Page 1

105

5 WORKING CAPITAL MANAGEMENT

5.1 INTRODUCTION

In working capital management, firms are employing more sophisticated

collection and disbursement systems. Maintaining appropriate cash balances or

inventory levels involves managing flows. Inefficient use of cash and materials

ultimately reduces the firm’s profitability. The C2C cycle time attempts to measure

the time elapsed between paying suppliers for material and getting paid by customers.

C2C cycle time is a unique financial performance metric that indicates how well an

entity is managing its working capital.

In integrated SCM, the problem arises when one or few companies enjoy the

pooled benefits at the detriment of the others. The idea of reallocation of benefits

may be good. But in reality, there must be a mechanism to identify opportunities to

strengthen all the channel members through strategic agreements. In the present

research work, A LPP model is developed with an objective of minimizing total

penalty to all entities (firm, suppliers and distributors / customers) in an integrated

approach. The LPP model provides optimal solution (payment period, collection

period and deferral period) associated with minimum penalty to all entities along the

Page 2

106

supply chain. Firms may use this model as a tool to benchmark the payment and

collection periods while formulating strategic partnerships with their counter parts.

5.2 EXPRESSION FOR C2C CYCLE TIME

The components of C2C cycle time are inventory days, average collection

period and average payment period.

C2C cycle time is estimated using the following relation:

C2C cycle time =

periodpayment

Averageperiodcollection

AveragedaysInventory

------ (5.1)

Where, Inventory days = 365XSoldGoodsofCost

InventoryAverage

------ (5.2)

Average collection period = 365Re XSalesNet

ceivableAccounts

----- (5.3)

Average payment period = 365XCostMaterialDirect

PaybleAccounts

---- (5.4)

All the above terms are expressed in same units (i.e., days).

Page 3

107

From industry specific goal, the companies try to achieve C2C cycle time that

is as low as reasonable (or even negative). A lower C2C cycle time indicates that the

company is more efficient in managing its cash flows as it turns its working capital

more times per year and generates more sales per rupee invested.

Reducing C2C cycle time leads to operational and financial improvements.

This also provides guidelines to business that seeks to obtain a proper mix between

the amount of resources deployed to working capital and to capital investments. It is

evident that a shorter C2C cycle time results in higher present value for net cash flows

generated by the assets and ultimately higher value for the business.

5.3 LP APPROACH TO OPTIMIZE C2C CYCLE TIME

C2C cycle time for any firm depends on two factors: firstly, inventory days

and secondly, the difference between average collection period and average payment

period (payment deferral period). The first factor is an internal operational

performance measure which reflects the inventory management of a firm. While the

second factor is cross-border performance measure which reflects cash conversion

efficiency as well as the buyer-vendor relationships upstream and downstream in a

supply chain.

Page 4

108

Maintaining longer credit periods (at suppliers’ end) may be beneficial to the

buying firm but supplier(s) are penalized by loss of interest on money blocked with its

customers. Similarly, at customers’ end, longer credit periods may be beneficial to

distributors / customers but the firm loses interest on credit sales. On the other hand,

shorter credit period leads to loss of interest on purchase price for distributors.

In this competitive world, every company tries to maintain shorter C2C cycle

time by making the difference of collection and payment periods minimum (or

negative). This practice definitely leads to weakened link(s) along the supply chain

as it is impossible to all firms along a supply chain to get benefited by achieving

minimum (or negative) difference. In an integrated approach to supply chain

performance measurement, we must arrive at an optimal combination of average

payment period and average collection period which is beneficial and acceptable for

buyer(s) and vendor(s) while formulating or revising strategic agreements.

5.3.1 Formulation of Linear Programming Problem

Variables declaration:

Let Tp = Average Payment Period (days)

Tc = Average Collection Period (days)

Page 5

109

X1 = Reduction in payment period (days)

X2 = Reduction in collection period (days)

r = Rate of interest

Now, the penalty to different entities may be as given below:

Penalty to Suppliers = 365

**)( 1 rPayablesXTp ----------------------- (5.5)

Penalty to Distributers = 365

*Re*2 rceivablesX --------------------- (5.6)

Penalty to Firm = 365

**365

*Re*)( 12 rXPayablesrceivablesXTc

-- (5.7)

Considering a simple case of one-tier supply chain, the total penalty to entities

along the chain is given by

Z =

365**

365*Re*)(

365*Re*

365**)(

12

21

rXPayablesrceivablesXTc

rceivablesXrPayablesXTp

--------- (5.8)

The above expression can be simplified as follows:

Let 365

*1

rPayablesa

365

*Re2

rceivablesa

Page 6

110

The objective is to find the optimal combination of payment and collection

periods that would minimize the total penalty to all firms along the supply chain. The

simplified objective function and constraints subject to which the objective function is

optimized are furnished below.

Minimize Z = 1121 *2** XaTcaTpa

Subject to

b1 ≤ Tp ≤ b2; (Constraint – 1)

b3 ≤ Tc ≤ b4; (Constraint – 2)

Tp - X1 ≥ b5; (Constraint – 3)

Tc - X2 ≥ b6; (Constraint – 4)

Tc - Tp ≥ b7; (Constraint – 5)

Tp, Tc, X1, X2 ≥ 0. (Constraint – 6)

In the LPP model, the right hand side values of constraints are current average

payment and collection periods (b2 and b4) or expected lower limits of decision

variables (b1, b3, b5, b6 and b7). The above LPP is solved using TORA (Windows

version 2.0, 2006) and the results i.e., the optimal combination of average payment

period and average collection period that would minimize total penalty to all firms

along the supply chain are tabulated.

