Reforming the Italian budget process: streghening the allocation function and integrating the spending review 36th Annual meeting of the OECD Senior Budget Officials 11-12 June 2015 / Rome, Italy

Transcript

Reforming the Italian budget process: streghening the allocation function and integrating the spending review

36th Annual meeting of the OECD Senior Budget Officials

11-12 June 2015 / Rome, Italy

Revisions to the legislative and regulatory framework

In the last four decades Italian legislation concerning public finance and accountancy has been gradually strengthened:

• the reference text dated back to law n. 468/ 1978, later amended by three laws: n. 362/1988, n. 94/1997 and n.208/1999

• a major reform was made with law n. 196/2009 and part of the subsidiary legislation delegated to Government must still be enacted (artt. 40 and 42)

Public finance and accounting rules were next revised to adapt to the new EU framework and to new institutional arrangements between central and local governments, also through a constitutional amendment and the introduction of a balanced budget provision (constitutional law n. 1/2012 and its implementation in law n. 243/2012)

The State budget is no longer a ‘formal' law and it contributes actively to defining the overall allocation of resources, through the possibility to introduce new taxes and new expenditures with the budget law (previously forbidden by art. 81 of the Constitution).

A relevant part of expenditure still remains determined by parameters set by mandatory spending laws that can not be automatically modified through the revision of budget appropriations but require a modification of the underlying enabling law.

Since 2009, the budget bill may contain a reallocation of ear-marked expenditure without a modification of the original enabling law, provided that it results in a zero-sum variation. The Parliament is informed through a specific table.

Thanks to the constitutional amendment the budget has already taken up a new role….

… but the allocation function of the budget remains weak.

Although in recent years Italy has reinforced rules and national institutions governing fiscal conduct, the allocation function of the budget remains weak. This is due:

o in part to the institutional framework,

o in part to the financial programming process,

o in part to the representativeness of the budget,

o in part to the management process.

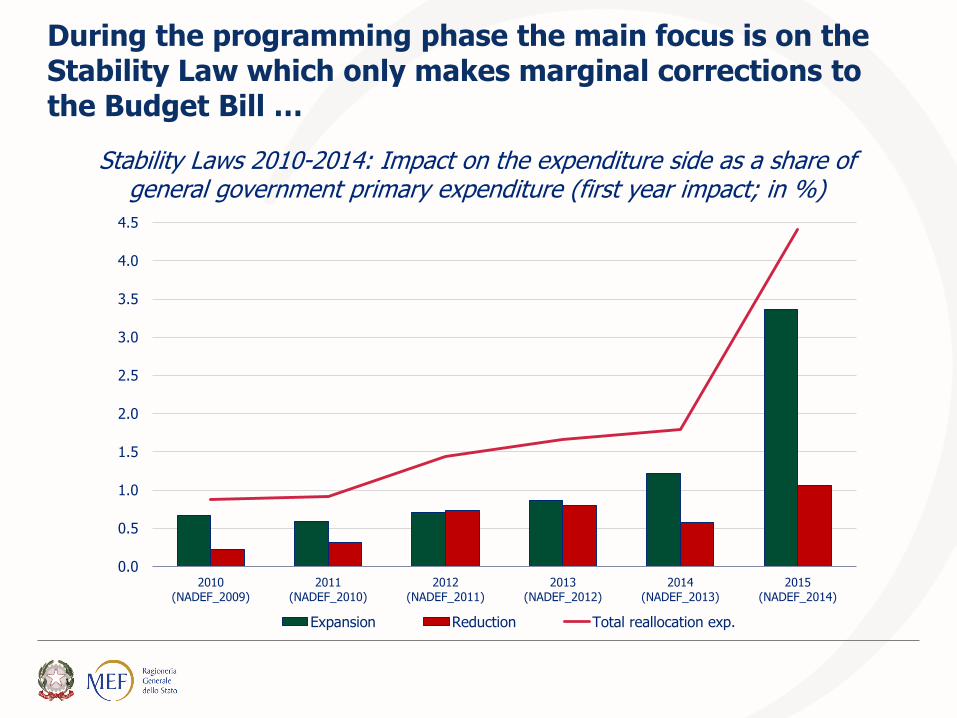

During the programming phase the main focus is on the Stability Law which only makes marginal corrections to the Budget Bill …

Stability Laws 2010-2014: Impact on the expenditure side as a share of general government primary expenditure (first year impact; in %)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2010(NADEF_2009)

2011(NADEF_2010)

2012(NADEF_2011)

2013(NADEF_2012)

2014(NADEF_2013)

2015(NADEF_2014)

Expansion Reduction Total reallocation exp.

