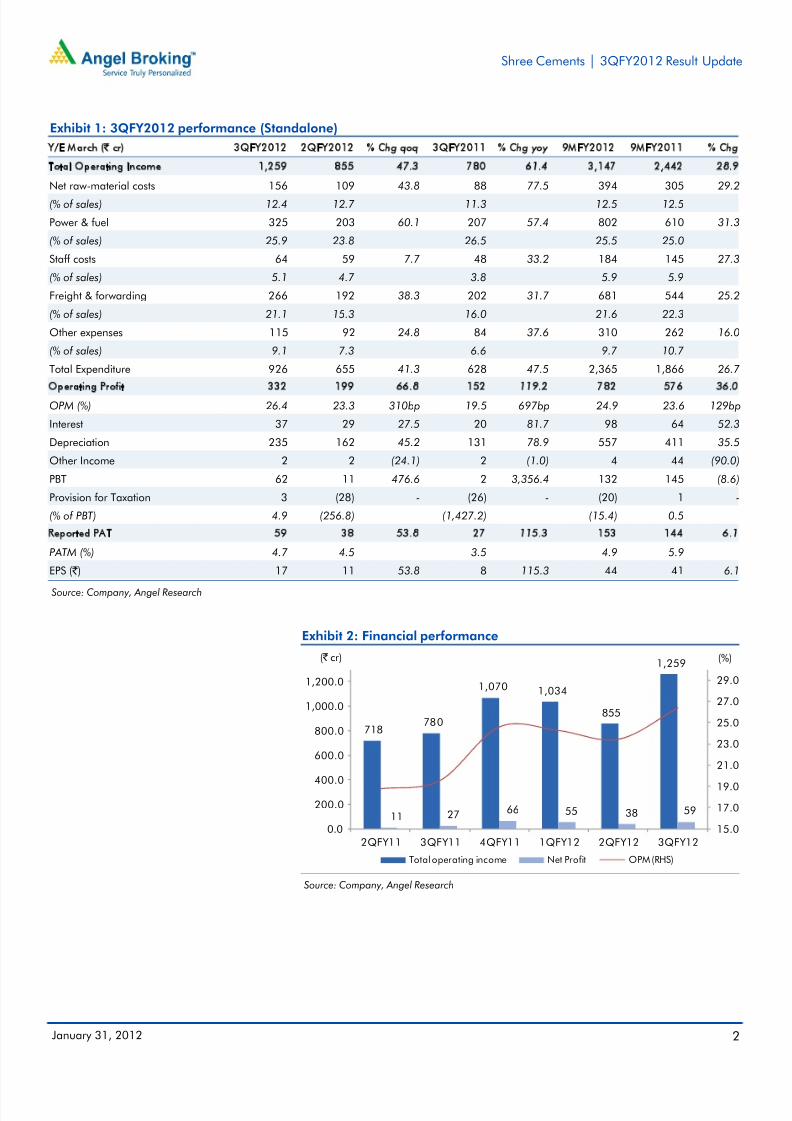

Please refer to important disclosures at the end of this report 1 Y/E Mar. ( ` cr ) 3QFY 2012 2QFY2012 % Chg qoq 3QFY2011 % Chg yoy Net sales 1,259 855 47.3 780 61.4 Operating profit 332 199 66.8 152 119.2 OPM (%) 26.4 23.3 310bp 19.5 697bp Net profit 59 38 53.8 27 115.3 Source: Company, Angel Research During 3QFY2012, Shree Cement (SRCM) posted 115.3% yoy growth in its bottom line to `59cr. Bottom-line growth was mainly driven by the cement business, which posted substantially higher realizations and reasonable 8.8% growth in volumes. PAT growth could have been higher, but it was restricted to a large extent by the sharp increase in depreciation cost (78.9% yoy) on account of capitalization of 150MW of new power capacity. We remain Neutral on the stock. OPM up by 697bp yoy, 310bp qoq: SRCM’s total operating income grew by61.4% yoy to `1,259cr, primarily on account of higher cement realization. The company’s cement realization improved by 33.2% yoy to `3,794/tonne (up 11.4% qoq) on account of higher cement prices and higher cement sales as a proportion of total cement and clinker sales (98% in 3QFY2012 vs. 88% in 3QFY2011, as it had 1.5mtpa of incremental grinding capacity operational). Revenue of the power business also grew by 429% yoy to `177cr due to a 244% increase in sale volumes to 256.4MUs. This revenue included `66cr from power trading operations. The company’s over all EBITDA margin expanded by 69 7bp yoy, as higher cement realization negated the cost pressures witnessed in freight cost and other expenses. Outlook and valuation: We expect SRCM to post a strong 23.8% CAGR in its top line over FY2011-13E, aided by an 8.9% CAGR in dispatches over the period. At the CMP, SRCM's cement business is trading at EV/tonne of US$84 on current capacity (US$59 on FY2013E capacity), which, when considering its unfavorable plant locations, in our view offers inadequate margin of safety. Hence, we maintain our Neutral recommendation on the stock. Key financials Y/E March ( ` cr) FY2010 FY2011 FY2012E FY2013E Net Sales 3,642 3,512 4,497 5,383 % chg 34.2 (3.6) 28.0 19.7 Net Profit 676 210 237 421 % chg 17.0 (69.0) 12.9 77.6 FDEPS(Rs) 194.0 74.1 68.0 120.7 OPM (%) 39.5 25.2 25.3 26.1 P/E(x) 11.6 30.4 33.2 18.7 P/BV(x) 4.3 4.0 3.6 3.1 RoE(%) 45.2 13.5 11.3 17.7 RoCE(%) 26.2 5.4 8.9 15.8 EV/Sales (x) 1.9 2.0 1.6 1.1 EV /EBITDA 4. 8 8.0 6. 2 4.4 Source: Company, Angel Research NEUTRAL CMP `2,255 Target Price -Investment Period - Stock Info Sector Bloomberg Code Shareholding Pattern (%) Promoters 64.8 MF / Banks / Indian Fls 5.0 FII / NRIs / OCBs 8.7 Indian Public / Others 21.5 Abs. ( %) 3m 1yr 3yr Sensex (2.9) (6. 2) 82.4 SRCM 18.9 35. 9 353.1 SRCM@IN BSE Sensex 17,194 Nifty 5,199 Reuters Code SHCM.BO 52 Week High / Low 2305/1505 Avg. Daily Volume 5,824 Face Value ( `) 10 Cement Market Cap ( `cr) 7,857 Beta 0.7 V.Srinivasan +91 22 39357800 Ext. 6833 [email protected]Sourabh Taparia +91 22 39357800 Ext. 6872 [email protected]Shree Cement Performance highlights 3QFY2012 Result Update| Cement January 31, 2012

