32

Analyst briefing 2Q15 performance results 13 th August 2015

| Date post: | 23-Apr-2019 |

| Category: |

Documents |

| Upload: | nguyentruc |

| View: | 219 times |

| Download: | 0 times |

Analyst briefing2Q15 performance results

13th August 2015

2

DISCLAIMER

The views expressed here contain information derived from publicly available sources that have not been independently verified. No representationor warranty is made as to the accuracy, completeness or reliability of the information. Any forward looking information in this presentation has beenprepared on the basis of a number of assumptions which may prove to be incorrect. This presentation should not be relied upon as a recommendationor forecast by PT. Indo Tambangraya Megah Tbk. Nothing in this release should be construed as either an offer to buy or sell or a solicitation of anoffer to buy or sell shares in any jurisdiction

3

Financial reviewCommercial reviewOperational reviewIntroduction

4321

4

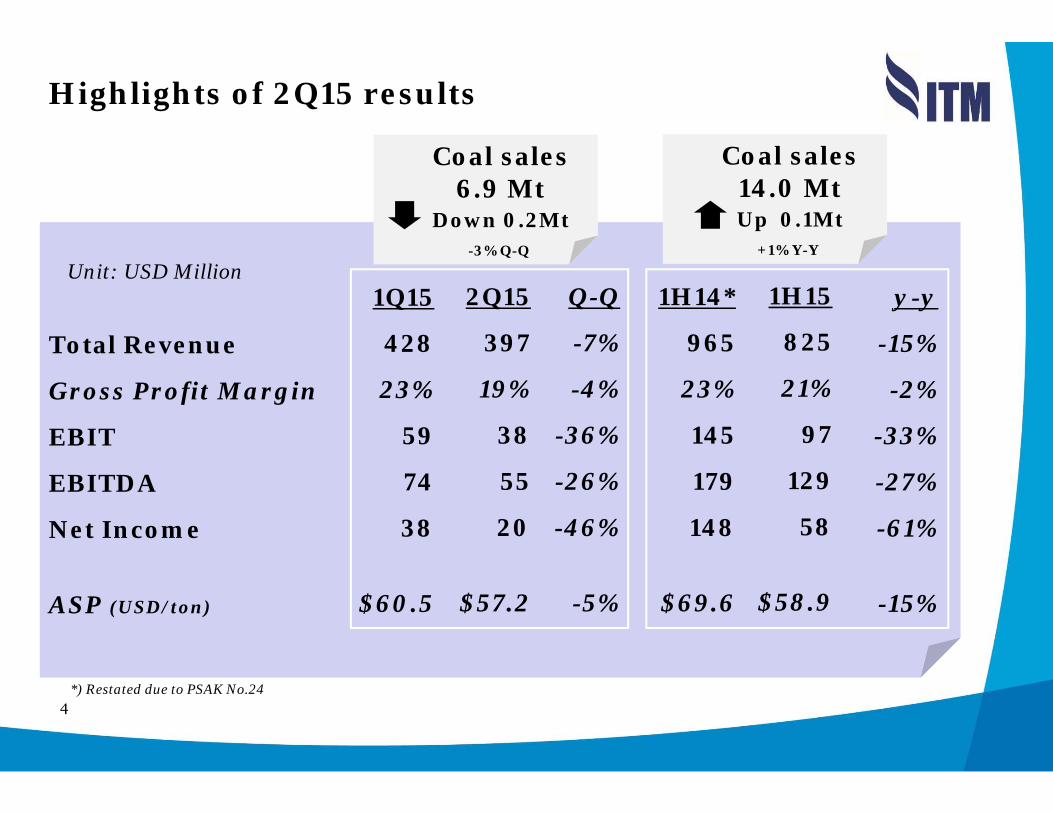

Highlights of 2Q15 results

Unit: USD Million

Total Revenue

Gross Profit Margin

EBIT

EBITDA

Net Income

ASP (USD/ton)

1Q15

428

23%

59

74

38

$60.5

y-y

-15%

-2%

-33%

-27%

-61%

-15%

2Q15

397

19%

38

55

20

$57.2

Q-Q

-7%

-4%

-36%

-26%

-46%

-5%

1H14*

965

23%

145

179

148

$69.6

Coal sales6.9 Mt

Down 0.2Mt -3% Q-Q

Coal sales14.0 MtUp 0.1Mt

+1% Y-Y

1H15

825

21%

97

129

58

$58.9

*) Restated due to PSAK No.24

5

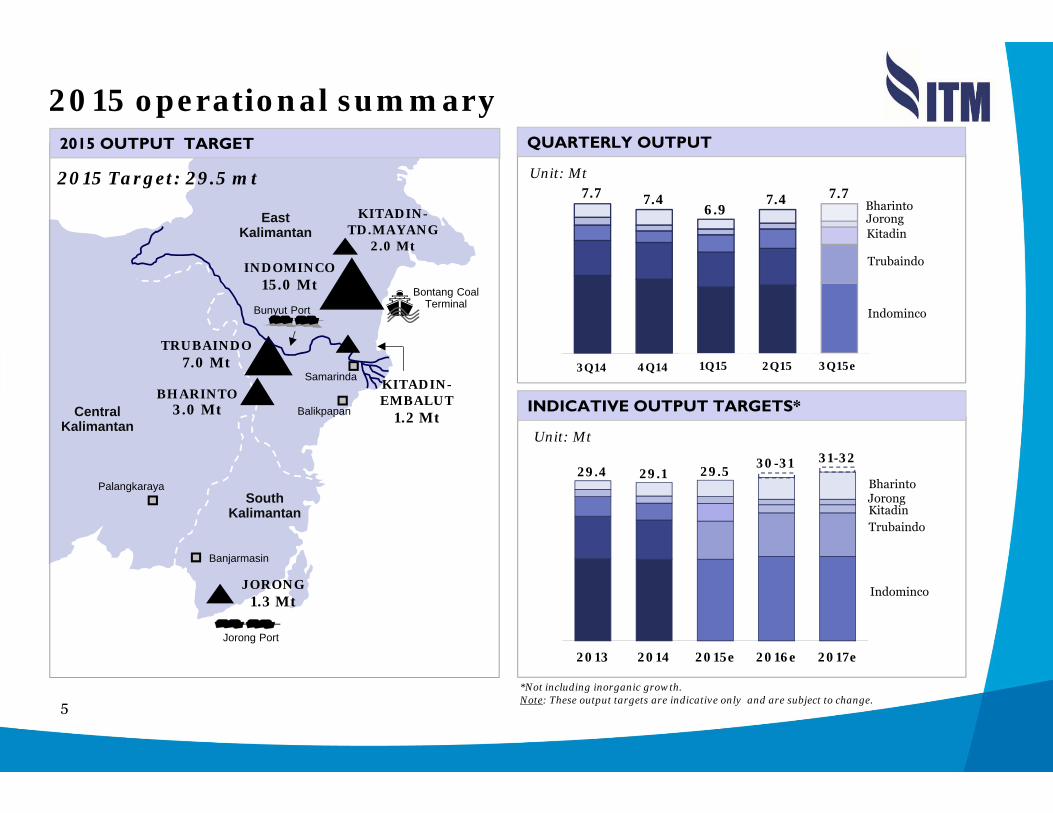

2015 operational summary

East Kalimantan

Bunyut Port

Balikpapan

Palangkaraya

Banjarmasin

Central Kalimantan

South Kalimantan

KITADIN-EMBALUT

1.2 Mt

INDOMINCO 15.0 Mt

TRUBAINDO 7.0 Mt

BHARINTO3.0 Mt

JORONG 1.3 Mt

Samarinda

Jorong Port

Bontang Coal Terminal

2015 Target: 29.5 mt

2015 OUTPUT TARGET

KITADIN-TD.MAYANG

2.0 Mt

2013 2014 2015e 2016e 2017e

3Q14 4Q14 1Q15 2Q15 3Q15e

Unit: Mt

Indominco

Trubaindo

Bharinto

KitadinJorong

INDICATIVE OUTPUT TARGETS*

*Not including inorganic growth.Note: These output targets are indicative only and are subject to change.

QUARTERLY OUTPUT

3Q14

Unit: Mt

TrubaindoKitadinJorongBharinto

Indominco

31-3229.4 29.1 29.5

4Q14

7.7

1Q15

30-31

2Q15

7.46.9

7.4

3Q15e

7.7

6

Financial reviewCommercial reviewOperational reviewIntroduction

4321

7

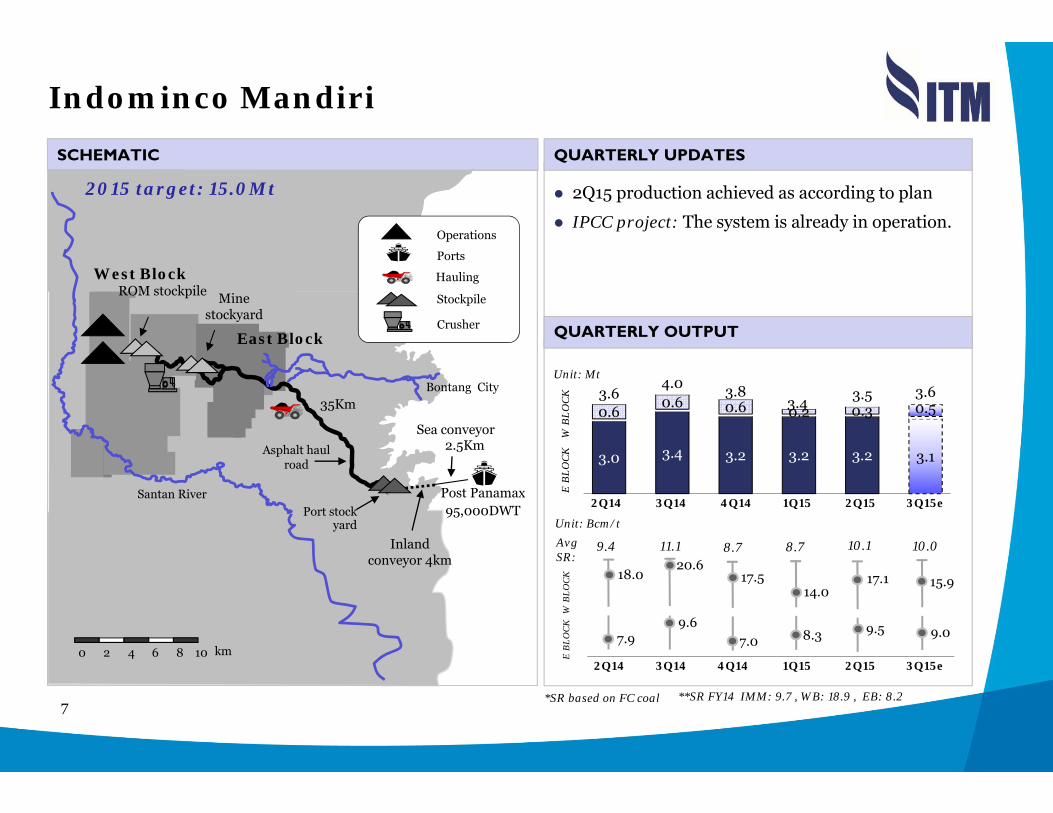

Indominco Mandiri

2Q15 production achieved as according to plan

IPCC project: The system is already in operation.

