Kellogg Company September 8, 2011 Page 1 of 22 • Click to edit Master text styles – Second level • Third level – Fourth level » Fifth level 1 | September 8, 2011 | Barclays 2011 Back to School Conference 1 This presentation contains, or incorporates by reference, “forward‐looking statements” with projections concerning, among other things, the Company’s strategy, and the Company’s sales, earnings, margin, operating profit, costs and expenditures, interest expense, tax rate, capital expenditure, dividends, cash flow, debt reduction, share repurchases, costs, brand building, ROIC, working capital, growth, new products, innovation, cost reduction projects, and competitive pressures. Forward‐looking statements include predictions of future results or activities and may contain the words “expects,” “forecasts,” “believes,” “should,” “will,” “will deliver,” “anticipates,” “projects,” “estimates,” or words or phrases of similar meaning. The Company’s actual results or activities may differ materially from these predictions. The Company’s future results could also be affected by a variety of factors, including the impact of competitive conditions; the effectiveness of pricing, advertising, and promotional programs; the success of innovation, renovation and new product introductions; the recoverability of the carrying value of goodwill and other intangibles; the success of productivity improvements and business transitions; commodity and energy prices; labor costs; disruptions or inefficiencies in supply chain; the availability of and interest rates on short‐term and long‐term financing; actual market performance of benefit plan trust investments; the levels of spending on systems initiatives, properties, business opportunities, integration of acquired businesses, and 2 | September 8, 2011 | Barclays 2011 Back to School Conference other general and administrative costs; changes in consumer behavior and preferences; the effect of U.S. and foreign economic conditions on items such as interest rates, statutory tax rates, currency conversion and availability; legal and regulatory factors; including changes in advertising and labeling laws and regulations; the ultimate impact of product recalls; business disruption or other losses from war, terrorist acts or political unrest; and other items. Forward‐looking statements speak only as of the date they were made, and the Company undertakes no obligation to publicly update them.

Transcript

Kellogg Company September 8, 2011

Page 1 of 22

• Click to edit Master text styles

– Second level

• Third level– Fourth level

» Fifth level

1 | September 8, 2011 | Barclays 2011 Back to School Conference1

This presentation contains, or incorporates by reference, “forward‐looking statements” with projections concerning, among

other things, the Company’s strategy, and the Company’s sales, earnings, margin, operating profit, costs and expenditures,

7 | September 8, 2011 | Barclays 2011 Back to School Conference

1) Internal metrics exclude the impact of foreign currency translation and if applicable, acquisitions,dispositions and shipping day differences.

2) Rolling 3‐year innovation.

Drive Innovation2 Grow Brand

Building1

Net Sales from innovation over 3 years

Net Sales from current –year innovation

12.3%13.5% ≈14%

16.0%

2009 2010 2011 Estimate

2012 Forecast

2009 2010 2011 Estimate

2012 Forecast

more than2011

more than2011

8 | September 8, 2011 | Barclays 2011 Back to School Conference

Estimate ForecastEstimate Forecast

Kellogg Company September 8, 2011

Page 5 of 22

DRIVERS

4 – 5% •Base price increase

•Trade spend decrease

•Coupon reductions

9 | September 8, 2011 | Barclays 2011 Back to School Conference

2009 2010 2011 Est.

• Innovation driving positive mix

Trade spend reduction – example

+12%$ sales vs YAG

Special K Year‐to‐Date

Results

20112010$2.99$2.50

10 | September 8, 2011 | Barclays 2011 Back to School Conference

Source: Nielsen 24 w/e 6/18/11 vs. YA; promoted price point increase on select Special K SKUs representing approximately 20% of total Special K gross sales

