Why does the Reaction to News Announcements Vary across Countries? + John M. Griffin a , + Nicholas H. Hirschey a , and Patrick J. Kelly b a University of Texas at Austin, McCombs School of Business, Austin, TX 78712, USA b University of South Florida, Tampa, FL 33620, USA October 10, 2008 + The first two authors are from the McCombs School of Business at the University of Texas at Austin. Griffin is currently visiting HKUST in Hong Kong and Kelly is at the University of South Florida. We thank Utpal Bhattacharya, Bernie Black, Miguel Ferreira, Jay Hartzell, Alok Kumar, Federico Nardari, Clemens Sialm, Sheridan Titman and seminar participants at the International Finance Conference at McGill University and the University of Texas at Austin for helpful comments and discussion. Email addresses: [email protected], [email protected], and [email protected].

Transcript

Why does the Reaction to News Announcements Vary across Countries?+

John M. Griffina,+ Nicholas H. Hirschey a, and Patrick J. Kellyb

a University of Texas at Austin, McCombs School of Business, Austin, TX 78712, USA b University of South Florida, Tampa, FL 33620, USA

October 10, 2008

+ The first two authors are from the McCombs School of Business at the University of Texas at Austin. Griffin is currently visiting HKUST in Hong Kong and Kelly is at the University of South Florida. We thank Utpal Bhattacharya, Bernie Black, Miguel Ferreira, Jay Hartzell, Alok Kumar, Federico Nardari, Clemens Sialm, Sheridan Titman and seminar participants at the International Finance Conference at McGill University and the University of Texas at Austin for helpful comments and discussion. Email addresses: [email protected], [email protected], and [email protected].

Abstract

We examine stock price reactions to large news events (earnings and takeover announcements) around the world. We find that the reactions to major events vary widely around the world—with some markets exhibiting large reactions and other markets with little or no reaction. We investigate possible explanations including: erroneous announcement dates, the lack of meaningful accounting numbers, delayed reaction to news, poor news quality, and insider trading. Overall, we find substantial support for the cross-country differences in reactions being driven by insider trading and press freedom as a proxy for news dissemination.

News announcements, such as annual earnings reports, are made for most traded firms in both

developed and emerging markets. Yet relatively little is known about how market participants

respond to this news. Does the strength of stock price reactions to news vary widely across

countries? If so, why do these reactions vary? Are they primarily driven by differences in the quality

of the information released or by the timing of when the news is traded on?

This paper examines the market reaction to common events around the world. We believe

such a study is useful for deepening our understanding of the information environment around the

world using an approach that is extremely systematic across countries. Our study reveals that stock

market reactions to news do vary widely around the world and they seem to vary mainly due to the

timing of when news is incorporated into prices.

In an innovative paper, Bhattacharya, et al (2000) track down news announcement dates in

Mexico from in a window from 1994 to 1997. Interestingly, they find that in Mexico there is no

stock price reaction on the announcement day. After examining possible explanations, they conclude

that this is due to rampant insider trading. In their abstract they state that their paper “points toward

a methodology for ranking emerging markets according to their market integrity.” The biggest

barrier that has stood in the way of such a systematic study is the difficulty in obtaining accurate

news event dates. For example, Bhattacharya et al. (2000), use 75 events that are hand collected from

Bloomberg. We also obtain event dates from Bloomberg, and we verify through hand checks of

alternate news services that Bloomberg announcement dates are indeed typically accurate (roughly

75 percent of the time). We use additional procedures to increase our event date accuracy up to an

estimated 90 percent accuracy. For earnings news we create two samples, one where Bloomberg

events are overlapping with IBES event dates and another where they are verified by Factiva news

articles. Our combined sample of earnings news event dates from January 2, 2001 to October 12,

2007 consists of 54,336 earnings announcements in developed markets (excluding the U.S.) and

13,884 emerging markets. Additionally, we obtain merger dates for target firms from three sources

and use only the earliest date for each event from among those sources.

Several papers have examined stock market reactions to earnings or news internationally.

The closest paper to ours is by DeFond, Hung, and Trezevant (2007), who examine the role that

investor protection, accounting standards, and insider trading laws play in explaining cross-country

differences in event reactions. The first major difference between their study and ours is that they

use IBES event reactions that we show (and they also acknowledge) often exhibit problems with

accuracy internationally. Second, they examine only 26 primarily developed markets, whereas we are

able to obtain events from many smaller markets. Third, their focus and conclusions are vastly

different from ours. Bailey, Karolyi, and Salva (2006) use earnings event reactions before and after a

U.S. cross-listing and find that U.S. accounting requirements lead to increases in earnings

announcement reactions. In an interesting study on takeovers Bris (2005) examines general patterns

of stock price run-ups prior to takeovers before and after the implementation of insider trading

laws.1

We first examine if news announcements vary across countries. We measure the average

absolute return over a three-day announcement window scaled by the average non-event day

volatility as our measure of normalized event volatility. We find that event dates reactions do vary

substantially across countries ranging from a value of two times normal event volatility to a value of

1.03 in Mexico, which indicates that an earnings event day in Mexico is essentially the same as any

other day. Nine emerging and three developed markets (Austria, Greece, and South Korea) have

event day reactions below 1.2 whereas nine developed markets exhibit reactions above 1.5.

1 Perhaps due to the scarcity of takeover events, in certain countries, his paper does not contain country-by-country analysis. Ackerman, Halteren, and Maug (2008) find that insider trading laws and not actual enforcement of the laws is more important for explaining pre-announcement price run-ups for takeovers.

We next turn to understanding the causes of the cross-country event reactions. There are

five main factors that may affect the reaction to a news event. First, if due to poor accounting quality

the earnings news is of low or no value, then there is little reason for stock prices to react. Second,

investors may not actively research stocks because the costs to collecting information are high,

which is typically referred to as investor inattention. Third, due to poor information dissemination

mechanisms, investors may be slow to receive the news. Fourth, investors may be able to anticipate

the news prior to the event through other public, non-announcement-related sources. Fifth, the

news may be largely impounded into prices through privately informed trade. We find support for

the third and fifth hypothesis.

We examine these hypotheses by studying differences in volatility and returns during

announcement, pre-announcement, and post announcement windows. This is followed by a joint

examination of these hypotheses in a cross-sectional, cross-country regression framework. To

examine the first hypothesis that poor earnings quality leads to smaller announcement period returns,

we examine the difference in abnormal stock returns between stocks with high and low changes in

earnings over the entire fiscal year. If low event reactions are driven by poor earnings quality, then

we expect a weak relation between stock prices and earnings in countries where there is little

reaction to earnings announcements. In contrast, we find that the difference between the returns of

firms with positive and negative changes in earnings is 21 percent per year in the quartile of

countries with the lowest reactions to earnings news. This is similar to the 26 percent per year

difference in the top quartile of countries with high event reactions. Next, since the strength of

takeover announcements does not depend on the quality of accounting data (like earnings), we

examine the relation between earnings event reactions. The cross-country correlation between

earnings and takeover event reactions is a highly significant 0.57.

To examine the second and third hypothesis we look for evidence of drift prior to earnings

announcements. In contrast to the predictions of these two hypotheses, we find substantial drift

prior to earnings announcements in both high and low earnings announcement countries, though

positive drift is somewhat higher in low reaction countries.

To examine the fourth and fifth hypotheses dealing with news being anticipated (either

through public or private channels), we examine if returns are moving in the same direction as

positive and negative earnings surprises (measured relative to IBES analyst forecasts). In low

reaction countries the relation between earnings surprises and prior period returns is similar to that

in high reaction countries even though the stock price movement on the announcement day is small

in the low reaction group. Additionally, merger announcements help us distinguish between the

public and private channels, since merger announcements are unscheduled events and in most cases

difficult to predict. In low reaction countries we find that 62.4 percent of the total price run-up is

reflected in the pre-announcement period, whereas in high event reaction markets, only 30.9 percent

of the run-up is in the pre-announcement period. Since we take the first takeover announcement

date, these findings seem to support the insider trading hypothesis over public information leakage.