QUARTERLY UPDATESSCHEMATIC

East Block

Santan RiverPort stock

yard

Bontang City

Asphalt haul road

2.5Km

35Km

Sea conveyor

Mine stockyard

Inland conveyor 4km

0 106 82 km4

West Block

Operations

Stockpile

Ports

Hauling

Crusher

ROM stockpile

Post Panamax95,000DWT

2015 target: 15.0Mt

E B

LOC

KW

BLO

CK

E B

LOC

KW

BLO

CK

Unit: Mt

Unit: Bcm/t

QUARTERLY OUTPUT

AvgSR:

17.5

7.0

8.7

17.1

9.5

10.1

15.9

9.0

10.0

2Q14 3Q14 4Q14 1Q15 2Q15 3Q15e

18.0

7.9

9.4

**SR FY14 IMM: 9.7 , WB: 18.9 , EB: 8.2

20.6

9.6

11.1

3.0 3.4 3.2 3.2 3.2 3.1

0.60.6 0.6 0.2 0.3 0.5

3.64.0 3.8

3.4 3.5 3.6

2Q14 3Q14 4Q14 1Q15 2Q15 3Q15e

14.0

8.3

8.7

*SR based on FC coal

8

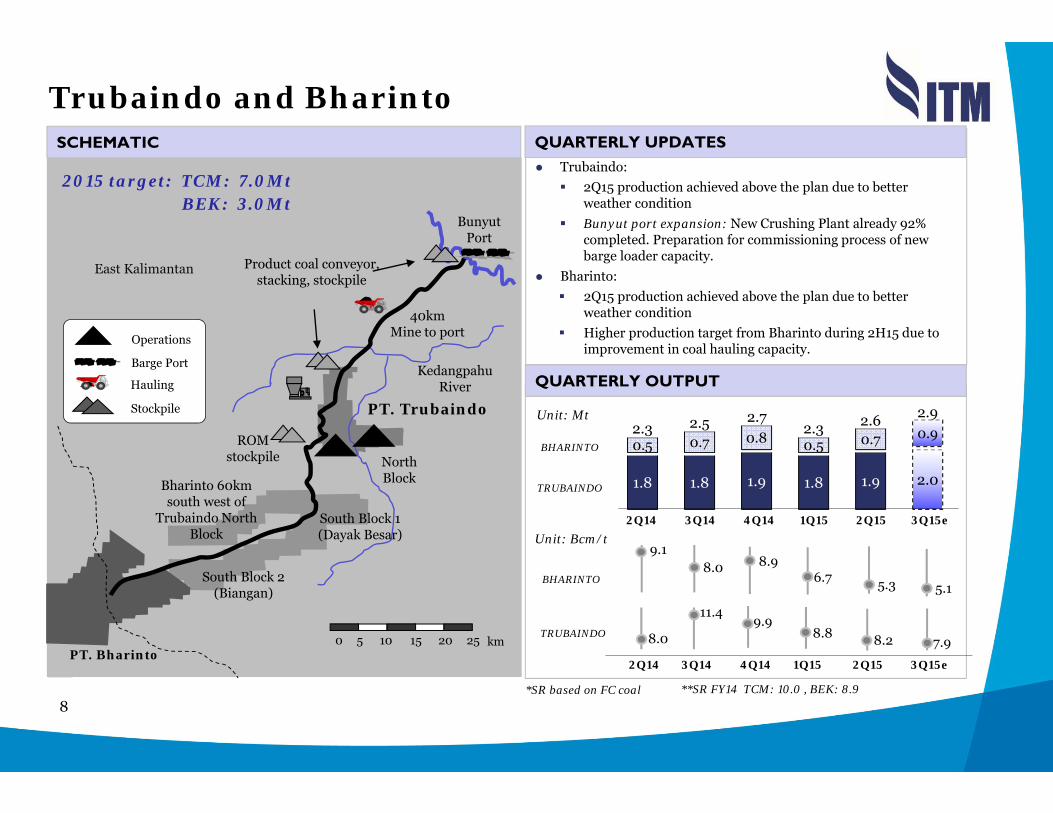

Trubaindo and Bharinto

Trubaindo: 2Q15 production achieved above the plan due to better weather condition Bunyut port expansion: New Crushing Plant already 92% completed. Preparation for commissioning process of new barge loader capacity.

Bharinto: 2Q15 production achieved above the plan due to better weather conditionHigher production target from Bharinto during 2H15 due to improvement in coal hauling capacity.

QUARTERLY UPDATESSCHEMATIC

Mahakam River

South Block 1(Dayak Besar)

North Block

40kmMine to port

KedangpahuRiver

ROM stockpile

BunyutPort

0 10 2515 205 km

Product coal conveyor, stacking, stockpile

East Kalimantan

Bharinto 60km south west of

Trubaindo North Block

South Block 2(Biangan)

PT. Bharinto

PT. Trubaindo

Operations

Stockpile

Hauling

Barge Port

2015 target: TCM: 7.0Mt BEK: 3.0Mt

TRUBAINDO

TRUBAINDO

BHARINTO

Unit: Mt

Unit: Bcm/t

BHARINTO

QUARTERLY OUTPUT

1.8 1.8 1.9 1.8 1.9 2.0

0.5 0.7 0.8 0.5 0.7 0.92.3 2.5 2.72.3 2.6 2.9

9.9

8.9

8.2

5.3

7.9

5.1

8.0

9.1

2Q14 3Q14 4Q14 1Q15 2Q15 3Q15e

**SR FY14 TCM: 10.0 , BEK: 8.9

11.4

8.0

2Q14 3Q14 4Q14 1Q15 2Q15 3Q15e

8.8

6.7

*SR based on FC coal

9

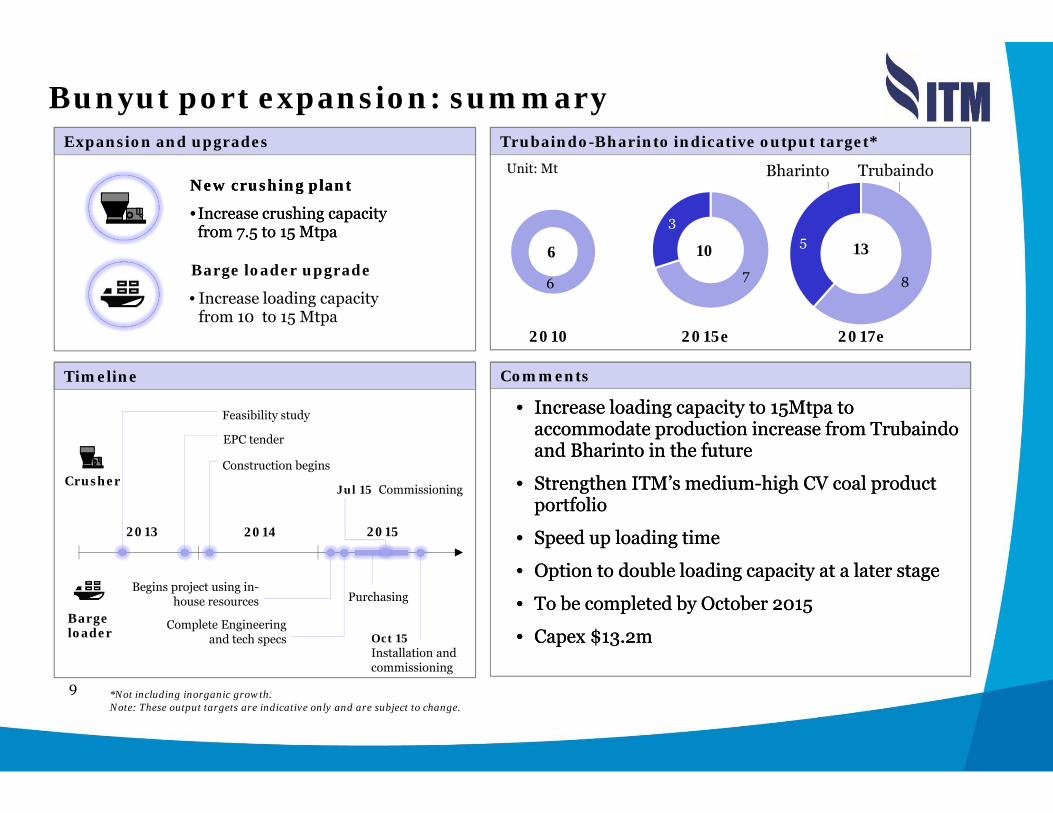

Bunyut port expansion: summaryExpansion and upgrades

New crushing plant

• Increase crushing capacity from 7.5 to 15 Mtpa

New crushing plant

• Increase crushing capacity from 7.5 to 15 Mtpa

Barge loader upgrade

• Increase loading capacity from 10 to 15 Mtpa

Comments

• Increase loading capacity to 15Mtpa to accommodate production increase from Trubaindoand Bharinto in the future

• Strengthen ITM’s medium-high CV coal product portfolio

• Speed up loading time

• Option to double loading capacity at a later stage

• To be completed by October 2015

• Capex $13.2m

• Increase loading capacity to 15Mtpa to accommodate production increase from Trubaindoand Bharinto in the future

• Strengthen ITM’s medium-high CV coal product portfolio

• Speed up loading time

• Option to double loading capacity at a later stage

• To be completed by October 2015

• Capex $13.2m

*Not including inorganic growth.Note: These output targets are indicative only and are subject to change.

