Stuart Briers, 40040306, Size: The most important leverage determinant? 1 Queen’s University Management School, Queen’s University Belfast Size: The most important leverage determinant? An empirical analysis of the U.S. Financial Crisis 2007-2009 Stuart Briers 40040306 BSc Finance John Turner Wed, 14 th May 2014 Abstract The Financial Crisis of 2007-2009 was the worst since the 1929 Great Depression and forced firms to reassess their capital structure and exposure to the market. Through this study of the top 1,200 U.S. firms during the period, firm size is assessed as the most important component in dictating leverage. The Pecking Order Theory is tested and analysed as the underlying reason why firm size affects leverage when considering retained earnings and debt. Existing evidence is compared on firm size and the Pecking Order Theory, with conclusions and future areas of research given based on the results of the sample. Previous studies in capital structure have been “hampered by a lack of consistent accounting and market information outside the United States” according to Rajan and Zingales (1995). Therefore, this paper will review capital structure changes in the U.S.A. in order to gain a broad understanding of how firms are structured; allowing inferences to be drawn on the effect firm size has on leverage. The U.S.A. is an ideal country to analyse due to its access to capital markets and as Myers (2001) points out; firms have the “broadest menu of financing choices”.

Transcript

Stuart Briers, 40040306, Size: The most important leverage determinant?

1

Queen’s University Management School,

Queen’s University Belfast

Size: The most important leverage determinant?

An empirical analysis of the

U.S. Financial Crisis 2007-2009

Stuart Briers

40040306

BSc Finance

John Turner

Wed, 14th May 2014

Abstract

The Financial Crisis of 2007-2009 was the worst since the 1929 Great Depression and

forced firms to reassess their capital structure and exposure to the market. Through

this study of the top 1,200 U.S. firms during the period, firm size is assessed as the most

important component in dictating leverage. The Pecking Order Theory is tested and

analysed as the underlying reason why firm size affects leverage when considering

retained earnings and debt. Existing evidence is compared on firm size and the Pecking

Order Theory, with conclusions and future areas of research given based on the results

of the sample.

Previous studies in capital structure have been “hampered by a lack of consistent accounting

and market information outside the United States” according to Rajan and Zingales (1995).

Therefore, this paper will review capital structure changes in the U.S.A. in order to gain a

broad understanding of how firms are structured; allowing inferences to be drawn on the

effect firm size has on leverage. The U.S.A. is an ideal country to analyse due to its access to

capital markets and as Myers (2001) points out; firms have the “broadest menu of financing

choices”.

Stuart Briers, 40040306, Size: The most important leverage determinant?

2

This paper investigates if firm size is the most important component in dictating

leverage and if it is positively correlated to it due to the Pecking Order Theory. This theory,

which was first introduced by Donaldson (1961) and modified by Myers and Majluf (1984),

states that firms use retained earnings until depleted, at which point they issue debt. Equity

will only be used when it is not feasible or sensible to issue more debt. The paper will analyse

if the Pecking Order Theory is relevant in the Financial Crisis or if other theories can be used,

such as the Trade-off Theory (Kraus and Litzenberger 1973), where the firm chooses its

mixture of debt and equity as a function of the present value of both tax shields and

bankruptcy costs. Most researchers in capital structure have acknowledged firm size as a

significant factor affecting leverage, but few have called it the most important leverage

determinant. This paper will analyse evidence to attempt to prove this thesis.

Other factors will also be considered including tangibility of assets, market-to-book

value and profitability. The Financial Crisis of 2007-2009 has been described as the worst

since the Great Depression by the IMF1, but due to publishing lags, little is known about how

firm size affected capital structure during this time. Miglo (2013) points out its importance as

the crisis “forced financial economists to look critically at capital structure theory because the

problems faced by many companies stemmed from their financing policies”. This paper will

attempt to fill this gap in literature by showing that the size of a firm has the effect to

significantly reduce investment (i.e. leverage see fig. 7a) during a crisis when financial

institutions cut lending. This theory is very clear in the 2007-2009 Financial Crisis.

After the abstract and introduction, the following section discusses existing literature

on firm size and its importance in determining leverage. Reasons for its effect on leverage are

given by different researchers and also existing evidence on the strength of the Pecking Order

Theory. Other variables are also considered.

