63

Investor Presentation January 2016 1

Investor Presentation

January 2016

1

2

Disclaimer and Warning About Language

This presentation has been prepared in order to inform investors.

All information in this document is classified and as such may not be disseminated, copied, altered or changed in any way, nor

may this information be printed for distribution purposes or forwarded as electronic attachments.

No representation or warranty, whether express or implied, as to the accuracy or completeness of this Company Presentation is

made or given by the Company, or any other person in relation to the Company. Any statement or commitment is not given in

verifying the feasibility and the reasonability of the projections, targets and estimates contained in this presentation.

In addition, the information contained in this presentation is not audited or independently verified by Ak Investment, the institution

that will perform management, arranging and sales operations in the sales to qualified investors. Ak Investment does not make

any commitment to verify this information, provide additional information to the buyer, update this presentation or make any

corrections in it. In this context, Ak Investment or its officers do not accept any responsibility on the accuracy, fairness and

completeness of the information given in this presentation.

This presentation does not contain every information needed in order to make an investment decision.

Contents

3

• Group Overview

• Financial Overview

• Divisions

− Construction

− Development

− Energy

• Bond Issue

• Appendix

Overview of the Rönesans Group Business

4

• Established in 1993

• Rönesans Holding is incorporated in Ankara

• Ultimate controlling party and major shareholder is the founder, Erman Ilıcak

• 35.7k employees (as of end-December 2015)

Rönesans Holding A.S.

Construction Development Energy

Provides contracting and construction

engineering services on commercial

buildings, industrial plants, and

infrastructure projects

Ranked #37 in 2015 worldwide, #10 in

Europe, Renaissance Construction in the

ENR Top 250 International Contractor’s

since 2006 in the top 100

Backlog of US$7.9bn as of end-September

2015

Develops commercial real estate such as

shopping malls, office buildings and

healthcare PPP projects

Leading player in Turkey and Russia with

20 income generating and 9 under real

estate properties

Net asset value (net of debt) of real estate

portfolio is US$2.3bn (2015E)

Hospital PPP projects of RSY with a total of

9,500 beds to be developed over 3.2m sqm

portfolio

Operational hydro portfolio size of 114 MW

and 313 GWhr of generation

Focused on electricity generation and

wholesale activities

Carries also a license development portfolio

at various phases

* Heavy Industries and Infrastructure businesses operate in all geographies and support the local businesses as specialized

units. Currently, Heavy Industries operates in Russia and Turkmenistan; Infrastructure operates in Germany, Switzerland,

Austria, Finland and Russia

TL110m

TL23m

Organization Chart

Rönesans Holding A.Ş.

5

RGHRCI REN

İpek Ilıcak (2.5%)

Bahar Ilıcak (2.5%)Erman Ilıcak

95% 5%

RGY RSYDESNA Other

Construction

• Residential

• Seaport

Energy

TL5,794m

TL1,273m

TL5,777m

TL2.408m

TL261m

TL187m

Revenues 2015E

Gross Profit 2015E

Turkey Real

Estate

Developme

nt

Russia Real

Estate

Developme

nt

Healthcare

PPPs Construction

Development

Energy

Rönesans Emlak

Geliştirme Holding

RC Ronesans

İnşaat Taahhüt A.Ş.Ronesans Enerji

Milestones in Group History – Celebrating 22 Years

6

Erman Ilıcak establishes

his fit-out contracting

business in St.Petersburg,

Russia

Moscow

office is

launched

The Group’s real estate

investment arm in Turkey

and Russia

Invests in a minority

stake at PORR

Enters ENR’s Top 100:

Ranks 61st in ENR225

Global and becomes 2nd

biggest contractor in

Russia

First out of 8 contracts

with IKEA for Mega

malls in Russia First contracts in Iraq

Heavy Industries

business is launched

First contracts in

Libya and

Turkmenistan

Ranks 64th on the ENR

Top 250 International

Contractors list, Top

Turkish contractor

Acquires Alpine’s stake in

Gotthard Tunnel and

launches transport

iinfrastructure business

Optimum Ankara,

the Group’s first

shopping mall opens

Optimum

Istanbul opens

4th office project

opens in

St.Petersburg

Group’s investment arm

in electricity generation

in Turkey

GIC Singapore

invests in 3

Optimum Malls

First

hydroplant

(HEPP)

becomes

operational

114MW operational HEPPs,

1,340MW license development

1st office project

opens in

St.Petersburg

3rd Piazza opens

1st office project

opens in Istanbul

3rd Aura opens in

Russia

MoscowCity project

launched

1st Aura shopping

mall opens in Russia

The group’s investment arm

in healthcare concessions

Portfolio of 5 projects, total

6,800 beds

Partnership on Adana PPP with

Meridiam

Piazza mall

developments

start in Turkey

4th Optimum

opens

Ranks 53rd on

the ENR Top 250

International

Contractors list

Acquires

Heitkamp of

Germany with

power sector

expertise

GIC takes

21% stake in

RGY, the

Turkish real

estate

platform

1993 2000 2001 2004 20092008200720062005 2010 2011 2012 2013 2014 2015

Acquisition of

Ballast

Nedam

Ranks

37th the

ENR Top

250,#10

in Europe

7

Russia and CIS

Employees: 24,634

Revenue: US$2,279m

Construction Backlog: US$4,813m

Real Estate Operational GLA: 228k m2

Russia

Türkmenistan

Azerbaijan

Kazakhistan

Belarus

Construction Investments

General

Building

Industry and

Infrastructure

Commercial

Real Estate Concessions Energy

Turkey and Europe

Employees: 4,895

Revenue: US$561m

Construction Backlog: US$2,798m

Real Estate Operational GLA: 495k m2

Note: Excluding Ballast Nedam acquisition

Turkey

Switzerland

Germany

Austria*

Finland

Middle East and Africa*

Employees: 1,523

Revenue: US$153m

Construction Backlog: US$288m

Iraq

Nigeria

Gabon

Mozambique

Qatar

*Only offices

Also, in addition, presence in KSA and new office in Algeria

Note: Employees (including subcontractors) as of Dec 2015, backlog and GLA (not stake adjusted) as of Sept’2015

Revenues as of Full Year 2014 after eliminations.

