26

Corporate Presentation Falabella JAN 2014 Confidential

Corporate

Presentation

Falabella

JAN 2014

Confidential

FALABELLA

CONSOLIDATED STATEMENTS

BUSINESS UNITS

INVESTMENT PLAN

Note: Financial data and outlets information as of September 2013 (LTM). FX rates as of 09/30/2013 (504.2 CLP/US$). Includes Sodimac Colombia revenues, which do not consolidate.

DE

PAR

TM

EN

T S

TOR

ES

Revenues

US$ 4,417m

Stores

89

HO

ME

IMP

RO

VE

ME

NT

Revenues

US$ 5,538m

Stores

196

SU

PE

RM

AR

KE

TS

Revenues

US$ 1,923m

Stores

80

FIN

AN

CIA

L S

ER

VIC

ES

Gross Loans

US$ 5,851m

CMR Accounts

4.2+ million

RE

AL

ES

TAT

E

GLA

1,7m sqmMalls / Power & Shopping

Centers18 / 14

3

FALABELLA AT A GLANCE

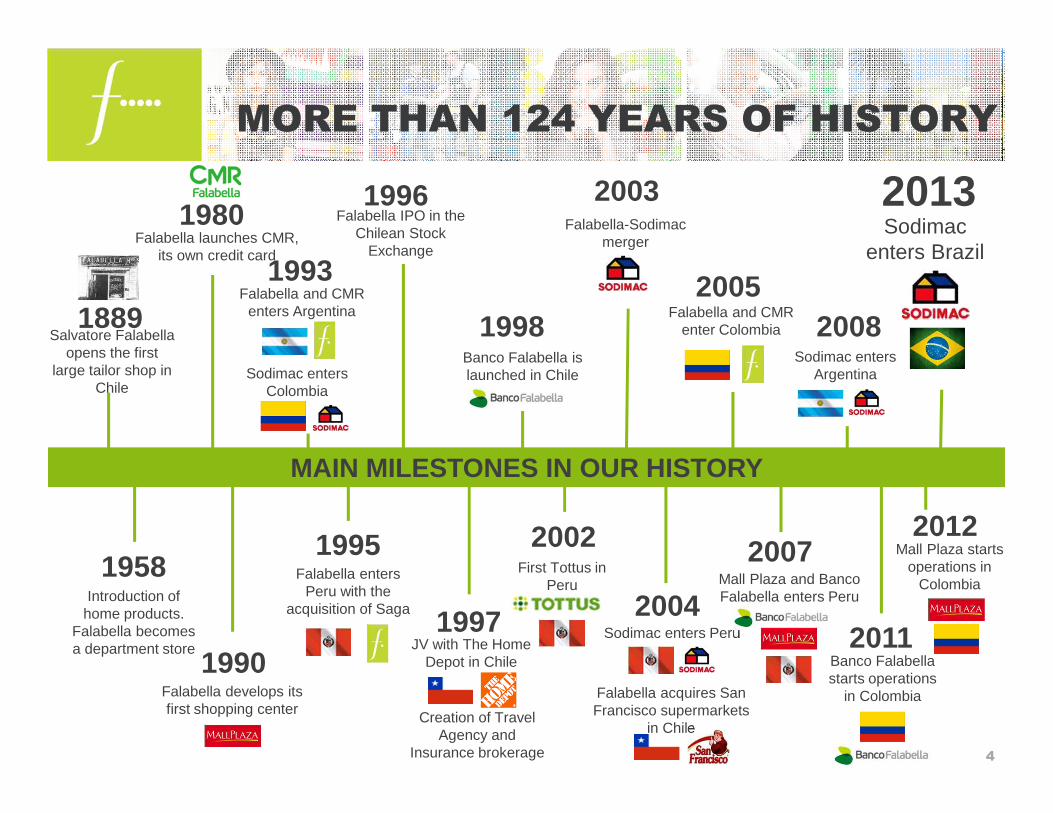

MORE THAN 124 YEARS OF HISTORY

Salvatore Falabella opens the first

large tailor shop in Chile

1889

Introduction of home products.

