36

Western Lithium www.westernlithium.com February 2011

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 1/37

Western Lithium

www.westernlithium.com

February 2011

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 2/37

2

Kings Valley Lithium ProjectCautionary Statement

This presentation contains projections and forward looking informationthat involve various risks and uncertainties regarding future events.Such forward-looking information can include without limitationstatements based on current expectations involving a number of risksand uncertainties and are not guarantees of future performance of theCorporation. These risks and uncertainties could cause actual results

and the Corporation's plans and objectives to differ materially fromthose expressed in the forward-looking information. Actual results andfuture events could differ materially from those anticipated in suchinformation. These and all subsequent written and oral forward-lookingstatements are based on estimates and opinions of management on the

dates they are made and expressly qualified in their entirety by thisnotice. The Corporation assumes no obligation to update forward-looking information should circumstances or management's estimates oropinions change.

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 3/37

3

Western Lithium USA Corp.

Advancing Development of a North American BasedReliable and Scalable Strategic Lithium Deposit to

Power Today’s Hybrid/Electric Cars and Mobile Devices

• One of the world’s largest known

lithium deposits• Located in the U.S.

• Cost Competitive

• Excellent infrastructure

• Experienced team of mine builders• Development stage project to coincide with rising demand

• Scalable project that can grow to meet market demand

• Focused lithium investment

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 4/37

4

0

10

20

30

4050

4

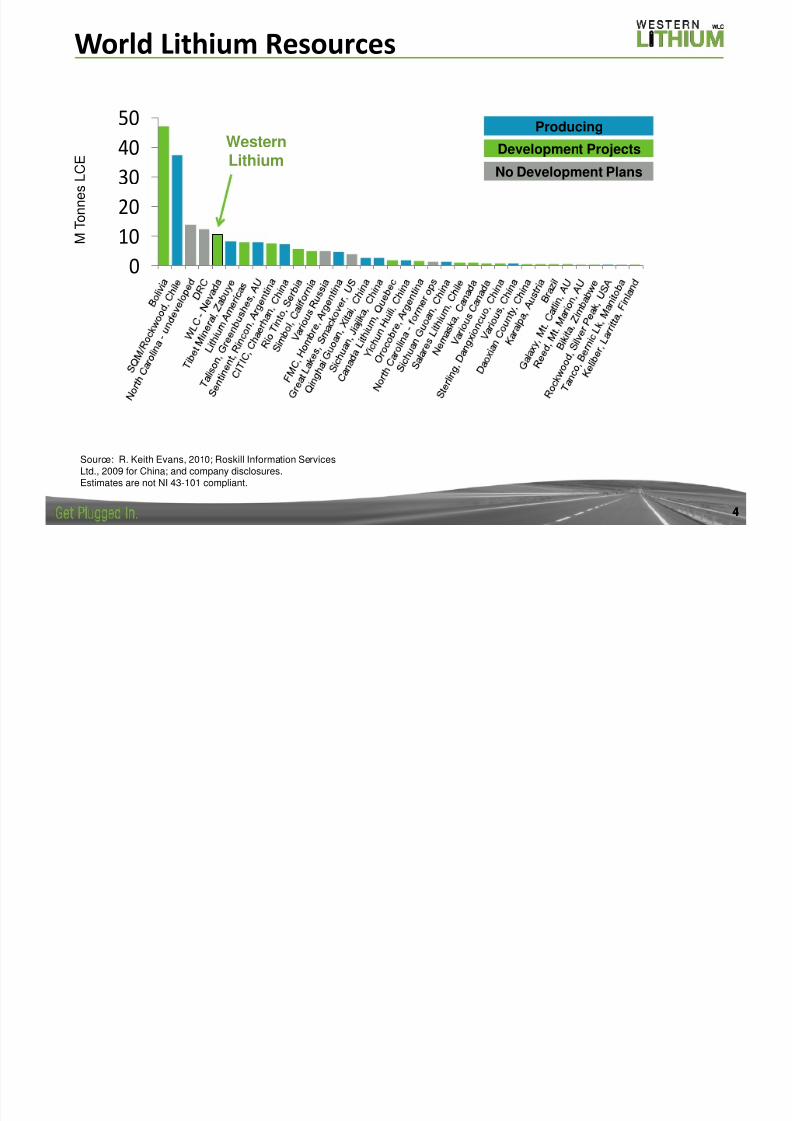

World Lithium Resources

WesternLithium

No Development Plans

Producing

Development Projects

Source: R. Keith Evans, 2010; Roskill Information ServicesLtd., 2009 for China; and company disclosures.Estimates are not NI 43-101 compliant.

M T o n n e s L C E

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 5/37

5

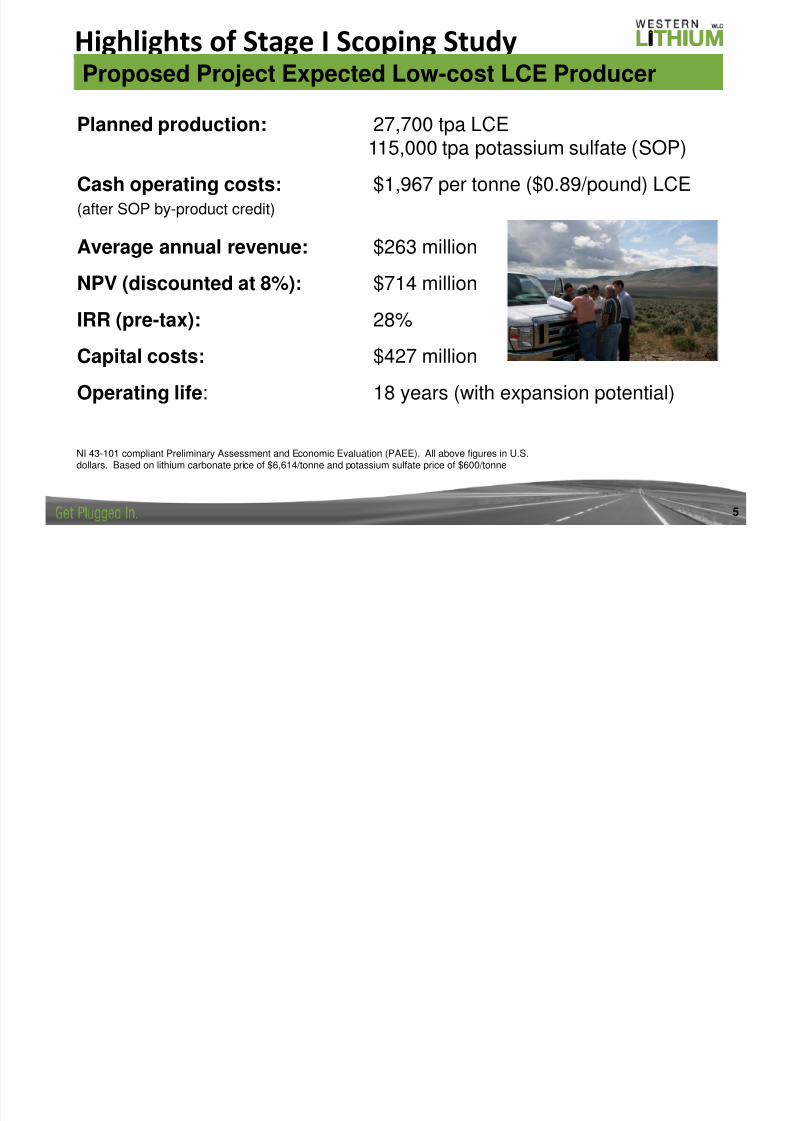

Highlights of Stage I Scoping Study

Proposed Project Expected Low-cost LCE Producer

Planned production: 27,700 tpa LCE115,000 tpa potassium sulfate (SOP)

Cash operating costs: $1,967 per tonne ($0.89/pound) LCE(after SOP by-product credit)

Average annual revenue: $263 million

NPV (discounted at 8%): $714 million

IRR (pre-tax): 28%

Capital costs: $427 million

Operating life: 18 years (with expansion potential)

NI 43-101 compliant Preliminary Assessment and Economic Evaluation (PAEE). All above figures in U.S.dollars. Based on lithium carbonate price of $6,614/tonne and potassium sulfate price of $600/tonne

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 6/37

6

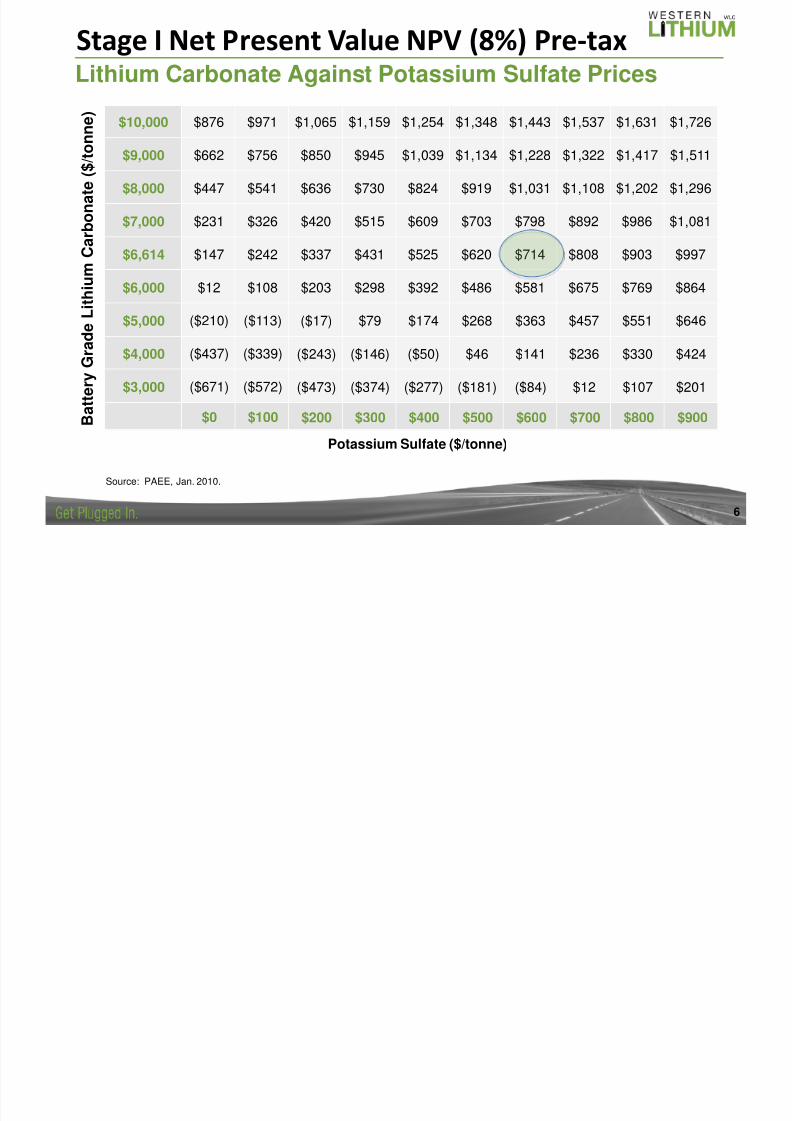

Stage I Net Present Value NPV (8%) Pre-taxLithium Carbonate Against Potassium Sulfate Prices

Source: PAEE, Jan. 2010.

$10,000 $876 $971 $1,065 $1,159 $1,254 $1,348 $1,443 $1,537 $1,631 $1,726

$9,000 $662 $756 $850 $945 $1,039 $1,134 $1,228 $1,322 $1,417 $1,511

$8,000 $447 $541 $636 $730 $824 $919 $1,031 $1,108 $1,202 $1,296

$7,000 $231 $326 $420 $515 $609 $703 $798 $892 $986 $1,081

$6,614 $147 $242 $337 $431 $525 $620 $714 $808 $903 $997

$6,000 $12 $108 $203 $298 $392 $486 $581 $675 $769 $864

$5,000 ($210) ($113) ($17) $79 $174 $268 $363 $457 $551 $646

$4,000 ($437) ($339) ($243) ($146) ($50) $46 $141 $236 $330 $424

$3,000 ($671) ($572) ($473) ($374) ($277) ($181) ($84) $12 $107 $201

$0 $100 $200 $300 $400 $500 $600 $700 $800 $900 B a t t e r y G r a d e L i t h i u m C a

r b o n a t e ( $ / t o n n e

)

Potassium Sulfate ($/tonne)

