The Development of the Petrochemical Industry and Turkey’s Energy Security

1Pagewww.bilgesam.org

Development of the Global Petrochemical Industry According to Daniel Ye-rgin’s seminal work on oil, although the first com-mercial oil well became operational in 1859, the pet-rochemical industry did not develop until WWII. Oil de-mand was a primary security concern for the great powers during two great wars and the interwar period. In the 1950’s, the increase in de-mand for synthetic materials enforced energy markets to develop more sophis-ticated civil and military technologies and new energy systems. Technologically speaking, once oil was refined, the second stage of crude oil has been its use in manufacturing over 70,000 different chemical products. The major product groups which make use of these chemicals, include rubber and plastic products, textiles, apparel, petroleum refining, pulp and paper, and primary metals.

During the last three decades, the ad-ministrative model and the market for the world petrochemical industry has dramatically altered. The US, Western Europe, and Japan previously domi-nated the production of primary pet-rochemicals. Not only did they supply

their own domestic demand but also exported it to other world markets. Prior to 1980, these technologically ad-vanced countries produced 80% of the world’s primary petrochemical prod-ucts. However, the large scale construc-tion of petrochemical facilities has also been on the rise in other parts of the world, and in turn expanded the petro-chemical market globally. In 2010, the three main countries accounted for only 37% of world primary petrochemicals production.

This research paper explores the ques-tion as to who depends on the energy sector. It argues that those countries which have developed energy technolo-gies, exploration, administration and

marketing strategies in countries which are rich in hydrocarbon deposits are in fact reliant on technologically advanced countries. This paper aims to prove that the petrochemical industry is the key sector in determining the relationship between producers and consumers.

World Petrochemical MarketAccording to the BMI 2011 report, it is estimated that the global petrochemical chemical industry accounted for $3.6 trillion (tn) in 2011, bearing in mind that there was $73 trillion of world trade the same year. However, due to the global financial crisis, there was a decline in the activity of the petro-chemical industrial activity, dropping 4.6% globally. Due to increased uncer-

by Süleyman Elik

The Development of the Petrochemical Industry and Turkey’s Energy Security

Wise Men Center for Strategic Studies (BILGESAM) Mecidiyeköy Yolu Caddesi, No:10, 34387 Şişli -İSTANBUL www.bilgesam.org www.bilgestrateji.com [email protected] Phone: 0212 217 65 91 - Fax: 0 212 217 65 93

The Development of the Petrochemical Industry and Turkey’s Energy Security

2Pagewww.bilgesam.org

tainty in the market, the US and European market growth is expected to be weaker.

