22

conjunctural survey of italian firms quarterly survey of the business tendency of italian firms and their relationships with banks presentation leaflet rome, january 2015 (13212fo)

| Date post: | 30-Jul-2015 |

| Category: |

Documents |

| Upload: | formatresearch |

| View: | 40 times |

| Download: | 2 times |

conjunctural survey of italian firmsquarterly survey of the business tendency of italian firms and their relationships with banks

presentation leaflet

rome, january 2015 (13212fo)

2

agenda survey's architecture

investigated phenomena

research perimeter

network of phenomena

methods

output

timing

quality plan

buying solutions

rights and code of conduct

references

3

• Format's Conjunctural Survey of Italian Firms represents a multiclient

research service, realized quarterly by Format Research since 2008.

• The survey analyzes the business tendency of Italian firms with

respect to a set of major indicators: their climate of trust, the financial

requirements, the demand for credit, etc., investigated on the basis

of the firms' structural characteristics (area, sector, size, etc.) and

their relationships with banks (use of banks, Brands, etc.)

• The study relies on a representative sample of Italian firms, whose

viewpoints are investigated by means of a structured interview /

questionnaire (CATI / CAWI1), aiming at measuring observed trends in

the considered quarter, and forecasted trends in the following quarter.

survey's architecture |

1 CATI: Computer Assisted Telephone Interview; CAWI: Computer Assisted Web Interview.

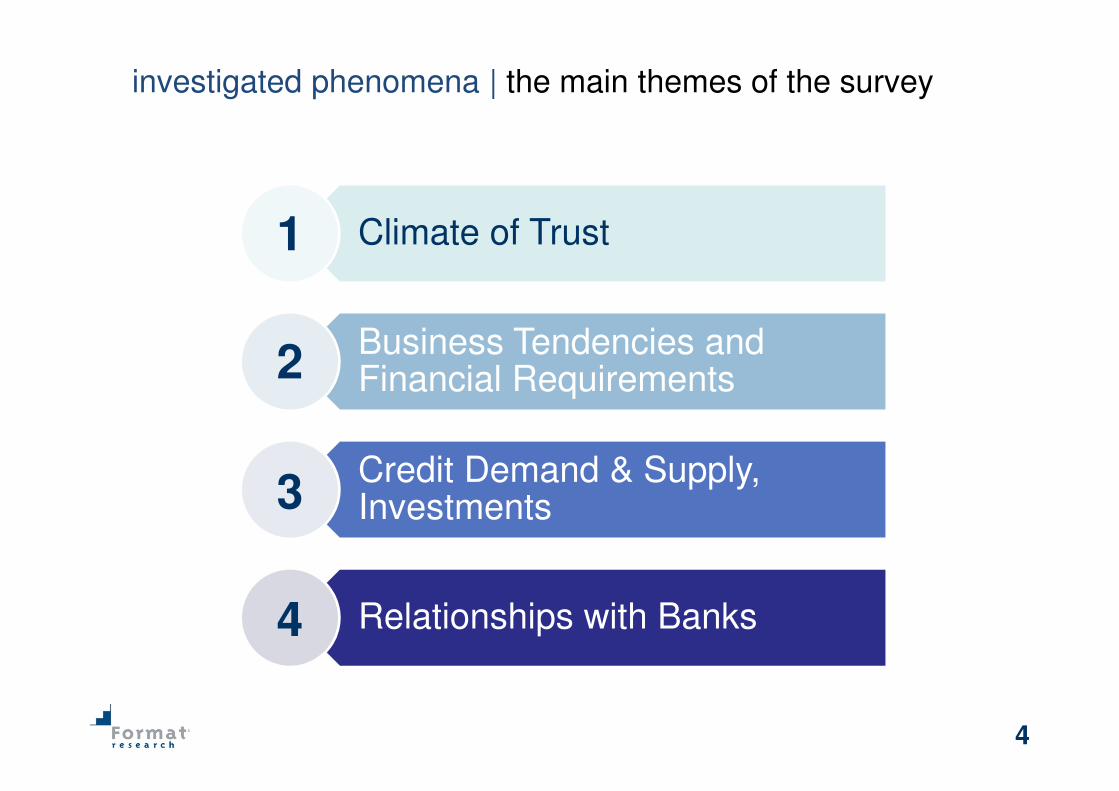

4

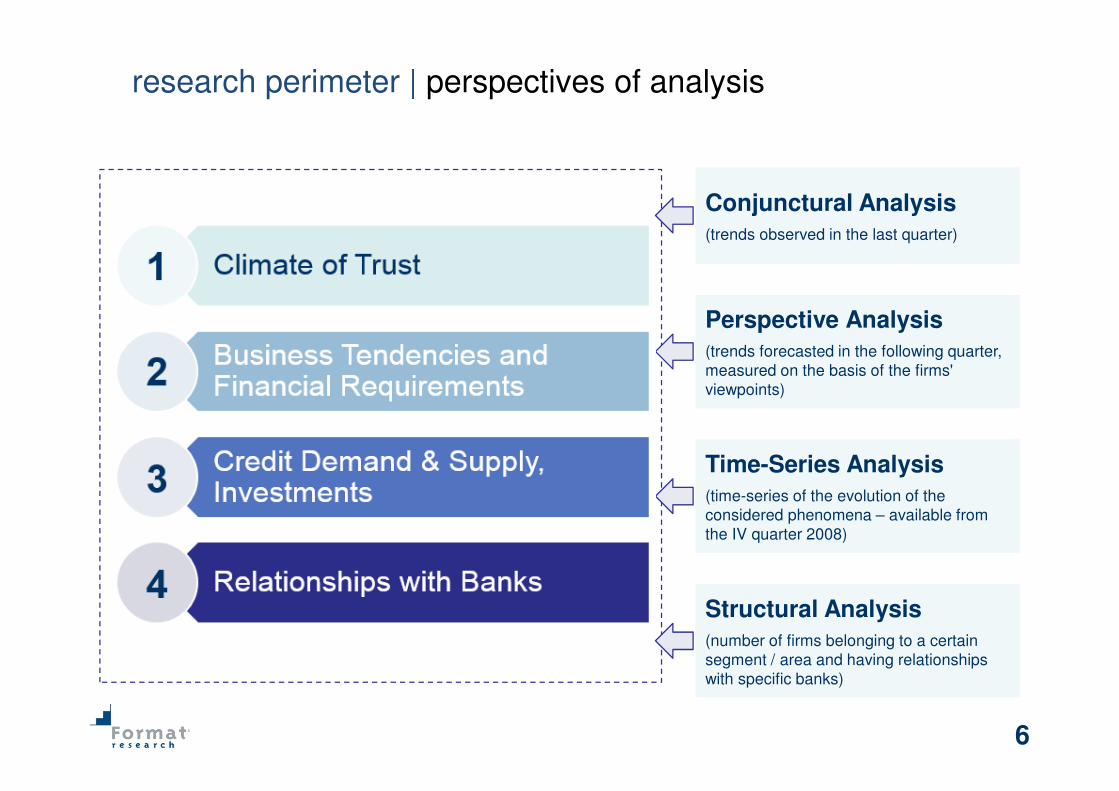

Climate of Trust

Business Tendencies and Financial Requirements

Credit Demand & Supply, Investments

Relationships with Banks

1

2

3

4

investigated phenomena | the main themes of the survey

5

Small Business(firms with a turnover up to €2.5 million)

- Size- Economic Sector- Area (Residence)

Small Business(firms with a turnover up to €2.5 million)

- Size- Economic Sector- Area (Residence)

Enterprises(firms with a turnover over €2.5 million)

- Size- Economic Sector- Area (Residence)

Enterprises(firms with a turnover over €2.5 million)

- Size- Economic Sector- Area (Residence)

Format's segmentation of firms is carried out according to different parameters (area, size, turnover up to / over €2.5million, etc.). Other types of segmentation can be requested and / or customized on the Client's demand and with no

additional charge, e.g. turnover up to / over €5 million, etc.

