CHAPTER 6 Investments and Receivables OVERVIEW OF EXERCISES, PROBLEMS, AND CASES Estimated Time in Learning Objective Exercises Minutes Level 1. Demonstrate an understanding of the accounting for various 1 15 Easy types of investments companies make. 2 15 Easy 3 15 Mod 4 10 Easy 5 20 Mod 6 25 Mod 7 25 Mod 16* 5 Easy 2. Demonstrate an understanding of how to account for accounts 8 20 Mod receivable, including bad debts. 9 25 Mod 10 20 Mod 16* 5 Easy 3. Demonstrate an understanding of how to account for 11 20 Mod interest-bearing notes receivable. 16* 5 Easy 4. Demonstrate an understanding of how to account for 12 15 Mod non-interest-bearing notes receivable. 5. Explain various techniques that companies use to accelerate13 15 Mod the inflow of cash from sales.

Transcript

CHAPTER 6

Investments and ReceivablesOVERVIEW OF EXERCISES, PROBLEMS, AND CASES

Estimated Time in

Learning Objective Exercises Minutes Level

1. Demonstrate an understanding of the accounting for various 1 15Easy

types of investments companies make. 2 15Easy

3 15 Mod4 10

Easy5 20 Mod6 25 Mod7 25 Mod

16* 5Easy

2. Demonstrate an understanding of how to account for accounts 8 20 Modreceivable, including bad debts. 9 25 Mod

10 20 Mod16* 5

Easy

3. Demonstrate an understanding of how to account for 11 20 Modinterest-bearing notes receivable. 16* 5

Easy

4. Demonstrate an understanding of how to account for 12 15 Modnon-interest-bearing notes receivable.

5. Explain various techniques that companies use to accelerate 13 15 Modthe inflow of cash from sales.

6. Explain the effects of transactions involving liquid assets 14 5Easy

on the statement of cash flows. 15 15 Mod16* 5

Easy

*Exercise, problem, or case covers two or more learning objectivesLevel = Difficulty levels: Easy; Moderate (Mod); Difficult (Diff)

FINANCIAL ACCOUNTING SOLUTIONS MANUAL

Problems Estimated and Time in

Learning Objective Alternates Minutes Level

1. Demonstrate an understanding of the accounting for various 1 30 Modtypes of investments companies make. 2 25 Mod

2. Demonstrate an understanding of how to account for 3 45 Diffaccounts receivable, including bad debts. 4 25 Mod

5 20 Mod9* 20 Mod

3. Demonstrate an understanding of how to account for 9* 20 Modinterest-bearing notes receivable.

4. Demonstrate an understanding of how to account for 6 25 Modnon-interest-bearing notes receivable.

5. Explain various techniques that companies use to accelerate 7 10 Modthe inflow of cash from sales.

6. Explain the effects of transactions involving liquid assets 8 20 Modon the statement of cash flows.

*Exercise, problem, or case covers two or more learning objectivesLevel = Difficulty levels: Easy; Moderate (Mod); Difficult (Diff)

6-2

CHAPTER 6 INVESTMENTS AND RECEIVABLES

EstimatedTime in

Learning Objective Cases Minutes Level

1. Demonstrate an understanding of the accounting for various 3* 20 Modtypes of investments companies make. 4* 20 Mod

6 25 Mod

2. Demonstrate an understanding of how to account for 1 25 Modaccounts receivable, including bad debts. 2 30 Mod

4* 20 Mod

3. Demonstrate an understanding of how to account for 5* 25 Modinterest-bearing notes receivable.

4. Demonstrate an understanding of how to account for 5* 25 Modnon-interest-bearing notes receivable. 7 30 Mod

5. Explain various techniques that companies use to acceleratethe inflow of cash from sales.

6. Explain the effects of transactions involving liquid assets 3* 20 Modon the statement of cash flows.

*Exercise, problem, or case covers two or more learning objectivesLevel = Difficulty levels: Easy; Moderate (Mod); Difficult (Diff)

6-3

FINANCIAL ACCOUNTING SOLUTIONS MANUAL

Q U E S T I O N S

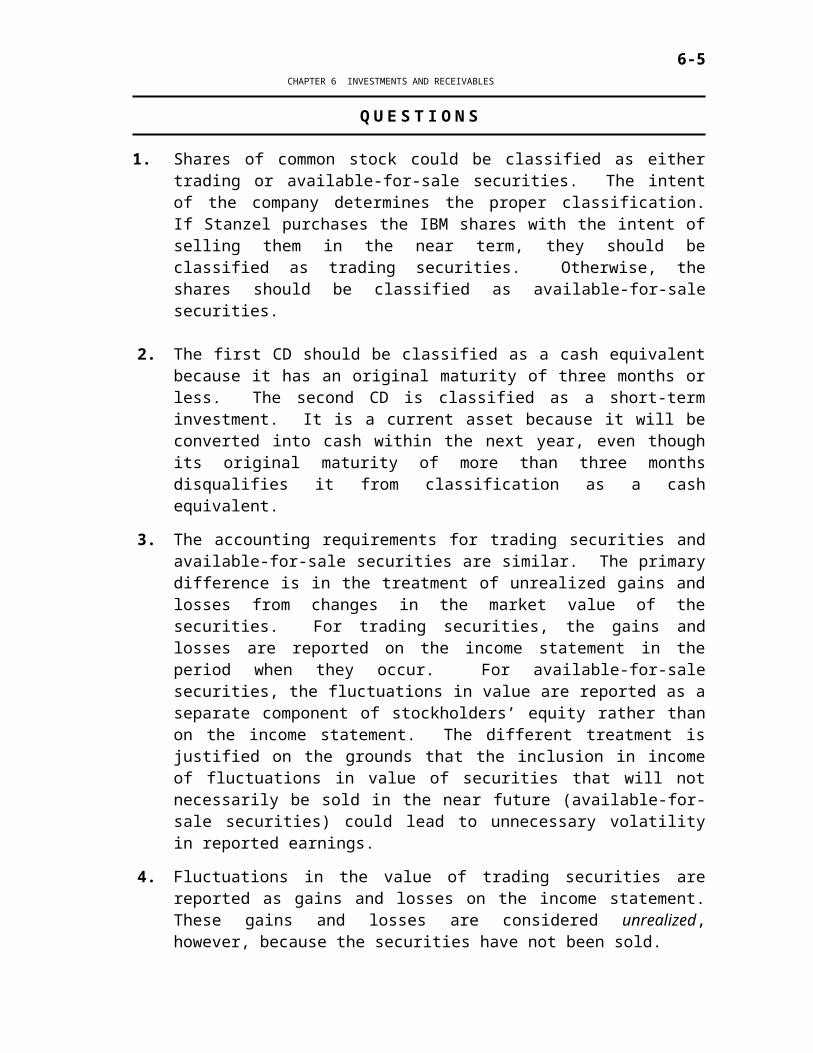

1. Shares of common stock could be classified as either trading or available-for-sale securities. The intent of the company determines the proper classification. If Stanzel purchases the IBM shares with the intent of selling them in the near term, they should be classified as trading securities. Otherwise, the shares should be classified as available-for-sale securities.

2. The first CD should be classified as a cash equivalent because it has an original maturity of three months or less. The second CD is classified as a short-term investment. It is a current asset because it will be converted into cash within the next year, even though its original maturity of more than three months disqualifies it from classification as a cash equivalent.

3. The accounting requirements for trading securities and available-for-sale securities are similar. The primary difference is in the treatment of unrealized gains and losses from changes in the market value of the securities. For trading securities, the gains and losses are reported on the income statement in the period when they occur. For available-for-sale securities, the fluctuations in value are reported as a separate component of stockholders’ equity rather than on the income statement. The different treatment is justified on the grounds that the inclusion in income of fluctuations in value of securities that will not necessarily be sold in the near future (available-for-sale securities) could lead to unnecessary volatility in reported earnings.

4. Fluctuations in the value of trading securities are reported as gains and losses on the income statement. These gains and losses are considered unrealized, however, because the securities have not been sold.

5. The allowance method of accounting for bad debts tries to match one of the costs associated with granting credit, i.e. uncollectible accounts, with the revenue of the period. Under the matching principle, an estimate of bad debts is made on the basis of either the sales of the period or the accounts receivable at the end of the period, and an expense is recognized.

6. When bad debts expense is estimated by using the percentage of accounts receivable approach, the balance already in the allowance account must be considered. For example, if the estimate of the accounts receivable that will prove to be uncollectible is $20,000 and the allowance account has a balance of $3,000 before adjustment, only $17,000 has to be added to it. Under the percentage of net credit sales approach, however, the emphasis is on the debit to bad debts expense. The balance in the allowance account before adjustment is ignored.

7. An aging schedule is a refinement of the percentage of accounts receivable approach to estimating bad debts. The accountant categorizes the various receivables by the length of time they are outstanding. The

6-4

CHAPTER 6 INVESTMENTS AND RECEIVABLES

estimate of the percent uncollectible increases as the age of the accounts go up.

8. A note receivable arises from a written promise by someone to pay a specific amount of money in the future with interest. An account receivable arises from granting a customer an open line of credit and does not normally include interest.

9. This statement is flawed in one important respect. Both interest-bearing and non-interest-bearing notes result in the recognition of interest revenue to the holder of the note. Interest is earned on a non-interest-bearing note. The interest is implicit in the agreement. Whether or not more interest is earned on an interest-bearing note or a non-interest-bearing note depends on the specific terms of the agreement.

10. When a note receivable is discounted with recourse, it means that if the customer fails to pay the bank the total amount due on the maturity date, the company that sold the note to the bank is liable to the bank for the full amount. Therefore, during the time a discounted note is outstanding, the seller of the note is contingently liable. Accounting standards do not require the seller to recognize the contingency as a liability, but a note is required to alert the statement reader of the uncertainty.