$ sales vs. YAG

Kellogg Company September 8, 2011

Page 6 of 22

Internal Net Sales TrendsYear‐over‐year growth

5% 5%

3%

‐1%

5%4 – 5%

11 | September 8, 2011 | Barclays 2011 Back to School Conference

2007 2008 2009 2010 2011Guidance

Gross Profit Dollar GrowthInternal, year‐over‐year growth

5%

2%

6%

‐2%

3%2 – 3%

12 | September 8, 2011 | Barclays 2011 Back to School Conference

Guidance

2007 2008 2009 2010 2011

Kellogg Company September 8, 2011

Page 7 of 22

Remain disciplined on overhead in 2011

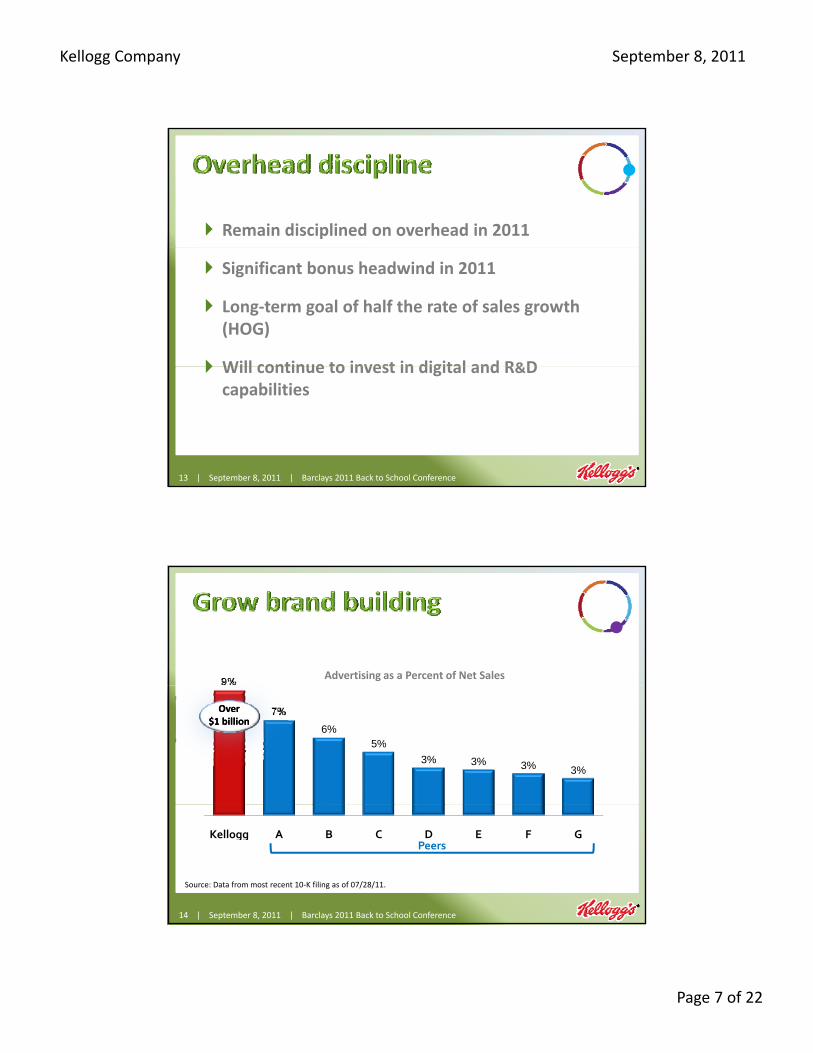

Significant bonus headwind in 2011

Long‐term goal of half the rate of sales growth (HOG)

Will continue to invest in digital and R&D

13 | September 8, 2011 | Barclays 2011 Back to School Conference

Will continue to invest in digital and R&D capabilities

9%Advertising as a Percent of Net Sales

9%

7%

6%5%

3% 3% 3% 3%

Over$1 billionOver

$1 billion

14 | September 8, 2011 | Barclays 2011 Back to School Conference

Kellogg A B C D E F G

Source: Data from most recent 10‐K filing as of 07/28/11.

