31

PX-PTA-Polyester in India YJ Kim PCI Xylenes & Polyesters Asia Thursday 30 October 2014 Mumbai 2014 Indian Petchem Conference

PX-PTA-Polyester in India

YJ Kim

PCI Xylenes & Polyesters Asia

Thursday 30 October 2014 Mumbai

2014 Indian Petchem Conference

Agenda

PX trade flows and margins.

PTA landscape and pricing changes

Polyester demand growth potential and profitability.

Thursday 30 October 2014 Mumbai2014Indian Petrochem Conference

World Paraxylene Capacity Growth 2012-2018

3 new units completed in 2013 and another 8 new units completed in 2014

MT%

2.44.8

0.41.2

2.9 7.5

4.7 11.3

3.5 7.7

2.54.8

2.7 4.9

Growth per annum

88%

90%

4.0

5.02014.

Utilisation rates drop from the high 80’s to the low 80’s.

Asset clos res (or idling) in Korea

84%

86%

2 0

3.0

n To

nnes

Asset closures (or idling) in Korea, Japan and Taiwan has been underway for 8 months. Anticipate similar asset outages in Europe and

80%

82%

1.0

2.0

Milli

on

g pNorth America.

Further slowing of announced investments anticipated to allow

76%

78%

-1.0

0.0

2012 2013 2014 2015 2016 2017 2018

some margin recovery in the 2017+ time frame.

2012 2013 2014 2015 2016 2017 2018

North America South AmericaEurope Middle East/AfricaAsia/Far East Utilisation (RHS)

Thursday 30 October 2014 Mumbai2014Indian Petrochem Conference

( )

India Paraxylene Supply Demand

Capacity doubles in a 2 year period

New investment supports downstream growth

94%7 p y y p

OMPL and RIL both have integration links to PTA (JBF and RIL)90%

92%

5

6

Utilization rates ease as potential for PTA and PX exports is limited

84%

86%

88%

4

5

on T

onne

s

80%

82%

84%

2

3

Mill

io

76%

78%

80%

0

1

2013 2014 2015 2016 2017 2018

Total Production Total ConsumptionCapacity Utilisation Rate

Thursday 30 October 2014 Mumbai2014Indian Petrochem Conference

p y

Paraxylene Capacity Status 2014Country Location Company Nameplate

Capacity or Expansion

(Thousand Tonnes)

Feedstock Actual or Proposed Startup

China Sichuan, Pengzhou Petrochina Sichuan Petrochemical 650 HVN Q1 2014

China Hainan, Yangpu Sinopec Hainan Refining 1 600 HVN Q1 2014

Japan Mats ama TS Aromatics 290 MX Q1 2014Japan Matsuyama TS Aromatics -290 MX Q1 2014

Saudi Arabia Al-Jubail SATORP 660 HVN Q1 2014

Korea Ulsan Ulsan Aromatics 1,000 MX/C7/C9 Q2 2014

India Mangalore ONGC Mangalore Petrochemicals 920 HVN Q3 2014

Korea Daesan Samsung Total 2 1,000 COND Q3 2014

Korea Inchon SK Energy 1,300 COND Q3 2014gy ,

Singapore Jurong Jurong Aromatics Corp 800 COND Q3 2014

Algeria Skikda Sonatrach 220 HVN Q4 2014

2014 Total 6 8602014 Total 6,860

Thursday 30 October 2014 Mumbai2014Indian Petrochem Conference

Paraxylene Capacity Status 2015-2016

Country Location Company Nameplate Capacity or

Feedstock Actual or Proposed

Expansion (Thousand Tonnes)

Startup

Kazakhstan Atyrau JSC KazMunaiGas 469 HVN Q2 2015

India Jamnagar Reliance Industries 4 2,250 HVN Q3 2015

Thailand Mab ta Phut PTTGC 120 HVN Q3 2015

2015 Total 2,839

Thailand Mab ta Phut PTTGC 85 MX Q1 2016

Thailand Mab ta Phut PTTGC 40 MX Q1 2016

Saudi Arabia Rabigh PetroRabigh 1,300 HVN Q3 2016

2016 Total 1,325

Thursday 30 October 2014 Mumbai2014Indian Petrochem Conference

Key Country PX Trade Flow Changes 2013-2018

6

7

4

5

6

2

3

4

n To

nnes

0

1

2

Mill

ion

2

-1

0

-2Korea Japan Singapore KSA India Indonesia Taiwan

2013 2014 2015 2016 2017 2018

Thursday 30 October 2014 Mumbai2014Indian Petrochem Conference

Cost Curve April 2014 (Asia Spot $1,209, PX-Naphtha $270)

Brent Crude Oil $108.15/barrel$

STDP $1,130

MX $1,200

TA $1 310TA $1,310

Chart Source: PCI’s Online Paraxylene Global Cost Model

Thursday 30 October 2014 Mumbai2014Indian Petrochem Conference

PCI Cost Model PX-Naphtha Values for March 2015 PX Forecast

$/Tonne Constrained Unconstrained

Cash Cost Breakeven 300 260Variable Cost B k 260 210Breakeven 260 210

Constrained = Production Balance, Supply=DemandUnconstrained = Supply>Demand, High Level of Competition