Trubaindo-Bharinto indicative output target*Unit: Mt

6 7

3

8

5

Bharinto Trubaindo

2010 2015e 2017e

6 10 13

Timeline

Barge loader

Crusher

Feasibility study

2013

EPC tender

Construction begins

2015

Complete Engineering and tech specs

Purchasing

Oct 15Installation and commissioning

2014

Begins project using in-house resources

Jul 15 Commissioning

10

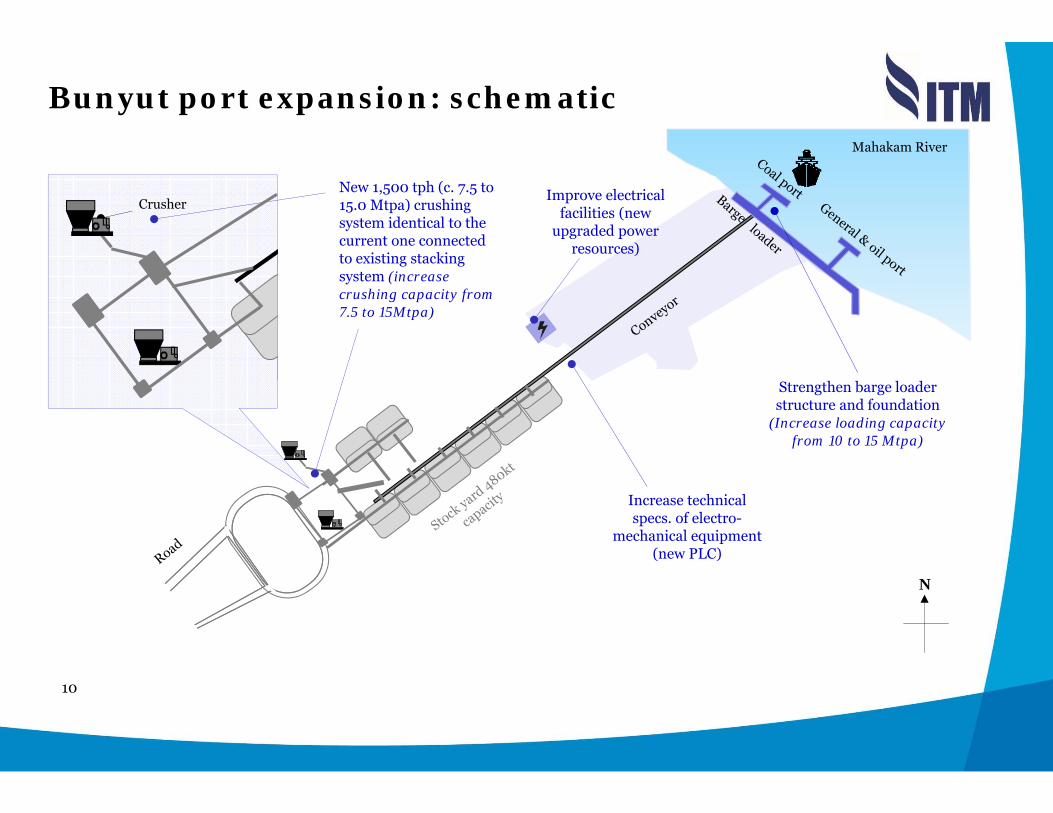

Bunyut port expansion: schematicMahakam River

New 1,500 tph (c. 7.5 to 15.0 Mtpa) crushing system identical to the current one connected to existing stacking system (increase crushing capacity from 7.5 to 15Mtpa)

Improve electrical facilities (new

upgraded power resources)

Increase technical specs. of electro-

mechanical equipment (new PLC)

N

Strengthen barge loader structure and foundation

(Increase loading capacity from 10 to 15 Mtpa)

Crusher

11

Bunyut port expansion: images

New CPP

New feed conveyor New CPP synchronize with existing TCM stacker

Frame and cable strengthening

New upgraded power resources 2x1029 kVA

New PLC and synchronize with existing

12

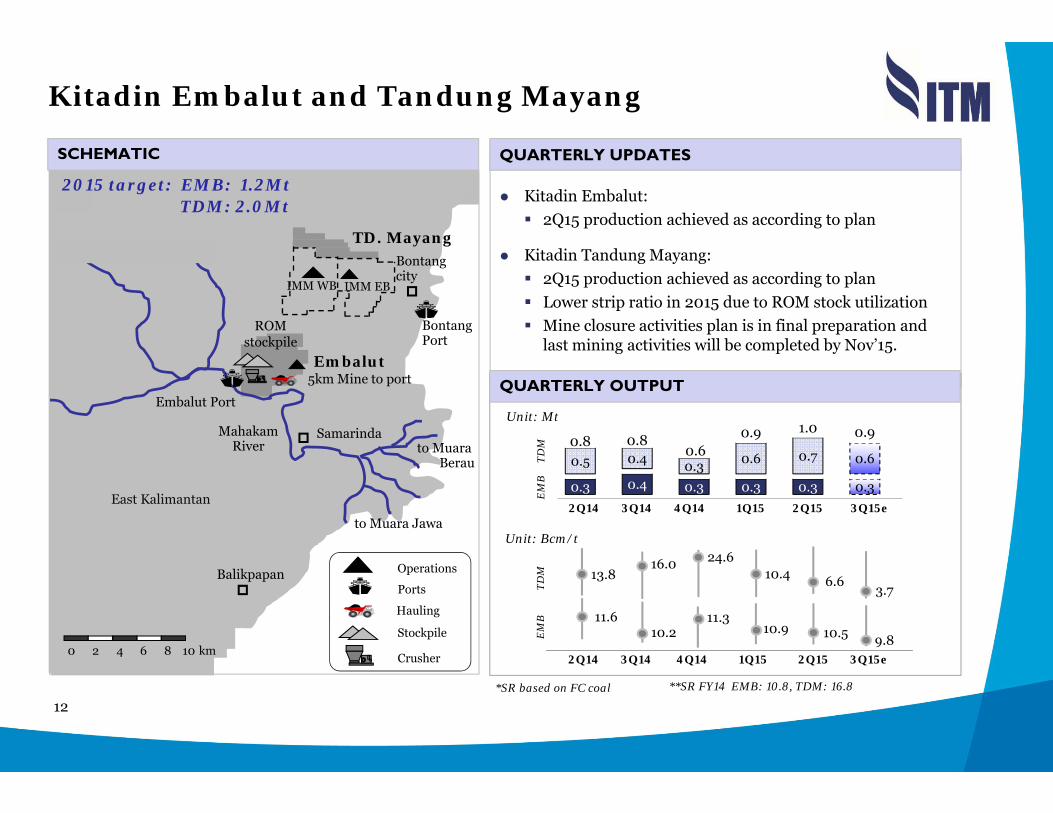

Kitadin Embalut and Tandung Mayang

Kitadin Embalut: 2Q15 production achieved as according to plan

Kitadin Tandung Mayang:2Q15 production achieved as according to planLower strip ratio in 2015 due to ROM stock utilizationMine closure activities plan is in final preparation and last mining activities will be completed by Nov’15.

QUARTERLY UPDATES

QUARTERLY OUTPUT

Balikpapan

MahakamRiver

Samarindato Muara

Berau

Bontangcity

Embalut

Embalut Port

to Muara Jawa

ROM stockpile

Operations

Stockpile

Ports

Hauling

Crusher0 106 82 km4

5km Mine to port

TD. Mayang

East Kalimantan

IMM EBIMM WB

BontangPort

TDM: 2.0Mt

TDM

EM

B

Unit: Mt

Unit: Bcm/t

2015 target: EMB: 1.2Mt

**SR FY14 EMB: 10.8, TDM: 16.8

2Q14 3Q14 4Q14 1Q15 2Q15 3Q15e

SCHEMATIC

EM

BTD

M

11.3

24.6

10.5

6.6

9.8

3.7

11.6

13.8

2Q14 3Q14 4Q14 1Q15 2Q15 3Q15e

10.2

16.0

10.9

10.4

*SR based on FC coal

0.3 0.4 0.3 0.3 0.3 0.3

0.5 0.4 0.3 0.6 0.7 0.60.8 0.8

0.60.9 1.0 0.9

13

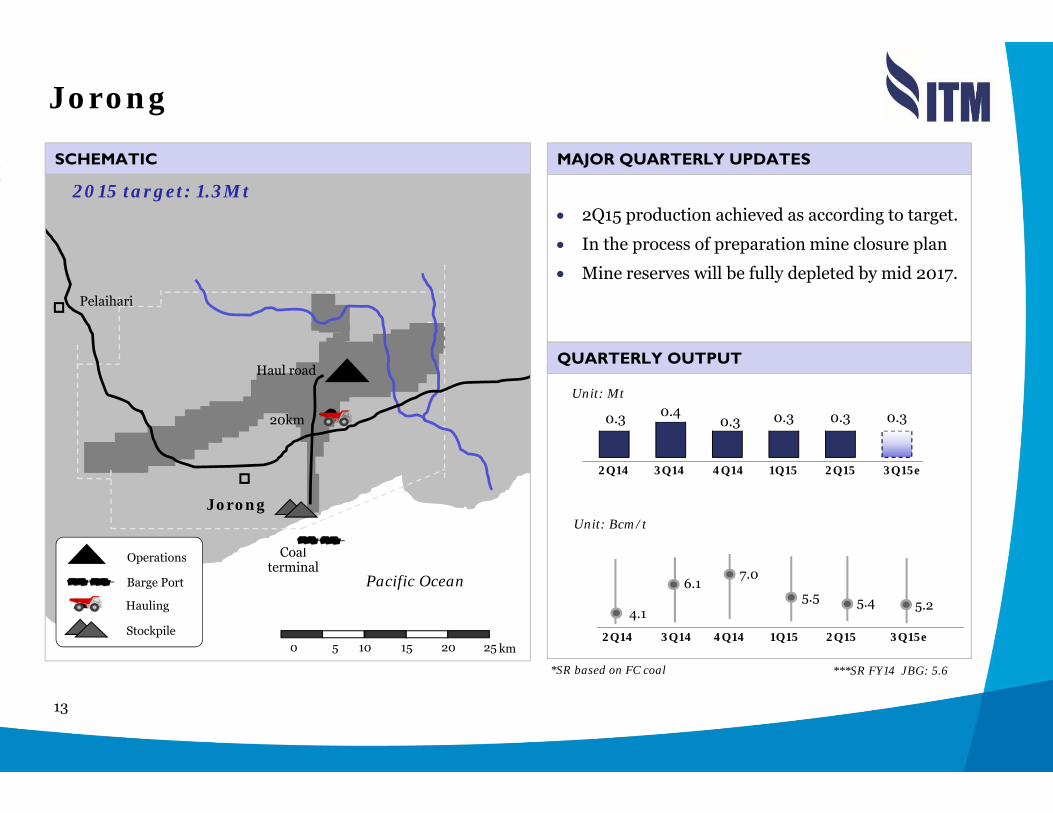

Jorong

Coal terminal

Jorong

Pelaihari

Pacific Ocean

Haul road

0 10 2515 205 km

20km

Operations

Stockpile

Hauling

Barge Port

2015 target: 1.3Mt • 2Q15 production achieved as according to target.

• In the process of preparation mine closure plan

• Mine reserves will be fully depleted by mid 2017.

