45

HAMA 2 October 2009 Bobby Bowers Smith Travel Research / STR Global

| Date post: | 29-Dec-2015 |

| Category: |

Documents |

| Upload: | charla-york |

| View: | 214 times |

| Download: | 0 times |

HAMA

2 October 2009

Bobby Bowers

Smith Travel Research /

STR Global

Presentation Outline

• Global / U.S. Overview

• Chain Scales

• Markets

• Pipeline

• 2009 / 2010 Forecast

www.strglobal.com

615.824.8664 x3321

Want a copy of the presentation?

Have questions about the presentation?

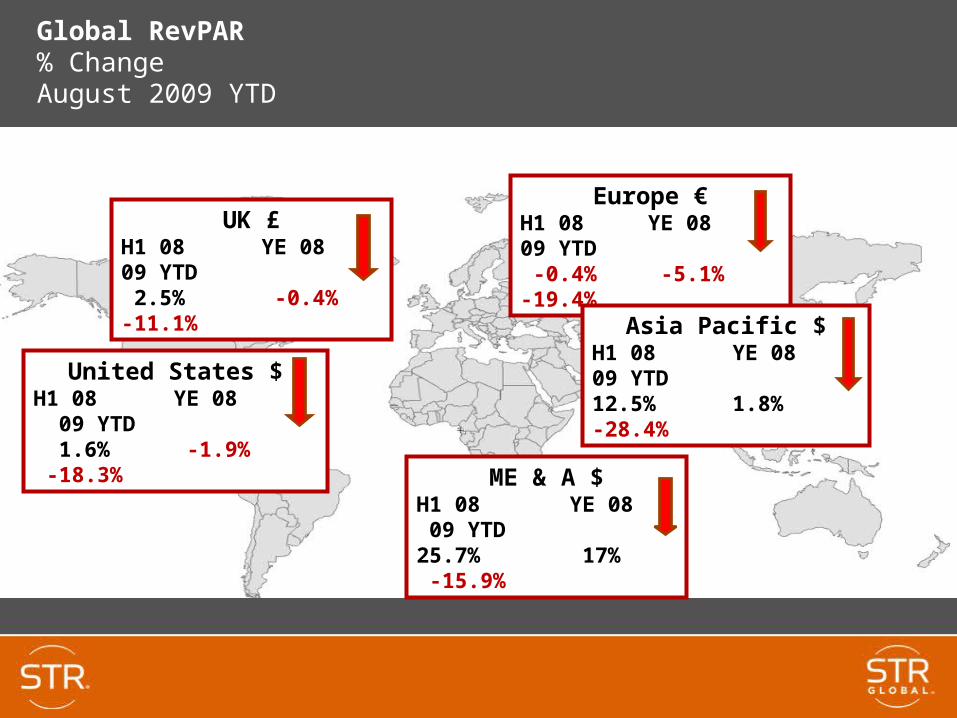

Europe €H1 08 YE 08 09 YTD -0.4% -5.1% -19.4%

ME & A $H1 08 YE 08 09 YTD25.7% 17% -15.9%

Asia Pacific $H1 08 YE 08 09 YTD12.5% 1.8% -28.4%United States $

H1 08 YE 08 09 YTD 1.6% -1.9% -18.3%

UK £H1 08 YE 08 09 YTD 2.5% -0.4% -11.1%

Global RevPAR% Change August 2009 YTD

-10.3

2.5

-1.8-4.2

-1.8

2.6 3.2

-9.0-7.4

-18.3

-25

-20

-15

-10

-5

0

5

10

Supply Demand Occ ADR RevPAR

2008 YTD 2009

Total United StatesKey Performance Indicators Percent ChangeFull Year 2008 / August 2009 YTD