PCI PX-Naphtha Spread Forecast $280/tonne

Transalkylation Variable Costs economic assumes constrained yproduction with marginal assets not quite covering full cash costs

Thursday 30 October 2014 Mumbai2014Indian Petrochem Conference

PCI Cost Model PX-Naphtha Values for June 2015 PX Forecast

$/Tonne Constrained Unconstrained

Cash Cost Breakeven 410 330Variable Cost B k 370 300Breakeven 370 300

Constrained = Production Balance, Supply=DemandUnconstrained = Supply>Demand, High Level of Competition

PCI PX-Naphtha Spread Forecast $350/tonne

Transalkylation Variable Costs not quite covered assumes y qconstrained production with marginal assets not quite covering variable costs

Thursday 30 October 2014 Mumbai2014Indian Petrochem Conference

A Future for ACP?

PX and PTA ACP negotiators should be able to support downstream polyester markets, end uncertainty and fix monthly ACP if PTA cost-plus system remains intactplus system remains intact.

PTA sector still needs to robustly negotiate PX values to protectPTA sector still needs to robustly negotiate PX values to protect integrity of polyester chain economics both upstream and downstream.

Stability and pricing visibility is more likely to lead to stronger growth than opaque, retrospective price-setting mechanisms of the past 8 months.

ACP should survive and provide a platform for polyester chain economics to be visible and support positive decision-making in every sector.

Thursday 30 October 2014 Mumbai2014Indian Petrochem Conference

Paraxylene Summary

PCI’s Online Paraxylene Global Cost Model indicates PX-Naphtha spread of between $280 and $350 per tonne, depending on the t th f th li lt tistrength of the gasoline alternatives.

This period of low PX margins is likely to last though 2016 with p g y grecovery beyond this dependent on slowing of announced investments to allow some margin recovery in the 2017+ time frame.

PX asset idling and rationalisation in all regions.

I di f th j t i 2015 17 b t b l India emerge as one of the major export in 2015-17 but balance stabilizes on robust local demand growth.

Thursday 30 October 2014 Mumbai2014Indian Petrochem Conference

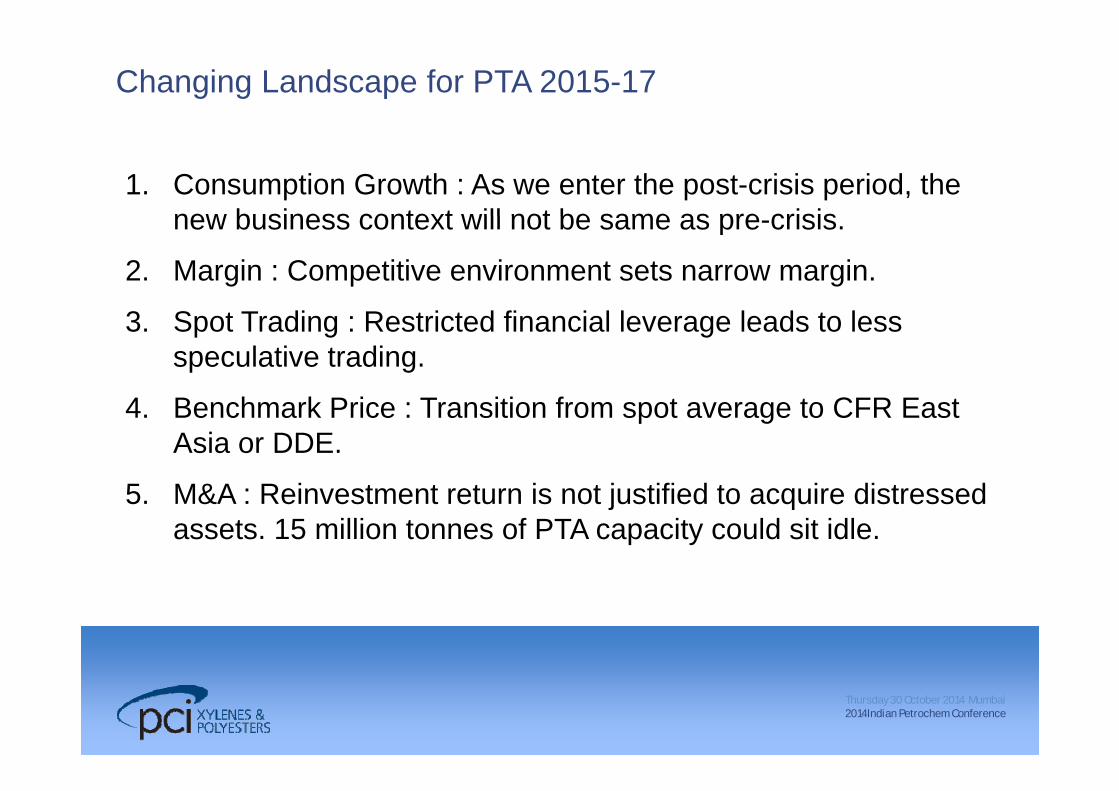

Changing Landscape for PTA 2015-17

1. Consumption Growth : As we enter the post-crisis period, the new business context will not be same as pre crisisnew business context will not be same as pre-crisis.