Format's segmentation of firms is carried out according to different parameters (area, size, turnover up to / over €2.5million, etc.). Other types of segmentation can be requested and / or customized on the Client's demand and with no

additional charge, e.g. turnover up to / over €5 million, etc.

research perimeter | domains and levels of analysis

6

Conjunctural Analysis(trends observed in the last quarter)

Conjunctural Analysis(trends observed in the last quarter)

research perimeter | perspectives of analysis

Perspective Analysis(trends forecasted in the following quarter,

measured on the basis of the firms'

viewpoints)

Perspective Analysis(trends forecasted in the following quarter,

measured on the basis of the firms'

viewpoints)

Time-Series Analysis(time-series of the evolution of the

considered phenomena – available from

the IV quarter 2008)

Time-Series Analysis(time-series of the evolution of the

considered phenomena – available from

the IV quarter 2008)

Structural Analysis(number of firms belonging to a certain

segment / area and having relationships

with specific banks)

Structural Analysis(number of firms belonging to a certain

segment / area and having relationships

with specific banks)

7

network of phenomena | business tendencies

Determinants of business tendencies as reported by the interviewed firms, with respect to the following domains:

- ...the estimation of

investments

- …the anticipation of the

cycle

- …the demand for credit

(loans / credit lines).

CLIMATE OF TRUST

� The country's economic situation

� The business tendencies of firms

FINANCIAL TRENDS AND REQUIREMENTS

� Profit

� Employment

� Delays in payments

� Vendor prices

� Financial requirements (ability to cope with

duties towards suppliers, employees, the

Government, banks, etc.)

8

network of phenomena | the credit market

� THE DEMAND FOR CREDIT.

Quarterly amount of firms

applying for a bank loan, a

credit line, or the refinancing

of existing loans / credit lines.

� CREDIT APPLICATION

OUTCOMES: accepted,

partially accepted (with

smaller amount than

expected), rejected, under

examination.

� Cash

� Investments

� Debt restructuring

MERIT OF CREDIT. Synthetic

indicator of the business size

and commercial reliability of

firms, obtained by the

combination of two different

indexes: Rating (class of merit),

and Failure Score (predictive

indicator of business

insolvencies). It allows

estimating the firm's reliability

and its technical ability to cope

with financial commitments

(varying from 0 to 100).

Merit of Credit data do not derive from interviews' results but from pre-existing databases, with no additional charge to the Client.

