rI CIT OF i UPPERU ARLINGTON

MISSION STATEMENTThe City of Upper Arlington is committed to providing superior services to all who

live and work in the community. The work of the City is founded on responsibleand responsive public participation, elected leadership and professional staffing.

COUNCIL CONFERENCE SESSIONMEETING MINUTES

August 19, 2013

City Council met in the Lower Level Conference Room of the Municipal ServicesCenter, 3600 Tremont Road, and was called to order by President Donald B.Leach, Jr. at 7:30 p.m.

MEMBERS PRESENT: Vice President Frank Ciotola, David DeCapua,Debbie Johnson, Michael Schadek, Erik F. Yassenoffand President Donald B. Leach, Jr.

MEMBERS ABSENT: John C. Adams

STAFF PRESENT: City Manager Theodore Staton, Assistant City ManagerJoe Valentino, Community Affairs Director EmmaSpeight, Public Services Director Darryl Hughes, Parksand Recreation Director Tim Moloney, Police ChiefBrian Quinn, Sergeant Tracy Hahn, Officer HeatherGalli, Detective Jason Messer, Community andEconomic Development Director Dean Sivinski,Economic Development Manager Bob Lamb,Information Technology Director Granville Harris, CityAttorney Jeanine Hummer, First Assistant City AttorneyTom Lindsey, Assistant Attorney Thad Boggs, FireChief Jeff Young, City Engineer Dave Parkinson,

Finance and Administrative Services Director CatheArmstrong, and City Clerk Molly Hildebrand

* * *

REPORTS/PRESENTATIONS/DISCUSSION ITEMS

1. Auditor's Report

Council Conference Meeting MinutesAugust 19, 2013Page 2

Bethany Staats of Julian & Grube, Inc. reviewed the Independent Auditor'sreport (attached hereto and incorporated herein by reference as Exhibit A)with CounciL.

In response to Mr. Leach, Ms. Staats stated that in general there is goodnews in the audit.

In response to Mrs. Johnson, Ms. Staats stated that there is nothingnegative in the audit.

Cathe Armstrong, Director of the Finance & Administrative ServicesDepartment, stated that there have been several years in a row with nofindings reported in the audit. Ms. Armstrong credits this to her hardworking staff.

Mr. Leach requested Ms. Armstrong to extend congratulations to theremainder of her department on a successful audit.

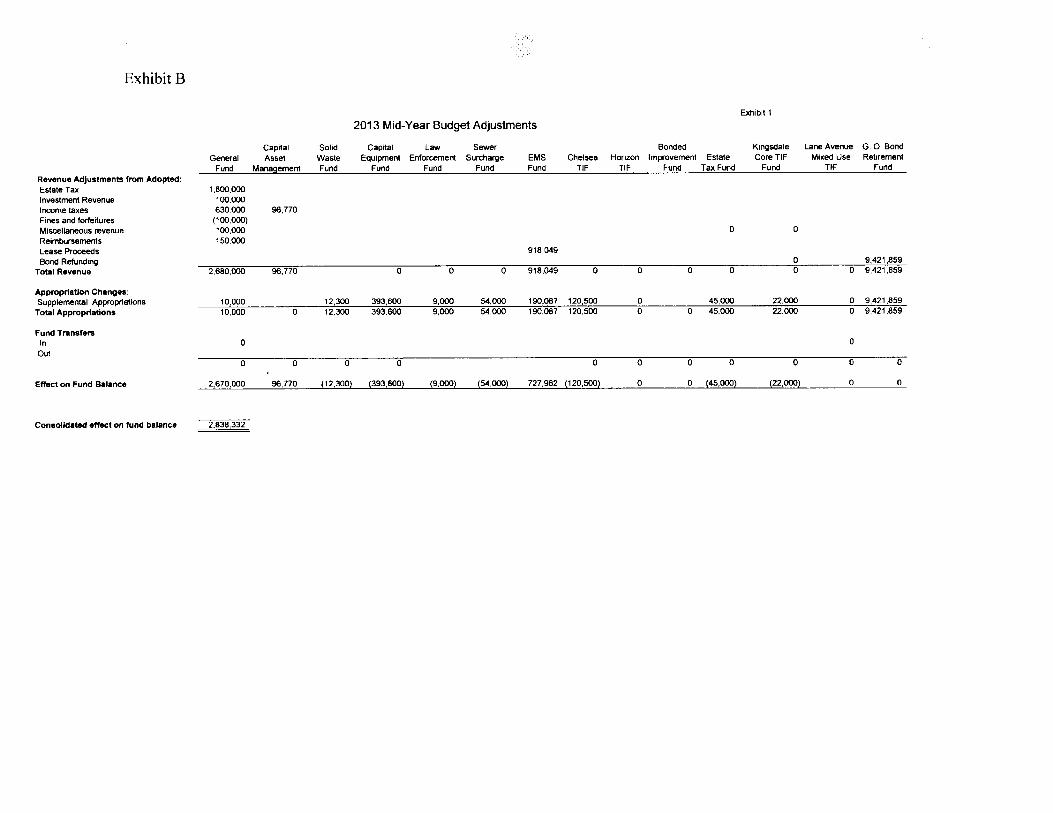

2. Mid-Year Budget Review

Ms. Armstrong reviewed the Mid-Year Budget documents (attached heretoand incorporated herein by reference as Exhibit B) with CounciL.

In response to Mr. Leach, Ms. Armstrong stated that the Chelsea TIFFund has changed due to a large retroactive refund to First CommunityVillage in which the City will have to return money under $300,000. Ms.Armstrong continued that the Fund will be made whole, just not today.

In response to Mrs. Johnson, Ms. Armstrong relayed that the money willbe returned to the general fund once it has been repaid.

3. TIRC and Economic Development Portolio Review

Bob Lamb, Economic Development Manager, provided an overview

(attached hereto and incorporated herein by reference as Exhibit C) of theTIRC and Economic Development Portfolio.

In response to Mr. Leach, Mr. Lamb stated that Council will vote to acceptthe suggested changes at the next Council Meeting.

Council Conference Meeting MinutesAugust 19, 2013Page 3

In response to Mr. Leach, Mr. Lamb relayed that the language ofcompliance and substantial compliance were used based on previousyears reports.

4. Real Estate Sales Analysis

Mr. Lamb provided an overview of data concerning real estate sales inUpper Arlington to CounciL.

In response to Mr. Ciotola, Mr. Lamb stated that home sales north of LaneAvenue are selling quickly and over the asking price. City Manager TedStaton added that the appreciation of home values is faster north of LaneAvenue then the whole City average.

Community Affairs Director, Emma Speight, provided data from a focusgroup (attached hereto and incorporated herein by reference as ExhibitD).

In response to Mr. Ciotola, Mrs. Speight stated that the focus group wasnot formal but was a good opportunity to gather information and data onreal estate sales in Upper Arlington.

In response to Mr. DeCapua, Mrs. Speight relayed that some concern wasexpressed in the focus group for real estate if the school levy fails. Mrs.Speight stated there was a larger emphasis on public entities being fiscallyresponsible and efficient.

5. Directing the City Engineer to Prepare Plans and Specifications for

Subject Improvements for Berkshire Road (between Brandon Roadand Beaumont Road) (Citizen-initiated Petitions)

Mr. Yassenoff requested a suspension of rules on this issue at the nextCity Council Meeting.

6. City Manager Update

a. Salt Storage Facilty

Council Conference Meeting MinutesAugust 19, 2013Page 4

Public Services Director Darryl Hughes relayed to Councilthat the current salt storage facility the City uses is over 30years old and is no longer structurally sound.

Mr. Hughes stated that after looking at different designs thebarn structure is what the City should build. This structurewould allow for easy access to trucks, hold the same amountof salt, and allow for future expansion.

In response to Mr. Schadek, Mr. Hughes stated that thestructure would cost $260,000.

In response to Mr. DeCapua, Mr. Hughes stated that thelarge pile of salt seen from the freeway does not belong toany city, but a supplier. Additionally, Mr. Hughes relayed thatsalt storage facilities are built with the city's needs in mindmaking it difficult to share this resource. In the past the Cityhas temporarily shared salt storage facilities, but for the longterm this is not plausible.

In response to Mr. Yassenoff, Mr. Hughes stated that Hilliardand Dublin have storage facilities on Cemetery Road.

In response to Mr. DeCapua, Mr. Hughes relayed that tarpswere considered but are not as strong a solution as the barndesign chosen.

In response to Mr. Staton, Mr. Hughes stated that there areenvironmental regulations concerning how the storagefacility drains water.

Mr. Leach requested that Mr. Hughes check on whereGrandview Heights salt storage facility is located.

Mrs. Johnson requested that Mr. Hughes look into thepossibility of building a joint facility with another city such asHilliard.

LEGISLATIVE AND/OR ADMINISTRATIVE ITEMS

7. Proposed Legislation - To Amend C.O. Section 315.02, Compliance

with Lawful Order of Law Enforcement Officers; Fleeing From LawEnforcement Officers, Relative to the Traffic Code, to Conform to

Council Conference Meeting MinutesAugust 19, 2013Page 5

Ohio Revised Code by Providing for a Class-Five Driver's LicenseSuspension

No questions or discussion was had on this item.

8. Proposed Legislation- To Amend C.O. Section 511.08, Possessionand Sale of Drug Paraphernalia, Relative to the General OffensesCode, by Adding Offenses Elevating Violation of C.O. § 511.08 to aMisdemeanor of the First Degree

No questions or discussion was had on this item.

9. Proposed Legislation- To Amend C.O. Section 507.05, Voyeurism,and Section 507.06, Public Indecency, Relative to the GeneralOffenses Code, to Conform to Ohio Revised Code; and Declaring anEmergency

No questions or discussion was had on this item.

10. Proposed Legislation- To Amend Section 1.08 Relationship toComprehensive Plan; Section 2.02 Definitions; Section 4.04(B)Amendment Process; Section 4.06(C)(8) Action by BZAP; Section4.06(E) Subdivision-Major; Section 4.06(F) Final Plat Amendment;Section 5.01 (B)(2) Permitted Uses; Section 5.01 (B)(3) ConditionalUses; Table 5-A Residential Uses; Table 5-D Mixed Uses; Table 5-E-

Residential Building Area, Density and Setback Standards, Table 5-FResidential Building Coverage and Height Standards; Article 5.01 (C)Districts; Article 5.02(A) Residential Districts; Article 5.03(B)Commercial Districts- Permitted, Prohibited, and Conditional Uses;Article 5.04(C) Planned Mixed-Use Districts Permitted andConditional Uses; Article 5.06(C) Establishment of Zoning Districts;Section 6.01 (B) Establishment of Zoning Districts; Section 6.04(H)Soil Sediment Regulations; Section 6.09(C)(1) Accessory Structures;Section 6.09(C)(2) Accessory Structures; Section 6.09(C)(5) AestheticConsideration; Section 6.09(D)(12) Private Swimming Pools and HotTubs; Article 6.11 (A)(2) Wireless Communication Facilties; Section7.06(B)(2) Building Facades; and Section 7.17 ResidentialConservation; To Add Section 5.01(B)(6) Secondary or AuxilaryUses; and Section 6.09(D)(13) Fences; Relative to the UnifiedDevelopment Ordinance

In response to Mr. Yassenoff, City Attorney Jeanine Hummer stated thatthis proposed legislation will be discussed at the next Council ConferenceSession to allow for more discussion prior to voting on the legislation.

Council Conference Meeting MinutesAugust 19, 2013Page 6

In response to Mrs. Johnson, Mrs. Hummer relayed that any editorialchanges should be emailed to her and she would be happy to answer anysubstantive questions.

11. Proposed Legislation- To Amend C.O. Chapter 202, TransientOccupancy Tax, Relative to the Revenue and Finance Code, byAmending Entities Exempt From the Hotel/Motel Excise Tax andVendors Required to Collect and Remit the Hotel/Motel Excise Tax

Ms. Armstrong informed Council that the Transient Occupancy Tax will becollected by the hotel (S&S) even if the occupant purchases the room onan internet website.

In response to Mrs. Johnson, Ms. Armstrong stated that if an occupantstays for over 30 days there are no taxes collected after that point as theyare no longer considered transient. Assistant City Attorney Thadd Boggsadded that transient is defined under state law and cannot be changed bythe City.

In response to Mr. Yassenoff, Ms. Armstrong stated that S&S tries not tosell rooms to internet companies as they are neither the hotel nor theCity's friend. Ms. Armstrong continued that when the internet companiesare utilized, the occupant will pay the tax on the price paid for the room.

Mrs. Hummer stated that legislation will reflect these concerns.

12. Proposed Legislation- To Amend Chapter 549, Alcoholic Beverages,by Amending Sections 549.01, Definitions, and 549.07, OpenContainer Prohibited, Relative to the General Offenses Code, toConform to the Ohio Revised Code

No questions or discussion was had on this item.

13. Proposed Legislation- To Appropriate and Transfer Funds

No questions or discussion was had on this item.

COUNCIL LIAISON REPORT

Mr. Leach informed Council to contact City Clerk Molly Hildebrand if they wish toregister for the Ohio Municipal League Conference.

Council Conference Meeting MinutesAugust 19, 2013Page 7

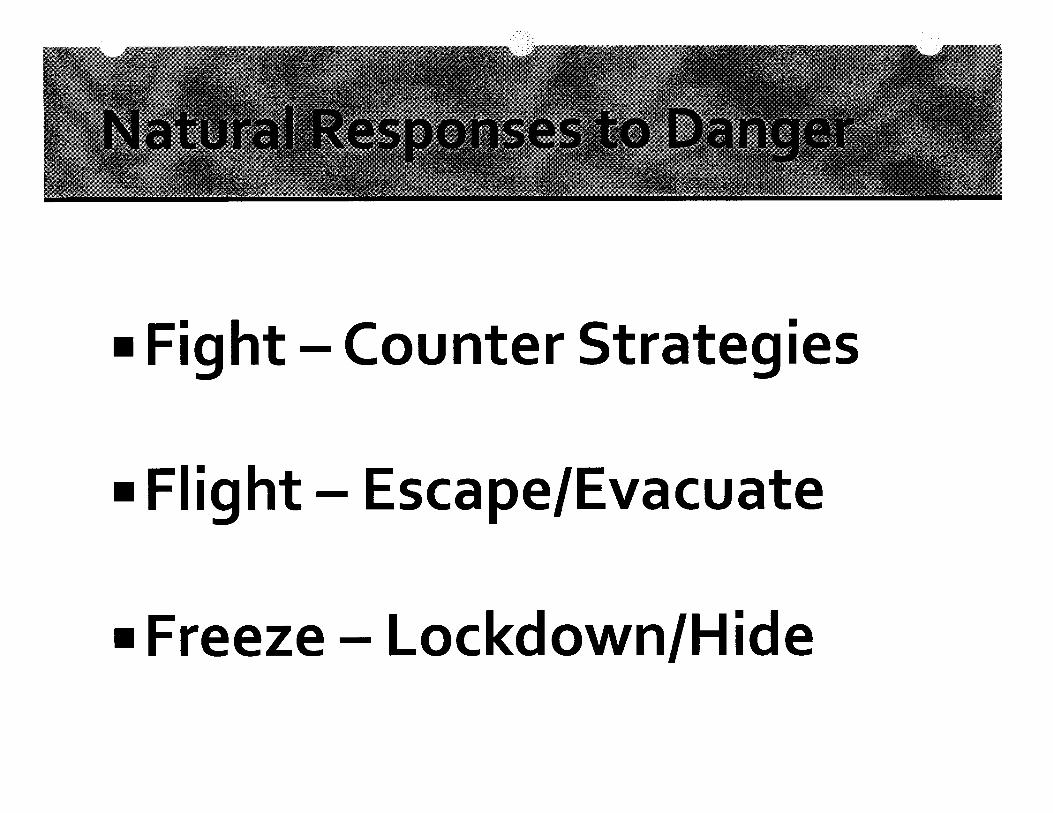

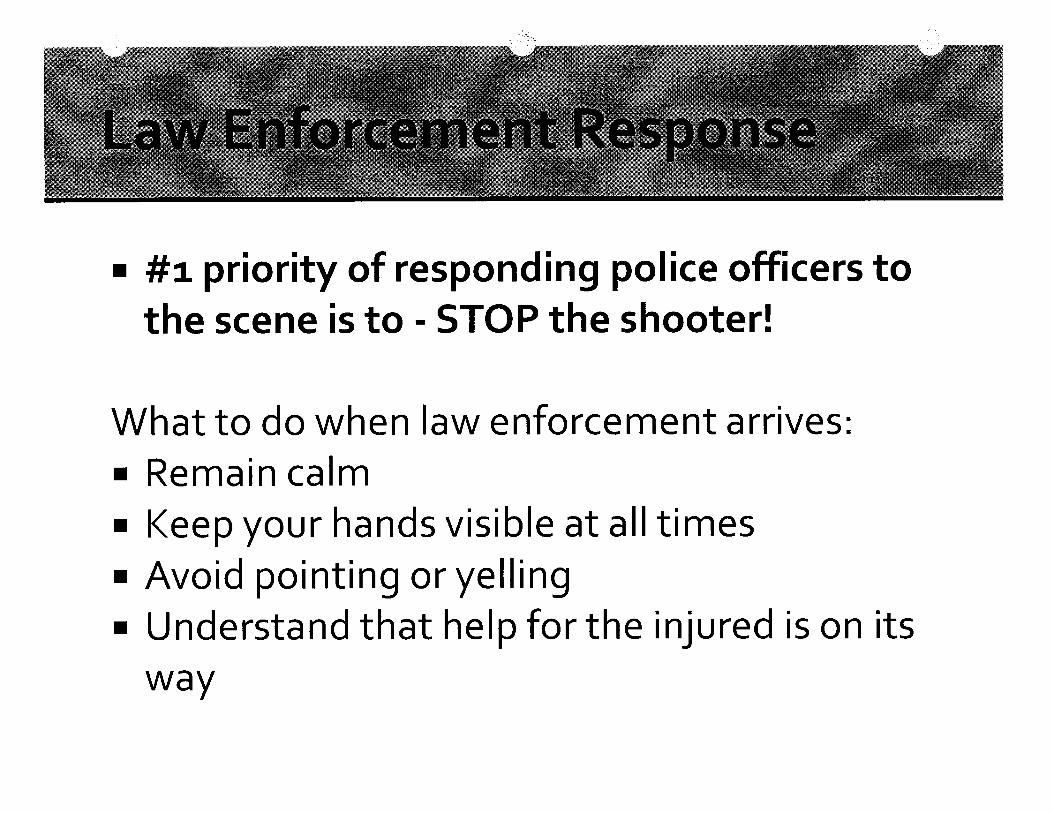

A.L.I.C.E. SAFETY TRAINING

Officer Heather Galli and Sergeant Tracey Hahn presented a PowerPoint(attached hereto and incorporated herein by reference as Exhibit E) concerningA.L.I.C.E. (Alert Lockdown Inform Counter Evacuate) safety training.

