49

Public Future Perspectives How digital disruption is shaping the Nordic business landscape and what business possibilities are emerging? A Nordics study 2017

| Date post: | 21-Jan-2018 |

| Category: |

Business |

| Upload: | tieto-corporation |

| View: | 609 times |

| Download: | 4 times |

Public

Future PerspectivesHow digital disruption is shaping the Nordic business landscape

and what business possibilities are emerging?

A Nordics study

2017

© Tieto Corporation

Public

In 2016, Tieto conducted the Foresight 2020 study to understand the

cross-industry business opportunities projected to shape the future of business

into the year 2020.

In 2016 and 2017, Tieto conducted the Future Perspectives study to deepen the insights of

Foresight 2020 in particular. The Future Perspectives study provides expert thoughts and

expectations about how technology-driven opportunities will unfold in the coming half-decade —

specifically, how business models and value chains will be affected and what kinds of business

possibilities will arise now and in the future.

Tieto’s Future Perspectives study was conducted via interviews and a questionnaire survey of 500

executives from a wide variety of industries in three Nordic countries. Data was collected and

analysed by the research company Kairos Future.

Future Perspectives: Nordic

insights on the effects and

possibilities of digital disruption

2

© Tieto Corporation

Public

3

53%

23%

15%

9%

Sweden

Finland

Norway

Others

500 Nordic respondents

representing a variety of industries

Wide

industry

coverage

25%

15%

12%

10%

9%

9%

5%

5%

5%

4%

2%

Other industries

Financial services

Public services

Energy & utilities

Manufacturing

Healthcare and welfare

Media

Telecom

Retail and wholesale

Forestry

Logistics

0%

to

30

%

Future Perspectives: The scope of the study

Source: Tieto Future Perspectives Research 2017

© Tieto Corporation

Public

4

Future Perspectives: Key findings

• 40% of senior executives are not worried about disruption

driven by industry innovation coming from insiders and

outsiders

• Nordic executives are not investing in some technology areas,

even though they identified them as containing opportunities.

• Digital disruptions create a Valley of Opportunity — which

makes becoming a pioneer and early adopter the best approach

for success.

• Digital possibilities for the future are opening up faster

than ever.

Future Perspectives:

Key insightsTraditional industries are merging together to forge

new opportunities

© Tieto Corporation

Public

5

Executive summary

THE CAUSE:

The speed of digital disruption hits a

new gear in the NordicsNordic executives expect more radical digital disruption in the

coming five years compared to the past five years.

72% of these executives foresee disruption coming from

outside their own industry.

Retail & wholesale, financial services and media industries are

seen as the industries most heavily disrupted by new tech

players.

THE EFFECT:

We are in the next wave of

business model innovation

82% of Nordic executives believe their value chain will

change drastically over the coming years.

72% of executives believe their current business models

will be obsolete within the next 5 years.

Current business models are anticipated to have shorter

lifespans.

© Tieto Corporation

Public

6

Executive summary

THE ENABLER:

Culture and leadership are key

to new business possibilities

The digital possibilities in the

Valley of Opportunity can offer

huge business potential.

The best approach is to be

a pioneer or an early adopter.

Culture and leadership are the greatest barriers to

opportunity domains.

WHAT WILL TOMORROW LOOK

LIKE?

Future digital possibilities for Nordic

businesses

In the short term, digital surveillance

and cyber security look to mature into important

opportunity domains.

Automation in everything — including production of goods, energy and

services — may become a central part of the mid-21st century economy.

Public

1The speed of digital disruption hits a new gear in the Nordics

© Tieto Corporation

Public

8

Key insights1. The speed of digital disruption hits

a new gear in the Nordics

Digital disruption is getting faster

• Nordic executives expect more radical digital disruption in the

coming five years compared to the past five years.

Digital disruption comes mostly from outside

• 74% of executives foresee disruption coming from

outside their own industry.

New tech players are shaking up traditional industries

• Retail & wholesale, financial services and media industries are

seen as the industries most heavily disrupted

by new tech players.

