Streamlined Sales Tax Establishing Best Practices in the Administration of State and Local Sales and Use Tax: Calling on All States to Help Shape the Solutions 2011 NESTOA CONFERENCE Wilmington, Delaware September 20, 2011 Russ Brubaker - Nat'l Tax Policy Advisor, State of Washington Deborah Bierbaum – Executive Director Tax Policy, AT&T Susan Mesner - Economist, State of Vermont Fred Nicely - Tax Counsel, COST Scott Peterson - Executive Director, SSTGB

Transcript

Streamlined Sales TaxEstablishing Best Practices in the Administration of State and Local Sales and Use Tax: Calling on All States to Help Shape the Solutions2011 NESTOA CONFERENCE

Wilmington, DelawareSeptember 20, 2011

Russ Brubaker - Nat'l Tax Policy Advisor, State of WashingtonDeborah Bierbaum – Executive Director Tax Policy, AT&TSusan Mesner - Economist, State of Vermont Fred Nicely - Tax Counsel, COSTScott Peterson - Executive Director, SSTGB

Overview

Streamlined Sales Tax Who We Are◦ Governing Board◦ State & Local Advisory Council◦ Business Advisory Council

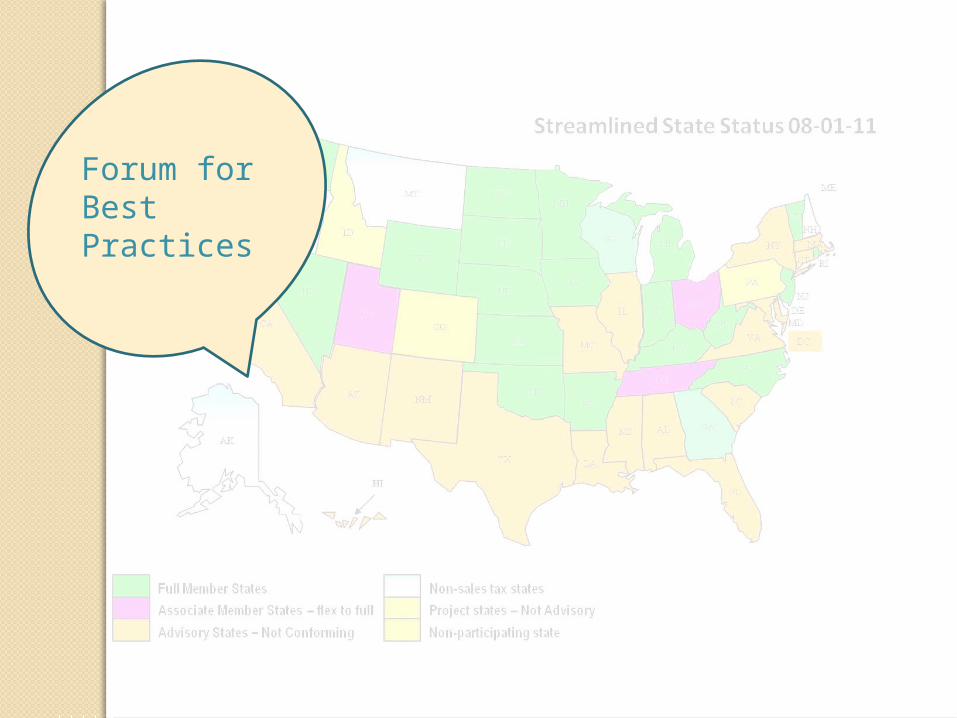

Forum for Best Practices◦ Best Practice Examples◦ Projects in progress

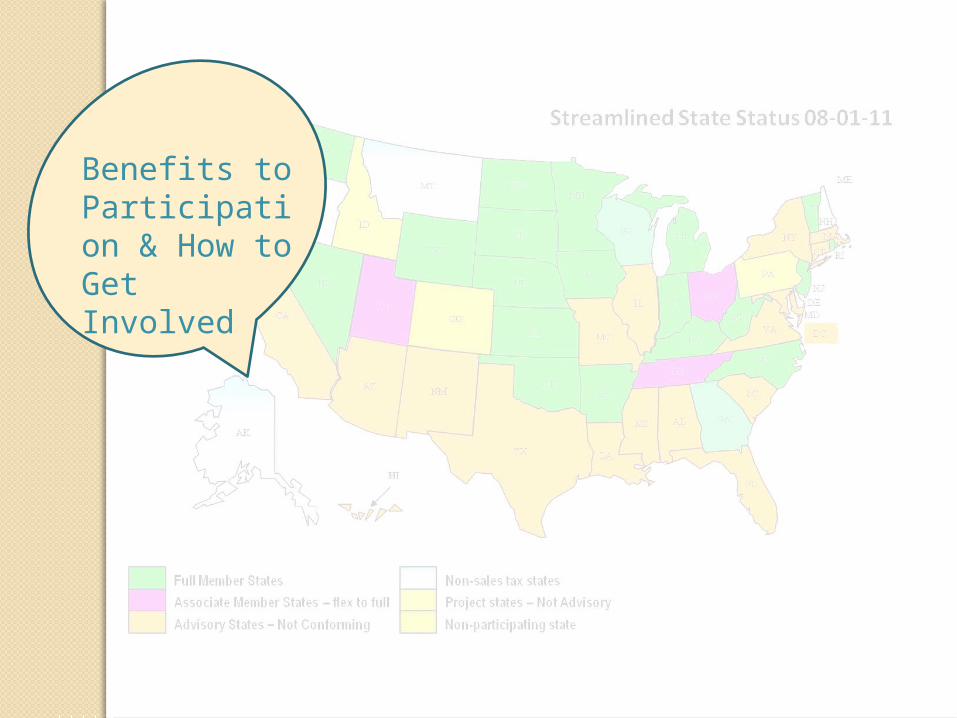

Benefits to Participation & How to Get Involved

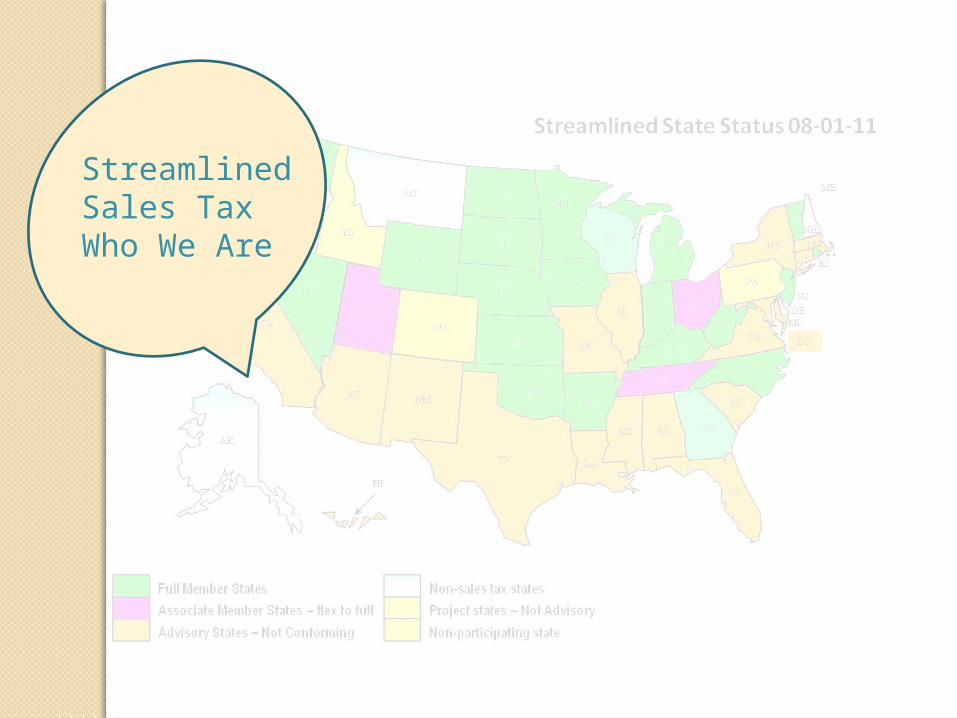

Streamlined Sales Tax Who We Are

Streamlined Sales Tax Agreement

• The objective of the Streamlined Sales & Use Tax Agreement (agreement) is to: “simplify and modernize sales and use tax

administration in the member states in order to substantially reduce the burden of tax compliance”

• Generally, the SSUTA intends to achieve its objective by adopting model laws related to the following:◦ Uniform Definitions◦ Administrative Simplifications◦ Technology & Collection Models

