The changing nature of outbound royalties from Ireland and their impact on the taxation of the profits of US multinationals May 2021 Seamus Coffey Department of Economics, University College Cork Disclaimer: This paper has been prepared by Seamus Coffey of University College Cork. The views presented in this paper are those of the author alone and do not represent the official views of the Department of Finance or the Minister for Finance. The paper was prepared in the context of ongoing analysis of Ireland's Corporation Tax regime and reflects the data available to the author at a given point in time.

Transcript

The changing nature of outbound

royalties from Ireland and their impact on the taxation of the profits of US

multinationals

May 2021

Seamus Coffey

Department of Economics,

University College Cork

Disclaimer: This paper has been prepared by Seamus Coffey of University College Cork. The

views presented in this paper are those of the author alone and do not represent the official

views of the Department of Finance or the Minister for Finance. The paper was prepared in

the context of ongoing analysis of Ireland's Corporation Tax regime and reflects the data

available to the author at a given point in time.

ii

Summary

Large outbound royalty payments are made from Ireland as license fees for intellectual

property developed elsewhere. These outbound payments were €84.3 billion in 2019 and

preliminary figures for 2020 show a figure of €83.6 billion. Both of these were in excess of

20 per cent of GDP, with the majority of the payments arising the operations of US

multinational companies in Ireland.

An analysis of the geographic breakdown of these flows from Balance of Payments data

shows a very significant change in 2020. Up to 2020, the majority of the outbound royalty

payments from Ireland were directed to offshore financial centres such as Bermuda and the

Cayman Islands. In 2020, a number of US MNCs, particularly in the ICT sector, announced

changes to the licensing arrangements for the use of their intellectual property by their

international operations. Several US ICT MNCs began licensing their intellectual property

from the United States during 2020. After averaging €8 billion a year in the five previous

years, royalty payments from Ireland to the US jumped to €52 billion in 2020, and are likely

to be higher in future years.

In a case study of a US ICT MNC, this report analyses the impact of the changing nature of

outbound royalties from Ireland on the taxation of the profits of US multinationals. In

particular, the analysis focuses on three elements of the 2017 Tax Cuts and Jobs Act. These

are the one-time transition tax on pre-2018 profits of US MNCs which had benefitted from

deferred taxation, the US tax due on what is deemed to be global intangible low-taxed

income, and the relief provided by the US for foreign derived intangible income. Using

publicly available information including financial statements, the case study explores how

these have impacted the effective tax rate of a US MNC.

In time, the impact of these revised structures which is already evident in balance of

payments data will also be evident in other datasets including the aggregate statistics

published by the IRS and the OECD from the country-by-country reports filed by

multinational companies. The changes will also have a significant impact on the data on the

Activities of US Multinational Enterprises published by the Bureau of Economic Analysis

which have historically overstated the level of profits earned by the subsidiaries of US

multinational companies in Ireland.

The changes highlighted in the case study illustrate that the use of “double irish” type

structures is ending. It is non-controversial that the Irish operations of US companies have

to pay for the use of technology that is developed elsewhere and, in many cases, these

payments will continue to be made in form of outbound royalties. However, it is not clear

that the scale of these payments is a signal of aggressive tax planning as a greater and

greater share of these payments, particularly from the ICT sector, will flow directly and in

full to the United States. The changed pattern of royalty flows from Ireland is now more in

line with the economic substance of these companies and the reporting of their profits is

better aligned with the function, assets and risks that generate those profits

Figure 2: Outbound Royalty Payments by Sector …………………………………….…………………………….2

Figure 3: Outbound Royalty Payments by Destination ……….…………………………..…………………….3

Figure 4: Outbound Royalty Payments to the Euro Area ……….……………..……………………………….6

Figure 5: Outbound Royalty Payments to Offshore Financial Centres…….……..……………………….7

Figure 6: Outbound Royalty Payments to the United States…………………..……………..……………….8

Figure 7: Profit in Bermuda by Ultimate Parent Jurisdiction………….…………………………………….15

List of Tables

Table 1: US ICT MNC Income from continuing operations before income taxes………………………8

Table 2: Holding Company Subsidiary of US MNC in Bermuda……………………………………………..…9

Table 3: Trading Company Subsidiary of US ICT MNC in Ireland……………………………………………10

Table 4: Consolidated Tax Reconciliation Statement of a US ICT MNC………………………………….12

Table 5: Profit of US Multinationals attributed to selected jurisdictions……………………………….16

Table 6: Income from continuing operations before income taxes of a US ICT MNC…….……....17

1

1 Introduction

The subsidiaries of US multinational companies (MNCs) operating in Ireland generate their

revenues from the sales of products and services that are the result of research and

development that is primarily undertaken in the United States. These include

pharmaceutical medicines and computer chips which are manufactured at Irish facilities and

advertising and other services sold on online platforms by information and communication

technology (ICT) companies that have their international headquarters in Ireland.