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 7/37

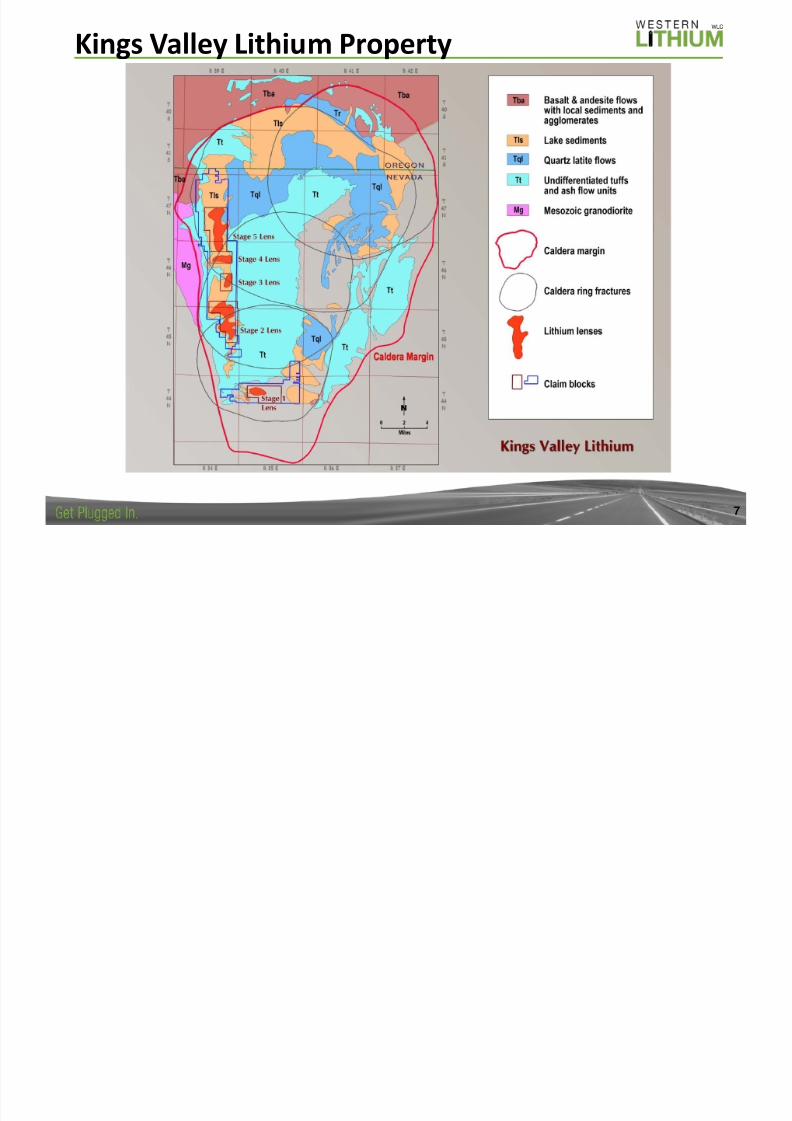

Kings Valley Lithium Property

7

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 8/378

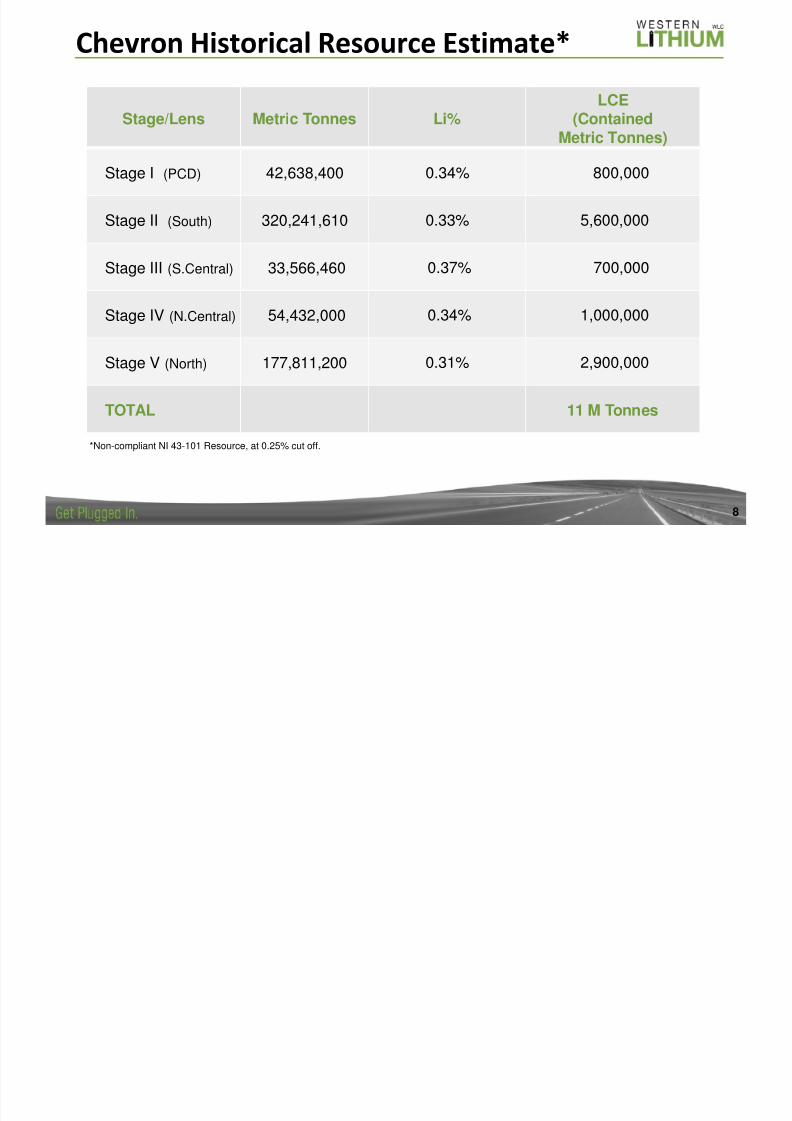

Chevron Historical Resource Estimate*

Stage/Lens Metric Tonnes Li%

LCE

(ContainedMetric Tonnes)

Stage I (PCD) 42,638,400 0.34% 800,000

Stage II (South) 320,241,610 0.33% 5,600,000

Stage III (S.Central) 33,566,460 0.37% 700,000

Stage IV (N.Central) 54,432,000 0.34% 1,000,000

Stage V (North) 177,811,200 0.31% 2,900,000

TOTAL 11 M Tonnes

*Non-compliant NI 43-101 Resource, at 0.25% cut off.

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 9/379

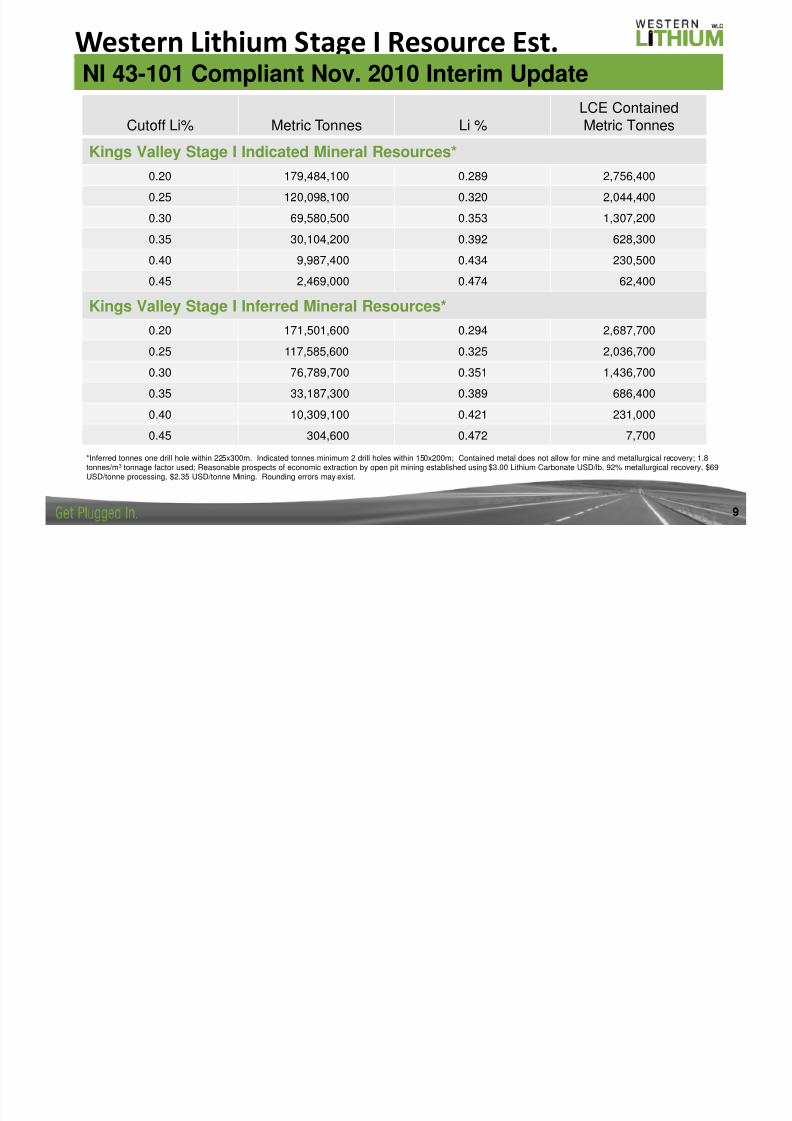

Western Lithium Stage I Resource Est.NI 43-101 Compliant Nov. 2010 Interim Update

Cutoff Li% Metric Tonnes Li %

LCE Contained

Metric Tonnes

Kings Valley Stage I Indicated Mineral Resources*

0.20 179,484,100 0.289 2,756,400

0.25 120,098,100 0.320 2,044,400

0.30 69,580,500 0.353 1,307,200

0.35 30,104,200 0.392 628,300

0.40 9,987,400 0.434 230,500

0.45 2,469,000 0.474 62,400

Kings Valley Stage I Inferred Mineral Resources*

0.20 171,501,600 0.294 2,687,700

0.25 117,585,600 0.325 2,036,700

0.30 76,789,700 0.351 1,436,700

0.35 33,187,300 0.389 686,400

0.40 10,309,100 0.421 231,000

0.45 304,600 0.472 7,700

*Inferred tonnes one drill hole within 225x300m. Indicated tonnes minimum 2 drill holes within 150x200m; Contained metal does not allow for mine and metallurgical recovery; 1.8tonnes/m3 tonnage factor used; Reasonable prospects of economic extraction by open pit mining established using $3.00 Lithium Carbonate USD/lb, 92% metallurgical recovery, $69USD/tonne processing, $2.35 USD/tonne Mining. Rounding errors may exist.

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 10/3710

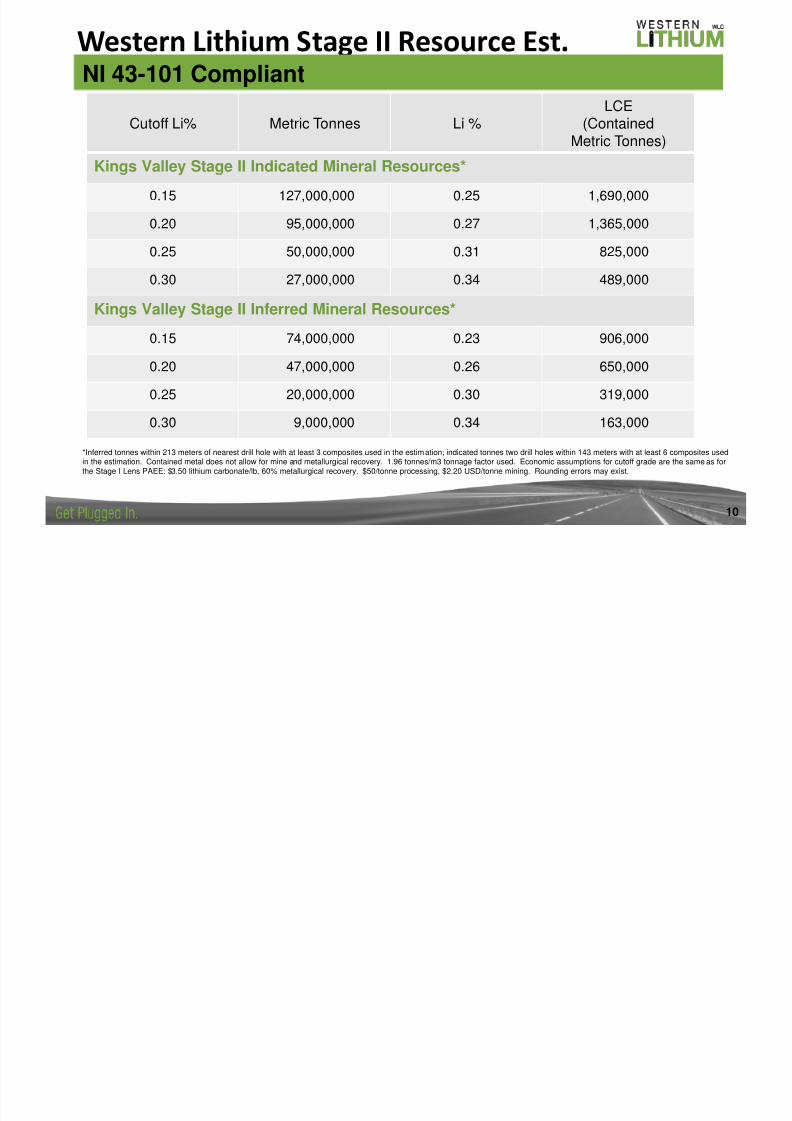

Western Lithium Stage II Resource Est.

Cutoff Li% Metric Tonnes Li %

LCE

(ContainedMetric Tonnes)

Kings Valley Stage II Indicated Mineral Resources*

0.15 127,000,000 0.25 1,690,000

0.20 95,000,000 0.27 1,365,000

0.25 50,000,000 0.31 825,000

0.30 27,000,000 0.34 489,000

Kings Valley Stage II Inferred Mineral Resources*

0.15 74,000,000 0.23 906,000

0.20 47,000,000 0.26 650,000

0.25 20,000,000 0.30 319,000

0.30 9,000,000 0.34 163,000

*Inferred tonnes within 213 meters of nearest drill hole with at least 3 composites used in the estimation; indicated tonnes two drill holes within 143 meters with at least 6 composites usedin the estimation. Contained metal does not allow for mine and metallurgical recovery. 1.96 tonnes/m3 tonnage factor used. Economic assumptions for cutoff grade are the same as forthe Stage I Lens PAEE: $3.50 lithium carbonate/lb, 60% metallurgical recovery. $50/tonne processing, $2.20 USD/tonne mining. Rounding errors may exist.