Geographical Focus of >35k Employees (end-2015)

*

8

Note: Reporting currency is TL, table reflects US$ values converted at the respective year’s central bank rates

* Revenue split before eliminations and asset split after eliminations

** IFRS EBITDA is based on equity pick-up method, Adjusted EBITDA reflecting proportionate consolidation is US$ 625mn

0,6 0,9 0,8

1,4

2,4

3,0

0,9

2,1

1,7 2,3

3,0

4,1

5,4 4,9 5,0

5,4

Revenues (US$ bn) Total Assets (US$ bn)

CAGR:

24%

CAGR:

21%

Financial Highlights (US$ m) 2008-2015E

Energy

94%

4%

1%1%

Construction

DevelopmentOther

Energy

Construction

Development

Other

36%

60%

4%

0%

2014 Revenue Breakdown by Segment* 2014 Asset Breakdown by Segment*

• IFRS EBITDA of US$523m**

• Net Debt of US$751m

0,5

1,2 1,3 1,5

2,0 2,0 2,1 2,0

Total Equity (US$ bn)

CAGR

26%

Key Figures for 2014

Partnerships at a glance

9

Platform level

Institution Info

GIC

(Government

of Singapore

Investment

Fund)

Became Minority

Shareholder with

21.4% through

capital increase

at Turkey real

estate platform,

RGY

4Q 2014

€250m injected

into RGY

Strategic benefits: Funding strategy, Equity raising, Risk diversification, Future exits

Some Consortium Partnerships

Institution Info

Sojitz

- Gazprom Salavat Acrylic

Acid Plant Project, Russia

- Ammonia&urea plant,

Turkmenistan

Gama - Yamal LNG (JV)

Mitsubishi

-Gazprom Salavat Acrylic Acid

Plant Project

-Phosagro Ammonia Plant

Kawasaki

Heavy

Industries

-Ammonia&urea plant,

-GTG plant Turkmenistan

YamataZapsib-2 Ethylene Cracker

Unit

Mitsui Turkmenhimiya Sulphuric Acid

Plant

Key Project/Asset level Partners

Institution Info

GIC

50% JV Partner in

Optimum malls:

Ankara, Istanbul,

Izmir

2012-2013

AGP

(Amstar

Growth

Properties)

Partnered at

development stage in 6

projects with 50%

(since 2009)

Meridiam

Partnered at

development stage with

joint management

rights in 4 projects;

Adana,Elazig, Yozgat,

Bursa

(2013-15)

10

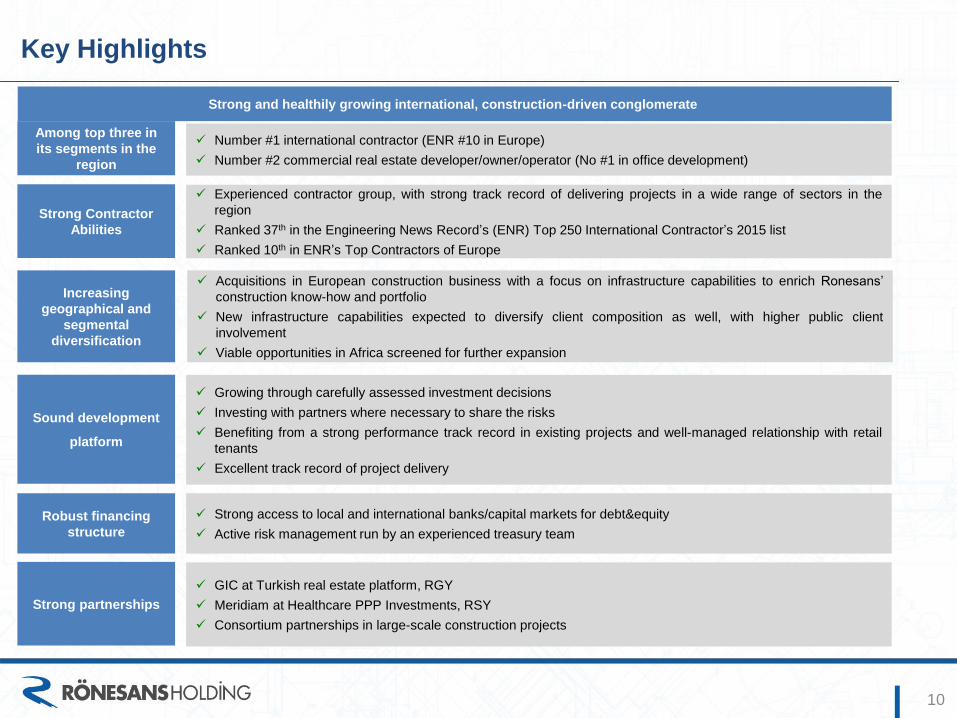

Key Highlights

Strong and healthily growing international, construction-driven conglomerate

Among top three in

its segments in the

region

Number #1 international contractor (ENR #10 in Europe)

Number #2 commercial real estate developer/owner/operator (No #1 in office development)

Strong Contractor

Abilities

Experienced contractor group, with strong track record of delivering projects in a wide range of sectors in the

region

Ranked 37th in the Engineering News Record’s (ENR) Top 250 International Contractor’s 2015 list

Ranked 10th in ENR’s Top Contractors of Europe

Increasing

geographical and

segmental

diversification

Acquisitions in European construction business with a focus on infrastructure capabilities to enrich Ronesans’

construction know-how and portfolio

New infrastructure capabilities expected to diversify client composition as well, with higher public client

involvement

Viable opportunities in Africa screened for further expansion

Sound development

platform

Growing through carefully assessed investment decisions

Investing with partners where necessary to share the risks

Benefiting from a strong performance track record in existing projects and well-managed relationship with retail

tenants

Excellent track record of project delivery

Robust financing

structure

Strong access to local and international banks/capital markets for debt&equity

Active risk management run by an experienced treasury team

Strong partnerships

GIC at Turkish real estate platform, RGY

Meridiam at Healthcare PPP Investments, RSY

Consortium partnerships in large-scale construction projects

11

Notes on Risks and Challenges

Operating in a turbulent region with robust market position and flexible maneuvering capabilities

Russia Exposure

Construciton

A wide range of clients with a private–driven client portfolio (rather than public) exposes Ronesans to a diversified

client exposure

Well-established presence and long history in Russia along with internalized know-how provide competitive

advantages: some worldwide big contractors cannot enter Russia due to difficulties of new entrance and lack of

quality-outsourcing possibilities

Strong alliances and consortiums further bring in complementary know-how and increase chances of winning in

big-ticket contracts

Increasing geographical and segmental diversification, where acquisitions enrich construction activities in Europe

as well as provide entry to new segments (i.e.infrastructure)