© Tieto Corporation

Public

Public

We are in a new era

of digital disruption

© Tieto Corporation

Public

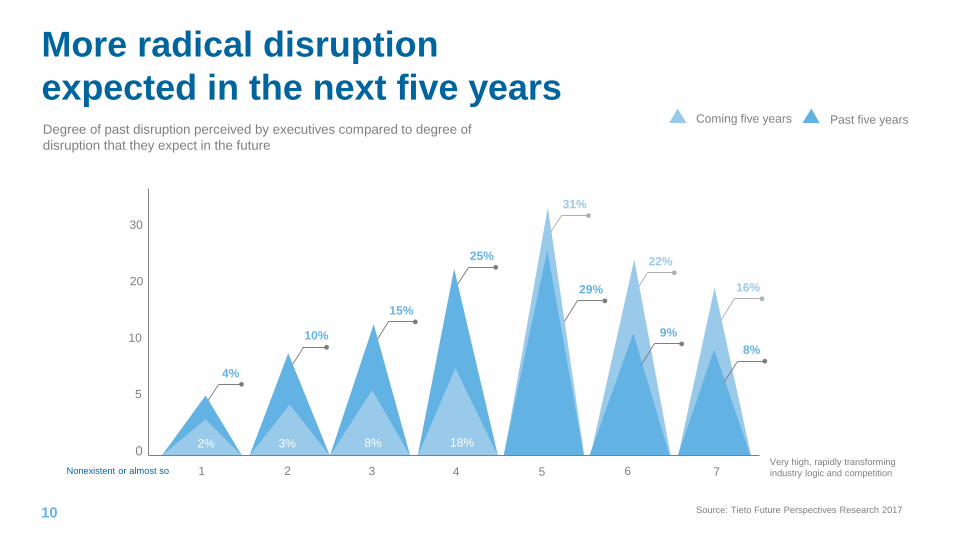

10

Degree of past disruption perceived by executives compared to degree of

disruption that they expect in the future

More radical disruption

expected in the next five yearsPast five yearsComing five years

22%

31%

25%

15%

1 2 3 4 5 6 7

0

5

10

20

30

4%

2%

10%

3% 8%

9%

16%

8%

Nonexistent or almost soVery high, rapidly transforming

industry logic and competition

18%

29%

Source: Tieto Future Perspectives Research 2017

© Tieto Corporation

Public

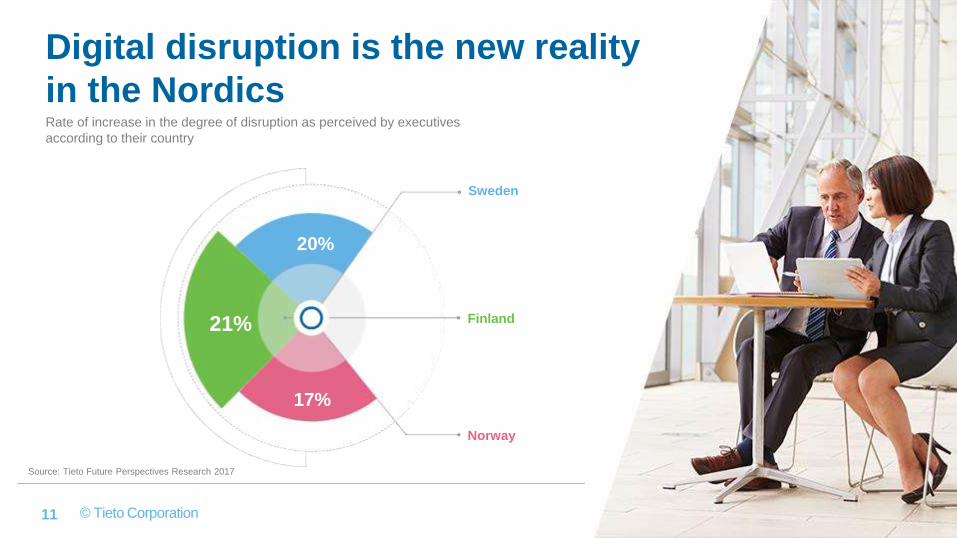

Rate of increase in the degree of disruption as perceived by executives

according to their country

Finland

Sweden

Norway

21%

20%

17%

Digital disruption is the new reality

in the Nordics

11

