M&A Quarterly For additional information or inquiries, please contact one of our team members: www.pmcf.com PLASTICS & PACKAGING THIRD QUARTER 2015 John D. Hart 248.223.3468 [email protected]Matt G. Jamison 248.223.3368 [email protected]Ryan R. Shuchman 248.603.5372 [email protected]Erik K. Wittbold 248.603.5397 [email protected]

Transcript

Top News in PLASTICS AND PACKAGING

M&A Quarterly

For additional information or inquiries, please contact one of our team members:

P&M Corporate Finance (“PMCF”) is an investment banking firm, focused exclusively on middle market transactions, with professionals in Chicago, Detroit, and across the globe through Corporate Finance International associates. Our dedicated Plastics and Packaging Group has deep industry knowledge and covers a wide range of processes including thermoforming, sheet and film extrusion, blow molding, injection molding, and resin and color compounding. Offering a breadth of advisory services, the Plastics and Packaging Group has helped clients worldwide meet their sale, acquisition, financing, and strategic growth objectives.

Investment Banking Services:

• Mergers & Acquisitions

• Sales & Divestitures

• Capital Raising

• Sale Planning

CHICAGO225 W. Washington Street, Suite 2700Chicago, IL 60606312.602.3600

DETROITTwo Towne Square, Suite 425Southfield, MI 48076248.603.5300

Engineered ComponentsInjection Molding and Extrusion

Company Merger withStrategic Partner

pmcf.com

M&A Quarterly – Plastics & Packaging

2

2015 plastics and packaging M&A volume reflected a flat, and slightly downward trend, in the second quarter of the year. However, the market may have simply been pausing for a breath as M&A deal count through the third quarter is now up signifi-cantly over 2014 levels. Plastics and packaging transactions totaled 251 through the third quarter in 2015 versus a total of 240 for the same period last year.

Driving this increase was strong buying activity from private equity platform investors driven in part by continued access to low cost debt. These buyers have been nearly 70% more active year to date in the plastics and packaging sector as compared to last year. Foreign financial buyers have also been increasingly active within plastics and packaging, completing 77% more deals through the third quarter of 2015 versus the same period in 2014.

Key Q3 2015 plastics and packaging M&A trends included the following:

• Aggressive private equity activity has pushed strategic buyers to their lowest overall percentage of transaction activity in several years at 58%

• Most plastic segments grew in terms of deal count year over year with the exception of resin and compounding. This likely does not reflect buyer interest, which remains strong, and is more attributable to timing of deal closings in our opinion

• Packaging deals are up 33 transactions through the third quarter of 2015 and have already exceeded 2014’s four quarter total. The largest M&A growth sector in plastic packaging was rigid converters followed by flexible converters

• Publicly traded plastic businesses who were outperforming the S&P 500 at the end of the second quarter this year are now trading at parity at the end of the third quarter

Key transactions for the quarter included the following:

• Gerresheimer AG’s (DB:GXI) acquisition of Centor, from Montagu private equity, for $725 million or 9.8x EBITDA

• Berry Plastics Group, Inc.’s (NYSE:BERY) acquisition of AVINTIV from The Blackstone Group for approximately $2.5 billion

• Jarden Corporation’s (NYSE:JAH) acquisition of The Waddington Group from private equity firm Olympus Partners for $1.35 billion

• Solvay SA’s (ENXTBR:SOLB) acquisition of competitor Cytec Industries (NYSE:CYT) for approximately $6.4 billion

• Ireland–based injection molder One51 plc’s acquisition of IPL Inc., from Novacap private equity, for approximately $220 million

Year to date activity clearly reflects a continuation of a strong M&A environment in plas-tics and packaging and what is generally agreed to be a “seller’s market.” We’ve received numerous inquiries as to whether the M&A market has peaked and when we believe it will start to decline. PMCF’s current view is that plastics and packaging M&A should continue to be strong in 2016 given the strategic and private equity buyer dynamics, low cost and availability of debt, and the generally positive economic outlook. Beyond 2016 however, we are more cautious given the cyclical nature of M&A and the fact we will be in our 7th year of a strong M&A market cycle.

