Tax Law Changes in the Farm Bill ??? Huh?

Guido van der Hoeven

Dept. Ag. and Resource Econ.919-515-9071, [email protected]

2008 Farm Bill Tax Law Changes

• Conservation Reserve Program• Optional Method for SE Tax• Conservation Easement Donations• Equine Depreciation• Commodity Credit Corp. Transactions• Agricultural Bonds• Limitation on Farming Losses• Agricultural Chemicals Security Credit• Like-kind Exchange of Shares

2008 Farm Bill Tax Law Changes

• Endangered-Species Recovery Deduction• Alternative and Renewable Fuels• Timber Provisions

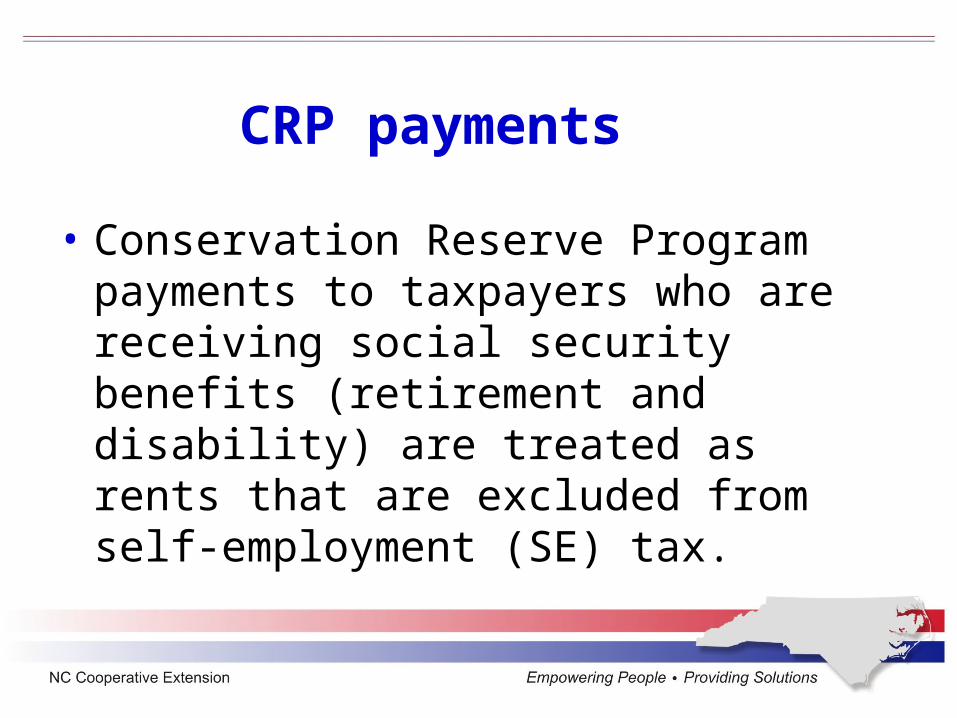

CRP payments

• Conservation Reserve Program payments to taxpayers who are receiving social security benefits (retirement and disability) are treated as rents that are excluded from self-employment (SE) tax.

Example 1

Guy Wire owns and operates 900 acres as a crop farm. In 2002 he enrolled 85 acres in the CRP. Guy turned 65 on March 15, 2004 and began receiving SS retirement benefits. He continues to farm full-time.

Beginning in 2008, his CRP payments are not subject to SE tax.

Example 2

Peach Blossom inherited a farm with a CRP contract in place in 2006. Peach is disabled and receives SS disability benefits. She hires a neighbor to maintain the CRP land.

Beginning in 2008, her CRP payments are not subject to SE tax.

Other recipients (not receiving SS benefits)

• Does law change imply that all CRP payments are rent that is excluded from SE tax?

• Non-material participation– IRS will argue that they are subject to SE

tax.– Taxpayer might argue that Congress

overturned the court case positions.