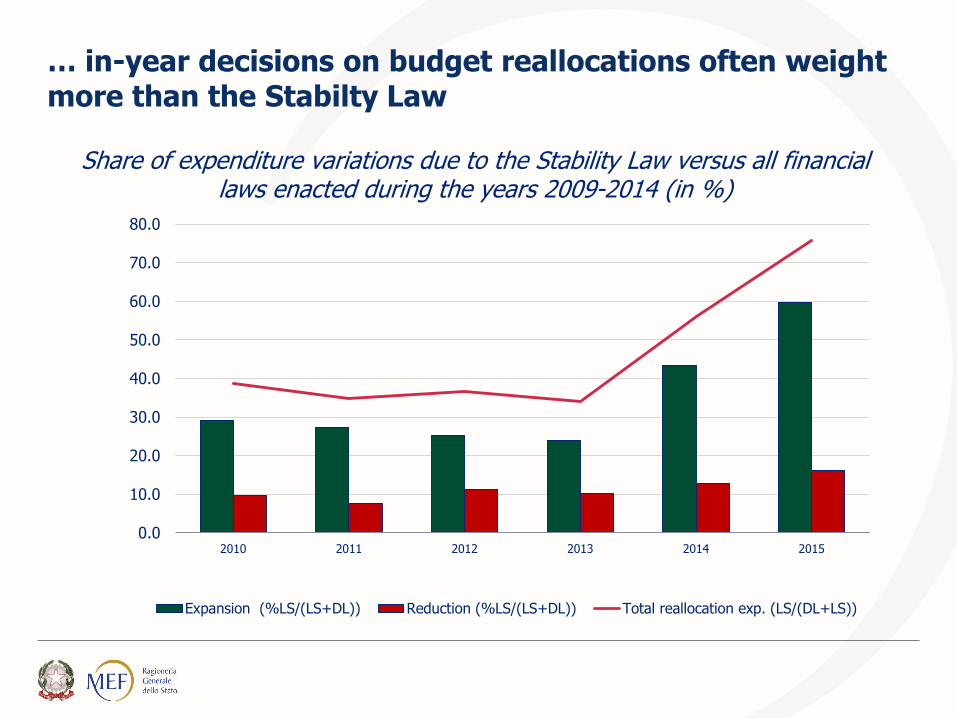

… in-year decisions on budget reallocations often weight more than the Stabilty Law

Share of expenditure variations due to the Stability Law versus all financial laws enacted during the years 2009-2014 (in %)

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

2010 2011 2012 2013 2014 2015

Expansion (%LS/(LS+DL)) Reduction (%LS/(LS+DL)) Total reallocation exp. (LS/(DL+LS))

Differences between initial appropriations and end-of-year reports are relevant …

Total in-year variation respect to initial appropriations (final-inital/initial, in %)

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

2009 2010 2011 2012 2013 2014

…. and there is a reallocation of resources between budget missions due to new expenditure laws as well as to several types of administrative variations

Share of reallocation between missions due to mid-year budget law, in-year new expendtiure laws, assignment of resources for arrears, ear-marked revenue, funds and other variations made by administrations (in %)

