28

Westlake Chemical Corporation Houston Chemical Intensity Day Goldman Sachs March 24, 2009

Westlake Chemical Corporation

Houston Chemical Intensity DayGoldman SachsMarch 24, 2009

2

SAFE HARBOR LANGUAGE

This presentation may include forward-looking statements, as defined in the Private Securities Litigation Reform Act of 1995, reflecting management’s current analysis and expectations, based on reasonable assumptions. Results could differ materially depending on such factors as business climate, business performance, economic and competitive uncertainties, ability to execute work process redesign and reduce costs, failure to complete transactions or to achieve benefit from transactions, higher manufacturing costs, change in strategies, reduced level of customer orders, risks in developing new products and technologies, adverse legal and regulatory developments including increases in the number or financial exposures of claims, lawsuits, settlements or judgments, or the inability to eliminate or reduce such financial exposures by collecting indemnity payments from insurers, environmental and safety regulations and clean-up costs, foreign exchange rates, and adverse changes in economic and political climates around the world. Accordingly, there can be no assurance that the Company will meet future results, performance or achievements expressed or implied by such forward-looking statements. As appropriate, additional factors are contained in reports filed with the Securities and Exchange Commission. This paragraph is included to provide safe harbor for forward-looking statements, which are generally not required to be publicly revised as circumstances change.

Investor Relations Contact

Steven BenderSr. Vice President, Chief Financial Officer

& Treasurer

Westlake Chemical Corporation2801 Post Oak Boulevard, Suite 600

Houston, Texas 77056713-960-9111

www.westlake.com

3

$ 3.7 BILLION INTEGRATEDPOLYMERS MATERIALS COMPANY

31% of Sales, $1.1 BVinyls Business(2)

450 MMlbsEthylene

1.85 BlbsVCM

550 MMlbsChlorine

1.10 BlbsFabricated Products

605 MMlbsCaustic Soda

2.00 Blbs PVC

$ (30) MMNet Loss

$ 88 MMEBITDA (1)

$ 3.7 B Sales

Westlake Chemical Corporation(FYE 2008)

(1) Non-GAAP financial measure(2) Capacities include China JV

69% of Sales, $2.5 B Olefins Business

980 MMlbsLLDPE & HDPE

570 MMlbsStyrene

1.50 BlbsLDPE

2.50 Blbs Ethylene

4

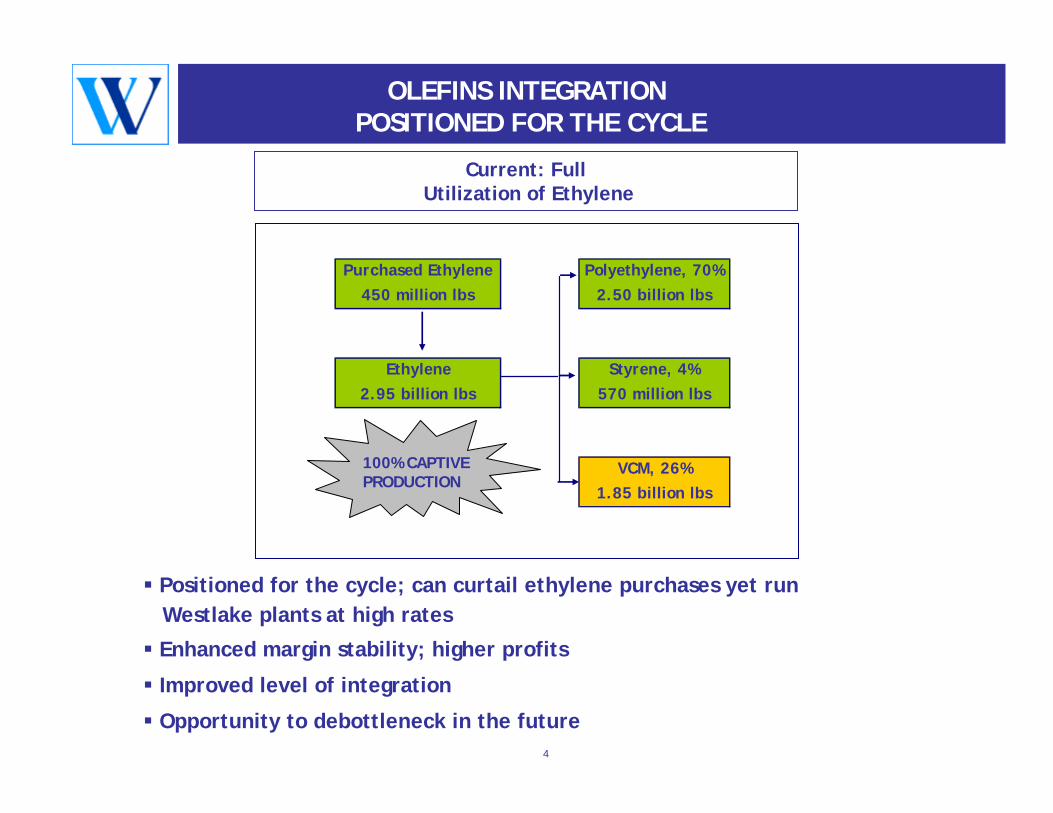

OLEFINS INTEGRATIONPOSITIONED FOR THE CYCLE

Current: FullUtilization of Ethylene

Positioned for the cycle; can curtail ethylene purchases yet runWestlake plants at high rates

Enhanced margin stability; higher profits

Improved level of integration

Opportunity to debottleneck in the future

Purchased Ethylene Polyethylene, 70%450 million lbs 2.50 billion lbs

Ethylene Styrene, 4%2.95 billion lbs 570 million lbs

VCM, 26%1.85 billion lbs

100% CAPTIVE 100% CAPTIVE PRODUCTIONPRODUCTION

5

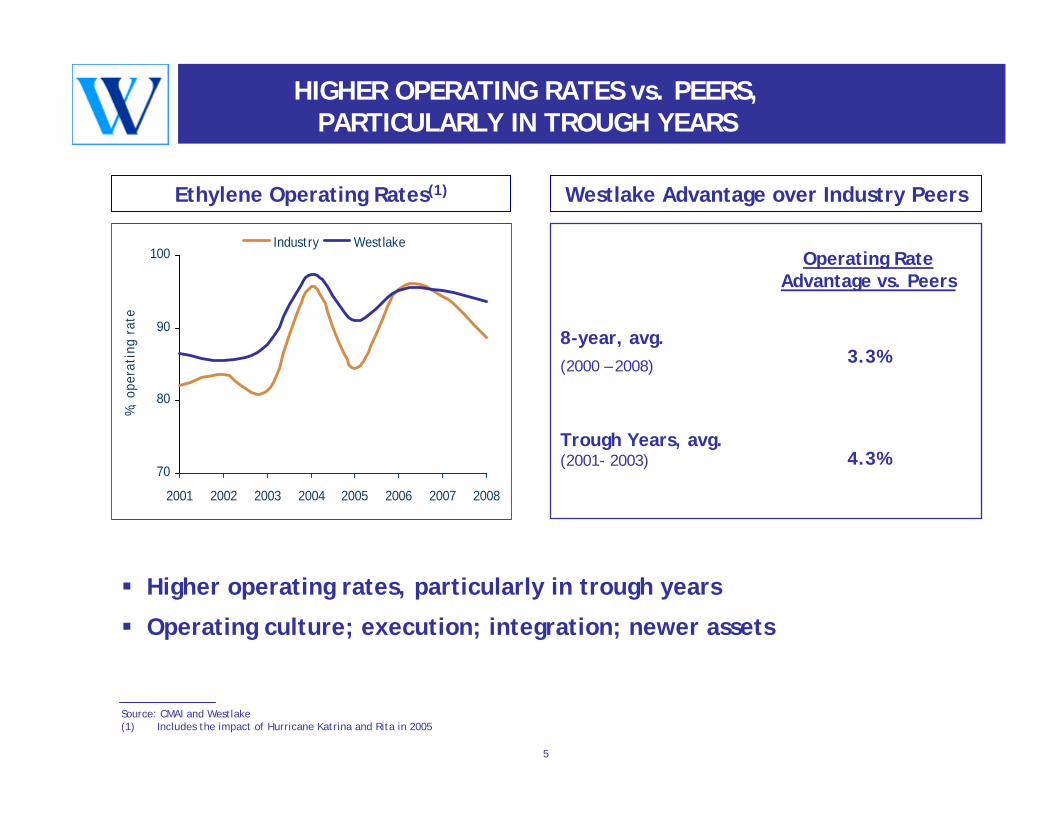

HIGHER OPERATING RATES vs. PEERS, PARTICULARLY IN TROUGH YEARS

Ethylene Operating Rates(1) Westlake Advantage over Industry Peers

Higher operating rates, particularly in trough years

Operating culture; execution; integration; newer assets

70

80

90

100

2001 2002 2003 2004 2005 2006 2007 2008

%,

oper

atin

g ra

te

Industry Westlake

4.3%Trough Years, avg.(2001- 2003)

3.3%8-year, avg.(2000 – 2008)

Operating Rate Advantage vs. Peers

Source: CMAI and Westlake(1) Includes the impact of Hurricane Katrina and Rita in 2005