-8.9

-19.9

-12.0-14.5

-6.3-8.8

-25

-20

-15

-10

-5

0

5

10

Occ ADR RevPAR

Weekday Weekend

Total United StatesWeekday / Weekend Percent ChangeAugust 2009 YTD

Weekends = Friday / Saturday

Total United StatesQuarterly RevPar Percent Change / 2007 - 2Q 09

5.3 6.2

2.0 1.4

-1.1

-9.8

-17.7-19.5

-17.3

6.05.6

-25

-20

-15

-10

-5

0

5

10

1Q 07 2Q 07 3Q 07 4Q 07 1Q 08 2Q 08 3Q 08 4Q 08 1Q 09 2Q 09 7/8 09

-8

-6

-4

-2

0

2

4

6

1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009

Supply % Change

Demand % Change

Total United StatesRoom Supply/Demand Percent ChangeTwelve Month Moving Average – 1989 to August 2009

2008 Smith Travel Research, Inc.

3.1%

-6.6%

-1.1%

- 4.8%

-12-10-8-6-4-202468

10

1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009

Occ % Chg

ADR % Chg

Total United StatesOccupancy/ADR Percent ChangeTwelve Month Moving Average – 1989 to August 2009

-3.4%

-6.8%-9.5%

-6.3%

-4.7%

0.1%

-20

-15

-10

-5

0

5

10

15

1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009

RevPAR % Chg

-2.7%

Total United StatesRevPAR Percent ChangeTwelve Month Moving Average – 1989 to August 2009

2008 Smith Travel Research, Inc.

-10.5% - 15.1%

Chain Scales

STR Chain ScalesSelected Brands by Category

• Luxury – Four Seasons, Ritz Carlton, Fairmont

• Upper Upscale – Marriott, Hilton, Hyatt, Sheraton

• Upscale – Courtyard, Springhill Suites, Crowne Plaza

• Midscale with F&B – Holiday Inn, Best Western, Quality

• Midscale no F&B – Hampton, TownePlace, H.I. Express

• Economy – Days Inn, Red Roof, Econolodge

8.9

4.9

9.1

-1.5

7.2

1.3

-4.9 -5.2

-2.1

-12.8

-4.7

-8.6

-20

-15

-10

-5

0

5

10

15

Luxury UpperUpscale

Upscale Mid w F&B Mid wo F&B Economy

SupplyDemand

Chain ScalesSupply/Demand Percent ChangeAugust 2009 YTD

-11.4

-5.9

-11.2

-9.7

-11.6-10.2

-9.9

-12.6

-5.8

-16.8

-9.9

-5.0

-20

-15

-10

-5

0

Luxury UpperUpscale

Upscale Mid w F&B Mid wo F&B Economy

OccupancyADR

Chain ScalesOccupancy/ADR Percent ChangeAugust 2009 YTD

61.7 62.5

51.9

58.0

51.0

64.6

30

35

40

45

50

55

60

65

70

Luxury UpperUpscale

Upscale MidscaleW/FB

Midscalew/o FB

Economy

Chain ScaleOccupancy PercentAugust 2009 YTD

$142.31

$108.73

$84.22

$51.88

$86.42

$241.44

25

75

125

175

225

275

Luxury UpperUpscale

Upscale MidscaleW/FB

Midscale w/oFB

Economy

Chain ScalesAverage Daily Rate August 2009 YTD

-30

-20

-10

0

10

20

1/31/08

Group Demand

Transient Demand

9/26/09

United States – Upper Tier Hotels28 Day Moving Average Group & Transient Demand % ChangeJan 31, 2008 – September 26th, 2009

-20

-10

0

10

1/31/08

Group ADR

Transient ADR

9/26/09

United States – Upper Tier Hotels28 Day Moving Average Group & Transient ADR % ChangeJan 31, 2008 – September 26th, 2009

-25

-20

-15

-10

-5

0

5

10

J F M A M J J A S O N D J F M A M J J A S

Total U.S. RevPAR - Monthly Percent ChangeJanuary 2008 – September 2009

20092008

September based on reporting through 9.26

-15

-10

-5

0

5

10

J F M A M J J A S O N D J F M A M J J A S

Total U.S.Average Daily Rate - Monthly Percent ChangeJanuary 2008 – September 2009

20092008

September based on reporting through 9.26

-15

-10

-5

0

5

J F M A M J J A S O N D J F M A M J J A S

Total U.S.Occupancy - Monthly Percent ChangeJanuary 2008 – September 2009

20092008

September based on reporting through 9.26

Market Performance

-11.9

-7.7

-10.5

-18.7

3.1

-10.2

3.2

-6.8-7.2

-13.6

-25

-20

-15

-10

-5

0

5

10

Supply Demand Occ ADR RevPAR

Top 25 Rest of U.S.

