Page 1

SR Research Report 2014/04/10

SBS Holdings, Inc.(2384)

Shared Research Inc. has produced this report by request from the company discussed in the report. The aim is

to provide an “owner’s manual” to investors. We at Shared Research Inc. make every effort to provide an

accurate, objective, and neutral analysis. In order to highlight any biases, we clearly attribute our data and

findings. We will always present opinions from company management as such. Our views are ours where stated.

We do not try to convince or influence, only inform. We appreciate your suggestions and feedback. Write to us at

[email protected] or find us on Bloomberg.

Page 2

SBS Holdings, Inc.(2384)

2014/04/10

http://www.sharedresearch.jp/ Copyright (C) Shared Research Inc. All Rights Reserved 2/50

SR Research Report

Contents

Executive summary ................................................................................. 3

Key financial data .................................................................................... 4

Recent updates ....................................................................................... 5

Highlights ............................................................................................ 5

Trends and outlook ............................................................................... 5

Business ................................................................................................ 9

Market and value chain ........................................................................ 32

Strategy ............................................................................................ 37

Historical performance ........................................................................... 39

Income statement .............................................................................. 40

Balance sheet .................................................................................... 42

Cash flow statement ........................................................................... 44

Other information .................................................................................. 46

History .............................................................................................. 46

Major shareholders ............................................................................. 46

Top management ................................................................................ 47

Employees ......................................................................................... 47

Shareholder returns ............................................................................ 47

IR ..................................................................................................... 47

By the way ........................................................................................ 48

Company ............................................................................................. 49

Page 3

SBS Holdings, Inc.(2384)

2014/04/10

http://www.sharedresearch.jp/ Copyright (C) Shared Research Inc. All Rights Reserved 3/50

SR Research Report

Executive summary

Business

The logistics business primarily offers company-to-company general logistics, food logistics and specialty

logistics services. The main logistics support service is in property management—SBS develops, rents and

sells logistics facilities. Logistics accounts for the bulk of sales and profits: 93% of sales and 31% of

operating profit in FY12/13.

After just 26 years in business, SBS has grown to annual sales of over JPY130bn in an industry full of

players with more experience. By the end of FY12/13, the company conducted investments of JPY29.7bn

in 25 companies. Companies acquired via M&A include businesses in fields such as food, apparel and

consumables, small lot deliveries, and long distance transport.

Four key growth drivers for the company are M&A, 3PL, overseas expansion, and its logistics facilities

development + private fund system. SBS achieved dramatic growth through M&A, and will continue to

use M&A as well as growth of its 3PL business to accelerate overseas expansion. By adding proprietary

expertise in logistics facilities development, its 3PL business will reach a higher level of competitiveness.

Overseas, increasing the number of logistics hubs providing logistics with Japanese-style quality will be a

key objective. Last, the private fund system will act as an exit strategy for logistics facilities development

with the added benefit of providing gains on transfers. It also serves to foster healthy corporate growth

without weighing down the balance sheet.

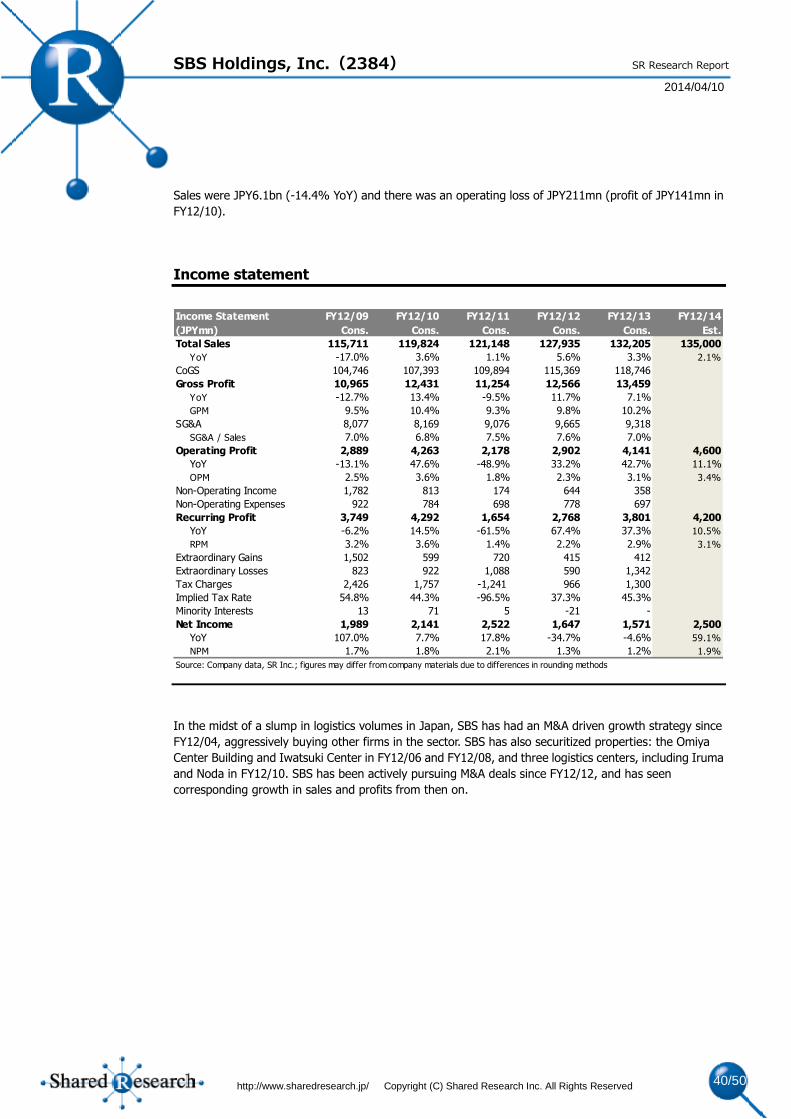

Trends

FY12/13 full-year consolidated sales came out at JPY132.2bn (+3.3% YoY), operating profit was

JPY4.1bn (+42.7%), recurring profit was JPY3.8bn (+37.4%), and net income was JPY1.6bn (-4.6%).

The company recorded extraordinary losses of JPY1.3bn, including JPY598mn on relocating and

regrouping logistics centers and brand unification, along with lease cancellation fees as it shut down

offices and warehouses, and other impairment losses.

The company forecasts consolidated sales of JPY135.0bn (+2.1% YoY), operating profit of JPY4.6bn

(+11.1%), recurring profit of JPY4.2bn (+10.5%), and net income of JPY2.5bn (+59.1%) in FY12/14.

In 2017, it will be 30 years since the company’s founding. The company has developed a four-year

medium-term management plan to mark this point in its history. The plan is set to last from FY12/14 to

FY12/17, and is called SBS Growth 2017. By focusing on M&A and development of logistics facilities, the

company hopes to achieve lasting sales growth by developing its overseas businesses—particularly in Asia,

and in the 3PL business. It also hopes that a full-scale move toward low cost operations will help it to

achieve greater profitability and a more solid financial base. Therefore, the company is targeting sales of

JPY200bn in 2017 (CAGR of 14%) and operating profit of JPY8bn (20.3%).

Strengths & weaknesses

SR believes the strengths of the company to be ambitious management hungry for growth, a solid track

record in developing logistics facilities, and a history of successful M&A deals. Weaknesses of the

company are an inherent difficulty in lifting profitability, a need for financial fortification, and limited

opportunities for growth due to insufficient personnel. (see Strengths and weaknesses)

Page 4

SBS Holdings, Inc.(2384)

2014/04/10

http://www.sharedresearch.jp/ Copyright (C) Shared Research Inc. All Rights Reserved 4/50

SR Research Report

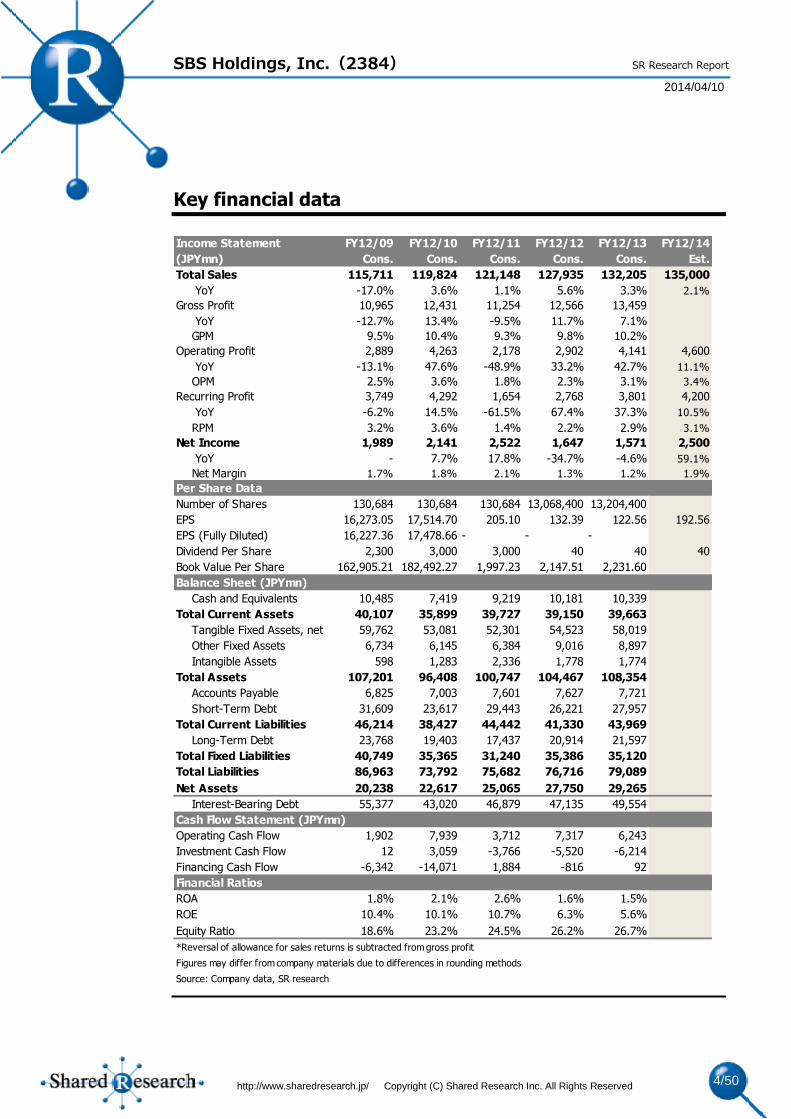

Key financial data

Income Statement FY12/09 FY12/10 FY12/11 FY12/12 FY12/13 FY12/14

(JPYmn) Cons. Cons. Cons. Cons. Cons. Est.

Total Sales 115,711 119,824 121,148 127,935 132,205 135,000

YoY -17.0% 3.6% 1.1% 5.6% 3.3% 2.1%

Gross Profit 10,965 12,431 11,254 12,566 13,459

YoY -12.7% 13.4% -9.5% 11.7% 7.1%

GPM 9.5% 10.4% 9.3% 9.8% 10.2%

Operating Profit 2,889 4,263 2,178 2,902 4,141 4,600

YoY -13.1% 47.6% -48.9% 33.2% 42.7% 11.1%

OPM 2.5% 3.6% 1.8% 2.3% 3.1% 3.4%

Recurring Profit 3,749 4,292 1,654 2,768 3,801 4,200

YoY -6.2% 14.5% -61.5% 67.4% 37.3% 10.5%

RPM 3.2% 3.6% 1.4% 2.2% 2.9% 3.1%

Net Income 1,989 2,141 2,522 1,647 1,571 2,500

YoY - 7.7% 17.8% -34.7% -4.6% 59.1%

Net Margin 1.7% 1.8% 2.1% 1.3% 1.2% 1.9%

Per Share Data

Number of Shares 130,684 130,684 130,684 13,068,400 13,204,400

EPS 16,273.05 17,514.70 205.10 132.39 122.56 192.56

EPS (Fully Diluted) 16,227.36 17,478.66 - - -

Dividend Per Share 2,300 3,000 3,000 40 40 40

Book Value Per Share 162,905.21 182,492.27 1,997.23 2,147.51 2,231.60

Balance Sheet (JPYmn)

Cash and Equivalents 10,485 7,419 9,219 10,181 10,339

Total Current Assets 40,107 35,899 39,727 39,150 39,663

Tangible Fixed Assets, net 59,762 53,081 52,301 54,523 58,019

Other Fixed Assets 6,734 6,145 6,384 9,016 8,897

Intangible Assets 598 1,283 2,336 1,778 1,774

Total Assets 107,201 96,408 100,747 104,467 108,354

Accounts Payable 6,825 7,003 7,601 7,627 7,721

Short-Term Debt 31,609 23,617 29,443 26,221 27,957

Total Current Liabilities 46,214 38,427 44,442 41,330 43,969

Long-Term Debt 23,768 19,403 17,437 20,914 21,597

Total Fixed Liabilities 40,749 35,365 31,240 35,386 35,120

Total Liabilities 86,963 73,792 75,682 76,716 79,089

Net Assets 20,238 22,617 25,065 27,750 29,265

Interest-Bearing Debt 55,377 43,020 46,879 47,135 49,554

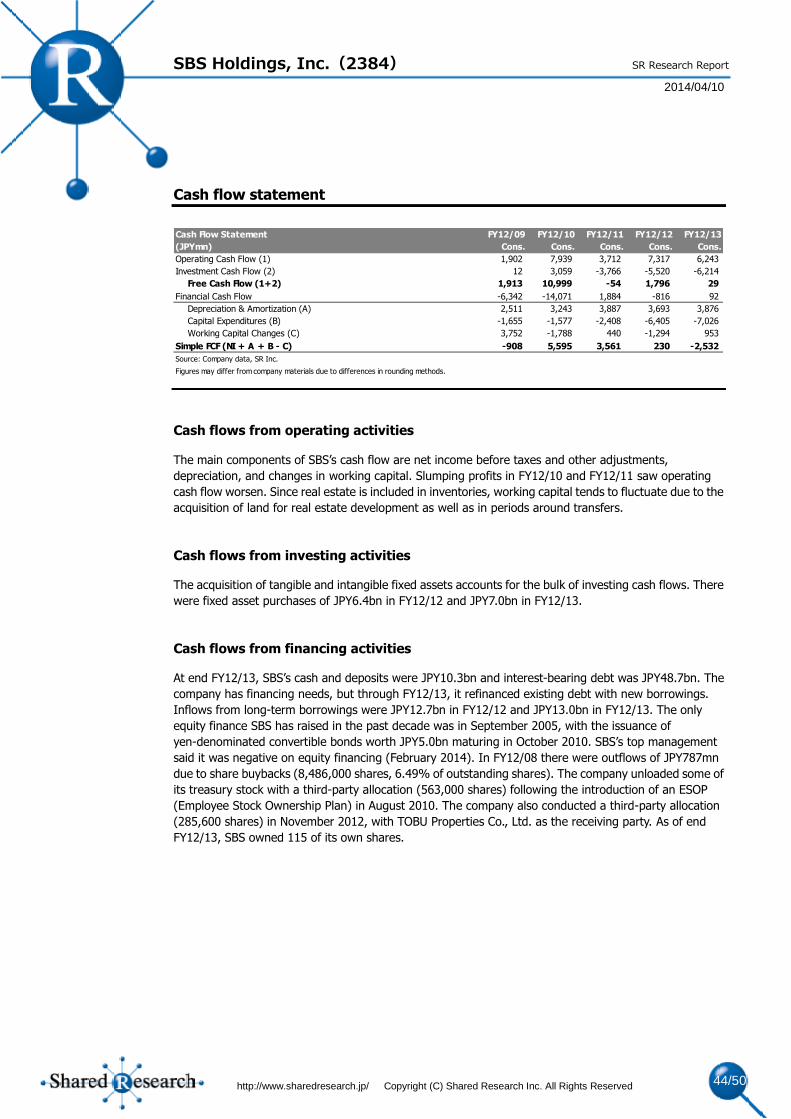

Cash Flow Statement (JPYmn)

Operating Cash Flow 1,902 7,939 3,712 7,317 6,243

Investment Cash Flow 12 3,059 -3,766 -5,520 -6,214

Financing Cash Flow -6,342 -14,071 1,884 -816 92

Financial Ratios

ROA 1.8% 2.1% 2.6% 1.6% 1.5%

ROE 10.4% 10.1% 10.7% 6.3% 5.6%

Equity Ratio 18.6% 23.2% 24.5% 26.2% 26.7%

*Reversal of allowance for sales returns is subtracted from gross profit

Figures may differ from company materials due to differences in rounding methods

Source: Company data, SR research

Page 5

SBS Holdings, Inc.(2384)

2014/04/10

http://www.sharedresearch.jp/ Copyright (C) Shared Research Inc. All Rights Reserved 5/50

SR Research Report

Recent updates

Highlights

SR initiates coverage of SBS Holdings, Inc. with this report.

