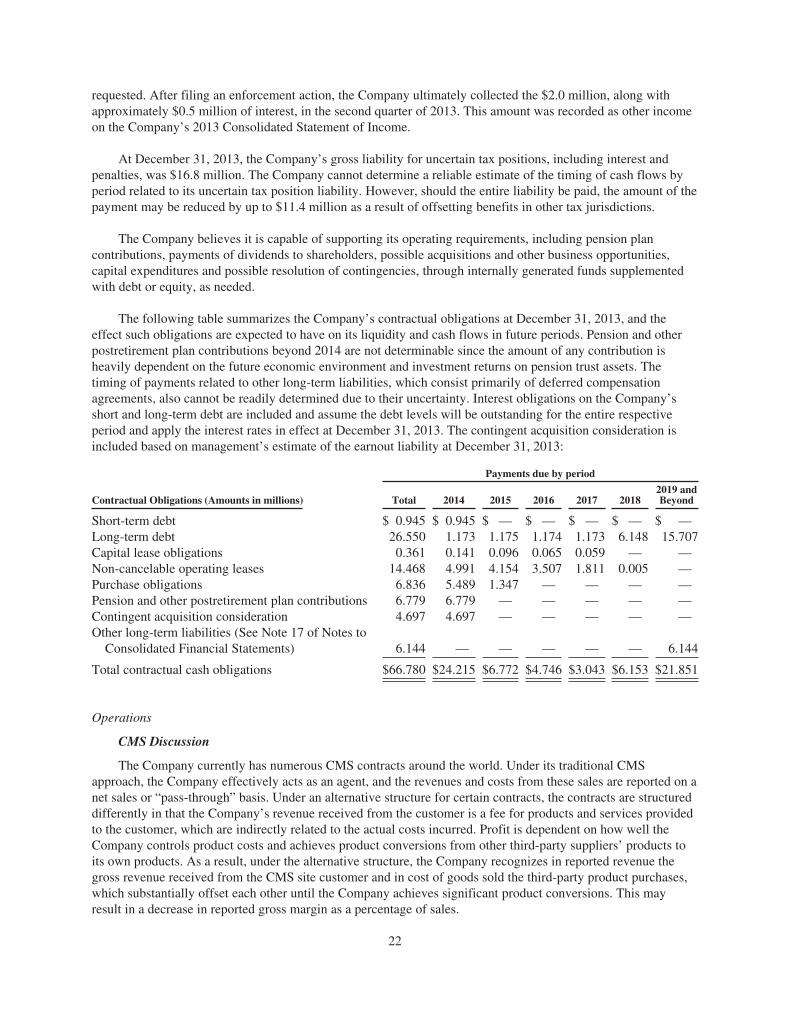

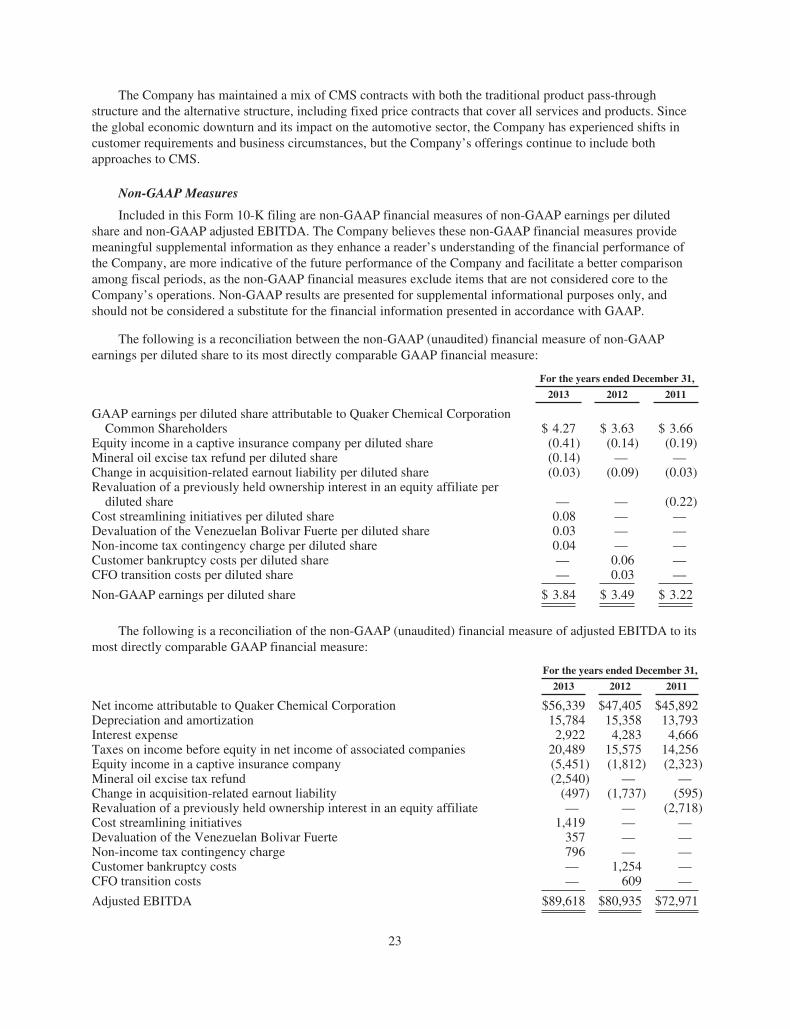

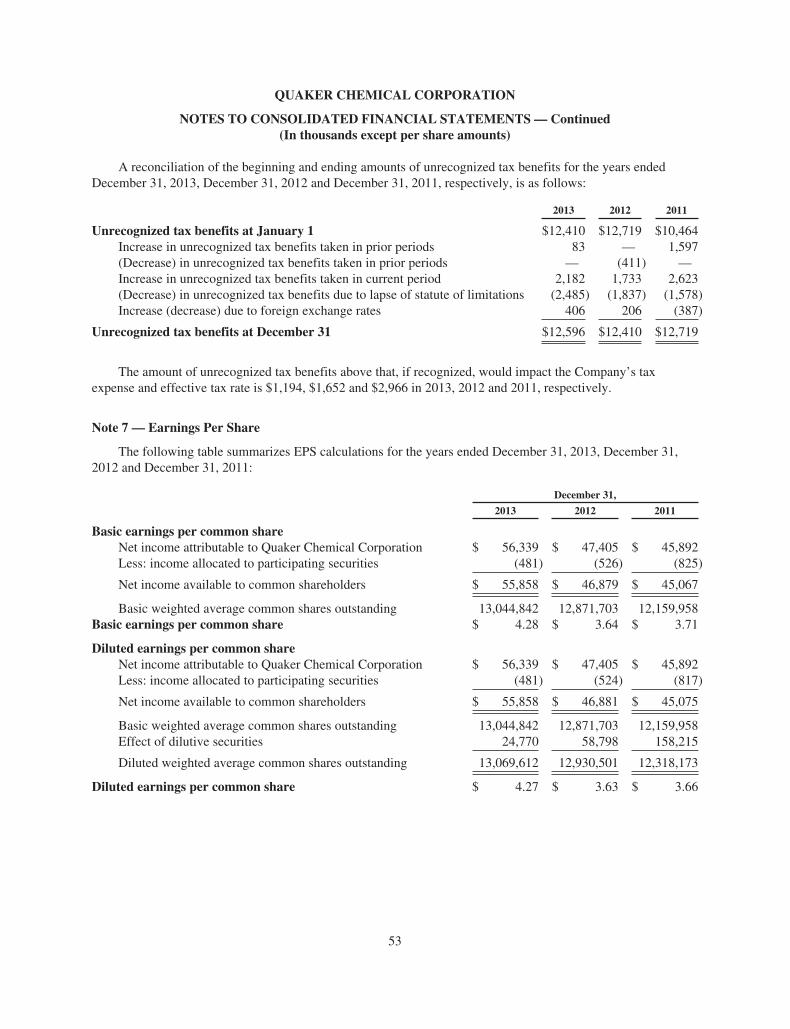

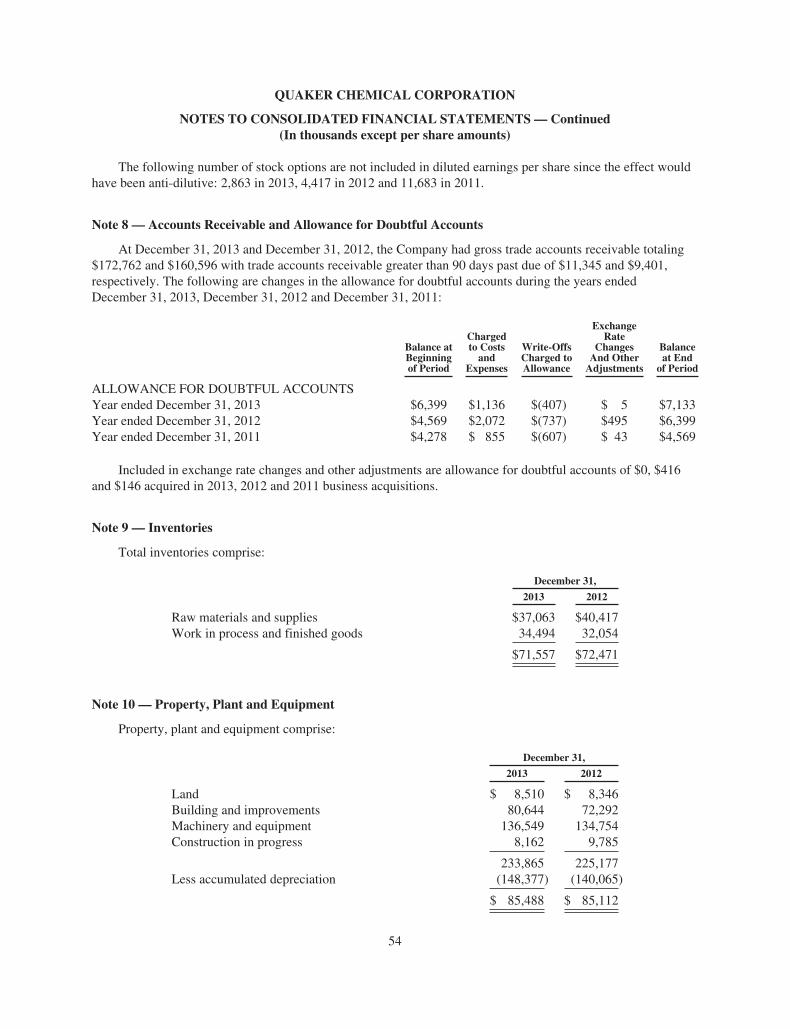

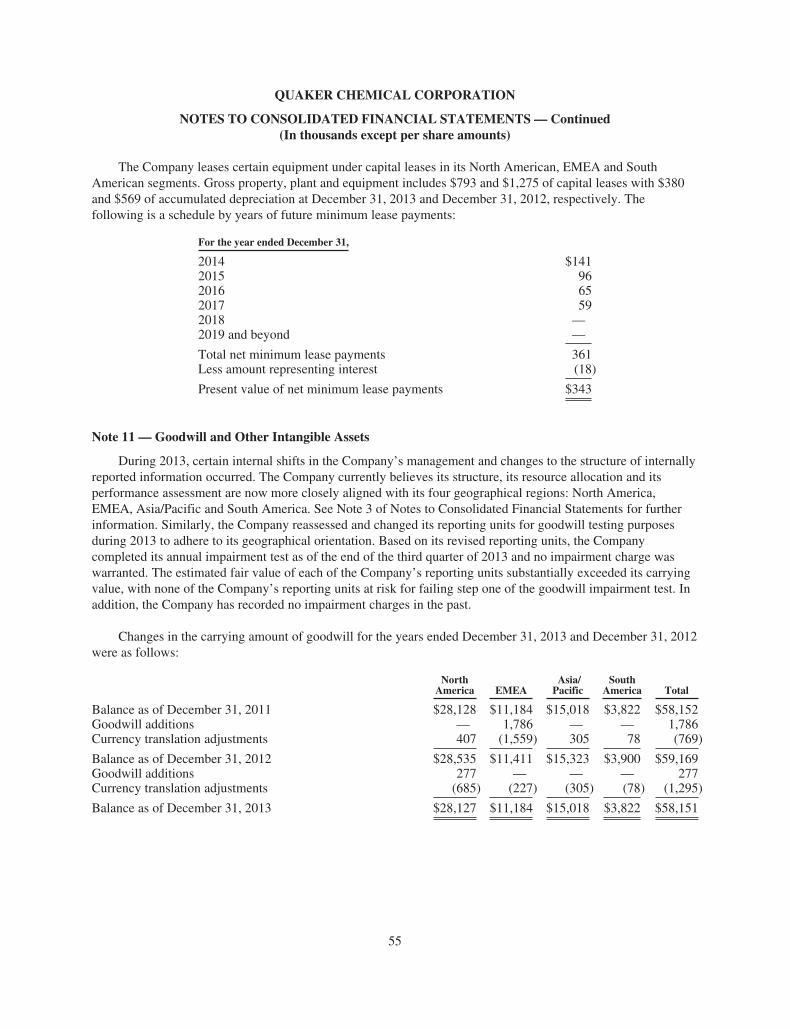

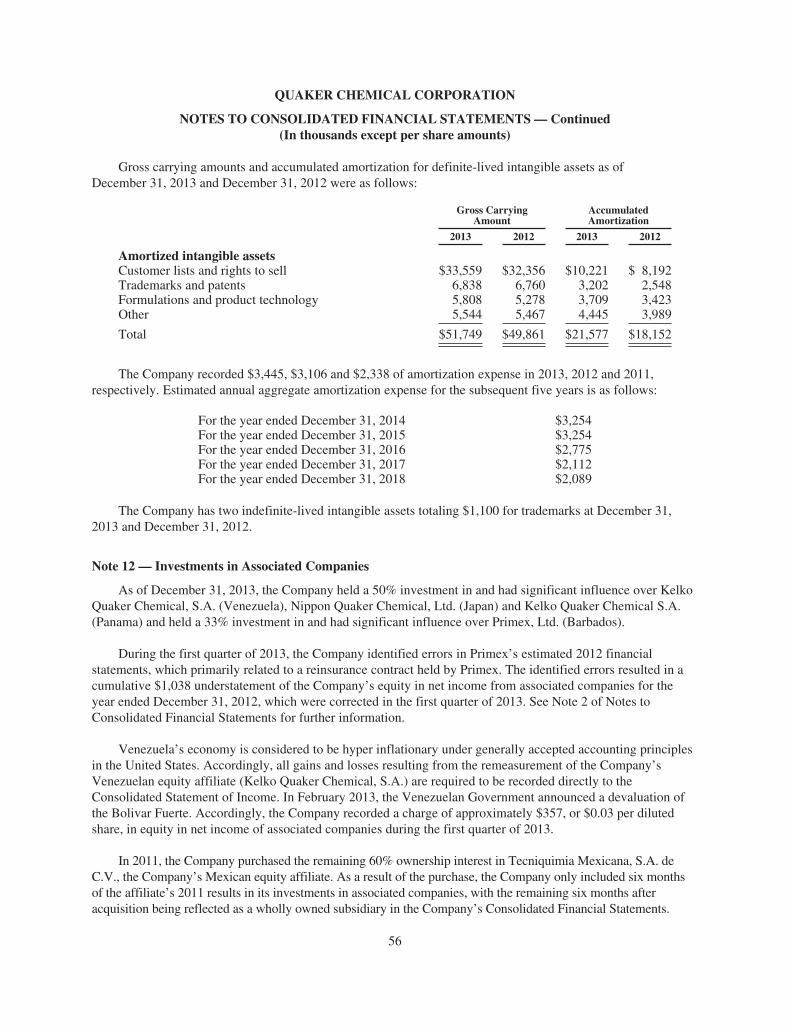

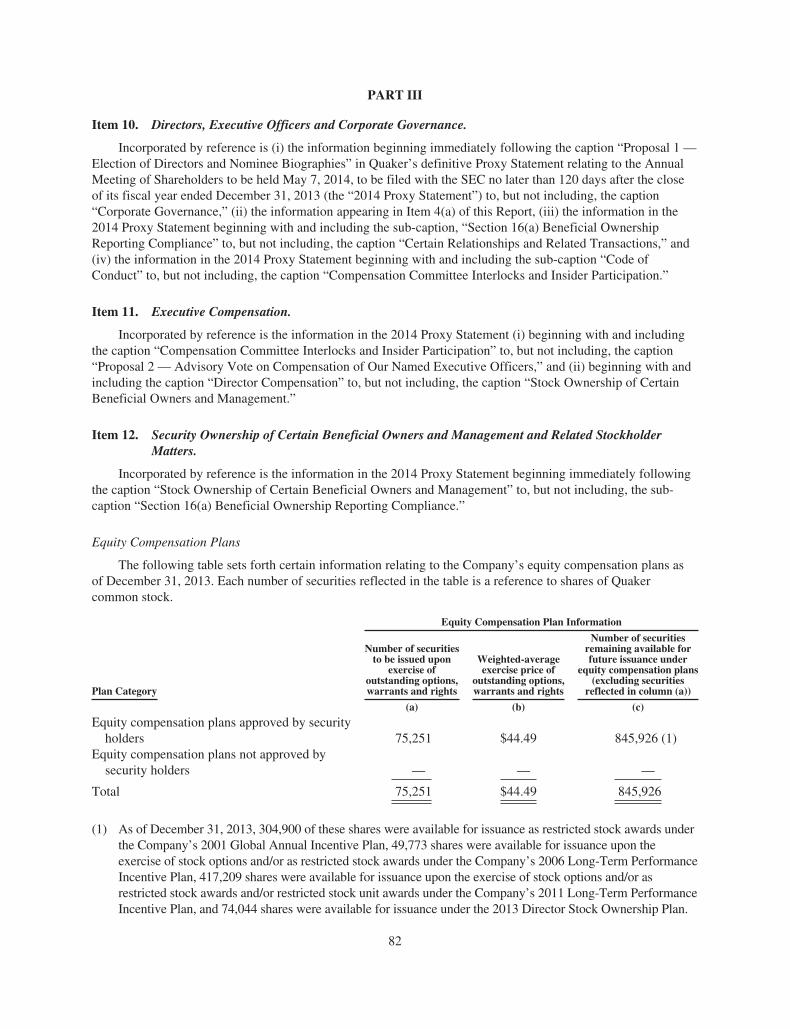

126

This is not what counts. Quaker Chemical Corporation | 2013 Annual Report

| Date post: | 15-Mar-2016 |

| Category: |

Documents |

| Upload: | quaker-chemical |

| View: | 214 times |

| Download: | 0 times |

This is not what counts.

Quaker Chemical Corporation | 2013 Annual Report

It’s what’s inside that counts®.

Products alone don’t solve problems. People do. At the core of everything Quaker

does is a genuine passion for helping our customers’ businesses grow ever stronger—

by making their processes more efficient, sustainable and competitive. This is

what defines our brand and what makes us stand out from our competitors. At Quaker,

we know what counts. It’s what’s inside.

Quaker Chemical Corporation P. 1

We know what counts.

You’ve got to put heart into it.

Achieving extraordinary results for our customers takes passion and energy. That

means 100% dedication, today and every day. For us, there is no other way of working.

At Quaker, we are driven by a sincere desire to unlock all the potential of our customer’s

business. Once on that path, there is no going back. We put our heart into all that

we do—no matter how challenging the problem, how gritty the environment or how

impossible the undertaking. Quaker. It’s what’s inside that counts.

P. 2 Quaker Chemical Corporation

You’ve got to put boots on the ground.

We know what counts.

Customer intimacy. It’s our strength—our secret ingredient. At a time when many of

our competitors have cut back on hands-on service, we are relentlessly committed to it.

By being on the plant floor and an integral part of our customer’s team, we glean

knowledge about them and their operations that is pure gold. Customers want deep and

meaningful conversations about their needs, their hopes and what keeps them up at

night. And we want that too. Quaker. It’s what’s inside that counts.

Quaker Chemical Corporation P. 3

You’ve got to feel the team spirit.

We know what counts.

What we do is definitely a team sport. Why? Because the challenges our customers

face are so complex and urgent that it takes the skills of many to deliver the “right”

solution. To get the job done, we draw on the brainpower of our full organization—

from our chemists and process engineers to our people in manufacturing and the

supply chain. Teamwork is so ingrained in our culture that the concept of not sharing

knowledge is unimaginable. Quaker. It’s what’s inside that counts.

P. 4 Quaker Chemical Corporation

Once you what cou you live it

Quaker Chemical Corporation P. 5

