348

dm{f©H {anmoQ© Annual Report 2015-16 Green Banking. Sustainable Future. h[aV ~¢qH J & gVV ^{dî` &

| Date post: | 02-Sep-2018 |

| Category: |

Documents |

| Upload: | nguyendiep |

| View: | 214 times |

| Download: | 0 times |

dm{f©H {anmoQ©Annual Report 2

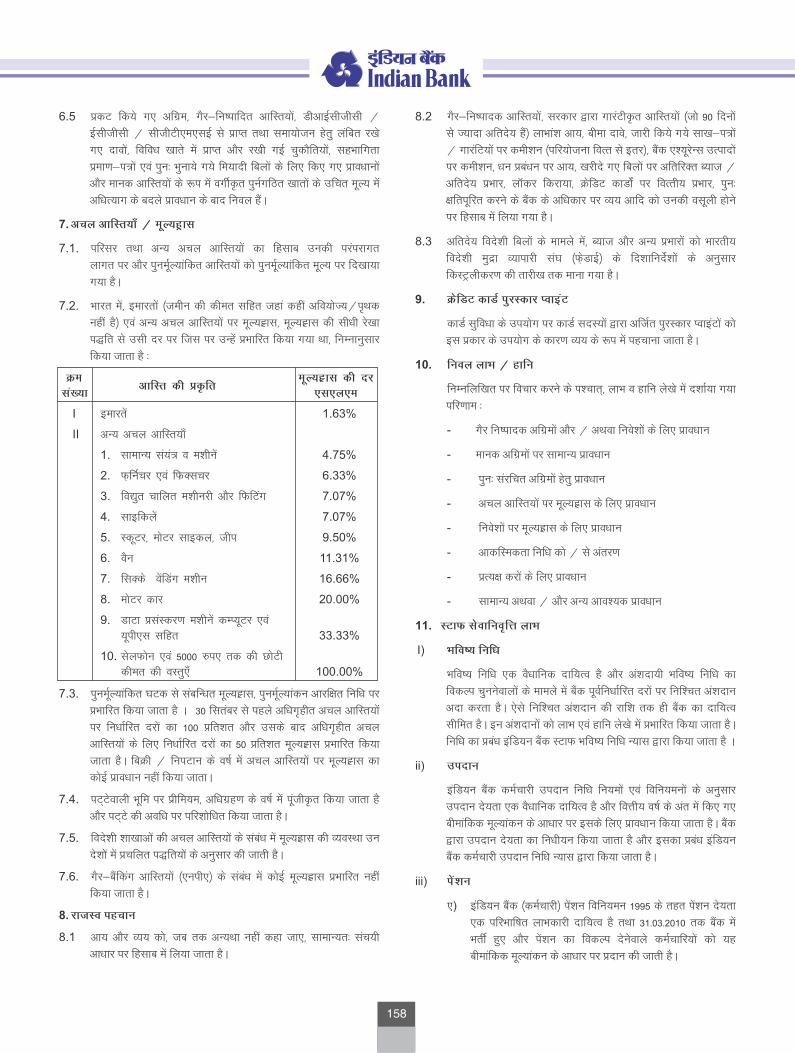

015

-16

Green Banking. Sustainable Future.h[aV ~¢qH J & gVV ^{dî` &

Shri. M.K. Jain, MD & CEO handing over dividend to Shri. Arun Jaitley, Hon’ble Union Finance Minster, GOI

Shri. Arun Jaitley, Hon’ble Union Finance Minister,GOI addressing the gathering, on virtualinauguration of 109 Branches and 109 BNAs/Recyclers on the eve of 109 Foundation Day ofthe Bank on August 21, 2015 at New Delhi.

th

Shri. M.K. Jain, MD & CEO receiving the prestigiousASSOCHAM Social Banking Excellence Award fromShri. Jayant Sinha, Hon’ble Minister of State forFinance, GoI during the 11 Annual Banking Summit,Mumbai. Indian Bank has been awarded underMedium Bank Class for

Winner UnderAgriculture BankingWinner under Urban BankingRunner up under Rural Banking

th

�

�

�

Jh egs'k dqekj tSu] çfu ,oa eqdkv }kjk Jh v#.k tsVyh] ekuuh; dsUæh; foÙk ea=h] Hkkjr ljdkj dks ykHkka'k lkSairs gq, A

21 2015 109

109 109

vxLr dks ubZ fnYyh esa cSad ds osa LFkkiukfnol ds miy{; esa 'kk[kkvksa rFkk cap uksV,DlsiVj @ jhlkbDyj ds opZqvy mn~?kkVu ds volj ijJh v#.k tsVyh] ekuuh; dsUæh; foÙk ea=h] Hkkjr ljdkj]lHkk dks lacksfèkr djrs gq, A

11osa okf"kZd cSafdax f'k[kj lEesyu] eqacbZ] esa Jh t;ar flUgk]ekuuh; foÙk jkT; ea=h] Hkkjr ljdkj ls Jh egs'k dqekjtSu] çfu ,oa eqdkv] çfrf"Br ,lkspse lkekftd cSafdaxmR—"Vrk iqjLdkj çkIr djrs gq, A bafM;u cSad dks eè;eJs.kh ds cSad ds varxZr bu iqjLdkjksa ls uoktk x;k &

f"k cSafdax ds varxZr fotsrk'kgjh cSafdax ds varxZr fotsrkxzkeh.k cSafdax ds varxZr mi fotsrk

�

�

�

—

BOARD OF DIRECTORS

funs'kd eaMy

ck,a ls nk,a %

From Left to Right :

Jh in~eukHku foV~By nkl Jh fouksn dqekj ukxj lqJh eqfnrk feJk

Jh vkj lqczef.k; dqekj dk;Zikyd funs'kd Jh egs'k dqekj tSu çcaèk funs'kd ,oa eq[; dk;Zikyd vfèkdkjh

Jh Vh lh osadV lqczef.k;u xSj&dk;Zikyd v/;{k Jh ch ih fot;sUnz Jh , ,l jktho dk;Zikyd funs'kd

Jh Jhjke jkepUnzu Jh nhid Mh lkear Jh ih osadV Ñ".k jko

, , ,

, , ,

, , ,

, ,

,

, ,

Mr Padmanaban Vittal Dass, Mr Vinod Kumar Nagar, Ms Mudita Mishra,

Mr R Subramania Kumar, Executive Director, Mr Mahesh Kumar Jain, Managing Director & CEO,

Mr T C Venkat Subramanian, Non-Executive Chairman, Mr B P Vijayendra, Mr A S Rajeev, Executive Director,

Mr Sriram Ramachandran, Mr Deepak D Samant, Mr P Venkata Krishna Rao

egk çcU/kd / GENERAL MANAGERS

Rangarajan G Udaya Bhaskara Reddy K Nagarajan Mjaxjktu th mn; HkkLdj jsìh ds ukxjktu ,e

Dharmaraj PèkeZjkt ih

Chezhian S Manimaran R Parthasarathy BpsfG;u ,l ef.kekju vkj ikFkZlkjFkh ch

Prasanth V A

ç'kkar oh ,Lakshmipathy Reddy GKrishnan S

—".ku ,l y{ehifr jsìh th

Om Prakash Ambasht

vkse çdk'k vac"VGopal V Venkatesa Perumal P Azad Singh Gandasxksiky oh osadVsl is#eky ih vktkn flag xaMl

Hanumanthu Sanyasiguqearq lU;klh

Chandra Reddy K Ramu AKarthikeyan MdkfrZds;u ,e pUæk jsìh ds jkew ,

S K Parida,l d¢ ifjnk

dkWiksZjsV dk;kZy; vOoS "k.eqxe lkyS

psUuS

okf"kZd fjiksVZfu"iknu dh izeq[k ckrsa

¼ djksM+ksa esa½

fooj.k

% 254 - 260

Corporate Office : 254-260, Avvai Shanmugam Salai

Chennai - 600 014

Annual Report 2015-16

PERFORMANCE HIGHLIGHTS

( in crore)

Particulars 31-03-12 31-03-13 31-03-14 31-03-15 31-03-16

A A

A A

A A

A A

A A

Total Business 211988 249136 286634 298057 310918

Deposits (Global) 120804 141980 162275 169225 178286

Advances (Global) 91184 107156 124359 128832 132632

Investments (Gross) 38208 42056 47635 46804 53418

Interest Income 12231 13898 15249 15853 16244

Non Interest Income 1232 1283 1372 1363 1781

Total Income 13463 15181 16621 17216 18025

Interest Expenses 7813 9368 10889 11391 11798

Operating Expenses 2187 2751 2831 2811 3195

Total Expenditure 10000 12119 13720 14202 14993

Operating Profit 3463 3061 2901 3014 3032

Net Profit 1747 1581 1159 1005 711

(%) Cost of Deposits (%) 6.68 7.07 7.15 7.10 6.76

(%) Yield on Advances (%) 11.28 11.03 10.38 10.19 9.63

(%)Net Interest Margin (%) 3.43 3.09 2.60 2.50 2.33

(%) Return on Average Assets (%) 1.31 1.02 0.67 0.54 0.36

Equity Share Capital 430 430 465 480 480

400 400 0 0 0Perpetual Non-Cumulative Preference Share Capital

Reserves & Surplus (excluding Revaluation Reserve) 8808 10009 11071 12078 12998

Net Worth 9638 10839 11536 12558 13478

(%) Gross NPA (%) 2.03 3.33 3.67 4.40 6.66

(%) Net NPA (%) 1.33 2.26 2.26 2.50 4.20

Capital Adequacy Ratio

- II - Basel II 13.47 13.08 13.10 13.24 13.67

- III - Basel III 12.64 12.86 13.20

( ) Earnings Per Share ( ) 39.57 35.80 26.07 21.62 14.81

( ) Book Value per Share ( ) 214.94 242.89 248.16 261.46 280.63

( ) Dividend per Equity Share ( ) 7.50 6.60 4.70 4.20 1.50*

No. of branches (Nos.) 1958 2092 2253 2412 2565

No. of employees (Nos.) 18782 18870 19429 20294 20140

Business per employee ( in lacs) 1114 1301 1453 1443 1531

dqy O;kikj

tek,a ¼Xykscy½

vfxze ¼Xykscy½

fuos'k ¼ldy½

C;kt vk;

xSj C;kt vk;

dqy vk;

C;kt O;;

ifjpkyuxr O;;

dqy O;;

ifjpkyuxr ykHk

fuoy ykHk

tekvksa dh ykxr

vfxzeksa ij izfrQy

fuoy C;kt ekftZu

vkSlr vkfLr;ksa ij izfrQy

bZfDoVh 'sk;j iwath

LFkk;h xSj⪅h vf/keku 'ks;j iwath

fjt+oZ ,oa vf/k'ks"k ¼iquewZY;u fjt+oZ dks NksM+dj½

fuoy laifRr

ldy ,uih,

fuoy ,uih,

iwath i;kZIrrk vuqikr

csly

csly

izfr 'sk;j vtZu

izfr 'ks;j cgh ewY;

izfr bZfDoVh 'ks;j ykHkka'k

'kk[kkvksa dh la[;k ¼uacj½

deZpkfj;ksa dh la[;k ¼uacj½

izfr deZpkjh dkjksckj ¼ yk[kksa esa½

* Proposed

. . . .

S.P. PURI & CO. C.K. PRUSTY & ASSOCIATES PADMANABHAN RAMANI & RAMANUJAM

G BALU ASSOCIATES PRAKASH CHANDRA JAIN & CO.

izLrkfor

,l ih iwjh ,.M da lh ds i`fLV ,.M ,lksfl;sV~l ineukHku ,.M jkekuqte

th ckyq ,lksfl;sV~l izdk'k panz u ,.M da

AUDITORSys[kk ijh{kdje.kh

tS

dkWiksZjsV dk;kZy; vOoS "k.eqxe lkyS

psUuS-

Okkf"kZd fjiksVZ

: 254-260,Corporate Office : 254-260, Avvai Shanumugam Salai

Chennai - 600 014

Annual Report 2015-16

fo"k;oLrq CONTENTSi`"B la

fuos’kd lsok,a d{k

. Page No.