Trends and outlook

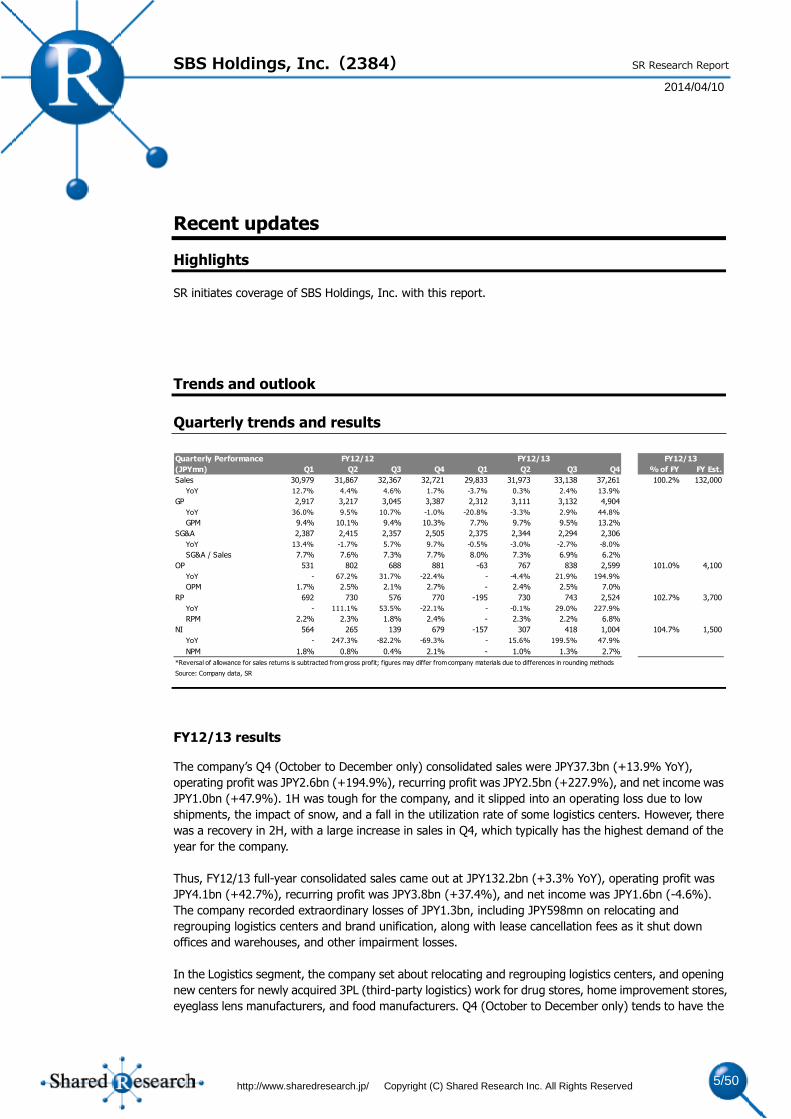

Quarterly trends and results

FY12/13 results

The company’s Q4 (October to December only) consolidated sales were JPY37.3bn (+13.9% YoY),

operating profit was JPY2.6bn (+194.9%), recurring profit was JPY2.5bn (+227.9%), and net income was

JPY1.0bn (+47.9%). 1H was tough for the company, and it slipped into an operating loss due to low

shipments, the impact of snow, and a fall in the utilization rate of some logistics centers. However, there

was a recovery in 2H, with a large increase in sales in Q4, which typically has the highest demand of the

year for the company.

Thus, FY12/13 full-year consolidated sales came out at JPY132.2bn (+3.3% YoY), operating profit was

JPY4.1bn (+42.7%), recurring profit was JPY3.8bn (+37.4%), and net income was JPY1.6bn (-4.6%).

The company recorded extraordinary losses of JPY1.3bn, including JPY598mn on relocating and

regrouping logistics centers and brand unification, along with lease cancellation fees as it shut down

offices and warehouses, and other impairment losses.

In the Logistics segment, the company set about relocating and regrouping logistics centers, and opening

new centers for newly acquired 3PL (third-party logistics) work for drug stores, home improvement stores,

eyeglass lens manufacturers, and food manufacturers. Q4 (October to December only) tends to have the

Quarterly Performance

(JPYmn) Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 % of FY FY Est.

Sales 30,979 31,867 32,367 32,721 29,833 31,973 33,138 37,261 100.2% 132,000

YoY 12.7% 4.4% 4.6% 1.7% -3.7% 0.3% 2.4% 13.9%

GP 2,917 3,217 3,045 3,387 2,312 3,111 3,132 4,904

YoY 36.0% 9.5% 10.7% -1.0% -20.8% -3.3% 2.9% 44.8%

GPM 9.4% 10.1% 9.4% 10.3% 7.7% 9.7% 9.5% 13.2%

SG&A 2,387 2,415 2,357 2,505 2,375 2,344 2,294 2,306

YoY 13.4% -1.7% 5.7% 9.7% -0.5% -3.0% -2.7% -8.0%

SG&A / Sales 7.7% 7.6% 7.3% 7.7% 8.0% 7.3% 6.9% 6.2%

OP 531 802 688 881 -63 767 838 2,599 101.0% 4,100

YoY - 67.2% 31.7% -22.4% - -4.4% 21.9% 194.9%

OPM 1.7% 2.5% 2.1% 2.7% - 2.4% 2.5% 7.0%

RP 692 730 576 770 -195 730 743 2,524 102.7% 3,700

YoY - 111.1% 53.5% -22.1% - -0.1% 29.0% 227.9%

RPM 2.2% 2.3% 1.8% 2.4% - 2.3% 2.2% 6.8%

NI 564 265 139 679 -157 307 418 1,004 104.7% 1,500

YoY - 247.3% -82.2% -69.3% - 15.6% 199.5% 47.9%

NPM 1.8% 0.8% 0.4% 2.1% - 1.0% 1.3% 2.7%

*Reversal of allowance for sales returns is subtracted from gross profit; figures may differ from company materials due to differences in rounding methods

Source: Company data, SR

FY12/13FY12/13FY12/12

Page 6

SBS Holdings, Inc.(2384)

2014/04/10

http://www.sharedresearch.jp/ Copyright (C) Shared Research Inc. All Rights Reserved 6/50

SR Research Report

highest demand of any quarter for the company, and this year was no exception with sales of JPY32.0bn

(+4.7% YoY), and operating profit of JPY932mn (+32.0%). Thus, full-year sales for the Logistics segment

were JPY120.8bn (+1.2%), and operating profit—held back by the loss in 1H—was JPY1.2bn (-29.5%).

Also, in November the company purchased land in Yokohama (Isogo, Sugita). It plans to build a 10,000

tsubo (33,000 m2) logistics center there by 2015.

Q4 sales in the Property Management segment were JPY2.9bn, and operating profit was JPY1.2bn. The

company transferred 51% of the trust beneficiary rights of its logistics facilities to SBS Logifund 1, a

private fund operated by a major financial institution. Full-year sales were JPY5.6bn (+121.8% YoY) and

JPY2.6bn (+111.3%), aided by rental income as the company increased its stake of facilities held for

rental purposes.

In terms of other businesses, sales were robust in the Personnel and Industrial Waste Recycling

businesses. In addition, other business sales were boosted by the sales of a new business—Solar Power

Generation—from 2H. However, full-year sales for other businesses nevertheless fell 3.9% YoY to

JPY5.9bn, as the results of a dispatch agency subsidiary were removed from the group’s consolidated

results. Operating profit leaped up 351.0% YoY to JPY202mn, thanks to recovery in the Marketing and

Industrial Waste Recycling businesses, and the contribution of the Personnel business as it moved into the

black.

The net debt/equity ratio was 1.37 (1.39 the previous year). The dividend per share (DPS) was

JPY40—consisting of a regular dividend of JPY30 and a special dividend of JPY10 to commemorate the

company’s listing on the First Section of the Tokyo Stock Exchange (the previous year saw a regular

dividend of JPY30 and a special dividend of JPY10 commemorating the company’s listing on the Second

Section of the TSE). The payout ratio was therefore 32.6%.

In December 2013, the company moved from the Second Section (mid-size companies) of the Tokyo

Stock Exchange to the First Section (large companies).

For details on previous quarterly and annual results, see the Historical performance section.

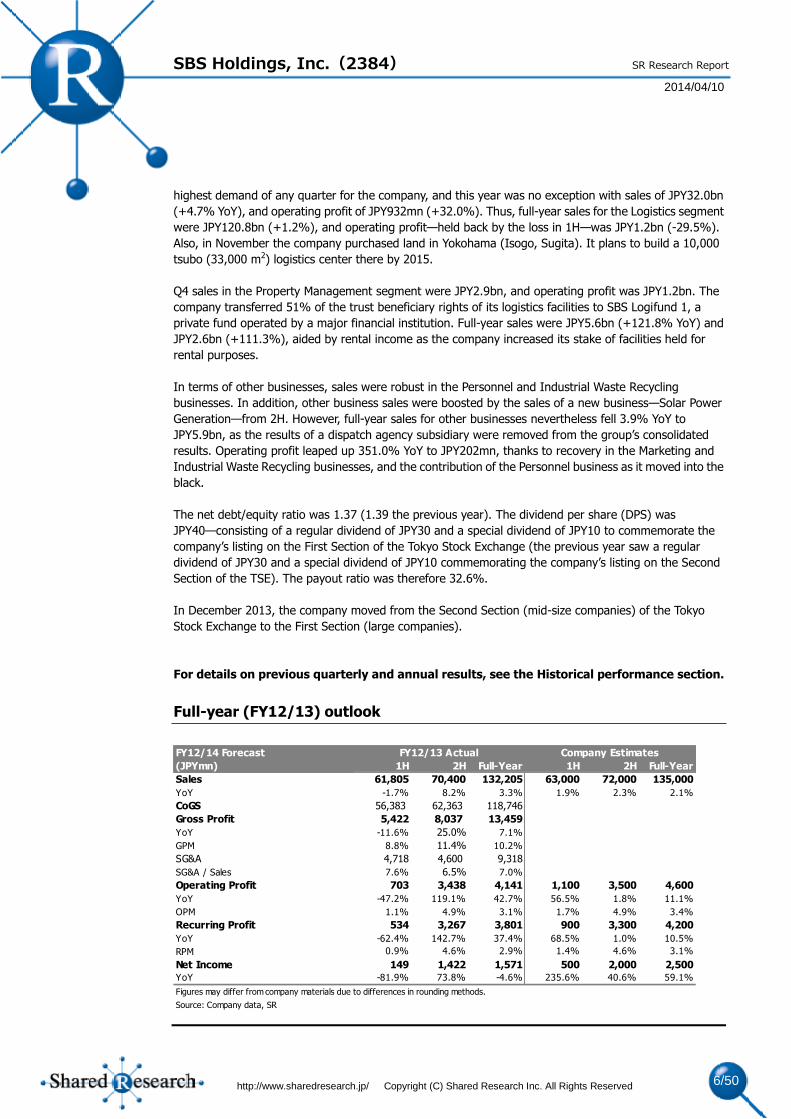

Full-year (FY12/13) outlook

FY12/14 Forecast

(JPYmn) 1H 2H Full-Year 1H 2H Full-Year

Sales 61,805 70,400 132,205 63,000 72,000 135,000

YoY -1.7% 8.2% 3.3% 1.9% 2.3% 2.1%

CoGS 56,383 62,363 118,746

Gross Profit 5,422 8,037 13,459

YoY -11.6% 25.0% 7.1%

GPM 8.8% 11.4% 10.2%

SG&A 4,718 4,600 9,318

SG&A / Sales 7.6% 6.5% 7.0%

Operating Profit 703 3,438 4,141 1,100 3,500 4,600

YoY -47.2% 119.1% 42.7% 56.5% 1.8% 11.1%

OPM 1.1% 4.9% 3.1% 1.7% 4.9% 3.4%

Recurring Profit 534 3,267 3,801 900 3,300 4,200

YoY -62.4% 142.7% 37.4% 68.5% 1.0% 10.5%

RPM 0.9% 4.6% 2.9% 1.4% 4.6% 3.1%

Net Income 149 1,422 1,571 500 2,000 2,500

YoY -81.9% 73.8% -4.6% 235.6% 40.6% 59.1%

Figures may differ from company materials due to differences in rounding methods.

Source: Company data, SR

Company EstimatesFY12/13 Actual

Page 7

SBS Holdings, Inc.(2384)

2014/04/10

http://www.sharedresearch.jp/ Copyright (C) Shared Research Inc. All Rights Reserved 7/50

SR Research Report

The company forecasts consolidated sales of JPY135.0bn (+2.1% YoY), operating profit of JPY4.6bn

(+11.1%), recurring profit of JPY4.2bn (+10.5%), and net income of JPY2.5bn (+59.1%) in FY12/14.

Forecasts by segment:

Logistics: sales JPY123.5bn (+2.2% YoY); operating profit JPY2.0bn (+60.0%);

Property Management: sales JPY5.3bn (-4.6%); operating profit JPY2.4bn (-5.9%);

Other businesses: sales JPY6.2bn (+5.7%); operating profit JPY250mn (+23.8%).

Logistics: the company is forecasting sales of JPY48.0bn (+4.1% YoY) in the 3PL business, as it

strengthens its proposal-based sales. It is also targeting sales of JPY7.7bn (+18.5%) in overseas logistics,

due to bolstered operations in the ASEAN region, India and East Asian region including China. Also, the

company forecasts large increases in profits, in line with the move to a low cost framework for operations.

Property Management: in the rental business, the company expects rental income to fall because it has

securitized a logistics facility (transferring half the trust beneficiary rights of the Kyotanabe facility).

Therefore it forecasts a corresponding fall in sales and profits. In the development business, the company

is planning for securitization of the remaining half of facilities around the Kyotanabe area, continuing from

the previous year. Construction at the Nagatsuta (Yokohama) facility, which is currently under

development, is expected to be completed in November.

Other businesses: the company is expecting the staffing business to maintain solid performance, and is

targeting sales of about JPY200mn in the Solar Power Generation business (sales of JPY100mn the

previous year).

The company is forecasting a jump in net income because it reported extraordinary losses of JPY1.3bn

the previous year. These losses were the result of costs associated with brand unification and the

relocating and regrouping of logistics centers (JPY598mn), along with lease cancellation fees as it shut

down offices and warehouses.

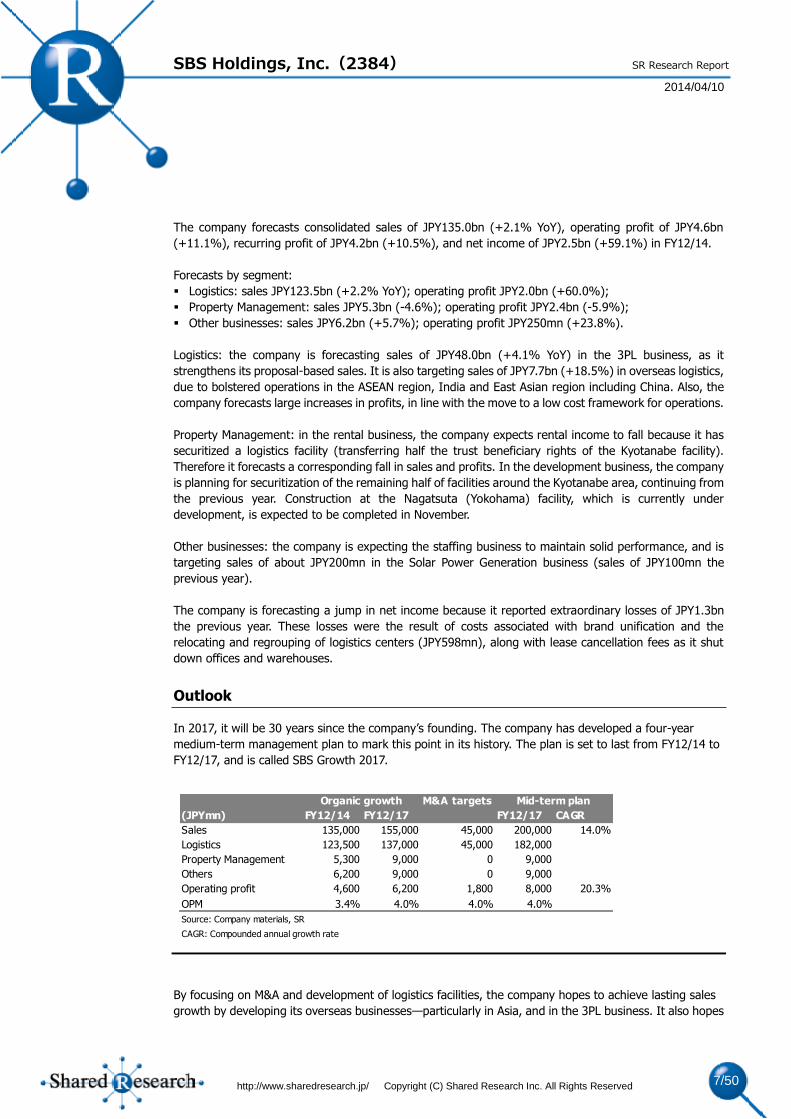

Outlook

In 2017, it will be 30 years since the company’s founding. The company has developed a four-year

medium-term management plan to mark this point in its history. The plan is set to last from FY12/14 to

FY12/17, and is called SBS Growth 2017.

