24

Ciat Technical Conference (Oct. 6-9, 2014) Santiago de Compostela, Spain Tax compliance determinants: Social perceptions in Bolivia and Panama ME Pecho

| Date post: | 03-Aug-2015 |

| Category: |

Law |

| Upload: | andre-dumoulin |

| View: | 26 times |

| Download: | 0 times |

Ciat Technical Conference (Oct. 6-9, 2014)Santiago de Compostela, Spain

Tax compliance determinants: Social perceptions in Bolivia

and Panama

ME Pecho

Mandate of the CIAT General Assembly

• Resolution of the 45th CIAT General Assembly (Quito, 2011) - "(...)Tax administrations should consider

implementing methodologies aimed at measuring tax morale and compliance of taxpayers, evaluating results and determining appropriate answers for improving both".

Traditional analysis of tax compliance

• A taxpayer who takes rational decisions (maximizing his/her well being), given a serie of perfectly observable parameters. Probability of being detected or audited Size of the sanction or penalty.

• The traditional analysis makes predictions which are counter-intuitive: Given reasonables (realistic) parameters values, no taxpayer

would decide to comply. Non-compliance varies according to the tax rate.

New approximations

• BISEP Model

• Forum of Tax Administration Model

• Tax Morale theory

• Applications of Behavioral Economics

New approximations

• The taxpayer does not always have all the information available The probability of being detected or audited is not known Sanctions vary and are sometimes unknown

• The decision to comply is not only of private nature. Attitudes and beliefs also matter.

• Attitudes and beliefs are transmitted through social interaction. Social networks are important.

Case studies sponsored by ITC-GIZ

Tax compliance

• Tax non-compliance level is perceived as 58% in Panama and 54% in Bolivia.

• In both countries there is a perception that compliance “has much or somehow improved" in recent years (68.8% in Panama and 68% in Bolivia).

• In Bolivia, 75.4% consider "very or somewhat likely" to improve the level of tax compliance in the coming years, while in Panama this percentage is 67.2%.

Determinants of tax compliance considered

• Social norms

• Deterrence

• Opportunities for non-compliance

• Justice and fairness of the tax system

Social norms

• "Positive" citizen values Panamanians and Bolivians perceive themselves as

“honest” (58.7% in Panama and 60% in Bolivia). Panamanians consider themselves as more “law-

abiding” than Bolivians (60.6% in Panama and 39.4% in Bolivia).

Panamanians and Bolivians perceive themselves as “showing solidarity” (69.1% in Panama and 73.7% in Bolivia).

Social norms

• Attitudes towards taxes: They are necessary so the State can “provide goods

or perform services” (72.5% in Panama and 74.3% in Bolivia).

Are a way of “redistributing wealth” (70.9% in Panama and 57.8% in Bolivia).

Constitute a “cívic duty” (62.5% in Panama and 71% in Bolivia).

Social norms

• Effects of tax non-compliance It is perceived that “it decreases the resources that

the State needs to provide goods or perform services” (34.3% in Panama and 36.9% in Bolivia).

It is perceived that it “demotivate those who pay correctly” (18.8% in Panama and 26.4% in Bolivia).

It is perceived as “unfair regarding those who comply” (19.4% in Panama y 16.5% in Bolivia).

Social norms

• Social interaction and compliance. Justifying non-compliance “because the other citizens

don’t pay either” is low in Panama and Bolivia. 38% of Panamanians and 54.2% of Bolivians indicate

“knowing those who don’t comply”.

Deterrence

• Knowledge of the tax system 96.6% of Panamanians declare having knowledge of

VAT, while only 49% of Bolivians express having knowledge of VAT (regarding the Transaction Tax only 43.2% say they have knowledge of it).

96% of Panamanians declare having knowledge of the Income Tax. Only 36.5% of interviewed Bolivians express knowledge of the VAT Complementary Regime and 31.4% express knowledge of the Corporate Income Tax.

Deterrence

• Probability of being detected Justifying non compliance because of a low

probability of being detected is more frequent in Panama than in Bolivia.

The factor perceived as having most influence on the improvement of tax compliance is the control performed by the tax administration (88.5% in Panama and 78.5% in Bolivia).

Deterrence

• However, very few Panamanians and Bolivians have knowledge of sanctions for those who don’t comply. Knowledge of individual sanctionned: 16.8% in Bolivia

an 13.3% in Panama. Knowledge of sanctionned companies: 22.5% in

Bolivia and 10.2% in Panama.