1 The Guardian: see http://www.theguardian.com/business/2008/apr/10/useconomy.subprimecrisis

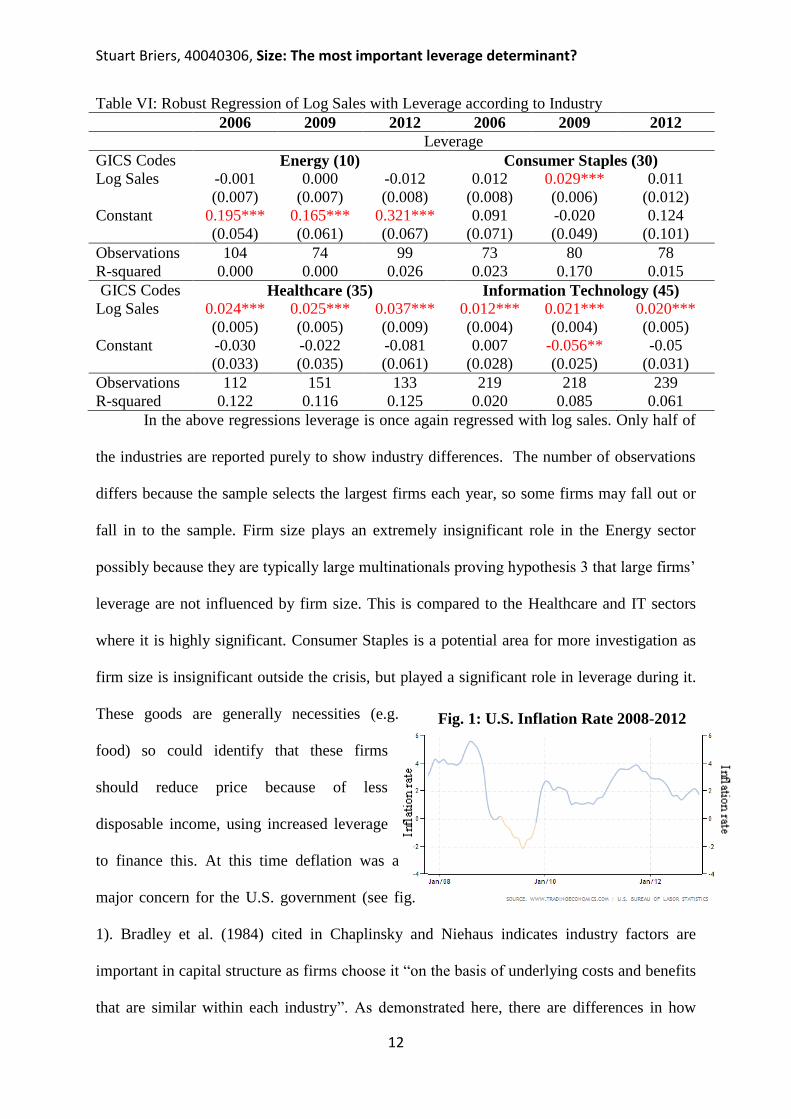

In the above regressions leverage is once again regressed with log sales. Only half of

the industries are reported purely to show industry differences. The number of observations

differs because the sample selects the largest firms each year, so some firms may fall out or

fall in to the sample. Firm size plays an extremely insignificant role in the Energy sector

possibly because they are typically large multinationals proving hypothesis 3 that large firms’

leverage are not influenced by firm size. This is compared to the Healthcare and IT sectors

where it is highly significant. Consumer Staples is a potential area for more investigation as

firm size is insignificant outside the crisis, but played a significant role in leverage during it.

These goods are generally necessities (e.g.

food) so could identify that these firms

should reduce price because of less

disposable income, using increased leverage

to finance this. At this time deflation was a

major concern for the U.S. government (see fig.

1). Bradley et al. (1984) cited in Chaplinsky and Niehaus indicates industry factors are

important in capital structure as firms choose it “on the basis of underlying costs and benefits

that are similar within each industry”. As demonstrated here, there are differences in how

Fig. 1: U.S. Inflation Rate 2008-2012

Stuart Briers, 40040306, Size: The most important leverage determinant?

13

firm size affects capital structure depending on industry.

F. Analysing Leverage Ratios

Considering all firms again, figure 2 shows a

polynomial trend for each period (excluding outliers

to analyse the main sample). Leverage ratios appear

to follow a wave-like cycle with firms in the 200-400

category using the highest leverage. It is interesting

to note that ratios have risen for the top 600 firms meaning they are taking on more debt or

retiring equity through share repurchases which is becoming increasingly common since

2009 (figure 33).

Looking historically, Myers (2001) has similar

findings in that “more shares are extinguished in

acquisitions and share repurchase programs than

are created by new stock issues”. For the

remaining firms leverage fell sharply in 2009 before returning to pre-crisis levels in 2012.

These firms reduced debt or found it was unavailable to them due to lending reductions by

financial institutions (see fig. 6).