By focusing on M&A and development of logistics facilities, the company hopes to achieve lasting sales

growth by developing its overseas businesses—particularly in Asia, and in the 3PL business. It also hopes

M&A targets

(JPYmn) FY12/14 FY12/17 FY12/17 CAGR

Sales 135,000 155,000 45,000 200,000 14.0%

Logistics 123,500 137,000 45,000 182,000

Property Management 5,300 9,000 0 9,000

Others 6,200 9,000 0 9,000

Operating profit 4,600 6,200 1,800 8,000 20.3%

OPM 3.4% 4.0% 4.0% 4.0%

Source: Company materials, SR

CAGR: Compounded annual growth rate

Organic growth Mid-term plan

Page 8

SBS Holdings, Inc.(2384)

2014/04/10

http://www.sharedresearch.jp/ Copyright (C) Shared Research Inc. All Rights Reserved 8/50

SR Research Report

that a full-scale move toward low cost operations will help it to achieve greater profitability and a more

solid financial base. Therefore, the company is targeting sales of JPY200bn in 2017 (CAGR of 14%) and

operating profit of JPY8bn (20.3%).

In its 3PL business, the company plans to move into new growth sectors such as consumer goods logistics,

manufacturing logistics, and online retail. Overseas, it will be targeting growth in the ASEAN region, India

and East Asian region including China. It is aiming for sales of JPY70bn in the 3PL business, and JPY30bn

in the International Logistics business, with a total of JPY182.0bn for the Logistics segment as a whole.

The company also plans to grow sales by JPY45bn and operating profit by JPY1.8bn through M&A deals.

The company’s plan calls for an operating profit margin (OPM) of at least 4% (3.1% in FY12/13), and a

return on equity (ROE) of at least 30% (26.7% in FY12/13).

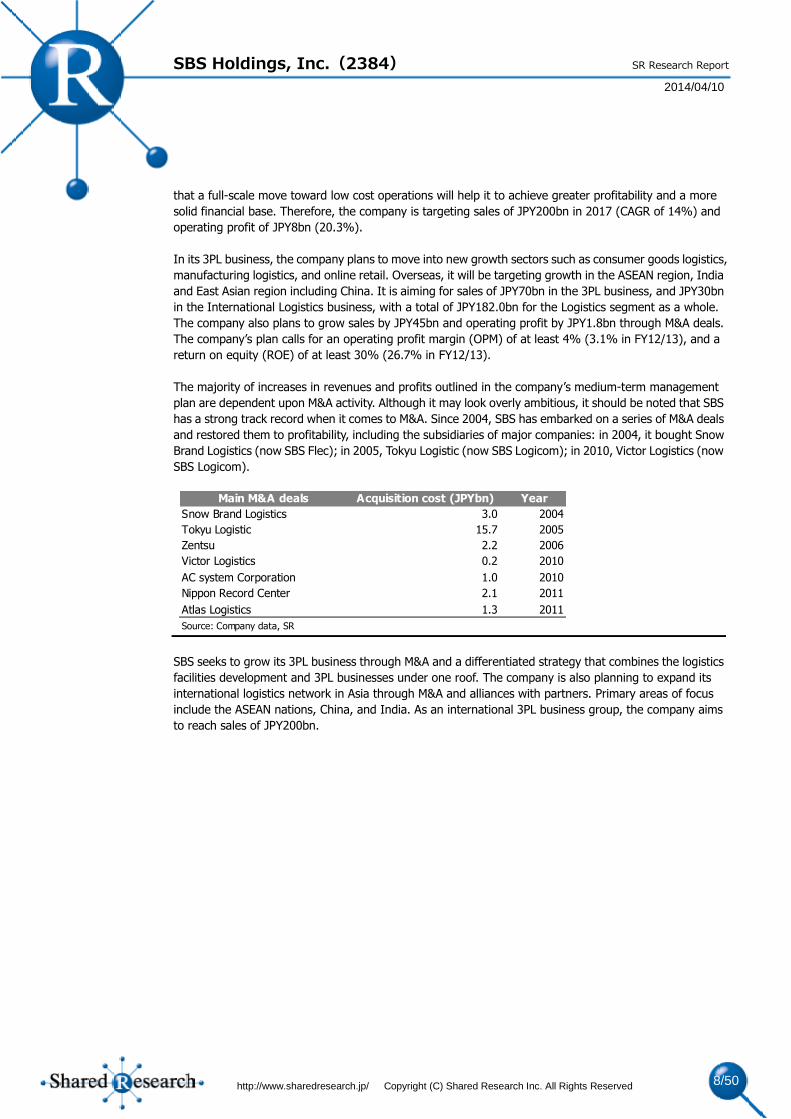

The majority of increases in revenues and profits outlined in the company’s medium-term management

plan are dependent upon M&A activity. Although it may look overly ambitious, it should be noted that SBS

has a strong track record when it comes to M&A. Since 2004, SBS has embarked on a series of M&A deals

and restored them to profitability, including the subsidiaries of major companies: in 2004, it bought Snow

Brand Logistics (now SBS Flec); in 2005, Tokyu Logistic (now SBS Logicom); in 2010, Victor Logistics (now

SBS Logicom).

SBS seeks to grow its 3PL business through M&A and a differentiated strategy that combines the logistics

facilities development and 3PL businesses under one roof. The company is also planning to expand its

international logistics network in Asia through M&A and alliances with partners. Primary areas of focus

include the ASEAN nations, China, and India. As an international 3PL business group, the company aims

to reach sales of JPY200bn.

Main M&A deals Acquisition cost (JPYbn) Year

Snow Brand Logistics 3.0 2004

Tokyu Logistic 15.7 2005

Zentsu 2.2 2006

Victor Logistics 0.2 2010

AC system Corporation 1.0 2010

Nippon Record Center 2.1 2011

Atlas Logistics 1.3 2011

Source: Company data, SR

Page 9

SBS Holdings, Inc.(2384)

2014/04/10

http://www.sharedresearch.jp/ Copyright (C) Shared Research Inc. All Rights Reserved 9/50

SR Research Report

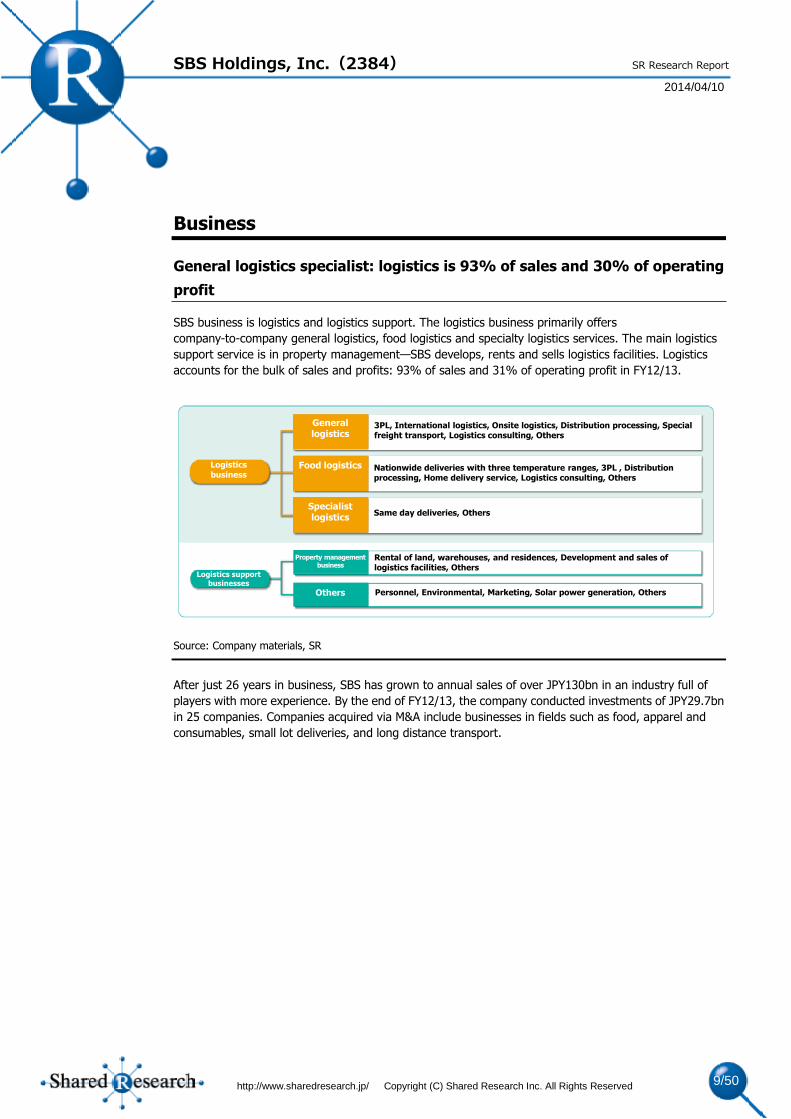

Business

General logistics specialist: logistics is 93% of sales and 30% of operating

profit

SBS business is logistics and logistics support. The logistics business primarily offers

company-to-company general logistics, food logistics and specialty logistics services. The main logistics

support service is in property management—SBS develops, rents and sells logistics facilities. Logistics

accounts for the bulk of sales and profits: 93% of sales and 31% of operating profit in FY12/13.

Source: Company materials, SR

After just 26 years in business, SBS has grown to annual sales of over JPY130bn in an industry full of

players with more experience. By the end of FY12/13, the company conducted investments of JPY29.7bn

in 25 companies. Companies acquired via M&A include businesses in fields such as food, apparel and

consumables, small lot deliveries, and long distance transport.

Logistics business

General logistics

Food logistics

Specialist logistics

3PL, International logistics, Onsite logistics, Distribution processing, Special freight transport, Logistics consulting, Others

Nationwide deliveries with three temperature ranges, 3PL , Distribution processing, Home delivery service, Logistics consulting, Others

Same day deliveries, Others

Logistics support businesses

Property management business

Others

Rental of land, warehouses, and residences, Development and sales of logistics facilities, Others

Personnel, Environmental, Marketing, Solar power generation, Others

Page 10

SBS Holdings, Inc.(2384)

2014/04/10

http://www.sharedresearch.jp/ Copyright (C) Shared Research Inc. All Rights Reserved 10/50

SR Research Report

Source: Company materials, SR

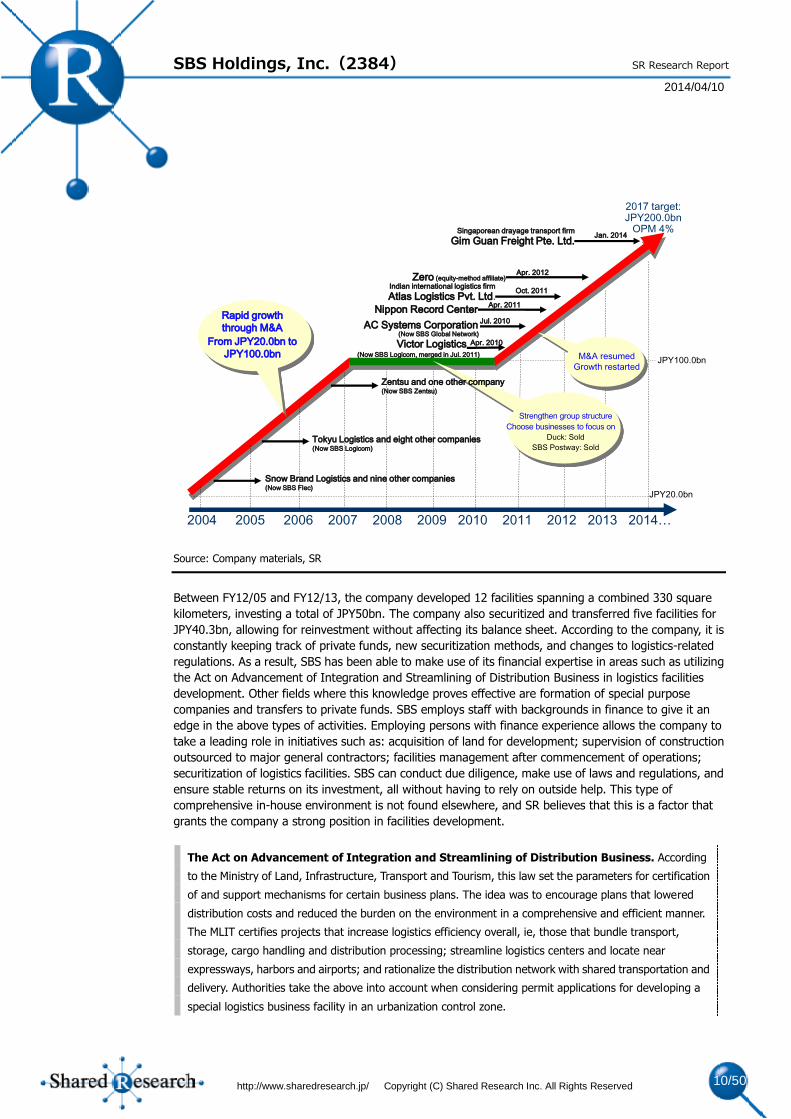

Between FY12/05 and FY12/13, the company developed 12 facilities spanning a combined 330 square

kilometers, investing a total of JPY50bn. The company also securitized and transferred five facilities for

JPY40.3bn, allowing for reinvestment without affecting its balance sheet. According to the company, it is

constantly keeping track of private funds, new securitization methods, and changes to logistics-related

regulations. As a result, SBS has been able to make use of its financial expertise in areas such as utilizing

the Act on Advancement of Integration and Streamlining of Distribution Business in logistics facilities

development. Other fields where this knowledge proves effective are formation of special purpose

companies and transfers to private funds. SBS employs staff with backgrounds in finance to give it an

edge in the above types of activities. Employing persons with finance experience allows the company to

take a leading role in initiatives such as: acquisition of land for development; supervision of construction

outsourced to major general contractors; facilities management after commencement of operations;

securitization of logistics facilities. SBS can conduct due diligence, make use of laws and regulations, and

ensure stable returns on its investment, all without having to rely on outside help. This type of

comprehensive in-house environment is not found elsewhere, and SR believes that this is a factor that

grants the company a strong position in facilities development.

The Act on Advancement of Integration and Streamlining of Distribution Business. According

to the Ministry of Land, Infrastructure, Transport and Tourism, this law set the parameters for certification

of and support mechanisms for certain business plans. The idea was to encourage plans that lowered

distribution costs and reduced the burden on the environment in a comprehensive and efficient manner.

The MLIT certifies projects that increase logistics efficiency overall, ie, those that bundle transport,

storage, cargo handling and distribution processing; streamline logistics centers and locate near

expressways, harbors and airports; and rationalize the distribution network with shared transportation and

delivery. Authorities take the above into account when considering permit applications for developing a

special logistics business facility in an urbanization control zone.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014…

Snow Brand Logistics and nine other companies (Now SBS Flec)

Tokyu Logistics and eight other companies(Now SBS Logicom)

AC Systems Corporation

Nippon Record CenterRapid growth

through M&A

From JPY20.0bn to

JPY100.0bnJPY100.0bn

JPY20.0bn

2017 target:JPY200.0bn

OPM 4%

Victor Logistics

Indian international logistics firm

Atlas Logistics Pvt. Ltd.