* * *

There being no further business to come before City Council, the meeting wasadjourned 9:23 p.m.

ATTEST:~~City lerk

Exhibit A

Julian & Grube, Inc.Serving Ohio Local Governments

333 County Line Rd. West, Westerville. OH 43082 Phone: 614846.1899 Fax: 614.846.2799

Independent Auditor's Report

City of Upper Arlington3600 Tremont RoadUpper Arlington, OH 4322 I

To the Members of Council and Mayor:

Report on the Financial Statements

We have audited the accompanying financial statements of the governmental activities, the business-typeactivities, the discretely presented component unit, each major fund, and the aggregate remaining fundinformation of the City of Upper Arlington, Franklin County, Ohio, as of and for the year ended

December 31,2012, and the related notes to the financial statements, which collectively comprise the Cityof Upper Arlington's basic financial statements as listed in the table of contents.

Management's Responsibilty for the Financial Statements

Management is responsible for preparing and fairly presenting these financial statements in accordancewith accounting principles generally accepted in the United States of America; this includes designing,implementing, and maintaining internal control relevant to preparing and fairly presenting financialstatements that are free from material misstatement, whether due to fraud or error.

Auditor's Responsibilty

Our responsibility is to opine on these financial statements based on our audit. We conducted our audit inaccordance with auditing standards generally accepted in the United States of America and the financialaudit standards in the Comptroller General of the United States' Government Auditing Standards. Thosestandards require us to plan and perform the audit to reasonably assure the financial statements are freefrom material misstatement.

An audit requires obtaining evidence about financial statement amounts and disclosures. The proceduresselected depend on our judgment, including assessing the risks of material financial statementmisstatement, whether due to fraud or error. In assessing those risks, we consider internal control relevantto the City of Upper Arlington's preparation and fair presentation of the financial statements in order todesign audit procedures that are appropriate in the circumstances, but not to the extent needed to opine onthe effectiveness of the City of Upper Arlington's internal control. Accordingly, we express no opinion.An audit also includes evaluating the appropriateness of management's accounting policies and thereasonableness of their significant accounting estimates, as well as our evaluation of the overall financialstatement presentation.

We believe the audit evidence we obtained is sufficient and appropriate to support our audit opinions.

Independent Auditor's ReportPage Two

Opinion

i n our opinion, the financial statements referred to above present fairly, in all material respects, therespective financial position of the governmental activities, the business-type activities, the discretelypresented component unit, each major fund, and the aggregate remaining fund information of the City ofUpper Arlington, Frankl in County, Ohio, as of December 31, 2012, and the respective changes in

financial position and where applicable, cash flows, thereof for the year then ended in accordance with theaccounting principles generally accepted in the United States of America.

Emphasis of Matters

As discussed in Note i 6 to the financial statements, during 20 i 2, the City of Upper Arlington adoptednew accounting guidance in Governmental Accounting Standards Board Statement No. 63, FinancialReporting of Deferred Outfows of Resources, Deferred Inflows of Resources. and Net Position and No.

65, Items Previously Reported as Assets and Liabilities. Also as discussed in Note i 6 to the financialstatements, the City of Upper Arlington has elected to recharacterize certain previous transfers toadvances. Our opinion is not modified with respect to these matters.

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require this presentation toinclude Management's discussion and analysis and required budgetary comparison schedules, listed inthe table of contents, to supplement the basic financial statements. Although this information is not part ofthe basic financial statements, the Governmental Accounting Standards Board considers it essential forplacing the basic financial statements in an appropriate operational, economic, or historical context. Weapplied certain limited procedures to the required supplementary information in accordance with auditingstandards generally accepted in the United States of America, consisting of inquiries of managementabout the methods of preparing the information and comparing the information for consistency withmanagement's responses to our inquiries, to the basic financial statements, and other knowledge weobtained during our audit of the basic financial statements. We do not opine or provide any assurance onthe information because the limited procedures do not provide us with suffcient evidence to opine or

provide any other assurance.

Supplementary and Other Information

Our audit was conducted to opine on the City of Upper Arlington's basic financial statements taken as awhole. The introductory section, the financial section's combining statements, individual fund statementsand schedules, and the statistical section information present additional analysis and are not a requiredpart of the basic financial statements.

2

Independent Auditor's ReportPage Three

The financial section's combining statements, individual fund statements and schedules, aremanagement's responsibility, and were derived from and relates directly to the underlying accounting andother records used to prepare the basic financial statements. We subjected these statements andschedules to the auditing procedures we applied to the basic financial statements. We also applied certainadditional procedures, including comparing and reconciling this information directly to the underlyingaccounting and other records used to prepare the basic financial statements or to the basic financialstatements themselves, and other additional procedures in accordance with auditing standards generallyaccepted in the United States of America. In our opinion, this information is fairly stated in all materialrespects in relation to the basic financial statements taken as a whole.

We did not subject the introductory section and statistical section information to the auditing proceduresapplied in the audit of the basic financial statements and, accordingly, we express no opinion or any otherassurance them.

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated June 14, 2013,on our consideration of the City of Upper Arlington's internal control over financial reporting and ourtests of its compliance with certain provisions of laws, regulations, contracts and grant agreements andother matters. That report describes the scope of our internal control testing over financial reporting andcompliance, and the results of that testing, and does not opine on internal control over financial reportingor on compliance. That report is an integral part of an audit performed in accordance with GovernmentAuditing Standards in considering the City of Upper Arlington's internal control over financial reportingand compliance.~~l7 ... .,€ ,~Julian & Grube, Inc.June 14,2013

3

CITY OF UPPER ARLINGTONFRANKLIN COUNTY, OHIO

Supplemental Reports

DECEMBER 3 I, 20 12

CATHERINE M. ARMSTRONG, FINANCE DIRECTOR

CITY OF UPPER ARLINGTONFRANKLIN COUNTY, OHIO

TABLE OF CONTENTS

Schedule of Expenditures of Federal Awards ..............................................................................

Independent Auditor's Report on Internal Control Over Financial Reporting and onCompliance and Other Matters Required by Government Auditing Standards ....................... 2 - 3

Independent Auditor's Report on Compliance With Requirements Applicableto Each Major Federal Program and on Internal Control Over Compliance

Required by OMB Circular A-i33 and the Schedule of Expendituresof Federal Awards .................................................................................................................. 4 - 6

Schedule of Findings OMB Circular A-i33 § .505...................................................................... 7

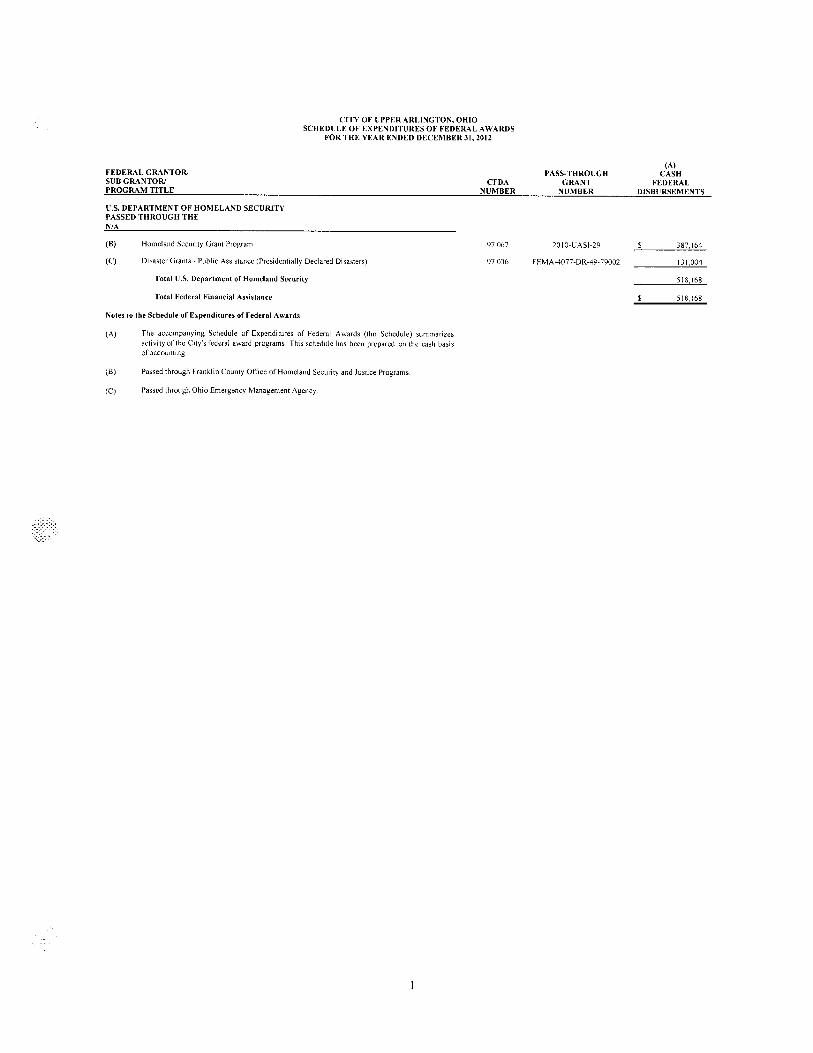

CITY OF UPPER ARLINGTON, OHIOSCHEDULE OF EXPENDITURES OF FEDERAL A WARDS

FOR THE YEAR ENDED DECEMBER 31, 2012

FEDERAL GRANTOR¡SUB GRANTOR!PROGRAM TITLE

CFDANUMBER

(A)CASH

FEDERALDISBURSEMENTS

U.S. DEPARTMENT OF HOMELAND SECURITYPASSED THROUGH THEN/A

(B)

(C)

Homeland Security Grant Program 97.067

Disaster Grants. Public Assistance (Presidentially Declared Disasters) 970J6

Total U.S. Department of Homeland Security

Total Federal Financial Assistance

Notes to the Schedule of Expenditures of Federal Awards

(A) The accompanying Schedule of Expenditures of Federal Awards (the Schedule) summarizesactivity of the City's federal award programs. This schedule has been prepared on the cash basisof accounting

(8) Passed through Franklin County Otlce of Homeland Secuiity and Justice Programs

(C) Passed through Ohio Emergency Management Agency.

PASS-THROUGHGRANT

NUMBER

20 I 0-UASI-29

FEMA-4077-DR-49.79002

J87, I 64

I J 1,004

518.168

518,168

Julian & Grube, Inc.Serving Ohio Local Governments

333 County Line Rd. West, Westervile, DB 43082 Phone: 614.846.1899 Fax: 614.846.2799

Independent Auditor's Report on Internal Control Over Financial Reporting and onCompliance and Other Matters Required by Government Auditng Standards

City of Upper Arlington3600 Tremont RoadUpper Arlington, OH 43221

To the Members of Council and Mayor:

We have audited, in accordance with auditing standards generally accepted in the United States and the ComptrollerGeneral of the United States' Government Auditing Standards, the financial statements of the governmental

activities, the business-type activities, the discretely presented component unit, each major fund, and the aggregateremaining fund information of the City of Upper Arlington, Franklin County, Ohio, as of and for the year endedDecember 31, 2012, and the related notes to the financial statements, which collectively comprise the Government'sbasic financial statements and have issued our report thereon dated June 14, 2013, wherein we noted in Note 16 tothe financial statements, during 2012, the City of Upper Arlington adopted new accounting guidance inGovernmental Accounting Standards Board Statement No. 63, Financial Reporting of Deferred Outfows of

Resources. Deferred Inflows of Resources, and Net Position and No. 65, Items Previously Reported as Assets andLiabilities and has elected to recharacterize certain previous transfers to advances.

Internal Control Over Financial Reporting

As part of our financial statement audit, we considered the City of Upper Arlington's internal control over financialreporting (internal control) to determine the audit procedures appropriate in the circumstances to the extentnecessary to support our opinions on the financial statements, but not to the extent necessary to opine on theeffectiveness of the City of Upper Arlington's internal control. Accordingly, we have not opined on it.

A deficiency in internal control exists when the design or operation of a control does not allow management oremployees, when performing their assigned functions, to prevent, or detect and timely correct misstatements. Amaterial weakness is a deficiency, or combination of internal control deficiencies resulting in a reasonablepossibility that internal control will not prevent or detect and timely correct a material misstatement of the City ofUpper Arlington's financial statements. A signifcant deficiency is a deficiency, or a combination of deficiencies, ininternal control that is less severe than a material weakness, yet important enough to merit attention by thosecharged with governance.

Our consideration of internal control was for the limited purpose described in the first paragraph of this section andwas not designed to identify all internal control deficiencies that might be material weaknesses or significantdeficiencies. Given these limitations, we did not identify any deficiencies in internal control that we consider

material weaknesses. However, unidentified material weaknesses may exist.

2

Members of Council and MayorCity of Upper Arlington

Compliance and Other Matters

As part of reasonably assuring whether the City of Upper Arlington's financial statements are free of materialmisstatement, we tested its compliance with certain provisions of laws, regulations, contracts, and grant agreements,noncompliance with which could directly and materially affect the determination of financial statement amounts.However, opining on compliance with those provisions was not an objective of our audit and accordingly, we do notexpress an opinion. The results of our tests disclosed no instances of noncompliance or other matters we must reportunder Government Auditing Standards.

Purpose of this Report

This report only describes the scope of our internal control and compliance testing and our testing results, and doesnot opine on the effectiveness of the City of Upper Arlington's internal control or on compliance. This report is anintegral part of an audit performed under Government Auditing Standards in considering the City of UpperArlington's internal control and compliance. Accordingly, this communication is not suitable for any other purpose.~.e~~Julian & Grube, Inc.June 14,2013

3

Julian & Grube, Inc.Ohio Local Governments

333 County Liiie Rd. West, Westerville, OH 43082 Phone: 614846.1899 Fax: 614.846.2799

Independent Auditor's Report on Compliance With Requirements Applicableto Each Major Federal Program and on Internal Control Over Compliance

Required by OMB Circular A-133 and the Schedule ofExpenditures of Federal Awards

City of Upper Arlington3600 Tremont RoadUpper Arlington, OH 43221

To the Members of Council and Mayor:

Report on Compliance for Each Major Federal Program

We have audited the City of Upper Arlington's compliance with the applicable requirements described in the U.S.Office of Management and Budget (OMB) Circular A-I33. Compliance Supplement that could directly andmaterially affect the City of Upper Arlington's major federal program for the year ended December 31, 2012. TheSummary of Audit Results in the accompanying schedule of findings identifies the City of Upper Arlington's majorfederal program.

Management's Responsibilty

The City of Upper Arlington's Management is responsible for complying with the requirements of laws, regulations,contracts, and grants applicable to its federal programs.

Auditor's Responsibilty

Our responsibility is to opine on the City of Upper Arlington's compliance for each of the City of Upper Arlington'smajor federal programs based on our audit of the applicable compliance requirements referred to above. Ourcompliance audit followed auditing standards generally accepted in the United States of America; the standards forfinancial audits included in the Comptroller General of the United States' Government Auditing Standards; andOMB Circular A-l33, Audits of States, Local Governments. and Non-Profit Organizations. These standards andOMB Circular A- i 33 require us to plan and perform the audit to reasonably assure whether noncompliance with theapplicable compliance requirements referred to above that could directly and materially affect a major federalprogram occurred. An audit includes examining, on a test basis, evidence about the City of Upper Arlington'scompliance with those requirements and performing such other procedures as we considered necessary in thecircumstances.