Top 25 Markets versus rest of U.S.Key Performance Indicators Percent ChangeAugust 2009 YTD

-27.4

-26.0

-23.1

-22.8

-22.4

-22.4

-20.6

-19.9

-19.7

-19.5

-18.7

-18.4

-18.3

-16.0

-7.1

-32.4

-35 -30 -25 -20 -15 -10 -5 0

NEW YORK

PHOENIX

CHICAGO

SAN DIEGO

MIAMI

LOS ANGELES

SAN FRANCISCO

ORLANDO

ANAHEIM

ATLANTA

DALLAS

BOSTON

HONOLULU

U.S.

HOUSTON

DC

Key 15 MarketsRevPar Percent ChangeAugust YTD 2009

Excludes Las Vegas

-2.2

-2.0

-1.8

-1.8

-1.2

-1.0

-1.0

0.6

1.9

2.6

3.1

3.4

4.9

-0.2

7.9

-5 0 5 10

Corbin/London, KY

Tacoma/Olympia, WA

Georgetown/Richmond, KY

Branson, MO

Lubbock, TX

Shreveport, LA

Charleston, WV

Pensacola, FL

Rapid City, SD

Lynchburg, VA

Gallup/Grants, NM

Evansville-Henderson, IL

Fargo, ND

Orangeburg/Sumter, SC

Bismarck, ND

15 Markets outside the Top 25RevPar Percent ChangeAugust YTD 2009

Pipeline

Total United StatesActive Development Pipeline - RoomsChange From Prior Year

Aug 2009 Aug 2008 Change % Chg

In Construction 130,471 195,947 -65,476 -33.4%

“Planned” Pipeline 345,050 463,843 -118,793 -25.6%

Planned Pipeline includes projects in Final Planning and Planning phases

Source: STR / TWR / Dodge Construction Pipeline

0

50

100

150

200

250

2003/01 2004/01 2005/01 2006/01 2007/01 2008/01 2009/01-60

-40

-20

0

20

40

60

80

UC Rooms % Change

Total U.S.Hotel Rooms Under Construction and Percent ChangeJanuary 2003 –August 2009

Under Construction room percentage change measured against same month, prior year.

Total United StatesRooms Under Construction by Scale – In ThousandsAugust 2009

5.7

12.8

34.7

43.0

9.0

5.0

20.3

0

10

20

30

40

50

60

Luxury Upper Upscale Upscale Mid w F&B Mid w/o F&B Economy Unaffiliated

Source: STR / Dodge Construction Pipeline

4.3

4.4

4.9

5.0

5.1

5.3

5.6

8.6

11.4

4.1

0 5 10 15

Candlewood

Courtyard

Fairfield

Marriott

Comfort

Springhill

Hilton G.I.

Holiday Inn

H.I. Express

Hampton Inn

Top Brands – Rooms Under ConstructionAugust 2009 – in Thousands

Top 10 brands = 45% U.S. under construction rooms

3.3

3.3

3.5

3.7

4.1

4.4

5.7

7.0

13.1

2.9

0 5 10 15

Los Angeles

Atlanta

Phoenix

Orlando

Dallas

DC

San Antonio

Houston

Las Vegas

New York

Top 10 MSAs – Rooms Under ConstructionAugust 2009 – in Thousands

39% of all under construction rooms

5.5

5.6

5.6

6.5

7.4

7.9

8.1

8.1

10.7

5.3

0 5 10 15

Richmond, VA

Austin

Oklahoma City

Phoenix

Indianapolis

Houston

Raleigh

Tulsa

New York

San Antonio

Top 10 MSAsRooms Under Construction - % Existing SupplyAugust 2009

Projections

U.S. Economic OutlookBlue Chip Economic Indicators – September 2009

2008 2009F 2010F

Real GDP +0.4% -2.6% +2.4%

CPI +3.8% -0.5% +1.8%

Corporate Profits -11.8% -8.1% +9.8%

Disp Personal Income +0.5% +0.8% +1.7%

Unemployment Rate 5.8% 9.2% 9.8%

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

1988q1 1991q1 1994q1 1997q1 2000q1 2003q1 2006q1 20091Q-10

-8

-6

-4

-2

0

2

4

6

8

GDP % Chg Demand % Chg

Total U.S.Hotel Rooms Sold vs. Real GDP ChangeQuarterly Change – 1988 to 2009 2Q

Real GDP and Lodging Demand measured against same quarter, prior year.Real GDP left scale / Rooms sold right scale.