Rent re-negotiations well-managed: in some assets a mix of fixing of rent currencies/switch to Ruble contracts are

accepted to maintain tenants’ health in performance

The profitability margins are mainly preserved

Mall occupancy rates are well-preserved: Aura Surgut at 98% (2014:98%), Aura Yaroslavl at 95% (2014: 92%)

New leasing: Primarily in Aura Yaroslavl, a total of net 2k sqm occupied by new tenants

Office occupancy rates well-preserved: ~80% (2015=2014)

Successful cost management initiatives provide buffer to Ronesans for maneuvering through market downturns

Diligent real estate

development /

business

development in other

operations

Increasing inclination towards switching to pure-project finance : refinancing initiatives being taken where optimal

A natural hedge principle is in place, where operational cash flows are matched with financial outflows

Through centrally established Treasury Department overseeing all the Group’s receivables/payables, financial

hedge initiatives are executed on a wide and holistic scale

Financing

Investment decisions always follow market sanity checks including demand-consultancy as well as financing potential

Only well-financed projects go through with equity commitments at about 20-30% of total cost

Two major pipeline projects in Russia, Moscow City and Morskoy Façade, carry no investment obligation,

hence Ronesans has carefully slowed down the works on these projects until market conditions improve

Potential partnership possibilities are always explored to diversify risk

Russia Exposure

Real Estate

Contents

12

• Group Overview

• Financial Overview

• Divisions

− Construction

− Development

− Energy

• Bond Issue

• Appendix

Holding – Financial Overview (TL m)

13

Holding P&L (TLm) FY12 FY13 FY14 % y/y 1H13 1H14 1H15 % y/y

Revenues 2,588 4,480 6,544 46% 1,995 2,821 2,408 -15%

Cost of Revenues -2,177 -3,755 -5,629 50% -1,680 -2,419 -2,074.22 -14%

Gross Profit 411 726 914 26% 315 402 334 -17%

Gross Margin 15.9% 16.2% 14.0% - 15.8% 14.3% 13.9% -

G&A -156 -213 -253 18% -113 -126 -154 22%

S&M -6 -6 -5 -16% -4 -3 -2 -43%

Net Other Operating Income 168 1,648 1,084 -34% 1,004 158 367 132%

EBIT 417 2,154 1,741 -19% 1,202 431 545 27%

EBITDA 449 2,229 1,823 -18% 1,241 474 596 26%

EBITDA margin 17.3% 49.8% 27.9% - 62.2% 16.8% 24.7% -

EBITDA excluding net other oper.income 281 581 739 27% 237 316 229 -27%

margin 10.9% 13.0% 11.3% - 11.9% 11.2% 9.5% -

Net Income (Expense) from investing activities 1 106 35 -67% 6 11 5 -58%

Share on P&L of Inv's valued using Equity Pick-Up 91 279 224 -20% 97 134 166 24%

Net Financial Income (Expense) -125 -475 -1,261 166% -266 -217 -168 -23%

Tax expenses -41 -282 -119 -58% -160 -43 -107 150%

Net Income 342 1,782 619 421% 879 316 441 -64%

Net margin 13.2% 39.8% 9.5% - 44.0% 11.2% 18.3% -

Geographical Revenues (TL m) 1H14 1H15

Turkey 349 447

Russia 2,067 1,529

Middle East-Africa 122 167

Turkmenistan 187 46

Europe 65 119

Other 31 100

Total 2,821 2,408

Source: Financials audited by Deloitte

14

Note: Reporting currency is TL, table reflects US$ values converted at the respective year’s central bank rates

• Revenue split before eliminations and asset split after eliminations

• ** IFRS EBITDA is based on equity pick-up method, Adjusted EBITDA reflecting proportionate consolidation is US$265m

2,0

2,8 2,4

1H 2013 1H 2014 1H 2015

9,2

12,0 13,4

1H 2013 1H 2014 1H 2015

Revenues (TL bn) Total Assets (TL bn)

Financial Highlights (1H13-1H15)

Energy

89%

4%

2%5%

Construction

DevelopmentOther

Energy

Construction

Development

Other

34%

61%

4%

1%

1H 2015 Revenue Breakdown by Segment* 1H 2015 Asset Breakdown by Segment*

• IFRS EBITDA of US$200m**

• Net Debt of US$761m

3,6

4,7

5,7

1H 2013 1H 2014 1H 2015

Total Equity (TL bn)

Key Figures for 1H 2015

Holding 30.06.2015 - Financial Ratios

15

30 June 31 December

2015 2014 % Change

Current Ratio 1.27 1.28 (0.92%)

Quick Ratio 1.14 1.19 (4.10%)

Net Working Capital Ratio 0.08 0.09 (11.77%)

Debt Ratio 0.57 0.59 (2.84%)

Debt to Equity Ratio 1.35 1.45 (6.69%)

Asset Turnover 0.36 0.57 (36.90%)

30 June 31 December

2015 2014 % Change

Gross Profit Margin 13.87% 13.97% (0.1pp)

Operating Margin 22.64% 26.60% (4.0pp)