G. Does the Pecking Order Theory exist in the sample?

According to figure 44, the difference in

retained earnings is largest in the top 200

firms, where it increased during the periods

due to capital adequacy increases by firms

who can afford it. A wave-like pattern exists

3 Share Repurchases by firms listed on major exchanges with S&P 500 Index: see http://opesforge.com/?p=340 4 Line of best fit omits extreme observations for visual reference

Stuart Briers, 40040306, Size: The most important leverage determinant?

14

similar to leverage. The general trend for the Pecking Order Theory appears to exist as

leverage and retained earnings are inversely related across the sample. However in taking a

snapshot for example in looking at the 200th firm, leverage and retained earnings both grow

during each period. Looking at smaller firms, retained earnings for the firms in the 400-600

category fell sharply (making losses) coupled with the largest sample increase in leverage,

supporting the theory. In 2009, leverage ratios fell sharply for firms outside the top 400

although retained earnings remained steady. This could be seen to represent a large fall in

capital expenditure during the crisis.

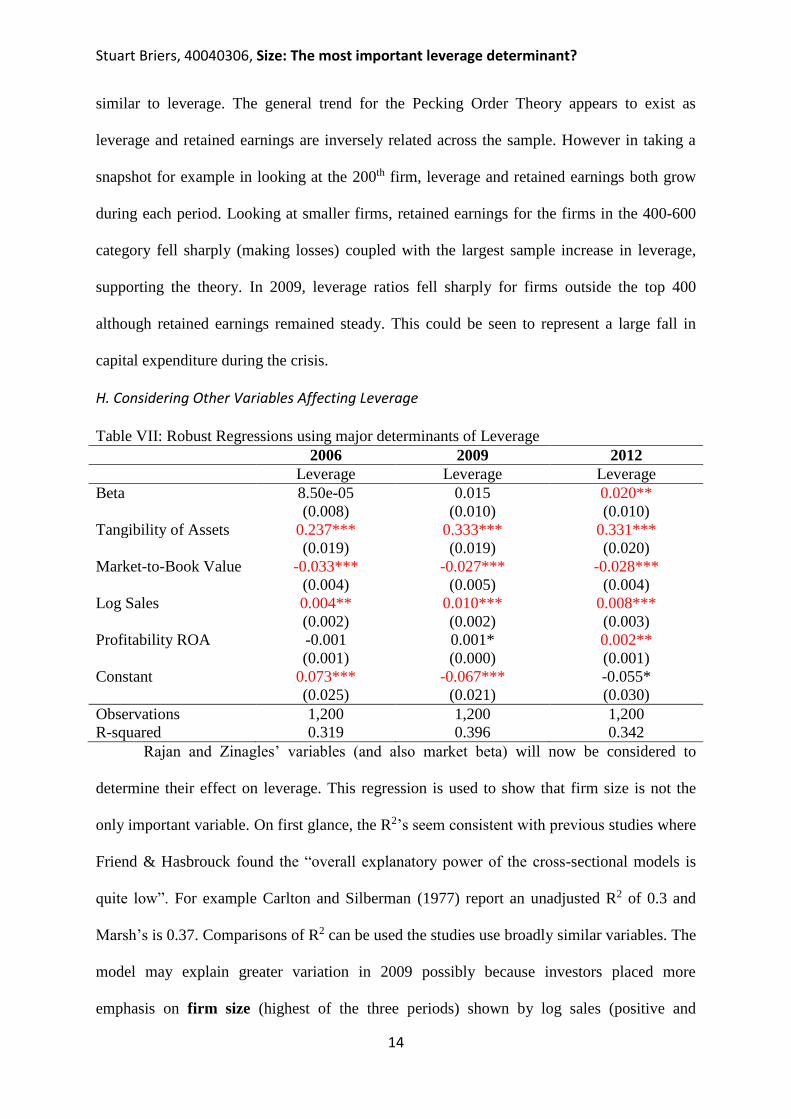

H. Considering Other Variables Affecting Leverage

Table VII: Robust Regressions using major determinants of Leverage

2006 2009 2012

Leverage Leverage Leverage

Beta 8.50e-05 0.015 0.020**

(0.008) (0.010) (0.010)

Tangibility of Assets 0.237*** 0.333*** 0.331***

(0.019) (0.019) (0.020)

Market-to-Book Value -0.033*** -0.027*** -0.028***

(0.004) (0.005) (0.004)

Log Sales 0.004** 0.010*** 0.008***

(0.002) (0.002) (0.003)

Profitability ROA -0.001 0.001* 0.002**

(0.001) (0.000) (0.001)

Constant 0.073*** -0.067*** -0.055*

(0.025) (0.021) (0.030)