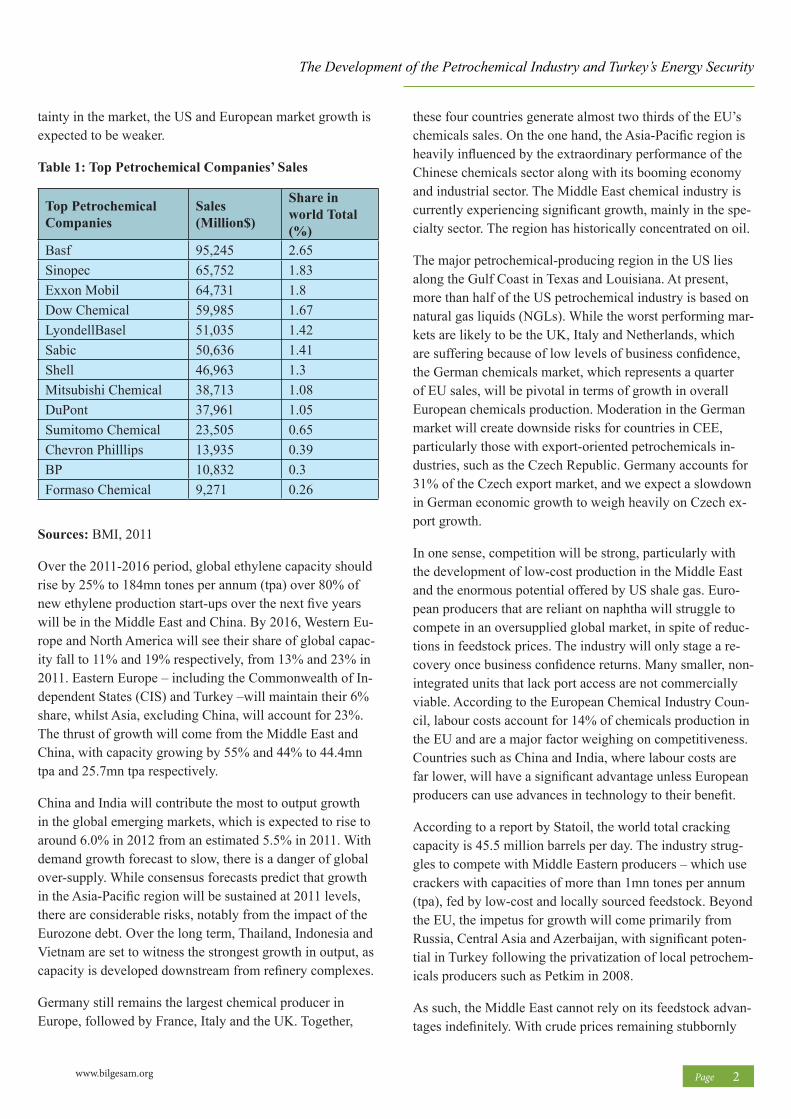

Table 1: Top Petrochemical Companies’ Sales

Sources: BMI, 2011

Over the 2011-2016 period, global ethylene capacity should rise by 25% to 184mn tones per annum (tpa) over 80% of new ethylene production start-ups over the next five years will be in the Middle East and China. By 2016, Western Eu-rope and North America will see their share of global capac-ity fall to 11% and 19% respectively, from 13% and 23% in 2011. Eastern Europe – including the Commonwealth of In-dependent States (CIS) and Turkey –will maintain their 6% share, whilst Asia, excluding China, will account for 23%. The thrust of growth will come from the Middle East and China, with capacity growing by 55% and 44% to 44.4mn tpa and 25.7mn tpa respectively.

China and India will contribute the most to output growth in the global emerging markets, which is expected to rise to around 6.0% in 2012 from an estimated 5.5% in 2011. With demand growth forecast to slow, there is a danger of global over-supply. While consensus forecasts predict that growth in the Asia-Pacific region will be sustained at 2011 levels, there are considerable risks, notably from the impact of the Eurozone debt. Over the long term, Thailand, Indonesia and Vietnam are set to witness the strongest growth in output, as capacity is developed downstream from refinery complexes.

Germany still remains the largest chemical producer in Europe, followed by France, Italy and the UK. Together,

these four countries generate almost two thirds of the EU’s chemicals sales. On the one hand, the Asia-Pacific region is heavily influenced by the extraordinary performance of the Chinese chemicals sector along with its booming economy and industrial sector. The Middle East chemical industry is currently experiencing significant growth, mainly in the spe-cialty sector. The region has historically concentrated on oil.

The major petrochemical-producing region in the US lies along the Gulf Coast in Texas and Louisiana. At present, more than half of the US petrochemical industry is based on natural gas liquids (NGLs). While the worst performing mar-kets are likely to be the UK, Italy and Netherlands, which are suffering because of low levels of business confidence, the German chemicals market, which represents a quarter of EU sales, will be pivotal in terms of growth in overall European chemicals production. Moderation in the German market will create downside risks for countries in CEE, particularly those with export-oriented petrochemicals in-dustries, such as the Czech Republic. Germany accounts for 31% of the Czech export market, and we expect a slowdown in German economic growth to weigh heavily on Czech ex-port growth.

In one sense, competition will be strong, particularly with the development of low-cost production in the Middle East and the enormous potential offered by US shale gas. Euro-pean producers that are reliant on naphtha will struggle to compete in an oversupplied global market, in spite of reduc-tions in feedstock prices. The industry will only stage a re-covery once business confidence returns. Many smaller, non-integrated units that lack port access are not commercially viable. According to the European Chemical Industry Coun-cil, labour costs account for 14% of chemicals production in the EU and are a major factor weighing on competitiveness. Countries such as China and India, where labour costs are far lower, will have a significant advantage unless European producers can use advances in technology to their benefit.