Falabella becomes a department store

1958

Falabella launches CMR, its own credit card

1980

Falabella develops its first shopping center

1990

Falabella and CMR enters Argentina

1993

Falabella enters Peru with the

acquisition of Saga

1995

Sodimac enters Colombia

Falabella IPO in the Chilean Stock

Exchange

1996

1997

Creation of Travel Agency and

Insurance brokerage

1998

JV with The Home Depot in Chile

Banco Falabella is launched in Chile

2002First Tottus in

Peru

Falabella-Sodimac merger

2004

Falabella acquires San Francisco supermarkets

in Chile

2005

Sodimac enters Peru

Falabella and CMR enter Colombia

2007Mall Plaza and Banco Falabella enters Peru

2008Sodimac enters

Argentina

2011Banco Falabella starts operations

in Colombia

2012Mall Plaza starts

operations in Colombia

20132003

MAIN MILESTONES IN OUR HISTORY

4

Sodimac enters Brazil

1 Through Falabella Perú S.A.A..

2 Not consolidated.

3 Consolidates from July 1st , 2013.

CORPORATE STRUCTURE

5

SACI FalabellaSACI Falabella

ChileChile Peru1Peru1 ArgentinaArgentina ColombiaColombia

Sodimac 100%

Imperial 60%

Tottus 88%

CMR 100%

Banco Falab. 100%

Rentas F. 100%

Mall Plaza 60%

Saga Falabella 95%

Sodimac 100%

Tottus 100%

Banco Falab. 100%

Open Plaza 100%

Avent. Plaza 40% 2

Falabella 100%

Sodimac 100%

CMR 100%

Falabella 65%

Banco Falab. 65%

Sodimac 49% 2

Mall Plaza

Falabella 100%

100%

94%

20%

BrazilBrazil

Construdecor 50.1% 3

6

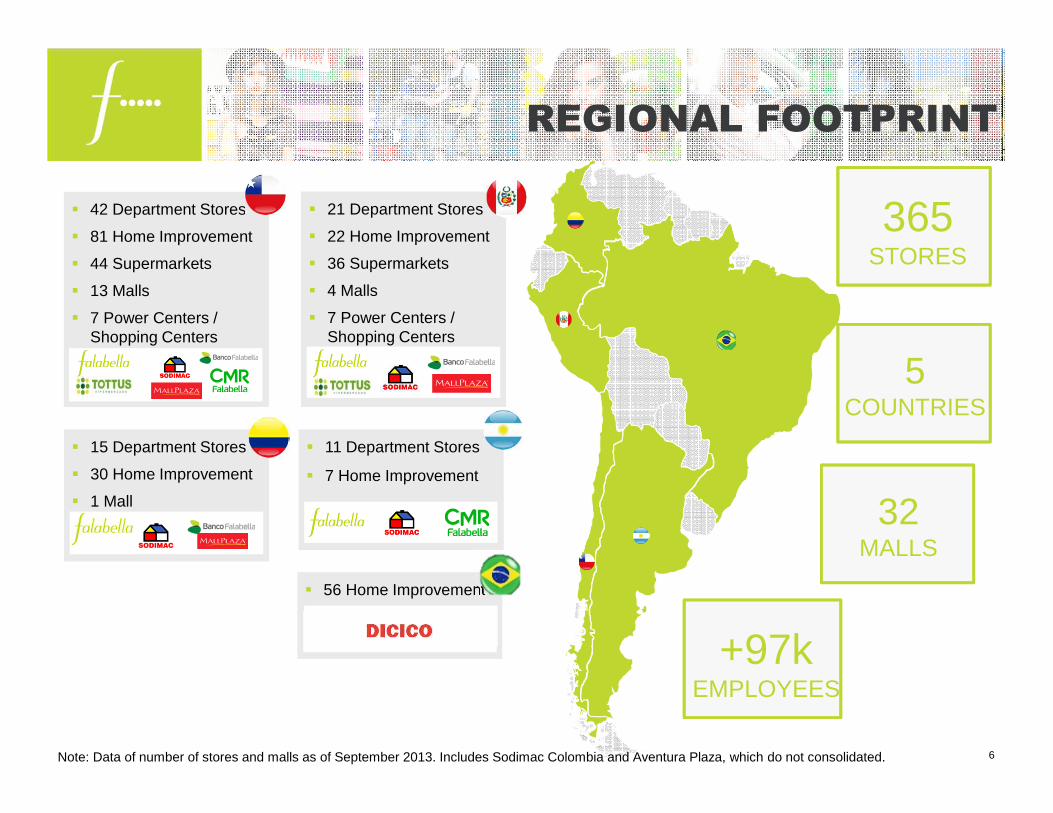

REGIONAL FOOTPRINT

365 STORES

32MALLS

+97kEMPLOYEES

5COUNTRIES

� 42 Department Stores

� 81 Home Improvement

� 44 Supermarkets

� 13 Malls

� 7 Power Centers / Shopping Centers

� 21 Department Stores

� 22 Home Improvement

� 36 Supermarkets

� 4 Malls

� 7 Power Centers / Shopping Centers

� 15 Department Stores

� 30 Home Improvement

� 1 Mall

� 11 Department Stores

� 7 Home Improvement

� 56 Home Improvement

Note: Data of number of stores and malls as of September 2013. Includes Sodimac Colombia and Aventura Plaza, which do not consolidated.

LATAM EXPOSURE

7

2006

9M 2013 (LTM)REVENUES

EBITDA9M 2013 (LTM)

2006

80%

17%

3%

Consistent interaction with our customers...

...and to anticipate their preferences and design targeted marketing campaigns