Strategic Financial Add-On Financial Platform

220

55

72

347

235

68

79

382

213

56

59

328

162

37

41

240

266

60

67

393

0

50

100

150

200

250

300

400

450

350

20142010 Q3 YTD ‘142011 2012 2013

Num

ber

of D

eals

233

49

59

341

146

43

62

251

Q3 YTD ‘15

Q3 2015 Market Summary & Outlook

Q3 YTD 2015

Q3 YTD 2014

Flexible

Rigid Packaging

9%

Industrial15%

Closures 2%

Bottles 5%

Resin18%

Custom Molding30%

Building Products 6%

FlexiblePackaging

14%

Consumer 1%

Sector‘14 – ’15

Change

Injection Molding

Blow Molding

Film

Resin/Color & Compounding

Sheet & Thermoforming

Specialty

Total

201322

86

60

68

38

54

328

22

95

63

72

23

66

341

17

72

42

51

16

42

240

7%

30%

18%

21%

7%

18%

100%

19

77

49

41

20

45

251

8%

31%

20%

16%

8%

18%

100%

% of Total

% of Total2014

% Change

Q3 YTD‘15

Q3 YTD‘14

2

5

7

-10

4

3

11

12%

7%

17%

-20%

25%

7%

5%Source: P&M Corporate Finance, Company Reports

Flexible

Rigid Packaging

17%

Industrial16%

Consumer3%

Bottles 4%

Resin15%

BuildingProducts

6%

FlexiblePackaging

15%

Custom Molding20%

Closures4%

Transactions by Product Segment

M&A Quarterly – Plastics & Packaging

PMCF

3

Global Plastic Packaging M&A

Trends in M&A:

• Plastic packaging related M&A experienced strong levels of transaction activity through the first three quarters of 2015, with transaction volume up by 33 deals year-over-year through Q3 YTD ‘15. Q3 packaging M&A activity doubled year-over-year

• Packaging businesses in the Food & Beverage, Consumer, and Medical end markets remain highly attractive to both financial and strategic buyers, with all three segments showing significant Q3 YTD ‘15 increases in deal volume versus the comparison period

• Rigid packaging deals accounted for the highest percentage of the overall increase in packaging transactions, with transaction mix for these deals shifting from 27% through Q3 YTD ’14 to 41% through Q3 YTD ‘15

Transactions by Buyer Type Transactions by End Market

0

20

40

60

80

100

120

140

65

53

118

Q3 YTD ‘14

66

48

114

2014

71

47

118

Q3 YTD ‘15

40

30

70

2011

56

43

2012

63

40

103

2013

Strategic Financial

Num

ber

of D

eals 99

Food and Beverage

Industrial

Consumer

Construction

Medical

Automotive

Transportation

Electronics

Total

38

16

10

-

5

1

-

-

70

57

13

23

-

10

-

-

-

103

Q3 YTD ‘15Q3 YTD ‘14

Featured Sector Transactions

July 2015 — Gerresheimer AG (DB:GXI), a global leader in pharmaceutical packaging based in Germany, has acquired Centor US Holding Inc., a former Rexam plc business. Gerresheimer paid $725 million to acquire Centor from Nemera Development which is owned by Montagu private equity. The purchase price reflects a multiple of 9.8x Centor’s LTM EBITDA. Centor’s prod-ucts include plastic vials & closures, applicators, droppers, ointment jars, and oval bottles primarily used in pharmaceutical packaging. Perrysburg, OH-based Centor is one of the leading producers of prescription plastic vials for North American market. The acquisition of Centor provides a significant platform for Gerresheimer to grow its North American operations.

July 2015 — Private equity firm Wellspring Capital Management LLC bought Ampac Holdings LLC which will merge with Pro-lamina Corp. to create a flexible packaging group called Prolampac Intermediate Corp. Ampac is based in Cincinnati and has five U.S. factories, in Cincinnati, OH; Auburn, WA; Minneapolis, MN; and Cary and Hanover Park, IL. According to Plastics News’ most recent ranking, Ampac generated estimated film packaging sales of $154 million. Westfield, MA-based Prolamina generated an estimated $300 million in sales from three factories, in Westfield and Neenah, WI; and Terrebonne, Quebec.