Our customers operate in a hyper-competitive world. They urgently need to lower their

costs, extend their resources and meet their own customers’ high expectations. We

understand where they’re coming from. We’re zealous about those things too. Every day

as Quaker people around the world go about their workday, they help customers reach

new levels of business success. They know what counts and they live it passionately—

and then wake up the next day fired up, ready to do it all again. Here are their stories…

Once you what cou you live it

know nts, every day.

P. 6 Quaker Chemical Corporation

Supercharging productivity from the ground up.

Quaker Chemical Corporation P. 7

We make the world’s most productive mills even more so.

While the demand for pipes for the energy industry is trending up worldwide, pipe

production remains a very competitive business. To be successful, pipe manufacturers have

to be super productive to compete in a global market. They have to produce products at

the lowest possible cost. Whether the products are low-cost or not, their end-user

customers have high expectations. It’s a market where consistent, high quality is not

a request. It’s a demand. Rejects and returns can be a persistent problem—hurting profits

and a manufacturer’s reputation.

Quaker works with many of the most productive pipe mills in the world. These customers

want more than products and troubleshooting from us. They want a partner that can help

them improve their processes and their business.

Here’s one example: When a global pipe manufacturer began planning a new greenfield

seamless plant, a top priority was to maximize overall productivity. Quaker’s charge:

to significantly improve the performance of the final coating—a fast-curing UV coating that

protects pipes from corrosion. To supplement the knowledge Quaker culled from years

of experience, we sought input from the entire value chain, including the industry’s toughest

customers. To meet their demands, we created a new-to-market coating in our lab, then

field-tested it in very different climates—from Houston to Dubai—to validate its durability.

Today, the plant is coating up to 2,000 pipes per day at a highly competitive total cost

per unit. But, that’s only the beginning of the story. We will continue to collaborate

with our customer to drive down costs and advance the performance of their UV coatings

operations. In this startup, we’ve gained a closely aligned customer and generated

additional opportunities for ongoing growth throughout the plant.

Strategic partner from the

start: In 2013 alone, Quaker

was selected for eight steel

plant startups against

tough competition. As each

new facility comes on line,

a new revenue stream is

created for Quaker.

P. 8 Quaker Chemical Corporation

Staying ahead in the race to exploit new materials.