Net Profit Margin 18.33% 9.47% 8.9pp

Return on Assets (ROA) 6.61% 5.41% 1.2pp

Return on Equity (ROE) 15.53% 13.24% 2.3pp

Source: Financials audited by Deloitte

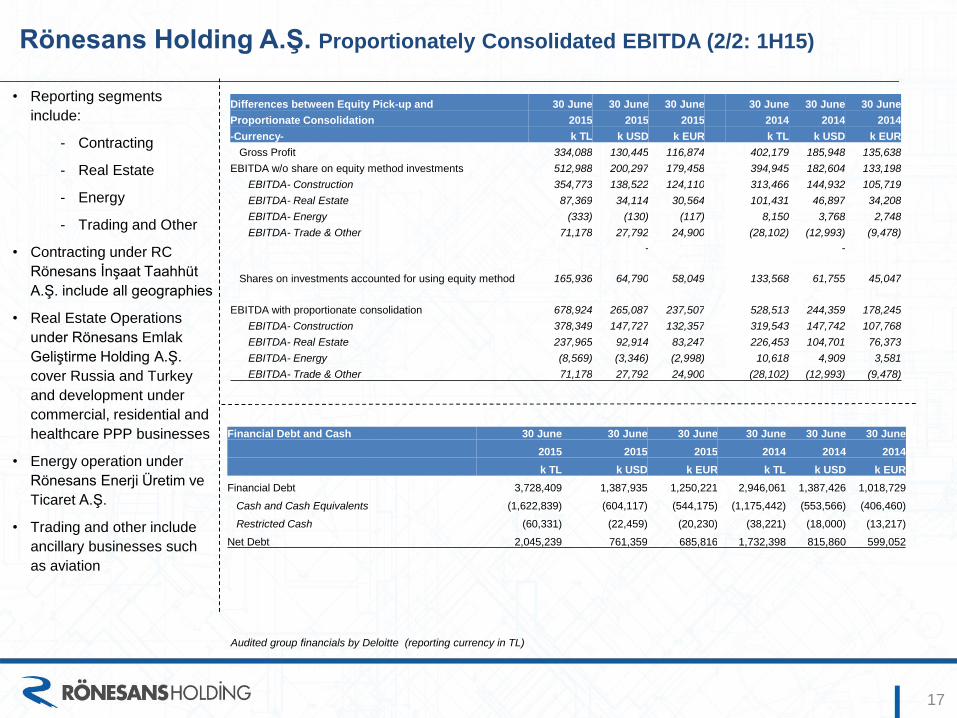

Rönesans Holding A.Ş. Proportionately Consolidated EBITDA (1/2: 2014)

16

• Reporting segments

include:

- Contracting

- Real Estate

- Energy

- Trading and Other

• Contracting under RC

Rönesans İnşaat Taahhüt

A.Ş. include all geographies

• Real Estate Operations

under Rönesans Emlak

Geliştirme Holding A.Ş.

cover Russia and Turkey

and development under

commercial, residential and

healthcare PPP businesses

• Energy operation under

Rönesans Enerji Üretim ve

Ticaret A.Ş.

• Trading and other include

ancillary businesses such

as aviation

Source: Audited group financials by Deloitte (reporting currency in TL)

31 December 31 December 31 December 31 December 31 December 31 December

2014 2014 2014 2013 2013 2013

k TL k USD k EUR k TL k USD k EUR

Gross Profit 914 418 315 726 381 287

EBITDA with equity pick-up method 1143 523 394 850 446 336

EBITDA- Construction 711 325 245 517 272 205

EBITDA- Real Estate 332 152 114 292 153 115

EBITDA- Energy 1 1 0 8 4 3

EBITDA- Trade & Other 99 45 34 33 17 13

Shares on investments acc. with equity method 224 103 77 279 147 110

EBITDA with proportionate consolidation 1367 625 471 1129 593 446

EBITDA- Construction 725 332 250 519 273 205

EBITDA- Real Estate 545 249 188 575 302 228

EBITDA- Energy -3 -1 -1 2 1 1

EBITDA- Trade & Other 99 45 34 33 17 13

Contracting Real estate Energy

Trading

and other Eliminations Total

Revenues 6,522 246 71 150 (445) 6,544

Gross Profit 746 186 -3 28 -43 914

Assets 4,056 6,879 483 2,492 (2,455) 11,455

31 December 2014

Rönesans Holding A.Ş. Proportionately Consolidated EBITDA (2/2: 1H15)

17

• Reporting segments

include:

- Contracting

- Real Estate

- Energy

- Trading and Other

• Contracting under RC

Rönesans İnşaat Taahhüt

A.Ş. include all geographies

• Real Estate Operations

under Rönesans Emlak

Geliştirme Holding A.Ş.

cover Russia and Turkey

and development under

commercial, residential and

healthcare PPP businesses

• Energy operation under

Rönesans Enerji Üretim ve

Ticaret A.Ş.

• Trading and other include

ancillary businesses such

as aviation

Audited group financials by Deloitte (reporting currency in TL)

Differences between Equity Pick-up and 30 June 30 June 30 June 30 June 30 June 30 June

Proportionate Consolidation 2015 2015 2015 2014 2014 2014

-Currency- k TL k USD k EUR k TL k USD k EUR

Gross Profit 334,088 130,445 116,874 402,179 185,948 135,638

EBITDA w/o share on equity method investments 512,988 200,297 179,458 394,945 182,604 133,198

EBITDA- Construction 354,773 138,522 124,110 313,466 144,932 105,719

EBITDA- Real Estate 87,369 34,114 30,564 101,431 46,897 34,208

EBITDA- Energy (333) (130) (117) 8,150 3,768 2,748

EBITDA- Trade & Other 71,178 27,792 24,900 (28,102) (12,993) (9,478)

- -

Shares on investments accounted for using equity method 165,936 64,790 58,049 133,568 61,755 45,047

EBITDA with proportionate consolidation 678,924 265,087 237,507 528,513 244,359 178,245

EBITDA- Construction 378,349 147,727 132,357 319,543 147,742 107,768

EBITDA- Real Estate 237,965 92,914 83,247 226,453 104,701 76,373

EBITDA- Energy (8,569) (3,346) (2,998) 10,618 4,909 3,581

EBITDA- Trade & Other 71,178 27,792 24,900 (28,102) (12,993) (9,478)

Financial Debt and Cash 30 June 30 June 30 June 30 June 30 June 30 June

2015 2015 2015 2014 2014 2014

k TL k USD k EUR k TL k USD k EUR

Financial Debt 3,728,409 1,387,935 1,250,221 2,946,061 1,387,426 1,018,729

Cash and Cash Equivalents (1,622,839) (604,117) (544,175) (1,175,442) (553,566) (406,460)

Restricted Cash (60,331) (22,459) (20,230) (38,221) (18,000) (13,217)

Net Debt 2,045,239 761,359 685,816 1,732,398 815,860 599,052

18

Ronesans Holding Debt & Commitment Breakdown (end-9M15)

RGH1.95445%

RCI95222%

REN3628%

HOL97523%

RHV842%

Holding Total Debt By Operation(TL m, %)

ST Bank Loan1.04424% Finance

lease992%

Corporate bonds43010%

LT Bank Loan2.75464%

Holding Total Debt By Type(TL m, %)

