37

©2013 Software AG. All rights reserved. Roadshow Investor Relations November 2013

©2013 Software AG. All rights reserved.

Roadshow

Investor Relations

November 2013

©2013 Software AG. All rights reserved.

2 |

This presentation contains forward-looking statements based on beliefs

of Software AG management. Such statements reflect current views of

Software AG with respect to future events and results and are subject

to risks and uncertainties. Actual results may vary materially from

those projected here, due to factors including changes in general

economic and business conditions, changes in currency exchange, the

introduction of competing products, lack of market acceptance of new

products, services or technologies and changes in business strategy.

Software AG does not intend or assume any obligation to update these

forward-looking statements.

Safe-Harbor-Statement

©2013 Software AG. All rights reserved.

3 |

Software AG - At a Glance

High performance database

Process Planning,

monitoring and analysis

Middleware to integrate data applications and

digital workflows

Big-data and In-memory technology

~ € 1bn revenue (FY 2012)

~ € 700m revenue (9m 2013)

~ 25% operating EBIT margin (9m 2013)

~ 15% free cash flow margin (9m 2013)

> 5,000 Employees worldwide

~ 1,000 R&D

> € 2bn market cap

66% free float

29% Software AG Foundation

70 Countries

Global customer base: 80% of Fortune 10,000

Technology leader in system integration,

process automation and data management

©2013 Software AG. All rights reserved.

4 |

I n te l l i gent Bus ines s Opera t ions

SOFTWARE AG - Portfolio

©2013 Software AG. All rights reserved.

5 |

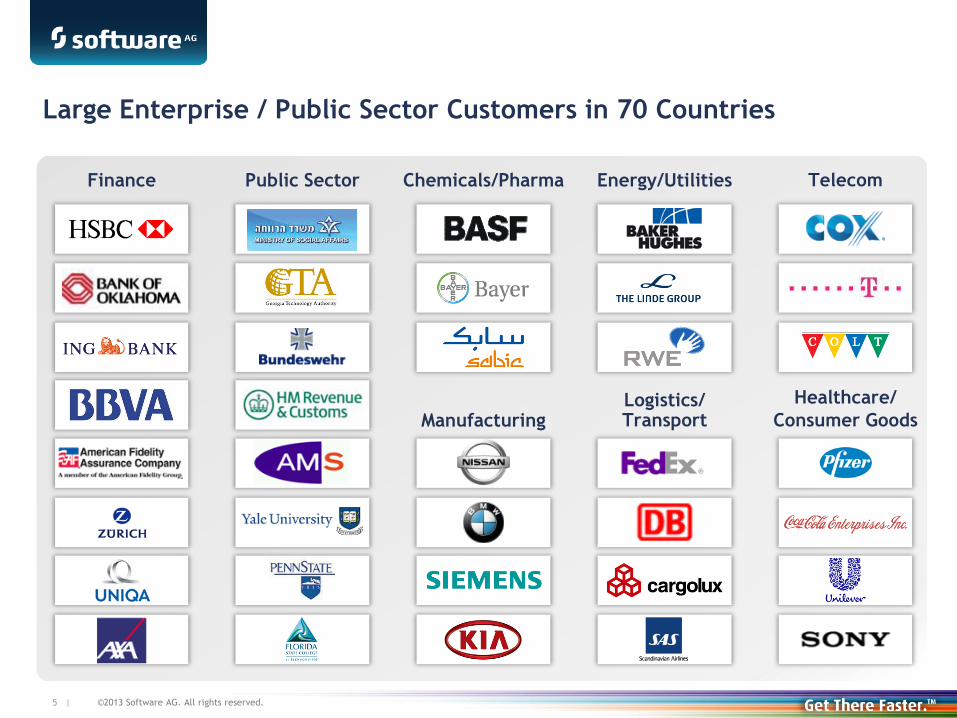

Large Enterprise / Public Sector Customers in 70 Countries

Finance Public Sector Telecom Chemicals/Pharma Energy/Utilities

Manufacturing Logistics/ Transport

Healthcare/

Consumer Goods

©2013 Software AG. All rights reserved.

6 |

Financial Sector

Public Sector

IT

Associ-ations

Services

Manu-facturing

Telcos

Logistics Retail

Other

*Based on product revenue FY 2012

Revenue Split – Well Balanced

20%

20%

EMEA

44%

Asia Pacific

8% Americas

48%

GER 15%

PIIGS < 4%

Product Revenue by Region* Product Revenue by Industry*

©2013 Software AG. All rights reserved.