Peers

Kellogg Company September 8, 2011

Page 8 of 22

Brand Building GrowthInternal, year‐over‐year

5%

‐2%

2%

0%

2%LSD

flat

15 | September 8, 2011 | Barclays 2011 Back to School Conference

2007 2008 2009 2010 2011Estimate

Note: LSD = low single‐digit

Stabilized our business in 2011 with t t li th d i bstrong top‐line growth driven by innovation

Will need to increase brand‐building investment in 2012 to continue regaining

t

16 | September 8, 2011 | Barclays 2011 Back to School Conference

momentum

Kellogg Company September 8, 2011

Page 9 of 22

SubheadingClick to edit Master title style

• Click to edit Master text styles

– Second level

• Third level– Fourth level

» Fifth levelPlaceholder

17 | September 8, 2011 | Barclays 2011 Back to School Conference9/7/2011 17

The right brandsThe right brands . . .

The right ideas . . .

The right investment . . .

18 | September 8, 2011 | Barclays 2011 Back to School Conference

Kellogg Company September 8, 2011

Page 10 of 22

Significant upgrade of our marketing capabilities in the last 2 years

Enhanced category understanding globally to create stronger portfolio design and investment focus

Strengthening our innovation capability and delivery while building stronger long‐term visibility

Improving returns on our marketing investment through significant upgrade in our creative, media / digital capability and focus

19 | September 8, 2011 | Barclays 2011 Back to School Conference

Becoming a stronger technology‐enabled organization to drive stronger participation in all aspects of the emerging digital agenda

A marketing function upgraded in talent and capability to operate effectively in the changing brand and consumer landscape

To maximize growth and returns,g ,

it is key that we optimize our portfolio

design by market to ensure we are

maximizing coverage of the core category needs

and aligning our investment accordingly.

20 | September 8, 2011 | Barclays 2011 Back to School Conference

and aligning our investment accordingly.

Kellogg Company September 8, 2011

Page 11 of 22

Global Segmentation • Common / category understanding across 16 markets

• Studies conducted amongst adults / moms

• Largest global study conducted at Kellogg• Provides common view, language and approach across markets

Benefits

21 | September 8, 2011 | Barclays 2011 Back to School Conference

Every brand plan

b ild dibilimust strive to build credibility

and relevance amongst users and non‐users.

We accomplish this by executing fresh and powerful ideas

that drive breakthrough and differentiation

22 | September 8, 2011 | Barclays 2011 Back to School Conference

within the categories in which we compete.