Source: Tieto Future Perspectives Research 2017

© Tieto Corporation

Public

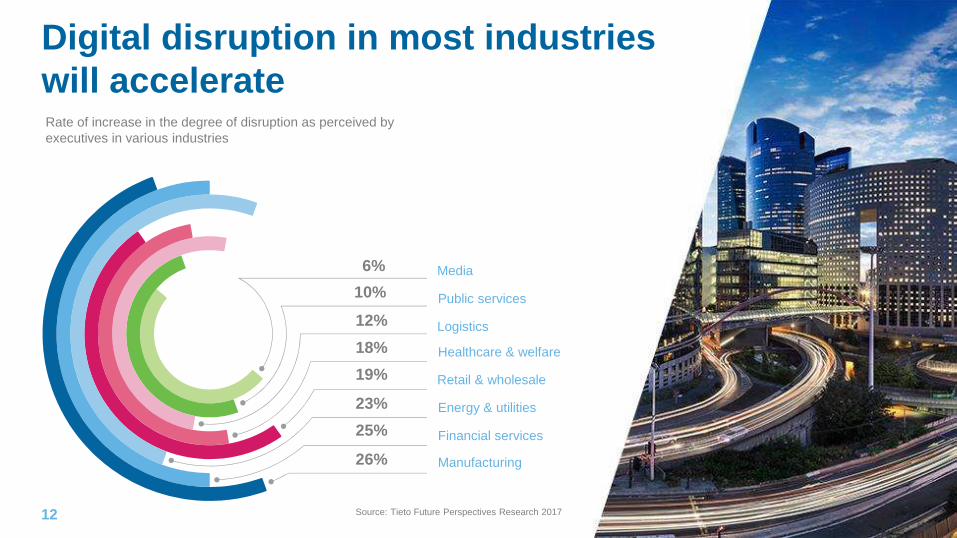

12

Rate of increase in the degree of disruption as perceived by

executives in various industries

Digital disruption in most industries

will accelerate

12 Source: Tieto Future Perspectives Research 2017

6%

10%

12%

18%

19%

23%

25%

26%

Media

Public services

Logistics

Healthcare & welfare

Retail & wholesale

Energy & utilities

Financial services

Manufacturing

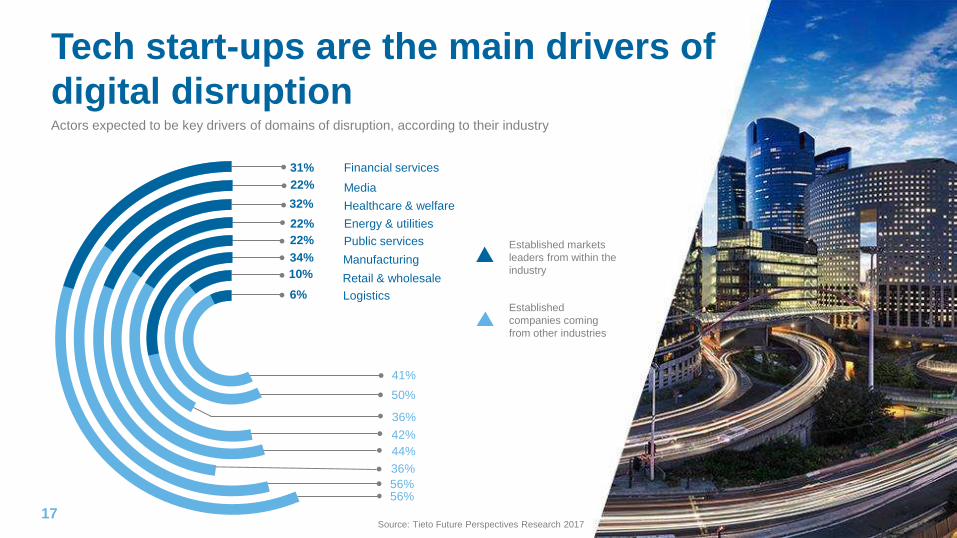

Public

of Nordic executives state that the new technology

based start-ups will be the most important drivers

of change for their industry.

44%

© Tieto Corporation

Public

14

74% foresee disruption coming

from outside their own industry Actors that executives expect to be key drivers of domains of disruption within their industry