2. Margin : Competitive environment sets narrow margin.

3. Spot Trading : Restricted financial leverage leads to less speculative trading.

4. Benchmark Price : Transition from spot average to CFR East Asia or DDE.

5 M&A R i t t t i t j tifi d t i di t d5. M&A : Reinvestment return is not justified to acquire distressed assets. 15 million tonnes of PTA capacity could sit idle.

Thursday 30 October 2014 Mumbai2014Indian Petrochem Conference

World PTA Supply Demand

Demand growth remains 95%90

solid at 6% +.

Overcapacity in Asia set to d i t k t d i80%

85%

90%

60

70

80

s dominate market dynamics for next 3 years.

Plant closures are being70%

75%

80%

40

50

60

lion

Tonn

es

Plant closures are being seen, mostly in Asia but do little to offset surplus 60%

65%

70%

20

30

40

Mill

capacity.

Production discipline in 2011 2012 2013 2014 2015 2016

50%

55%

0

10

China is the key to market stability.

2011 2012 2013 2014 2015 2016

Total Production Total ConsumptionCapacity Utilisation Rate

Thursday 30 October 2014 Mumbai2014Indian Petrochem Conference

Indian Subcontinent PTA Supply Demand

One of few current net Market will be in transition in 2015

90%9import areas but 1 million tonne import disappear in 201586%

88%

90%

7

8

9

2015.

Demand growth forecast at 9%82%

84%

86%

5

6

n To

nnes

9%.

Large scale PTA capacity growth will swing India’s 78%

80%

82%

2

3

4

Mill

ion

g gtrade position.

Reliance and JBF start-ups 74%

76%

0

1

2

will directly impact Korea/Thailand balances.

2011 2012 2013 2014 2015 2016

Total Production Total ConsumptionCapacity Utilisation Rate

Thursday 30 October 2014 Mumbai2014Indian Petrochem Conference

Monthly PX Price Page

FAR EAST 24-Jun-14 31-Jul-14 29-Aug-14PTA PCI Index * CFR $/tonne 974 1 018 1 1 030PTA PCI Index CFR $/tonne 974 1,018 1,030PTA East Asia (new price) CFR $/tonne n/a n/a 1,020PTA China Domestic DEL RMB/tonne 7,450 7850-7900 7675-7750PTA China Delivered Dollar

Eq i alent (ne price)DDE DEL $/tonne n/a n/a 1,011

Equivalent (new price)

PTA China Imports CFR $/tonne 955-965 995-1105 1 1000-1020PTA China Spot * CFR $/tonne 897-977 960-1009 990-1035PTA China ChiPIX * CFR $/tonne 956.35 994.17 1011.71PTA India Domestic EXW Rs/tonne 64,300 67,400 71,700PTA Pakistan L/C opening CFR $/tonne 995 1,020 1 1,033DMT Imports CFR $/tonne 1420-1430 1480-1490 1455-1465MEG PCI L/C opening CFR $/tonne 1065-1090 1110-1130 1140-1150MEG PCI L/C opening CFR $/tonne 1065 1090 1110 1130 1140 1150Methanol Imports CFR $/tonne 430 410 410PET Resin Exports FOB $/tonne 1300-1350 1350-1400 1320-1350Polyester Chip Imports CFR $/tonne 1250-1260 1290-1300 1290-13001 5 d St l R i l CFR ¢/lb 60 66 64 68 62 671.5 den Staple Regional CFR ¢/lb 60-66 64-68 62-67150 den POY Regional CFR ¢/lb 59-61 59-61 60-61Exchange Rate Average Indian Rupee : US$ 59.74 60.06 60.92Exchange Rate Average Chinese RMB : US$ 6.23 6.2 6.16

Thursday 30 October 2014 Mumbai2014Indian Petrochem Conference

Outlook for PTA

Asia margins could be volatile as China’s production discipline will be constantly challenged by themselveswill be constantly challenged by themselves.

Rate of investment is slowing, but capacity will continue to be added into 2015 driving down overall industry utilizationadded into 2015, driving down overall industry utilization.

Plant closures have been carried out and more are planned, but are too small and too few to have any meaningful impact onare too small and too few to have any meaningful impact on utilisation and margin in the next 18 months.

Asset renewal is one of the few options for survival, but this canAsset renewal is one of the few options for survival, but this can lead to further unwanted capacity, keeping margins persistently low and extending to current down cycle for several more years tto come.