To examine all our five main hypotheses jointly in a cross-country framework, we regress

our average normalized event volatility ratio on variables reflecting aspects of accounting quality, the

information environment, trading activity, insider trading law and practice, laws regarding investor

protection and trade, the level of economic and market development, and trading costs. Of the

thirty three variables related to these hypotheses that we examine in univariate regressions, we then

examine 153 regressions of unique combinations of the 18 significant variables in bivariate

regressions. From these regressions we examine the top seven in multivariate specifications (Panel C

in Table V). Of these variables, two survey response measures from the World Economic Forum’s

Global Competitiveness Report (GCR) Executive Opinion Survey emerge as significant in nearly

every specification: freedom of the press (a proxy for the quality of the information environment)

and prevalence of insider trading. We also estimate Panel regressions with firm-level controls and

find that these two variables are highly significant, along with a GCR survey variable on the

prevalence of ethical firms. Countries with a more ethical business environment, where there is less

of a perception of insider trading, and with greater press freedom exhibit stronger event reactions.

In sum, both our sorting results as well as cross-sectional regressions suggest that cross-country

differences in the way that firms respond to news are driven by the prevalence of insider trading and

strength of the financial press.

Our paper relates to a large international literature that examines the effect of insider trading

laws or the enforcement of these laws on issues such as the cost of capital [Bhattacharya and Daouk

(2002) and Beny (2007)], volatility [Du and Wei (2004)], idiosyncratic volatility [Fernandes and

Ferreira (2007)], and stock return autocorrelations patterns [Durnev and Nain (2007)]. The existence

of a law or its enforcement is only a proxy for the prevalence of insider trading. Bhattacharya (2006)

argues that even in a developed market such as Canada with prior enforcements that insider trading

may be widespread and that larger penalties and more enforcements can improve market conditions.

We add to this literature by providing a proxy to partially measure the extent to which insider trading

may occur across markets.

Section I describes and outlines our five main hypotheses. Section II describes our data

sources and process of gathering announcements and in insuring accuracy. Section III displays our

event reactions and Section IV shows various sorting tests to shed light on our hypotheses and

Section V further tests them through cross-country regressions. Section VI concludes.

I. News Channels

This section outlines potential causes for between-country differences in the reaction to the

public release of firm-specific information. Before discussing hypotheses, a basic point is important

to emphasize: Without accurate event dates, any analysis of news events is fundamentally flawed.

For this reason, we use announcements that have been verified from two different databases. In

addition, we confirm news announcements with independent news sources as we describe in much

more detail in our data section.

At its most basic level, the price reaction to a given news event is a function of the

magnitude of the valuation change signaled by the news. The price reaction is further affected by 1)

the quality and precision of that signal and 2) whether there is information leakage prior to the news

announcement. Our five hypotheses derive from these two basic principles.

A. Accounting Quality

First, the strength of the earnings news reactions may vary across countries due to the

importance or accuracy of financial accounting across countries, i.e. the quality and precision of the

valuation signal. In the extreme, a country with meaningless accounting standards would have no

reaction to earnings related news because investors assign no meaning or value to the accounting

information content of the news. Ball, Kothari, and Robin (2000) find evidence that the variation in

international accounting standards is sufficient to produce economically significant differences in

financial statements. If firms rely more on the financial markets for funding, they may be more

inclined to provide accurate and timely financial statements (see Ball, Kothari, and Robin (2000)).

Similarly, Ali and Hwang (2000) show that the value of accounting information is decreasing in a

country’s dependence on bank finance. This paper uses measures of earnings management, the level

of financial disclosure within a country, and a country’s reliance on the stock market or banks for

announcement reactions. Also, we examine news announcements from takeovers as an alternative

form of news that is not typically subject to the quality of accounting information.

B. Inattentive Investors and Poor Information Environment

Second, reactions may be delayed due to inattentive investors. In the extreme, even in the

face of significant news, stock prices might not move simply because investors are not reacting to

news [Huberman and Regev (2001), Peng and Xiong (2006)]. In the U.S., inattention has been

shown to lead to less reaction and more post-earnings drift on days with multiple earnings

announcements [Hirshleifer, Lim, and Teoh (2007)] and on Fridays [DellaVigna and Pollet (2008)].

We examine the magnitude of inattention by looking at the strength of post-earnings announcement

drift across markets and whether the magnitude of event day reactions is associated with the amount

of active trading in the market.

Third, a closely related hypothesis is that investors are slow to react not because they are

inattentive but because information is slow to reach the investor. If investors are not aware of an

event, then they cannot react to it. Consequently, one would expect stronger market reactions in

countries where information is transmitted relatively quickly and effectively. There may also be a

secondary effect; Grossman and Stiglitz (1980) note that when information acquisition costs are high

less information will be gathered. If poor communications infrastructure represents a component of

information acquisition costs, then in countries with poor communications infrastructure, not only is

it harder for investors to acquire firm-specific information, but they may also be inclined to collect

less of it. To analyze such effects we use controls for the quality of information dissemination within

a country.

A final related variant of both of these hypotheses is that investors simply do not respond at

all to news because the market is informationally inefficient. This could either occur due to fully

inattentive investors or because news is so poorly disseminated that the marginal investor does not

receive it. With the inattentive investor hypothesis or slow news dissemination, we expect to have

little event reaction but substantial post-announcement drift but with a completely inefficient market

there should be no movements in the direction of price announcements in either the pre-, post-, or

event period. As such, a completely informationally inefficient market is similar to a market where

the accounting information is invalid. In this case, the market would have neither drift in the

direction of the earnings surprise nor any pre-announcement price movement in the direction of the

news.

C. Pre-Announcement Trading through Public or Private Information

Our fourth and fifth hypotheses posit that the magnitude of news announcement reactions

is reduced by information leakage prior to the event day. This could occur due to news being

released through public channels outside of the official earnings announcement such as through

public conference calls with analysts, our fourth hypothesis, or it could be do to investors with

privileged knowledge trading on information before it is released to the public, our fifth hypothesis.

Such trading will dampen market reactions to information releases, since market participant reveal

information when they trade [Grossman (1981)]. It is important to note that we use the term

“insiders” to denote trading on to information not released through public channels. It is difficult to

pin down whether this trading is due to trading that is explicitly illegal in nature, though in cross-

country analysis we will investigate linkages to perception of insider trading and its relation to insider

trading laws.

We examine preannouncement run-up to explore the possibility that information gets to the

market prior to earnings events. If information is dispersed into prices through insider trading or

other public or private information based trade then we should see prices moving in the direction of

the earnings surprise before the reaction in countries with little event reaction. To separate the

public and private channel of early information release (our fourth and fifth hypotheses), we use the

prevalence of insider trading (a country level variable) to examine whether average country level

reactions are lower in countries with more insider trading.

Most of the evidence that we use to investigate each of these five hypotheses also has

implications for the other hypotheses, which we discuss in greater detail when describing our

findings. In addition, we use cross-sectional regressions and country-level variables to investigate

additional aspects of what features are related to event reactions across countries.

II. Data

The main data in this paper consist of firm stock returns and accounting variables, country-

level descriptive variables, and most importantly earnings and takeover announcements.

A. Preliminaries: Return, Accounting, and IBES data

Daily returns accounting for dividends and capital structure changes, and market

capitalization series are from CRSP for the United States and from Thomson Financial’s Datastream

for the rest of the world. Since we wish to restrict our sample to common equity, we use stocks with

CRSP share code of 10 or 11 in the U.S. For non-U.S. securities we follow the substantial screens of

Griffin, Kelly, and Nardari (2008) which eliminate preferred stock, warrants, unit or investment

trusts, duplicates, GDRs or cross-listings, and other non-common equity. We also use their return

filters to smooth potential data errors. We use Datastream’s value-weighted total market index

returns. Because our reactions are relative to local indices, we leave returns in local currency. For

annual earnings we use Worldscope annual earnings. Analyst forecast information internationally is

obtained from IBES. Annually rebalanced size portfolios are created using U.S. market capitalization

breakpoints by sorting all stocks listed on NYSE, AMEX, and NASDAQ into three market

capitalization portfolios. Each non-U.S. firm’s market capitalization is converted into U.S. dollars

using spot exchange rates from Datastream and is sorted into one of the US-size portfolios based on

its December-end market cap.

B. Country-level Variables

Developed or emerging classifications are based on World Bank income classifications in

November 2005. Country-level variables are primarily taken from the World Bank Development

Database or the World Economic Forum’s 1999 Global Competitiveness Report (GCR). This

source aggregates hard data and also reports the results of a survey of over 4,000 executives in 59

countries. The book reports an average response for each country and question asked. A key GCR

variable of interest is a survey question that asks executives if “insider trading in your country’s stock

markets is (1=pervasive, 7=extremely rare).” We aggregate the responses in the editions from 1999,

2000, and 2002-2003, but the World Economic Forum seemed to have stopped asking the question

in more recent surveys. We also use and extend the Bhattacharya and Daouk (2002) survey for

those countries in our sample that had not yet prosecuted a case of insider trading as of their sample

in December 1998. We contacted the 46 exchanges and regulators for markets covered by either

Datastream or FactSet and we received definitive answers about the first enforcement of insider

trading laws from 24. We received no conclusive responses from the remaining 22 countries, so in

these cases we use the anti-insider trading enforcement dates found by Bhattacharya and Daouk

(2002).