Source:

FIRMS NOT APPLYING FOR

CREDIT. Firms having own

resources, ... with previous

successful applications, ...

fearing rejection of a loan

request, ...turning to other

financial operators.

REASONS FOR GIVING UP

TO ECONOMIC GROWTH

PROGRAMS. Reasons for

firms to give up to investments

or favourable business

activities in the last three

months: low trust in the

economic situation, ...lack of

resources, ...need for credit.

THE DEMAND FOR

CREDIT

REASONS FOR

REQUESTING

CREDIT

MERIT OF CREDIT

9

network of phenomena | the credit market …existing loans:

qualitative data, consistencies from the bank of italy

MARKET SHARESSEGMENTATION

FOR SINGLE BANKS

SEGMENTATION

FOR TECHNICAL

FORM OF LOANS

THE VIEWPOINT OF

FIRMS ON CREDIT

CONDITIONS

Market shares of firms applying for bank credit, segmented according to structural characteristics: size, sector, turnover, etc.

Segmentation of firms' market shares according to the banks used (Brands), and existing loans.

N.B: Market shares are not relevant to the value of loans (i.e. consistencies) but the amount (%) of firms currently holding a loan / credit line.

Segmentation of market shares for technical form of existing loans:

- financing and credits to return within the financial year;

- middle / long term financings.

Market shares data do not derive from interviews' results but from firms' balance sheets, with no additional charge to the Client.

Source:

The amount of loans expressed in consistencies will be however provided in the final research report (with no additional charge), with segmentation for structural characteristics of firms (economic sector, size, area, etc.) and Italian province, providing QUARTERLY AND MONTHLY TIME-SERIES.

Tendency of interest rates as reported by the firms.

Tendency of "other costs and conditions" relevant to loans / credit lines (e.g. commitment fees, bank inquiry, etc.) as reported by the firms.

Tendency of the "length of credit history" as reported by the firms.

Tendency of "requested guarantees" to cover financings and loans, as reported by the firms.

Tendency of the cost of bank services (e.g. accounting, dispositions, payments, etc.) as reported by the firms.

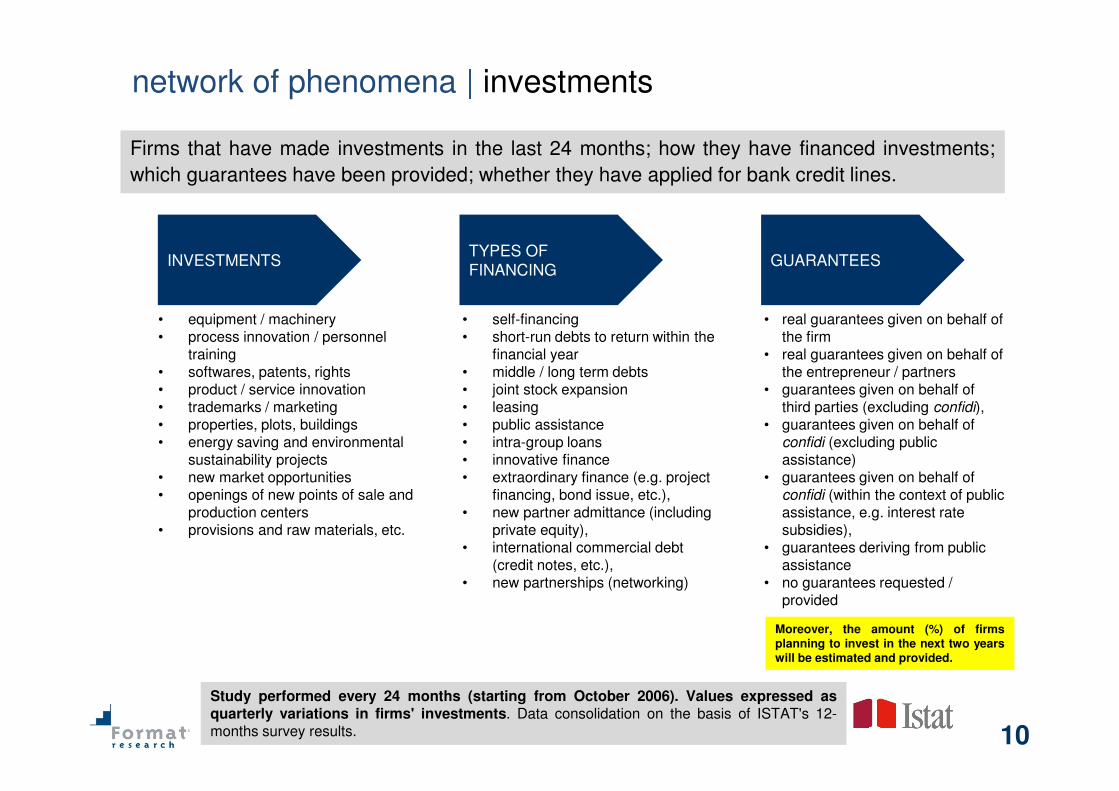

10

network of phenomena | investments

INVESTMENTSTYPES OF

FINANCING GUARANTEES

• equipment / machinery • process innovation / personnel

training• softwares, patents, rights• product / service innovation• trademarks / marketing • properties, plots, buildings • energy saving and environmental

sustainability projects• new market opportunities• openings of new points of sale and

production centers• provisions and raw materials, etc.