Kellogg Company September 8, 2011

Page 12 of 22

To win in our categories, we must have bigger and better ideas

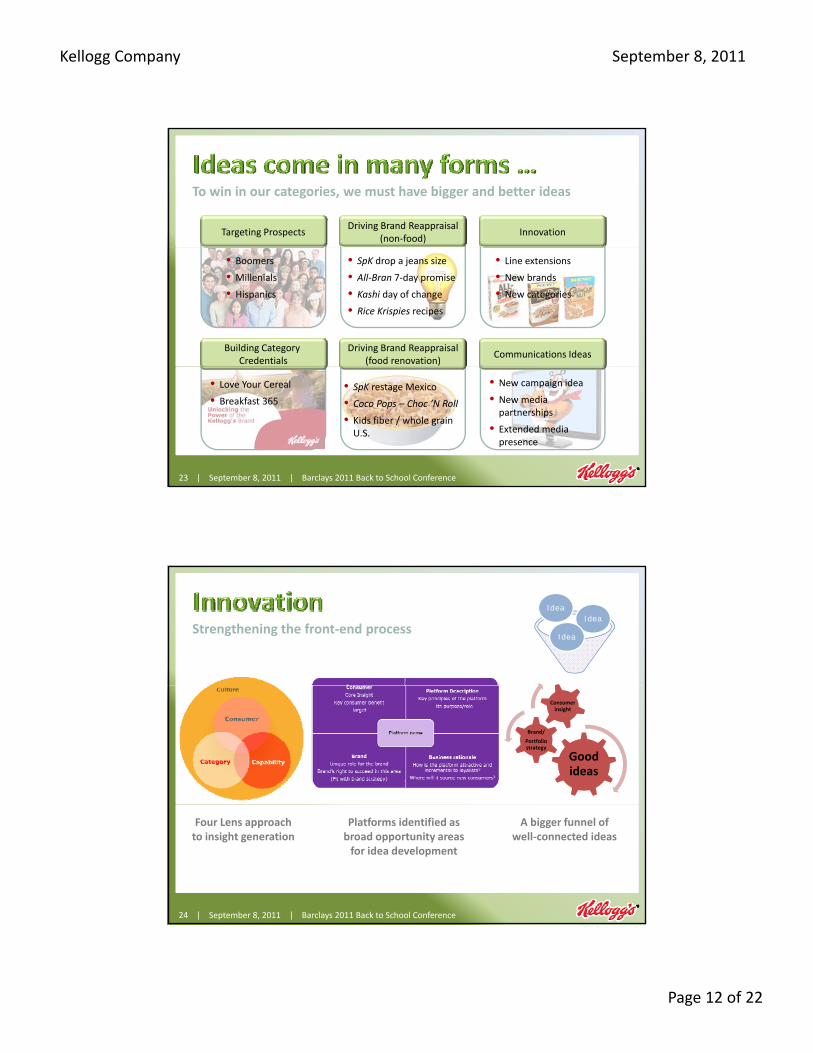

Targeting ProspectsDriving Brand Reappraisal

(non‐food)Innovation

• Boomers

• Millenials

• Hispanics

• SpK drop a jeans size

• All‐Bran 7‐day promise

• Kashi day of change

• Rice Krispies recipes

• Line extensions

• New brands

• New categories

Building Category Credentials

Communications IdeasDriving Brand Reappraisal

(food renovation)

23 | September 8, 2011 | Barclays 2011 Back to School Conference

• Love Your Cereal

• Breakfast 365

• SpK restage Mexico

• Coco Pops – Choc ’N Roll

• Kids fiber / whole grain U.S.

• New campaign idea

• New media partnerships

• Extended media presence

Strengthening the front‐end process

IdeaIdea

Idea

Good ideas

Brand/

Portfolio strategy

Consumer insight

24 | September 8, 2011 | Barclays 2011 Back to School Conference

Four Lens approach to insight generation

Platforms identified as broad opportunity areas for idea development

A bigger funnel of well‐connected ideas

Kellogg Company September 8, 2011

Page 13 of 22

Line Extension / Existing Brands

Expansion of Ideas across Markets New to Category

• Special K Clusters (Europe)

• Crunchy Nut from UK to US

• All‐Bran Golden Crunch (UK)

• Mini‐WheatsTouch of Fruit

• Trésor from France to UK to Mexico

• Special K Cracker Chips (US)

• Be Natural Cereal (Australia)

25 | September 8, 2011 | Barclays 2011 Back to School Conference

(US)

• Eggo – Thick & Fluffy Waffle (US)

• Fiber Plus from US to Canada & UK

Development3–5 years

Priority Setting & LT Visibility

Discovery

Development

Consumer InsightsTrendsBrands

New Science and Technology

36‐Month Business Unit Calendar

PortfolioPrioritization

ResourceAllocation

Aligned Hunting Grounds

26 | September 8, 2011 | Barclays 2011 Back to School Conference

Global R&D

Allocation

Advanced Innovation & Technology

MARKETING INNOVATION

Kellogg Company September 8, 2011

Page 14 of 22

As the consumer marketing landscape

grows increasingly complex, having the ability to reach

the right people,

with the right message

at the right time and place

27 | September 8, 2011 | Barclays 2011 Back to School Conference

g p

is essential to advancing the effectiveness and

efficiency of our marketing investment.