NI 43-101 Compliant

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 11/3711

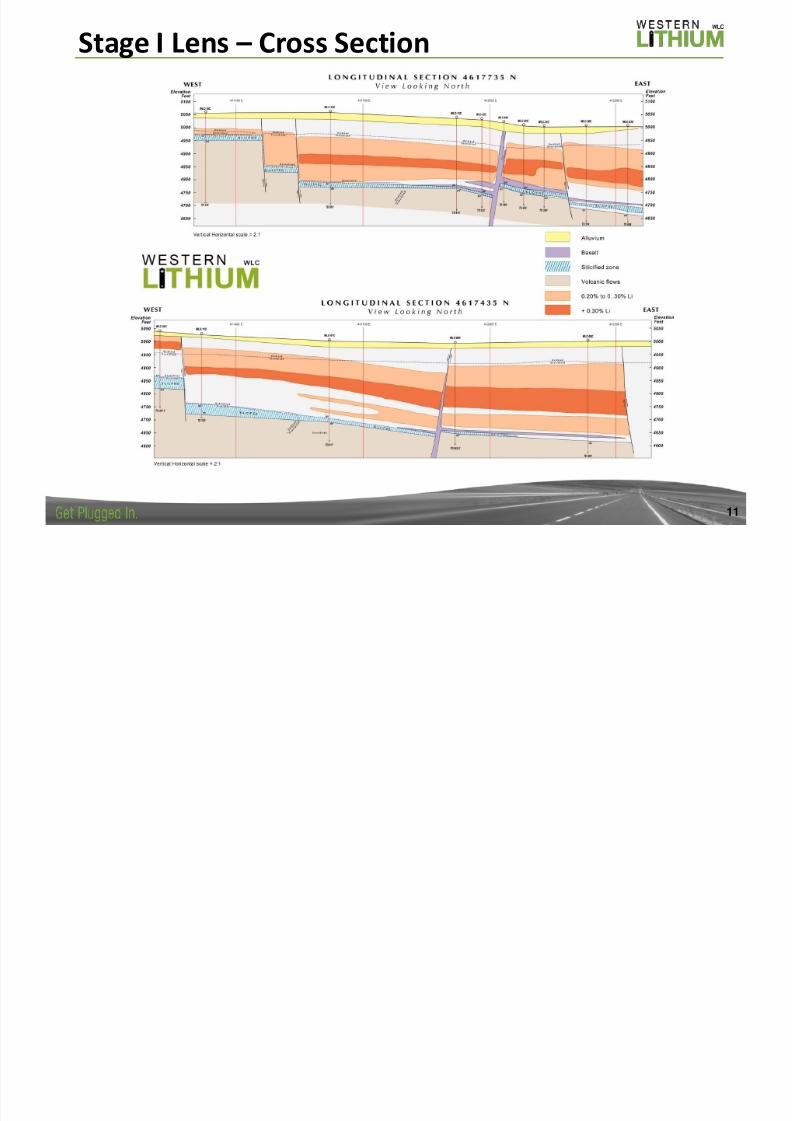

Stage I Lens – Cross Section

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 12/3712

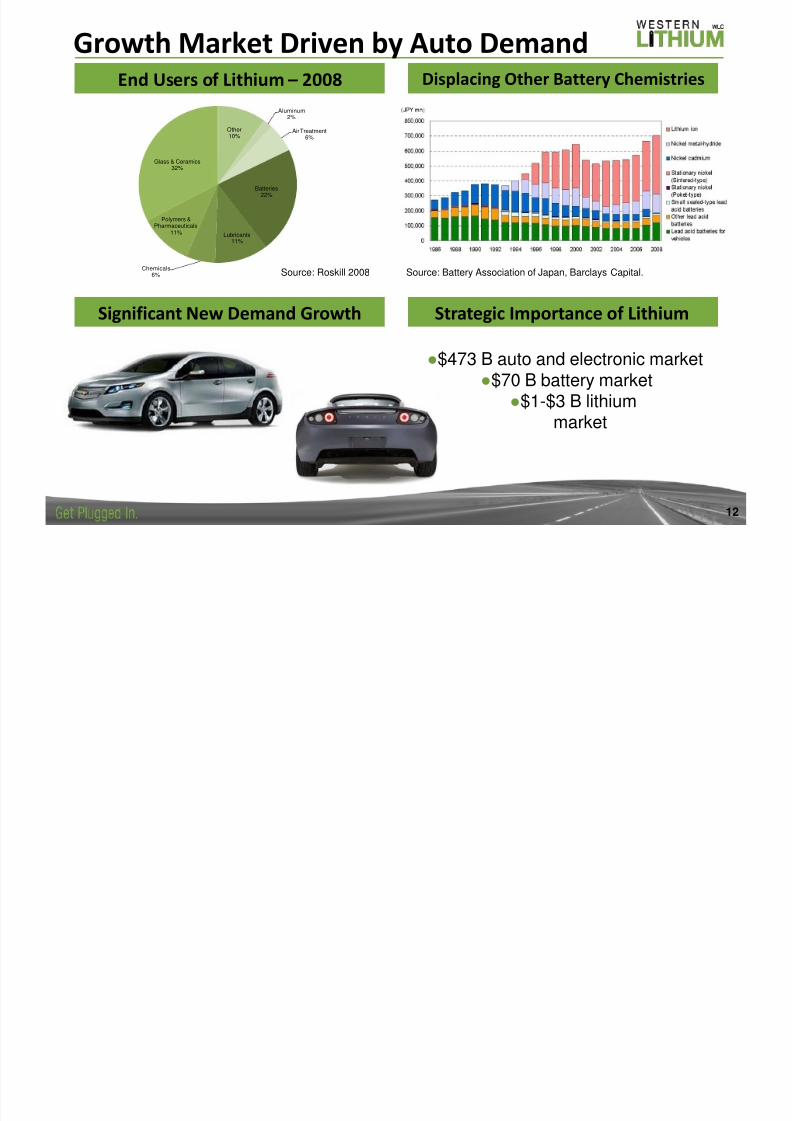

Growth Market Driven by Auto Demand

Other10%

Aluminum2%

Air Treatment6%

Batteries22%

Lubricants11%

Chemicals6%

Polymers &Pharmaceuticals

11%

Glass & Ceramics32%

Source: Roskill 2008

End Users of Lithium – 2008

Source: Battery Association of Japan, Barclays Capital.

●$473 B auto and electronic market●$70 B battery market

●$1-$3 B lithiummarket

Displacing Other Battery Chemistries

Significant New Demand Growth Strategic Importance of Lithium

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 13/37

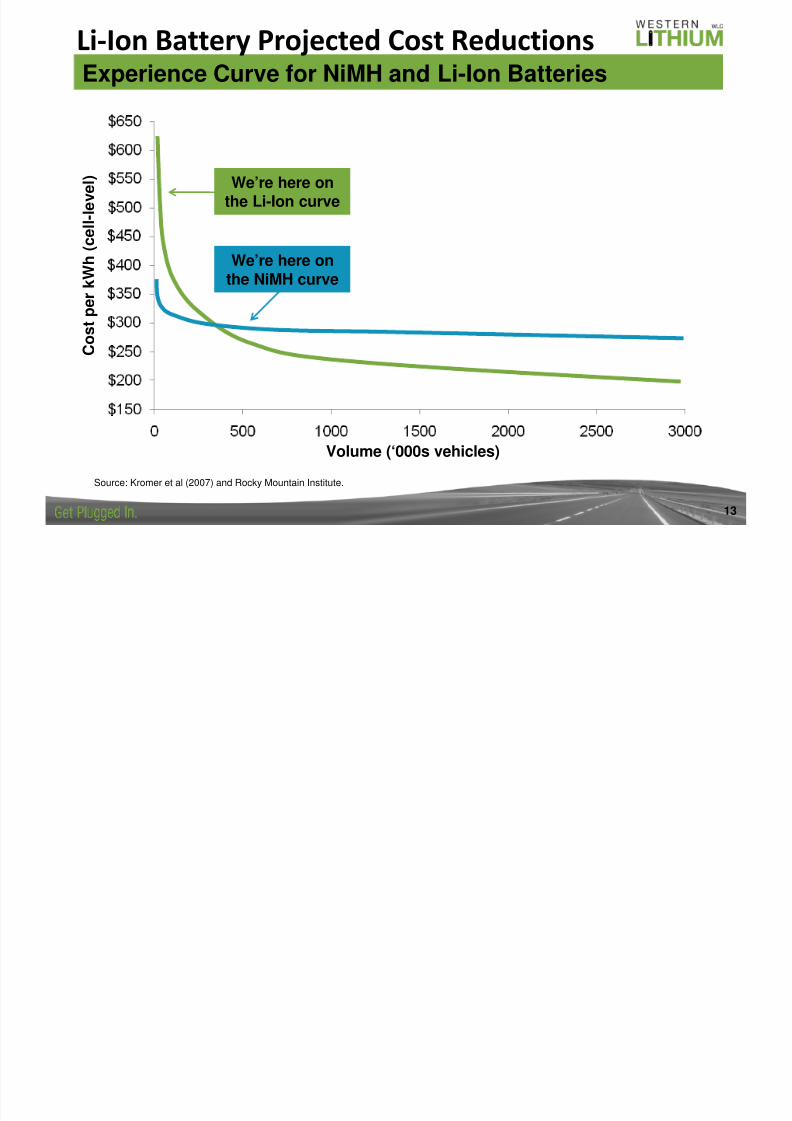

Li-Ion Battery Projected Cost Reductions

13

Experience Curve for NiMH and Li-Ion Batteries

Source: Kromer et al (2007) and Rocky Mountain Institute.

Volume (‘000s vehicles)

C o s t p e r k W h ( c e l l - l e v e l ) We’re here on

the Li-Ion curve

We’re here onthe NiMH curve

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 14/3714

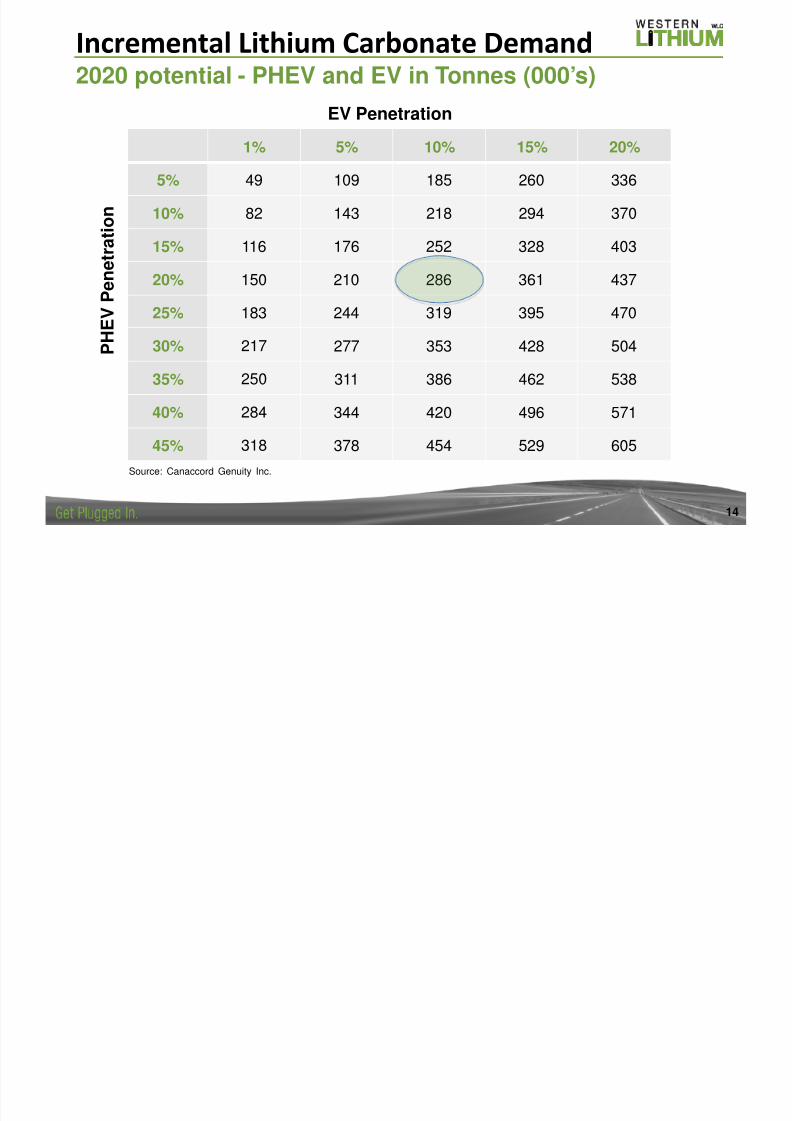

Incremental Lithium Carbonate Demand2020 potential - PHEV and EV in Tonnes (000’s)

1% 5% 10% 15% 20%

5% 49 109 185 260 336

10% 82 143 218 294 370

15% 116 176 252 328 403

20% 150 210 286 361 437

25% 183 244 319 395 470

30% 217 277 353 428 504

35% 250 311 386 462 538

40% 284 344 420 496 571

45% 318 378 454 529 605

Source: Canaccord Genuity Inc.