C. Earnings Announcement Dates

We choose earnings announcements as our main news event because we seek to investigate

a common event across countries, as well as an event with a standardized data source. Because firms

in many countries only announce earnings annually, for consistency we only examine reactions to

annual earnings announcement dates in all countries.

C.1. Data Collection procedure

For our international earnings announcement dates, we start with announcement dates from

Bloomberg. We also collect earnings announcements dates from IBES. We first examine the

accuracy by managing research assistants to check a sample of all events for five firms in each

country in our sample. In order to examine the accuracy of these databases, we begin in Appendix

Table A1, by matching and comparing all annual earnings announcement dates from IBES and

Bloomberg from 1994 through 2005 where both IBES and Bloomberg have announcement dates

for the same fiscal year. The count column shows the number of matched events. The next shows

the number of times the event dates were identical in both datasets. IBES Earlier is the count of the

number of times the IBES announcement is earlier than the Bloomberg date. More Bloomberg

dates are earlier (BB Earlier) in all countries except Colombia. If dates are not falsely reported early,

then Bloomberg dates appear to be much more accurate than the dates provided by IBES. In

fairness to IBES, they do not claim to provide announcement dates. They instead provide the date

the data were entered into their databases. In the U.S. the entry dates are the announcement dates,

but this does not appear to be true around the world.

To further investigate the database accuracy we sample five firms per country and examine

the accuracy of each and every event announcement for each of the five companies per country by

comparing these announcement dates to what we find when we search Factiva “by hand.” Table AII

reports that of the 1346 events checked and find that Bloomberg are accurate 75 percent of the time

in developed markets and 3 percent of the time in emerging markets. By contrast IBES dates are

accurate only 8 percent of the time in emerging markets and 23 percent of the time in developed. In

unreported results we restrict the sample to only the dates where IBES and Bloomberg match within

3 days of each other. This reduces the sample to only 201 dates over all, but the accuracy jumps to

91%.2

For this reason, we start with Bloomberg as our primary source even though we use IBES

dates for cross-checking. Even though we are able to collect Bloomberg announcement dates back

to 1994, we begin our sample in January 2001 since there have been significant changes over the last

ten years over which the speed and manner in which information is released and reported. Our last

earnings announcement date is on October 12, 2007. For U.S. firms, this sample consists of IBES

dates confirmed by Compustat.

To further check our international sample, we collect dates through Factiva as well. We took

a sample of fifty firms in each of the developed markets and half of all emerging market firms (at

least 100 per market where available) and downloaded all Factiva earnings news articles for these

firms. Because of the large volume of articles we automated the date confirmation process for this

sample. To begin we required articles be tagged as earnings related by Factiva. Then we checked to

see if any article has a number within five percent of the actual earnings figure (as reported by

Worldscope). If the publication date of such matched article from Factiva is within ±3 days of the

date reported by Bloomberg, we use the earlier of these two dates as our announcement date and

label the event as crossed with Factiva. We also construct a combined sample that we use for most

of our analysis that is simply the combination of the Bloomberg date that were either verified by

IBES or Factiva. If a Bloomberg date was verified by Factiva but we find an IBES announcement

2 These calculations are based on the assumption that the research assistant accuracy is 100 percent for the hand checked sample. The accuracy rate of the combined Bloomberg plus IBES sample could likely exceed 91 percent.

that is earlier then we exclude the event in the combined sample. To avoid imprecise inferences, we

also require that each country have at least 20 earnings news events over our combined sample to be

included in any analysis.

C.2. Sample Summary Statistics

Panel A and B of Table 1 shows summary statistics for both developed and emerging market

earnings announcements. Panel A first displays the number of firms with Datastream data and the

number of these firms that match to Bloomberg and where Bloomberg has earnings dates. In

developed markets, the average developed market has 1,151 common equity firms on Datastream

and 854 of these firms have Bloomberg announcement dates. The average emerging market has 725

firms with 543 having Bloomberg dates. On average, firms have slightly more than six annual

earnings announcement for a average of 5,245 unverified announcement dates in developed markets

and 3,313 in emerging markets. We are only able to check a limited set of dates with Factiva.

Because the IBES crossed with Bloomberg gathers such a large sample in most developed markets,

we only check a smaller sample of fifty firms from Factiva in Developed markets and end up with

data for an average of 17 firms and 42 events in each developed market. For emerging markets we

sample a much larger set of firms and end up with 164 firms and 277 events on average in each

market. The combined data includes the Bloomberg and IBES intersection—this drastically

increases the sample in developed markets. On average, there are 657 firms with data coverage in

developed markets and 2,470 events. In emerging markets there are on average 260 firms and 659

events. There are four emerging markets with less than 50 combined events (Egypt, Hungry,

Pakistan, and Peru). While this may seem like a small number of events, it is not when compared to

the previous literature. Bhattacharya et al. (2000)’s sample consisted of 19 earnings events and 75

total events in Mexico. In contrast, our sample of 118 Mexican earnings announcements has a

similar number of total announcements and six times the number of earnings announcements.

DeFond, Hung, and Trezevant (2007) do not even have Mexico, and many other emerging markets

in their sample.

Panel C presents the percent of the Factiva sample that occurs each year. Most of the sample

occurs after 2004. We suspect the low rate of earnings matching prior to 2004 is due to the

infrequent use of the earnings tag in this part of the sample.

D. Merger Announcement Dates

The sample of merger announcements is comprised of data from three sources: SDC,

FactSet, and Bloomberg. While there is significant overlap among sources, each source contains

some events that are not present in either of the other two. The sample is restricted to initial bids;

any bid for a target in any one of the databases within two years of a previous bid is thrown out. The

announcement date used for this study is the first date from among the three sources.

Panel D of Table 1 reports the number of merger events for which there was data in each

country. The number of events per country ranges from a maximum of 807 in the U.K. to a

minimum of 2 in Luxembourg. The small number of events in some countries make accurate

estimation of the associated country effect difficult. So that our findings are not driven by imprecise

measurement, if any country has less than ten merger announcement dates it is excluded from the

sample. The sample consists of 38 countries with over ten merger dates as compared to 42 countries

with over 30 earnings announcement dates. On average the 22 developed markets have 188 events

per country and the 16 emerging markets have 61 events per country. The merger sample is

significantly smaller than the earnings sample yet still a significant sample size of 5,114. There are

only 3,943 events in this sample.

III. Earnings Event Reactions Across Countries

We wish to examine whether significant news is disseminated on the announcement day.

Since no study has comprehensively examined the stock price reaction around news announcements

for a broad cross-section of emerging market countries, we do not know if the Bhattacharya et al.

(2000) case of Mexico in the early and mid 1990s is the exception or the norm. Given that the

amount of trading in most emerging markets has increased dramatically since the late 1990s, there

are reasons to think that responses of stock price reaction to news may have changed since 1994-

1997, even in Mexico. Here we first outline our main methodology for examining event reactions

and then we turn to examining event reactions around the world.

A. Preliminaries

Even though positive earnings news is typically accompanied by a positive stock price

reaction, our concern is whether information released is concentrated around news events, and not

the direction of the news itself. Hence, we focus our analysis on announcement volatility, although

in later analyses we will aloes look at signed announcement returns.

Reactions are most commonly based on Dimson-beta adjusted abnormal returns (Dim. Adj.)

although we check our main inferences with market-adjusted abnormal returns and find that they are

similar. The market factor in both models is the value-weighted local stock market return since a

local model is shown by Griffin (2002) to lead to more precise return forecasts than more

complicated global or international models. Betas are calculated following Dimson (1979), using

three leads and lags of the value-weighted local market return. The reaction statistics are composed

of two parts: event volatility and normal volatility. Event volatility is the mean absolute abnormal

return over the [-1, 2] event window relative to the earnings announcement date. Normal volatility

is the mean absolute abnormal return during the [-55, -2] and [3, 55] windows. Normalized volatility

is event volatility divided by normal volatility and has intuitive appeal in that it measures absolute

event returns in proportion to absolute returns outside of the earnings window. If the two periods

are equivalent, the ratio will take a value of one. Differenced volatility is event volatility minus

normal volatility. To assess significance, we use a non-parametric rank-deviation test for differences

in abnormal absolute returns, first proposed by Corrado (1989) and implemented by Bhattacharya, el

al (2000).