6

0

4

8

12

16

20

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

E

2012

E

Cen

ts /

lb

Naptha Cash Margin Ethane Cash Margin

6

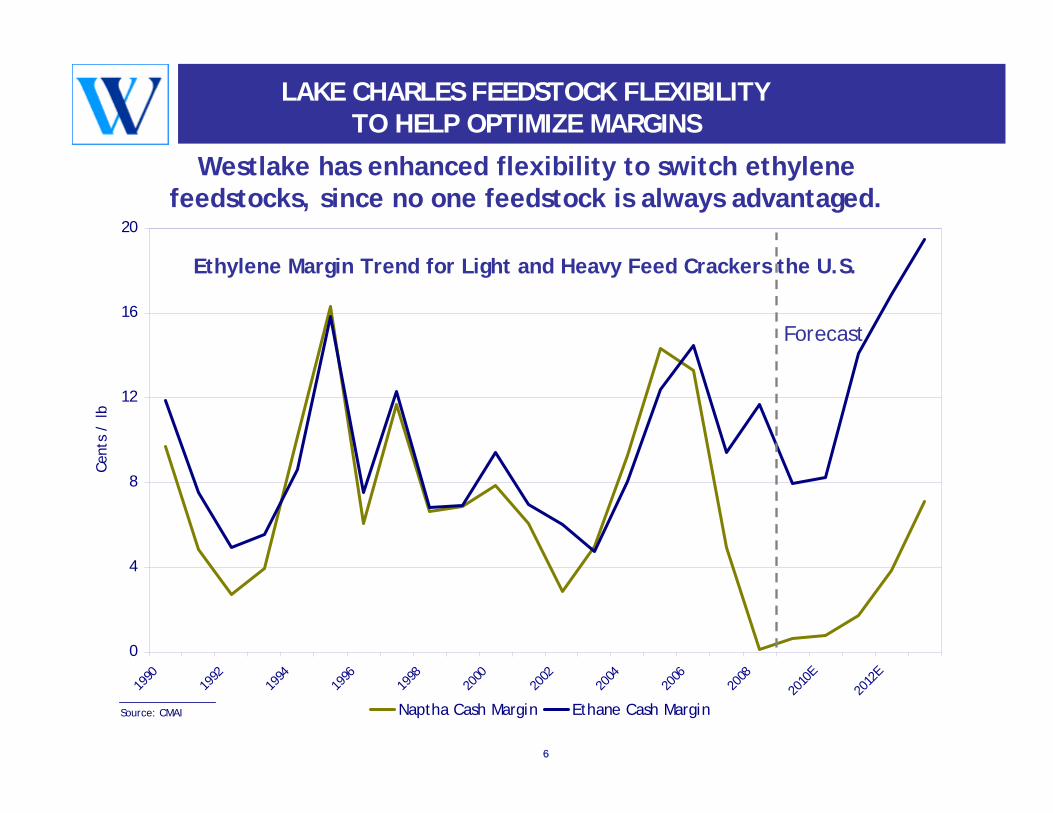

LAKE CHARLES FEEDSTOCK FLEXIBILITY TO HELP OPTIMIZE MARGINS

Westlake has enhanced flexibility to switch ethylene feedstocks, since no one feedstock is always advantaged.

Source: CMAI

Forecast

Ethylene Margin Trend for Light and Heavy Feed Crackers the U.S.

77

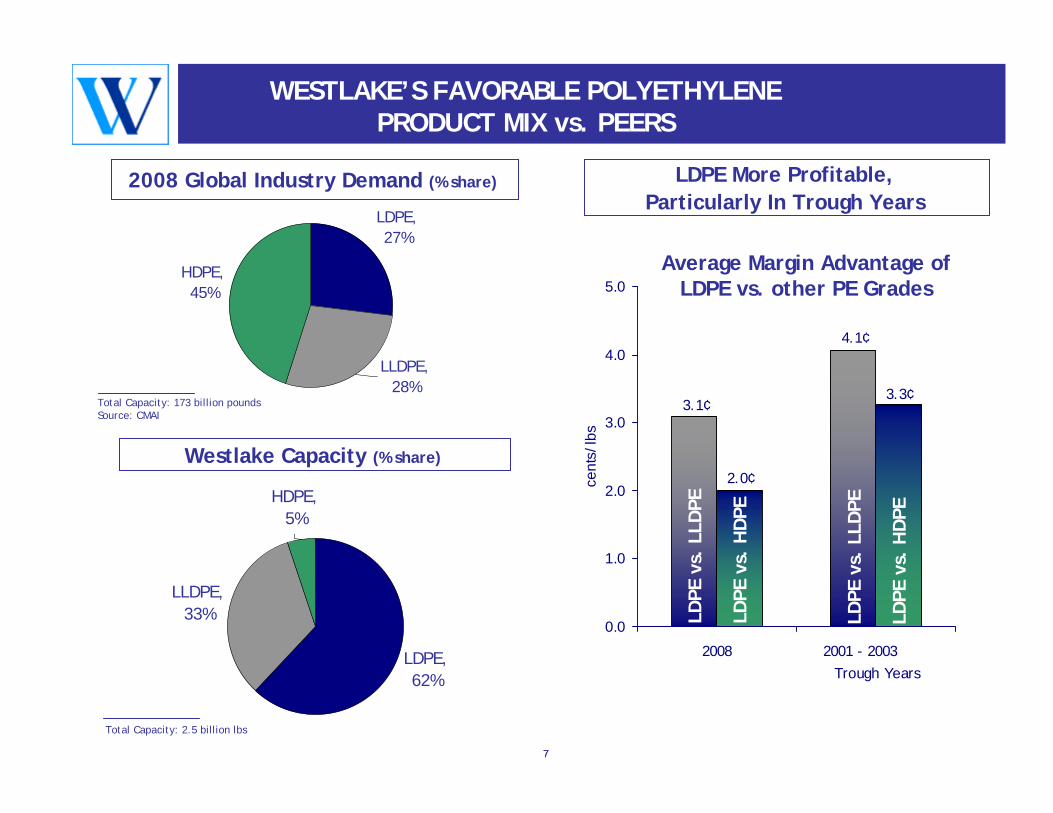

4.1¢

3.1¢3.3¢

2.0¢

0.0

1.0

2.0

3.0

4.0

5.0

2008 2001 - 2003 Trough Years

cent

s/ lb

s

LDPE More Profitable, Particularly In Trough Years

Befo

re

LLDPE, 28%

LDPE, 27%

HDPE, 45%

Total Capacity: 173 billion poundsSource: CMAI

2008 Global Industry Demand (% share)

Westlake Capacity (% share)

LLDPE, 33%

HDPE, 5%

LDPE, 62%

Total Capacity: 2.5 billion lbs

Average Margin Advantage of LDPE vs. other PE Grades

WESTLAKE’S FAVORABLE POLYETHYLENE PRODUCT MIX vs. PEERS

LDPE

vs.

LLD

PE

LDPE

vs.

HD

PE

LDPE

vs.

HD

PE

LDPE

vs.

LLD

PE

88

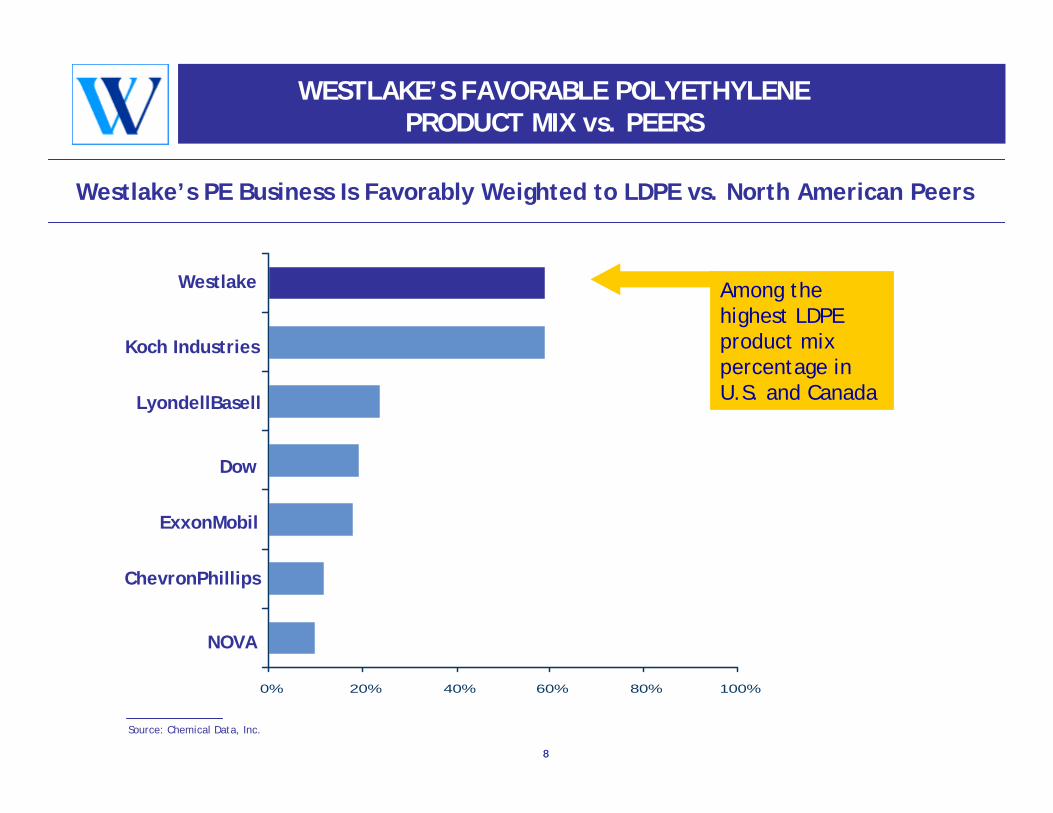

WESTLAKE’S FAVORABLE POLYETHYLENE PRODUCT MIX vs. PEERS

Westlake’s PE Business Is Favorably Weighted to LDPE vs. North American Peers

0% 20% 40% 60% 80% 100%

Among the highest LDPE product mix percentage in U.S. and Canada

Westlake

Koch Industries

LyondellBasell

Dow

ExxonMobil

ChevronPhillips

NOVA

Source: Chemical Data, Inc.

