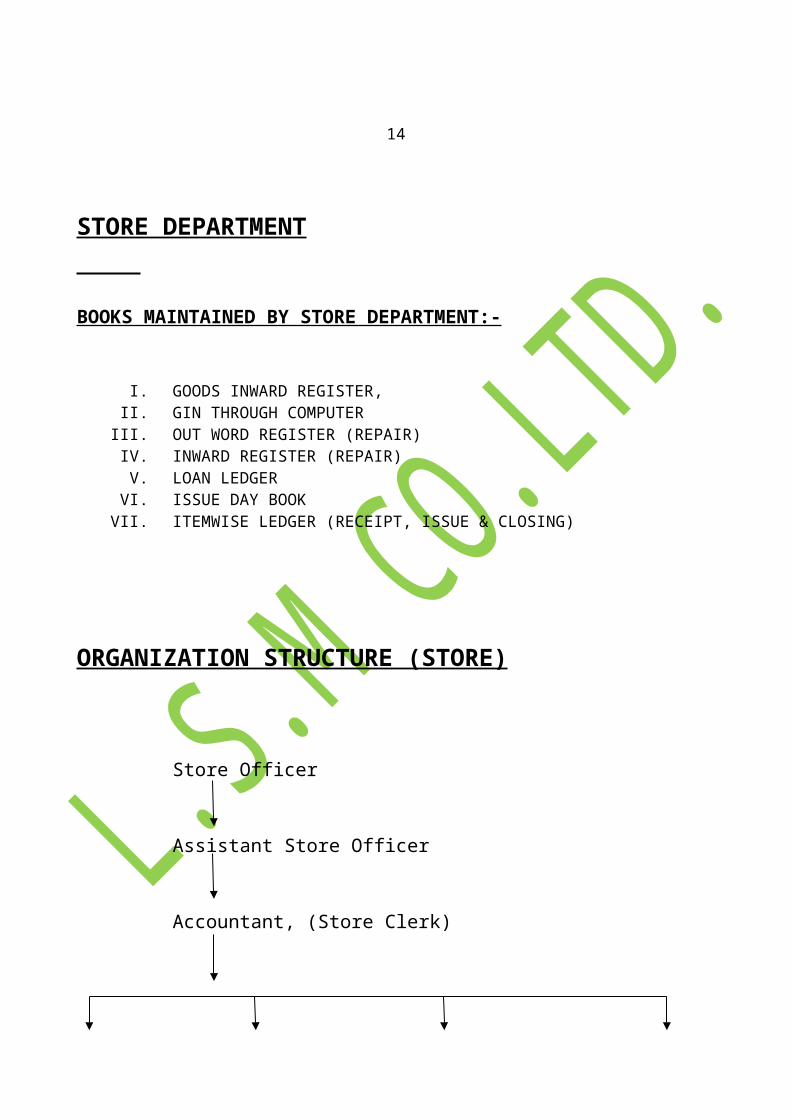

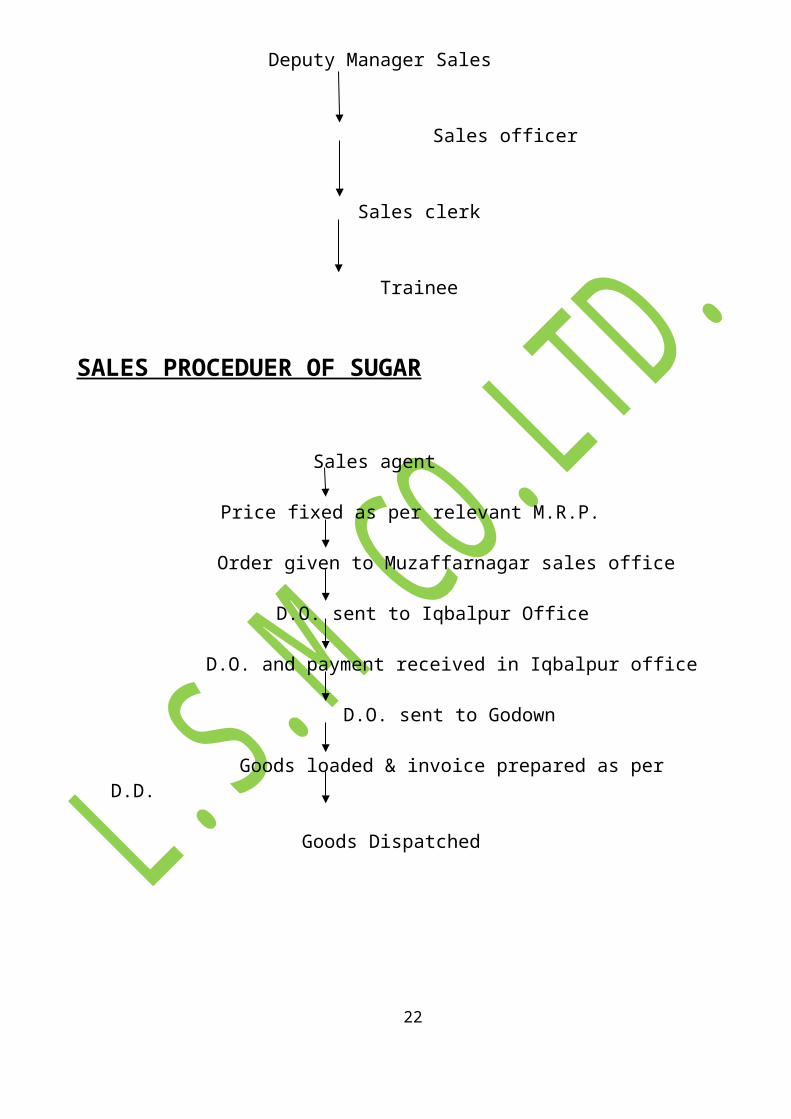

ORGANIZATION STRUCTURE OF SALES DEPARTMENT

Deputy Manager Sales

Sales officer

Sales clerk

Trainee

SALES PROCEDUER OF SUGAR

Sales agent

Price fixed as per relevant M.R.P.