We believe our audit provides a reasonable basis for our compliance opinion on the City of Upper Arlington's majorprogram. However, our audit does not provide a legal determination of the City of Upper Arlington's compliance.

4

Members of Council and MayorCity of Upper Arlington

Opinion on Each Major Federal Program

In our opinion, the City of Upper Arlington complied, in all material respects with the compliance requirements

referred to above that could directly and materially affect its major federal program for the year ended December 3 I,2012.

Report on Internal Control over Compliance

The City of Upper Arlington's management is responsible for establishing and maintaining effective internal controlover compliance with the applicable compliance requirements referred to above. In planning and performing ourcompliance audit, we considered the City of Upper Arlington's internal control over compliance with the applicablerequirements that could directly and materially affect a major federal program, to determine our auditing proceduresappropriate for opining on each major federal program's compliance and to test and report on internal control overcompliance in accordance with OMS Circular A- i 33, but not to the extent needed to opine on the effectiveness ofinternal control over compliance. Accordingly, we have not opined on the effectiveness of the City of UpperArlington's internal control over compliance.

A deficiency in internal control over compliance exists when the design or operation of a control over compliancedoes not allow management or employees, when performing their assigned functions, to prevent, or to timely detectand correct, noncompliance with a federal program's applicable compliance requirement. A material weakness ininternal control over compliance is a deficiency, or combination of deficiencies in internal control over compliance,such that there is a reasonable possibility that material noncompliance with a federal program's compliancerequirement will not be prevented, or timely detected and corrected. A signifcant deficiency in internal control overcompliance is a deficiency, or a combination of deficiencies, in internal control over compliance with federalprogram's applicable compliance requirement that is less severe than a material weakness in internal control overcompliance, yet important enough to merit attention by those charged with governance.

Our consideration of internal control over compliance was for the limited purpose described in the first paragraph ofthis section and would not necessarily identify all deficiencies in internal control over compliance that might bematerial weaknesses or significant deficiencies. We did not identify any deficiencies in internal control overcompliance that we consider to be material weaknesses. However, material weaknesses may exist that have not beenidentified.

This report only describes the scope of our tests of internal control over compliance and the results of this testingbased on OMS Circular A-133 requirements. Accordingly, this report is not suitable for any other purpose.

5

Members of Council and MayorCity of Upper Arlington

Report on the Schedule of Federal Award Expenditures

We have also audited the financial statements of the governmental activities, the business-type activities, thediscretely presented component unit, each major fund and the aggregate remaining fund information of the City ofUpper Arlington, Franklin County, Ohio, as of and for the year ended December 31, 2012, and the related notes tothe financial statements, which collectively comprise the City of Upper Arlington's basic financial statements. Weissued our unmodified report thereon dated June 14, 2013. Our opinion also explained that the City of Upper

Arlington adopted Governmental Accounting Standard No. 63 and 65 during the year, and has elected torecharacterize certain previous transfers to advances. We conducted our audit to opine on the City of UpperArlington's basic financial statements. The accompanying schedule of expenditures of federal awards presentsadditional analysis required by the U.S. Offce of Management and Budget Circular A-133, Audits of States. LocalGovernments, and Non-Profit Organizations and is not a required part of the basic financial statements. Theschedule is management's responsibility, and was derived from and relates directly to the underlying accounting andother records management used to prepare the basic financial statements. We subjected this schedule to the auditingprocedures we applied to the basic financial statements. We also applied certain additional procedures, includingcomparing and reconciling this schedule directly to the underlying accounting and other records used to prepare thebasic financial statements or to the basic financial statements themselves, in accordance with auditing standardsgenerally accepted in the United States of America. In our opinion, this schedule is fairly stated, in all materialrespects, in relation to the basic financial statements taken as a whole.

~."~~Julian & Grube, Inc.June 14,2013

6

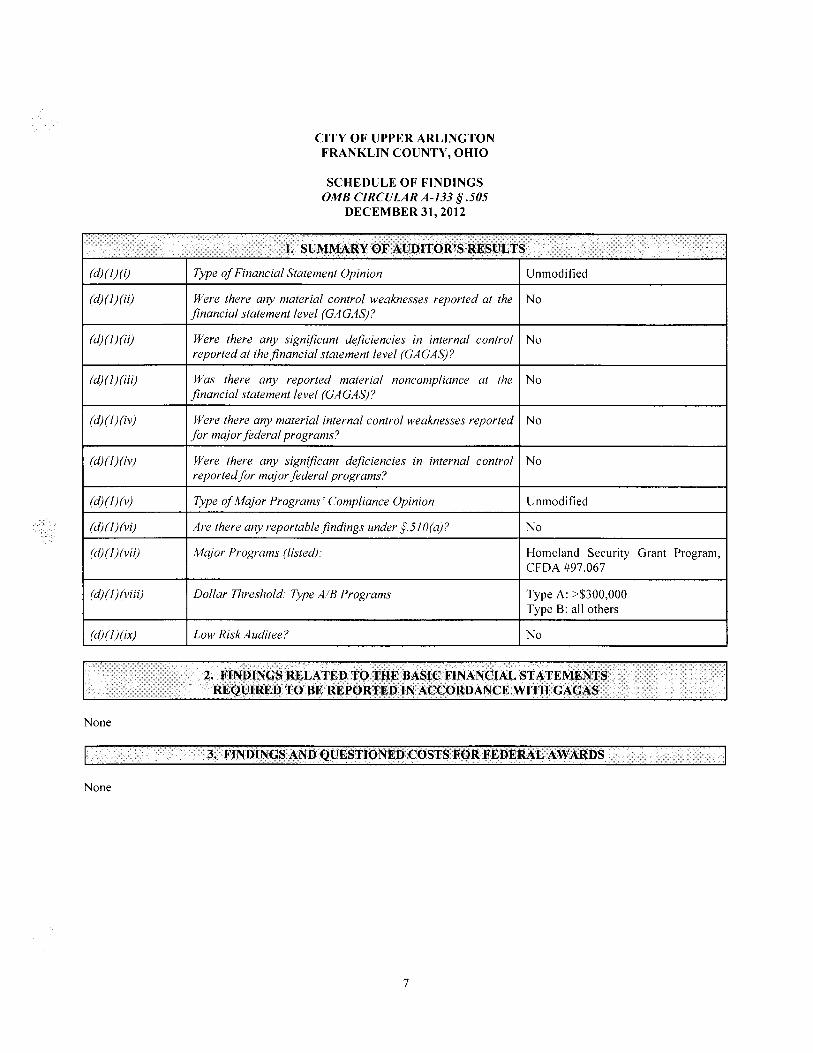

CITY OF UPPER ARLINGTONFRANKLIN COUNTY, OHIO

SCHEDULE OF FINDINGSOMB CIRCULAR A-133 § .505

DECEMBER 31, 2012

(d)(l)(i)

(d)(l)(ii)

Type of Financial Statement Opinion UnmodifiedWere there any material control weaknesses reported at the No

financial statement level (GAGAS)?

(d)(l)(ii) Were there any signifcant deficiencies in internal control Noreported at the financial statement level (GAGAS)?

(d)(l)(iii)

(d)(l)(iv)

Was there any reported material noncompliance at the No

financial statement level (GAGAS)?

Were there any material internal control weaknesses reported Nofor major federal programs?

(d) (l)(iv) Were there any signifcant deficiencies in internal control Noreportedfor major federal programs?

Unmodified(d)(l)(v)

(d)(l)(vi)

(d)(l)(vii)

Type of Major Programs' Compliance Opinion

Are there any reportable findings under §.51 O(a)?

Major Programs (listedJo

No

Homeland Security Grant Program,CFDA #97.067

(d) (l)(viii) Dollar Threshold' Type AlB Programs Type A: /$300,000Type B: all others

(d)(l)(ix) Low Risk A uditee? No

None

INANCIAL STATERDANCE WITH G

3. FINDINGS AND QUESTIONED COSTS FOR FEDERAL AWARDS

None

7

Exhibit B

Exhibit 1

2013 Mid-Year Budget Adjustments

Capital Solid Capnal Law Sewer Bonded Kingsdale Lane Avenue G. O. BondGeneral Asse Waste Equipment Enforcement Surcharge EMS Chelsea Horizon Improvement Estate Core TIF Mixed Use Retirement

Fund Managemnt Fund Fund Fund Fund Fund TIF TIF Fund Tax Fun Fund TIF Fund

Revenue Adjustments from Adopte:Estate Tax 1.800.00Investment Revenue 100,00Ince taxes 630.00 96.770Fines and for1enures (100.00)Miscllaneous revenue 100.00 a aReimbursements 150.00Leese Procs 918.049Bond Refunding a 9,421,859

Total Revenue 2.680.00 96.770 a a a 918,049 a a a a a a 9,421.859

Approprlatlon Changes:Supplementai Apprprations 10.000 12,30 393,600 9,00 54,00 190,087 120.500 0 45,00 22,00 0 9,421,859

Total Approprlatlons 10.000 a 12.30 393.600 9.00 54.00 190.087 120.500 0 a 45.00 22.00 a 9,421.859

Fund TransfenlIn a a

Outa a a a a a a a a a a

Effect on Fund Balance 2.670.000 96.770 (12.300) (393.600) (9.00) (54.00) 727.962 (120.50) 0 a (45.00) (22.00) a a

Consolidate efft on fund bslance 2.838,332

Fund

Supplemental Appropriations

GeneralTotal General Fund

Solid Waste FundCapital Equipment FundCapital Equipment FundCapital Equipment FundCapital Equipment FundChelsea TIF FundEMS FundEstate Tax Capital Projects FundGeneral Bond Retirement FundKingsdale Core TIF FundKingsdale Core TIF FundLaw Enforcement FundSewer Surcharge Fund

Department

Mayors Court

FinanceCity ClerkPoliceElectricalBuilding MaintenanceFinanceFinancePublic ServiceFinanceFinanceFinancePoliceUtilities

Exhibit 22013 Mid-year Review

Supplemental Appropriations

GrantedCategory Request

OTPS

OTPSCapitalCapitalCapitalCapitalOTPSCapitalPSOTPSPSOTPSOTPSCapital

Description

10,000 Additional cost for jail bill10,000

12,300 Operating expenses

4,000 Replacement of Microfische machine123,500 Capital previously appropriated in LEF

6,100 Additional amount needed for increase in street light poles260,000 Replacement of the Salt Barn120,500 Refund of prior year revenue190,087 First of five lease payments for ladder truck45,000 Charges for Engineering work

9,421,859 Record refunding of bonds and treasurer/auditing feees3,000 Charges for Engineering work

19,000 Bond Issuance Costs and additional for School TIF payment9,000 DNA testing

54,000 Replacement of sewer camera and transporter10,278,346

S\Mid Year Information\2013\13_Mid-Year_Review

2013 Mld-year trnsfer of Approrlatns

From ToFund Departent Category Fund Departent Cateory

Tranafera wiin the same fundGeneral Fund Cit Manager OTPS Geneal Fund City Manager PSLAU Stre Capitl LAU Strs PSla Enforcment Fund Police PS la Enfoment Fund Police OTPSLaw Enforcmet Fund Police PS la Enforent Fund Police CapitalBonded Improvement Fund Strts Capil Bonded Improvement Fund Public Seces PSInfrstrure Fund Strts Capital Infrstruure F udn PubliC servces PS

Amount Desption

13.700 Transfer funds for intems not previously budget10.000 Engineering Inspeon4,000 Lese paen for morce5.100 Additinal capital for in car data terminals

25.000 Engineeng Inspeon12.000 Engineeng Inspeion

Exhibit 3

13_Mid-Year_Revie

Exhibit B

2013 Mid-Year Budget Adjustments

Capital Solid CapKal law Sewr Boned Klngsdale lane Avenu G.O. BoGeneral Asset Walle Equipme Enfotcement SUTch.ge EMS Cheliea Horizon imprment Esi.t. Cor.TIF Mix.ci Ui. R.tirem.nt

Fund Man.gemnt Fund Fun Fund Fund Fund TIF TIF Fun Tax Fun Fund TIF FundR.v.nu. Adjustments from Adopted:

Eitøt Tax 1,800.00Inveitment Revenue 100,00Incoretaxei 630,00 96,770Fines and fort.Kures (100,00)Miscllaneous renue 100,00 0 0Relmburs.ments 150,00Le..e Procees 918.Q.9Bond Refnding 0 9.421,859

TolBl Revenue 2.880,00 96,770 0 0 0 918,Q.9 0 0 0 0 0 0 9,421.859

Approprt.tion Ch.ng..:Supplemental Approprøllons 10,000 12,30 393.800 9,00 54,00 190,087 120.500 0 45,00 22,00 0 9.421.859TOIBI Approprl.tlon. 10.00 0 12,300 393,600 9,00 54,00 190,087 120,500 0 0 45,00 22,00 0 9,421,859

Fund Tr.n.f...

In 0 0Out

0 0 0 0 0 0 0 0 0 0 0

Eff.ct on Fund B.I.nce 2,670,00 96,770 (12,300) (393,80) (9,00) (54,00) 727,982 (120,50) 0 0 (45,00) (22,00) 0 0

Con.olld.ted ."eet on fund b.l.nce 2,838,332

Fund

Supplemental Appropriations

GeneralTotal General Fund

Solid Waste FundCapital Equipment FundCapital Equipment FundCapital Equipment FundCapital Equipment FundChelsea TIF FundEMS FundEstate Tax Capital Projects FundGeneral Bond Retirement FundKingsdale Core TIF FundKingsdale Core TIF FundLaw Enforcement FundSewer Surcharge Fund

Department

Mayors Court

FinanceCity ClerkPoliceElectricalBuilding MaintenanceFinanceFinancePublic ServiceFinanceFinanceFinancePoliceUtilties

2013 Mid-year Review .Supplemental Appropriations

GrantedCategory Request

OTPS

OTPSCapitalCapitalCapitalCapitalOTPSCapitalPSOTPSPSOTPSOTPSCapital

Description

10,000 Additional cost for jail bil10,000

12,300 Operating expenses

4,000 Replacement of Microfische machine123,500 Capital previously appropriated in LEF

6,100 Additional amount needed for increase In street light poles260,000 Replacement of the Salt Barn120,500 Refund of prior year revenue190,087 First of five lease payments for ladder truck45,000 Charges for Engineering work

9,421,859 Record refunding of bonds and treasurer/auditing feees3,000 Charges for Engineering work

19,000 Bond Issuance Costs and additional for School TIF payment9,000 DNA testing

54,000 Replacement of sewer camera and transporter10,278,346

S:\Mid Year Information\2013\13_Mid-Year_Review

2013 MkI-y..r Inn.fer of Approprletn.

From To

Fund Depertent Category Fund Departnt Cat!!Tl'ni'.,. wlln thi um. fundGeniral Fund Cit Manii OTPS Genal Fund Cliy Mlllgir PS

lAU Slreel Capitl I. Slre PS

law Enforcment Fund Pollee PS l8W Enforcmenl Fund Polic OTPS

law Enforcmet Fund Polic PS law Enform.ent Fund Polic Capital

Bonde Impromenl Fund Slrls Capil Boned IrproV4menl Fund Public SlIeel PS

Infraitiure Fund Slreels Capital Infritrure Fudn Pubic Servcei PS

Amounl Descpton

13,700 Tranirer fui lo Inlemi nol prviosly buget10,000 Englniirlng inspeio4,000 leaii peen fo motoe5,100 Aditial capll fo In ca data Iermlnali