EV Penetration

P H E V P e n e t r a

t i o n

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 15/3715

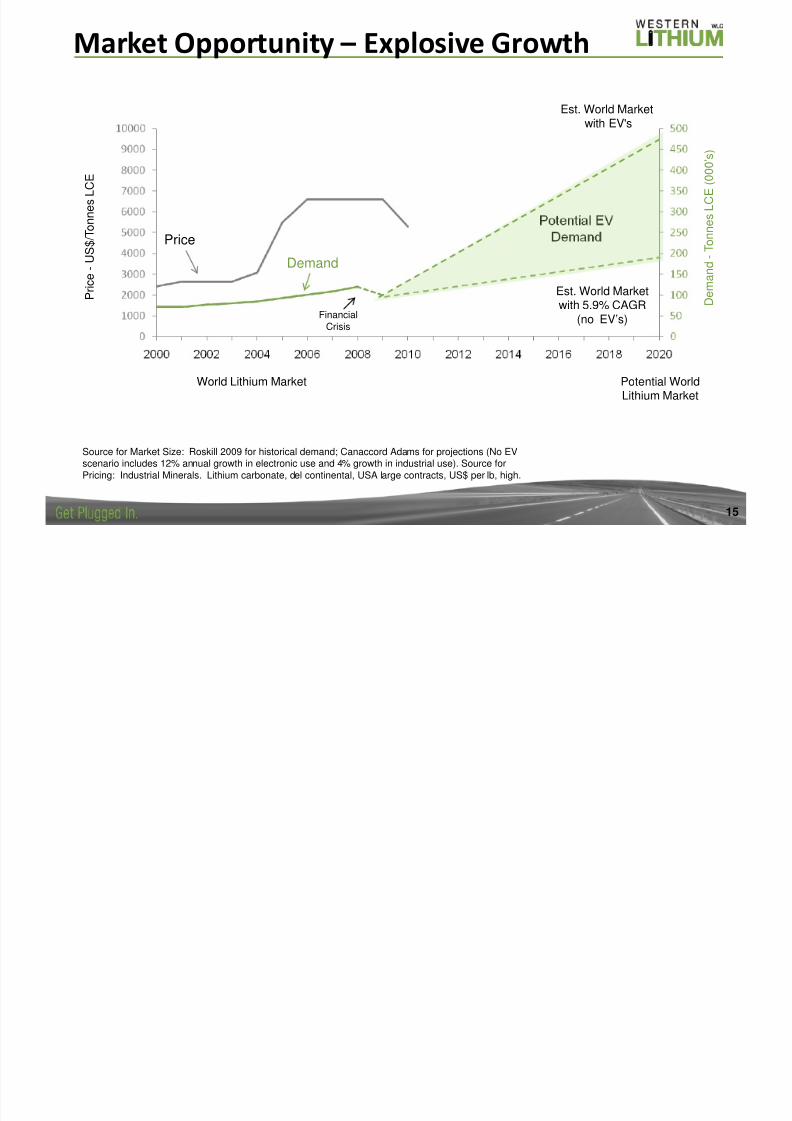

Market Opportunity – Explosive Growth

D e m a n d - T o n n e s L C E ( 0 0 0 ’ s )

World Lithium Market Potential WorldLithium Market

Source for Market Size: Roskill 2009 for historical demand; Canaccord Adams for projections (No EVscenario includes 12% annual growth in electronic use and 4% growth in industrial use). Source forPricing: Industrial Minerals. Lithium carbonate, del continental, USA large contracts, US$ per lb, high.

Est. World Market

with EV's

Est. World Marketwith 5.9% CAGR

(no EV’s)FinancialCrisis

P r i c e - U S $ / T o n n e s L C E

Price

Demand

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 16/37

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 17/37

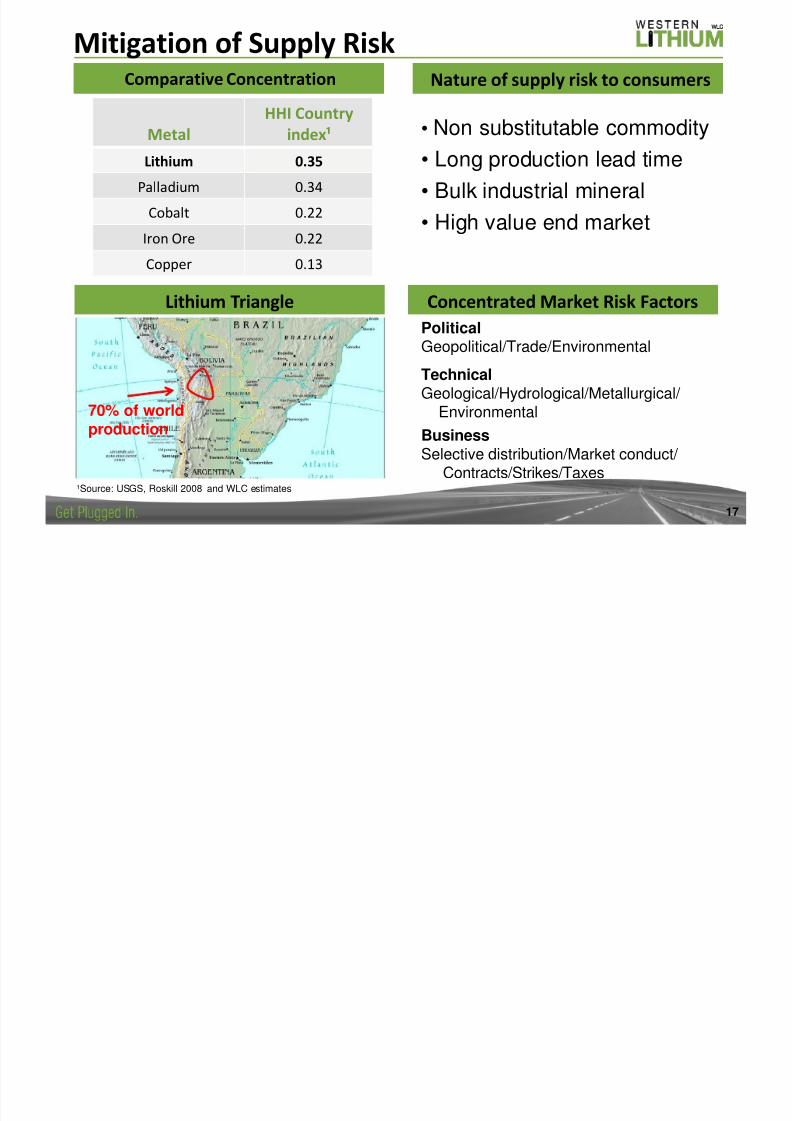

17

Mitigation of Supply RiskNature of supply risk to consumersComparative Concentration