1.044

641

867

321

158

768

<1 year 1-2years

2-3years

3-4years

4-5years

5+years

Holding Bank Loan by Maturity(TL m)

USD2.097 55%

EURO1.543 41%

TL146 4%

Bank Loans by Currency (TL m, %)

Mortgages2.833 37%

Letter of guarantee

3.920 51%

Surety&Guarantee882

12%

Holding Commitments&Contingencies(TL m, %)

Total Financial Debt TL4,328m

Commitments&Contingencies TL6,606m

Rönesans Holding A.Ş. Financial Statements (1/2 : 2014)

19

Source: Audited group financials (reporting currency in TL)

31.12.2014 31.12.2013

ASSETS TL M TL M

Current Assets 4.722 4.493

Cash and cash equivalents 1.546 1.437

Trade receivables 1.208 1.176

Inventories 348 443

Prepaid expenses 260 423

Due from customers under construction contracts 535 304

Other current assets 287 345

Assets classified as held for sale 538 365

Non-Current Assets 6.733 7.007

Investments accounted for using the equity method 1.372 976

Investment properties 3.718 4.677

Property, plant and equipment 839 716

Intangible assets 164 157

- Goodwill 143 139

- Other intangible assets 21 18

Prepaid expenses 57 2

Deferred tax assets 96 139

Other non-current assets 641 341

TOTAL ASSETS 11.455 11.501

31.12.2014 31.12.2013

LIABILITIES TL M TL M

Current Liabilities 3.682 3.567

Short term financial debts 78 46

Short term portion of long term financial debts 863 415

Trade payables 562 565

Due to customers under construction contracts 178 217

Deferred revenue 1.220 1.627

Other short term liabilities 545 510

Liabilities directly associated with assets

classified as held for sale 236 187

Non-Current Liabilities 3.094 3.639

Long term financial debts 2.401 2.680

Other long term liabilities 693 959

SHAREHOLDERS' EQUITY 4.679 4.295

Equity Attributable to Owners of the Parent 4.183 4.069

Paid in capital 1.100 1.100

Retained earnings and other 3.031 1.270

Net profit for the period 548 1.699

TOTAL EQUITY AND LIABILITES 11.455 11.501

Rönesans Holding A.Ş. Financial Statements (1/2 : 2014)

20

Source: Audited group financials (reporting currency in TL)

31.12.2014 31.12.2013

P&L TL M TL M

- Revenue 6.544 4.480

- Cost of sales (-) (5.629) (3.755)

GROSS PROFIT 914 726

- General administrative expenses (-) (258) (219)

- Other operating income from main activities,net 1.084 1.648

OPERATING PROFIT 1.741 2.154

- Income from investing activities,net 35 106

- Share on profit / loss of investments valued - -

using equity method 224 279

- Financial expense (-) (1.261) (475)

PROFIT BEFORE TAXATION 739 2.064

Tax expenses (119) (282)

NET PROFIT FOR THE PERIOD 619 1.782

Allocation of net profit for the period

Non-controlling interest 71 83

Owners of the parents 548 1.699

619 1.782

Rönesans Holding A.Ş. Financial Statements (2/2 : 2015)

21

Source: Audited group financials (reporting currency in TL)

30.6.2015 31.12.2014

ASSETS TL M TL M

Current Assets 5.025 4.722

Cash and cash equivalents 1.623 1.546

Trade receivables 1.481 1.208

Inventories 519 348

Prepaid expenses 367 260

Due from customers under construction contracts 663 535

Other current assets 371 287

Assets classified as held for sale - 538

Non-Current Assets 8.338 6.733

Investments accounted for using the equity method 1.466 1.372

Investment properties 4.936 3.718

Property, plant and equipment 888 839

Intangible assets 261 164

- Goodwill 240 143

- Other intangible assets 21 21

Prepaid expenses 97 57

Deferred tax assets 122 96

Other non-current assets 787 641

TOTAL ASSETS 13.363 11.455

30.6.2015 31.12.2014

LIABILITIES TL M TL M

Current Liabilities 3.954 3.682

Short term financial debts 101 78

Short term portion of long term financial debts 842 863

Trade payables 457 562

Due to customers under construction contracts 197 178

Deferred revenue 1.803 1.220

Other short term liabilities 555 545

Liabilities directly associated with assets

classified as held for sale - 236

Non-Current Liabilities 3.725 3.094

Long term financial debts 2.786 2.401

Other long term liabilities 939 693

SHAREHOLDERS' EQUITY 5.683 4.679

Equity Attributable to Owners of the Parent 4.803 4.183

Paid in capital 1.100 1.100

Retained earnings and other 4.213 3.031

Net profit for the period 371 548

TOTAL EQUITY AND LIABILITES 13.363 11.455

Rönesans Holding A.Ş. Financial Statements (2/2 : 2015)

22

Source: Audited group financials (reporting currency in TL)

2015 (6-Month) 2014 (6-Month) 2014 (6-Month)

P&L TL M TL M TL M

- Revenue 2.408 2.821 6.544

- Cost of sales (-) (2.074) (2.419) (5.629)

GROSS PROFIT 334 402 914

- General administrative expenses (-) (155) (129) (258)

- Other operating income from main activities,net 367 158 1.084

OPERATING PROFIT 545 431 1.741

- Income from investing activities,net 5 11 35

- Share on profit / loss of investments valued

using equity method 166 134 224

- Financial expense (-) (168) (217) (1.261)

PROFIT BEFORE TAXATION 548 359 739

Tax expenses (107) (43) (119)

NET PROFIT FOR THE PERIOD 441 316 619

Allocation of net profit for the period

Non-controlling interest 71 12 71

Owners of the parents 371 304 548

441 316 619

Earnings per share 34% 28% 50%

Contents

23

• Group Overview

• Divisions

− Construction

− Development

− Energy

• Bond Issue

• Appendix

24

Growing competencies in heavy industries sector with projects like:

• Fertilizer and other gas chemicals plants

• One of a kind: gas to gasoline plant

• Polypropylene, PVC plants

• Acrylic acid, sulphuric acid plants

• Refineries

• Steel production facilities

• Other such as gas turbine test bench, oil extraction and processing

plants

Strategically increasing infrastructure exposure through acquisitions since

2009

3,0

3,8 4,3

6,5

7,5 7,9

2010 2011 2012 2013 2014 9M15

CAGR:

26%

ENR Listed Renaissance Construction with Steady Backlog Growth

Backlog, Period End (US$ bn)

Proven key competencies in building

construction as a leader in:

• Retail and business centers

• Public centers: education, government

• Hotels and recreation facilities

• Residential

• Infrastructure and transportation

• Light industry plants: automobile and

machinery, construction materials, food

industry, processing

Russia46%

Turkmenistan11%

Azerbaijan, Kazakhstan,

Belarus4%

Turkey33%

Europe2%

MEA4%

9M15 Backlog Distribution

40%

32%

20%

7% 2%

Commercial

Social & Government

Heavy Industry

Infrastructure

Light Industry

25

World Records

GBA= 330.000sqm

Height = 462 m

İstanbul İkitelli Integrated

Health Campus

• GBA= ~1.000.000sqm

Adana Integrated Health

Campus

• GBA= ~545.000sqm

In Lakhta Center’s main

tower

19,624m3 of concrete

pouring in 49 hours

Improving the world record

by 3,000m3

GBA= 464.700sqm

Completed in 23 months

İncludes the world’s highest

cylinder shaped aquarium (23

m)

Consisting of two

57‐kilometre‐long single‐track

tubes

26

Ronesans Construction Unit Overview

Ronesans Construction

General Buildings and

Light IndustryHeavy Industries Infrastructure

Medical and Healthcare

Campuses

• Since 1993

• Managed under three

distinct geographically

organized entities:

- Russia and CIS.

- Turkey

- Middle East and Africa

• Distinguishing focus:

- High rise buildings

- Retail, missed use and

commercial buildings

- Light industries and

processing plants

• Since 2011

• Active in Russia,

Turkmenistan

• Business development in

CIS, Turkey and Africa

• Distinguishing focus:

- Gas chemicals such as

fertilizer, polypropylene

plants

- Oil and gas processing

such as gas-to-gasoline

complexes

- Power plants

- Chemicals processing for

sulphuric, phosphoric acid

• Since 2009

• Active in Europe

• Built up of acquisitions by

- 2013: Hergiswil GmbH

from Alpine in Switzerland

- 2014: Heitkamp Ingenieur-

und Kraftwerksbau GmbH

in Germany

- 2015: Ballast Nedam NV

in the Netherlands

- 2009: minority share

purchase of Porr AG of

Austria

• Distinguishing focus:

- Transport infrastructure:

57km rail tunnel

- Energy infrastructure

• Since 2012

• Active in Turkey

• Dedicated to building large

integrated healthcare

projects

• Up to 3.2 million square

meters under contract

General Building and Light Industry: Selected Projects

27

Evolution Tower,

Moscow

GBA: 142k sqm

Contract: USD 291 mn

Client: Snegiri

Development

Avia Park, Moscow

GBA: 465k sqm

Contract: USD 450 mn

Client: AMMA Development

Telecom City, Moscow

Contract: USD 262 mn

Client: PPF Real Estate

Cement Plant, Kaluga

Contract: USD 145 mn

Client: LaFarge

Renaissance Tower,

Istanbul

GBA: 85k sqm

Contract: USD 88 mn

Client: Renaissance

Development: First LEED

Platinum office building

in Turkey

: Largest shopping mall in Europe

Unit1 Unit 2 Unit 3 Unit 4

General Building and Light Industry: High Rise Expertise

28

Federation Tower Renaissance Moscow Towers Evolution Tower Administrative & Trade Complex Renaissance TowerLakhta Center

Unit1 Unit 2 Unit 3 Unit 4

Mary Fertilizer Plant

Turkmenhimiya

JV with Kawasaki

Technology by KBR/Uhde/Stanicarbon

2011-2014

Heavy Industries: Selected Projects

29

* Excludes hydro electric power plant projects in Turkey and cement plant projects in Russia

ZapSib Neftekhim Petrochemical

Complex

Sibur

Technology by Linde

2015-2019 (all phases)

Togliatti Ammonia and Hydrogen

Plant

Linde Azot Togliatti

Subcontractor to Linde

Technology by Linde

2014-2016

Acrylic Acid Plant

Gazprom Neftekhim

JV with Sojitz and MHI

Technology by Mitsubishi Chemical

2013-2015

Stoilensky Gok Pelletizing Plant

NLMK Novolipetsk Steel

Siemens equipment, Outotec

processing technology

2014-2016

Gas Turbine Manufacturing Plant

GE

2013-2015

Ammonia Fertilize Plant

PhosAgro

JV with Sojitz and MHI

Technology by Haldor Topsoe

2014-2017

PVC Integrated Plant

RusVinyl: Sibur+Solvay JV

Subcontractor to Technip

2011-2014

Lebap Sulphric Acid Plant

Turkmenabat

JV with Mitsui

2013-2016

Gas to Gasoline Plant – Phase I

Turkmen Gas

JV with Kawasaki

Technology by Haldor Topsoe

2014-2018

Sunflower Oil Extraction Plant

Cargill

2013-2015

Vacuum Gasoil Deep Conversion

(Refinery Modernization)

LukOil

Subcontractor to Tecnicas Reunidas

2013-2015

Tobolsk Polypropylne Plant

Sibur

Subcontractor to Linde

2012-2014

Project Management and

Feasibility Studies

Turkey, Posco Steel Cold Rolling Mill

Facility, 2011-2012

Iraq, Ammonia Fertilizer Plant for

local private investor, 2012

Qatar, Low Density Polyethylene

Project Name

Client

JV partner if applicable

Technology provider if applicable

Project Start and End Dates

Unit 1 Unit 2 Unit 3 Unit 4

Infrastructure: Overview excl. Ballast Nedam

30

Porr Hergiswil Heitkamp

Renaissance acquired a stake

in Austrian Porr in 2009

Porr is Austria’s 2nd largest

construction company and a

full service provider in

infrastructure

Over 90% of workload

generated in five markets:

Austria, Germany,

Switzerland, Poland and the

Czech Republic

Ranked #72 in 2014 ENR

In 2013, Renaissance Construction

acquired 100% stake in the Alpine

Bau GmBH Hergiswil and its

participations in 3 JVs responsible for

the construction of the Gotthard Base

Tunnel with a total contract volume

above USD 1.1bn

The Gotthard Base Tunnel is a

railway tunnel that consists of two 57-

kilometre-long single-track tubes. The

total length of the tunnel system,

including all cross-passages, access

tunnels and shafts, is over 152 km.