Importantly, we wish to avoid capturing non-reactions which are due to stock price

illiquidity or the fact that a stock does not trade. For this reason, in order to be included in any of

our samples, we require a stock to exhibit at least 50 days of non-zero returns or volume during the

period of -250 to -126 prior to the event.

B. Event Reaction Results

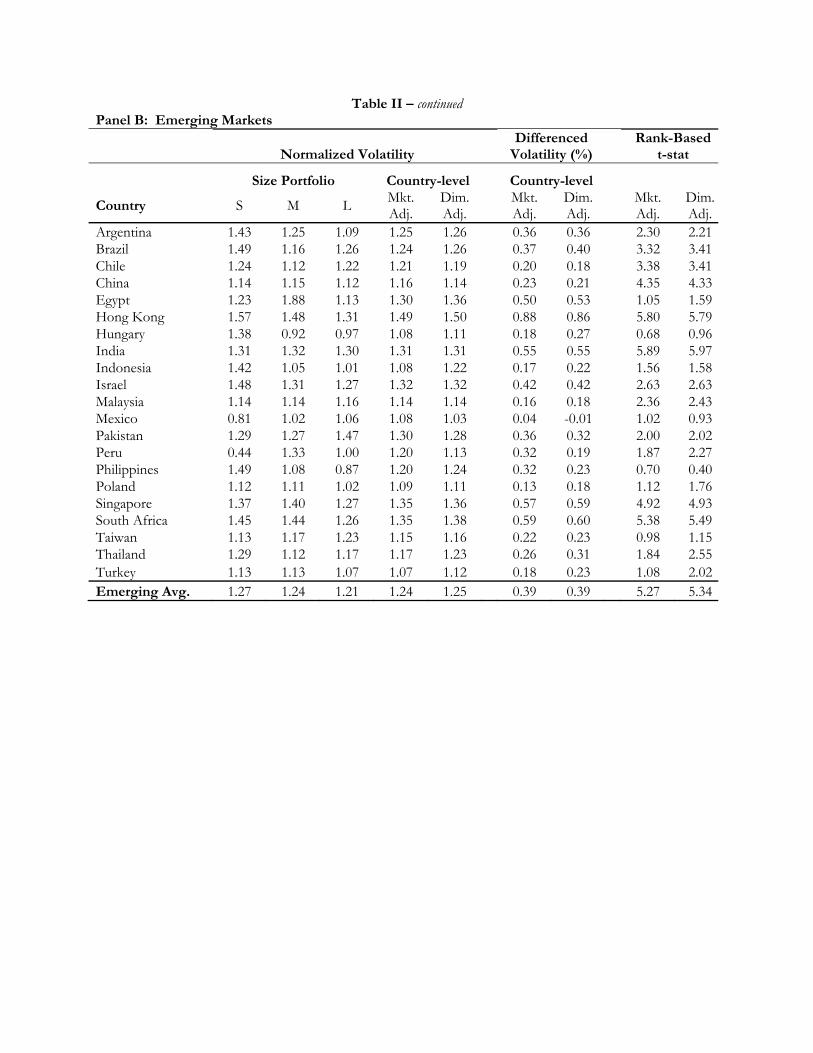

Table II first reports normalized volatility at the country-level and by size portfolio with

Panel A for developed markets and Panel B for emerging for our combined sample. Size portfolios

are based on prior December NYSE/AMEX/NASDAQ tercile breakpoints. First, Table II shows

that country reactions vary widely across countries. Second, there are typically relatively small

differences in reactions across size portfolios. Yet, in many developed markets there is a slight

tendency for reactions to be larger among larger firms. For example, in small developed markets the

average event reaction is 1.44 in small firms and 1.57 in large firms. In emerging markets the

reactions for small firms (1.27) is slightly larger than that for large firms (1.21). Third, there is little

difference in the Dimson market-model adjusted ratios as compared to those calculated using a

simple return minus the market. Unless otherwise stated, we use abnormal returns calculated with

the Dimson measure throughout the paper.

Figure 1 ranks all of our countries from highest to lowest volatility event ratio. Developed

markets are blue (light) and emerging markets are in red (dark) and significance at the five percent

level is indicated by stripes. First, the figure highlights how event reactions vary widely around the

world. The U.K. has an event reaction of two, meaning that event volatility is double normal stock

volatility, while Mexico has an insignificant event reaction of only 1.03. Second, the developed

markets typically have much higher event reactions. The emerging markets with high event reactions

like Hong Kong and Singapore have well developed capital markets and would be thought of as

advanced if not for our World Bank classifications. Third, the non-parametric t-statistics for the

Figure are also reported in the last columns of Table II and show that eight markets exhibit

insignificant reactions (Egypt, Philippines, Thailand, Indonesia, Taiwan, Hungry, Poland, South

Korea, and Mexico). Finally, many countries with reactions that are statistically different from one

have reactions that are economically close to one and much different from the reaction in most

developed markets. For example, Chile, Austria, China, Malaysia, Peru, Greece, and Turkey all

exhibit statistically significant reactions between 1.1 and 1.2. In contrast, U.K., Netherlands, Finland,

Sweden, Switzerland, France, Belgium, and the U.S. all exhibit reactions that are at least above 1.5

times the volatility on a normal trading day.

Panel B of Figure 1 shows the difference in volatility reaction from the event period to the

normal period. To facilitate comparison, the ordering is kept the same as in Panel A. While the

precise ordering varies somewhat across countries, the Panel shows that the overall ordering is

similar with the difference in volatility measure. Markets like Hong Kong and the U.S. exhibit

relatively higher measures with the difference in event volatility. The volatility ratio is relatively

smaller ratios for these markets because the abnormal returns during ‘normal’ or the non-earnings

window is relatively more volatile. We are not able to tell whether this volatility during the ‘normal’

period is due to news or private trading days. Conceptually, we prefer the volatility ratio to the

volatility difference, because the ratio makes for more intuitive comparisons of abnormal volatility

among countries.

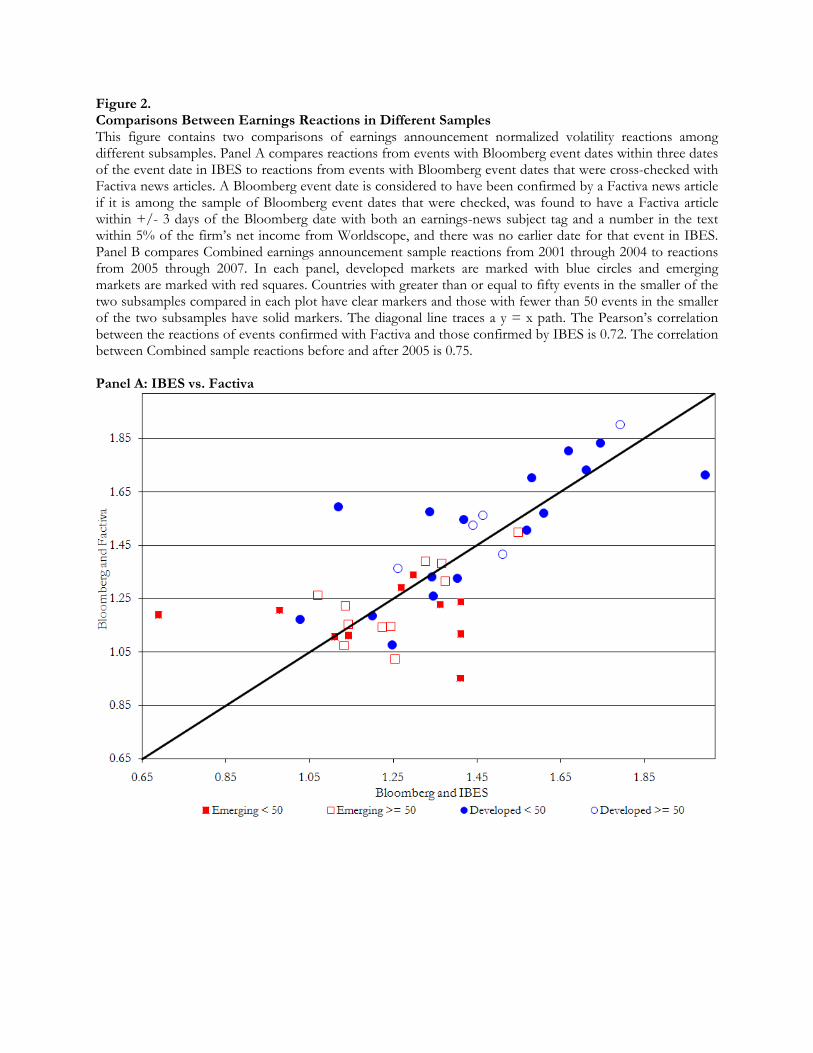

We now turn to examining how sensitive the volatility ratio is to differences in date

confirmation methodology by examining the relation between our sample of Bloomberg dates that is

confirmed by IBES as compared to those verified by Factiva. Figure 2 shows a scatterplot of the

average volatility ratio for each market where red (dark) circles are for emerging markets and blue

(grey) boxes for developed markets. Markets with less than fifty events in the smaller of the two

subsample are in boxes and circles that are solid, while countries with more observations are hollow.

