41

The Movie Industry Today

The Movie Industry Today

The Players

• Production

– Studios contract with known producers

– Studios finance indie producers

• Distribution

– studios

• Exhibition

– Theaters

– Ancillary markets

Demand for Flickers

• Prices and elasticity

– Demand for hit movies is inelastic

– Demand for complementary goods is not• Babysitter

• Dinner

• Parking/transportation

• That really good buttered popcorn

– Demand for “regular” movies is elastic• Rush hour specials

• Student/senior discounts

Markets for Movies

• Historically theaters were the only market

for movies

• Technology → ancillary markets

• Culture + technology =

– Piracy

– Impatience – I don’t want to wait six months to

rent/stream anymore

Marketing

– Distributing

• Sequential patterns (decreasing order of

MR/time)

– Theater

– Streaming/video on demand

– DVD/Blu-ray

– Pay TV

– Network TV

• Decreasing theater release window over time

Release Patterns

Markets for Movies

• Ancillary markets

– Decreased average cost of distributing

• A DVD is cheaper to produce than a film print

• Electronic version is even cheaper

– Increased revenue streams

– Profits are not necessarily increased

• Costs have risen faster than revenues

• Who are customers in ancillary markets?

– Marginal viewers who would not go to theater anyway

– Viewers who substitute streaming/rental for trip to theater

Markets for Movies• Ancillary markets

– Change in source of revenue over time

1980 1990 2000 2018

Theatrical box office 52.4% 25.0 29.4 16

Domestic 29.6 15.9 15.2 5.6

Foreign 22.8 9.1 14.2 10.4

Home video 7.0 38.6 38.2 27

Pay cable 6.0 8.3 7.8 8

Network TV 10.8 0.8 1.5 46

(merch

and

digital

3%)

Syndication 3.8 4.6 3.9

Foreign TV 2.5 7.6 6.9

“Made for TV” films 17.5 15.2 12.3

Financing a film– Major Studio

• Bank loan on distribution contract

• Invest own capital

– Independent producer• Presales

• Deal with major studio

– Funding requires that movie be cast (function of agent)• Storyline

• Actors

• Directors

• Estimated budget

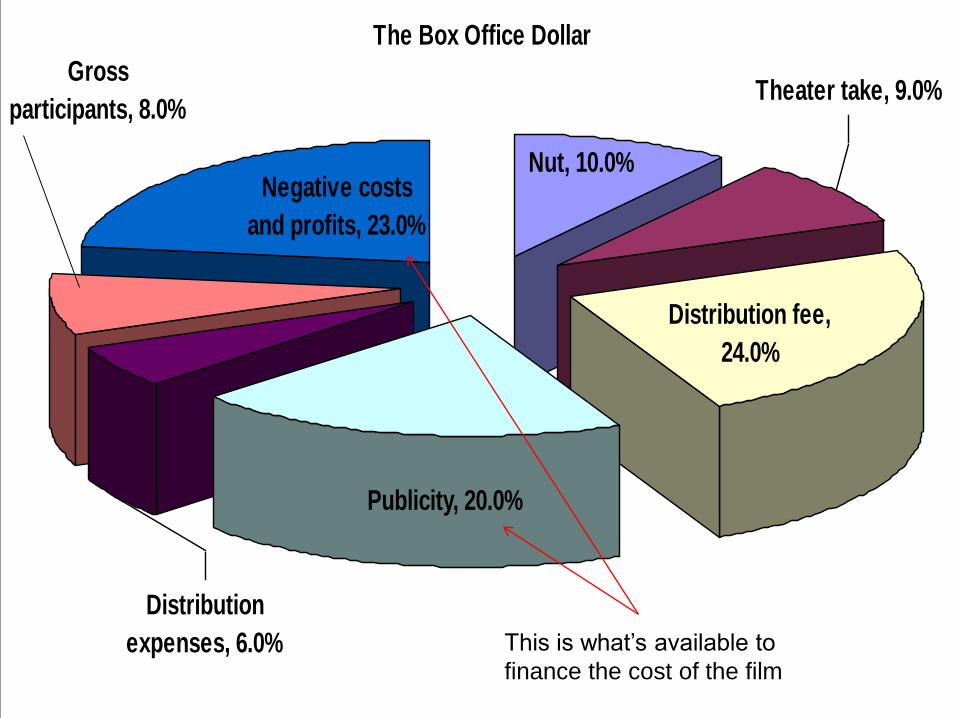

The Box Office Dollar

Gross

participants, 8.0%

Negative costs

and profits, 23.0%

Distribution fee,

24.0%

Theater take, 9.0%

Distribution

expenses, 6.0%

Publicity, 20.0%

Nut, 10.0%

This is what’s available to

finance the cost of the film

Distributor-exhibitor contracts

• exhibitor covers “nut” before splitting box

office

– rent, utilities, insurance

• sliding % of box office gross

• territorial exclusivity for theater

• advances and floors

– Advance: non-refundable down payment

– floor required by distributor to protect against

bomb.