7 |

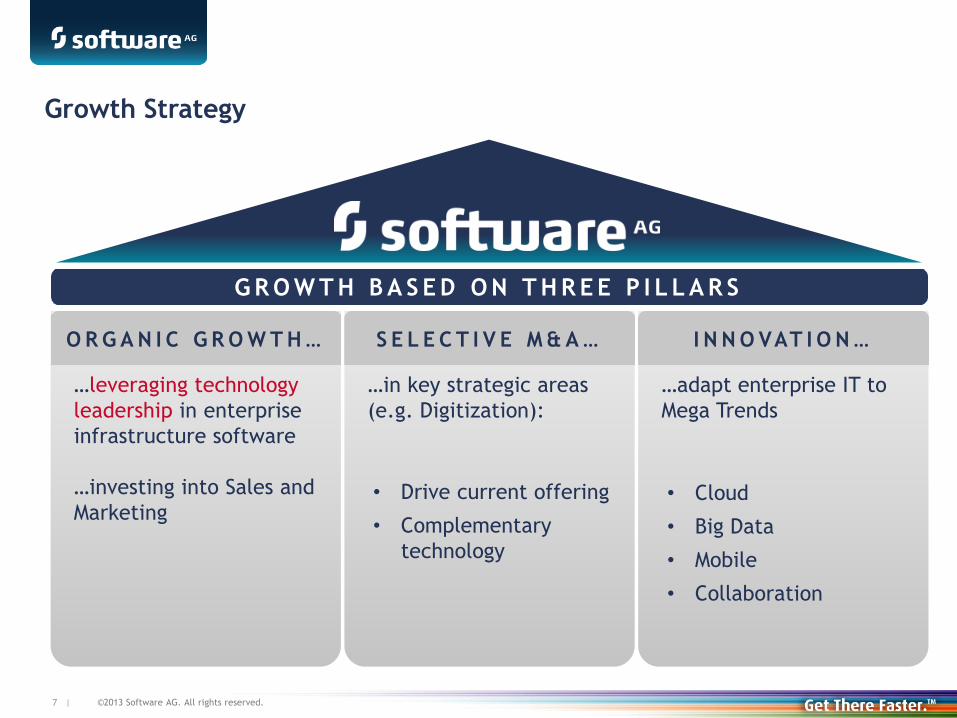

Growth Strategy

G R O W T H B A S E D O N T H R E E P I L L A R S

…leveraging technology

leadership in enterprise

infrastructure software

…investing into Sales and

Marketing

O R G A N I C G R O W T H …

…in key strategic areas

(e.g. Digitization):

S E L E C T I V E M & A …

…adapt enterprise IT to

Mega Trends

I N N O VAT I O N …

• Drive current offering

• Complementary

technology

• Cloud

• Big Data

• Mobile

• Collaboration

©2013 Software AG. All rights reserved.

8 |

Technology Leadership

Gartner’s Magic Quadrant for Application Integration Suites

“Leaders in infrastructure that supports systematic

application integration provide a comprehensive

ESB suite offering as well as the ability to

integrate that offering with other relevant

technologies (including community management,

data integration, SOA and integration governance,

and BPM). This is combined with a strong

commitment to this market, which is expressed

through focused value propositions and go-to-

market strategies (for example, by packaging

platforms and/or by providing integrated product

and service offerings specific for this market).”

Source: Gartner, Inc., Magic Quadrant for On-Premises Application Integration Suites, Jess Thompson, et

al., June 27, 2013

This graphic was published by Gartner, Inc. as part of a larger research document and should be evaluated

in the context of the entire document. The Gartner document is available upon request from Software AG.

Gartner does not endorse any vendor, product or service depicted in its research publications, and does

not advise technology users to select only those vendors with the highest ratings. Gartner research

publications consist of the opinions of Gartner's research organization and should not be construed as

statements of fact. Gartner disclaims all warranties, expressed or implied, with respect to this research,

including any warranties of merchantability or fitness for a particular purpose.

©2013 Software AG. All rights reserved.

9 |

Technology Leadership

Application Integration Suites • • • • • Business Process Analysis Tools • • • Business Process Management Suites • • • Enterprise Architecture Tools • • Governance, Risk and Compliance • • • Integrated IT Portfolio Analysis Apps • Application Services Governance • • Complex Event Processing Platforms • • • Comprehensive Integration Solutions • • • • • EA Management Suites • Elastic Caching Platforms • • • ESB • • • • Integrated SOA Governance • • SOA Service Life-cycle Management •

©2013 Software AG. All rights reserved.

10 |

Acquisitions Support Technology Leadership and Innovation

©2013 Software AG. All rights reserved.

11 |

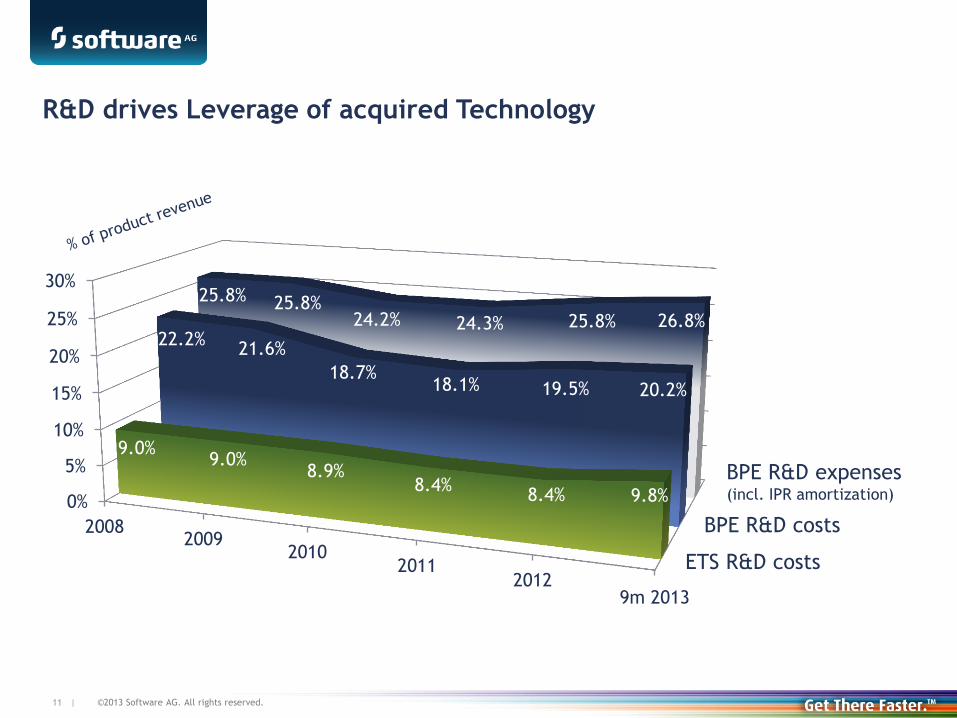

R&D drives Leverage of acquired Technology

BPE R&D expenses (incl. IPR amortization)

BPE R&D costs

ETS R&D costs

0%

5%

10%

15%

20%

25%

30%

20082009

20102011

20129m 2013

9.0% 9.0%

8.9% 8.4%

8.4% 9.8%

22.2% 21.6%

18.7% 18.1% 19.5% 20.2%

25.8% 25.8% 24.2% 24.3% 25.8% 26.8%

©2013 Software AG. All rights reserved.