Page 7

111

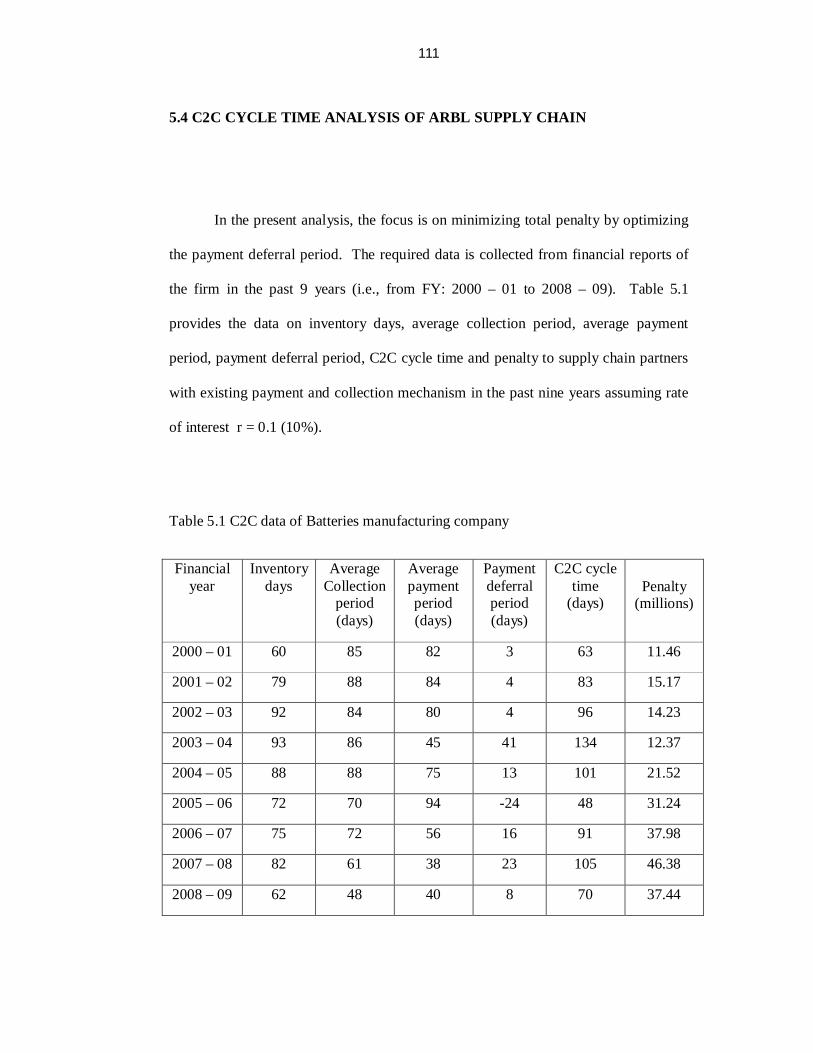

5.4 C2C CYCLE TIME ANALYSIS OF ARBL SUPPLY CHAIN

In the present analysis, the focus is on minimizing total penalty by optimizing

the payment deferral period. The required data is collected from financial reports of

the firm in the past 9 years (i.e., from FY: 2000 – 01 to 2008 – 09). Table 5.1

provides the data on inventory days, average collection period, average payment

period, payment deferral period, C2C cycle time and penalty to supply chain partners

with existing payment and collection mechanism in the past nine years assuming rate

of interest r = 0.1 (10%).

Table 5.1 C2C data of Batteries manufacturing company

Financial year

Inventory days

Average Collection

period (days)

Average payment period (days)

Payment deferral period (days)

C2C cycle time

(days) Penalty

(millions)

2000 – 01 60 85 82 3 63 11.46

2001 – 02 79 88 84 4 83 15.17

2002 – 03 92 84 80 4 96 14.23

2003 – 04 93 86 45 41 134 12.37

2004 – 05 88 88 75 13 101 21.52

2005 – 06 72 70 94 -24 48 31.24

2006 – 07 75 72 56 16 91 37.98

2007 – 08 82 61 38 23 105 46.38

2008 – 09 62 48 40 8 70 37.44

Page 8

112

From table 5.1, it is understood that the firm has achieved a minimum of 48

days C2C cycle time but with penalty to its suppliers (by delayed payments). Higher

values of C2C cycle time are due to large difference between collection and payment

periods (in FYs’ 2003 – 04, 2004 – 05 & 2007 - 08). Mostly, the average payment

period is less than the average collection period (except in FY: 2005 – 06). Still, there

is wide scope for improving C2C cycle time by decreasing inventory days and

minimizing payment deferral period. Excluding abnormal values (in FY: 2003 – 04

and 2005 – 06), the correlation between payment deferral period and penalty is

0.8514. Which means that there exists a very high correlation between them.

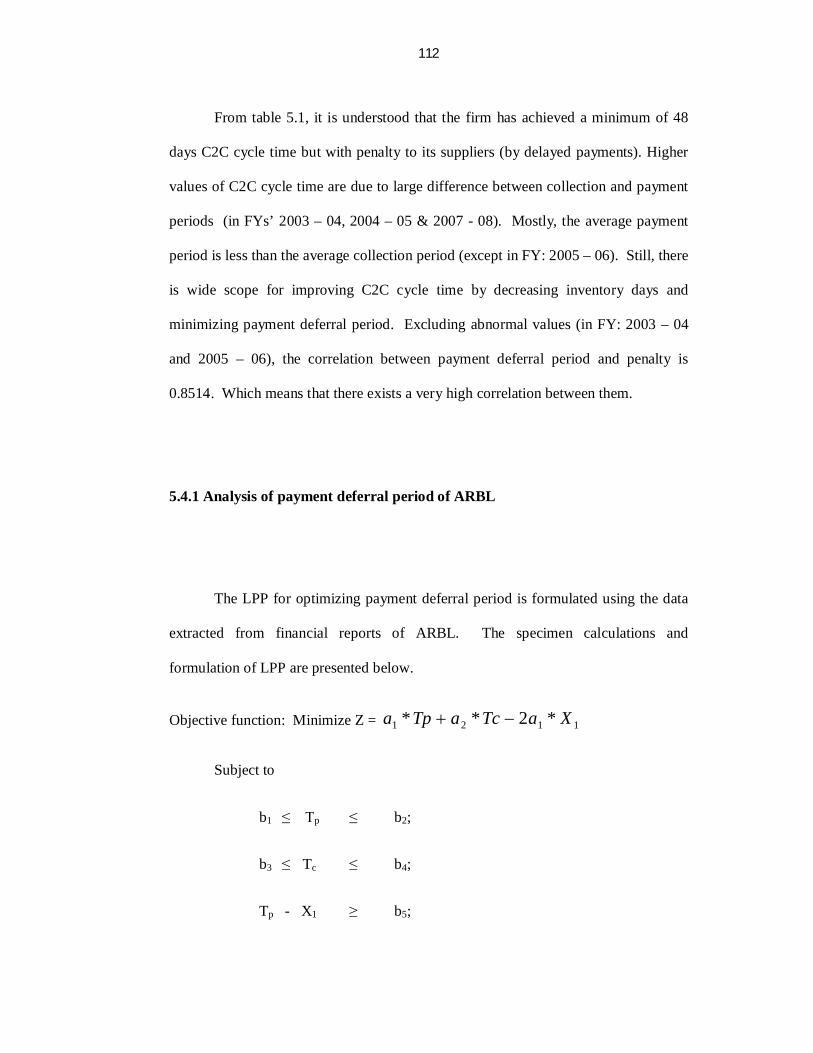

5.4.1 Analysis of payment deferral period of ARBL

The LPP for optimizing payment deferral period is formulated using the data

extracted from financial reports of ARBL. The specimen calculations and

formulation of LPP are presented below.

Objective function: Minimize Z = 1121 *2** XaTcaTpa

Subject to

b1 ≤ Tp ≤ b2;

b3 ≤ Tc ≤ b4;

Tp - X1 ≥ b5;

Page 9

113

Tc - X2 ≥ b6;

Tc - Tp ≥ b7;

Tp, Tc, X1, X2 ≥ 0.

The values of payables and receivables are extracted from table 3.5 and the

specimen calculations are carried out for the year 2000 – 01 as follows.