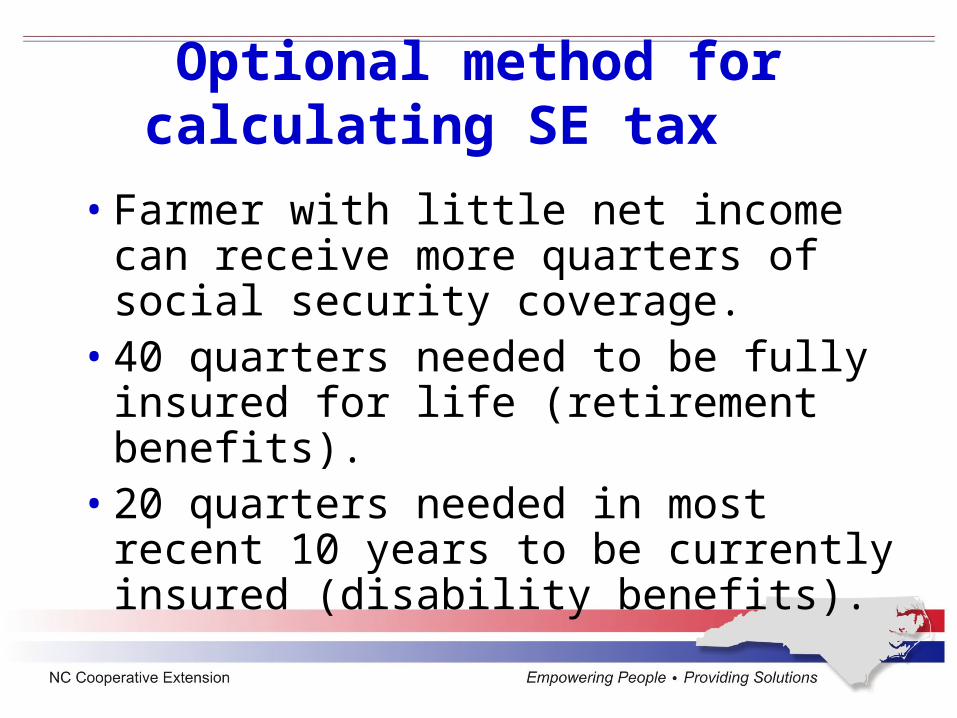

Optional method for calculating SE tax

• Farmer with little net income can receive more quarters of social security coverage.

• 40 quarters needed to be fully insured for life (retirement benefits).

• 20 quarters needed in most recent 10 years to be currently insured (disability benefits).

Prior law

• If gross farm income < $2,400, pay SE tax on 2/3 of gross farm income.

• If gross farm income > $2,400, and net farm income < $1,733, pay SE tax on $1,600.

• $1,050 of SE income in 2008 yields one quarter of coverage.

Law change

• $1,600 replaced by lower limit (earnings for 4 quarters of coverage—$4,200 for 2008)

• $2,400 replaced by upper limit (150% of lower limit—$6,300 for 2008)

Gross < upper limit

• If gross farm income is less than upper limit, pay SE tax on 2/3 of gross farm income.

• Example—$4,500 of gross farm income; loss on Schedule F; pay SE tax on $3,000 and earn two quarters of coverage.

Gross > upper limit

• If gross farm income > upper limit, and 92.35% of net income < lower limit, pay SE tax on lower limit.

• Example—$6,500 gross farm income; $2,000 net farm income; elect to pay SE tax on $4,200 to receive four quarters of coverage.

Most important for young families

• The ability to obtain some disability coverage for young families should not be discounted.

• Generally, the Earned Income Credit will “pay” the Optional SE tax.