Financial Statements – Indian Bank

Consolidated Financial Statements

Indian Bank

Investor Services Cell

Share Transfer Agent

Cameo Corporate Services Limited

Unit : Indian Bank

v/;{k dk lans’k

çfu ,oa eqdkv dk lans'k

funs’kdksa dh fjiksVZ

izcU/ku fopkj foe’kZ ,oa fo’ys"k.k

dkWiksZjsV vfHk’kklu ij fjiksVZ

dkWiksZjsV vfHk’kklu ij ys[kk ijh{kdksa dh fjiksVZ

rqyu i=] ykHk ,oa gkfu ys[kk vkSj vuqlwfp;k¡

eq[; ys[kkdj.k uhfr;ka

ys[kksa ij fVIif.k;ka

ys[kk ijh{kdksa dh fjiksVZ

rqyu i=] ykHk ,oa gkfu ys[kk vkSj vuqlwfp;k¡

eq[; ys[kkdj.k uhfr;ka

ys[kksa ij fVIif.k;ka

ys[kk ijh{kdksa dh fjiksVZ

vfrfjDr izdVhdj.k

1 Chairman's Message 4

7 MD & CEO’s Message 10

14 Directors’ Report 15

26 Management Discussion and Analysis 27

100 Report on Corporate Governance 101

138 Auditors’ Certificate on Corporate Governance 139

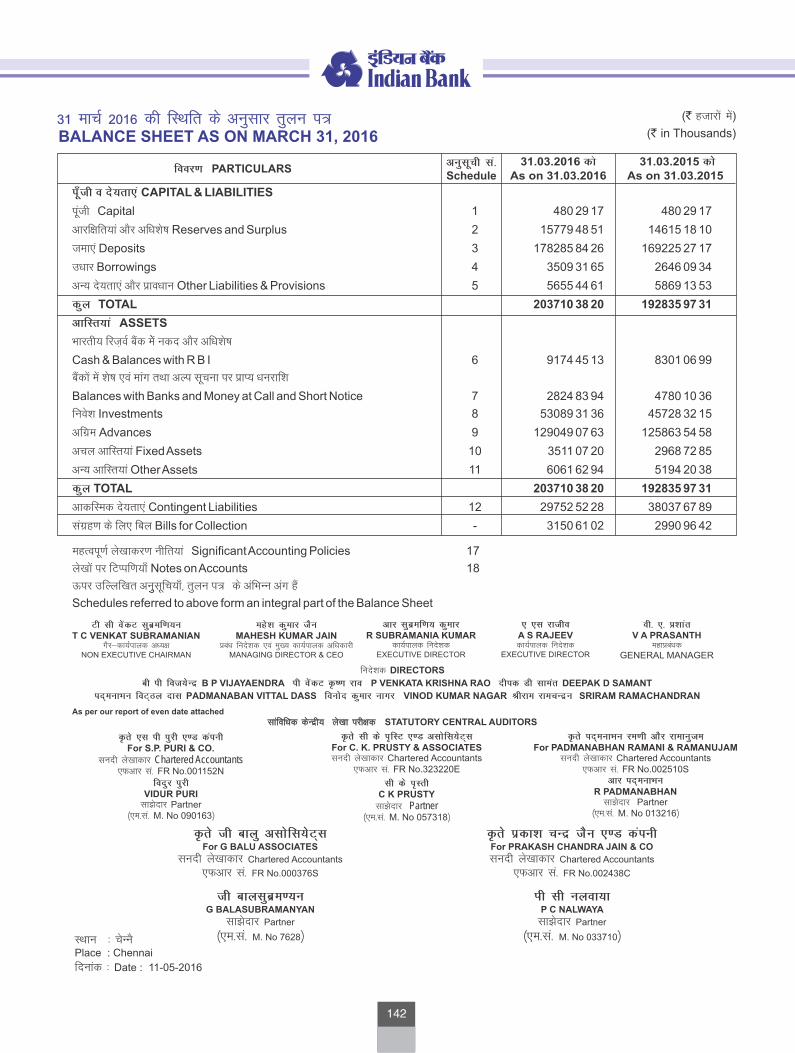

142 Balance Sheet, Profit and Loss Account and Schedules 142

152 Significant Accounting Policies 153

162 Notes on Accounts 163

224 Auditors’ Report 225

228 Balance Sheet, Profit and Loss Account and Schedules 228

236 Significant Accounting Policies 237

250 Notes on Accounts 251

276 Auditors’ Report 277

Additional Disclosures 279

. 254-260, No.254-260, Avvai Shanmugam Salai

Royapettah

– 600 014 Chennai - 600 014

044 28134076; Fax No.044 28134075 Tel No. 044 28134076; Fax No. 044 28134075

: [email protected] E – Mail : [email protected]

, Subramanian Building, 1, Club House Road

– 600 002 Chennai - 600 002

044 28460718; . 044 28460129 Tel No. 044 28460718; Fax No. 044 28460129

: [email protected] E – Mail : [email protected]

foRrh; fooj.k & bafM;u cSad

lesfdr foRrh; fooj.k

� �

� �

� �

� �

� �

� �

� �

� �

278

:

bafM;u cSad

la[;k vOoS "k.eqxe lkyS

jk;isV~Vk

psUuS

nwjHkk"k la

bZ&esy

'ks;j varj.k ,tsaV

dsfe;ks dkWiksZjsV lfoZlst+ fyfeVsM

;wfuV% bafM;u cSad

lqczef.k;u fcfYMax] 1 Dyc gkml jksM

psUuS

nwjHkk"k la- QSDl la

bZ&esy

1

vè;{k dk lans'k

fç; 'ks;jèkkjdksa]

eq>s vkids cSad ds foÙkh; o"kZ 2015&16 dh okf"kZd fjiksVZ çLrqr djrs gq, vfr

çlUurk gks jgh gSA

loZçFke eSa cSad ds çfr vkids vfojr foÜokl] leFkZu ,oa fu"Bk ds fy, xgu

vkHkkj O;ä djrk gw¡ A vius dk;Zdky ds 109 osa o"kZ dh lekfIr ij blds

vf[ky Hkkjrh; usVodZ esa o`f) ,oa Hkkjr Hkj esa vius 'kk[kk usVodZ dks c<kus ds

fy,] cSafdax lsokvksa ls oafpr vkSj de cSafdax lsok,a çkIr {ks=ksa rd viuh igq¡p

dks c<kus ds fy, cSad us orZeku o"kZ esa 153 'kk[kk,a vkSj 440 ,Vh,e@ch,u,

[kksys gSa ftles 2562 ikjaifjd 'kk[kk,¡ ,oa 2784 ,Vh,e ¼blesa udnh

jhlkbfDyax dk;Z{kerk ls ;qä 253 cap uksV ,DlsIVj Hkh lfEefyr gSa½ lfgr

dqy 5346 lqiqnZxh pSuy jgs A

eq>s ;g crkrs gq, vfr çlUurk gks jgh gS fd o"kZ 2015&16 ds nkSjku cSad us]

u dsoy Hkkjrh; vFkZO;oLFkk dh pqukSfr;ksa dk lkeuk djrs gq, vius vk?kkr

lgus ds lkeF;Z dks n'kkZ;k gS] cfYd lkFk gh jk"Vªh; y{;ksa ds varxZr çkFkfed

{ks= ds çR;sd Js.kh ds rgr _.k nsus esa csgrj çn'kZu djus dh fujarjrk dks

cuk, j[kk gS] tSls çkFkfed {ks= esa vfxzeksa ds varxZr 40-85 ¼vfuok;Z 40 ½

dk Lrj] —f"k esa 18-68 ¼18 ½] detksj oxksZa dks vfxze 11-30 ¼10 ½ ,oa

,e,l,ebZ ds varxZr lw{e m|eksa ds fy, 8-12 ¼7 ½ dk _.k çnku fd;k

x;k gSA

oSfÜod vkfFkZd ifjçs{; esa olwyh dh çfØ;k rks tkjh gS ijarq ;g çfØ;k èkheh

,oa nqcZy xfr ds lkFk vkxs c<+ jgh gS A oSfÜod fodkl ds ifjis{; esa o"kZ 2016

dk ç{ksi.k fiNys o"kZ ds leku gh ekewyh ¼3-2 çfr'kr½ jgk gSA eq[;r% mHkjrs

cktkj ,oa fodkl'khy vFkZO;oLFkk esa vkbZ rsth ds dkj.k nckoxzLr vFkZO;oLFkk

dh fLFkfr èkhjs&èkhjs lkekU; gks jgh gS] ftlds ifj.kkeLo:i o"kZ 2017 esa olwyh

çfØ;k dks cy nsrs gq, 3-5 çfr'kr ,oa mlls vfèkd dh olwyh dk iwokZuqeku

yxk;k x;k gSA

% %

% % % %

% %

oSfÜod & vkfFkZd ifj–';

o"kZ 2017 ds i'pkr oSfÜod fodkl esa o`f) dk vuqeku gS tks o"kZ 2021 dh var

rd 4 çfr'kr ds vanj jgsxh] tks vkusokys le; esa mHkjrs ckt+kj ,oa

fodkl'khy vFkZO;oLFkk ear vkusokyh rsth dks fodkl dks n'kkZ jgh gSA

;g ifj.kke mu leLr egRoiw.kZ vuqekuksa ij fuHkZj djrk gS tks c`gr

vèkkstksf[ke ds fo"k; ls lac) gS tSls bl le; ncko esa py jgs

dbZ vFkZO;oLFkkvksa dh fLFkfr esa èkhjs&èkhjs gks jgs lqèkkj] i.;ksa ds fu;kZr esa gks

jgs lqèkkj] phu dh vFkZO;oLFkk dk lQy iqulZarqyu ,oa vU; mHkjrs cktkj

rFkk fodkl'khy vFkZO;oLFkkvksa dh vk?kkr&lg o`f) A bl lanHkZ esa] oSfÜod

fodkl dh xfr dks rhoz djus esa egRoiw.kZ Hkwfedk vnk djusokys ,oa rhoz

xfr ls fodflr gksusokys phu ,oa Hkkjr tSls ns'kksa dk oSfÜod egRo èkhjs&èkhjs

c<+sxk A

vkèkkjHkwr lhfer ekax rFkk ,d laHkkO; o`f) esa O;kid Lrj ij deh ds

rgr mUur vFkZO;oLFkkvksa esa o`f) visf{kr gSA laHkkO; o`f) esa deh ds

eq[; dkjd] c<+rh gqbZ tula[;k] tksfd orZeku nj ij Je cktkj

Hkkxhnkjh ij jkstxkj çpyu dks de dj nsxh( fuf"Ø; fuos'k rFkk dqy

?kVd mRikndrk o`f) esa deh vkfn gSaA laHkkfor vkmViqV c<+krs le;]

;g {kf.kd vuqeku O;kid i‚fylh çfrfØ;k dh vR;ko';drk dks c<+krk gS

rFkk vuqj{kk dk çcaèku djrk gSA mPp rFkk nh?kZdkfyd o`f) lqfuf'pr djus ds

fy, lajpukRed lqèkkj] lrr ekSfæd uhfr la;kstu] rFkk jktdks"kh; foLrkj

i‚fylh dh çkFkfedrk,a gSaA

Hkfo"; esa] oSfÜod vFkZO;oLFkk esa lqèkkj dh bl xaHkhj fLFkfr esa tksf[ke

dh laHkkouk gksus ij o`f) dks çksRlkfgr djus ds fy, cgqi{kh; dk;Z&;kstukvksa

dh vko';drk gSA cM+h vFkZO;oLFkkvksa esa vfrfjä uhfrxr dkjZokb;ksa dh

igpku gksuh pkfg, tksfd 'kh?kz gh dk;kZfUor gks ldsa A ;fn ;g ladsr gksa fd

oSfÜod udkjkRed tksf[kesa ewrZ :i ysus okyh gSa] rks mHkjrh gqbZ vFkZO;oLFkkvksa

ls tks mPp mipr uqd+lkuksa ls de‚fMVh ,DLiksVZjksa dks lqjf{kr djus ds fy,

rFkk xSj vkfFkZd uqd+lkuksa ls vkfFkZd Iyouksa ls lqj{kk djus ds fy, oSfÜod

foÙkh; ra= etcwr cuk;k tkuk pkfg,A

Jh Vh lh osadV lqczef.k;kuxSj&dk;Zikyd vè;{k

vFkZO;oLFkk ds {ks= esa Hkkjrh; vFkZO;oLFkknqfu;k esa lcls rsth ls fodflr gksusokysvFkZO;oLFkk esa ls ,d cudj] oSfÜodvFkZO;oLFkk ds {ks= esa ,d csgrjhu eqYd ds:i esa mHkjk gSA