Specimen Calculation:

Payables = 133.496712 million rupees

Receivables = 361.964041 million rupees

365

*1

rPayablesa

365

1.0*496712.133

= 0.0365 ≈ 0.04

365

*Re2

rceivablesa

3651.0*964041.361

= 0.0992 ≈ 0.1

Page 10

114

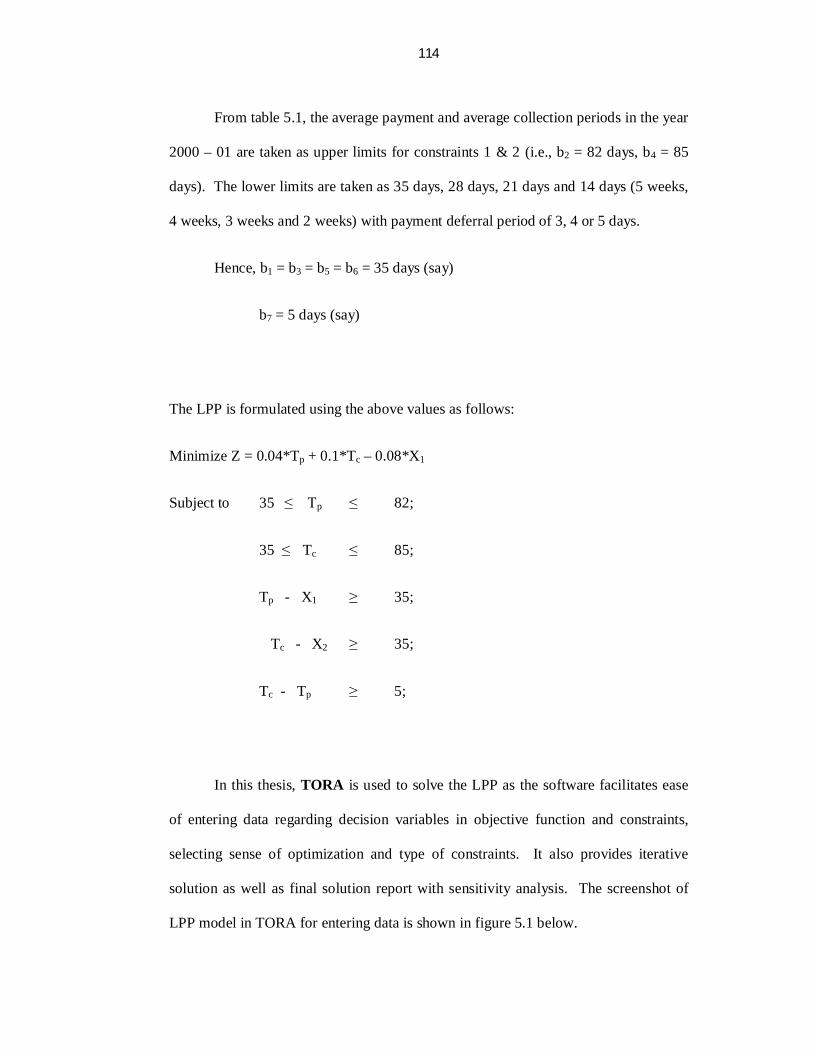

From table 5.1, the average payment and average collection periods in the year

2000 – 01 are taken as upper limits for constraints 1 & 2 (i.e., b2 = 82 days, b4 = 85

days). The lower limits are taken as 35 days, 28 days, 21 days and 14 days (5 weeks,

4 weeks, 3 weeks and 2 weeks) with payment deferral period of 3, 4 or 5 days.

Hence, b1 = b3 = b5 = b6 = 35 days (say)

b7 = 5 days (say)

The LPP is formulated using the above values as follows:

Minimize Z = 0.04*Tp + 0.1*Tc – 0.08*X1

Subject to 35 ≤ Tp ≤ 82;

35 ≤ Tc ≤ 85;

Tp - X1 ≥ 35;

Tc - X2 ≥ 35;

Tc - Tp ≥ 5;

In this thesis, TORA is used to solve the LPP as the software facilitates ease

of entering data regarding decision variables in objective function and constraints,

selecting sense of optimization and type of constraints. It also provides iterative

solution as well as final solution report with sensitivity analysis. The screenshot of

LPP model in TORA for entering data is shown in figure 5.1 below.

Page 11

115

Figure 5.1 Screen shot showing the formulation of LPP in TORA

The computations have been made for different right hand side values of

constraints and coefficients in objective function. In each case, an optimal solution is

obtained. The results clearly indicate that the optimal combination of average

payment period and average collection period are acceptable for pair(s) of trading

partners both upstream and downstream the supply chain.

Page 12

116

Table 5.2 provides the optimal average collection and payment periods for

which the total penalty will be minimum (at rate of interest r = 10%) by solving LPP

model using TORA. The analysis carried out for different Right Hand Side (RHS)

values (taking 2 weeks, 3 weeks, 4weeks and 5 weeks as payment period) reveal that

the penalty decreases with decrease in payment deferral period as well as average

payment and collection periods.

Table 5.2 Optimal payment & collection periods for ARBL (FY: 2000-01)

Payment period (14 days)

Payment period (21 days)

Payment period (28 days)

Payment period (35 days)

Optimal Tp (days)

14 14 14 21 21 21 28 28 28 35 35 35

Optimal Tc (days)

17 18 19 24 25 26 31 32 33 38 39 40

Optimal Deferral period (days)

3 4 5 3 4 5 3 4 5 3 4 5

Penalty

(Millions) 2.26 2.36 2.46 3.24 3.34 3.44 4.22 4.32 4.42 5.2 5.3 5.4

(a1 = 0.04, a2 = 0.1 for payables = 133 millions & receivables = 362 millions)

The penalty values in table 5.2 for different payment periods reveals that the

total penalty along the supply chain is decreasing as the payment and collection

period are decreased, for the given values of receivables and payables (sundry debtors

and sundry creditors). The screen shots of formulation and solution of LPP using

TORA for different values of objective function coefficients and RHS values (from

Page 13

117

FY: 2000 – 01 to 2008 – 09) are furnished in appendix – A. The optimal payment and

collection periods associated with minimum penalty in successive financial years have

been furnished in tables 5.3 to 5.10.

Table 5.3 Optimal payment & collection periods for ARBL (FY: 2001 - 02)

Payment period (14 days)

Payment period (21 days)

Payment period (28 days)

Payment period (35 days)

Optimal Tp (days) 14 14 14 21 21 21 28 28 28 35 35 35

Optimal Tc (days) 17 18 19 24 25 26 31 32 33 38 39 40

Optimal Deferral period (days)

3 4 5 3 4 5 3 4 5 3 4 5

Penalty

(Millions) 2.81 2.93 3.06 4.03 4.15 4.27 5.24 5.37 5.49 6.46 6.59 6.71

(a1 = 0.05, a2 = 0.124 for payables = 184 millions & receivables = 453 millions)

Table 5.4 Optimal payment & collection periods for ARBL (FY: 2002 - 03)

Payment period (14 days)

Payment period (21 days)

Payment period (28 days)

Payment period (35 days)

Optimal Tp (days) 14 14 14 21 21 21 28 28 28 35 35 35

Optimal Tc (days) 17 18 19 24 25 26 31 32 33 38 39 40

Optimal Deferral period (days)

3 4 5 3 4 5 3 4 5 3 4 5

Penalty

(Millions) 2.78 2.91 3.03 3.99 4.11 4.24 5.19 5.32 5.44 6.39 6.52 6.64

(a1 = 0.047, a2 = 0.125 for payables = 173 millions & receivables = 456 millions)

Page 14

118

Table 5.5 Optimal payment & collection periods for ARBL (FY: 2003 - 04)