Flexible

Public Acquirer

26%

PrivateAcquirer

32%

PE to PE13%

Private Equity(PE)29%

RigidFlexibleBottlingCaps & Closures

Total

19 33 11 7 70

27% 47% 16% 10% 100%

# % Packaging # % Packaging 42 39 11 11 103

41% 37% 11% 11% 100%

Q3 YTD ‘15Q3 YTD ‘14

Q3 YTD ‘14 Q3 YTD ‘15

Buyer Type

Packaging Transaction Detail

Sources: P&M Corporate Finance, Plastics News, Company Reports

PublicAcquirer

39%

Private Acquirer

20%

Private Equity(PE)35%

PE to PE6%

pmcf.com

M&A Quarterly – Plastics & Packaging

4

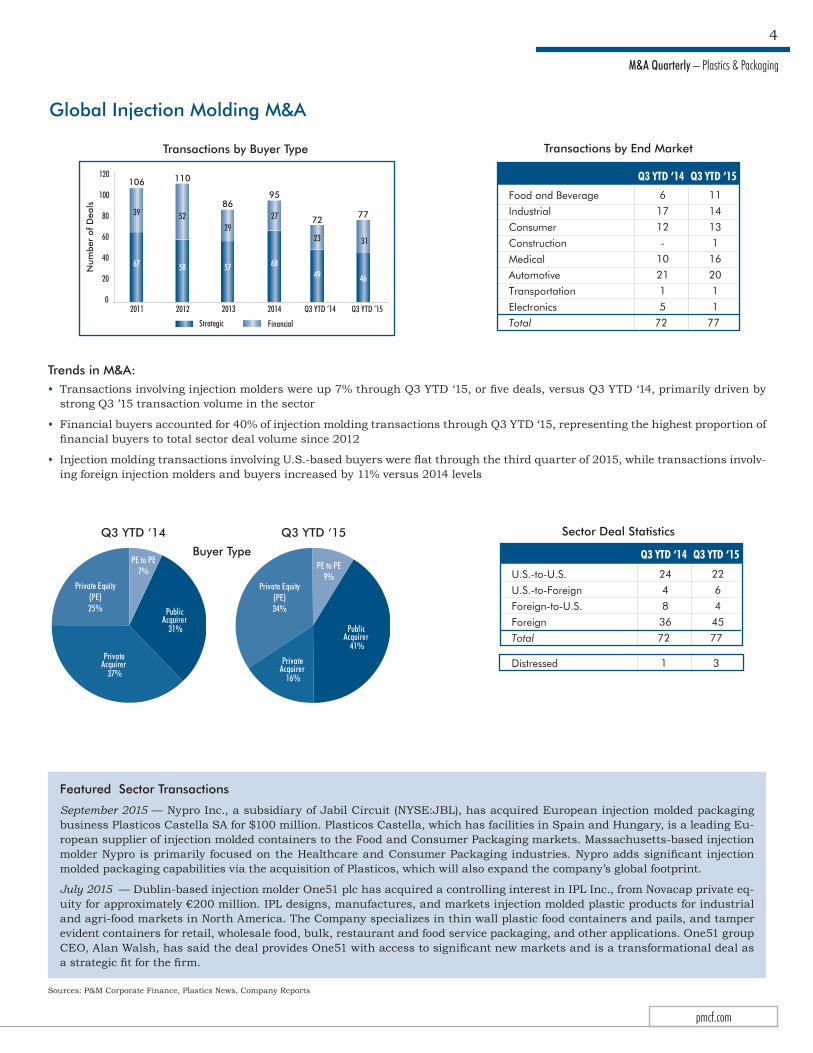

Global Injection Molding M&A

Trends in M&A:• Transactions involving injection molders were up 7% through Q3 YTD ‘15, or five deals, versus Q3 YTD ‘14, primarily driven by

strong Q3 ’15 transaction volume in the sector

• Financial buyers accounted for 40% of injection molding transactions through Q3 YTD ‘15, representing the highest proportion of financial buyers to total sector deal volume since 2012

• Injection molding transactions involving U.S.-based buyers were flat through the third quarter of 2015, while transactions involv-ing foreign injection molders and buyers increased by 11% versus 2014 levels

Q3 YTD ‘14 Q3 YTD ‘15

Buyer Type

Public Acquirer

31%

Private Acquirer

37%

Private Equity(PE)25%

PE to PE7%

Flexible Public

Acquirer41%

Private Acquirer

16%

Private Equity(PE)34%

PE to PE9% U.S.-to-U.S.

U.S.-to-Foreign

Foreign-to-U.S.