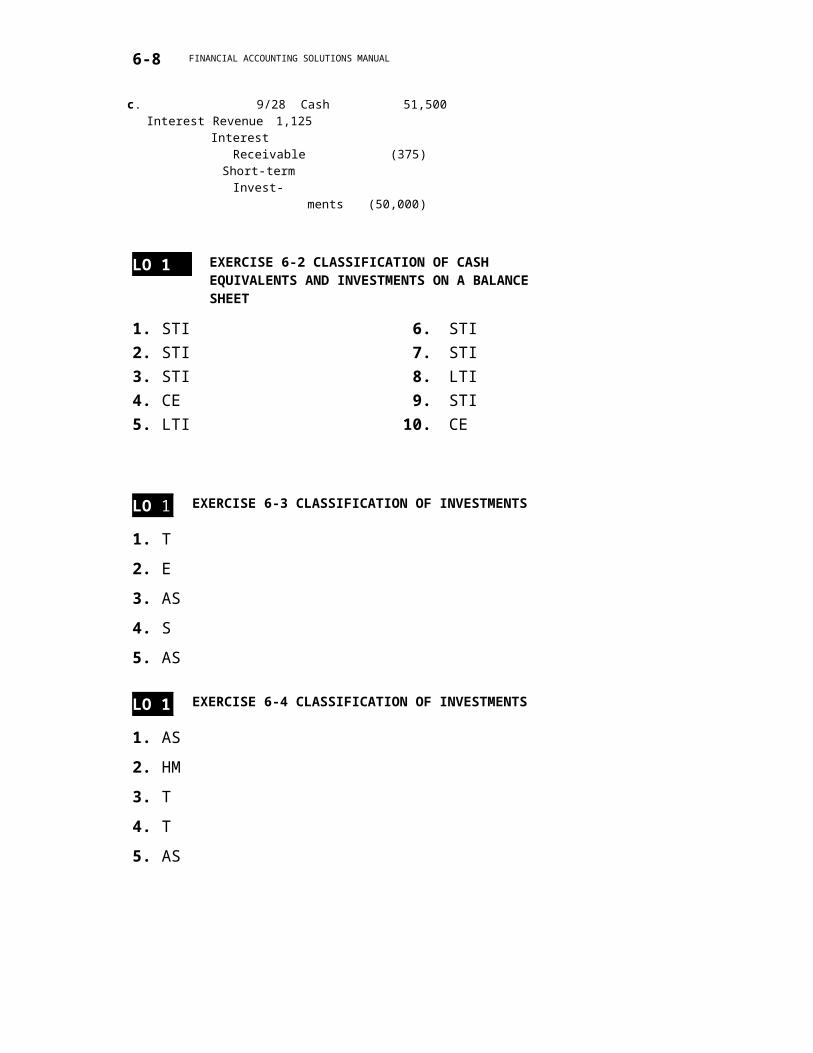

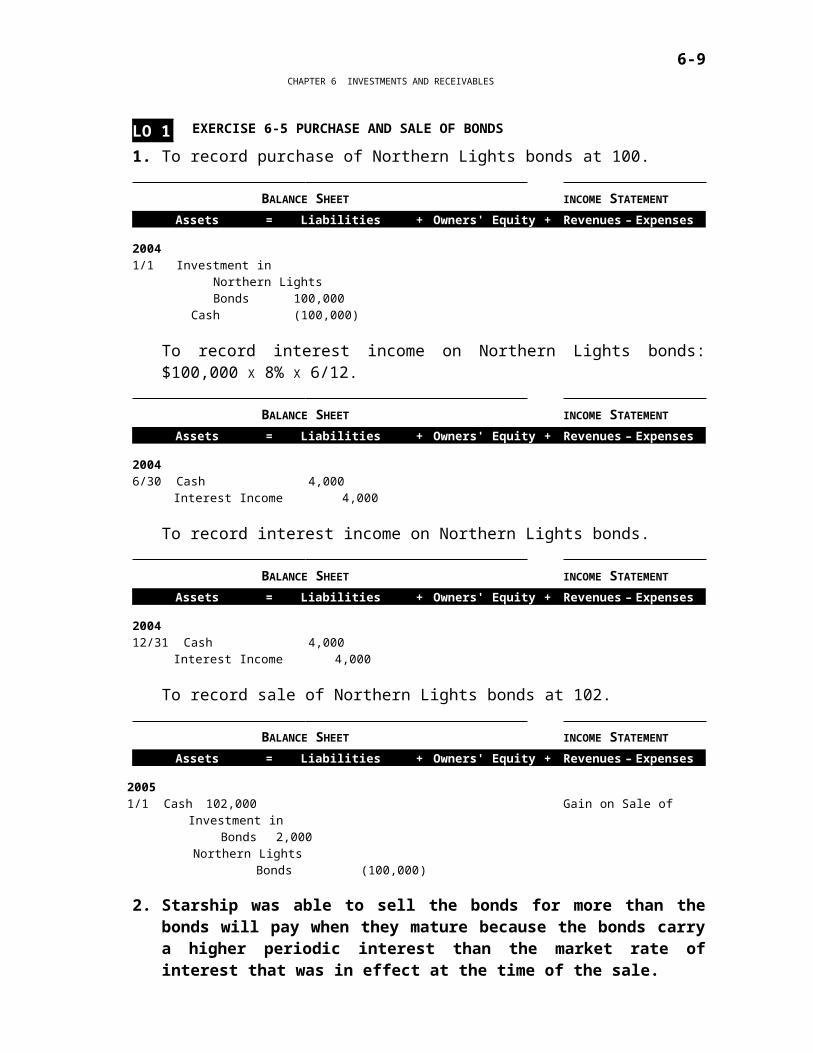

2. Starship was able to sell the bonds for more than the bonds will pay when they mature because the bonds carry a higher periodic interest than the market rate of interest that was in effect at the time of the sale.

6-7

FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 1 EXERCISE 6-6 INVESTMENT IN STOCK

1. Chicago should classify its investment in Denver stock as trading securities because it plans to hold the stock for a short time and profit from an increase in its market price.

2. To record purchase of trading securities for cash.

200412/20 Dividends Dividend Income 1,000 Receivable 1,000

To adjust trading securities to fair value.Fair value (1,000 shares X $42 per share) $ 42,000Cost: 1,000 shares X $40 per share 40,000 Unrealized gain $ 2,000

Investment in Stock 3,000Denver PreferredStock (42,000)

3. Chicago should classify its investment on its December 31 balance sheet as a current asset.

LO 1 EXERCISE 6-7 INVESTMENT IN STOCK

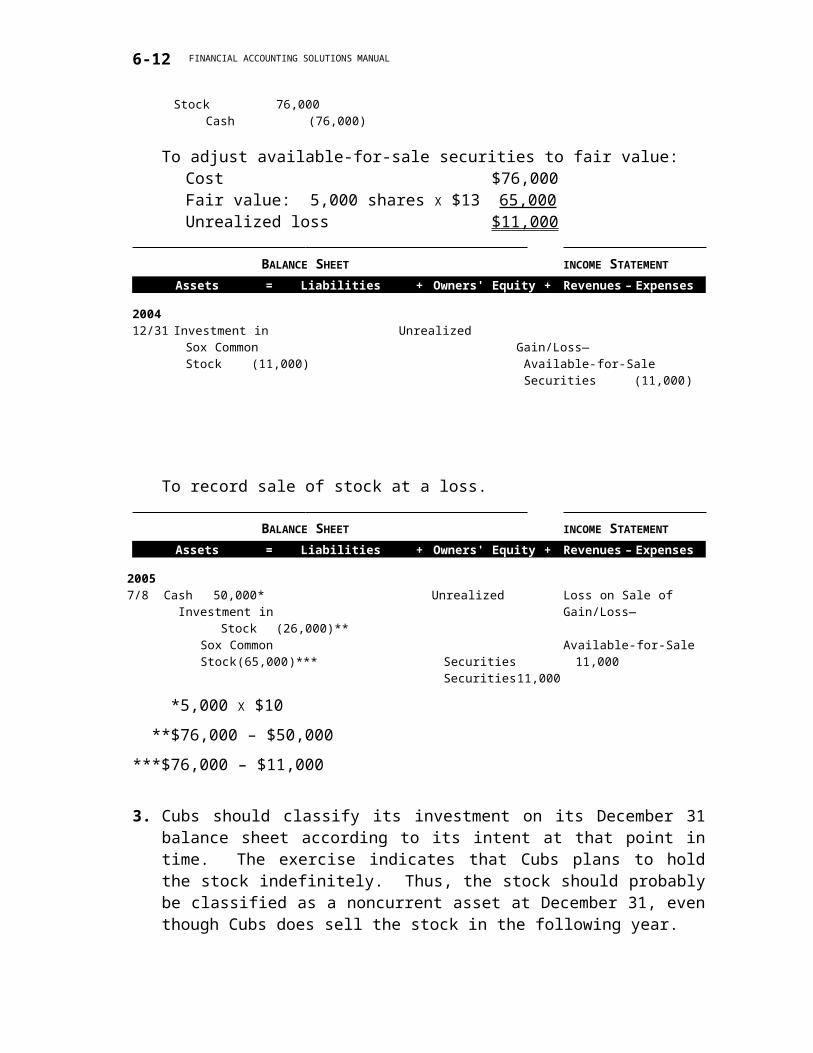

1. Cubs should classify its investment in Sox stock as available-for-sale because it plans to hold the stock indefinitely rather than as a part of its active trading portfolio. Only bonds can qualify as held-to-maturity securities.

2. To record purchase of available-for-sale securities for cash: 5,000 shares X $15 per share + $1,000 fees.

20057/8 Cash 50,000* Unrealized Loss on Sale of Investment in Gain/Loss— Stock (26,000)** Sox Common Available-for-Sale Stock (65,000)*** Securities 11,000

Securities 11,000

*5,000 X $10

**$76,000 – $50,000

***$76,000 – $11,000

3. Cubs should classify its investment on its December 31 balance sheet according to its intent at that point in time. The exercise indicates that Cubs plans to hold the stock indefinitely. Thus, the stock should probably be classified as a noncurrent asset at December 31, even though Cubs does sell the stock in the following year.

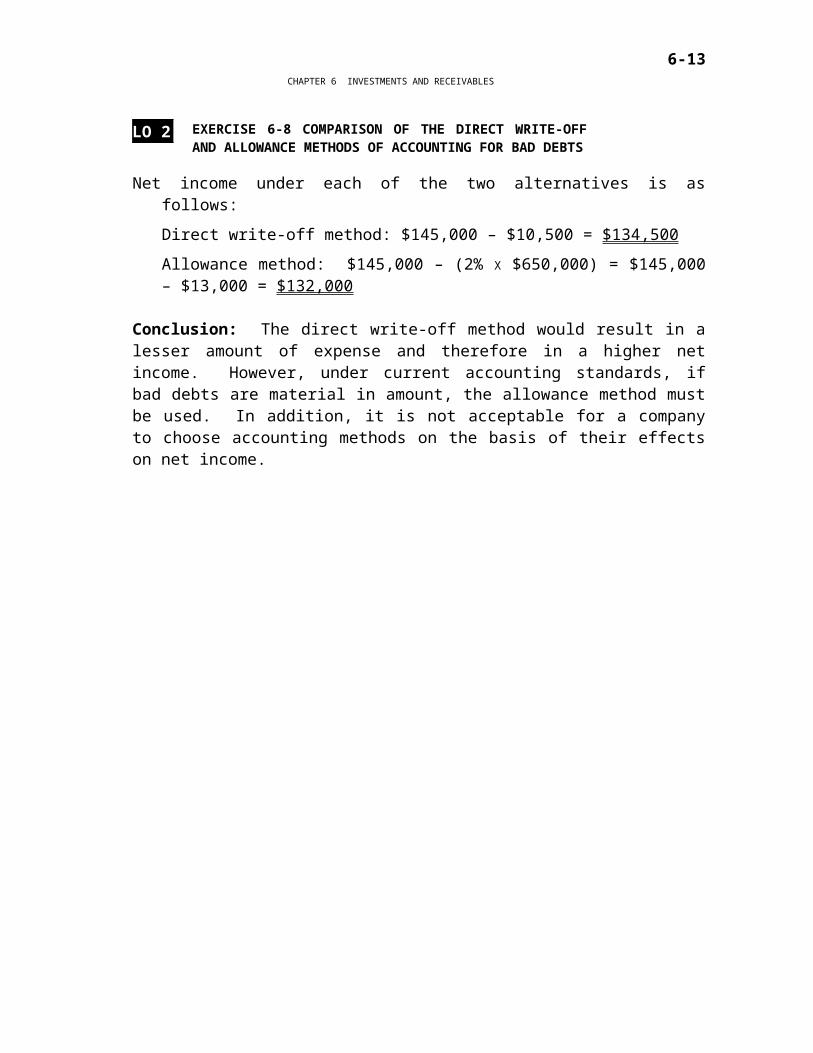

LO 2 EXERCISE 6-8 COMPARISON OF THE DIRECT WRITE-OFF AND ALLOWANCE METHODS OF ACCOUNTING FOR BAD DEBTS

Net income under each of the two alternatives is as follows:

Direct write-off method: $145,000 – $10,500 = $134,500

Conclusion: The direct write-off method would result in a lesser amount of expense and therefore in a higher net income. However, under current accounting standards, if bad debts are material in amount, the allowance method must be used. In addition, it is not acceptable for a company to choose accounting methods on the basis of their effects on net income.

6-10

CHAPTER 6 INVESTMENTS AND RECEIVABLES

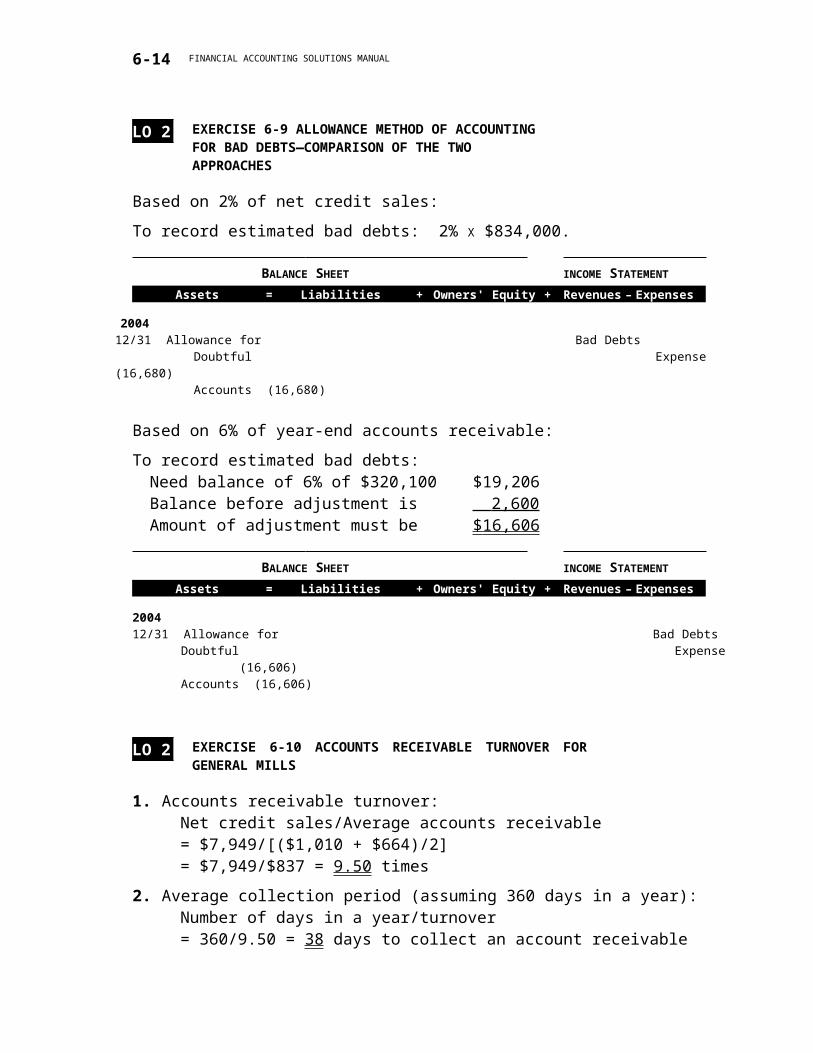

LO 2 EXERCISE 6-9 ALLOWANCE METHOD OF ACCOUNTING FOR BAD DEBTS—COMPARISON OF THE TWO APPROACHES

Whether or not an average of 38 days to collect an account is reasonable depends on several factors. For example, how does this compare with other companies in the same industry as General Mills? How does it compare with prior years? What are General Mills’ credit terms? If its credit terms

6-11

FINANCIAL ACCOUNTING SOLUTIONS MANUAL

are 2/10, net 30, an average collection period of 38 days may be need to be investigated.