Payment period (14 days)

Payment period (21 days)

Payment period (28 days)

Payment period (35 days)

Optimal Tp (days) 14 14 14 21 21 21 28 28 28 35 35 35

Optimal Tc (days) 17 18 19 24 25 26 31 32 33 38 39 40

Optimal Deferral period (days)

3 4 5 3 4 5 3 4 5 3 4 5

Penalty

(Millions) 2.58 2.71 2.84 3.68 3.81 3.94 4.78 4.91 5.04 5.88 6.01 6.14

(a1 = 0.0279, a2 = 0.129 for payables = 102 millions & receivables = 472 millions)

Table 5.6 Optimal payment & collection periods for ARBL (FY: 2004 - 05)

Payment period (14 days)

Payment period (21 days)

Payment period (28 days)

Payment period (35 days)

Optimal Tp (days) 14 14 14 21 21 21 28 28 28 35 35 35

Optimal Tc (days) 17 18 19 24 25 26 31 32 33 38 39 40

Optimal Deferral period (days)

3 4 5 3 4 5 3 4 5 3 4 5

Penalty

(Millions) 4.11 4.29 4.47 5.89 6.08 6.26 7.69 7.87 8.04 9.48 9.65 9.83

(a1 = 0.0775, a2 = 0.178 for payables = 283 millions & receivables = 650 millions)

Page 15

119

Table 5.7 Optimal payment & collection periods for ARBL (FY: 2005 - 06)

Payment period (14 days)

Payment period (21 days)

Payment period (28 days)

Payment period (35 days)

Optimal Tp (days) 14 14 14 21 21 21 28 28 28 35 35 35

Optimal Tc (days) 17 18 19 24 25 26 31 32 33 38 39 40

Optimal Deferral period (days)

3 4 5 3 4 5 3 4 5 3 4 5

Penalty

(Millions) 6.19 6.43 6.66 8.94 9.17 9.41 11.7 11.9 12.2 14.4 14.7 14.9

(a1 = 0.157, a2 = 0.235 for payables = 574 millions & receivables = 857 millions)

Table 5.8 Optimal payment & collection periods for ARBL (FY: 2006 - 07)

Payment period (14 days)

Payment period (21 days)

Payment period (28 days)

Payment period (35 days)

Optimal Tp (days) 14 14 14 21 21 21 28 28 28 35 35 35

Optimal Tc (days) 17 18 19 24 25 26 31 32 33 38 39 40

Optimal Deferral period (days)

3 4 5 3 4 5 3 4 5 3 4 5

Penalty

(Millions) 9.14 9.54 9.94 13.1 13.5 13.9 17.1 17.5 17.9 21.0 21.4 21.8

(a1 = 0.167, a2 = 0.4 for payables = 608 millions & receivables = 1460 millions)

Page 16

120

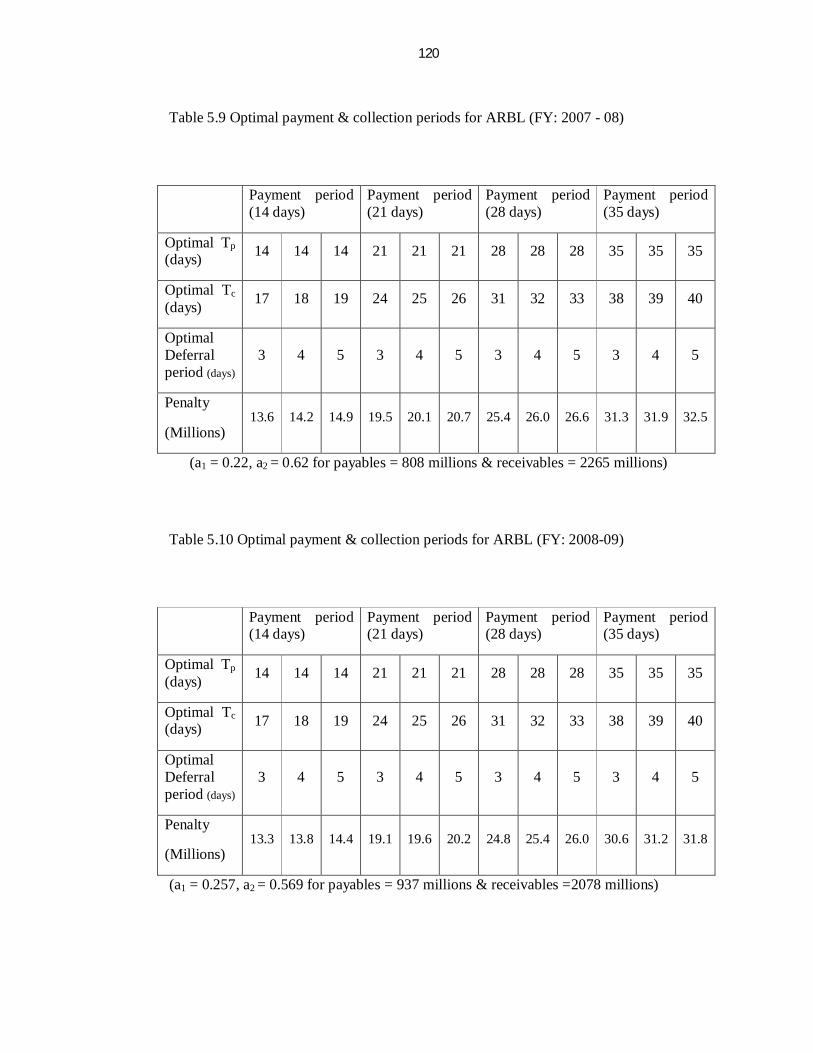

Table 5.9 Optimal payment & collection periods for ARBL (FY: 2007 - 08)

Payment period (14 days)

Payment period (21 days)

Payment period (28 days)

Payment period (35 days)

Optimal Tp (days) 14 14 14 21 21 21 28 28 28 35 35 35

Optimal Tc (days) 17 18 19 24 25 26 31 32 33 38 39 40

Optimal Deferral period (days)

3 4 5 3 4 5 3 4 5 3 4 5

Penalty

(Millions) 13.6 14.2 14.9 19.5 20.1 20.7 25.4 26.0 26.6 31.3 31.9 32.5

(a1 = 0.22, a2 = 0.62 for payables = 808 millions & receivables = 2265 millions)

Table 5.10 Optimal payment & collection periods for ARBL (FY: 2008-09)

Payment period (14 days)

Payment period (21 days)

Payment period (28 days)

Payment period (35 days)

Optimal Tp (days) 14 14 14 21 21 21 28 28 28 35 35 35

Optimal Tc (days) 17 18 19 24 25 26 31 32 33 38 39 40

Optimal Deferral period (days)

3 4 5 3 4 5 3 4 5 3 4 5

Penalty

(Millions) 13.3 13.8 14.4 19.1 19.6 20.2 24.8 25.4 26.0 30.6 31.2 31.8

(a1 = 0.257, a2 = 0.569 for payables = 937 millions & receivables =2078 millions)

Page 17

121

From tables 5.2 to 5.10, it could be understood that the penalty is decreasing

with decrease in payment and collection periods as well as the deferral period. Also,

the optimal payment and collection periods are independent of the current payment

and collection periods of the firm.