Relationship with our

Customer

Immediate Necessities

Access to goods through installment

payments

Benefits

Purchase frequency

Client Understanding

Suitable Deals-of-

the-day

Lower Risks

Bus

ines

s In

telli

genc

e

Cus

tom

er’s

DN

A

When does she purchase

Where does she purchase

What does she

like

What are her

interests

How much does she

spend

Means of payment

What does she

buy

...allows us to evolve and remain close to our customers

8

CUSTOMER CENTRIC STRATEGY

...both in traditional and online platforms…

9

CORPORATE GOVERNANCE

�Most Convincing and Coherent Strategy in Latam

�Highest standard of corporate governance in Latam

MARKET RECOGNITION Highly experienced leadership team, with more than 13 years in average in the Group

Independent director at holding level and in relevant subsidiaries

Controlling group consisting of 7 families

10

SUSTAINABLE BUSINESS

COMMUNITY� Commitment to the

communities where we work

CUSTOMERS� Responsible Marketing prompt

complains management customer service

HUMAN RESOURCES� Great Place To Work Institute: Top

Rankings By Falabella, Sodimac, Tottus and CMR Chile

SUSTAINIBILITY REPORT� We prepare a Corporate

Sustainability Report, jointly with the reports launched by our 5 business units

SUPPLIERS� Feria Pyme:

Supporting the develoment of small business suppliers

ENVIRONMENT� Member of the US Green

Building Council� Leed Certified Stores

FALABELLA

CONSOLIDATED STATEMENTS

BUSINESS UNITS

INVESTMENT PLAN

3Q & 9M 2013 INCOME STATEMENT

12Note: Financial Statements in CLP translated at FX as of 09/30/2013 (504.2 CLP/US$)

Mill. of USD 3Q '12 % Rev. 3Q '13 % Rev. Var. 13/12 9M '12 % Rev. 9M '13 % Rev. Var. 13/12

Revenues of Non-Banking Operations 2,603 2,936 12.8% 7,762 8,582 10.6%

Revenues of Banking Operations 202 236 16.6% 594 663 11.6%

TOTAL REVENUES 2,805 3,172 13.1% 8,356 9,245 10.6%

COGS of Non-Banking operations (1,767) -67.9% (1,972) -67.2% 11.6% (5,267) -67.9% (5,716) -66.6% 8.5%

COST of Banking Operations (104) -51.4% (104) -44.1% 0.2% (311) -52.3% (307) -46.3% -1.2%

GROSS PROFIT 934 33.3% 1,096 34.5% 17.3% 2,779 33.3% 3,221 34.8% 15.9%

SG&A Expenses (677) -24.1% (808) -25.5% 19.3% (1,993) -23.8% (2,293) -24.8% 15.1%