“

2

bl mHkjrs cktkj ,oa fodkl'khy vFkZO;oLFkkvksa ls o"kZ 2017 esa oSfÜod fodkl

ds {ks= esa] vfxze vFkZO;oLFkk ds varxZr 2-0 çfr'kr dh rqyuk esa 4-6 çfr'kr ds

iwokZuqekfur o`f) ds lkFk] lokZfèkd ;ksxnku dh vis{kk fd;k tk jgk gSA oSfÜod

O;kikj o`f) lkekU; jgus dh mEehn gS ijarq mHkjrs cktkj ,oa fodkl'khy

vFkZO;oLFkk ds {ks= esa eq[;r% ?kjsyw ekax esa gks jgh O;kid o`f) ds ifj.kke Lo:i

oSfÜod O;kikj o`f) esa 2016 ls èkhjs – èkhjs o`f) gks jgh gSA

vFkZO;oLFkk ds {ks= esa Hkkjrh; vFkZO;oLFkk nqfu;k esa lcls rsth ls fodflr

gksusokys ns'kksa esa ls ,d cudj oSfÜod vFkZO;oLFkk ds {ks= esa ,d csgrjhu

eqYd ds :i esa mHkjk gSA dbZ dkjd Hkkjr dks ,d mHkjrk cktkj cukrs gSa A

Hkkjr ,d cM+k rsy vk;krd ns'k gS ,oa rsy dh dherksa esa fxjkoV ls eqækLQhfr

dks de djus esa enn feyh gSA gky gh esa ldy ?kjsyw mRikn ¼thMhih½ esa gks jgs

fodkl ls lac) vkadM+s dsaæh; lkaf[;dh dk;kZy; }kjk tkjh fd;k x;k tks ;g

n'kkZrk gSa fd ekpZ 2016 dks lekIr frekgh esa Hkkjr dh vFkZO;oLFkk esa 7-9

çfr'kr dh o`f) gqbZ gS tks fiNyh frekgh dks mikftZr 7-2 çfr'kr dh o`f) dh

rqyuk esa ,d Rofjr fodkl dks n'kkZrk gS A foÙkh; o"kZ dh pkSFkh frekgh ds

l'kä çn'kZu ds ifj.kke Lo:i o"kZ 2014&15 ds iwjs o"kZ dk fodkl nj 7-2

çfr'kr ls c<+dj 7-6 çfr'kr] 2013&14 dk 6-6 çfr'kr ,oa 2012&13 dk 5-6

çfr'kr gks x;kA ;g o`f) blfy, mYys[kuh; gS D;ksafd ,d nh?kZdkfyd ,oa

O;kid lw[ks ds ckotwn bls çkIr fd;k x;k Fkk ftlus fuf'pr :i ls xzkeh.k

ekax de fd;k Fkk A

iwjs o"kZ ds fy, ldy ewY; laofèkZr ¼thoh, ½ cqfu;knh ewY;ksa esa çkofèkd 7-2

çfr'kr dh o`f) gqbZ gS] ftlesa fiNys o"kZ 2014&15 dks dsoy 7-1 çfr'kr dh

o`f) gqbZ Fkh] tks Hkkjrh; fjtoZ cSad }kjk iwokZuqekfur 7-4 çfr'kr dh o`f) dh

rqyuk esa de gSA thoh, ds vkadM+sa blfy, egRoiw.kZ gS D;ksafd ;g fn[kkrh gS fd

;s dj ,oa lfClMh ldy thMhih ij egRoiw.kZ çHkko Mkyrh gSA

orZeku frekgh rFkk 'ks"k o"kZ dh laHkkouk,a cgqr dqN bl o"kZ ds ekulwu ij

fuHkZj gSa A çFker% o"kkZ dh çek=k ij rFkk vkxs HkkSxksfyd o ekSleh forj.k ij]

oSls gh dqN fuos'k çksRlkgu çnku djus dh ft+Eesnkjh vfèkd yksd O;; ykxr

ij fuHkZj gksxk D;ksafd futh {ks= esa fuos'k de gqvk gS rFkk iqu#Tthou ds fy,

dksbZ mik; ugha gSA

ljdkj dh ^esd bu bafM;k*] ^LVSaM vi bafM;k*] ^LVkVZ vi bafM;k* ,oa ^fMftVy

bafM;k* rFkk lkrosa osru vk;ksx ds dk;kZUo;u tSlh igyksa ds ifj.kke

Lo:i vFkZO;oLFkk esa rsth vkus dh vis{kk gSA Hkkjr ljdkj dk nwljk

eq[; eqík xzkeh.k vFkZO;oLFkk dks iqu#Tthfor djuk gS tks ns'kHkj esa LFkkfud

o"kkZ ,oa xaHkhj lw[ks ds dkj.k vfèkd fodkl ugha fn[kk ikbZA Hkkjrh;

?kjsyw vkfFkZd ifjçs{;–

ekSle foKku foHkkx ¼vkbZ,eMh½ us iwjs ns'k esa lkekU; ckfj'k gksus ds ldkjkRed

ladsr fn, gSa tks vFkZO;oLFkk dks c<+kok nsxh ,oa vfèkd xzkeh.k ekax Hkh l`ftr

djsxhA

fcxM+rh vkfLr xq.koÙkk rFkk mlds dkj.k cSadksa dh _.k tksf[ke lafoHkkx ij

vlj o"kZ 2015&16 cSafdax {ks= ds fy, fo{kqCèk jgk gSA vkfLr xq.koÙkk dh

pqukSfr;ka i.; ewY;ksa esa Hkko dks de djus ls rFkk vkfFkZd gsMfoaM esa o`f) gks xbZ

gS tksfd çeq[k {ks= tSls ewyHkwr lajpuk] fctyh] LVhy rFkk fuekZ.k ij vlj

Mkyk gS A

vkfLr xq.koÙkk esa fxjkoV csly ds vuqikyu esa] ykHk çnÙkk rFkk

iwath vko';drkvksa ij vlj Mkyrk gS A cSafdax {ks= ds fy, vU; pqukSfr;k¡

rFkk y?kq foÙk rFkk isesaV cSadksa dk ços'k fj[Fk foghu fMftVy IySVQ+keZ dk

leFkZu] ;qok deZpkfj;ksa }kjk ukSdjh NksM+uk rFkk vuqHkoh LVkQ dh lsokfuo`fÙk

d‚ikZsjsV {ks= dks c‚UMksa rFkk okf.kT; i=ksa ds tfj;s fufèk;ksa ds oSdfYid lzksrksa

dh miyCèkrk dh eè;LFkrk can gksuk bR;kfn gSA cSafdax ykHk çnrk ij nwljh

çeq[k pqukSrh gS vUrjkf"Vª; foÙkh; fji¨ÉVx ekud vkbZ,Q+vkj,l dk

dk;kZUo;u A

foÙkh; o"kZ 2016 esa lHkh vuqlwfpr okf.kT; cSadksa esa _.k dh o`f) 11-3 çfr'kr

rd c<+h] tcfd fiNys o"kZ esa tks 9-0 çfr'kr jgk gS rFkk tekvksa dh o`f) fiNys

o"kZ ds 10-7 çfr'kr ls bl foÙkh; o"kZ esa 9-9 çfr'kr rd ?kVh A

bl ifj–'; esa eSa çeq[k {ks=ksa esa] cSad }kjk fd, x, fu"iknu ds eq[; ckrksa dk

voyksdu djuk pkgrk gw¡A

cSad ds dkjksckj dh fLFkfr o"kZ ds nkSjku #i;s 3]00]000 djksM+ ds ekby

LVksu dks ikj dj fy;k gS A 31 ekpZ 2016 dks lekIr o"kZ ds fy, dkjksckj

4-31 çfr'kr c<+dj #i;s 3]10]918 djksM+ gks x;k] tcfd tekvksa esa o`f)

#i;s 9061 djksM+ ls c<+h gS ;k 5-35 dh o`f) ls #i;s 1]78]286 djksM+ gks

x;k gS A vfxze esa #i;s 3800 djksM+ dh o`f) gqbZ gS ;k 2-95 çfr'kr dh

o`f) ls #i;s 1]32]632 djksM+ gks x;k gSA

cSad dk ifjpkyuxr ykHk #i;s 3032 djksM+ jgk] tcfd fuoy ykHk #i;s

711 djksM+ gS A

cSad dh fuoy ekfy;r #i;s 13]478 djksM+ rd c<+ xbZ gS A

III

�

�

�

cSafdax {ks= ds fu"iknu

dkjksckj rFkk foÙkh; miyfCèk;ka

:

:

3

�

�

çfr 'ks;j vk; ¼okf"kZd—r½ rFkk çfr 'ks;j vafdr ewY; Øe'k% #i;s 14-81

vkSj #i;s 280-63 jgk A fiNys foÙkh; o"kZ 2015&16 ds fy, bfDoVh ij

çfrykHk 5-46 çfr'kr jgk A

ekpZ 2016 ds var esa csly III ds vèkhu cSad dh foÙkh; fLFkjrk lhvkj,vkj

¼tksf[ke Hkkfjr vkfLr dh rqyuk esa iwath dk vuqikr½ ds vuqlkj 13-20

çfr'kr ij etcwr Fkk A cSad bl vuqikr ds lacaèk esa yxkrkj f'k[kj fLFkfr

ij gS rFkk i;kZIr :i ls iwath çkIr gS A

eq>s ;g lwfpr djus esa g"kZ gks jgk gS fd cSad ds funs'kd e.My us 15 çfr'kr ds

ykHkka'k dh ?kks"k.kk dh gS A 4-25 djksM+ xzkgdksa ls çkIr foÜokl gesa yxkrkj dbZ

o"kksZa esa csgrj fu"iknu djus ds fy, çsfjr fd;k gS A

cSad dk è;ku blij dsfUær gksxk fd ,e,l,ebZ eè; d‚ikZsjsV] [kqnjk vkSj —f"k

dks igpkudj _.k] y?kq ,oa eè;e m|e vkSj [kqnjk xzkgdksa dks çnku djus ls

lEiw.kZ _.k cgh esa o`f) gksxh] rkfd bl foÙkh; o"kZ esa _.k dh o`f) dk pkyd

cus A [kqnjk _.k cgh rsth ls c<~us okys ,e,l,ebZ {ks= ij fuHkZj gksdj vkokl

_.k ls lq–<+ cusxk A vc ljdkj ls bl {ks= dks fn;s tkusokys t+ksj ls

,e,l,ebZ dk Hkfo"; mTtoy gS A

vkxs Hkfo"; dh vksj

[kqnjk ,oa eè;e d‚ikZsjsV {ks= ij dsUæh; è;ku gksus ds fy, cSad bu çeq[k {ks=ksa esa

ofVZdYl cukus dh çfØ;k esa gS ;Fkk _.k dks lfEefyr dj caèkd _.k] eè;e

{ks= esa ,e,l,ebZ rFkk eè;e d‚ikZsjsV _.k dks lfEefyr dj vkSj vU; [kqnjk

_.k esa —f"k] y?kq ,oa lw{e m|e dks lfEefyr dj A

gekjs 'ks;j èkkjdksa] xzkgdksa] fgrSf"k;ksa ds vuojr leFkZu vkSj gekjs deZpkfj;ksa ds

vFkd ç;klksa ls vkSj lkFk gh Hkkjr ljdkj vkSj Hkkjrh; fjtoZ cSad ls leFkZu ds

dkj.k eq>s foÜokl gS fd vkidk cSad mR—"Vrk ds f'kdkj ij igq¡pus gsrq lnSo

ç;kljr jgsxk A

'kqHkdkeukvksa ds lkFk

vkidk

Vh lh osadV lqczef.k;u

xSj&dk;Zikyd vè;{k

4

Chairman’s Message

It gives me immense pleasure to present the Annual Report of

your Bank for the Financial Year 2015-16.

At the outset, I would like to express my deep sense of

gratitude for your continuous trust, support and loyalty

extended to the Bank. On the eve of completion of its

109 year of operations, Bank had opened 153 branches and

440 ATMs / BNAs in the current year to touch 5346 delivery

points, including 2562 Brick & Mortar branches and

2784ATMs (including 253 Bunch Note acceptors enabled with

cash recycling functionality), towards enhancing its -India

network and to extend its reach to the under-banked and

unbanked areas.

I am pleased to report that during the year 2015-16, Bank not

only displayed its resilience to challenges in the Indian

economy, but also sustained its performance by surpassing

the National goals under Priority Sector lending for each

category viz., Level of 40.85% (Mandatory 40%) under Priority

Sector advances, 18.68% (18%) in Agriculture, 11.30% (10%)

for Advances to weaker sections and 8.12% (7%) in lending to

Micro Enterprises under MSME.

From the global economic perspective, the recovery

continues, but at a slow and increasingly fragile pace.

Projection for global growth in 2016 is a modest 3.2%, broadly

in line with last year. The recovery is projected to strengthen in

2017 to 3.5% and beyond, driven primarily by emerging

market and developing economies, as conditions in stressed

economies start to normalize gradually.

Global growth is projected to increase further beyond 2017, to

just below 4% by the end of the forecast horizon in 2021,

th

pan

Dear Shareholders,

Economic overview - Global

reflecting a further pickup in growth in emerging market and

developing economies. This outcome relies on a number of

important assumptions which are subject to sizable downside

risks viz., gradual normalization of conditions in several

economies currently under stress, pickup in activity in

commodity exporters, successful rebalancing of China's

economy and resilient growth in other emerging market and

developing economies. In this context, the gradual increase in

the global weight of fast-growing countries such as China and

India would also play a role in boosting global growth.

Growth in advanced economies is expected to be modest

under the baseline, reflecting subdued demand and a broad-

based weakening of potential growth. The main factors

underlying the weakening in potential growth are population

aging, which would reduce trend employment at current rates

of labour market participation, sluggish investment and

weakening of total factor productivity growth. This fragile

conjuncture increases the urgency of a broad-based policy

response that safeguards near-term growth, while raising

potential output, and manages vulnerabilities. The policy

priorities for securing higher and sustainable growth are:

structural reforms, continued monetary policy accommodation

and fiscal expansion.

Going forward, there is a need for multilateral actions to boost

growth while containing risks at this critical stage of global

recovery. In the larger economies there should be proactive

identification of additional policy actions that could be

implemented quickly if there are signs that global downside

risks are about to materialize, global financial safety net

should be strengthened to protect emerging economies who

are commodity exporters from high susceptible shocks and

protecting economies from spillovers from non-economic

shocks.

Shri. T C Venkat SubramanianNon-executive Chairman

The Indian Economy has emerged as

a in the world economy,

becoming one of the fastest growing

economies in the world.