The sensitivity analysis reports for different objective coefficients and RHS

values of constraints from FY: 2000 – 01 to 2008 – 09 is furnished in appendix – B.

The results of sensitivity analyses for different objective coefficients are presented in

table 5.11.

The optimal solution given by the LPP model is helpful for firms while

negotiating on terms and conditions of supply. The firms can use these values during

benchmarking average payment and collection periods. Practically, some tolerance

may be allowed on either side of optimal value while taking strategic decisions.

Hence, this model helps to identify the penalty associated with different

combinations of average payment and collection periods associated with minimum

penalty and shorter C2C cycle time for any firm and its supply chain in an integrated

approach.. Through the practice of scientific estimation of payment and collection

periods, this ideology can be extended to successive echelons for the profit of all

firms along the supply chain.

Page 18

122

Table 5.11 Results of sensitivity analysis for different objective coefficients

Financial

year

Payables

(million

Rupees)

Receivables

(million

Rupees)

Objective Coefficients

a1 a2 X1

Current Min Max Current Min Max Current Min Max

2000 - 01 133 362 0.0400 -0.0200 α 0.1000 0.0400 α -0.0800 -0.1400 α

2001 - 02 184 453 0.0500 -0.0240 α 0.1240 0.0500 α -0.1000 -0.1740 α

2002 - 03 173 456 0.0470 -0.0310 α 0.1250 0.0470 α -0.0940 -0.1720 α

2003 - 04 102 472 0.0279 -0.0732 α 0.1290 0.0279 α -0.0558 -0.1569 α

2004 - 05 283 650 0.0775 -0.0230 α 0.1780 0.0775 α -0.1550 -0.2555 α

2005 - 06 574 857 0.1570 0.0790 α 0.2350 0.1570 α -0.3140 -0.3920 α

2006 - 07 608 1460 0.1670 -0.0660 α 0.4000 0.1670 α -0.3340 -0.5670 α

2007 - 08 808 2265 0.2200 -0.1800 α 0.6200 0.2200 α -0.4400 -0.8400 α

2008 - 09 937 2078 0.2570 -0.0550 α 0.5690 0.2570 α -0.5140 -0.8260 α

Page 19

123

5.5 INVENTORY TURNOVER RATIO

ITR is defined as the ratio of sales to average inventory with both numerator

and denominator being valued at either selling price or original cost. The success of

any firm basically depends on how efficiently it is controlling its inventories existing

in various forms at different stages of the operations of the firm. Manufacturing firms

need to maintain inventories to accommodate unexpected fluctuations in demand and

supply.

The volume of inventories depends on procurement lead time, the firm’s

purchasing strategies such as taking advantage of price discounts on bulk purchases,

geographical location of suppliers, scarcity of raw materials, expected rise in prices,

the accuracy of demand forecast, extent of subcontracting and service level of the

firm.

By formulating strategic partnership with suppliers, adapting VMI, strategic

sourcing decisions such as make / buy / sub-contracting, developing supplier relations

(shared vision and objectives), tracking of inventory (Ashwani Kumar, 2007),

minimizing inventory record keeping errors (Elgar Fleisch, Christian Tellkamp,2005),

customer relationship management (CRM) and so on, the firms can operate with

minimum levels of inventory.

Page 20

124

A significant number of inventory related issues such as inventory inaccuracy

and its impact on supply chain performance [George M Sheppard & Karen A. Brown

(1993), Elgar Fleisch & Christian Tellkamp (2005)], multi-echelon inventory

management system [A. Alfieri & R. Brandimarte (1997)], inventory capability &

distribution system flexibility [Prashant C. Palvia & D. Lim (2001)], bullwhip effect

[Richard Metters (1997), A. Gunasekaran & E.W.T. Ngai, (2004), Bradley Hull

(2005), Jiuh-Biing Sheu (2005)], expected inventory level and the stock out

probability [Ming Dong & F. Frank Chen (2005)], global inventory visibility [Scott

J.Mason et al., (2003)] and Inventory-Distribution coordination [Douglas J. Thomas

& Paul M. Griffin (1996)], impact of VMI on buyer-supplier relationship in a single

echelon supply chain [A. Mahamani & Dr. K. Prahlada Rao (2010)] have been

analyzed by researchers.

So far, there is no focus of earlier researchers on the effect of ITR on supply

chain performance. ITR is also an important aspect in inventory management which

reflects the performance of a firm and its supply chain.

C. Madhusudhana Rao & Dr. K. Prahlada Rao (2009) carried out a case study

in batteries manufacturing firm (i.e., ARBL) considering ITR as a supply chain

performance measure. The methodology to calculate ITR and analysis of ITR

discussed in this chapter is published in Serbian Journal of Management, an

International Journal for Theory and Practice of Management Science, Volume: 4

Number: 1, in the year 2009.

Page 21

125

Inventory turnover is best thought of as the number of times that an

inventory "turns over" or cycles through the firm in a year. Inventory turnover of 12

means the average inventory moves through the firm once per month. For a number of

years top-class companies have been focusing on SCM for improving their

competitiveness. They were able to demonstrate their success through improved

revenue, profit margins and decreased costs (Peter Bolstorff, 2002).

Lean is a great method to help organize work areas, reduce WIP and speedup

material flow through the entire manufacturing process. Successful lean initiatives

yield lower inventory cost, higher productivity and flexibility and faster response time

to the customer. ITR is an important measure of performance that indicates the

effective utilization of financial resources of the firm.

Inventory for customer use is an expensive investment of company money.

Instead of investing in people, technology or other important assets that can

potentially assist in growing a business faster, companies who invest in inventory

have no Return On Net Assets (RONA) until they sell the inventory.

In many businesses, inventory is turning at the lowest levels in history and

below industry averages. Studies have shown that manufacturers and wholesalers

have over 60 days of inventory and that retailers have over 90 days of inventory

Page 22

126

capital tied up. These times (inventory days) do not include inbound inventory in the

supply chain. Real supply chain inventory is 25% higher.

5.5.1 Various causes for inventory

The following are the causes for accumulation of inventory in any firm and its

supply chain.

(a) Revisions and variance in Supply Chain Management Inputs

(b) Inadequate process norms

(c) Non moving stocks

(d) High lead times & batch quantities

(e) Variance in material receipt

(f) Variance in consumption with actual versus Bill of Material

(g) Design and type changes without valid lead time.

5.5.2 The inventory turnover formula

Inventory turnover is a critical performance metric to assess the effectiveness

of inventory management. Because it is so extensively used as a diagnostic tool, it is

Page 23

127

imperative that inventory turnover be calculated using appropriate and valid

techniques.

Inventory turnover is calculated using the following formula:

ITR = monthspasttheduringinvestmentinventoryAverage

monthspasttheduringsalesstockfromSoldGoodsofCost12

12 ------- (5.9)

Alternately, the firms using Manufacturing Resource Planning (MRP - II)

software are using the following relations also to calculate ITR.