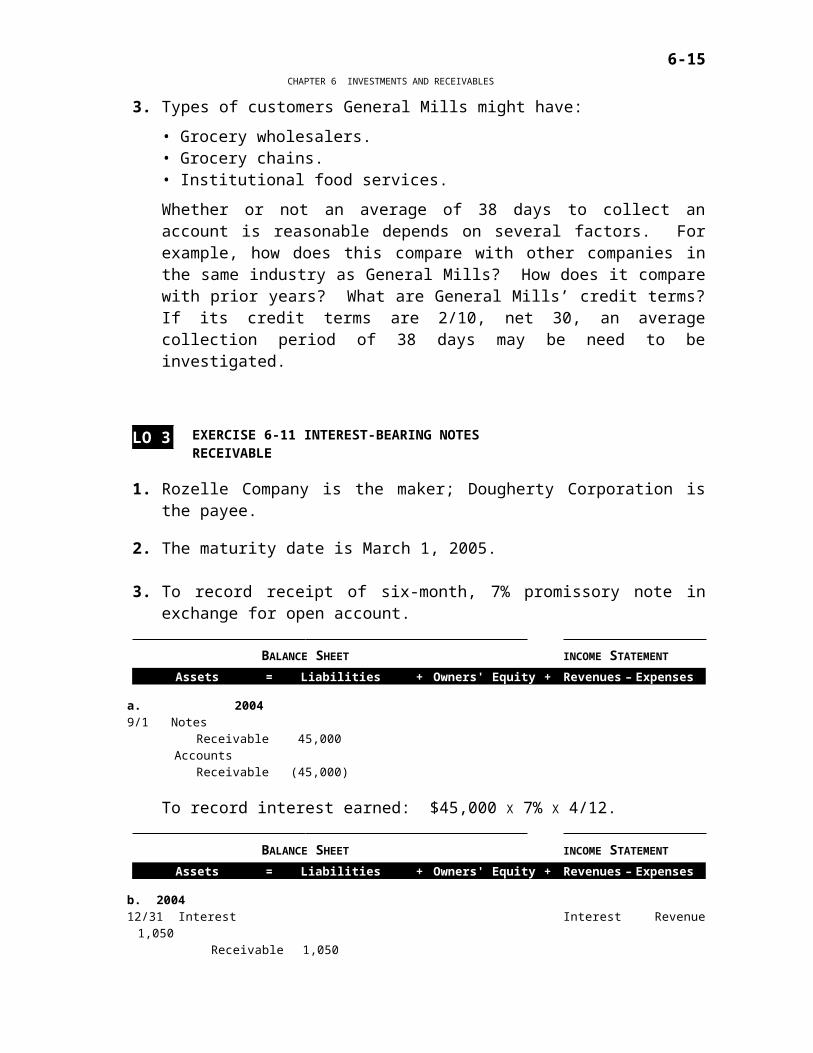

LO 3 EXERCISE 6-11 INTEREST-BEARING NOTES RECEIVABLE

1. Rozelle Company is the maker; Dougherty Corporation is the payee.

2. The maturity date is March 1, 2005.

3. To record receipt of six-month, 7% promissory note in exchange for open account.

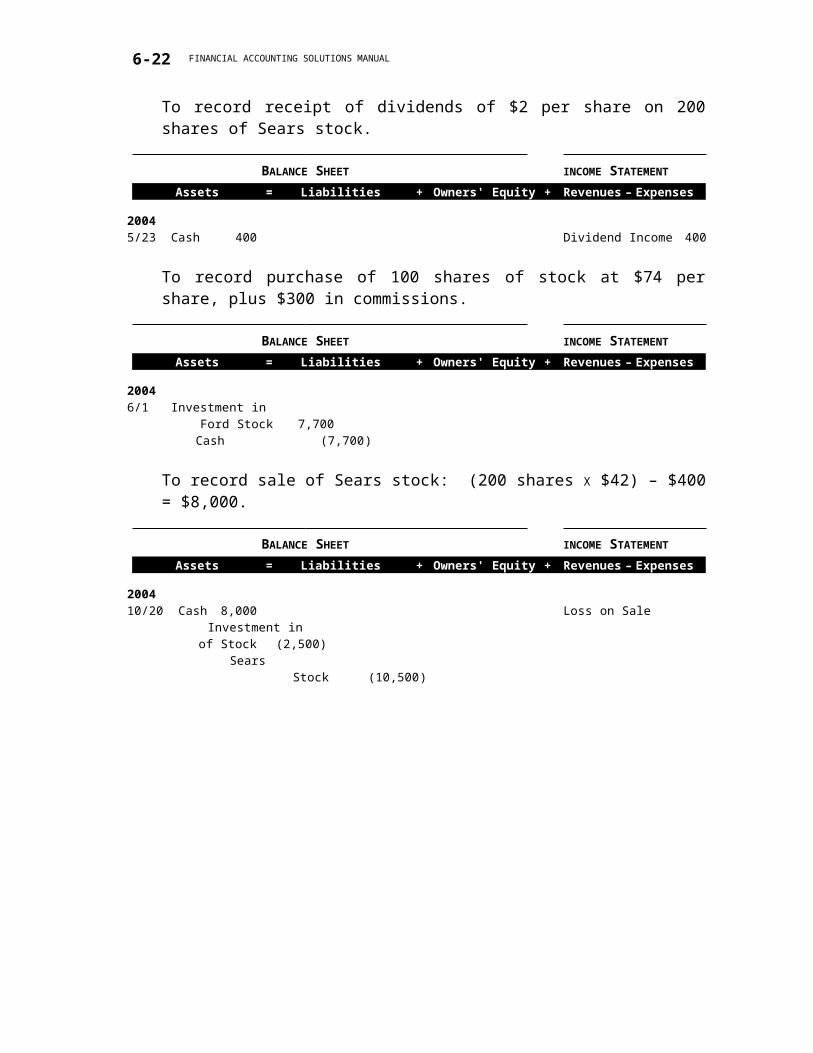

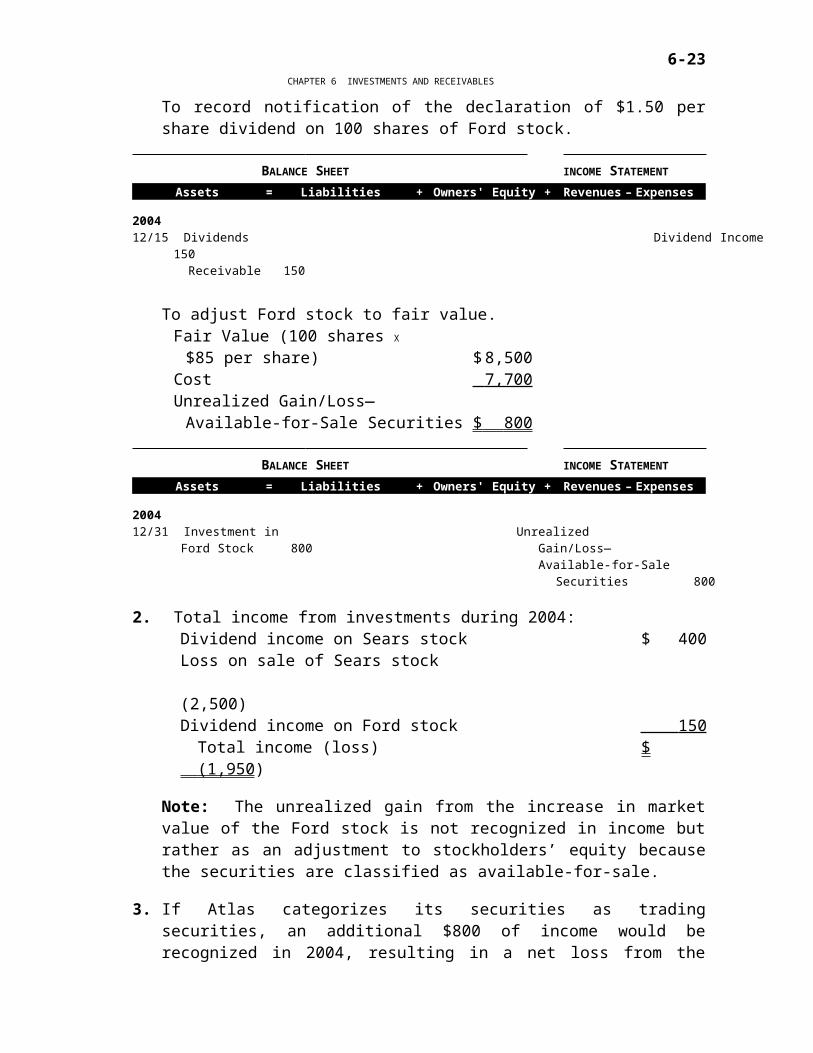

2. Total income from investments during 2004:Dividend income on Sears stock $ 400Loss on sale of Sears stock (2,500)Dividend income on Ford stock 150

Total income (loss) $ (1,950 )

Note: The unrealized gain from the increase in market value of the Ford stock is not recognized in income but rather as an adjustment to stockholders’ equity because the securities are classified as available-for-sale.

3. If Atlas categorizes its securities as trading securities, an additional $800 of income would be recognized in 2004, resulting in a net loss from the investments of $1,950 – $800, or $1,150. Increases and decreases in the value of trading securities are recognized on the income statement but not for available-for-sale securities.