• self-financing• short-run debts to return within the

financial year• middle / long term debts• joint stock expansion• leasing• public assistance• intra-group loans • innovative finance• extraordinary finance (e.g. project

financing, bond issue, etc.), • new partner admittance (including

private equity), • international commercial debt

(credit notes, etc.), • new partnerships (networking)

• real guarantees given on behalf of the firm

• real guarantees given on behalf of the entrepreneur / partners

• guarantees given on behalf of third parties (excluding confidi),

• guarantees given on behalf of confidi (excluding public assistance)

• guarantees given on behalf of confidi (within the context of public assistance, e.g. interest rate subsidies),

• guarantees deriving from public assistance

• no guarantees requested / provided

Firms that have made investments in the last 24 months; how they have financed investments;

which guarantees have been provided; whether they have applied for bank credit lines.

Study performed every 24 months (starting from October 2006). Values expressed asquarterly variations in firms' investments. Data consolidation on the basis of ISTAT's 12-months survey results.

Moreover, the amount (%) of firmsplanning to invest in the next two yearswill be estimated and provided.

11

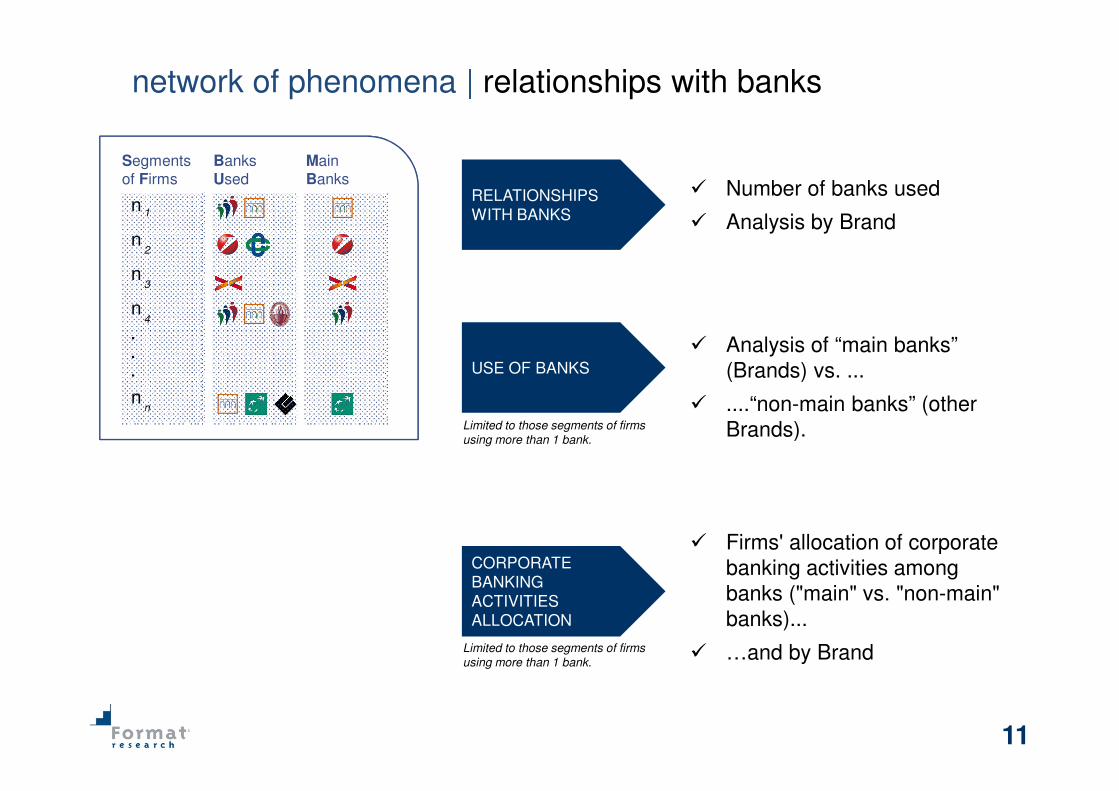

network of phenomena | relationships with banks

Segments of Firms

n 1

n

n

n

2

3

4

nn

.

.

.

BanksUsed

Main Banks

RELATIONSHIPS

WITH BANKS

� Number of banks used

� Analysis by Brand

� Analysis of “main banks”

(Brands) vs. ...

� ....“non-main banks” (other

Brands).

USE OF BANKS

Limited to those segments of firms

using more than 1 bank.

� Firms' allocation of corporate

banking activities among

banks ("main" vs. "non-main"

banks)...

� …and by Brand

CORPORATE

BANKING

ACTIVITIES

ALLOCATION

Limited to those segments of firms

using more than 1 bank.