Thursday 30 October 2014 Mumbai2014Indian Petrochem Conference

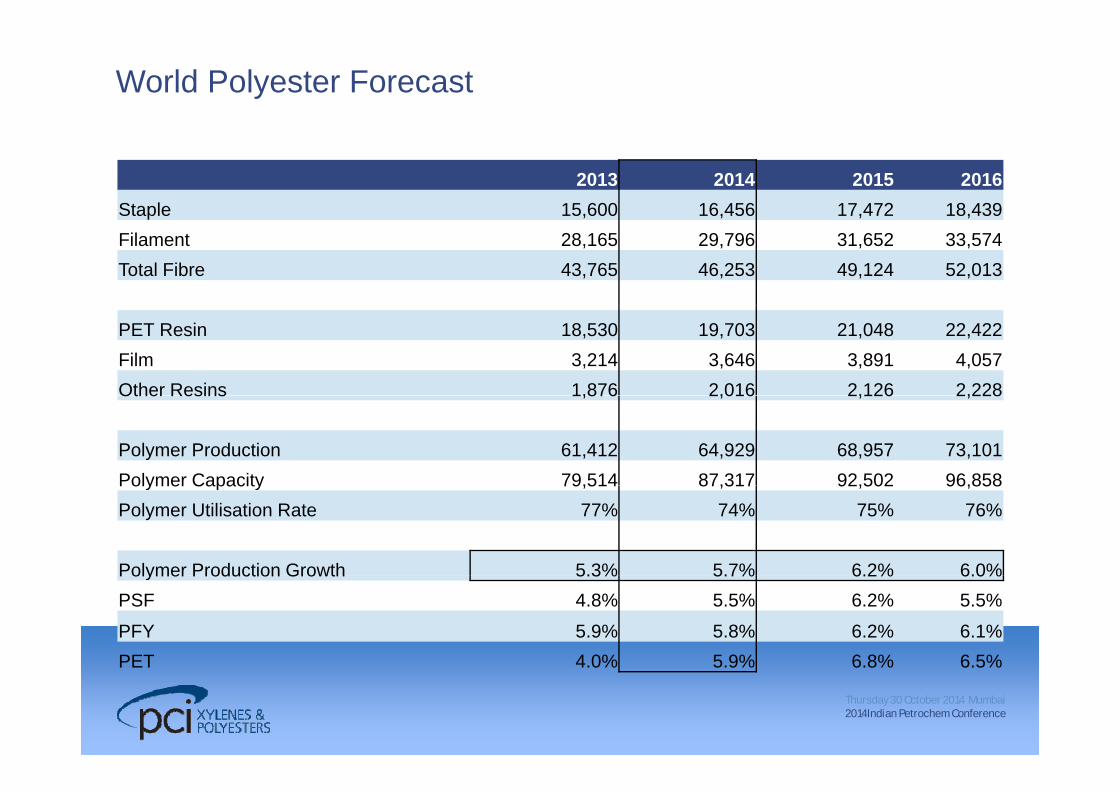

World Polyester Forecast

2013 2014 2015 2016Staple 15,600 16,456 17,472 18,439p , , , ,Filament 28,165 29,796 31,652 33,574Total Fibre 43,765 46,253 49,124 52,013

PET Resin 18,530 19,703 21,048 22,422Film 3,214 3,646 3,891 4,057Other Resins 1,876 2,016 2,126 2,228Other Resins 1,876 2,016 2,126 2,228

Polymer Production 61,412 64,929 68,957 73,101Polymer Capacity 79,514 87,317 92,502 96,858Polymer Capacity 79,514 87,317 92,502 96,858Polymer Utilisation Rate 77% 74% 75% 76%

Polymer Production Growth 5.3% 5.7% 6.2% 6.0%Polymer Production Growth 5.3% 5.7% 6.2% 6.0%PSF 4.8% 5.5% 6.2% 5.5%

PFY 5.9% 5.8% 6.2% 6.1%PET 4 0% 5 9% 6 8% 6 5%

Thursday 30 October 2014 Mumbai2014Indian Petrochem Conference

PET 4.0% 5.9% 6.8% 6.5%

China textile mill consumption

60000

'000 tonnes

50000

60000WoolAcrylicPolypropylene

Source: PCI Fibres Green Book.

40000

yp pyNylon stapleNylon carpet filamentNylon industrial + other fil

20000

30000 Nylon textile filamentCellulosicPolyester staple

10000

Polyester other filamentPolyester industrial filamentPolyester textile filament

0

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Cotton

Thursday 30 October 2014 Mumbai2014Indian Petrochem Conference

China Polyester Forecast

2013 2014 2015 2016Staple 9,748 10,137 10,832 11,482Staple 9,748 10,137 10,832 11,482Filament 19,873 21,092 22,519 24,110Total Fibre 29,621 31,229 33,351 35,592

PET Resin 5,332 5,550 5,670 5,851Film 961 1,213 1,333 1,383Other Resins 243 258 284 320

Polymer Production 33,052 34,789 36,798 39,050Polymer Capacity 39,856 44,874 47,783 50,712y p y , , , ,Polymer Utilisation Rate 82.9% 77.5% 77.0% 77.0%

Polymer Production Growth 7.7% 5.3% 5.8% 6.1%yPSF 4.9% 4.0% 6.9% 6.0%PFY 6.6% 6.1% 6.8% 7.1%PET 14.2% 4.1% 2.2% 3.2%

Thursday 30 October 2014 Mumbai2014Indian Petrochem Conference

India Polyester Forecast

2013 2014 2015 2016Staple 1,230 1,335 1,450 1,590Staple 1,230 1,335 1,450 1,590Filament 2,890 3,130 3,320 3,530Total Fibre 4,120 4,465 4,770 5,120

PET Resin 900 1,020 1,140 1,320Film 393 430 480 540Other Resins 12 10 10 10

Polymer Production 5,210 5,664 6,124 6,676Polymer Capacity 7,044 7,735 8,488 8,887y p y , , , ,Polymer Utilisation Rate 73.8% 73.1% 72.0% 75.1%

Polymer Production Growth 9.5% 8.8% 8.1% 9.2%yPSF 9.4% 8.5% 8.6% 9.7%PFY 7.0% 8.3% 6.1% 6.3%PET 25.0% 13.3% 11.8% 15.8%

Thursday 30 October 2014 Mumbai2014Indian Petrochem Conference

India textile mill consumption

14000

'000 tonnes

12000

14000WoolAcrylicPolypropylene

Source: PCI Fibres Green Book.