According to a report by Statoil, the world total cracking capacity is 45.5 million barrels per day. The industry strug-gles to compete with Middle Eastern producers – which use crackers with capacities of more than 1mn tones per annum (tpa), fed by low-cost and locally sourced feedstock. Beyond the EU, the impetus for growth will come primarily from Russia, Central Asia and Azerbaijan, with significant poten-tial in Turkey following the privatization of local petrochem-icals producers such as Petkim in 2008.

As such, the Middle East cannot rely on its feedstock advan-tages indefinitely. With crude prices remaining stubbornly

Top Petrochemical Companies

Sales (Million$)

Share in world Total (%)

Basf 95,245 2.65Sinopec 65,752 1.83Exxon Mobil 64,731 1.8Dow Chemical 59,985 1.67LyondellBasel 51,035 1.42Sabic 50,636 1.41Shell 46,963 1.3Mitsubishi Chemical 38,713 1.08DuPont 37,961 1.05Sumitomo Chemical 23,505 0.65Chevron Philllips 13,935 0.39BP 10,832 0.3Formaso Chemical 9,271 0.26

The Development of the Petrochemical Industry and Turkey’s Energy Security

3Pagewww.bilgesam.org

high, Middle Eastern ethane-based petrochemicals produc-tion is still likely to prove a challenge to naphtha-based production, particularly in Europe. However, the choice of ethane as the preferred feedstock, particularly in Saudi Arabia, could put the region at a disadvantage in terms of butadiene and propylene, which are largely produced down-stream from oil refineries and limit the range of products,

although Kuwait and the UAE are cracking naphtha. In poly-mers, this will invariably lead to an overwhelming reliance on polyethylene (PE) grades.

The second category in the petrochemical industry is an emerging market in Asia (India, China, South Korea, Viet-nam, Indonesia, and Thailand), Middle East, Africa and CIS countries. This emerging market challenges the prices of the petrochemical industry products, potentially creating a global over-supply problem that will depress prices. Even though, they lack downstream diversification, which limits the value added to the industry.

The Latin American petrochemicals industry is also a grow-ing market and led by Brazil’s Braskem, which now aims to be among the world’s top five petrochemicals companies by 2020. In the Middle East, there is a great emphasis on basic petrochemicals, with little specialisation or innova-tion. Although Brazil remains a relatively closed economy by regional and global standards, insulating Brazilian firms from external competition, any significant increase in out-put will be directed primarily towards the export markets, which Petrobras and Braskem do not believe will absorb the increase in output at healthy margins until 2017. Conversely, the governments of Argentina, Bolivia and Venezuela have taken a more interventionist stance, increasing their roles

in upstream activities and raising the cost of investment for foreign majors.

Table 2 below is an example of LDPE and PP prices in dif-ferent petrochemical produced regions. The table shows that low-cost petrochemicals are being produced by Middle Eastern firms. For example calculating LDPE and PP prices

together with shipment cost to Turkey, the final prices will be approximately 1380 US$ for LDPE and 1428 US$ for the PP.

The Global Investment of Leading Petrochemical Companies The Middle East and Asian markets attract FDI flows from the petrochemical giants. It is essential to note that technol-ogy transfer and licencing issues play an essential role in terms of cooperation between advanced and developing countries. For instance, companies such as SABIC are at-tempting to address this situation, with most new investment likely to be focused on stepping up technological capacities and diversification. The Gulf region’s petrochemicals indus-try will attract about $50 billion (bn) in investment in 2010-2015, a significant proportion of which will be channelled into diversifying away from commodity chemicals. Half of all the new ethylene projects being developed globally are located in the Gulf. Saudi Arabia accounts for around 63% of total investment in the region, while Qatar comes sec-ond, with a 14% share. Bahrain is the only GCC state with no petrochemicals facilities and no plans to build any. The GPCA has forecast that the region will account for 40% of total global petrochemicals production within 10 years, but has also warned that this would bring fresh challenges for the region’s producers in terms of the need to secure more

CFR FE Asia ($/mt) FD NWE ($/mt) FCA Antwerp ($/mt) FAS Houston ($/mt) FOB Middle East

* FOB Middle East netback denotes CFR Far East Asia assessments minus the prevailing container freight rate from Al-Jubail to Shanghai for a standard 20-foot container.