Apr. 2010

Jul. 2010

Apr. 2011

Oct. 2011

(Now SBS Logicom, merged in Jul. 2011)

Strengthen group structure

Choose businesses to focus on

Duck: Sold

SBS Postway: Sold

(Now SBS Global Network)

Zentsu and one other company(Now SBS Zentsu)

M&A resumed

Growth restarted

Zero (equity-method affiliate)Apr. 2012

Singaporean drayage transport firm

Gim Guan Freight Pte. Ltd.Jan. 2014

Page 11

SBS Holdings, Inc.(2384)

2014/04/10

http://www.sharedresearch.jp/ Copyright (C) Shared Research Inc. All Rights Reserved 11/50

SR Research Report

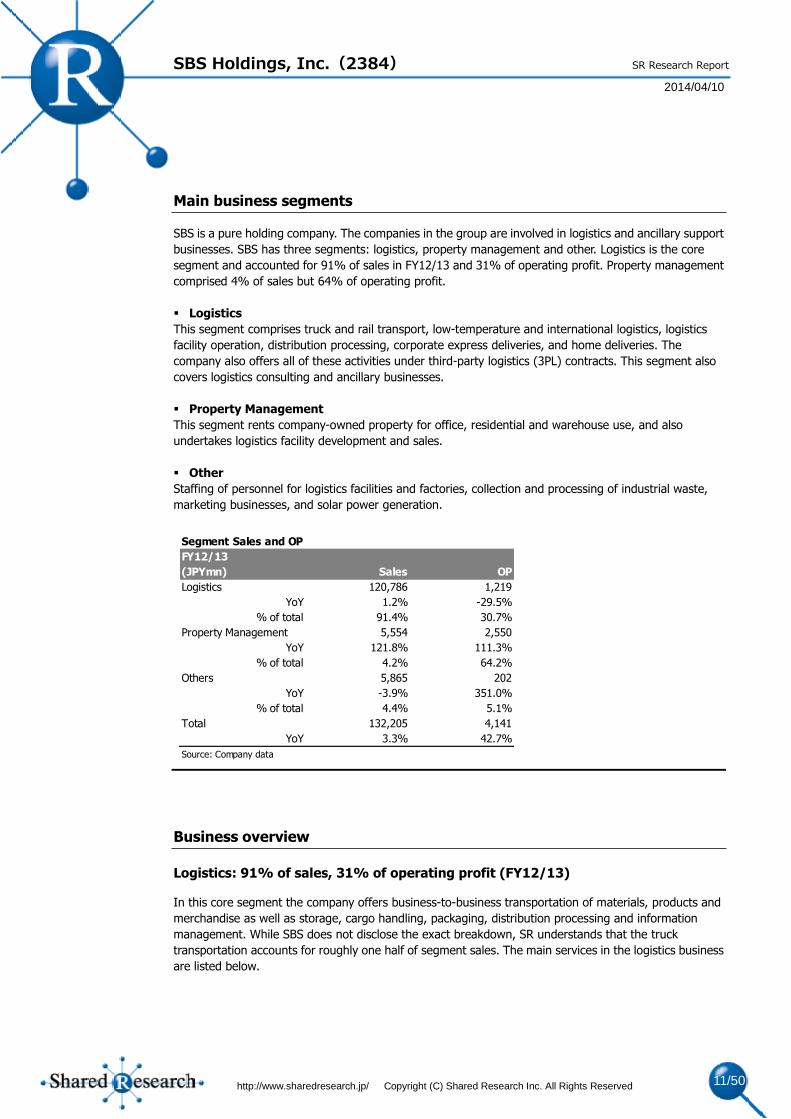

Main business segments

SBS is a pure holding company. The companies in the group are involved in logistics and ancillary support

businesses. SBS has three segments: logistics, property management and other. Logistics is the core

segment and accounted for 91% of sales in FY12/13 and 31% of operating profit. Property management

comprised 4% of sales but 64% of operating profit.

Logistics

This segment comprises truck and rail transport, low-temperature and international logistics, logistics

facility operation, distribution processing, corporate express deliveries, and home deliveries. The

company also offers all of these activities under third-party logistics (3PL) contracts. This segment also

covers logistics consulting and ancillary businesses.

Property Management

This segment rents company-owned property for office, residential and warehouse use, and also

undertakes logistics facility development and sales.

Other

Staffing of personnel for logistics facilities and factories, collection and processing of industrial waste,

marketing businesses, and solar power generation.

Business overview

Logistics: 91% of sales, 31% of operating profit (FY12/13)

In this core segment the company offers business-to-business transportation of materials, products and

merchandise as well as storage, cargo handling, packaging, distribution processing and information

management. While SBS does not disclose the exact breakdown, SR understands that the truck

transportation accounts for roughly one half of segment sales. The main services in the logistics business

are listed below.

Segment Sales and OP

FY12/13

(JPYmn) Sales OP

Logistics 120,786 1,219

YoY 1.2% -29.5%

% of total 91.4% 30.7%

Property Management 5,554 2,550

YoY 121.8% 111.3%

% of total 4.2% 64.2%

Others 5,865 202

YoY -3.9% 351.0%

% of total 4.4% 5.1%

Total 132,205 4,141

YoY 3.3% 42.7%

Source: Company data

Page 12

SBS Holdings, Inc.(2384)

2014/04/10

http://www.sharedresearch.jp/ Copyright (C) Shared Research Inc. All Rights Reserved 12/50

SR Research Report

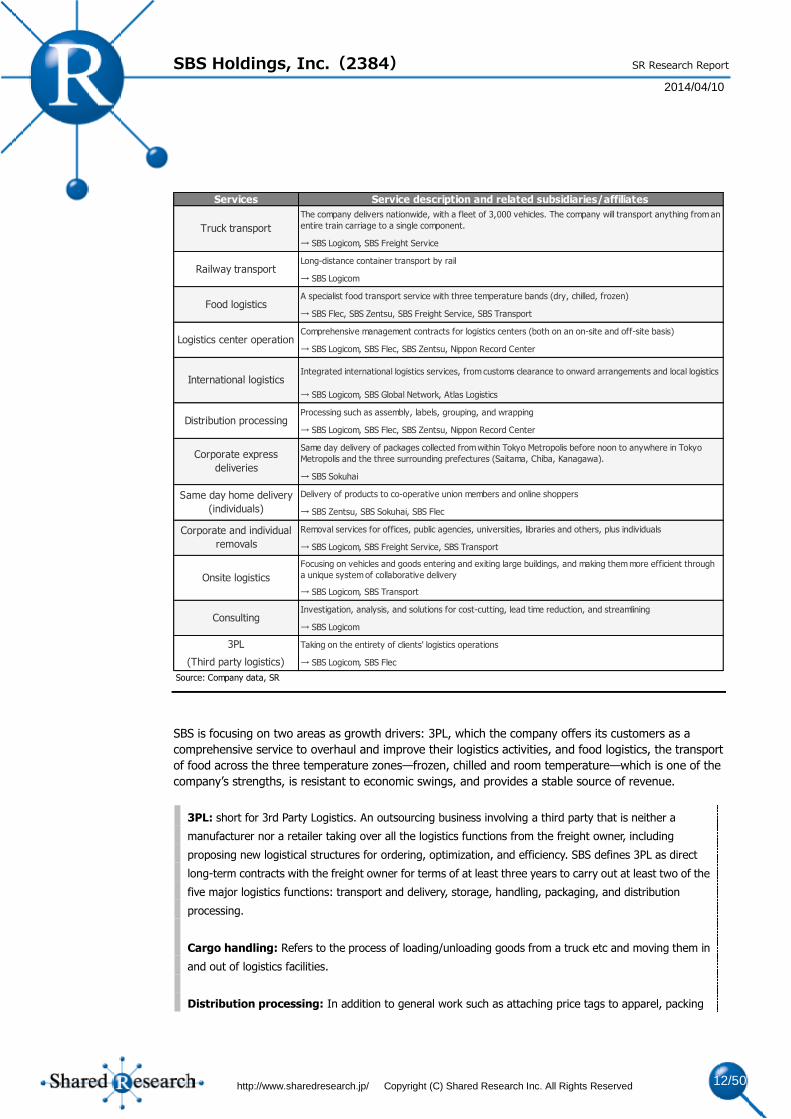

SBS is focusing on two areas as growth drivers: 3PL, which the company offers its customers as a

comprehensive service to overhaul and improve their logistics activities, and food logistics, the transport

of food across the three temperature zones—frozen, chilled and room temperature—which is one of the

company’s strengths, is resistant to economic swings, and provides a stable source of revenue.

3PL: short for 3rd Party Logistics. An outsourcing business involving a third party that is neither a

manufacturer nor a retailer taking over all the logistics functions from the freight owner, including

proposing new logistical structures for ordering, optimization, and efficiency. SBS defines 3PL as direct

long-term contracts with the freight owner for terms of at least three years to carry out at least two of the

five major logistics functions: transport and delivery, storage, handling, packaging, and distribution

processing.

Cargo handling: Refers to the process of loading/unloading goods from a truck etc and moving them in

and out of logistics facilities.

Distribution processing: In addition to general work such as attaching price tags to apparel, packing

Services Service description and related subsidiaries/affiliates

The company delivers nationwide, with a fleet of 3,000 vehicles. The company will transport anything from an

entire train carriage to a single component.

→ SBS Logicom, SBS Freight Service

Long-distance container transport by rail

→ SBS Logicom

A specialist food transport service with three temperature bands (dry, chilled, frozen)

→ SBS Flec, SBS Zentsu, SBS Freight Service, SBS Transport

Comprehensive management contracts for logistics centers (both on an on-site and off-site basis)

→ SBS Logicom, SBS Flec, SBS Zentsu, Nippon Record Center

Integrated international logistics services, from customs clearance to onward arrangements and local logistics

→ SBS Logicom, SBS Global Network, Atlas Logistics

Processing such as assembly, labels, grouping, and wrapping

→ SBS Logicom, SBS Flec, SBS Zentsu, Nippon Record Center

Same day delivery of packages collected from within Tokyo Metropolis before noon to anywhere in Tokyo

Metropolis and the three surrounding prefectures (Saitama, Chiba, Kanagawa).

→ SBS Sokuhai

Delivery of products to co-operative union members and online shoppers

→ SBS Zentsu, SBS Sokuhai, SBS Flec

Removal services for offices, public agencies, universities, libraries and others, plus individuals

→ SBS Logicom, SBS Freight Service, SBS Transport

Focusing on vehicles and goods entering and exiting large buildings, and making them more efficient through

a unique system of collaborative delivery

→ SBS Logicom, SBS Transport

Investigation, analysis, and solutions for cost-cutting, lead time reduction, and streamlining

→ SBS Logicom

3PL Taking on the entirety of clients' logistics operations

(Third party logistics) → SBS Logicom, SBS Flec

Source: Company data, SR

Consulting

Distribution processing

Corporate express

deliveries

Same day home delivery

(individuals)

Corporate and individual

removals

Onsite logistics

Truck transport

Railway transport

Food logistics

Logistics center operation

International logistics

Page 13

SBS Holdings, Inc.(2384)

2014/04/10

http://www.sharedresearch.jp/ Copyright (C) Shared Research Inc. All Rights Reserved 13/50

SR Research Report

New Year’s and midsummer gifts in boxes, and replacing labels on imported goods, it can involve

outsourcing some tasks that are often handled on the production line, such as simple assembly and

finishing of products and shrink wrapping.

3PL business

The 3PL business accounts for around 40% of SBS’s logistics revenue, of which about 80% is from

comprehensive contracts where SBS performs all of the five major logistics functions (FY12/13). SBS

entered the 3PL market in 2006, and is aiming for JPY48.0bn in sales in FY12/14 (+4.1% YoY). The 3PL

clients tend to be new relationships rather than early existing customers (as of February 2013).

SBS maintains that its expertise is in achieving greater efficiencies of warehouse processes. The company

won the Logistics Rationalization Award for three years running through 2010 at the All-Japan Logistics

Improvement Case Study Convention by the Japan Institute of Logistics Systems. It also won the

Rationalization Endeavor Award in 2011. In 2008, the institute praised improvements in SBS’s food

distribution in-warehouse work flow as “improved work flow due to layout changes and increased

productivity due to product quality improvements.” In 2010, the institute presented the company with an

award for “reducing inventory held in storage for just-in-time shipments.”

The key customers in this segment are BALS Corp Inc (since June 2009), with annual revenue of around

JPY1.8bn (FY12/12) and Shimachu Co., Ltd. (since June 2013, TSE1: 8184), with annual revenue of

around JPY1.3bn (FY12/13).

The items in BALS’ Francfranc and other brands’ lineup are mainly interior accessories and furniture made

in China. The merchandise is delivered, inspected and temporarily stored at SBS’s logistics centers. It is

subsequently sorted, prepared for distribution and packed on order for delivery to over 100 domestic

stores. For Shimachu, SBS created a logistics center specifically for Shimachu products and sorts,

prepares for distribution and packs (on a per-store basis by delivery time) furniture, interior goods and

DIY materials from vendors which it then distributes to around 50 Shimachu stores nationwide. Targets

for new 3PL customers will be focused on the following categories: catalog sales; internet sales;

household goods; drinks; chilled and frozen.

Food distribution business

SBS does not disclose sales of the food distribution business, but it composes over 60% of sales of the

distribution business overall. Food distribution, which is highly specialized, is divided into frozen food,

chilled food, and room-temperature food. Frozen food encompasses instant rice and noodles dishes, ice

cream, cakes and other confectionery, and frozen meat and fish. Chilled food is primarily composed of

cheeses, butter, and other dairy products; beverages and yogurt; soy-based products; ham and

sausages; and other foods typically consumed on a regular basis. The core subsidiary engaged in this

business is SBS Flec (FY12/12 sales: JPY41.9bn, 33% of group sales; formerly a logistics subsidiary of

Snow Brand). SBS Flec has a nationwide sales network that can deliver large-lot simultaneous shipments

of dairy products anywhere in Japan, but it is also capable of handling frequent small-lot deliveries

through its delivery network, which is capable of all three temperature schemes. Concerning the frozen

3PL Sales

FY12/10 FY12/11 FY12/12 FY12/13 FY12/13

JPYbn 35.4 42.3 44.3 46.1 48.0

YoY 10.5% 19.5% 4.7% 4.1% 4.1%

Figures may differ from company materials due to differences in rounding methods

Source: Company data, SR

Page 14

SBS Holdings, Inc.(2384)

2014/04/10

http://www.sharedresearch.jp/ Copyright (C) Shared Research Inc. All Rights Reserved 14/50

SR Research Report

and chilled foods distribution sector, SBS Flec consistently ranks within the top 5 players. SBS Zentsu

(FY12/12 sales: JPY14.3bn, 11% of group sales) has strength in delivering goods to consumer co-ops.

Serving as the main artery connecting the co-op logistics centers with delivery depots, it also delivers

fresh meats and produce directly to co-op member homes. SBS Zentsu is also a unique distribution

company in that it has acquired certification for subdivision of organic produce, allowing it to process and

distribute food as well. As food demand is insensitive to the ups and downs in the economic cycle,

shipment volumes tend to be stable.

Consumer cooperatives: collectives formed, owned, and managed by their members. Many cooperatives

exist to supply members with everyday goods—such as food and drink, cleaning products, and clothing—but

there are also cooperatives working in areas such as health, insurance, and housing. As of 2012, 586 co-ops

were members of the Japanese Consumers’ Co-Operative Union (source: The CO-OP Facts and Figures 2012,

Japanese Consumers’ Co-operative Union).

Fee structure in logistics

SBS charges fees in three different ways. The first is a per-load fee charging a certain amount per load

handled; second is a per-truck fee, where the customer is charged for the use of a whole truck; and third

is a value-based fee. For instance, under a per-truck contract, a two-ton truck with driver costs

JPY25,000/day; a four-ton truck, JPY32,000; and a 10-ton truck, JPY43,000 (February 2014). Fees may

vary with length of contract and distance travelled. The value-based fees are typically 3-5% of the retail

sales value of the goods that pass through SBS’s logistics facilities.

In the 3PL business, value-based fees are the norm. This is because it is easy for the shippers to

understand and because different industries have different logistics patterns (large one-off deliveries,

small frequent deliveries, store route deliveries and so on). Also the lot quantities vary, so it is possible to

display common prices across the shipping customer base with value-based fees. Since the shippers

dislike having distribution costs (including transport) becoming fixed costs, it is easy to get their

agreement for charges that rise with sales. However, in the 3PL business, some customers employ a mix

of per-load and per-truck fees for deliveries and value-based fees in the warehouse. Outside the 3PL

business, it appears that there are slightly more contracts on a per-truck basis than a per-load basis.

Major customers

In FY12/13 SBS had approximately 8,000 logistics customers. Food and beverage manufacturers and

wholesalers accounted for around 45% of the group’s sales. Megmilk Snow Brand is the main customer,

with sales of JPY13.2bn, or 12.6% of logistics segment sales. This was followed by consumer co-ops with

JPY9.9bn in sales, 9.4% of the segment total.