25,00 Enginering Inipe12,00 Enginering Inspe

13_Mld-Year_Revt8W

Exhibit B

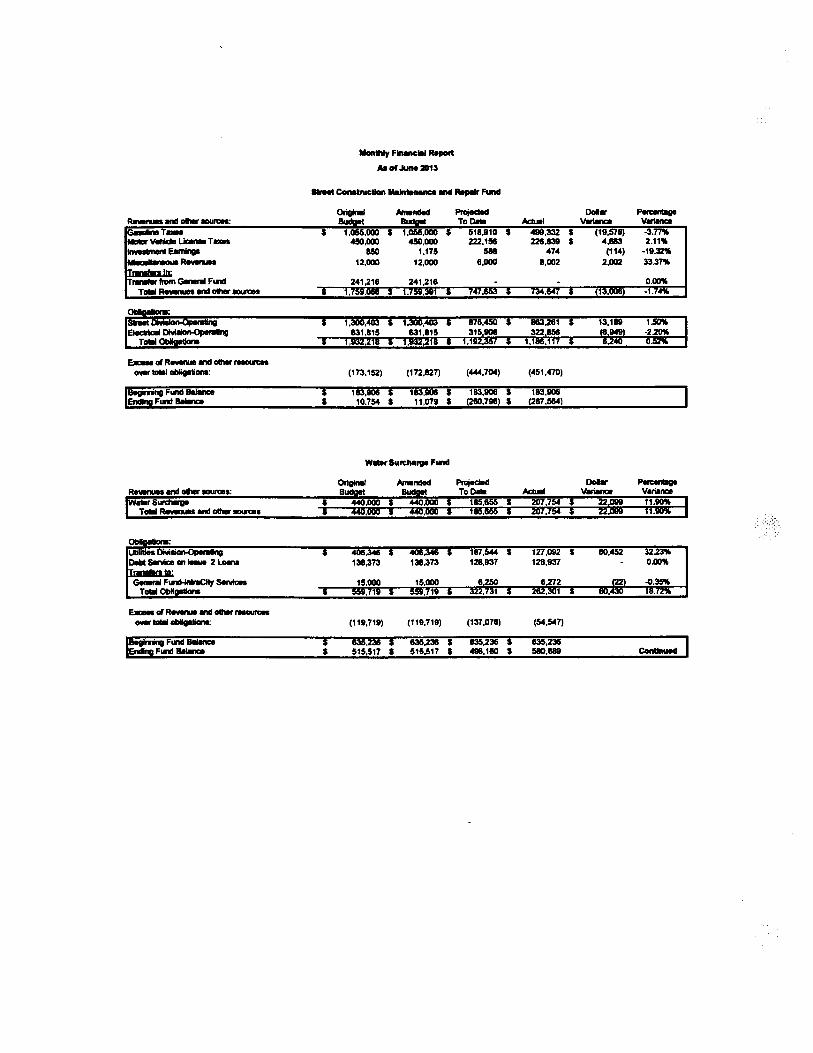

0r1n Ai Pr Do'" PeII IY I2 ~ ~ ~Inc Tii 5 13,676,8! 5 14,30,8! 5 1,55,48 5 8,54,21 5 95,76 1.12'~I & io Pr Tii 5,35,518 5,35,518 2,94,01 2,82,512 (16,57) -0.56%E. Tii 1,00,00 2,10,00 2,00,34 2,00.34 0 O.llL- Gc FlI 1,00,21 1,00,21 85,20 68,010 9,801 1.51%Pr Tii RoIll 76,00 786,00 312,50 371,150 (4,35) -1.14%ui en Pe 94,00 94,00 58,77 51,521 (15,21) -2.55%C' rc se 90,00 90,00 72,89 75,03 34,34 4.75'FN, CO & For 42,00 32,00 192,070 186,587 (6,473) -3.37'I~Ea 184,120 28,120 184,~i 191,33 11,451 3.49e. TV FrM F_ 58,00 58,00 367,186 40,2 42,074 11.48....R_ 25,00 35,00 297,50 324,11 27,35 9.2R~ 75,00 22.00 20,50 ~,n5 1,2 0.1lI :Tii in Rw FlI 5,00 5,00 - - - O.lls. S- Flß & I' 29.00 29,00 12,08 10,08 (1,99) -18.50%W.. Su F~ & fu 15,00 15,00 8,250 8,22 22 0.35%Sl ~ F~ & fu 28,00 28,00 11,867 7,25 (4,415) -3.84%- - linPo en Fin Pe Fun 2,56,00 2,55,00 1,275,00 1,12,174 37,174 2.92Ha T1F Fii 1,379,711 1,379,711 . - 0 O.llTiM ~ .. Cl IO S 29,l~T Ii Ii 11S,li.44 Ii 2I,2 .1%

IIIy i=i "-rtAs or Ju 203

Gell Fii

OI.i:Po Dh 5 7,39,18 5 7,39,18 5 4,116.871 $ 3,9n,242 5 139,63 3.39Fin DI 8,29,759 8,29,759 4,43,52 4,219,92 210,60 4.75%EI ~ Hu 211,548 211,54 211,54 20,79 4,754 O.llP. .. Reio 2,913,879 2,1113,879 1,81,021 1,55,531 34,410 18.14%Cc & Ec:c Dela oe 1,08,750 1,08,750 615.46 59,824 17,641 2.87'PUIC Si Ai 1,03,1172 1,03,972 55,31 38,159 170,2 3O.48S1 DI 45,94 45,94 136.48 115,470 21,014 15.4OFI Me Di 710,6111 710,819 38,641 38,03 17,80 4.1lCi.. 747,2 747,2 44,158 43,_ 5,55 1.2Ci An 740,481 740:481 423,58 40,314 20,246 4.7nCi1 Cle 273,m 273,9n 159,82 122,11 37,158 23.25'Ci1 CoI 136,58 138,58 73,537 89,181 4,35 5.92CIe~Cc 312,641 312,841 171,85 189,331 (10,471) -l.lIFnn 1,157,2 1,157,2 881,72. 60,031 57,89 8.72FdI Miil_ic 175,750 175,750 4I,55 43,10 57,95 11.67'Ir Tec 14,12 14,82 470,367 43,108 36,2 7.71%~ Ad 1,59,62 1,59,82 1,133,115 1,073,34 59.77 5.2T"ep~ 28,71,_ 21,788,16 18,38,64 15,190,151 1,193,482 7.2%Ti: Tii 1n1.1I Fii 3,675,48 3,675,48 3,675.48 - O.llEc oe II FlI 50,00 5O,OO - - - O.lli. A_ MI u. T1F FlI 110,071 110,071 - - - O.llCMI s. Co 20,00 20,00 20,00 20,00 - O.llsi Co M8 & Rep FlI 241,218 241,218 150,00 150,00 - O.llir FlI 75,00 750,00 75.00 75,00 - O.llTci Obiø S S 34,135,641 S S 19JII,II S 1.193,48 ~e- ~ R- MI Cl ~_tiot~: (51,310,755) (2,30,241) (2,58,lI (1,165,21)

TCù IlmI FlI iiEndFlI~En FlI ~TiM En FlI B8

519,30,2435,46,3812,53,123, ',-

518,30,2435,487,3811,53,637

S17,lI,lI

$19,30,2435.467.3811,2711,992

518,30,2435,487,3612,875,iin

Iil1S,l4J,04Conue

Monly Fliw Rert

M or Ju 203

8t Coc1on ..i-na_ ui R..Ir FundAi Pr oc Pene~ en ai Il ToC. ~I v. v.

GaInT_ $ $ lI,58 $ 66,378 $ 53,78 8.84%MaVlhcl Uc T_ 281,675 28,lI 1,017 0.39III e. 58 474 (114) -11.32Miiiie R- 7,00 8,152 1,152 16.46Ti In:rwfn Ge Fin 241,216 241,216 150,00 150,00 0.00Tea ~ II oI IO 1, 1,

$ 1.30,40 1,30,40 $ 15.54.42 $ 16,991 $831,815 631,815 38,55.75 375,82

, 1

e- øi R- .n oI..__ ia oblp: (173,152) (172,82 (29,249) (26,818)

$ 183,10 $ 183,10 $ 183,10 $ 183,10$ 10.754 $ 11,078 S (115.34) S (7,012)

Wni 8imllrg Fund

OriM ~ed Pr 00.. Peee~.. ai.c: To DI Ad Vii.- v.W..Sw $ S 215,270 $ 23,56 S 21,313 1.9OTol ~ II oI IC " 1

Ull1 Oivi8 S 40,34 $ 40,34 $ 218,80 $ 147,178 $ 71,624 32.~Oell Se on i- 2 ~ 138,373 138,373 128,83 128,937 0.00T..to:Ge Fiiniit 5e 15,00 15,00 6,250 -8,272 22 -4.35%

T_Obl , 1

e- ølR- en oi__1D oblp: (119,711) (119,719) (138,719) (45,80)

Be Fin s. $ 63,236 $ 63,2 $ 63,236 $ 63,23Fin a.18 $ 515,517 $ 515,517 $ 49,517 S 58,43 Conue

ii Finane'" RertM or Ju 2013

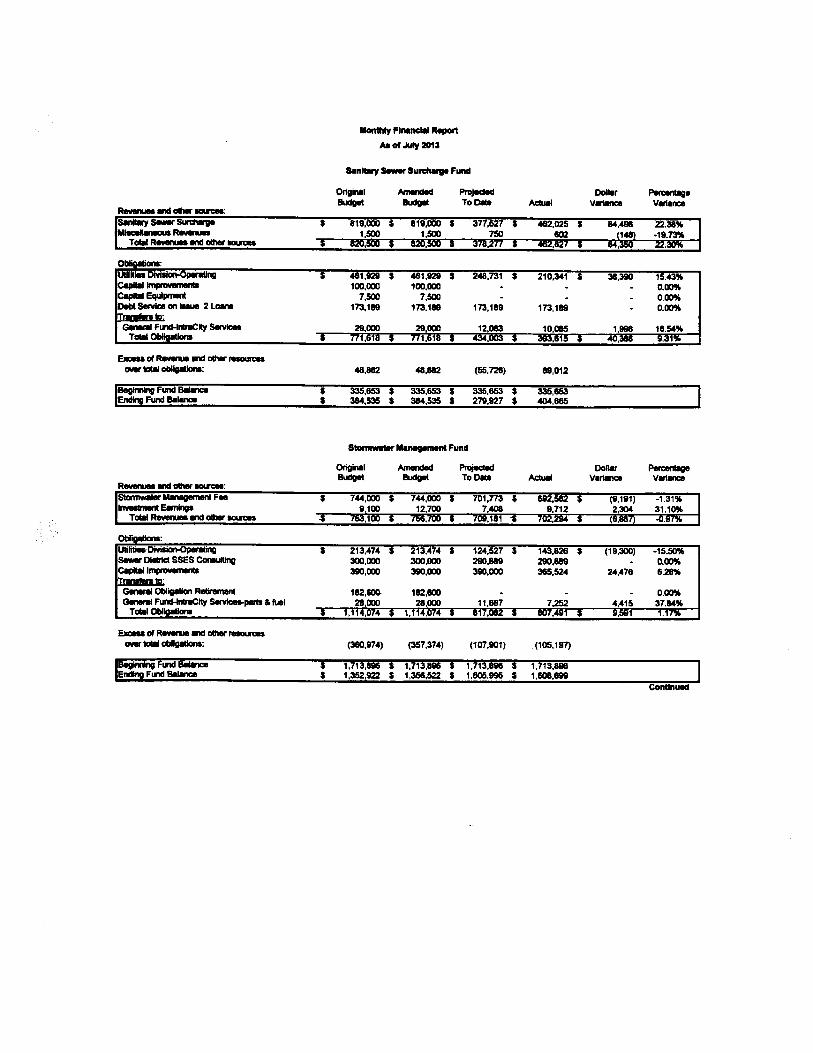

"nltry S- Surcig Fun

Orinai Amed Prje Coiir PeBu Bu Too. Ad V.- VarR-8I00_S- SI . 819,00 . 819,00 . 377,527 . 46,025 .~R_ 1,50 1,50 750 10Toll R- .. 00 Il

O~:Ul . 481.92 . 481,92 . 248,731 S 210,341 $ 38,39 15.43%c. ir 100,00 100,00 0.00c. Equii 7,50 7,50 0.00o. Se on ia 2 L- 173,189 173.189 173,189 173,189 0.00

GI Finnl1t Se 29,00 29,00 12,08 10,08 1,_ 111.54%Tol T T7i ,618 $ 77I,ti111 $ 4a,lI $ ;),115 $ 41,_ 9.31%

e- at R. n ol-.lM lo obig: 48,88 48,882 (55,72) 11,012

il Fun ii . 33,65 $ 33,65 S 33,65 $ 33,65Fun 8Ii. $ 38,53 $ 38,53 S 279,927 $ 40,86

Stomi MaMgnt Fund

Orinal Am PrIl Coll Pe ceeBu Bu ToDi Ad Verl VerR-. nol_S1 Me Fee . 744,00 . 744;0 S 701,77 . 692,58 . (9,191) -1.31%In Ee 9,100 12,70 7,40 9,712 2,30 31.10'Tol ~ n ol -. ,I ,1 ( .

UlIi DiOpin S 213,474 $ 213.474 $ 124,527 $ 143.82 S (19,30) -15.~S- Di SSES Co 30,00 30,00 29,889 29,_ 0.00CeIni_,... 39,00 39,00 39,00 36.524 24,476 6.2GI OIip Re 182,sæ 111,60 0.00~ FlIlI s.pe & ful 28,00 28,00 11,667 7,25 4,415 37.11%Tol OIii T 1,114,074 . ,114,074 $ 1117,ll $ li7.491 $ 11.511 .17%

e- at R- 8I ol I8lM ta ci: (36,974) (357,374) (107.901) (105,197)

BI Fun Bi $ 1,713,896 $ 1,713,8l $ 1,713,81 $ 1,713,896Fun 8I $ 1,35,92 $ 1,35,522 $ 1,60.99 $ 1,60.69

COnue

IIIy Fina'" R.,M CI Ju 203

Soid W..... Fun

OrIMII AmBudge

PrTo o. Ad

Do_Vln.

Pe.. illV.-R-.ln ai -.'s. d .i S 1,421,00 S 1,421,00 S 13,122 S 137,73 S 4,914 0.51s.d~ 20 20 100 - (100) -100.00Ai .. F_ 541,00 541,00 53,188 50,3l (29,873) -S.81 'l

p_ ti pr 1. 30,00 30,00 30,00 27,750 (2,250) 0.00I"" .. 2,00 7Ò 40 1.042 13 155.18%Toa R-1n ai IO :5 1,99.2 :5 1,!l,1I :5 1,39,_ :5 1,_,823 :5 (2t,ti75) -1.111""

0b1p:RI .. rein cole co S 1,887,074 S 1,187,074 S 876,93 S li,724 S 13,nK) -o.39.. tm pr 1. 30,00 30,00 17,50 17,05 45 2.57'~ .-fe 8,00 6,00 4,50 - 4,50 100.00Dlfw 318,188 318,188 184,44 184,33 107 0.06Ml-i.. (bliln .. & 8l1c pr) 14,00 14,00 5.13 7,619 (1,78) -30.61%

Tei :5 2,ll,2t S 2,ll.2 :5 1,lBl,210 :5 ,1Bl, r21 :5 (5111) -0.04""

~ d R-... ol If_lc oI.i:Be~ Fun BUEnl Fun a.

ss

(88,06)

88,2 S147 S

(70,36)

69,2 S(1,153) S

69,2 S275,497 S

69,2248,30

20,2 179,09

Swming POL Fund

Orna Cu Pr Do_ Peni8u Bu Too. Adl V.n v.iR_.. ol 1O:C/ fO Se S 84,00 S 84,00 S 54,515 S 47,311 -7.93Tcil R_~ .. lI IO , 1

S 65,961 S 65,961 S 32,481 S 319,997 S 5,48 1.88'l1

~ d R__1n ol r._ til obl: (10,961) (10,961) 271,34 22,518

Be Fun BI S 411,13 S 493,63 S 49,63 S 493,83En Finøm S 482,615 S 482,675 S 784,981 S 723,154

Conue

IIIy FIM'" R.". Of July 203

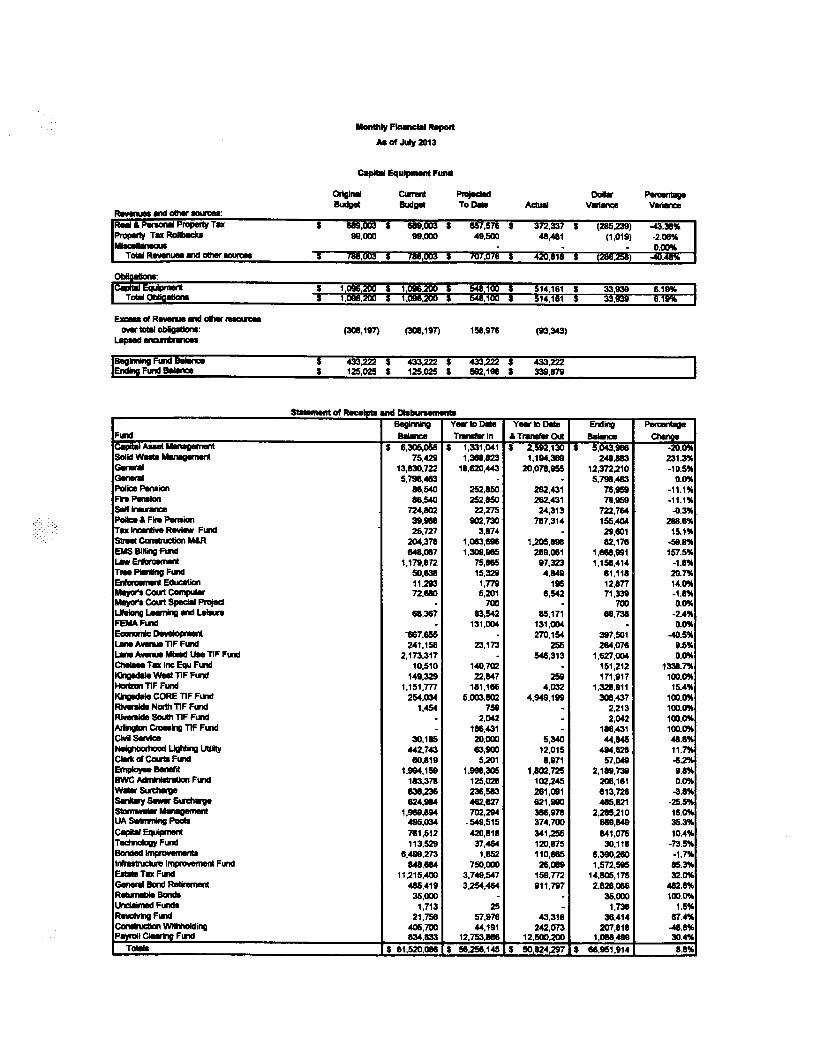

c. Equipm func

OriMI Cu Pr Do.. P.Bu Buli To DI Ac V.n V.nR_II 0l 1C:Re & P. Pn T.. $ 88,00 $ 61,00 $ 857,576 $ 372,337 $ (28,2) -4.31%ii T.. Raii 99,00 99,00 49,50 41,411 (1,019) -2.08Mi- 0.00Tci ~U8I1 0l IO ii 'lM,uu ii 'lM,UU ii IU/,U/rJ ii 4¡¡,1l111 ii 12l1,2:) -4._