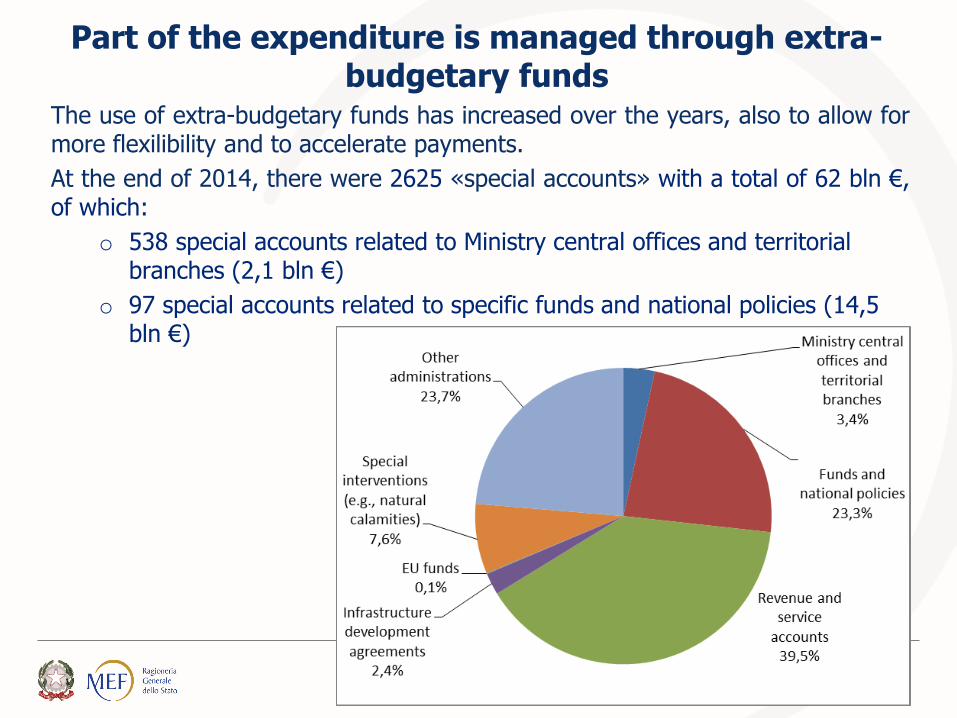

The use of extra-budgetary funds has increased over the years, also to allow for more flexilibility and to accelerate payments.

At the end of 2014, there were 2625 «special accounts» with a total of 62 bln €, of which:

o 538 special accounts related to Ministry central offices and territorial branches (2,1 bln €)

o 97 special accounts related to specific funds and national policies (14,5 bln €)

Part of the expenditure is managed through extra-budgetary funds

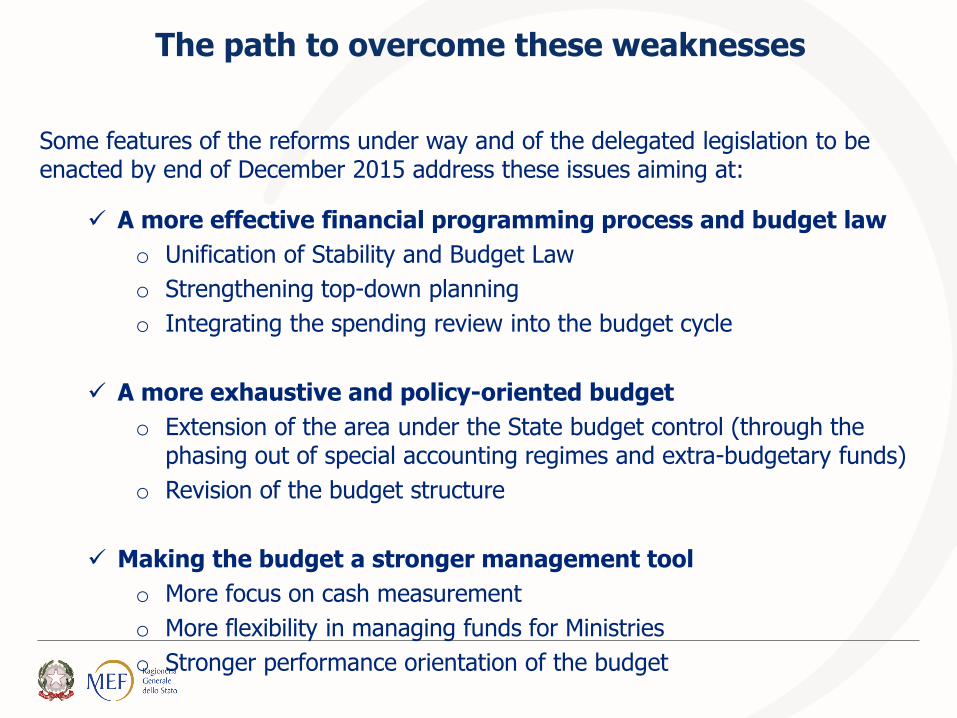

Some features of the reforms under way and of the delegated legislation to be enacted by end of December 2015 address these issues aiming at:

A more effective financial programming process and budget law

o Unification of Stability and Budget Law

o Strengthening top-down planning

o Integrating the spending review into the budget cycle

A more exhaustive and policy-oriented budget

o Extension of the area under the State budget control (through the phasing out of special accounting regimes and extra-budgetary funds)

o Revision of the budget structure

Making the budget a stronger management tool

o More focus on cash measurement

o More flexibility in managing funds for Ministries

o Stronger performance orientation of the budget

The path to overcome these weaknesses

Until the recent Constitutional reform, the “budget bill” was a reflection of the amount required to fund existing legislation, while the Government’s proposal of reallocation and innovations was made through the Stability Law:

o starting from 2017, the Budget law (total already foreseen amount) and Stability Law (marginal corrections) will be presented in a unified Budget Bill in order to focus the programming decisions on the overall amount of resources allocated to each function/policy

o instead of verifying that new current expenditure (or revenue reductions) introduced by the Stability law is compensated with the new resources made available through the Stability law, the new framework requires that the whole budget balance is in line with the medium-term objective (MTO)

.

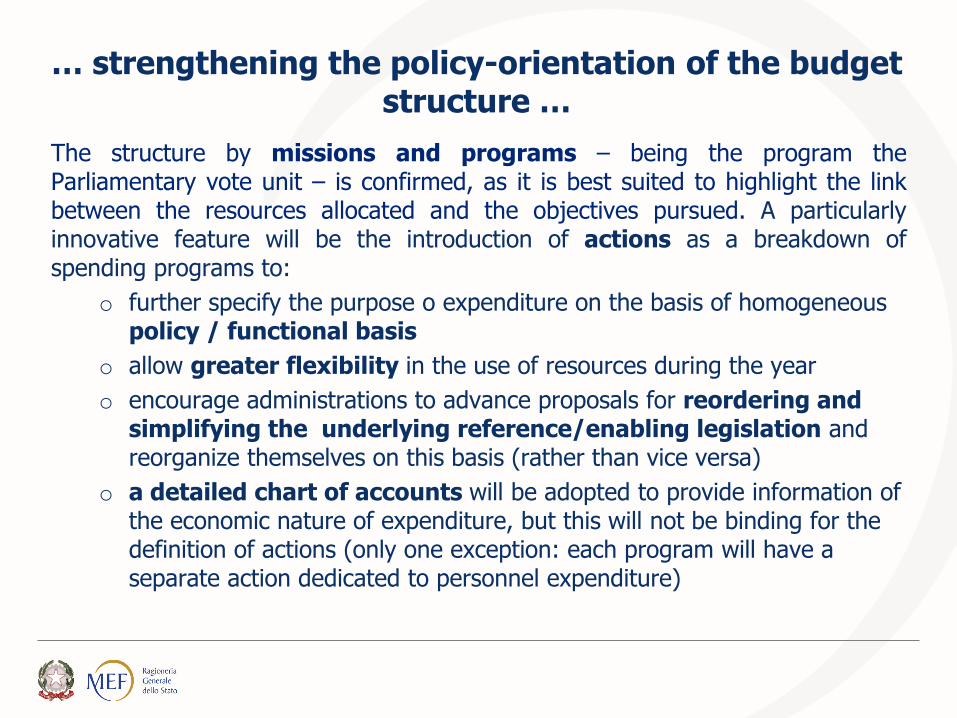

Towards a more effective budget law ….