* Euro prices converted to US Dollars based on 1 Euro=1.29 US$

* Prices are weekly average and based on Platts PolymerScan Report dated 28th of November 2012

Table 2: Average LDPE and PP Spot Prices

Sources: Platts, 2013

The Development of the Petrochemical Industry and Turkey’s Energy Security

4Pagewww.bilgesam.org

feedstock. Similarly, Azerbaijan can attract direct investment and know-how technology and does not to be depending on trade with Russia. Instead it needs market diversification to-wards to Europe.

In fact, Kazakhstan and Uzbekistan are dependent on the Russian export market. In the recent years, the combined Kazakh and Uzbek ethylene capacity is expected to expand from 240,000 tpa in 2011 to 1.49 mn tpa over the subsequent five years, aided by the completion of the Kazakhstan Pet-rochemicals Industries (KPI) complex and a Uzbekneftegas joint venture with five Korean firms. One of the disadvantag-es of the Russian petrochemical market is its low grade tech-nology compared with Western Europe and North America. The rate of state-controlled enterprises probably account for 35-40% of total Russian petrochemicals production which is risky considering the interdependent relationship between Russia and CIS countries. Traditionally, the largest importers of Russian petrochemicals are China, Finland, Ukraine and Kazakhstan.

Development of the Petrochemical Industry in TurkeyWhilst Turkey has limited oil production, approximately 2.3 million tons (less than 0.8% of total demand), its consump-tion was approximately 31.5 million tons in 2012.The gap between demand and supply demonstrates a potential growth in the Turkish oil sector. One of the new developments in the Turkish energy sector is the increased exploration, which will provide promising results in the future. Turkey’s oil production is conducted primarily by three companies: the Turkish State Petroleum Company (TPAO in Turkish)

and the foreign opera-tors, Royal Dutch/Shell (Shell) and ExxonMo-bil. The new Petroleum Market Law introduced several incentives for oil exploration, distribution and retail in the energy sector. The law also lim-ited the dominance of the Turkish Petroleum Company.

Oil exploration in the Black Sea region has been operated by TPAO in joint ventures with

international companies. 18 petroleum regions have been identified by the former law with the South-eastern Anato-lian region taking 92% of the share in oil exploration. Ac-cording to the new law, the licensing period was arranged as 5+2+2 years on land and 8+3+3 years on sea. The applicant has to give 2% of the investment that he or she proposes in the license application or petition to extend the timetable. This ratio is 1% on the sea. The new regulations are meant to protect existing and potential investors in the sector.

Table 3: Turkey’s oil reserves, production, consumption and imports

Proven oil reserves (2000E) 299 million barrels

Oil production (1999E) 69,000 bbl/da

Crude oil production (1999E) 65,000 bbl/d

Oil consumption (1999E) 624,000 bbl/d

Net oil imports (1999E) 555,000 bbl/d

Crude oil refining capacity (2000E) 690,915 bbl/d

Turkey imports 60% of its total oil demand as raw refinery materials from Russia, Iran, Iraq, Saudi Arabia, Libya, Rus-sia, Kazakhstan and Azerbaijan. The privatization in petro TÜPRAŞ, a market leader in the refinery business, currently has four different refineries in Izmir, Kırıkkale and Batman. The Izmir refinery has the largest refining capacity. Azerbai-jan is one of the foreign investors of the Star Refinery which

Figure 1: Top Petrochemical Companies Investment in Globe

Source:Compiled by author, 2014.

The Development of the Petrochemical Industry and Turkey’s Energy Security

5Pagewww.bilgesam.org

is still under construction and expected to become opera-tional in 2017

Turkey has already increased the capacity utilization ratio of the refineries from 74.7% in 2011 to 78.7% in 2012. Given that 60% of the total oil demand is refined in Turkey and that demand is growing, there is ample room for refinery invest-ments, although the market entry barriers are high in light of the very high CAPEX requirements. A similar situation applies for opportunities in importing finished petroleum products.