Established markets leaders from

within the industry

Established companies coming

from other industries

New technology based start-ups

Others

44%

28%

26%

3%

Percentages are rounded off

Source: Tieto Future Perspectives Research 2017

Public

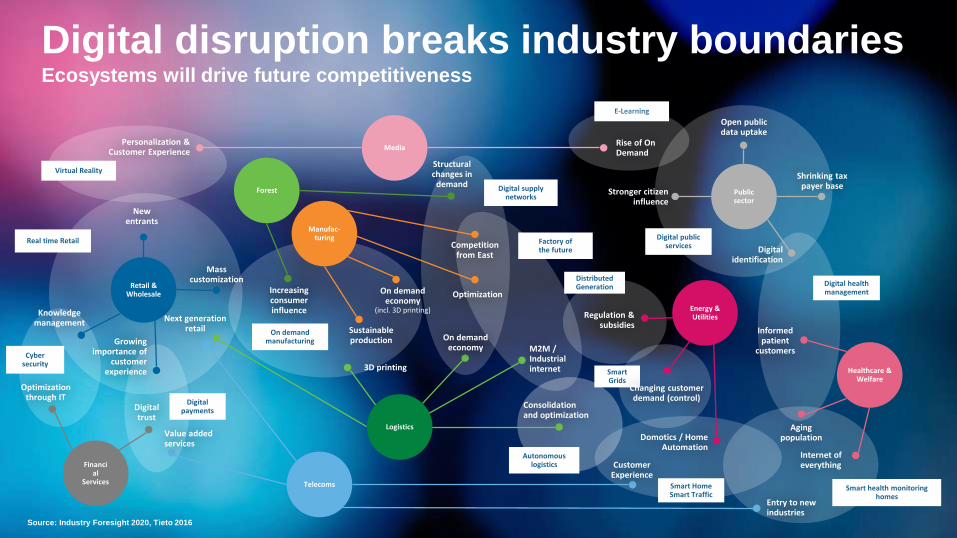

Global insights from the Tieto Foresight 2020 study:

Digital disruption breaks traditional industry boundaries

© Tieto

Corporation

Confidential

Digital disruption breaks industry boundariesEcosystems will drive future competitiveness

E-Learning

Digital health management

Smart health monitoring homes

Cyber security

Digital payments

Real time Retail

On demand manufacturing

Digital supply networks

Factory of the future

Virtual Reality

Smart HomeSmart Traffic

Smart Grids

Distributed Generation

Digital public services

Autonomous logisticsFinanci

alServices

Digital trust

Optimization through IT

Retail &Wholesale

New entrants

Growing importance of

customer experience

Knowledge management

Masscustomization

Manufac-turing

On demand economy

(incl. 3D printing)

Sustainable production

Optimization

Competition from East

Forest

Structural changes in

demand

Increasingconsumerinfluence

3D printing

On demand economy M2M /

Industrialinternet

Consolidationand optimization

MediaPersonalization &

Customer ExperienceRise of On Demand

Informed patient

customers

Healthcare & Welfare

Aging population

Internet ofeverything

Publicsector

Stronger citizen influence

Open public data uptake

Digitalidentification

Shrinking tax payer base

Energy & UtilitiesRegulation &

subsidies

Changing customer demand (control)

Telecoms

Logistics

Next generation retail

Domotics / Home Automation

Value added services

Customer Experience

Entry to new industries

Source: Industry Foresight 2020, Tieto 2016

© Tieto Corporation

Public

17

Actors expected to be key drivers of domains of disruption, according to their industry

Tech start-ups are the main drivers of

digital disruption

22%

22%

6%

32%

10%

22%

31%

34%

Media

Public services

Logistics

Healthcare & welfare

Retail & wholesale

Energy & utilities

Financial services

Manufacturing

50%

42%

56%

44%

56%

36%

41%

36%

Established markets

leaders from within the

industry

Established

companies coming

from other industries

17Source: Tieto Future Perspectives Research 2017

© Tieto Corporation

Public

18

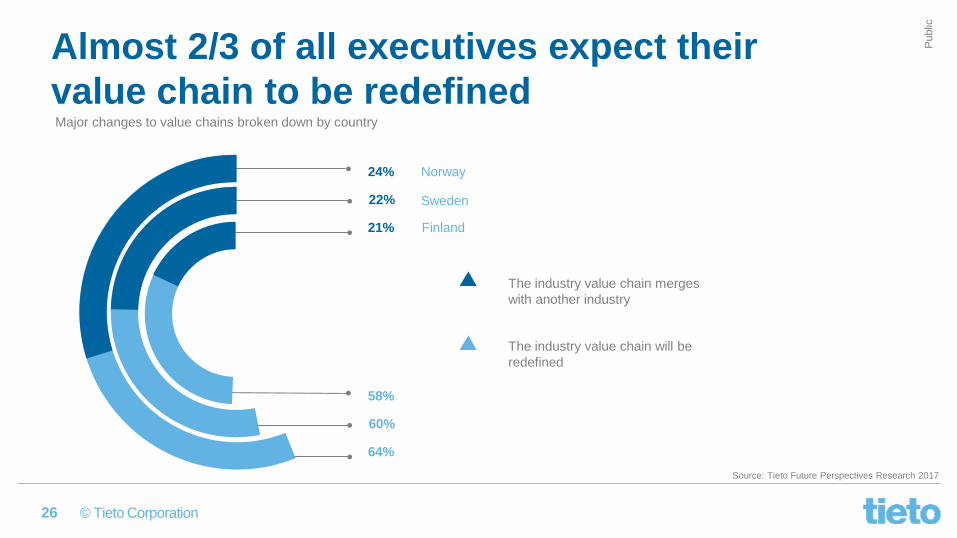

Major changes to value chains broken down by country

38%

34%

51%

24%

32%

27%

Established companies coming

from other industries

New technology based start-ups

Sweden

Finland

Norway

Disruption by tech-startups is

most evident in Sweden

Source: Tieto Future Perspectives Research 2017

Public

2

We are in the next wave of

business model innovationDigital disruption is the new normal in the Nordics

— but what happens now?