'bright spot'

“

5

Emerging and Developing Economies are expected to

contribute lion's share in the global growth in 2017 with a

projected growth of 4.6% as compared to 2.0% growth in

Advanced Economies. Global trade growth is projected to

remain moderate but to pick up gradually from 2016 onward,

primarily reflecting stronger growth in domestic demand in

emerging market and developing economies.

The Indian economy has emerged as a bright spot in the world

economy, becoming one of the fastest growing economies

in the world. Several factors make India an attractive emerging

market. India is a net oil importer and the decline in oil prices

has helped in bringing the inflation down. The latest

Gross Domestic Product (GDP) growth data released by the

Central Statistics Office show that India's economy expanded

by 7.9% in the three months ended March 2016, a sharp

acceleration from the marginally downsized 7.2% achieved in

the preceding quarter The result of the strong fiscal

fourth-quarter performance is that growth for the full year was

lifted to 7.6%, from 7.2% in 2014-15, 6.6% in 2013-14 and

5.6% in 2012-13. This growth is noteworthy, having been

achieved despite a prolonged and widespread drought, which

would certainly have dampened rural demand

Gross Value Added (GVA) at basic prices provisionally grew

7.2% for the full year, barely improving from the 7.1% posted in

2014-15, and slower than the Reserve Bank of India's

projection for 7.4% growth. The GVA figure is significant

because it strips the impact that taxes and subsidies have on

the overall GDP number.

The outlook for the current quarter and the rest of this year may

hinge a lot on this year's monsoon: firstly, in terms of the

volume of rainfall, and then critically in its geographical and

seasonal distribution. Similarly the onus of providing some

investment stimulus may depend on increased public

expenditure outlays in as much as private sector investment

having slowed and showing barely any signs of revival.

Government's various initiatives such as

, and and the

implementation of the Seventh Pay Commission is expected

to boost demand in the economy. Another key focus of the

Government of India is to revive the rural economy which has

not shown a major growth owing to severe drought across the

country and spatial rainfall. Given the positive indication of

.

.

'Make in India',

'Stand Up India' 'Start Up India' 'Digital India'

Economic overview - Domestic

normal monsoon across the country as per Indian

Meteorological Department (IMD), growth in agriculture is

expected, which would boost the economy and would also

create more rural demand. The movement of both the rural

and urban demand would shape the economic growth in the

long run and help reach the potential 8 per cent growth.

For the banking sector, the year 2015-16 had been a turbulent

one due to worsening asset quality and its implication on the

credit risk profile of banks. The asset quality challenges have

been exacerbated by softening commodity prices and

economic headwinds (both domestic and international),

which have significantly impacted key sectors such as

infrastructure, power, steel and construction.

Bank's Business level crossed the milestone of

3,00,000 crore during the year. The Business grew by

4.31% to 3,10,918 crore for the year ended March 2016.

While Deposits grew by 9061 crore or 5.35 % to

1,78,286 crore, Advances grew by 3800 crore or

2.95 % to 1,32,632 crore.

Operating profit of the Bank was at 3032 crore while

Net Profit stood at 711 crore.

Networth of the Bank increased to 13,478crore.

�

�

�

`

`

`

` `

`

`

`

`

,

Performance of Banking Sector:

Bank's Business and FinancialAchievements

Deterioration in asset quality has an impact on profitability and

capital requirement for Basel III compliance. The other

challenges for banking sector are the entry of Small Finance

and Payment banks backed by digital platforms with zero

legacy, attrition of young employees and retirement of

experienced staff, disintermediation with availability of

alternate sources of funds to corporate sector through bonds

and Commercial Papers. Another important challenge on

banks' profitability is the implementation of International

Financial Reporting Standards (IFRS).

In FY 2016, credit growth of all Scheduled Commercial Banks

improved to 11.3% as against 9.0% in the previous year while

Deposits growth declined from 10.7% in the previous year to

9.9% in FY 2015-16.

Against this backdrop, I would like to give an overview of the

Bank's performance in important parameters.

6

�

�

Earnings per share (annualised) and Book Value per

share were at 14.81 and 280.63 respectively. Return

on Equity was at 5.46 % for FY 2015-16.

Bank's financial soundness as reflected by the CRAR

(Capital to Risk weighted Assets Ratio) was strong with

CRAR at 13.20% under Basel III as at end March 2016.

Bank is consistently at the top in respect of this ratio and is

sufficiently capitalized.

I am also happy to inform you that the Board of Directors of the

Bank has recommended a dividend of 15%. The confidence of

4.25 crore customers has inspired us to put in consistently

better performance year after year.

The focus of the Bank would be to push credit to small and

medium enterprises and retail customers to grow the overall

loan book by identifying MSME, Mid corporate, retail and

agriculture as the drivers of credit growth for the current

Financial Year. The retail loan book will in turn be driven by

housing loans with reliance on fast-growing MSME sector

where prospects are high given the attention this sector is

receiving from the Government.

` `

Looking ahead

For a dedicated focus on Retail & Mid Corporate segment, the

bank is in the process of creating Verticals in three major

areas, viz., Mortgage loans including Home loans, Mid

Segment comprising of MSME and Mid Corporate loans and

Other Retail Loans including Agriculture, Small and Micro

Enterprises.

With the continued support of our shareholders, customers,

well-wishers and the unrelenting efforts of our employees,

together with the support of the Government of India and the

Reserve Bank of India, I am sure, your Bank will continue to

strive to move ahead in its quest for excellence.

With best wishes

Yours sincerely

T C VENKAT SUBRAMANIAN

NON-EXECUTIVE CHAIRMAN

7

cSad us eè;e ls nh?kZdkfyd ;kstuk ds rgr

ds lkFk&lkFk^^ ds :i esa [kqn dks LFkkfir djus dh

ifjdYiuk dh gSA

^^[kqnjk vkSj eè; d‚ikZsjsV lsxesaV ijè;ku nsus eè; vkdkj dscSad

Jh egs'k dqekj tSu

“

fç; 'ks;jèkkjdkss]

vkids cSad dh foÙkh; o"kZ 2015&16 dh okf"kZd fjiksVZ çLrqr djrs gq, eq>s cgqr

çlUurk gks jgh gSA bl volj ij] eSa vkids lrr leFkZu rFkk fu"Bk dk vkHkkj

O;ä djuk pkgrk gw¡ ftlus cSad dks m|ksx esa vius csgrj fu"iknu rFkk mÙke

jhfr ls çfr"Bk cuk, j[kus esa] fo'ks"kr% foijhr vfLFkj cSafdax ifjos'k esa bldh

ykHkçnrk dks cuk, j[kus esa leFkZ cuk;k gSA

foÙkh; o"kZ 2015&16 ds nkSjku oSfÜod vFkZO;oLFkk us nksuksa fojklrksa oSfÜod

foÙkh; ladV rFkk vusd ubZ pqukSfr;ksa }kjk ckfèkr] ean o vleku xfr ds lkFk

o`f) dhA ifj.kke Lo:i detksj oSfÜod ifjos'k us viuk çHkko ?kjsyw

vFkZO;oLFkk ij NksM+kA pwafd cSafdax {ks= cfgtkZr uqd+lkuksa ds çfr vlqjf{kr

jgrk gS] cSadksa ls _.k dh gYdh ekax jgh ftlls vFkZO;oLFkk dh ean xfr rFkk

nckoxzLr vkfLr;ksa esa c<+ksÙkjh gqbZA bl dkj.k _.k lqiqnZxh esa ckèkk gqbZAA

vFkZO;oLFkk us Hkkjr ljdkj }kjk fofHkUu eè;orÊ uhfr;ksa o dkuwuh vfèkfu;e

ds ekè;e ls miyCèk djkbZ xbZ o`f) dh vksj è;ku dsfUær fd;k rFkk iqu#RFkku

ds ladsrksa dks çksRlkgu iwoZd çnf'kZr djuk vkjaHk dj fn;k gSA

çxfr dh vksj laLFkk dks etcwr] l{ke o nq#Lr cukus ds fy,] cSad us bl o"kZ

cgqr ls ehy ds iRFkjksa dks ikj fd;k gSA eq>s vkidks lwfpr djrs gq, çlUurk gks

jgh gS fd cSad us foÙkh; o"kZ 2015&16 esa 3]00]000 djksM+ O;kikj ds ehy ds

iRFkj dks ikj dj fy;k gSA vxj iwath dh ckr djsa rks cSad yxkrkj ykHk vftZr

djrs gq, vkRefuHkZj jgk rFkk 2007 ls vius 'ks;j èkkjdksa dks ykHkka'k forfjr

djrs gq, viuh fiNyh miyfCèk;ksa dks cuk, j[kkA

,sls pqukSrhiw.kZ ifjos'k ds chp] cSad us vius [kqnjk O;kikj dh vksj è;ku dsfUær

djrs gq, j.kuhfrd ç;kl ds :i esa viuh _.k cfg;ksa dks lesfdr fd;k gSA

tekvksa dh ykxr dks de djus dh fn'kk esa] dklk esa o`f) ij fo'ks"k è;ku

dsfUær djrs gq,] [kqnjk tekvksa ds vuqikr esa o`f) djrs gq, lalkèku ds la?kVu

esa c<+ksÙkjh gsrq çcq) fu.kZ; fy;k x;kA —f"k ,oa ,e,l,ebZ esa cSad dh lkeF;Z

dks lq–<+ cukus ds fy,] caèkd _.k rFkk fofHkUu vU; [kqnjk _.kksa ds vykok bu

ikjaifjd {ks=ksa ij fo'ks"k è;ku dsfUær djrs gq, [kqnjk O;kikj esa lqèkkj ykus ds

fy, _.k esa o`f) fo'ks"k :i ls fuèkkZfjr fd;k x;k y{; FkkA blds vfrfjä]

vkfFkZd ifj–';

vkids cSad dk fu"iknu

`

o`f)'khy xSj fu"ikfnr vkfLr;ksa dh 'kh?kz igpku] e‚fuVfjax lqèkkjkRed dk;Z

;kstukvksa] lk>k dh xbZ tkudkjh ds ekè;e ls fu;af=r djrs gq, rFkk Hkfo"; esa

blds vkorZu dks jksddj vkfLr xq.koÙkk cuk, j[kus dks lokZsPp çkFkfedrk nh

xbZA

bl i`"BHkwfe esa] eSa eq[; ekin.Mksa esa cSad ds fu"iknu dh eq[; ckrksa dks çLrqr

djuk pkgrk gw¡A

ekpZ 2016 dks lekIr o"kZ esa tekvksa esa 9061 djksM+ ¼5-35 ½ dh o`f) ntZ

djrs gq, 1]78]286 djksM++ rFkk vfxzeksa esa 3800 djksM+ ¼2-95 ½ dh o`f)

ntZ djrs gq, 1]32]632 djksM+ dh o`f) ds lkFk dkjksckj 4-31 c<+dj

3]10]918 djksM gks x;kA

cSad dk lq–<+ iwathdj.k vkfLr;ksa@ifjlaifÙk;ksa ls lacafèkr tksf[keksa dks

nwj j[kus esa cgqr cM+h Hkwfedk fuHkkrk gSA ekpZ 2016 ds var esa cslsy ds

rgr 13-20 lhvkj,vkj ds lkFk] bl vuqikr ds lacaèk esa m|ksx esa cSad

yxkrkj f'k[kj ij jgkA 2015 esa Hkkjr ds mR—"V cSadksa dh Qkbusaf'k;y

,Dlçsl jSafdax ds ekunaMksa ij iwath i;kZIrrk rFkk LFkk;h iwath ¼ ½ ds

rgr lkoZtfud cSadksa esa cSad çFke LFkku ij jgkA

de ykxr pkyw [kkrk vkSj cpr [kkrk ¼dklk ns'kh ½ tekvksa ds vuqikr ds

lkFk i;kZIr lalkèku çksQ+kby 31-94 ds Lrj rd igqapk x;k tks 14-81

çfr'kr dh o"kZ&nj&o"kZ o`f) ls ;g 55]153 djksM+ #i, gks xbZ gSA dklk

o`f) cSad dks jk"Vªh;—r cSadksa esa pkSFks LFkku ij vkus esa ennxkj cuk;kA

cpr cSad tekvksa ¼ns'kh½ esa 15-57 çfr'kr dh o"kZ&nj&o"kZ o`f) ls ;g

46]407 djksM+ #i;s gks xbZ gSaA

31-03-2016 rd dqy tek ds yxHkx 83 çfr'kr [kqnjk tek dh mPp

vuqikr] cSad ds etcwr czkaM ewY; dk ladsr FkkA

�

�

�

�

�

�

�

%

%

%

III

%

%

]