Quaker Chemical Corporation P. 9

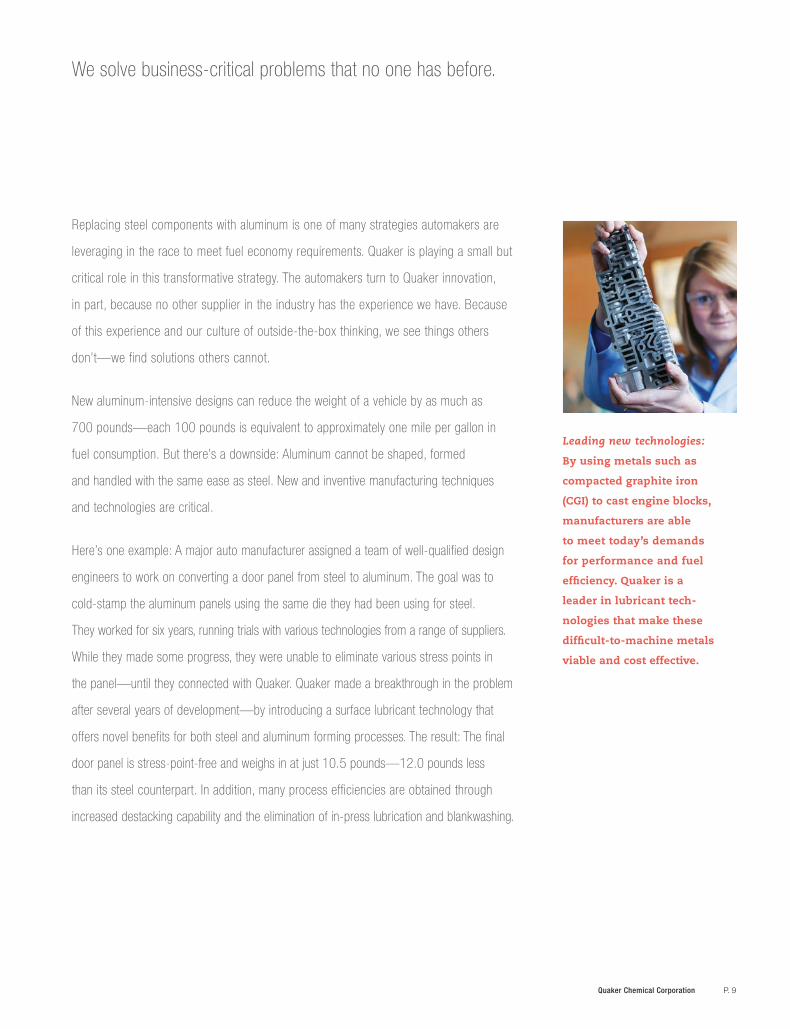

We solve business-critical problems that no one has before.

Replacing steel components with aluminum is one of many strategies automakers are

leveraging in the race to meet fuel economy requirements. Quaker is playing a small but

critical role in this transformative strategy. The automakers turn to Quaker innovation,

in part, because no other supplier in the industry has the experience we have. Because

of this experience and our culture of outside-the-box thinking, we see things others

don’t—we find solutions others cannot.

New aluminum-intensive designs can reduce the weight of a vehicle by as much as

700 pounds—each 100 pounds is equivalent to approximately one mile per gallon in

fuel consumption. But there’s a downside: Aluminum cannot be shaped, formed

and handled with the same ease as steel. New and inventive manufacturing techniques

and technologies are critical.

Here’s one example: A major auto manufacturer assigned a team of well-qualified design

engineers to work on converting a door panel from steel to aluminum. The goal was to

cold-stamp the aluminum panels using the same die they had been using for steel.

They worked for six years, running trials with various technologies from a range of suppliers.

While they made some progress, they were unable to eliminate various stress points in

the panel—until they connected with Quaker. Quaker made a breakthrough in the problem

after several years of development—by introducing a surface lubricant technology that

offers novel benefits for both steel and aluminum forming processes. The result: The final

door panel is stress-point-free and weighs in at just 10.5 pounds—12.0 pounds less

than its steel counterpart. In addition, many process efficiencies are obtained through

increased destacking capability and the elimination of in-press lubrication and blankwashing.

Leading new technologies:

By using metals such as

compacted graphite iron

(CGI) to cast engine blocks,

manufacturers are able

to meet today’s demands

for performance and fuel

efficiency. Quaker is a

leader in lubricant tech-

nologies that make these

difficult-to-machine metals

viable and cost effective.

P. 10 Quaker Chemical Corporation

Closing in on zero waste by re-imagining processes.

Quaker Chemical Corporation P. 11

We change the way manufacturers think about chemicals.

To make significant gains in sustainability, manufacturers need more than new chemical

products—they need new thinking. Quaker provides just that. We are a positive force

for change, helping customers think differently about how they use and dispose of their

chemicals. Our innovations have helped customers dramatically reduce their environmental

footprint and production costs.

By analyzing each process in the manufacturing operation sequentially, manufacturers

can achieve incremental improvements to waste production. Quaker’s thinking, however,

goes further. We view the entire operation holistically, as a circular system. This means

we can develop chemicals that are compatible for reuse in upstream processes. This

transforms entire manufacturing processes. These innovations in process design are game-

changing, especially for our customers that are large-scale manufacturers.

Here’s one example: A global manufacturer of automotive braking systems was looking

to reduce waste in its machining operations. Quaker devised an innovative approach—

a next-generation fluid and a complete overhaul of the way chemicals are introduced into

the process. This solution resulted in a 90% reduction in waste generation and brought

with it significant savings. The approach Quaker developed was a versatile, two-part fluid

that can be repurposed. First, the fluid is used as a process cleaner. When the cleaner

solution becomes saturated, instead of being disposed, it is added to the machining fluid

tank to “top-up” the volume—being used twice.

Quaker has been running this process in more than 60 central systems globally, some

for nearly eight years. There are still many untapped opportunities for us to be a catalyst

for positive change—and this means opportunities for our customers as well.

Rethinking waste in a

rolling mill: Quaker mini-

mized the sheer volume of

waste by separating (and

subsequently recycling) the

wastewater in a centrifuge.

The result: Waste was

reduced by 89% and the cost

of treatment by 90%.

P. 12 Quaker Chemical Corporation

Partnering for innovations in seemingly unlikely places.

Quaker Chemical Corporation P. 13

In pursuit of answers to help our customers overcome their challenges, we are always

exploring. But our quest goes far beyond current customer needs. We invest in research

and development because it’s vital to our growth and our ability to continue to be a

catalyst for our customers’ business success.

For us, research and technical development is a collaborative process. It requires

complex data, diverse expertise and forward-thinking people who like us, can’t help

asking “What if?” True next-generation solutions are almost never accomplished

alone. At Quaker, we form unique partnerships—with customers, equipment suppliers,

academia and even competitors. Some partnerships might surprise you.

Here’s one example: Bearings and the grease to lubricate them are critical to the

operation of nearly everything with a motor—from work rolls for making steel coils,

to wind turbines, to heavy equipment and light vehicles. To advance our bearing grease

portfolio, Quaker developed an uncommon partnership with an auto racing team.

Here’s why this seemingly unlikely partnership works. Race cars operate under extreme

conditions—conditions that vary greatly from track to track. It’s a perfect “real-world” test

situation. Plus, race engineers rely heavily on data—exactingly monitoring every small

detail of stress placed on the bearings—including speed, load and temperatures. They even

measure the temperature on the inside of the bearing case. The benefits for Quaker:

We leveraged the data to develop new bearing greases for extreme stress and temperature

conditions. The benefits for the race team engineers: They obtained an advantaged

grease—one that is helping them gain that extra fraction of a second advantage often

enough to mean the difference between first and third place. Truly, a win-win situation.

We relentlessly pursue next-generation solutions.

A two-way learning

relationship: By working on

specialized projects with

universities worldwide,

Quaker gains emerging

knowledge about industrial

metalworking processes

and properties of advanced

materials. At the same

time, the university teams

gain invaluable experience.

P. 14 Quaker Chemical Corporation

In 2013, we delivered record performance in sales, net income, adjusted

EBITDA and net operating cash flow. Our average share price has never

been higher. We generated double-digit earnings growth.

REVENUES:

$729.4million

Revenue grew 3% in 2013, despite challenging markets.

NET INCOME:

$56.3million

Profits rose by 19% in 2013, well over the increase in revenue.

NET OPERATING CASH FLOW:

$73.8million

Increased by 17% in 2013.

ADJUSTED EBITDA:

$89.6million

Increased 11% from 2012.

AVERAGE SHARE PRICE:

$66.29An all-time high, contributing to an excellent shareholder return.

EARNINGS PER DILUTED SHARE:

$4.27Earnings per diluted share were up 18% compared to 2012.

A year of record highs.

Quaker Chemical Corporation P. 15

A MESSAGE FROM MICHAEL F. BARRY, CHAIRMAN, CHIEF EXECUTIVE OFFICER AND PRESIDENT

DEAR SHAREHOLDERS, CUSTOMERS AND ASSOCIATES:

In 2013, we delivered record performance in sales, net

income, adjusted EBITDA and net operating cash flow.

We’re proud of this performance, especially because we

achieved these record-breaking results despite weaker than

expected economies in most regions. Over the last five

years, earnings have nearly tripled—from $1.45 per

diluted share in 2009 to $4.27 per diluted share in 2013.

Adjusted EBITDA increased to $90 million. In addition, our

strong cash flow continues to strengthen our balance sheet

and we now have more cash than debt.

Quaker’s total shareholder return outperformed many major

stock indices. The appreciation in stock price and dividends

yielded a 45% return to shareholders in 2013 on top of

a 42% return in 2012. Once again, Quaker’s average stock

price—$66.29 per share—was an all-time high. In the

second quarter, the Board approved an increase in our

quarterly dividend to $0.25 per share—the 37th time we

increased our dividend in 42 years as a public company.

CAPTURING GROWTH OPPORTUNITIES. During the year,

we experienced a slowdown in steel demand and industrial

activity in Europe, North America and South America, as

well as other economic uncertainties around the globe.

Despite these external challenges in 2013, our revenues grew

to $729 million, a 3% increase over 2012. Over the same

period, we achieved double-digit growth in net income.

We maximized our opportunities for revenue growth in 2013.

We increased sales to existing customers, gained market

share in our core businesses, re-established relationships

with prior customers and developed new business with new

customers. For example, of the new steel mills that were

commissioned globally last year, we won 8 of the 10 mills

where we participated in the bidding process. I want to thank

our associates for making these growth opportunities happen

despite the difficult environment.

We have made and continue to make good progress against

the strategic plan we put in place in 2009. In primary metals,

we continue to increase our share of our customers’ business.

We’ve outperformed

the major stock indices

over the last five years.

And in 2013, Quaker’s

total shareholder return

yielded a 45% return to

our shareholders.

400

$700

500

600

2009 2010 2011 2012

2009 2010 2011 2012

2013

2013

400

450

550

650

$750

500

600

2009 2010 2011 2012 20130

10

20

30

40

50

$60

1.00

$4.00

2.00

3.00

2009 2010 2011 2012

Dec 2011 Dec 2012 Dec 2013Dec 2010Dec 2009Dec 2008

Quaker Chemical Corporation S&P SmallCap 600 IndexS&P 600 Materials Group Index

S&P 600 Specialty Chemicals Index

0

100

200

300

400

500

700

$600

50

100

150

200

250

300

0

30

40

50

60

$70

10

20

*Excludes Unusual Items

0

60

$80

20

40

2005 to 2008 Avg

2012F201120102009

2012 Avg 2013 Avg2011 Avg2010 Avg2009 Avg30

40

50

60

70

80

$90

2012 2013201130

40

50

60

70

80

$90

2012 20132011

COMPARISON OF CUMULATIVE FIVE-YEAR TOTAL RETURN(assumes an investment of $100 on December 31, 2008)

P. 16 Quaker Chemical Corporation

400

$700

500

600

2009 2010 2011 2012

2009 2010 2011 2012

2013

2013

400

450

550

650

$750

500

600

2009 2010 2011 2012 20130

10

20

30

40

50

$60

1.00

$4.00

2.00

3.00

2009 2010 2011 2012

Dec 2011 Dec 2012 Dec 2013Dec 2010Dec 2009Dec 2008

Quaker Chemical Corporation S&P SmallCap 600 IndexS&P 600 Materials Group Index

S&P 600 Specialty Chemicals Index

0

100

200

300

400

500

700

$600

50

100

150

200

250

300

0

30

40

50

60

$70

10

20

*Excludes Unusual Items

0

60

$80

20

40

2005 to 2008 Avg

2012F201120102009

2012 Avg 2013 Avg2011 Avg2010 Avg2009 Avg30

40

50

60

70

80

$90

2012 2013201130

40

50

60

70

80

$90

2012 20132011

400

$700

500

600

2009 2010 2011 2012

2009 2010 2011 2012

2013

2013

400

450

550

650

$750

500

600

2009 2010 2011 2012 20130

10

20

30

40

50

$60

1.00

$4.00

2.00

3.00

2009 2010 2011 2012

Dec 2011 Dec 2012 Dec 2013Dec 2010Dec 2009Dec 2008

Quaker Chemical Corporation S&P SmallCap 600 IndexS&P 600 Materials Group Index

S&P 600 Specialty Chemicals Index

0

100

200

300

400

500

700

$600

50

100

150

200

250

300

0

30

40

50

60

$70

10

20

*Excludes Unusual Items

0

60

$80

20

40

2005 to 2008 Avg

2012F201120102009

2012 Avg 2013 Avg2011 Avg2010 Avg2009 Avg30

40

50

60

70

80

$90

2012 2013201130

40

50

60

70

80

$90

2012 20132011

REVENUE TREND(dollars in millions)

NET INCOME TREND(dollars in millions)

In metalworking, we are working to build a market-leader

position in the tube & pipe and engines & transmissions

segments—and are making headway. And, to ensure our

future and take into account an ever-changing and challenging

environment, we reviewed and updated our strategic plan.