Retail and Distribution Companies in the petrochemical industry are very competitive. Turkey’s regulatory author-ity, EMRA, ensures fair competition in the oil sector. The distribution market is highly fragmented where the five top players, namely BP, Shell, Opet, Total and OMW-POAS dominate the market. Distribution activity is licensed by EMRA, with 58 licensees’ at the end of 2012. According to EMRA by 2012, the top 10 companies made 83% of the total distributed volume. According to EMRA, approx. 86% of oil is used in transportation. The total number of vehicles has steadily increased since 2000 along with a population growth. Expansion in domestic production and the discount received from the special consumption tax also affected growth in the number of vehicles. Parallel to the vehicle in-crease, fuel consumption has also significantly increased in recent years.

Subsectors in the Turkish Petrochemical IndustryThe basic subsectors in the Turkish petrochemical industry can be classified as petrochemicals, textiles, fertilizers, phar-maceuticals, home and personal care, paints and costing, soda, chrome and boron sector. There are two petrochemical giants in the Turkish chemical industry market, which have refinery capacity. Petkim’s Aliaga petrochemicals complex in Izmir, reached an annual capacity of 3.2 million tons. Products include LDPE, HDPE, PVC and PP products, mas-terbatches, olefins, fibre and aromatics. These products are important inputs for the construction, electricity, electronic, packaging, textile and also medical, dyeing, detergent and

Refinery Company Processing Capacity Storage Capacity Status

İzmir /Star Refinery Socar N/A N/A Under construction

Adana/ Doğu Akdeniz Petrochemicals and Refinery Çalık Holding N/A N/A Under construction

Batman Refinery TÜPRAŞ 1.1 million tons/year 228 thousand m3 Operational

Kırkkale Refinery TÜPRAŞ 5.0 mn tons per year 1,23 million m3 Operational

İzmir Aliağa Refinery TÜPRAŞ 10.0 mn tons per year 1,92 million m3 Operational

İzmit Refinery TÜPRAŞ 11.5 mn tons per year 2,19 million m3 Operational

Table 4: Oil Refining Companies in Turkey

Sources: TÜPRAŞ

The Development of the Petrochemical Industry and Turkey’s Energy Security

6Pagewww.bilgesam.org

cosmetic sectors. Additionally, Tupras, Turkey’s largest pe-troleum company with a crude processing capacity of 28.1 million tons per annum, owns a petrochemical production facility with an annual capacity of 50,000 tons. Also, around 4,000 companies operate in the chemical industry and em-ploy more than 81,500 people in Istanbul, Kocaeli, Sakarya,

Adana, Gaziantep and Ankara.

Turkey is ranked as the seventh largest producer of cotton with a capacity of 1.8 million of 480 Ib. bales in 2009/2017. Turkey’s textile exports increased during the last decades from $ 3.4 billion in 2000 to $ 9.5 billion in 2010. The Turk-ish fertilizer production has increased reaching 5.8 million tons since the last decades. There are seven top companies,

Tupraş-Turkiye Petrol Rafinerileri A.Ş. 14 Petkim Petrokimya Holding A.Ş. Petrochemicals

Petkim Petrokimya Holding A.Ş Petrochemicals

Unilever Sanayi ve Ticaret Turk A.Ş. 33 Aksa Akrilik Kimya Sanayii A.Ş. Personal& Home Care

Aksa Akrilik Kimya Sanayi A.Ş. Textile

Eti Maden İşletmeleri Genel Mudurluğu MiningSoda Sanayii A.Ş. MiningTurk Henkel Kimya San. ve Tic. A.Ş. Personal& Home Care