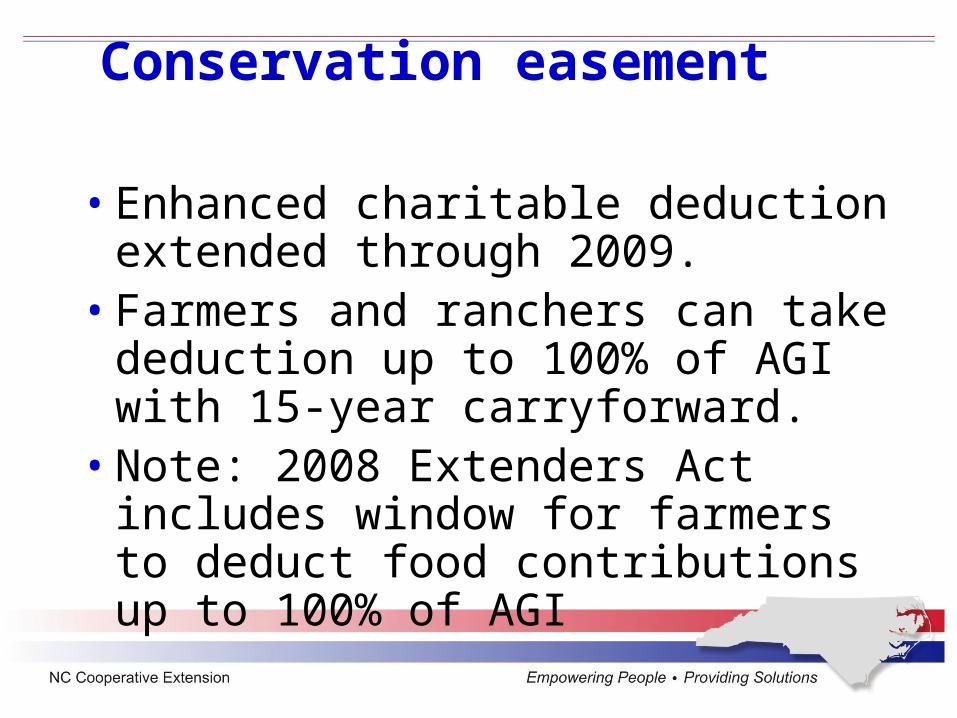

Conservation easement

• Enhanced charitable deduction extended through 2009.

• Farmers and ranchers can take deduction up to 100% of AGI with 15-year carryforward.

• Note: 2008 Extenders Act includes window for farmers to deduct food contributions up to 100% of AGI

Equine depreciation

• Cost-recovery period is 3 years for all race horses placed in service in 2009-2013.

• Cost-recovery periods for work horses and breeding horses are not changed still remains 3 years.

CCC loans

• CCC is required to report market gain from repayment of a loan on Form CCC-1099-G, whether the taxpayer repays the loan with cash or uses CCC certificates.

Be careful not to double-report if farmer included loan in income.

Aggie bonds

• Low-interest loans for first-time farmers and ranchers

• Loan limit raised to $450,000

• Substantial farmland is parcel of land > 30% of median size of farm in same county; no minimum FMV

Farm loss limitation• Begins in 2010• Affects recipients of CCC loans or direct

or countercyclical payments• Farm loss deduction limited to > of

–$300,000, or –5-year aggregate net farm income

• Farm business includes processing of commodities

Examples

1.—$350,000 farm loss but no government payments or loans, allowed the loss

2.—$350,000 farm loss reduced by $100,000 profit from processing activity, allowed the loss because net loss is below $350,000.

3.—$500,000 loss with $550,000 net income during prior 5 years, allowed the loss because loss is less than 5 yr net income.

Exclusions

• Casualty, disease, drought losses• Example 4.—subtract drought loss

before applying limit, $150,000 of $400,000 loss is drought, $250,000 loss allowed.

Partnerships, LLCs and S-Corps

• Pass through; pro rate the loss.• Example 5.— S corp loss of

$500,000; 2 equal owner’s share is less than deduction limit, $250,000 pass through loss allowed.

Agricultural chemicalssecurity credit

• Businesses that sell specified agricultural chemicals at retail predominantly to farmers and ranchers

• Businesses that manufacture, formulate, distribute, or aerially apply specified agricultural chemicals

• 30% credit for security expenditures• $100,000 annual and 6-year cap per facility

Endangered species recovery deduction

• Site-specific measures included in Endangered Species Act plans are deductible conservation expenses under I.R.C. § 175.

• Total deduction is still limited to 25% of gross income from farming.

Fuel credits

• Cellulosic biofuels credit will be up to $1.01 per gallon (reduced for alcohol) for 2009-2012 production.

• Ethanol incentive reduced from 51¢ per gallon to 45¢ per gallon in 2009 and later if 7.5 billion gallons are produced or imported in 2008.

Corporations 15% timber tax rate

• Trees held longer than 15 years• I.R.C. § 631(a) and (b) gain• 15% tax on corporation’s gain from

5/22/08 through 5/22/09• Tax years ending after 5/22/08 and

beginning before 5/22/09