8000

10000yp py

Nylon stapleNylon carpet filamentNylon industrial + other fil

4000

6000Nylon textile filamentCellulosicPolyester staple

2000

4000 Polyester other filamentPolyester industrial filamentPolyester textile filament

0

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Cotton

Thursday 30 October 2014 Mumbai2014Indian Petrochem Conference

Asia Polyester Production Growth by Key Country 2013-2020

18 020.0

18.1A A l G th

12 014.016.018.0

es

18.1Average Annual GrowthChina vs India 2011‐2015 2016‐2020

China 2.3 2.6

India 0 370 0 734

8.010.012.0

lion

Tonn

e India 0.370 0.734

India Growth as % of China 16% 28%

2.04.06.0

Mill

3.1 2.4 2.93.2 2.4

-2.00.0

2011 2012 2013 2014 2015 2016-2020 CumulativeCumulative

Growth

China India Korea Taiwan Indonesia Thailand

Thursday 30 October 2014 Mumbai2014Indian Petrochem Conference

Polyester Staple Supply/Demand - India

ti t'000 t

Production Mill Consumption Capacity Utilisation

100%2500

operating rate'000 tonnes

Source: PCI Fibres Green Book.

60%

80%

1500

2000

40%1000

20%500

0%0

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Thursday 30 October 2014 Mumbai2014Indian Petrochem Conference

Polyester Filament Supply/Demand - India

Production Mill Consumption Capacity Utilisation

100%6000operating rate'000 tonnes

Source: PCI Fibres Green Book.

60%

80%

3600

4800

40%2400

20%1200

0%0

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Thursday 30 October 2014 Mumbai2014Indian Petrochem Conference

Global Trade Flows Forecast-PET

4000

2000

3000

0

1000

2012 2013 2014 2015 2016 2017 2018Metri

c Ton

s

-2000

-1000

2012 2013 2014 2015 2016 2017 2018

000 M

-4000

-3000

4000North America South America West EuropeEast Europe Africa & Middle East Indian SubcontinentChina NE Asia Rest of Asia

Thursday 30 October 2014 Mumbai2014Indian Petrochem Conference

Polyester Profitability ($/ton equivalent)

250

300

150

200

50

100

100

-50

0

-150

-100

Jul Aug Sep Sep W3 Sep W4 Oct W1 Oct W2

SD Polyester Chip PSF POY PET FDY DTY

Thursday 30 October 2014 Mumbai2014Indian Petrochem Conference

Outlook for Polyester

Margin cycle may have bottomed out for polyester, with increasingly competitive PX/PTA prices giving some positiveincreasingly competitive PX/PTA prices giving some positive outlook.

Inventory release from China’s cotton stockpile may negatively Inventory release from China s cotton stockpile may negatively impact PSF.

Scale investment continues to drive the business cycleScale investment continues to drive the business cycle, although at reduced rate.

Many polyester assets sit idle in China, Korea, and Taiwan butMany polyester assets sit idle in China, Korea, and Taiwan but those plants are likely to be scrapped as M&A options are limited.