Lithium Triangle Concentrated Market Risk Factors

PoliticalGeopolitical/Trade/Environmental

TechnicalGeological/Hydrological/Metallurgical/

Environmental

BusinessSelective distribution/Market conduct/

Contracts/Strikes/Taxes

• Non substitutable commodity• Long production lead time

• Bulk industrial mineral

• High value end market

Metal

HHI Country

index¹

Lithium 0.35

Palladium 0.34

Cobalt 0.22

Iron Ore 0.22

Copper 0.13

¹Source: USGS, Roskill 2008 and WLC estimates

70% of worldproduction

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 18/37

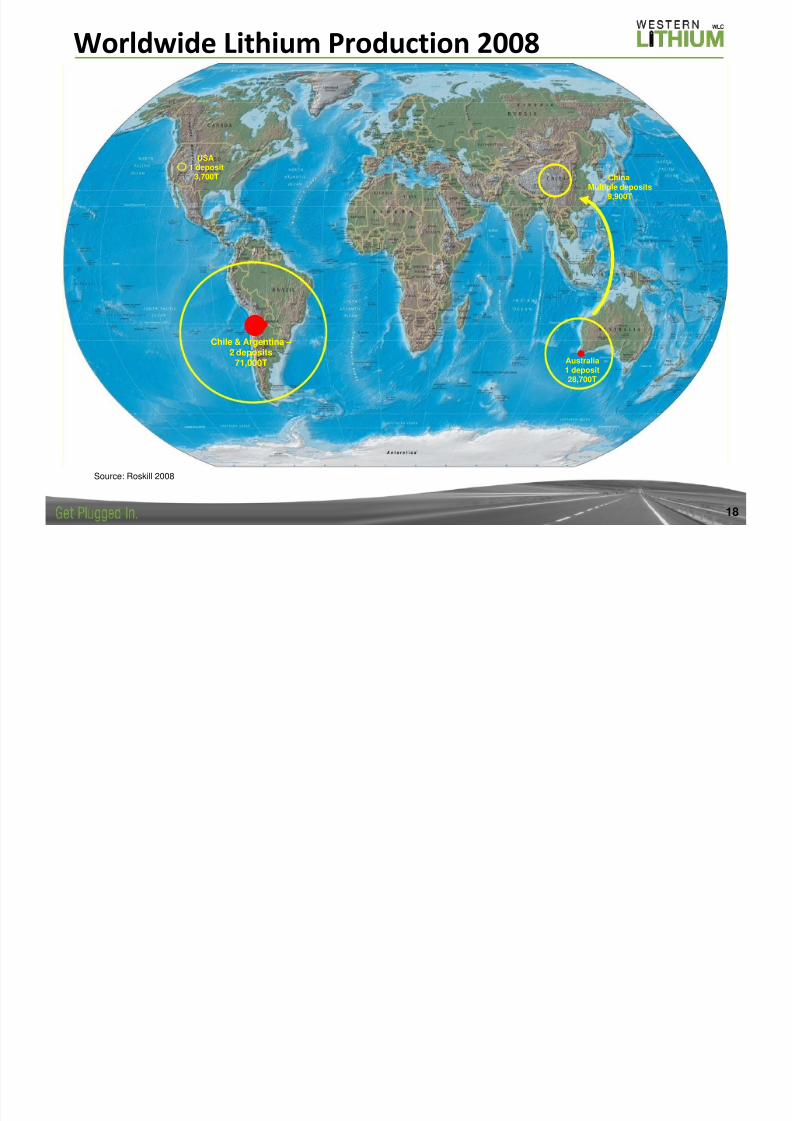

18

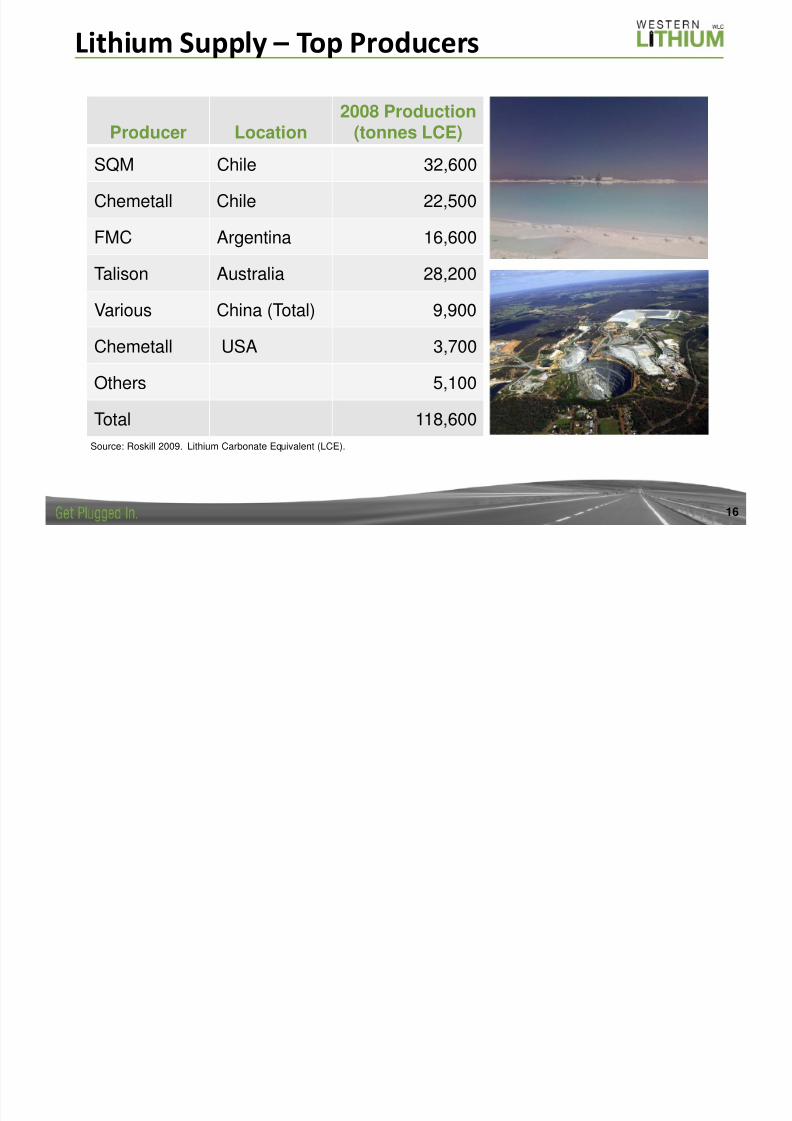

Worldwide Lithium Production 2008

Chile & Argentina –2 deposits

71,000T

USA1 deposit

3,700T

Australia

1 deposit28,700T

ChinaMultiple deposits

9,900T

Source: Roskill 2008

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 19/37

19

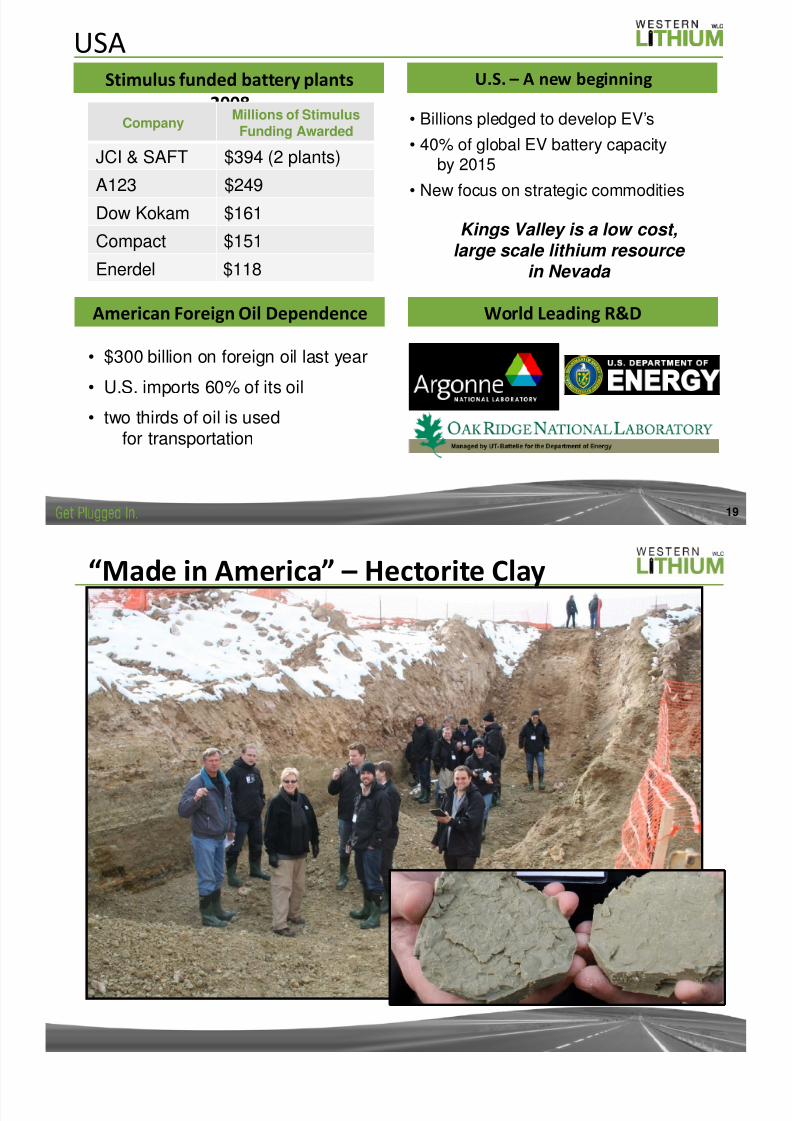

USAStimulus funded battery plants

2008

U.S. – A new beginning

American Foreign Oil Dependence World Leading R&D

• Billions pledged to develop EV’s• 40% of global EV battery capacity

by 2015

• New focus on strategic commodities

Kings Valley is a low cost,

large scale lithium resource in Nevada

CompanyMillions of StimulusFunding Awarded

JCI & SAFT $394 (2 plants)

A123 $249

Dow Kokam $161

Compact $151Enerdel $118

• $300 billion on foreign oil last year

• U.S. imports 60% of its oil

• two thirds of oil is usedfor transportation

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 20/37

“Made in America” – Hectorite Clay

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 21/37

21

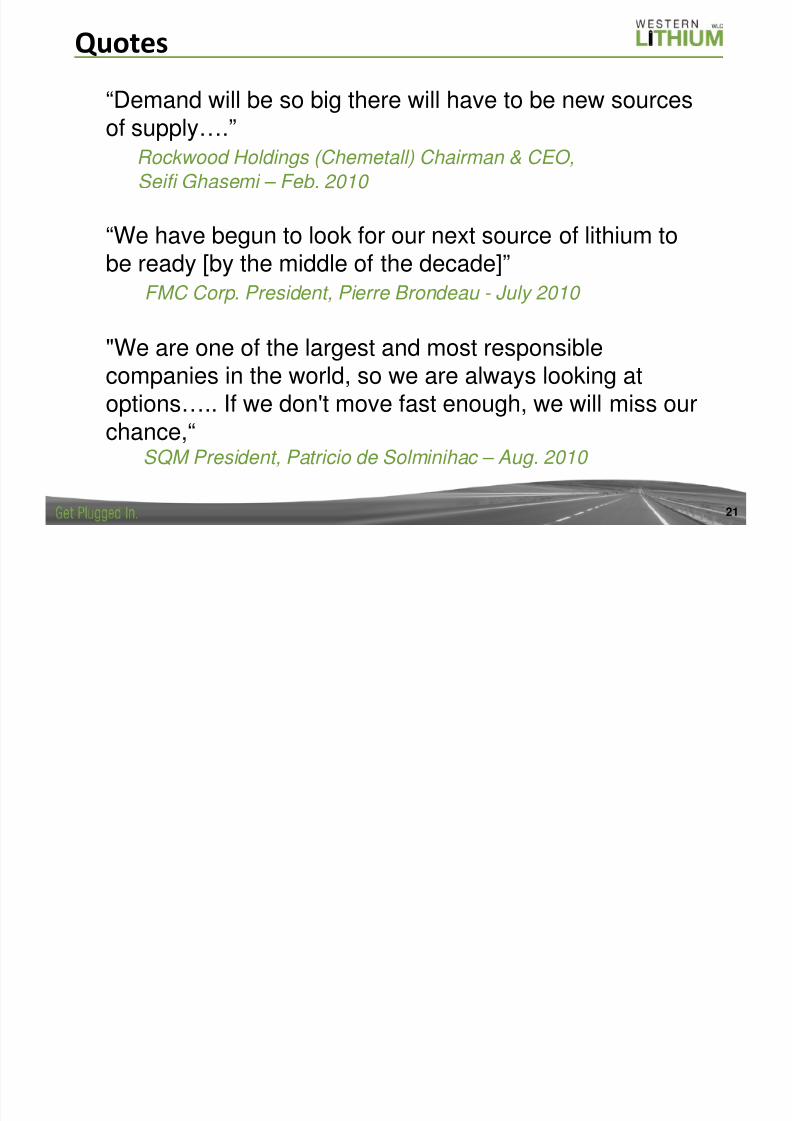

Quotes

“Demand will be so big there will have to be new sources

of supply….”Rockwood Holdings (Chemetall) Chairman & CEO,

Seifi Ghasemi – Feb. 2010

“We have begun to look for our next source of lithium tobe ready [by the middle of the decade]”

FMC Corp. President, Pierre Brondeau - July 2010

"We are one of the largest and most responsible

companies in the world, so we are always looking atoptions….. If we don't move fast enough, we will miss ourchance,“

SQM President, Patricio de Solminihac – Aug. 2010

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 22/37

22

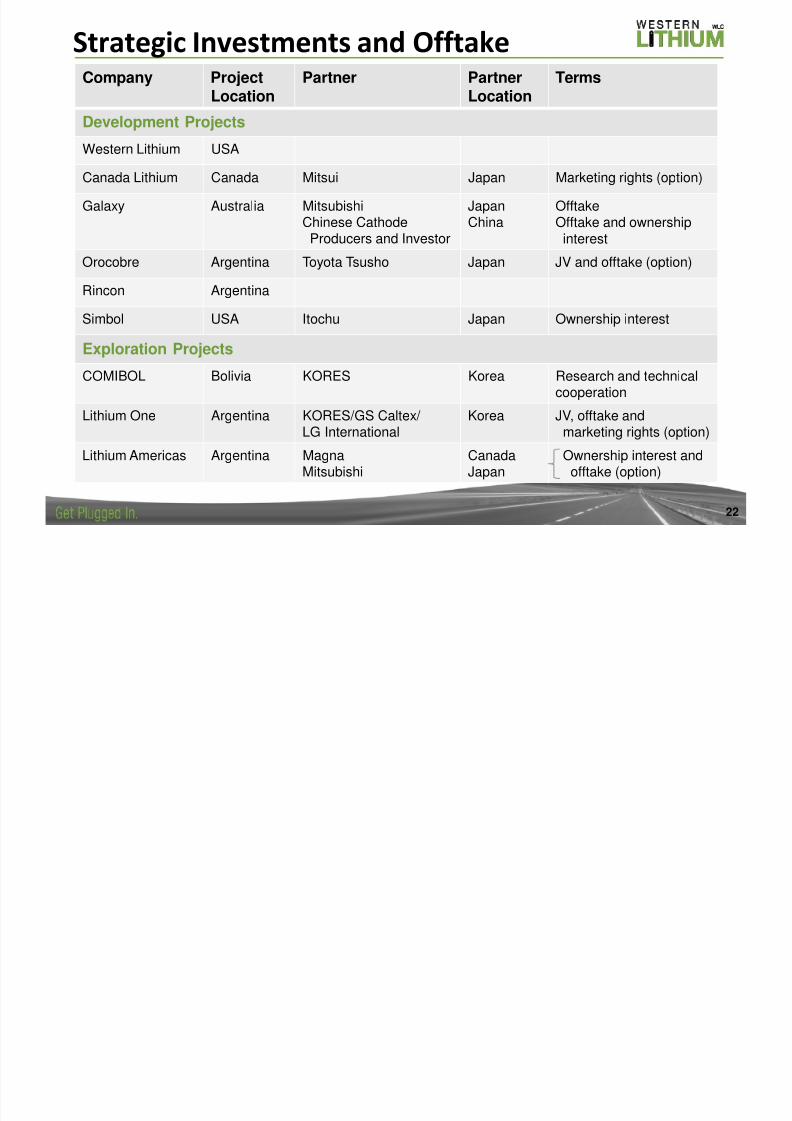

Strategic Investments and OfftakeCompany Project

LocationPartner Partner

LocationTerms

Development ProjectsWestern Lithium USA

Canada Lithium Canada Mitsui Japan Marketing rights (option)

Galaxy Australia MitsubishiChinese CathodeProducers and Investor

JapanChina

OfftakeOfftake and ownershipinterest

Orocobre Argentina Toyota Tsusho Japan JV and offtake (option)

Rincon Argentina

Simbol USA Itochu Japan Ownership interest

Exploration Projects

COMIBOL Bolivia KORES Korea Research and technicalcooperation

Lithium One Argentina KORES/GS Caltex/ LG International

Korea JV, offtake andmarketing rights (option)

Lithium Americas Argentina MagnaMitsubishi

CanadaJapan

Ownership interest andofftake (option)

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 23/37

2323

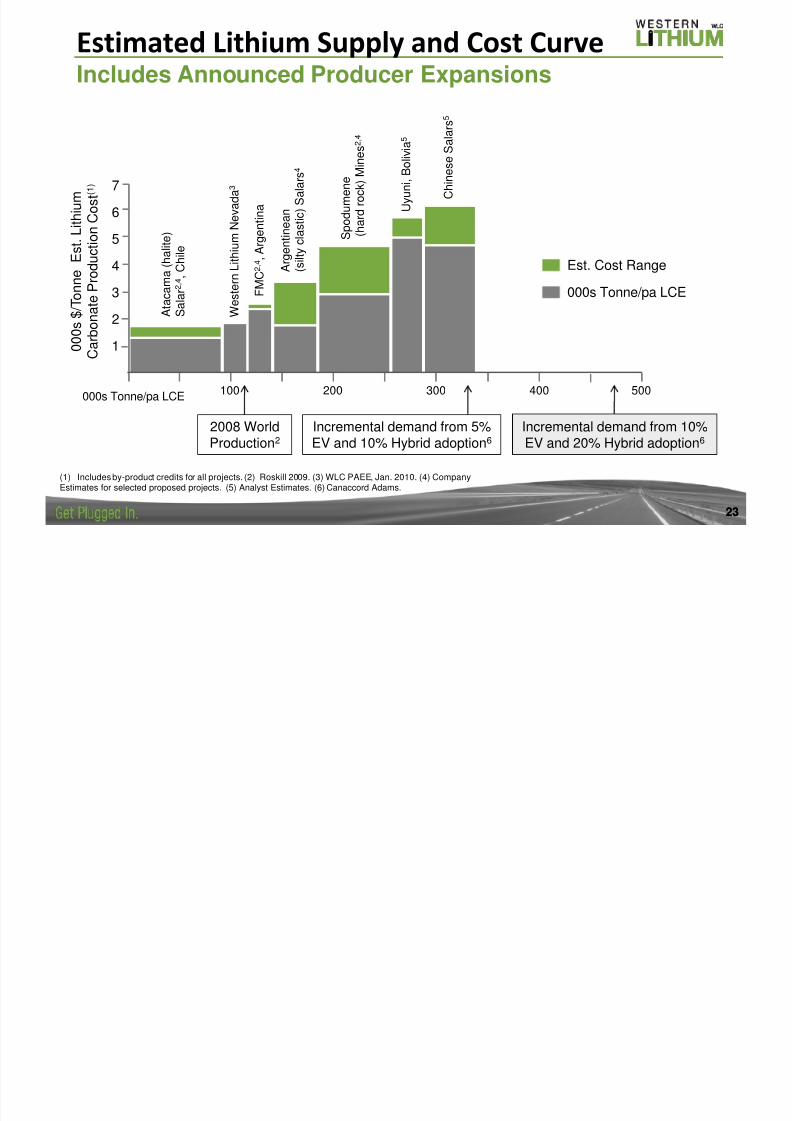

Estimated Lithium Supply and Cost CurveIncludes Announced Producer Expansions

(1) Includes by-product credits for all projects. (2) Roskill 2009. (3) WLC PAEE, Jan. 2010. (4) CompanyEstimates for selected proposed projects. (5) Analyst Estimates. (6) Canaccord Adams.