foÙkh; fof'k"Vrk,a

`

` `

`

`

`

`

foRrh; o"kZ 2015&16 esas cSad dk ifjpkyuxr ykHk 3032 djksM jgk

tcfd fuoy ykHk 711 djksM Fkk A

jk"Vªh;—r cSadksa ds chp vkfLr;ksa ij 0-36 izfr'kr izfrykHk yxkrkj

loZJs"B jgkA

çcaèk funs'kd ,oa eq[; dk;Zikyd vfèkdkjh dk lans'k

çcaèk funs'kd ,oaeq[; dk;Zikyd vfèkdkjh

8

�

�

�

�

�

�

�

�

�

�

o"kZ 2015&16 ds nkSjku tekvksa dh ykxr lapkyu gsrq ,d etcwr vkèkkj

çnku djus ds fy, ] cSad è;kuiwoZd [kqnjk tek ij è;ku dsafær dj jgk gS

vkSj bl çfØ;k esa 5782 djksM+ #i;s ds mPp ykxr Fkksd tekvksa ¼ihMh ,oa

lhMh½ esa vkuqikfrd rkSj ij deh dh gSA

Hkkjr ljdkj }kjk fuèkkZfjr jkf"Vª; y{;ksa dks çkIr djuk] cSad ds ,tsaMk esa

lokZsPp Fkk vkSj fuèkkZfjr ekun.Mksa dks gkfly fd;k x;k vFkkZr çkFkfedrk

{ks= ds vfxzeksa tksfd #i;s 50]333-52 djksM+ ij lek;ksftr fuoy cSad

_.k ¼,,uchlh½ dk 40-85 çfr'kr Fkk vkSj —f"k _.kn tksfd #i;s

23]017-56 djksM+ ij lek;ksftr fuoy cSad _.k ¼,,uchlh½ dk 18-68

çfr'kr FkkA

ns'kHkj esa cSad dh 73 fo'ks"kh—r 'kk[kk,a gSa tks vuU; :i ls lw{e] y?kq vkSj

eè;e m|e ¼,e,l,ebZ½ {ks= dh vko';drkvksa dh iwfrZ djrh gSaA

,e,l,ebZ lafoHkkx esa #i;s 18]642-95djksM+ ls 12-81çfr'kr dh c<ksÙkjh

gqbZ vkSj ;g#i;s 21]031-56djksM jgkA

31 ekpZ 2016 dks ldy ,uih, dh rqyuk esa ldy vfxze vuqikr rFkk

fuoy ,uih, dh rqyuk esa fuoy vfxze vuqikr Øe'k% 6-66 çfr'kr vkSj

4-20 çfr'kr jgsA dqy nckoxzLr cgh 31-03-2015 dks 12-12 çfr'kr dh

rqyuk esa 31-03-2016dks ?kVdj 11-46 çfr'kr gks xbZA

Hkkjr Hkj esa vius 'kk[kk usVodZ dks c<kus ds fy,] cSafdax lsokvksa ls oafpr

vkSj de cSafdax lsok,a çkIr {ks=ksa rd viuh igq¡p dks c<kus ds fy, cSad us

orZeku o"kZ esa 153 'kk[kk,a vkSj 440 ,Vh,e @ ch,u, [kksys gSa ftlesa

2562 ikjaifjd 'kk[kk,a ,oa 2784 ,Vh,e lfgr dqy 5346 lqiqnZxh pSuy

jgsA blesa udnh jhlkbfDyax dk;Z{kerk ls ;qä 253 cap uksV ,DlsIVj Hkh

lfEefyr gSa A

flaxkiqj] tkQuk vkSj Jhyadk esa cSad dh varjkZ"Vªh; mifLFkfr gSA

,l,pth dks fo'ks"kh—r _.kn ds fy, cSad dh 43 vuU; ekbØkslsV

'kk[kk,a gSaA o"kZ 2015&16 ds nkSjku] bu 'kk[kkvksa us 12627 ,l,pth dks

doj djrs gq, 500-20 djksM+ :i;s jkf'k dh _.k çnku dh gSa rFkk ekpZ

2016 ds var rd 36]195 ,l,pth dks doj djrs gq, dqy cdk;k vfxzeksa

dh jkf'k 701djksM :i;s jghA

ÞpsUuS ck<+ß] ftlls psUuS rFkk miuxjksa vkSj vkl&ikl ds ftys% ;Fkk

dkaphiqje] fr#oYywj] dMywj rFkk foyqIiqje Hkkjh o"kkZ vkSj ck<+ ds dkj.k

çHkkfor gq,] ds nkSjku ck<+ jkgr mik;ksa esa cSad lcls vkxs jgkA

cSad us 75518 ck<+ ihfM+rksa dks 935 djksM+ :i;s dh jkf'k dk u;k _.k

miyCèk djk;k A

cSad ds LVkQ+ vkink ds nkSjku [kqn dks uqdlku gksus ds ckotwn ladV dh

vofèk ds nkSjku ekbØks@cksV ,Vh,e dk ç;ksx djrs gq, udn laforj.k

dh O;oLFkk dh A cSad }kjk fd, x, ç;Ruksa dks igpkurs gq, ,uihlhvkbZ

}kjk fo'ks"k iqjLdkj çnku fd;k x;kA

lkekftd mÙkjnkf;Ro

�

�

�

�

�

�

�

�

�

�

LoPN Hkkjr vfHk;ku%

iklcqd fd;kLd

eksckby ,i ^^baMis^^

^baM ekschbZth*

102 LFkkuksa ij

bZ&ykmat

baVjusV cSafdax

cSad ,d laxBu ds :i esa ekuuh; ç/kkuea=h ds

jk"Vªh; vkºoku dks ysdj] u dsoy vius ifjlj ds Hkhrj lkQ&lQkbZ

cuk, j[kus dh xfrfof/k tkjh j[kh cfYd ckgj Hkh ejhuk chp] psUubZ {ks=

dh lQkbZ dks cM+s mRlkg ds lkFk fy;kA

thou dks cpkus esa jä ds egRo dks eglwl djrs gq,] cSad us vf[ky

Hkkjrh; Lrj ij 102 jänku f'kojksa dk vk;kstu fd;k vkSj 4346 jä

bdkb;ksa dh ekax dh A ns'k ds ukxfjdksa dh lykerh lqfuf'pr djus dh

fn'kk esa] fofHkUu LokLF; igy 'kq: dh xbZ ftuesa 21157 yksxksa dks ykHk

igqapkrs gq, 137 LokLF; f'kfoj vk;ksftr fd;k x;k rFkk blesa 2433 yksxksa

us LosPNk ls nku nsus ds fy, us= @ vax nku f'kfoj esa Hkkx fy;kA

vius xzkgdksa ds muds l'kfädj.k dh fn'kk esa csgrj fMthVy lsok çnku djus

dh fn'kk esa cSad us o"kZ ds nkSjku fofHkUu çks|ksfxdh igyksa dh 'kq#vkr dh ftuesa

ls çeq[k igy bl çdkj gS%

216 LFkkuksa ij yxk, tkus ds ifj.kkeLo:i 24 çfr'kr

'kk[kk ysunsuksa dk çolu gqvk gS rFkk iklcqd ds eqæ.k ls lacaf/kr xzkgd

lqfo/kk esa lq/kkjgqbZ gSA

us 'kqHkkjaHk ls ysdj 4-88 yk[k iathdj.k ds lkFk 30

yk[k ekfld foÙkh; @ xSj foÙkh; ysunsuksa dks ikj dj fy;k gSA bl Øe

esa uohure lqfo/kk D;wvkj vk/kkfjr ^LdSu ,aM is* gSA

,d ;w,l,lMh vk/kkfjr eksckby ,I gSA

xzkgdksa dks 24 7 vk/kkj ij cSafdax lsokvksa dh miyC/krk lqfuf'pr djus

ds fy,] tek @ udn vkgj.k dh lqfo/kk ds lkFk

miyC/k djk, x, gSaA

440 u, ,Vh,e @ ch,u, LFkkfir fd, x, tksfd cSafdax lqfo/kk dks lqxe

cukrs gq, 59 çfr'kr 'kk[kk ysunsuksa ds çolu dk ifj.kke gSA

31-03-2016 rd IysVQ‚eZ] 11-2 yk[k xzkgdksa dh cSafdax

vko';drkvksa dks iwjk djrs gq, ysu&nsuksa ds ekeys esa 25 çfr'kr dh o`f)

ntZ dh gSA

LoPN vkSj 'kq) okrkoj.k çnku djus ds fy, lekt ds çfr vius drZO;

dks eglwl djrs gq,] cSad us gfjr igy mik; ds varxZr iwjs ns'k esa

1]20]273 ikS/kkjksi.k fd;k gSA

ÅtkZ laj{k.k ds mik; ds :i esa] d‚iksZjsV dk;kZy; ,oa vU; dk;kZy;ksa ds

Nr ij lksyj flLVe ,oa ,ybZMh yxk, x,] ftlds ifj.kke Lo:i dsoy

d‚iksZjsV dk;kZy; esa gh 4&5 çfr'kr ÅtkZ dh [kir esa deh vkbZA

lekt ds de lqfo/kk çkIr vkSj oafpr oxksaZ ds çfr viuh lsok esa] fiNM+s oxksaZ dks

foÙkh; lsok,¡ o le; ij rFkk i;kZIr _.k miyC/k gksus dks lqfuf'pr djus ds

fy, cSad us ç/kkuea=h tu&/ku ;kstuk ¼ih,etsMhokbZ½ ds rgr ljkguh;

çn'kZu fd;k gS] tks bl çdkj gS%

x

çks|ksfxdh ds iw.kZ ç;ksx%

gfjr igy%

foÙkh; lekos'k igy%

9

�

�

�

�

�

�

�

�

�

�

�

�

�

fnukad 31-03-2016 rd 29-93 yk[k csfld cpr cSad tek [kkrs

¼ch,lchMh½ [kksys x, rFkk 29-59 yk[k ch,lchMh [kkrk /kkjdksa dks #is

dkMZ tkjh fd, x,A bl Øe esa cSad bl [kaM esa Hkh ges'kk vxz.kh jgk gSA

[kksys x, [kkrksa dks #is MsfcV dkMZ ds tkjh fd, tkus esa mPpre vuqikr

vFkkZr 98-86 çfr'kr gSA

#is dkMZ ysu&nsuksa dks djus ds fy,] ek= 49-89 çfr'kr dh m|ksx vkSlr

ds eqdkcys esa 100 çfr'kr ihvks,l ¼fcØh dsUæksa½ midj.kksa dks l{ke fd;k

x;kA

ih,etsMhokbZ ds varxZr fofHkUu jkT; Lrjh; cSadlZ lfefr;ksa

¼,l,ychlh½ }kjk 2975 mi&lsok {ks= vkSj 2023 'kgjh okMZ vkcafVr fd,

x,A lHkh 2975 ,l,l, dks cSafdax lsok,¡ çnku djkbZ xbZ gSa rFkk buesa ls

2517 ,l,l, dks cSad fe= ¼O;kikj laifdZ;ksa½ ds tfj, vkSj 458 ,l,l,

dks 'kk[kkvksa ds tfj, cSafdax lsok,¡ miyC/k djkbZ tkrh gSaA

cSad dks foÙkh; o"kZ 2015&16 esa çfrf"Br iqjLdkjksa ls lEekfur fd;k x;k]

ftlesa fuEuor gSa%

¼o"kZ 2012&13 rFkk

2013&14 ds nkSjku Lo;a lgk;rk lewgksa dks vf/kdre _.k çnku djus

gsrq½ rfeyukMq ds ekuuh; eq[; ea=h] lsYoh ts- t;yfyrk ls çkIrA

& ;Fkk] e/;e Js.kh cSad ds

varxZr —f"k cSafdax esa fotsrk] e/;e Js.kh cSad ds varxZr 'kgjh cSafdax esa

fotsrk rFkk e/;e Js.kh cSad ds varxZr xzkeh.k cSafdax gsrq mi&fotsrkA

o"kZ 2014&15 ds fy, rfeyukMq jkT; rFkk iqnqPpsjh esa

A

o"kZ fnlEcj 2015 dks lekIr vof/k ds fy, ,ihokbZ vfHknkrkvksa dks tqVkus

gsrq lkoZtfud {ks=d cSadksa esa mÙke cSad & nwljh Js.kh rFkk ekpZ 2016 rd

lHkh cSadksa esa pkSFkh Js.khA

lkoZHkkSfed Lo.kZ c‚UM ¼ 2 pj.kksa esa½ ds tkjhdj.k esa lHkh cSadksa esa f}rh;