Foreign

Total

Distressed

22

6

4

45

77

3

24

4

8

36

72

1

Q3 YTD ‘15Q3 YTD ‘14

Sector Deal Statistics

Sources: P&M Corporate Finance, Plastics News, Company Reports

Transactions by Buyer Type Transactions by End Market

0

20

40

60

80

100

120

58

52

110

Q3 YTD ‘14

67

39

106

2014

57

29

86

Q3 YTD ‘15

49

23

72

2011

68

27

95

2012

46

31

77

2013

Strategic Financial

Num

ber

of D

eals

Food and Beverage

Industrial

Consumer

Construction

Medical

Automotive

Transportation

Electronics

Total

6

17

12

-

10

21

1

5

72

11

14

13

1

16

20

1

1

77

Q3 YTD ‘15Q3 YTD ‘14

Featured Sector Transactions

September 2015 — Nypro Inc., a subsidiary of Jabil Circuit (NYSE:JBL), has acquired European injection molded packaging business Plasticos Castella SA for $100 million. Plasticos Castella, which has facilities in Spain and Hungary, is a leading Eu-ropean supplier of injection molded containers to the Food and Consumer Packaging markets. Massachusetts-based injection molder Nypro is primarily focused on the Healthcare and Consumer Packaging industries. Nypro adds significant injection molded packaging capabilities via the acquisition of Plasticos, which will also expand the company’s global footprint.

July 2015 — Dublin-based injection molder One51 plc has acquired a controlling interest in IPL Inc., from Novacap private eq-uity for approximately €200 million. IPL designs, manufactures, and markets injection molded plastic products for industrial and agri-food markets in North America. The Company specializes in thin wall plastic food containers and pails, and tamper evident containers for retail, wholesale food, bulk, restaurant and food service packaging, and other applications. One51 group CEO, Alan Walsh, has said the deal provides One51 with access to significant new markets and is a transformational deal as a strategic fit for the firm.

M&A Quarterly – Plastics & Packaging

PMCF

5

Global Film M&A

Trends in M&A:

• Transactions involving film extruders and converters increased by 7 deals through Q3 YTD ’15, with the year-over-year shift driven primarily by increasing deal volume in the Consumer and Food & Beverage end markets

• Foreign M&A transactions involving film businesses experienced a sharp increase through the first three quarters of 2015, up 8 deals, or 29% versus the comparison period

• Strategic buyers remained the most active buyers in the film segment, representing 59% of total transaction volume through Q3 YTD ’15. This percentage was slightly down from the same period last year

Q3 YTD ‘14 Q3 YTD ‘15

Buyer Type

Flexible

PrivateAcquirer

36%

Public Acquirer

26%Private Equity(PE)31%

PE to PE7%

Flexible

PrivateAcquirer

24%

Public Acquirer

35%Private Equity(PE)37%

PE to PE4% U.S.-to-U.S.

U.S.-to-Foreign

Foreign-to-U.S.

Foreign

Total

Distressed

9

2

3

28

42

2

Q3 YTD ‘14

11

2

-

36

49

-

Q3 YTD ‘15

Sector Deal Statistics

Sources: P&M Corporate Finance, Plastics News, PE Hub, Company Reports

Transactions by Buyer Type Transactions by End Market

Food and Beverage

Industrial

Consumer

Construction

Medical

Automotive

Transportation

Electronics

Total

26

13

7

-

2

-

-

1

49

Q3 YTD ‘15

22

14

4

-

2

-

-

-

42

Q3 YTD ‘14

Featured Sector Transactions

• September 2015 — Berry Plastics Group, Inc. (NYSE:BERY) has acquired AVINTIV from The Blackstone Group for approxi-mately $2.5 billion. AVINTIV is a leading global supplier of polypropylene and polyethylene flexible nonwoven products and other specialty materials primarily used in infection prevention and personal care markets. AVINTIV employs over 4,500 people and has 23 locations in 14 countries. Berry Plastics, which generated annual sales of roughly $5 billion in 2014, adds a number of new technologies and products to its diversified plastic packaging platform with the acquisition. Roughly half of Berry’s revenue was generated through flexible packaging prior to acquiring AVINTIV.

• September 2015 — Private equity group Olympus Partners has acquired Liqui-Box Holdings Inc. from investment firm The Sterling Group. Liqui-Box, a former DuPont Co. subsidiary based in Virginia, is a leading producer of bag-in-box packaging for the dairy, beverage, food, and wine markets. Liqui-Box represents a new platform for Stamford, CT-based Olympus Partners, who has made prior investments in a number of plastics and packaging businesses including Pregis and The Waddington Group. Olympus hopes to leverage its experience and relationships in the industry to expand Liqui-Box to new customers, geographies, and products.