Thursday 30 October 2014 Mumbai2014Indian Petrochem Conference

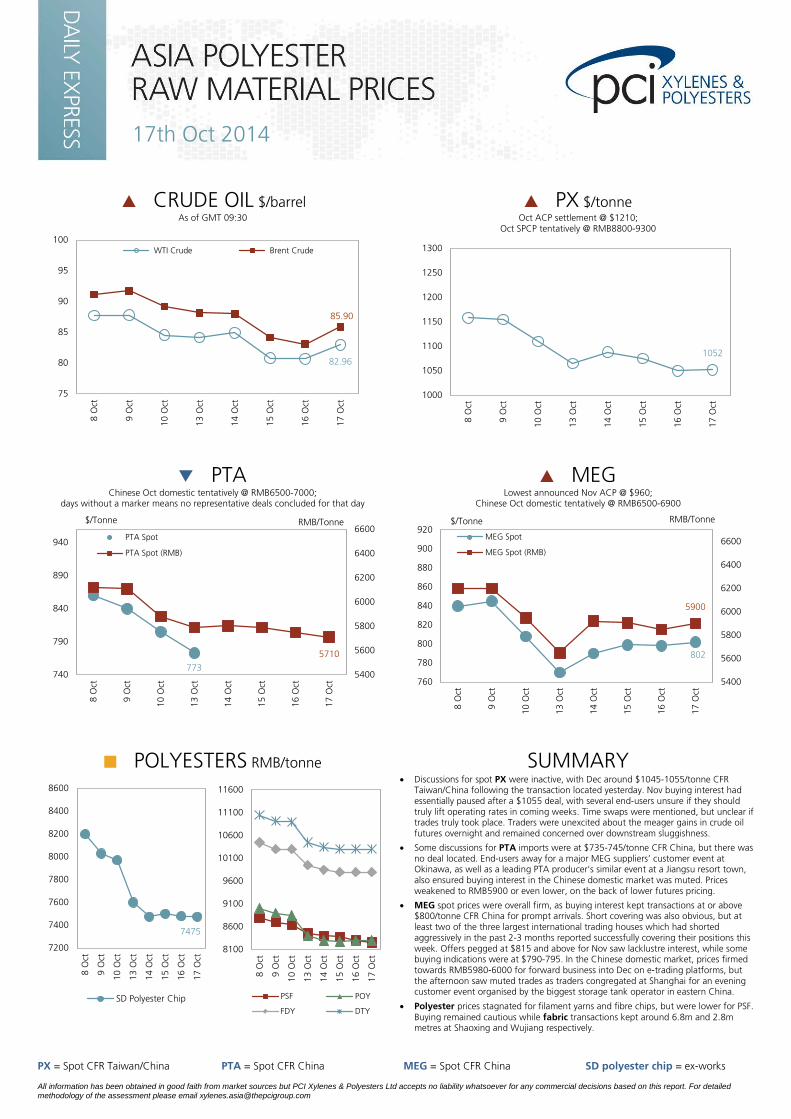

17th Oct 2014

PX = Spot CFR Taiwan/China PTA = Spot CFR China MEG = Spot CFR China SD polyester chip = ex-works All information has been obtained in good faith from market sources but PCI Xylenes & Polyesters Ltd accepts no liability whatsoever for any commercial decisions based on this report. For detailed methodology of the assessment please email [email protected]

CRUDE OIL $/barrel As of GMT 09:30

PX $/tonne Oct ACP settlement @ $1210;

Oct SPCP tentatively @ RMB8800-9300

PTA Chinese Oct domestic tentatively @ RMB6500-7000;

days without a marker means no representative deals concluded for that day

MEG Lowest announced Nov ACP @ $960;

Chinese Oct domestic tentatively @ RMB6500-6900

POLYESTERS RMB/tonne

SUMMARY • Discussions for spot PX were inactive, with Dec around $1045-1055/tonne CFR

Taiwan/China following the transaction located yesterday. Nov buying interest had essentially paused after a $1055 deal, with several end-users unsure if they should truly lift operating rates in coming weeks. Time swaps were mentioned, but unclear if trades truly took place. Traders were unexcited about the meager gains in crude oil futures overnight and remained concerned over downstream sluggishness.

• Some discussions for PTA imports were at $735-745/tonne CFR China, but there was no deal located. End-users away for a major MEG suppliers’ customer event at Okinawa, as well as a leading PTA producer’s similar event at a Jiangsu resort town, also ensured buying interest in the Chinese domestic market was muted. Prices weakened to RMB5900 or even lower, on the back of lower futures pricing.

• MEG spot prices were overall firm, as buying interest kept transactions at or above $800/tonne CFR China for prompt arrivals. Short covering was also obvious, but at least two of the three largest international trading houses which had shorted aggressively in the past 2-3 months reported successfully covering their positions this week. Offers pegged at $815 and above for Nov saw lacklustre interest, while some buying indications were at $790-795. In the Chinese domestic market, prices firmed towards RMB5980-6000 for forward business into Dec on e-trading platforms, but the afternoon saw muted trades as traders congregated at Shanghai for an evening customer event organised by the biggest storage tank operator in eastern China.

• Polyester prices stagnated for filament yarns and fibre chips, but were lower for PSF. Buying remained cautious while fabric transactions kept around 6.8m and 2.8m metres at Shaoxing and Wujiang respectively.

82.96

85.90

75

80

85

90

95

100

8 O

ct

9 O

ct

10 O

ct

13 O

ct

14 O

ct

15 O

ct

16 O

ct

17 O

ct

WTI Crude Brent Crude

1052

1000

1050

1100

1150

1200

1250

1300

8 O

ct

9 O

ct

10 O

ct

13 O

ct

14 O

ct

15 O

ct

16 O

ct

17 O

ct

773

5710

5400

5600

5800

6000

6200

6400

6600

740

790

840

890

940

8 O

ct

9 O

ct

10 O

ct

13 O

ct

14 O

ct

15 O

ct

16 O

ct

17 O

ct

RMB/Tonne $/Tonne

PTA Spot

PTA Spot (RMB)

802

5900

5400

5600

5800

6000

6200

6400

6600

760

780

800

820

840

860

880

900

920

8 O

ct

9 O

ct

10 O

ct

13 O

ct

14 O

ct

15 O

ct

16 O

ct

17 O

ct

RMB/Tonne $/Tonne

MEG Spot

MEG Spot (RMB)