Recent years have seen significant changes introduced that impact on the taxation of these

companies. These changes include those brought about through the Organisation for

Economic Cooperation and Development’s original Action Plan under the Base Erosion and

Profit Shifting (BEPS) project, the Tax Cuts and Jobs Act signed into US law in 2017 and

changes to corporate tax residency rules in Ireland. These changes have been significant

and have triggered significant responses.

This note examines some of these changes and, in particular, focusses on outbound royalty

payments from Ireland. Section 2 looks at the major changes that have occurred since the

start of 2020 in the destination of these royalty payments. Section 3 provides some case-

study analysis exploring the evidence of revised structures of US MNCs from publicly-

available data. Section 4 continues this analysis and looks at the taxation of the profits from

such royalties with an emphasis on the relevant provisions of the US tax code including

those introduced by the Tax Cuts and Jobs Act of 2017 and also provides a brief analysis of

how the revised structures are likely to impact on some of the data sources used to assess

the activities of US MNCs. Section 5 draws together the main conclusions.

2 Aggregate analysis of changes in royalty payments

It is non-controversial that the Irish operations of US companies have to pay for the use of

technology that is developed elsewhere. There are essentially two ways in which this can be

achieved:

1. An outright purchase with the subsidiary in Ireland acquiring the rights or license to

use the technology;

2. Recurrent payments with the subsidiary in Ireland getting access to the technology

via royalty payments.

Historically, the latter was the main method used and recent years have seen an increase in

outright purchases or a combination of the two. Even still, it is likely that royalty payments

from Ireland will remain very significant over the coming years. However, there have been

important changes in the nature of these payments.

Figure 1 shows that in 2019, outbound royalties from Ireland were €84.3 billion, with the

preliminary figures for 2020 recording a small drop to €83.6 billion. Latest estimates are

that Irish GDP in 2020 was €366.5 billion meaning that the outbound royalty payments

made were equivalent to around 22.5 per cent of GDP.

2

The headline totals in recent years may have been relatively stable but there have been very

significant changes in the composition of outbound royalties from Ireland. In this section,

aggregate data by sector and by destination will be considered with Section 3 providing a

case study of company-specific outturns.

2.1 Sectoral analysis Some of the changes in the composition of outbound royalties can be seen if we look at the

contribution of the pharmaceutical and ICT sectors to the total in recent years. Figure 2

shows that, in 2016, the amount of outbound royalties for the ICT and pharmaceutical

sectors were broadly the same. In recent years these amounts have diverged, with

outbound royalties in the ICT sector rising and those for the pharmaceutical sector falling.

0

20,000

40,000

60,000

80,000

€million

2012 2013 2014 2015 2016 2017 2018 2019 2020

Source: Central Statistics Office, Balance of Payments

Value of Annual Irish Royalty Imports with all Countries

Figure 1: Outbound Royalty Imports

0

20,000

40,000

60,000

80,000

€million

2016 2017 2018 2019 2020 Source: Central Statistics Office, Balance of Payments

Value of Annual Irish Royalty Imports with all Countries by selected NACE Categories

Figure 2: Outbound Royalty Imports by Sector

Other Sectors

Pharmaceutricals

Information and Communication

3

Compared to 2016, outbound royalty payments by the pharmaceutical sector in Ireland

have reduced from €24 billion to €14 billion. Over the same period, outbound royalty

payments linked to the ICT sector have risen from €28 billion to €57 billion. Payments from

all other sectors excluding these two have also declined.

The share of outbound royalties from Ireland arising from the ICT sector has risen from 40

per cent in 2016 to almost 70 per cent in 2020. As a result of this much of the subsequent

analysis, including the case study beginning in Section 3, focusses on the ICT sector.

2.2 Destination analysis

Royalty payments leaving Ireland for technology developed elsewhere is only a part of the

story. Where they go to is also relevant. Up to recently the largest destination of these

royalties had been what are termed ‘offshore financial centres’. In the notes for its Balance

of Payments statistics, Ireland’s Central Statistics Office sets out that:

This category overlaps with the regions referred to above and covers Andorra, Antigua and Barbuda, Anguilla, Netherlands Antilles, Barbados, Bahrain, Bermuda, Bahamas, Belize, Cook Islands, Curacao, Dominica, Grenada, Guernsey, Gibraltar, Hong Kong, Isle of Man, Jersey, Jamaica, St. Kitts and Nevis, St Maarten, Turks and Caicos Islands, Cayman Islands, Lebanon, Saint Lucia, Liechtenstein, Liberia, Marshall Islands, Montserrat, Maldives, Nauru, Niue, Panama, Philippines, Singapore, Saint Vincent and the Grenadines, British Virgin Islands, US Virgin Islands, Vanuatu, Samoa.

Figure 3 provides a geographic breakdown of the main destinations of outbound royalty

payments from Ireland. In 2019, €37 billion or almost 45 per cent of total outbound

royalties from Ireland were paid to offshore financial centres.