12 |

Innovation - Big Data

Cloud Events

and SaaS

App Events

Mobile &

Location

Events

Hadoop & Data

Warehouse

Financial

and Trading

Events

$ £ € ¥

Social Media

Events

Low Latency

Universal Messaging

In Memory Data &

Analytics

Real-time Analytics

& Intelligent Action

Real-time Visual

Analytics

System Alerts,

Sensors & Machine

Events

©2013 Software AG. All rights reserved.

13 |

Multi-payments Data

Interoperability

Continuously

Optimize

Operations

Do More With Less

Continuously

Manage Risk

Profit in an Environment

of Changing Regulation

Continuous

Visibility

Better, Faster Decisions

Fix Problems Early

Capitalize on Real-

time Revenue

Opportunities

Outperform Your

Competitors

Real Time Business Intelligence

©2013 Software AG. All rights reserved.

14 |

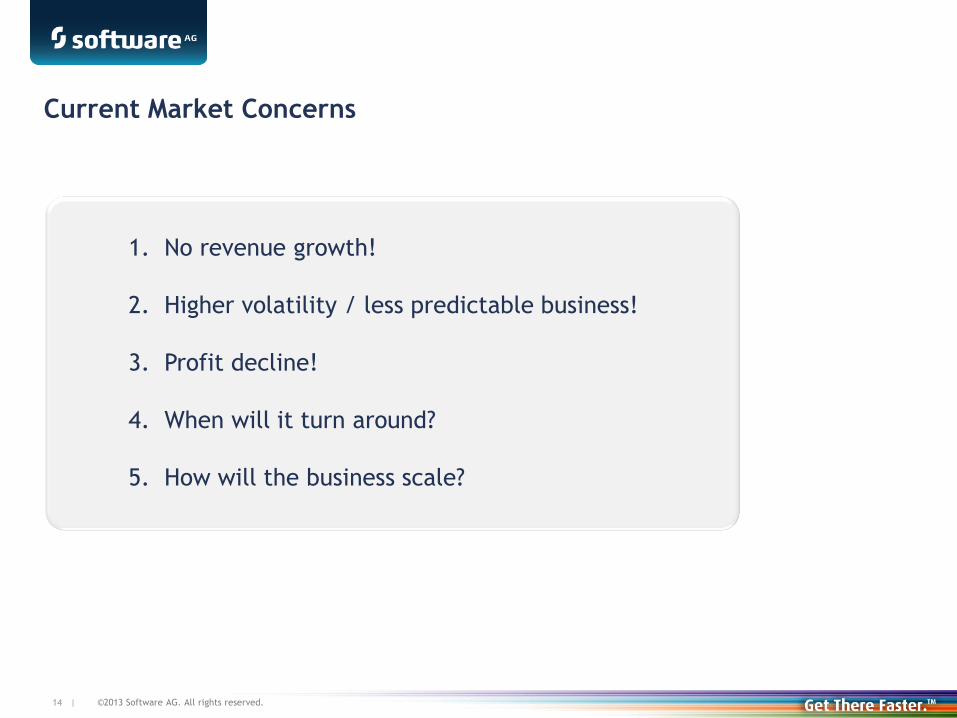

Current Market Concerns

1. No revenue growth!

2. Higher volatility / less predictable business!

3. Profit decline!

4. When will it turn around?

5. How will the business scale?

©2013 Software AG. All rights reserved.

15 |

Revenue Drivers in Transition –

BPE outnumbers ETS / Consulting is in Consolidation

0

100

200

300

400

500

600

700

800

2008 2010 2012 2013e*

(€m)

BPE

Consulting

ETS

39% 46%

54% 60%

539

423

712

335

182

697

* Analyst consensus; own poll

©2013 Software AG. All rights reserved.

16 |

0

20

40

60

80

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23

New Customers and Bigger Deals grow License Revenue

(€m)

(€m)

In the quarter: volatile

Four quarter rolling: steady growth

40

80

120

160

200

240

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23

2008 2009 2010 2013 2011 2012

2008 2009 2010 2013 2011 2012

©2013 Software AG. All rights reserved.

17 |

Cost Ratios & Profitability – 9m 2013/2012 (€m)

Total

Revenue

Gross

Profit R&D

Sales & Marketing

9m 2013

9m 2012

479.3

-78.5 -219.3

770.6

701.2

481.1

-74.8

-54.2

11%* 31%*

10%* 24%*

*as % of total revenue

68%*

172.9

135.1

62%*

-181.3

+2.1

-52.5 +6.1

Admin Other

7%*

7%*

38 38

EBIT

(IFRS)

©2013 Software AG. All rights reserved.

18 |

Strengthen Software AG’s Sales Organization - Worldwide

BPE S&M costs

ETS S&M costs

0%

10%

20%

30%

40%

50%

60%

20082009

20102011

20129m 2013

23.0% 21.6%

20.7% 21.3% 20.9% 22.6%

44.9% 42.2%

39.2% 37.1% 39.1%

48.8%

+ 2 0 0 S & M i n

B P E d i v i s i o n

©2013 Software AG. All rights reserved.