In 2014, Renaissance Construction

acquired 100% stake in Heitkamp

Ingenieur- und Kraftwerksbau

GmbH (HIKB)

The company is specialized in

nuclear power and other thermal

power plants, cooling towers,

sewage treatment plants, and

industrial complexes

Unit 1 Unit 2 Unit 3 Unit 4

Infrastructure: Ballast Nedam 2015

31

1969: Merger of Ballast (founded in 1877) and Nedam (founded in 1899)

1994: Ballast Nedam listed at the Amsterdam Small Cap Index (AScX) of NYSE Euronext

2002: Sale of dredging division, focus on Dutch market with focus on integrated projects in transport

and social infrastructure, industrial sector

2015: One of the Netherlands' top six construction companies

Operating mainly in the Netherlands with approximately 2,500 employees

Ownership as of Dec 31, 2015: 98% Renaissance Infrastructure BV (a Renaissance company)

2% public free float

Zaanstad penitentiary A9 Gaasperdammerweg, AmsterdamA2 Maastricht A15 Maasvlakte - Vaanplein

Ministries of Security & Justice and the Interior, Den Haag Erasmus Medical Centre, RotterdamHigh-yield Waste Processing

Unit 1 Unit 2 Unit 3 Unit 4

Infrastructure: Ballast Nedam Divisions

32

Unit 1 Unit 2 Unit 3 Unit 4

Medical Construction Projects

33

Unit 1 Unit 2 Unit 3 Unit 4

34

Construction Backlog Overview

General Buildings and Light Industry

39%

Heavy Industries

23%Infrastructure

8%

Medical&Healthcare30%

2015E Backlog Breakdown by Unit

General Buildings and Light Industry

41%

Heavy Industries

20%

Infrastructure25%

Medical&Healthcare Concessions

14%

2016E Revenue Breakdown by Unit*

2016E Revenues more representative because of Ballast Nedam

Russia46%

Turkmenistan11%

Azerbaijan, Kazakhstan, Belarus

4%

Turkey33%

Europe2%

MEA4%

Latest (9M15-end) Backlog Breakdown by Region

Please see Appendix for detailed

Project Backlog as of 9M15-end

Contents

35

• Group Overview

• Financial Overview

• Divisions

− Construction

− Development

− Turkish Real Estate: RGY

− Russia Real Estate : Desna

− Healthcare PPPs : RSY

− Energy

• Bond Issue

• Appendix

36

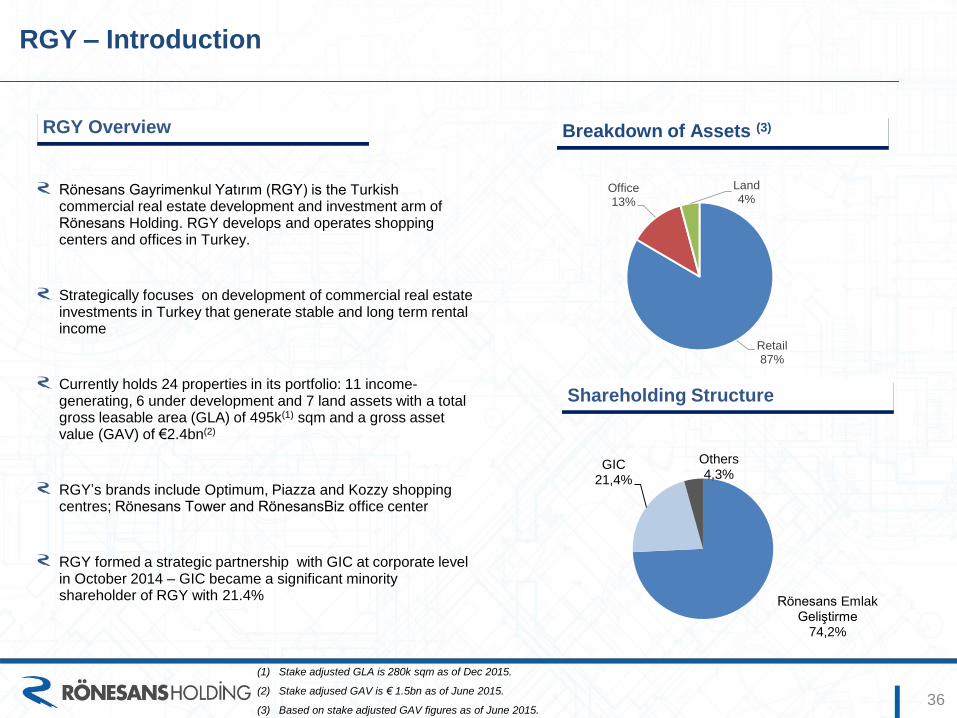

Shareholding Structure

Rönesans Gayrimenkul Yatırım (RGY) is the Turkish commercial real estate development and investment arm of Rönesans Holding. RGY develops and operates shopping centers and offices in Turkey.

Strategically focuses on development of commercial real estate investments in Turkey that generate stable and long term rental income

Currently holds 24 properties in its portfolio: 11 income-generating, 6 under development and 7 land assets with a total gross leasable area (GLA) of 495k(1) sqm and a gross asset value (GAV) of €2.4bn(2)

RGY’s brands include Optimum, Piazza and Kozzy shopping centres; Rönesans Tower and RönesansBiz office center

RGY formed a strategic partnership with GIC at corporate level in October 2014 – GIC became a significant minority shareholder of RGY with 21.4%

RGY Overview

(1) Stake adjusted GLA is 280k sqm as of Dec 2015.

(2) Stake adjused GAV is € 1.5bn as of June 2015.

(3) Based on stake adjusted GAV figures as of June 2015.

Breakdown of Assets (3)

RGY – Introduction

Retail87%

Office 13%

Land 4%

Rönesans EmlakGeliştirme

74,2%

GIC21,4%

Others4,3%

56 62

94

155

2015 2016 2017 2018

37

Dynamic shopping centre (SC) and office portfolio owner and developer; CAGR of GLA from 2008 to 2015 is %26.

