A

DETAILED

PROJECT REPORT

ON

“CONSUMER BEHAVIOUR”

Submitted to RAI BUSINESS SCHOOL, New Delhi in partial

fulfillment of the requirement for the award of degree of Post

Graduate Program in Planning and Entrepreneurship

Submitted To

Prof. GUNJAN A RANA

Submitted By

MADHUSUDAN PATEL

(PGPP09A055)

Batch of JULY 2009-11 (Ind.Int.)

Specialization: Marketing

1

DECLARATION

I hereby declare that this detailed project report on “CONSUMER BEHAVIOUR” has been written and prepared by me. The project was done by me without any guidance and supervision. This is to declare that I have carried out this project work myself in partial fulfillment of the Post Graduate Program in Planning Entrepreneurship (PGPPE) Degree course of Rai Business School during 2011.

I further declare that this project is the result of my own effort and has not

been submitted to any other centre or institution or published anywhere earlier for the

award of any Diploma/Degree.

Madhusudan Patel

PGPP09A055

New Delhi

2

ACKNOWLEDGEMENT

A Project Report can’t be completed without the guidance, assistance, inspiration and

co-operation from various quarters. This study also bears the inspiration of many

persons whom I would like to acknowledge.

It is indeed of great pleasure to express my senses of gratitude & indebtness to all the

people who have been instrumental in making my project work a rich experience.

I express my sincere feelings of gratitude towards Prof. GUNJAN A RANA, who has taught me so well to make my report highly result oriented.

Last but not the least, I am grateful to all those people who have directly or indirectly

helped me in making this project a successful one.

3

TABLE OF CONTENTS

Page No.

Abstract…………….…………………………………………...-6

Chapter-1 - Introduction…………………………………..….7-13

Chapter-2 – Industry & Company Profile India Processing

Industry………………………………………....14-18

Chapter-3 – Finding And Analysis……. ……………………19-27

Chapter-4- Research Objective And Methodology….………...-28

Chapter-5- Data Analysis Interpretation………….…………29-42

Chapter-6- Conclusion & recommendation ………………..43-44

Conclusion......................................................…………………-44

Bibliography……………………………………………………-45

Appendix, Questionnaires …………………………………..46-48

4

“ADVERTISING AND CONSUMER BEHAVIOR STUDY WITH RESPECT TO ITC BINGO”

5

ABSTRACT

Around 1,000 snack items and 300 types of savories of diverse tastes, forms

textures, aromas, bases, sizes, and fillings are sold in India1. Potato chips

and potato based products are by far the largest product category with over

85 percent share of the salty snack market, followed by snack nuts, chickpea

and other pulse-based savory snacks. Popcorn, diet snacks (soy nuts, bread

sticks), breakfast cereals, baked & roasted snacks (biscuits, specialty breads,

chocolate coated snacks, cookies etc.) and cheese snacks are in high

demand across organized retail chains. Health foods, health food

supplements and convenient foods are also rapidly growing segments.

The present study was undertaken to analyze the impact and role of

advertising in the Consumer behavior towards “ITC-Bingo”.

In the branded snacks market, to get down to basics, Frito Lay commands a

share of 45%, followed by Haldiram’s at 27% and ITC at 16%. The rest is

divided between a handful of new entrants, wannabes and many regional

players. Out of these ITC’s Bingo is a new entrant in the market, which was

launched in 2007. ITC has launched Bingo in a wide variety of flavors and

formats, ranging from potato chips to finger snacks. Because of its different

and catchy advertisements Bingo has created a buzz in the market.

Therefore, my aim was to find out the most popular flavor of Bingo among all

the offerings. The analysis was undertaken by dividing people into those who

like to eat snacks and those who don’t. The study is based on the survey of

people who like to eat snacks. To collect the data a questionnaire was

designed and the survey was conducted in Delhi.

6

CHAPTER-1

INTRODUCTION

Snacks are a part of Consumer Convenience/ Packaged Foods segment.

Snack is described as a small quantity of food eaten between meals or in

place of a meal. Snack food generally comprises bakery products, ready-to-

eat mixes, chips, namkeen and other light processed foods According to the

ministry of food processing, the snack food industry is worth Rs. 100 billion in

value and over 4,00,000 tonnes in terms of volume. Though very large and

diverse, the snacks industry is dominated by the unorganized sector.

According to an APEDA survey almost 1,000 snack items and 300 types of

savouries are sold across India. The branded snacks are sold at least 25%

higher than the unbranded products. Savoury snacks have been a part of

Indian food habit, since almost ages. Though there is no particular time for

snacks, normally they are consumed at teatime. The variety is almost mind-

boggling with specialties from all regions, which have gained national

acceptance.

The industry has been growing around 10% for the last three years, while the

branded segment is growing around 25% per annum to stand at Rs 5,000-Rs

5,500 crore, due to various reasons like Multiplex culture, snacking at home

while watching TV, pubs and bars (where they are served free). AC Nielsen's

retail audit shows that the large sales volumes are due to a marked

preference for ethnic foods, regional bias towards indigenous snacks and

good value-for-money perception. Of course the branded segment is much

smaller at Rs 2,200 crore, which is what makes it so attractive to food

Companies that are looking at bigger shares. As per an industry estimate, the

branded and organized snack food segment dominated by major players such

as Frito Lay, Con Agra, Kellogg’s, Marico, Dabur, HLL, ITC, Parle, Haldiram’s,

Nestle, Britannia, Cadbury, Bikano and Balaji is estimated to grow by 15 to 20

percent per year; whereas the growth of un-branded snack food is likely to

grow modestly at 8 percent per year in the near future (table 1).

7

Product pricing for branded products are normally 15 to 20 percent greater

than for the un-branded food segment due to higher overhead expenses.

Snack food packaging ranges from 35/40 gm sachets to 400 gm economy

packs. Small packs work very well in India.