CONTINUING TO INVEST IN GROWTH INITIATIVES. We have

completed seven acquisitions since mid-2010, including the

2013 acquisitions of a business primarily related to tin plating

in the U.S. and a chemical milling maskants distribution network

in China. Integration of these businesses into Quaker is still in

its early stages, but we have begun to realize their benefits.

By introducing our newly acquired technologies to our existing

customers and leveraging our global reach to enter new markets,

we are gaining a wide range of new opportunities. In our specialty

grease business (acquired in December 2010), we grew existing

business, enhanced profitability and identified “next steps” to

expand into global markets. In aluminum hot rolling (acquired

in July 2010), we have added new business in Europe and the

Middle East. And in die casting (acquired in October 2011), we

gained business in China, Southeast Asia and South America.

We are confidently investing capital and resources to establish

a larger footprint and build capacity in regions where growth is

most robust for us. During 2013, we built a new manufacturing

plant in Qingpu, China to keep pace with that region’s growing

opportunities. At the same time, we made progress in our plan

to build a new facility in India.

A LOOK TOWARD THE FUTURE. While traditionally the purpose

of this letter is to report on the past year, most of you, like me, are

more interested in the future. The future looks bright for Quaker.

With our strategic growth initiatives and implementation plans in

place, we’re on the right track to continue to increase our revenue

and profits. We have many reasons to be positive about what’s

next for us. And the financial strength we’ve generated over the

past five years gives us the flexibility to fund our growth initiatives

and to act quickly on acquisition opportunities.

“Where will future growth come from?” Essentially, Quaker will

draw on four sources—our base markets, market share, prior

acquisitions, and future acquisitions.

A MESSAGE FROM MICHAEL F. BARRY, CHAIRMAN, CHIEF EXECUTIVE OFFICER AND PRESIDENT

Quaker Chemical Corporation P. 17

400

$700

500

600

2009 2010 2011 2012

2009 2010 2011 2012

2013

2013

400

450

550

650

$750

500

600

2009 2010 2011 2012 20130

10

20

30

40

50

$60

1.00

$4.00

2.00

3.00

2009 2010 2011 2012

Dec 2011 Dec 2012 Dec 2013Dec 2010Dec 2009Dec 2008

Quaker Chemical Corporation S&P SmallCap 600 IndexS&P 600 Materials Group Index

S&P 600 Specialty Chemicals Index

0

100

200

300

400

500

700

$600

50

100

150

200

250

300

0

30

40

50

60

$70

10

20

*Excludes Unusual Items

0

60

$80

20

40

2005 to 2008 Avg

2012F201120102009

2012 Avg 2013 Avg2011 Avg2010 Avg2009 Avg30

40

50

60

70

80

$90

2012 2013201130

40

50

60

70

80

$90

2012 20132011

ADJUSTED EBITDA*(dollars in millions)

400

$700

500

600

2009 2010 2011 2012

2009 2010 2011 2012

2013

2013

400

450

550

650

$750

500

600

2009 2010 2011 2012 20130

10

20

30

40

50

$60

1.00

$4.00

2.00

3.00

2009 2010 2011 2012

Dec 2011 Dec 2012 Dec 2013Dec 2010Dec 2009Dec 2008

Quaker Chemical Corporation S&P SmallCap 600 IndexS&P 600 Materials Group Index

S&P 600 Specialty Chemicals Index

0

100

200

300

400

500

700

$600

50

100

150

200

250

300

0

30

40

50

60

$70

10

20

*Excludes Unusual Items

0

60

$80

20

40

2005 to 2008 Avg

2012F201120102009

2012 Avg 2013 Avg2011 Avg2010 Avg2009 Avg30

40

50

60

70

80

$90

2012 2013201130

40

50

60

70

80

$90

2012 20132011

STOCK PRICE TREND(average share price in dollars)

> Growth in our base markets. We expect our base markets

to grow at a faster rate than they have in the past few years.

We anticipate at least modest growth in all regions of the

world during 2014—a welcome change from the previous

environment where at least one part of the world was

experiencing a weakened economy. And, we foresee a brighter

outlook for our core end-markets—steel and automotive.

> Gains in market share. Over the past several years, we had

to overcome the uneven global markets and grow organically

by increasing our market share. We expect our success in

growing share to continue. Our “customer intimate” business

model differentiates us from our competitors. This is a model

based on establishing strong relationships at multiple levels

in our customers’ organizations, gaining a deep understanding

of their needs, and solving their critical business challenges

with urgency—unique in the specialty chemicals industry and

difficult for others to duplicate. Committed to implementing our

model successfully, we believe we will retain this advantage. Our

delivery on this model, combined with our exceptional talent and

technology, makes us confident we will continue to gain share.

> Leveraging our acquisitions. In addition to organic growth

and market share gains, we expect our recent acquisitions to

contribute to our bottom line. Through our recent acquisitions,

we gained five new product technologies. We are in the midst

of using our global infrastructure and customer relationships

to market these technologies in new regions around the world.

* See page 23 of Form

10-K for reconciliation

of Adjusted EBITDA.

P. 18 Quaker Chemical Corporation

While we are still in the early stages of doing this, I’m optimistic

that these recent acquisitions will be a strong source for our

future growth.

> New strategic acquisitions. Moving forward, we will

continue to explore new acquisition targets to strengthen

our position in our existing markets and to bring new

technologies to our markets. We believe there will be potential

acquisition opportunities in our market space over the

next several years that can create significant value for our

shareholders. As I mentioned earlier, our strong cash flow

and balance sheet positions provide us tremendous financial

flexibility to make these acquisitions.

POWER IN DISTINCTION. We have been on a path to establish

ourselves as a market leader with a clear and recognizable

difference compared to our competitors. We made a

commitment to become a company that creates true value

for our customers by delivering tangible solutions that help

their business success. While there is always more work to do,

we are now that company.

Our strong performance in 2013 is a testament to the strength

of this differentiation and to the discipline and ability of Quaker

associates to execute our strategic growth initiatives around

the world. Our associates work hard, have determination and

are driven to find “right solutions” to challenges every day.

And they have staying power. I’m proud to say, we have low

turnover at Quaker. This is key for us because our associates

are our most valuable asset. Our culture fosters continual

learning and development with opportunities for advancement

into key positions. In addition, we have been fortunate to

attract new and experienced talent in all regions to further our

competitive advantage.

In the coming year, we remain committed to achieving

outstanding performance, returning value to our stakeholders

and being a progressive force in our customers’ success.

In closing, I thank all of you—our shareholders, our customers

and our associates—for your continued support and

confidence. Our future together continues to be bright.

Best regards,

Michael F. Barry

Chairman of the Board, Chief Executive Officer and President

A MESSAGE FROM MICHAEL F. BARRY, CHAIRMAN, CHIEF EXECUTIVE OFFICER AND PRESIDENT

Quaker Chemical Corporation P. 19

PRODUCT LINES

GLOBAL PRESENCE

SUSTAINABILITY / CORPORATE SOCIAL RESPONSIBILITY

WHO WE SERVE

NET SALES

• North America $308.4 million

• EMEA $187.8 million

• Asia/Pacific $169.5 million

• South America $63.7 million

Selling our products in more than 75 countries to a diverse base of customers, Quaker has an increasingly broad geographic distribution of revenue.

We are committed to creating a positive social, environmental and economic impact on our world and those we touch, using our Core Values as a guide.

During 2013, we took some important steps to strengthen our program and improve metrics and oversight by:

• Gaining a better understanding of customer expectations

• Collecting baseline data on our current practices

• Creating regional Green Teams in each Quaker location

MARINE

MINING

PRIMARY METALS

TUBE AND PIPE

AEROSPACE

AUTOMOTIVE

CANS

CONSTRUCTION PRODUCTS

HEAVY EQUIPMENT

STRATEGIC ACQUISITIONS

$729.4 million

PROCESS FLUIDS

Quaker provides custom-formulated process chemicals for heavy industrial and manufacturing applications. We are the global leader in rolling lubricants used for the hot and cold rolling of steel. Our metalworking fluids are used in nearly every manufacturing process and include lubricants for casting, forming, cutting, finishing, stamping, drawing, machining and grinding, as well as cleaners and corrosion preventives.

FLUID POWER

Quaker is a global leader in the manufacture and sale of synthetic, non-toxic, fire-resistant hydraulic fluids. Our extensive experience—in more than 50,000 hydraulic systems around the world—has built our strong reputation among equipment manufacturers and end users.

COATINGS

Quaker’s coatings business provides temporary and permanent coatings for metal and concrete products, chemical milling maskants for the aerospace industry, and sealants and protective coatings for construction products.

CHEMICAL MANAGEMENT SERVICES

Quaker offers a full range of custom-designed chemical management services from chemical and inventory control to process management. This is an integrated product, application support, and service offering that puts Quaker in charge of virtually all chemi-cals used in a customer’s operation. The services have been proven to lower total cost, increase productivity, and improve product quality.