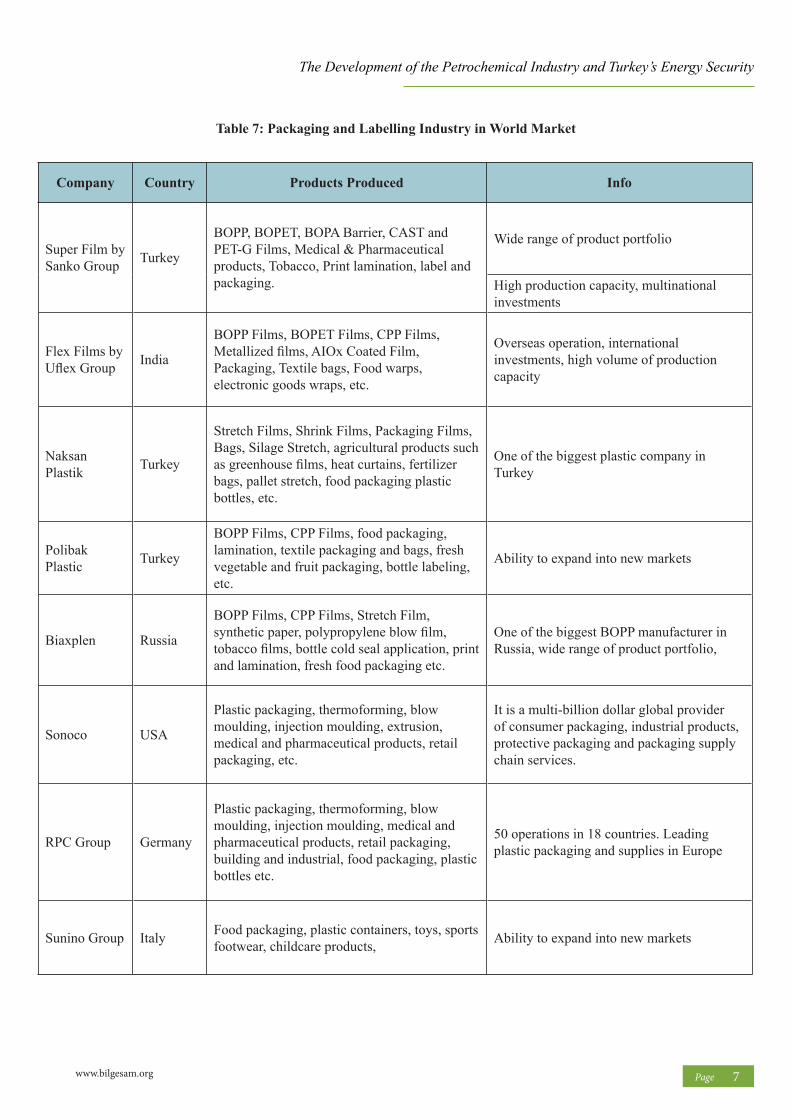

Overseas operation, international investments, high volume of production capacity

Naksan Plastik Turkey

Stretch Films, Shrink Films, Packaging Films, Bags, Silage Stretch, agricultural products such as greenhouse films, heat curtains, fertilizer bags, pallet stretch, food packaging plastic bottles, etc.

One of the biggest plastic company in Turkey

Polibak Plastic Turkey

BOPP Films, CPP Films, food packaging, lamination, textile packaging and bags, fresh vegetable and fruit packaging, bottle labeling, etc.

Ability to expand into new markets

Biaxplen Russia

BOPP Films, CPP Films, Stretch Film, synthetic paper, polypropylene blow film, tobacco films, bottle cold seal application, print and lamination, fresh food packaging etc.

One of the biggest BOPP manufacturer in Russia, wide range of product portfolio,

Sonoco USA

Plastic packaging, thermoforming, blow moulding, injection moulding, extrusion, medical and pharmaceutical products, retail packaging, etc.

It is a multi-billion dollar global provider of consumer packaging, industrial products, protective packaging and packaging supply chain services.

RPC Group Germany

Plastic packaging, thermoforming, blow moulding, injection moulding, medical and pharmaceutical products, retail packaging, building and industrial, food packaging, plastic bottles etc.

50 operations in 18 countries. Leading plastic packaging and supplies in Europe

Sunino Group Italy Food packaging, plastic containers, toys, sports footwear, childcare products, Ability to expand into new markets