Table 1: Overview of the Indian Snack Food Business

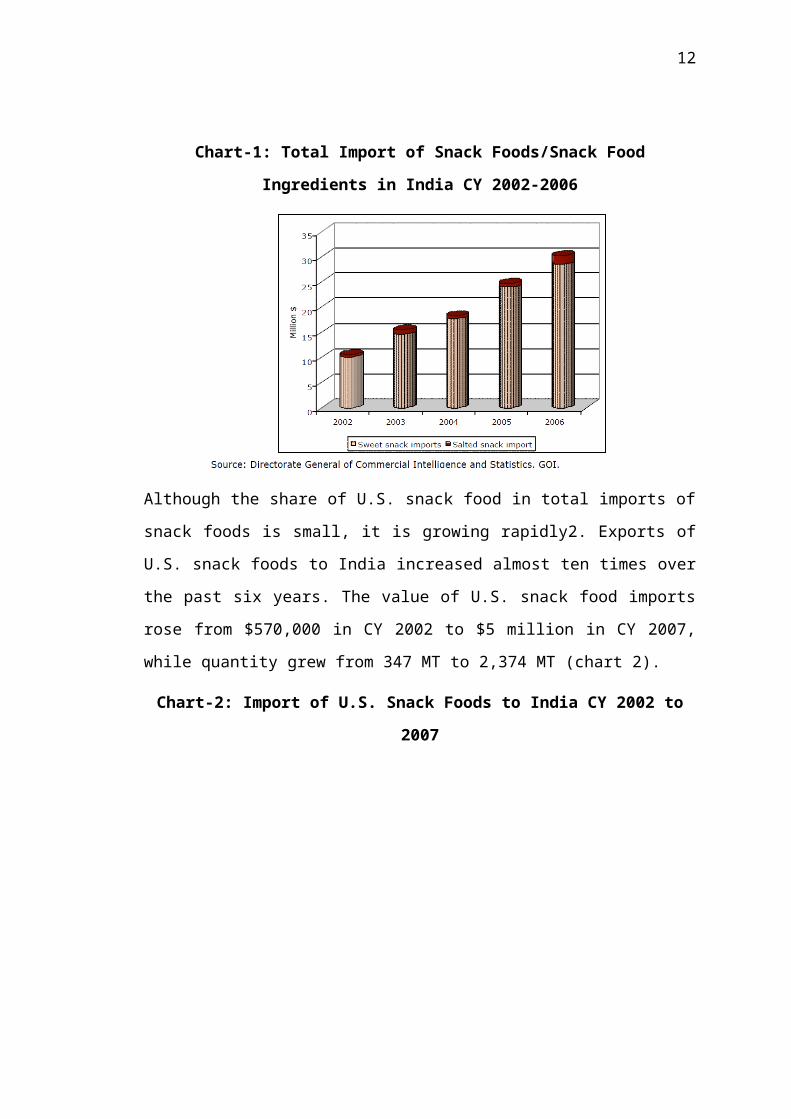

Import Market

India’s imports of snacks/snack food ingredients rose from $10 million in CY

2002 to $30 million in CY 2006 (chart 1). Food items under the sweet snack

category constituted the major share of imports and imports rose from $10

million to $29 million (94 percent of total imports in CY 2006). Major exporters

of snack foods/food ingredients to India are the United States, Malaysia,

Indonesia, Thailand, China, Singapore, South Korea, Switzerland, UAE,

Australia, U.K., Germany, South Africa and Portugal.

8

Chart-1: Total Import of Snack Foods/Snack Food Ingredients in India

CY 2002-2006

Although the share of U.S. snack food in total imports of snack foods is small,

it is growing rapidly2. Exports of U.S. snack foods to India increased almost

ten times over the past six years. The value of U.S. snack food imports rose

from $570,000 in CY 2002 to $5 million in CY 2007, while quantity grew from

347 MT to 2,374 MT (chart 2).

Chart-2: Import of U.S. Snack Foods to India CY 2002 to 2007

9

The value of U.S. salted snacks increased from $429,000 in CY 2002 to $3

million in CY 2007; however its share in total imports of U.S. snack foods

declined from 75 to 60 percent in CY 2007. Meanwhile, the value of sweet

snacks increased from $141,000 in CY 2002 to $ 1.82 million in CY 2007, with

its share of total U.S. snack food imports growing from 22 to 37 percent in CY

2007 (chart 3).

Chart-3: Import of U.S. Sweet and Salted Snacks CY 2002 to 2007

Snack foods that registered significant growth in U.S. exports from CY 2002 to

CY 2007 were potato chips (prepared/preserved), confectionery (containing

sweetening agent instead of sugar), popcorn (microwaveable package & ex

seed), confectionary, sweetmeats (without containing cocoa), chewing gum

(whether or not sugar coated), cookies (sweet biscuits), corn chips and similar

crisp savory snacks.

In CY 2007 potato chips, confectionary and popcorn constituted almost 68

percent of India’s snack food imports from the United States. Imports of potato

chips rose from

$332,000 in CY 2002 to $2 million in CY 2007, popcorn rose from $454,000 to

$936,000 and confectionary (sweetening agent) rose from $70,000 to

$253,000 (chart 4).

10

The market for frozen snack foods is limited due to lack of refrigerated

warehousing and transportation facilities. Imported food items are largely

confined to organized retail and grocery stores, catering mostly to high end

consumers.

Chart-4: Major U.S. Snack Foods Imported to India CY 2002 to 2007

Most U.S. products are trans-shipped through regional hubs, such as Dubai

and Singapore, due to their more liberal trade policies, efficient handling, and

reduced transport times. Transport time from California to India is at least 30

days, and in some cases as long as 45 days. The primary points of entry are

Mumbai followed by Chennai and Calcutta. Container handling facilities are

available at most major ports and in several cities.

11

Table 2: Indian / Multi-national Companies in the Snack Food Segment

In this research we intended to find out the most popular flavor of BINGO in

the market from the selected sample. Snacks as such are a very minor part of

the food processing industry because snacks sector is largely unorganized.

The project purports to decipher the satisfaction level as well as the

preferences of consumers pertaining to the various flavors of BINGO- a new

range of savory snacks launched by ITC. The aim was to analyze the

success, marketability and future growth prospects of BINGO. The aim was

also to study the spending habits and motivation of consumers for buying

snacks.