0 0 0 s $ / T o n n e E s t . L i t h i u m

C a r b o n a t e P r o d u c t i o n C o s t ( 1 )

S p o d u m e n e

( h a r d r o c k ) M i n e s 2 , 4

C h i n e s e S a l a r s

5

W e s t e r n L i t h i u

m N e v a d a 3

F M C 2 , 4 , A r g e n t i n a

A r g e n t i n e a n

( s i l t y

c l a s t i c ) S a l a r s 4

U y u n i , B o l i v i a 5

2008 WorldProduction2

Incremental demand from 5%EV and 10% Hybrid adoption6

Incremental demand from 10%EV and 20% Hybrid adoption6

Est. Cost Range

A t a c a m a ( h a l i t e )

S a l a r 2 , 4 , C h i l e

000s Tonne/pa LCE

7

6

5

4

3

2

1

400000s Tonne/pa LCE

500300200100

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 24/37

24

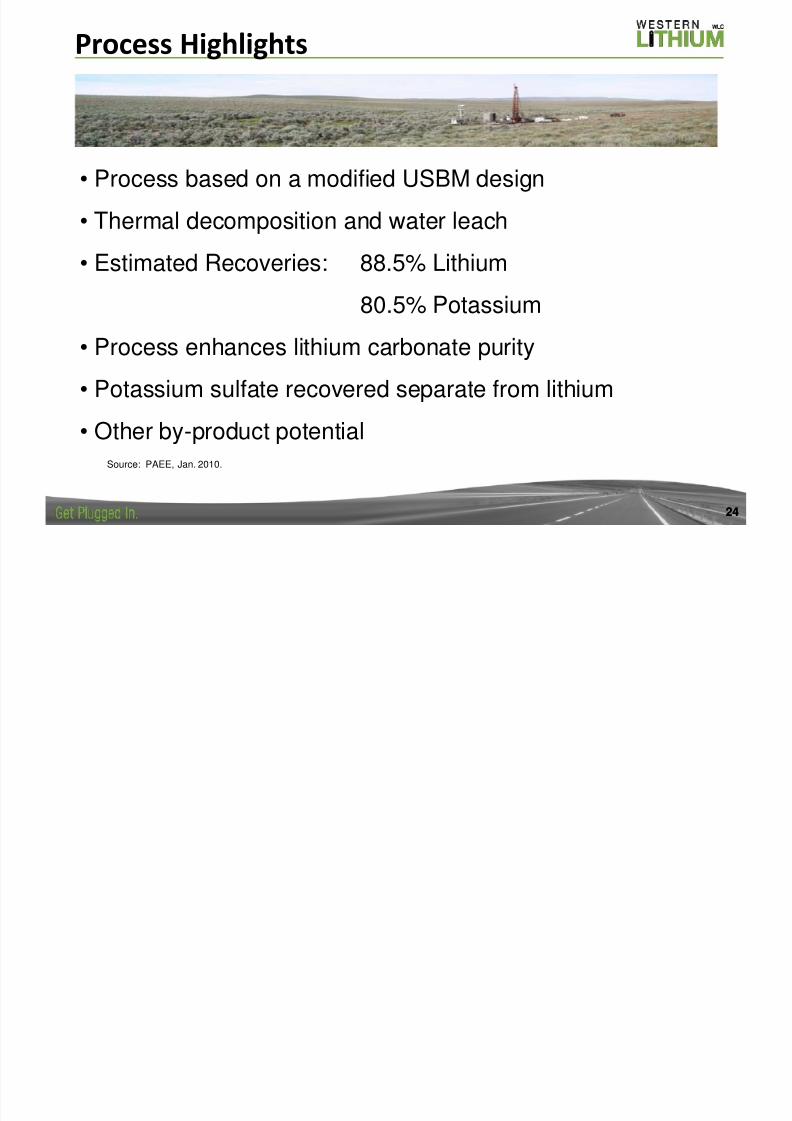

Process Highlights

24

• Process based on a modified USBM design

• Thermal decomposition and water leach

• Estimated Recoveries: 88.5% Lithium

80.5% Potassium

• Process enhances lithium carbonate purity

• Potassium sulfate recovered separate from lithium

• Other by-product potentialSource: PAEE, Jan. 2010.

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 25/37

25

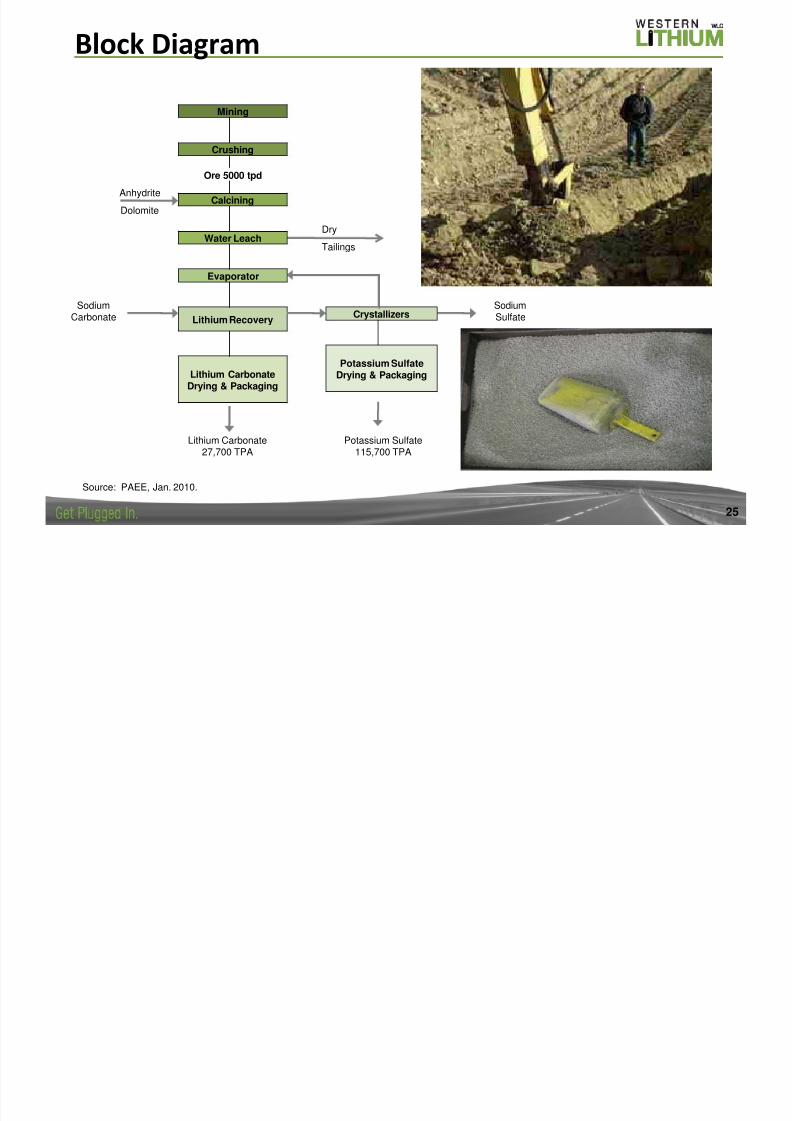

Block Diagram

Mining

Crushing

Ore 5000 tpd

Calcining

Water Leach

Evaporator

Lithium Recovery

Lithium CarbonateDrying & Packaging

Crystallizers

Potassium Sulfate

Drying & Packaging

Anhydrite

Dolomite

Dry

Tailings

SodiumCarbonate

Lithium Carbonate27,700 TPA

Potassium Sulfate115,700 TPA

SodiumSulfate

Source: PAEE, Jan. 2010.

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 26/37

26

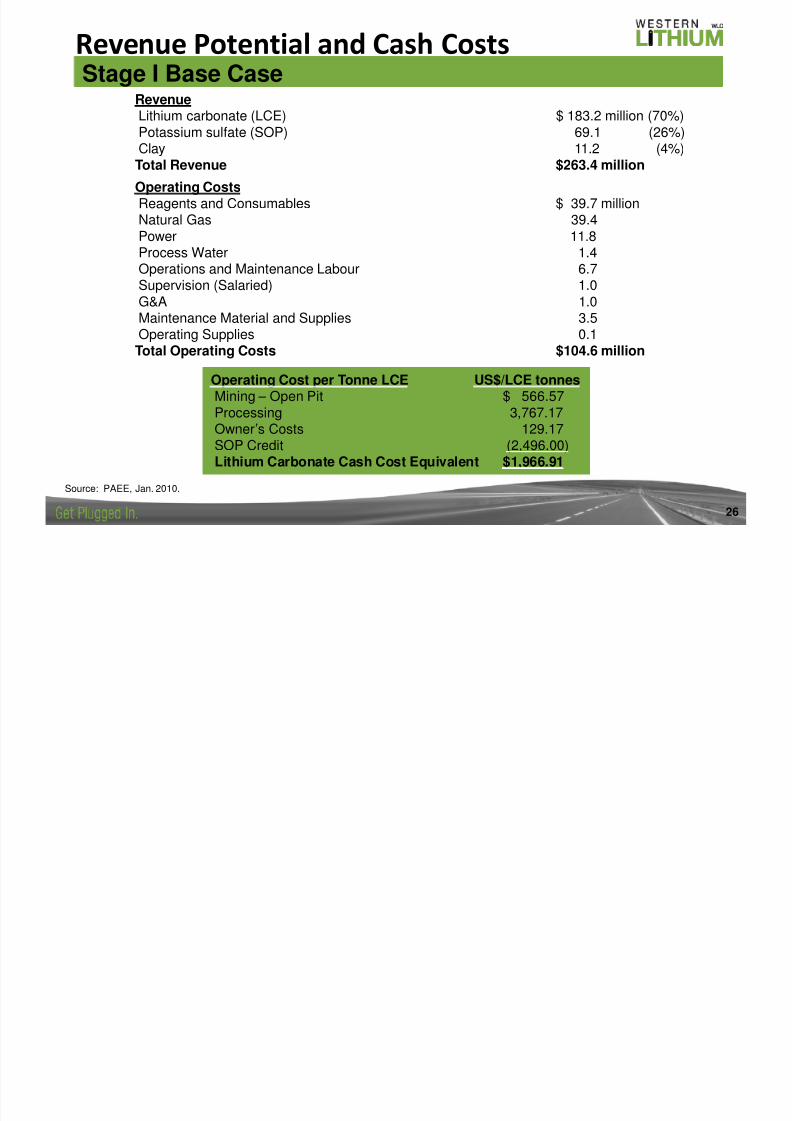

Revenue Potential and Cash CostsStage I Base Case

Source: PAEE, Jan. 2010.

RevenueLithium carbonate (LCE) $ 183.2 million (70%)Potassium sulfate (SOP) 69.1 (26%)Clay 11.2 (4%)Total Revenue $263.4 million

Operating CostsReagents and Consumables $ 39.7 millionNatural Gas 39.4Power 11.8

Process Water 1.4Operations and Maintenance Labour 6.7Supervision (Salaried) 1.0G&A 1.0Maintenance Material and Supplies 3.5Operating Supplies 0.1Total Operating Costs $104.6 million

Operating Cost per Tonne LCE US$/LCE tonnesMining – Open Pit $ 566.57Processing 3,767.17Owner’s Costs 129.17SOP Credit (2,496.00)Lithium Carbonate Cash Cost Equivalent $1,966.91