(a) ITR = 12monthcurrentofinventoryEnding

monthcurrentinsalesforsoldgoodsofCost ----------- (5.10)

(b) ITR = 12monthpreviousforinventoryEnding

monthcurrentinsalesforsoldgoodsofCost ----------- (5.11)

When product flow varies throughout the year and inventories expand and

contract during different periods, more frequent measures of the inventory level need

to be taken to generate an accurate measure of the average inventory. The inventory

turnover often is reported as the inventory period, which is the number of days’ worth

of inventory on hand, calculated by dividing the inventory by the average daily cost of

goods sold. This metric not only helps a firm as diagnostic measure but also helps to

improve C2C cycle time of a firm.

Page 24

128

Inventory Period (days) = 365cos

soldgoodsoftAnnual

inventoryAverage ------ (5.12)

The following points kept in mind when calculating turnover ratio:

1. Consider only cost of goods sold from stock sales which are filled from

warehouse inventory. Non-stock items and direct shipments are not included.

2. The cost of goods sold figure in the formula includes transfers of stocked

products to other branches and quantities of these products used for internal

purposes such as repairs and assemblies.

3. Inventory turnover is based on the cost of items (what the company paid for

them) but not sales dollars (what the company sold them for).

Inventory turnover depends on the average value of stocked inventory. To

determine average inventory investment,

1. The total value of every product in inventory is to be calculated (quantity on-

hand times cost) every month, on the same day of the month. One must be

consistent in using the same cost basis (average cost, last cost, replacement

cost, etc.) in calculating both the cost of goods sold and average inventory

investment.

Page 25

129

2. If the company’s inventory levels tend to fluctuate throughout the month, then

it has to calculate the total inventory value on the first and fifteenth of every

month.

3. To determine the average inventory value, a firm has to take average of all

inventory valuations recorded during the past 12 months.

All the above points were considered while collecting data and manipulated as

per the requirements of the present research work.

5.5.3 Turnover goals

1. As a company determines its inventory turnover goals, it should consider the

average gross margin it receives on the sale of products. Most distributors who

have 20% - 30% gross margins should strive to achieve an overall turnover rate of

five to six turns per year. Distributors with lower margins require higher stock

turnover. If the company enjoys high gross margins, it can afford to turn its

inventory less often.

Page 26

130

2. A turnover rate of six turns per year doesn’t mean that the stock of every item will

turn six times. The stock of popular, fast moving items should turn more often (up

to 12 times per year). Slow moving items may turn only once, or not at all.

3. Finally, inventory turnover should be calculated separately for every product line

in every warehouse. This will allow a company to identify situations in which its

inventory is not providing an adequate return on investment. To improve

inventory turnover, a company should consider reducing the quantity it normally

buy from the supplier. Inventory turns improve when a company buys less of

product, more often.

4. Companies have limited funds available to invest in inventory. They cannot

stock a lifetime supply of every item. In order to generate the cash necessary to

pay their bills and return a profit, one must sell the materials they have bought.

The inventory turnover rate measures how quickly the firm is moving inventory

through its warehouse. Combined with other measurements such as customer

service level and return on investment, inventory turnover can provide an accurate

barometer of a company’s success.

Page 27

131

5.6 ANALYSIS OF INVENTORY TURNOVER RATIO

As this performance metric reflects not only the internal operational

performance but also affects the working capital management of a firm, this is more

important performance measure. The companies can benchmark ITR by computing

current ITR value and comparing with that of the companies in the same industry

sector. If benchmark values are not available, a firm can set benchmark levels by

itself basing on earlier performance. As the inventory days depends on ITR, larger

the value of ITR, smaller will be the inventory days and in turn shorter the C2C cycle

time.

5.6.1. ITR calculations of IBD

In the present research work, the ITR of IBD has been analyzed. After finding

the gaps in performance (in terms of ITR), a set of alternatives have been identified to

increase ITR. The courses of action adapted for implementation are furnished below:

(a) Revision of stocking policy of A - class materials so as to maintain stocks for

15 to 20 days of consumption.

(b) Revision of ordering policy for B & C - class items as per lead time and

Economic Order Quantity (EOQ) of purchase department.

Page 28

132

(c) MRP computation as per 1 + 2 months production plan.

(d) To reduce the forecast variance of marketing (Market Research Information).

(e) Information on design and type changes with valid lead time and clear action

to dilute existing stocks.

Implementation of these plans has improved the ITR of industrial battery

division tremendously in the past five years. The data required to calculate ITR is

obtained from sales data and inventory levels of raw materials, work in process and

finished goods including those in transit and available at ware houses / market outlets.

As a part of continuous improvement program, by closely monitoring the ITR, a firm

can continuously improve its capability to rotate money as many times as possible in a

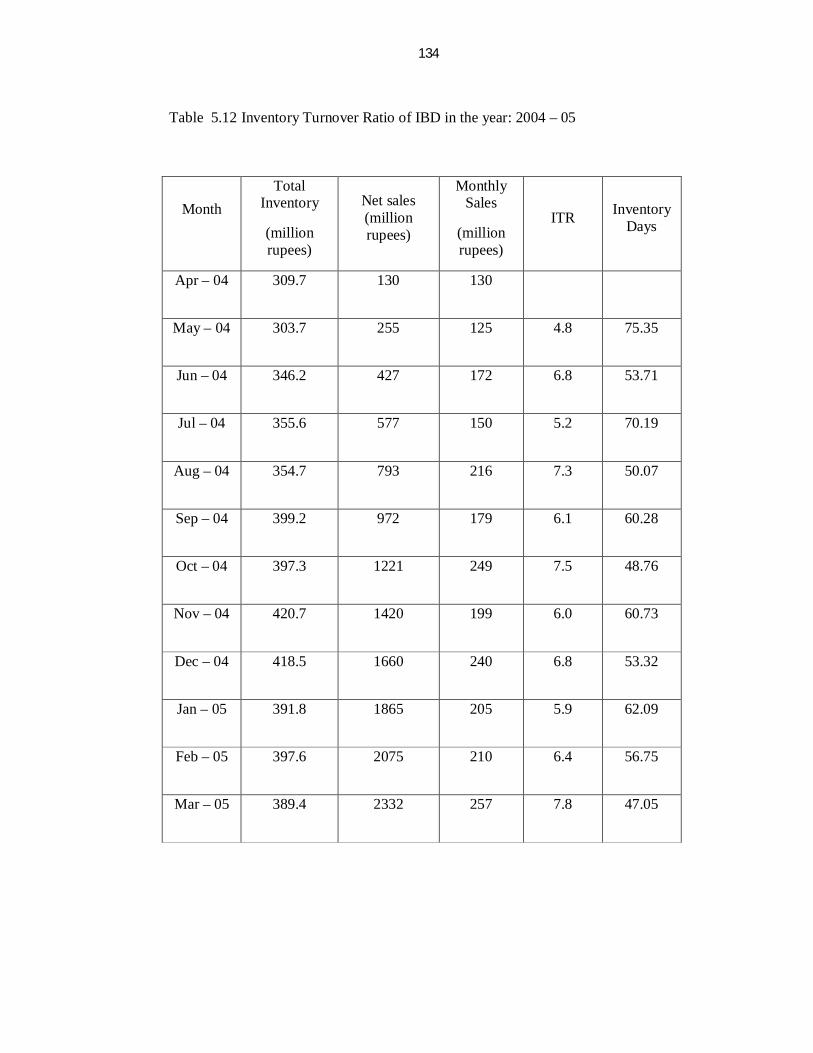

year. Specimen calculation of ITR and inventory days for the month May – 2004 is

given below. The ITR trend of IBD in the past five financial years calculated using

equation (5.11) is furnished in the tables 5.12 to 5.16.