Strategic Financial

45

23

68

Q3 YTD ‘14

48

27

75

2014

41

19

60

Q3 YTD ‘15

26

16

42

2011

35

28

63

2012

29

20

49

2013

Num

ber

of D

eals

0

10

20

30

40

60

80

50

70

pmcf.com

M&A Quarterly – Plastics & Packaging

6

Global Resin and Color & Compounding M&A

Trends in M&A:

• Transactions involving resin suppliers and color & compounders were down 20% year-over-year through the first three quarters of 2015 versus Q3 YTD 2014 results and appear to be trending below 2014’s high point. However, our view is that this is likely a timing-based trend versus lack of buyer interest which remains robust

• Resin suppliers accounted for 66% of transaction mix in Q3 YTD 2015, a 7% increase in their proportion of total deal volume versus the comparison period

• The declining number of domestic transactions involving the sale of U.S. resin suppliers and color & compounders was a signifi-cant driver of the overall decrease in deal volume, falling by 10 deals in Q3 YTD 2015 compared to Q3 YTD 2014 levels

Q3 YTD ‘14 Q3 YTD ‘15

Buyer Type

Flexible

PrivateAcquirer

25%

Public Acquirer

43%

Private Equity(PE)25%

PE to PE6%

Flexible

PrivateAcquirer

16%

Public Acquirer

45%

Private Equity(PE)30%

PE to PE9% U.S.-to-U.S.

U.S.-to-Foreign

Foreign-to-U.S.

Foreign

Total

Distressed

8

2

5

26

41

-

Q3 YTD ‘15

18

5

2

26

51

2

Q3 YTD ‘14

Sector Deal Statistics

Sources: P&M Corporate Finance, Plastics News, Company Reports

Transactions by Buyer Type

Featured Sector Transactions

• July 2015 — Belgian chemical company Solvay SA (ENXTBR:SOLB) has acquired American competitor Cytec Industries (NYSE:CYT) for approximately $5.5 billion in cash. Solvay paid $75.25 a share for Cytec, which represents a 29% premium to the company’s July 28th closing price. The deal values Cytec at $6.4 billion including debt. New Jersey-based Cytec produces a variety of specialty chemicals and resin systems primarily for aerospace and industrial applications. The company has 49 locations globally and employs more than 4,500 people. Solvay, which is based in Belgium, is a leading global supplier of spe-cialty chemicals and materials to the aerospace, automotive, and electronics industries.

• July 2015 — Germany-based Domo Chemicals has acquired American compounder Technical Polymers LLC. Buford, GA-based Technical Polymers develops and manufactures high-performance engineering polymers and specialized elastomers. The company has annual sales of approximately $35 million, with 60 to 70 percent of annual sales to major U.S. automakers according to Technical Polymers CEO Ron Kay. The acquisition will provide Domo with a platform for footprint expansion in the U.S., specifically in the U.S. southeast to support the growing number of German automotive OEM’s in the region.

• Sheet and thermoforming transactions were up by 4 deals through Q3 YTD ‘15, an increase of 25% compared to Q3 YTD ‘14 levels, as deal volumes trend toward a potentially higher level than 2014

• Transaction mix was heavily weighted toward Food & Beverage deals through Q3 YTD 2015, accounting for 60% of total deals versus 25% through three quarters in 2014

• Foreign sheet and thermoforming deals represented 75% of total transaction volume in Q3 YTD 2015, reflecting the high levels of consolidation within the US market which has limited available acquisition targets

Q3 YTD ‘14 Q3 YTD ‘15

Buyer Type

Flexible

Private Equity(PE)44%

Private Acquirer

31%

Public Acquirer

25%Flexible Private Equity

(PE)30%

PE to PE5%

Public Acquirer

45%

Private Acquirer

20%

U.S.-to-U.S.

U.S.-to-Foreign

Foreign-to-U.S.