Order given to Muzaffarnagar sales office

D.O. sent to Iqbalpur Office

D.O. and payment received in Iqbalpur office

D.O. sent to Godown

Goods loaded & invoice prepared as per D.D.

Goods Dispatched

22

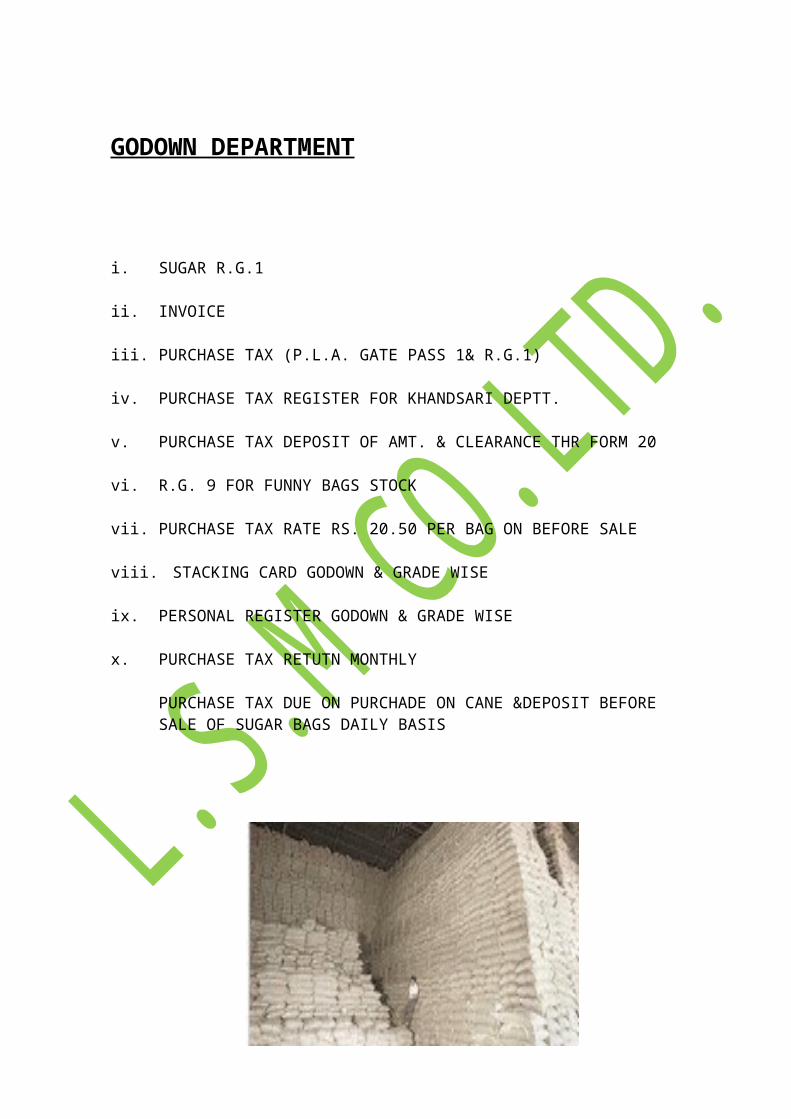

GODOWN DEPARTMENT

i. SUGAR R.G.1

ii. INVOICE

iii. PURCHASE TAX (P.L.A. GATE PASS 1& R.G.1)

iv. PURCHASE TAX REGISTER FOR KHANDSARI DEPTT.

v. PURCHASE TAX DEPOSIT OF AMT. & CLEARANCE THR FORM 20

vi. R.G. 9 FOR FUNNY BAGS STOCK

vii. PURCHASE TAX RATE RS. 20.50 PER BAG ON BEFORE SALE

viii. STACKING CARD GODOWN & GRADE WISE

ix. PERSONAL REGISTER GODOWN & GRADE WISE

x. PURCHASE TAX RETUTN MONTHLY

PURCHASE TAX DUE ON PURCHADE ON CANE &DEPOSIT BEFORESALE OF SUGAR BAGS DAILY BASIS

23

ACCOUNT DEPARTMENT

i. PREPARATION OF VOUCHERS (CASH, BANK, JOURNAL& PURCHASE

ii. CASH BOOK

iii. DAY BOOK (BANK, JOURNAL & PURCHASE)

iv. GENERAL LEDGER

v. SUB LEDGER (CUSTOMERS, SUGAR, SUPPLIERS, CONTRACTORS ADV. TO EMP. & OTHERS CANE TRANSPORTERS ETC.

vi. TRIAL BALANCE

vii. CASH FLOW ACTUAL (C-II)

viii. CASH FLOW FROJECTED (C-II)

ix. PROFITABILITY

x. COST RECORDS (COST AUDIT)

xi. STOCK AUDIT (PNB)

xii. TAX AUDIT

xiii. TDS RETURN

xiv. SALES TAX RETURN

xv. EXCISE AUDIT (PREVENTIVE)

xvi. PROFIT 7 LOSS AND BALANCE SHEET

24

TIME – OFFICE DEPARTMENT

Books Maintained By Time- Office Department

I. Attendance Registera) General Attendance register b) Shift wise Attendance Register

II. Leave Record booka) Temporary & Seasonalb) Permanent

III. Salary Sheets

IV. Gratuity

V. Bonus Calculation & Payment Sheets

VI. Leave Encashment Records

VII. Special Wages (over time)

VIII. Service Records

25

ORGANISATIONAL CHART OF TIME-OFFICE

HEAD OF DEPARTMENT

SENIOR TIME KEEPER

TIME KEEPER

TIME OFFICE TIME OFFICE TIME OFFICE CLERK (1) CLERK (2) CLERK (3)

26

27

WORKING CAPTIAL MANAGEMENT

INTRODUCTION

Every business needs founds for two purposes – for its establishment and to carry out its day-to-day operations. Long-term funds are required to create production facilities through purchases of fixed assets such as plant, land, building etc. investment in these assets represents that part of firm’s capital which is blocked on fixed basis and is called fixed capital. Funds are also needed for short-term purposes for the purchases of row materials payment of wages and other day-to-day exp. These funds are known as working capital. Working capital may be regarded as life blood of a business. Its affective provision can do much to ensure the success of a business, while its inefficient management can lead not only to loss of profit but also lead to the ultimate downfall of a concern. Hence, working capital management if carried out effectively, efficiently and consistently, will assure the heath of an organization.