9

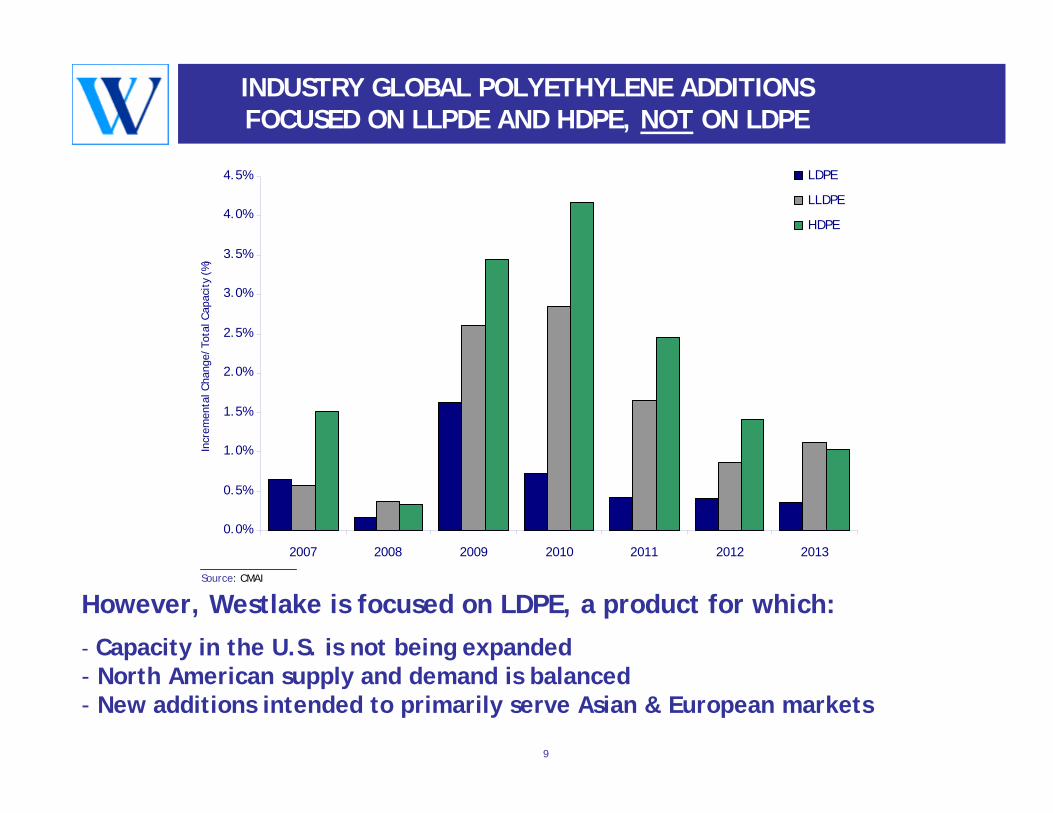

INDUSTRY GLOBAL POLYETHYLENE ADDITIONS FOCUSED ON LLPDE AND HDPE, NOT ON LDPE

However, Westlake is focused on LDPE, a product for which:

- Capacity in the U.S. is not being expanded- North American supply and demand is balanced- New additions intended to primarily serve Asian & European markets

Source: CMAI

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

2007 2008 2009 2010 2011 2012 2013

Incr

emen

tal C

hang

e/To

tal C

apac

ity

(%)

LDPE

LLDPE

HDPE

10

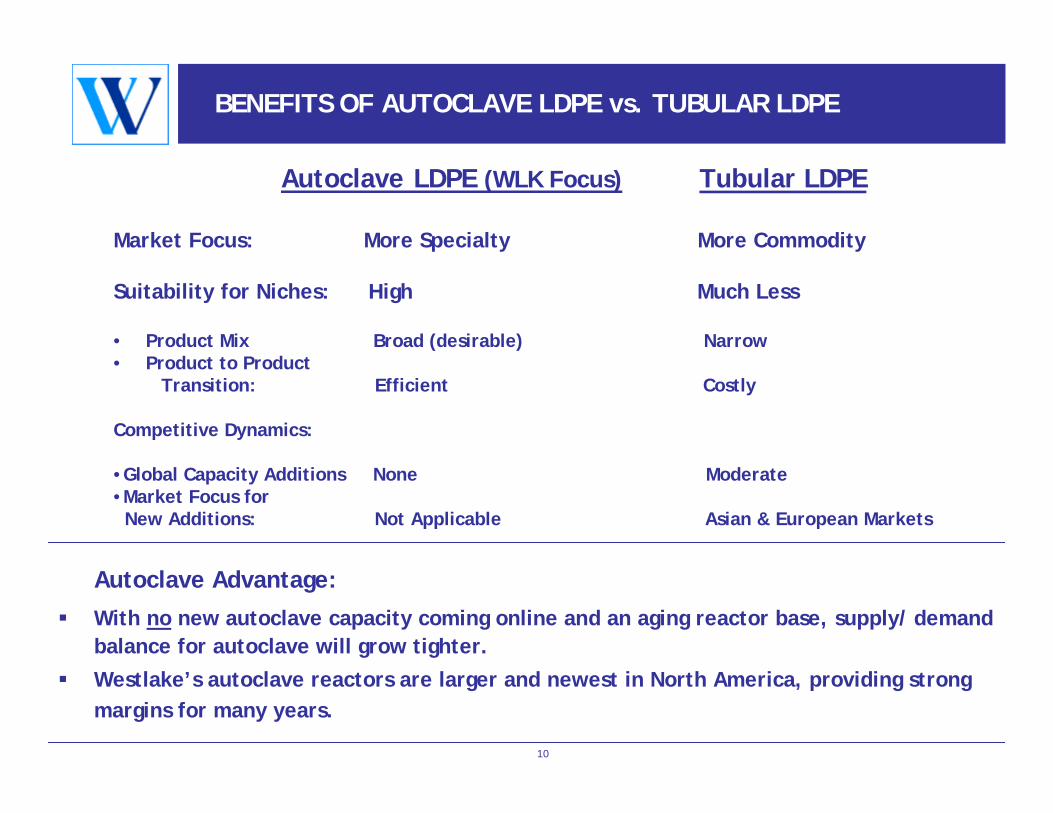

BENEFITS OF AUTOCLAVE LDPE vs. TUBULAR LDPE

Autoclave Advantage:

With no new autoclave capacity coming online and an aging reactor base, supply/ demand balance for autoclave will grow tighter.Westlake’s autoclave reactors are larger and newest in North America, providing strong margins for many years.

Autoclave LDPE (WLK Focus) Tubular LDPE

Market Focus: More Specialty More Commodity

Suitability for Niches: High Much Less

• Product Mix Broad (desirable) Narrow• Product to Product

Transition: Efficient Costly

Competitive Dynamics:

•Global Capacity Additions None Moderate•Market Focus for

New Additions: Not Applicable Asian & European Markets

1111

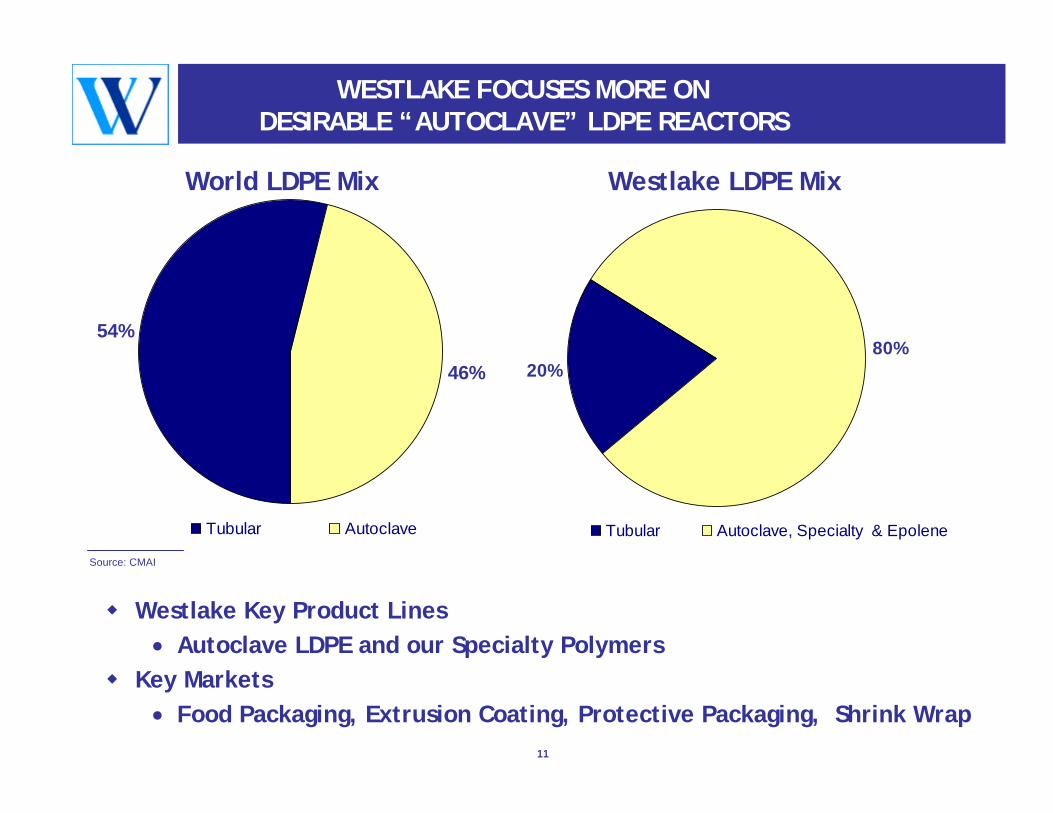

WESTLAKE FOCUSES MORE ON DESIRABLE “AUTOCLAVE” LDPE REACTORS

20%80%

Tubular Autoclave, Specialty & Epolene

Westlake Key Product Lines• Autoclave LDPE and our Specialty Polymers

Key Markets• Food Packaging, Extrusion Coating, Protective Packaging, Shrink Wrap