19 |

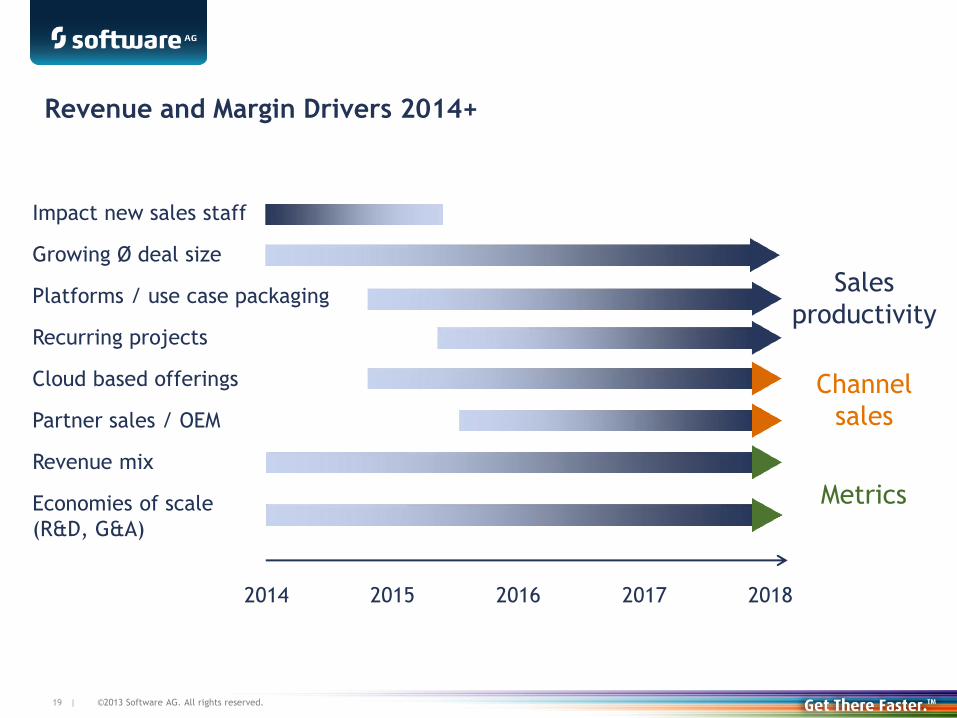

Revenue and Margin Drivers 2014+

2014 2015 2016 2017 2018

Impact new sales staff

Growing Ø deal size

Platforms / use case packaging

Recurring projects

Cloud based offerings

Partner sales / OEM

Revenue mix

Economies of scale

(R&D, G&A)

Metrics

Channel

sales

Sales

productivity

©2013 Software AG. All rights reserved.

20 |

Enterprise Transaction Systems

ETS

• Manage structural

decline (high single

digit % p.a.)

• Manage cost to

maintain segment

result margin > 60%

Business Process Excellence

• Product revenue: growth ca. 15-20% p.a.

(incl. a 50-100% growth from Big Data)

• > 50% contribution to group result

• Expand Big Data offering by Intelligent

Business Operations platform

BPE

• Transform technology

leadership into

market leadership

• Strategic acquisitions

(cash-only; Cloud/

Big Data)

• Develop 3rd product

line

• Increase revenue with

new products (non

ETS) to € 1bn

• Grow EPS in a range

of 10-20% p.a.

Software AG Group

S H A R E O F P R O D U C T R E V E N U E *

Business Targets 2018 (2018, base: 2012)

* According to mid-term business goals

BPE

IT PORTFOLIO

MANAGEMENT

REAL-TIME INTELLIGENCE AND BIG DATA

PROCESS AUTOMATION

AND INTEGRATION

COLLABORATIVE

PROCESS ANALYSIS

DATABASE MANAGEMENT &

APPLICATION MODERNIZATION

©2013 Software AG. All rights reserved.

21 |

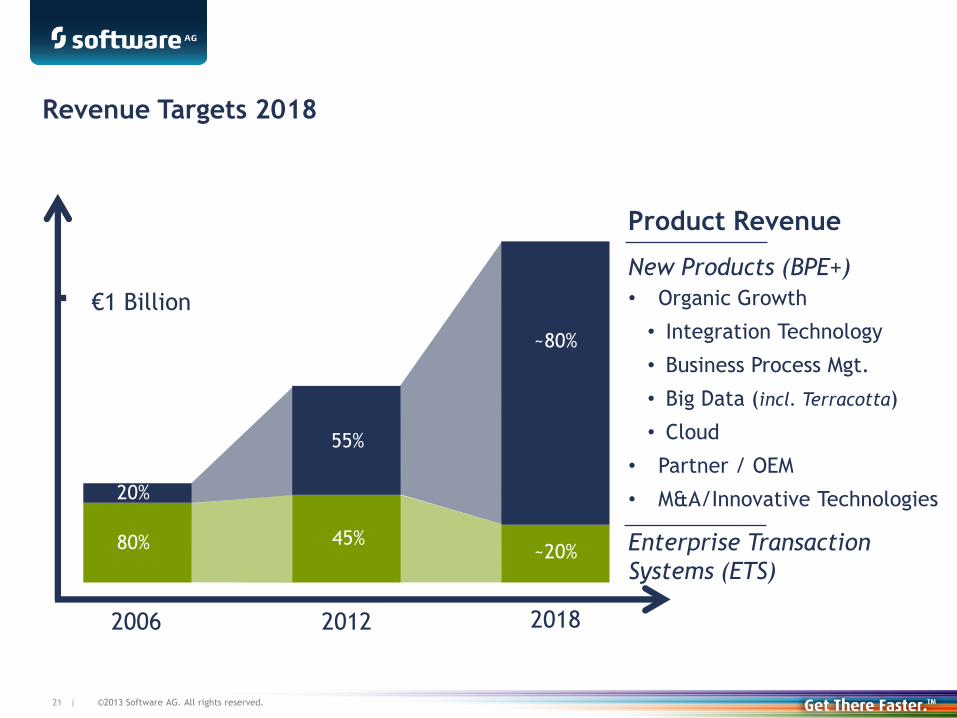

~80%

Enterprise Transaction

Systems (ETS)

New Products (BPE+)

• Organic Growth

• Integration Technology

• Business Process Mgt.