Working capital in general practice, refer to the excess of current assets over current liabilities.

Working capital = current assets – current liabilities

Management of working capital therefore, is concerned with the problems that arise in attempting to manage the current assets, the current liabilities and the inter- relationships that exists between them in other words, it refers to all aspects of administration of both current assets and current liabilities.

For the proper understanding of working capital, it is necessary to understand the various concept of working capital. The main concept of working capital is as follows:

1. QUANTITATIVE CONCEPT

2. QUALITATIVE CONCEPT

28

1. Quantitative concept:-

This is also known as “gross working capital concept “ according to this concept working capital is the total of all the current assets. This view places more emphasis on quantitative aspect of working capital rather then its qualitative aspect. The argument given in support of this view is that as all the current assets assist in the conduct of business operations, it does not make any difference whether they are financed by long term funds of by current or shot-term liabilities.

2. Qualitative concepts :-

This concept gives more emphasis on the qualitative aspect rather than the quantitative aspect of working capital. This is also known as “Net working capital concepts. According to this concept the excess of the current assets over current liabilities are equal; it indicate absence of working capital in the business. On the other hand, if the amount of current liabilities exceeds the amount of current assets, such a situation is known as deficit of working capital. This situation does not generally exist in a business firm because this is generally a situation of crisis. This concept is known as qualitative concept because it show the liquidity position of the business and also indicate the extent to which the working capital has financed through ling-term funds.

The net working capital concept, however, is also important for the following reasons:

1. It is a qualitative concept which indicates the firm ability to meets its operating exp. And short-term liabilities.

2. It indicates the margin of protection available to the short-term creditors, i.e., the excess of current assets over current liabilities.

3. It is an indicator of the financial sound ness of an enterprise.

4. It suggests the need for financing a part of the working capital requirements out of permanent sources of funds.

29

TYPES OF WORKING CAPITAL

Working capital can be classified on the following two basis:-

1. On the basis of concepts

2. On the basis of necessities

1. On the Basis of Concepts:-

On the basis of concepts working capital can be of two types:

(a). Gross Working Capital:-

Gross working capital is the amount of funds invested in the various components of current assets.

(b). Net Working Capital:-

The working capital is the difference between current assets and current liabilities the concepts of net working capital enables a firm to determine how much amount is left for operational requirements. This is more acceptable connotation of the term working capital.

30

2. On the Basis of Necessities:- Working Capital can be divided into two categories on the basis of necessities:

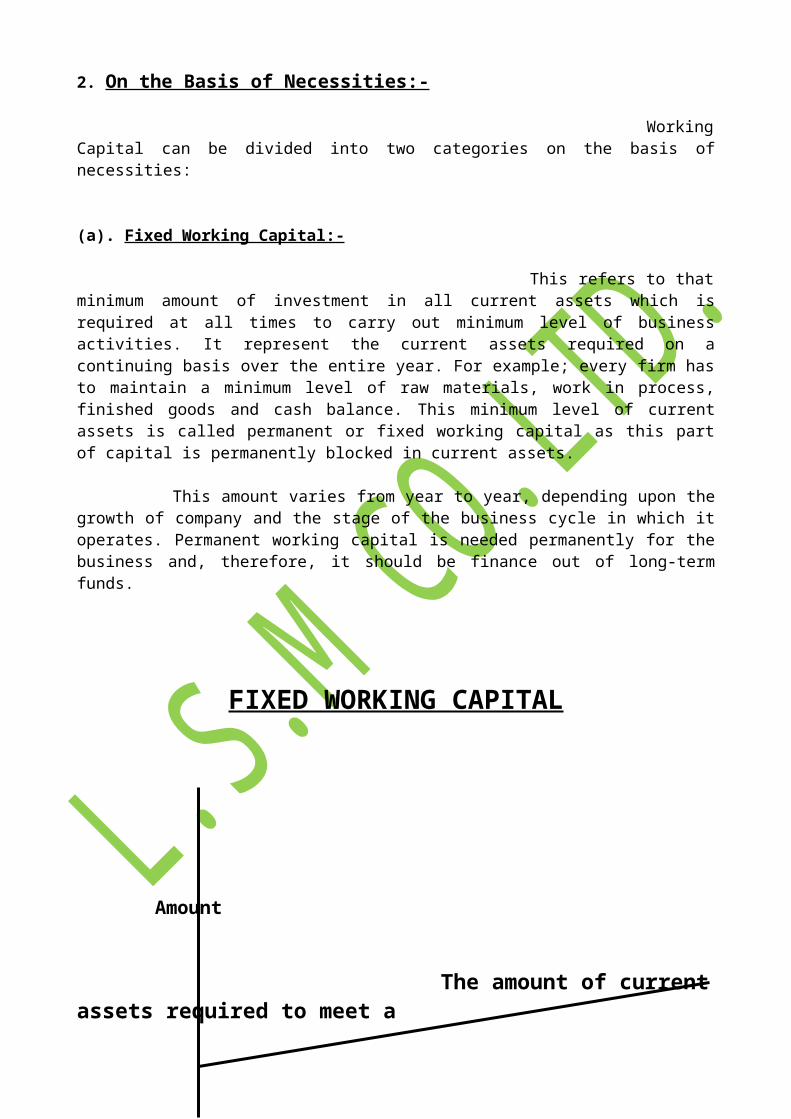

(a). Fixed Working Capital:- This refers to that minimum amount of investment in all current assets which is required at all times to carry out minimum level of business activities. It represent the current assets required on a continuing basis over the entire year. For example; every firm has to maintain a minimum level of raw materials, work in process, finished goods and cash balance. This minimum level of current assets is called permanent or fixed working capital as this part of capital is permanently blocked in current assets.