Page 15

SBS Holdings, Inc.(2384)

2014/04/10

http://www.sharedresearch.jp/ Copyright (C) Shared Research Inc. All Rights Reserved 15/50

SR Research Report

Company-owned trucks; drivers

Almost all SBS trucks are leased by SBS Finance to other group companies. Of the 2,700 trucks in the

group as of December 2013, around 75% were on five- to eight-year leases, with the remaining 25%

owned. Thirty-five percent were small (under five tons); 45% were medium (four tons) and 20% were

large. Small trucks under two tons are depreciated over three years; the rest over four years. Around 70%

of SBS’s trucks are five years old or older (FY12/12). With measures to for greater environmental

regulation in the industry, there is a trend for truck ages to fall.

The group as a whole hires 4,000-5,000 trucks every month, accounted for in vehicle-hire expenses.

Vehicle hire involves hiring a truck with driver from other transport companies. SBS Flec is uses about

3,000 trucks per month under long-term (units are years) contracts.

SBS’s truck drivers are either regular employees or contract employees. Contract employees are under

long-term contracts lasting several years. Under transport regulations set by the Road Transportation Act,

the employment of day laborer truck drivers is prohibited, as it is impossible to manage safety. In line with

other industry players, most of SBS’s drivers are over 40 years of age. The number of drivers is gradually

declining and there appears to be a shortage.

Property Management business: 4% share of sales, 64% share of operating profit

(FY13/12)

There are two divisions in the property management business: a rental business that leases the

company-owned facilities for use as warehouses, offices and residences, as well as the development

business, which develops and sells logistics facilities.

Sales by Industry

FY12/11 FY12/12

Food & Beverage Manufactures 27.8% 27.3%

Chemical 8.0% 8.8%

Cosmetics and Toiletries 2.5% 2.1%

Others 5.9% 7.2%

Food & Food Wholesalers 18.8% 18.3%

Other Wholesalers 2.5% 2.7%

co-op 9.5% 9.4%

Supermarkets 3.4% 3.7%

DIY Stores 3.5% 3.4%

Department Stores 2.5% 2.4%

Other retailers 4.6% 3.8%

Services 4.7% 4.6%

Real Estate 0.0% 0.0%

Others 6.2% 6.2%

Source: Company data, SR

FY12/10 FY12/11 FY12/12

Number of Drivers 2,104 2,081 2,033

Source: Company data, SR

Page 16

SBS Holdings, Inc.(2384)

2014/04/10

http://www.sharedresearch.jp/ Copyright (C) Shared Research Inc. All Rights Reserved 16/50

SR Research Report

Rental business

The rental business involves the rental of assets acquired by the company through M&A, and rental of

logistics facilities. Group companies such as SBS Logicom and SBS Transport that own real estate rent it to

third parties, mainly in the Tokyo Metro Area. The rental buildings are mainly used for logistics, although

there are also office buildings, residences and open land among them as well.

According to SBS, in FY12/13 the yield on rental properties (relative to then-current market values) was

5% for both offices and residential property, and 7.5% for logistics facilities. However, some of the

properties acquired through M&A have low book values. In FY12/12, the vacancy rate for offices and

residential were both under 3%. Because the offices are in prime urban locations, vacancy rates are low.

Most of the residential property is rented by companies for worker accommodation, so vacancy rates are

low there as well. For logistics facilities, those customers that only pay rent on warehouses are accounted

for in the property management business, but warehouse storage undertaken as part of 3PL activities is

accounted for by the logistics business. Warehouse rents vary by region, but SBS said that they average

around JPY3,000-JPY4,000/tsubo. Note: tsubo is a unit of area equating to about 3.3m2. As of February

2014, the company currently has over 50 rental properties which include land, warehouses, offices, and

residences. Book values of real estate acquired through M&A of subsidiaries are consolidated at market

values, and SR estimates the current value of these properties to be between JPY15.0bn and JPY20.0bn.

Development business

In 2004, SBS established A-Max, a real estate securitizer and developer, and made it a subsidiary. A-Max

and its subsidiaries are primarily responsible for planning and developing low-cost logistics facilities for

their corporate customers, mainly in the Tokyo Metro Area. The company aims for average annual returns

of 7.5%.

Business Business description and related subsidiaries/affiliates

Leasing out its facilities as offices, accommodation, and warehouses

→ SBS Logicom, A-Max

Developing and selling logistics facilities such as logistics centers (real estate securitization)

→ A-MAX

Source: Company data, SR

Rental business

Development business

Key rental properties

Shibuya Minamiguchi Building Minami-Shinjuku SK Building Iidabashi Building

Source: Company data, SR Inc.

Page 17

SBS Holdings, Inc.(2384)

2014/04/10

http://www.sharedresearch.jp/ Copyright (C) Shared Research Inc. All Rights Reserved 17/50

SR Research Report

The company’s real estate development fundamentally differs from other logistics facilities developers

such as Prologis and Mitsui Real Estate in one key area. As opposed to developing properties first and

then seeking tenants, SBS acquires contracts with key tenants before development begins. The company

also does not determine rents based upon land prices, but conducts the process in reverse; after

determining the market price for rents in a given area, SBS will then decide on how much to pay for land

acquisition and construction costs. Making accurate assessments of future tenant activity allows facilities

development to remain profitable, even during downturns in the property management sector. The

company also works in tandem with key customers to seek approval under the Act on Advancement of

Integration and Streamlining of Distribution Business for development of facilities in prime locations near

expressway interchanges. SBS can also acquire land at lower prices due to its ability to participate in

auctions that are limited to participants with possession of port operator licenses or warehousing licenses.

These unique traits allow the company to develop facilities in areas that are inaccessible to ordinary real

estate developers.

The company’s ability for comprehensive development of logistics facilities is a strength when seeking

new 3PL clients. In the 3PL business, project proposals to customers are differentiated from those of

competitors through a multi-faceted approach, outlining ideal locations and specifications at rental rates

that are lower than market prices. SBS believes that the quality of logistics facilities is the main factor in

determining the total cost of 3PL.

Deciding on whether or not to move forward with development relies primarily on being able to fill at least

half of the floor space with key clients. The remaining floor space is used for new customers, or for

customers currently renting in a separate SBS facility to consolidate operations. In this way, facilities will

be fully operational and rented immediately after construction is complete. As a result, the company’s

logistics facilities are lower risk than facilities developed by real estate developers. The quality and credit

of tenants are also desirable, and such tenants can be expected to provide the company with stable cash

flows over the medium to long term.

Contract periods are generally ten years or longer, and interest rates are fixed. However, rental rates may

be adjusted in the event of a change in interest rates.

Aside from a rental revenue, which provides a stable yield of around 7.5% per year, the company also

counts operational revenue as a source of income. Operations cover actions undertaken at logistics

facilities such as shipping and receiving, storage, and distribution processing. SBS is also contracted for

deliveries to and from the logistics facilities.

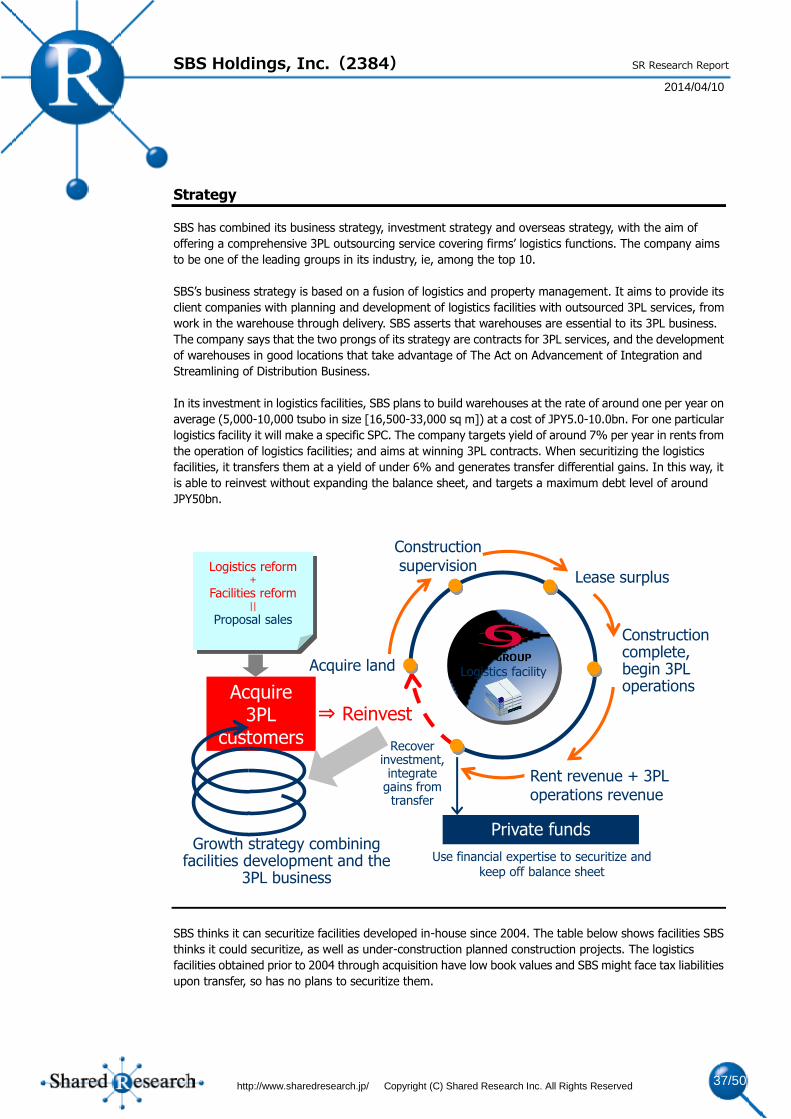

In order to prevent buildup on its balance sheet from logistics facilities development, SBS has raised

capital through securitization of facilities from an early stage. From 2005 until 2013, total investment in

facilities development totaled JPY50.0bn. During this period, the company transferred (securitized) five

facilities to recover JPY40.0bn of this investment. Of the JPY40.0bn, the gain from transfer was JPY10.0bn.

By transferring at below 6%, the coupon on warehouse rentals, SBS collected a gain on transfer in

addition to the gain on sales. Recovered funds and proceeds from the transfer are then used to invest in

development for the next facility, and the virtuous cycle begins anew. The process is an important

element for the company to sustain growth despite a comparatively weak financial standing.

SBS, with its high level of financial expertise, has a business model that integrates finance and logistics to

create a platform for sustained growth. Specifically, this involves logistics facilities development and

corresponding expansion of the logistics (3PL) business. This type of business model is unique to SBS and

has not been attempted by any other firm.

Page 18

SBS Holdings, Inc.(2384)

2014/04/10

http://www.sharedresearch.jp/ Copyright (C) Shared Research Inc. All Rights Reserved 18/50

SR Research Report

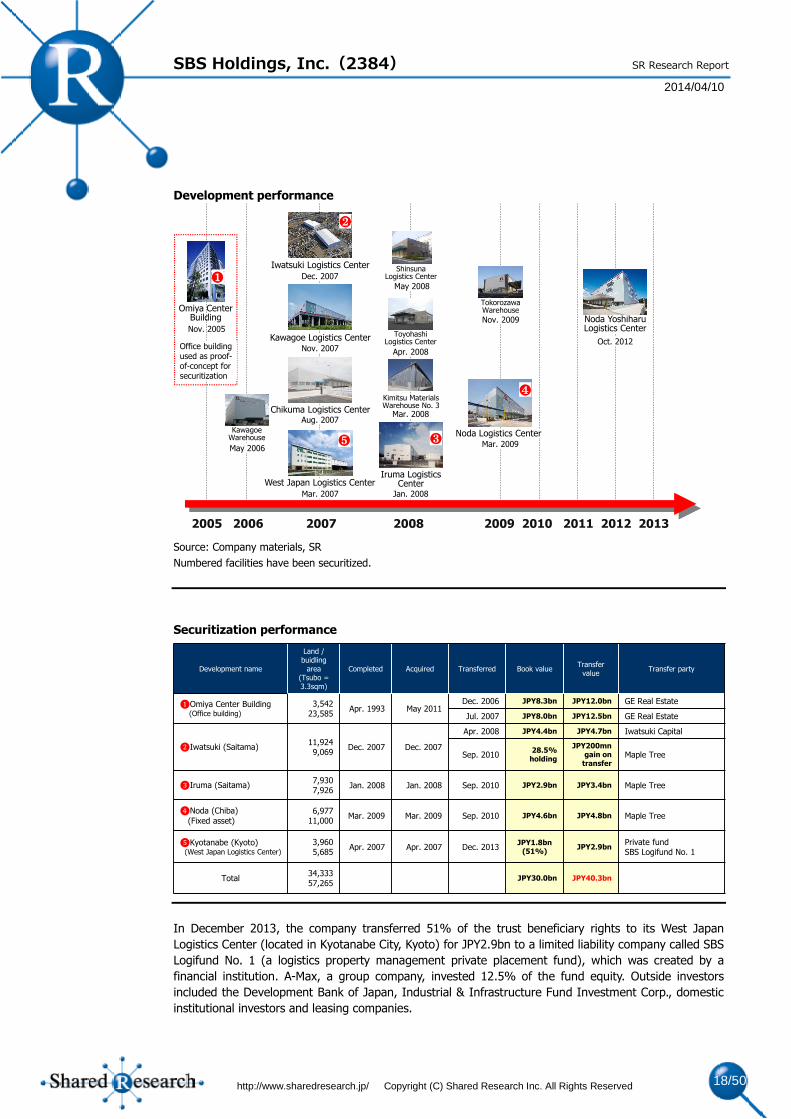

Development performance

Source: Company materials, SR

Numbered facilities have been securitized.

Securitization performance

In December 2013, the company transferred 51% of the trust beneficiary rights to its West Japan

Logistics Center (located in Kyotanabe City, Kyoto) for JPY2.9bn to a limited liability company called SBS

Logifund No. 1 (a logistics property management private placement fund), which was created by a

financial institution. A-Max, a group company, invested 12.5% of the fund equity. Outside investors

included the Development Bank of Japan, Industrial & Infrastructure Fund Investment Corp., domestic

institutional investors and leasing companies.

2005 2006 2007 2008 2009 2010 2011 2012 2013

Kawagoe Warehouse

May 2006

West Japan Logistics Center

Mar. 2007

Chikuma Logistics CenterAug. 2007

Kawagoe Logistics CenterNov. 2007

Iwatsuki Logistics Center

Dec. 2007

Iruma Logistics Center

Jan. 2008

Kimitsu Materials Warehouse No. 3

Mar. 2008

Toyohashi Logistics Center

Apr. 2008

Noda Logistics CenterMar. 2009

Tokorozawa Warehouse

Nov. 2009 Noda Yoshiharu Logistics Center

Oct. 2012

❺

❷

❸

❹

Omiya Center Building

Nov. 2005

❶

Office building used as proof-of-concept for securitization

ShinsunaLogistics Center

May 2008

Development name

Land / buidling

area (Tsubo = 3.3sqm)

Completed Acquired Transferred Book valueTransfer

valueTransfer party

❶Omiya Center Building(Office building)

3,54223,585

Apr. 1993 May 2011Dec. 2006 JPY8.3bn JPY12.0bn GE Real Estate

Jul. 2007 JPY8.0bn JPY12.5bn GE Real Estate

❷Iwatsuki (Saitama)11,9249,069

Dec. 2007 Dec. 2007

Apr. 2008 JPY4.4bn JPY4.7bn Iwatsuki Capital

Sep. 201028.5%

holding

JPY200mn gain on

transferMaple Tree

❸Iruma (Saitama)7,9307,926

Jan. 2008 Jan. 2008 Sep. 2010 JPY2.9bn JPY3.4bn Maple Tree

❹Noda (Chiba)

(Fixed asset)6,977

11,000Mar. 2009 Mar. 2009 Sep. 2010 JPY4.6bn JPY4.8bn Maple Tree

❺Kyotanabe (Kyoto)(West Japan Logistics Center)

3,9605,685

Apr. 2007 Apr. 2007 Dec. 2013JPY1.8bn

(51%)JPY2.9bn

Private fundSBS Logifund No. 1

Total34,33357,265

JPY30.0bn JPY40.3bn

Page 19

SBS Holdings, Inc.(2384)

2014/04/10

http://www.sharedresearch.jp/ Copyright (C) Shared Research Inc. All Rights Reserved 19/50