$ 1,09,2 $ 1,09,20 $ 54,100 $ 514,161 $ 3393 6.19%1, 1, 14, 1

~ TI R- II oI___ti~: (30,197) (3,197) 158,976 (9,34)i. enBeinn FlI EI $ 43,2 $ 43,2 $ 43,2 43,2Fun EI S 125,02 S 125.02 S 58,198 . 33,879

sm Of R__ and D11iBelm v..1DDI V..ID Di Endin Pe

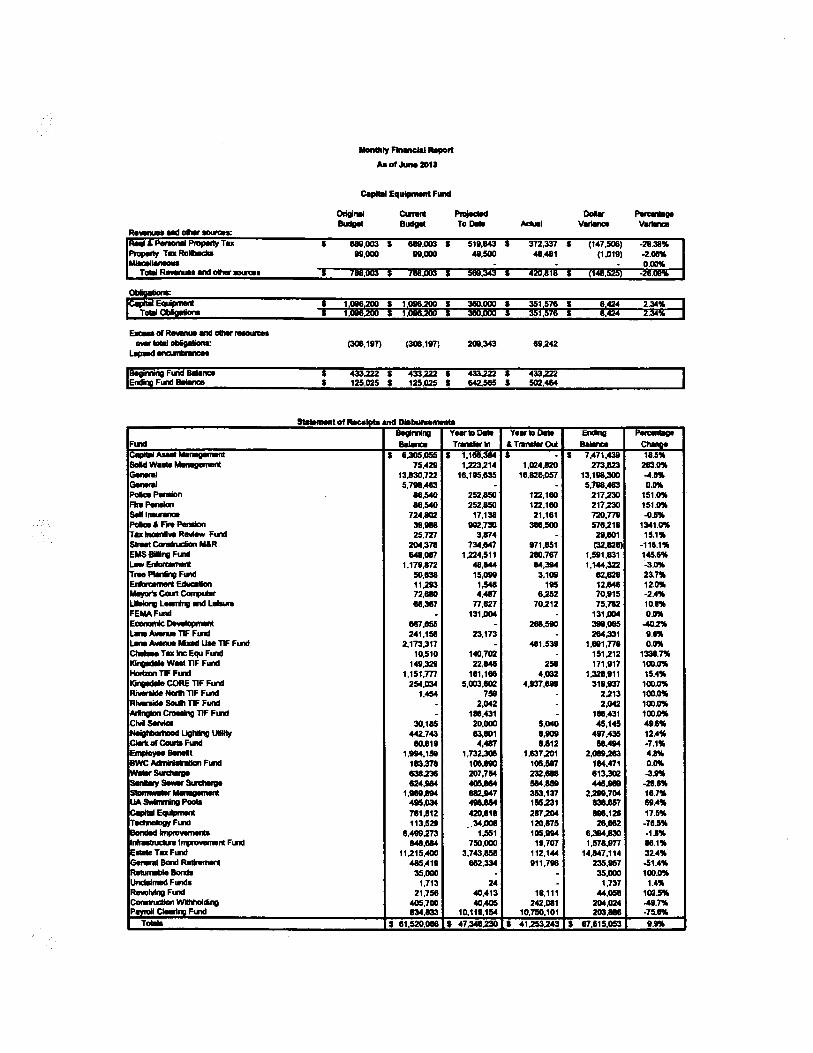

Fun Il T,.ln &TI'OU Ba CICa A. MaiM S 8,30,05 S 1,331,041 I ii 2,58.130 S 5,04,98 -20.0%Soid W.. Ma 75,42 1,38,82 1,194,. 249,88 231.3%~ 13,83,722 18,82,44 20,078,95 12,372,210 -10.5%Ge 5,79,48 - - 5,79,48 0.0%Poic Peio 88,54 25,850 26,431 78,96 -11.1%Fn~ 88,54 25,85 26431 76,96 -11.1%Se In 724,80 22,275 24,313 72,784 -0.3%Po & Fn Pe 39,_ 90,73 787,314 155,4O 28.8'IT.. ii Re Fun 25,727 3,874 - 29,801 15.1%iS Co M& 20,378 1,083,89 1.2,888 82,178 -5.nEM Bill Fu 84,087 1,30,1I 289,081 1,88,991 157.5%LI Ei ib Ci 1,179,872 75,86 97,32 1,158,414 -1.8%T_ PI Fun 5O,l3 15,32 4,ll 81,118 2O.7'ElGG cal'" Ec 11.29 I,m 195 12,8n 14.0%Mai CC Cc 72,88 5,201 8,542 71,33 -1.nMa CC si Pn - 70 - 70 0.0%L. L. an L. 68,367 83,54 85,171 68,73 -2.4%FEFun . 131,00 131,00 - 0.0%Eco De -'7,85 - 270,154 397,501 -4.5%i. A_ TIl' Fun 241,158 23,173 25 26,078 9.5%.. "- Mlø u. TIl' Fun 2,173,317 - 54,313 1,627,00 0.0%ci r.. In Equ Fun 10,510 140,702 - 151,212 133.7'Kl W8 TIl' Fun 149,32 22,847 25 171,917 100.0%Ho TIl' Fun 1,151,m 181,188 4,03 1,328,911 15.4%~ COR TIl' Fun 254,03 5.00.80 4.94,199 30,437 100.0%Ri No TIl' Fun 1,45 758 - 2,213 100.0%Ri So TIl' FlI - 2,04 - 2,042 100.0%Ailn Cr Tl Fun - 188,431 - 188,431 100.0%Civ Se 30.185 20,00 5,34 44,84 48.8'~ Ug l/llt 442,743 83,90 12,015 49,62 11.7'Ci. TI Cc FlI 80.819 5,21 8,971 57,04 ~.2eni Ilil 1.99,158 1.99,30 1,80,72 2,189,73 9.8%øw Ad FlI 183,378 125,02 102,245 20,181 0.0%W*Sw l3,23 23,58 281,091 813,72 -3.8%Sa se ~ 624.ll 48,827 821,ll 48,621 -25.5%Sblis..r M8-ø 1,98,89 70,29 38,1178 2,28,210 18.0%UA Sw Po 49,03 .54,515 374,70 66,849 35.3%Cal Eq 781,512 420,818 341,2 841,075 10.4%Tecog FlI 113.52 37,4& 120,875 30,118 -73.5%Bo In 6.49,273 1,85 110,86 6,39,2 -1.7'IrI imi Fun 84.68 750,00 28,08 1,57,58 85.3%EI T.. FlI 11,215,40 3,749,547 158,m 14,80,175 32.0%Gel Bo Re 48.419 3,25,4& 911,797 2,82,08 48.8%Ri II 35,00 - - 35,00 100.0%lJ Fun 1,713 25 - 1,73 1.5%Re Fun 21,758 57,976 43,318 36,414 87.4%Cll WIing 40,70 44,191 242,07 207,818 ...8%P8v1-Ci Fun 83.83 12,753,88 12,50,20 1,08,49 30.4%

T'" S 81,52.08 S 56.2,145 S 50,824,27 S 86.951,914 8.n

ii Fii ReAa or Ju 203

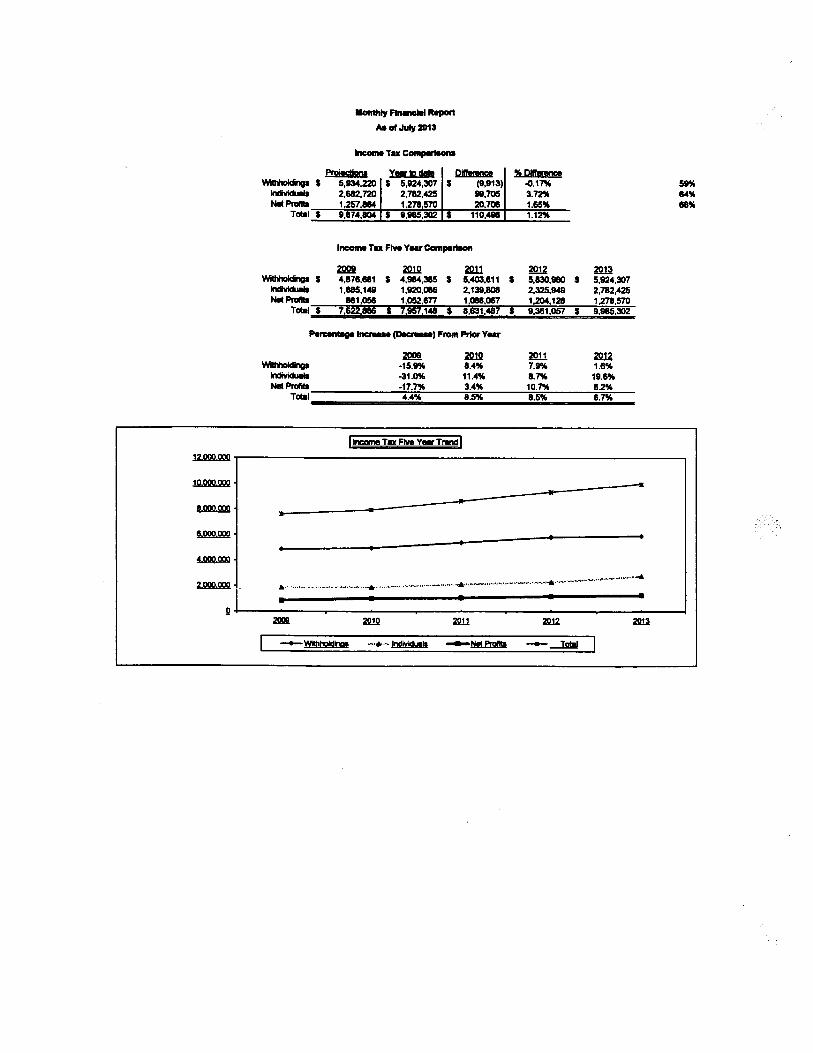

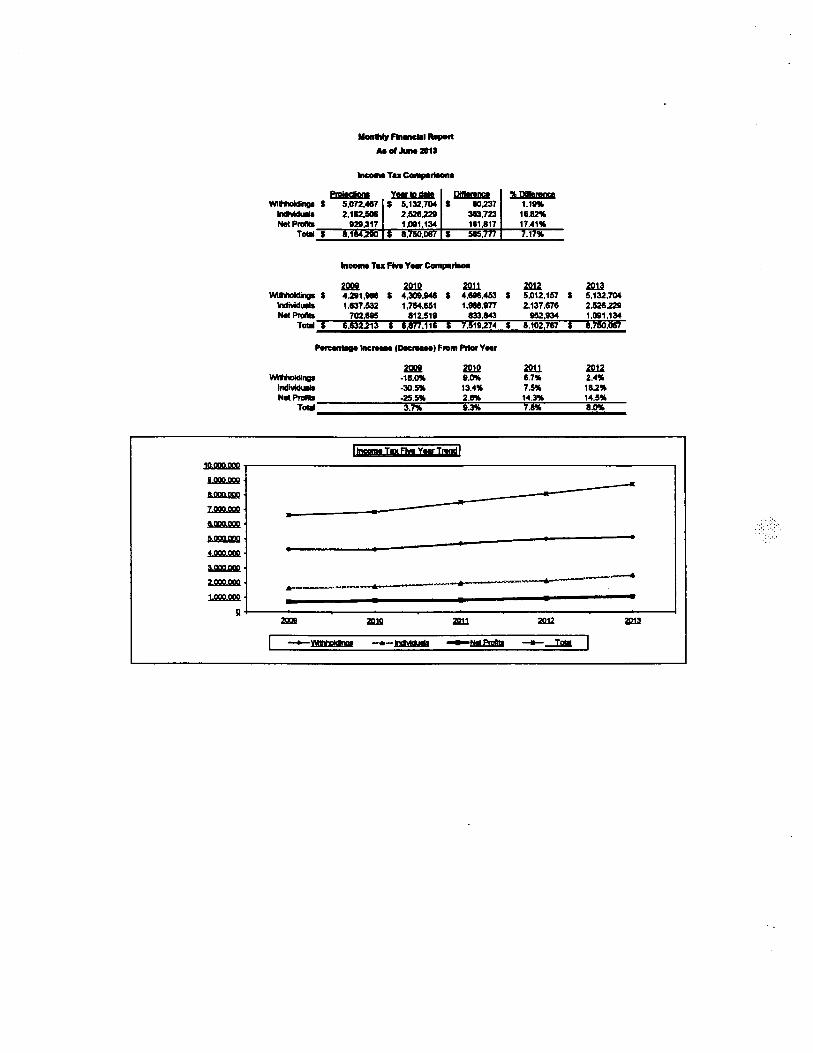

in Ta COliia

WlngInNe Pn

Toii

Pi ywtidl Ql % tl$ 5,13,22 $ 5,924,307 $ (9,913) -o.17'

2,61,72 2,78,42 99,70 3.72'1,57,88 1,278,570 20,708 1.65%

$ 9,874,80 $ 11,11,30 $ 110,498 1.12'

!i11%88%

Inme Ta Fiv Y..Copert

ZQ ~ 2Q ~ 2013WIng $ 4,876.111 S 4,98,38 $ 5,40.611 $ 5,83,98 S 5,924,307In 1,88,149 1,92,08 2,139,80 2,32,94 2,782,425Ne Pn 861,05 1,05.677 1,08,087 1,2,128 1,278,570

Toi $ 7,62,_ $ 7,95.148 S 8,631,487 $ 9,361.05 $ 9:85,302

Pvli Inc_ (oe) Fro Prr Year

WiInIlNe Pro

Toii

ZQ-15.9%-31.0'-17.7'4.4%

2l8.4%11.4%3.4%8.5%

2Q7.9%8.7'10.7'8.5%

ml1.8'19.6'1I.28.7'

IIn Ta Fiv Y.. Trw I12.1:i

-..IJ .110000~

.........."............,....."...... ._.-......-....._._..-..._".....~................ ...... -"......................... .................. . . .Z.