Foreign

Total

Distressed

3

2

1

14

20

-

Q3 YTD ‘15

6

-

2

8

16

1

Q3 YTD ‘14

Sector Deal Statistics

Sources: P&M Corporate Finance, Plastics News, Company Reports

Transactions by Buyer Type Transactions by End Market

Food and Beverage

Industrial

Consumer

Construction

Medical

Automotive

Transportation

Electronics

Total

12

4

1

-

-

1

2

-

20

Q3 YTD ‘15

4

7

2

-

1

-

2

-

16

Q3 YTD ‘14

Featured Sector Transactions

• July 2015 — Global consumer products conglomerate Jarden Corporation (NYSE:JAH) has acquired The Waddington Group from private equity firm Olympus Partners for $1.35 billion. Waddington, which has annual sales of approximately $800 mil-lion, is a leading supplier of food-service products. Waddington employs 2,900 people across 17 manufacturing facilities in Europe and North America. The acquisition significantly expands Jarden Corp’s thermoforming capabilities and also adds additional injection molding technology. Jarden Corp also adds well known brand names such as WNA, Polar Pak, Par-Pak, Waddington, and Eco Products to its existing portfolio of over 120 brands.

• August 2015 — Swiss packaging group Stäger & Co. has acquired Czech Republic-based thermoformer Innovac s.r.o. Innovac produces packaging solutions that include component carriers, blisters, and trays for the automotive, electronics, and con-sumer goods industries. Stäger & Co. manufacturers a variety of transparent packaging products and has production facili-ties in the United Kingdom, Czech Republic, and Switzerland. Stäger will relocate Innovac’s production and management team to a modern production facility to allow for expansion and the installation of additional equipment.

• Transaction volume among blow molders remained relatively flat through the first three quarters of 2015, up by 2 deals versus the same period in 2014

• Publicly traded buyers accounted for 42% of blow molding transactions through Q3 YTD 2015, increasing their proportion of total deal volume by 7%, while privately held and financial buyers both experienced a drop in their proportion of deals compared with Q3 YTD 2014 levels

• Transactions involving industrial blow molders were up 50% through Q3 YTD 2015 versus Q3 YTD 2014, recording the highest proportion of end market transaction mix during the period

Q3 YTD ‘14 Q3 YTD ‘15

Buyer Type

Flexible

Private Equity(PE)24%

Private Acquirer

24%

Public Acquirer

35%PE to PE

17%Flexible

Private Equity(PE)32%

Private Acquirer

21%

Public Acquirer

42%PE to PE

5%

U.S.-to-U.S.

U.S.-to-Foreign

Foreign-to-U.S.

Foreign

Total

Distressed

3

-

1

15

19

2

Q3 YTD ‘15

6

-

1

10

17

4

Q3 YTD ‘14

Sector Deal Statistics

Transactions by Buyer Type Transactions by End Market

Food and Beverage

Industrial

Consumer

Construction

Medical

Automotive

Transportation

Electronics

Total

8

4

3

-

-

2

-

-

17

Q3 YTD ‘14

5

6

6

-

1

1

-

-

19

Q3 YTD ‘15

Featured Sector Transactions

• August 2015 — Eastern Trading Co Ltd., parent company of All Joy Foods, has acquired South African blow molder Winplas Packaging Limited. Winplas, who operates manufacturing facilities in Cape Town and Johannesburg, produces PET bottles and jars for the food and beverage markets. Eastern Trading Co, which is also based in South Africa, operates a number of food processing businesses. The acquisition of Winplas provides vertical integration into PET plastic packaging, which will support expansion into long shelf life food and beverage products.

• July 2015 — Hong Leong Asia Ltd. (SGX:H22) has acquired the remaining 75% equity stake in blow molded packaging joint venture Tianjin Rex Packaging Co. through its subsidiary Rex Holdings. China-based Tianjin Rex Packaging manufactures a range of blow molded packaging products including bottles, drums, pails, and other industrial containers. Hong Leong Asia is a diversified industrial manufacturing conglomerate that currently operates four plastic packaging facilities in China and Malaysia. The acquisition of Tianjin Rex Packaging will add a wholly owned 300,000 foot manufacturing facility to Hong Le-ong’s existing industrial packaging platform.

Sources: P&M Corporate Finance, Plastics News, Company Reports

M&A Quarterly – Plastics & Packaging

PMCF

9

Additional Global Specialty Sector Activity

Trends in M&A:

• Q3 YTD ‘15 transactions involving specialty plastic process types, including rotational molding, foam, pipe & tube, profile extrusion, and composites, experienced a slight increase in deal volume, up by 7% compared to Q3 YTD ‘14

• Mix between financial and strategic buyers shifted in Q3 YTD ’15 as M&A activity among financial buyers rose significantly, accounting for 42% of specialty M&A volume versus 21% through the same period in 2014

• Trends experienced during the first half continued through the third quarter of 2015 as industrial activity increased while construction related specialty deals leveled off

FEATURED SECTOR TRANSACTIONS

Pipe & Tube

August 2015 — Denmark-based Micro Matic A/S, a subsidiary of Nielsen & Nielsen Holding, has acquired Valpar Industrial Ltd. from the O’Neill Group. Valpar, which is headquartered in Northern Ireland, is one of the world’s largest manufacturers of beverage tubes and dispensing “pythons” for the beverage industry. The company produces a number of specialty tubing products for the beverage, automotive, and industrial industries. Micro Matic, a diversified supplier of dispensing equipment and components, will add significant extruding capabilities and tubing products to its portfolio via the acquisition.