• Big Data (incl. Terracotta)

• Cloud

• Partner / OEM

• M&A/Innovative Technologies

2012 2018

45%

€1 Billion

20%

80%

2006

55%

~20%

Revenue Targets 2018

Product Revenue

©2013 Software AG. All rights reserved.

22 |

Solid Business Foundation

1. Footprint: Established global software player with blue chip customer base

2. Financials: Strong balance sheet and cash generation

3. Assets: Experienced management team and loyal expert staff

4. USP: Unique technology leadership in IT mega-trends / growth segments

5. Timing: Almost past ramp-up investments for future growth /

margin leverage ahead

©2013 Software AG. All rights reserved.

24 |

Euro 37%

US Dollar 26%

Other 9%

ILS 5%

AUD 5%

ZAR 3%

GBP 5%

CAD 3%

BRL 7%

(in €m; yoy)

Q3

2013

Q3

in %

YTD

2013

YTD

in %

Licenses -4.5 -5% -9.3 -4%

Maintenance -6.3 -6% -11.3 -4%

Consulting &

Other -1.7 -3% -3.2 -2%

Total -12.5 -5% -23.8 -3%

Currency impact on revenue

Currency impact on revenue

Q3 2013 / YTD 2013 (9 months)

37% revenue in Euro

63% revenue in foreign currency

Currency split YTD 2013

©2013 Software AG. All rights reserved.

25 |

Revenue Q3 2013 / YTD 2013 (9 month)

(in €m) Q3

2013

Q3 2012

Δ%

Δ%

acc

YTD

2013

YTD 2012

Δ%

Δ%

acc

Product 175.1 178.3 -2% 4% 501.3 515.3 -3% 1%

Licenses 79.9 80.5 -1% 5% 219.3 221.8 -1% 3%

Maintenance 95.2 97.8 -3% 4% 282.0 293.5 -4% -

Consulting & services 63.2 78.2 -19% -17% 199.0 253.7 -22% -20%

Other 0.2 0.9 - - 0.9 1.6 - -

Total 238.5 257.4 -7% -2% 701.2 770.6 -9% -6%

©2013 Software AG. All rights reserved.

26 |

(in €m) Q3

2013

Q3

2012

Δ% Δ% acc

YTD

2013

YTD

2012

Δ% Δ% acc

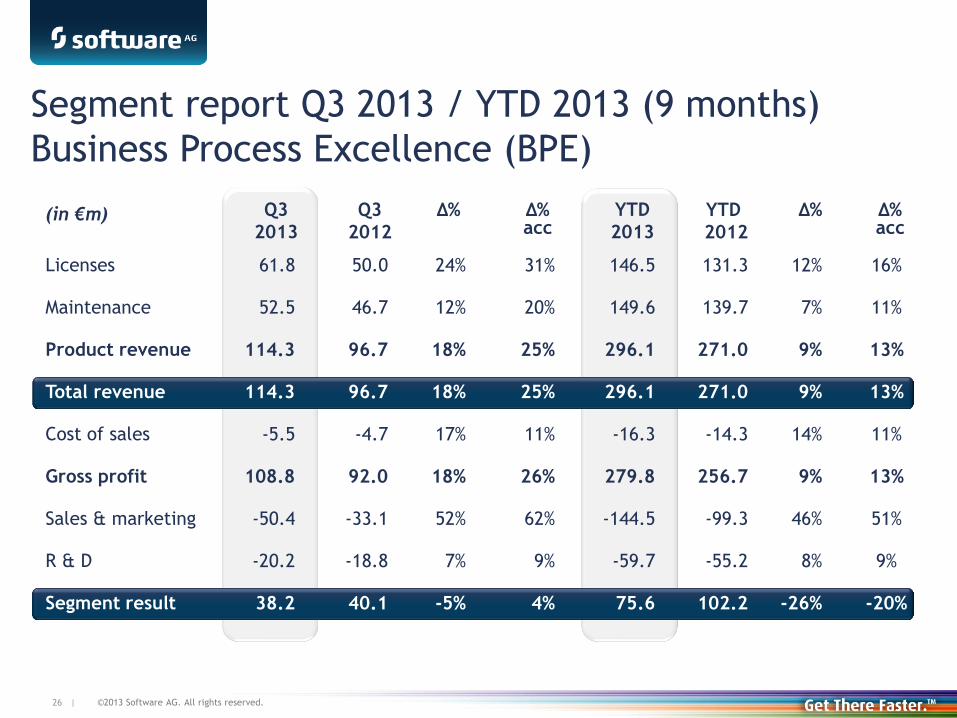

Licenses 61.8 50.0 24% 31% 146.5 131.3 12% 16%

Maintenance 52.5 46.7 12% 20% 149.6 139.7 7% 11%

Product revenue 114.3 96.7 18% 25% 296.1 271.0 9% 13%

Total revenue 114.3 96.7 18% 25% 296.1 271.0 9% 13%

Cost of sales -5.5 -4.7 17% 11% -16.3 -14.3 14% 11%

Gross profit 108.8 92.0 18% 26% 279.8 256.7 9% 13%

Sales & marketing -50.4 -33.1 52% 62% -144.5 -99.3 46% 51%

R & D -20.2 -18.8 7% 9% -59.7 -55.2 8% 9%

Segment result 38.2 40.1 -5% 4% 75.6 102.2 -26% -20%

Segment report Q3 2013 / YTD 2013 (9 months)

Business Process Excellence (BPE)

©2013 Software AG. All rights reserved.