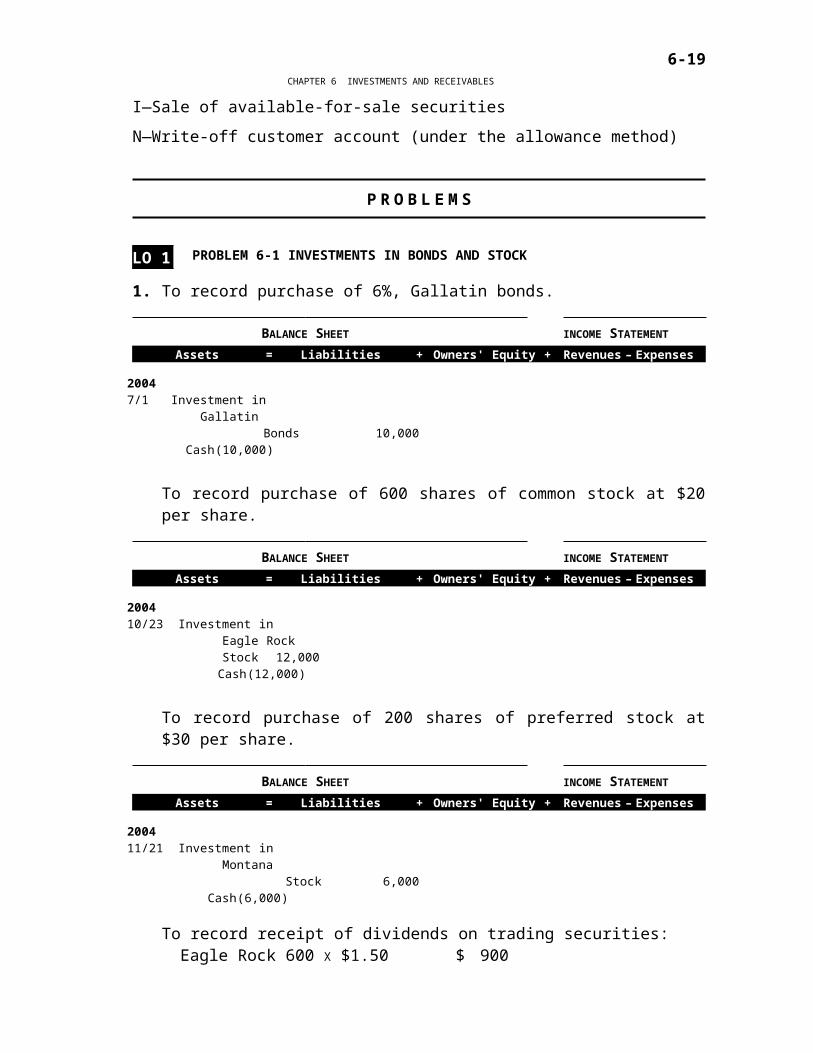

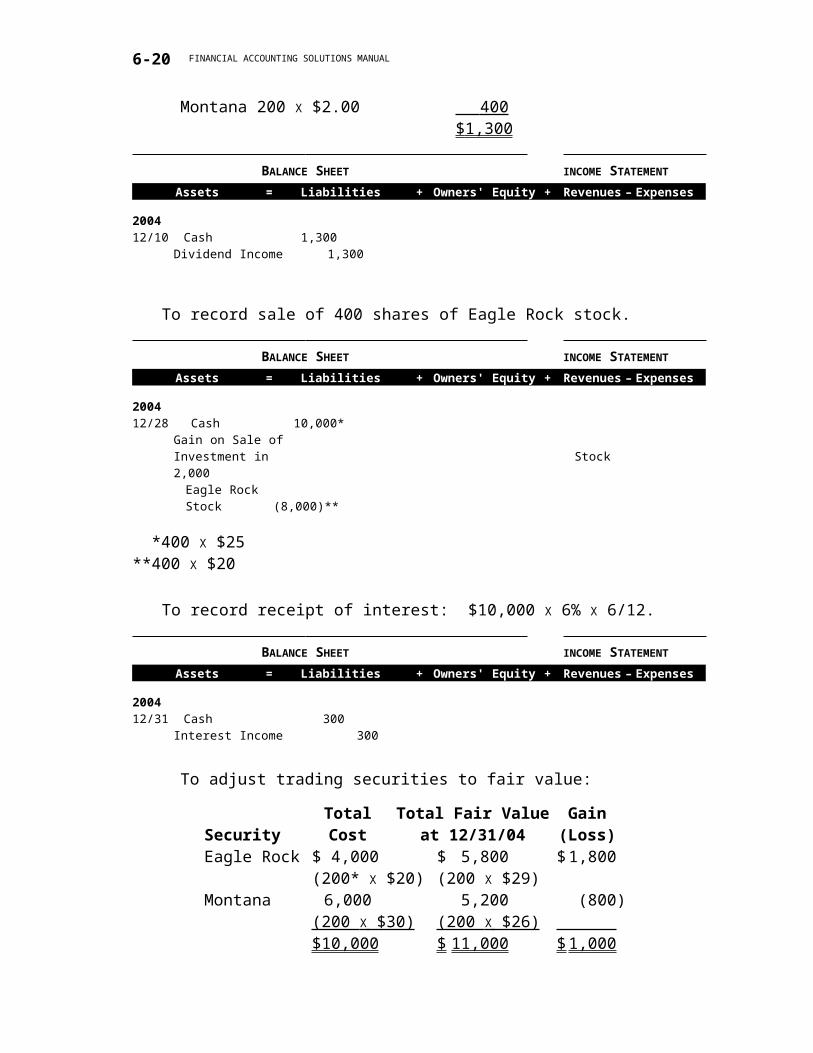

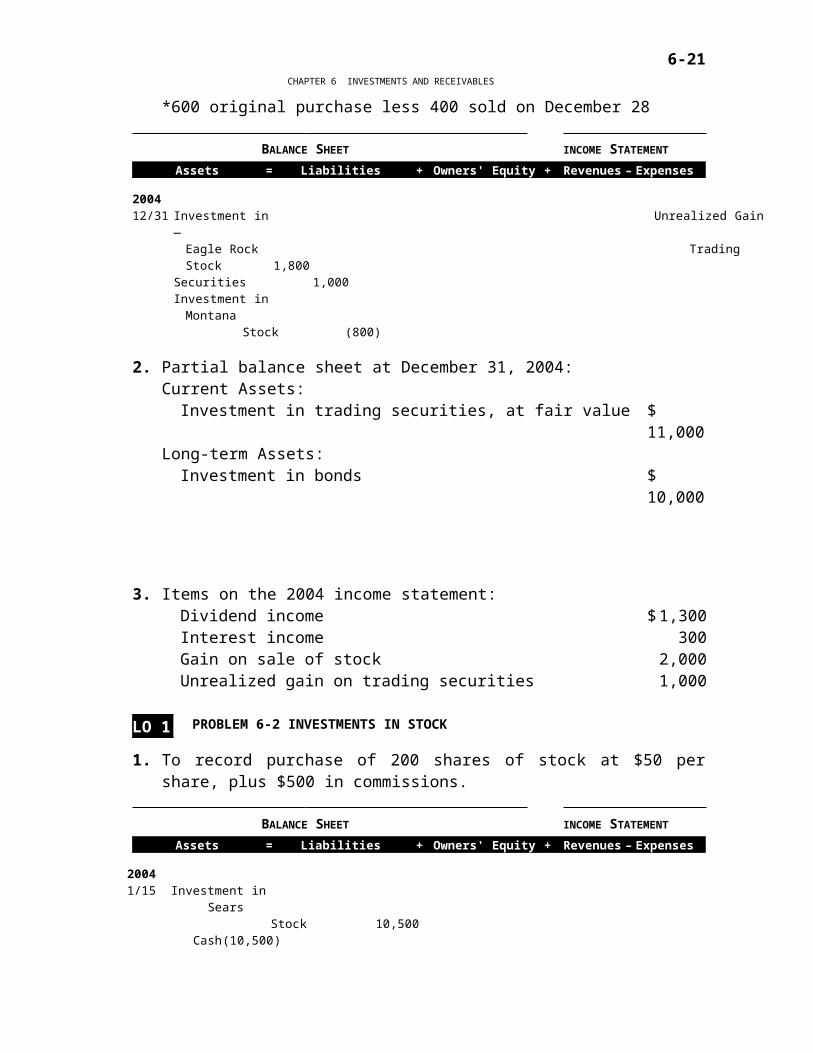

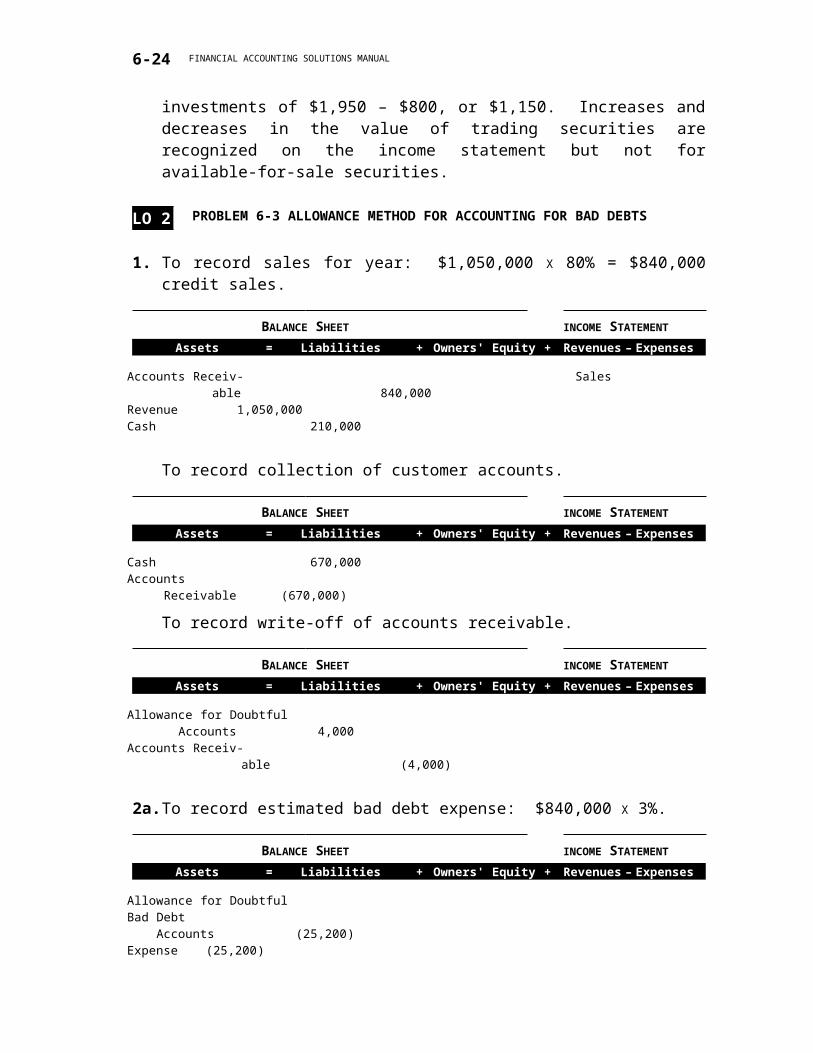

LO 2 PROBLEM 6-3 ALLOWANCE METHOD FOR ACCOUNTING FOR BAD DEBTS

1. To record sales for year: $1,050,000 X 80% = $840,000 credit sales.

Allowance for Doubtful Bad Debt Accounts (20,010) Expense (20,010)

3a. The net realizable value of accounts receivable on December 31, 2004 is $282,450:

Accounts receivable, Dec. 31 (from Part 2b.) $ 306,000Less: Allowance for doubtful accounts, Dec. 31

($2,350 – $4,000 + $25,200) 23,550 Net realizable value, December 31 $ 282,450

6-19

FINANCIAL ACCOUNTING SOLUTIONS MANUAL

3b. The net realizable value of accounts receivable on December 31, 2004 is $287,640:

Accounts receivable, Dec. 31 (from Part 2b.) $ 306,000Less: Allowance for doubtful accounts, Dec. 31

($2,350 – $4,000 + $20,010) 18,360 Net realizable value, December 31 $ 287,640

4. The recognition of bad debt expense reduces the net realizable value by the amount recorded in bad debt expense and the allowance for doubtful accounts. The write-off of accounts has no effect on the net realizable value.