Distributor-Exhibitor Relations

Example of distributor rental calculations

Week 1 Week 2

Box office gross (one week) $16,000 $6000

Less “nut” - 1500 -1500

Theater “net” revenue 14,500 4500

Min rental (70% box office gross) (11,200) - 4200

Max rental (90% of “net”) -13,050 (4050)

Theater operating revenue 1450 300

Distributor Costs

• distributor fee is cost to access distribution pipeline

• ≈ 1/2 of fee pays for distributor costs

– overhead

– annual operating expenses

– other publicity and promotional expenses

• remaining 1/2 of fee is “profit”

– provides cash flow to finance other films

– compensates for risk of financing movie

– covers losses of box office bombs– only at box office can a film generate negative return, because box office

attendance determines revenue

– ancillary market distribution contracts are written to guarantee TR > TC

Marketing• Advertising

– Often as much as 50% of total cost

– Advertising = f(competition)

• Competition = f(release date)

• release strategy

– wide release requires lots of ads

– slow build-up can rely more on word-of-mouth ads

Supply and Demand

• Seasonal admission cycles

Normalized Domestic Movie Ticket Sales: 2006

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

7-Jan

28-Ja

n

18-F

eb

11-M

ar

1-Apr

22-A

pr

13-M

ay

3-Jun

24-Ju

n

15-Ju

l

5-Aug

26-A

ug

16-S

ep

7-Oct

28-O

ct

18-N

ov

9-Dec

30-D

ec

Week Ending Date

Percen

tag

e o

f W

eek E

nd

ing

Ju

ly 8

th

Profit and the Box Office

• Profit = Total revenue – total costs

• TR = box office + ancillary

• TC = production + distribution + publicity

2018 Studio Share Domestic Box Office

Studio

Mkt

Share

Box Office

Gross (mils)

Number of

films

Buena Vista 26 % $3092 13

Warner Brothers 16.3% $1940 49

Universal 14.9% $1772 23

Sony/Columbia 10.9% $1304 28

20th Century Fox 9.1% $1082 17

Paramount 6.4% $757 12

Lionsgate 3.3% $389 20

STX Entertainment 2.3% $297 10

Focus Features 1.4% $167 13

MGM/UA 1.4% $164 3

Fox Searchlight 1.2% $145 6

Top Six Studios 2018• 74.5% of domestic box office

• Averaged 23.7 releases

• Average production cost $140 million

• 23.7 x $140 = $3.3 billion

• On average 25% of cost recovered at domestic box office, 75% from ancillary sources

• Average box office take for distributor = 42%

• for studio to recover $825 million in costs from box office, its box office gross must be $825/.42 = $1.96 billion

• Total 2018 box office $11.8 billion

• Each studio needed 16.6% (1.96 bil/11.8 bil) share of market to break even

2018 Studio Share Domestic Box Office

Studio

Mkt

Share

Box Office

Gross (mils)