New Reality

All media is becoming

New Opportunity

Deliver integrated

Restructured Agency Model

Creating Integrated Experience Plans

AdvancingCapability & Process

Fewer,

All media is becoming digitally‐enabled media

Deliver integrated experiences across Paid, Owned, Earned media

28 | September 8, 2011 | Barclays 2011 Back to School Conference

Paid Own Earn

,Better,

Aligned

Kellogg Company September 8, 2011

Page 15 of 22

Out of Home

Media Partnerships –Print & On‐line

SmartPhone

TVDesktop

29 | September 8, 2011 | Barclays 2011 Back to School Conference

Display

Store

Social Media

EARNED

ROI Learnings Driving Continued Improvement

Global Return on Investment

Digital Venture FundCreative Quality

One modelThree partnersCommon global application

Fueling andCreative Idea

+80% of copy testedsi

on Rating

1

2 3

30 | September 8, 2011 | Barclays 2011 Back to School Conference

Fueling and funding inspiration

Idea

TechnologyExperience

copy tested performedStrong to

Very Strong

Weighted Persuas

Awareness Index Rating

1) Cost per thousand media impressions 2)Click‐through rate 3) Cost per click

Kellogg Company September 8, 2011

Page 16 of 22

Invite

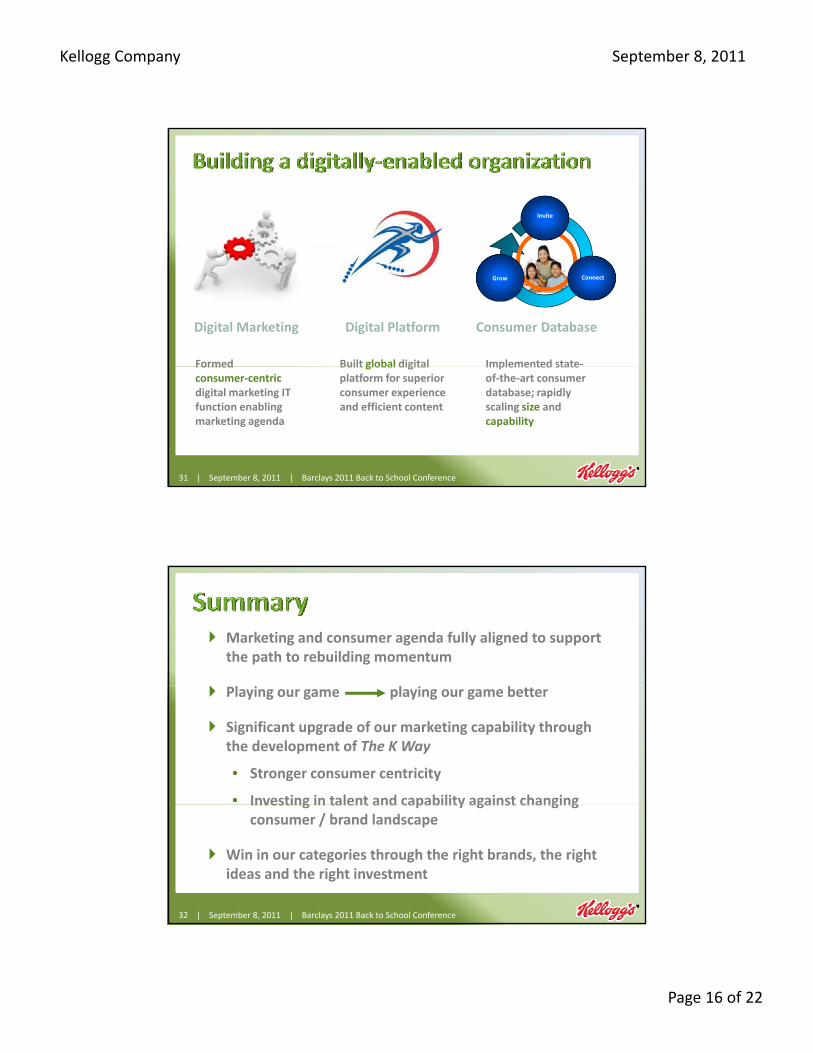

ConnectGrow

Formed Built global digital Implemented state‐

Digital Marketing Digital Platform Consumer Database

31 | September 8, 2011 | Barclays 2011 Back to School Conference

Formed consumer‐centric digital marketing IT function enabling marketing agenda

Built global digital platform for superior consumer experience and efficient content

Implemented stateof‐the‐art consumer database; rapidly scaling size and capability

Marketing and consumer agenda fully aligned to support the path to rebuilding momentum