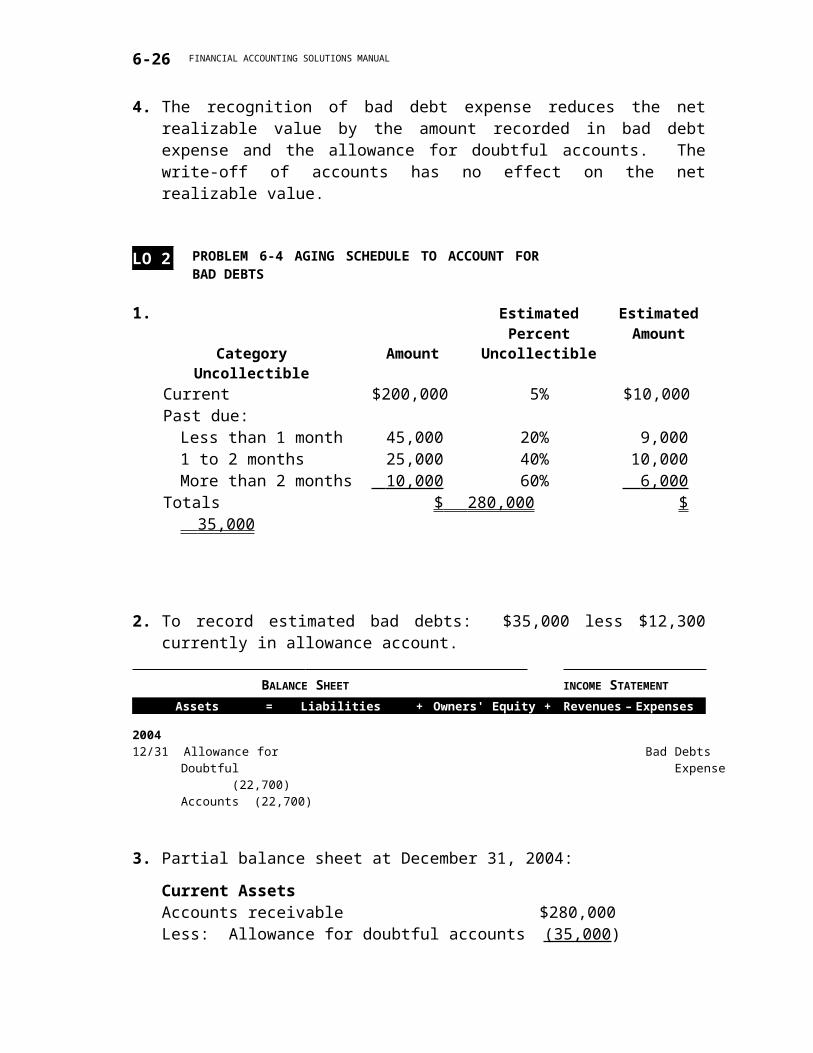

LO 2 PROBLEM 6-4 AGING SCHEDULE TO ACCOUNT FOR BAD DEBTS

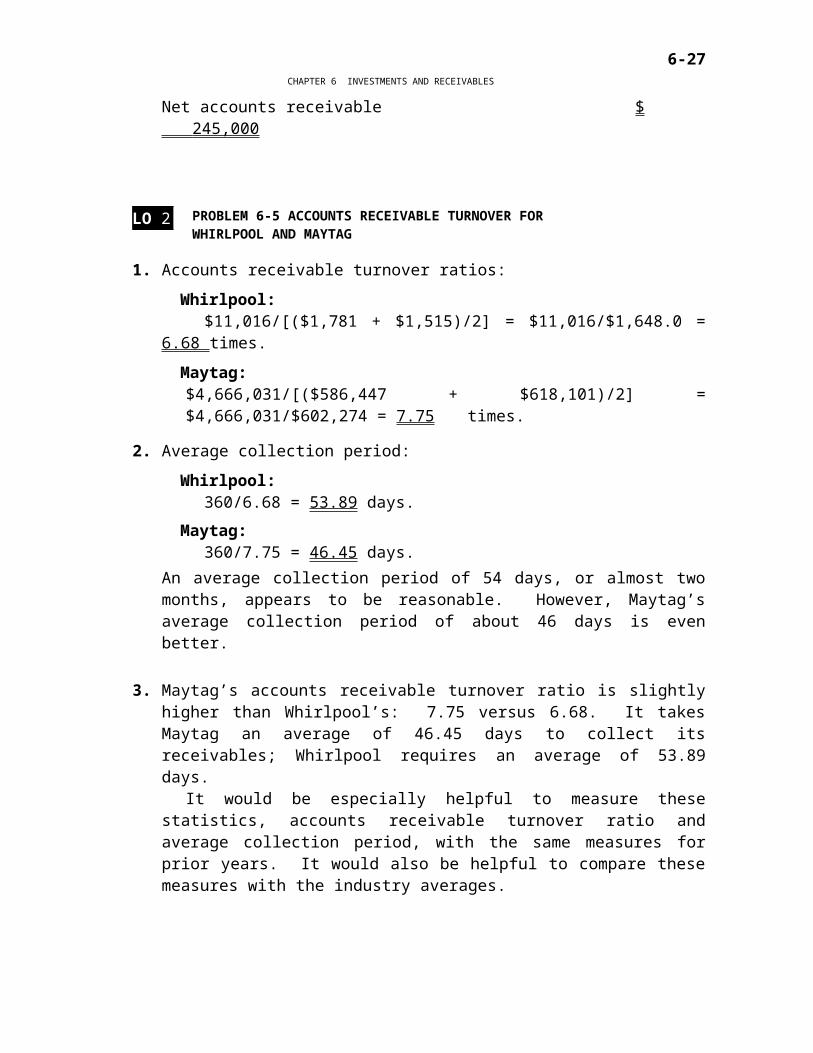

An average collection period of 54 days, or almost two months, appears to be reasonable. However, Maytag’s average collection period of about 46 days is even better.

3. Maytag’s accounts receivable turnover ratio is slightly higher than Whirlpool’s: 7.75 versus 6.68. It takes Maytag an average of 46.45 days to collect its receivables; Whirlpool requires an average of 53.89 days.

It would be especially helpful to measure these statistics, accounts receivable turnover ratio and average collection period, with the same measures for prior years. It would also be helpful to compare these measures with the industry averages.

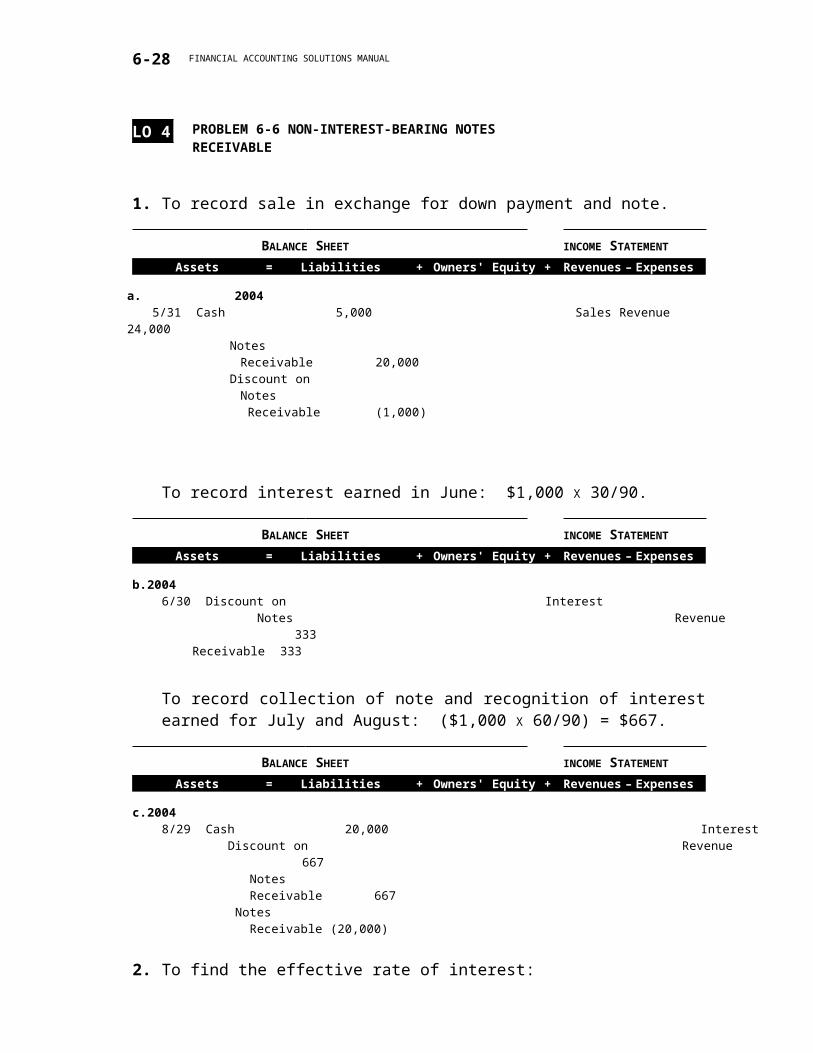

LO 4 PROBLEM 6-6 NON-INTEREST-BEARING NOTES RECEIVABLE

1. To record sale in exchange for down payment and note.

c. 2004 8/29 Cash 20,000 Interest Discount on Revenue 667 Notes Receivable 667 Notes Receivable (20,000)

2. To find the effective rate of interest:

1. Cash selling price $24,000Less: Down payment 5,000 Unpaid cash balance $19,000Amount of promissory note 20,000 Implicit interest in the note 1,000

2. Length of note 90 days3. Number of 90-day periods in a year 44. Amount of interest that would apply

to a full year: 1,000 X 4 $ 4,0005. Effective annual interest rate: $4,000/$19,000 21%

LO 5 PROBLEM 6-7 CREDIT CARD SALES

1. Net selling price $1.00Cost of goods sold .75 Gross margin $ .25

The owner must net $1 per gallon on the selling price. The amount per gallon he would have to charge credit card customers is

X – .02X = 1.00.98X = 1.00

X = $ 1 .02 per gallon

(It is worth noting that not all gas companies charge a higher price for credit card purchases.)

6-22

CHAPTER 6 INVESTMENTS AND RECEIVABLES

2. If his normal charge is $1.02 to credit card customers, he can offer a $.02 discount to cash customers and still maintain his gross margin.

LO 6 PROBLEM 6-8 EFFECTS OF CHANGES IN RECEIVABLE BALANCES ON STATEMENT OF CASH FLOWS

1. Statement of cash flows:STEGNER INC.

STATEMENT OF CASH FLOWSFOR THE YEAR ENDED DECEMBER 31, 2004

Net income $ 130,000Adjustments to reconcile net income to net cash

used by operating activities:Increase in accounts receivable $ (140,000)*Decrease in notes receivable 5,000 ** (135,000 )

Cash flows from operating activities $ (5,000)Cash, December 31, 2003 110,000 Cash, December 31, 2004 $ 105,000

*$223,000 – $83,000 **$100,000 – $95,000

2. Memorandum to the president:TO: Owner of Stegner, Inc.

FROM: Student’s name

DATE: January XX, 2005

SUBJECT: Cash Flows

You recently expressed concern about the decrease in the company’s cash balance in spite of the profitable year that was reported on this year’s income statement. My thoughts and a copy of the company’s 2004 statement of cash flows follow.

Although net income on an accrual basis was $130,000, the company’s cash balance declined by $5,000 during the year for two reasons. Most importantly, accounts receivable increased by $140,000 during the year from $83,000 to $223,000; we did not collect amounts due from our customers as sales were made. This drain on cash was partially offset by a $5,000 decrease in notes receivable during the year, from $100,000 to $95,000.

We can better manage our cash flow by increasing our collection efforts.

6-23

FINANCIAL ACCOUNTING SOLUTIONS MANUAL

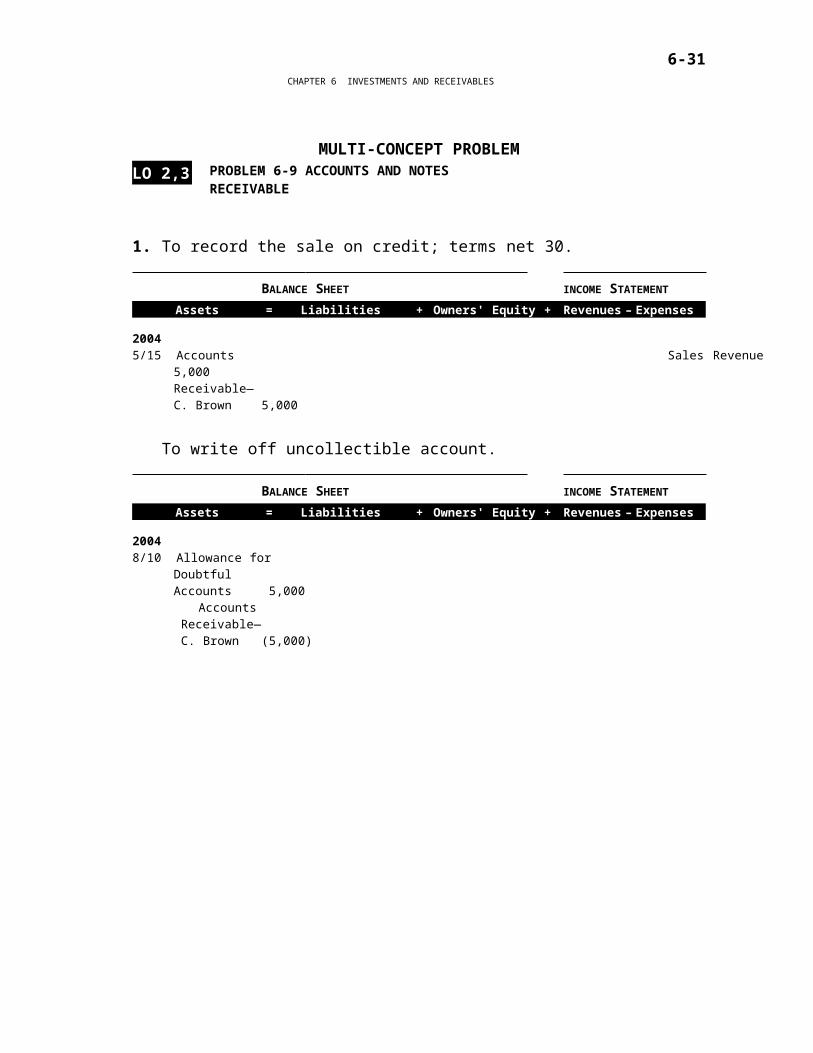

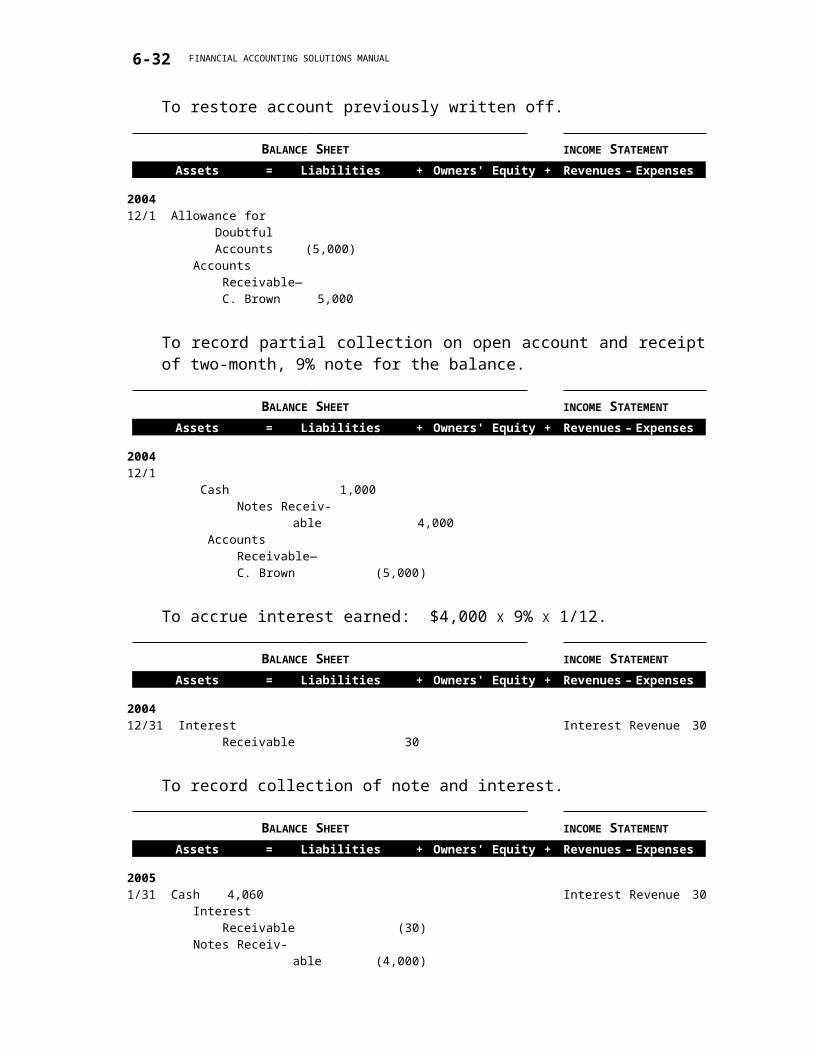

MULTI-CONCEPT PROBLEMLO 2,3 PROBLEM 6-9 ACCOUNTS AND NOTES

2. Brown is interested in reestablishing a good credit standing with its supplier, Linus, and for this reason has sent the check and signed a note for the balance.