Westlake LDPE Mix

54%

46%

Tubular Autoclave

World LDPE Mix

Source: CMAI

12

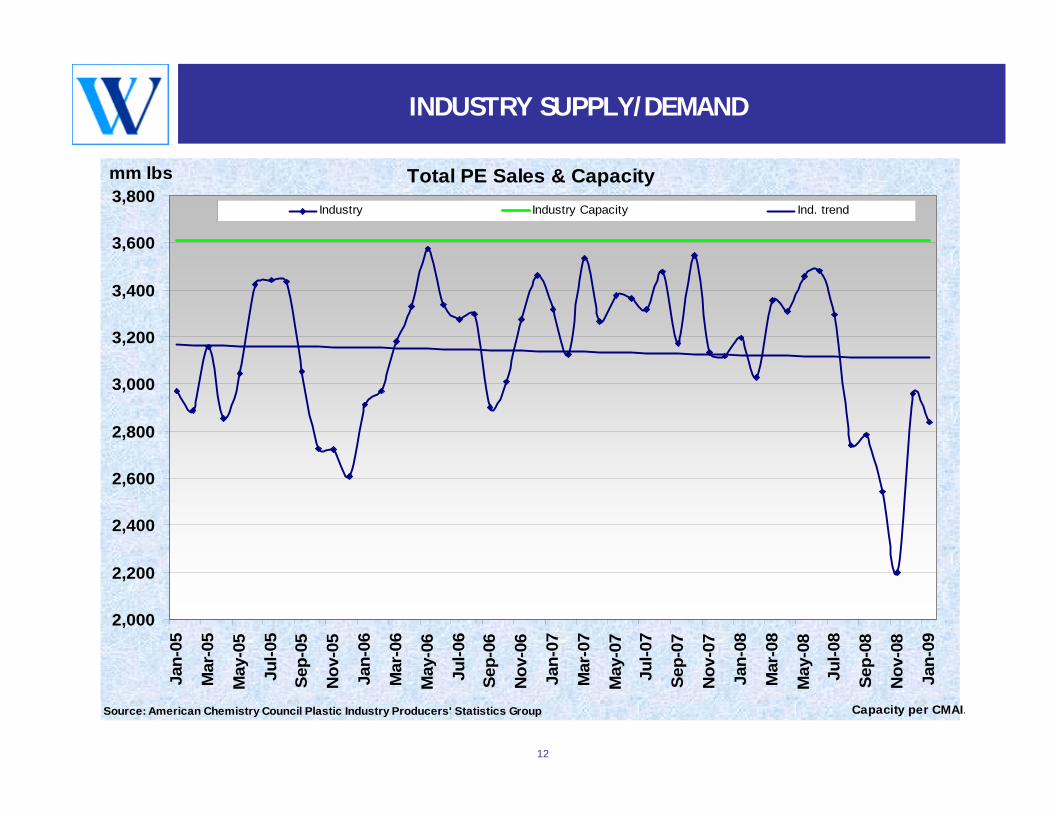

INDUSTRY SUPPLY/DEMAND

Total PE Sales & Capacity

2,000

2,200

2,400

2,600

2,800

3,000

3,200

3,400

3,600

3,800Ja

n-05

Mar

-05

May

-05

Jul-0

5

Sep-

05

Nov

-05

Jan-

06

Mar

-06

May

-06

Jul-0

6

Sep-

06

Nov

-06

Jan-

07

Mar

-07

May

-07

Jul-0

7

Sep-

07

Nov

-07

Jan-

08

Mar

-08

May

-08

Jul-0

8

Sep-

08

Nov

-08

Jan-

09

mm lbs

Industry Industry Capacity Ind. trend

Capacity per CMAI.Source: American Chemistry Council Plastic Industry Producers' Statistics Group

13

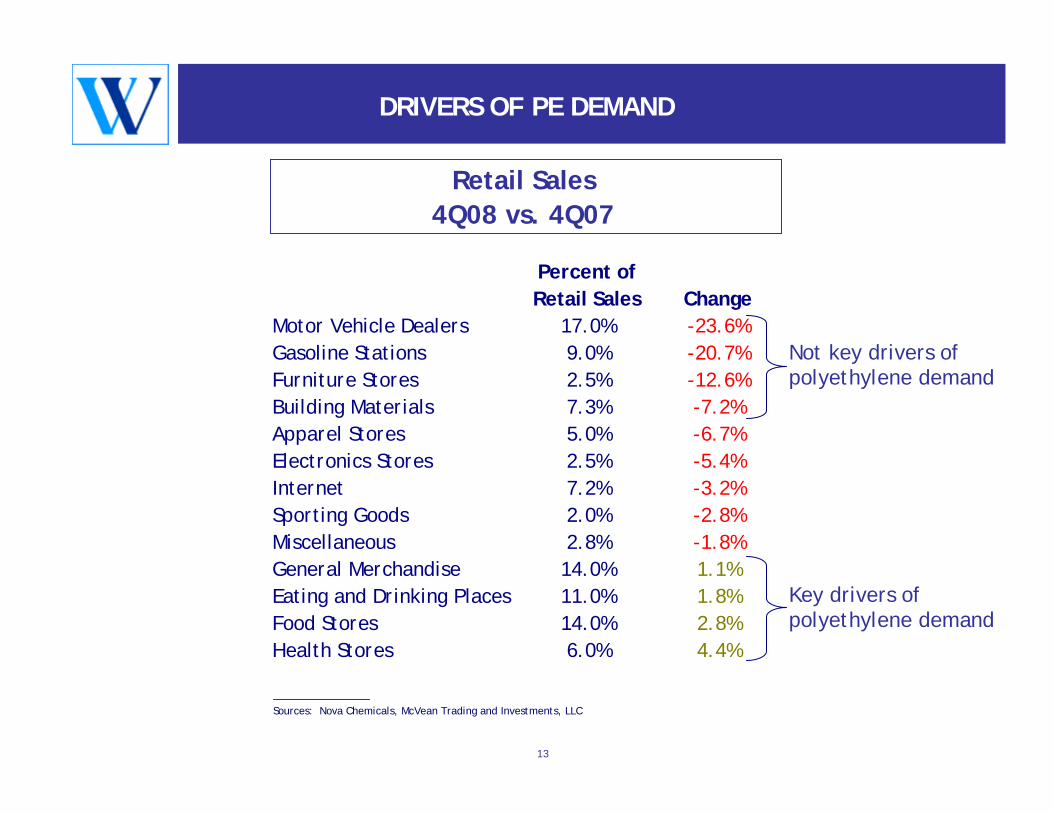

DRIVERS OF PE DEMAND

Retail Sales 4Q08 vs. 4Q07

Percent of Retail Sales Change

Motor Vehicle Dealers 17.0% -23.6%Gasoline Stations 9.0% -20.7%Furniture Stores 2.5% -12.6%Building Materials 7.3% -7.2%Apparel Stores 5.0% -6.7%Electronics Stores 2.5% -5.4%Internet 7.2% -3.2%Sporting Goods 2.0% -2.8%Miscellaneous 2.8% -1.8%General Merchandise 14.0% 1.1%Eating and Drinking Places 11.0% 1.8%Food Stores 14.0% 2.8%Health Stores 6.0% 4.4%