© Tieto Corporation

Public

20

Key insights

2. We are in the next wave of business

model innovation

Many business models will become extinct

• 72% of the executives believe that their current business

models will be obsolescent within the next 5 years.

Value chains will transform

• 82% of Nordic executives believe their value chain

will change drastically over the coming years.

Current business models are anticipated to have

shorter lifespans.

Public

Value chains will merge across industries, putting

an increasing emphasis on continuous innovation

Public

of executives believe their value chain will

change drastically over the coming years.

82%

© Tieto Corporation

Public

23

Traditional value chains will

experience structural changesExpected structural change in the future of value chains

The industry value chain will be

redefined

The industry value chain will merge

with another industry

The industry value chain will remain

unchanged

Other

58%

23%

18%

1%

Source: Tieto Future Perspectives Research 2017

© Tieto Corporation

Public

2424

Value chains across

all industries will be affected Major changes to the value chain, broken down by industry

23%

21%

21%

22%

21%

28%

21%

15%

Media

Public services

Logistics

Healthcare & welfare

Retail & wholesale

Energy & utilities

Financial services

Manufacturing

44%

58%

68%

53%

67%

60%

37%

65%

The industry value chain merges

with another industry

The industry value chain will be

redefined

Source: Tieto Future Perspectives Research 2017

© Tieto Corporation

Public

Watches

OTT content

on tablet

Records a

video blog

25

An example: how the value chain of the media

industry is evolvingThe map below illustrates the flow of money between actors in the value chain for a person setting up a business, and it

highlights the potential of different activities in the future.

LowMediumHighEstimated level

of disurption

New payment, monetization

models

Automated production,

distribution and marketing

Increase in visual / video

communication

Self-service re-bundling

Person

wakes upReads a subscribed

to newspaperArrives at

work

Drives to work

listening to

radio

Has several

phone calls

during the day

Collects

advertising

from post box

Buys product on sale, as seen

in newspaper advertising

Watches

linear TV

Writes a

blog post

Media house funded

by advertising and

subscription

Reads a

book

Retailer investing in

TV and Print

advertising

Source: Industry Foresight 2020, Tieto 2016

Listens to (and watches)

personalized media

content via car

infotainment system

Video-conferencing,

via same device but

different providers

Digital signage and beacon

technology delivers

targeted ads based on big

data analytics

Video-conferencing,

via same device but

different providers

Generates

revenue from

ads

Produces

novel

content

Targeted

marketing

distributed

digitally

Accesses a media content

aggregators’ platform for

personalized selection of

sources and content

Investing in e.g.

affiliate promotion

model

Watches

customized

personal content

Content selected

automatically

through big data

analytics

Primarily re-

distributes

automatically

collected content

Funded by advertising

and a freemium content

model

© Tieto Corporation

Public

26

Major changes to value chains broken down by country

58%

60%

64%

24%

22%

21%

The industry value chain merges

with another industry

The industry value chain will be

redefined

Sweden

Finland

Norway

Almost 2/3 of all executives expect their

value chain to be redefined

Source: Tieto Future Perspectives Research 2017

Public

Most of today’s

successful

business models

will have shorter

lifespans.

Public

of Nordic executives state that their business model of

today will be obsolete within the next five years.