SCHEMATIC

Unit: Mt

Unit: Bcm/t

0.3 0.40.3 0.3 0.3 0.3

2Q14 3Q14 4Q14 1Q15 2Q15 3Q15e

7.0

5.24.1

2Q14 3Q14 4Q14 1Q15 2Q15 3Q15e

***SR FY14 JBG: 5.6

6.15.5 5.4

*SR based on FC coal

MAJOR QUARTERLY UPDATES

QUARTERLY OUTPUT

14

Financial reviewCommercial reviewOperational reviewIntroduction

4321

15

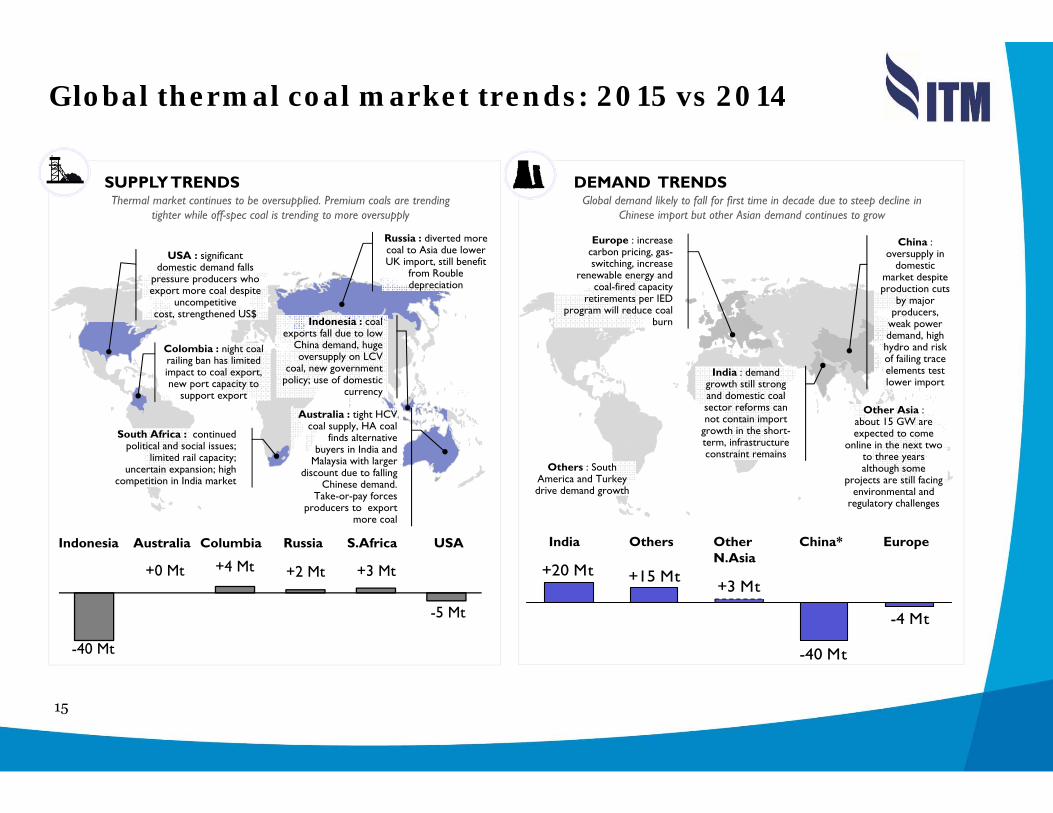

Global thermal coal market trends: 2015 vs 2014

SUPPLY TRENDS

-40 Mt

+0 Mt +4 Mt +2 Mt +3 Mt

-5 Mt

USA : significant domestic demand falls

pressure producers who export more coal despite

uncompetitivecost, strengthened US$

Russia : diverted more coal to Asia due lower UK import, still benefit

from Rouble depreciation

Indonesia : coal exports fall due to low

China demand, huge oversupply on LCV

coal, new government policy; use of domestic

currency

Australia : tight HCV coal supply, HA coal

finds alternative buyers in India and

Malaysia with larger discount due to falling

Chinese demand. Take-or-pay forces

producers to export more coal

Colombia : night coal railing ban has limited impact to coal export, new port capacity to

support export

South Africa : continuedpolitical and social issues;

limited rail capacity; uncertain expansion; high

competition in India market

Indonesia Australia RussiaColumbia S.Africa USA

Thermal market continues to be oversupplied. Premium coals are trending tighter while off-spec coal is trending to more oversupply

DEMAND TRENDS

India Others OtherN.Asia

EuropeChina*

Europe : increase carbon pricing, gas-switching, increase

renewable energy and coal-fired capacity

retirements per IED program will reduce coal

burn

China : oversupply in

domestic market despite production cuts

by major producers,

weak power demand, high hydro and risk of failing trace elements test lower import

India : demand growth still strong and domestic coal sector reforms can not contain import

growth in the short-term, infrastructure constraint remains

Others : South America and Turkey drive demand growth

Other Asia :about 15 GW are expected to come

online in the next two to three years although some

projects are still facing environmental and

regulatory challenges

Global demand likely to fall for first time in decade due to steep decline in Chinese import but other Asian demand continues to grow

-4 Mt

+3 Mt+15 Mt+20 Mt

-40 Mt

16

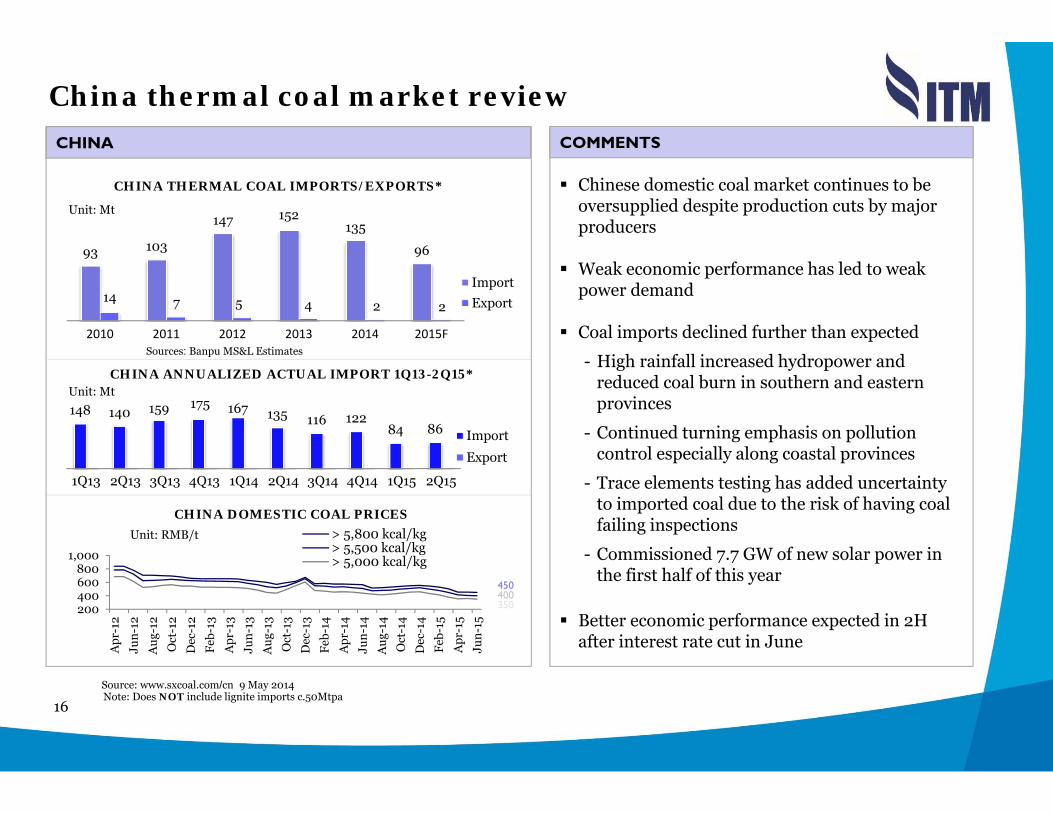

China thermal coal market review

Note: Does NOT include lignite imports c.50Mtpa

CHINA ANNUALIZED ACTUAL IMPORT 1Q13-2Q15*

CHINA THERMAL COAL IMPORTS/EXPORTS*

CHINA DOMESTIC COAL PRICES

93 103

147 135

96

14 7 5 4 2 2

2010 2011 2012 2013 2014 2015F

ImportExport

Sources: Banpu MS&L Estimates

Unit: Mt 152

148 140 159 167 135 116 12284 86

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15

Import

Export

Unit: Mt

200400600800

1,000

Apr

-12

Jun-

12

Aug

-12

Oct

-12

Dec

-12

Feb-

13

Apr

-13

Jun-

13

Aug

-13

Oct

-13

Dec

-13

Feb-

14

Apr

-14

Jun-

14

Aug

-14

Oct

-14

Dec

-14

Feb-

15

Apr

-15

Jun-

15

> 5,800 kcal/kg> 5,500 kcal/kg> 5,000 kcal/kg

Unit: RMB/t

400350

CHINA

175

450

Source: www.sxcoal.com/cn 9 May 2014

Chinese domestic coal market continues to be oversupplied despite production cuts by major producers

Weak economic performance has led to weak power demand

Coal imports declined further than expected

- High rainfall increased hydropower and reduced coal burn in southern and eastern provinces

- Continued turning emphasis on pollution control especially along coastal provinces

- Trace elements testing has added uncertainty to imported coal due to the risk of having coal failing inspections

- Commissioned 7.7 GW of new solar power in the first half of this year

Better economic performance expected in 2H after interest rate cut in June

COMMENTS

17

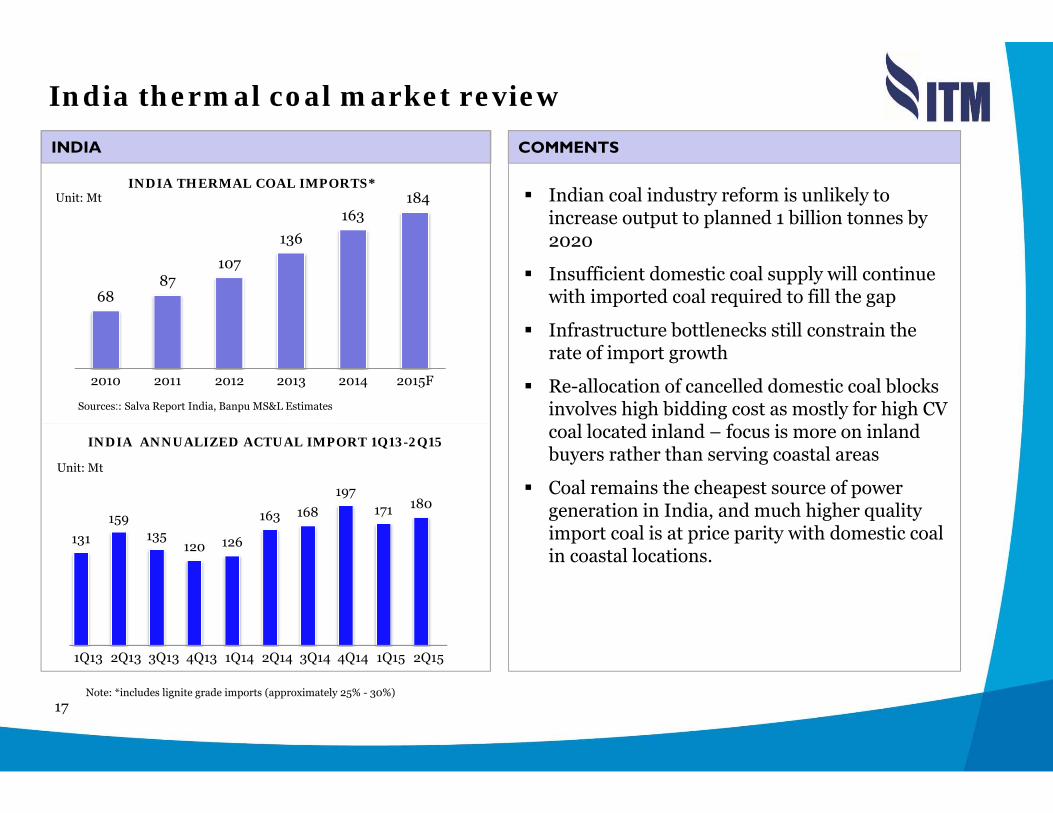

India thermal coal market review

INDIA THERMAL COAL IMPORTS*

INDIA ANNUALIZED ACTUAL IMPORT 1Q13-2Q15

Sources:: Salva Report India, Banpu MS&L Estimates

131159

135120 126

163 168197

171 180

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15

Unit: Mt

Unit: Mt

Indian coal industry reform is unlikely to increase output to planned 1 billion tonnes by 2020

Insufficient domestic coal supply will continue with imported coal required to fill the gap

Infrastructure bottlenecks still constrain the rate of import growth

Re-allocation of cancelled domestic coal blocks involves high bidding cost as mostly for high CV coal located inland – focus is more on inland buyers rather than serving coastal areas

Coal remains the cheapest source of power generation in India, and much higher quality import coal is at price parity with domestic coal in coastal locations.