Value of Annual Irish Royalty Imports with Selected Regions

Figure 3: Outbound Royalty Imports by Destination

Other Regions Euro Area

Offshore Financial Centres United States

4

It can be seen that the amounts going to offshore financial centres were relatively modest

up to 2013 after which they increased rapidly. A likely reason for this is that up to then

Ireland levied a withholding tax on outbound royalty payments paid to non-treaty

countries. If royalty payments were made by an Irish resident person or entity to these

jurisdictions some of the payment would have to be withheld and paid to the Irish tax

authority, the Revenue Commissioners, to cover potential tax liabilities.

There was a fairly straightforward workaround for companies to avoid Ireland’s withholding

tax on outbound royalties to non-treaty countries. Under the EU’s Interest and Royalties

directive EU Member States cannot levy a withholding tax on royalty payments made by a

company to an associated company that is resident of another Member State.1

And as is well known The Netherlands does not levy a withholding tax on outbound

payments from there to locations such as Bermuda. This means that Figure 3 does not fully

represent the amount of outbound royalties from Ireland that are directed to ‘offshore

financial centres’.

Data on royalty flows from Ireland to The Netherlands is not available from Eurostat for all

years. However, for those years which it is available, the data shows that almost all of the

royalty payments made from Ireland to the rest of the euro area went to The Netherlands.

For example, in 2019, of the €29.0 billion of royalties from Ireland to the euro area, €26.4

billion went to The Netherlands. Similar shares are evident for the other years for which

data is available. Further, as will be shown in the next section, it is safe to assume that via

this “dutch sandwich” these royalties from Ireland were further transferred from The

Netherlands to jurisdictions such as Bermuda.

All of the companies involved in these transactions are US multinationals. The US tax

system has allowed (and incentivised) US companies to locate licenses for the use of their

technologies outside the US in low-tax jurisdictions such as Caribbean Islands.

So, while the Irish subsidiaries were correctly paying for the use of technology generated

elsewhere these payments were going to locations where the companies had no substance

rather than where the technology was actually developed, i.e., the United States. The

primary tax payments affected by these strategies are US tax payments.

There are many reasons why these strategies will no longer be effective. Revisions to the

OECD Transfer Pricing Guidelines including those brought about by Actions 8 to 10 of Action

Plan from BEPS v1.0 means that while such payments to entities that license the technology

can be made, they should not be retained if the legal owners have no or limited involvement

in the functions that lead to the development of the intellectual property being licensed.

This is formally set out in paragraph 6.42 of the 2017 update to the OECD’s Transfer Pricing

Guidelines:

1 An associated company is where Company A holds 25 per cent of the voting power in Company B; or Company C holds 25 per cent of the voting power of Companies A and B.

5

6.42 While determining legal ownership and contractual arrangements is

an important first step in the analysis, these determinations are separate and

distinct from the question of remuneration under the arm’s length principle.

For transfer pricing purposes, legal ownership of intangibles, by itself, does

not confer any right ultimately to retain returns derived by the MNE group

from exploiting the intangible, even though such returns may initially accrue

to the legal owner as a result of its legal or contractual right to exploit the

intangible. The return ultimately retained by or attributed to the legal owner

depends upon the functions it performs, the assets it uses, and the risks it

assumes, and upon the contributions made by other MNE group members

through their functions performed, assets used, and risks assumed. For

example, in the case of an internally developed intangible, if the legal owner

performs no relevant functions, uses no relevant assets, and assumes no

relevant risks, but acts solely as a title holding entity, the legal owner will not

ultimately be entitled to any portion of the return derived by the MNE group

from the exploitation of the intangible other than the arm’s length

compensation, if any, for holding title.

OECD (2017), p.262

Under these guidelines if the owner of the intangible asset does not undertake the relevant

functions a set of service transactions must be entered to pay for these functions. The price

set in these transactions will determine the profit that accrues to the owner of the

intangible asset. This will depend on the level of functions carried out by the owner of the

intangible and the pricing approach used by the jurisdiction where the functions are

undertaken.

As well as these changes to the OECD’s transfer pricing guidelines, revisions to Ireland’s

residence rules for Corporation Tax meant it was no longer as feasible for US companies to

avail of the deferral provisions in the US tax code such as the “same country exemption” –

with the original basis for the “double irish” being that two companies were registered in

the same country.2 Significantly, the Tax Cuts and Jobs Act (TCJA) effectively abolished the

principle of deferral for the US tax due on the profit from passive income such as royalties

which was the primary motivation for the creation of these structures.

2 These structures were multi-layered and a similar outcome could be achieved a number of ways. For example, the introduction by the IRS in 1997 of the “check the box” election for entity classification facilitated the broader use of ‘disregarded entities’ for tax purposes in the structures of US MNCs. This election was formalised via the temporary introduction of the ‘look-through rule’ for disregarded entities into Subpart F of the US tax code. There were a number of occasions on which the ‘look-through rule’ was set to expire but each time the US Congress passed an Act that included a provision for its extension. A feature of the “same country exemption” is that it is a permanent feature of the US tax code that did not require a Congressional vote for its extension or rely on an IRS regulation which could be changed.