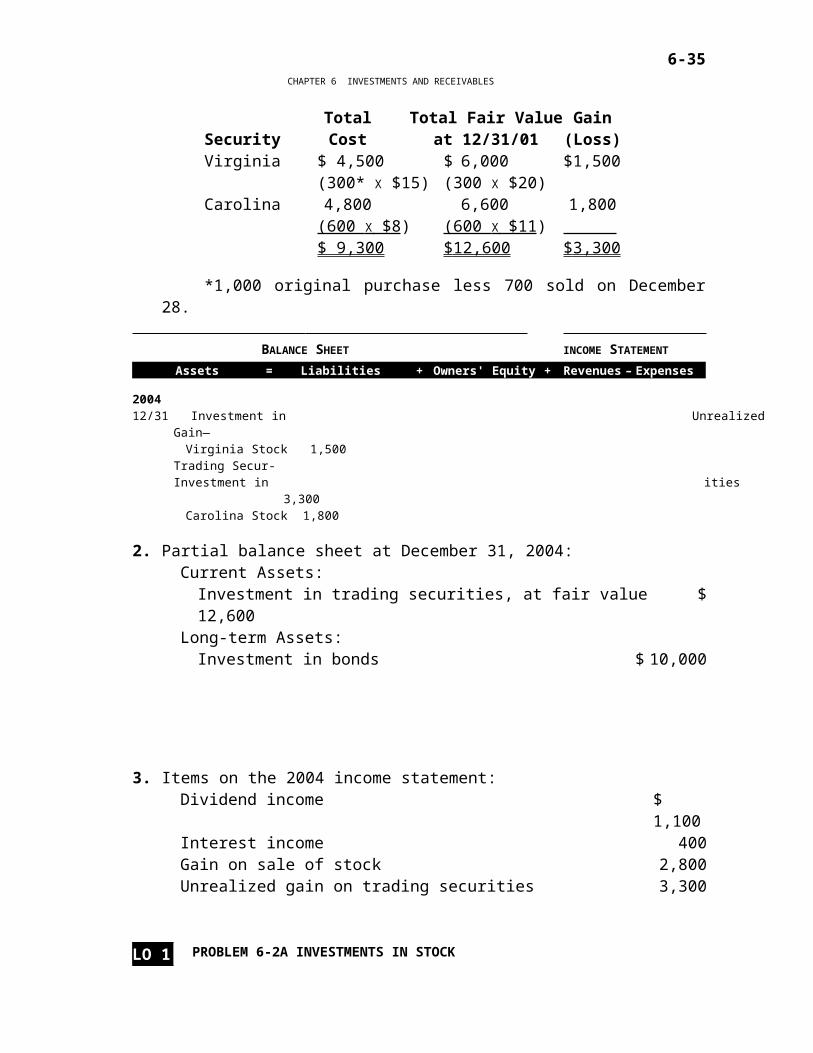

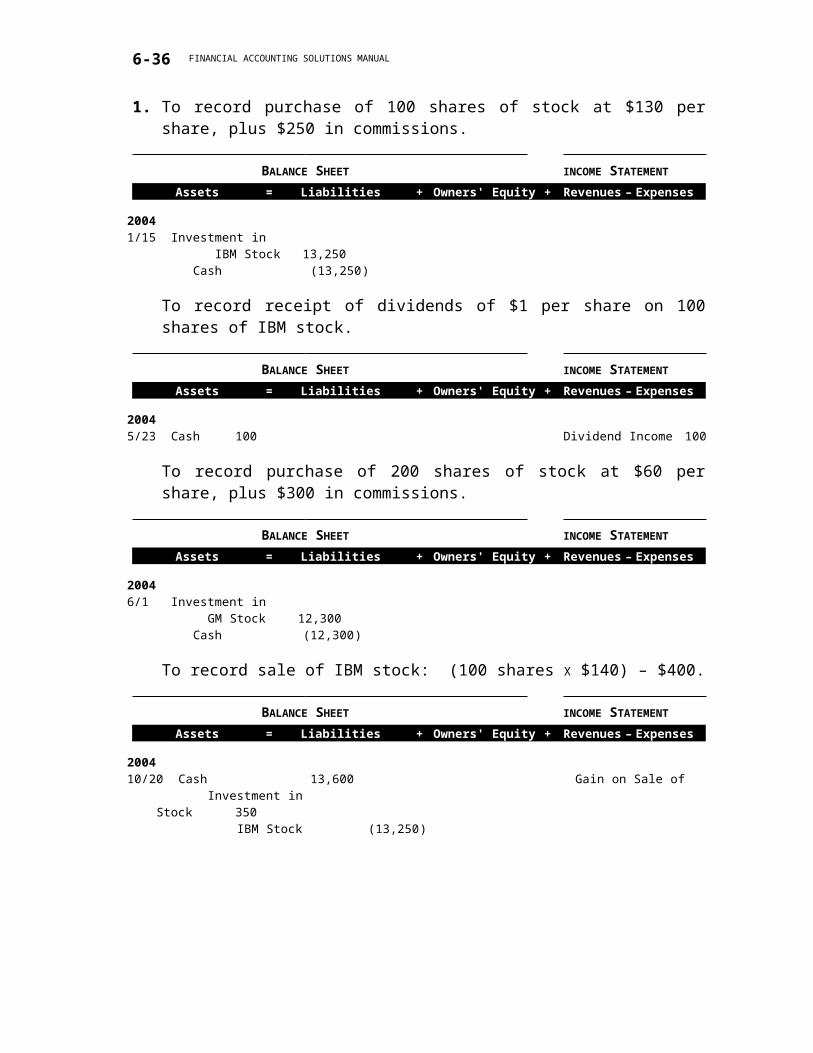

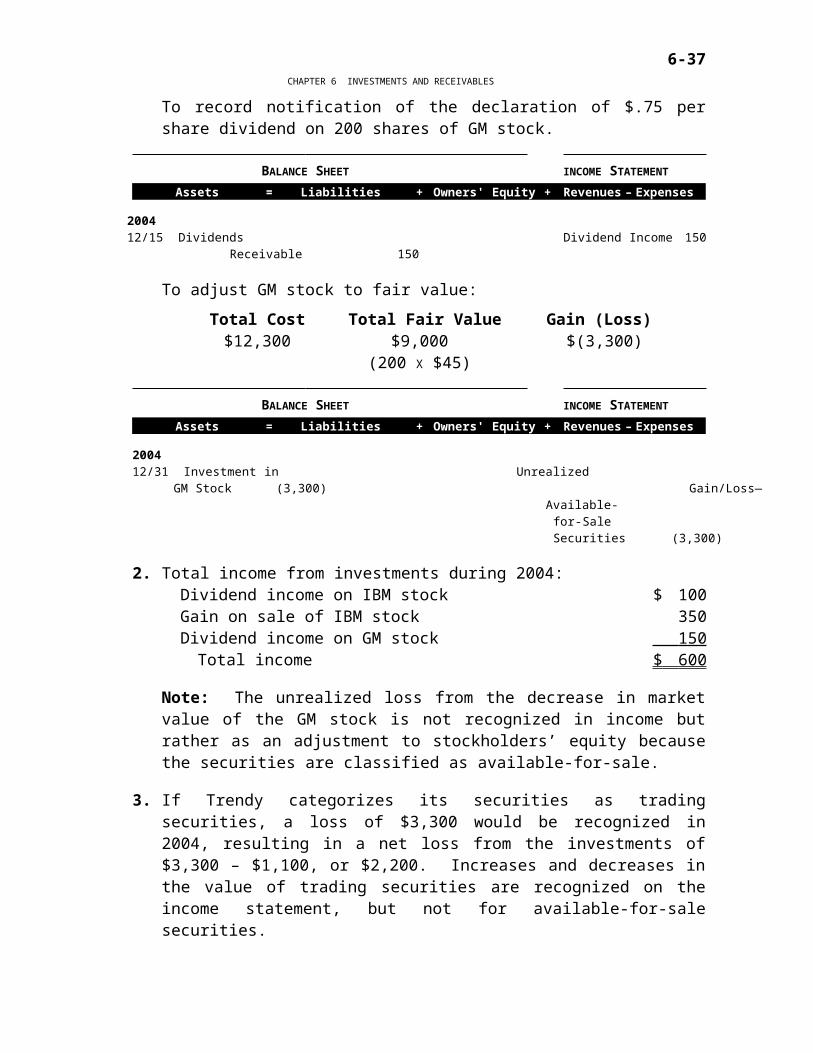

2. Total income from investments during 2004:Dividend income on IBM stock $ 100Gain on sale of IBM stock 350Dividend income on GM stock 150

Total income $ 600

Note: The unrealized loss from the decrease in market value of the GM stock is not recognized in income but rather as an adjustment to stockholders’ equity because the securities are classified as available-for-sale.

3. If Trendy categorizes its securities as trading securities, a loss of $3,300 would be recognized in 2004, resulting in a net loss from the investments of $3,300 – $1,100, or $2,200. Increases and decreases in the value of trading securities are recognized on the income statement, but not for available-for-sale securities.