MAY ’13 TIN PLATING BUSINESS Complementary technologies

JAN ’13 CHEMICAL MILLING MASKANTS DISTRIBUTION NETWORK Strengthens position in China

JUL ’12 METAL SURFACE TREATMENT PRODUCTS Complementary technologies

OCT ’11 DIE-CASTING LUBRICANTS Complementary product line

JUL ’11 REMAINING INTEREST IN JOINT VENTURE Strengthens position in Mexico

DEC ’10 SPECIALTY GREASES Complementary technologies

JUL ’10 ALUMINUM HOT ROLLING OILS—U.S. BUSINESS Complementary product line

Quaker At-a-Glance

P. 20 Quaker Chemical Corporation

DIRECTORS

Joseph B. Anderson, Jr. (2,4)

Chairman and Chief Executive Officer, TAG Holdings, LLC, a parent company for a variety of manufacturing and service- based enterprises

Patricia C. Barron (3,4)

Corporate Director; Lead Director

Michael F. Barry (1)

Chairman of the Board, Chief Executive Officer and President

Donald R. Caldwell (1,2,3)

Chairman and Chief Executive Officer, Cross Atlantic Capital Partners, Inc., a venture capital management company; Executive Committee Chairman

Robert E. Chappell (1,4)

Former Chairman and Chief Executive Officer, The Penn Mutual Life Insurance Company, a mutual life insurance company; Governance Committee Chairman

William R. Cook (1,2)

Former President and Chief Executive Officer, Severn Trent Services, Inc., a water purification products and laboratory and operating services company; Audit Committee Chairman

Mark A. Douglas (2,4)

President, FMC Agricultural Solutions, FMC Corporation, a diversified chemical company

Jeffry D. Frisby (2,3)

President and Chief Executive Officer, Triumph Group, Inc., a company that, through its subsidiaries, designs, engineers, manufactures, repairs, overhauls and distributes aircraft components

Robert H. Rock (1,3)

President, MLR Holdings, LLC, an investment company operating in the publishing and information industry; Compensation/Management Development Committee Chairman

Committees of the Board:

(1) Executive (2) Audit (3) Compensation/Management Development (4) Governance

Michael F. BarryChairman of the Board, Chief Executive Officer and President

Margaret M. LoeblVice President, Chief Financial Officer and Treasurer

D. Jeffry Benoliel Vice President and Global Leader—Metalworking, Can and Corporate Secretary

Dieter Laininger Vice President and Managing Director—South America and Global Leader— Primary Metals

Joseph A. Berquist Vice President and Managing Director— North America

Quaker Leadership

Quaker Chemical Corporation P. 21

CHAIRMEN EMERITI

Peter A. BenolielFormer Chairman of the Board and Chief Executive Officer of the Company

Ronald J. NaplesFormer Chairman of the Board and Chief Executive Officer of the Company

OFFICERS

Michael F. Barry Chairman of the Board, Chief Executive Officer and President

D. Jeffry BenolielVice President and Global Leader— Metalworking, Can and Corporate Secretary

Joseph A. BerquistVice President and Managing Director— North America

Ronald S. EttingerVice President—Human Resources

Dieter LainingerVice President and Managing Director— South America and Global Leader— Primary Metals

Margaret M. LoeblVice President, Chief Financial Officer and Treasurer

Joseph F. MatrangeVice President and Global Leader—Coatings

Jan F. NiemanVice President and Global Leader— Grease, Fluid Power and Mining

Wilbert PlatzerVice President and Managing Director— EMEA

Adrian Steeples Vice President and Managing Director— Asia/Pacific

Irene M. KisleikoAssistant Corporate Secretary and Manager, Investor Relations

John H. YardleyGlobal Tax Director

Ronald S. EttingerVice President— Human Resources

Jan F. Nieman Vice President and Global Leader—Grease, Fluid Power and Mining

Wilbert Platzer Vice President and Managing Director—EMEA

Joseph F. Matrange Vice President and Global Leader—Coatings

Adrian Steeples Vice President and Managing Director—Asia/Pacific

P. 22 Quaker Chemical Corporation

Global Operations

CORPORATE HEADQUARTERS

Quaker Chemical Corporation One Quaker Park 901 E. Hector Street Conshohocken, Pennsylvania 19428-2380 Phone: 610-832-4000 Fax: 610-832-8682 Website: www.quakerchem.com

Quaker Chemical Corporation Wilmington, Delaware

NORTH AMERICAN OPERATIONS

Quaker Chemical Corporation – Downers Grove, Illinois – Bingham Farms, Michigan – Detroit, Michigan – Middletown, Ohio – Conshohocken, Pennsylvania

AC Products, Inc.Whittier, California

Epmar CorporationSanta Fe Springs, California

G.W. Smith and Sons, Inc.Dayton, Ohio

Q2 Technologies, LLCMontgomery, Texas (70% owned)

Quaker Chemical Canada LimitedToronto, Ontario

Quaker Chemical Corporation Mexico, S.A. de C.V.Mexico City, Mexico

Quaker Chemical HR Mexico, S.A. de C.V.Mexico City, Mexico

Summit Lubricants, Inc.Batavia, New York

Tecniquimia Mexicana S.A. de C.V.Monterrey, Mexico

H.L. Blachford, Ltd.Mississauga, Ontario Licensee

EUROPEAN OPERATIONS

NP Coil Dexter Industries, S.r.l.Gorgonzola, Italy

Quaker Chemical B.V.Uithoorn, The Netherlands

Quaker Chemical Europe B.V.Uithoorn, The Netherlands

Quaker Chemical Limited Stonehouse, England

Quaker Chemical S.A.Gennevilliers, France

Quaker Chemical, S.A.Barcelona, Spain

Quaker Chemical Hungary Ltd.Budapest, Hungary

Quaker Italia S.r.l.Tradate, Italy

Quaker Chemical B.V.(Representative Office) Moscow, Russia

SOUTH AFRICAN OPERATIONS

Quaker Chemical South Africa (Pty.) Ltd.Wadeville, Republic of South Africa (51% owned)

ASIA/PACIFIC OPERATIONS

Nippon Quaker Chemical, Ltd.Osaka, Japan (50% owned)

Quaker Chemical (Australasia) Pty. LimitedSeven Hills, New South Wales, Australia (51% owned)

Quaker Chemical (China) Co. Ltd. Shanghai, China

Quaker Chemical India Limited Kolkata, India (55% owned)

Quaker Chemical LimitedHong Kong, China

Quaker Shanghai Trading Co., Ltd.Shanghai, China

Quaker (Thailand) Ltd.Bangkok, Thailand

SOUTH AMERICAN OPERATIONS

Quaker Chemical Indústria e Comércio Ltda.Rio de Janeiro, Brazil

Quaker Chemical Operações Ltda.Rio de Janeiro, Brazil

Quaker Chemical S.A.Buenos Aires, Argentina

Kelko Quaker Chemical, S.A.Caracas, Venezuela (50% owned)

Quaker Chemical Corporation P. 23

INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

PricewaterhouseCoopers LLP Two Commerce Square, Suite 1700 2001 Market Street Philadelphia, Pennsylvania 19103-7042

STOCK TRANSFER AGENT

For address changes, dividend checks, lost stock certificates, share ownership and other administrative services, contact: American Stock Transfer & Trust Company, LLC, 6201 15th Avenue, Brooklyn, NY 11219. Phone: 1-800-937-5449; Website: www.amstock.com

INVESTOR RELATIONS

Security analysts, portfolio managers and representatives of financial institutions seeking information about the Company are invited to contact: Margaret M. Loebl, Vice President, Chief Financial Officer and Treasurer at 610-832-4160.

Copies of the Company’s Annual Report on Form 10-K and other corporate filings will be provided without charge upon request by contacting: Irene M. Kisleiko, Assistant Corporate Secretary and Manager, Investor Relations at 610-832-4119 or via email to [email protected].

We also invite you to visit the Investor Relations section of our website www.quakerchem.com for expanded information about the Company and to view our online, interactive annual report.

ANNUAL MEETING

The Annual Meeting of Shareholders will be held at the Company’s headquarters located at One Quaker Park, 901 E. Hector Street, Conshohocken, Pennsylvania, on May 7, 2014 at 8:30 a.m.

DIVIDEND REINVESTMENT & STOCK PURCHASE PLAN

Quaker’s Dividend Reinvestment and Stock Purchase Plan offers shareholders a convenient and economical way to purchase additional Quaker Common Shares through the reinvestment of dividends and/or voluntary cash contributions without commissions or transaction fees. For further information concerning the Plan, contact American Stock Transfer & Trust Company, LLC at 1-877-724-6458.

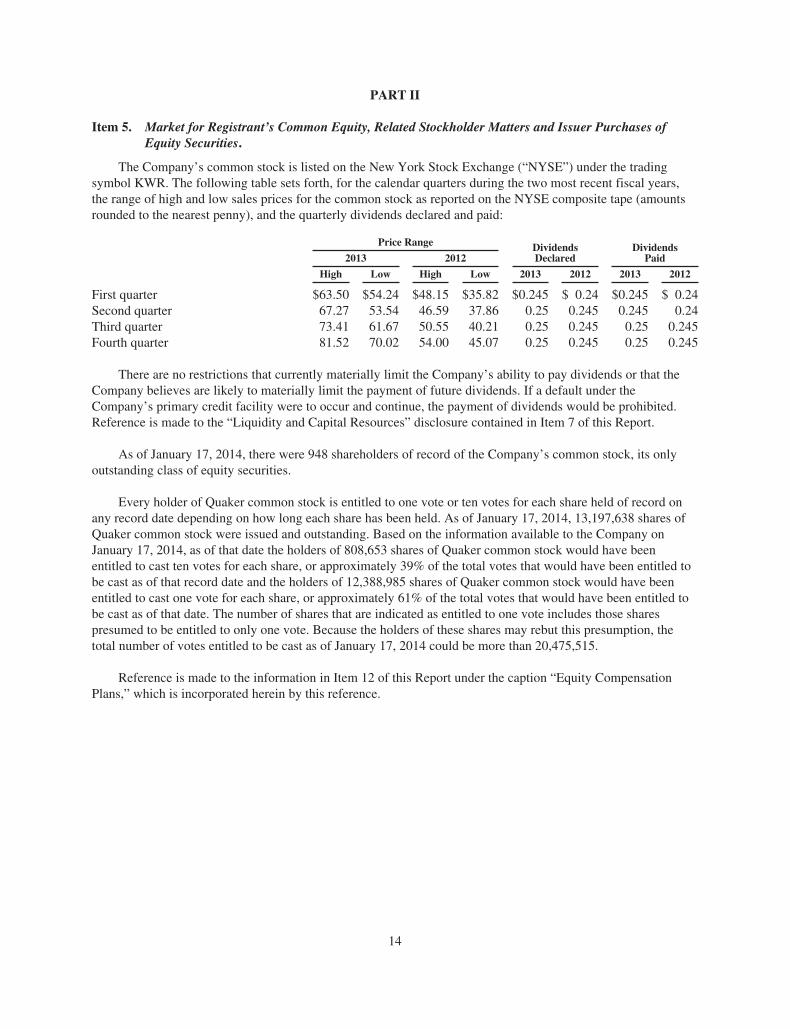

QUARTERLY STOCK INFORMATION

The following table sets forth, for the calendar quarters during the past two years, the range of high and low sales prices for the common stock as reported on the NYSE composite tape (amounts rounded to the nearest penny) and the quarterly dividends paid:

2013 2012 Dividends Paid

High Low High Low 2013 2012

First Quarter $63.50 $54.24 $48.15 $35.82 $0.245 $0.24

Second Quarter 67.27 53.54 46.59 37.86 0.245 0.24

Third Quarter 73.41 61.67 50.55 40.21 0.25 0.245

Fourth Quarter 81.52 70.02 54.00 45.07 0.25 0.245

As of January 17, 2014, there were 948 shareholders of record of the Company’s common stock, $1.00 par value, its only outstanding class of equity securities. This number does not include shareholders whose shares were held in nominee name.