Specialty Converting

August 2015 — Plastic box converters Printex Packaging Inc. and Transparent Packaging have merged to create a leading regional supplier of specialty packaging. The combined entity will operate as Printex Transparent Packaging, Inc. and have manufacturing facilities located in St. Laurent, Quebec and Islandia, New York. The company’s primary products, transpar-ent plastic boxes, offer a stylish alternative to paper folding carton and corrugated packaging options. These products are typically converted from PET sheet and utilized in consumer packaging applications.

Engineered Foam

September 2015 — Unique Fabricating, Inc. (NYSE MKT:UFAB) has acquired Michigan-based Great Lakes Foam Tech-nologies, Inc. Great Lakes produces a range of molded polyurethane components for the Automotive, ORV, and Industrial Equipment industries. Unique Fabricating, which is also headquartered in Michigan, engineers and manufactures foam, rubber, and plastic components utilized in noise, vibration and harshness management applications primarily for the Automotive market. Unique Fabricating paid $12 million in cash at closing, representing a 6.0x multiple of Great Lake’s 2014 EBITDA of $2 million.

Source: P&M Corporate Finance, Plastics News, Company Reports

Transactions by Buyer Type Transactions by End Market

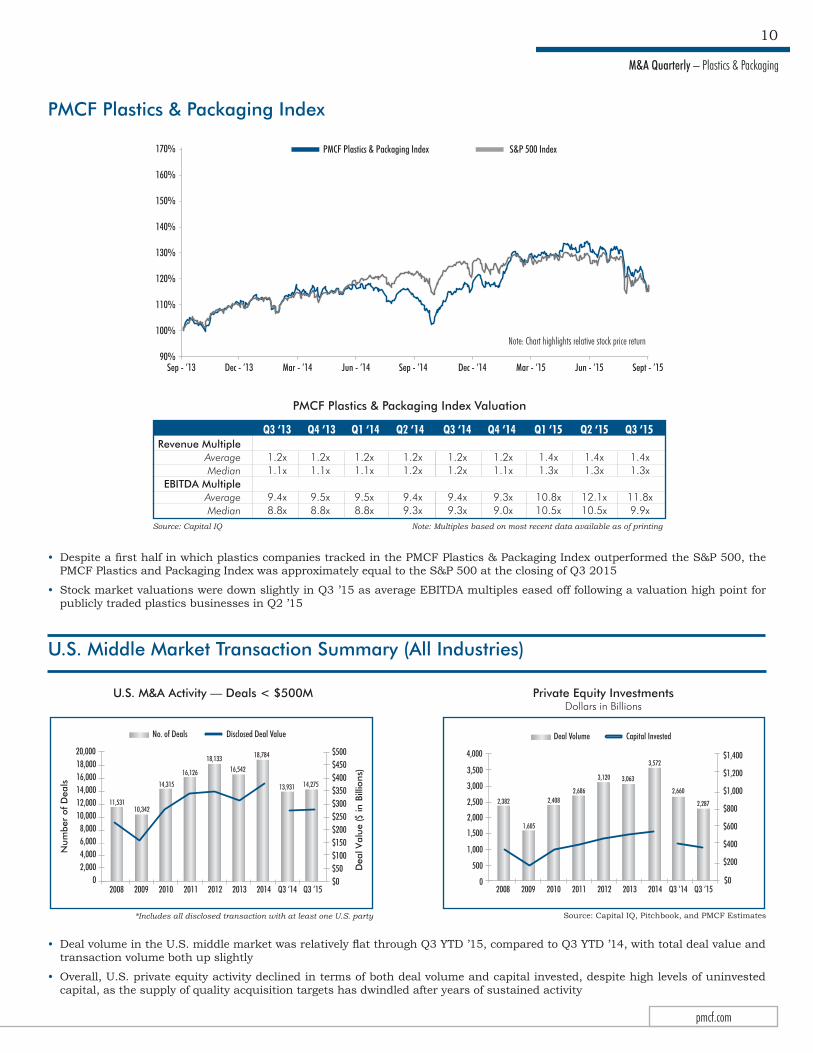

• Despite a first half in which plastics companies tracked in the PMCF Plastics & Packaging Index outperformed the S&P 500, the PMCF Plastics and Packaging Index was approximately equal to the S&P 500 at the closing of Q3 2015