12

For this a survey was conducted in Delhi where respondents were asked to fill

a questionnaire. The data was collected and analyzed to obtain conclusions.

This report carries an introduction of the company profile, detail of the

methodology followed detailed data analysis and the results so obtained with

the variety of graphs along with given.

13

CHAPTER-2

INDUSTRY & COMPANY PROFILE

INDIAN FOOD PROCESSING INDUSTRY

Food processing industry in India is a sunrise sector that has gained

prominence in the recent years. Availability of raw materials, changing

lifestyles and relaxation in policies has given a considerable push to the

industry’s growth. This sector is among the few that serves as a vital link

between the agriculture and industrial segments of the economy.

Strengthening this link is of critical importance to improve the value of

agricultural produce; ensure remunerative prices to farmers and at the same

time create favorable demand for Indian agricultural products in the world

market. A thrust to the food processing sector implies significant development

of the agriculture sector and ensures value addition to it.

Ministry of Food Processing Industries

The Ministry was set up in 1998 and the industry segments that come under

its purview are:

Fruit & Vegetable processing (including freezing and dehydration)

Grain Processing

Processing of Fish (including canning and freezing)

Processing and refrigeration of certain agricultural products, dairy

products, poultry and eggs, meat and meat products

Industries related to bread, oilseeds, meals (edible), breakfast foods,

biscuits, confectionery, savory snacks, malt extract, protein isolate,

high protein food, weaning food and extruded food products (including

other ready-to-eat foods)

Beer, including non-alcoholic beer

Alcoholic drinks from non-molasses base

14

Aerated water and soft drinks

Specialized packaging for food processing industries.

The Ministry of Food Processing Industries, GoI, has estimated the size of the

Indian food market at US$ 191 bn (Rs 8,600 bn). The processed food market

is projected to be over US$ 100 bn, of which the primarily processed food

market accounts for 60%, while the value-added processed food market is

around 40%.

The average annual growth of the food processing industry has been around

8% between FY01-FY06. The segments that have driven the growth are the

beverages and meat & meat products and processed fish sectors. The food

processing industry in India has a share of 1.5% in the total GDP of the

country, and as part of total manufacturing accounts for 9%. India’s share in

world trade in respect of processed food is about 1.6%.

An extensive and highly fragmented industry, the food processing sector

largely comprises of the following sub-segments: fruits & vegetables, milk and

milk products, beer & alcoholic beverages, meat and poultry, marine products,

grain processing, packaged/convenience food and packaged drinks. A large

number of players in this industry are small sized companies, and are largely

concentrated in the unorganized segment. This segment accounts for more

than 70% of the output in volume terms and 50% in value terms. However,

though the organized sector is comparatively small, it is growing at a much

faster pace

15

INDIAN SNACKS INDUSTRY:

Snacks are a part of Consumer Convenience/ Packaged Foods segment.

Snack is described as a small quantity of food eaten between meals or in

place of a meal. Snack food generally comprises bakery products, ready-to-

eat mixes, chips, namkeen and other light processed foods According to the

ministry of food processing, the snack food industry is worth Rs 100 billion in

value and over 4,00,000 tonnes in terms of volume.Though very large and

diverse, the snacks industry is dominated by the unorganized sector.

According to an Apeda survey almost 1,000 snack items and 300 types of

savouries are sold across India. The branded snacks are sold at least 25%

higher than the unbranded products. Savoury snacks have been a part of

Indian food habit, since almost ages. Though there is no particular time for

snacks, normally they are consumed at teatime. The variety is almost mind-

boggling with specialties from all regions, which have gained national

acceptance.

The industry has been growing around 10% for the last three years, while the

branded segment is growing around 25% per annum to stand at Rs 5,000-Rs

5,500 crore, due to various reasons like Multiplex culture, snacking at home

while watching TV, pubs and bars (where they are served free). AC Nielsen's

retail audit shows that the large sales volumes are due to a marked

16

preference for ethnic foods, regional bias towards indigenous snacks and

good value-for-money perception. Of course the branded segment is much

smaller at Rs 2,200 crore, which is what makes it so attractive to food

Companies that are looking at bigger shares. In the branded snacks market,

to get down to basics, Frito Lay commands a share of 45%, followed by

Haldiram’s at 27% and ITC at 16%. The

rest is divided between a handful of new entrants, wannabes and many

regional players.

Of the wide range of snacks available, potato chips constitute a sizeable

segment of the Indian snack food industry, according to India Infoline. The

potato chip market is generally an unorganized industry. Nearly all potato chip

snack products are manufactured and sold locally. There is also no uniform

standard for packaging, as there is in Europe, the United States and other

more developed regions. Many snack foods are sold loose or packaged in

poly-pouches, which may only be folded, or in some cases, stapled closed. As

the Indian economy continues to grow, and production standards improve,

many snack food companies are making significant investments into plant

equipment and packaging machinery.

Pepsi Foods Ltd., now known as Frito-Lay India Ltd., produces India's largest

snack food manufacturers brands, including Ruffles, Hostess, Cheetos and

Uncle Chips. Frito Lay's story is an example of how American recipes were

adjusted to satisfy local tastes. Procter & Gamble's Pringles brand of potato

crisp was launched in Delhi in 1999. Pringles is also a baked potato crisp,

unlike many other potato based Indian snack foods that are fried. P&G

currently imports the Pringles product and therefore the product has been

priced at a premium and is marketed to a micro-niche.

SWOT Analysis of Snacks Industry

Strengths

Abundant availability of raw material

Vast network of manufacturing facilities all over the country

17

Vast domestic market

Urbanisation

Weaknesses

Low availability of adequate infrastructural facilities

Lack of adequate quality control & testing methods as per international

standards

Inefficient supply chain due to a large number of intermediaries

High requirement of working capital

Opportunities

Rising income levels and changing consumption patterns

Favourable demographic profile and changing lifestyles

Integration of development in contemporary technologies such as

electronics, material science, bio-technology etc. offer vast scope for

rapid improvement and progress

Opening of global markets

Threats

Affordability and cultural preferences of fresh food

High inventory carrying cost

High taxation

High packaging cost

Competition between national and regional players.