Js.khA

920 çfrHkkfx;ksa ds e/; 4 ,uihlhvkbZ ¼Hkkjrh; jk"Vªh; Hkqxrku fuxe½

vokMZ çkIr fd,] ;Fkk& ,u,lh,p – fotsrk vokMZ ¼,ihch @ ujsxk

Hkqxrku½] ,u,Q,l & la;qä fotsrk vokMZ ¼,Vh,e ifjpkyu½] lhVh,l

&la;qä fotsrk vokMZ ¼psd Vªads'ku½

ekbØks ,Vh,e ds tfj, udn çnku djus gsrq rFkk psUuS esa ck<+ ls ihfM+r

O;fä;ksa dks vk/kkj igpku djus gsrq fo'ks"k iqjLdkjA

ÞvkbZch LekVZ fjeksVß eksckby ,fIyds'ku ds fy, Ld‚p çkS|ksfxdh

uoksUes"kh vokMZA

loZJs"B çks|ksfxdh uoksUes"k ds fy, bafM;u cSad ds çkS|ksfxdh mRikn Þ

bZ&ilZß dks cSafdax fQUuksosfV ÝafV;j iqjLdkj ls uoktk x;kA

loZJs"B fu"ikfnr lkoZtfud {ks=d cSad vokMZ

,lkspse lkekftd cSafdax mR—"Vrk vokMZ

,l,pth cSad

_.k lgc)rk gsrq ukckMZ }kjk LFkkfir mPp iqjLdkj

iqjLdkj ,oa ç'kfLr;k¡%

Hkfo"; dh vksj

egs'k dqekj tSu

çfu ,oa eqdkv

pkyw foÙk o"kZ 2016&17] o"kkZ&_rq ds ldkjkRed ladsr vkSj ns'k esa xzkeh.k {ks=ksa

esa ek¡x esa ifj.kkeh c<+ksrjh ds lkFk fodkl dk lky gksus dh mEehn gSA ljdkj

}kjk ykxw fofHkUu uhfrxr igyqvksa }kjk vFkZO;oLFkk esa fofuekZ.k {ks= vkSj

jkstxkj esa rsthiu gksus dh mEehn gSA lkekU; o"kkZ&_rq dks /;ku esa j[krs gq,

eqækLQhfr dk mnkjoknh jgus dk vuqeku ds lkFk] çeq[k dksj {ks=ksa ds fodkl esa

o`f)] rFkk dkjksckj dks ljy :i ls djus gsrq lq/kkj djus ds Øe esa] ljdkj

}kjk mBk, x, ç;klksa dks /;ku esa j[krs gq, fuos'k dk ekgkSy vkSj vkxs c<+us dh

mEehn ds lkFk vU; çeq[k vkfFkZd ladsrd Hkh vFkZO;oLFkk ds fodkl esa lgk;rk

djus dh çR;k'kk j[krs gSaA

cSad] e/;e ,oa nh?kZdkfyd ;kstuk esa [kqnjk vkSj e/; d‚jiksjsV lsxesaV ij

/;ku nsus ds lkFk [kqn dh fLFkfr ds fy, ,d e/; vkdkj cSad ds :i esa

ifjdYiuk djrk gSA [kqnjk vkSj e/; d‚jiksjsV lsxesaV ij lefiZr /;ku nsus

gsrq] cSad rhu çeq[k {ks=ksa esa dk;Z{ks= dk fuekZ.k djus dh çfØ;k esa gS] ;Fkk&

ca/kd _.k ftlesa x`g _.k 'kkfey gS] e/;e [kaM ftlesa ,e,l,ebZ rFkk e/;

d‚iksZjsV _.k 'kkfey gS vkSj vU; [kqnjk _.k ftlesa —f"k] y?kq ,oa e/;e m|e

'kkfey gSA

dk;Z{ks= okafNr vkd"kZ.k çkIr djsaxs vkSj xzkgdksa ds laidZ dsUæksa dks de djus ls

U;wure VuZvjkm.M le; gkfly dj ldrs gSA 'kq# ls var rd ds ifjpkyuksa

dks fMftVSl djus ls okafNr n{krk miyCèk gksxh vkSj ifjpkyu dh ykxr dks

de djsxk rFkk xzkgd larqf"V dks c<+k;sxkA bu è;kudsaæh; dk;Z{ks=ksa ls igq¡p

vfèkdrj oS;fäd xzkgdksa dks gksxh ftlls gekjs xzkgd çksQkby esa [kqnjk

xzkgd dh la[;k c<+sxh vkSj cSad dks mudh çR;k'kkvksa rFkk mEehnksa dks iwjk djus

esa enn gks ldrh gSA bu dk;Z{ks=ksa dks vkØked foi.ku j.kuhfr;ksa ls ;qä ;qok

r F k k rdu hd h f o ' k s " k K k s a l s le F k Z u fd; k t k ,x k

vkSj dsaæh—r iksVZQksfy;ksa v‚fMV ds tfj, vkfLr;ksa dh xq.krk dks lqfuf'pr

fd;k tk,xkA bu –f"Vdks.kksa ls oSyV 'ks;j rFkk cSad dh ykHkçnrk esa lqèkkj

gksxhA

cSad dh ifjpkyuxr n{krk dks lqèkkjus gsrq fotusl çklsl bathfu;fjax rFkk

mRikndrk dks c<+kus gsrq ekuo lalkèku esa ifjorZu dk dk;Z dj jgk gS A foÙkh;

lekos'k dk dk;kZUo;u 'kgjh {ks=ksa esa Hkh fd;k tk,xk] rkfd cSad lekt ds

çR;sd {ks= dks lsok çnku dj lds A

eq>s foÜokl gS fd vkids lrr lg;ksx rFkk gekjs Bksl ç;klksa ls] cSad vkxs c<+

ldsxk vkSj i.; èkkjdksa ds ewY; esa o`f) yk ik,xk A

'kqHkdkeukvksa lfgr

vkidk

10

MD & CEO's Message

Dear Shareholders,

I am pleased to place Annual Report of your Bank for the

Financial Year 2015-16. On this occasion, I would like to thank

you for your continued support and loyalty which enabled the

Bank to better its performance and position itself admirably in

the industry, especially in terms of its bottom line in the

otherwise turbulent banking environment.

During FY 2015-16, the world economy continued to grow at a

moderate and uneven pace, encumbered by both the legacies

of the global financial crisis and a number of new challenges.

The weak global scenario in turn had its impact in the domestic

economy as well. As the banking sector remains vulnerable to

exogenous shocks, there was muted demand for credit from

banks, accentuated by slowdown in economy and increase in

stressed assets in the banks. This in turn constrained credit

delivery.

The Economy has since started looking up and commenced

showing signs of revival with impetus for growth provided by

Government of India through its various policy interventions

and enactment of laws.

In its stride towards creating a strong, efficient and sound

organisation, Bank had achieved many significant milestones

this year. I am happy to inform that the Bank has surpassed the

milestone of 3,00,000 crore business in FY 2015-16.

The Bank has been self sustaining in terms of capital by

continuous plough back of profit and has been continuously

maintaining its track record of paying dividends to its

shareholders since 2007.

Amidst such a challenging environment, Bank as a strategic

move, consolidated its loan book by shifting its focus towards

retail business. Towards reducing cost of the deposits,

conscious decision was taken to augment resource

mobilization by increasing the proportion of retail deposits,

with specific focus on growth of CASA. Reinforcing the

strength of the Bank in Agriculture and MSME, credit growth

`

Economic overview

Your Bank's performance

primarily aimed at improving the retail business with specific

focus on these traditional areas besides mortgage loans and

various other retail loans. In addition, maintaining asset

quality was accorded top priority by restricting incremental

non-performing assets through early detection, monitoring,

corrective action plans, shared information and disclosures to

keep future recurrence in check.

Against this backdrop, I would like to present a snapshot of the

Bank's performance in key parameters.

Business grew by 4.31% to 3,10,918 crore for the year

ended March 2016 with growth of deposits by 9061 crore

(5.35%) to 1,78,286 crore andAdvances by 3800 crore

2.95%) to 1,32,632 crore.

Operating profit of Bank was at 3032 crore while Net

Profit stood at 711 crore.

Bank's strong capitalization provides cushion against

asset side risks. With CRAR at 13.20 % under Basel III as

at end March 2016, the Bank is consistently at the top in

the industry in respect of this ratio. Bank was ranked first

among Public Sector Banks under Capital adequacy and

Core Capital (%) parameters on Financial Express

Ranking of India's Best Banks 2015.

Return on Assets at 0.36% continues to be the best

among Nationalised Banks.

Adequate resource profile with proportion of low-cost

current account and savings account (CASA Domestic)

deposits at 31.94%, recorded a growth of 14.81% (y-o-y)

to touch 55,153 crore. CASA growth enabled the Bank

to be ranked 4 among Nationalized Banks

Saving Bank Deposits (Domestic) recorded a (y-o-y)

growth of 15.57% to reach 46,407 crore.

High proportion of retail deposits at around 83% of total

deposits as on 31.03.2016 was indicative of the strong

brand value of the Bank.

�

�

�

�

�

�

�

(

,

`

`

` `

`

`

`

`

`

th

Financial highlights

Bank envisages to position itself as a

in

the Medium to Long Term plan.

“Mid Sized Bank with focus on

Retail & Mid Corporate segment”

Shri. Mahesh Kumar JainManaging Director &

Chief Executive Officer

“

11

�

�

�

�

�

�

�

�

�

�

To provide a strong footing for managing the cost of

deposits, Bank consciously focused on retail deposits and

in the process proportionately reduced high cost bulk

deposits (PDs and CDs) to the tune of 5,782 crore during

the year 2015-16.

Achieving National goals set by Government of India was

on top of the Bank's agenda and the norms stipulated

were duly met i.e. Priority Sector Advances at

50,333.52 crore was 40.85% of the Adjusted Net Bank

Credit (ANBC) and Agriculture lending which at

23,017.56 crore was 18.68% of the Adjusted Net Bank

Credit (ANBC) as on March 31, 2016.

Bank has 73 specialised branches across the country

exclusively catering to the Micro Small & Medium

Enterprises (MSME) sector; the MSME portfolio

increased by 12.81% to 21,031.56 crore from

18,642.95 crore.

Gross NPAs to GrossAdvances ratio and Net NPAs to Net

Advances ratio stood at 6.66% and 4.20% respectively as

on 31 March 2016. The total stressed book reduced from

12.12% as on 31.03.2015 to 11.46% as on 31.03.2016.

Towards enhancing its India network and to extend its

reach to the under-banked and unbanked areas, 153

branches and 440ATMs/BNAs were opened in the current

year to touch 5346 delivery points, including 2562 Brick &

Mortar branches and 2784 ATMs. This included 253

Bunch Note acceptors enabled with cash recycling

functionality.

Bank has international presence in Singapore and

Colombo & Jaffna in Sri Lanka.

For specialized lending to SHGs, Bank has exclusive

43 Microsate branches. These branches have extended

credit to the tune of 500.20 crore covering 12627 SHGs

during FY 2015-16 and the total outstanding advances as

at end-March 2016 stood at 701 crore covering 36,195

SHGs.

Bank was in the forefront in Flood relief measures during

the “Chennai Floods” which affected Chennai, its suburbs

and nearby districts viz., Kancheepuram, Tiruvallur,

Cuddalore and Villupuram were severely affected due to

heavy rain and flood.

Bank extended fresh loans amounting to 935 crore to

75518 flood affected victims.

Bank's staff despite being themselves impacted during

the catastrophe arranged for disbursal of cash using

Micro/BoatATMs during the crisis period. The effort of the

Bank was recognized by NPCI in the form of a prestigious

award.

`

`

`

`

`

`

`

`

st

pan-

Social Responsiveness

�

�

�

�

�

�

�

�

�

Swachh Bharat Abhiyan

.

Passbook Kiosks

Mobile Application “IndPay”

Ind MobiEasy', .

e-Lounges at 102 locations

440 new ATMs/BNAs

Internet Banking

: Bank as an organization rose

upto the National call from the Hon'ble Prime Minister with

great enthusiasm, undertaking the activity of maintaining

cleanliness not only within its premises but also outside by

cleaning an area in Marina Beach, Chennai

Realizing the importance of blood in saving lives, the Bank

had arranged 102 Blood donation camps -India and

solicited 4346 blood units Towards ensuring the well

being of the citizens of the country, various health

initiatives were undertaken which included 137 Health

camps benefitting 21157 persons and Eye/organ donor

camps numbering 2433 volunteered for the donation.

In its stride towards offering better digitalized service for its

customers towards their empowerment, Bank had initiated

several technology initiatives during the year, notable among

them being:

at 216 locations, resulted in migration

of 24% of branch transactions and enhanced customer

convenience relating to printing of passbook.

attracted 4.88 lakh

registrations since launch with monthly financial /

non-financial transactions crossing 30 lakh numbers. QR

based 'Scan and Pay' feature being the latest addition in

this application.

an USSD based MobileApp

, ensuring availability of

basic banking services to customers on 24X7 basis, with

facility to deposit/withdraw cash..

installed resulting in migration of

59% of branch transactions, facilitating convenience of

banking.

platform catering to the banking

requirements of 11.2 lakh customers as on 31.03.2016

registered a growth of 25% in terms of transactions.

Realizing its duty towards the Society for providing a clean

and pure environment, Bank as a green initiative measure

had planted 1,20,273 saplings across the country.

As an energy conservation measure, roof top Solar

system and LED fixtures were installed at Corporate

Office and other Offices, resulting in saving of around

4 - 5% in energy consumption at Corporate Office alone.

In its service towards the less privileged and under privileged

sections of the society, Bank had performed commendably

under Pradhan Mantri Jan-Dhan Yojana (PMJDY) ensuring

access to financial services and timely & adequate credit to the

excluded sections is as follows:

pan

Leveraging Technology

Green Initiatives

Financial Inclusion initiatives

12

�

�

�

�

�

�

�

�

�

�

�

�

�

29.93 lakh Basic Savings Bank Deposit Accounts (BSBD)

opened and RuPay Cards issued to 29.59 lakh BSBD

Account holders as on 31.03.2016. By doing so, Bank

continues to be a leader in this segment also.