Table 7: Packaging and Labelling Industry in World Market

The Development of the Petrochemical Industry and Turkey’s Energy Security

8Pagewww.bilgesam.org

all private, which produce fertilizers: Tugsas, Igsas, Bagfas, Toros Gubre, Ege Gubre, Akdeniz Gubre and Gubre Fabri-kalari. Additionally, the pharmaceuticals industry is one of the major subsectors within the chemical industry providing approximately 10 per cent of the industry’s production. The size of the Home and Personal care market was around $ 1.2 million. The Paints and Coatings sector has significantly developed in Turkey’s construction, automotive and marine industries. There are around 600 manufacturing facilities in the Turkish market and the production capacity has reached 800,000 tons. Turkey has a specific competitive advantage as one of the main global producers of soda ash, chrome and boron. Turkey has around 72 % of the world’s proven boron reserves. Boron products are used for in agriculture, deter-gent and soaps, ceramics, insulation fiberglass, timber pres-ervation, flame-retardants, nuclear power plants, cosmetics and medicine, metallurgy, and many other industries. Tur-key’s pure boron exports totalled USD 435 million in 2009.

Major players in the Turkish chemicals industry, selected from a list of the first 500 manufacturers, are listed in the following table.

Turkey’s chemicals exports increased by 29 % in July 2010 to USD 4.4 billion compared with July 2009 USD 3.4 bil-lion after the global economic downturn in 2009. In 2009, exports of chemicals constituted around 6.2 % of all Turkish exports, ranking the industry 4th by total value of exports after automotive, steel, and textiles. Germany, France, the United Kingdom and Italy are major destinations for Turkish chemicals exports (28.5 % of the total).

Turkey-Azerbaijan Energy Interdependence RelationsIt is important to note that Turkey-Azerbaijan relations play a key role in their petrochemical investment. There has been an interdependent relationship between Turkey and Azerbaijan in the energy sector, especially as regards the Baku Tbilisi-Ceyhan Crude Oil Pipeline, (BTC), Shah Deniz Natural Gas Pipeline Project, Baku- Tbilisi-Kars Railway Project, Petkim Project in Izmir (STAR Refinery), Shah Deniz Phase II Project and the Trans Anatolian Natural Gas Pipeline Project (TANAP). It is estimated that in 2018, Azer-baijan’s investment in Turkey will reach $17 billion. Despite having such investment, economic relations between Turkey and Azerbaijan are unbalanced in the framework of Foreign Direct Investment flow.

Turkish companies need to increase their direct investment into Azerbaijan’s energy sector in order to strengthen the interdependence. In the comparative case study below, it seems that the relationship is very fragile and vulnerable

to a break in trade relations. However, the relationship has established a trade mechanism, which is not effected by any political change in domestic politics. In this sense Azerbai-jan can use Turkey both as a market for its petrochemical industry and a gateway for the South Eastern European (SEE) market.

Though German chemical giants dominate the SEE petro-chemical market, both Azerbaijan and Turkey can co-operate with the German companies by allowing the FDI from EU companies. This would bring knowhow, technology and experience to Azerbaijan’s petrochemical industry as well as Turkey’s.

Baku-Tbilisi-Kars Railway Transportation Line A railroad is expected to open in 2014. Its length will be 826 km and it is estimated that it will be able to transport 1 million passengers and 6.5 million tons of freight in the first stage. This capacity will then reach 3 million passengers and over 15 million tons of freight. The total cost of the project will be around $600 million, including $422 million

dedicated to the construction of a railroad between Kars and Akhalkalaki and to the rehabilitation of the railroad between Akhalkalaki and Marabda. The implementation of the East-West energy corridor has laid the foundations for increased economic and political ties between Azerbaijan, Georgia and Turkey. At the economic level, since the beginning of the 2000s, the trade volume between these three countries has been constantly increasing. Noticeably, the energy corridor has contributed to the increase in the volume of trade, and there is no doubt that the BTK railroad will further contrib-ute to such an increase.

In addition to these three countries, Uzbekistan is interested

From: Middle EastTo: Below countries 25-100 mt >100 mtEast China 15-30 10-25South China 15-30 10-25India 40-45 35-40Southeast Asia 30-40 25-35NW Europe 65-75 60-70Turkey 65-75 60-70US Gulf 135-145 130-140Latin America 160-170 155-165

* By vessel* Prices are based on dated 11.28.2012

Table 8: Polymer Freight Rate ex-Middle East (US$/mt)

The Development of the Petrochemical Industry and Turkey’s Energy Security

9Pagewww.bilgesam.org

in the BTK railroad, which is now presented as the “Iron Silk Road” because it will connect Europe to China when completed. This road will secure the SCIP supply of petro-chemicals to Europe, Turkey and the Asian countries through committable transportation costs. Presently, the Middle East petrochemical producers transport petrochemical products via vessels since no direct road or railway connection exists. Hence, Azerbaijan’s chemical industry has increased po-tential, if market conditions and high-technology is brought together with a railway network.