Observations 1,200 1,200 1,200

R-squared 0.319 0.396 0.342

Rajan and Zinagles’ variables (and also market beta) will now be considered to

determine their effect on leverage. This regression is used to show that firm size is not the

only important variable. On first glance, the R2’s seem consistent with previous studies where

Friend & Hasbrouck found the “overall explanatory power of the cross-sectional models is

quite low”. For example Carlton and Silberman (1977) report an unadjusted R2 of 0.3 and

Marsh’s is 0.37. Comparisons of R2 can be used the studies use broadly similar variables. The

model may explain greater variation in 2009 possibly because investors placed more

emphasis on firm size (highest of the three periods) shown by log sales (positive and

Stuart Briers, 40040306, Size: The most important leverage determinant?

15

significant throughout), because they wanted to retain earnings due to market conditions (as a

capital buffer) and therefore issue more debt. This potential explanation contradicts the

Pecking Order Theory. Debt issuers would be prudent and favour larger firms due to

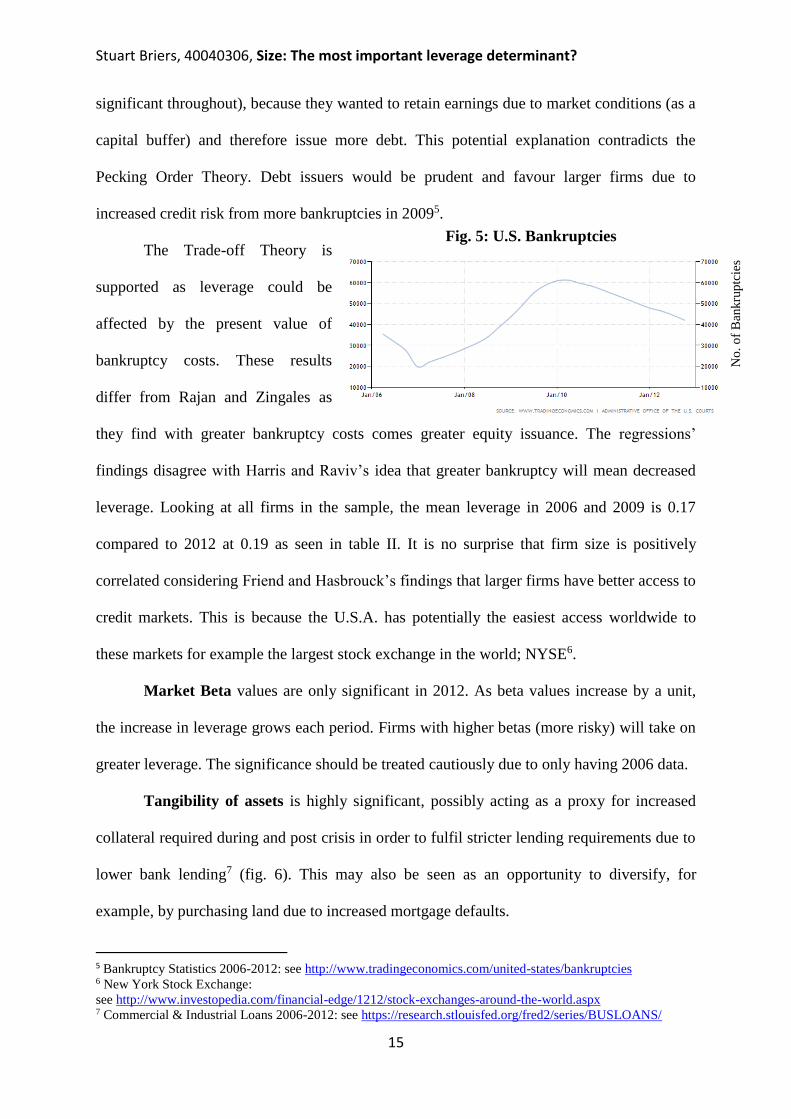

increased credit risk from more bankruptcies in 20095.

The Trade-off Theory is

supported as leverage could be

affected by the present value of

bankruptcy costs. These results

differ from Rajan and Zingales as

they find with greater bankruptcy costs comes greater equity issuance. The regressions’

findings disagree with Harris and Raviv’s idea that greater bankruptcy will mean decreased