Playing our game playing our game better

Significant upgrade of our marketing capability through the development of The K Way

• Stronger consumer centricity

• Investing in talent and capability against changing

32 | September 8, 2011 | Barclays 2011 Back to School Conference

Investing in talent and capability against changing consumer / brand landscape

Win in our categories through the right brands, the right ideas and the right investment

Kellogg Company September 8, 2011

Page 17 of 22

Town HouseFrosted Flakes

Special K All‐Bran (Australia)

33 | September 8, 2011 | Barclays 2011 Back to School Conference

•Text

SubheadingClick to edit Master title style

• Click to edit Master text styles

TextTextText

•Text•Text•Text

– Second level

• Third level– Fourth level

» Fifth level

34 | September 8, 2011 | Barclays 2011 Back to School Conference9/7/2011 34

Kellogg Company September 8, 2011

Page 18 of 22

Operating Principles

Grow Internal Net Sales1

LT Outlook: 3 to 4%

Grow Gross Profit Dollars1

LT Outlook: grow in line with l li htl b

SustainableGrowth

LT Outlook: 3 to 4%

Overhead Discipline1

LT Outlook: half the rate of sales growth

sales or slightly above

Improve Price / MixLT Outlook: improvements

to mitigate inflation

35 | September 8, 2011 | Barclays 2011 Back to School Conference

1) Internal metrics exclude the impact of foreign currency translation and if applicable, acquisitions,dispositions and shipping day differences.

2) Rolling 3‐year innovation.

Drive Innovation2

LT Outlook: approx. 15% of net sales Grow Brand Building1

LT Outlook: low to mid single‐digit growth

Operating Principles

Grow Net EarningsLT Outlook: mid single‐digit growth

Managefor Cash

Increase Return on Invested Capital

LT Outlook: improve over time

Reduce CoreWorking Capital

LT Outlook: continuous improvement

36 | September 8, 2011 | Barclays 2011 Back to School Conference

Return Cash to Shareowners– dividends– share repurchases

Prioritize Capital ExpenditureLT Outlook: 3 to 4% of sales

Kellogg Company September 8, 2011

Page 19 of 22

•Dividends per share (five‐year CAGR1) +8%

•Average annual share repurchases2 >$650 million

Dividends

(billions)

$0.7

$1.1 $1.1

$1.6

$1.4 est.

Share Repurchases

37 | September 8, 2011 | Barclays 2011 Back to School Conference

2007 2008 2009 2010 2011Estimate

1) CAGR base year 2006 to estimate for 2011. 2) Average annual share repurchases 2007 through estimate for 2011.

Net Debt5(billions)

Allocation of CashCumulative 2007 – 20111(billions)

38 | September 8, 2011 | Barclays 2011 Back to School Conference

Net cash from operations

Share repurchases

Dividends

Discretionary pension contributions

Acquisitions

2 1) Data for 2011 are estimates only.2) Cash proceeds from issuances of stock related to employee stock

option exercises.3) Cash from operations less capital spending before incremental

pension contributions.4) Incremental pension contribution above base, net of tax.5) Net debt includes current maturities of long‐term debt, notes

payable, and long‐term debt less total cash and cash equivalents.