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 27/37

27

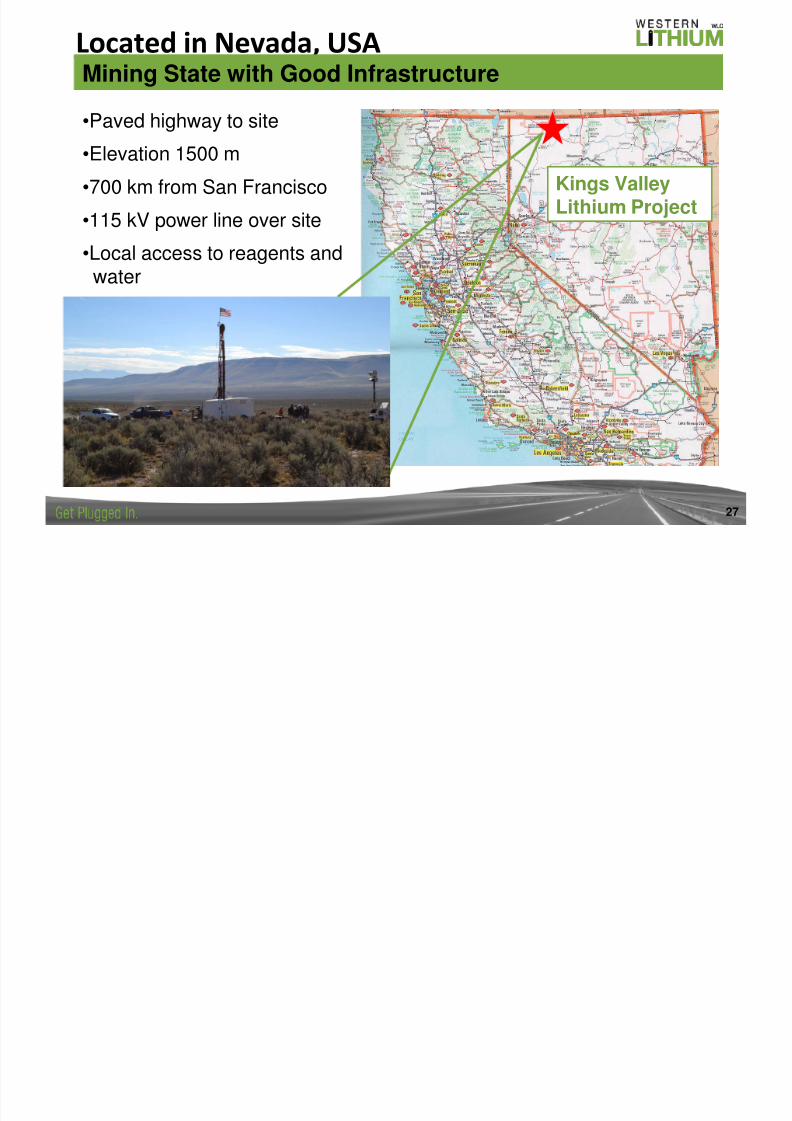

Located in Nevada, USAMining State with Good Infrastructure

Kings ValleyLithium Project

•Paved highway to site•Elevation 1500 m

•700 km from San Francisco

•115 kV power line over site

•Local access to reagents andwater

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 28/37

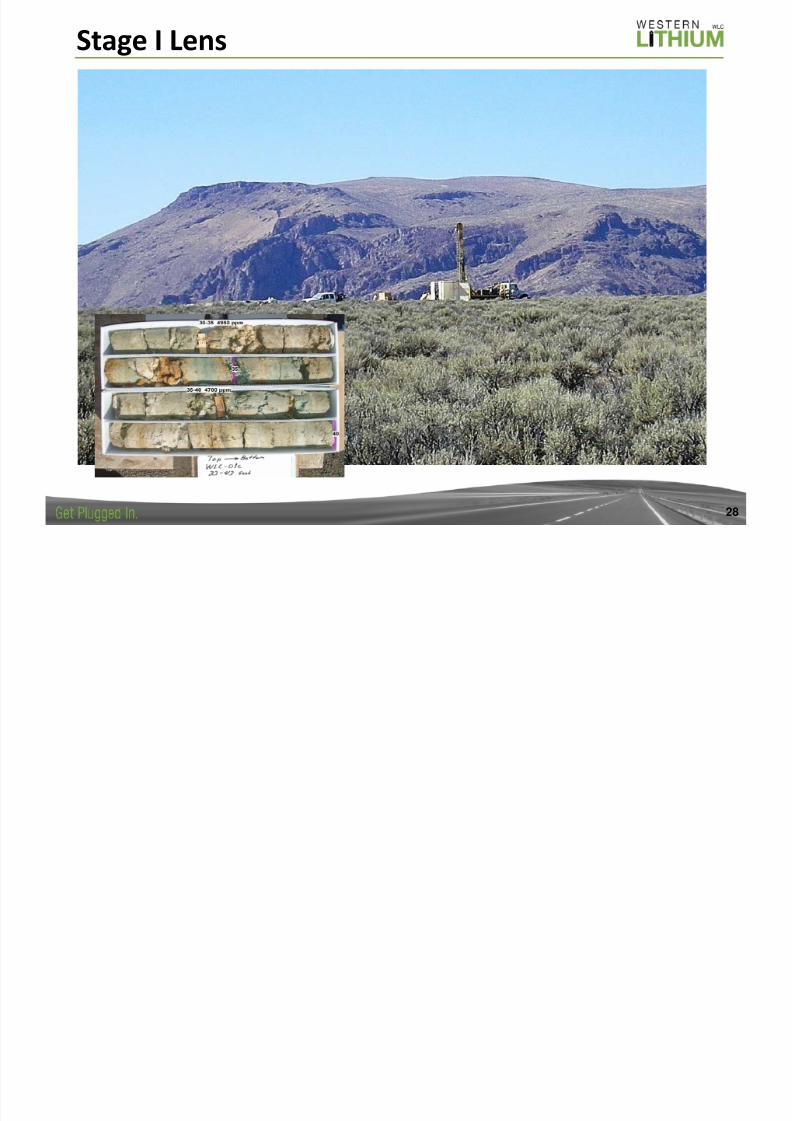

28

Stage I Lens

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 29/37

29

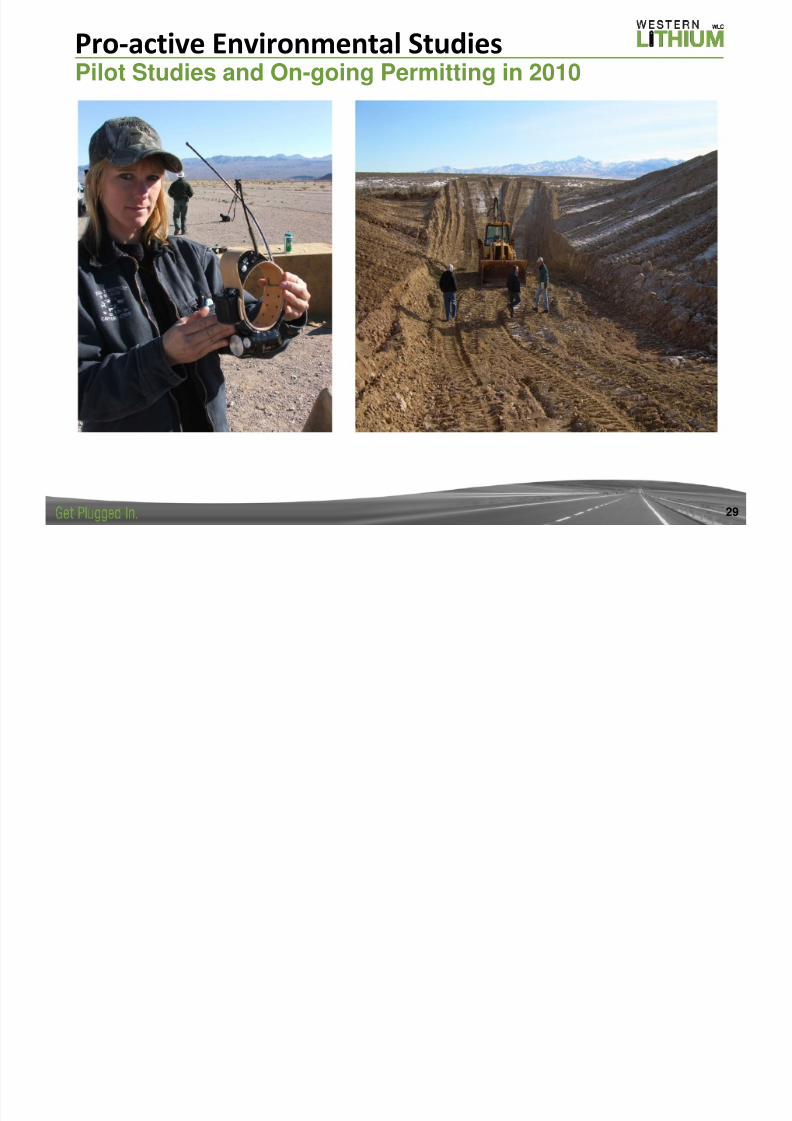

Pro-active Environmental StudiesPilot Studies and On-going Permitting in 2010

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 30/37

30

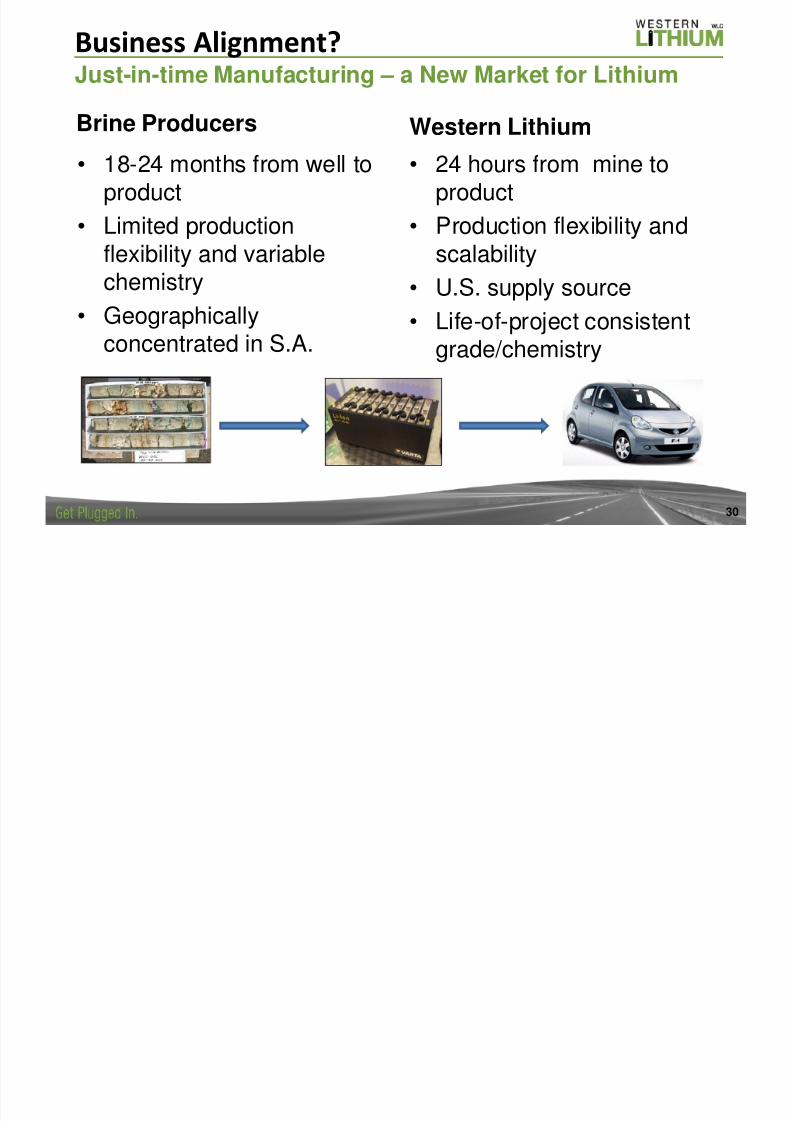

Brine Producers• 18-24 months from well to

product

• Limited production

flexibility and variablechemistry

• Geographicallyconcentrated in S.A.

Western Lithium• 24 hours from mine to

product

• Production flexibility and

scalability• U.S. supply source

• Life-of-project consistentgrade/chemistry

Business Alignment?Just-in-time Manufacturing – a New Market for Lithium

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 31/37

31

Historical Process Engineering

US Geological Survey – 1970s•Identified a rare lithium occurrence at Kings Valley

Chevron Resources – 1970s and early 1980s•Geological delineation of historical lithium lenses•Flow sheet development and economic analysis

US Bureau of Mines – 1980s

•Extractive metallurgical testing, economic studies and pilot plant

Independent Laboratories for Western Lithium – 2007/2008•Confirmatory testing of Chevron studies

Western Lithium with Independent Laboratories – 2008/2009

•Laboratory for process flow sheet development and ongoing testing

Western Lithium & Independent Engineers – 2009/2010/2011•PAEE (Scoping Study) complete, pilot production of high quality lithiumcarbonate, additional pilot production and engineering studies underway