INDIA

Note: *includes lignite grade imports (approximately 25% - 30%)

COMMENTS

6887

107

136163

2010 2011 2012 2013 2014 2015F

184

18

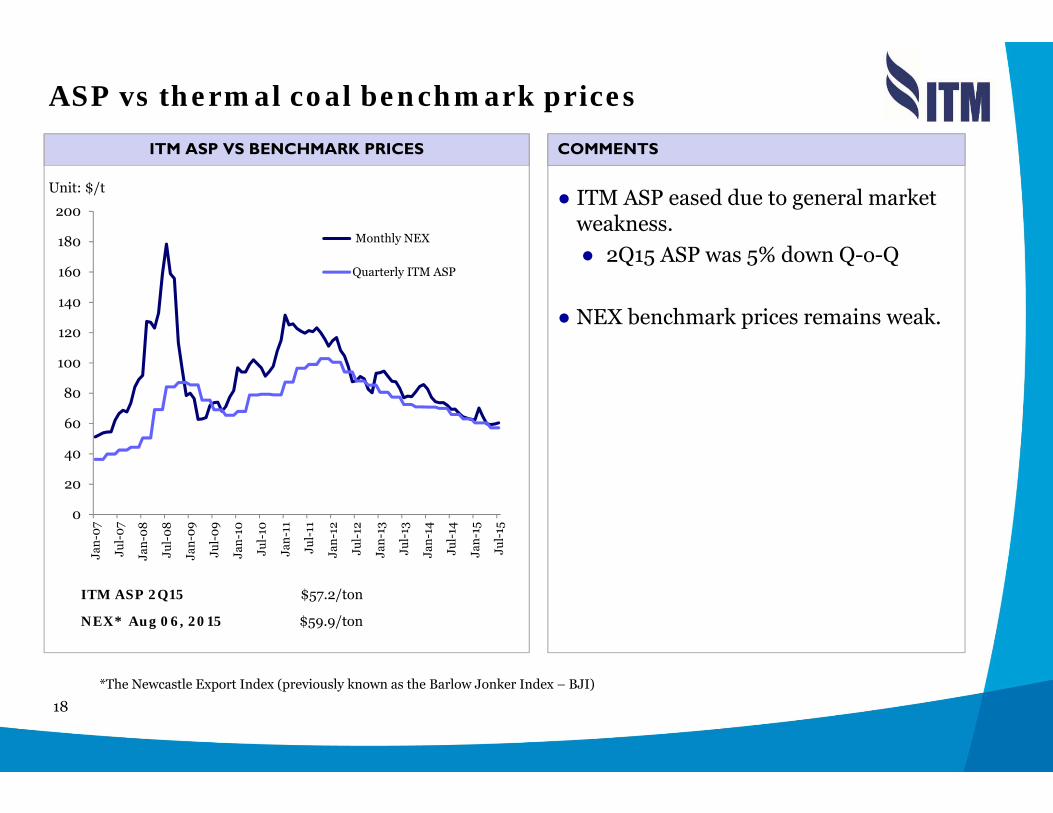

ASP vs thermal coal benchmark prices

● ITM ASP eased due to general market weakness.● 2Q15 ASP was 5% down Q-o-Q

● NEX benchmark prices remains weak.

ITM ASP VS BENCHMARK PRICES

*The Newcastle Export Index (previously known as the Barlow Jonker Index – BJI)