SR Research Report

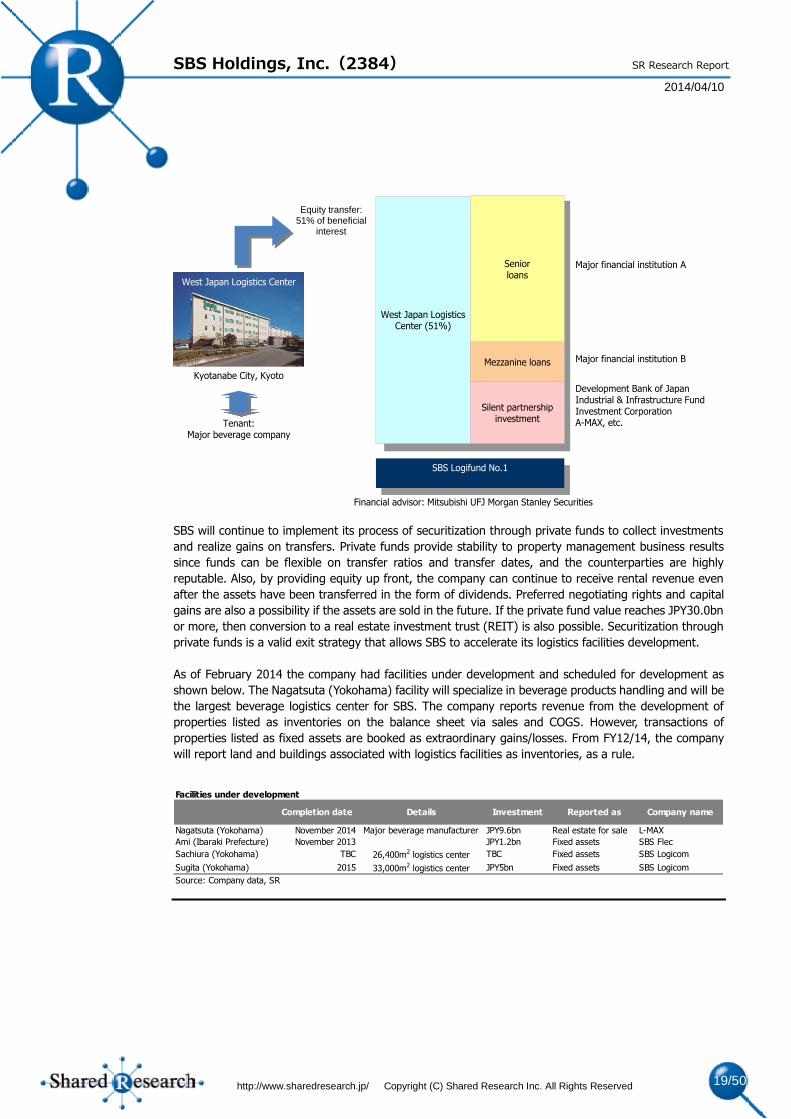

SBS will continue to implement its process of securitization through private funds to collect investments

and realize gains on transfers. Private funds provide stability to property management business results

since funds can be flexible on transfer ratios and transfer dates, and the counterparties are highly

reputable. Also, by providing equity up front, the company can continue to receive rental revenue even

after the assets have been transferred in the form of dividends. Preferred negotiating rights and capital

gains are also a possibility if the assets are sold in the future. If the private fund value reaches JPY30.0bn

or more, then conversion to a real estate investment trust (REIT) is also possible. Securitization through

private funds is a valid exit strategy that allows SBS to accelerate its logistics facilities development.

As of February 2014 the company had facilities under development and scheduled for development as

shown below. The Nagatsuta (Yokohama) facility will specialize in beverage products handling and will be

the largest beverage logistics center for SBS. The company reports revenue from the development of

properties listed as inventories on the balance sheet via sales and COGS. However, transactions of

properties listed as fixed assets are booked as extraordinary gains/losses. From FY12/14, the company

will report land and buildings associated with logistics facilities as inventories, as a rule.

Tenant:Major beverage company

Equity transfer:51% of beneficial

interest

West Japan Logistics Center (51%)

Seniorloans

Silent partnership investment

Mezzanine loans

SBS Logifund No.1

Major financial institution B

Development Bank of JapanIndustrial & Infrastructure Fund Investment CorporationA-MAX, etc.

Major financial institution A

Financial advisor: Mitsubishi UFJ Morgan Stanley Securities

West Japan Logistics Center

Kyotanabe City, Kyoto

Facilities under development

Completion date Details Investment Reported as Company name

Nagatsuta (Yokohama) November 2014 Major beverage manufacturer JPY9.6bn Real estate for sale L-MAX

Ami (Ibaraki Prefecture) November 2013 JPY1.2bn Fixed assets SBS Flec

Sachiura (Yokohama) TBC 26,400m2 logistics center TBC Fixed assets SBS Logicom

Sugita (Yokohama) 2015 33,000m2 logistics center JPY5bn Fixed assets SBS Logicom

Source: Company data, SR

Page 20

SBS Holdings, Inc.(2384)

2014/04/10

http://www.sharedresearch.jp/ Copyright (C) Shared Research Inc. All Rights Reserved 20/50

SR Research Report

SBS plans to develop logistics facilities in Asian locations such as Thailand, Malaysia, India and Vietnam. It

is constructing its first overseas distribution center in Thailand (the center is scheduled to begin

operations in June 2014). Beginning in December 2014, SBS aims to use its ties with local partners to

develop more facilities, providing logistics centers with Japanese quality not only to Japanese

corporations overseas, but to local companies as well.

Other businesses: share of sales, 4%; share of operating profit, 5% (FY12/13)

Other businesses comprise financial (insurance agency); marketing (sales support for client companies);

personnel (recruiting service); and environmental businesses (industrial waste recycling). SBS believes

that these businesses ancillary to logistics enable it to offer a one-stop shopping service to its logistics

The Nagatsuta Project

Source: Company data, SR

Thai Logistics Center Project

Source: Company data, SR

Page 21

SBS Holdings, Inc.(2384)

2014/04/10

http://www.sharedresearch.jp/ Copyright (C) Shared Research Inc. All Rights Reserved 21/50

SR Research Report

customers and differentiate it from competition.

Since FY12/13 SBS has operated 5-megawatt solar power generation facilities on the roofs of logistics

centers in Shibayama, Noda, Kawagoe and Chikuma in order to make full use of use its locations and

logistics facility rooftops. This generated sales of around JPY100m in FY12/13; in 2014, the company

planned to commence rooftop solar power generation at its Kyotanabe facility, and in 2015, the Nagatsuta

logistics facility.

Sales offices by region

SBS has most of its sales offices in the Tokyo Metro Area, where freight shipments are relatively firm;

most of its operations are in and around Tokyo as well. Tokyo and the three neighboring prefectures

account for 58.8% of sales, and the wider Kanto area for 66.3%. Next comes Kansai with 7.4% and

Chubu with 6.6%.

Business Business description and related subsidiaries/affiliates

PersonnelSBS Staff Co., Ltd. provides a staff dispatch service, sending out staff to handle labor needs in clients'

logistics facilities, as well as staffing needs in other fields, such as events and removals. The company also

provides a general labor dispatch service.

EnvironmentSBS Support Logi Co., Ltd. provides intermediary clean-up and collection services for industrial waste, as well

as recycling resources.

MarketingMarketing Partner Co., Ltd. and PAM Co., Ltd. and its subsidiaries act as an advertising agency, supporting

client firms' sales activities, and producing catalogs and websites where necessary for new product

promotional campains. The company also runs an e-commerce business.

Solar power generationSBS Logicom Co., Ltd. maximizes benefits received from existing assets, while at the same time, working to

reduce greenhouse emissions and expand use of renewable energy sources. As a way to move closer to a

low-carbon society, it has implemented solar power generation as a key initiative.

OthersSBS Finance Co., Ltd. runs an insurance agency business, a leasing business (mainly truck rentals), and a tire

and fuel sales business. Large group purchases mean the company has a cheap, stable supply of fuel and

tires.

Source: Company data, SR

Solar panels on the roof of the Noda Yoshiharu Logistics Center

Source: Company data, SR

Page 22

SBS Holdings, Inc.(2384)

2014/04/10

http://www.sharedresearch.jp/ Copyright (C) Shared Research Inc. All Rights Reserved 22/50

SR Research Report

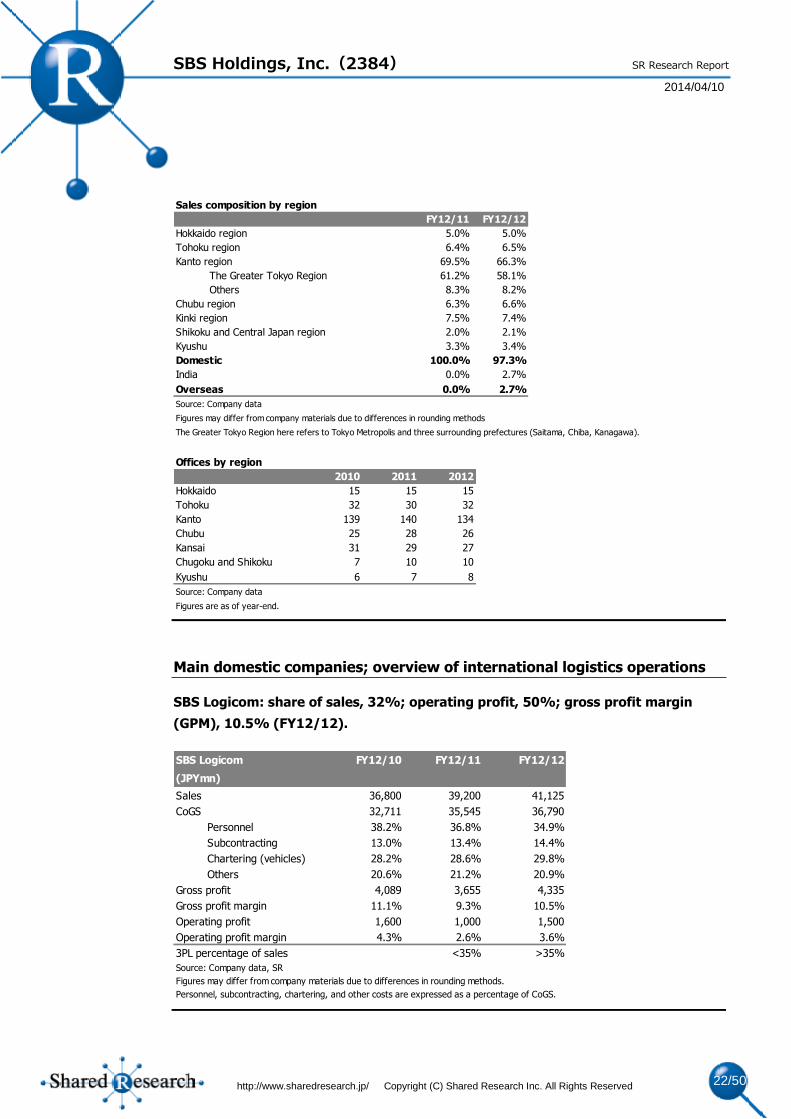

Main domestic companies; overview of international logistics operations

SBS Logicom: share of sales, 32%; operating profit, 50%; gross profit margin

(GPM), 10.5% (FY12/12).

Sales composition by region

FY12/11 FY12/12

Hokkaido region 5.0% 5.0%

Tohoku region 6.4% 6.5%

Kanto region 69.5% 66.3%

The Greater Tokyo Region 61.2% 58.1%

Others 8.3% 8.2%

Chubu region 6.3% 6.6%

Kinki region 7.5% 7.4%

Shikoku and Central Japan region 2.0% 2.1%

Kyushu 3.3% 3.4%

Domestic 100.0% 97.3%

India 0.0% 2.7%

Overseas 0.0% 2.7%

Source: Company data

Figures may differ from company materials due to differences in rounding methods

The Greater Tokyo Region here refers to Tokyo Metropolis and three surrounding prefectures (Saitama, Chiba, Kanagawa).

Offices by region

2010 2011 2012

Hokkaido 15 15 15

Tohoku 32 30 32

Kanto 139 140 134

Chubu 25 28 26

Kansai 31 29 27

Chugoku and Shikoku 7 10 10

Kyushu 6 7 8

Source: Company data

Figures are as of year-end.

SBS Logicom FY12/10 FY12/11 FY12/12

(JPYmn)

Sales 36,800 39,200 41,125

CoGS 32,711 35,545 36,790

Personnel 38.2% 36.8% 34.9%

Subcontracting 13.0% 13.4% 14.4%

Chartering (vehicles) 28.2% 28.6% 29.8%

Others 20.6% 21.2% 20.9%

Gross profit 4,089 3,655 4,335

Gross profit margin 11.1% 9.3% 10.5%

Operating profit 1,600 1,000 1,500

Operating profit margin 4.3% 2.6% 3.6%

3PL percentage of sales <35% >35%

Source: Company data, SR

Figures may differ from company materials due to differences in rounding methods.

Personnel, subcontracting, chartering, and other costs are expressed as a percentage of CoGS.

Page 23

SBS Holdings, Inc.(2384)

2014/04/10

http://www.sharedresearch.jp/ Copyright (C) Shared Research Inc. All Rights Reserved 23/50

SR Research Report

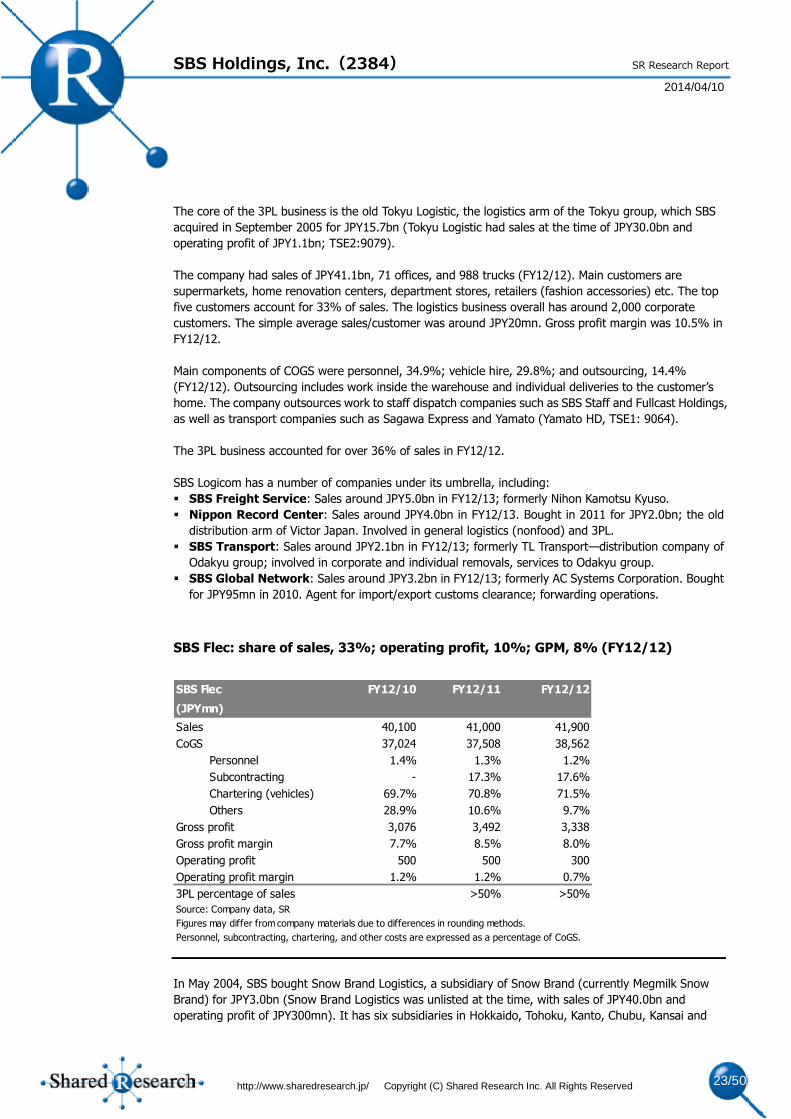

The core of the 3PL business is the old Tokyu Logistic, the logistics arm of the Tokyu group, which SBS

acquired in September 2005 for JPY15.7bn (Tokyu Logistic had sales at the time of JPY30.0bn and

operating profit of JPY1.1bn; TSE2:9079).

The company had sales of JPY41.1bn, 71 offices, and 988 trucks (FY12/12). Main customers are

supermarkets, home renovation centers, department stores, retailers (fashion accessories) etc. The top

five customers account for 33% of sales. The logistics business overall has around 2,000 corporate

customers. The simple average sales/customer was around JPY20mn. Gross profit margin was 10.5% in

FY12/12.

Main components of COGS were personnel, 34.9%; vehicle hire, 29.8%; and outsourcing, 14.4%

(FY12/12). Outsourcing includes work inside the warehouse and individual deliveries to the customer’s

home. The company outsources work to staff dispatch companies such as SBS Staff and Fullcast Holdings,

as well as transport companies such as Sagawa Express and Yamato (Yamato HD, TSE1: 9064).

The 3PL business accounted for over 36% of sales in FY12/12.