12

CLUSTER 3East Europe (non-UE)

CLUSTER 2Asia (Japan)Asia (China) Asia (Australia and New Zealand) Asia (other)

CLUSTER 4Middle East

CLUSTER 1North America (USA and Canada)

CLUSTER 5South America (Mexico)South America (Brazil) South America (Other)

CLUSTER “UE”Other UE countries

network of phenomena | customization… focus on the

internationalization of firms

In-depth analyses are available on request, e.g. regarding the internationalization of firms. In this case, an oversampling of

manufacturing firms would be provided, particularly those with more than 9 employees and turnover higher than €2,5 million,

segmented by export destination country. Such analyses are targeted to six different clusters (one relevant to UE countries vs. 5

relevant to Extra UE countries). For each cluster, “Share-of-Wallet” studies are also available, i.e. analyses of banks

serving Italian firms that operate abroad.

13

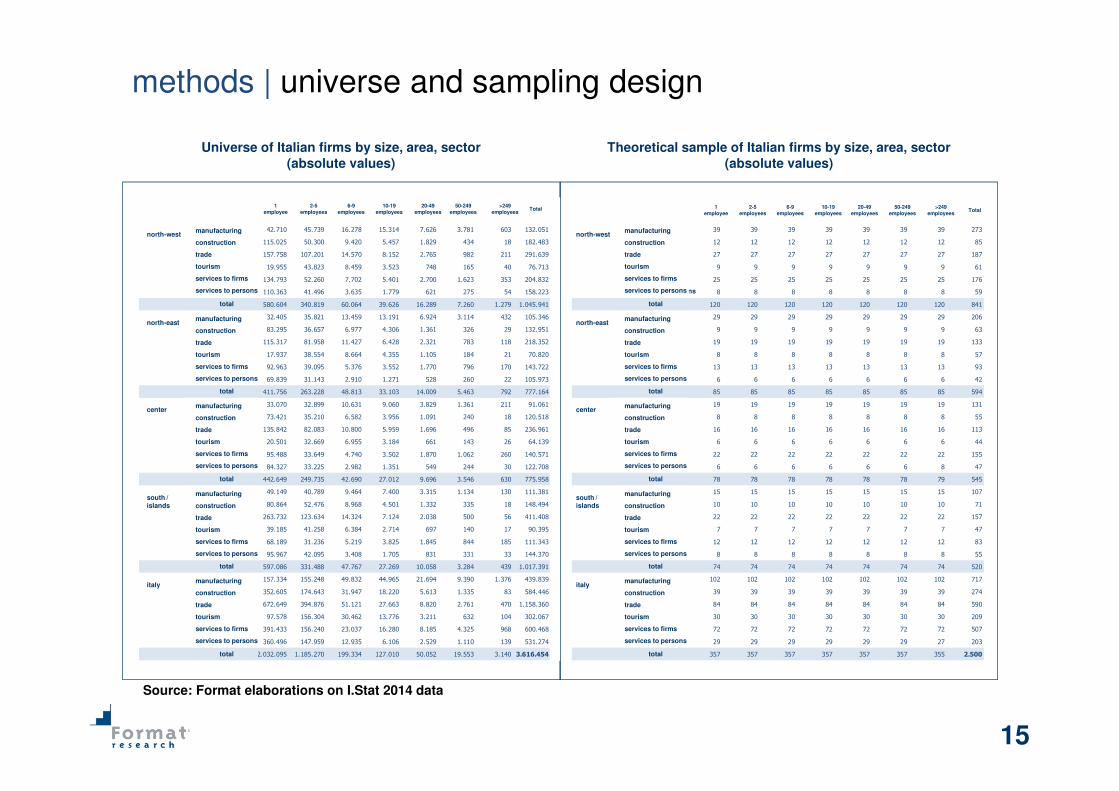

methods | technical characteristics

Sample

Representative sample of Italian firms, excluding agriculture and finance. Sample: 2,500 interviews perquarter (10,000 interviews per year). Confidence interval: 0,95. Error: +2,1%. Sample expansion is availableon request, up to 8,000 cases per quarter (32,000 per year) with regional representativity.

Area

Sample representative of the following Italian geographical areas: North-West, North-East, Center,South/Islands. Regional representativity is available on request (19 regions and 2 autonomous provinces).

Sectors

Sample representative of the following sectors: Manufacturing, Construction, Trade, Tourism (reclassificationof different ATECO 2007 / NACE clusters), Services to Firms, Services to Persons.

Size

Sample representative of the following dimensional classes: Number of employees (Micro, 1-9 employees;Small, 10-49 employees; Medium, 50-249 employees; Big, >249 employees); Turnover (Small Business,<€2.5 million turnover; Enterprise, >€2.5 million turnover).

Contact and Data Collection Methods

Data Collection Technique: CATI (Computer Assisted Telephone Interview), and CAWI (Computer AssistedWeb Interview) structured interviews / questionnaires; CAWI is default at medium and big firms.Target person: entrepreneur or any person holding a position of responsibility within the firm (Director,Executive, Senior Manager, etc.).