ITM ASP 2Q15 $57.2/ton

NEX* Aug 06, 2015 $59.9/ton

Unit: $/t

COMMENTS

0

20

40

60

80

100

120

140

160

180

200

Jan-

07

Jul-

07

Jan-

08

Jul-

08

Jan-

09

Jul-

09

Jan-

10

Jul-

10

Jan-

11

Jul-

11

Jan-

12

Jul-

12

Jan-

13

Jul-

13

Jan-

14

Jul-

14

Jan-

15

Jul-

15

Monthly NEX

Quarterly ITM ASP

19

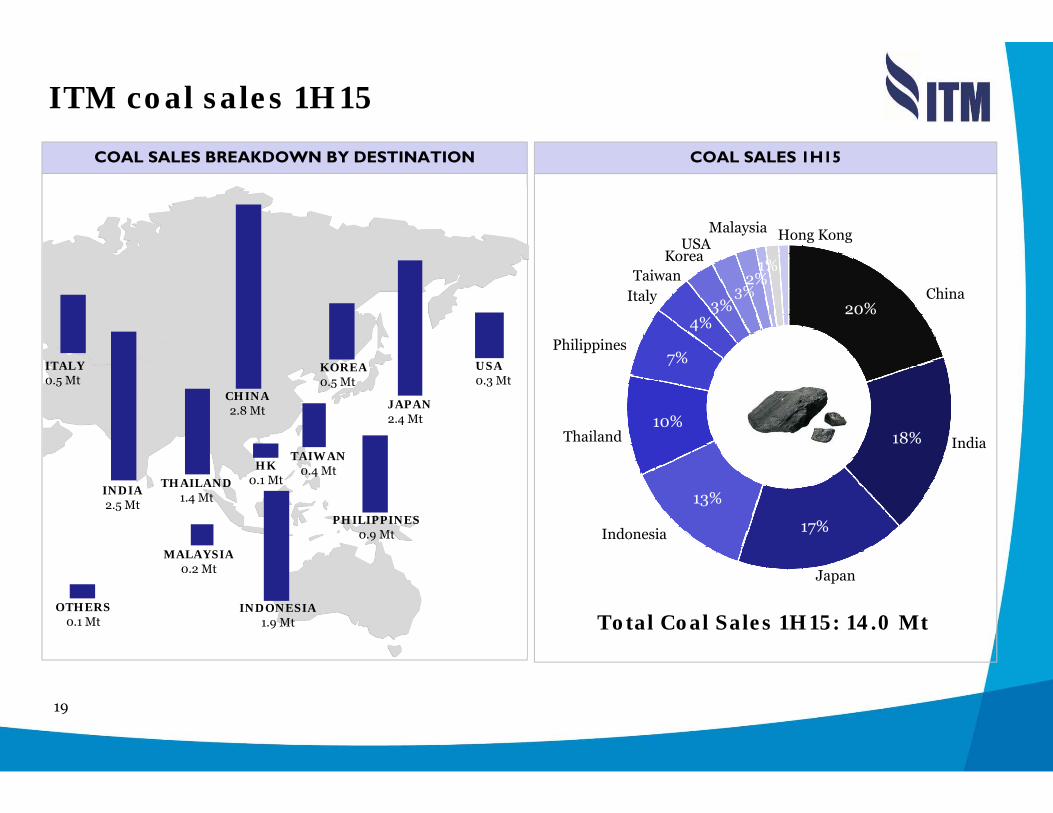

ITM coal sales 1H15

COAL SALES 1H15 COAL SALES BREAKDOWN BY DESTINATION

Total Coal Sales 1H15: 14.0 Mt

JAPAN2.4 Mt

PHILIPPINES 0.9 Mt

THAILAND1.4 MtINDIA

2.5 Mt

HK0.1 Mt

KOREA0.5 Mt

CHINA2.8 Mt

TAIWAN0.4 Mt

ITALY0.5 Mt

1.5

INDONESIA1.9 Mt

MALAYSIA0.2 Mt

OTHERS0.1 Mt

USA0.3 Mt

20%

18%

17%

13%

10%

7%

4%3%

3%2%

1%

Japan

ChinaTaiwan

Korea

Italy

Thailand

Philippines

Hong Kong

India

Indonesia

MalaysiaUSA

20

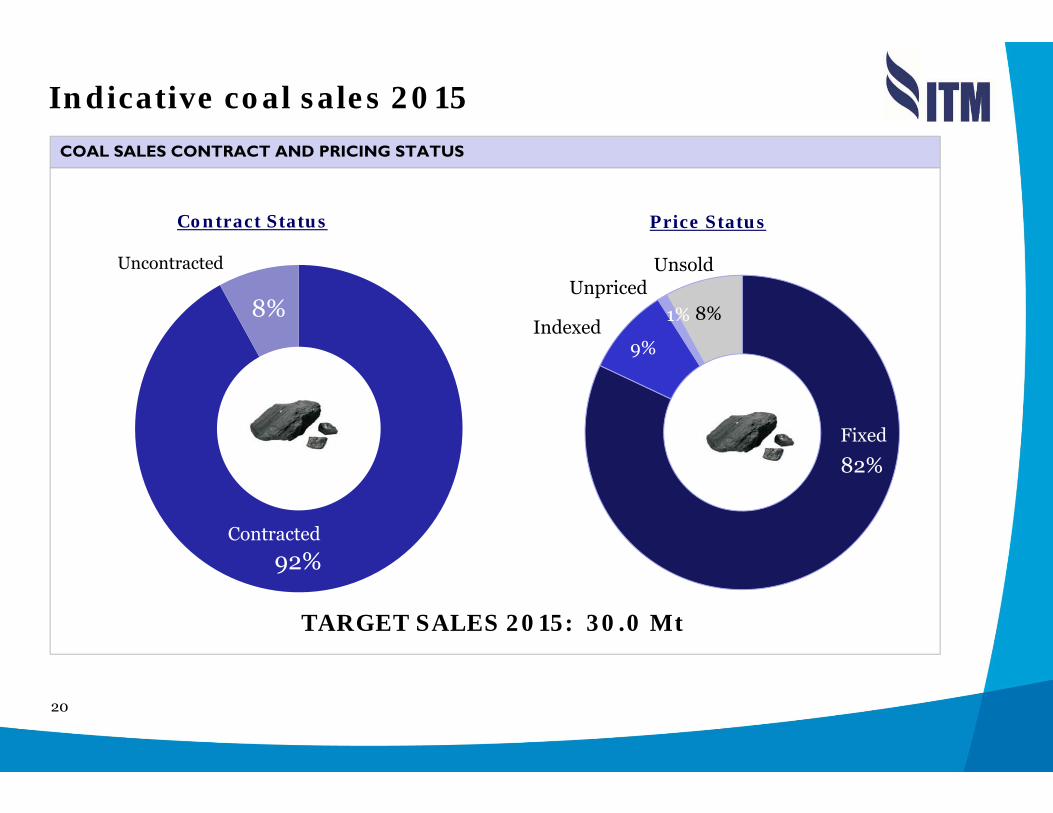

Indicative coal sales 2015COAL SALES CONTRACT AND PRICING STATUS

TARGET SALES 2015: 30.0 Mt

Contract Status Price Status

82%

1%

Fixed

Indexed

92%

8%

Contracted

UnpricedUnsold

9%

8%

Uncontracted

21

Financial reviewCommercial reviewOperational reviewIntroduction

4321

22

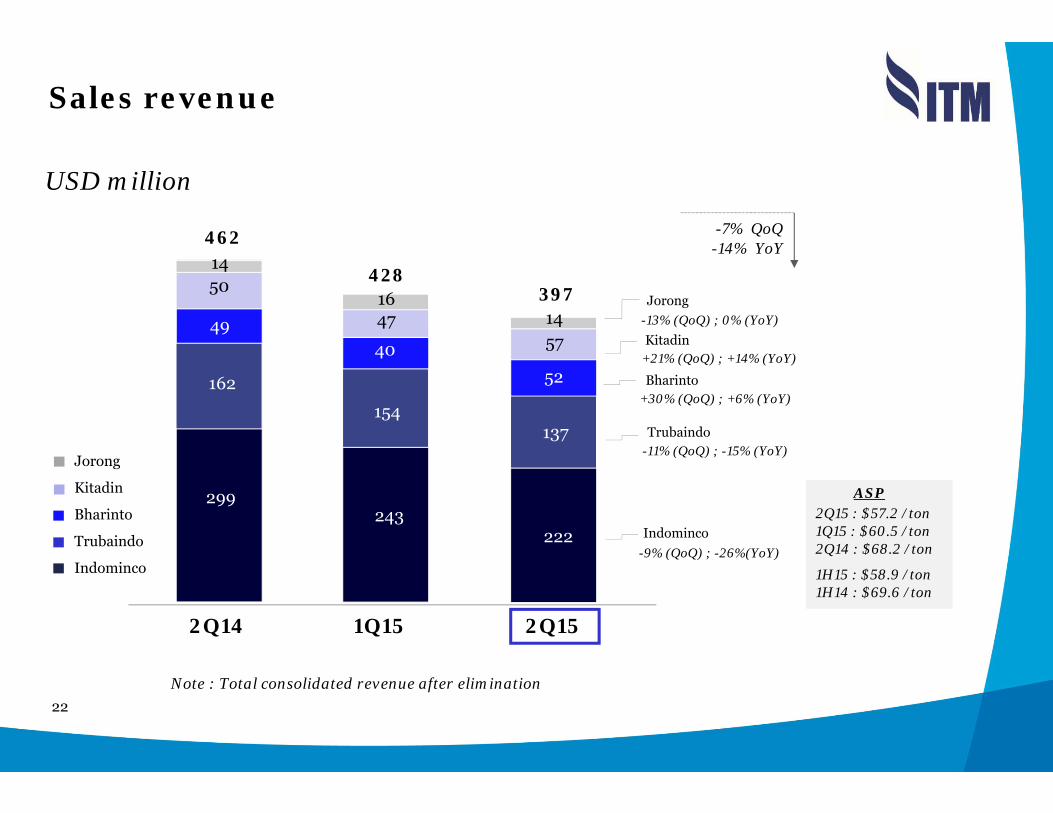

Sales revenue

Note : Total consolidated revenue after elimination

USD million

2Q14 1Q15 2Q15

397

222

137

52

5714

-7% QoQ

Jorong

Kitadin

Bharinto

Trubaindo

Indominco

-14% YoY

Indominco-9% (QoQ) ; -26%(YoY)

Trubaindo-11% (QoQ) ; -15% (YoY)

Bharinto+30% (QoQ) ; +6% (YoY)

Kitadin+21% (QoQ) ; +14% (YoY)

Jorong-13% (QoQ) ; 0% (YoY)

ASP2Q15 : $57.2 /ton1Q15 : $60.5 /ton2Q14 : $68.2 /ton

1H15 : $58.9 /ton1H14 : $69.6 /ton

462

299

162

49

5014

428

243

154

40

4716

23

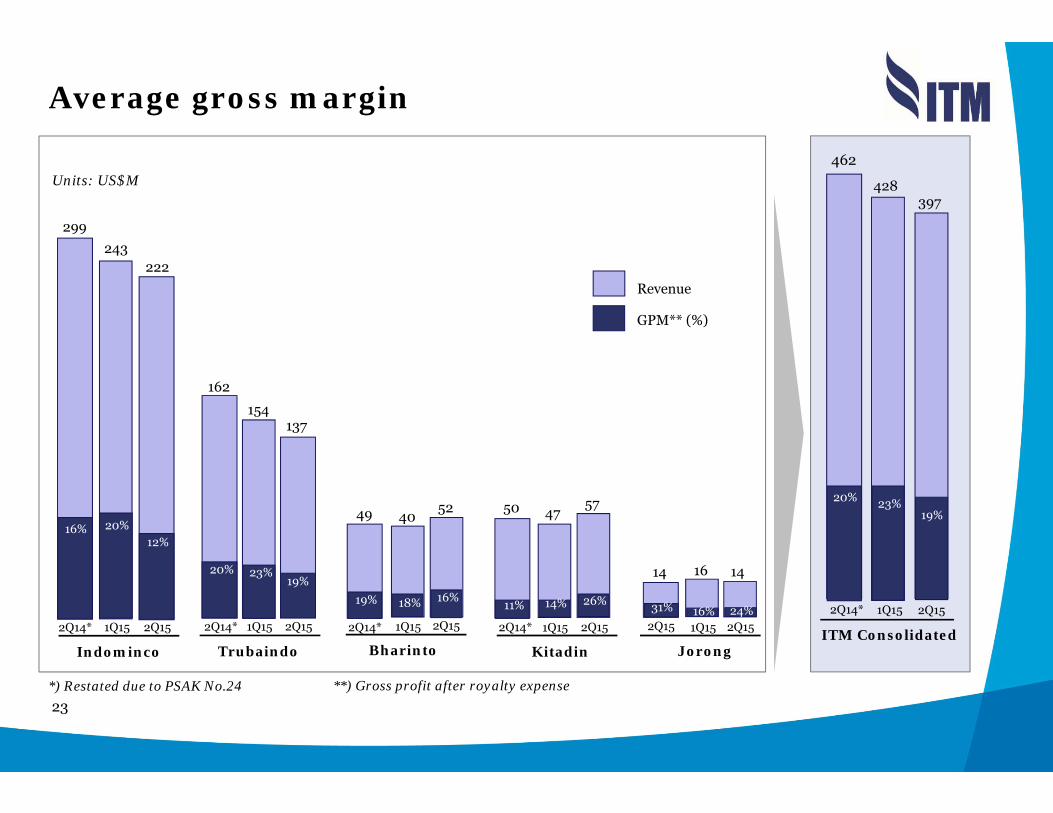

Average gross margin

Revenue

GPM** (%)

Units: US$M

Indominco Trubaindo Kitadin Jorong

39%

28%

Bharinto

243

20%

1Q15

154

23%

47

14%

14

16%

4049

1Q15 1Q15 1Q152Q14* 1Q15

18%

ITM Consolidated

2Q15

397

19%

1Q15

428

23%

2Q14*

462

20%

299

16%

2Q14*

162

20%

2Q14*

50

11%

2Q14*

14

31%2Q15

222

12%

137

19%

57

26%

16

24%

52

16%

2Q15 2Q15 2Q15 2Q152Q15

19%

*) Restated due to PSAK No.24 **) Gross profit after royalty expense

24

Cash cost

2Q14 3Q14 4Q14 1Q15 2Q15

Unit: US$/Ltr

2Q14 3Q14 4Q14 1Q15 2Q15

Unit: Bcm/t Unit: US$/t

WEIGHTED AVERAGE STRIP RATIO CASH PRODUCTION COST

FUEL PRICE

Avg. FY13: 11.2Avg. FY14: 10.0

Avg. FY13: $45.2/tAvg. FY14: $43.6/t

Avg. FY13: $1.02/ltrAvg. FY14: $1.02/ltr

9.2

10.9

1.10

9.8

1.11

0.82

Unit: US$/t

TOTAL CASH COST*

* Cash production cost + royalty + SG&A

Avg. FY13: $60.3/tAvg. FY14: $57.7/t

8.7

0.57

8.6

0.61

2Q14 3Q14 4Q14 1Q15 2Q15

2Q14 3Q14 4Q14 1Q15 2Q15

42.347.3

40.433.5 33.7

56.861.1

54.947.0 46.3

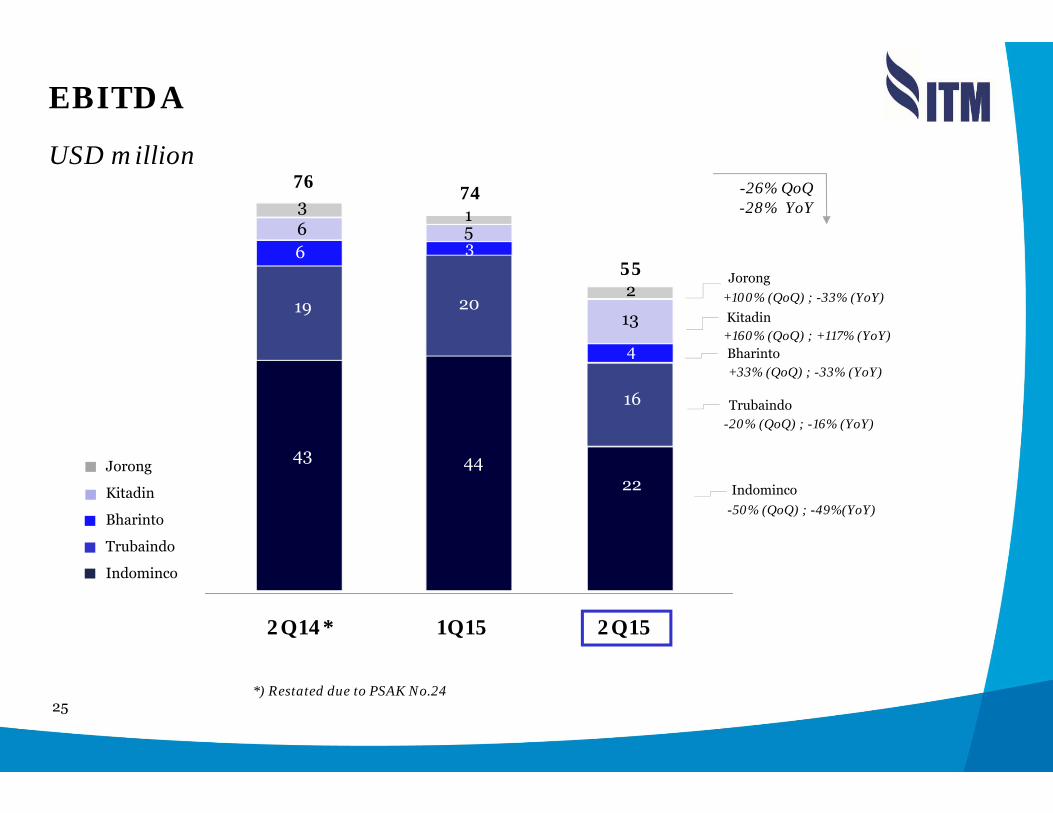

25

EBITDA

USD million

55

22

16

4

13

2

Jorong

Kitadin

Bharinto

Trubaindo

Indominco

2Q14* 1Q15 2Q15

-26% QoQ-28% YoY

Indominco-50% (QoQ) ; -49%(YoY)

Trubaindo-20% (QoQ) ; -16% (YoY)

Bharinto+33% (QoQ) ; -33% (YoY)

Kitadin+160% (QoQ) ; +117% (YoY)