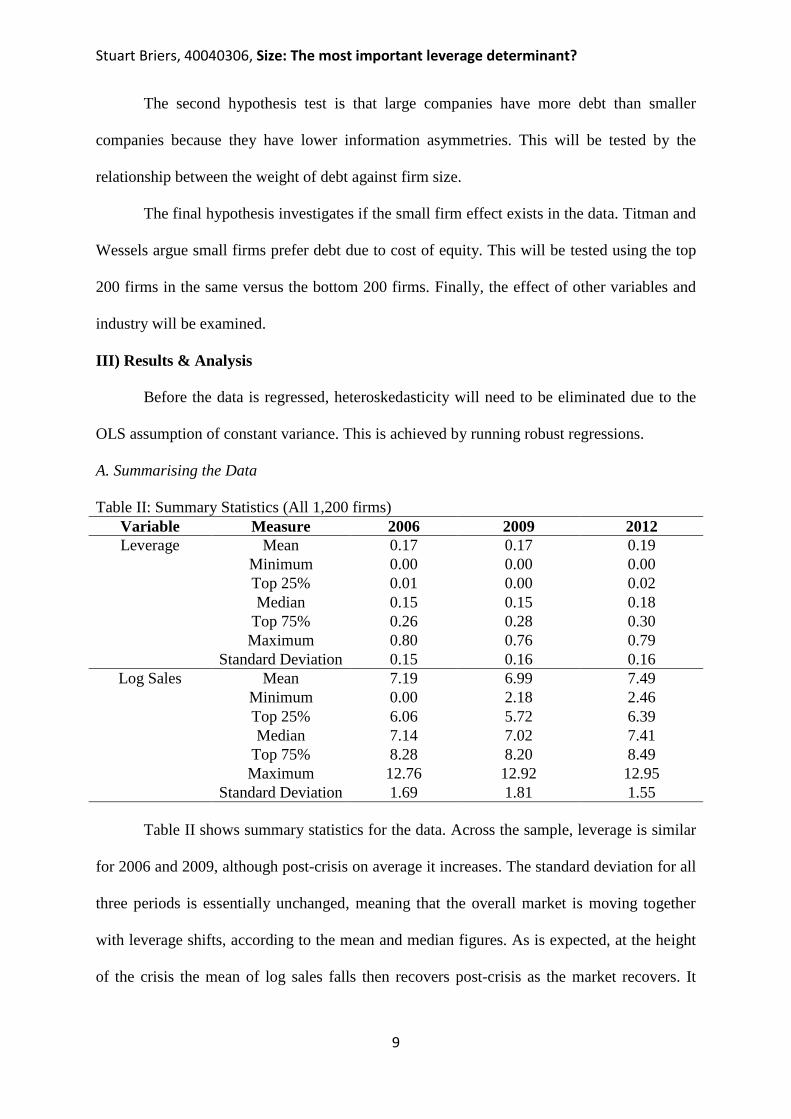

leverage. Looking at all firms in the sample, the mean leverage in 2006 and 2009 is 0.17

compared to 2012 at 0.19 as seen in table II. It is no surprise that firm size is positively

correlated considering Friend and Hasbrouck’s findings that larger firms have better access to

credit markets. This is because the U.S.A. has potentially the easiest access worldwide to

these markets for example the largest stock exchange in the world; NYSE6.

Market Beta values are only significant in 2012. As beta values increase by a unit,

the increase in leverage grows each period. Firms with higher betas (more risky) will take on

greater leverage. The significance should be treated cautiously due to only having 2006 data.