This amount varies from year to year, depending upon the growth of company and the stage of the business cycle in which it operates. Permanent working capital is needed permanently for the business and, therefore, it should be finance out of long-term funds.

FIXED WORKING CAPITAL

Amount

The amount of current assets required to meet a Firm’s long- term minimum need

Permanent current assets

TIME

31

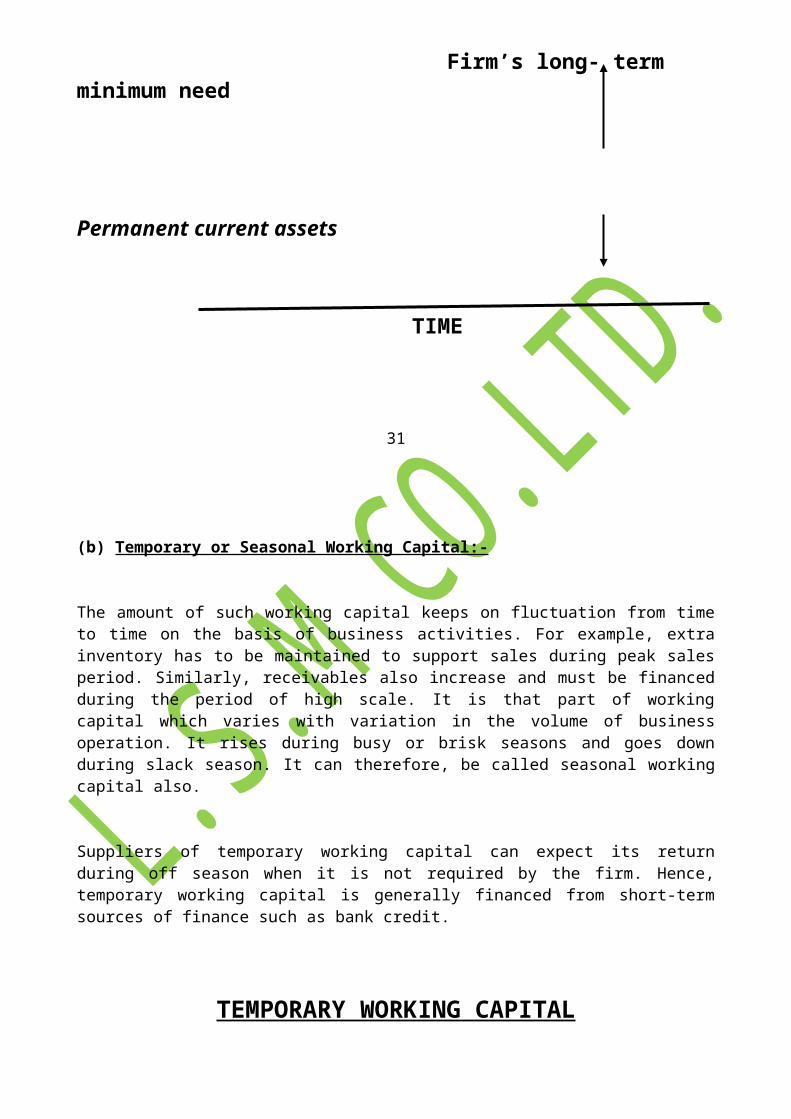

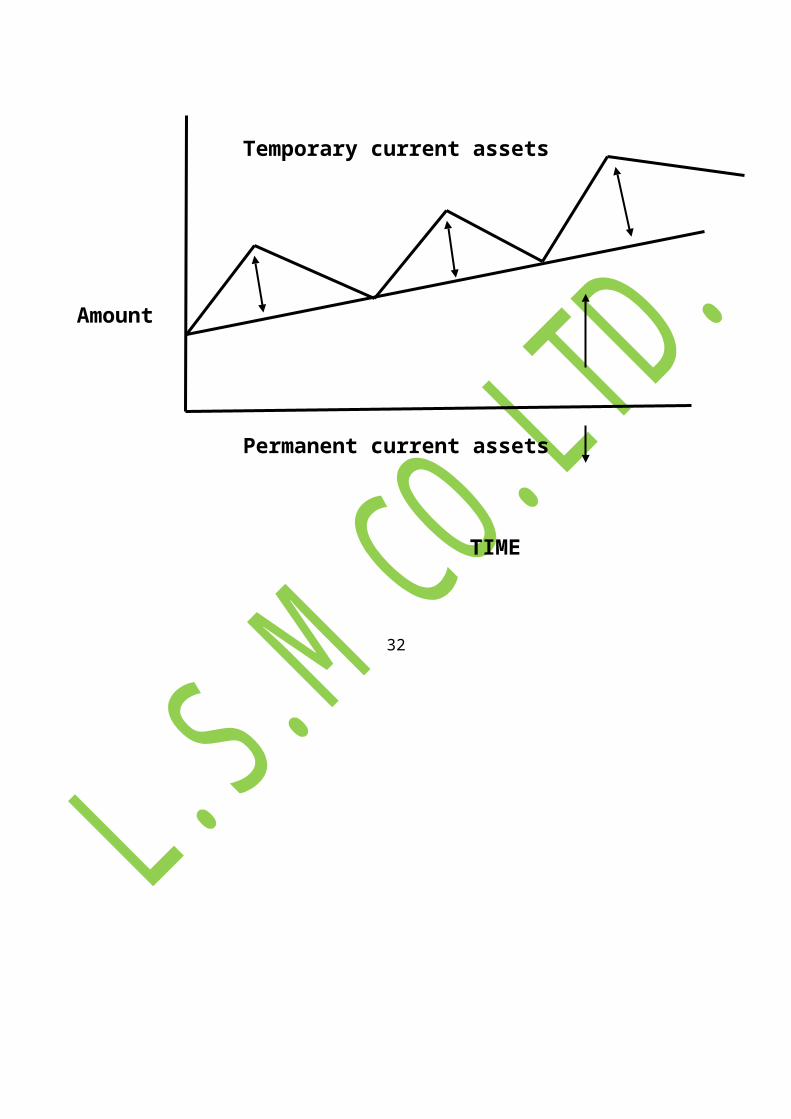

(b) Temporary or Seasonal Working Capital:-

The amount of such working capital keeps on fluctuation from time to time on the basis of business activities. For example, extra inventory has to be maintained to support sales during peak sales period. Similarly, receivables also increase and must be financed during the period of high scale. It is that part of working capital which varies with variation in the volume of business operation. It rises during busy or brisk seasons and goes down during slack season. It can therefore, be called seasonal working capital also.

Suppliers of temporary working capital can expect its return during off season when it is not required by the firm. Hence, temporary working capital is generally financed from short-term sources of finance such as bank credit.

TEMPORARY WORKING CAPITAL

Temporary current assets

Amount

Permanent current assets

TIME

32

APPROACHES

The objective of Working capital management is to maintain the optimum balance of each of the working capital components. This includes making sure that funds are held as cash in bank deposits for as long as and in the largest amount possible, thereby maximizing the interest earned. However, such cash may more appropriately be “invested” in other assets or in reducing other liabilities.

Working capital management takes place on two levels:-

1. Ratio analysis can be used to monitor overall trends in working capital and to identify areas requiring closer management.

2. The individual components of working capital can be effectively managed by using various techniques and strategies.

When considering these techniques and strategies, departments need to recognize that each department has a unique mix of working capital components. The emphasis that needs to be placed on each component varies according to department. For example, some departments have significant inventory levels; others have little if any inventory.

Furthermore, working capital management is not an end in itself. It is an integral part of department’s overall management. The needs of efficient working capital management must be considered in relation to other aspects of the department’s financial and non financial performance.

33

THE NEED OF WORKING CAPITAL

The need for working capital cannot be over emphasized. Every business need some amount of working capital. The need for working capital arises due to the time gap between production and realization of cash from sales. There is an operating cycle involved in the sales and realization of cash. There are time gaps in purchase of raw material and production; production and sales; and sales and realization of cash.

Thus working capital is needed for the following purposes:

1. For the purpose of raw material, components and spares.

2. To pay wages and salaries.