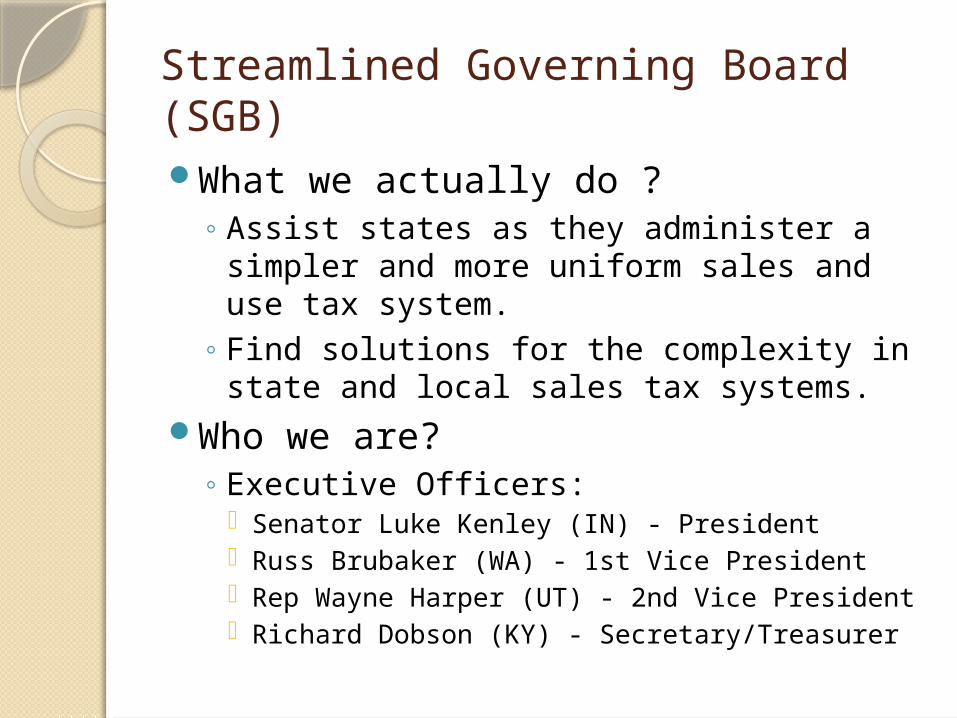

Streamlined Governing Board (SGB)

What we actually do ?◦ Assist states as they administer a simpler

and more uniform sales and use tax system.

◦ Find solutions for the complexity in state and local sales tax systems.

Who we are?◦ Executive Officers:

Senator Luke Kenley (IN) - President Russ Brubaker (WA) - 1st Vice President Rep Wayne Harper (UT) - 2nd Vice President Richard Dobson (KY) - Secretary/Treasurer

Streamlined States

State & Local Advisory Council (SLAC)Advise the SGB on matters pertaining to

the administration of the agreement.Consider and respond to issues as

requested by the SGB.Recommend issues for consideration.Provide a forum for non-member state

and local government officials to express their ideas and concerns.

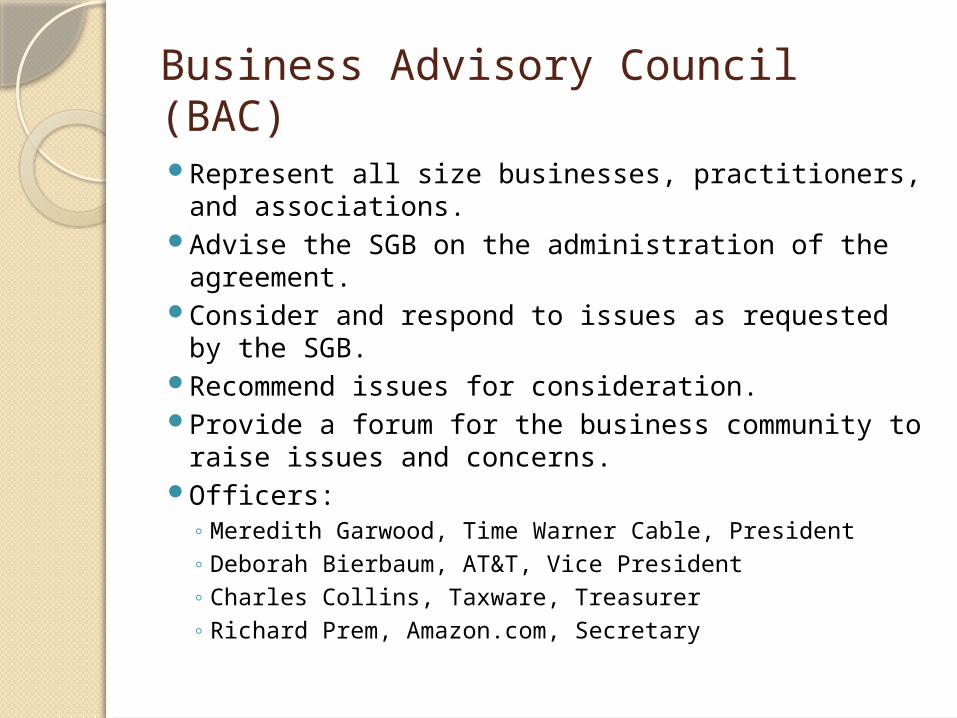

Represent all size businesses, practitioners, and associations.

Advise the SGB on the administration of the agreement.

Consider and respond to issues as requested by the SGB.