18

CHAPTER-3

FINDINGS AND ANALYSIS

Snacks are a part of Consumer Convenience/ Packaged Foods segment.

Snack is described as a small quantity of food eaten between meals or in

place of a meal. Snack food generally comprises bakery products, ready-to-

eat mixes, chips, namkeen and other light processed foods According to the

ministry of food processing, the snack food industry is worth Rs 100 billion in

value and over 4,00,000 tonnes in terms of volume.

Though very large and diverse, the snacks industry is dominated by the

unorganized sector. According to an Apeda survey almost 1,000 snack items

and 300 types of savouries are sold across India. The branded snacks are

sold at least 25% higher than the unbranded products. Savoury snacks have

been a part of Indian food habit, since almost ages. Though there is no

particular time for snacks, normally they are consumed at teatime. The variety

is almost mind-boggling with specialties from all regions, which have gained

national acceptance.

The industry has been growing around 10% for the last three years, while the

branded segment is growing around 25% per annum to stand at Rs 5,000-Rs

5,500 crore, due to various reasons like Multiplex culture, snacking at home

while watching TV, pubs and bars (where they are served free). AC Nielsen's

retail audit shows that the large sales volumes are due to a marked

preference for ethnic foods, regional bias towards indigenous snacks and

good value-for-money perception. Of course the branded segment is much

smaller at Rs 2,200 crore, which is what makes it so attractive to food

Companies that are looking at bigger shares. In the branded snacks market,

to get down to basics, Frito Lay commands a share of 45%, followed by

Haldiram’s at 27% and ITC at 16%. The rest is divided between a handful of

new entrants, wannabes and many regional players.

Of the wide range of snacks available, potato chips constitute a sizeable

segment of the Indian snack food industry, according to India Infoline. The

19

potato chip market is generally an unorganized industry. Nearly all potato chip

snack products are manufactured and sold locally. There is also no uniform

standard for packaging, as there is in Europe, the United States and other

more developed regions. Many snack foods are sold loose or packaged in

poly-pouches, which may only be folded, or in some cases, stapled closed. As

the Indian economy continues to grow, and production standards improve,

many snack food companies are making significant investments into plant

equipment and packaging machinery.

Pepsi Foods Ltd., now known as Frito-Lay India Ltd., produces India's largest

snack food manufacturers brands, including Ruffles, Hostess, Cheetos and

Uncle Chips. Frito Lay's story is an example of how American recipes were

adjusted to satisfy local tastes. Procter & Gamble's Pringles brand of potato

crisp was launched in Delhi in 1999. Pringles is also a baked potato crisp,

unlike many other potato based Indian snack foods that are fried. P&G

currently imports the Pringles product and therefore the product has been

priced at a premium and is marketed to a micro-niche.

MARKET AND COMPETITION

Indian Foods market is a monopolistic market. There are many competitors in

all the categories and although they all have similar products available at

similar prices, they are trying to prove themselves different through their

marketing strategies. However, entry to this business is easy and ITC has

utilized this fact very efficiently to their benefit as they entered into the several

categories among this Foods business.

READY TO EAT

ITC entered into the branded and packaged foods business in with the launch

of Kitchens of India brand. In 2004, the company launched KoI brand fruits

and spice conserves and cooking pastes. The fruits and spice conserves,

were developed jointly with Karen Anand, a food expert. Priced at Rs. 70,

these were targeted at the premium segment. The KoI cooking pastes, which

were priced at Rs.30 for a 100g pack, also targeted the high-end market.

20

Multi-purpose cooking pastes were also launched under the Aashirvaad brand

and these were priced at Rs. 10 for 80g pack. The manufacturing of these

products was outsourced to contract manufacturers for saving the operating

cost.

ITC entered the branded spices market in 2005 and the Instant Mix segment

in 2006, both under the Aashirvaad Brand. As on April 2006, the total turnover

in the Indian ready-to-eat and ready-to-cook segments was only around Rs.

700 million, but it continued to post an annual growth of 20%. By early 2006,

though ITC had captured a 35% market share in the ready-to-eat segment,

MTR was the clear market leader with close to 60% in market share. ITC

exported 40-50% of KoI brand products (in terms of volumes) to the US,

Canada, the UK, Switzerland, and Australia.

In May 2006, ITC planned to introduce ten more varieties under the KoI brand within

a price range of Rs. 35 to Rs. 98. In 2007, some new products have been launched

under Ready To Eat category like chutneys, curries, conserves, biryanis (Noor Mahal,

Bhori Biryani and some new range of products under Gharana (Paneer Malai, Keema

Mutter). After launching all these products ITC FOODS is looking to share 50 to 60%

of market by 2008-2009.Following are the major competitors ITC is competing with

in Ready to Eat category:

Brands Description

Gits

Gits produces the selected range of popular ready to cook and

instant foods that cover a range of ethnic Indian cuisine-and

where the recipes have "Global pallete acceptance".

Haldirams

Offers packaged Bhel puri chats such as Sev Puri, Chana

Masala, Samosa, Pakoras, Alu Tikki, Pao Bhaji, Gol Gappa,

Dhokla among others

Ethnic

Kitchens

Offers packaged sweets,syrups,namkeens, cookies, pickles,

aloo Masala, Bhujia, Bhelpuri, Chana Dal, Kajui Ladoo and

many more items.

21

MTRMTR foods currently comprise twenty-two delicious and

completely authentic Indian curries, gravies and rice.

Priyafoods

Priya has a range of popular traditional recipes starting from

Dal Makhani, Navaratan Kurma to Palak Paneer, Paneer Butter

Masala, Punjabi Chhole and Rajma Masala along with true

southern delicacies like Andhra Veg Pulav, Mango Dal,

Gongura Dal.