The structure by missions and programs – being the program the Parliamentary vote unit – is confirmed, as it is best suited to highlight the link between the resources allocated and the objectives pursued. A particularly innovative feature will be the introduction of actions as a breakdown of spending programs to:

o further specify the purpose o expenditure on the basis of homogeneous policy / functional basis

o allow greater flexibility in the use of resources during the year

o encourage administrations to advance proposals for reordering and simplifying the underlying reference/enabling legislation and reorganize themselves on this basis (rather than vice versa)

o a detailed chart of accounts will be adopted to provide information of the economic nature of expenditure, but this will not be binding for the definition of actions (only one exception: each program will have a separate action dedicated to personnel expenditure)

… strengthening the policy-orientation of the budget structure …

A better integration of the budget accounting data and those of the Treasury and the progressive elimination of special Treasury accounts and extra-budgetary funds (constituted thanks to resources originally in the budget) is foreseen in the next few years:

o gradual transition through the digitalization of the payment procedures and the integration of ordinary extra-budgetary accounts into the budget accounting system

o suppression of special accounts and regimes and reacquisition of their stocks to the State budget and, when this not possible, IT development of the management of the remain special accounts

o adoption of harmonized classification scheme for the annual reporting of the remaining off-balance sheet operations excluded from this rationalization process

o enhancement of the IT management system (SICOGE) with the electronic invoice, payment plan and more consistency with monthly requirement forecasts

… as well as the integration between budget and Treasury accounts

The spending review should be part of the budget process

There have been several spending review (SR) initiatives in Italy, all on an ad hoc basis. When measures were devised with the direct involvement of line Ministries, they were more effective. Moreover, integration of the SR in the budget cycle can be used to promote the reallocation of resources.

The reform aims at introducing some typical features of top-down programming and giving Ministries three-year spending targets in terms of:

o reductions to be met, entailing a selective choice on how to contribute the general fiscal targets

o increases to be made, on the basis of new spending initiatives that the Government is committed to achieve (priorities).

These targets will be monitored during the year under specific “agreements” by MoF in collaboration with each line Ministry from both a financial and results-based approach.

Further spending initiatives should in most cases be funded by Ministries on the basis of their own reallocation proposals, avoiding general requests to the Government to increase total funding.

February/ March

April / May

June / August

September (NADEF)

October/ January

Result of monitoring of the last three-year agreements for each administration Report of deviations to Council of Ministers

DEF (10 April) with macroeconomic framework and general govnt expenditure rule (UE benchmark) Decree of the PM setting government priorities and three year spending targets for each Ministry Budget preparation Circular

Definition of the Ministries proposals on how to meet the spending targets through: • Efficiency

increases through administrative actions

• Legislative

proposals

MoF coordination of the proposals and check of macroeconomic framework

the budget bill (integrated with Stability law) contains the legislative proposals following the approval of the Budget Law, the signature of three-year agreements (by January 30)