SBS Logicom has a number of companies under its umbrella, including:

SBS Freight Service: Sales around JPY5.0bn in FY12/13; formerly Nihon Kamotsu Kyuso.

Nippon Record Center: Sales around JPY4.0bn in FY12/13. Bought in 2011 for JPY2.0bn; the old

distribution arm of Victor Japan. Involved in general logistics (nonfood) and 3PL.

SBS Transport: Sales around JPY2.1bn in FY12/13; formerly TL Transport—distribution company of

Odakyu group; involved in corporate and individual removals, services to Odakyu group.

SBS Global Network: Sales around JPY3.2bn in FY12/13; formerly AC Systems Corporation. Bought

for JPY95mn in 2010. Agent for import/export customs clearance; forwarding operations.

SBS Flec: share of sales, 33%; operating profit, 10%; GPM, 8% (FY12/12)

In May 2004, SBS bought Snow Brand Logistics, a subsidiary of Snow Brand (currently Megmilk Snow

Brand) for JPY3.0bn (Snow Brand Logistics was unlisted at the time, with sales of JPY40.0bn and

operating profit of JPY300mn). It has six subsidiaries in Hokkaido, Tohoku, Kanto, Chubu, Kansai and

SBS Flec FY12/10 FY12/11 FY12/12

(JPYmn)

Sales 40,100 41,000 41,900

CoGS 37,024 37,508 38,562

Personnel 1.4% 1.3% 1.2%

Subcontracting - 17.3% 17.6%

Chartering (vehicles) 69.7% 70.8% 71.5%

Others 28.9% 10.6% 9.7%

Gross profit 3,076 3,492 3,338

Gross profit margin 7.7% 8.5% 8.0%

Operating profit 500 500 300

Operating profit margin 1.2% 1.2% 0.7%

3PL percentage of sales >50% >50%

Source: Company data, SR

Figures may differ from company materials due to differences in rounding methods.

Personnel, subcontracting, chartering, and other costs are expressed as a percentage of CoGS.

Page 24

SBS Holdings, Inc.(2384)

2014/04/10

http://www.sharedresearch.jp/ Copyright (C) Shared Research Inc. All Rights Reserved 24/50

SR Research Report

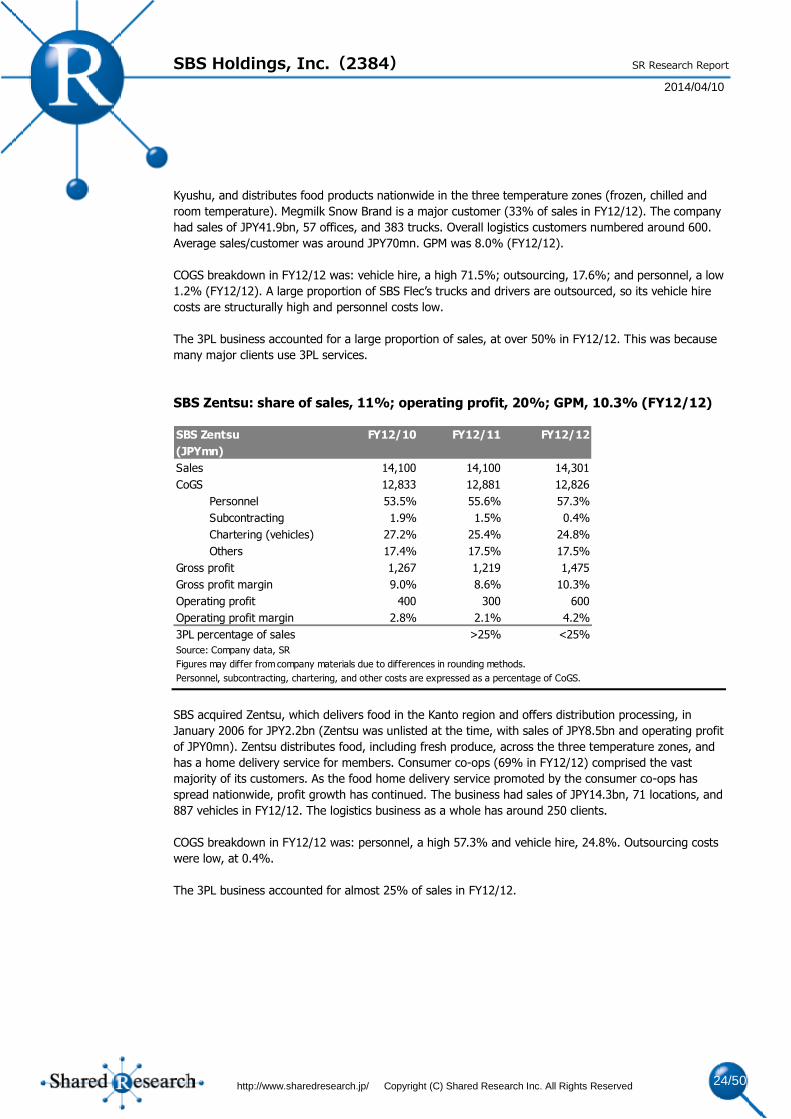

Kyushu, and distributes food products nationwide in the three temperature zones (frozen, chilled and

room temperature). Megmilk Snow Brand is a major customer (33% of sales in FY12/12). The company

had sales of JPY41.9bn, 57 offices, and 383 trucks. Overall logistics customers numbered around 600.

Average sales/customer was around JPY70mn. GPM was 8.0% (FY12/12).

COGS breakdown in FY12/12 was: vehicle hire, a high 71.5%; outsourcing, 17.6%; and personnel, a low

1.2% (FY12/12). A large proportion of SBS Flec’s trucks and drivers are outsourced, so its vehicle hire

costs are structurally high and personnel costs low.

The 3PL business accounted for a large proportion of sales, at over 50% in FY12/12. This was because

many major clients use 3PL services.

SBS Zentsu: share of sales, 11%; operating profit, 20%; GPM, 10.3% (FY12/12)

SBS acquired Zentsu, which delivers food in the Kanto region and offers distribution processing, in

January 2006 for JPY2.2bn (Zentsu was unlisted at the time, with sales of JPY8.5bn and operating profit

of JPY0mn). Zentsu distributes food, including fresh produce, across the three temperature zones, and

has a home delivery service for members. Consumer co-ops (69% in FY12/12) comprised the vast

majority of its customers. As the food home delivery service promoted by the consumer co-ops has

spread nationwide, profit growth has continued. The business had sales of JPY14.3bn, 71 locations, and

887 vehicles in FY12/12. The logistics business as a whole has around 250 clients.

COGS breakdown in FY12/12 was: personnel, a high 57.3% and vehicle hire, 24.8%. Outsourcing costs

were low, at 0.4%.

The 3PL business accounted for almost 25% of sales in FY12/12.

SBS Zentsu FY12/10 FY12/11 FY12/12

(JPYmn)

Sales 14,100 14,100 14,301

CoGS 12,833 12,881 12,826

Personnel 53.5% 55.6% 57.3%

Subcontracting 1.9% 1.5% 0.4%

Chartering (vehicles) 27.2% 25.4% 24.8%

Others 17.4% 17.5% 17.5%

Gross profit 1,267 1,219 1,475

Gross profit margin 9.0% 8.6% 10.3%

Operating profit 400 300 600

Operating profit margin 2.8% 2.1% 4.2%

3PL percentage of sales >25% <25%

Source: Company data, SR

Figures may differ from company materials due to differences in rounding methods.

Personnel, subcontracting, chartering, and other costs are expressed as a percentage of CoGS.

Page 25

SBS Holdings, Inc.(2384)

2014/04/10

http://www.sharedresearch.jp/ Copyright (C) Shared Research Inc. All Rights Reserved 25/50

SR Research Report

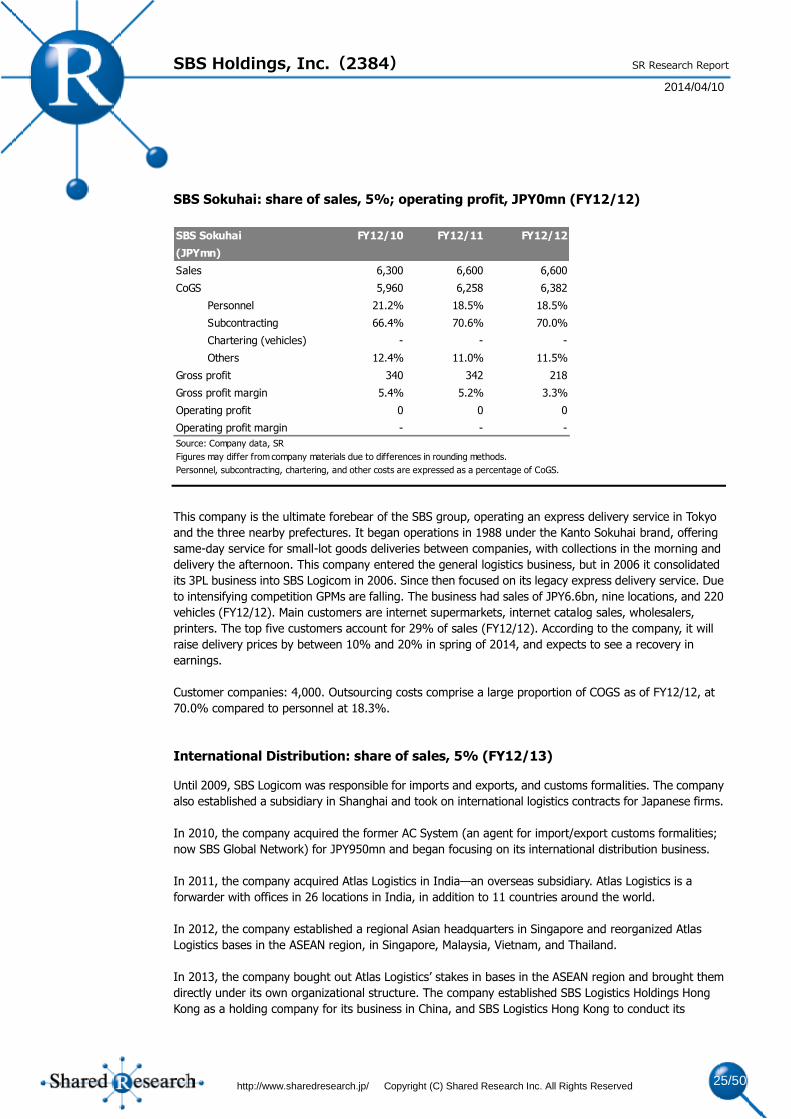

SBS Sokuhai: share of sales, 5%; operating profit, JPY0mn (FY12/12)

This company is the ultimate forebear of the SBS group, operating an express delivery service in Tokyo

and the three nearby prefectures. It began operations in 1988 under the Kanto Sokuhai brand, offering

same-day service for small-lot goods deliveries between companies, with collections in the morning and

delivery the afternoon. This company entered the general logistics business, but in 2006 it consolidated

its 3PL business into SBS Logicom in 2006. Since then focused on its legacy express delivery service. Due

to intensifying competition GPMs are falling. The business had sales of JPY6.6bn, nine locations, and 220

vehicles (FY12/12). Main customers are internet supermarkets, internet catalog sales, wholesalers,

printers. The top five customers account for 29% of sales (FY12/12). According to the company, it will

raise delivery prices by between 10% and 20% in spring of 2014, and expects to see a recovery in

earnings.

Customer companies: 4,000. Outsourcing costs comprise a large proportion of COGS as of FY12/12, at

70.0% compared to personnel at 18.3%.

International Distribution: share of sales, 5% (FY12/13)

Until 2009, SBS Logicom was responsible for imports and exports, and customs formalities. The company

also established a subsidiary in Shanghai and took on international logistics contracts for Japanese firms.

In 2010, the company acquired the former AC System (an agent for import/export customs formalities;

now SBS Global Network) for JPY950mn and began focusing on its international distribution business.

In 2011, the company acquired Atlas Logistics in India—an overseas subsidiary. Atlas Logistics is a

forwarder with offices in 26 locations in India, in addition to 11 countries around the world.

In 2012, the company established a regional Asian headquarters in Singapore and reorganized Atlas

Logistics bases in the ASEAN region, in Singapore, Malaysia, Vietnam, and Thailand.

In 2013, the company bought out Atlas Logistics’ stakes in bases in the ASEAN region and brought them

directly under its own organizational structure. The company established SBS Logistics Holdings Hong

Kong as a holding company for its business in China, and SBS Logistics Hong Kong to conduct its

SBS Sokuhai FY12/10 FY12/11 FY12/12

(JPYmn)

Sales 6,300 6,600 6,600

CoGS 5,960 6,258 6,382

Personnel 21.2% 18.5% 18.5%

Subcontracting 66.4% 70.6% 70.0%

Chartering (vehicles) - - -

Others 12.4% 11.0% 11.5%

Gross profit 340 342 218

Gross profit margin 5.4% 5.2% 3.3%

Operating profit 0 0 0

Operating profit margin - - -

Source: Company data, SR

Figures may differ from company materials due to differences in rounding methods.

Personnel, subcontracting, chartering, and other costs are expressed as a percentage of CoGS.

Page 26

SBS Holdings, Inc.(2384)

2014/04/10

http://www.sharedresearch.jp/ Copyright (C) Shared Research Inc. All Rights Reserved 26/50

SR Research Report

operations in Hong Kong. Domestically, the company also combined SBS Logicom’s international

distribution organization with SBS Global Network. The company also changed its structure to allow it to

be at the center of growth in the international distribution business.

Forwarder: A freight shipping company. Receives freight from the owner, and uses a third party’s

transportation services (ship, airplane, train, truck) to ship the goods.

The company is preparing a supply-chain management network to serve clients at its offices in four

ASEAN countries. In countries such as Thailand it offers integrated cross-border international logistics

services, ranging from the procurement of raw materials for electronic components to the transportation

of finished products. The company also plans to bring its first overseas logistics center online in Thailand

in June 2014 (two warehouses of 3,000 tsubo [9,900 sq m]). The company was in negotiations with

Japanese electronics and auto manufacturers regarding their logistics needs in the region. It has also

begun offering forwarding, warehousing and customs clearing services to Japanese companies operating

in Hong Kong and South Central China. The company’s business in India is subject to a number of

conditions specific to that country. Therefore, the company plans to use Atlas Logistics’ network within

India and abroad to expand its forwarding and cargo operations (the company acquired Atlas Logistics for

JPY1.3bn in 2011). According to the company, growth in the Indian domestic logistics market is viable if it

leverages its expertise in the transport, warehousing and 3PL businesses.

The company’s local subsidiaries in China and the ASEAN region are not classed as consolidated

subsidiaries. Atlas Logistics is the only consolidated overseas subsidiary.

Main group companies

SBS uses a holding company structure. As of December 2013, it was composed of SBS and 40 subsidiaries

(including 23 consolidated subsidiaries), and eight affiliates (including one equity method affiliate).

The table below shows the group companies other than the four key companies. SBS’s stake is in

brackets.