II 2! 2l 21 2! 21-- Witi .....-. ~ _Ne Pr -- --

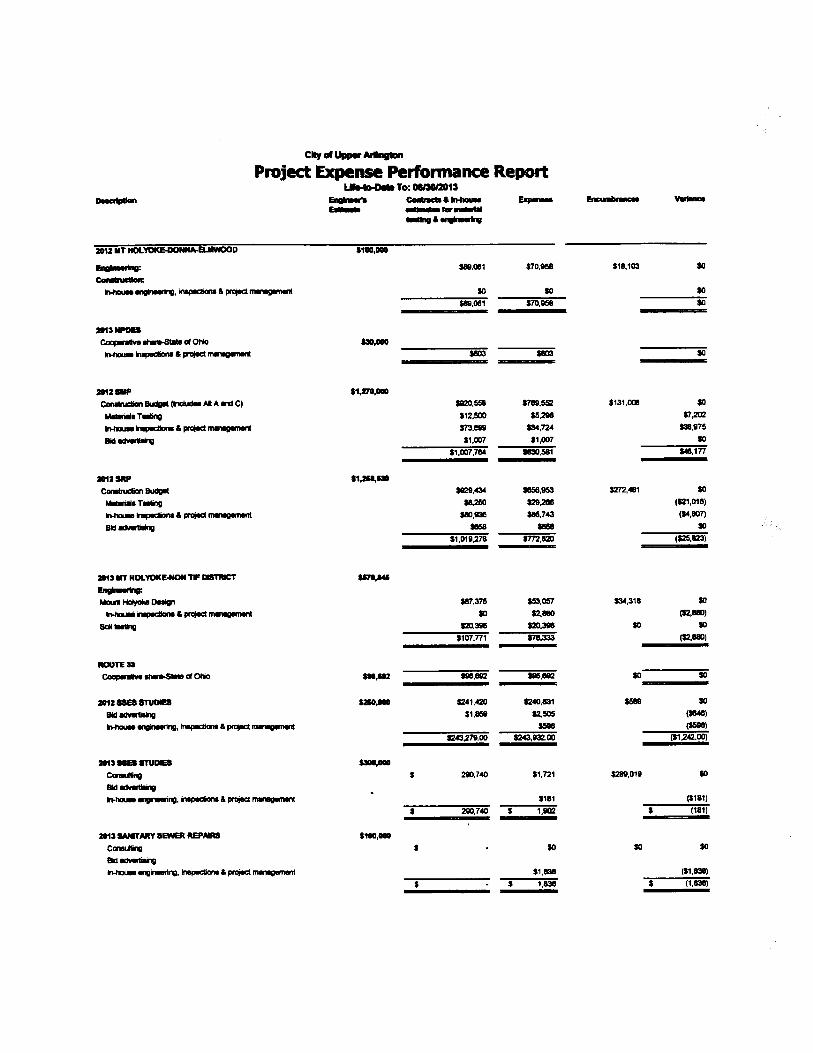

CIt of Uppe ArInProje Expense Perfnnnce Report

LI To: 1l13o- ~ e:._ E. ~ v._ie ..to-......202 IIE Pt IEi.~.. S2216 $læ,127 1111,0l so~ 11,21,_ea Bu $8,li $8,li so so~T.i 17.50 so so 17,!iin -v, inar & pr rn 174,144 53,96 $4,1811I.i S3 $3 so

11,20,100 '-,33 $47.881

203 -.E PH.~e: $2....Ca BuT.. ìn Ri $99 $97 112 so..T-.in ~. mi &- --i- $170 (1170)Bi~

1919 11,077 (1170)

202 GAWI CULVE ".0~CG Il $6.80 $6,80 so_T-- 1750 1750in ~. Np & pr mr $3,120 171 S239

18,870 ini $3,148

203 ANNUA im II 11,M1~Ca Bu $8,745 19.745_T-- 111.11 (111,11)in ... ii & pr-,... 119,2 (119,22)1I~ Il (I

~9,745 $31,758 lI,'J202 LAE AVEUE. WE WATEESII..-~.' 1128,88 1123824 $4.857 so~ 11.aa~Bu ",æ1 ",æ1_T.- 115.00 115,00in np _ prlI 1115,788 11,172 1114,614

11,1*,~i 11,172 11.æ3,lI

..2 LM AVEUE DET . TR CA 110.0En-i 11~,20 18,175 $4,03 so~II & c_ Tr8 c. $6,475 15.250 12.221 soIn on. no & pr ma 115,00 124 $14,976

$2.6l 1147,45 114,978

CI 01 Up ArinPrjec Exns Perfrmance Report

~ To: 0I13IM rn c:__ Ei En.. -~ ....-.-.-....i~20Z lI Il YOE-NNAEU $1.,_En 18,0i1 $70,95 $18,103 soc:.. en, in & pr II so so so

18,0i1 $70,95 so

203NPDc: -. c6 0I S3,_.. in & pr ~ 16 16 so

20Z.. $1.m,DCø El (ir No A .- C) Sl.55 S789.55 $131.00 so_..T-. 112.!l $5,21 S7.2l.. i. & pr II $73,_ $3,n4 $3,975

Bi ec $1,007 $1,007 so

11,007,7ti S8.581 $4,1n

20S1P $1.-13Cø El sø,43 $8,95 $2,481 so_T-. 18,25 12,2 ($1,0111)

.. np & pr II $8,83 18,704 ($,80Bi~ $8 $8 so

$1,0111,278 S72,S2 ($,82)

20UI1' HOL YOE-N TW ii SIEii....=Mo Ho Da $8,375 S5,D5 13,318 so..ii & pr ~ so $288 ($2,88)

SC-. $2,3l $2,_ so so

$107.n1 $1,33 11,88)

RO'Æ33eo ~ or OIo ..m .,8l ..I~ 10 10

20Z lI STUDIES .. $241.42 $240,831 S5 soBi~ $1,1l $250 (J)in ~. ri & pr nwen .- (S5)

$2,271.00 $2.ll00 ($1,242.00)

203l1 STDI $3-Ci: 1 29,740 $1,n1 $2,0111 so

BI ecin~, inon & pi ii... $181 ($181)

1 m.74O $ 1,02 1 (181)

203l1ITMY SEW REAIRS $100._Ccng 1 so so so

Bid m-Ir .., in & pr ~ 11.83 ($1,83)$ 1 1,83 1 (1,83

-piCI 01 Uppe Arn

Projec Expnse Perfnnnce Report~ To: lI13~ e:i.. EiEo ....-i..1...-.~ v.

213 WM TH RO PH., AND. S31t114Can Bu~ 54.010 14,828 13,182 soC_ Np $175,5l so 175,5l so- en, inon, pnli & n. $13,1I $10,_ S3,3l7

$2,e $5,317 S33l7

CAE CUVET I ED DlIU $111'-

COI Bu Sl.2l S4.lI $2.. so~T.i So,0! $183 13,870e-np $12,3l $4,52 ($1,137)_ np & pm.c ~ $1,84 18,135 ($4Bid-- $l (18)Sl,3l 541,36 (S,ol)

IIY BRIECo Bu $3,_ S3,00in. i' & pn II 12,471 (12.471)EnMW Sl,II 151,418 $12,189 so

S3.1I S5.88 so

LAE AVEUE 1U1IE DEEN $1.80_t. A.. R.. Il si $35,00 $35.00.. A~ e.W _ Sl $100.88 15.878 18,189 soLo Ec De Ad 18,00 $8,00 sow-.. .,00 18.00Ml Ho R-i De $101,82 $14,m 33,348 soMI. Hc Coid. _ru So12,5O S42,5OT..~ $13,50 $11,88 $1,83 soCa (e.o & ii 1l) $24I,45 $207,524 381,83 so~T"'~ so so soC_ ir $2,_ 12,174 18,43 so..- in& pr~ S23 12,711 ($.488)ii & Ed.. 141,82.00 $141,82 so

So,017.8l 12._,157 18,00

"-..-ii~""'~31,2IJ

..__~T..101 ~FLr 2.lI.512111 Pa Pw FLr 22.41104 Ff"-FLr 22.41107 "' and Ff Pw FLr 7~._101 e. E~ Fun 372.337

301 8i R. Fun 472.014

5.017.55

.... Uo "'~254 i.-.nFFLr 23173

255 a-T.I_E~FLr 138,0l25 Ai Cl TIF FLr 111,517

25 ~ WMTIF Fu 22111

25 .-nFFLr 1.,.,.25 Ki Cc nF FLr 174.lI281 __nFFLr 758

26 _ Sc nF Fu 2,042

Tll 7m.1I

_Tu101 eiFLr 1I,ll,21111 c._Ma_..dFLr 1.331.041

Taii 11._.31

~Tu101 eiFu 2.007,34

......,._å1_101 Li Go Fu lI.01025 ~CO nF _ 040 e- Twx CI Pn 18.587245 FE FLr 131.00~Tu~.___~:101 ei Fin 378.150

103104107 "' wn F"n _ Fun 161.73LOL Cw Eqo Fu ...41130 ei 8i ~ 1li.3225 a- Twx I.. ECl Fin 1.ll25 ..CnTwxl__Di 25.111425 io WM nF Fu 111T_ 1.11111.411-~

20 sn __ & ~Fu ll.37S--~20 s. __ & Rw Fun 26.11

i._'*101 Ge Fin 58.528

---.-~TwII II Jiir:n. au

0...,...101 coFI 75,032( ~.. & ReFun 0

217 T_ PI Fun 15,32

210 EMS II Fun 38,81828 Ni..,_ Li Fun 81,4l240 UI Ui L. & ~ Fun 83,5C

72 -~- 231.51T3 S- Si F_ 41025740 s.lJF. _5l750 hn Po F. 54,515710 5a__&___ 1.31,781

T*l 4.618,05

FI and F-101 ei Fun 115,587

23 MNa Co c: Fun 5.21231 MNa Co Sp Pr Fin 7l2111 E- E_ Fun 1,772l ei d Co Fun 5.21

T*l 111,478..EM_1m coFun 181,33

105 W I.. Fun 3,e&m Sir.. & Repa Fun 474

740 S-lJFun 11,712

215 i-E..Fin 5.351

28 ~_ üg Fun 2,152

40 ee im Fun 1.&5

40 e-T..FI 55,04710 So _ Fun 1,04

Ti.ii 27,44

--_....,,,. II J¡ it, 2l3

....Ag-.1110 Ei ii 1._.30ll øw_Fun 125.02

INI R..ti_ 0

lI lh F_ 25

I~ ~Fun 57,1178

lI Co WI 44,1111T_~ 2.2.52

F_ TJ &__~i101 ~Fun 1,312, 17.

118 c.l Eqi Fun 0

2C1 lI La ~ & t. Fun 0

111 Tec Fun 0

2a sn __ _ ii Fun 15O,DD

215 i- Ei Fun 0

2l Ch Se Fun 2D.DD

25 lM A.. _ U- T1F Fun 0

25 a-T1FFun 0

'2 Hi T1F Fw 0

2S Ki CO T1F Fi -0

25 E_ i: Fu 0

3D Ba R8 Fun 2.58130~ II II FWl 0

CI ~Fun 75.DD750 Sw Pa Fun 0

72 _~Fun 0

73 s- s. Fun 0

710 Sa W- Fun 0

CI E_TuFun 3.75._T__ 1I..ll,7l

T.. 431I

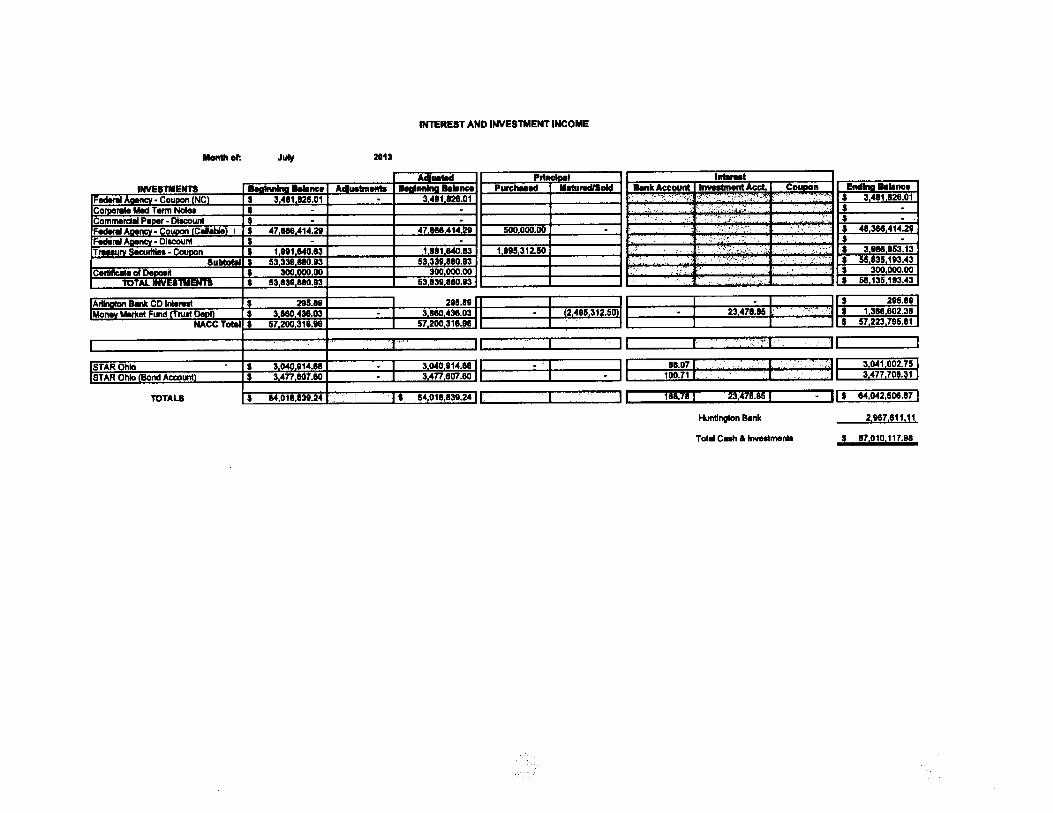

INTREST AND INVESTMENT INCOME

Mon of: J~ 2113

A..tI PrlnelD I..tINVESTMENT 1I.a1N "ne. A..tn ..nn-.._ Purli Ii.iNdDi "'nk Accnt Invnn Aeet Co..n Endln "Line.

F..11 Aøa. Cou"" NC S 3411111211.01 . 341111128.01 "¡,'I. ~,~~ S 341111128.01

Coroi.e Me Ter Noe. . - - .. ~ S -

Commerd. Pioer - OllCnt T ...,. '.,. '\,,'."' .' S- . !"'"' ". -

Fed Aoenc. COUD Celeb\ ! T 47 18 414.29 4786 414.r2 500000.00 . ::',,' ö' . ~, S 411 36 414.28

F..11 Aoe - Dlicnt T - - S -

T..urv Serl - COIlIn S 188184.83 .1 88184.113 1885312.50 T... A' " ":-:,¡~'-~:'..\::',:;:.. "

S 3888 853.13

Suli i 53 338 110.83 53 338 11110.83 'CO",', , ,.' .... i 55 1135 183.43

ClHe of DeIl'~ I 300 00,00 300 000.00'. , ',; '..) .... ..... ,. i 300 00.00

TOTAL INESTMENTS S 53 138 110.83 63 138 11li.83 S 61135 183.43

Arlnaan Sri CD Ini_11 i 295.11 I 285.118 II I

I

23,4711~15 l) ..

:I~.¡

295.119

Mone Meel Fund errul1 Oeoll S 3 ii 438.03 - I 3 1li 438.03 II - 2495312.5011 . . +f.A' 1311802.311

HACCY.. S 57200 318.8 I 57200 3111.98 II 1 57 223 795.1111

I 'J' I I l r ,.,.. ....."1 II I". ,.

STAR Ohio S 3 04 814.88 - I 3 040 814.81

I

.Î I

1111.071,

'i'.' ....:\1:

3041 002.751

ISTAR Ohi Bond Accunt S 3477807.0 . I 3477807.80 - 100.71... 3477 7011.31

TOTALS S 84,0111,1138.24 .' IS 84,0111,11311.24 I I I 188.78 I 23,478.15 I - II i 14,042.506.87 I

Huntngon Sink

ToIII Cee & Invmenl.

2,987,811.11

S 17,010,117.98

Exhibit B

o. Am Pn 00. "-IY 1I ~ ~ Y! Y!~. I 13.171.15 I 13.171.15 I 7.075._ I 7.51,~i I 50,_ 7.17"R. & Pw Pn Tax 5,3.511 5.35,51' 3.021._ 2.lI.512 (91.54) -3.lI&!T. 1.00.00 1.12e.23 2Jm.3 2.lI,3 - 0.0lc Gc Fin 1.00,2 1.00,21 55,314 56.121 18.10 3.D..Pi Ta: Ro 71l.00 715.00 31,50 371,1S1 14,3) .1.14"Li an Pe li.00 14.00 50,45 480.121 (18.33) -3.11"ci fD Se 10.00 80.00 51.07 110,00 23.114 4.onFI. Co & Forit 42,00 425.00 211.715 1111.58 155.120) ~5.43"~E8 184,120 28.120 132.1I 175,74 43.314 321Ic. TV Fiw F_ 58,00 58.00 21.00 30... 13.18 4.n....,. 2S1.00 2S1.oo 111.729 211.~i 113,2 17.1Z'~ 75.00 75.00 37.118 71.432 34.314 1144..

Ta: ii A8 Fin 5.00 5,00 - . . 0.0SM S-F.. &.. 29.00 29.0 12.01 10.01 (1,9) -18.54"w. Sw Fii & fu 15.00 15.00 1,Z 11,22 Z2 0.3..~ ..... Fii & fu 21.00 21,00 11.1I7 7,2 (4.415) -37.""