7475

7200

7400

7600

7800

8000

8200

8400

8600

8 O

ct

9 O

ct

10 O

ct

13 O

ct

14 O

ct

15 O

ct

16 O

ct

17 O

ct

SD Polyester Chip

8100

8600

9100

9600

10100

10600

11100

11600

8 O

ct

9 O

ct

10 O

ct

13 O

ct

14 O

ct

15 O

ct

16 O

ct

17 O

ct

PSF POY

FDY DTY

13th Oct 2014

NOTE: Spot prices reflect weekly averages extracted from PCI’s Daily Express Report. Please contact Salmon Lee, [email protected], if you require a copy of the methodology. Key: PCI Index = Weighted PCI Price in Asia; ChiPIX = PCI monthly mean price CFR China; SD Polyester Chip, PSF, POY, PET = ex-works RMB converted to US$; F = Forecast; T = Tentative, TBC=To be confirmed; SA = Spot Price Average (no contract settlement) All information has been obtained in good faith from market sources but PCI Xylenes & Polyesters Ltd accepts no liability whatsoever for any commercial decisions based on this report.

CRUDE OIL $/barrel

PARAXYLENE $/tonne

PTA $/tonne + RMB/tonne

MEG $/tonne + RMB/tonne

PRICES AT A GLANCE

WEEKLY Oct W1 Oct W2 Week-on-Week

Trend One-Week Projection

Crude Oil WTI Contract $/Barrel 91.44 87.62 N/A Crude Oil Brent $/Barrel 93.30 90.09 N/A Paraxylene Spot (Taiwan/China) CFR $/Tonne 1243 1141 PTA* Weekly Spot Average (China domestic) RMB/Tonne 6525 6036 MEG Weekly Spot Average (China) CFR $/Tonne 897 831 MEG Weekly Spot Average RMB/Tonne 6548 6116 DEG Weekly Spot (China) CFR $/Tonne 1165 1085 DEG Weekly Spot (East China) RMB/Tonne 8800 8250 DEG Weekly Spot (South China) RMB/Tonne 8850 8300

MONTHLY Sep Oct Monthly Trend One-Month Projection

Paraxylene Asian Contract Price CFR $/Tonne 1254SA 1210 Paraxylene SPCP China domestic contract RMB/Tonne 9150 8800T PTA** ChiPIX (China) CFR $/Tonne N/A N/A - PTA*** East Asia CFR $/Tonne 930 829F PTA Chinese domestic contract RMB/Tonne 6900-7050 6500-7000T PTA*** Delivered Dollar Equivalent CFR $/Tonne 919 856T PTA Contract (China) CFR $/Tonne 930 N/A MEG Lowest announced ACP (Asia) CFR $/Tonne 1150 1100T MEG ChiPIX (China) CFR $/Tonne 929.10 830F MEG Chinese domestic contract RMB/Tonne 7075 6500

* quoted in RMB/tonne from September 2014; ** to be discontinued after December 2014; ***new Asia PTA price series

102.92

96.38 93.21 93.54 93.11

91.44

87.62

106.52

101.28

97.14 96.84 95.10

93.30

90.09

Jul Aug Sep Sep W3 Sep W4 Oct W1 Oct W2

WTI Brent Crude Oil

1415SA

1356SA

1255SA 1210

1105 1100

1415

1356

1254 1243 1251 1243

1141

Jul Aug Sep Sep W3 Sep W4 Oct W1 Oct W2 Oct Nov F Dec F

Contract Spot

1000 1010

1018 1029

943

994.17 1011.71 930

829 789 796

6680 6608 6525

6036

7875 7713

6975

Jul Aug Sep Sep W3 Sep W4 Oct W1 Oct W2 Oct F Nov F Dec F

CFR China (Contract) PCI Index ChiPIX CFR East Asia Spot (RMB) China Contract (RMB)

1110 1140 1150 1100

929 891 897 831 830

780 780

991.87 990.81 929.10

1220 1165 1165

1085

6850 6553 6548

6116

Jul Aug Sep Sep W3 Sep W4 Oct W1 Oct W2 Oct F Nov F Dec F

MEG Lowest Announced ACP MEG Spot

MEG ChiPIX DEG Spot

MEG Spot (RMB)

SA = no official settlement; spot price average

13th Oct 2014

NOTE: Spot prices reflect weekly averages extracted from PCI’s Daily Express Report. Please contact Salmon Lee, [email protected], if you require a copy of the methodology. Key: PCI Index = Weighted PCI Price in Asia; ChiPIX = PCI monthly mean price CFR China; SD Polyester Chip, PSF, POY, PET = ex-works RMB converted to US$; F = Forecast; T = Tentative, TBC=To be confirmed; SA = Spot Price Average (no contract settlement) All information has been obtained in good faith from market sources but PCI Xylenes & Polyesters Ltd accepts no liability whatsoever for any commercial decisions based on this report.

THE WEEK AT A GLANCE WTI & Brent Crude: A lacklustre global economy, falling US dollar and talk of extra supplies dragged energy levels lower.