Not key drivers of polyethylene demand

Key drivers of polyethylene demand

Sources: Nova Chemicals, McVean Trading and Investments, LLC

14

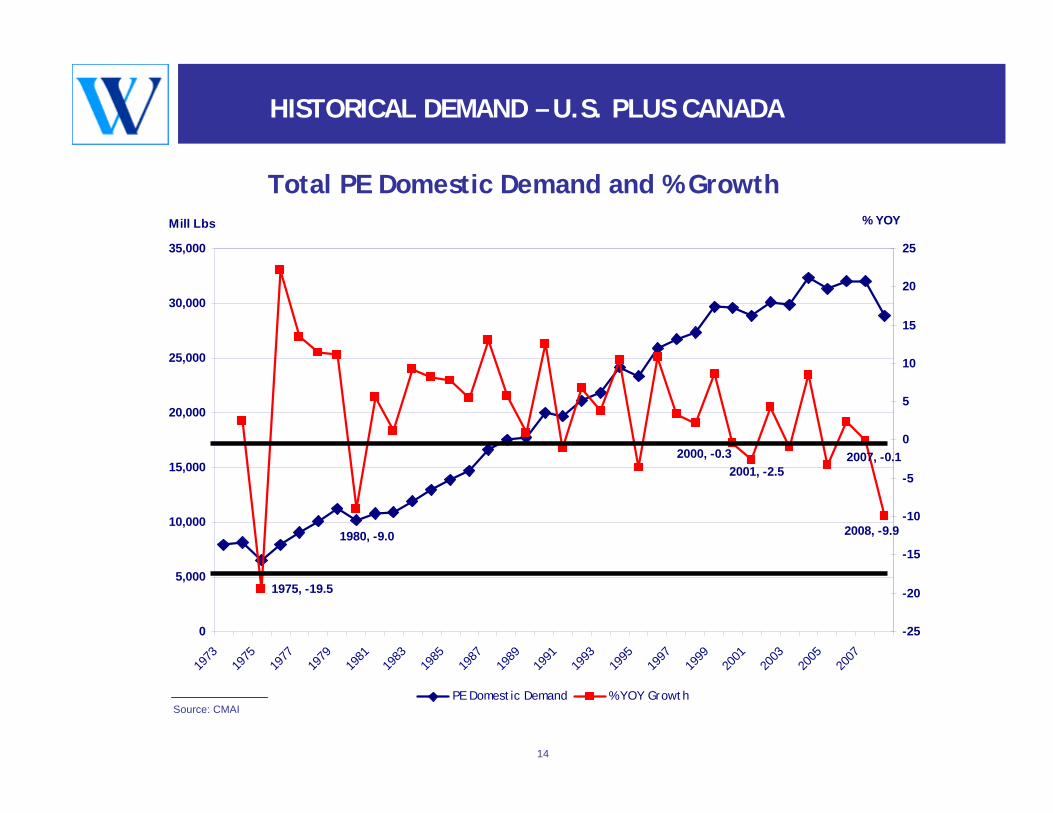

HISTORICAL DEMAND – U.S. PLUS CANADA

2007, -0.1

2008, -9.91980, -9.0

2000, -0.32001, -2.5

1975, -19.5

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

Mill Lbs

-25

-20

-15

-10

-5

0

5

10

15

20

25

% YOY

PE Domestic Demand % YOY GrowthSource: CMAI

Total PE Domestic Demand and % Growth

15

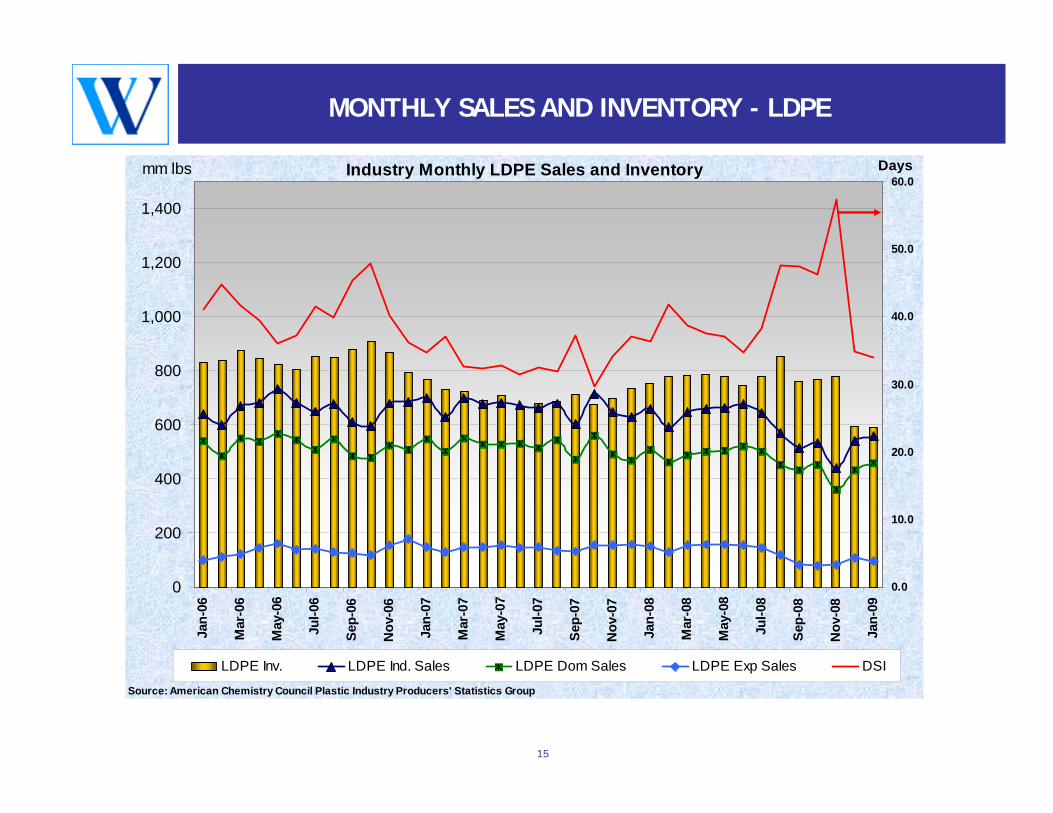

MONTHLY SALES AND INVENTORY - LDPE

Industry Monthly LDPE Sales and Inventory

0

200

400

600

800

1,000

1,200

1,400Ja

n-06

Mar

-06

May

-06

Jul-0

6

Sep-

06

Nov

-06

Jan-

07

Mar

-07

May

-07

Jul-0

7

Sep-

07

Nov

-07

Jan-

08

Mar

-08

May

-08

Jul-0

8

Sep-

08

Nov

-08

Jan-

09

mm lbs

0.0

10.0

20.0

30.0

40.0

50.0

60.0

LDPE Inv. LDPE Ind. Sales LDPE Dom Sales LDPE Exp Sales DSI

Source: American Chemistry Council Plastic Industry Producers' Statistics Group

Days

16

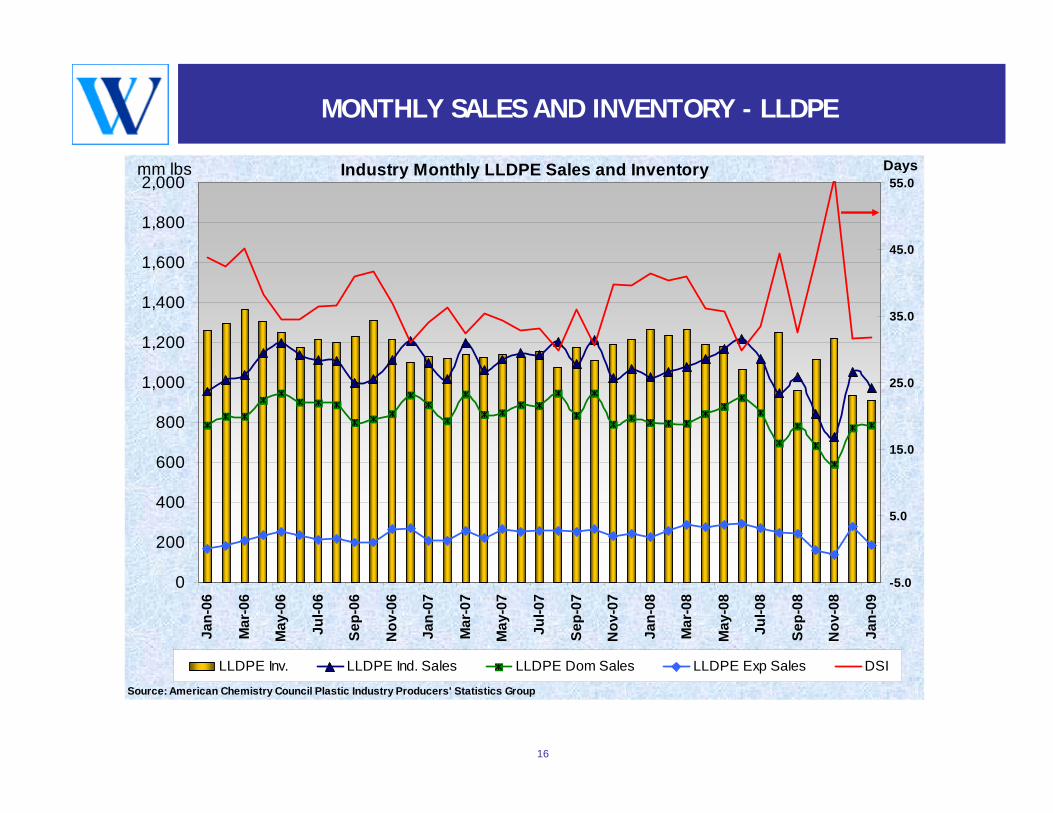

MONTHLY SALES AND INVENTORY - LLDPE

Industry Monthly LLDPE Sales and Inventory

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000Ja

n-06

Mar

-06

May

-06

Jul-0

6

Sep-

06

Nov

-06

Jan-

07

Mar

-07

May

-07

Jul-0

7

Sep-

07

Nov

-07

Jan-