Page 27

SBS Holdings, Inc.(2384)

2014/04/10

http://www.sharedresearch.jp/ Copyright (C) Shared Research Inc. All Rights Reserved 27/50

SR Research Report

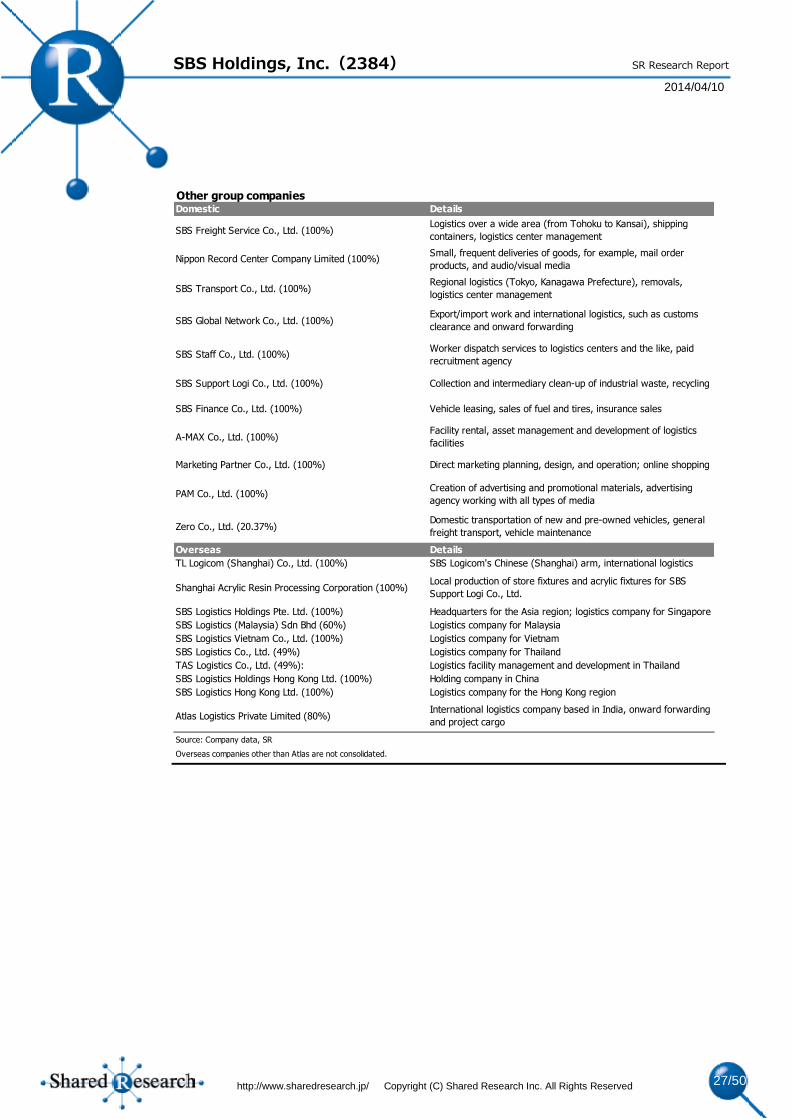

Other group companies Domestic Details

SBS Freight Service Co., Ltd. (100%)Logistics over a wide area (from Tohoku to Kansai), shipping

containers, logistics center management

Nippon Record Center Company Limited (100%)Small, frequent deliveries of goods, for example, mail order

products, and audio/visual media

SBS Transport Co., Ltd. (100%)Regional logistics (Tokyo, Kanagawa Prefecture), removals,

logistics center management

SBS Global Network Co., Ltd. (100%)Export/import work and international logistics, such as customs

clearance and onward forwarding

SBS Staff Co., Ltd. (100%)Worker dispatch services to logistics centers and the like, paid

recruitment agency

SBS Support Logi Co., Ltd. (100%) Collection and intermediary clean-up of industrial waste, recycling

SBS Finance Co., Ltd. (100%) Vehicle leasing, sales of fuel and tires, insurance sales

A-MAX Co., Ltd. (100%)Facility rental, asset management and development of logistics

facilities

Marketing Partner Co., Ltd. (100%) Direct marketing planning, design, and operation; online shopping

PAM Co., Ltd. (100%)Creation of advertising and promotional materials, advertising

agency working with all types of media

Zero Co., Ltd. (20.37%)Domestic transportation of new and pre-owned vehicles, general

freight transport, vehicle maintenance

Overseas Details

TL Logicom (Shanghai) Co., Ltd. (100%) SBS Logicom's Chinese (Shanghai) arm, international logistics

Shanghai Acrylic Resin Processing Corporation (100%)Local production of store fixtures and acrylic fixtures for SBS

Support Logi Co., Ltd.

SBS Logistics Holdings Pte. Ltd. (100%) Headquarters for the Asia region; logistics company for Singapore

SBS Logistics (Malaysia) Sdn Bhd (60%) Logistics company for Malaysia

SBS Logistics Vietnam Co., Ltd. (100%) Logistics company for Vietnam

SBS Logistics Co., Ltd. (49%) Logistics company for Thailand

TAS Logistics Co., Ltd. (49%): Logistics facility management and development in Thailand

SBS Logistics Holdings Hong Kong Ltd. (100%) Holding company in China

SBS Logistics Hong Kong Ltd. (100%) Logistics company for the Hong Kong region

Atlas Logistics Private Limited (80%)International logistics company based in India, onward forwarding

and project cargo

Source: Company data, SR

Overseas companies other than Atlas are not consolidated.

Page 28

SBS Holdings, Inc.(2384)

2014/04/10

http://www.sharedresearch.jp/ Copyright (C) Shared Research Inc. All Rights Reserved 28/50

SR Research Report

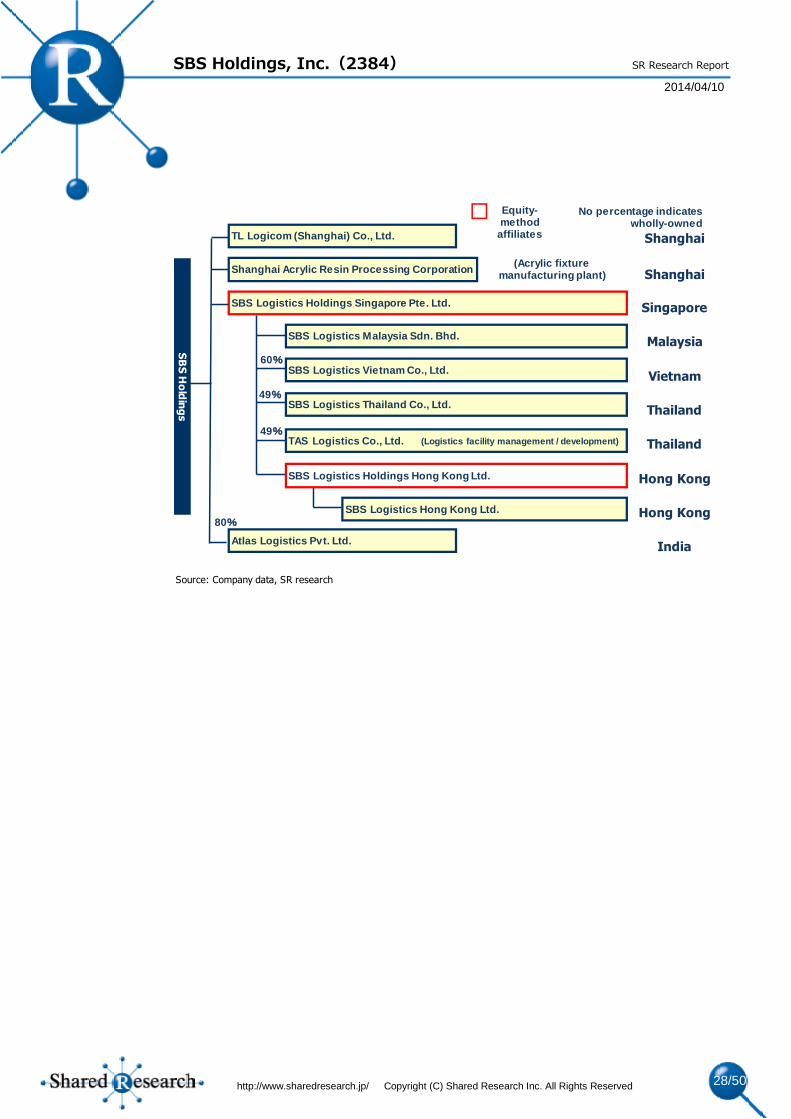

Source: Company data, SR research

Equity-method

affiliatesTL Logicom (Shanghai) Co., Ltd.

SBS Logistics Holdings Singapore Pte. Ltd.

SBS Logistics Vietnam Co., Ltd.

SBS Logistics Thailand Co., Ltd.

Atlas Logistics Pvt. Ltd.

Shanghai Acrylic Resin Processing Corporation

SBS Logistics Hong Kong Ltd.

SBS Logistics Malaysia Sdn. Bhd.

TAS Logistics Co., Ltd.

Shanghai

Shanghai

Singapore

Malaysia

Vietnam

Thailand

Thailand

Hong Kong

Hong Kong

India

SB

S H

old

ing

s

(Acrylic fixture manufacturing plant)

49%

80%

60%

No percentage indicates wholly-owned

49%(Logistics facility management / development)

SBS Logistics Holdings Hong Kong Ltd.

Page 29

SBS Holdings, Inc.(2384)

2014/04/10

http://www.sharedresearch.jp/ Copyright (C) Shared Research Inc. All Rights Reserved 29/50

SR Research Report

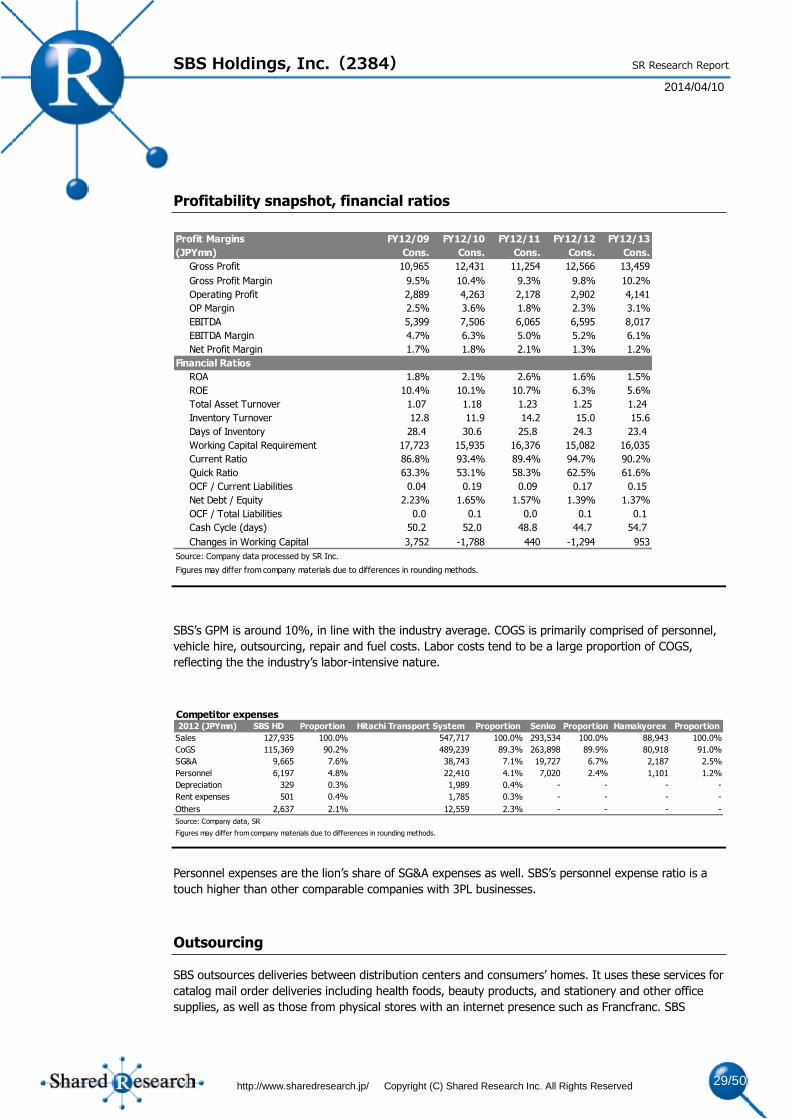

Profitability snapshot, financial ratios

SBS’s GPM is around 10%, in line with the industry average. COGS is primarily comprised of personnel,

vehicle hire, outsourcing, repair and fuel costs. Labor costs tend to be a large proportion of COGS,

reflecting the the industry’s labor-intensive nature.

Personnel expenses are the lion’s share of SG&A expenses as well. SBS’s personnel expense ratio is a

touch higher than other comparable companies with 3PL businesses.

Outsourcing

SBS outsources deliveries between distribution centers and consumers’ homes. It uses these services for

catalog mail order deliveries including health foods, beauty products, and stationery and other office

supplies, as well as those from physical stores with an internet presence such as Francfranc. SBS

Profit Margins FY12/09 FY12/10 FY12/11 FY12/12 FY12/13

(JPYmn) Cons. Cons. Cons. Cons. Cons.

Gross Profit 10,965 12,431 11,254 12,566 13,459

Gross Profit Margin 9.5% 10.4% 9.3% 9.8% 10.2%

Operating Profit 2,889 4,263 2,178 2,902 4,141

OP Margin 2.5% 3.6% 1.8% 2.3% 3.1%

EBITDA 5,399 7,506 6,065 6,595 8,017

EBITDA Margin 4.7% 6.3% 5.0% 5.2% 6.1%

Net Profit Margin 1.7% 1.8% 2.1% 1.3% 1.2%

Financial Ratios

ROA 1.8% 2.1% 2.6% 1.6% 1.5%

ROE 10.4% 10.1% 10.7% 6.3% 5.6%

Total Asset Turnover 1.07 1.18 1.23 1.25 1.24

Inventory Turnover 12.8 11.9 14.2 15.0 15.6

Days of Inventory 28.4 30.6 25.8 24.3 23.4

Working Capital Requirement 17,723 15,935 16,376 15,082 16,035

Current Ratio 86.8% 93.4% 89.4% 94.7% 90.2%

Quick Ratio 63.3% 53.1% 58.3% 62.5% 61.6%

OCF / Current Liabilities 0.04 0.19 0.09 0.17 0.15

Net Debt / Equity 2.23% 1.65% 1.57% 1.39% 1.37%

OCF / Total Liabilities 0.0 0.1 0.0 0.1 0.1

Cash Cycle (days) 50.2 52.0 48.8 44.7 54.7

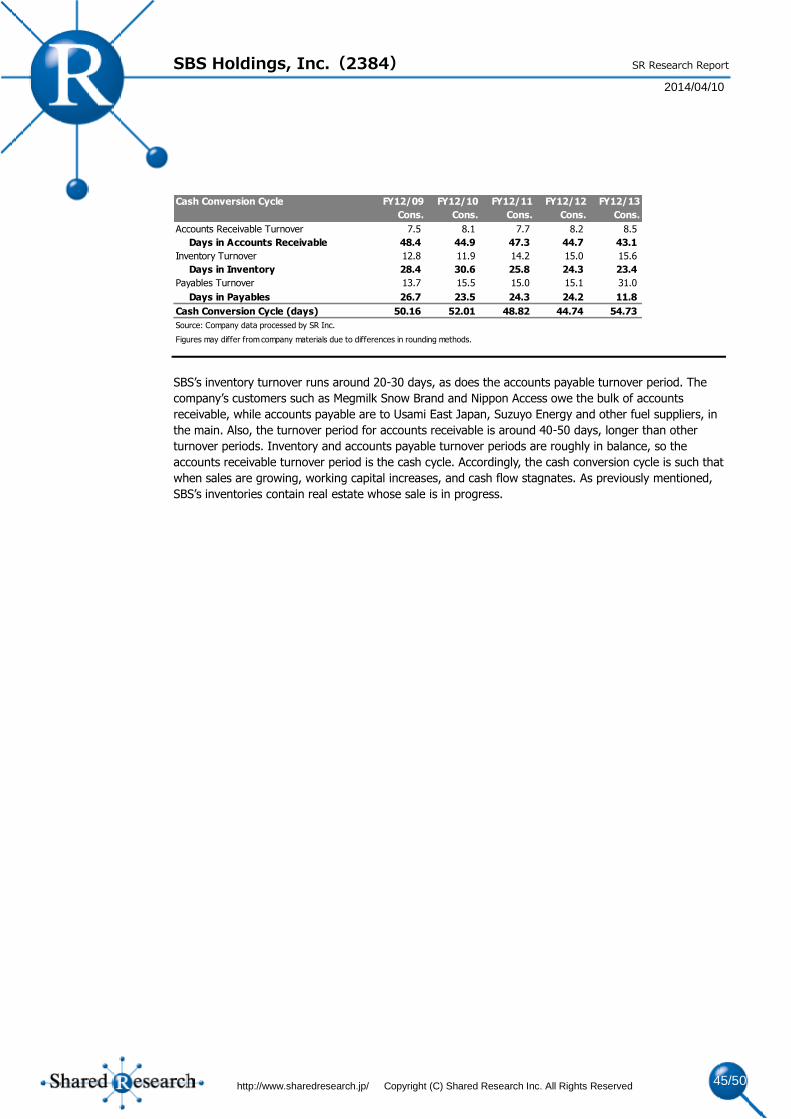

Changes in Working Capital 3,752 -1,788 440 -1,294 953

Source: Company data processed by SR Inc.

Figures may differ from company materials due to differences in rounding methods.

Competitor expenses2012 (JPYmn) SBS HD Proportion Hitachi Transport System Proportion Senko Proportion Hamakyorex Proportion

Sales 127,935 100.0% 547,717 100.0% 293,534 100.0% 88,943 100.0%

CoGS 115,369 90.2% 489,239 89.3% 263,898 89.9% 80,918 91.0%

SG&A 9,665 7.6% 38,743 7.1% 19,727 6.7% 2,187 2.5%

Personnel 6,197 4.8% 22,410 4.1% 7,020 2.4% 1,101 1.2%

Depreciation 329 0.3% 1,989 0.4% - - - -

Rent expenses 501 0.4% 1,785 0.3% - - - -

Others 2,637 2.1% 12,559 2.3% - - - -

Source: Company data, SR