Corporate Information

P. 24 Quaker Chemical Corporation

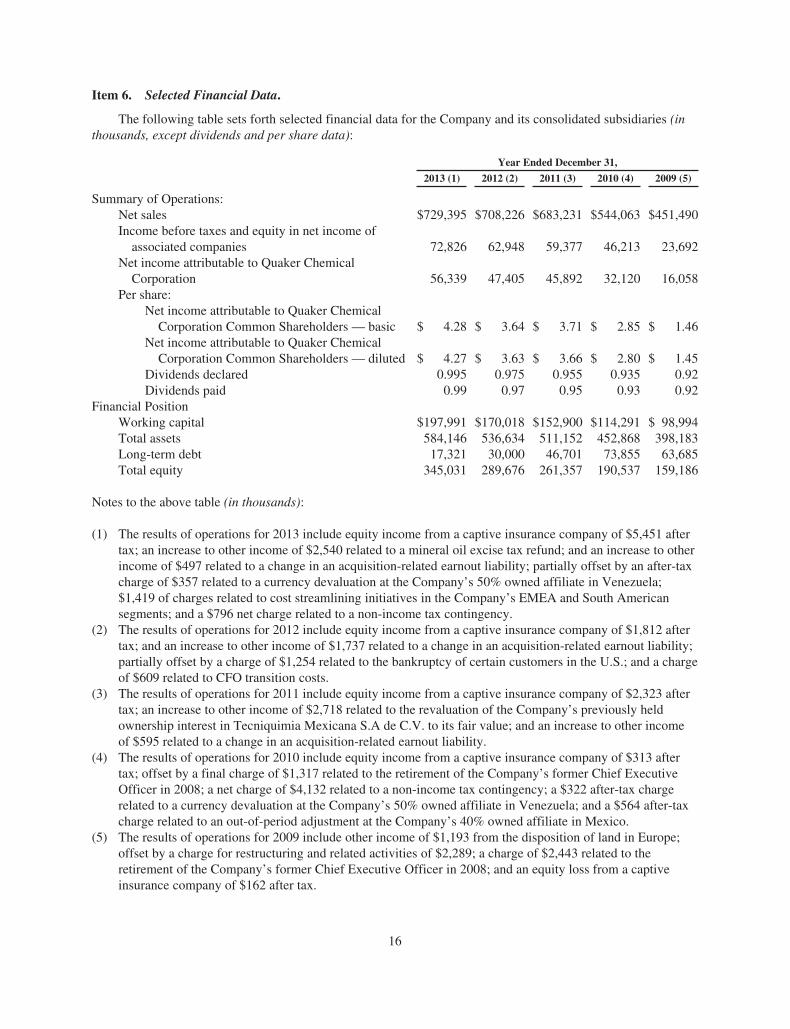

SUMMARY OF OPERATIONSNet sales $729,395 $708,226 $683,231 $544,063 $451,490Income before taxes 72,826 62,948 59,377 46,213 23,692Net income attributable to Quaker Chemical Corporation 56,339 47,405 45,892 32,120 16,058Per share

Net income attributable to Quaker Chemical Corporation Common Shareholders—basic 4.28 3.64 3.71 2.85 1.46

Net income attributable to Quaker Chemical Corporation Common Shareholders—diluted 4.27 3.63 3.66 2.80 1.45

Dividends declared 0.995 0.975 0.955 0.935 0.92Dividends paid 0.99 0.97 0.95 0.93 0.92

FINANCIAL POSITIONCurrent assets 328,847 277,810 259,549 215,482 199,174Current liabilities 130,856 107,792 106,649 101,191 100,180Working capital 197,991 170,018 152,900 114,291 98,994Property, plant and equipment, net 85,488 85,112 82,916 76,535 67,426Total assets 584,146 536,634 511,152 452,868 398,183Long-term debt 17,321 30,000 46,701 73,855 63,685Total equity 345,031 289,676 261,357 190,537 159,186

OTHER DATACurrent ratio 2.51/1 2.58/1 2.43/1 2.13/1 1.99/1Capital expenditures 11,439 12,735 12,117 9,354 13,834Net income as a percentage of net sales 7.7% 6.7% 6.7% 5.9% 3.6%Return on average equity 17.8% 17.2% 20.3% 18.4% 11.0%Equity per share at end of year 26.15 22.12 20.24 16.58 14.36Common stock per share price range:

High 81.52 54.00 46.02 45.80 23.82Low 53.54 35.82 24.11 16.14 4.65

Number of shares outstanding at end of year 13,196 13,095 12,912 11,492 11,086Number of employees at end of year:

Consolidated subsidiaries 1,783 1,711 1,643 1,385 1,252Associated companies 74 65 81 225 152

Selected Financial Data

(1) The results of operations for 2013

include equity income from a captive

insurance company of $5,451 after tax;

an increase to other income of $2,540

related to a mineral oil excise tax refund;

and an increase to other income of

$497 related to a change in an

acquisition-related earnout liability;

partially offset by an after tax charge of

$357 related to a currency devaluation

at the Company’s 50% owned affiliate in

Venezuela; $1,419 of charges related to

cost streamlining initiatives in the

Company’s EMEA and South American

segments; and a $796 net charge

related to a non-income tax contingency.

(2) The results of operations for 2012

include equity income from a captive

insurance company of $1,812 after tax;

and an increase to other income

of $1,737 related to a change in an

acquisition-related earnout liability;

partially offset by a charge of $1,254

related to the bankruptcy of certain

customers in the U.S.; and a charge of

$609 related to CFO transition costs.

(3) The results of operations for 2011

include equity income from a captive

insurance company of $2,323 after

tax; an increase to other income of

$2,718 related to the revaluation of

the Company’s previously held

ownership interest in Tecniquimia

Mexicana S.A. de C.V. to its fair value;

and an increase to other income of

$595 related to a change in an

acquisition-related earnout liability.

(4) The results of operations for 2010

include equity income from a captive

insurance company of $313 after tax;

offset by a final charge of $1,317

related to the retirement of the

Company’s former Chief Executive

Officer in 2008; a net charge of

$4,132 related to a non-income tax

contingency; a $322 after tax charge

related to a currency devaluation at the

Company’s 50% owned affiliate in

Venezuela; and a $564 after tax

charge related to an out-of-period

adjustment at the Company’s 40%

owned affiliate in Mexico.

(5) The results of operations for 2009

include other income of $1,193 from

the disposition of land in Europe;

offset by a charge for restructuring and

related activities of $2,289; a charge

of $2,443 related to the retirement of

the Company’s former Chief Executive

Officer in 2008; and an equity loss

from a captive insurance company of

$162 after tax.

(In thousands except per share data, percentages, and number of employees) 2013(1)

2012(2)

2011(3)

recast 2010

(4)

recast 2009

(5)

recast

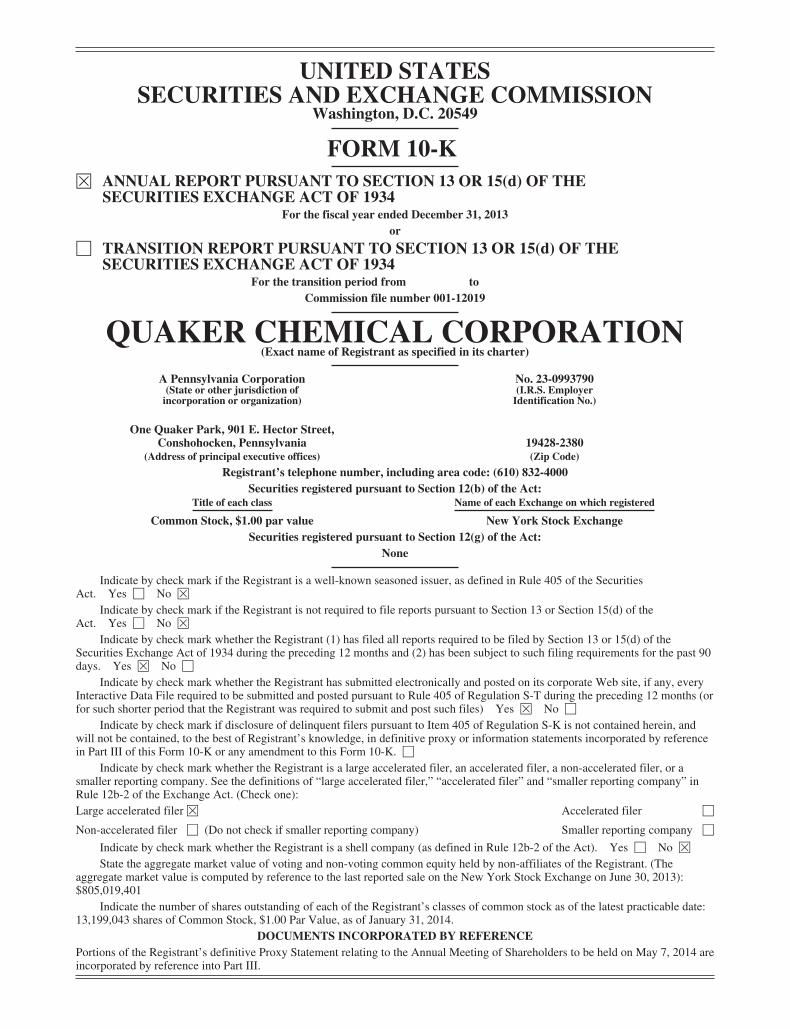

UNITED STATESSECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-KÈ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934For the fiscal year ended December 31, 2013

or

‘ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THESECURITIES EXCHANGE ACT OF 1934

For the transition period from toCommission file number 001-12019

QUAKER CHEMICAL CORPORATION(Exact name of Registrant as specified in its charter)

A Pennsylvania Corporation No. 23-0993790(State or other jurisdiction of

incorporation or organization)(I.R.S. Employer

Identification No.)

One Quaker Park, 901 E. Hector Street,Conshohocken, Pennsylvania 19428-2380

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (610) 832-4000Securities registered pursuant to Section 12(b) of the Act:

Title of each class Name of each Exchange on which registered

Common Stock, $1.00 par value New York Stock ExchangeSecurities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the SecuritiesAct. Yes ‘ No È

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of theAct. Yes ‘ No È

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of theSecurities Exchange Act of 1934 during the preceding 12 months and (2) has been subject to such filing requirements for the past 90days. Yes È No ‘

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, everyInteractive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (orfor such shorter period that the Registrant was required to submit and post such files) Yes È No ‘

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, andwill not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by referencein Part III of this Form 10-K or any amendment to this Form 10-K. ‘

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or asmaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” inRule 12b-2 of the Exchange Act. (Check one):Large accelerated filer È Accelerated filer ‘

Non-accelerated filer ‘ (Do not check if smaller reporting company) Smaller reporting company ‘

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ‘ No È

State the aggregate market value of voting and non-voting common equity held by non-affiliates of the Registrant. (Theaggregate market value is computed by reference to the last reported sale on the New York Stock Exchange on June 30, 2013):$805,019,401

Indicate the number of shares outstanding of each of the Registrant’s classes of common stock as of the latest practicable date:13,199,043 shares of Common Stock, $1.00 Par Value, as of January 31, 2014.

DOCUMENTS INCORPORATED BY REFERENCEPortions of the Registrant’s definitive Proxy Statement relating to the Annual Meeting of Shareholders to be held on May 7, 2014 areincorporated by reference into Part III.

PART I

As used in this Report, the terms “Quaker,” the “Company,” “we” and “our” refer to Quaker ChemicalCorporation, its subsidiaries, and associated companies, unless the context otherwise requires.

Item 1. Business.