Panel A of Figure 2 shows that there is a linear relation between the two samples with most

countries, particularly those with over fifty events mapping to each other. Overall, the cross-country

correlation between the two samples is 0.72. Additionally, the mean of the two samples is nearly

identical with a cross-country sample average of 1.35 for those dates confirmed by IBES and 1.36

for those confirmed by Factiva. If one of the two approaches led to inaccurate dates but the other

sample was accurate, then we would expect a large difference between the two subsamples. The

strong relation between the two samples provides some support for the accuracy of our dates

through both methods. With bad dates from both methods one would obtain no reactions in both

countries. However, it would be odd that our dates would be extremely accurate using both methods

in most countries but inaccurate using both methods in a few.

In Panel B of Figure 2 we examine if the reaction on two earnings dates shifted dramatically

through time. There is tight linear relation between the two subperiods and the cross-country

correlation between the two samples is 0.75. If there are shifts in news accuracy or large changes in

issues related to the hypothesis we developed in Section I, then we would expect the samples to

differ dramatically through time. The tight relation through time provides confidence that the event

reactions are relatively accurate and stable through time within a country.

IV. Hypothesis Testing

We investigate our five hypotheses using several tests and methodologies.

A. Earnings and Returns

Event reactions may be small in many countries because accounting earnings are of poor or

no quality. To investigate this possibility we examine if stock returns are moving in the same

direction as earnings information in the course of a year prior to just after the announcement (-230, -

2). Firms are placed into bins based on the ordering of high to low abnormal event reactions based

on the ordering of the normalized volatility ratio in Figure 1. We examine the abnormal stock

returns over the year for both firms with positive changes in earnings and those with negative

changes in earnings. The analysis is similar in spirit to the sorting approach used in the international

study of the relation between earnings and returns performed by Alford, et al. (1993).

Figure 3 shows that for the combined sample, the relation between news and abnormal

returns is strong in all four periods, though stronger in the high reaction countries. Nevertheless,

even in the lowest reaction set of countries there stocks with positive news over the year earn five

percent abnormal returns over the year, whereas countries with negative news announcements earn

below 16 percent—a more than 21 percent difference in returns. By comparison the difference in

returns between positive and negative news firms is over 26 percent in event reaction markets and

over 22 percent in the next to highest event reaction market. At first glance one might say that

stocks in low reaction countries exhibit stronger reactions to negative earnings news than to positive

news—this inference is incorrect. Since abnormal returns are calculated based on the returns in the

market over the year, the benchmark itself in may contain many positive earnings firms. Over our

2001 to 2007 period the emerging markets in the low reaction countries experienced much stronger

growth in earnings and returns than those in developed markets. This would be reflected in positive

market returns in each market. Panel B shows return differences between those with positive and

negative earnings changes over the year for firms in the sample verified by Factiva (2004- 2007). In

sum, both for the combined and Factiva-only sample earnings are tightly linked with stock returns in

both high and low reaction markets providing evidence against the hypothesis that low reactions are

due to low earnings quality.

We also turn to examining an event that does not rely on accounting information—

takeovers. Table III displays diagnostics of target firm abnormal event reactions on the

announcement day. These results are displayed by size portfolio, as well as with both market and

Dimson (1979) adjusted returns. One country that stands out is Norway where the average

abnormal volatility on takeover announcement days is 14 times that of a normal day. The average

developed market has an event reaction of 2.19 as compared to an event reaction of 3.59 for

emerging markets.

Figure 4 plots the relation between our combined earnings sample to the reaction of

takeovers. As should be expected, takeover reactions are much larger than earnings reactions. For

the most markets there is a clear relation between the abnormal takeover reaction and the abnormal

earnings reaction. Across countries there is a correlation of 0.57 between event reactions and

earnings reactions. This again provides evidence that cross-country patterns in earnings event

reactions are not primarily driven by differences in accounting conventions across markets.

Nevertheless, we will also further examine the relation between accounting variables and cross-

country reactions later in our cross-sectional regression analysis.

B. Inattentive Investors and the Information Environment

We next examine whether investor inattention or a low quality information environment is

partially responsible for slow or no reactions in low reaction countries. If earnings are meaningful,

but not incorporated upon the announcement, then one should see post-earnings announcement

drift [Ball and Brown (1968)]. Griffin, Kelly, and Nardari (2008) find substantial drift in both

developed and emerging markets but do not look at the relations between event reactions and drift.

We calculate earnings surprises as the difference between the actual reported earnings per

share and the mean analyst earnings per share forecast. We include only the last forecast for each

analyst at least 14 calendar days and not more than 182 calendar days before the reporting date. This

difference between actual and expected earnings is then scaled by price six calendar days prior to the

reporting date in order to normalize across different firms. Within a country, we sort events into the

positive (negative) portfolio if SUE is in the top (bottom) 60 percent of positive (negative) SUEs.

We first wish to see if returns over the three-day event window are in the same direction as

the earnings surprise. Panel A of Figure 5 shows that for firms with positive earnings surprises the

relation monotonically declines across portfolios from 1.9% in the high reaction country to 0.3% in

the low reaction country. For negative earnings surprises there is not a monotonic relation due to

only a small negative surprise in the next to highest reaction group of countries. Nevertheless, there

are large differences across groups, with firms in high reaction countries exhibiting negative returns

of 1.6% in high reaction countries and only 0.6% in low reaction countries. Panel B also shows

similar patterns for the part of the sample that is verified with Factiva though the differences are not

significant in the high reaction countries, likely due to the scarcity of observations here since many

more firms were sampled in emerging markets. The main point from these figures is that inferences

using earnings surprises yield a consistent picture as those from using volatility ratios. Having

established this fact, we turn to measuring post-event price movements.

Panel B shows that there is post-earnings announcement drift in the period from 3 to 55

trading days following the earnings announcement. The difference between the average returns to

positive earnings announcements minus the return from negative earnings announcements is 0.8%

percent in high reaction markets and 2.0% in low reaction markets. For the Factiva sample there is

actually a smaller difference between positive and negative post-earnings drift in the low reaction

market than in many of the other groups.

Panel C examines drift in the window of 56 to 125 trading days following the announcement.

Here there is little drift in high reaction countries but substantial negative drift (over three percent)

in low reaction countries. Overall, the results from Panels C and D show some more drift in low

reaction countries, although the differences are not large. To sum up we find only weak support for

the inattentive investors or poor news environment hypotheses. In a later section we use cross-

sectional regression analysis to disentangle these competing hypotheses.

C. Pre-Announcement Trading through Public or Private Information

We next examine whether there is pre-announcement information leakage in the same

direction as the earnings surprise. Panel D of Figure 5 shows that in the combined sample there is

more trading in the direction of positive earnings surprise events in the prior period [-55, -2] in all

four reaction portfolios, though the pre-announcement returns are largest in the low reaction sample

(5.1 percent return). Interestingly, however, firms with negative earnings surprises also have positive

returns in the low reaction sample (3.1 percent). The result is that the pre-announcement drift is

similar in high and low reaction countries. The sample that is verified with Factiva also yields similar

inferences. In Panel E we also examine post-announcement trading in the period from [-125, -56].

Here we find that in low reaction countries high earnings stocks outperform low earnings stocks by

over seven percent whereas in high reaction markets the difference is only over three percent. This

is consistent with information leakage occurring earlier in low reaction countries. However, the

results are not as strong with the smaller Factiva verified sample.

For low reaction firms, since earnings typically move in the same direction as the analyst

forecast and in similar or greater magnitude to that in high reaction markets in both the pre- and

post-announcement period, both the pre- and post-announcement results also provide strong

evidence against the first hypothesis that earnings are not moving in the announcement window in

low reaction countries due to poor earnings quality. Our results seem to point to significant trading

in the same direction as the news announcement which is consistent with some form of information

leakage.