Real GDP Growth ForecastQuarterly Percent Change vs. Same Quarter Prior Year

0.0

-3.3

-2.5

-0.6

1.7

2.6 2.6 2.7

-3.9

-1.9

-5

-4

-3

-2

-1

0

1

2

3

4

5

3Q 08 4Q 08 1Q 09 2Q 09 3Q 09 4Q 09 1Q 10 2Q 10 3Q 10 4Q 10

Source: Blue Chip Economic Indicators – 10 September 2009

-0.6

-9.7

-5.5

-8.4

-17.1

3.01.8

-3.4

1.3

-4.0

-20

-15

-10

-5

0

5

10

Supply Demand Occ ADR RevPAR

2009 F 2010 F

Total United StatesKey Performance Indicators Percent ChangeFull Year 2009 & 2010 Forecast

Total US Industry Consecutive Quarterly DeclinesKey Indicators

1990/1991

2001/2002

Current(Q2-09)

Estimate 2008/09

Demand 3 5 6 9

Occupancy 7 6 7 11

ADR 0 5 3 9

RevPAR 5 5 4 9

Room Revenue 2 5 4 7

3.0

-4.5

-7.3

2.0

0.2

-1.8

1.7

2.6

0.91.3

3.0

1.7

2.7

-3.4

-0.8-1.0

-3.3

2.4

-10

-5

0

5

Supply Demand Occupancy

Total United StatesSupply, Demand & Occupancy ForecastQ3 2009 – Q4 2010

2008 Smith Travel Research, Inc.

-11.0

-17.5

-15.0

-4.4

-6.1

-4.2

-2.2-1.3

0.4

-1.5

0.2

1.5

-13.0

-10.6-9.9

-5.6-6.5

-8.7

-20

-15

-10

-5

0

5

ADR RevPar Revenue

Total United StatesADR, RevPar and Room Revenue ForecastQ3 2009 – Q4 2010

Total United StatesOccupancy Percent2003 – 2010P

59.2

61.4

63.1 63.3 63.1

60.4

55.4 55.1

50

60

70

2003 2004 2005 2006 2007 2008 2009P 2010P

$86.40$91.16

$97.99

$106.78

$96.43$93.16

$82.95

$104.07

$50

$75

$100

$125

2003 2004 2005 2006 2007 2008 2009P 2010P

Total United States Average Daily Rate 2003 – 2010P

86.40 91.16 104.07 106.78 96.43 93.1684.0685.29 97.9982.9582.82

$87.73$89.11

$91.15

$93.57

$96.74

$99.86

$105.90$107.81$106.65

$85.30

$102.71

80

90

100

110

Nominal ADRYr 2000, Grown by CPI

If year 2000 ADR had increased by CPI each year…

Total US Room RatesActual vs. Inflation Adjusted2000 – 2010E

STR Chain Scale Forecast

2009 2010Segment RevPar Chg RevPar Chg

Luxury -25.0 / -28.0 -7.0 / -10.0

Upper Upscale -18.0 / -21.0 -1.0 / -4.0

Upscale -16.0 / -19.0 -5.0 / -8.0

Midscale with F&B -12.5 / -15.5 -3.0 / -6.0

Midscale without F&B -10.5 / -13.5 +1.0 / -2.0

Economy -13.0 / -16.0 Flat / -3.0

Forecast produced August 2009

Takeaways

• Decline is global

• Supply growth still an issue

• Demand declines may be near bottom

• ADR weakness continues

• “Less Worse” 2H 2009

• Moderate improvement 2010

• Meaningful growth anticipated 2011