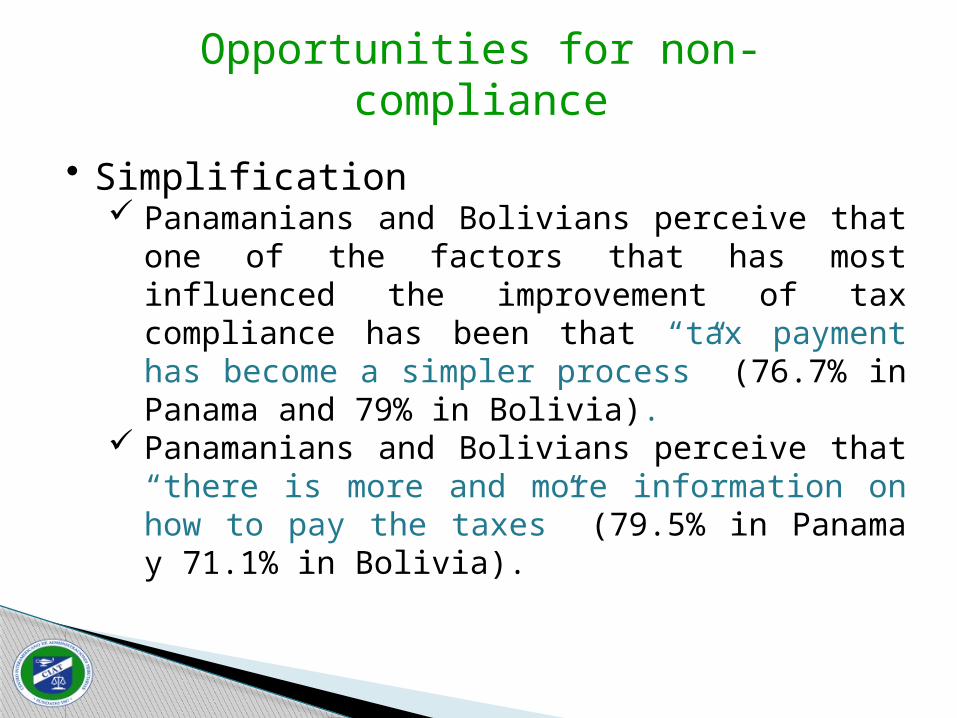

Opportunities for non-compliance

• Simplification Panamanians and Bolivians perceive that one of the

factors that has most influenced the improvement of tax compliance has been that “tax payment has become a simpler process” (76.7% in Panama and 79% in Bolivia).

Panamanians and Bolivians perceive that “there is more and more information on how to pay the taxes” (79.5% in Panama y 71.1% in Bolivia).

Opportunities for non-compliance

• Risks of non-compliance are higher in the segment of independent workers. Panamanians and Bolivians perceive that one of the

factors which has most influenced in the improvement of tax compliance has been “the increase in numbers of people who (….) pay taxes because part of their salary is withheld” (83.9% in Panama and 75.3% in Bolivia).

Justice and fairness of the tax system

• Social contract Lack of clarity in the fiscal exchange: “taxes are what

the State force us to pay without knowing very well in return for what” (62.2% in Panama and 54.3% in Bolivia).

Panamanians and Bolivians perceive that one of the factors that has most influenced in the improvement of tax compliance has been “the improvement in the relationship between public goods and services received and taxes paid” (79.6% in Panama and 72.6% in Bolivia).

Justice and Fairness of the tax system

• Progressivity The majority of Panamanians perceive that those who

have less are those who pay more taxes, which show a perception of “unfairness in taxation”.

On the other hand, the majority of Bolivians perceive that those who have more are those who pay more taxes, which show a perception of better “fairness in taxation”.

Justice and Fairness of the tax system

• Governance Justifying non-compliance “because there is obvious

corruption and lack of transparency in the political class” is much more emphasized in Bolivia than in Panama.

Justifying non-compliance “because there is no trust in public management” is also much more frequent in Bolivia than in Panama.

Some conclusions

• Civic values and attitudes towards taxes are not necessarily reflected in tax compliance.

• Effects of non-compliance are partially internalized.

• The formation of beliefs regarding non compliance seems to be weak.

Some conclusions

• Much lower knowledge of the tax system in Bolivia than in Panama.

• Lower risk perception in Panama than in Bolivia.

• Little knowledge of the sanctions imposed to those who don’t comply.

• Simplification induces compliance.

Some conclusions

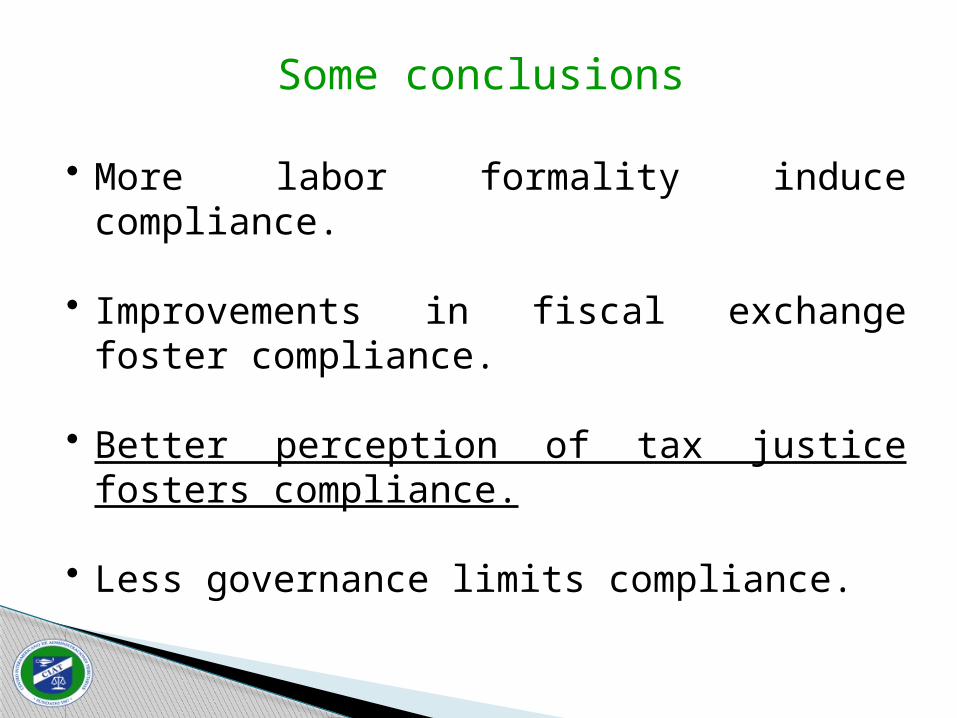

• More labor formality induce compliance.

• Improvements in fiscal exchange foster compliance.

• Better perception of tax justice fosters compliance.

• Less governance limits compliance.

Ciat Technical Conference (Oct. 6-9, 2014)Santiago de Compostela, Spain

Tax compliance determinants: Social perceptions in Bolivia

and Panama

ME Pecho