6

3 The revised structures of US ICT MNCs

It is only US companies that have structures similar to the “double irish with a dutch

sandwich”. A number of companies, most notably in the ICT sector, have made public

statements that they are ending this arrangement. In its annual filing with the Securities

and Exchange Commission (SEC) for 2020, one US ICT company announced:

“As of December 31, 2019, we have simplified our corporate legal entity

structure and now license intellectual property from the U.S. that was

previously licensed from Bermuda resulting in an increase in the portion of

our income earned in the U.S.”

While another US ICT MNC, which previously made payments directly from Ireland to an

offshore financial centre, issued a statement in December 2020 which said:

“Intellectual property licenses related to our international operations have

been repatriated back to the US. This change, which has been effective since

July this year, best aligns corporate structure with where we expect to have

most of our activities and people. We believe it is consistent with recent and

upcoming tax law changes that policymakers are advocating for around the

world.”

3.1 Identifying revised structures in Ireland’s Balance of Payments statistics These changes have been made and the impact on royalty payments can be seen in the

data. As noted above, Eurostat don’t provide a complete series for royalty payments from

Ireland to the Netherlands (many of the values are redacted) but there is a complete series

for quarterly royalty payments from Ireland to the Euro Area and this is shown in Figure 4.

The available data suggest that payments to The Netherlands make up 90 per cent of royalty

payments from Ireland to the Euro Area.

0

2,500

5,000

7,500

10,000

€million

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Source: Eurostat, Balance of Payments

Value of quarterly outbound royalties from Ireland to the rest of the Euro Area (EA19)

Figure 4: Royalty Imports with the Euro Area

7

It is clear there was a significant change at the start of 2020 with a large drop in royalties

payments made from Ireland to the Euro Area, which means there was a large drop in these

payments from Ireland to The Netherlands.

This change doesn’t make a significant immediate difference to the companies’ operations

in Ireland. The Irish company must still pay for the right to use the technology or platform it

is using but these license payments or royalties are no longer going to an offshore financial

centre via The Netherlands. The ending of this arrangement will not have a material impact

on the amount of Corporation Tax paid in Ireland.

There is also evidence of the changes that were flagged for July of 2020 in the second

company statement above. As shown in Figure 5, outbound royalty payments from Ireland

to offshore financial centres had been relatively stable from Q1 2015 to Q2 2020 but they

fell steeply in Q3 2020 in line with the announced change in the statement reproduced

above.

Royalty payments from Ireland to offshore financial centres averaged just over €8 billion a

quarter from Q1 2015 to Q2 2020. For the final two quarters of 2020 these payments fell to

€2 billion a quarter – a 75 per cent reduction.

The aggregate analysis in Section 2 shows that total outbound royalties from Ireland in 2020

were largely unchanged from what they were in 2019, with the total for both years being

close to €85 billion. This means that the reductions in payments shown Figure 4 for royalty

payments to the Euro Area and Figure 5 for royalty payments to offshore financial centres

were offset by increases in royalty payments to other destinations. Figure 6 shows data

from Eurostat for quarterly royalty payments from Ireland to the United States.

0

2,500

5,000

7,500

10,000

€million

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Source: Eurostat, Balance of Payments