3. To incur day-to-day expenses and over head cost such as fuel, power and office expenses etc.

4. To meet the selling cost as packing, advertising etc.

5. To provided credit facilities to the customers.

6. To maintain the inventories of raw material, work in progress, stores and spares and finished stock.

34

COMPONENTS AND SOURCES OF WORKING CAPITAL

COMPONENTS

There are two components of working capital:-

1. Current Assets

2. Current liabilities

1. CURRENT ASSETS:-

Current assets are those assets which can be converted into cash in the normal course of business within a short period-say a maximum of one year. They are also called floating or circulating assets because they cannot be put to constant use. They are meant for resale or produced for the purpose of sale i.e. converting them into cash.

The list of current assets comprises of:-

a) Cash in hand and bank balances.b) Bills receivables.c) Sundry debtors.d) Short terms loans and advances.e) Inventories of stock:

Raw material Work in progress Stores and Spares Finished goods

f) Temporary investment of surplus funds.g) Prepaid expenses.h) Accrued income.

35

2. CURRENT LIABILITIES:-

Current liabilities are those liabilities which are intended to be paid in the ordinary course of business within a short period of normally one accounting year out of the current assets or the income of the business.

Examples of current liabilities are:-

a) Bills payableb) Sundry creditorsc) Outstanding expensesd) Short term loans, advances and depositse) Dividend payablesf) Bank overdraftg) Provision for taxation

SOURCES

A firm can arrange Working capital from the following two sources:-

1. LONG TERM SOURCES:-

The sources of long term financing can be broadly classified into the following two categories:

a) Owned Sources:- Owned sources includes

Issue of shares Retained Earnings Reserves

b) Borrowed Sources:- It mainly includes the issue of debenture or long term loans.

36

2. SHORT TERM SOURCES:-

For financing the working capital requirements short term sources can be classified into the following two broad categories:

a) Internal Sources:-

Depreciation provision Outstanding liabilities Provision for taxation

b) External Sources:-

Trade credit Bank credit Short term loans from financial institutional Public deposit Advance from customer

37

IMPORTANCE OF WORKING CAPITAL

Adequate working capital helps in maintaining solvency of the business by providing uninterrupted flow of production.

Sufficient working capital enables a business concerns to make prompt payments and hence helps in creating and maintaining goodwill.

A concern having adequate working capital, high solvency and good credit standing can arrange loans from banks and other financial institution on easy and favorable terms.

Sufficient working capital ensures regular supply of raw materials and continuous production.

Working capital helps in regular payment of salaries, wages and other day to day commitments.

Working capital can exploit favorable market condition such as purchasing its requirements in bulk when the prices are lower and by holding its inventories for higher price.

Working capital helps to face the business crisis.

It also helps in giving quick and regular return to the investors.