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 32/37

Stage I Development Timeline

32

Detailed Engineering& Construction

ResourceDelineation

Pilot Testing

Permitting

Commissioning

2008 2009 2010 2011 2012 2013 2014

Engineering Scoping &Feasibility Studies

32

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 33/37

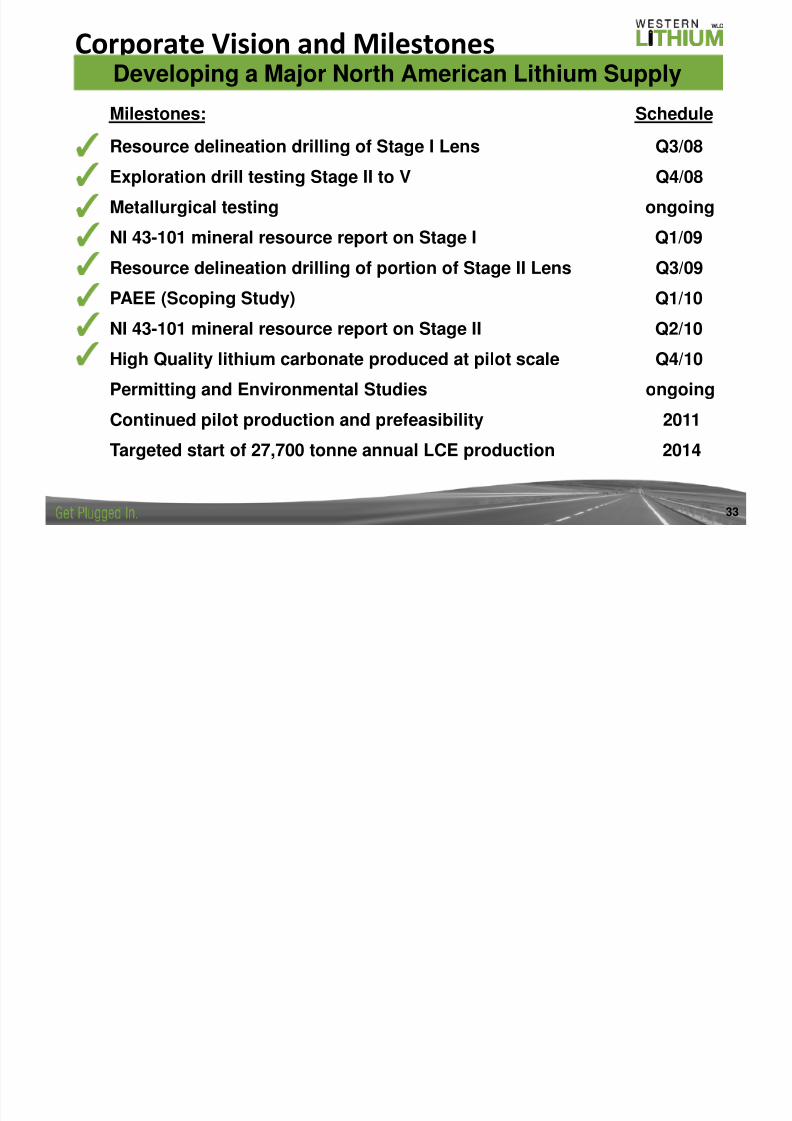

33

Corporate Vision and MilestonesDeveloping a Major North American Lithium Supply

Milestones: Schedule

Resource delineation drilling of Stage I Lens Q3/08

Exploration drill testing Stage II to V Q4/08

Metallurgical testing ongoing

NI 43-101 mineral resource report on Stage I Q1/09

Resource delineation drilling of portion of Stage II Lens Q3/09

PAEE (Scoping Study) Q1/10

NI 43-101 mineral resource report on Stage II Q2/10

High Quality lithium carbonate produced at pilot scale Q4/10

Permitting and Environmental Studies ongoing

Continued pilot production and prefeasibility 2011

Targeted start of 27,700 tonne annual LCE production 2014

✓

✓

✓

✓

✓

✓

✓

✓

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 34/37

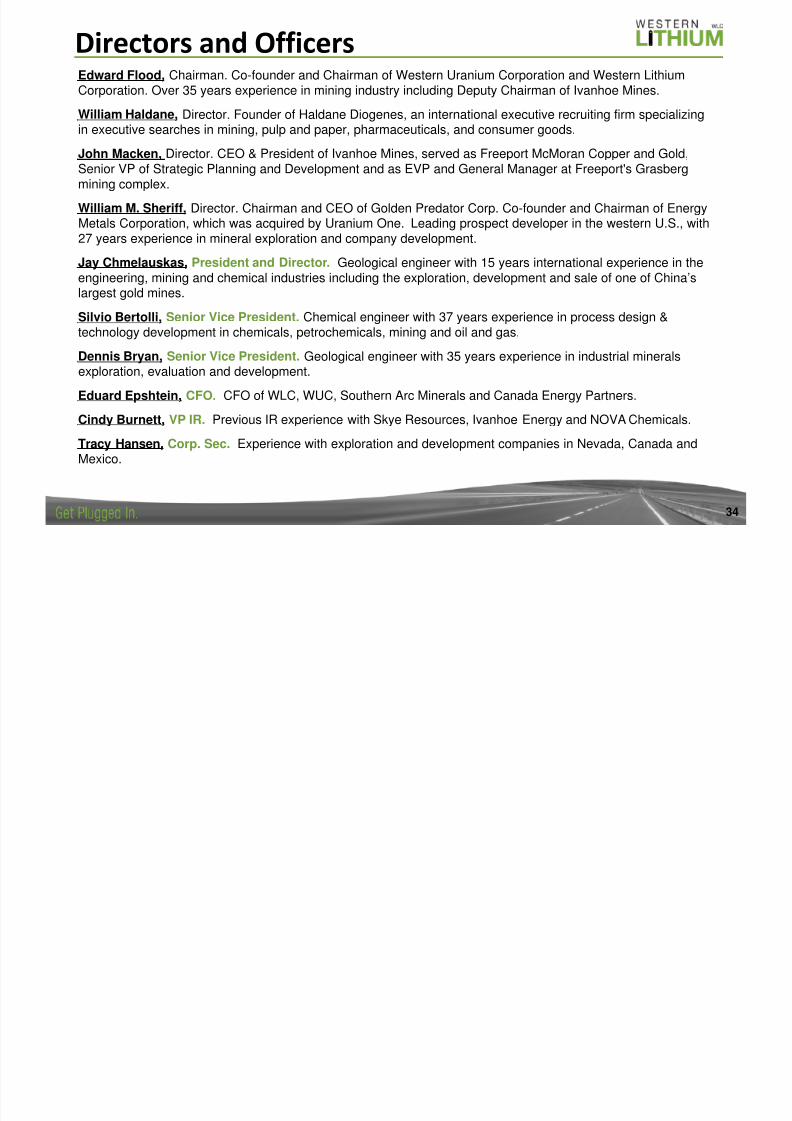

34

Directors and OfficersEdward Flood, Chairman. Co-founder and Chairman of Western Uranium Corporation and Western LithiumCorporation. Over 35 years experience in mining industry including Deputy Chairman of Ivanhoe Mines.

William Haldane, Director. Founder of Haldane Diogenes, an international executive recruiting firm specializing

in executive searches in mining, pulp and paper, pharmaceuticals, and consumer goods.

John Macken, Director. CEO & President of Ivanhoe Mines, served as Freeport McMoran Copper and Gold,Senior VP of Strategic Planning and Development and as EVP and General Manager at Freeport's Grasbergmining complex.

William M. Sheriff, Director. Chairman and CEO of Golden Predator Corp. Co-founder and Chairman of EnergyMetals Corporation, which was acquired by Uranium One. Leading prospect developer in the western U.S., with27 years experience in mineral exploration and company development.

Jay Chmelauskas, President and Director. Geological engineer with 15 years international experience in theengineering, mining and chemical industries including the exploration, development and sale of one of China’slargest gold mines.

Silvio Bertolli, Senior Vice President. Chemical engineer with 37 years experience in process design &technology development in chemicals, petrochemicals, mining and oil and gas.

Dennis Bryan, Senior Vice President. Geological engineer with 35 years experience in industrial minerals

exploration, evaluation and development.

Eduard Epshtein, CFO. CFO of WLC, WUC, Southern Arc Minerals and Canada Energy Partners.

Cindy Burnett, VP IR. Previous IR experience with Skye Resources, Ivanhoe Energy and NOVA Chemicals.

Tracy Hansen, Corp. Sec. Experience with exploration and development companies in Nevada, Canada andMexico.

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 35/37

35

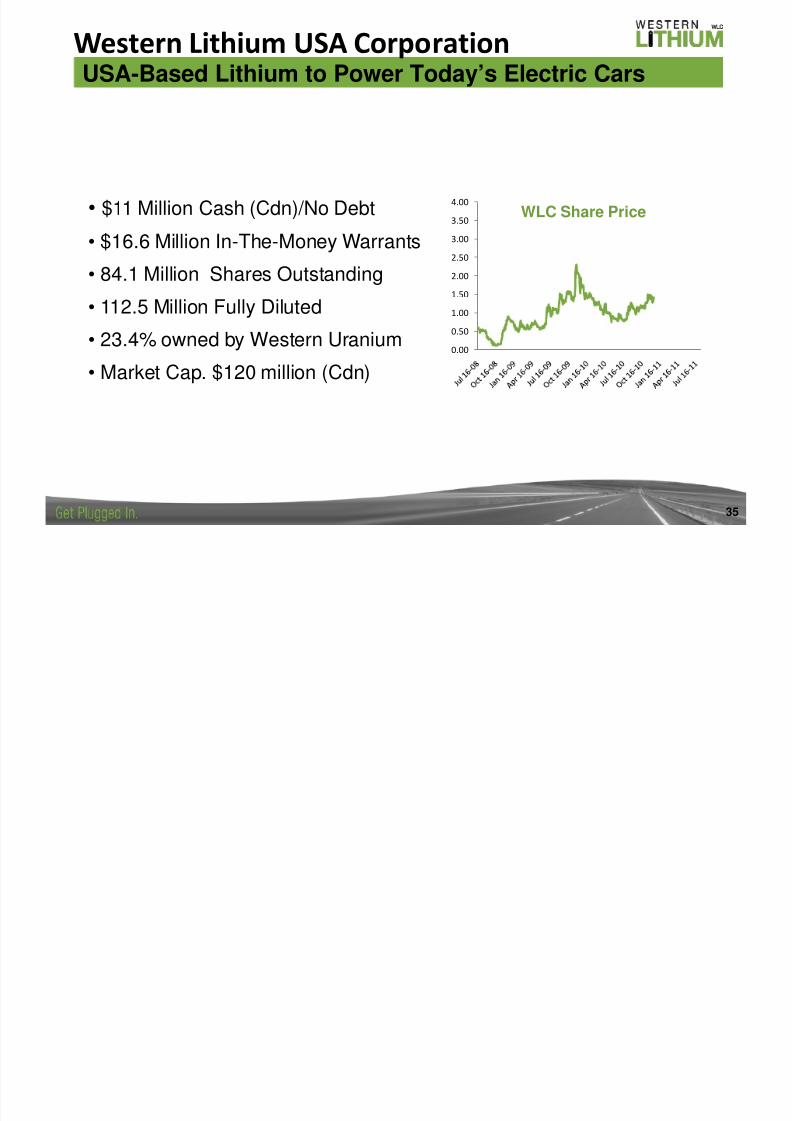

Western Lithium USA Corporation

WLC Share Price• $11 Million Cash (Cdn)/No Debt

• $16.6 Million In-The-Money Warrants• 84.1 Million Shares Outstanding

• 112.5 Million Fully Diluted

• 23.4% owned by Western Uranium

• Market Cap. $120 million (Cdn)

USA-Based Lithium to Power Today’s Electric Cars

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 36/37

36

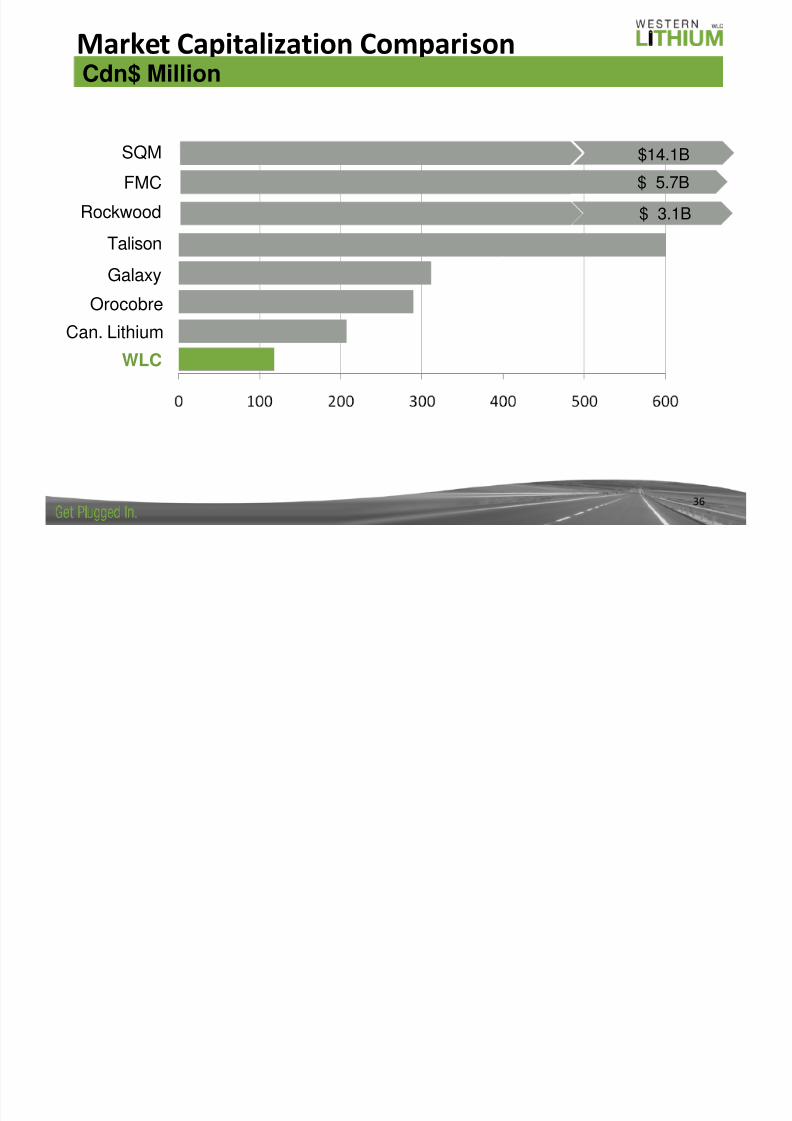

Market Capitalization ComparisonCdn$ Million

SQM

FMC

Rockwood

TalisonGalaxy

Orocobre

WLC

Can. Lithium

$14.1B

$ 5.7B

$ 3.1B

8/3/2019 WLC - Feb Website Version

http://slidepdf.com/reader/full/wlc-feb-website-version 37/37

www.westernlithium.comEmail: [email protected]

Western Lithium Investor Relations: 1-604-681-3071Exchange Symbols: TSX: WLC; OTCQX: WLCDF