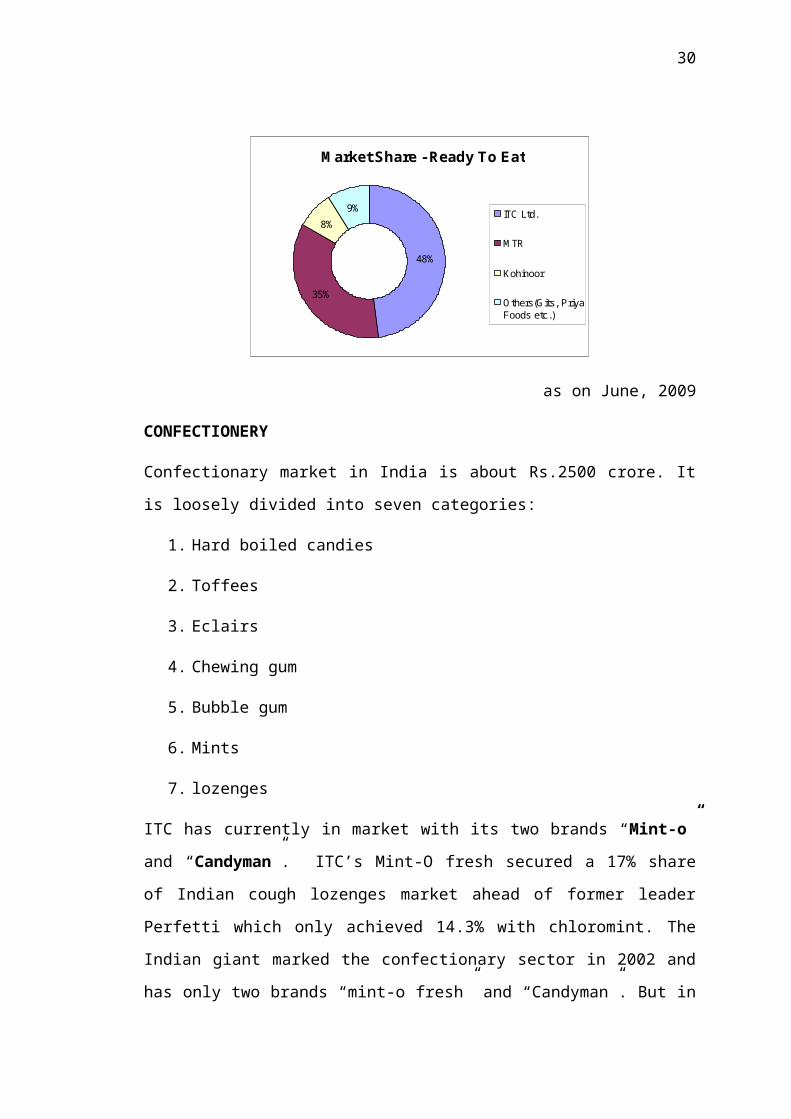

Market Share - Ready To Eat

48%

35%

8%

9%ITC Ltd.

MTR

Kohinoor

Others(Gits, PriyaFoods etc.)

as on June, 2009

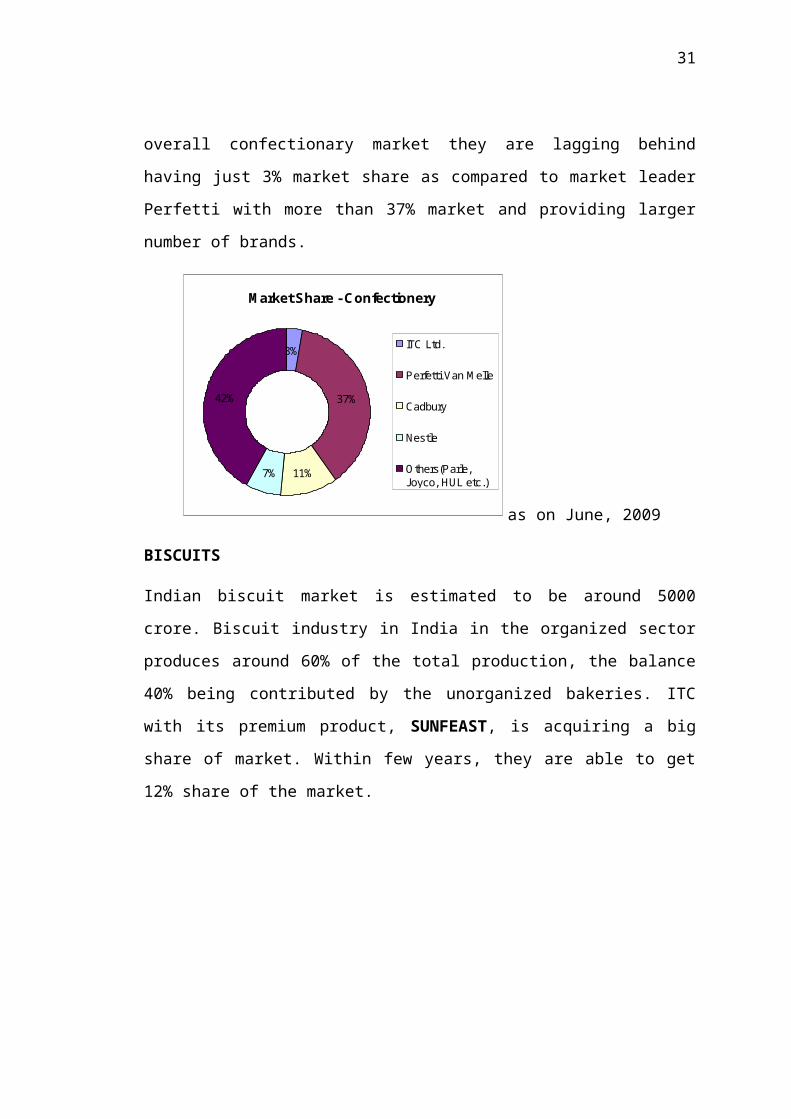

CONFECTIONERY

Confectionary market in India is about Rs.2500 crore. It is loosely divided into

seven categories:

1. Hard boiled candies

2. Toffees

3. Eclairs

4. Chewing gum

5. Bubble gum

6. Mints

7. lozenges

22

ITC has currently in market with its two brands “Mint-o” and “Candyman”.

ITC’s Mint-O fresh secured a 17% share of Indian cough lozenges market

ahead of former leader Perfetti which only achieved 14.3% with chloromint.