Monitoring of three-year agreements

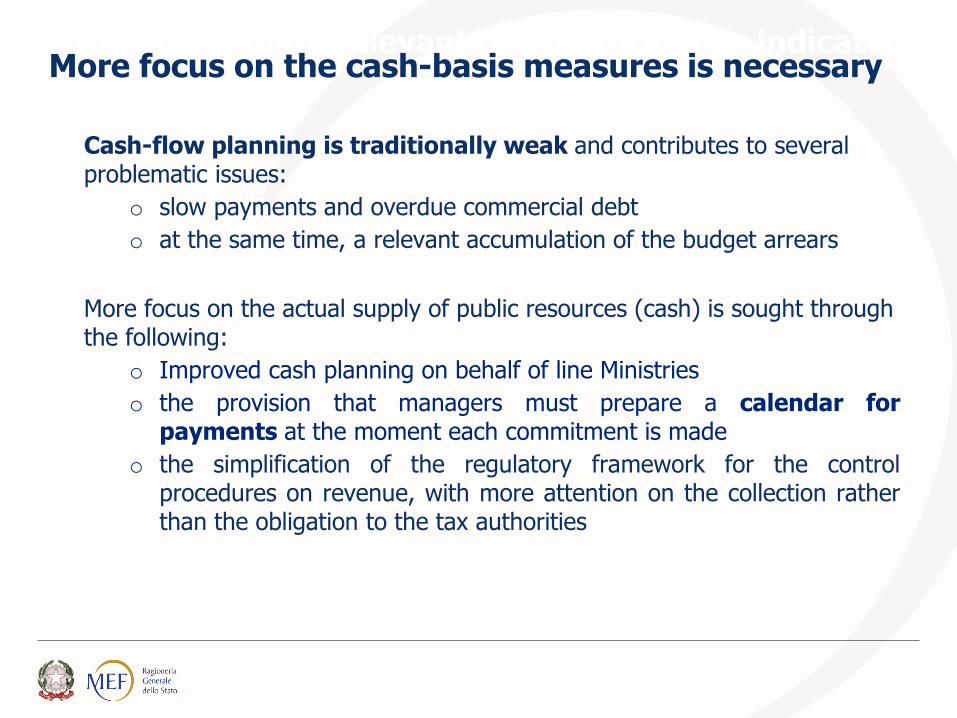

Cash-flow planning is traditionally weak and contributes to several problematic issues:

o slow payments and overdue commercial debt

o at the same time, a relevant accumulation of the budget arrears

More focus on the actual supply of public resources (cash) is sought through the following:

o Improved cash planning on behalf of line Ministries

o the provision that managers must prepare a calendar for payments at the moment each commitment is made

o the simplification of the regulatory framework for the control procedures on revenue, with more attention on the collection rather than the obligation to the tax authorities

Towards a more relevant use performance indicators More focus on the cash-basis measures is necessary

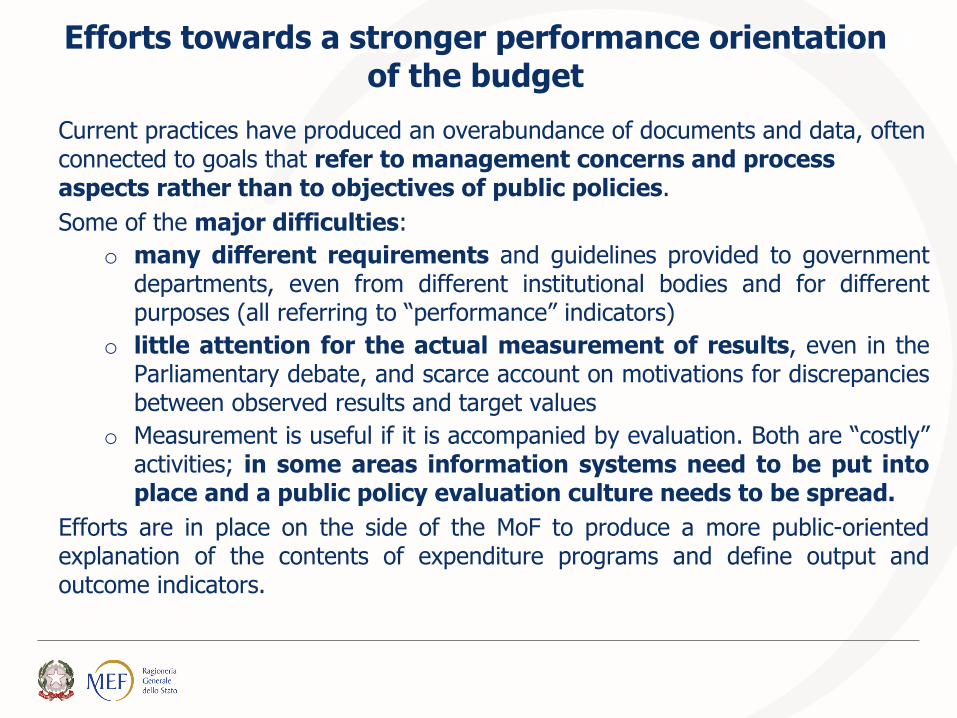

Current practices have produced an overabundance of documents and data, often connected to goals that refer to management concerns and process aspects rather than to objectives of public policies.

Some of the major difficulties:

o many different requirements and guidelines provided to government departments, even from different institutional bodies and for different purposes (all referring to “performance” indicators)

o little attention for the actual measurement of results, even in the Parliamentary debate, and scarce account on motivations for discrepancies between observed results and target values

o Measurement is useful if it is accompanied by evaluation. Both are “costly” activities; in some areas information systems need to be put into place and a public policy evaluation culture needs to be spread.

Efforts are in place on the side of the MoF to produce a more public-oriented explanation of the contents of expenditure programs and define output and outcome indicators.

Towards a more relevant use performance indicators Efforts towards a stronger performance orientation of the budget