High quality low-cost production activities and transporta-tion of petrochemical products will need to be introduced in order to compete with the regional and international market. Without doubt, the BTK railway network will provide inex-pensive and speedy transportation between Azerbaijan and Europe. For instance, the city of Gaziantep, which is the centre for the plastic industry, if connected with Turkey’s domestic railway line through the BTK, transportation costs between Azerbaijan and city will reduce from $ US100 mt $US 50 mt. Azerbaijan has the potential to be an energy hub in the petrochemical industry market if Azerbaijan attracted the FDI, information-technology and established ties with the global chemical industry market.

Concluding RemarksSince the beginning of industrial revolution, Western Eu-rope, and US have been the dominant actors because of their use of state-of-art-technology in the petrochemical industry sector. Developed countries have been very successful in market liberalisation, administration of petrochemical indus-try sites, and codification of law in environmental protec-tion, arbitration and so on. The developing countries would like to keep their technological initiatives, and to maintain their dominance in determining of the norms of international market regime. This research has concluded that there is a dependency relationship between the developed countries and developing countries in the petrochemical industry. Therefore, the countries, which have not enough experience in liberal market regulation and environmentally friendly infrastructure developments in Specialised Economic Zones (SEZ), need to attract Foreign Direct Investment and know-how technology, transfer from developed countries. Established petrochemical industry sites and Special Eco-nomic Zones create an economic boom in Western Europe and United States.We believe that there is a general ten-dency towards the Autonomous Private Model in developed countries, especially in Western Europe and U.S. There is a necessity for efficient mechanisms by reducing the role of state-controlled economic zones in order to attract FDI flow

or minimize government initiatives to establish quick mech-anism’s which overlap with market demands and conditions.

The dominance of TÜPRAŞ in the Turkish petrochemi-cal sector needs to be balanced with foreign and national companies. The fact that refineries determine the end-user prices in the petroleum sector means that the new players, Çalık Holding and Socar cannot provide a balance in the liberalized market. Turkey needs to develop a petrohemical site even if she does not have enough hydrocarbon sources. Turkey also needs to develop an interdependent relation-ship with Iraq, especially Northern Iraq and Iran. Due to the tecnological weakness of Iran and Iraq, there is a reliance on refined oil and jet fuel from abroad. Turkey can sell refined oil to Kurdish Regional Authority, which in turn will create an interdependent relationship. I believe that as an energy hungry country, Turkey needs focus on research and devel-opment in energy technology and systems.

The Development of the Petrochemical Industry and Turkey’s Energy Security

10Pagewww.bilgesam.org

About BILGESAM

Established in 2008, the Wise Men Center for Strate-gic Studies (BILGESAM) is one of the leading think tanks in Turkey. As a non-profit, non-partisan organi-zation BILGESAM operates under the guidance of a group of well-respected academics from different disciplines, retired military generals and diplomats; and aims to contribute regional and global peace and prosperity. Closely following the domestic and international developments, BILGESAM conducts research on Turkey’s domestic problems, foreign policy and security strategies, and the developments in the neighbouring regions to provide the Turkish decision-makers with practical policy recommenda-tions and policy options.

About Author

Süleyman Elik is currently working at Istanbul Medeniyet University, the Faculty of Political Science/ International Relations. After he completed his PhD in Durham University, he used to work at the Energy Institute of School of Government and International Affairs, Durham University (UK) as a Visiting Research Fellow and thought “Middle East Politics” in Newcastle University/ Politics department, acting module leader of “the Politics of Middle East” from October 2009 to June 2010. Dr. Elik is International Security Studies fellow at the Wise Men Center for Strategic Studies (BILGESAM).He is author of a book; “Iran-Turkey Relations, 1979-2011: Conceptualizing the Dynamics of Politics, Religion and Security in Middle-Power States,” (London: Routledge, 7th October 2011).