The Indian giant marked the confectionary sector in 2002 and has only two

brands “mint-o fresh” and “Candyman”. But in overall confectionary market

they are lagging behind having just 3% market share as compared to market

leader Perfetti with more than 37% market and providing larger number of

brands.

Market Share - Confectionery

3%

37%

11%7%

42%

ITC Ltd.

Perfetti Van Melle

Cadbury

Nestle

Others(Parle,Joyco, HUL etc.)

as on June, 2009

BISCUITS

Indian biscuit market is estimated to be around 5000 crore. Biscuit industry in

India in the organized sector produces around 60% of the total production, the

balance 40% being contributed by the unorganized bakeries. ITC with its

premium product, SUNFEAST, is acquiring a big share of market. Within few

years, they are able to get 12% share of the market.

23

Britannia ITC Ltd

(Sunfeast)

Parle Priyagold

Tiger

Nutrichoice

Junior

Good Day,

50 50,

Treat

Pure Magic,

Milk Bikis

Good

Morning.

Marie

Dream cream

Milky Magic

Fit kit

Choco Nut

Butter Nut

Parle-g

Krack-Jack

Monaco

Kreams

Hide and Seek

Milk Shakti

Butter Bite

Classic Cream

Butter Lite

Big Boss

Marie Lite

Magic Gold

Market Share - Biscuits

12%

10%

38%

32%

8%ITC Ltd.

Priyagold

Britannia

Parle

Others(Bonn,Anmol etc.)

as on June,2009

24

BINGO!

No Confusion Great Combination

ABOUT BINGO

The Bingo brand of chips was launched by ITC on 14th March 2007 with an

aim to capture at least 25 percent market share of the Rs 2000 crore branded

snack market within five yrs. The launch is symbolic of ITC Foods' distinct

approach of introducing innovative and differentiated products in a largely

undifferentiated market place. Bingo’s launch was strategically timed around

the World Cup. The idea was to get the consumer to take that first bite.

This was an extremely ambitious target according to observers as the market

was dominated by the Frito Lay group (owned by Pepsi Co) with a slew of

brands like Lays, Kurkure and Uncle Chipps holding 50 per cent of the market

share. The other was the Haldiram group with 25 percent of the market share.

Bingo’s portfolio includes an array of products in both Potato Chips & Finger

Snacks segment. Bingo! is positioned as a youthful and innovative snack,

offering the consumers a choice of flavours that are fast becoming popular.

Bingo used combination of leveraging synergies, building on consumer

insights and high decibel advertising can win the game. The company

leveraged its existing distribution network and relationship established with

farmers. Its earlier foray into categories like atta and biscuits had already

given it access to the supply chain.

25

BEFORE THE LAUNCH

Research: After making the decision to launch Bingo it started by sending a

cross-functional team of eight individuals were sent across the country to

research the snacking habits of the Indian consumer. After travelling to 14

cities and speaking to more than 1,000 people, the team came back with an

insight that Indian consumers were looking for novelty and excitement in

existing snacks.

The team found that while vada pavs and samosas still sell vada pav with

cheese and paneer-filled samosas, or for that matter, tomato-flavored khakra

were the ones that excited the Indian consumer. Based on this information,

the company decided to look at chips with innovative flavors.

Taste: For the recipes, the company went to the chefs in its hotels. The chefs

came up with 16 flavors with innovative twists like bindaas masti chaas,

chatkila nimbu achar and tandoori paneer tikka-flavoured potato chips, chilli

and tomato-flavored mad angles — inspired by khakras — and other snacks.

The organized snacks category is subdivided into the Traditional segment

(Bhujia,Chana etc) dominated by Haldiram. The second category is the

Western segment (potato chips,cheese balls,puffs etc) and the Finger snacks

segment which is an adaptation of traditional snacks to the western format.

The latter two categories are dominated by the Frito Lay group. ITC has

launched an aggressive marketing campaign to gain entry into and capture a

sizeable market share in the extremely competitive world of snack foods.

Bingo’s success in the market is backed by ITC’s strong distribution network,

which allows it to stock its products in shops that previously did not sell snack

food. Additionally, ITC Foods provides shopkeepers with plastic molded

shelves that allow local vendors a convenient way to stock their product, and

the company benefits by increased visibility for its brand.

The packaging is very attractive with dominant variant color, crimp border

colors and a pictorial view of the flavor. This property of flavor depiction is

very informative for consumers and a layman can also associate with it. Bingo

26

has a unique musical sound that is loved by everyone. It is one of the

properties that are remembered by everyone and it is used to recall the brand

by every age group.

MAIN COMPETITORS:

1. Frito-Lay

Lays

Kurkure

Uncle Chipps

Cheetos

2. Haldiram

3. Regional Players like Balaji

COMPARISON OF PRICES:

Product Price

(ITC Ltd)

Product Price

(Frito Lay)

Product Price

(Haldiram)

Bingo

Rs. 5

Rs. 10

Rs. 20

Lays

Rs. 5

Rs. 10

Rs. 20

Uncle Chipps

Rs. 10

Rs. 20

Kurkure

Rs. 5

Rs. 10

Rs. 20

Namkeen

Rs. 5

Rs. 10

Rs. 20

27

CHAPTER-4

RESEARCH OBJECTIVE AND METHODOLOGY

RESEARCH OBJECTIVES

To point out the positive and negative aspects of advertising (print &

electronic media)

To analyze the impact of advertising (print & electronic media) on

customers’ buying behavior, particularly in case of “ITC-Bingo”.

To obtain the customers’ response and attitude towards advertising (print

& electronic media) carried out by “ITC-Bingo”

RESEARCH METHODOLOGY

Secondary Data: News Papers, books, internet, Reports, Business

magazines

Tools: Bar Diagrams, pie-charts, tabulation

Sampling method: Random sampling method

Sample size: 100

Target audience: Interviews and Questionnaires with the Consumers in

FMCG Sector

28

CHAPTER-5

DATA ANALYSIS & INTERPRETATION

In order to extract the meaningful information from the data collected an

analysis of data is done using pie charts, bar graphs etc.