6-29

FINANCIAL ACCOUNTING SOLUTIONS MANUAL

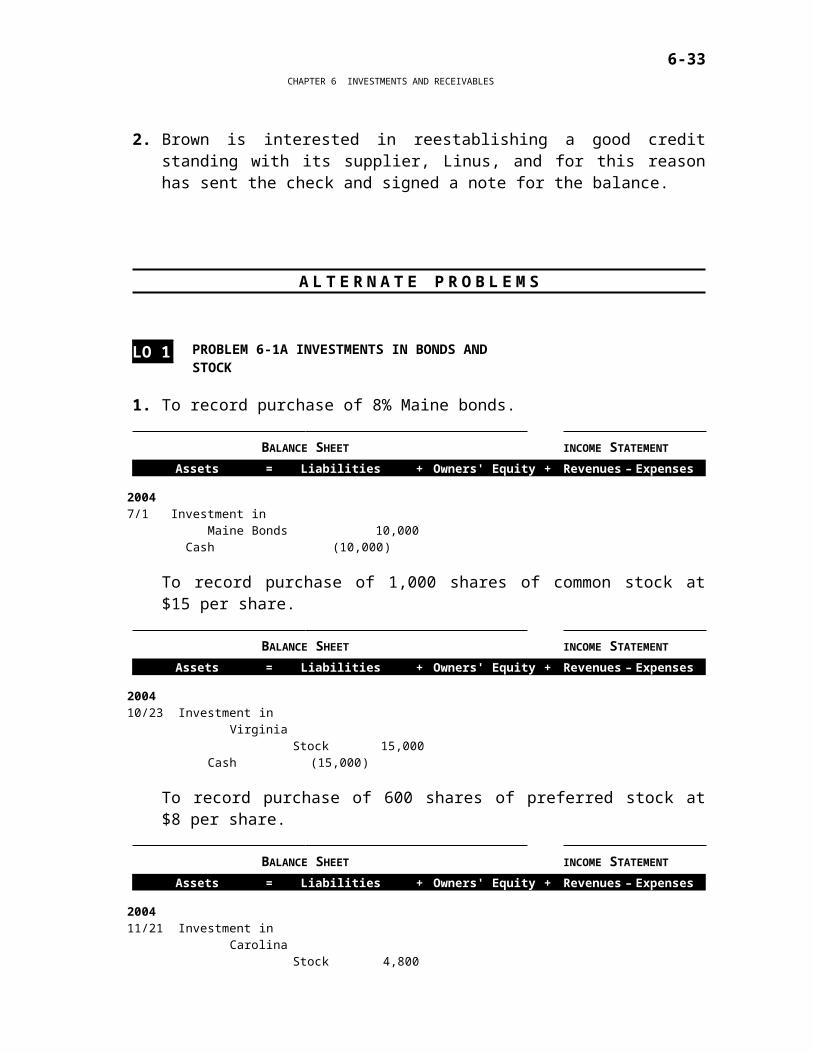

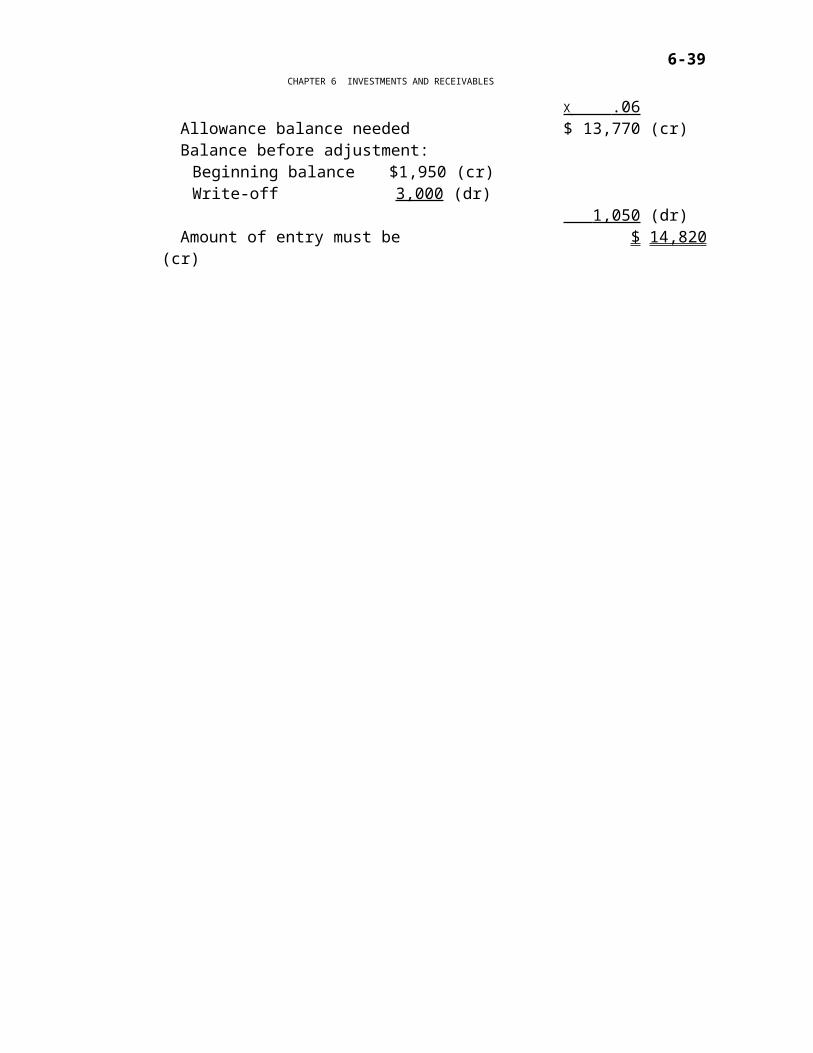

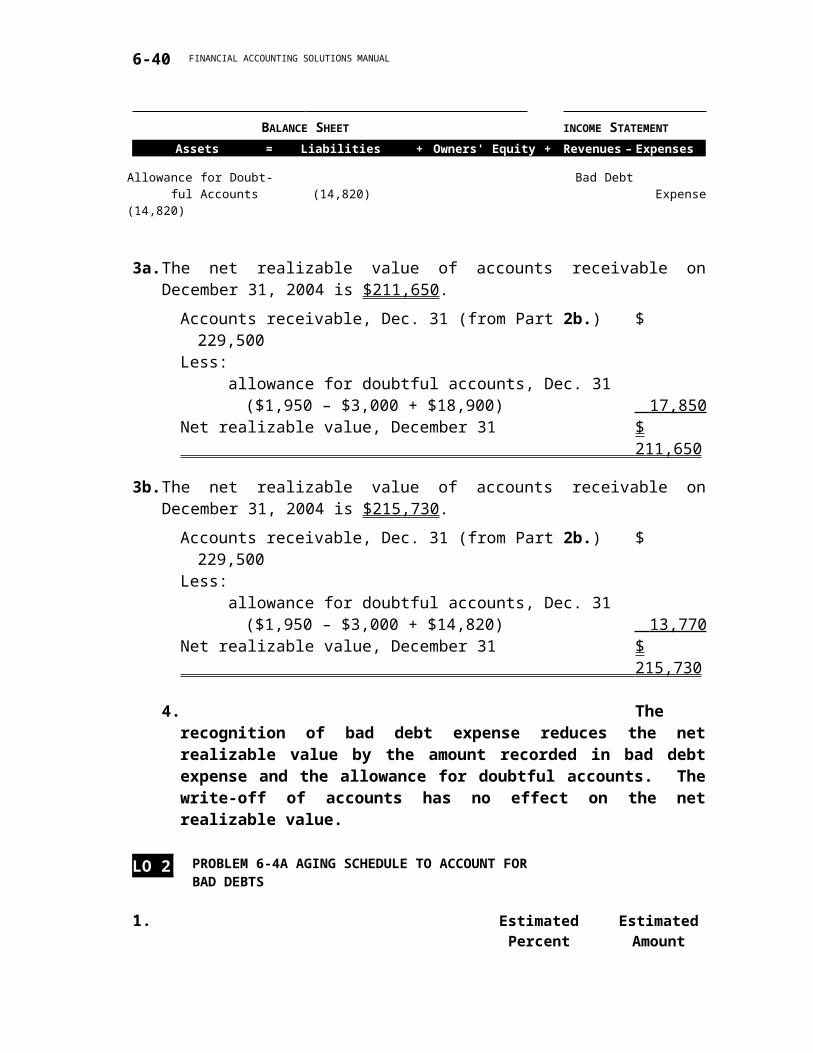

LO 2 PROBLEM 6-3A ALLOWANCE METHOD FOR ACCOUNTING FOR BAD DEBTS

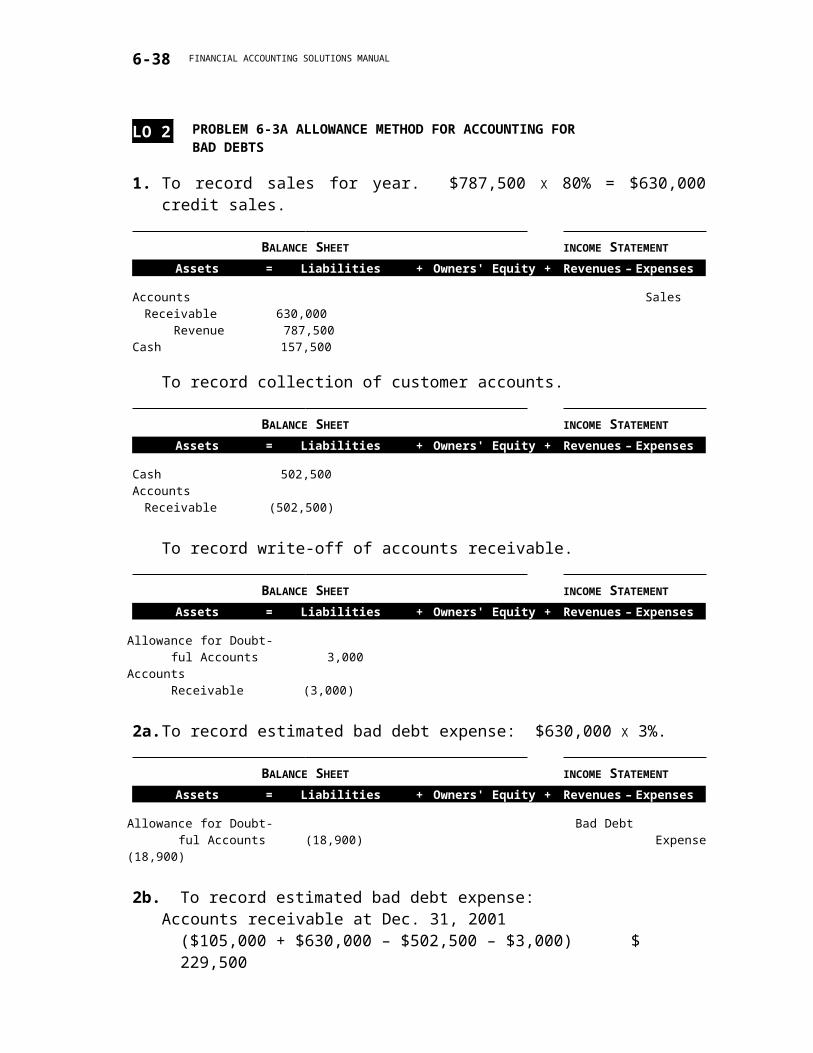

1. To record sales for year. $787,500 X 80% = $630,000 credit sales.

Allowance for Doubt- Bad Debt ful Accounts (14,820) Expense (14,820)

3a. The net realizable value of accounts receivable on December 31, 2004 is $211,650.

Accounts receivable, Dec. 31 (from Part 2b.) $ 229,500Less: allowance for doubtful accounts, Dec. 31

($1,950 – $3,000 + $18,900) 17,850 Net realizable value, December 31 $ 211,650

3b. The net realizable value of accounts receivable on December 31, 2004 is $215,730.

Accounts receivable, Dec. 31 (from Part 2b.) $ 229,500Less: allowance for doubtful accounts, Dec. 31

($1,950 – $3,000 + $14,820) 13,770 Net realizable value, December 31 $ 215,730

4. The recognition of bad debt expense reduces the net realizable value by the amount recorded in bad debt expense and the allowance for doubtful accounts. The write-off of accounts has no effect on the net realizable value.

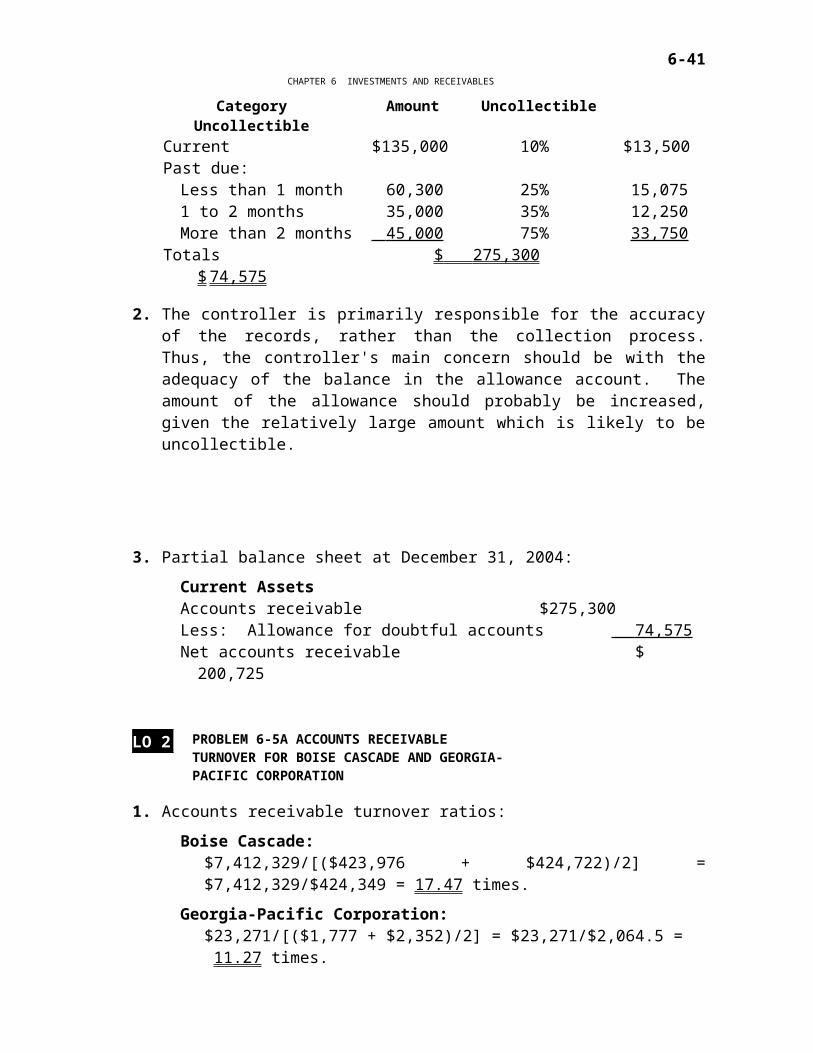

LO 2 PROBLEM 6-4A AGING SCHEDULE TO ACCOUNT FOR BAD DEBTS

Less than 1 month 60,300 25% 15,0751 to 2 months 35,000 35% 12,250More than 2 months 45,000 75% 33,750

Totals $ 275,300 $ 74,575

2. The controller is primarily responsible for the accuracy of the records, rather than the collection process. Thus, the controller's main concern should be with the adequacy of the balance in the allowance account. The amount of the allowance should probably be increased, given the relatively large amount which is likely to be uncollectible.

6-31

FINANCIAL ACCOUNTING SOLUTIONS MANUAL

3. Partial balance sheet at December 31, 2004:

Current AssetsAccounts receivable $ 275,300Less: Allowance for doubtful accounts 74,575 Net accounts receivable $ 200,725

LO 2 PROBLEM 6-5A ACCOUNTS RECEIVABLE TURNOVER FOR BOISE CASCADE AND GEORGIA-PACIFIC CORPORATION

Average collection periods of either 21 days or 32 days appear reasonable for customers of companies that manufacture paper products.