08

Mar

-08

May

-08

Jul-0

8

Sep-

08

Nov

-08

Jan-

09

mm lbs

-5.0

5.0

15.0

25.0

35.0

45.0

55.0

LLDPE Inv. LLDPE Ind. Sales LLDPE Dom Sales LLDPE Exp Sales DSI

Source: American Chemistry Council Plastic Industry Producers' Statistics Group

Days

17

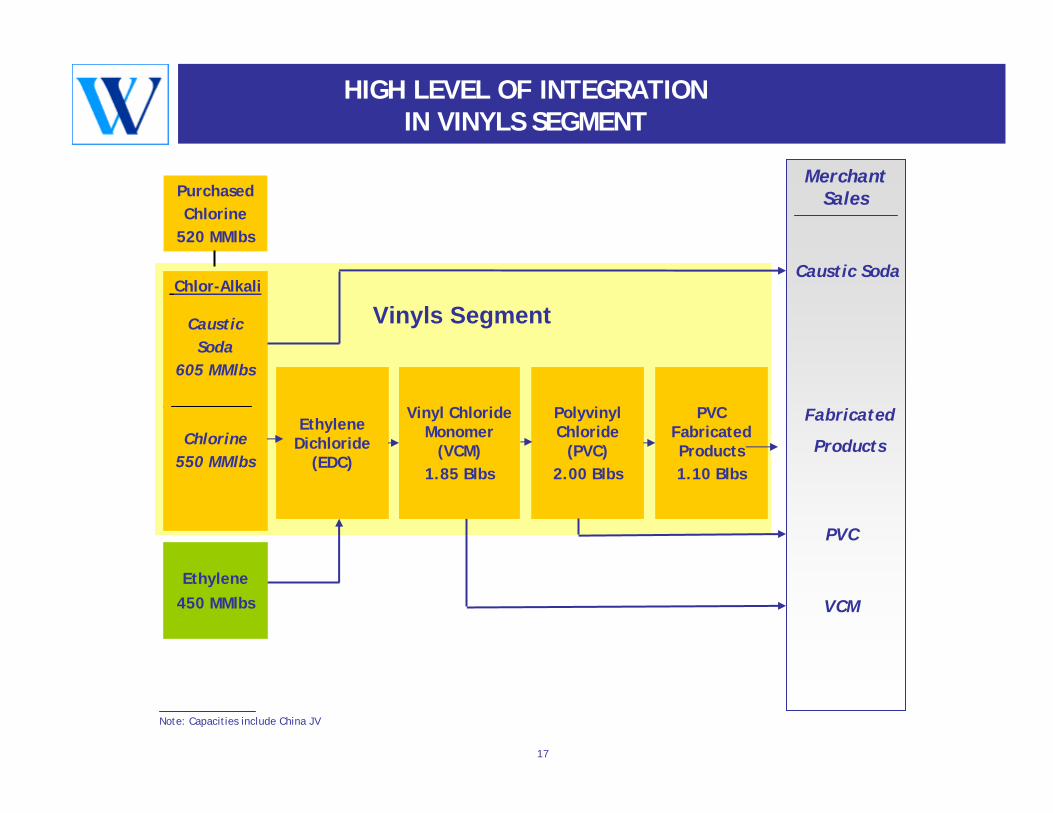

HIGH LEVEL OF INTEGRATION IN VINYLS SEGMENT

Polyvinyl Chloride

(PVC)2.00 Blbs

Caustic Soda

Fabricated

Products

PVC

VCM

PVC Fabricated Products1.10 Blbs

Vinyl Chloride Monomer

(VCM)1.85 Blbs

Ethylene Dichloride

(EDC)

CausticSoda

605 MMlbs

Chlorine550 MMlbs

Ethylene450 MMlbs

Vinyls Segment

PurchasedChlorine

520 MMlbs

Merchant Sales

Chlor-Alkali

Note: Capacities include China JV

18

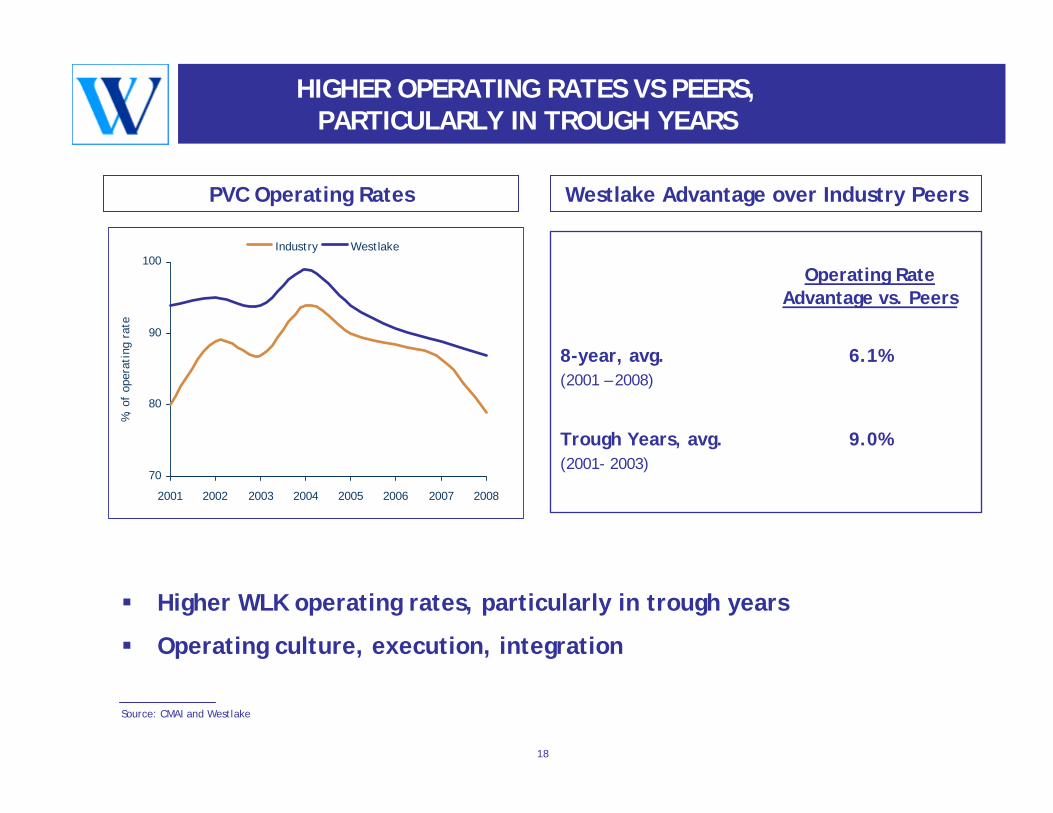

HIGHER OPERATING RATES VS PEERS, PARTICULARLY IN TROUGH YEARS

70

80

90

100

2001 2002 2003 2004 2005 2006 2007 2008

%,

of o

pera

ting

rat

e

Industry Westlake

Higher WLK operating rates, particularly in trough years

Operating culture, execution, integration

Westlake Advantage over Industry Peers

9.0%Trough Years, avg.(2001- 2003)

6.1%8-year, avg.(2001 – 2008)

Operating RateAdvantage vs. Peers

PVC Operating Rates

Source: CMAI and Westlake

19

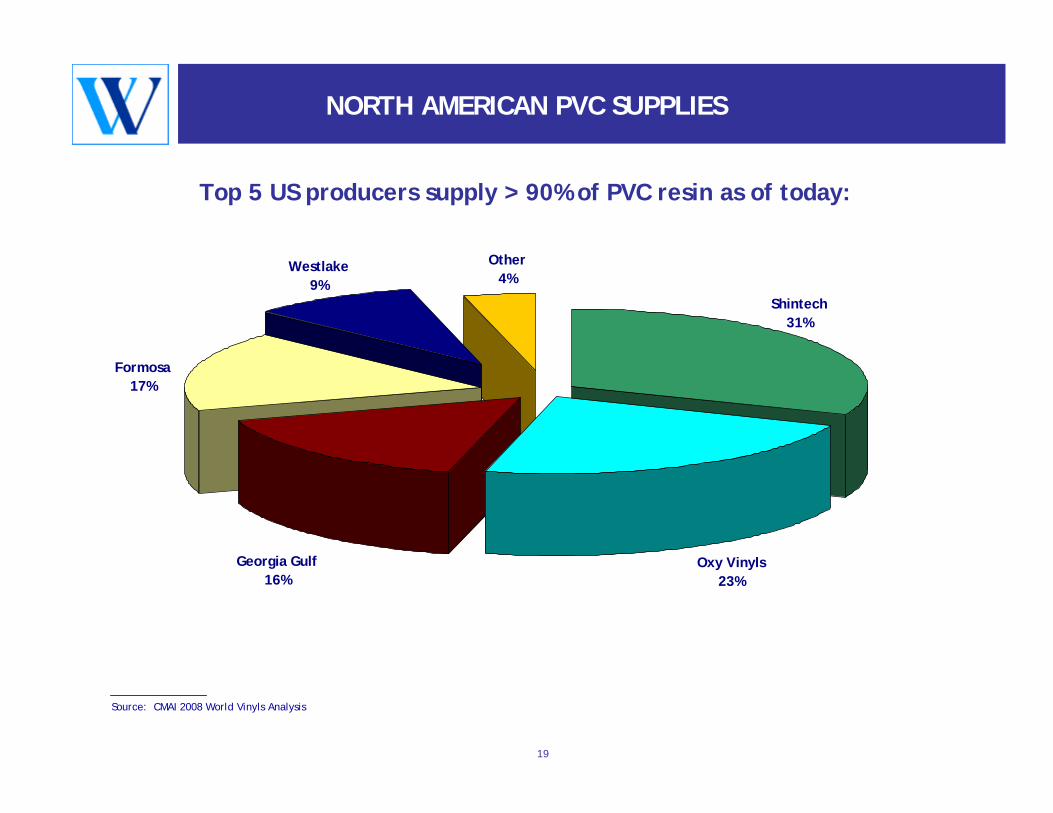

NORTH AMERICAN PVC SUPPLIES

Top 5 US producers supply > 90% of PVC resin as of today:

Source: CMAI 2008 World Vinyls Analysis

Oxy Vinyls23%

Other4%

Georgia Gulf16%

Formosa17%

Westlake9%

Shintech31%

20

THOUGHTS ON PVC

Many expect late 2008 demand levels to continue

Expect a few bright spotsRising global demand for clean water Infrastructure projects play to Westlake’s strategy of large diameter PVC pipe

PVC demand levels continue to support caustic pricing

Both producers and converters continue to manage inventories due to risks in pricing swings

21

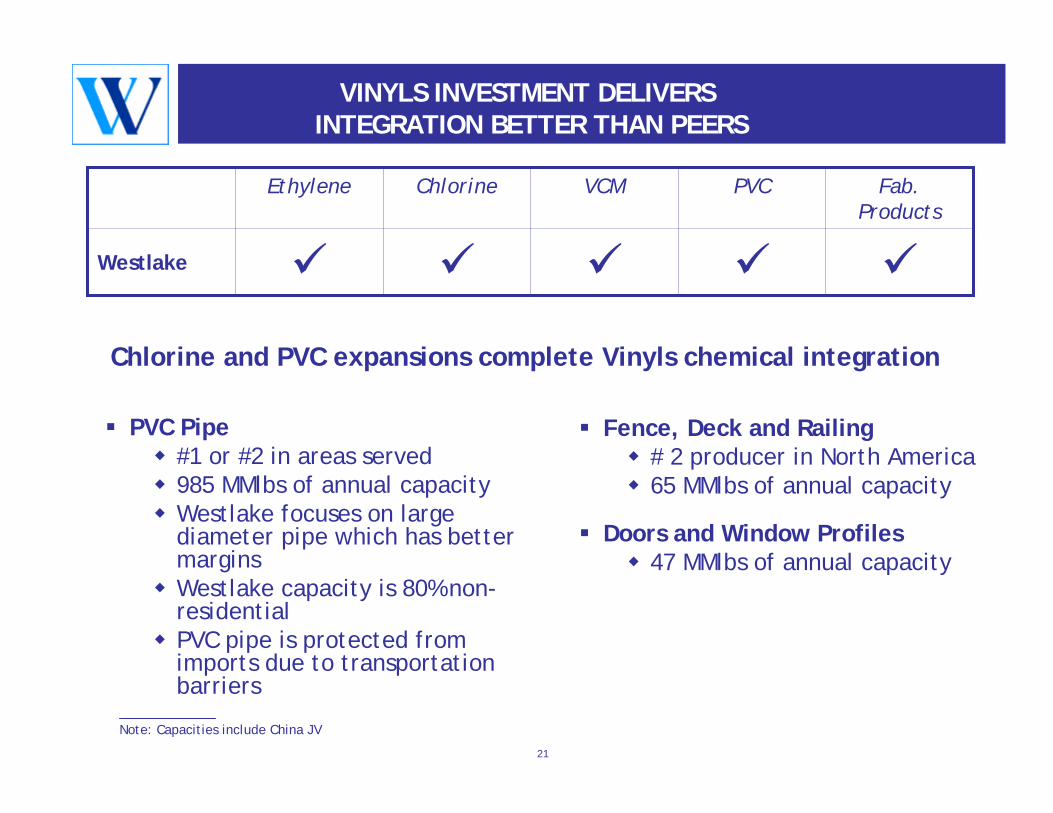

VINYLS INVESTMENT DELIVERSINTEGRATION BETTER THAN PEERS

Westlake

Fab. Products

PVCVCMChlorineEthylene

PVC Pipe#1 or #2 in areas served 985 MMlbs of annual capacityWestlake focuses on large diameter pipe which has better marginsWestlake capacity is 80% non-residentialPVC pipe is protected from imports due to transportation barriers