Operational Income 257 9.2% 287 9.1% 11.9% 786 9.4% 928 10.0% 18.1%

Depreciation+Amortization 71 2.5% 84 2.7% 19.7% 207 2.5% 243 2.6% 17.4%

EBITDA 327 11.7% 372 11.7% 13.6% 992 11.9% 1,171 12.7% 18.0%

Non- Operating Profit (27) -1.0% (59) -1.9% 119.6% (100) -1.2% (137) -1.5% 36.7%

Profit Before Tax Expenses 230 8.2% 228 7.2% -0.8% 685 8.2% 791 8.6% 15.4%

Income Tax (112) (53) -52.6% (196) (176) -10.2%

Minority Interest 1 (23) -2993.1% (42) (68) 60.2%

NET PROFIT / (LOSS) 118 4.2% 152 4.8% 28.2% 447 5.4% 547 5.9% 22.3%

BALANCE SHEET as of SEP. 2013

13

US$ million Sep-2013ASSETSNon-Banking OperationsCurrent AssetsCash & cash equivalents 290Current trade & other receivables 8Inventories 1,690Others 2,638

Total Current Assets 4,627

Non-Current AssetsNon-Current trade & other receivables 309Goodwill 614PP&E 3,274Others 4,407

Total Non-Current Assets 8,603Total Non-Banking Operations Assets 13,230

Loans and accounts receivable from clients 3,514

Others 1,414

Total Assets from Banking Operations 4,928

TOTAL ASSETS 18,157

US$ million Sep-2013EQUITY & TOTAL LIABILITIESNon-Banking OperationsCurrent LiabilitiesOther current financial liabilities 879Current trade & otherpayables 1,341Others 350

Total Current Liabilities 2,570

Non-Current LiabilitiesOther non-current financial laibilities 4Others 3,971

Total Non-Current Liabilities 3,975Total Non-Banking Oper. Liabilties 6,545

Total Liabilities from Banking Oper. 4,128

TOTAL LIABILITIES 10,673

Shareholders' Equity 7,485

TOTAL EQUITY & LIABILITIES 18,157

Note: Financial Statements in CLP translated at FX as of 09/30/2013 (504.2 CLP/US$)

FINANCIAL SITUATION

14

LEVERAGE (w/o Banking Operations) (times)

DEBT BY TYPE

(w/o Banking Oper.)

NET FINANCIAL DEBT/EBITDA (w/o Banking Oper.)

(times)

DEBT BY MATURITY

(w/o Banking Oper.)

Financial Debt (w/o Banks):

US$ 4,256 MM

Duration:5.53years

15

2013 OPENINGS

Chile Peru

Mall Plaza Iquique Open Plaza Pucallpa

Mall Plaza Egaña

Open Plaza Rancagua

Open Plaza Ovalle

� In 2013, the Falabella Group reached 382 stores in the region, adding 86 new stores to its operation during the year:

� 30 new stores in Chile, Peru and Colombia� 56 stores through the acquisition of Construdecor in Brazil

� Moreover, the Group added 5 shopping centers in 2013, reaching to a total of 36 malls in the region.

New Stores: New Malls:

Chile Peru Colombia Brazil

Ovalle Lima Norte Bucaramanga

Egaña Cañete

Ica

Pucallpa

Santa Cruz Ate Armenia

Ovalle SJ Lurigancho Rionegro

Cañete Chia

Huacho

Sullana

Pucallpa

Vitacura Cañete

Egaña Canta Callao

El Trébol Chiclayo

Ovalle Pacasmayo

Quilpué Arequipa Parra

Pucallpa

Sullana

Falabella

Sodimac

Tottus

+ 56

Dicico

stores

FALABELLA

CONSOLIDATED STATEMENTS

BUSINESS UNITS

INVESTMENT PLAN

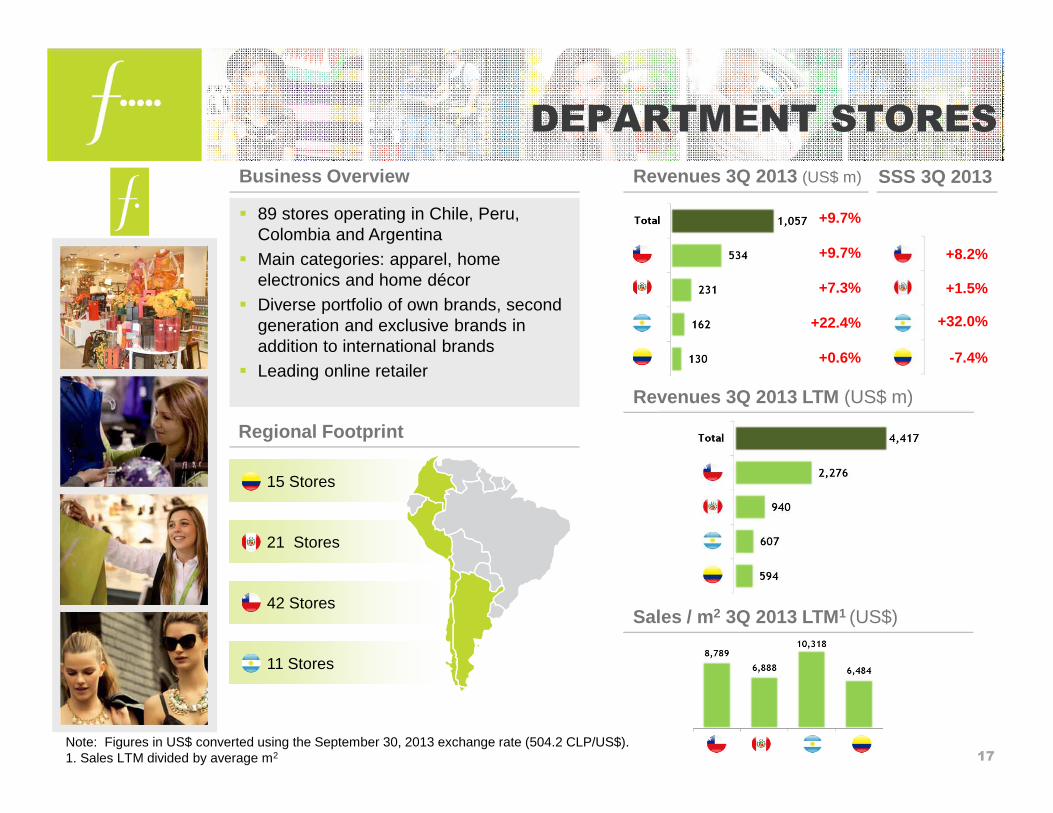

Regional Footprint

� 89 stores operating in Chile, Peru, Colombia and Argentina

� Main categories: apparel, home electronics and home décor

� Diverse portfolio of own brands, second generation and exclusive brands in addition to international brands

� Leading online retailer

Business Overview

21 Stores

42 Stores

15 Stores

11 Stores

Note: Figures in US$ converted using the September 30, 2013 exchange rate (504.2 CLP/US$).1. Sales LTM divided by average m2

DEPARTMENT STORES

17

Revenues 3Q 2013 (US$ m)

Revenues 3Q 2013 LTM (US$ m)

+9.7%

+9.7%

+7.3%

+22.4%

+0.6%

SSS 3Q 2013

+8.2%

+1.5%

+32.0%

-7.4%

Sales / m 2 3Q 2013 LTM1 (US$)

+6.4%

+8.7%

+21.8%

+2.2%

+8.5%

Note: Figures in US$ converted using the September 30, 2013 exchange rate (504.2 CLP/US$).1. Sales LTM divided by average m2. Does not include Brazil as information for 2012 is not available.