In Table IV we also exhibit information leakage for takeovers. Pre-announcement leakage is

lower in low reaction market. However, the total premium appears to be much lower as well.

Takeover targets in low earnings reaction countries exhibit a much lower event reaction (3.5 percent)

than those in high reaction markets (17.4 percent) but when averaged across the two prior

subperiods ([-126, -56] and [-55, -2]) still exhibit pre-announcement leakage (5.8 percent) which is

almost as great as that in the high reaction markets (7.8 percent). The end result is that in low

reaction markets 62.4 percent of the total price run-up from [-126, +2] is reflected in the pre-

announcement period whereas in high earnings reaction markets only 30.9 percent of the total run-

up is reflected in the pre-announcement period. Unlike with earnings events, with mergers, we see

no drift for low reaction markets. In contrast to earnings announcement, merger announcements are

unplanned and unscheduled. Hence, the relatively larger stock price increase in the pre-

announcement period for low reaction countries is suggestive of informed (or insider) trading. In the

next section we explore how average event reactions with a country are associated with country-level

measures of insider trading to further shed light on whether the lower event reactions associated

with information leakage is the result of public or private sources of information.

V. Cross-Country Analysis

In this section we bring additional evidence to bear on the five hypothesized factors

influencing the magnitude of announcement reaction: accounting quality, investor attention and

information environment, public pre-announcement information release, and insider trade. We first

describe our cross-sectional data, then precede to univariate and multivariate cross-country

regressions followed by checking the robustness of our inferences to firm-level controls with panel

regressions.

A. Cross-Country Data

Event reaction characteristics can and do vary across companies, but they have a strong

country-level component as well. For example, while companies within a market can have differing

levels of accounting quality, base levels of accounting quality are something that is often mandated

by rule or law for all firms listing in a market. As such, we may find differences in event reactions

across markets as a function of differences in country-wide characteristics.

In the following subsections we examine whether a broad set of variables that relate to these

characteristics is associated with the size of the event reaction. The variables are taken from a variety

of sources and are chosen because they reflect aspects of accounting quality, the information

environment, trading activity, insider trading law and practice, laws regarding investor protection and

trade, and the level of economic and market development that relate to our hypotheses. Where data

availability permits we take the average value of the variable over our 2001 to 2007 sample.4

We conduct our analysis of the cross-country evidence for our five hypotheses by first

examining univariate regressions with event reaction as the dependent variable and proxies for

accounting quality, insider trading law and practice, etc. as the independent variables. It is important

to note that our regressions are not meant to imply causality but are merely capturing associations

between variables. We then progress to bivariate regressions and trivariate regressions in order to

explore which of these country-level characteristics is most important in the cross section.

4 We have also collected variables from other papers or from data sources that only cover part of the 2001 to 2007 period, in these cases we use the average value of the data available.

B. Univariate Cross-Country Regressions

Panel A of Table V presents the coefficients, t-statistics, and adjusted R2s from regressions in

which we regress a measure of earnings announcement reaction on variables reflecting aspects of

accounting quality, the information environment, trading activity, insider trading law and practice,

laws regarding investor protection and trade, the level of economic and market development, and

trading costs. For each event within a market the earnings announcement reaction is measured as

the natural log of the normalized volatility ration (as used in Table II and Figure 1). The equally

weighted average event reaction is calculated for each country, pooling across all years. We are

concerned that countries with fewer events might have less precise average earnings announcements,

which might induce bias in our regressions. To mitigate this concern we weight the observations by

the number of earnings announcements in each country in the left panel of Panel A. We also present

unweighted regressions for comparison in the right panel. The results are qualitatively the same.

B.1 Accounting Quality

Our first hypothesis is that the strength of the earnings news reactions may vary across

countries due to the importance or accuracy of financial accounting across countries. In the top

panel we see that countries with better quality of financial disclosure and stronger accounting

standards, and less earnings management (from Leuz, et al (2003)) are all associated with stronger

event reactions, consistent with the notion that better accounting quality results in more informative

valuation signals.

B.2 Inattentive Investors and Poor Information Environment

The second and third hypotheses posit that event reactions may be muted due to investor

inattention or information that is slow to arrive. As a proxy for attention we examine turnover by

value and the value of trade to GDP. The table shows that simple turnover is significantly positively

associated with greater event reactions, which is consistent with greater attention in the market

resulting in rapid information incorporation, although as one cannot infer causality from these

regressions other interpretations are possible. Better quality information could either improve the

speed of information incorporation, increasing event reactions or a surfeit of information could

overload investors and result in slow information diffusion into prices. These univariate regressions

show that a better quality information environment has a pronounced relation to stronger event

reactions. Both Availability of Information, which asks if “Information about businesses is extensive

and easily available” and Freedom of the Press, a response to the question whether “the media can

publish/broadcast stories of their choosing without fear of censorship or retaliation,” are both

strongly related to differences in average earnings announcement reaction volatility explaining just

over half of the variation across countries.

B.3 Private Information

Country level measures do a poor job of reflecting whether news is publicly pre-released

prior to earnings announcements, so we turn straight away to the fifth hypothesis: Information

leakage resulting insider trading will dampen the impact of news announcements on price. In these

univariate regressions, we see that event reactions are larger where insider trading laws have been

enforced and in countries where surveys indicate the perception of less insider trade and firms which

tend to behave ethically. 5 Both are consistent with the notion that information leakage occurs when

insider trading is common.

Finally, we also examine a number of indicators of economic and financial developed to see

whether differences are predominantly related to market development. Notably, sophistication of

financial markets and technological sophistication are strong correlates of event reactions. In the 5 Prevalence of Insider Trading is a CEO survey response variable from the Global Competitiveness Report (1=pervasive; 7=extremely rare). The Ethical Firms question asks if “corporate ethics (ethical behavior in interactions with public officials, politicians, and other enterprises) of your country’s firms in your industry are among the best in the world.”

next section we include significant variables from these univariate regressions in bi- and trivariate

regressions in order to distill the more important correlates of the size of event reactions.

C. Multivariate Cross-Sectional Regressions

We follow the procedure outlined in Griffin, Nardari, and Stulz (2007) and take the

significant variables from Panel A and examine these variables in multiple combinations of bivariate

regressions to uncover the stronger correlates of earnings announcement reactions. We

systematically examine all 153 unique combinations of the 18 significant variables from the

univariate regressions. In the interest of space the panel only presents a sampling of the results. The

first column of Panel B of Table V indicates the number of times that a particular variable is

significant in combination with others.

Each category (quality of accounting, etc.) contains variables frequently associated with

greater event reactions, but two in particular stand out. Absence of insider trading as captured by the

Prevalence of Insider Trade (1=pervasive; 7=extremely rare) and a strong information environment

as reflected in a Press Freedom survey measure, stand out as strong correlates of the magnitude of

earnings announcement reactions. Notably, insider trading law enforcement appears to be less

significant than the survey response to the Prevalence of Insider Trade, but perhaps this is not

surprising since enforcement of insider trading laws does not mean that insider trading does not

occur. A survey variable may be a much more direct measure of perceptions within the market.

In Panel C, we perform 35 trivariate regressions with each of seven variables significant in

over half of bivariate regressions. Again Press Freedom and Prevalence of Insider Trade stand out as

significant in all specifications. Prevalence of Insider trade is at worst marginally insignificant in only

one specification out of all the 35. This is displayed in specification 8, where Availability of

Information and Quality of Financial Disclosure are collinear. Freedom of the Press is significant in

every single specification.

In summation, we find some evidence in cross country data for each of the hypotheses

examined in this section but only robust evidence is found for two of the hypotheses. Accounting

quality generally makes for larger event reactions as does greater investor attention, and stronger

legal protections for investors. However, the greatest impact is the prevalence of insider trading and

the quality of information environment. Together these explain nearly 66 percent of the variation in

country average event reactions (Panel B, specification 1). Broadly, these findings are consistent the

hypothesis that insider trading prior to events mutes the impact of news and they suggest that a

generally poor information environment reduces the magnitude of announcement reactions.