Fence, Deck and Railing # 2 producer in North America65 MMlbs of annual capacity

Doors and Window Profiles47 MMlbs of annual capacity

Chlorine and PVC expansions complete Vinyls chemical integration

Note: Capacities include China JV

22

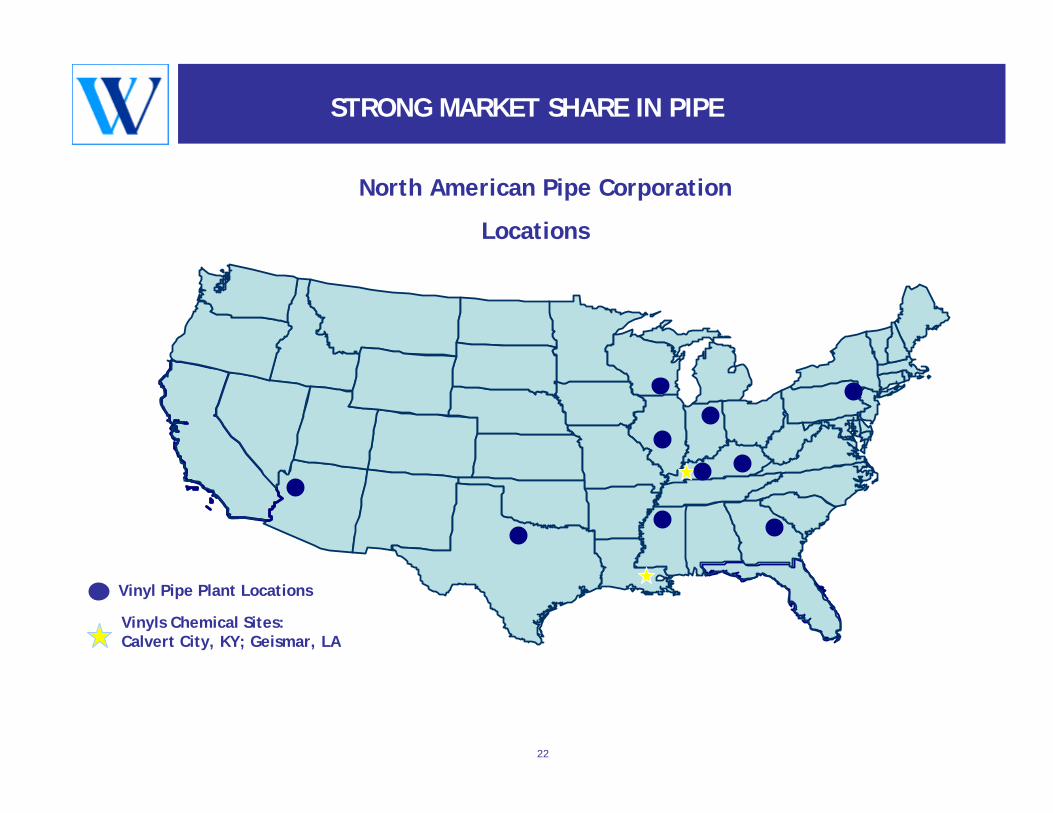

STRONG MARKET SHARE IN PIPE

North American Pipe Corporation

Locations

Vinyl Pipe Plant Locations

Vinyls Chemical Sites: Calvert City, KY; Geismar, LA

23

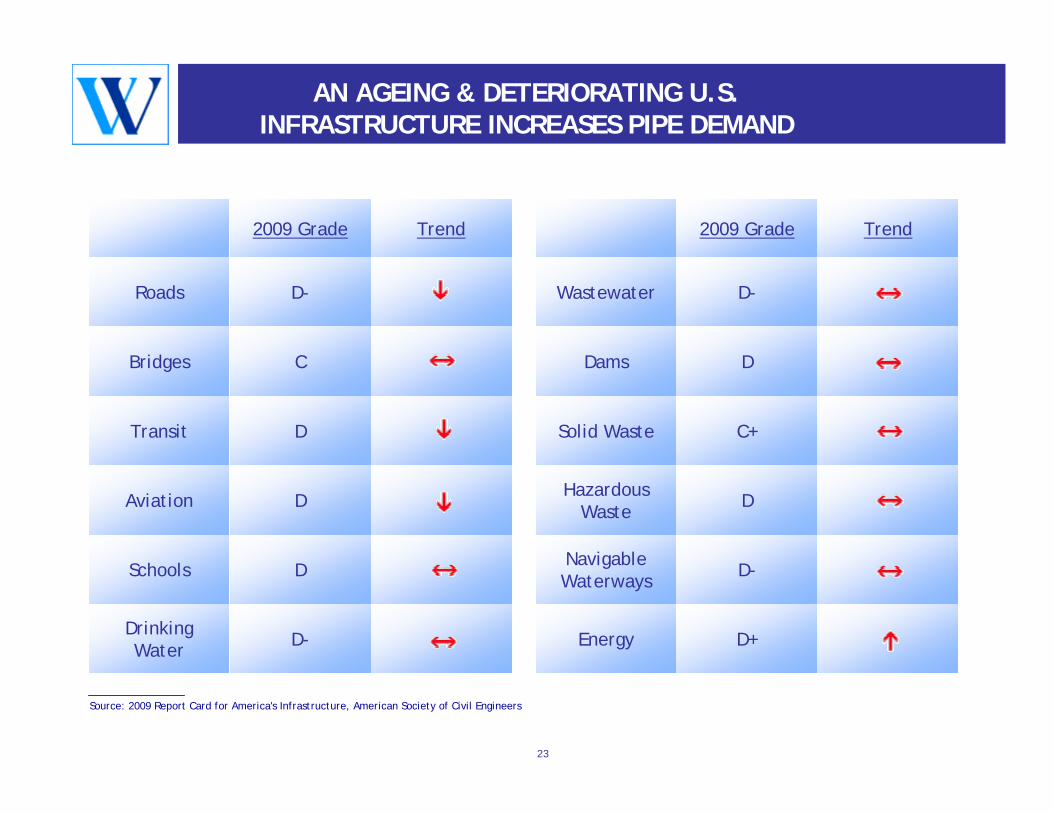

AN AGEING & DETERIORATING U.S. INFRASTRUCTURE INCREASES PIPE DEMAND

D-Drinking Water

DSchools

DAviation

DTransit

CBridges

D-Roads

Trend2009 Grade

D+Energy

D-Navigable Waterways

DHazardous Waste

C+Solid Waste

DDams

D-Wastewater

Trend2009 Grade

Source: 2009 Report Card for America's Infrastructure, American Society of Civil Engineers

24

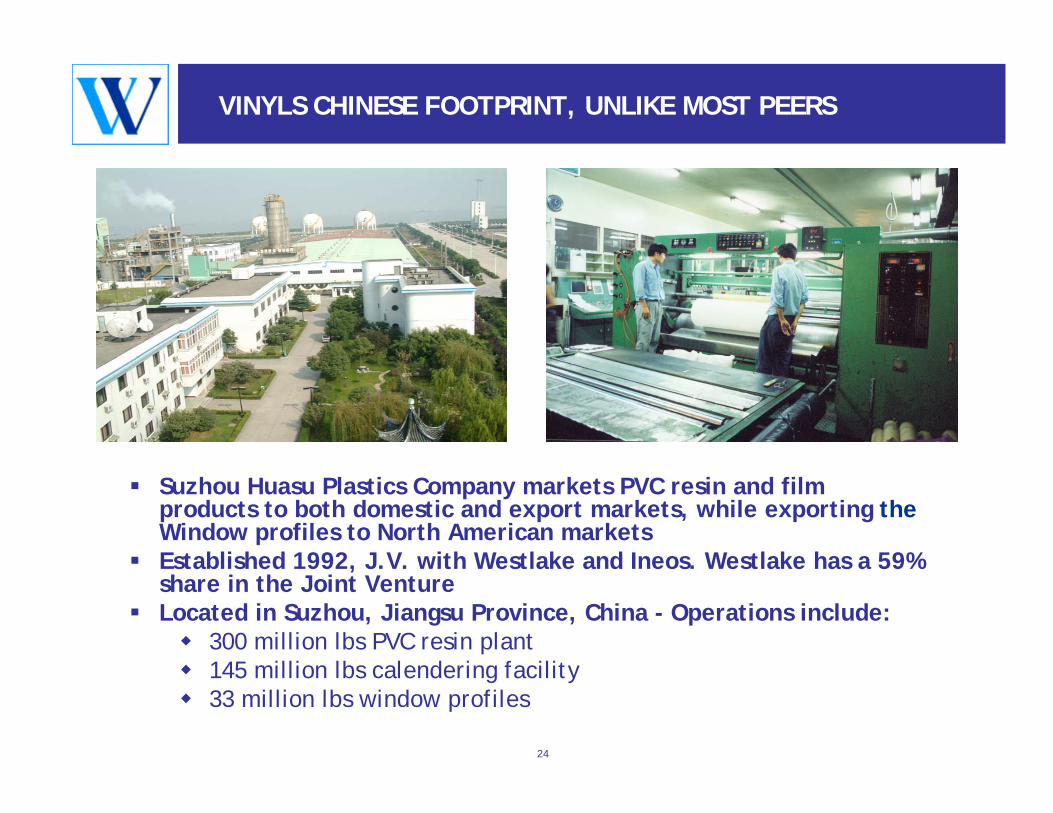

VINYLS CHINESE FOOTPRINT, UNLIKE MOST PEERS

Suzhou Huasu Plastics Company markets PVC resin and film products to both domestic and export markets, while exporting theWindow profiles to North American marketsEstablished 1992, J.V. with Westlake and Ineos. Westlake has a 59% share in the Joint Venture Located in Suzhou, Jiangsu Province, China - Operations include:

300 million lbs PVC resin plant145 million lbs calendering facility33 million lbs window profiles

25

THOUGHTS ON FABRICATED PRODUCTS

PVC window producers will undergo consolidationPVC window consolidation positions our China JV to be able to capture a growing share of the market as it consolidates

Small diameter PVC pipe producers will continue to rationalize production to meet demand

Larger diameter PVC pipe producers, while challenged, will see the bulk of any up-tick in demand and will disproportionally benefit from new infrastructure projects

26

WESTLAKE STRENGTHS

Consistently Demonstrated Profitable Growth

Strategically located asset base

Vertical integration with high operating rate

Feedstock Flexibility

LDPE driven product mix in Olefins

Earnings leverage based on product diversification

Financial flexibility

28

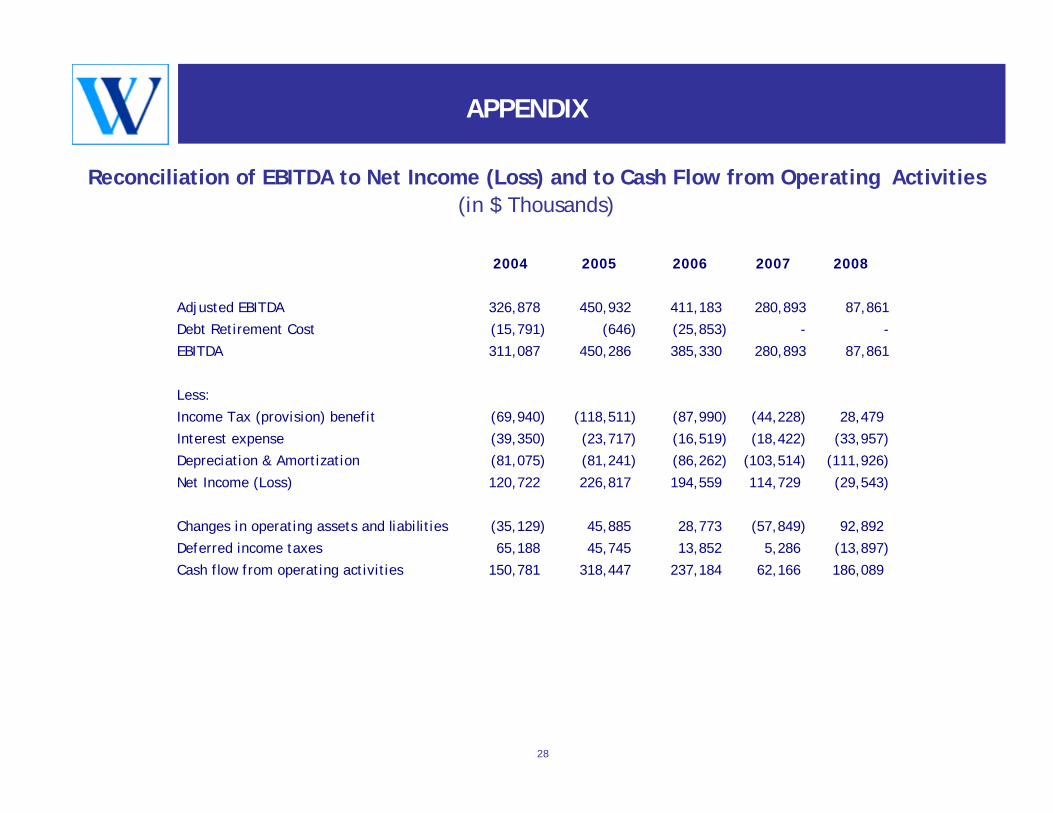

APPENDIX

2004 2005 2006 2007 2008

Adjusted EBITDA 326,878 450,932 411,183 280,893 87,861

Debt Retirement Cost (15,791) (646) (25,853) - -

EBITDA 311,087 450,286 385,330 280,893 87,861

Less:

Income Tax (provision) benefit (69,940) (118,511) (87,990) (44,228) 28,479

Interest expense (39,350) (23,717) (16,519) (18,422) (33,957)

Depreciation & Amortization (81,075) (81,241) (86,262) (103,514) (111,926)

Net Income (Loss) 120,722 226,817 194,559 114,729 (29,543)

Changes in operating assets and liabilities (35,129) 45,885 28,773 (57,849) 92,892

Deferred income taxes 65,188 45,745 13,852 5,286 (13,897)

Cash flow from operating activities 150,781 318,447 237,184 62,166 186,089

Reconciliation of EBITDA to Net Income (Loss) and to Cash Flow from Operating Activities (in $ Thousands)