General Description

Quaker develops, produces, and markets a broad range of formulated chemical specialty products and offerschemical management services (“CMS”) for various heavy industrial and manufacturing applications in a globalportfolio throughout its four regions: the North America region, the Europe, Middle East and Africa (“EMEA”)region, the Asia/Pacific region and the South America region. The principal products and services in Quaker’sglobal portfolio include: (i) rolling lubricants (used by manufacturers of steel in the hot and cold rolling of steeland by manufacturers of aluminum in the hot rolling of aluminum); (ii) corrosion preventives (used by steel andmetalworking customers to protect metal during manufacture, storage, and shipment); (iii) metal finishingcompounds (used to prepare metal surfaces for special treatments such as galvanizing and tin plating and toprepare metal for further processing); (iv) machining and grinding compounds (used by metalworking customersin cutting, shaping, and grinding metal parts which require special treatment to enable them to tolerate themanufacturing process, achieve closer tolerance, and improve tool life); (v) forming compounds (used tofacilitate the drawing and extrusion of metal products); (vi) hydraulic fluids (used by steel, metalworking, andother customers to operate hydraulically activated equipment); (vii) chemical milling maskants for the aerospaceindustry and temporary and permanent coatings for metal and concrete products; (viii) construction products,such as flexible sealants and protective coatings, for various applications; (ix) specialty greases; (x) die castinglubricants; (xi) technology for the removal of hydrogen sulfide in various industrial applications; and(xii) programs to provide chemical management services. Individual product lines representing more than 10% ofconsolidated revenues for any of the past three years are as follows:

2013 2012 2011

Rolling Lubricants 20.7% 20.7% 22.0%Machining and grinding compounds 17.7% 17.6% 18.8%Hydraulic fluids 12.9% 13.5% 12.9%Corrosion preventives 12.5% 12.4% 11.5%

A substantial portion of Quaker’s sales worldwide are made directly through its own employees and itsCMS programs with the balance being handled through distributors and agents. Quaker employees visit theplants of customers regularly and, through training and experience, identify production needs which can beresolved or alleviated either by adapting Quaker’s existing products or by applying new formulations developedin Quaker’s laboratories. Quaker relies less on the use of advertising, and more heavily upon its reputation in themarkets which it serves. Generally, separate manufacturing facilities of a single customer are served by differentpersonnel. As part of the Company’s chemical management services, certain third-party product sales tocustomers are managed by the Company. Where the Company acts as principal, revenues are recognized on agross reporting basis at the selling price negotiated with its customers. Where the Company acts as an agent, suchrevenue is recorded using net reporting as service revenues at the amount of the administrative fee earned by theCompany for ordering the goods. Third-party products transferred under arrangements resulting in net reportingtotaled $41.6 million, $39.3 million and $50.9 million for 2013, 2012 and 2011, respectively. The Companyrecognizes revenue in accordance with the terms of the underlying agreements, when title and risk of loss havebeen transferred, when collectability is reasonably assured, and when pricing is fixed or determinable. Thisgenerally occurs for product sales when products are shipped to customers or, for consignment-typearrangements, upon usage by the customer and, for services, when they are performed. License fees and royaltiesare included in other income when recognized in accordance with agreed-upon terms, when performanceobligations are satisfied, when the amount is fixed or determinable, and when collectability is reasonably assured.

1

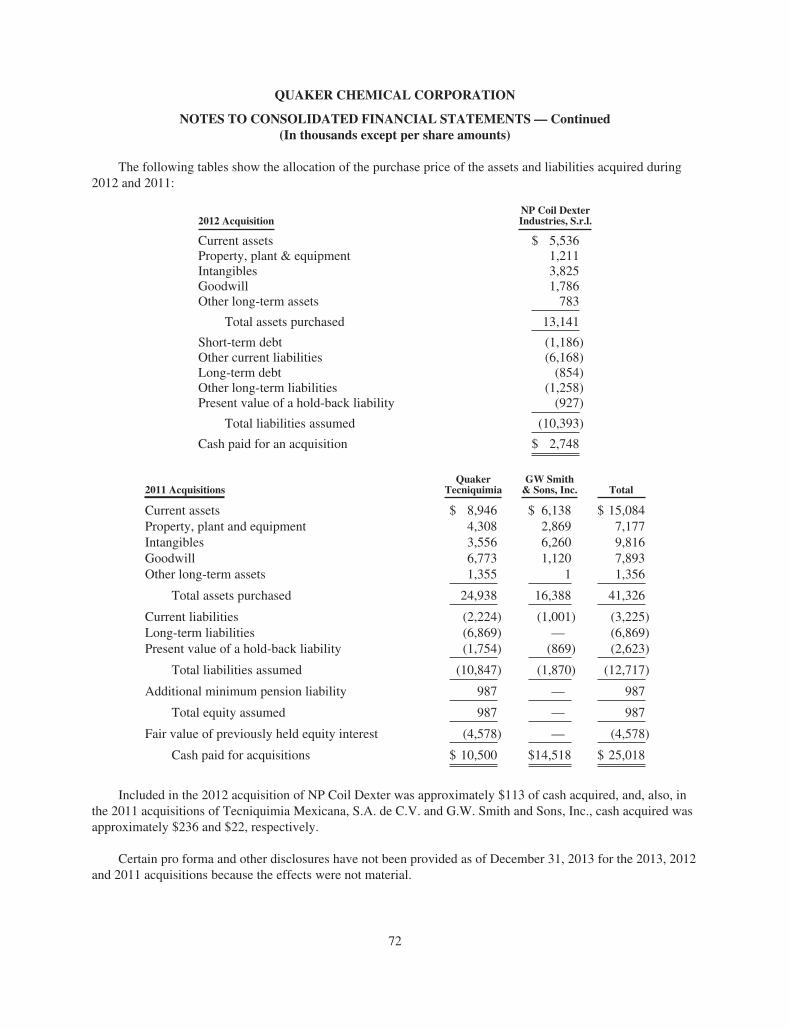

In 2013, the Company acquired a chemical milling maskants distribution network for net consideration ofapproximately $0.7 million and a business that primarily related to tin plating for net consideration ofapproximately $1.8 million. In July 2012, the Company acquired NP Coil Dexter Industries, S.r.l., forapproximately $2.7 million. NP Coil Dexter is a European manufacturer and supplier of metal surface treatmentproducts.

Competition

The chemical specialty industry comprises a number of companies of similar size as well as companieslarger and smaller than Quaker. Quaker cannot readily determine its precise position in every industry it serves.Based on information available to Quaker, however, it is estimated that Quaker holds a leading global position(among a group in excess of 25 other suppliers) in the market for process fluids to produce sheet steel. It is alsobelieved that Quaker holds significant global positions in the markets for process fluids in portions of theautomotive and industrial markets. The offerings of many of our competitors differ from Quaker, with some whooffer a broad portfolio of fluids, including general lubricants, to those who have a more specialized productrange, and all of whom provide different levels of technical services to individual customers. Competition in theindustry is based primarily on the ability to provide products that meet the needs of the customer, rendertechnical services and laboratory assistance to the customer and, to a lesser extent, on price.

Major Customers and Markets

In 2013, Quaker’s five largest customers (each composed of multiple subsidiaries or divisions with semi-autonomous purchasing authority) accounted for approximately 18% of our consolidated net sales, with thelargest customer (Arcelor-Mittal Group) accounting for approximately 9% of our consolidated net sales. Asignificant portion of Quaker’s revenues are realized from the sale of process fluids and services tomanufacturers of steel, automobiles, appliances, and durable goods, and, therefore, Quaker is subject to the samebusiness cycles as those experienced by these manufacturers and their customers. Furthermore, steel customerstypically have limited manufacturing locations as compared to metalworking customers and generally use highervolumes of products at a single location. Accordingly, the loss or closure of a steel mill or other major customersite can have a material adverse effect on Quaker’s business.

Raw Materials

Quaker uses over 1,000 raw materials, including mineral oils and derivatives, animal fats and derivatives,vegetable oils and derivatives, ethylene derivatives, solvents, surface active agents, chlorinated paraffiniccompounds, and a wide variety of other organic and inorganic compounds. In 2013, three raw material groups(mineral oils and derivatives, animal fats and derivatives, and vegetable oils and derivatives) each accounted forat least 10% of the total cost of Quaker’s raw material purchases. The price of mineral oil can be affected by theprice of crude oil and its refining capacity. In addition, animal fat and vegetable oil prices are impacted byincreased biodiesel consumption. Accordingly, significant fluctuations in the price of crude oil can have amaterial effect upon the Company’s business. Many of the raw materials used by Quaker are “commodity”chemicals, and, therefore, Quaker’s earnings can be affected by market changes in raw material prices. Referenceis made to the disclosure contained in Item 7A of this Report.

Patents and Trademarks

Quaker has a limited number of patents and patent applications, including patents issued, applied for, oracquired in the United States and in various foreign countries, some of which may prove to be material to itsbusiness. Principal reliance is placed upon Quaker’s proprietary formulae and the application of its skills andexperience to meet customer needs. Quaker’s products are identified by trademarks that are registered throughoutits marketing area.

2

Research and Development — Laboratories

Quaker’s research and development laboratories are directed primarily toward applied research anddevelopment since the nature of Quaker’s business requires continual modification and improvement offormulations to provide chemical specialties to satisfy customer requirements. Quaker maintains quality controllaboratory facilities in each of its manufacturing locations. In addition, Quaker maintains facilities inConshohocken, Pennsylvania; Santa Fe Springs, California; Batavia, New York; Uithoorn, The Netherlands; Riode Janiero, Brazil; and Qingpu, China that are devoted primarily to applied research and development.

Research and development costs are expensed as incurred. Research and development expenses during2013, 2012 and 2011 were $21.6 million, $20.0 million and $18.8 million, respectively.

Most of Quaker’s subsidiaries and associated companies also have laboratory facilities. Although not ascomplete as the Conshohocken, Santa Fe Springs, Batavia, Uithoorn, Rio de Janiero or Qingpu laboratories, thesefacilities are generally sufficient for the requirements of the customers being served. If problems are encounteredwhich cannot be resolved by local laboratories, such problems may be referred to the laboratory staff inConshohocken or Uithoorn.

Regulatory Matters

In order to facilitate compliance with applicable Federal, state, and local statutes and regulations relating tooccupational health and safety and protection of the environment, the Company has an ongoing program of siteassessment for the purpose of identifying capital expenditures or other actions that may be necessary to complywith such requirements. The program includes periodic inspections of each facility by Quaker and/or independentexperts, as well as ongoing inspections and training by on-site personnel. Such inspections address operationalmatters, record keeping, reporting requirements and capital improvements. Capital expenditures directed solelyor primarily to regulatory compliance amounted to approximately $0.6 million, $1.0 million and $1.0 million in2013, 2012 and 2011, respectively. In 2014, the Company expects to incur approximately $1.4 million for capitalexpenditures directed primarily to regulatory compliance.

Number of Employees

On December 31, 2013, Quaker’s consolidated companies had 1,783 full-time employees of whom 563were employed by the parent company and its U.S. subsidiaries and 1,220 were employed by its non-U.S.subsidiaries. Associated companies of Quaker (in which it owns less than 50% and has significant influence)employed 74 people on December 31, 2013.

Company Segmentation

The Company’s reportable operating segments evidence the structure of the Company’s internalorganization, the method by which the Company’s resources are allocated and the manner by which theCompany assesses its performance. During 2013, certain internal shifts in the Company’s management andchanges to the structure of internally reported information occurred. The Company currently believes itsstructure, its resource allocation and its performance assessment are now more closely aligned with its fourgeographical regions: North America, EMEA, Asia/Pacific and South America. Therefore, the Company changedits reportable operating segments from those categorized by product nature to those organized by geography andrecast all prior period information to reflect the four regions as the Company’s new reportable operatingsegments. See Note 3 of Notes to Consolidated Financial Statements included in Item 8 of this Report.

Non-U.S. Activities

Since significant revenues and earnings are generated by non-U.S. operations, Quaker’s financial results areaffected by currency fluctuations, particularly between the U.S. Dollar and the E.U. Euro, the Brazilian Real, theChinese Renminbi and the Indian Rupee, and the impact of those currency fluctuations on the underlying

3

economies. Incorporated by reference is (i) the foreign exchange risk information contained in Item 7A of thisReport, (ii) the geographic information in Note 3 of Notes to Consolidated Financial Statements included inItem 8 of this Report and (iii) information regarding risks attendant to foreign operations included in Item 1A ofthis Report.

Quaker on the Internet

Financial results, news and other information about Quaker can be accessed from the Company’s Web siteat http://www.quakerchem.com. This site includes important information on the Company’s locations, productsand services, financial reports, news releases and career opportunities. The Company’s periodic and currentreports on Forms 10-K, 10-Q and 8-K, including exhibits and supplemental schedules filed therewith, andamendments to those reports, filed with the Securities and Exchange Commission (“SEC”) are available on theCompany’s Web site, free of charge, as soon as reasonably practicable after they are electronically filed with orfurnished to the SEC. Information contained on, or that may be accessed through, the Company’s Web site is notincorporated by reference in this Report and, accordingly, you should not consider that information part of thisReport.