Highest ratio of RuPay Debit card issuance to accounts

opened i.e. 98.86%.

100% of PoS (Point of Sales) devices enabled for carrying

out RuPay Card transactions as against the industry

average of only 49.89%.

2975 Sub Services Areas (SSAs) and 2023 Urban wards

allotted by various State Level Bankers' Committee

(SLBCs) under PMJDY. All the 2975 SSAs provided with

banking services and of these, 2517 SSAs are provided

banking services through Bank Mitrs (Business

Correspondents) and 458 SSAs through Branches.

Bank was bestowed with coveted awards in FY 2015-16,

notable among them being:

(for

highest lending to Self Help Groups during 2012-13 and

2013-14), received from Hon'ble Chief Minister,

Tamilnadu, Selvi J Jayalalitha.

viz.,

Winner Medium Bank Class for Agriculture Banking,

Winner Medium Bank Class for Urban Banking and

Runner up under Medium Bank Class Rural Banking

in the state of Tamil Nadu and

Puducherry, for the year 2014-15.

for the period ended

December 2015 and 4 position among all banks upto

March 2016.

among all banks in issue of Sovereign Gold

Bonds (2 tranches).

from among 920 participants viz., NACH –

Winner Award (APB/NREGA Payments), NFS – Joint

Winner Award (ATM Operations), CTS – Joint Winner

Award (Cheque Truncation).

for making cash available through Micro-

ATMs and Aadhar identification to flood stranded people

in Chennai.

for “IB Smart

Remote” MobileApplication.

for the Best

Technology Innovation was conferred on the Bank for the

Technology product 'E-Purse'.

“Best Performing Public Sector Bank Award”

Assocham Social Banking Excellence Awards

Top awards instituted by NABARD, for SHG Bank

Credit Linkage

2 Best Performing Bank among Public Sector Banks

in mobilization of APY subscribers

2 position

4 NPCI (National Payments Corporation of India)

Awards

Special award

SKOCH Technology Innovation Award

Banking Frontier's Finnoviti Award

nd

nd

th

Awards andAccolades

Way forward

MAHESH KUMAR JAIN

MD & CEO

The current financial year 2016-17 is expected to be the year

of growth with positive indication of monsoon and resultant

boost in rural demand in the economy. Various policy initiatives

implemented by the Government is expected to rally the

manufacturing sector and employment in the economy. Other

key economic indicators are also expected to aid growth in the

economy with inflation estimated to moderate assuming

normal monsoon, increase in growth in key core sectors and

investment climate is estimated to grow further owing to efforts

taken by the Government to improve the ease of doing

business.

The Bank envisages to position itself as a

in the

Medium to Long Term plan. For a dedicated focus on Retail &

Mid Corporate segment, the Bank is in the process of creating

Verticals in three major areas, viz., Mortgage loans including

Home loans, Mid Segment comprising of MSME and Mid

Corporate loans and Other Retail Loans including Agriculture,

Small and Micro Enterprises.

These Verticals would bring in the desired focus and achieve

the minimum Turn-around-time by reducing touch points for

customers. Digitizing the end-to-end operations would result

in much desired efficiency and reduce the cost of operations

and enhance customer experience. These focused Verticals

with outreach mostly amongst individual customers will

increase the retail customer proportion in our Customer profile

and enable the Bank to meet their aspirations and

expectations. The Verticals would be supported by aggressive

marketing strategies with a young and tech-savvy outbound

team and ensuring quality of assets through a centralized

Portfolio Audit exercise. These approaches would improve

the wallet share and thereby the profitability of the Bank.

Bank is also undertaking Business Process Engineering to

improve the operational efficiency coupled with Human

Resources transformation to increase the productivity.

Financial Inclusion will expand and implement at urban

locations as well enabling the Bank to reach every segment of

the society.

I am confident that with your continued patronage and our

concerted efforts, Bank would be able to surge ahead and

further enhance stakeholders' value.

With best wishes

Yours sincerely

“Mid Sized Bank

with focus on Retail & Mid Corporate segment”

13

This page is intentionally left blank

bl i`"B d¨ tkucw>dj fjä j[kk x;k gSA

lsok esa

lnL;ksa dks----

vkids funs'kdksa dks vkids cSad ds 31 ekpZ 2016 dks lekIr o"kZ ds ys[kk ijhf{kr

ys[kksa dk fooj.k vkSj udnh çokg fooj.k ds lkFk cSad dh okf"kZd fjiksVZ çLrqr

djus esa vR;fèkd g"kZ gks jgk gSA

foÙkh; o"kZ 2015&16 ds nkSjku vkids cSad ds fu"iknu dh eq[; ckrsa fuEukuqlkj

gSa %

cSad dk oSf'od dkjksckj o"kZ ds nkSjku 4-31 izfr'kr dh o`f) ntZ djrs gq,

3]10]896 djksM+ rd igqapkA

dqy tek,¡ esa 9061 djksM+ ;kfu 5-35 çfr'kr dh o`f) ls foÙkh; o"kZ

2015&16 esa 1]78]286 djksM+ gks xbZaZ A

31-03-2016 rd ldy vfxzeksa esa 3800 djksM+ dh o`f) ;kfu 2-95 izfr'kr

ntZ dh xbZ gS ;s 1]32]632 djksM+ jgsA lexz _.k tek vuqikr 74-39

izfr'kr jgkA

31-03-2016 rd izkFkfedrk {ks= ds vfxzeksa esa 4265 djksM+ dh o`f) ;kfu

9-26 izfr'kr gqvk gS ;s 50]333-52 djksM+ jgs tksfd ,u,uchlh dk 40-

85 izfr'kr FkkA

Ñf"k _.k 23]017-56 djksM+ jgk tks lek;ksftr fuoy cSad _.k

¼,,uchlh½ dk 18-68 izfr'kr gSA

Hkkjr ljdkj }kjk dh xbZ izkFkfedrkvksa ds vuqlkj 31 ekpZ 2016 dks

vtk@vttk dks iznRr cSad vfxze 2146-34 djksM+ gks x, tksfd dqy

izkFkfedrk {ks= vfxzeksa dk 4-55 izfr'kr jgsA

foRrh; o"kZ 2015&16 esa fuoy C;kt ekftZu 2-33 izfr'kr jgkA

ifjpkyuxr ykHk 3032-09 djksM+ rd c<+k tcfd foRrh; o"kZ 2014&15

ds fy, ;g ykHk 3013-71 djksM+ FkkA

foRrh; o"kZ 2014&15 ds fy, 1005-18 djksM+ dh rqyuk esa foRrh; o"kZ

2015&16 dk fuoy ykHk 711-38 djksM+ jgkA

vkSlr vkfLr;ksa ij izfrykHk 0-36 izfr'kr FkkA

ekpZ 2015 ds 12-86 izfr'kr dh rqyuk esa iwath i;kZIrrk vuqikr ¼cslyAAA½

13-20 izfr'kr jgkA

foRrh; o"kZ 2014&15 esa 8-34 izfr'kr dh rqyuk esa foRrh; o"kZ 2015&16 ds

fy, usVoFkZ ij izfrykHk 5-46 izfr'kr jgkA

ekpZ 2015 dks 4-40 izfr'kr dh rqyuk eas ldy ,uih, 6-66 jgk tcfd

ekpZ 2015 ds 2-50 izfr'kr dh rqyuk eas fuoy ,uih, 4-20 izfr'kr ij

jgkA

foRrh; o"kZ 2015&16 ds nkSjku ,uih, esa dqy olwyh 901 djksM+ jgh

tcfd fiNys o"kZ ds nkSjku ;g 848 djksM+ FkhA

foÙk ls lacafèkr eq[; ckrsa

�

�

�

�

�

�

�

�

�

�

�

�

�

�

`

`

`

`

`

`

`

`

`

`

`

`

`

`

`

�

�

�

�

�

�

�

�

fnukad 31@03@2016 ds nkSjku izfr 'ks;j vtZu 14-81 jgk vkSj izfr

'ks;j cgh ewY; 280-63 jgkA

31-03-2016 dks Hkkjr esa cSad dk dqy ns'kh; 'kk[kk usVodZ 2409 ls 2562

rd c<+ x;k A blds vykok cSad dh 3 vksojlht+ 'kk[kk,a gSaA

,Vh,eksa dh dqy la[;k 2344 ls 2531 rd c<+ xbZA buesa 649 vkWQlkbV

,Vh,e 'kkfey gSa vkSj ¼,u ,Q ,l½'ks;j fd, x, ,Vh,e usVodZ esa xzkgd]

2-21 yk[k ls vf/kd ,Vh,e dk iz;ksx dj ldrs gSaA

o"kZ ds nkSjku] cSad us iqupZØ.k lqfo/kk;qDr dS'k fMikflV e'khu@cap uksV

vDlsIVlZ yxk;k gS ftlesa e'khu udnh izkIr dj ldrk gS rFkk xzkgdksa

dks udn miyC/k dj ldrk gSA cSad us o"kZ ds nkSjku fofHkUu LFkkuksa ij

102 bZ&ykÅat dh LFkkiuk dh gS] t¨ ch ,u , ;qä Lo;a pkfyr fdvksLd

gSa vkSj ;gk¡ 24 7 lqjf{kr ikl cwd ÇÁÇVx rFkk psd tek vkfn fd;k tk

ldrk gSA

o"kZ ds nkSjku cSad dh dqy vk; 4-70 izfr'kr c<+dj 18]025-20 djksM+ gks

xbZ] ftlesa C;kt vk; 16]243-79 djksM+ jgh vkSj vU; vk; 1781-42

djksM+A

cSad dk dqy O;; 14-993-11 djksM+ jgk] tksfd 790-54 djksM+ ¼5-57½

izfr'kr dh o`f) n'kkZrk gSA

foÙkh; o"kZ 2014&15 esa 2810-92 djksM+ dh rqyuk es foÙkh; o"kZ 2015&16

ds fy, dqy ifjpkyukxr O;; 3195-51 djksM+ jgkA

vfxzeksa ij izfrykHk

tekvksa dh ykxr

vkfLr;ksa ij izfrykHk

ykxr&vk; vuqikr

izfr deZpkjh dkjksckj ¼ yk[kksa esa½

izfr deZpkjh ykHk ¼ yk[kksa esa½

funs'kd eaMy us foRrh; o"kZ 2015&16 ds fy, 15 izfr'kr ds ykHkka'k dh

vuq'kalk dh gSA cSad }kjk foRrh; o"kZ 2015&16 ds fy, vnk fd;k

tkusokyk ykHkka'k] dj dh dVkSrh ds v/;/khu gksxkA foRRkh; o"kZ 2015&16

ds ykHkka'k ds dkj.k dqy cfgiZzokg ykHkka'k dj ds vfrfjDr 72-04 djksM+

#i;s gSA is&vkmV vuqikr 10-13 izfr'kr curk gSA

`

`

`

` `

` `

`

`

`

`

`

X

vk; ,oa O;;

2014&15 ds fy, egRoiw.kZ vuqikr fuEukuqlkj gSa%&

¼çfr'kr esa½

ekinaM

ykHkka'k

9.63 10.19

6.76 7.10

0.36 0.54

51.31 48.26

1531.19 1443.40

3.53 4.95

2015-16 2014-15

funs'kdksa dh fjiksVZ 2015&16

14

To

The Members,

Your Directors have immense pleasure in presenting the

Bank's Annual Report along with the Audited Statement of

Accounts and the Cash Flow statement for the year ended

31 March 2016.

The major highlights of your Bank's performance during

FY 2015-16 are as follows:

Global Business of the Bank reached 3,10,918 crore

during the year, registering a growth of 4.31%.

Total Deposits grew by 9061 crore, i.e. 5.35% for the

financial year 2015-16 t o 1,78,286 crore.

Gross Advances at 1,32,632 crore, registered an

increase of 3800 crore i.e. 2.95% as on 31.03.2016.

Overall Credit-Deposit ratio was at 74.39%.

Priority Sector Advances was at 50,333.52 crore as on

31.03.2016 and accounted for 40.85% of Adjusted Net

Bank Credit (ANBC).

Agriculture Credit was at 23,017.56 crore and accounted

for 18.68% of ANBC.

In accordance with the priorities accorded by the

Government of India, the Bank's Advances to SC/STs

reached 2146.34 crore as of March 31, 2016, constituting

4.55% of total Priority SectorAdvances.

Net Interest Margin was at 2.33% in FY 2015-16.

Operating Profit increased to 3032.09 crore as against

3013.71 crore in FY 2014-15.

Net Profit for FY 2015-16 was at 711.38 crore as

compared to 1005.17 crore for 2014-15.

Return onAverageAssets was at 0.36%.

Capital Adequacy Ratio (BASEL III) was at 13.20% as

compared to 12.86% as of March 31, 2015.

Return on Net worth for FY 2015-16 was at 5.46%, as

compared to 8.34% in FY 2014-15.

Gross NPA was at 6.66% as against 4.40% in

March 31, 2015 while Net NPA was at 4.20% as against

2.50% in March 31, 2015.