Value of quarterly outbound royalties from Ireland to Offshore Financial Centres

Figure 5: Royalty Imports with Offshore Financial Centres

8

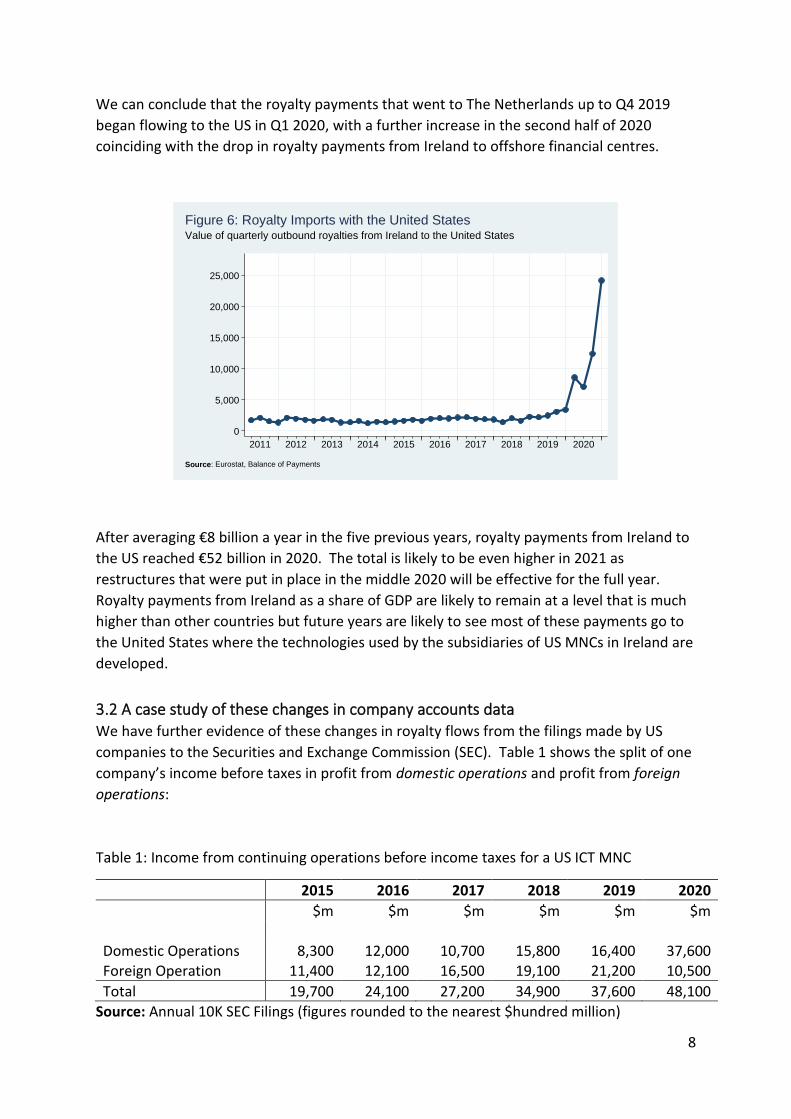

We can conclude that the royalty payments that went to The Netherlands up to Q4 2019

began flowing to the US in Q1 2020, with a further increase in the second half of 2020

coinciding with the drop in royalty payments from Ireland to offshore financial centres.

After averaging €8 billion a year in the five previous years, royalty payments from Ireland to

the US reached €52 billion in 2020. The total is likely to be even higher in 2021 as

restructures that were put in place in the middle 2020 will be effective for the full year.

Royalty payments from Ireland as a share of GDP are likely to remain at a level that is much

higher than other countries but future years are likely to see most of these payments go to

the United States where the technologies used by the subsidiaries of US MNCs in Ireland are

developed.

3.2 A case study of these changes in company accounts data We have further evidence of these changes in royalty flows from the filings made by US

companies to the Securities and Exchange Commission (SEC). Table 1 shows the split of one

company’s income before taxes in profit from domestic operations and profit from foreign

operations:

Table 1: Income from continuing operations before income taxes for a US ICT MNC

Source: Annual 10K SEC Filings (figures rounded to the nearest $hundred million)

0

5,000

10,000

15,000

20,000

25,000

€million

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Source: Eurostat, Balance of Payments

Value of quarterly outbound royalties from Ireland to the United States

Figure 6: Royalty Imports with the United States

9

In the context of US MNCs, the figures for domestic operations refer to the income

attributed to the functions, assets and risks that are located in the United States and foreign

operations refers to activities in other jurisdictions. For this multinational, up to 2019, more

of its income was deemed as foreign rather than domestic. For the five years from 2015 to

2019, an average of 55 per cent of income before income taxes was attributed to foreign

operations. This is somewhat at odds with the economic footprint of these companies as

most of the functions, assets and risks that generate their profits, most notable the research

and development activities, are located in the US.

Included in those foreign profits up to 2019 would have been the profit from the royalty

flows out of Ireland. The outbound royalties from Ireland were payment for technology

developed in the US but the US approach to transfer pricing allowed the rights to this

technology to be advantageously placed offshore. Companies were then able to locate

these licenses in no-tax jurisdictions such as Bermuda and the approach at the time allowed

them to fully attribute the profit from these licenses to their legal owners. Table 2 gives the

income statement for the years from 2017 to 2019 for an IP holding company based in

Bermuda of a US ICT MNC.