During 3QFY2012, Shree Cement (SRCM) posted 115.3% yoy growth in its

bottom line to ` 59cr. Bottom-line growth was mainly driven by the cement

business, which posted substantially higher realizations and reasonable 8.8%growth in volumes. PAT growth could have been higher, but it was restricted to a

large extent by the sharp increase in depreciation cost (78.9% yoy) on account of

capitalization of 150MW of new power capacity. We remain Neutral on the stock.

OPM up by 697bp yoy, 310bp qoq: SRCM’s total operating income grew by

61.4% yoy to ` 1,259cr, primarily on account of higher cement realization. The

company’s cement realization improved by 33.2% yoy to ` 3,794/tonne (up

11.4% qoq) on account of higher cement prices and higher cement sales as a

proportion of total cement and clinker sales (98% in 3QFY2012 vs. 88% in

3QFY2011, as it had 1.5mtpa of incremental grinding capacity operational).

Revenue of the power business also grew by 429% yoy to ` 177cr due to a 244%

increase in sale volumes to 256.4MUs. This revenue included ` 66cr from powertrading operations. The company’s overall EBITDA margin expanded by 697bp

yoy, as higher cement realization negated the cost pressures witnessed in freight

cost and other expenses.

Outlook and valuation: We expect SRCM to post a strong 23.8% CAGR in its top

line over FY2011-13E, aided by an 8.9% CAGR in dispatches over the period.

At the CMP, SRCM's cement business is trading at EV/tonne of US$84 on current

capacity (US$59 on FY2013E capacity), which, when considering its unfavorable

plant locations, in our view offers inadequate margin of safety. Hence,

we maintain our Neutral recommendation on the stock.

Key financialsY/E March (` cr) FY2010 FY2011 FY2012E FY2013E

Research Team Tel: 022 - 39357800 E-mail: [email protected] Website: www.angelbroking.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investmentdecision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliablesources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as thisdocument is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report .

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to thelatest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may haveinvestment positions in the stocks recommended in this report.

Disclosure of Interest Statement Shree Cement

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock No

3. Angel and its Group companies' Directors ownership of the stock No

4. Broking relationship with company covered No

Ratings (Returns): Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)Reduce (-5% to 15%) Sell (< -15%)

Note: We have not considered any Exposure below`

1 lakh for Angel, its Group companies and Directors