Methodological paper available on requestMethodological paper available on request

14

SUBSECTOR ATECO 2007 N % SECTOR

Agriculture, Forestry and Fishing A 1.620.884 26,9 AGRICULTURE EXCLUDED

Mining and Quarrying B 2.493 0,0 MANUFACTORING

Manufactoring C 422.067 7,0 MANUFACTORING

Electricity, Gas, Steam and Air Conditioning Supply D 6.535 0,1 MANUFACTORING

Water Supply, Sewage, Waste Management and Remediation E 8.744 0,1 MANUFACTORING

Construction F 584.446 9,7 CONSTRUCTIONS

Wholesale and Retail Trade G 1.158.360 19,2 TRADE

Transportation and Storage H 132.768 2,2 SERVICES TO FIRMS

Tourism I 302.067 5,0 TOURISM

Information and Communication J 96.265 1,6 SERVICES TO FIRMS

Financial and Insurance Activities K 90.805 1,5 SERVICES TO FIRMS EXCLUDED

Real Estate Activities L 227.882 3,8 SERVICES TO FIRMS

Professional, Scientific and Technical Activities M 693.770 11,5 SERVICES TO FIRMS EXCLUDED

Administrative and Support Service Activities N 143.553 2,4 SERVICES TO FIRMS

Education P 24.825 0,4 SERVICES TO PERSONS

Human Health and Social Work Activities Q 246.770 4,1 SERVICES TO PERSONS

Arts, Entertainment and Recreation R 61.527 1,0 SERVICES TO PERSONS

Other Service Activities S 198.152 3,3 SERVICES TO PERSONS

TOTAL (comprised of excluded sectors) 6.021.913 100,0

TOTAL (utilized for the survey)* 3.616.454 60,1

methods | universe

Source: Format elaborations on I.Stat 2014 data

“TOTAL UTILIZED FOR THE SURVEY” represents Format's major sampling classification, i.e. representative sampling of Italian firms excluding those

operating in the following sectors: Finance and Insurance, Agriculture, Forestry and Fishing; Professional, Scientific, and Technical Activities.

15

Theoretical sample of Italian firms by size, area, sector(absolute values)

Source: Format elaborations on I.Stat 2014 data

Universe of Italian firms by size, area, sector(absolute values)

methods | universe and sampling design

1

addetto

2-5

addetti

6-9

addetti

10-19

addetti

20-49

addetti

50-249

addetti

> 249

addettiTotale

1

addetto

2-5

addetti

6-9

addetti

10-19

addetti

20-49

addetti

50-249

addetti

> 249

addettiTotale

nord ovest manifattura 42.710 45.739 16.278 15.314 7.626 3.781 603 132.051 nord ovest manifattura 39 39 39 39 39 39 39 273

costruzioni 115.025 50.300 9.420 5.457 1.829 434 18 182.483 costruzioni 12 12 12 12 12 12 12 85

commercio 157.758 107.201 14.570 8.152 2.765 982 211 291.639 commercio 27 27 27 27 27 27 27 187

turismo 19.955 43.823 8.459 3.523 748 165 40 76.713 turismo 9 9 9 9 9 9 9 61

servizi alle imprese 134.793 52.260 7.702 5.401 2.700 1.623 353 204.832 servizi alle imprese 25 25 25 25 25 25 25 176

servizi alle persone 110.363 41.496 3.635 1.779 621 275 54 158.223 servizi alle persone 8 8 8 8 8 8 8 59

totale 580.604 340.819 60.064 39.626 16.289 7.260 1.279 1.045.941 totale 120 120 120 120 120 120 120 841

nord est manifattura 32.405 35.821 13.459 13.191 6.924 3.114 432 105.346 nord est manifattura 29 29 29 29 29 29 29 206

costruzioni 83.295 36.657 6.977 4.306 1.361 326 29 132.951 costruzioni 9 9 9 9 9 9 9 63

commercio 115.317 81.958 11.427 6.428 2.321 783 118 218.352 commercio 19 19 19 19 19 19 19 133

turismo 17.937 38.554 8.664 4.355 1.105 184 21 70.820 turismo 8 8 8 8 8 8 8 57

servizi alle imprese 92.963 39.095 5.376 3.552 1.770 796 170 143.722 servizi alle imprese 13 13 13 13 13 13 13 93

servizi alle persone 69.839 31.143 2.910 1.271 528 260 22 105.973 servizi alle persone 6 6 6 6 6 6 6 42

totale 411.756 263.228 48.813 33.103 14.009 5.463 792 777.164 totale 85 85 85 85 85 85 85 594

centro manifattura 33.070 32.899 10.631 9.060 3.829 1.361 211 91.061 centro manifattura 19 19 19 19 19 19 19 131

costruzioni 73.421 35.210 6.582 3.956 1.091 240 18 120.518 costruzioni 8 8 8 8 8 8 8 55

commercio 135.842 82.083 10.800 5.959 1.696 496 85 236.961 commercio 16 16 16 16 16 16 16 113

turismo 20.501 32.669 6.955 3.184 661 143 26 64.139 turismo 6 6 6 6 6 6 6 44

servizi alle imprese 95.488 33.649 4.740 3.502 1.870 1.062 260 140.571 servizi alle imprese 22 22 22 22 22 22 22 155

servizi alle persone 84.327 33.225 2.982 1.351 549 244 30 122.708 servizi alle persone 6 6 6 6 6 6 8 47

totale 442.649 249.735 42.690 27.012 9.696 3.546 630 775.958 totale 78 78 78 78 78 78 79 545

sud e isole manifattura 49.149 40.789 9.464 7.400 3.315 1.134 130 111.381 sud e isole manifattura 15 15 15 15 15 15 15 107

costruzioni 80.864 52.476 8.968 4.501 1.332 335 18 148.494 costruzioni 10 10 10 10 10 10 10 71