72%

© Tieto Corporation

Public

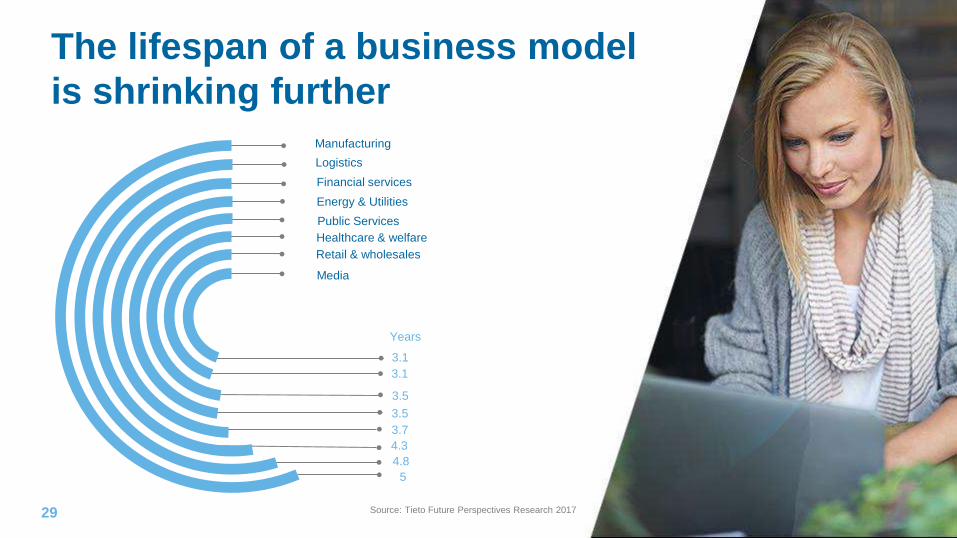

29

Media

Logistics

Healthcare & welfare

Retail & wholesales

Energy & Utilities

Financial services

Manufacturing

3.1

3.5

5

3.7

4.8

3.5

3.1

4.3

Public Services

The lifespan of a business model

is shrinking further

Years

Source: Tieto Future Perspectives Research 2017

Public

3

Culture and leadership are the

key to new business possibilities

Digital disruptions create a “Valley of

Opportunity” — domains with huge potential

for companies who recognise these

possibilities.

© Tieto Corporation

Public

31

Key insights3. Culture and leadership are the key to

new business possibilities

The Valley of Opportunity presents uncharted business

possibilities

• The digital possibilities in the “Valley of Opportunity” can offer huge

potential.

• Leaders acknowledge the opportunities, but do not invest in them.

Leadership and culture needs to develop — or innovation

can falter

• Nordic executives identify culture (51%) and leadership (50%)

as the greatest barriers to seizing opportunities.

The Nordics are early adopters of disruptive technologies.

© Tieto Corporation

Public

Estimated

time horizon for

significant impact

2015

2025+

2020

Estimated time

horizon for

significant impact2015 2025+2020

Digital payments On-demand

manufacturing

Autonomous

logistics

Digital supply networks

Real time retail

Digital Identification

Cyber

security

Digital public

services

Smart

Traffic

Factory of

the future

VirtualR

eality

E-LearningDigital health

management

Smart health

monitoring homes

Distributed

Generation

Smart

Grid

EUR 10–20 billion

EUR 50–100 billion

EUR 100–200 billion

Estimated global market value*

EUR 20–50 billion

* The majority of the opportunities identified in this report

comprise a mix of separate markets and technologies, and

thus exact market values are therefore difficult to specify.

The market value bands identified have been calculated by

adding together market sizes for separate components

belonging to each of the domains.

EUR >200 billion

Source: Industry Foresight 2020, Tieto 2016

Foresight 2020 excerpt:

16 previously identified opportunity domains

© Tieto Corporation

Public

33

New business possibilities are born from digital disruptions

• Under-utilized opportunity domains with huge potential

— especially as businesses and whole industries

continue to digitalize.

• Companies who can seize opportunity domains in the

Valley of opportunity at an early stage are

likely to be big winners.

• Companies should be ready to invest as soon

as a valuable opportunity presents itself.

What is the Valley of

Opportunity?

© Tieto Corporation

Public

Nordic executives are

increasingly willing to invest in

the opportunity domains

32%

30%

23%

23%20%

20%18%

10%

11%Media

Logistics

Healthcare & welfare

Retail & wholesale

Energy & utilities

Financial services

Manufacturing

Public services

Telecom

34

Source: Tieto Future Perspectives Research 2017

© Tieto Corporation

Public

35

Nordic leaders are missing out

in the “Valley of Opportunity”