Total recovery of NPAs during FY 2015-16 amounted to

901 crore as against 848 crore in the previous year.

st

FINANCIAL HIGHLIGHTS

�

�

�

�

�

�

�

�

�

�

�

�

�

�

`

`

`

`

`

`

`

`

`

`

`

`

` `

�

�

�

�

�

�

�

�

Earnings per share were at 14.81 and Book value was at

280.63 as on 31.03.2016.

Total domestic branch network of the Bank in India

increased to 2562 from 2409 as on 31.03.2016. Besides,

the Bank has 3 overseas branches, taking the total branch

network to 2565.

Total number ofATMs increased to 2531 as on 31.03.2016

from 2344 as on 31.03.2015, which includes 649 offsite

ATMs and customers can access more than 2.21 lakh

ATMs in the (NFS) shared network.

During the year, Bank deployed 253 Cash Deposit

Machines / Bunch Note Acceptors with recycling

functionality, wherein the machines can receive and

dispense cash to the customers. Bank installed

102 e-lounges at various locations, which are unmanned

kiosks with BNAs, secured pass book printers and cheque

deposit machines with 24 x 7 operations on all days

including holidays.

During the year, total income of the Bank increased by

4.70 per cent to 18,025.20 crore, with Interest Income at

16,243.79 crore and Other Income at 1781.42 crore.

The Bank's total expenditure increased by 790.54 crore

(5.57%) to 14,993.11 crore.

Total operating expenses was at 3195.51 crore for

FY2015-16 as compared to 2810.92 crore in FY2014-15.

(in %)

Yield on Advances 9.63 10.19

Cost of Deposits 6.76 7.10

Return on Assets 0.36 0.54

Cost Income ratio 51.31 48.26

Business per employee ( in lakh) 1531.19 1443.40

Profit per employee ( in lakh) 3.53 4.95

The Board of Directors has recommended a dividend of

15% for FY 2015-16. The dividend shall be subject to tax

on dividend to be paid by the Bank. The total outflow on

account of dividend for FY 2015-16 is 72.04 crore,

excluding dividend tax. The payout ratio works out to

10.13%.

`

`

`

` `

`

`

`

`

`

`

`

INCOMEAND EXPENDITURE

IMPORTANT RATIOS FOR THE PERIOD OF 2015-16 ARE

AS UNDER:

Parameters 2015-16 2014-15

DIVIDEND

DIRECTORS' REPORT 2015-16

15

fuoy ekfy;r ,oa lhvkj,vkj

¼çfr'kr esa½

csly AAA fuEu rkjh[k dks

ekpZ 2016 ekpZ 2015

HkrÊ @ çf'k{k.k

o"kZ ds nkSjku cksMZ esa ifjorZu %

�

�

�

�

�

�

�

�

�

cSad dh fuoy ekfy;r 31-03-2015 ds 12557-73 djksM+ ls c<+dj 31-

03-2016 dks 13478-5 djksM+ gks xbZ] blesas 7-3 izfr'kr dh o`f) ntZ dh

xbZ gSA

csly AAA ds ekunaMksa ds vuqlkj] ekpZ 2015 dks 12-86 izfr'kr dh rqyuk

esa ekpZ 2016 dks iw¡th dh rqyuk esa tksf[ke lek;ksftr vkfLr;ksa dk

vuqikr ¼lhvkj,vkj½ 13-20 izfr'kr gS tcfd bldh U;wure vko';drk

9-625 izfr'kr dh gh gSA lhbZVh A dk vuqikr ekpZ 2015 dks 10-61 izfr'kr

dh rqyuk esa ekpZ 2016 dks 11-68 izfr'kr jgkA tcfd bldh U;wure

vko';drk 6-125 izfr'kr gSA fV;j A iw¡th dk lhvkj,vkj ekpZ 2015 dks

10-61 dh rqyuk esa ekpZ 2016 dk 12-08 izfr'kr jgk tcfd bldh U;wure

vko';drk 7-625 izfr'kr gSA

lhbZVh & A

fV;j A & iw¡th

fV;j AA & iw¡th

dqy

ljdkjh fn'kkfunZs'kksa ds vuqlkj] lhèkh HkrÊ vkSj vkarfjd inksUufr dh

çfØ;k ds nkSjku] vtk @vttk deZpkfj;ksa dks HkrÊ iwoZ vkSj inksUufr iwoZ

çf'k{k.k iznku fd;k x;kA

Jh Vh ,e Hklhu] izcU/k funs'kd ,oa eq-dk-vf/kdkjh ds in ij fnukad 31

ekpZ 2015 rd jgsA

Jh ch-jktdqekj] dk;Zikyd funs'kd us vf/kof"kZrk ij fnukad 31 ebZ 2015

dks dk;ZHkkj NksMkA

Jh Vh ,e Hklhu] izcU/k funs'kd ,oa eq-dk-vf/kdkjh us lhohlh esa lrdZrk

vk;qDr ds :i esa fu;qDr gksus ij fnukad 10-06-2015 dks dk;ZHkkj NksMkA

Jh ,e-ds-tSu] dk;Zikyd funs'kd fnukad 11 twu 2015 ls fnukad

1 uoEcj 2015 rd izcU/k funs'kd ,oa eq-dk-v-¼vfrfjDr izHkkj½ ds in ij

jgsA

Jh ,e-ds-tSu us izcU/k funs'kd ,oa eq-dk-vf/kdkjh ds :i esa fnukad

2 uoacj 2015 dks dk;ZHkkj laHkkykA

`

`

11.68 10.61

12.08 10.61

1.12 2.25

13.20 12.86

Jh Vh lh osadV lqczef.k;u us fnukad 14-08-2015 d¨ va'kdkfyd xSj

ljdkjh funs'kd ,oa xSj dk;Zikyd v/;{k dk dk;ZHkkj laHkkykA

�

�

�

�

�

�

�

�

�

lqJh eqfnrk feJk dks cksMZ esa ljdkj ds ukferh ds :i esa] MkW-,u-Jhfuokl

jkWo tks fnlEcj 15] 2015 ls funs'kd ugha jgs] ds LFkku ij fu;qDr fd;k

x;k A

Jh vkj lqczef.k; dqekj us dk;Zikyd funs'kd ds :i esa fnukad

22 tuojh 2016 dks dk;ZHkkj laHkkykA

Jh , ,l jktho us dk;Zikyd funs'kd ds :i esa fnukad 22 tuojh 2016

dks dk;ZHkkj laHkkykA

funs'kd laiq"V djrs gSa fd ekpZ 31] 2016 dks lekIr o"kZ ds fy, okf"kZdys[kk rS;kj djrs le; %

egRoiw.kZ fopyu] ;fn gksa] ds laca/k esa mfpr Li"Vhdj.k lfgr iz;ksT;ys[kk ekudksa dk ikyu fd;k x;k gSA

Hkkjrh; fjt+oZ cSad ds fn'kkfunsZ'kkuqlkj xfBr ys[kkadu uhfr;ksa dksyxkrkj ykxw fd;k x;kA

foRrh; o"kZ ds var rd cSad ds dk;Zdyki o fLFkfr ij lgh ,oa U;k;ksfprn`f"V rFkk 31 ekpZ] 2016 rd cSad ds ykHk dk lgh fp= nsus ds fy, mfpr,oa foosdiw.kZ fu.kZ; ,oa vkdyu fd, x,A

Hkkjr esa cSadksa dks vf/k'kkflr djusokys iz;ksT; dkuwuksa ds izko/kkuksa dsvuq:i i;kZIr ys[kkadu fjdkWMkZsa dks cuk, j[kus ds fy, mfpr vkSj i;kZIrlko/kkuh cjrh xbZA vkSj

ys[kksa dks ykHkdkjh dkjksckj okyh laLFkk ds vk/kkj ij rS;kj fd;k x;k gSA

cksMZ] Hkkjr ljdkj] Hkkjrh; fjt+oZ cSad vkSj Hkkjrh; izfrHkwfr o fofue; cksMZ dkmuds ewY;oku ekxZn'kZu vkSj lgk;rk ds fy, vkHkkj O;Dr djrk gSA cksMZfoRrh; laLFkkuksa vkSj laidhZ cSadksa dks Hkh muds lg;ksx o leFkZu ds fy,/kU;okn nsrk gSA cksMZ vius xzkgdksa o 'ks;j/kkjdksa ls feys vuojr leFkZu dsizfr vkHkkj O;Dr djrk gSA

cksMZ] Jh Vh ,e Hklhu] Jh ch jktdqekj rFkk MkW ,u Jhfuokl jko }kjk fn;s x;sewY;oku ;ksxnku ds fy, viuh ljkguk O;Dr djrk gS] ;s bl o"kZ ds nkSjkulnL; ugha jgsA

cSad ds lexz fu"iknu ds fy, LVkQ lnL;ksa }kjk iznRr fu"Bkoku lsok,a rFkk;ksxnku ds izfr cSad viuh ljkguk O;Dr djrk gSA

funs'kdksa dh ftEesnkjh dFku

vkHkkjksfDr

funs'kd eaMy ds fy, o mudh vksj ls

egs'k dqekj tSuçcaèk funs'kd ,oa eq[; dk;Zikyd vfèkdkjh

16

NETWORTHAND CRAR

BASEL IIIAs on

March 2016 March 2015

RECRUITMENT / TRAINING

CHANGES IN THE BOARD DURING THE YEAR

�

�

�

�

�

�

�

�

�

Networth of the Bank improved to 13,478.35 crore as on

31.03.2016 from 12,557.73 crore as on 31.03.2015,

registering a growth of 7.3%.

As per Basel III norms, the Capital to Risk Weighted

Assets Ratio (CRAR) was at 13.20% as on March 2016,

compared to 12.86% as of March 2015, against the

minimum requirement of 9.625%. The CET - I ratio was

11.68% as of March 2016 as compared to 10.61% as of

March 2015 and against the minimum requirement of

6.125%. The CRAR of Tier I capital was 12.08% as of

March 2016 as compared to 10.61% as of March 2015 and

as against the minimum requirement of 7.625%.

(in %)

CET - I 11.68 10.61

Tier- I Capital 12.08 10.61

Tier-II Capital 1.12 2.25

Total 13.20 12.86

As per Government guidelines, pre-recruitment and

pre-promotion trainings were offered to SC/ST employees

during the process of direct recruitment and internal

promotions.

Shri. T M Bhasin was Chairman & Managing Director upto

March 31, 2015.

Shri. B Rajkumar, Executive Director demitted office

on May 31, 2015 on superannuation.

Shri. T M Bhasin, Managing Director & CEO demitted

office on June 10, 2015 on his appointment as Vigilance

Commissioner in CVC.

Shri M K Jain, Executive Director was MD & CEO

( A d d i t i o n a l C h a r g e ) f r o m J u n e 11 , 2 0 1 5

to November 1, 2015.

Shri M K Jain assumed charge as MD & CEO

on November 2, 2015.

Shri T C Venkat Subramanian assumed charge as

Part-Time Non-Official Director & Non-Executive

Chairman onAugust 14, 2015.

`

`

�

�

�

�

�

�

�

�

�

Ms. Mudita Mishra was appointed as Government of India

nominee to the Board on January 07, 2016 in place of

Dr. N Srinivasa Rao who ceased to be Director from

December 15, 2015.

Shri. R Subramania Kumar assumed charge as Executive

Director on January 22, 2016.

Shri. A S Rajeev assumed charge as Executive Director

on January 22, 2016.

The Directors confirm that in the preparation of the annual

accounts for the year ended March 31, 2016: –

The applicable accounting standards have been followed

along with proper explanation relating to material

departures, if any;

The accounting policies framed in accordance with the

guidelines of the Reserve Bank of India, were consistently

applied;

Reasonable and prudent judgment and estimates were

made so as to give a true and fair view of the state of affairs

of the Bank at the end of the financial year and of the profit

of the Bank for the year ended March 31, 2016.

Proper and sufficient care were taken for the maintenance

of adequate accounting records in accordance with the

provisions of applicable laws governing banks in India;

and

The accounts have been prepared on a going concern

basis.

The Board expresses its deep sense of gratitude to the

Government of India, Reserve Bank of India and Securities &

Exchange Board of India for the valuable guidance and

support received from them. The Board also thank the

financial institutions and correspondent banks for their

co-operation and support. The Board acknowledges the

unstinted support of its customers and shareholders.

The Board places on record its appreciation for the valuable

contribution made by Shri T M Bhasin, Shri B Raj Kumar and

Dr. N Srinivasa Rao who ceased to be members during the

year.

The Board places on record its appreciation for the dedicated

services and contribution made by members of staff for the

overall performance of the Bank.

For and on behalf of Board of Directors

DIRECTORS' RESPONSIBILITY STATEMENT

ACKNOWLEDGEMENT

MAHESH KUMAR JAIN

Managing Director & CEO

17

�

�

rfeyukMq ds ekuuh; eq[;ea=h] lsYoh ts t;yfyrk us ÞloZJs"B fu"ikfnr

lkoZtfud {ks=d cSad vokMZß ¼2012&13 vkSj 2013&14 ds nkSjku Lo;a

lgk;rk lewgksa dks vfèkdre _.k nsus ds ds fy, ½ bafM;u cSad ds çfu ,oa

eqdkfu Jh ,e-ds-tSu dks çnku fd;kA