commercio 263.732 123.634 14.324 7.124 2.038 500 56 411.408 commercio 22 22 22 22 22 22 22 157

turismo 39.185 41.258 6.384 2.714 697 140 17 90.395 turismo 7 7 7 7 7 7 7 47

servizi alle imprese 68.189 31.236 5.219 3.825 1.845 844 185 111.343 servizi alle imprese 12 12 12 12 12 12 12 83

servizi alle persone 95.967 42.095 3.408 1.705 831 331 33 144.370 servizi alle persone 8 8 8 8 8 8 8 55

totale 597.086 331.488 47.767 27.269 10.058 3.284 439 1.017.391 totale 74 74 74 74 74 74 74 520

italia manifattura 157.334 155.248 49.832 44.965 21.694 9.390 1.376 439.839 italia manifattura 102 102 102 102 102 102 102 717

costruzioni 352.605 174.643 31.947 18.220 5.613 1.335 83 584.446 costruzioni 39 39 39 39 39 39 39 274

commercio 672.649 394.876 51.121 27.663 8.820 2.761 470 1.158.360 commercio 84 84 84 84 84 84 84 590

turismo 97.578 156.304 30.462 13.776 3.211 632 104 302.067 turismo 30 30 30 30 30 30 30 209

servizi alle imprese 391.433 156.240 23.037 16.280 8.185 4.325 968 600.468 servizi alle imprese 72 72 72 72 72 72 72 507

servizi alle persone 360.496 147.959 12.935 6.106 2.529 1.110 139 531.274 servizi alle persone 29 29 29 29 29 29 27 203

totale 2.032.095 1.185.270 199.334 127.010 50.052 19.553 3.140 3.616.454 totale 357 357 357 357 357 357 355 2.500

north-west manufacturing

construction

trade

tourism

services to firms

services to persons

north-eastmanufacturing

construction

trade

tourism

services to firms

services to persons

north-westmanufacturing

construction

trade

tourism

services to firms

services to persons

centermanufacturing

construction

trade

tourism

services to firms

services to persons

south /islands

manufacturing

construction

trade

tourism

services to firms

services to persons

italymanufacturing

construction

trade

tourism

services to firms

services to persons

total

total

total

total

total

north-eastmanufacturing

construction

trade

tourism

services to firms

services to persons

north-westmanufacturing

construction

trade

tourism

services to firms

services to persons

centermanufacturing

construction

trade

tourism

services to firms

services to persons

south /islands

manufacturing

construction

trade

tourism

services to firms

services to persons

italymanufacturing

construction

trade

tourism

services to firms

services to persons

total

total

total

total

total

1employee

2-5employees

6-9employees

10-19employees

20-49employees

50-249employees

>249employees

Total 1employee

2-5employees

6-9employees

10-19employees

20-49employees

50-249employees

>249employees

Total

16

..........

Manufacturing

North-West

Enterprise (>€2.5 million turnover)

Small business

Variations estimated on the basis of the previous year.

output | representation of phenomena

0,0

10,0

20,0

30,0

40,0

50,0

60,0

70,0

80,0

90,0

100,0

III IV 13 II III IV 14 II III IV 15 II III IV

contrazione

espansione

REPRESENTATION OF RESULTS: FREQUENCY DISTRIBUTIONS (%)AND SYNTHETIC INDICATORS

Brand Secondary Bank Number of banksMain Bank

percentuali indicatore

periodo migliore uguale peggiore saldo

2013 I I 0,3 54,5 45,2 27,6

2013 I I I 0,2 53,5 46,3 27,0

2013 I V 0,3 51,0 48,7 25,8

2014 I 0,3 53,0 46,7 26,8

2014 I I 1,0 52,0 47,0 27,0

2014 I I I 1,5 53,0 45,5 28,0

improved unchanged worsenedquarter indicator

expansion

crunch

17,1 15,6 13,2 12,9 12,5 13,0 15,6 17,8 18,8

III IV 13 II III IV 14 II III

"Hanno chiesto un fido, o la rinegoziazione di un fido esistente, nei trimestri" (% di imprese)

0,0

10,0

20,0

30,0

40,0

50,0

60,0

70,0

80,0

90,0

100,0

III IV 13 II III IV 14 II III

Percentuali di imprese che hanno chiesto un credito al sistema bancario nel terzo trimestre 2014

45,4

15,0

25,6

11,0 3,0

Accolta Accolta (inferiore) Non accolta In attesa (non farà richiesta prox

trim)

In attesa (farà richiesta prox

trim)

"Esiti delle richieste delle imprese che hanno chiesto un fido, o la rinegoziazione di un fido esistente, nel trimestre" (% di imprese)

Irrigidimento

Stabilità e/o allentamento

45,4

40,6

44,0

39,4

Percentages of firms that have applied for a bank loan / credit line in the 3rd quarter of 2014

Firms that have applied for an overdraft or the refinancing of an existing overdraft in the quarters (%)

Credit application outcomes 3rd quarter of 2014 (percentages of firms)

Approved Partially approved (smaller amount than

requested)

Rejected Under examination (not applying next quarter)

Under examination

(applying next quarter)