It also creates an environment of security, confidence, and high morale and creates overall efficiency in a business.

38

FACTORS AFFECTING WORKING CAPITAL

There is no set of universally applicable rules to ascertain working capital needs of a business organization. Since, it varies from firm to firm, industry to industry and even in the different seasons of the same firm. Therefore, a large number of factors influence the requirements of working capital.

The factors are as under:-

1. Nature and size of business: -

The requirement of working capital of a firm is widely related to the nature and size of the business unit. In the case of manufacturing concern which sells its product on credit basis and has a long operating cycle, need s a large amount of working capital. Moreover the size of the firm is also an important factor. Because a smaller firm needs smaller amount of working capital on the basis of its production activities and vice-versa in the opposite case.

2. Length of production cycle: -

The time taken to convert raw materials into finished product is known as the production cycle. The level of working capital depends upon the production cycle. Longer the production cycle, more will be the need for working funds in order to finance current assets during the prolonged manufacturing cycle. On the other hands, if the production cycle is shorter, the requirements of working capital will also be less.

3. Seasonal operation: -

If a firm is operating in goods and services having seasonal fluctuation in demand, then the working capital requirement will also fluctuate with every change. If the operations are smooth and even throughout the year then working capital requirement will be constant and will not be affected by the seasonal factors.

4. Market competitiveness: -

In view of the competitive conditions prevailing in the market, the firm may have to offer liberal credit terms to the customers relating in higher debtors. Even larger inventories may be maintained to serve an order as and when received; the customer may go to some other supplier. Thus, the working capital tends to be high as a result of greater investment in inventories and receivables. A monopolistic firm may not require large working capital.

39

5. Credit policy: -

The totally of terms and conditions on which goods are sold and purchased. A firm has to interact with two types of credit policies at a time:

(a) The credit policy of the supplier of raw materials, goods etc.

(b) The credit policy relating to the credit which it extends to its customers.

In both the cases, however, the firm while deciding its credit policy has to take care of the credit policy of the market. The working capital requirement of this firm will be lower than that of a firm which is purchasing cash but has to sell on credit basis.

6. Supply condition: -

The time taken by a supplier of raw materials, goods etc. after placing an order, also determines the working capital requirement. If goods are received as soon as or in a short period after placing an order, then the purchaser will not like to maintain a high level of inventory of that goods. Otherwise, larger inventories should be kept.

7. Growth and diversification of business:-

Growth and diversification of business call for larger volume of working fund. The need for increased working capital does not follow the growth of business but precedes it. Working capital need is in fact assessed in advance in reference to the business plan.

8. Banking relations: -

A good bank-customer relationship is a pre-requisite of a successful working capital management policy. Commercial banks these days normally finance the working capital gap. Credit authorization scheme has also been liberalized after 1986. Thus customers receive an assured bank finance which minimizes the need for making over investment assets.

9. Price level changes: -

Changes in the price level also affect the working capital requirements. Generally, the rising will require the firm to maintain larger amount of working capital as more funds will be require the firm to maintain the same current assets. The effect of rising prices may not be affected firms. Some firms may be affected much while some others may not be affected at all by the rise in prices.