3. Boise Cascade’s accounts receivable turnover ratio is higher than Georgia-Pacific’s: 17.47 versus 11.27. It takes Boise Cascade an average of only 20.6 days to collect its receivables; Georgia-Pacific requires an average of 31.9 days.

It would also be helpful to measure these statistics—accounts receivable turnover ratio and average collection period—with the same measures for prior years. It would also be helpful to compare these measures with the industry averages.

LO 4 PROBLEM 6-6A NON-INTEREST-BEARING NOTE RECEIVABLE

1. To record collection of note:Cash selling price $ 48,000Less: Down payment 12,000 Unpaid cash balance $ 36,000Amount of promissory note 36,900 Implicit interest in the note $ 900

20048/29 Notes Receiv- Sales Revenue 48,000 able 36,900 Cash 12,000 Discount on Notes Re- ceivable (900)

2. To find the effective rate of interest:

1. Length of note 90 days2. Number of 90-day periods in a year 43. Amount of interest that would apply to a full year:

$900 (from Part 1.) X 4 $ 3,6004. Effective annual interest rate: $3,600/$36,000 10%

LO 5 PROBLEM 6-7A CREDIT CARD SALES

1. Cost of credit card operation per outlet:Equipment/phone line $ 800Sales fee:

Credit sales: $800,000 X 5% $40,000X Fee X .015 600 Total cost $ 1,400

Conclusion: to cover the cost of the new equipment in the first year, new sales would need to net $1,400 per outlet.

2. The company should also consider competition in its decision on the use of credit cards. It may in fact suffer a loss of sales if its competitors start offering credit to customers and it does not. The company may find that customer goodwill is increased by the offer to use a credit card.

6-33

FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 6 PROBLEM 6-8A EFFECTS OF CHANGES IN RECEIVABLE BALANCES ON STATEMENT OF CASH FLOWS

1. Statement of cash flows:

ST. CHARLES ANTIQUE MARKETSTATEMENT OF CASH FLOWS

FOR THE YEAR ENDED DECEMBER 31, 2004

Net loss $ (6,000)Adjustments to reconcile net loss to net cash provided by operating activities:

Decrease in accounts receivable 47,000*Increase in notes receivable (7,800 )**

Cash flows from operating activities $ 33,200Cash, December 31, 2003 3,100 Cash, December 31, 2004 $ 36,300

*$126,000 – $79,000**$104,800 – $112,600

2. Memorandum to the president:TO: Owner of St. Charles Antique Market

FROM: Student’s name

DATE: January XX, 2005

SUBJECT: Cash Flows

You recently questioned the increase in the company’s cash balance in light of this year’s net loss. My thoughts and a copy of the company’s 2004 statement of cash flows follow.

St. Charles Antique Market was able to generate a significant amount of cash from operations even though the company incurred an accrual basis net loss during 2004 of $6,000. Most importantly, the amount of accounts receivable decreased by $47,000 during the year from $126,000 to $79,000; collections of accounts receivable generated cash for the company. This cash flow was partially offset by a $7,800 increase in notes receivable during the year, from $104,800 to $112,600.

2. P.D. Cat is interested in reestablishing a good credit standing with its supplier, Tweedy, and for this reason has sent the check and signed a note for the balance.

D E C I S I O N C A S E S

READING AND INTERPRETING FINANCIAL STATEMENTS

LO 2 DECISION CASE 6-1 READING AND INTERPRETING WINNEBAGO INDUSTRIES’ FINANCIAL STATEMENTS

1. The balance in the Allowance for Doubtful Accounts is found on the balance sheet. The balance is $120,000 at the end of 2002 and $244,000 at the end of 2001. The net realizable value at the end of 2002 was $28,616,000, and at the end of 2001, $21,571,000.

2. 8/31/02 8/25/01Allowance for doubtful accounts $ 120,000 $244,000Divided by:

3. There are any number of possible reasons why Winnebago Industries might decide to decrease the estimated percentage uncollectible. It may be because the company has tightened its credit terms and therefore customers are more likely to pay their bills. Alternatively, they may feel as if the economy is improving and it is more likely that customers will be able to pay. Furthermore, we do not know whether they have based their bad debt expense and a decrease in the allowance for doubtful accounts on a percentage of sales or on a percentage of accounts receivable.

6-36

CHAPTER 6 INVESTMENTS AND RECEIVABLES

LO 2 DECISION CASE 6-2 COMPARING TWO COMPANIES IN THE SAME INDUSTRY: WINNEBAGO INDUSTRIES AND MONACO COACH CORPORATION

1. Monoco Coach’s Allowance for Doubtful Accounts contains balances of $799,000 and $541,000 at the end of 2002 and 2001, respectively. The net realizable value of the receivables are $116,647,000 and $82,885,000 at the end of 2002 and 2001, respectively.

2. The ratio of the Allowance for Doubtful Accounts to Gross Receivables for Monaco Coach Corporation at the end of each of the two years is:

2002: $799/$116,647 + $799 = $799/$117,446 = .7%

2001: $541/$82,885 + $541 = $541/$83,426 = .6%

Winnebago Industries ratios were .4% and 1.1% at the end of 2002 and 2001. The comparison of the ratios for the two companies indicates that in 2002, the receivables of Winnebago Industries were slightly more collectible, i.e. the ratio of uncollectible accounts to receivables was higher for Monaco Coach. In contrast, Monaco Coach’s receivables were more collectible in 2001.

3. An increase in trade receivables could be due to a number of factors, such as an increase in sales, a loosening of credit policies or difficulty in collecting from customers.

4. The receivables turnover ratios for the two companies for 2002 are found by dividing net sales by average accounts receivable:

Winnebago Industries: $825,269/[($28,616 + $21,571)/2] = $825,269/$25,093.5 = 32.9 times

On the basis of these ratios, it would appear that Winnebago Industries turns its inventory more often than does Monaco Coach. However, it must be noted that only the account titled “Receivables” was included in the computation of Winnebago Industries ratio. They have a significant amount on their balance sheet in the account “Dealer Financing Receivables.”

6-37

FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 1,6 DECISION CASE 6-3 READING PEPSICO'S STATEMENT OF CASH FLOWS

1. PepsiCo spent $62 million in 2002 to acquire short-term investments. This is significantly less than in 2001 and 2000 when the company spent $2,537 million and $4,950 million, respectively.

2. The company received $833 million from investments that matured in 2002. This is significantly less than in 2001 and 2000 when PepsiCo received $2,078 million and $4,585 million, respectively.

3. PepsiCo both spent less and received less for its investments in 2002 than in the two prior years. For many companies short-term investments are made when there is an excess of cash available that is not needed immediately. It may have been that PepsiCo did not need to either invest idle cash nor redeem short-term investments to generate cash to the extent that it found necessary in the two prior years.

MAKING FINANCIAL DECISIONS

LO 1,2 DECISION CASE 6-4 LIQUIDITY

TO: The President of FNB of Verona Heights

FROM: Joe Smith, Loan Officer

DATE: X/X/XX

SUBJECT: Loan proposals

I have reviewed the loan proposals recently submitted by R Montague and J Capulet and would like to summarize for you my findings. Because of limited resources available for short-term loans, my recommendation is that we make a six-month $10 million loan to J Capulet only.

The total current asset positions of the two companies are identical. Each has $33 million in current assets. However, the composition of the current assets differs considerably between the two companies. On the surface, R Montague may appear to be stronger because it has twice the amount of cash on hand that J Capulet does. However, cash is essentially a non-earning asset, and I am skeptical as to why R Montague feels it necessary to maintain that much cash on hand, and consequently, why it feels as if it needs to borrow an additional $10 million.

The accounts receivable for J Capulet is significantly larger than that for R Montague. Assuming that the estimates of bad debts are reasonably reliable, R Montague has a bigger problem with uncollectibles than does J

Capulet. R Montague has an allowance that is 1/15, or 6.67% of accounts receivable, while J Capulet's percentage is only 1/23, or 4.35%.

In summary, I feel that J Capulet is a better candidate at the present time for a loan. I recommend that we make a six-month $10 million loan to J

6-38

CHAPTER 6 INVESTMENTS AND RECEIVABLES

Capulet at the current market rate of interest. Please call if you need any further details in connection with these two loan requests.

LO 3,4 DECISION CASE 6-5 NOTES RECEIVABLE

1. Regardless of which offer it accepts, Warren should recognize $75,000 from the sale of the lot. This represents the cash equivalent selling price because it is the fair value of the property according to a recent appraisal. Both builders would pay more than this amount for the lot, but this is because they would be paying over a period of time.

2. First, the president is wrong to claim that the loan to Builder B would not involve interest. Because Builder B would pay more than fair value for the lot ($75,000) over the next year, there is an interest charge. It is implicit—that is, interest is built into the agreement.

The sales manager is also wrong to claim that it doesn't matter which offer is accepted because both involve the receipt of more than the appraised value of the property. One of the two offers is better if we consider the time value of money. Both builders would pay $100,000 over the next year. However, of this total amount, Builder B would pay a higher amount immediately: $20,000 down as opposed to only $12,000 down from Builder A. Warren should accept the offer from Builder B.

ACCOUNTING AND ETHICS: WHAT WOULD YOU DO?

LO 1 DECISION CASE 6-6 FAIR MARKET VALUES FOR INVESTMENTS

1. Net income under two different assumptions:

(a) Stock is classified as a trading security:

Net income before adjustment $ 400,000Unrealized loss (250,000)*Net income $ 150,000

*10,000 shares X ($100 – $75).

(b) Stock is classified as an available-for-sale security:Net income $ 400,000

(Any unrealized gains or losses on available-for-sale securities are reported as a component of stockholders’ equity and are not reported on the income statement.)

2. The proper classification of the Clean Air stock is a matter of judgment. Given the circumstances, however, it seems most appropriate to classify the stock as trading securities. The case indicates that Kennedy regularly holds stocks of various companies in a trading securities portfolio. There is

6-39

FINANCIAL ACCOUNTING SOLUTIONS MANUAL

nothing in the case to suggest that the objective in holding the Clean Air stock is any different.

3. The treasurer’s advice presents the controller with a clear ethical dilemma. Should the proper classification of an investment for financial reporting purposes be dictated, or at least influenced, by the effect of the classification on net income? The treasurer is accurate in stating that regardless of this decision, the stock will be reported on the balance sheet at fair value. However, accounting standards call for the recognition of a loss on the income statement for declines in value of trading securities. Reporting the security as available-for-sale fails to recognize the loss on the income statement.

If the investment is listed as available-for-sale, when it should be classified as a trading security the information presented does not faithfully represent what it claims to represent. By misclassifying the investment (if there is no intent to hold the security past the normal term for a trading security), the company benefits and outsiders are harmed. The company’s performance appears to be better when the securities are recorded as available- for sale. This method of reporting misleads outside investors and creditors and they may make incorrect investment and lending decisions. Management looks like they are doing a better job when the income is higher.

LO 4 DECISION CASE 6-7 NOTES RECEIVABLE

1. The suggestion for recording the sale of the property violates two principles: the revenue recognition principle and the historical cost principle. Revenue is recognized at the appropriate time, when a sale takes place, but for the wrong amount. The fair value of the property, $7.5 million, should be used as a measure of the amount of revenue to be recognized, rather than the face value of the note.

2. TO: Vice-president

FROM: Student’s name

DATE: 12/31/XX

SUBJECT: Land sale

This is in response to your suggestion about the proper accounting for the recent sale of our 100-acre tract for the new shopping center. I have considered your recommendation that we recognize revenue in the amount of $10 million, which is equivalent to the $2 million installments on the note over each of the next five years.

Please understand my interest in maximizing profits to our shareholders whenever possible. The suggested treatment for this sale, however, is a clear violation of generally accepted accounting principles. The reason for the violation is straightforward: $10 million is not the value of the asset we sacrificed in exchange for the five-year note. The property was recently

6-40

CHAPTER 6 INVESTMENTS AND RECEIVABLES

appraised at a fair market value of $7.5 million. The difference between the $10 million in face value of the note and the $7.5 million fair value of the property represents the interest we will earn over the next five years as we collect on the note. We will, in fact, recognize this difference of $2.5 million as income, but only over the life of the note, and as interest income rather than sales revenue. For now the amount of revenue we should recognize is $7.5 million.

Please call me at any time if you would like to discuss this matter further.

FROM CONCEPT TO PRACTICE 6.1

PepsiCo’s accounts and notes receivable increased by $389 million during 2002. These receivables are very significant, comprising 39.5% of the company’s total current assets at the end of 2002. Accounts receivable arising from selling to customers on an open account while notes receivable result from requiring customers to sign a promissory note to purchase products.

FROM CONCEPT TO PRACTICE 6.2

In the note, Winnebago Industries explains that the allowance account is based on previous loss experience. Although it is not possible for certain to tell which method it uses, it is likely that the company uses the percentage of accounts receivable approach to estimate bad debts. Bad debts expense is most likely included in general and administrative expenses on the income statement.