17

output | materials

apr | DB

RResearch Report I quarter Database (Macrodata)

mayU

| Newsletter (Updates)

jun |

jul | DB

RResearch Report II quarter Database (Macrodata)

augU

| Newsletter (Updates)

sep |

DBoct |R

Research Report III quarter Database (Macrodata)

novU

|

dec |

janU

|

feb DB|R

Research Report IV quarter Database (Macrodata)

mar |

Newsletter (Updates)

Newsletter (Updates)

18

January February March April

May June July August

September October November December

Data Collection and Analysis

Quarterly Report(about the 15th of each indicated release month)

Newsletter – Updates(about the 15th of each indicated release month)

timing | release calendar

19

Quality audit of the services provided will be guaranteed by means of specific project cycle management

procedures and preliminary identification of management responsibilities. Periodic checks and

assessments will allow continuous monitoring of the state of the project and relevant activities, their

compliance with organizational, logistical, time, and quality standards with respect to the expected product

and the program shared with the Client. In case of proven non-compliance, in agreement with the Client,

major determinants will be investigated, and subsequently valid corrective actions will be systematically

implemented. The approach offered by our institute is either simple and structured, as it focuses on eight

priority objectives that are consistent to the ISO9001 certification:

quality plan |

Garantire la sicurezza e la riservatezza

Accurate procedure interne per la sicurezza fisica e logica dei dati e dei deliverable

Garantire la continuità

Corretta allocazione e gestione delle risorse durante la realizzazione del progetto e costante trasferimento del know how

Verificare la soddisfazione del cliente

Monitoraggio periodico dei livelli di soddisfazione del cliente mediante l’utilizzo di strumenti standard (es. Questionari, interviste, …)

Assicurare la qualità dei deliverables

Analisi e revisione della documentazione prodotta a più livelli (es. Responsabile di progetto, Consulenti senior)

Pianificare il progetto

Pianificazione di dettaglio di attività, risorse, tempo, milestones, deliverables

Monitorare l’andamento del progetto

Indicatori quantitativi di performance sulle attivitàsvolte (es. APQ rilevati)

Consuntivare i risultati

Schede di avanzamento lavoro standard per tutta la durata del progetto

Comunicare e condividere i risultati

Riunioni di lavoro ed utilizzo di strumenti informatici per la condivisione dello stato del progetto e della base informativa disponibile

Piano della qualità

1

2

3

45

6

7

8

Ensuring Safety and Confidentiality

Accurate internal procedures aimed at ensuring

physical and logical protection of data and

deliverables

Ensuring Continuity

Allocation and management of resources

over the whole project execution and

constant know-how transfer

Customer Satisfaction

Periodical customer satisfaction analyses

by means of standardized tools

(questionnaires, interviews, ...)

Project Management

Detailed planning of activities, resources,

time, milestones, deliverables

Project Monitoring

Estimation of quantitative activity

performance indicators (e.g. APQ)

Preliminary Results Exploration

Production of reports on the state-of-the-

project over the whole project execution

Sharing of Final Results

Live and remote sharing of final results

and the available information base

by means of meetings and electronic tools

QualityPlan

QUALITY PLAN – PRIORITIES

Quality Assessment of Deliverables

Multi-level assessment and review of

deliverables (by Project Leaders, Senior

Consultants, etc.)

20

rights and ethical code |

RIGHTS

All rights of the Conjunctural Survey of Italian Firms are the property of FormatSrl - ricerche di mercato. It is explicitly prohibited to disclose it to third partiesfor commercial purposes. All the results of the customizations are the propertyof the Client.

ETHICAL CODE

The survey is conducted in respect of the following rules:

� ICC/ESOMAR Code on Market and Social Research

� ASSIRM Code

� Code of the SIS (Italian Statistical Society)

� Italian Law on Privacy D.lgs 196/03

21

Emanuele FinoAccount Researcher

Tel: +39 06 86328681

Email: [email protected]

Scientific

Director

Info

Pierluigi Ascani

Chairman of the Board of Directors

Philosopher. Founder, President and Scientific Director of Format

Research since 1992. Twenty-year experience in marketing research,

customer satisfaction, political, economical and social studies. Adjunct

Professor in Social Research Methods at Sapienza University of Rome,

Faculty of Philosophy.

Mobile: +39 320 7489273

Email: [email protected]

Daniele Serio

Project Leader

Statistician, working in Format Research since 2008. Manager and

coordinator of several quantitative research projects in the area of

economics and its application to financial systems and organizations.

Mobile: +39 345 3397685

Email: [email protected]

references |

22

This document is the base for an oral presentation,without which it has limited significance and maygive rise to misunderstandings.

Reproductions, albeit partial, of the content of thisdocument, are forbidden without previous writtenauthorization by Format.

2015 © Copyright Format Srl – ricerche di mercato

format S.r.l. LEGAL RESIDENCE & OPERATIONAL HEADQUARTER: via ugo balzani 77, 00162 roma, italiatel +39.06.86.32.86.81, fax +39.06.86.38.49.96, email: [email protected]

format nord estOPERATIONAL DIVISION: via caboto 22, 33170 pordenone, italia

vat number: 04268451004economic administrative index: roma 747042joint stock. € 10.340,00 i.v.

www.formatresearch.com