Jorong+100% (QoQ) ; -33% (YoY)

*) Restated due to PSAK No.24

76

43

19

663

74

44

20

351

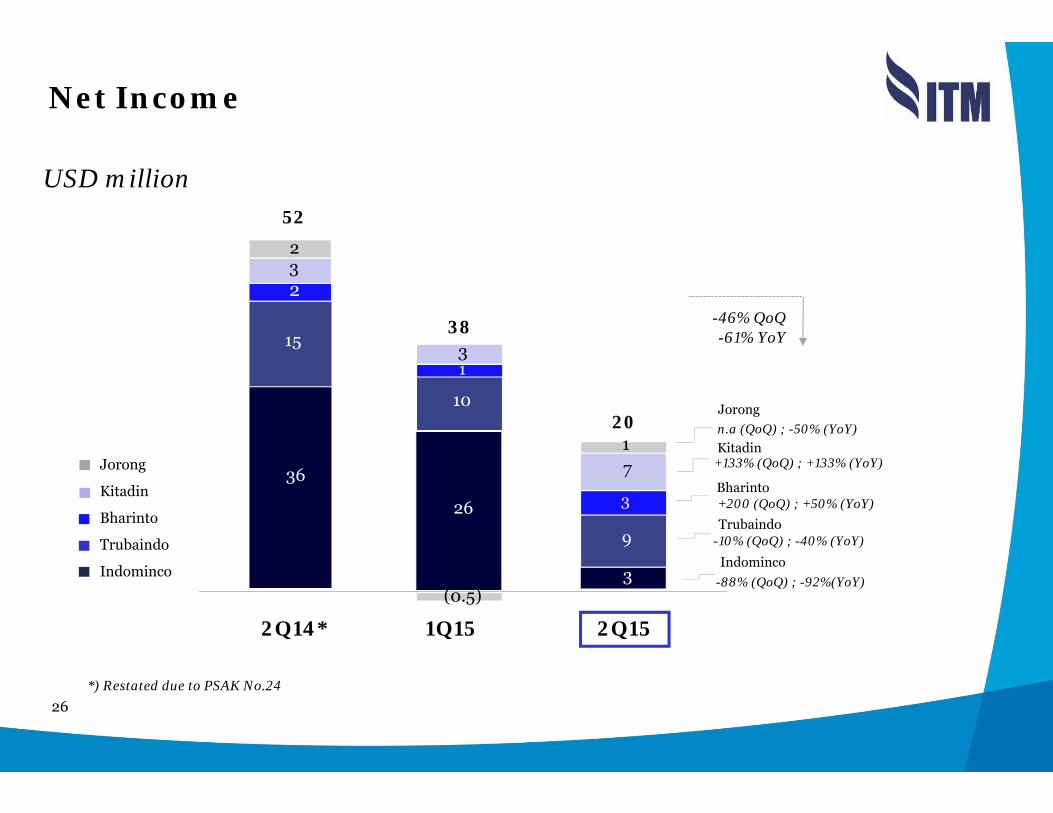

26

Net Income

USD million

20

3

9

3

7Jorong

Kitadin

Bharinto

Trubaindo

Indominco

2Q14* 1Q15 2Q15

-46% QoQ-61% YoY

Indominco-88% (QoQ) ; -92%(YoY)

Trubaindo-10% (QoQ) ; -40% (YoY)

Bharinto+200 (QoQ) ; +50% (YoY)

Kitadin+133% (QoQ) ; +133% (YoY)

Jorongn.a (QoQ) ; -50% (YoY)

*) Restated due to PSAK No.24

52

36

15

23

1

2

38

26

10

13

(0.5)

27

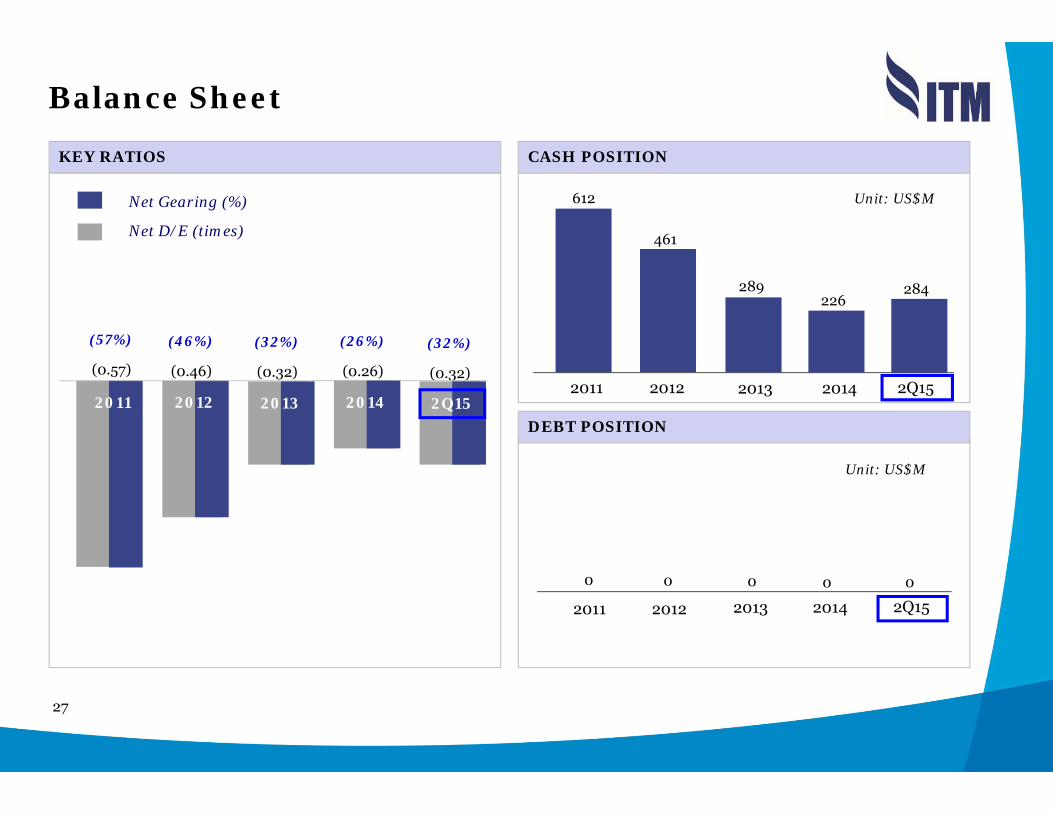

Balance Sheet

CASH POSITION

Net Gearing (%)

Net D/E (times)

KEY RATIOS

Unit: US$M

2Q15

(0.32)

(32%)

(0.57)

(57%)

2011 2012

(0.46)

(46%)

2013

(0.32)

(32%)

2014

(0.26)

(26%)

DEBT POSITION

2011

612

2Q152012

461

2013

289

2014

226284

Unit: US$M

0

2011

0 0

2012 2013

0

2014

0

2Q15

28

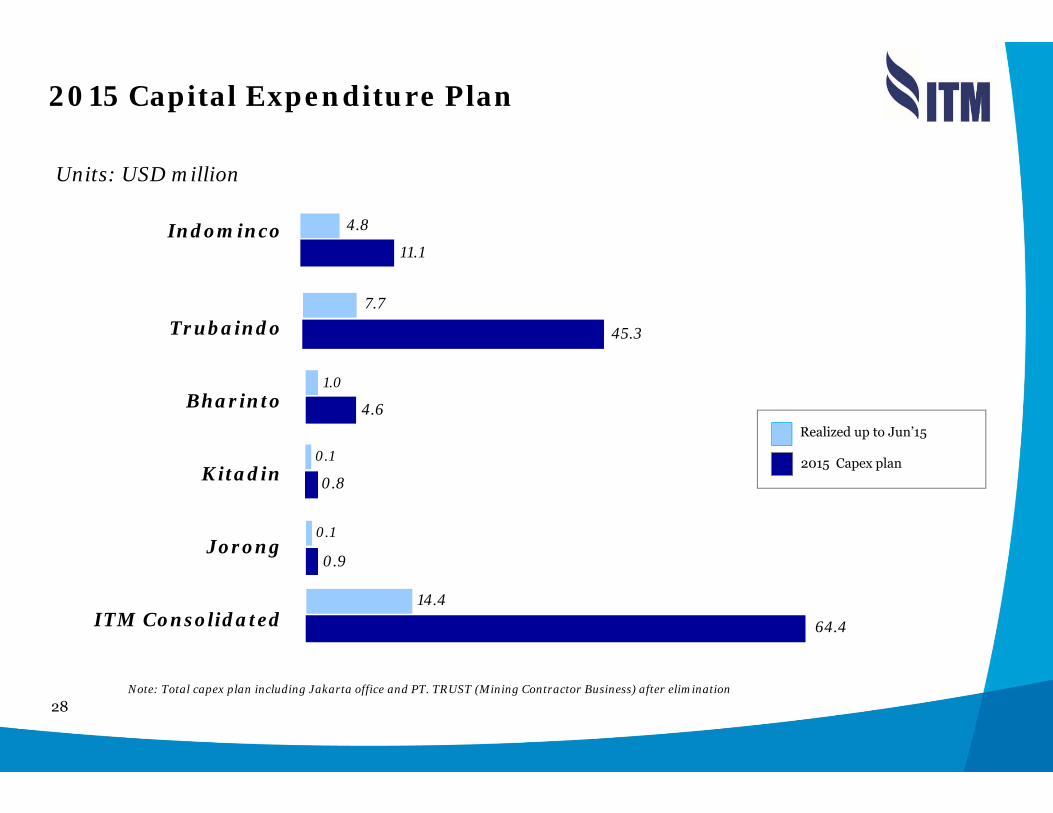

2015 Capital Expenditure Plan

Note: Total capex plan including Jakarta office and PT. TRUST (Mining Contractor Business) after elimination