40

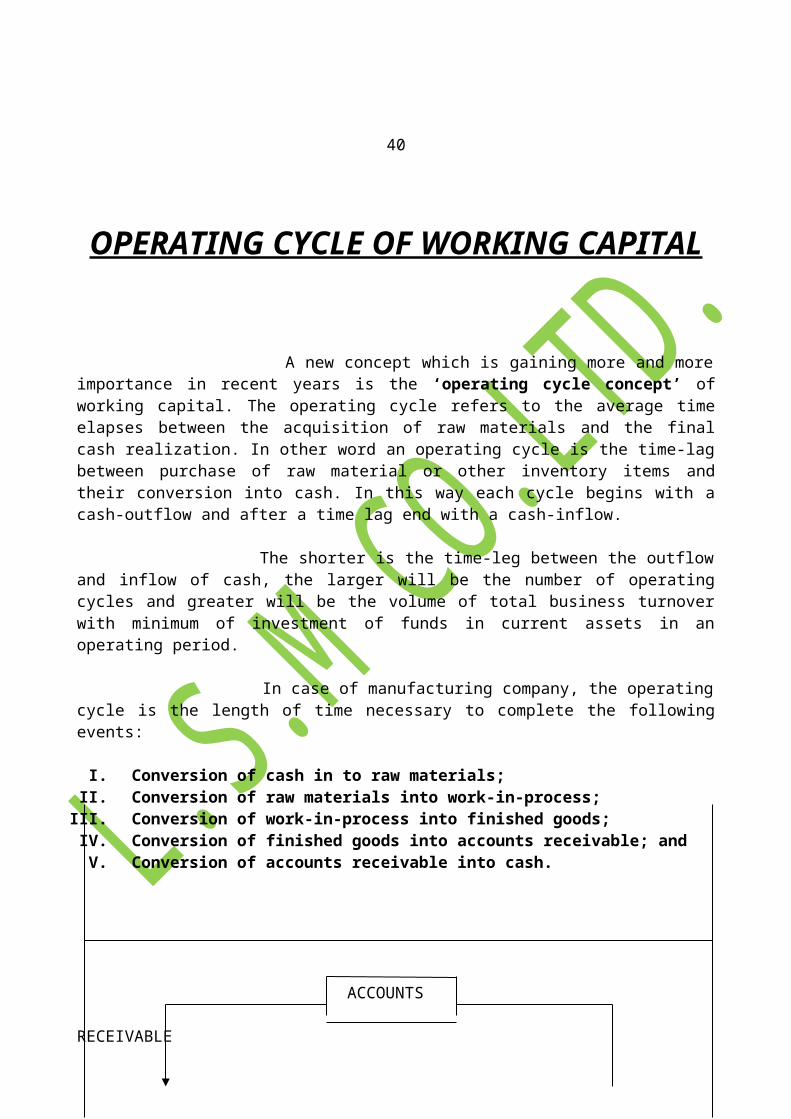

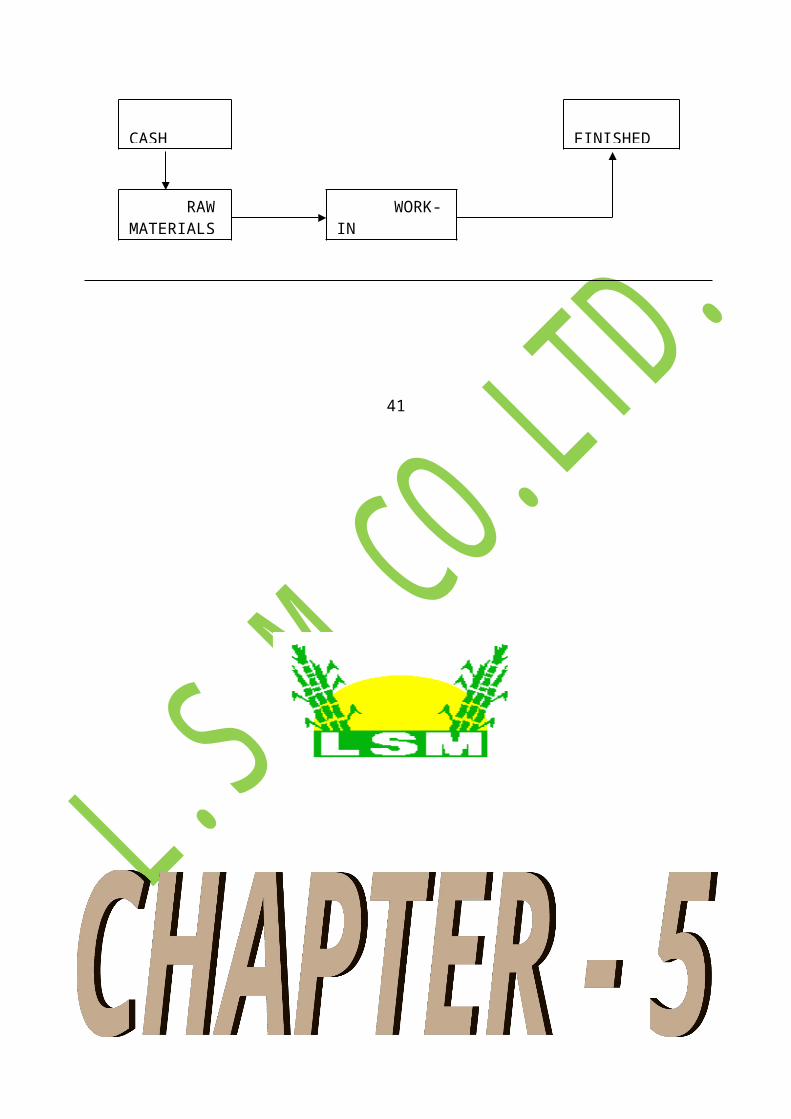

OPERATING CYCLE OF WORKING CAPITAL

A new concept which is gaining more and more importance in recent years is the ‘operating cycle concept’ of working capital. The operating cycle refers to the average time elapses between the acquisition of raw materials and the final cash realization. In other word an operating cycle is the time-lag between purchase of raw material or other inventory items and their conversion into cash. In this way each cycle begins with a cash-outflow and after a time lag end with a cash-inflow.

The shorter is the time-leg between the outflow and inflow of cash, the larger will be the number of operating cycles and greater will be the volume of total business turnover with minimum of investment of funds in current assets in an operating period.

In case of manufacturing company, the operating cycle is the length of time necessary to complete the following events:

I. Conversion of cash in to raw materials;II. Conversion of raw materials into work-in-process;

III. Conversion of work-in-process into finished goods;IV. Conversion of finished goods into accounts receivable; and V. Conversion of accounts receivable into cash.

ACCOUNTS

RECEIVABLE

CASH FINISHED GOODS

RAWMATERIALS

WORK-IN PROCESS

41

42

PRODUCT PROFILE

1. SUGAR :-

Sugar is a carbohydrate that occurs naturally in every fruit and vegetable. It is a major product of photosynthesis, the process by which plants transform the sun's energy into food. Sugar occurs in greatest quantities in sugarcane from which it is separated for commercial use.

The natural sugar stored in the cane stalk is separated from rest of the plant material through a process known as refining.

For sugarcane, the process of refining is carried out in following steps:

Pressing of sugarcane to extract the juice.

Boiling the juice until it begins to thicken and sugar begins to crystallize.

Spinning the crystals in a centrifuge to remove the syrup, producing raw sugar.

Shipping the raw sugar to a refinery where it is washed and filtered to remove remaining non-sugar ingredients and color.

Crystallizing, drying and packaging the refined sugar.

Sugar Production is Divided into Three Categories:-

1. M – 31 ( medium size)2. S - 31 ( small size )3. L – 31 ( large size )

43

STOCK MAINTAINED BY COMPANY:- 10% FOR LEVY SALE

TOTAL PRODUCTION OF SUGAR 90% FOR FREE SALE

LEVY SUGAR:-It stands for the quota for government which is maintained by the

Company. This is 10% of total production and the levy is maintained for Defense supply and for government quota by which the product is Distributed to those peoples who comes under the category of below Poverty line.

FREE SUGAR:- It stands for the quota for company which is sold freely by the company in market. This is 90% of total production.

2. BAGASSES :-

It is a residue from cane which is obtained after the extraction of juice. It is used as a fuel in boil generation of steam. Surplus bagasse, if any, is sold off.