Number of

films

Buena Vista 26 % $3092 13

Warner Brothers 16.3% $1940 49

Universal 14.9% $1772 23

Sony/Columbia 10.9% $1304 28

20th Century Fox 9.1% $1082 17

Paramount 6.4% $757 12

Lionsgate 3.3% $389 20

STX Entertainment 2.3% $297 10

Focus Features 1.4% $167 13

MGM/UA 1.4% $164 3

Fox Searchlight 1.2% $145 6

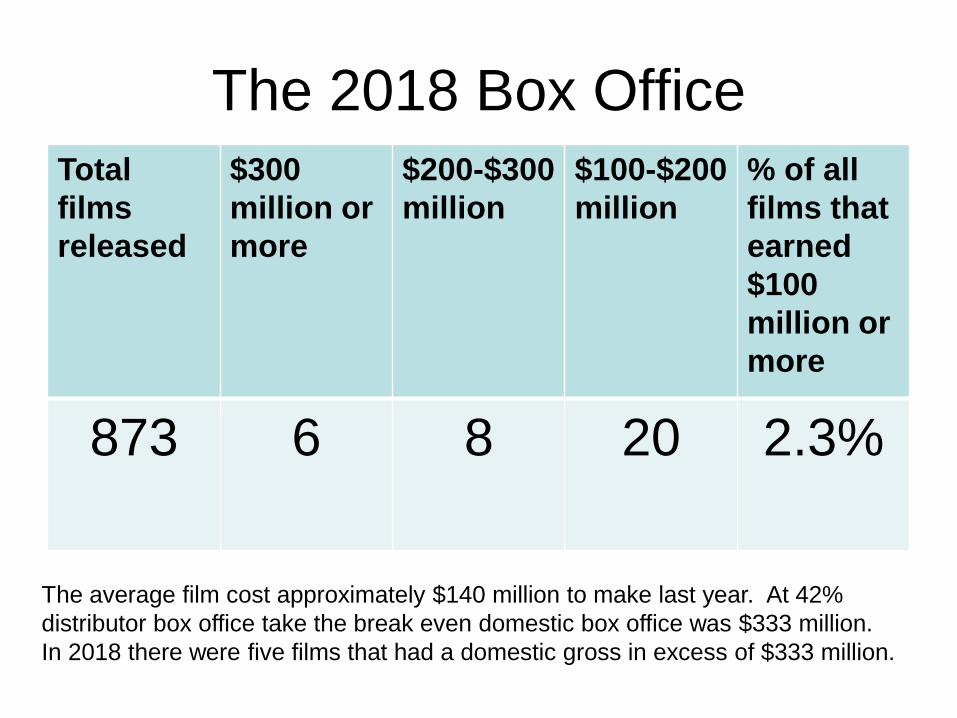

The 2018 Box Office

Total

films

released

$300

million or

more

$200-$300

million

$100-$200

million

% of all

films that

earned

$100

million or

more

873 6 8 20 2.3%

The average film cost approximately $140 million to make last year. At 42%

distributor box office take the break even domestic box office was $333 million.

In 2018 there were five films that had a domestic gross in excess of $333 million.

2018 Domestic Box Office Leaders

Film

World

Box

office

(mils)

% from

domestic

box

office

Opening

wknd

(mils)

% open

wknd to

dom bo

Prod

Cost

(mil)

Break

even dom

bo (est)

not incl

marketing

Black Panther $1346.9 52% $202 28.8% $200 $476.2

Avengers:

Infinity War $2048.4 33.1% $257.7 38% $300 $714.3

Incredibles 2 $1242.8 49% $182.7 30% $200 $476.2

Jurrasic World $1309.5 31.9% $148 35.3% $170 $404.8

Aquaman $1142.9 29.2% $67.9 20.4% $160 $381

Deadpool 2 $778.9 70.9% $125.5 22.6% $110 $262

Hollywood Economics

Arthur DeVany

London: Routledge, 2004

Arthur DeVany

Survival of the fittest

• How long does a movie last?

Likelihood of remaining in Top 50

Who produces the movies?

• The movie Lorenz curve

• The studio Lorenz curve

• A top-heavy industry

Equitable distribution

2018 Studio Share Domestic Box Office

* Percentage of US based studios

Studio

Mkt

Share

Box Office

Gross (mils)

Number of

films

Buena Vista 26 % $3092 13

Warner Brothers 16.3% $1940 49

Universal 14.9% $1772 23

Sony/Columbia 10.9% $1304 28

20th Century Fox 9.1% $1082 17

Paramount 6.4% $757 12

TOTALS 83.6% $9947 142

% of INDUSTRY TOTAL 4.0% 84.3% 16.2%

What did Buena Vista do right?

Produce five of the

eight movies that

grossed $200 at the

domestic box office

Release strategies

• Wide release

versus slow

build up

• Performance by

release strategy

• Good movies

have legs

• Dogs slink away

Performance over time

• Two-thirds of movies earn their max box-

office revenue in first week

• Slow releases are the exception

• Second week is usually the week of widest

release for most movies

A bomb And a hit

Star power

• Why stars are paid so

much

• How valuable is a

star?

• Can a big name save

a big bomb?

The expectation of a

movie’s performance is

dominated by unlikely

events

That is, nobody

really knows what to

expect

What makes a hit?

• Rating, Genre or Star?

• Predicting performance

Since film

rentals

are

approx

one half

of box-

office

revenues,

a gross

return of

2 would

be the

break

even

point

same

mean

but diff

std dev

The current philosophy

• Minimize risk by offering something

familiar

– Sequels, stars, franchises

• Diversify

– Major studios are parts of conglomerates

• Brand your product

– Think toys, video games, etc

Summary

• The movie industry is built on the

blockbuster model

– Stars are the safest bet among a selection of

risky bets

– Because movies are experience goods,

subject to the ever changing whims of the

audience, copycat producing is a safe bet

– Tension between artist and financier

Summary

• The importance of ancillary markets

• Studios finance and distribute

• Marketing costs depend on competition

and release strategy

• The bulk of the box office dollar goes to

the distributor

Questions?