Specimen Calculation:

The Net Sales in the month May – 2004 = 125 Million Rupees

Ending inventory of the month April – 2004 = 309.6 Million Rupees

Inventory Turnover Ratio (ITR) in May - 2004 = 126.309

125

= 4.8

Page 29

133

Inventory Days for the month May – 2004 = ITR365 Days

= 8.4

365

= 75.35 days

Similarly, the ITR and Inventory Days of Supply (IDS) have been calculated

for each month from May – 2004 to March – 2009. The values furnished in tables:

5.11 to 5.15 indicate improved ITR with corresponding decrease in IDS (calculated

using equation 5.12) during that period.

Page 30

134

Table 5.12 Inventory Turnover Ratio of IBD in the year: 2004 – 05

Month Total

Inventory

(million rupees)

Net sales (million rupees)

Monthly Sales

(million rupees)

ITR Inventory Days

Apr – 04 309.7 130 130

May – 04 303.7 255 125 4.8 75.35

Jun – 04 346.2 427 172 6.8 53.71

Jul – 04 355.6 577 150 5.2 70.19

Aug – 04 354.7 793 216 7.3 50.07

Sep – 04 399.2 972 179 6.1 60.28

Oct – 04 397.3 1221 249 7.5 48.76

Nov – 04 420.7 1420 199 6.0 60.73

Dec – 04 418.5 1660 240 6.8 53.32

Jan – 05 391.8 1865 205 5.9 62.09

Feb – 05 397.6 2075 210 6.4 56.75

Mar – 05 389.4 2332 257 7.8 47.05

Page 31

135

Table 5.13 Inventory Turnover Ratio of IBD in the year: 2005 – 06

Month Total

Inventory

(million rupees)

Net sales (million rupees)

Monthly Sales

(million rupees)

ITR Inventory Days

Apr – 05 399.2 210 210 6.5 56.40

May – 05 386.9 459 249 7.5 48.71

Jun – 05 412.5 726 267 8.3 44.08

Jul – 05 429.8 961 235 6.8 53.39

Aug – 05 431.2 1255 294 8.2 44.51

Sep – 05 481.0 1534 279 7.8 47.06

Oct – 05 482.4 1863 329 8.2 44.43

Nov – 05 467.4 2212 349 8.7 42.04

Dec – 05 435.2 2567 355 9.1 40.06

Jan – 06 456.6 2950 383 10.6 34.53

Feb – 06 435.6 3309 359 9.4 38.73

Mar – 06 404.6 3701 392 10.8 33.80

Page 32

136

Table 5.14 Inventory Turnover Ratio of IBD in the year: 2006 – 07

Month Total

Inventory

(million rupees)

Net sales (million rupees)

Monthly Sales

(million rupees)

ITR Inventory Days

Apr – 06 449.0 389 389 11.5 34.43

May – 06 492.3 792 403 10.8 33.89

Jun – 06 519.5 1231 439 10.7 34.11

Jul – 06 560.1 1703 472 10.9 33.48

Aug – 06 654.9 2198 495 10.6 34.42

Sep – 06 690.9 2782 584 10.7 34.11

Oct – 06 727.0 3398 616 10.7 34.11

Nov – 06 655.0 4077 679 11.2 32.57

Dec – 06 626.6 4693 616 11.3 32.34

Jan – 07 605.3 5298 605 11.6 31.50

Feb – 07 557.8 5863 565 11.2 32.59

Mar – 07 471.7 6407 544 11.7 31.19

Page 33

137

Table 5.15 Inventory Turnover Ratio of IBD in the year: 2007 – 08

Month Total

Inventory

(million rupees)

Net sales (million rupees)

Monthly Sales

(million rupees)

ITR Inventory Days

Apr – 07 667.1 528 528 13.4 27.13

May – 07 735.0 1306 778 14.0 26.08

Jun – 07 737.3 2254 948 15.5 23.58

Jul – 07 772.3 3129 875 14.2 25.63

Aug – 07 732.4 4094 965 15.0 24.34

Sep – 07 746.3 4921 827 13.6 26.94

Oct – 07 861.0 5836 915 14.7 24.81

Nov – 07 774.4 6909 1073 15.0 24.41

Dec – 07 798.8 7854 945 14.6 24.92

Jan – 08 983.4 8801 947 14.2 25.66

Feb – 08 853.6 10165 1364 16.6 21.93

Mar – 08 788.6 11247 1082 15.2 24.00

Page 34

138

Table 5.16 Inventory Turnover Ratio of IBD in the year: 2008 – 09

Month Total

Inventory

(million rupees)

Net sales (million rupees)

Monthly Sales

(million rupees)