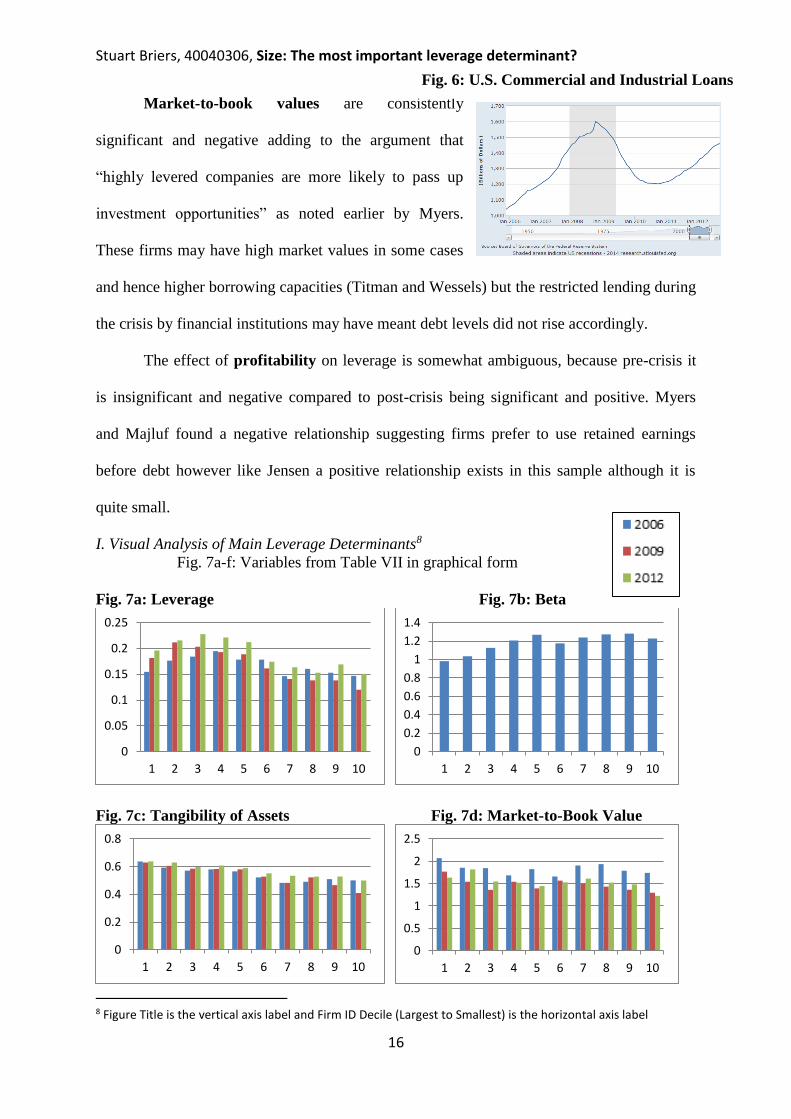

Tangibility of assets is highly significant, possibly acting as a proxy for increased

collateral required during and post crisis in order to fulfil stricter lending requirements due to

lower bank lending7 (fig. 6). This may also be seen as an opportunity to diversify, for

example, by purchasing land due to increased mortgage defaults.

5 Bankruptcy Statistics 2006-2012: see http://www.tradingeconomics.com/united-states/bankruptcies 6 New York Stock Exchange:

see http://www.investopedia.com/financial-edge/1212/stock-exchanges-around-the-world.aspx 7 Commercial & Industrial Loans 2006-2012: see https://research.stlouisfed.org/fred2/series/BUSLOANS/

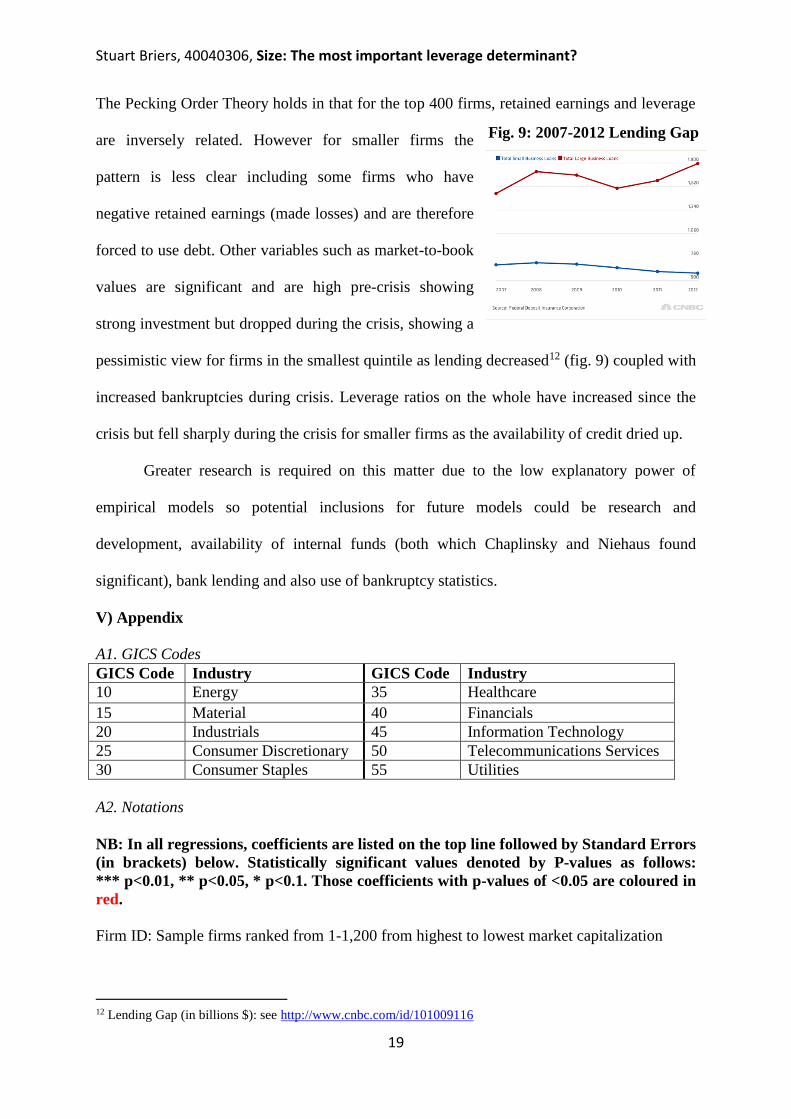

Leverage is discussed in the previous section but importantly it hits a trough

during the crisis for smaller firms (deciles 6-10) because they have greater systematic risk

(due to the small firm effect) as seen with higher betas in fig. 7b. Due to data limitations, only

the 2006 beta is shown and as expected for the top decile (making up the greatest percentage

of the market) their beta is roughly 1.0.