PX: The Oct ACP settlement at $1210 and absence of Chinese players in the first half of the week, due to the seven-day National Day holiday, did not prevent PX spot prices falling. Traders all but gave up hope that Chinese end-users would absorb the stray spot volumes, even as Chinese PTA utilisation rates are expected to rise this month. Tumbling crude oil and naphtha futures weighed heavily on the broader aromatics sector, and all it needed was a poor showing in the downstream segments of the polyester chain to drag PX towards $1110-1115 by the end of the week.

PTA: Affected by the sharp decline in energy and PX values, PTA buying slowed considerably even as the Chinese players returned to the market after the National Day break mid-week. Sentiment was extremely bad, as those traders with regular supplies dumped whatever they had at hand for the month, convinced that prices could tumble further. That sent Chinese domestic prices on a downspin towards RMB6000 and below. It was similar for imports; prices look set to test $800 and below soon, and local Chinese pricing slipped below RMB5900 by Fri.

MEG: The price collapse in the chain spared few, and MEG spot values took a hard beating as well. Imports dived towards $800 by Fri, an almost $100 tumble since the start of the holidays. Many buyers defaulting for deals concluded earlier contributed to the panic, both on the import and the Chinese domestic arena. Shorting by several international traders also became intense after Wed. Consequently, domestic prices broke below RMB6000, and e-trading for forward business saw few participants for most of the week. A weak recovery later afternoon Fri saw some buying especially for short covering, but still not enough to reverse the overall downtrend for the week.

Futures & forward: PTA futures at Zhengzhou led the way down, while MEG e-trading platforms saw few players as the number of sellers far outstripped buyers.

Polyester Raw Material Costs: Any hope of a rebound in polyester values were smashed this week, when crude-oil, PTA and MEG all dived south. With leading producers in China actually forced to lower their PTA and MEG tentative pricing for the month sharply from the original RMB7000 and RMB6900 respectively buying all but came to a stop mid-week for filament yarns, even as fabric transactions persisted. Feeling uncertainty rather than despair, polyester producers scrambled to lower the offers of their products to move sales. This effort paid off and by the end of the week sales against daily output picked up again towards 100% or just below for most. But that also meant some gain in product inventories, already on the rise after the week-long holidays the week earlier. Fortunately, polyester profits remained intact theoretically, as feedstock costs fell more sharply. But this massive decline spells ill for the biggest of polyester producers which depend on contract PTA and MEG, as it was a foregone conclusion that raw material costs for the month earlier were much higher than the prevailing levels, and unless prices of their products stage a strong recovery later the month, it could still mean a significant squeeze on profits. For this reason if nothing else, buying of feedstocks slowed to a trickle among these polyester makers, further hurting the already badly bruised sentiment.

SPOT PRICE: PX ; PTA ; MEG ; DEG

SPOT PRICE PROJECTIONS:

PX ; PTA ; MEG ; DEG

UPSTREAM PRICES:

Crude ; Naphtha ; Mixed Xylene ; Ethylene

CHINESE ECONOMIC CLIMATE: Poor industrial performance at home, sub-par global economy prove double whammy

DOWNSTREAM MARKET CONDITIONS:

Polyester Utilisation Rates: 68-75% ↔

Daily Sales/Output Ratio: 50-120%

Downstream Demand: STABLE to SOFT Product/Inventories: 9-22 days

Price Trends: Price Projections:

Margins: Collapse in feedstock pricing smashes all hopes of price gains, but margins still positive for now

PRODUCTION NEWS MEG: The MTO based plant by Fund Energy (formerly Ningbo Heyuan or Skyford) in eastern China expected down for 2 weeks Nov, instead of the originally planned dates Oct. In Saudi Arabia, the JUPC 2 line of SABIC is planned for a shutdown starting this month, to facilitate change in reactors. Sister facility YANPET 2 will undergo a catalyst change this month, with downtime about 45 days. Next week: PTA updates.

CHINA CHARTS

POLYESTER PRICES VS FEEDSTOCK COSTS

DAILY FABRIC TRANSACTIONS Million Metres

POLYESTER PROFITABILITY $/tonne equivalent

950

1000

1050

1100

1150

1200

1250

1300

1350

Jul Aug Sep Sep W3

Sep W4

Oct W1 Oct W2 Oct F Nov F Dec F

$/tonne

Feedstock Portion SD Polyester Chip PSF POY PET

0

2

4

6

8

10

12

14

16

18

21 J

ul

28 J

ul

04 A

ug

11 A

ug

18 A

ug

25 A

ug

01 S

ep

08 S

ep

15 S

ep

22 S

ep

29 S

ep

06 O

ct

Shaoxing (China Textile City) Wujiang Shaoxing + Wujiang

-150

-100

-50

0

50

100

150

200

250

300

Jul Aug Sep Sep W3 Sep W4 Oct W1 Oct W2

SD Polyester Chip PSF POY PET FDY DTY

![Untitled-2 [radekoncar.com.mk]radekoncar.com.mk/wp-content/uploads/2019/06/Elektricni-ormari-.pdf · PP2 polyester PW3 polyester PP3 polyester PW4 polyester PP4 polyester PW5 polyester](https://static.documents.pub/doc/80x56/5fc2e1f5b98d77452302c149/untitled-2-pp2-polyester-pw3-polyester-pp3-polyester-pw4-polyester-pp4-polyester.jpg)