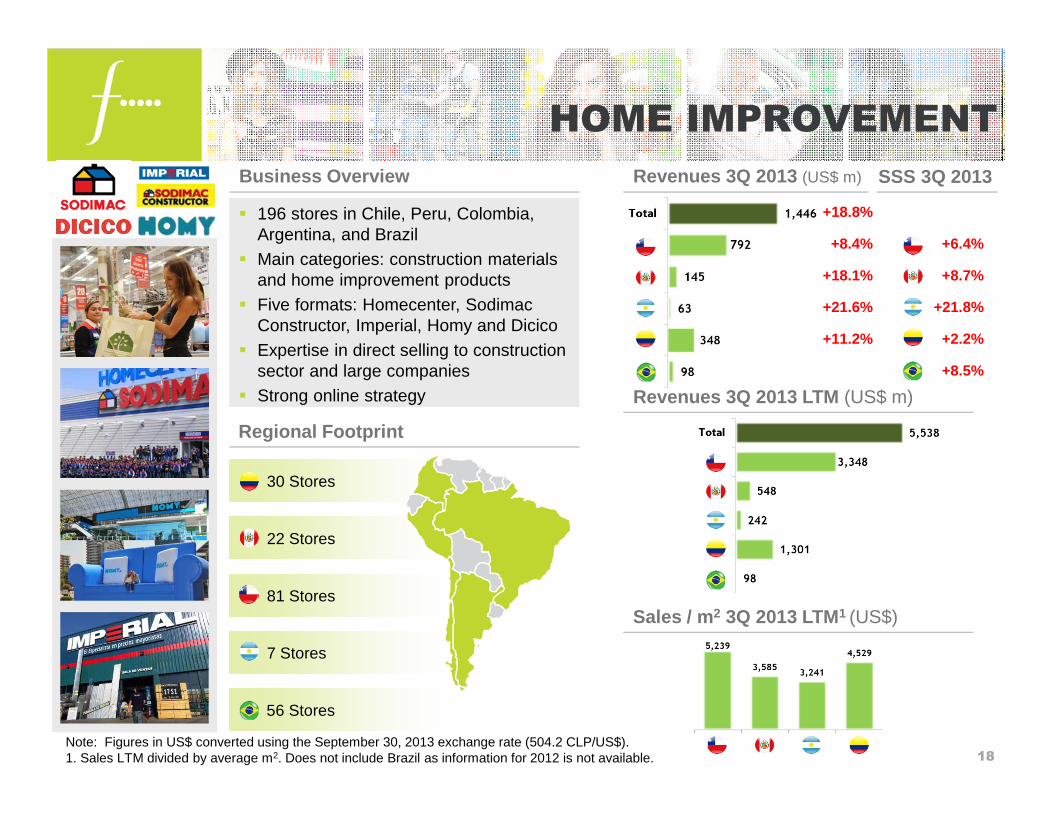

� 196 stores in Chile, Peru, Colombia, Argentina, and Brazil

� Main categories: construction materials and home improvement products

� Five formats: Homecenter, Sodimac Constructor, Imperial, Homy and Dicico

� Expertise in direct selling to construction sector and large companies

� Strong online strategy

22 Stores

81 Stores

30 Stores

7 Stores

HOME IMPROVEMENT

18

Business Overview

Regional Footprint

+18.8%

+8.4%

+18.1%

+21.6%

+11.2%

SSS 3Q 2013Revenues 3Q 2013 (US$ m)

Revenues 3Q 2013 LTM (US$ m)

Sales / m 2 3Q 2013 LTM1 (US$)

56 Stores

Note: Figures in US$ converted using the September 30, 2013 exchange rate (504.2 CLP/US$).1. Sales LTM divided by average m2

� Started operations in 2002 in Peru under Tottus brand and entered Chilean market in 2004 with the acquisition of San Francisco

� Operates 80 stores in Chile and Peru, with two main formats: hypermarkets and supermarkets

� Increased penetration of private labels� Developed online platform

19

36 Stores

44 Stores

Business Overview

Regional Footprint

+11.7%

+14.2%

+8.8%

SSS 3Q 2013

+6.7%

+2.7%

SUPERMARKET

Revenues 3Q 2013 (US$ m)

Revenues 3Q 2013 LTM (US$ m)

Sales / m 2 3Q 2013 LTM1 (US$)