Table 2: Holding Company Subsidiary of US ICT MNC in Bermuda

2017 2018 2019

$m $m $m

Statement of Profit and Loss and Other Comprehensive Income

Turnover 22,334 25,740 26,520

Cost of sales -94 -108 -87

Gross profit 22,240 25,632 26,433

Administration expenses -10,552 -11,122 -14,123

Other operating income 44 - 39

Other operating expenses -27 -56 -1

Operating profit 11,704 14,454 12,347

Income from shares in group undertakings 1,974 3 598

Interest receivable and other income 869 1,075 767

Interest payable and other expenses -18 -15 -1

Profit on ordinary activities before tax 14,529 15,517 13,711

Tax on profit on ordinary activities - - -

Profit for the financial year 14,529 15,517 13,711

Source: Filings with Irish Companies Registration Office

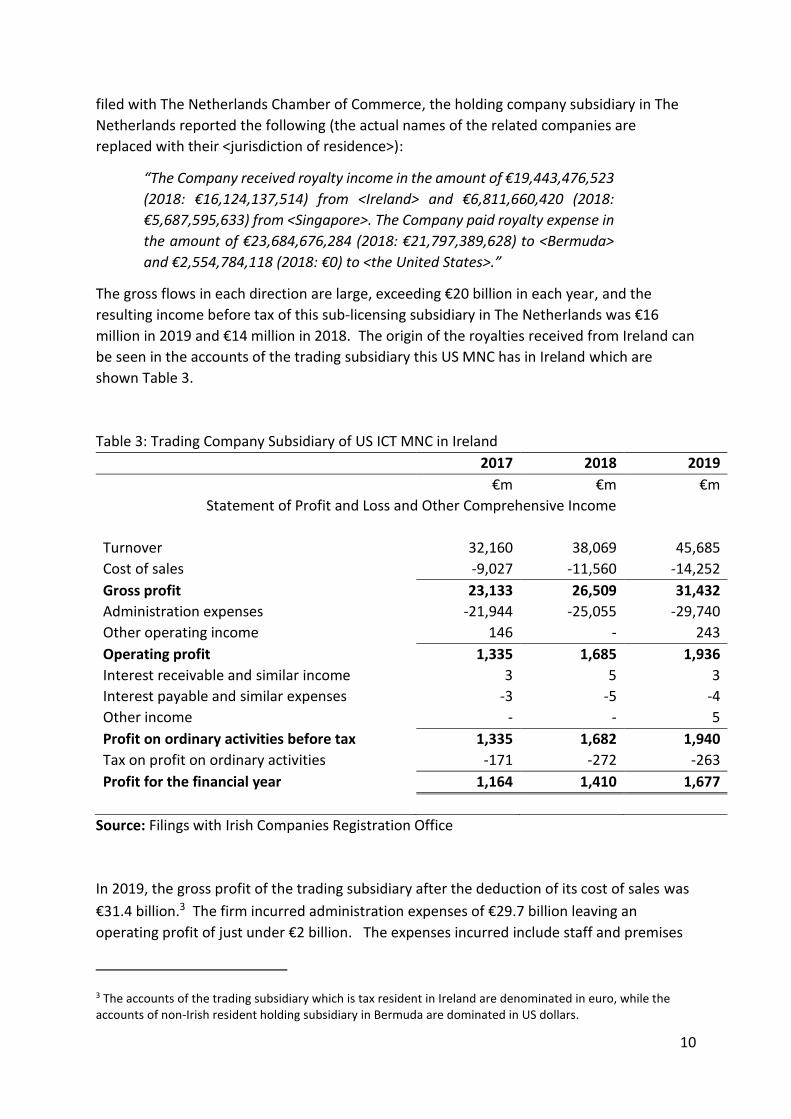

The turnover of this holding company subsidiary was the royalties received from a related

holding company subsidiary in The Netherlands. In turn, the subsidiary in The Netherlands

received royalties from trading subsidiaries in Ireland and Singapore. In its 2019 accounts

10

filed with The Netherlands Chamber of Commerce, the holding company subsidiary in The

Netherlands reported the following (the actual names of the related companies are

replaced with their <jurisdiction of residence>):

“The Company received royalty income in the amount of €19,443,476,523

(2018: €16,124,137,514) from <Ireland> and €6,811,660,420 (2018:

€5,687,595,633) from <Singapore>. The Company paid royalty expense in

the amount of €23,684,676,284 (2018: €21,797,389,628) to <Bermuda>

and €2,554,784,118 (2018: €0) to <the United States>.”

The gross flows in each direction are large, exceeding €20 billion in each year, and the

resulting income before tax of this sub-licensing subsidiary in The Netherlands was €16

million in 2019 and €14 million in 2018. The origin of the royalties received from Ireland can

be seen in the accounts of the trading subsidiary this US MNC has in Ireland which are

shown Table 3.

Table 3: Trading Company Subsidiary of US ICT MNC in Ireland

2017 2018 2019

€m €m €m

Statement of Profit and Loss and Other Comprehensive Income

Turnover 32,160 38,069 45,685

Cost of sales -9,027 -11,560 -14,252

Gross profit 23,133 26,509 31,432

Administration expenses -21,944 -25,055 -29,740

Other operating income 146 - 243

Operating profit 1,335 1,685 1,936

Interest receivable and similar income 3 5 3

Interest payable and similar expenses -3 -5 -4

Other income - - 5

Profit on ordinary activities before tax 1,335 1,682 1,940

Tax on profit on ordinary activities -171 -272 -263

Profit for the financial year 1,164 1,410 1,677

Source: Filings with Irish Companies Registration Office

In 2019, the gross profit of the trading subsidiary after the deduction of its cost of sales was

€31.4 billion.3 The firm incurred administration expenses of €29.7 billion leaving an

operating profit of just under €2 billion. The expenses incurred include staff and premises

3 The accounts of the trading subsidiary which is tax resident in Ireland are denominated in euro, while the accounts of non-Irish resident holding subsidiary in Bermuda are dominated in US dollars.

11

costs in Ireland and fees paid to other group undertakings to provide services and support

to customers in local jurisdictions. However, by far the largest component of these expenses

incurred by the Irish trading subsidiary is the royalty it must pay for the license to use the

MNC’s platform and technology. As the accounts of the subsidiary in The Netherlands show,

these payments were equal to €19.4 billion in 2019 and €16.1 billion in 2018, with almost all

of this subsequently paid to an IP holding company subsidiary in Bermuda.