3. PRESS MUD :-

This is obtained in the clarification process of juice due to change in mfg. process system. Now it has sold for use as fertilizer and fuel purpose.

44

4. MOLASSES :-

It is obtained when further crystallization of sugar is not possible from the syrup. It is a controlled and free sale commodity and control share is sold to the allottees as per state government order and free sale to be sold in open market.

45

PROCESS OF MANUFACTURE

The plant uses double sulphitation process for manufacturing of white sugar.

The juice extracted in mills is heated up to 70 degree C. in juice heaters and sent to sulphitors, where milk of lime (calcium hydroxide) is added and sulphur-di-oxide gas was passed.

Final pH is maintained 7.0 some non sugar are observed in the precipitates formed due to the reaction of lime and sulphur-di-oxide gas. This precipitated juice heated up to 102-105 degree C. and then sent to Dorr clarifier for settling. The settled concentrated mud is sent to filter station where it is filtered through vacuum filters. The precipitated impurities are removed as filter cake and the filtered juice is against sent for process.

The decanted juice heated up to 105 degree C. and then sent to evaporators and concentrated up to 60-65 degree Bx. The concentrated juice is now called syrup is again sulphited to pH 5.2 to 5.4 and sent to pan station for further concentration and crystallization of sugar.

The crystallized sugar mass obtained in pan is known as massecuite which is sent to crystallizer for cooling & further crystallization. The mesquite is then passed through centrifugal for separation of sugar and molasses. The sugar is bagged after cooling and grading while the molasses are boiled for further extraction of sugar in it. The final molasses, from which further extraction of sugar is not feasible, is sent to storage tank.

The By-Products are:-

1. Bagasses 2. Press Mud 3. Molasses

46

47

RESEARCH METHODOLOGY

All study is based upon primary as well as secondary data. Therefore, information has been collected frpm various magazine, journal, website, and bulletin, trainee of last year student etc.

Research Design

The formidable problem that follows the task of defining the research problem is the preparation of the design of the research project, populary known as the “research design”. Decision regarding what, when, how much, by what means concerning an inquiry or a research study constitute a research design.

Data Collection

Collection of data is the critical point in the research process. There are two basic methods of the data collection.

L 31 (Large size) M 31 (medium size) S 31 (Small size)

49

OBJECTIVE OF THE STUDY

This research project covers the most important aspects or features of the functioning of the SALES & FINANCE ACCOUNTS DEPARTMENT of the LAKSHMI SUGAR MILLS CO.LTD.

This part includes both, an analytical as well as an academic study that involves an analysisof the working capital management policies of the organization- L.S.M Co. Ltd.

The main objectives of this study are:-

1) To understand the working capital management policies of the organization.

2) To understand the importance of working capital.

3) To analyze the liquidity position of the organization.

4) To analyze the short term financing policies and patterns, which affects the working capital of the organization.

5) To study the factors that affects the sales & working capital management at L.S.M Co. Ltd.

6) To find out the profitability and operational efficiency of the organization.

7) To analyze the data and information of the previous years to know the actual position of funds, investment and liabilities of the organization.

8) To identify some broad policy measures to improve the working capital position of the organization.

9) To estimate the working capital requirements of the organization in the near future.

From the above data we study that in year 2008-09 the production of main product and their by products are more in camparision to the other years the main resion behind this is that in the following year the availability of raw materil is hight and regarding this the company having long crushing period

We study frome the above data that price of main product in the year 2007-08 is hight this is becouse of low production in the year 2006-07 due to this low production the supply didn’t full fill the demand of product in the market which causes rising price of the product

From the above data we finds that in the year 2009-10 the sale of main product is hight in camparision to other years. This is becouse the production of the sugar in the year 2007-08 is more and the avialability or supply is hight in the market that’s why price for the product goes downward in the year 2009-10.

55

Capital structure of L.S.M. Co. Ltd.

Sources AmountShare capital (Promoter contr.) 432.9Loan from Finance Institution 2119.5Loan from S.D.F. 1695.6

From the data we understand about the capital structure of the company. This data shows that the 50% of the total capital is borrowed form the financial institutions and only 10% is invested by the promoters of the company this shows that company maintains their goodwill in the market and better financial position.

56

Current Assets and Current Liabilities of L.S.M Co.Ltd.

From the study of Current Assets and liabilities we understand that company is growing year by year. There was a rapid growth in current assets in the year 2008-09.But the liabilities of the

company also increases in the year 2009-10.

57

Yearly Changes in Working Capital of L.S.M Co. Ltd.

From the study of above data we finds that in the year 2008-09 there was a maximum availability of working capital but due to the payment of liabilities or the increase in the liabilities in the year 2009-10 the company’s working capital goes downwards in the year 2009-10.

58

59

LIMITATIONS

The purchase price of raw material and selling price of finished goods are declared by the state and central government of the country.

Limited area for the purchase of raw material. This area for raw material also given under the guide lines of the government.

The presence of competitors is high where the area for collecting the raw material is limited.

Illegal competitors (kholous, crashers) are also effects the performance of the company. And against them government cannot take any action.

Company also maintains the government quota of products (sugar, molasses) against which government didn’t give the actual price for that, only little amount amount was given to the company.

Company also affected by the political factors and by the government policies.

60

61

CONCLUSION

During the time of training I found most of the factors are against the company but still the company works efficiently and effectively. In this field the government plays an important role to control the sale of the products and purchase of raw material.

The following conclusion can be drawn from the project that I have completed:-

The company bears the low amount against the supply of government quota.

For the better production company needs the raw material in huge amount, so for this company encourages the farmers and giving the knowledge for new techniques of farming.

Company also provides the new verities of sugarcane and fertilizers which are used in the farming at sufficient price.

I also study that company borrowed 50% of total capital invested from the financial institutions which shows that company having a good strategy for the upliftment of the company.

Over all the company depends upon the environmental and political factors.