27 |

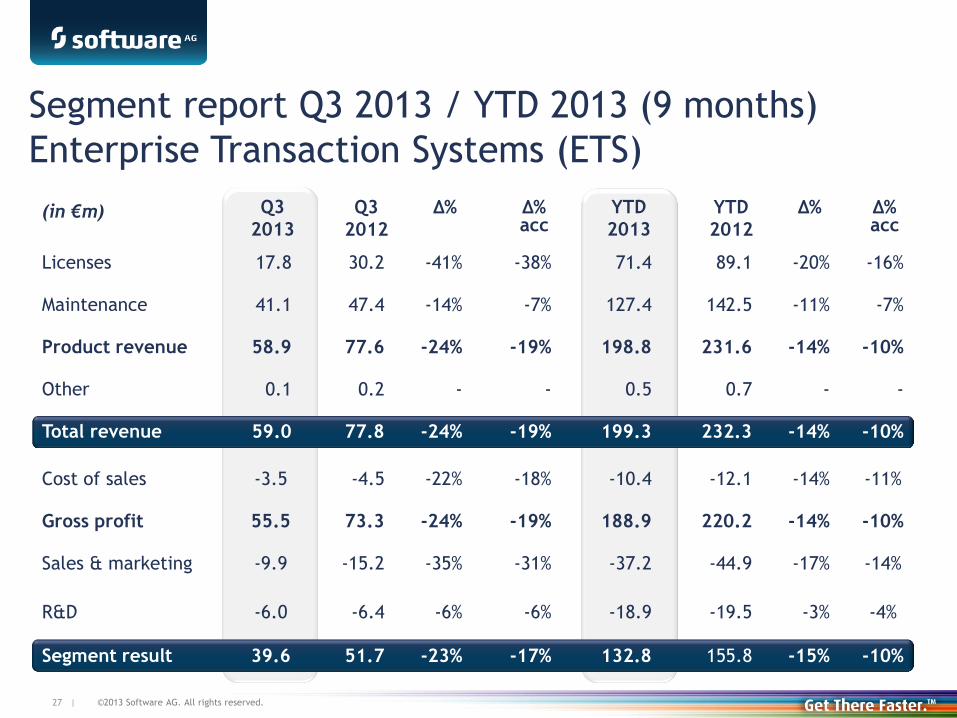

(in €m) Q3

2013

Q3

2012

Δ% Δ% acc

YTD

2013

YTD

2012

Δ% Δ% acc

Licenses 17.8 30.2 -41% -38% 71.4 89.1 -20% -16%

Maintenance 41.1 47.4 -14% -7% 127.4 142.5 -11% -7%

Product revenue 58.9 77.6 -24% -19% 198.8 231.6 -14% -10%

Other 0.1 0.2 - - 0.5 0.7 - -

Total revenue 59.0 77.8 -24% -19% 199.3 232.3 -14% -10%

Cost of sales -3.5 -4.5 -22% -18% -10.4 -12.1 -14% -11%

Gross profit 55.5 73.3 -24% -19% 188.9 220.2 -14% -10%

Sales & marketing -9.9 -15.2 -35% -31% -37.2 -44.9 -17% -14%

R&D -6.0 -6.4 -6% -6% -18.9 -19.5 -3% -4%

Segment result 39.6 51.7 -23% -17% 132.8 155.8 -15% -10%

Segment report Q3 2013 / YTD 2013 (9 months)

Enterprise Transaction Systems (ETS)

©2013 Software AG. All rights reserved.

28 |

(in Mio. €) Q3

2013

Q3

2012

Δ% Δ% acc

YTD

2013

YTD

2012

Δ% Δ% acc

Licenses 0.3 0.3 - - 1.3 1.5 -13% -7%

Maintenance 1.6 3.7 -57% -57% 5.1 11.2 -54% -55%

Product revenue 1.9 4.0 -53% -52% 6.4 12.7 -50% -49%

Services & other 63.3 79.0 -20% -18% 199.3 254.6 -22% -20%

Total revenue 65.2 83.0 -21% -19% 205.7 267.3 -23% -22%

Cost of sales -56.1 -74.9 -25% -24% -175.4 -245.2 -28% -27%

Gross profit 9.1 8.1 12% 19% 30.3 22.1 37% 41%

Sales & marketing -8.1 -8.6 -6% 1% -26.3 -26.7 -1% 3%

Segment result 1.0 -0.5 - - 4.0 -4.6 - -

Segment report Q3 2013 / YTD 2013 (9 months)

Consulting

©2013 Software AG. All rights reserved.

29 |

44

Results Q3 2013 / YTD 2013 (9 months)

(in €m) Q3

2013

Q3

2012

Δ% Δ% acc

YTD

2013

YTD

2012

Δ% Δ% acc

Total revenue 238.5 257.4 -7% -2% 701.2 770.6 -9% -6%

Cost of sales -72.6 -90.2 -20% -18% -221.9 -289.5 -23% -23%

Gross profit 165.9 167.2 -1% 6% 479.3 481.1 - 4%

Margin in % 69.6% 65.0% 68.4% 62.4%

R & D -26.1 -25.2 4% 6% -78.5 -74.8 5% 6%

Sales & marketing -72.5 -60.4 20% 27% -219.3 -181.3 21% 25%

Administration -17.3 -20.0 -14% -11% -52.5 -54.2 -3% -1%

Other

income/expense -0.9 -0.5 - - 6.1 2.1 - -

EBIT 49.1 61.1 -20% -10% 135.1 172.9 -22% -15%

Margin in % 20.6% 23.7% 22.0% 19.3% 22.4% 20.3%

©2013 Software AG. All rights reserved.