I' .. F.. Pe F.. 2.55.00 2,5,00 137.50 110.118 (2..1) ~.1"Ho TI Fin 1,38.711 1,3.711 - . . 0.00T"~lIol_ . n.1411.4U . . 1:1._."" . . :i.ff~ ...:

..1I1y FIMI.-poAa of Ju :13

Ge Fund

PoOI.. I 7.31.11 I 7.312,~i I 3.58,_ I 3,4211,270 I 158.4Zl 4.42"Fin Dili 1,83,758 11,2.758 3.13.315 3,1I7,111 184.424 4.2Bol1He 211.548 211,54 201,5 20,5 (9) O.OP... R- Z,13.179 2.813,1 1.3l,53 1,2.ii 72.54 5.3Co & Ec: Denw Denl 1,01,750 1,01,750 53.01 52,n3 11,317 2.10'Pu Se Mi..... 1,03.m l.38,87 4l197 331,113 141,114 30.81"sn Il 45.84 45,84 136,48 101,311 35.123 Z5.73FI_ Di 710.1118 710.118 32,871 315,38 12,114 3.8..Ci.. 747,2 747,2 35.1711 35,84 1.73 0.49'ic N1 740.411 740,411 35;780 34,4-10 11,3 4.lCiCl m.8n 273.97 13"'. 104.15 32.33 23.11"Ci Co 131._ 131~ 13.031 58,707 3,34 5.2..Clll Co 312.~I 312.141 157.1. 158,518 (2,31) -1.48FI 1.157,2 1.157,2 58,0l 53.1. 28.lI 4.7IF.... 175.7S1 175.7S1 42.111 40,2 28,J 1.2in Tec 14.12 14.l 40._ 38.11 18, 4.0lGe~ . 1.5I,1Z 1,5l.11 lI.113 1.03.711 131.m -3.llT" ~ eiri ze718... 28,18.. 13,9.1115 13,50.515 I~,3 4.92"

&! Ta: ~iij_. Fin 3.175.4~ 3.175,4~ 3.175.4~ - 0.00Ea DwII8 Fin 50.00 50.00 . - . 0.00...._ M. u. TlF FlI 180.071 110.071 - . - 0.00Ci Se Co.i 20.00 20.00 20.00 20.00 - O.Os- Co ~ & RiPlir Fin 241,111 241,111 - - 0.00"* Fin 750.00 7S1,OO 750.00 7S1.oo - 0.00

Tci I . ;M.l;,...l . la.~...l a 1,._.wl . aa.oo

e-l1R-- ..0l___1ø obgl: 11,310.755) 14,258.1111) (2,73,43) (1,50.31)

Tal Be FinllEiFin~EiFin~Toi End Fin øaii

1I 18.3,243 I 18.30,243 I 18.30,243 I 19.3,2435.417.31 5.48,3 5,41,31 5,48.3112,5.123 9.511,2 11,103.44 12,34.512

li "._',_ li l:1.04.ti:1 li lli.:lll1'- li "...,..., Cc

Moi, FIMi. Repo

,. of Ju 2013

a- Co Ma MI "-piII FuOr Pn Do. "-R8 .. _ 8lrw: TaDñ Ad VI V.iGa _ I 518.910 I 4..33 I (19,578) -3.77

MoYe U- T_ 22.156 22,83 I 4.81 2.11".. e. 58 474 (114) -19.32..-~ 8,00 8,002 2.00 33.37"

T,.1l Ge Fin 241,218 241,18 O.llTøIR_lIaI_ -1. 4

Elc:~TøI

~fIR__..__- -. Cl: (173,152) (172,82) (44,704) (451,470)

il Fin ii I 183,80 I 183,90 183.80E Fin~ I 10.754 I 11,079 (28.5&)

W_8u~ivF"'OIgi Pn Do. P-R_.. al ioun.: B TaDñ ~I v. Vwne

W..Sim I 185.65 207,754 ,08 11.~TøI~II__Ulll . 'Ii 80.45 32.2..De Se.a i- 2 la O.l~ FUI 5e 15,00 15,00 8.2 11272 -G.3K

TøIOb ,1 1 1

~fIR__..___1I ci: (119,719) (118,718) (137,078) (54,547)

il Fin.. ll,23Fin ø. 58.11 Ca

II Fll RiAaDf..2113

Sull S-lun:"".. Fund

OrMl Ai Pn Do.. P--Il Ik ToO. Ad V.ri V1rt$ 1119,00 S 1119,00 S 3 :. S 40,11 S

1.50 1,50 750 210

S 461,92 S 45,2 S 211,97 S 181,50 30,45 14.37'1100,00 100,00 0.00

7.50 10,1117 10,187 9,lI 50 4.~173.111 173,111 173.119 173.119 O.O

c; Funnill Se. 2900 29,00 12.08 10,0B 1,~i 111.54'1TaI 1,1

EJølR_1n ol_ow la oi: 48,8 48,112 (28,128) 31,414

1=1' Fin LìIli 33,65 i 33,65 i 335,85 i 33,85

En. Fin Il S 38,53 S 38,5 S 30,524 S 3l.0e

.....'.._Fun0r Am Pn oc PwBu1 Il Too. Ad V1i1 v.

R_.nd li..:si M8 F.. S 744,00 S 744,00 S 111,117 S li4,12O S (7,57) -1.0'in e. 8.100 12.700 8,50 11.127 2,477 39.01'1TaI Rein__""Il____UI. Dh--ni s 213,474 S 213.474 S 106,737 $ 120,518 S (13,119) -12.91'1s- oi SSES e- 30,00 30.00 2li,_ 29,_ 0.0011I. .. 39,00 39,00 39,00 31,54 24.478 1.2Ge Cl ~ 112,10 112,10 0.00ø.runii Se wi & .. 28.00 28,00 11.887 7252 4,415 37.84'1

TaI ¡ 1,114,U74 ¡ 1,114,074 ¡ 7Øl,2 ¡ 7IM,1111 ¡ 1:1,112 1._e-ølR_In__- -. at: (3,874) (3 ,374) (111,2) (101,2)

I 1,713,_ I 1.713.8I 1,35,822 I 1,1112,11

Coue

IIIy Fini. "-it

lo of J_ 2l3

SoW._..nt Fund

oiørEI AiEI PnToO. Adl

Do.,V.n ~VlR_en ae__.is. of ii II 1.421.00 II 1,421.00 S 702,244 S 89.815 $ (8,82) -1.3%s. of rK 200 20 100 - (100) .100.00Ar Mn Fe 541.00 541,00 513,2 !I,925 (12,373) -2.41%P_ii pi ,. 30,00 30,00 30,00 27,750 (2,2) 0.001~.. 2.00 700 35 924 574 184.00Tal ~.nd ol... II 1,W4.z II ,~,-. II l,z4:i.lNl II 1,z;'oZ14 i In,"1I1 - r.ii'l

R-lI~oi_ 1.817.074 1,817,074 837,372 841.182 13,790) ~.45%P_ii pi ,. 30,00 30,00 15,00 14.83 38 2.41%MI .- .. 8,00 8,00 4,!I . 4.!I 100.0001.... 318,181 318,181 151,09 151.780 1,3 0.84%Miia (billi.. & IIcb~) 14,00 14,00 5,13 7,819 (1,788) -3.81%

Tci Obpt II Z.Ol,28 II Z,Ol,Z82 II 1,OZ,7l1 II I,02U,179 II IiZl U.UI'l

e-ofR_ enae_OW ia oI:

~Fin~1IE Fin BIIi

(11,082)

89,2 S147 S

22,183 20,03

SS

(70,382)

81,2 S1,153) S

8I,2 S29.40 S

81,20i272,244

Swin POL Fun

0r Cw Pm Do PeEI II To Dl Ad \I v.riR.en ae_:t==ndol-.i S li,00 S li,00 l Mt:il :

498,85: g:::i

-5.41%I 64,öö I 64.00 49.85 05.4111

I~,. S 85,.1 S 85,981 S 111,288 S 174,261 S 21,027 10.n%I lI,981 S 85,981 S 1!1.288 S ¡R211l s 21,bZ1 10.114

e- ofR_ en OI___ eø oI: (10.161) (10,.1) 332,08 324,583

II Fin ~nc 483,83Fin BIIi 818,2

IIIy Fin IlAa or.. 2D13

C...I Eqii Fun0i Cu Pr Do. ~Bu Il To o. "' V.i v.

i 88,00 S 8l.00 I 519.84 I 372,337 I (147,50) -28.3"91,00 91.00 49.50 48.491 (1.019) -2.0l

0.0Dli fll,UW li 71l.UW li :M.;M li 421,818 li 1141,:i:U -28.ll"

:1.01,20 I 1.01.2 S 36.00 I 351,571 I 8,424 2.34'll.iIl62oo $ 1,01Uoo $ 3i.lI $ 351,576 $ 8.42 2.3411

(3,187) (30.187) 20.34 19,242

43,2 S 43,2 I 43,2 I 433,2S 125,025 S 125.025 I 11.58 I 50,4&

Re.. ol _:RM & P- PY TiiPr Ta Ro'"..ToI R_ 8n oi_i

Cl:(~qu~~~ 01 R- 8I ei..i_.. obpl:Li en

~torAeIi..d oi~~ V_toe. V..toe. En "-Fin ii T..in &T..o. ii CNC.._M8ie S 6,3.05 I 1.IM.3I I - I 7.471,43 18...SoWl"'~ 75.429 1,2,214 1,024.l 27,8 2l.lGe 13,83,72 16.195,11 16.828,05 13,188.3 -4.llGe 5.71.48 - 5,71,48 O.llPo Pe 86,5 252,8 122,180 217,2 151.lFi18P. 86,54 252.85 122.180 217,2 15~.lSe 1_ 724,80 17,138 21,161 720,77 -o.llPo & Fl Pe 3l,lI 9l,73 3l.5O 576,218 1341.0'.. irw Rt_ Fin 25,727 3,174 - 21,801 15.1"si Cc MaR 20,378 734,67 871,851 (3,86) -'16.1"EM SIni Fin 64,Ø1 1.24,511 280,717 1,!1,81 145.6"lA En 1.178,172 48.84 84,31 1.14,3 -3.D',. PI Fi 50,11 15,09 3,10i 82,828 23.7'Enb Edon 11,2 1,5 195 12,84 12.0'.. Cc Cc 72._ 4,48 1,2 70,915 -2.4"UI L.. .. leis 68,367 n,1I7 70,212 75.78 10.llFEMAFin - 131,D - 131,D O.D'Eci De.1I 68,65 - 28.59 38.0i -4.2L- "- T1F Fin 241.151 23.173 - 264,31 U'lL- "- r. U- T1F Fin 2.173,317 - 481.53 1,1l1,ni O.D'ci y..in Equ Fin 10,10 140,702 - 151,212 133.7'IQni Wee T1F Fii 149,32 22.. 251 171,817 1OD.D'Ho TI Fin 1,151,m 111,186 4,032 1,3,811 15.4"Ki,. CO T1F Fii 254,03 5,00.60 4,937._ 318,937 1OD.0'Ri No T1F Fin 1.45 7!l - 2,13 1OD.0'R.. So T1F Fii - 2,042 - 2,02 1OD.0'Ar Cn T1F Fin - 186,431 - 186.431 1OD.0'Civ Se 30,185 20.00 5.0i 45,145 48.llNe l. Ul 44.743 63,li1 1,1l 487.43 12.4"CI vi Co Fi li.118 4,48 8,12 5l484 -7.1"Em Bet l.lI.1. 1.73.30 1,117,21 2,0i,2 4.lBWC Adi.ieiii Fun 111,378 lDl,_ 105.58 184.471 O.Dw. Su 63,2 207,754 23._ 613,3 -3fts. s. Si 824,11 40,88 58.85 +I.lI -28.llsi "'-i 1,1I.lI lI,847 35.137 2,2.7D4 16.7"UA Swll Po 495.03 4.,85 155,231 631.57 111..c. EcP 781,512 42,111 28,2 .,121 17.5"TlI Fin 113.521 . .34,OO 120,875 28,16 -76.5'lBoIm_ 6,99,2 1,551 105,81 1,3,8 .1.1"i~ Impn1 Fin ...11 750,00 18,707 1,58,9n 86.1"E..T..Fin 11,15,40 3.743,15 112.1+4 14,847,114 32.4"Ge Bo Rett 48,418 16,33 811.7. 23,11 -51.4"RIl Bo 35,ll - - 35.00 lOD.O'lJ F.. 1.713 24 - 1,737 1.4'lReiv Fin 21,751 40,413 18.111 +4.O 102.5'lCOI WIci 40,700 40,40 242.011 20,024 -49.7'lPnn cie Fin 13,13 10.118,154 10,750,101 20_ -75.1'

ToI S 151.52._ $ 47,341.30 S 41,2,243 S 87,115,05 U..

II ~I ReAa of Ju 203

in Ta C..ri

fmS 5,on.4l2,182.ll

12S,317

~S 10,237

38,723181,817

.. Q!!lUK1'.~17.41'"

.1'"

XW"'-S 5,132,704

2.52.21,011,1348, SO, $

WllhInNe Pni

Toi $

in_ Ta Fiv V_ eo....

2l ~ Zl 2m ZQWlit S 4.21,_ S 4.30,11 S 4.81,45 $ 5,012,157 S 5,132,70InUI 1.37,53 1.754,851 U88,lin 2,137,676 2,5,2Ne Pr 70,61 812,5111 83,84 æz,13 1,011,134

ToI S 6.83,213 $ 8,m.11' s 7.511,24 $ 8,102:787 S 8.50,êi

"-"'..in_IDe_1 Fiom P!rV..r

WitnlnivlNe Pr

Toi

2l-18.ll-30.5'-25.5'3.7'

Zl8.7'"7.5'"14.3'"7.n.

zm2.4'"lB.2'"14.5'"B.ll

ilI.ll13.4'"2.n.1.3'

miIJIJi.IJUlUluiZ.1.U

I !n Til Fhi X. Tr I

-." . .

.. . . _.--....--.._.....----. . . .

2l 2lza ziZl--lI -. Db -!I -- --

CI of Up ArInProjec Expense Perfnnance Report~ To: lI13ii .. ea1o_ E. -- -El _fa-.-.Io...w¥ll

2l2 .1l I' IEn."..I"g: 122,218 510i,127 Sll1,OI 10e- S1.z..ea ii Sl,ll Sl,ll 10 10..TMl 57,~ 10 so S7,!iInIi ~, in.,Cl & pn rn 574,144 $3,ll $0,181EI~ S3 S3 10

11,210,100 _,33 147,881

au .RKHI PME .Ei..wwii'~ 12-.-Cc EIT.. in at 1919 Sl '12 soMI TMlIr M1ni. in & pn.. 1170 (5170)EI.i

.18 51.on (5170)

2l2 GAVI CUVE ",-eoCc EI 1l,8O Sl,8O 10

MI T..11 me 1750Ir M1. in & pn.- $3,120 1721 S23l_,870 171 $3.149

2lS ANNUA STET lITE .1...eoCCI EI '-.745 _,745~T..ni 111,lI (lll,lI)n._~, in & pn ~ 518,2 (118,22)EI-. Il (1l

_.745 $31,758 SI.1l7

2l2 LAE AVEUE I. WE _TEIEI....: 1128,111 1123,114 S4.1l 10~ 11,DICc II Sl,0I1 Sl,0I1M* T.. 115,00 S15,oo.. ir - pnlM Sl15,711 11,172 1114.814

11,0i,18 51,172 51,OllI

a12 LA AVEE DE & TR CA S1oo._Ei 1138,20 SI,175 $4,03 soc-B.. & C.... Tni c.imi 18,475 $5,2 12,21 so

.. M1ni, in'" & pn ..en 115,00 124 S14.978

$2,ll 1147,45 S14.m

cit aI Up AiProjec Expens Perfnnance Report

L. To: lI13IM En c: a in Ei ~ v_~ _..-.-.a.......202 lI HOlOE-DNHEUD 'taa,_Ei..ii S8.0I1 $7D,15 $18,103 II~-- en, inl & pnll 10 II 10

S8,0I1 $70,15 10

.,3NP~-SofOtj ".0__ Np a pnlN S8 S8 10

.,2" $1,2,_Cø II (I HI " _ C) $1,55 '789,55 $131,00 IIM8 Til $lUOO 15'- $7,2-- ~ & pn mr m.. $3,n4 13.8751I-. $1,DD '1,00 II

$',OO,7f5 18,511 14177

202 Sl .t....CI Il 11.43 Sl,lI S2,4l II~TII 1825 13.2 (121,018)

__ ~& prec_lIne lI._ 18,743 (1,80Bi m- I8 SØ II

11,018,278 171,82 (12,12)

203 lI MO YOEol TF Il ~.-En- Ha De 18.375 $5,05 $3,318 II- Np & pn rn II S281 ($,88)Sc~ 12,39 12.39 II II

1107,771 178,33 ($,88)

1IT1;se: -. of Ol ",82 _,81 _,81 so so

202 UES ST S2,_ 121.420 1240,83' S5 soBi-- $1,& S250 (1l)- en, in & pn ii... I5 ($)S2,27i.DO S2,lI.00 (11,242.00)

.,3 I8 STDI ...0C.. 1 2l,740 11,n1 12.D'8 so

BId-aIrli. ~ng, ii & pn_iBd $'81 ($181)

1 2l,740 1 1,80 $ (181)

203l1ITMY SEW REPAIRS 110,_Cll 1 so so IIBi-a-- _o-. In & pnll 1'.83 (11.83)1 1 1,83 1 (1,83)

o-CI of Up ArIn

Projec Expnse Perfrmnce ReportLJ To: 0l13.. e-a_ E.~ -_--........ ~ v....