D. Panel Regressions

The cross-sectional regressions are advantageous in that they average affects across firms

within a country and are careful not to overweight countries simply because they contain more

observations (in our case, events). However, market reactions to the release of firm-specific

information may vary by the type of which about which the news in generated. Accordingly,

accounting for firm differences may be necessary to isolate true country-level variation. Such

differences will be determined by the strength of value-relevant information available from outside

sources. For example, one may form a relatively precise estimate of an oil firm’s quarterly earnings

ahead of the announcement date by utilizing information available in the commodities markets. For

a different firm, such as a software company, there may exist little information outside that

produced by the company that is relevant for the calculation of firm value. One way to isolate

similar firms is to use industry affiliation. For international stock returns, Griffin and Karolyi (1998)

find that industry composition is largely averaged out when computing country-level stock returns.

Nevertheless, Brown and Ball (1967) show that a firm’s earnings contain a significant industry

component it is possible that the industry composition could be driving cross-country averages. We

use Datastream industry dummies for 17 industries.6 Importantly, we can control for the strength of

the news by using the magnitude of the earnings surprise relative to the IBES forecast. We include

U.S. market cap size dummies to capture simple differences in reactions across firm-size groupings.

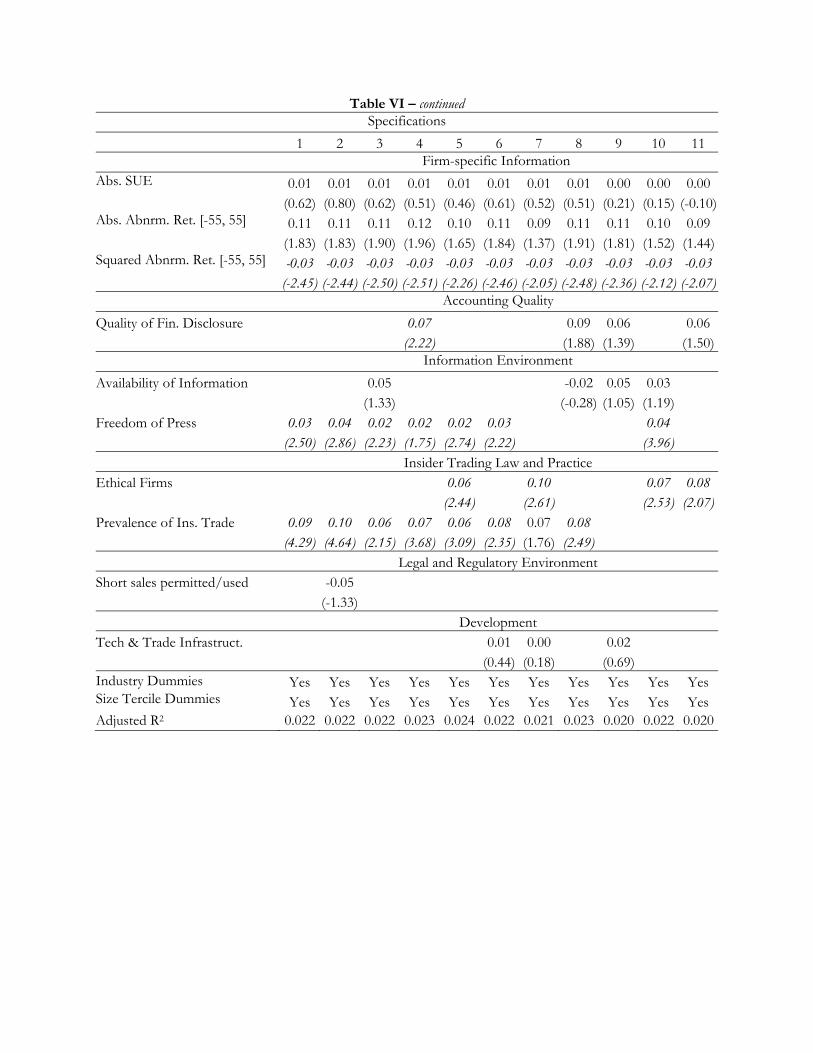

Table VI shows the Panel regressions with firm controls and industry and size tercile

dummies. We estimate panel regressions with exactly the same cross-country variables as in Panel C

of Table V. Surprisingly, the main inferences from the simple cross-sectional regressions are

essentially unchanged. Both the freedom of the press variable and prevalence of insider trade are

significant in all specifications except for one specification each. The only difference is that the

Ethical firms are significant as well which indicates that countries with stronger corporate ethics

have stronger event reactions.

VI. Conclusion

This paper finds that stock market reactions to news events vary widely around the world,

with most developed markets exhibiting large reactions to news and some emerging markets

exhibiting only miniscule reactions. We examine possible explanations including poor accounting

quality, inattentive investors, poor news dissemination, public pre-announcement trading, and

insider trading.

In countries with low event reactions, prices move strongly with earnings over annual

horizons. Returns move in the same direction as the earnings surprise both prior to the earnings

announcement and afterward. This is strong evidence that it is not poor earnings quality driving the

lack of event reactions in some markets. The post-announcement drift in the same direction of the

6 Because we use Datastream industry codes we currently exclude U.S. firms until we can map the U.S. SIC industries to Datastream.

earnings announcement is consistent with inattentive investors or poor news dissemination. Pre-

announcement trading is consistent with early news dissemination either through public or private

information sources. Merger announcements provide an interesting event to test these two

hypotheses, since takeover announcements usually catch the market by surprise. For our sample of

mergers, we find much more of the total price run-up is released in the period prior to the merger

than for firms in high reaction countries. This provides some suggestive evidence of informed or

insider (non-public) trading.

To more fully disentangle these hypotheses we systematically examine over 33 cross-country

variables related to these hypotheses and find that two main variables emerge: press freedom and the

perception of insider trading. One interpretation of this finding is that a stronger and freer press is

associated with more rapid information dissemination and incorporation into prices. In markets with

rampant insider trading the information news from the press is not a surprise as it is already

impounded into prices.

Our event reactions may be useful to policy markets, stock exchanges, and investors as they

seek to understand the relative magnitudes and extent of non-public information based trading in a

market. Additionally, since understanding the extent of private trading has implications for many

other aspects of financial markets, we hope to see additional research using the magnitude of the

event reaction as an empirical metric to help understand other cross-country differences in trading

volume, liquidity, foreign (outsider) ownership, and market valuations.

REFERENCES

Ackerman, Abraham, Jörn van Halteren, and Ernst Maug, 2008, Insider trading legislation and acquisition announcements: Do laws matter? Working Paper, University of Mannheim.

Alford, Andrew, Jennifer Jones, Richard Leftwich, and Mark Zmijewski, 1993, The relative

informativeness of accounting disclosures in different countries. Journal of Accounting Research 31, 183-223

Ali, Ashiq, and Lee-Seok Hwang, 2000, Country-specific factors related to financial reporting and

the value relevance of accounting data, Journal of Accounting Research 38, 1-21. Ball, Ray, S. P. Kothari, and Ashok Robin, 2000, The effect of international institutional factors on

properties of accounting earnings, Journal of Accounting and Economics 29, 1-51. Ball, Ray, and Philip Brown, 1968, An empirical evaluation of accounting income numbers, Journal of

Accounting Research 6, 159-178. Bailey, Warren, George Andrew Karolyi, and Carolina Salva, 2006, The economic consequences of

increased disclosure: Evidence from international cross-listings, Journal of Financial Economics 81, 175-213.

Beck, Thorsten, Asli Demirgüç-Kunt, and Ross Levine, 2000, A new database on the structure and

development of the financial sector, World Bank Economic Review 14, 597-605. Beny, Laura N., 2007, Insider trading rules can affect attractiveness of country’s stock markets,

University of Michigan Law Quadrangle Notes 50, 73-75. Bhattacharya, Utpal, 2006, Enforcement and its impact on cost of equity and liquidity of the market,

Working paper, Indiana University. Bhattacharya, Utpal, and Hazem Daouk, 2002, The world price of insider trading, Journal of Finance

57, 75-108. Bhattacharya, Utpal, Hazem Daouk, Brian Jorgenson, and Carl-Heinrich Kehr, 2000, When an event

is not an event: The curious case of an emerging market, Journal of Financial Economics 55, 69-101. Boehmere, Ekkehart, Jim Masumeci, and Annette B. Poulsen, 1991, Event-study methodology

under conditions of event-induced variance, Journal of Financial Economics 30, 253-272. Bris, Arturo, 2005, Do insider trading laws work? European Financial Management 11, 267-312. Bris, Arturo, William N. Goetzmann, and Ning Zhu, 2007, Efficiency and the bear: short-sales and

markets around the world, Journal of Finance 62, 1029-1079. Brown, Philip, and Ray Ball, 1967, Some preliminary findings on the association between the

earnings of a firm, its industry, and the economy, Journal of Accounting Research 5, 55-77.