• Telco enabled

ecosystems

• Factory of the Future

• Smart grids

• Distributed generation

• Virtual reality

• Smart health monitoring systems

• On-demand manufacturing

• Real-time retail

• Smart traffic

• Autonomous logistics

• Digital health management

• E-learning

• Digital supply networks

• Digital public services

• Digital payments

• Cyber security

Valley Of Opportunity

Industry-Specific Society-encompassing

High

investment

readiness

Low

investment

readiness

Source: Tieto Future Perspectives Research 2017

© Tieto Corporation

Public

36

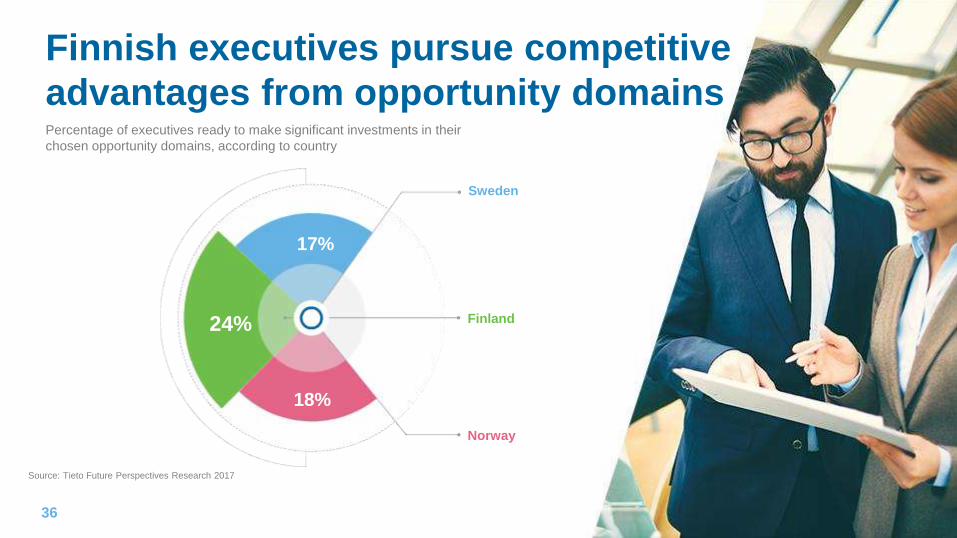

Percentage of executives ready to make significant investments in their

chosen opportunity domains, according to country

Finland

Sweden

Norway

24%

17%

18%

Finnish executives pursue competitive

advantages from opportunity domains

Source: Tieto Future Perspectives Research 2017

Public

of those who stated that digital public services would be

relevant for their industry in the future showed a high

willingness to invest in this opportunity domain.

However, only 18% of those interested in smart health monitoring

showed a high interest in investing.

52%

© Tieto Corporation

Public

38

Percentage of executives that cite various factors are essential for exploiting new disruptive

opportunity domains

Culture and leadership are essential for

utilizing new business opportunities

Technology

Leadership

51%

50%

23%

22%14%

13%

Culture

ProcessesAmbition

Ownership

0% - 60%

Source: Tieto Future Perspectives Research 2017

Public

Culture and leadership

can also be the greatest

barriers to opportunity

domains.

Public

of executives consider culture as the

most important barrier to exploring technology-driven

opportunity domains.

51%

Public

Being a pioneer

is the best approach to

utilizing these opportunity

domains and building

competitive advantages.

Public

of executives aged 30–39 preferred to be early adopters

or pioneers.

And 61% stated that their business had taken

this strategic posture.

67%

© Tieto Corporation

Public

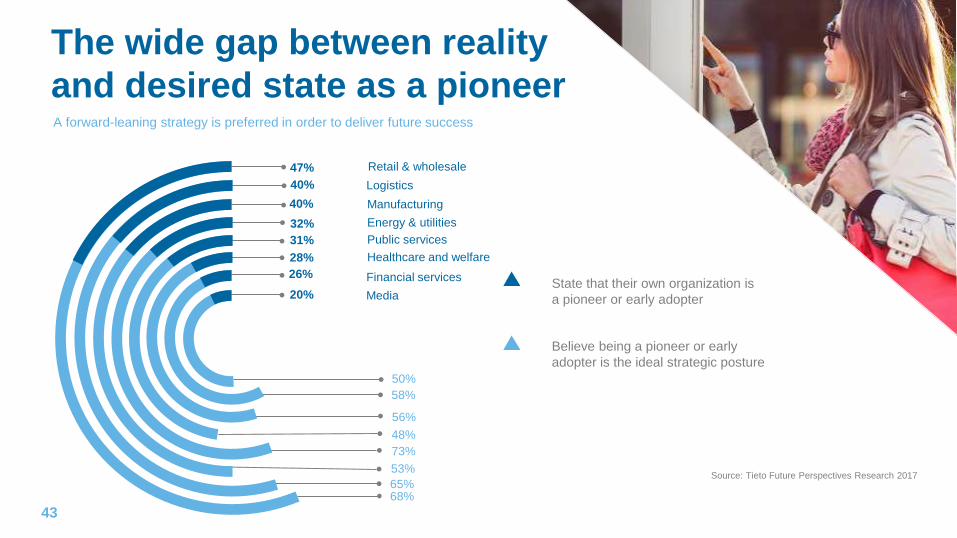

A forward-leaning strategy is preferred in order to deliver future success

The wide gap between reality

and desired state as a pioneer

State that their own organization is

a pioneer or early adopter

Believe being a pioneer or early

adopter is the ideal strategic posture

40%

31%

20%

40%

26%

32%

47%

28%

Media

Logistics

Public services

Retail & wholesale

Energy & utilities

Healthcare and welfare

Manufacturing

58%

48%

68%

73%

65%

56%

50%

53%

Financial services

43

Source: Tieto Future Perspectives Research 2017

Public

of pioneers considered culture the most important

barrier to change.