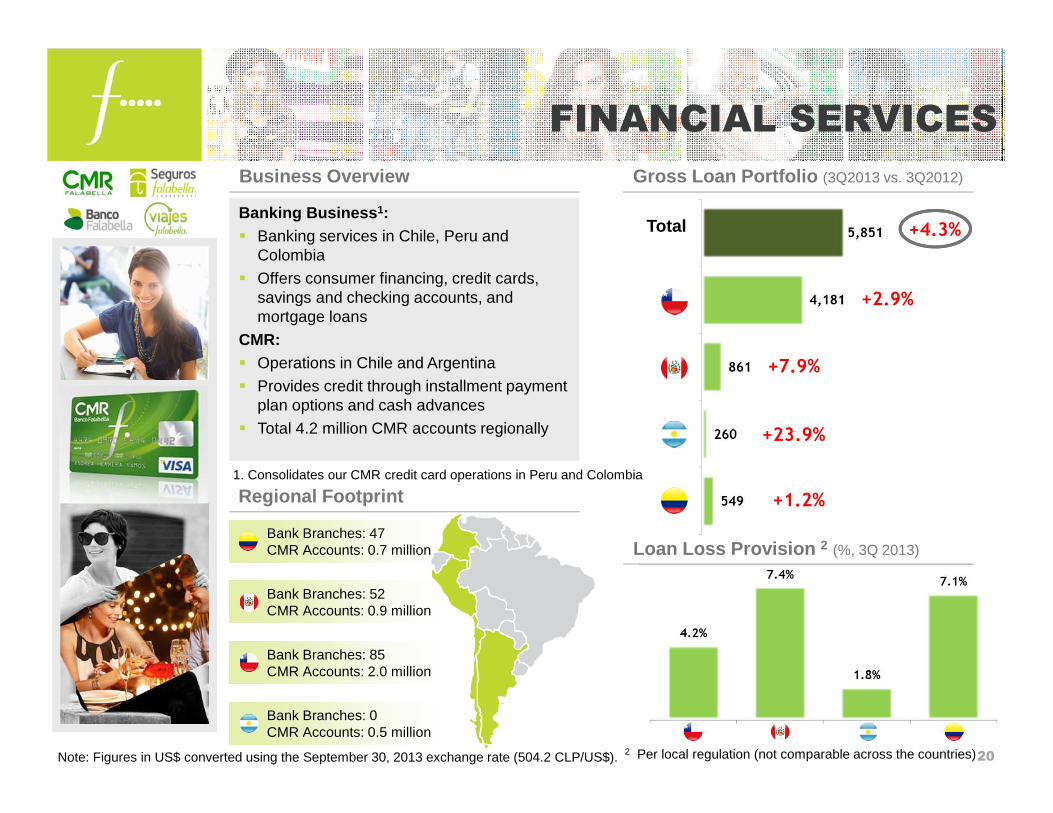

Bank Branches: 52 CMR Accounts: 0.9 million

Bank Branches: 85CMR Accounts: 2.0 million

Bank Branches: 47 CMR Accounts: 0.7 million

Bank Branches: 0CMR Accounts: 0.5 million

Note: Figures in US$ converted using the September 30, 2013 exchange rate (504.2 CLP/US$).

Banking Business 1:� Banking services in Chile, Peru and

Colombia

� Offers consumer financing, credit cards, savings and checking accounts, and mortgage loans

CMR: � Operations in Chile and Argentina

� Provides credit through installment payment plan options and cash advances

� Total 4.2 million CMR accounts regionally

2 Per local regulation (not comparable across the countries)

1. Consolidates our CMR credit card operations in Peru and Colombia

FINANCIAL SERVICES

20

Gross Loan Portfolio (3Q2013 vs. 3Q2012)

Total +4.3%

+2.9%

+7.9%

+23.9%

+1.2%

Business Overview

Regional Footprint

Loan Loss Provision 2 (%, 3Q 2013)

REAL ESTATE

21

� Largest operator in Chile and Peru, and one of the leaders in Latin America:� Mall Plaza : Operates large shopping malls in Chile , Peru (through Aventura Plaza)

and Colombia.� Rentas Falabella and Open Plaza : Operates small shopping centers with 2 or 3 of our

retail formats as anchor stores, as well as other third-party minor stores.

� Stores revenues of Mall Plaza shopping malls grew by 13.1% in the quarter.

� Opening of Mall Plaza Egaña by the end of 2013, being the first sustainable mall in Chile.

Main Highlights

1 Owned by the company.

Business Overview

Free Standing Stores (Falabella, Sodimac, Tottus) 1

666 684

FALABELLA

CONSOLIDATED STATEMENTS

BUSINESS UNITS

INVESTMENT PLAN

INVESTMENT PLAN 2014-2017

23

157STORES

15MALLS

US$4.1bnInvestment (US$ mm)

# Stores & Malls

63%14%

23%

24

CONTACT INFORMATION

Jordi Gaju N.

Chief Development Officer

Phone: +56 2 2380 2012

Alejandro González D.

Chief Financial Officer

Phone: +56 2 2380 2205

Lucrecia Fittipaldi

Corporate Development Manager / Head of IR

Phone: +56 2 2380 2012

Catalina Escaffi

IR / Development Associate

Phone: +56 2 2380 2012

25

This presentation contains forward-looking statements, includingstatements regarding the intent, belief or current expectations of theCompany and its management. Investors are cautioned that any suchforward-looking statements are not guarantee of future performance andinvolve a number of risks and uncertainties including, but not limited to, therisks detailed in the company’s financial statements, and the fact that actualresults could differ materially from those indicated by such forward-lookingstatements.

IMPORTANT DISCLAIMER

JAN 2014

Confidential

Corporate

Presentation

Falabella