• Stock market valuations were down slightly in Q3 ’15 as average EBITDA multiples eased off following a valuation high point for publicly traded plastics businesses in Q2 ’15

Revenue MultipleAverageMedian

EBITDA MultipleAverageMedian

1.4x1.3x

12.1x10.5x

Q3 ‘15

1.2x1.1x

9.4x8.8x

1.4x1.3x

11.8x9.9x

Q3 ‘13

1.2x1.1x

9.5x8.8x

Q4 ‘13

1.2x1.1x

9.5x8.8x

Q1 ‘14 Q2 ‘14

1.2x1.2x

9.4x9.3x

1.2x1.2x

9.4x9.3x

Q3 ‘14

1.2x1.1x

9.3x9.0x

Q4 ‘14

1.4x1.3x

10.8x10.5x

Q1 ‘15 Q2 ‘15

Private Equity InvestmentsDollars in Billions

No. of Deals Disclosed Deal Value

Num

ber

of D

eals

0

Dea

l Val

ue ($

in B

illio

ns)

$0$50$100$150$200$250$300$350$400$450$500

2,000 4,000 6,000 8,000

10,000 12,000 14,000 16,000 18,00020,000

2008

18,784

2009

11,531

2010

10,342

2011

14,315

2012

16,126

2013

18,133

2014

16,542

Q3 ‘14 Q3 ‘15

13,931 14,275

Deal Volume Capital Invested

Num

ber

of D

eals

$00

Dea

l Val

ue ($

in B

illio

ns)

2008 2009

3,572

2010

2,382

2012

1,605

2014

2,408

Q3 ‘14

2,686

Q3 ‘15

3,120 3,063

$200

$400

$600

$800

$1,000

$1,200

$1,400

500

1,000

1,500

2,000

2,500

3,000

4,000

3,500

2,660

2,287

2011 2013

• Deal volume in the U.S. middle market was relatively flat through Q3 YTD ’15, compared to Q3 YTD ’14, with total deal value and transaction volume both up slightly

• Overall, U.S. private equity activity declined in terms of both deal volume and capital invested, despite high levels of uninvested capital, as the supply of quality acquisition targets has dwindled after years of sustained activity

U.S. M&A Activity — Deals < $500M

U.S. Middle Market Transaction Summary (All Industries)

Source: Capital IQ, Pitchbook, and PMCF Estimates

Note: Multiples based on most recent data available as of printingSource: Capital IQ

*Includes all disclosed transaction with at least one U.S. party

plastics.pmcf.com

Suite 425Two Towne SquareSouthfield, MI 48076

This market overview is not an offer to sell or a solicitation of an offer to buy any security. It is not intended to be directed to investors as a basis for making an investment decision. This market overview does not rate or recommend securities of individual companies, nor does it contain sufficient information upon which to make an investment decision.

P&M Corporate Finance, LLC will seek to provide investment banking and/or other services to one or more of the companies mentioned in this market overview.

P&M Corporate Finance, LLC, and/or the analysts who prepared this market update, may own securities of one or more of the companies mentioned in this market overview.

The information provided in this market overview was obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. It is not to be construed as legal, accounting, financial, or investment advice. Information, opinions, and estimates reflect P&M Corporate Finance, LLC’s judgment as of the date of publication and are subject to change without notice. P&M Corporate Finance, LLC undertakes no obligation to notify any recipient of this market overview of any such change.

The charts and graphs used in this market overview have been compiled by P&M Corporate Finance, LLC solely for illustrative purposes. All charts are as of the date of issuance of this market overview, unless otherwise noted.

The PMCF Plastics Index may not be inclusive of all companies in the plastics industry and is not a composite index of the plastic industry sector returns. Index and sector returns are past performance which is not an indicator of future results.

This market overview is not directed to, or intended for distribution to, any person in any jurisdiction where such distribution would be contrary to law or regulation, or which would subject P&M Corporate Finance, LLC to licensing or registration requirements in such jurisdiction.