Conversely, only 38% of late followers listed this

as a key challenge.

62%

Public

4

Future digital possibilities for

Nordic businesses

How will the business models of the future look

and what possibilities will emerge?

© Tieto Corporation

Public

Telecom companies have

more detailed data about

the citizens of the Nordic

countries than their

government do.

More than half of all

companies employ cyber

security firms to protect

their data.

Digitally monitoring supply

chains at least 12 months

in advance is the industry

norm, which ensures on-

time and appropriate

deliveries.

Digital disruptions on the horizon

2020 2025

30% of the top 50 retail

chains feature virtual

reality stores, allowing

customers to try products

via VR.

50% of customer service

in Europe (call center

activities by voice or text)

are performed by

software.

It becomes possible for

industries to custom-order

a computer component

from a factory and receive

the first shipment the

following day.

MOOCs (massive online

open courses) completely

replace conventional

corporate training for most

major companies.

More than half of senior

citizens (over 65) use a

digital health monitoring

device on at least a daily

basis.

More than 10% of Nordic

households produce and

sell excess energy to the

grid.

How do Nordic executives see the future unfolding?

46

Source: Tieto Future Perspectives Research 2017

© Tieto Corporation

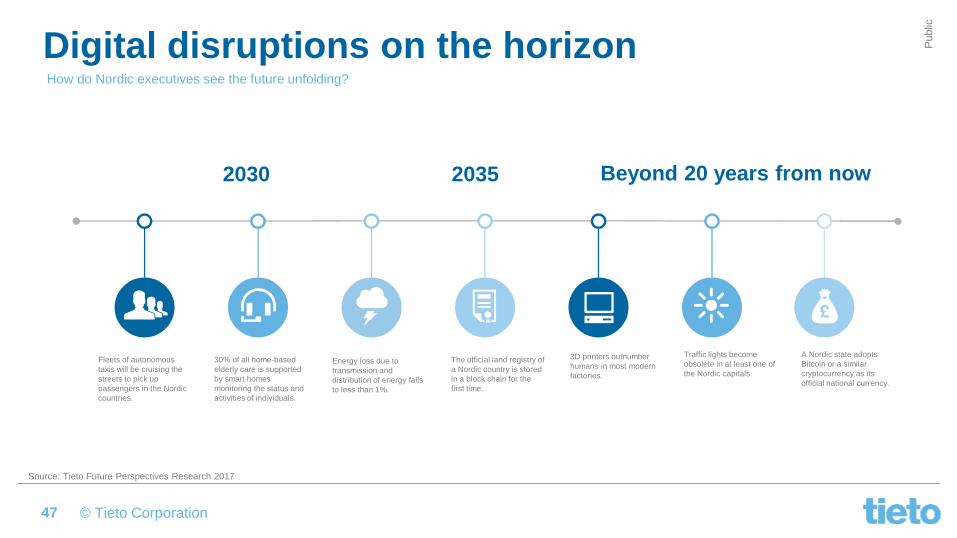

Public

47

Fleets of autonomous

taxis will be cruising the

streets to pick up

passengers in the Nordic

countries.

Digital disruptions on the horizon

2030 2035

30% of all home-based

elderly care is supported

by smart homes

monitoring the status and

activities of individuals.

Energy loss due to

transmission and

distribution of energy falls

to less than 1%.

The official land registry of

a Nordic country is stored

in a block chain for the

first time.

3D printers outnumber

humans in most modern

factories.

Traffic lights become

obsolete in at least one of

the Nordic capitals.

Beyond 20 years from now

A Nordic state adopts

Bitcoin or a similar

cryptocurrency as its

official national currency.

How do Nordic executives see the future unfolding?

Source: Tieto Future Perspectives Research 2017

© Tieto Corporation

Public

Public

What is your next move? Will you be the one defining

tomorrow’s business opportunities or following the pioneers.

The choice is yours.

Public

Ahmad Qureshi

Head of Tieto Digitalization and Strategic Development

Raghunath Koduvayur

Head of Strategic Marketing

Päivi Huuhtanen

Head of Digital Communications and External Affairs