The Bermudan IP holding company obtained the rights that allowed it to charge royalties for

the use of the MNCs technology in markets outside the Americas via a cost-sharing

agreement. This meant the IP holding company had to make a contribution to the overall

research and development costs incurred by the multinational, with this cost-sharing

payment forming the bulk of the Administration expenses in the Statement of Profit and

Loss of the IP holding company subsidiary shown in Table 2.

For the three years for which the income statement of the holding company is shown, the

operating margin of the holding company was around 50 per cent. That is, it paid out

around 50 per cent of the turnover received (the royalties that originated in Ireland and

Singapore) with the bulk of this going to fund the R&D activities in the US.

As of the start of 2020, this cycle of flows has ended. For this US multinational, the royalty

from Ireland which previously went to Bermuda with about half being paid onwards to the

US to cover expenses now directly, and in full, flows to the United States. This payment

structure is in line with the economic reality and substance of the MNC as the technology

used by the Irish subsidiary to generate sales was almost wholly developed in the United

States.

This is evident from Table 1 in the 2020 split of the MNCs profit into domestic and foreign.

The MNC’s domestic profit rose from $16.4 billion in 2019 to $37.6 billion in 2020. There

was an offsetting change to profits from foreign operations which fell from $23.2 billion in

2019 to $10.5 billion in 2020.

These changes can be fully explained by the transfer of the 2020 equivalent of $13.7 billion

of profit reporting by the holding company in Bermuda in 2019 into the US in 2020. This

MNC is no longer using a “double-irish” structure involving two Irish-registered subsidiaries

– one a trading company in Ireland and the other a holding company in an offshore financial

centre.4 The trading company in Ireland continues as before but there is no longer a role for

the IP holding company in a no-tax jurisdiction. The MNC has transferred the IP assets of

this holding company back to the US and is now reporting most its profit where the

functions, risks and assets that generate it are located – in the US. The figures from Table 1

show that in 2020 around 80 per cent of the income before taxes of the MNC were

attributed to operations in the US.

4 The trading company was resident in Ireland for tax purposes but the IP holding company was not.

12

4 The impact on tax of the identified changes in royalty flows

We can get some insights into the tax implications of these changes from Table 4 which is

the reconciliation of the MNC’s effective tax rate with the statutory federal corporate

income tax rate in the US. It should be noted that this rate was 35 per cent up to 2017 and

has been 21 per cent since.

Table 4: Consolidated Tax Reconciliation Statement of a US ICT MNC

2015 2016 2017 2018 2019 2020

% % % % % %

U.S. federal statutory tax rate 35.0 35.0 35.0 21.0 21.0 21.0

Foreign income taxed at different rates (13.4) (11.0) (14.2) (4.4) (4.9) (0.3)

5 This table is similar to Table 1 for the company examined in the case study in Section 3.

18

Again, we see a very significant change in 2020 with a much larger share of the MNC’s profit

being attributed to its domestic, i.e., US, rather than foreign operations. In 2019, over 75

per cent of this MNCs income before taxes was attributed to foreign operations. In 2020

this fell to 25 per cent. This is because this multinational transferred the license to sell

services on its online platforms in international markets from the Cayman Islands back to

the US.

We could go through the same analysis on the one-time transition tax and the impact of the

GILTI and FDII provisions for this US multinational as undertaken in the case study in

sections 3 and 4, but it is not necessary. The conclusion is simple: the “double-irish” is

redundant. The heretofore foreign profit of some of the US MNCs that used such structures

has been shifted back to the US.

The fact that these profits were already subject to US tax6 means this has not resulted in a

significant increase in these companies’ effective tax rates but the changes do mean that

much more of the profit of these US MNCs is reported where the functions, risks and assets

that generate those profits are located.

4.6 Complying with a Country-Specific Recommendation The European Commission have raised concerns with the level of outbound royalty

payments from Ireland. In its 2020 Country-Specific Recommendations to Ireland, the

Commission note:

“[T]he high level of royalty and dividend payments as a percentage of GDP

suggests that Ireland’s tax rules are used by companies that engage in

aggressive tax planning, and the effectiveness of the national measures

will have to be assessed.”

European Commission (2020), p.7

The analysis in this note has shown that royalty payments from Ireland are likely to continue

at a high level as a percentage of GDP relative to the levels seen in other Member States.

However, it is not clear that this is a signal of aggressive tax planning as a greater and

greater share of these payments, particularly from the ICT sector, flow directly and in full to

the United States. Are national measures being effective if, in conjunction with changes

agreed internationally, they are resulting in a large reduction in the level of outbound

royalty payments being directed to offshore financial centres? The pattern of royalty flows

from Ireland is now more in line with the economic substance of these companies.

6 Either upon repatriations under the pre-TCJA US corporate income tax regime, under the one-off transition tax introduced by the TCJA or under the GILTI provisions of the same Act.