283 WA Tt RO PK IA AND. $3111114~1l~ $o,010 14.11 13182 soC_InCl $175,!l so 175,!l so~~, Np, pn-...- $13,_ $10._ $3.38$2,45 $5,317 $3397

CAII CULVE & l!ÐI Dl ..17_Cc II $8,2 $4,13 $2.04 $0_T.- $4,05 $183 $3.170ea np $12,3l 34,52 ($1,137)~ in. pn ~ $7,lI .,13/ ($Bi-. $l (Sl)l8,31 $41,38 ($,43)

IIY BIlClIll $3'- $3,00-- ir& pn ~ S2471 ($2,471)En.. 18,li $51,4111 $12,111 soS3,1I $5,~i7 $0

LAE AVEE II US Il $7.00i. A.. R-. lhNa si $35,00 335.00i..... ~w I! si $100,1l $5.1711 $1,111 soLo ea o... $8,00 $8,00 so--.- _,00 _,00Ml ~ Ro DI Sl07,ll $74,577 33,34 soMl Hc Ca.. S. i. $412,50 $412.50T.. AN $13.50 $11,~i7 $1,83 so~ (E & ii Bu) S2,45,45 $207,524 381,1l so..T~ so so soC_ ir S2,_ S2,174 ",43 so~~&pn~ 1213 $2711 ($2-)Øn & i: 141,1I.00 $141,11 so

$4.017.~i7 $2_,151 $8.00

~

R8ue and ~oun: by Type

Aa of June 30, 2013

lrargovminl Renue

101 Locl Govemrnt Fund 567,121259 Kisdale CORE TIF Fund 0405 Estate Tax capitl Project 18,597245 FEMA Fund 131,00

Pr Tex RoIl Reimursments and Inleffst Subsi:101 Geral Fund 378,150103+104+107 Polic and Fire Pens Funs 164,738

106 capital Equipment Fun 48,481301 Geral Bo Retirent 190,320255 Chelse Tax Incrmen Equialent Fund 1,63256 Arington Crosing Tax Incntive Di 25,914258 Kingsdale West TIF Fun 630Total 1,526.591

GallneTu..207 Stt Maintnanc & Repai Fund 499,332

Motr V.hlcle Tu..20 Stt Maintenance & Repair Fund_ 22,839

Lans and Peit

101 Gel Fun 490,121

Riwue and Reur by Type

Al of June 30, 2013

M1celi.neua Revenue

101 Geral Fund 58,873207 Stt Repair & Maintnc Fund 8,002

108 Teclogy Fun 34,008

205 Tax Incntve Review Fund 3,874

217 Tre Plantng Fund 0

215 Law Enfoment Fim 43,942

405 Esate Tax Capital Improvement Fund 0

730 ser Surcrg Fun 210

710 Soid Waste 0

740 $tter Manament Fund 0

750 Swmming POO Fund 0

Total 676,90

Relmburunint & R8rl.

101 Geral Fund 71,432

108 Tecy Fun 0

215 Law Enment Fun 0

301 Geral Bo Retiment Fun 0

106 Capi Equip Fun 0

250 Ecomi Devent 0

405 Estte Tax Impme 0

280 Neighbrhood lihtng Fun 0

105 Self-Insranc Fund 14,149

40 Infrstre Fund 0

258 Mingon Crng Tax Incetive Fun 0

720 Water Surce Fund 0

740 Stormr Manament Fun 0

Total 85,581

RemburMnt (Intit)101 Geral Fund 23,609

INTEREST AND INVESTMNT INCOME

Month ot Jun. 2GU

Allue Prlnc- i..tINVEllIENTI ..lnnlni ..nc Aii..tr.. ..Innln "ne. Pur"'. lIoI BenliAccount Inww Acc COUDn End-"

F.. Aoinc - Couoo INCI S 3411128.01 - 3411128.01 \):,..'-~ '..,' S 3411128.01C_.. Me T-m Na S - - , S -

ci.i P... . D11C . - . ... . -F.. Aae. CouoolCii . 45 387 018.21 45 387 018.28 488800.00 12 488 875.00 ;¡ .. S 4718 414.21F.. Aoill. DIIC $ - - ... $ .TrNUf Seri . CouDOn 3012421.87 3012421.87 8 8887.50 12 000 418.74 . ,. '. . ,. .... S 1881 &4.83Iii 51 881 337.17 51 881 337.17 S 53 338110.83C.itll. 01 DeiiM 300 00.00 300 00.00 '... :c" $ 30000.00

TOTAL INESTMENT 52 181 337.17 52181 337.17 . 53 838 180.83

4500312.50 : 15145887.5011 I

I

28,245~31 IIAilnaon s. CD In1_l S 285.19 I 285.89 II II S 295.19.1IMoii MMel Fun rTlI DeI I 5 275 383.50 - I 5 275 383.50 II . 1,202.11 II $ 3 180 438.03 I

HACC Toll . 57 1 M 700.71 I 57 1M 700.71 II II $ 57200 318.96 I..

I r II i L. .

11 I" t I I

1 STAR Ohio I 3lM 811.90 . I 3000811.90 II .I II

102.71 f

I. I

3lM 914.881ISTAR Ohio IBond AccunlJ II 34n398.37 - I 34n.388.37 II - 211.23 3:m:107.80

83,964,801.lI II ' I 'II :Š1i.1! 29,45.1! 1,202.1811' 64.018,139.24 ITOTALI $ 113,964,90.91 '..." .1 $0'"

Hunlni BaT ci Cell & lnvNme

3,5l1,024.34

$ 67,81..83.51

Exhibit C

æmCITY OF I UPPER

ARLINGTON

COUNCIL CONFERENCE SESSION

STAFF REPORTCITY MANAGER'S OFFICE

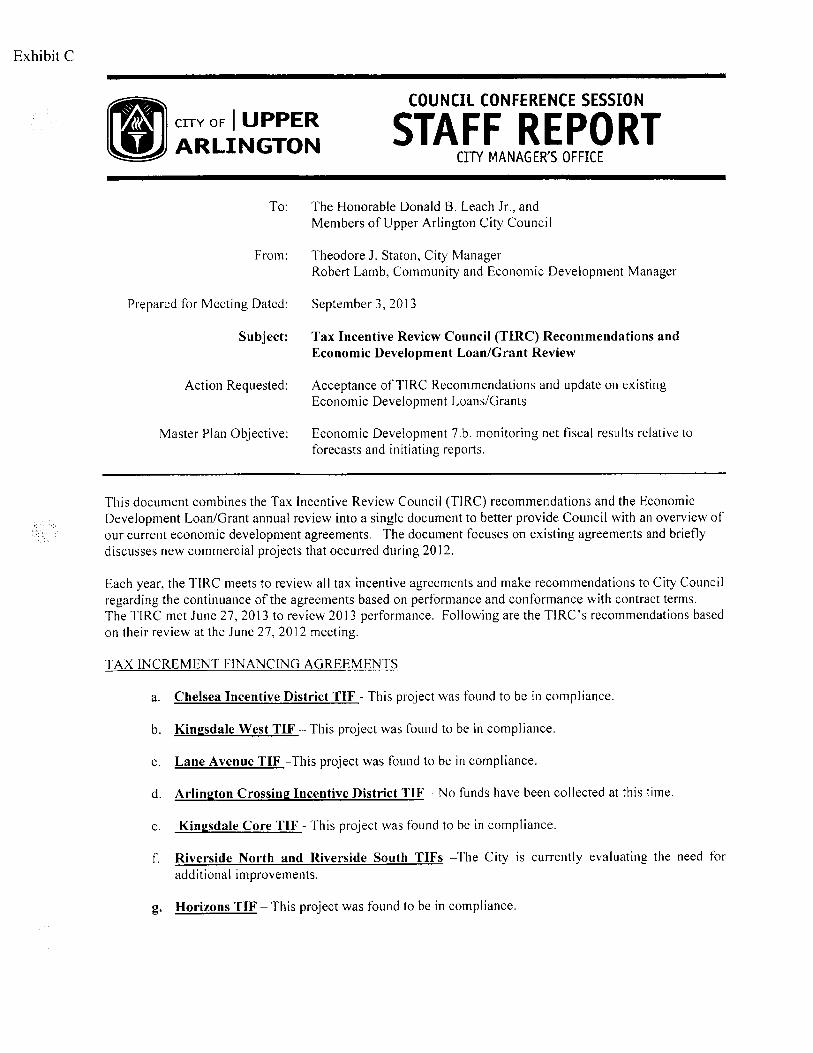

To: The Honorable Donald B. Leach Jr., andMembers of Upper Arlington City Council

From: Theodore J. Staton, City ManagerRobert Lamb, Community and Economic Development Manager

Preparcd for Meeting Dated: September 3,2013

Subject: Tax Incentive Review Council (TIRC) Recommendations andEconomic Development Loan/Grant Review

Action Requested: Acceptance ofTIRC Recommendations and update on existingEconomic Development Loans/Grants

Master Plan Objective: Economic Development 7.b. monitoring net fiscal results relative toforecasts and initiating reports.

This document combines the Tax Incentive Review Council (TIRC) recommendations and the EconomicDevelopment Loan/Grant annual review into a single document to better provide Council with an overview ofour current economic development agreements. The document focuses on existing agreements and brieflydiscusses new commercial projects that occurred during 2012.

Each year, the TIRC meets to review all tax incentive agreements and make recommendations to City Councilregarding the continuance of the agreements based on performance and conformance with contract terms.The TIRC met June 27, 2013 to review 2013 performance. Following are the TIRC's recommendations basedon their review at thc June 27, 2012 meeting.

TAX INCREMENT FINANCING AGREEMENTS

a. Chelsea Incentive District TIF - This project was found to be in compliance.

b. Kingsdale West TIF - This project was found to be in compliance.

c. Lane Avenue TIF -This project was found to be in compliance.

d. Arlington Crossing Incentive District TIF -- No funds have been collected at this time.

e. Kingsdale Core TIF - This project was found to be in compliance.

f. Riverside North and Riverside South TIFs -The City is currently evaluating the need foradditional improvements.

g. Horizons TIF - This project was found to be in compliance.

T AX ABATEMENT AGREEMENTSa. Orthopedic Medical Properties LLC (075-000001) 3842 W Henderson Road

Found agreement in substantial compliance.b.l Sheikh Properties LLC (formerly Jacobson Ave LLC & EMCW LLC) (075-000019) 5001

Horizons Drive Suite 210The propert tax abatement should remain at 0%.

b.2 Hersh Realty LLC (075-000017,075-000018) 5001 Horizons Dr 100-200

Board voted to have the City Attorney's Office review the agreement to determine ittheagreement can be terminated and the claw backs available to the City agreement for non-compliance.

c.i CAM Development II LTD (075-000020) 5003 Horizons Drivec.2 CAM Development II LTD (075-000021) 5003 Horizons Drivec.3 CAM Development Co. LTD (075-000022) 5003 Horizons Drive

Found agreement in substantial compliance.

d. 5009 Horizons LLC (Irth Solutions) (075-000025) 5009 Horizons DriveFound agreement in compliance.

c. i KDA Real Estate LLC (075-000027) 5005 Horizons Drive

Found agreement in substantial compliance.

e.2 Arlington Falls LLC (075-000028) 5005 Horizons Drive

Propert owner shall be notified in writing that agreement will be placed on probation withrecommendation to terminate next year if the revenue numbers have not improved or are notlikely to improve.

eJ G&B Ventures LLC (075-000029) 5005 Horizons DriveFound agreement in substantial compliance.

f 5007 Arlington Falls LLC (075-000030, 31 and 32) 5007 Horizons Drive

Found agreement in substantial compliance.

g. Central Ohio Medicine Bldg. Assoc. LLC (075-000004) 4030 W. Henderson Road.

Found in substantial compliance.

ECONOMIC DEVELOPMENT LOANS/PROGRAMS

The City currently has or will soon have economic development incentive agrcemcnts with 21 organizationslocated in Upper Arlington, beyond the TIF and CRAs currently in place, used to track payroll andemployment numbers. The vast majority of these agreements are in compl iance, and the City is receiving aneconomic benefit from these agreements. FUltherinore, the City entered into a new economic developmentagreement with the Lane Avenue Redevelopment, LLC; Lane Avenue Enterprise, LTD; and Crawford Hoyingthat will bring the City's first hotel to fruition.

In 2012, the City recorded over $80,000,000 in construction work value within City limits. This is anincrease of38% from the previous year. The City supported the acquisition of the office building located at

2245 North Bank Drive by National Church Residences, a purchase that will allow National ChurchResidences to continue to grow in Upper Arlington, maintaining their position as the largest private employerin the City. The City continued its support of the Lane Avenue Mixed-Use Project by providing TIF fundsand using the City's Triple-A rating to back the bonds. Along with the Mixed-Use Project, Lane Avenue alsosaw the remodeling of Whole Foods and the acquisition of 2011 Riverside Drive by Thomas & Marker.

These projects, along with many others, continue Upper Arlington's tradition of moving forward whileretaining the community's unique identity.

J?~J J-Theodore J. Staton i

City Manager

J(/(vÍ~i.'r (h~Robert LambCommunity and Economic Development Manager

Exhibit D

iI CIY OF I UPPERU ARLINGTONCITY MANAGER'S OFFICE

3600 Tremont Road · Upper Arlington, Ohio 43221-1595

Phone: 614-583-5040 . Fax: 614-457-6620 . www.uaoh.net

July 30, 2013 UA Realtor Focus Group

Meeting Summary

Attendees:· Cindy Braun, Jim Edwards, Kyle Edwards, Stacy McVey - Keller Williams Classic Properties

· Jane Coughlin, Diane Koontz, Barbara Lach, Jane Stone - Coldwell Banker

· Doug Ryan - Douglas Real Estate

· Bob McCarthy - Howard Hanna Real Estate

· Debbie Phillips-Bower, Susan Toothman - Re/Max Premier Choice

· Jane Jones, Susan Mullenix - Real Living HER

· Annie Means, Carrie Mimnaugh - Street Sotheby's International Realty

· Theodore J. Staton, City Manager, Emma Speight, Community Affairs Director, Megan Hoffman,

Intern - City of Upper Arlington

1. How many years have you been a realtor in the Upper Arlington market?Range: 3-40 years

Median: 20 years

· 1-14 years: 2· 15-29 years: 9· 30 or more years: 4

2. What is the typical sales market you focus on (price range, locations/etc.)?

Range: Times mentioned:

$200,000 + 2

$200,000-$400,000 2

$200,000-$700,000 i$350,000 + 2

$500,000 + 2

All 3

Entry-level iNo response 2

July 30, 2013 Realtor Focus Group SummaryPage i of6

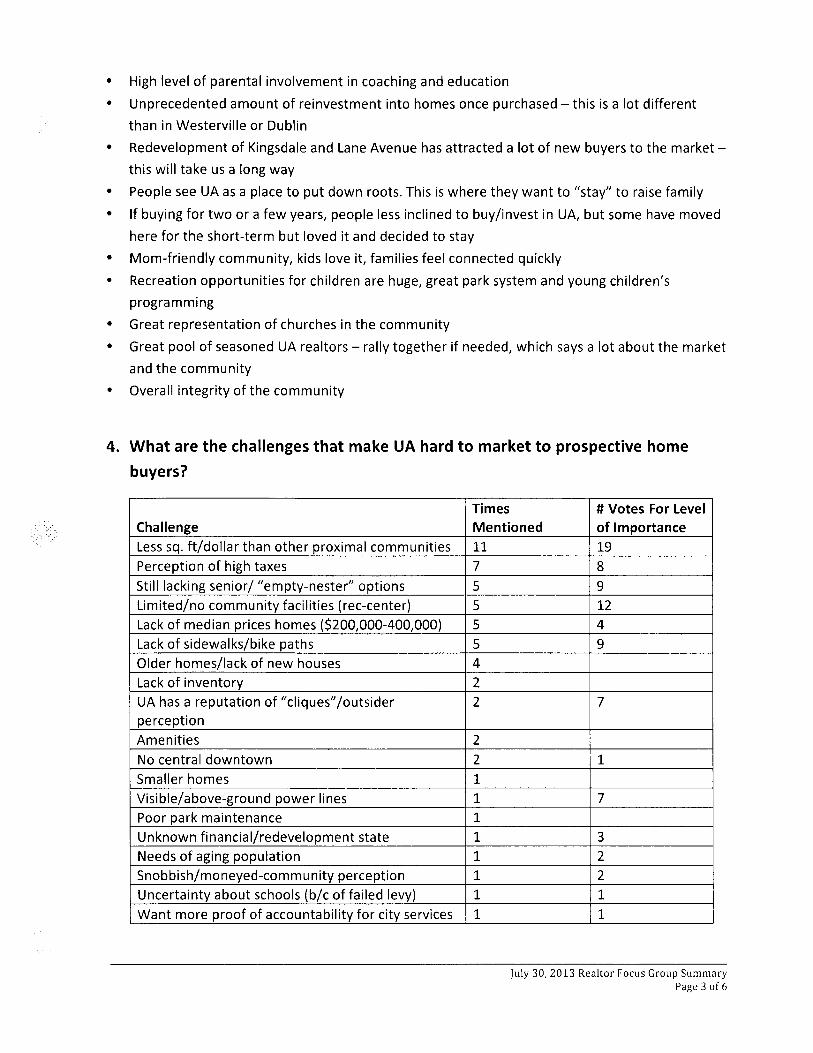

3. What are UA's best attributes from your perspective when marketing homes toprospective buyers?

#Times # Votes For Level

Attribute Mentioned of ImportanceSchools 15 20Location/proximity to Columbus/OSU/region 14 7

Sense/sprit of community/pride 9 13

Stability of real estate market 5 15

Landlocked community 4 3

Safety 3 6

Diverse architecture of homes 3 3

Charm/tradition 3