30 |

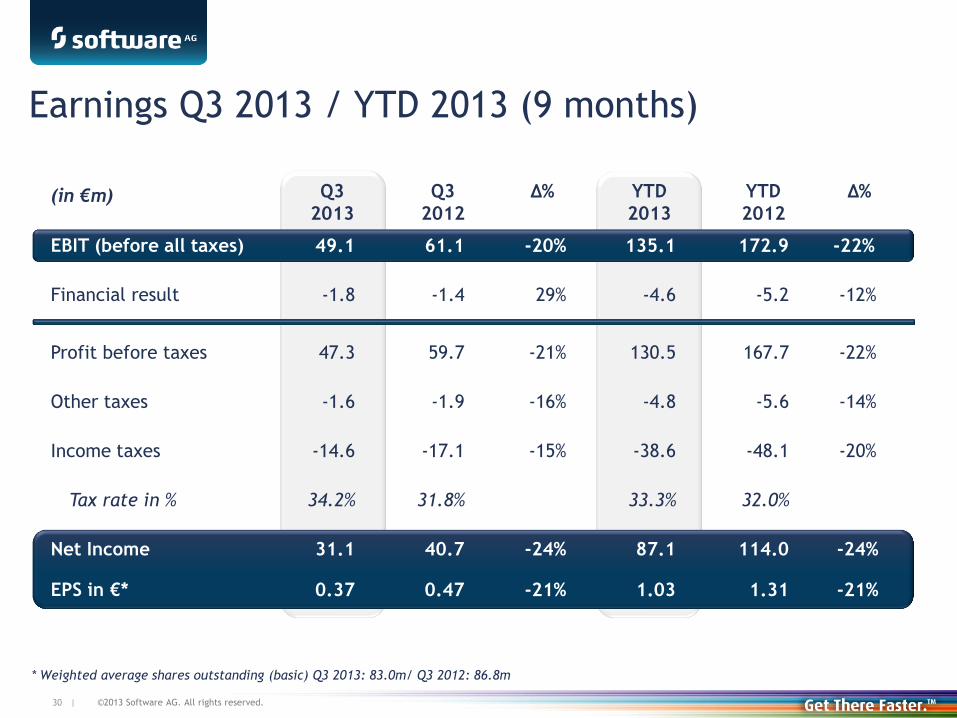

Earnings Q3 2013 / YTD 2013 (9 months)

(in €m) Q3

2013

Q3

2012

Δ% YTD

2013

YTD

2012

Δ%

EBIT (before all taxes) 49.1 61.1 -20% 135.1 172.9 -22%

Financial result -1.8 -1.4 29% -4.6 -5.2 -12%

Profit before taxes 47.3 59.7 -21% 130.5 167.7 -22%

Other taxes -1.6 -1.9 -16% -4.8 -5.6 -14%

Income taxes -14.6 -17.1 -15% -38.6 -48.1 -20%

Tax rate in % 34.2% 31.8% 33.3% 32.0%

Net Income 31.1 40.7 -24% 87.1 114.0 -24%

EPS in €* 0.37 0.47 -21% 1.03 1.31 -21%

* Weighted average shares outstanding (basic) Q3 2013: 83.0m/ Q3 2012: 86.8m

©2013 Software AG. All rights reserved.

31 |

Non-IFRS Earnings Q3 2013 / YTD 2013 (9 months)

* Based on average outstanding shares: Q3 2013: 83.0m / Q3 2012: 86.8m // 9m 2013: 84.2m / 9m 2012: 86.8m

(in €m) Q3

2013

Q3

2012

YTD

2013

YTD

2012

EBIT (before all taxes) 49.1 61.1 135.1 172.9

Share based payment 0.5 2.2 -0.8 4.2

Amortization on acquisition related

intangible assets 11.5 9.7 31.0 28.4

Reduction product revenue

by purchase price allocation 0.9 - 0.9 1.0

Other acquisition impacts 0.3 0.1 1.6 0.6

Restructuring/severances 4.0 0.7 9.2 2.5

EBIT (Non-IFRS) 66.3 73.8 177.0 209.6

in % of revenue (Non-IFRS) 27.7% 28.7% 25.2% 27.2%

Net income (Non-IFRS) 43.0 49.6 114.4 139.7

EPS (Non-IFRS)* 0.52 0.57 1.36 1.61

©2013 Software AG. All rights reserved.

32 |

Cash flow Q3 2013 / YTD 2013 (9 months)

(in €m) Q3

2013

Q3

2012

Δ% YTD

2013

YTD

2012

Δ%

Operating cash flow 36.6 28.7 28% 115.4 133.5 -14%

./. CapEx* -3.3 -4.1 -9.8 -8.0

Free cash flow 33.3 24.6 35% 105.6 125.5 -16%

as % of revenue 14% 9.6% 15.1% 16.3%

Free cash flow per share** 0.40 0.28 43% 1.25 1.45 -14%

* Cash flow from investing activities except acquisitions and except investments in debt instruments

** Based on average outstanding shares: Q3 2013: 83.0m / Q3 2012: 86.8m // 9m 2013: 84.2m / 9m 2012: 86.8m

©2013 Software AG. All rights reserved.