The first objective of the research project is concerned with finding out

what percentage of people likes to eat snacks. The chart given below is

clear on the percentage of people who like to eat snacks.

Ques 1:- Do you eat snacks?

Comments: -The primary and the secondary form of data collection, says that

nearly 100 percent of the people love to eat snacks. The snacks are the

compliment for the Hot and Cold Beverages Company. People always

consume it with Tea, Coffee or with Cold Drinks.

29

Ques 2:- Have you Heard of ITC Bingo?

Comments: -As per the survey done, the 90% people know about the ITC

Bingo. The Bingo has a good image over the students (Less than 25 years)

and male (25-35years) but the females (25-35 years) are not much aware

about the product. The Kurkure is more popular in Female segment. There is

a need to advertise in such a manner, so that the product can target females

too.

30

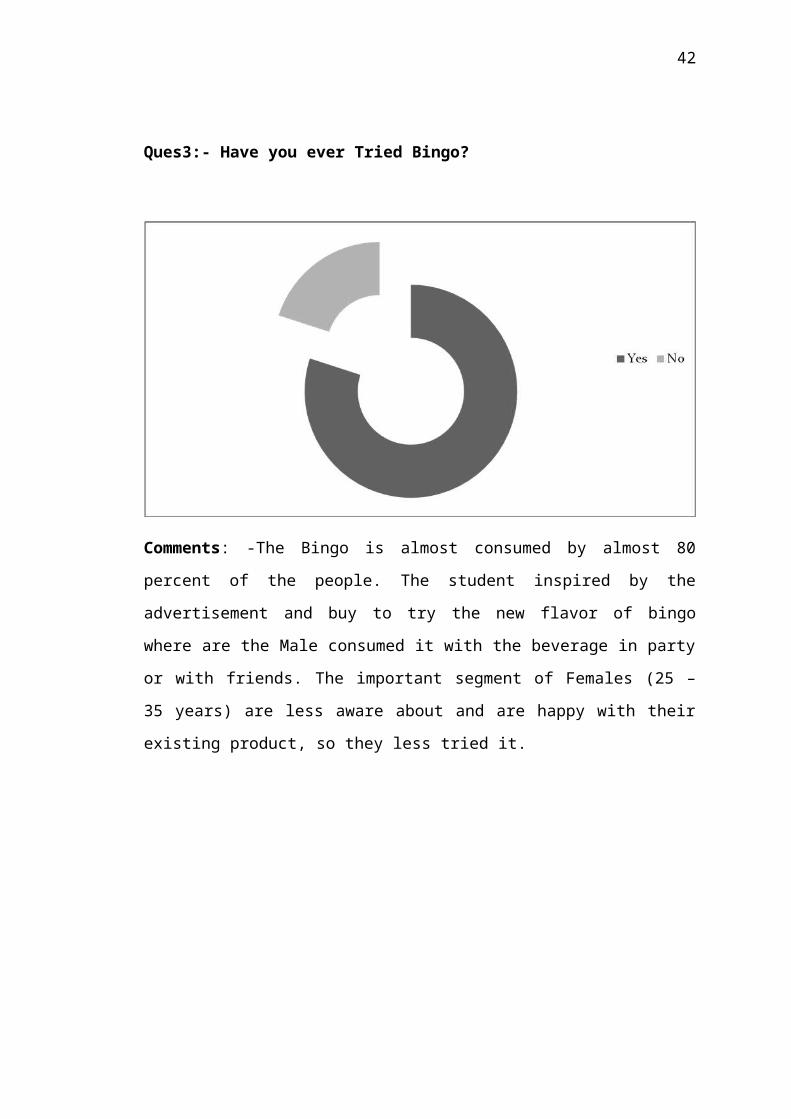

Ques3:- Have you ever Tried Bingo?

Comments: -The Bingo is almost consumed by almost 80 percent of the

people. The student inspired by the advertisement and buy to try the new

flavor of bingo where are the Male consumed it with the beverage in party or

with friends. The important segment of Females (25 – 35 years) are less

aware about and are happy with their existing product, so they less tried it.

31

The second objective is concerned with finding out which flavor of

Bingo is most preferred.

Ques 4:- Which flavor do you like most?

Comments: -The most popular flavor of Bingo is Tedhe Medhe and Mad

Angles in the student group. The Males prefer Tomato Potato Chips and the

Females prefers Masala Potato chips and Nimbu achar flavor. The reason of

Bingo popularity is due to different flavors.

32

Ques 5:- How many times do you consume BINGO?

Comments: -Although ITC Bingo is very popular but the everyday

consumption of BINGO product is very less in compare to other snacks. In the

question all the 3 segments (Students, Males, Females) are not consuming it

on the daily basis, Most people consume it on the once in a week or less

basis.

33

Ques 6:-How much do you weekly spend on snacks?

Comments: -This is the most important and interesting area of the survey,

The student group who consume Bingo only are spending less than 50 Rs.

Weekly on snacks where as the males and females are spend 50-100 Rs per

week on their snacks consumption. The married couple are spending more

than 100 Rs on snacks, but they also prefer the other brands too (like

Kurkure, Lays etc)

34

Third objective was to find out how much people are satisfied with Bingo.

Following pie chart shows the satisfaction level of people

Ques 7:-How much satisfied are you with Bingo?

Comments: -The Males are very satisfied with the Bingo product as it is the

ITC product. Whereas flavor conscious students are satisfied or unsatisfied

with the Bingo product and the health conscious Females are very unsatisfied

with the bingo product.

35

The Fourth objective was to analyze the reasons for the popularity of

the most preferred flavor. For this the respondents were asked what do

they like most about Bingo. Following pie chart shows their responses.

Ques 8:-What do you like about Bingo?

Comments: -The majority of males and females like the taste of the bingo

product but the student segment like BINGO because it offers a lot of verity

and flavor. As it is the ITC product so, it has a good image in the public eyes

in terms of quality.

36

Ques 9:-Is the price of Bingo is satisfactory?

Comments: -Nearly all the snacks available in the market is about the same

price so all the 3 segments are satisfy with the price, where as few people

wants that the price must be according to flavor. The price must be

competitive so the people can switch on with the Bingo product.