Factors that May Affect Our Future Results

(Cautionary Statements under the Private Securities Litigation Reform Act of 1995)

Certain information included in this Report and other materials filed or to be filed by Quaker with the SEC(as well as information included in oral statements or other written statements made or to be made by us) containor may contain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, asamended, and Section 21E of the Securities Exchange Act of 1934, as amended. These statements can beidentified by the fact that they do not relate strictly to historical or current facts. We have based these forward-looking statements on our current expectations about future events. These forward-looking statements includestatements with respect to our beliefs, plans, objectives, goals, expectations, anticipations, intentions, financialcondition, results of operations, future performance, and business, including:

• statements relating to our business strategy;

• our current and future results and plans; and

• statements that include the words “may,” “could,” “should,” “would,” “believe,” “expect,”“anticipate,” “estimate,” “intend,” “plan” or similar expressions.

Such statements include information relating to current and future business activities, operational matters,capital spending, and financing sources. From time to time, oral or written forward-looking statements are alsoincluded in Quaker’s periodic reports on Forms 10-K, 10-Q and 8-K, press releases, and other materials releasedto, or statements made to, the public.

Any or all of the forward-looking statements in this Report, in Quaker’s Annual Report to Shareholders for2013, and in any other public statements we make may turn out to be wrong. This can occur as a result ofinaccurate assumptions or as a consequence of known or unknown risks and uncertainties. Many factors will beimportant in determining our future performance. Consequently, actual results may differ materially from thosethat might be anticipated from our forward-looking statements.

We undertake no obligation to publicly update any forward-looking statements, whether as a result of newinformation, future events or otherwise. However, any further disclosures made on related subjects in Quaker’ssubsequent reports on Forms 10-K, 10-Q and 8-K should be consulted. These forward-looking statements aresubject to risks, uncertainties and assumptions about us and our operations that are subject to change based onvarious important factors, some of which are beyond our control. A major risk is that the demand for the

4

Company’s products and services is largely derived from the demand for its customers’ products, which subjectsthe Company to uncertainties related to downturns in a customer’s business and unanticipated customerproduction shutdowns. Other major risks and uncertainties include, but are not limited to, significant increases inraw material costs, worldwide economic and political conditions, foreign currency fluctuations, terrorist attacksand other acts of violence, each of which is discussed in greater detail in Item 1A of this Report. Furthermore, theCompany is subject to the same business cycles as those experienced by steel, automobile, aircraft, appliance,and durable goods manufacturers. These risks, uncertainties, and possible inaccurate assumptions relevant to ourbusiness could cause our actual results to differ materially from expected and historical results. Other factorsbeyond those discussed in this Report could also adversely affect us. Therefore, we caution you not to placeundue reliance on our forward-looking statements. This discussion is provided as permitted by the PrivateSecurities Litigation Reform Act of 1995.

Item 1A. Risk Factors.

Changes to the industries and markets that Quaker serves could have a material adverse effect on theCompany’s liquidity, financial position and results of operations.

The chemical specialty industry comprises a number of companies of similar size as well as companieslarger and smaller than Quaker. It is estimated that Quaker holds a leading and significant global position in themarkets for process fluids to produce sheet steel and significant global positions in portions of the automotiveand industrial markets. The industry is highly competitive, and a number of companies with significant financialresources and/or customer relationships compete with us to provide similar products and services. Ourcompetitors may be positioned to offer more favorable pricing and service terms, resulting in reducedprofitability and a loss of market share for us. In addition, several competitors could potentially consolidate theirbusinesses to gain scale to better position their product offerings, which could have a negative impact to ourprofitability and market share. Historically, competition in the industry has been based primarily on the ability toprovide products that meet the needs of the customer and render technical services and laboratory assistance tothe customer and, to a lesser extent, on price. Factors critical to the Company’s business include successfullydifferentiating the Company’s offering from its competition, operating efficiently and profitably as a globallyintegrated whole, and increasing market share and customer penetration through internally developed businessprograms and strategic acquisitions.

The business environment in which the Company operates remains uncertain. The Company is subject to thesame business cycles as those experienced by steel, automobile, aircraft, appliance, and durable goodsmanufacturers. A major risk is that the Company’s demand is largely derived from the demand for its customers’products, which subjects the Company to uncertainties related to downturns in our customers’ business andunanticipated customer production shutdowns or curtailments. The Company has limited ability to adjust its costlevel contemporaneously with changes in sales and gross margins. Thus, a significant downturn in sales or grossmargins due to weak end-user markets, loss of a significant customer, and/or rising raw material costs could havea material adverse effect on the Company’s liquidity, financial position, and results of operations.

Our business depends on attracting and retaining qualified management personnel.

The unanticipated departure of any key member of our management team could have an adverse effect onour business. Given the relative size of the Company and the breadth of its global operations, there are a limitednumber of qualified management personnel to assume the responsibilities of management level employeesshould there be management turnover. In addition, because of the specialized and technical nature of ourbusiness, our future performance is dependent on the continued service of, and our ability to attract and retain,qualified management, commercial and technical personnel. Competition for such personnel is intense, and wemay be unable to continue to attract or retain such personnel. In an effort to mitigate such risks, the Companyutilizes retention bonuses, offers competitive pay and maintains continued succession planning, but there can beno assurance that these mitigating factors will be adequate to attract or retain qualified management personnel.

5

Inability to obtain sufficient price increases or contract concessions to offset increases in the costs of rawmaterial could have a material adverse effect on the Company’s liquidity, financial position and results ofoperations. Price increases implemented could result in the loss of sales.

Quaker uses over 1,000 raw materials, including mineral oils and derivatives, animal fats and derivatives,vegetable oils and derivatives, ethylene derivatives, solvents, surface active agents, chlorinated paraffiniccompounds, and a wide variety of other organic and inorganic compounds. In 2013, three raw material groups(mineral oils and derivatives, animal fats and derivatives, and vegetable oils and derivatives) each accounted forat least 10% of the total cost of Quaker’s raw material purchases. The price of mineral oil can be affected by theprice of crude oil and its refining capacity. In addition, many of the raw materials used by Quaker are“commodity” chemicals. Accordingly, Quaker’s earnings can be affected by market changes in raw materialprices.

In the past, Quaker experienced significant volatility in its raw material costs, particularly crude oilderivatives. In addition, refining capacity can be constrained by various factors, which can further contribute tovolatile raw material costs and negatively impact margins. Animal fat and vegetable oil prices also can beimpacted by increased biodiesel consumption. Although the Company has been successful in the past inrecovering a substantial amount of the raw material cost increases while retaining customers, there can be noassurance that the Company can continue to recover raw material costs or retain customers in the future. As aresult of the Company’s past pricing actions, customers may become more likely to consider competitors’products, some of which may be available at a lower cost. A significant loss of customers could result in amaterial adverse effect on the Company’s results of operations.

Availability of raw materials, including sourcing from some single suppliers and some suppliers in volatileeconomic environments, could have a material adverse effect on the Company’s liquidity, financial positionand results of operations.

The chemical specialty industry can experience some tightness of supply for certain raw materials. Inaddition, in some cases, we choose to source from a single supplier and/or suppliers in economies that haveexperienced instability. Any significant disruption in supply could affect our ability to obtain raw materials,which could have a material adverse effect on our liquidity, financial position and results of operations. Inaddition, the Company’s raw materials are subject to various regulatory laws, and a change in the ability tolegally use such raw materials may impact Quaker’s liquidity, financial position and results of operations.

Loss of a significant manufacturing facility may materially and adversely affect the Company’s liquidity,financial position and results of operations.

Quaker has multiple manufacturing facilities throughout the world. In certain countries such as Brazil andChina, there is only one such facility. If one of the Company’s facilities was damaged to such extent thatproduction was halted for an extended period, the Company may not be able to timely supply affected customers.This could result in a loss of sales over an extended period or permanently. The Company does take steps tomitigate against this risk, including contingency planning and procuring property and casualty insurance(including business interruption insurance). Nevertheless, the loss of sales in any one region over any extendedperiod of time could have a significant material adverse effect on Quaker’s liquidity, financial position andresults of operations.

Bankruptcy of a significant customer could have a material adverse effect on our liquidity, financial positionand results of operations.

A significant portion of Quaker’s revenues is derived from sales to customers in the steel and automotiveindustries; including some of our larger customers, where a number of bankruptcies have occurred in the past andcompanies have experienced financial difficulties. As part of the bankruptcy process, the Company’s pre-petitionreceivables may not be realized, customer manufacturing sites may be closed or contracts voided. The

6

bankruptcy of a major customer could have a material adverse effect on the Company’s liquidity, financialposition, and results of operations. Steel customers typically have limited manufacturing locations as comparedto metalworking customers and generally use higher volumes of products at a single location. The loss or closureof a steel mill or other major site of a significant customer could have a material adverse effect on Quaker’sbusiness.

During 2013, our five largest customers (each composed of multiple subsidiaries or divisions with semi-autonomous purchasing authority) together accounted for approximately 18% of our consolidated net sales, withthe largest customer (Arcelor-Mittal Group) accounting for approximately 9% of our consolidated net sales.

Failure to comply with any material provision of our credit facility or other debt agreements could have amaterial adverse effect on our liquidity, financial position and results of operations.

The Company maintains a $300.0 million unsecured credit facility (the “Credit Facility”) with a group oflenders, which can be increased to $400.0 million at the Company’s option if lenders agree to increase theircommitments and the Company satisfies certain conditions. The Credit Facility, which matures in 2018, providesthe availability of revolving credit borrowings. In general, the borrowings under the Credit Facility bear interestat either a base rate or LIBOR rate plus a margin based on the Company’s consolidated leverage ratio.

The Credit Facility contains certain limitations on investments, acquisitions and liens, as well as defaultprovisions customary for facilities of its type. While these covenants and restrictions are not currently consideredto be overly restrictive, they could become more difficult to comply with as our business or financial conditionschange. In addition, deterioration in the Company’s results of operations or financial position could significantlyincrease borrowing costs.

Quaker is exposed to market rate risk for changes in interest rates, due to the variable interest rate applied tothe Company’s borrowings under its Credit Facility. Accordingly, if interest rates rise significantly, the cost ofdebt to Quaker will increase, perhaps significantly, depending on the extent of Quaker’s borrowings under theCredit Facility. At December 31, 2013, the Company had no outstanding borrowings under the Credit Facility.

Environmental laws and regulations and pending legal proceedings may materially and adversely affect theCompany’s liquidity, financial position and results of operations.

The Company is a party to proceedings, cases, and requests for information from, and negotiations with,various claimants and Federal and state agencies relating to various matters, including environmental matters. Anadverse result in one or more matters or any potential future matter of a similar nature could materially andadversely affect the Company’s liquidity, financial position and results of operations. Incorporated herein byreference is the information concerning pending asbestos-related litigation against an inactive subsidiary andamounts accrued associated with certain environmental non-capital remediation costs in Note 22 of Notes toConsolidated Financial Statements which appears in Item 8 of this Report.

Compliance with a complex global regulatory environment could have an impact on the Company’s publicperception and/or a material adverse effect on the Company’s liquidity, financial position and results ofoperations.

Changes in the Company’s regulatory environment, particularly, but not limited to, the United States,Brazil, China and the European Union, could lead to heightened regulatory scrutiny, could adversely impact ourability to continue selling certain products in our domestic or foreign markets and could increase the cost ofdoing business. For instance, the European Union’s Registration, Authorization and Restriction of Chemicals(“REACH” and analogous non-E.U. laws and regulations), or other similar laws and regulations, could result infines, ongoing monitoring and other future business activity restrictions, which could have a material adverseeffect on the Company’s liquidity, financial position and results of operations. In addition, non-compliance with

7

the U.S. Foreign Corrupt Practices Act (“FCPA”), the UK Bribery Act and other similar laws and regulations,could result in a negative impact to the Company’s reputation, potential fines or ongoing monitoring, whichcould also have an adverse effect on the Company.

Climate change and greenhouse gas restrictions may materially affect the Company’s liquidity, financialposition and results of operations.