19

5 Conclusion

The subsidiaries of US multinationals operating in Ireland generate significant sales through

the use of technologies developed in the US. It is incontrovertible that the Irish operations

of these multinationals pay for the use of technology and much of these payments are made

in the form of outbound royalties. In 2020, outbound royalty payments from Ireland were

€83.4 billion which is equivalent to 22.5 per cent of Irish GDP in that year.

There was a significant change in 2020 in the destination of these royalty payments. Many

US MNCs, most notably in the ICT sector, have restructured the licensing arrangements for

their technology as a result of changes to the OECD Transfer Pricing Guidelines, revisions to

Ireland’s residency rules for Corporation Tax and the changes to the US tax code introduced

by the Tax Cuts and Jobs Act of 2017. A case study of US MNCs in the ICT sector shows that

under the revised structures the use of technology in international markets is no longer

licensed from jurisdictions such as Bermuda and the Cayman Islands but instead is licensed

directly from the United States. This is in line with the economic footprint of these

companies and aligns the reporting of their profits with the location of their substance. The

annual reports for 2020 for these companies show a large rise in the share of their profits

being attributed to domestic, or US-based, operations. These US operations include the

bulk of these companies’ research and developments activities which is a key driver of their

profits.

Outbound royalty payments continue to be made from Ireland for the use of the resulting

technology but rather than being routed to offshore financial centres benefitting from a

deferral of US tax as was the case under the pre-2018 US tax regime, this income is now

being directed to the United States. In 2020, around 60 per cent of the royalty payments

from Ireland went to the United States. This share is likely to increase in coming years.

20

REFERENCES

Clausing, K., Saez, E. and Zucman, G. (2021). Ending corporate tax avoidance and tax

competition: A plan to collect the tax deficit of multinationals. UCLA School of Law, Law-

Econ Research Paper No. 20-12, http://dx.doi.org/10.2139/ssrn.3655850

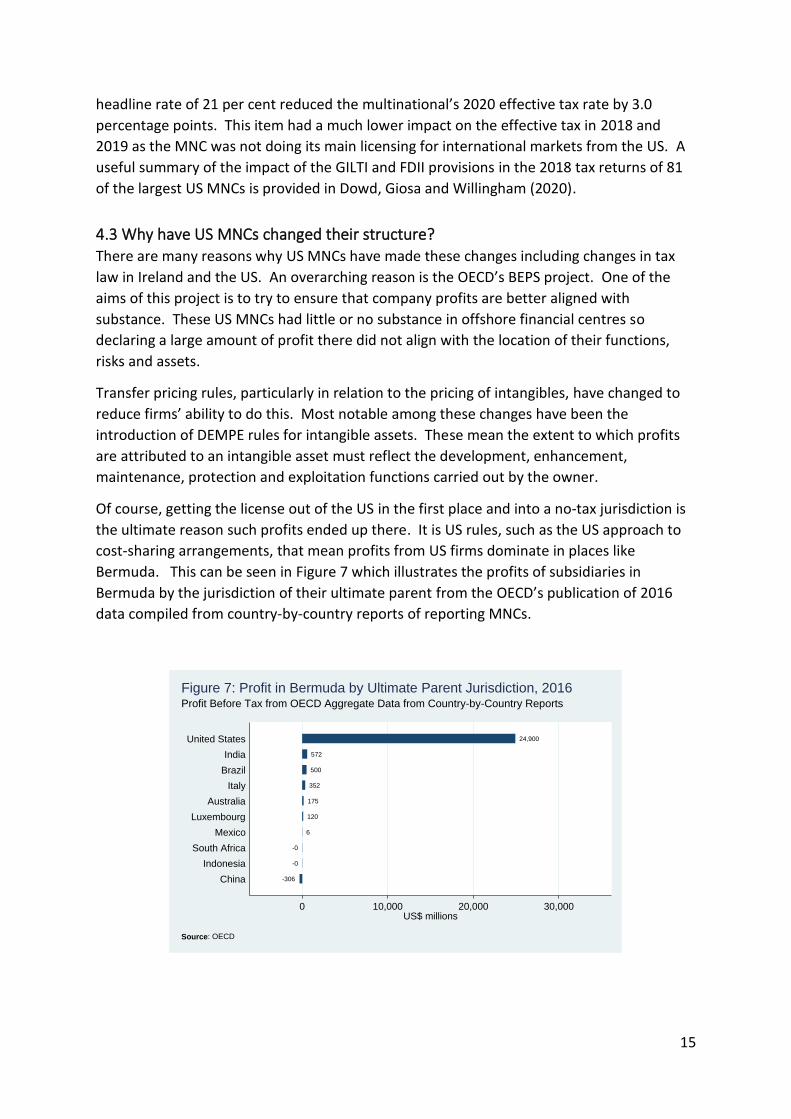

Dowd, T. and Giosa, C.P. and Willingham, T. (2020). Corporate behavioral responses to TCJA