The tangibility of assets increased during the crisis due to stricter lending

requirements on collateral, but for the top decile it was effectively unchanged. Apart from

these firms, tangibility of assets is greatest after the crisis, as a measure to prevent another

securitisation crisis as these are intangible products which can be price sensitive.

Market-to-book value levels are extremely high pre-crisis; due to the cheap supply of

credit available for investment or perhaps due to over-valuations, for example in property.

They fall during the crisis as expected because the outlook is more pessimistic and due to

lower lending figures there is less chance of obtaining this credit to invest. Firms in the 4th,

5th and 10th decile categories have negative retained earnings so the only method of

investment for these firms is through equity.

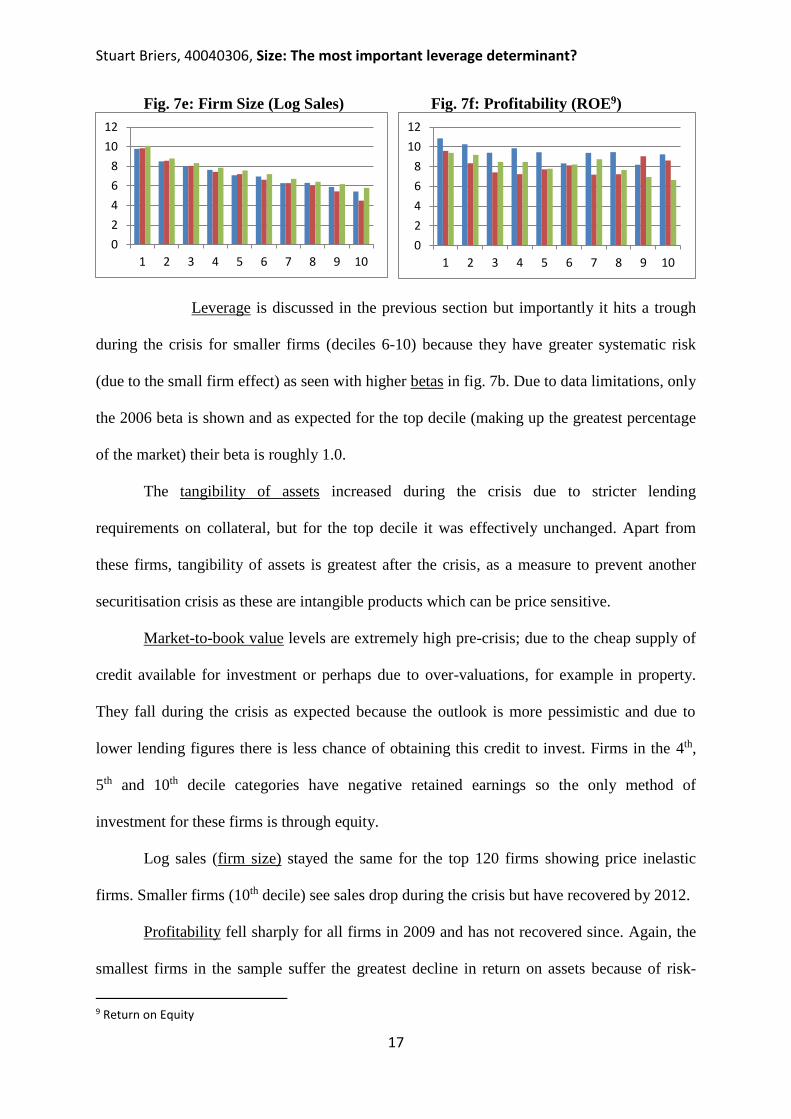

Log sales (firm size) stayed the same for the top 120 firms showing price inelastic

firms. Smaller firms (10th decile) see sales drop during the crisis but have recovered by 2012.

Profitability fell sharply for all firms in 2009 and has not recovered since. Again, the

smallest firms in the sample suffer the greatest decline in return on assets because of risk-

9 Return on Equity

0

2

4

6

8

10

12

1 2 3 4 5 6 7 8 9 100

2

4

6

8

10

12

1 2 3 4 5 6 7 8 9 10

Stuart Briers, 40040306, Size: The most important leverage determinant?