Units: USD million

Realized up to Jun’15

2015 Capex plan

Indominco

Trubaindo

Bharinto

Kitadin

Jorong

ITM Consolidated

4.8

11.1

45.3

4.6

64.4

0.8

14.4

0.9

0.1

7.7

1.0

0.1

29

Appendices

30

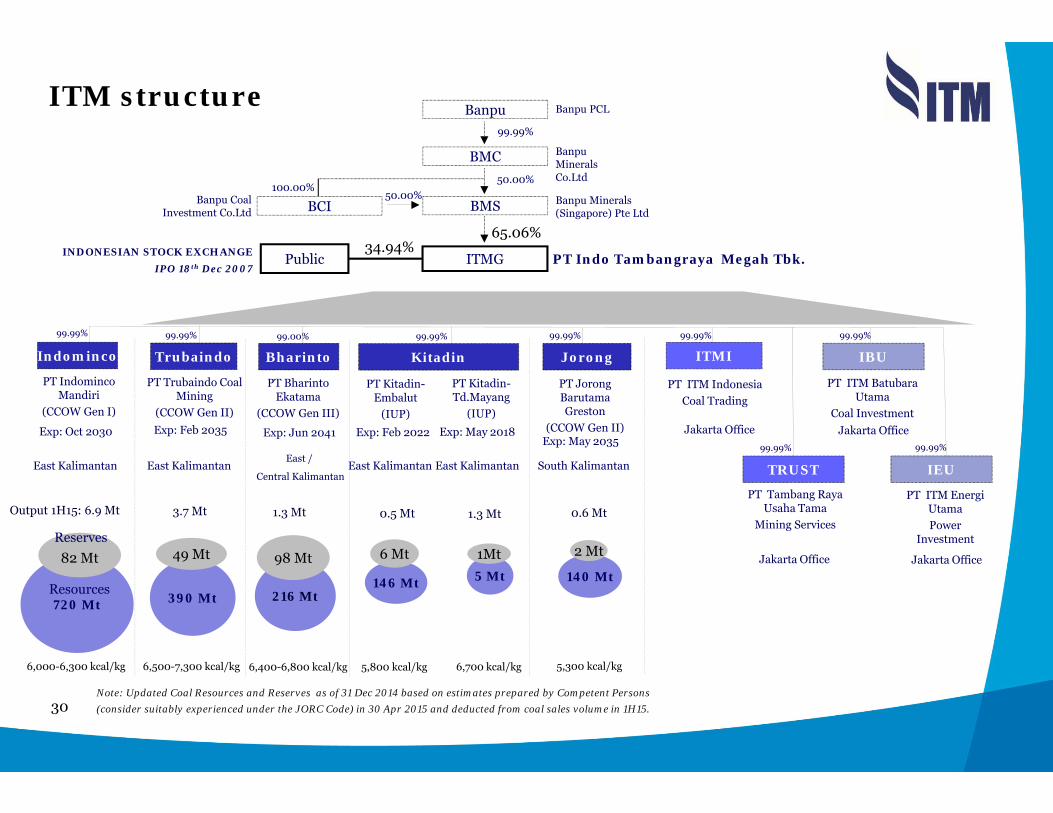

ITM structure

ITMG

65.06%

PT Indominco Mandiri

(CCOW Gen I)

PT Trubaindo Coal Mining

(CCOW Gen II)

PT Kitadin-Embalut

(IUP)

PT JorongBarutama Greston

(CCOW Gen II)

50.00%

PT Indo Tambangraya Megah Tbk.

Banpu Minerals (Singapore) Pte Ltd

99.99% 99.99% 99.99% 99.99%

BanpuMinerals Co.Ltd

BMS

99.99%

BMC

Banpu PCLBanpu

Public34.94%

PT Kitadin-Td.Mayang

(IUP)

BCI50.00%

100.00%Banpu Coal

Investment Co.Ltd

East Kalimantan East Kalimantan South KalimantanEast Kalimantan

INDONESIAN STOCK EXCHANGEIPO 18th Dec 2007

6,500-7,300 kcal/kg6,000-6,300 kcal/kg 5,800 kcal/kg 6,700 kcal/kg 5,300 kcal/kg

Output 1H15: 6.9 Mt 3.7 Mt 0.5 Mt 0.6 Mt

PT Bharinto Ekatama

(CCOW Gen III)

99.00%

East /

Central Kalimantan

6,400-6,800 kcal/kg

1.3 Mt

East Kalimantan

720 Mt

82 Mt

Resources

Reserves

390 Mt

49 Mt

146 Mt

6 Mt

216 Mt

98 Mt140 Mt5 Mt

1Mt

99.99%

Jakarta Office

PT Tambang Raya Usaha Tama

Mining Services

99.99%

Jakarta Office

PT ITM IndonesiaCoal Trading

Exp: Oct 2030 Exp: Feb 2035Exp: May 2035

Exp: May 2018Exp: Jun 2041 Exp: Feb 2022

PT ITM EnergiUtamaPower

Investment

PT ITM Batubara Utama

Coal Investment

99.99%

99.99%

Jakarta Office

Jakarta Office 2 Mt

ITMI

TRUST

Indominco Trubaindo KitadinBharinto Jorong

IEU

IBU

1.3 Mt

Note: Updated Coal Resources and Reserves as of 31 Dec 2014 based on estimates prepared by Competent Persons (consider suitably experienced under the JORC Code) in 30 Apr 2015 and deducted from coal sales volume in 1H15.

31

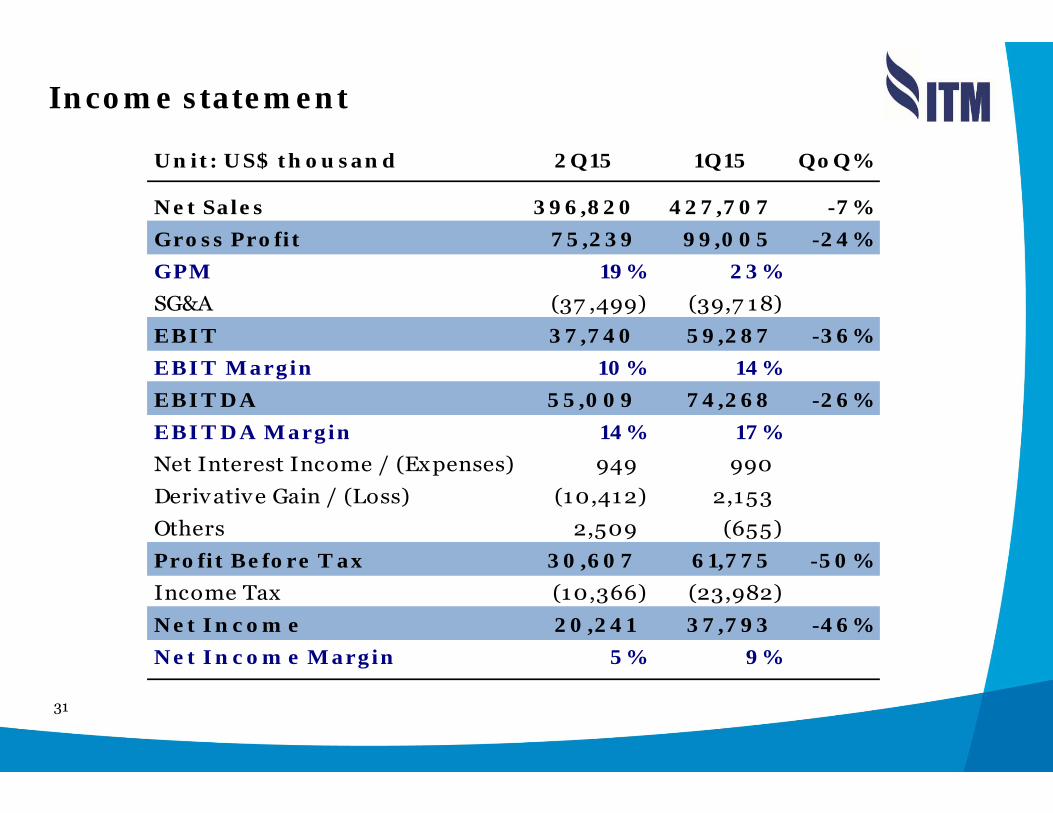

Income statement

Unit: US$ thousand 2Q15 1Q15 QoQ%

Net Sales 396,820 427 ,7 07 -7 %Gross Profit 7 5,239 99,005 -24%GPM 19% 23%SG&A (37 ,499) (39,7 18) EBIT 37 ,7 40 59,287 -36%EBIT Margin 10% 14%EBIT DA 55,009 7 4,268 -26%EBIT DA Margin 14% 17 %Net Interest Income / (Expenses) 949 990 Deriv ative Gain / (Loss) (10,412) 2,153 Others 2,509 (655) Profit Before T ax 30,607 61,7 7 5 -50%Income Tax (10,366) (23,982) Net Incom e 20,241 37 ,7 93 -46%Net Incom e Margin 5% 9%

32

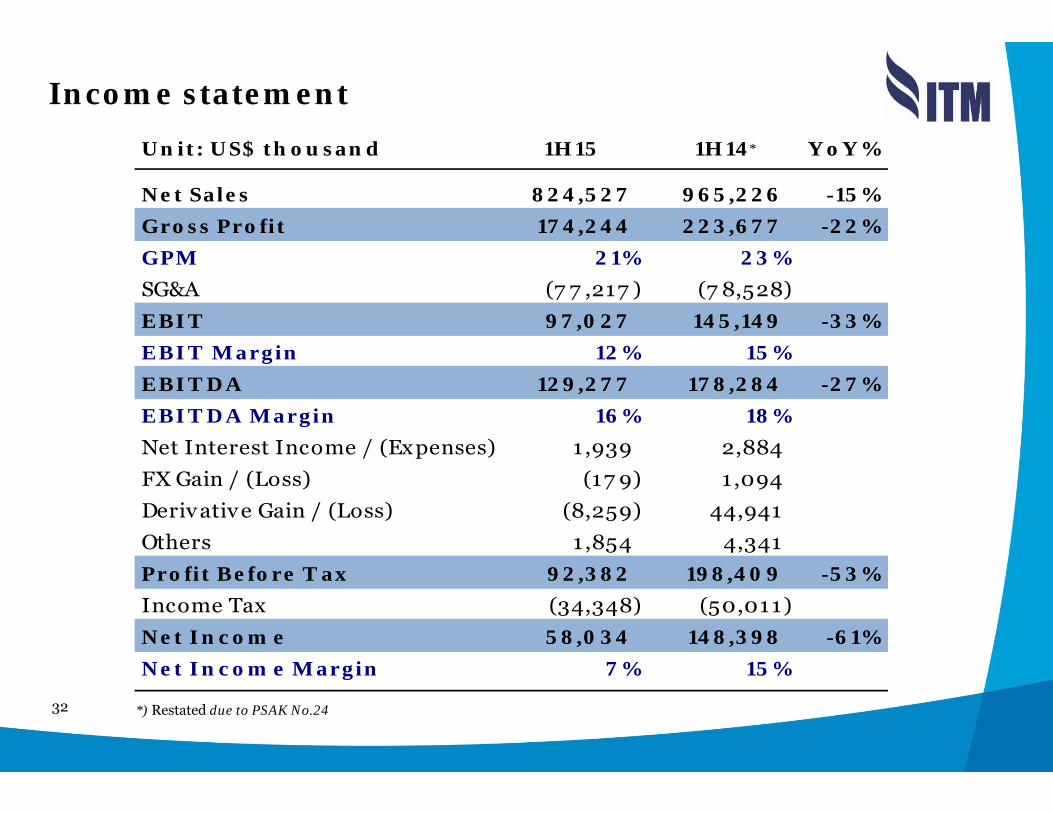

Income statementUnit: US$ thousand 1H15 1H14 YoY%

Net Sales 824,527 965,226 -15%Gross Profit 17 4,244 223,67 7 -22%GPM 21% 23%SG&A (7 7 ,217 ) (7 8,528) EBIT 97 ,027 145,149 -33%EBIT Margin 12% 15%EBIT DA 129,27 7 17 8,284 -27 %EBIT DA Margin 16% 18%Net Interest Income / (Expenses) 1 ,939 2,884 FX Gain / (Loss) (17 9) 1 ,094 Derivative Gain / (Loss) (8,259) 44,941 Others 1 ,854 4,341 Profit Before T ax 92,382 198,409 -53%Income Tax (34,348) (50,011) Net Incom e 58,034 148,398 -61%Net Incom e Margin 7 % 15%

*) Restated due to PSAK No.24

*