Corrado, Charles J., 1989, A non-parametric test for abnormal security-price performance in event studies, Journal of Financial Economics 23, 385-395.

DeFond, Mark, Mingyi Hung, and Robert Trezevant, 2007, Investor protection and the information

content of annual earnings announcements: International evidence, Journal of Accounting and Economics 43, 37-67.

DellaVigna, Stefano, and Joshua Pollet, 2008, Investor inattention and Friday earnings

announcements, forthcoming in Journal of Finance. Dimson, Elroy, 1979, Risk measurement when shares are subject to infrequent trading. Journal of

Financial Economics 7, 197-226. Djankov, Simeon, Rafael La Porta, Florencio Lopez-de-Silanes, and Andrei Shleifer, 2008, The law

and economics of self-dealing, forthcoming in Journal of Financial Economics. Du, Julan, and Shang-Jin Wei, 2004, Does insider trading raise market volatility? The Economic Journal

114, 916-942. Durnev, Art A., and Amrita S. Nain, 2007, Does insider trading regulation deter private information

trading? International evidence, Pacific-Basin Finance Journal 15, 409-433. Fernandes, Nuno, and Miguel Ferreira, 2007, Enforcement of insider trading laws and stock price

informativeness, forthcoming in Review of Financial Studies. Griffin, John M., 2002, Are the Fama and French factors global or country-specific? Review of

Financial Studies 10, 783-803. Griffin, John M., and George Andrew Karolyi, 1998, Another look at the role of the industrial

structure of markets for international diversification strategies, Journal of Financial Economics 50, 351-373.

Griffin, John M., Patrick J. Kelly, and Federico Nardari, 2008, Measuring short-term international

stock market efficiency, Working Paper, University of Texas. Griffin, John M., Federico Nardari, and René M. Stulz, 2007, Do investors trade more when stocks

have performed well? Evidence from 46 countries, Review of Financial Studies 20, 905-951. Grossman, Sanford J., and Joseph E. Stiglitz, 1980, On the impossibility of informationally efficient

markets, American Economic Review 70, 393-408. Hasbrouck, Joel, 2004, Liquidity in the futures pits: inferring market dynamics from incomplete data,

Journal of Financial and Quantitative Analysis, 39, 2. Hirshleifer, David, Sonya Seongyeon Lim, and Siew Hong Teoh, 2007, Driven to distraction:

Extraneous events and underreaction to earnings news, working paper, University of California, Irvine.

Huberman, Gur, and Tomer Regev, 2001, Contagious speculation and a cure for cancer: A nonevent

that made stock prices soar, The Journal of Finance 56, 387-396. La Porta, Rafael, Florencio Lopez-de-Silanes, and Andrei Shleifer, 1999, Corporate ownership

around the world, The Journal of Finance 54, 471-517. Lesmond, David A., Joseph P. Ogden, and Charles A. Trzcinka, 1999, A new estimate of transaction

costs, Review of Financial Studies 12, 1113-1141. Leuz, Christian, Dhananjay Nanda, and Peter D. Wysocki, 2003, Earnings management and investor

protection: an international comparison, Journal of Financial Economics 69, 505-527. Newey, Whitney K., and Kenneth D. West, 1987, A simple, positive semi-definite, heteroskedasticity

and autocorrelation consistent covariance matrix, Econometrica 55, 703-708. Peng, Lin, and Wei Xiong, 2006, Investor attention, overconfidence and category learning, Journal of

Financial Economics 80, 563-602.

Table AI Earnings Announcement Date Timing

All Bloomberg and IBES annual earnings announcement dates for 1994 through 2005 were matched based on the fiscal year of the report. Count is the total number of announcement dates. Both Equal is the number of times both sources report the same announcement date. IBES Earlier counts the number of times the IBES date is earlier and BB Earlier is the number of times Bloomberg has the earlier announcement date. Developed Markets Emerging Markets

A random sample of five firms per country was chosen. For each firm all available Bloomberg and IBES earnings announcement dates were compared to those found through Factiva to check for accuracy. The number to the right of the “/” represents the number of announcements in the country sample for which data could be found in Factiva. The number to the left is the number of those announcements which fall within the [-1, +1] window relative to the date found in Factiva. Developed Markets Emerging Markets Country IBES Bloomberg Country IBES BloombergAustralia 3/27 21/27 Argentina 4/37 17/37Austria 9/23 8/23 Brazil 0/33 23/33Belgium 4/28 25/28 Chile 1/39 15/39Canada 3/20 14/20 China 5/17 15/17Denmark 10/26 25/26 Columbia 0/22 1/22Finland 12/30 21/30 Croatia 4/18 7/18France 7/31 22/31 Cyprus 0/11 5/11Germany 1/23 3/23 Czech Republic 2/32 13/32Greece 0/10 0/10 Egypt 0/15 3/15Iceland 0/14 9/14 Ghana 0/3 0/3Ireland 0/20 11/20 Hong Kong 11/47 25/47Italy 2/17 12/17 Hungary 5/26 20/26Japan 16/42 34/42 India 1/24 14/24Luxembourg 1/22 21/22 Indonesia 1/9 5/9Netherlands 18/46 42/46 Israel 1/21 18/21New Zealand 5/26 26/26 Jordan 0/8 0/8Norway 4/17 13/17 Kenya 0/10 4/10Portugal 2/36 32/36 Kuwait 0/6 3/6Spain 7/25 23/25 Lithuania 0/11 2/11Sweden 2/33 29/33 Malaysia 4/31 12/31Switzerland 16/43 32/43 Mauritius 0/5 2/5U.K. 18/49 33/49 Mexico 12/37 26/37 Morocco 0/10 2/10 Pakistan 0/19 3/19 Peru 0/22 10/22 Philippines 1/16 3/16 Poland 0/25 1/25 Romania 0/10 0/10 Singapore 4/35 30/35 South Africa 0/23 16/23 Sri Lanka 0/11 0/11 Taiwan 2/15 3/15 Thailand 3/41 17/41 Turkey 0/11 2/11 Venezuela 1/24 0/24 Zimbabwe 0/9 5/9

Total 140/608 456/608 Total 62/738 323/738

Figure 1. Earnings Announcement Reactions This figure plots two types of earnings announcement reaction volatilities. These volatilities are calculated using Dimson-beta adjusted abnormal returns. Betas are calculated following Dimson (1979), using three leads and lags of the value-weighted local market return. In order for an event to be included, there must be at least 50 non-missing returns in the period 250 to 126 days before the event for the purposes of market model estimation. The reaction statistics are composed of two parts: event volatility and normal volatility. Event volatility is the mean absolute abnormal return over the [-1, 2] event window relative to the earnings announcement date. Normal volatility is the mean absolute abnormal return during the [-55, -2] and [3, 55] windows. The Normalized Volatility Reactions in Panel A are event volatility divided by normal volatility. Differenced Volatility Reactions in Panel B are event volatility minus normal volatility. Developed market countries are marked with red (dark) bars and emerging market countries are marked with blue (light) bars. Countries with event volatility significantly greater than normal volatility are denoted by striped bars. Significance is determined by a Corrado (1989) non-parametric rank t-test. Panel A: Combined Earnings Announcement Sample Normalized Volatility

Figure 2. Comparisons Between Earnings Reactions in Different Samples This figure contains two comparisons of earnings announcement normalized volatility reactions among different subsamples. Panel A compares reactions from events with Bloomberg event dates within three dates of the event date in IBES to reactions from events with Bloomberg event dates that were cross-checked with Factiva news articles. A Bloomberg event date is considered to have been confirmed by a Factiva news article if it is among the sample of Bloomberg event dates that were checked, was found to have a Factiva article within +/- 3 days of the Bloomberg date with both an earnings-news subject tag and a number in the text within 5% of the firm’s net income from Worldscope, and there was no earlier date for that event in IBES. Panel B compares Combined earnings announcement sample reactions from 2001 through 2004 to reactions from 2005 through 2007. In each panel, developed markets are marked with blue circles and emerging markets are marked with red squares. Countries with greater than or equal to fifty events in the smaller of the two subsamples compared in each plot have clear markers and those with fewer than 50 events in the smaller of the two subsamples have solid markers. The diagonal line traces a y = x path. The Pearson’s correlation between the reactions of events confirmed with Factiva and those confirmed by IBES is 0.72. The correlation between Combined sample reactions before and after 2005 is 0.75. Panel A: IBES vs. Factiva

Panel B: Combined Reactions Before and After 2005