18

averse investors who favour safer (larger) firms; although due to financial amnesia10 the

situation will probably soon return to pre-crisis levels. Zwiebel finds firms with better

investment opportunities (high market-to-book values) and high profitability to have less

leverage due to requiring less debt to avert a takeover. This generally occurs in this sample

particularly towards the top firms.

IV) Conclusion

The results show that firm size is the most important leverage determinant however it

depends on market capitalisation and industry ranking. Firm size was found to be positively

correlated with leverage and the weight of debt, in each case being highly significant. Log

sales were relatively sticky during the three periods for the top decile showing price inelastic

firms. Smaller firms (10th decile) seen log sales drop during the crisis but recovering by 2012.

The firm needs to be considered within its relative placing in the economy as the very top

firms find firm size is insignificant in affecting leverage, whereas the bottom firms of the

sample find firm size plays a highly significant role in affecting leverage.

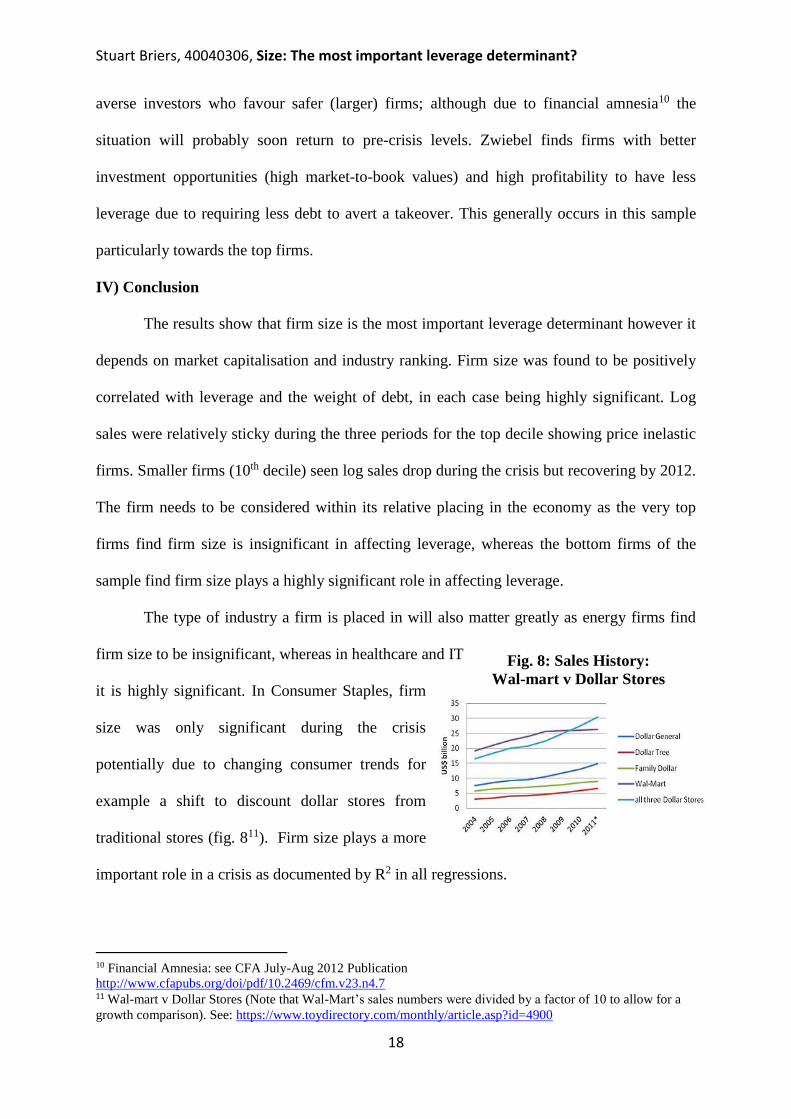

The type of industry a firm is placed in will also matter greatly as energy firms find

firm size to be insignificant, whereas in healthcare and IT

it is highly significant. In Consumer Staples, firm

size was only significant during the crisis

potentially due to changing consumer trends for

example a shift to discount dollar stores from

traditional stores (fig. 811). Firm size plays a more

important role in a crisis as documented by R2 in all regressions.

10 Financial Amnesia: see CFA July-Aug 2012 Publication

http://www.cfapubs.org/doi/pdf/10.2469/cfm.v23.n4.7 11 Wal-mart v Dollar Stores (Note that Wal-Mart’s sales numbers were divided by a factor of 10 to allow for a