Recommend issues for consideration.Provide a forum for the business community to

raise issues and concerns.Officers:

◦ Meredith Garwood, Time Warner Cable, President◦ Deborah Bierbaum, AT&T, Vice President◦ Charles Collins, Taxware, Treasurer◦ Richard Prem, Amazon.com, Secretary

Forum for Best Practices

Best Practices

Promote Sound Tax Policy◦ Simplicity – provide taxpayers clear rules on what the

law requires◦ Efficiency – reduces costs of compliance◦ Stability – provide rules meets the test of time◦ Equality – treat taxpayers equally and fairly

Reduces risk of class action law suits for sellers.Provides a model policy and process for all

states and we encourage non-streamlined states to consider adopting some or all of the best practices and participating in development of solutions even if they do not intend to become a member.

Best Practice ExamplesUniform SourcingThe agreement sets forth uniform

destination-based rules for sourcing retail sales of products.

The rule provides a hierarchy of steps to determine where the sale occurs.

Special rules provided for select goods and services.

Looming – Election for origin sourcing for intrastate sales where the information is known to the seller in their tax systems.

Best Practice Examples Communications SourcingUniform rules for determining the

taxing locations for sales of Telecommunications, Ancillary Services and Internet Access Services.

Special rules for mobile telecommunications, private communications services and postpaid calling services.

Prepaid calling services follow the general sourcing rules.

Best Practice ExamplesUniform Definitions – Food ProductsExperience in the states with the agreement

definition showed that it worked the majority of the time. However, some questions were coming before the interpretations committee, particularly with candy.

Through a collaborative process including member and non-member states and industry a clarifying rule was developed.

The rule:◦ Created a method for state and sellers to exclude

categories of food from candy that are not commonly thought of as candy.

◦ Clarified items that are included or excluded from the definition of candy.

Best Practice ExamplesUniform Definitions – TelecomThe telecommunications definitions broadly

define the services without regard to technology. The agreement also defines components of telecommunications.

The structure of the definitions allows flexibility state and local governments to closely match their existing tax bases if they so choose.

An amendment to the rules jointly developed by states and the industry is under consideration. It would clarify that “unlimited monthly” plans meet the definition of prepaid wireless calling service.

Best Practice ExamplesDatabase RequirementsMember States with local taxing jurisdictions

must provide and maintain databases in a common format for:◦ Boundary changes and the effective date.◦ Sales and use tax rates.◦ Assign zip codes to a taxing jurisdiction and the

proper tax rates for each level of jurisdiction.Member states relieve sellers using the

databases from liability to the state and its local jurisdictions for having charged or collected the incorrect tax.

Business relying on state provided databases are following reasonable business practices.

Best PracticesStreamlined toolsNon-member states can help their taxpayers

comply by providing information to sellers similar to agreement requirements for member states including:◦ Taxability matrix – provides information on the state’s tax

treatment of various goods and services and identifies exemptions. It also provides sellers with the citations for the information.

◦ Annual review – through a certificate of compliance process member states are providing information that taxpayers can utilize to see how the state conforms to certain administrative provisions of the agreement such as acceptance of the streamlined exemption certificate.

Certified service provider benefits - how this collection model and tool have lessons for all states.

Best Practice Examples Bundled Transactions• The agreement includes a definition

of a bundled transaction which all member states must adopt in their statutes.

• A special rule applies for the computation of tax for a bundle that includes any of the following services: telecommunications, ancillary, Internet access or video programming.− The rule provides that tax is only applied to the

taxable components of the bundle if the provider can show the taxable and non-taxable portions in its books and records.

Projects in Progress

Sales Price Definition◦ The agreement provides a comprehensive

administrative definition of sales price. Work groups have been formed on areas identified as needing further clarification: What properly constitutes taxes on the seller? What is the proper handling of vouchers and

layaway fees?

Credit for Taxes Paid◦ New provision for the agreement.

How much uniformity is needed? How will the credit work when sourcing differs

between member and non-member states?

Projects In Progress

Sourcing of Services◦ Personal services and services to tangible

personal property -- rules have been developed.

◦ Services with respect to tangible personal property rule is currently under development.

◦ Digital Goods and Services are next up.

Benefits to Participation & How to Get Involved

Benefits to Participation

Provides a forum for discussing common issues that arise as new products and services challenge state and local tax laws.

Brings leaders in Government and Industry together to share ideas and find creative solutions.

Provides a mechanism to seek interpretations and clarifications early and for multiple states to avoid costly litigation.

How to Get Involved

Non-member State and Local Governments – participate in SLAC and the various working groups and share your knowledge and challenges you are facing.

Businesses and Practitioners – join BAC and participate in the various working groups and subcommittees.

![Sales and Use Tax 101[1].ppt - North Carolina• Sales made to other businesses for resale are exempt from tax when a properly completed Form E-595E, Streamlined Sales and Use Tax](https://static.documents.pub/doc/80x56/5f4b68155ca6893afa12154d/sales-and-use-tax-1011ppt-north-carolina-a-sales-made-to-other-businesses.jpg)