37

Ques 10:-Compare to other snacks (such as Kurkure, Lays, Haldiram

etc) that are available, would you say that Bingo is?

The Fifth objective was to find out the preferences of people for different

brands. Here, we aim to find out the most popular brand of snacks

excluding Bingo.

38

Comments: - In the above graph we can see that Kurkure is the most popular

brand among people followed by Uncle Chips and Lays. Next is Bingo and

Haldiram’s Namkeens.

The males are satisfy and mush satisfied with Bingo. Students are somewhat

satisfied or same satisfied with bingo where as females are not very much

satisfied with Bingo product. The second chart shows that still kurkure is the

market leader of the snacks, then people prefer bingo and then the other

products.

Ques 11:-How likely are you to recommend BINGO to others?

Comments: -The majority of the people are in favor to recommend the bingo

product. The main advantage of bingo product is it available in a lot of Varity.

39

Ques 12:-How did you first discover BINGO?

Comments: -The bingo advertisements make it popular in all segment and

few people first tried bingo when offered by friends/family member with

beverages.

Ques 13:-Before switching on to BINGO, which snack did you prefer?

40

Comments: -As the price of bingo is not very much competitive so the people

are still consuming the other snacks like kurkure and lays, even haldiram

Namkeens are also preferred by consumers to serve the hot and cold

beverages.

Ques 14:-What do you considered while buying Bingo?

Comments: -The student and the Males segment buy the snacks on the

basis of their flavor whereas females (health conscious segment) are buying it

because of the quality. The availability and brand ambassador are not very

much preferred by any of the segment.

41

SUMMARY OF OTHER FINDINGS

16 people out of 36 people who like to eat snacks feel that as compared to

other brands Bingo is much better. Other 12 feel that Bingo is somewhat

better and 8 feel that Bingo is about the same as other brands. None feel that

Bingo is somewhat worse or much worse than other brands.

When asked how often they eat Bingo 22 people said once a week or more

often, 11 people said everyday and 3 people said 2-3 times a month.

After conducting the survey we are in a position to say that ever since its

launch Bingo as a preferred brand is on a rise. Although Frito Lays is the most

popular brand Bingo has carved a niche for itself. Bingo is in the growth stage

of its life cycle. Given more time it is capable of capturing a larger market

share and giving tough competition to other brands.

42

CHAPTER-6

CONCLUSION & RECOMMENDATION

CONCLUSION

Although Frito Lays is the most popular brand Bingo has carved a niche for

itself. Bingo is in the growth stage of its life cycle. Given more time it is

capable of capturing a larger market share and giving tough competition to

other brands. Its focus is more on product innovation and distribution and

invests heavily in promotion. In the coming years it will become a dominant

player in the domestic market.

RECOMMENDATION

Brand Packaging: Bingo can come up with different shapes of packaging.

Different packaging always attracts consumers. Usage of different colors

for packaging will be helpful as the customers will be able to differentiate

among various products.

Brand promotions: Company can opt for seasonal promotions. Gift packs

or combos with 4-5 flavours can be introduced. Can tie up with beverages

like Coca Cola during festive season or can sponsor events like cricket

tournaments etc.

Advertising: The existing advertisements have been successful in creating

brand awareness. Now its time to focus more on taste and variety of

flavours, tempting the consumers to purchase the product. An animated

character can be used to describe the flavour.

Flavours: Having too many flavours is causing some problem because the

customers are not able to differentiate between different variants. Even

though it’s a good strategy as people are forced to try each flavour, the

ones which are not going good in the market should be removed from the

company’s portfolio. This would reduce the problem of confusion amongst

the consumers.

43

Contests: The company should launch a contest like “Send in your Bingo

recipe” which can help the company to increase its market share.

44

BIBLIOGRAPHY

1. www.itcportal.com

2. www.allbusiness.com

3. http://www.financialexpress.com/news/Just-munch-it/271873/0

4. www.wikipedia.org

5. www.moneycontrol.com

6. www.economictimes.indiatimes.com

7. www.bingeonbingo.com

8. www.google.com

45

APPENDIX

QUESTIONNAIRE

Name: _________________ Age : ___________ (DD/MM/YY)

Signature: _______________ Email : __________________

General Instructions:

1. Answer all questions.

2. Indicate your answer by marking a tick against an appropriate option.

3. Mark only one option in all questions.

Q1. Do you like to eat snacks?

Yes No

Q2. Have you heard of ITC’s BINGO?

Yes No

Q3. Have you ever tried BINGO?

Yes No

Q4. Which flavour do you like the most?

1. Masala Potato Chip

2. Salted Potato Chip

3. Tomato Potato Chip

4. Chatkila Nimbu Achar Potato Chip

5. Tandoori Paneer Tikka Potato Chip

6. Mad Angles

7. Tedhe Medhe

8. Livewires

46

Q5. How often do you have BINGO?

Once a week or more often Everyday

2 to 3 times a month 2 or more per day

Q6. How much do you spend weekly on snacks?

Below Rs. 50 Rs. 50-100 More than Rs. 100

Q7. Overall, how much satisfied are you with BINGO?

Very satisfied Somewhat satisfied Unsatisfied

Q8. What do you like about BINGO?

Taste Variety Quality

Price Quantity Packaging

Q9. Is the price of bingo is satisfactory?

Yes No

If No (Please specify price, according to you) ____________________

Q10. Compared to other snacks (such as Kurkure, Lays, Haldiram etc.) that

are available, would you say that BINGO is?

Much better Somewhat Better

About the same Somewhat Worse

Much Worse

Q11. How likely are you to recommend BINGO to others?

Definitely will recommend Probably will recommend

Not sure Probably will not recommend

Definitely will not recommend

Q12. How did you first discover BINGO?

Advertising- T.V, Newspaper, Radio Friends/ Family

Saw it in store Other

47

Q13. Before switching on to BINGO, which snack did you prefer?

Lays Kurkure

Uncle chips Haldiram Namkeens

Q14. What do you considered while buying your brand?

Flavour Product quality

Availability Brand ambassador

Other (please specify) ________________________________

48