ITR Inventory Days

Apr – 08 1027.5 1023 1023 15.6 23.40

May – 08 973.9 2148 1125 13.1 27.78

Jun – 08 946.6 3306 1158 14.3 25.58

Jul – 08 914.8 4438 1132 14.3 25.44

Aug – 08 954.4 5621 1183 15.5 23.52

Sep – 08 875.8 6865 1244 15.6 23.34

Oct – 08 941.5 7939 1074 14.7 24.80

Nov – 08 1110.7 9152 1213 15.5 23.61

Dec – 08 1199.4 10585 1433 15.5 23.57

Jan – 09 1148.9 12128 1543 15.4 23.64

Feb – 09 1112.5 13597 1469 15.3 23.79

Mar – 09 1041.5 14934 1337 14.4 25.31

Page 35

139

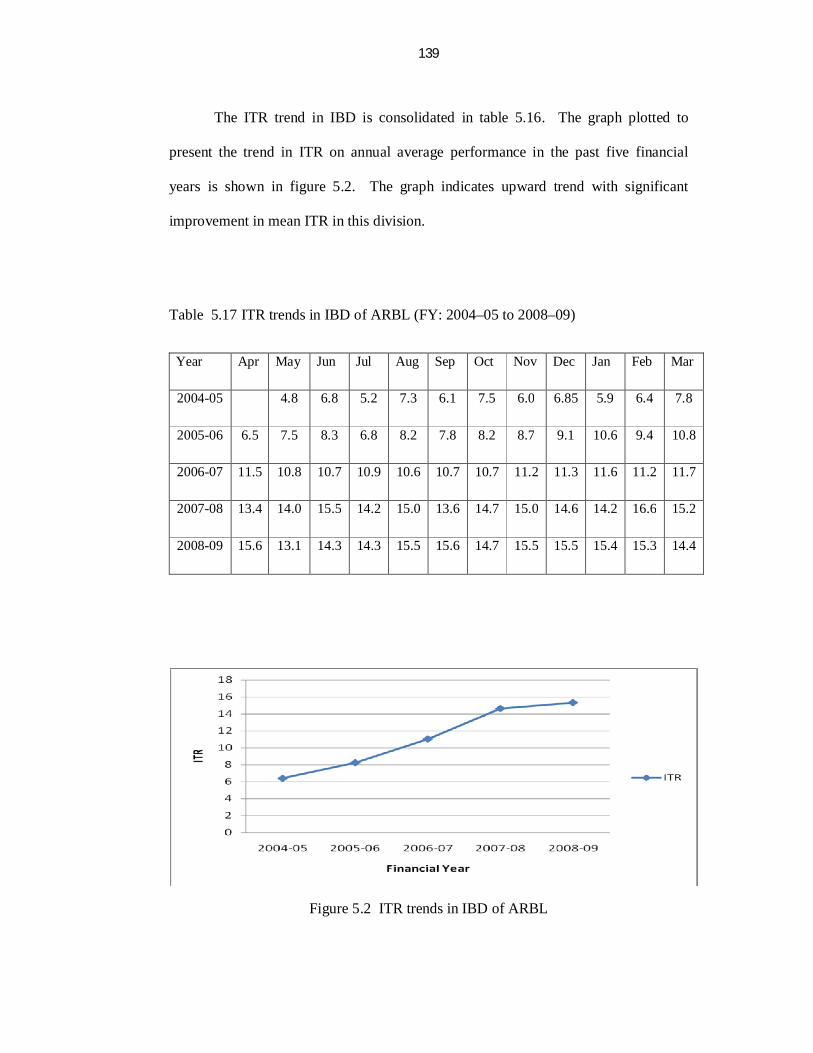

The ITR trend in IBD is consolidated in table 5.16. The graph plotted to

present the trend in ITR on annual average performance in the past five financial

years is shown in figure 5.2. The graph indicates upward trend with significant

improvement in mean ITR in this division.

Table 5.17 ITR trends in IBD of ARBL (FY: 2004–05 to 2008–09)

Year Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

2004-05 4.8 6.8 5.2 7.3 6.1 7.5 6.0 6.85 5.9 6.4 7.8

2005-06 6.5 7.5 8.3 6.8 8.2 7.8 8.2 8.7 9.1 10.6 9.4 10.8

2006-07 11.5 10.8 10.7 10.9 10.6 10.7 10.7 11.2 11.3 11.6 11.2 11.7

2007-08 13.4 14.0 15.5 14.2 15.0 13.6 14.7 15.0 14.6 14.2 16.6 15.2

2008-09 15.6 13.1 14.3 14.3 15.5 15.6 14.7 15.5 15.5 15.4 15.3 14.4

Figure 5.2 ITR trends in IBD of ARBL

Page 36

140

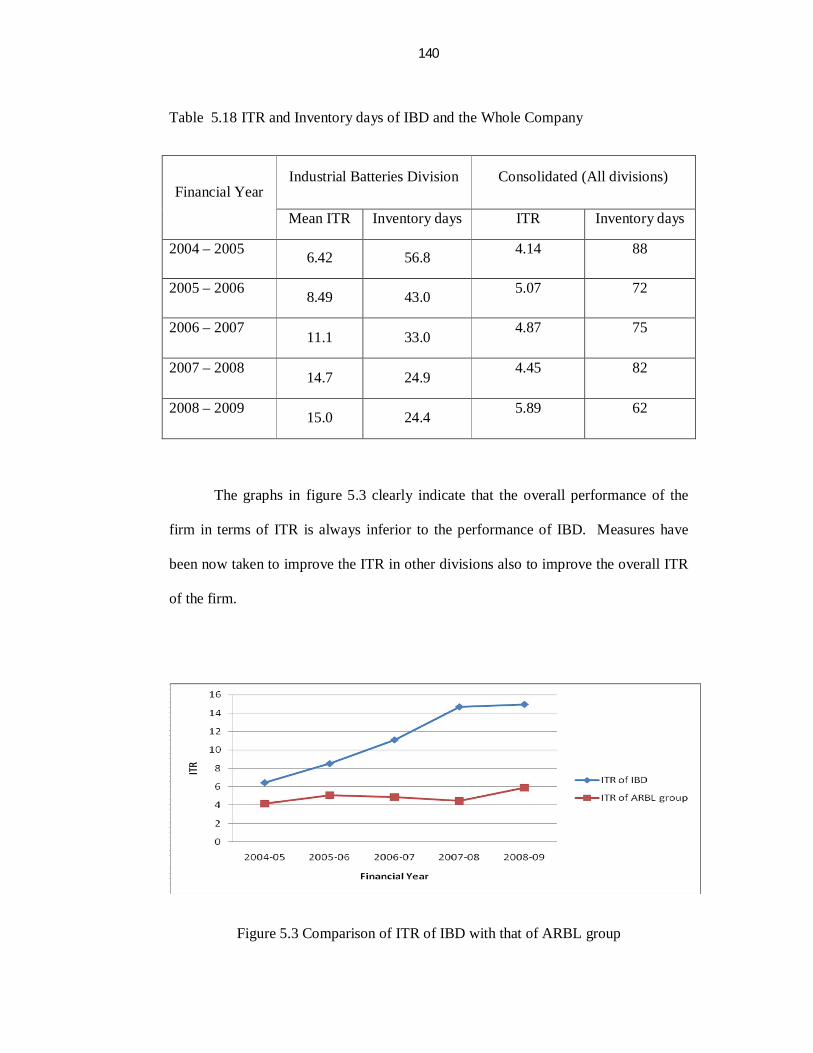

Table 5.18 ITR and Inventory days of IBD and the Whole Company

Financial Year Industrial Batteries Division Consolidated (All divisions)

Mean ITR Inventory days ITR Inventory days

2004 – 2005 6.42 56.8 4.14 88

2005 – 2006 8.49 43.0 5.07 72

2006 – 2007 11.1 33.0

4.87 75

2007 – 2008 14.7 24.9

4.45 82

2008 – 2009 15.0 24.4 5.89 62

The graphs in figure 5.3 clearly indicate that the overall performance of the

firm in terms of ITR is always inferior to the performance of IBD. Measures have

been now taken to improve the ITR in other divisions also to improve the overall ITR

of the firm.

Figure 5.3 Comparison of ITR of IBD with that of ARBL group

Page 37

141

The results of analysis indicate clearly that the benefit of improving ITR or

decreasing inventory days is two fold: Firstly, the working capital management will

be more effective. Secondly, the C2C cycle time will be improved which leads to

lesser penalty to all parties along the supply chain and better buyer-supplier

relationships along the value chain.

5.7 SUMMARY

In this chapter, the attempt is to develop LPP model to find optimal payment

and collection periods that would minimize penalty to all the entities i.e., suppliers,

firm and customers. The data collected from financial reports of ARBL is analyzed

and optimal payment and collection periods associated with minimal penalty have

been found in each case. The results of analysis strongly support that the penalty will

be less when payment period and diferral periods are short which in turn will lead to

shorter C2C cycle time. Also, this analysis helps firms in benchmarking payment and

collection periods at supplier and customer ends for the benefit of all the firms along

the supply chain in an integrated approach. The analysis of ITR also strongly support

that improved ITR will help firms in optimizing their inventory management and at

the same time, the small the inventory days shorter will be the C2C cycle time.

Hence, it is essential for firms in an integrated supply chain management to focus on

improved ITR through inventory visibility and collaborative planning forecasting and

replenishment that helps all the firms along the supply chain.