3

Cash from options4

Kellogg Company September 8, 2011

Page 20 of 22

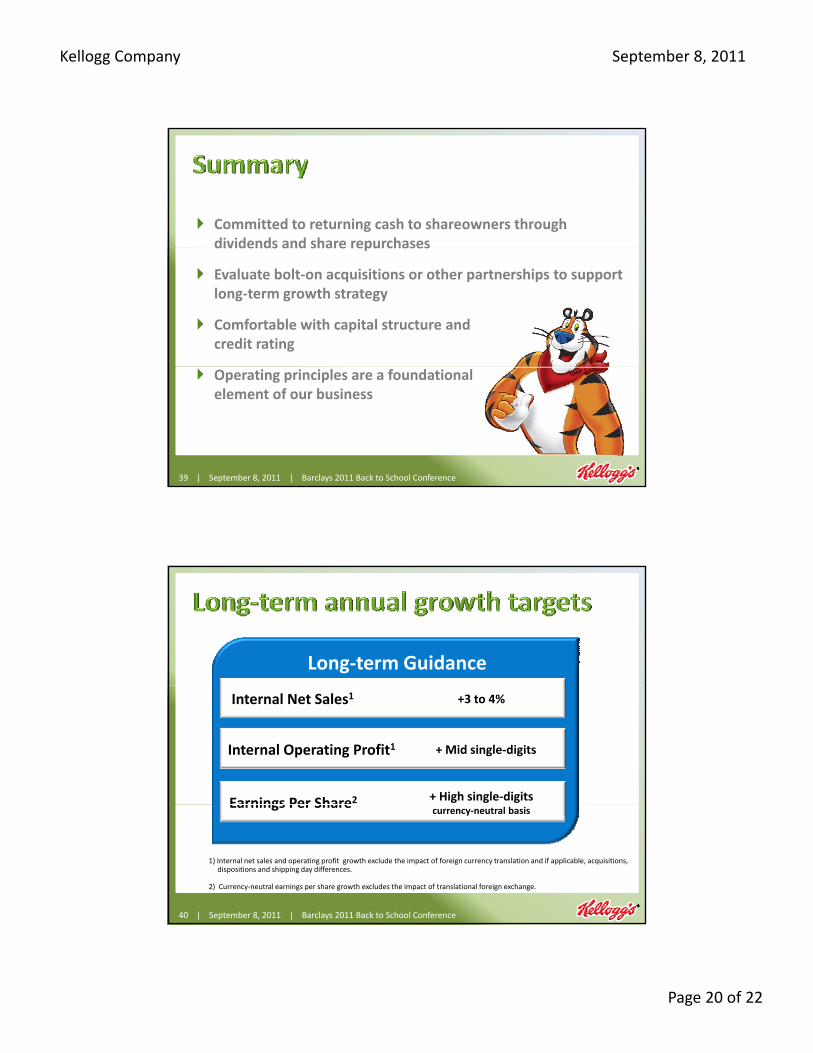

Committed to returning cash to shareowners through dividends and share repurchasesdividends and share repurchases

Evaluate bolt‐on acquisitions or other partnerships to support long‐term growth strategy

Comfortable with capital structure andcredit rating

39 | September 8, 2011 | Barclays 2011 Back to School Conference

Operating principles are a foundationalelement of our business

Long‐term Guidance

Internal Net Sales1

Internal Operating Profit1

Earnings Per Share2

+3 to 4%

+ High single‐digits

+ Mid single‐digits

40 | September 8, 2011 | Barclays 2011 Back to School Conference

1) Internal net sales and operating profit growth exclude the impact of foreign currency translation and if applicable, acquisitions,dispositions and shipping day differences.

2) Currency‐neutral earnings per share growth excludes the impact of translational foreign exchange.

Earnings Per Sharecurrency‐neutral basis

Kellogg Company September 8, 2011

Page 21 of 22

•Text

SubheadingClick to edit Master title style

• Click to edit Master text styles

TextTextText

•Text•Text•Text

– Second level

• Third level– Fourth level

» Fifth level

41 | September 8, 2011 | Barclays 2011 Back to School Conference9/7/2011 41

42 | September 8, 2011 | Barclays 2011 Back to School Conference

Total Company 3 to 4%North America Frozen

Note: Pie chart excludes other businesses not in these categories such as global foodservice and specialty channels, totaling less than $1 billion. 1Core RTEC includes United States, Canada, United Kingdom, Ireland, Australia and New Zealand.2Internal net sales growth exclude the impact of foreign currency translation and if applicable, acquisitions, dispositions and shipping day differences.

Kellogg Company September 8, 2011

Page 22 of 22

Committed to realistic goals and managing the business for the long termbusiness for the long term

Committed to brand building and innovationto sustainably win in the marketplace

Exciting long‐term growth

43 | September 8, 2011 | Barclays 2011 Back to School Conference

g g gpotential

44 | September 8, 2011 | Barclays 2011 Back to School Conference