33 |

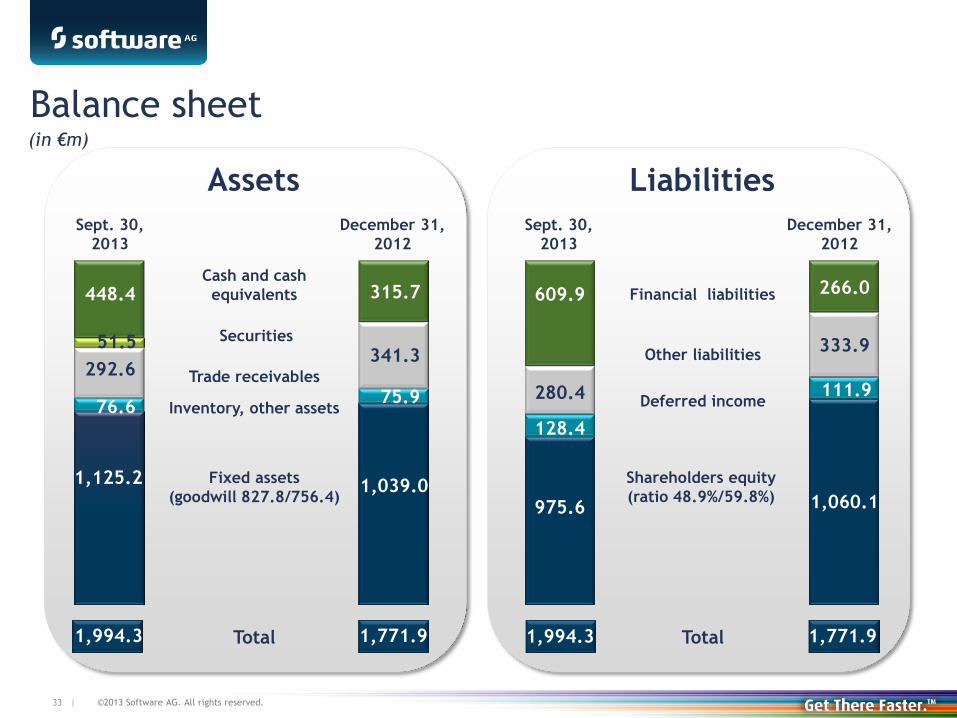

Sept. 30,

2013

Sept. 30,

2013

1,994.3 1,994.3

448.4

292.6

76.6

1,125.2

609.9

280.4

128.4

975.6

1,771.9

315.7

341.3

75.9

1,039.0

1,771.9

266.0

333.9

111.9

1,060.1

Cash and cash

equivalents

Trade receivables

Inventory, other assets

Fixed assets

(goodwill 827.8/756.4)

Total

Financial liabilities

Other liabilities

Deferred income

Shareholders equity

(ratio 48.9%/59.8%)

Total

Assets Liabilities

Balance sheet (in €m)

December 31,

2012

December 31,

2012

Securities 51.5

©2013 Software AG. All rights reserved.

34 |

Headcount by functional areas* and geography

(in FTE) Sept.30,

2013

June 30,

2013

Δ% qoq

Sept.30,

2012

Δ% yoy

Total 5,356 5,375 - 5 5,436 -1%

Consulting & services 2,375 2,484 -4% 2,715 -13%

R & D 1,005 941 7% 892 13%

Sales & marketing 1,261 1,229 3% 1,084 16%

Administration 715 721 -1% 745 -4%

USA 804 769 5% 739 9%

Germany 1,735 1,777 -2% 1,783 -3%

Rest of world 2,817 2,829 - 2,914 -3%

* According to P+L structure

©2013 Software AG. All rights reserved.

35 |

Non-IFRS Earnings (Q1 – Q3 2013)

*Based on average outstanding shares: Q1 2013: 85.8m / Q1 2012: 86.8 // Q2 2013: 83.8m / Q2 2012: 86.8m //

Q3 2013: 83.0m / Q3 2012: 86.8m

(in €m) Q1

2013

Q1

2012

Q2

2013

Q2

2012

Q3

2013

Q3

2012

EBIT (before all taxes) 41.6 54.8 44.4 57.1 49.1 61.1

Share based payment -0.6 0.7 -0.7 1.3 0.5 2.2

Amortization on acquisition

related intangible assets 9.4 9.2 10.1 9.5 11.5 9.7

Reduction product revenue

by purchase price allocation - 0.6 - 0.4 0.9 -

Other acquisition impacts 0.1 0.2 1.2 0.3 0.3 0.1

Restructuring/severances 1.5 0.4 3.7 1.4 4.0 0.7

EBIT (Non-IFRS) 52.0 65.9 58.7 70.0 66.3 73.8

in % of revenue (Non-IFRS) 23.1% 25.8% 24.7% 27.0% 27.7% 28.7%

Net income (Non-IFRS) 33.2 44.3 38.1 46.0 43.0 49.6

EPS (Non-IFRS)* 0.39 0.51 0.45 0.53 0.52 0.57

Net income (IFRS) 27.2 35.9 28.8 37.5 31.1 40.7

©2013 Software AG. All rights reserved.

36 |

Amortization / depreciation impact 2013ff

(preliminary)

Q3

2013

2.7

8.8

3.2

GJ

2013

GJ

2014ff*

* Estimated

Amortization IDS

(in €m)

Amortization other

Depreciation

10.6

32.2

13.1

10.6

32.4

12.8

©2013 Software AG. All rights reserved.

Follow us on Twitter:

@SoftwareAG_IR

Investor Relations

Uhlandstrasse 12

64297 Darmstadt

Germany

phone: +49 (0) 6151 / 92 1900

fax: +49 (0) 6151 / 9234 1900

softwareag.com

e-mail: [email protected]