Portfolio concentrated on retail assets with a

stake adjusted gross asset value of EUR

1.6 billion (100%: EUR 2.4 billion)

RGY covers all the stages of a real estate investment including initial land and

project development, leasing, property and asset management with its specialized

teams

Stake adjusted NOI in 2015 is expected as

€56m, it is expected to reach €155m in 2018

Investment

Development

Leasing

Property

Management

Asset Management

96196 211

281 336

502 495 495

2008 2009 2010 2011 2012 2013 2014 2015

GLA 000sqm

NOI €m

RGY – General Overview

Yielding60%

Under Development

34%

Land 6%

GAV Breakdown

38

Istanbul

Izmir

Ankara

Adana Gaziantep

Istanbul

Antalya

Samsun

Şanlıurfa

K. Maraş

Bursa

Location

İstanbul and Marmara R.

1. Optimum İstanbul

Ataşehir

2. Küçükyalı SC & Hotel

Maltepe

3. Kozzy

Kadıköy

4. Küçükyalı Office & School

Maltepe

5. Maltepe Mixed-Use Project

Maltepe

6.Mecidiyeköy Office

Mecidiyeköy

7.Ataşehir Office

Ataşehir

8.Ümraniye Land

Ümraniye

9. Park Bravo Land

Maslak

10. Silivri Land

Silvri

11. İzmit Land

İzmit

12. Bursa Land

Bursa

Ankara

13. Optimum Ankara

Eryaman

14. Mamak Land

İzmir

15. Optimum İzmir

Gaziemir

16. Konak Mixed-Use Project

Konak

17. Turan Mixed-Use Project

Bayraklı

18. Karşıyaka SC

Karşıyaka

Adana

19. Optimum Adana

Properties under development

Land

Retail

Office

Mixed use

Location

Antalya

20. Antalya Land

Gaziantep

21. Sanko Park

Samsun

22. Piazza Samsun & Anemon Hotel

Şanlıurfa

23. Piazza Şanlıurfa

K.Maraş

24. Piazza K. Maraş

A portfolio of 24 properties :

11 income generating

6 under development

7 in landbank

RGY – Portfolio Map

Top 10 Tenants by GLA (1) - Retail Top 10 Tenants by GLA (2) - Office

39

(1) Based on leased GLA as of end of Oct’15

(2) Rent from top 10 Tenants (Retail) corresponds to 20,4% of the total rent.

Tenant CategoryGLA

(Sqm)

% of total

GLA(1)# of

assets

Hypermarket 35.612 8,86% 8

DIY 21.527 5,36% 4

Electronics 19.812 4,93% 7

Clothing 17.915 4,46% 9

Clothing 15.131 3,76% 11

Cinema 14.821 3,69% 5

Entertainment 13.445 3,34% 8

Cinema 13.213 3,29% 4

Sportswear 9.391 2,34% 3

Clothing 8.210 2,04% 9

TOTAL (2)169.077 42,07 %

Lease maturity (% of leased GLA) Lease maturity (% of leased GLA)

Tenant CategoryGLA

(Sqm)

% of total

GLA(2)# of

assets

GSM 38.262 57,81% 1

Electronics 13.502 20,40% 1

Sportswear 5.310 8,02% 1

Clothing 3.168 4,79% 1

ult Insurance 2.434 3,68% 1

Food 688 1,04% 1

Electronics 631 0,95% 1

Agency 501 0,76% 1

Chemistry 370 0,56% 1

İk Food 267 0,40% 1

TOTAL 65.133 98,41 %

1

2

3

4

5

6

7

8

9

10

1

2

3

4

6

7

8

9

10

5

0,4%7,9% 2,4%

89,4%

0%

20%

40%

60%

80%

100%

2015 2016 2017 2018 2019 2020 2021>

1% 4% 2%13% 12% 8%

59%

0%

20%

40%

60%

80%

2015 2016 2017 2018 2019 2020 2021>

RGY – Tenant Base Lease Expiration Schedule (Oct’ 2015)

RGY – Rent Sustainability

40

12,3% 12,6%13,2%

11,6%

14,5%

15,4% 15,1%

16,2%

11,9%12,5%

10,7%

11,7%

13,3%14,2%

13,2%13,8%

14,4%

12,6%

0,0%

2,0%

4,0%

6,0%

8,0%

10,0%

12,0%

14,0%

16,0%

18,0%

İstanbul Ankara İzmir Kozzy Adana Samsun Maraş Urfa

Change in OCR (1) Actuals Last 12 Months End Q3 2015 Non LfL to Actuals Last 12 Months End Q3 2014 Non LfL

OCR Actuals Last 12 Months End Q3 2014Non LfLOCR Actuals Last 12 Months End Q3 2015Non LfLPortfolio Last 12 Months End Q3 2014 Non-LfL (k€)Portfolio Last 12 Months End Q3 2015 Non-LfL (k€)

Occ

up

ancy

Rat

es

(1) OCR is a method of the profitability calculation of a specific shop, as well as the overall performance of

the Shopping Center as a whole. Calculated by dividing the shops’ total cost into total turnover of the

shop, in the specific same period .

Mall 2015 Oct

İstanbul Optimum AVM 98,4%

Ankara Optimum AVM 94,6%

İzmir Optimum AVM 99,5%

Adana Optimum AVM 94,7%

Kozzy 98,4%

Samsun Piazza AVM 95,9%

Maraş Piazza AVM 92,6%

Urfa Piazza AVM 95,1%

Contents

41

• Group Overview

• Divisions

− Construction

− Development

− Turkish Real Estate: RGY

− Russia Real Estate : Desna

− Healthcare PPPs : RSY

− Energy

• Bond Issue

• Taxation

• Appendix

42

Shareholding Structure

Desna Gayrimenkul Yatirim A.S. (Desna) is the Russian commercial real estate development and investment arm of Rönesans Holding

Develops and operates offices, business centers.shopping centers and mixed type complexes in Russian Federation

Strategically focuses on development of commercial real estate investments that generate stable and long term rental income

Currently holds 14 properties in its portfolio: 9 income-generating, 3 under development and 2 land assets with a total operating gross leasable area (GLA) of 228(1) sqm and a gross asset value (GAV) of US$1.3bn(2)

Income generating properties: 2 shopping malls, 6 office buildings and 1 office/hotel complex

Desna’s shopping mall brand is Aura

Overview Breakdown of Assets in terms of GAV (2)

Desna – Introduction

RGH95%

5% Management

(1) Based on operating GLA and GAV are the same with total GLA and GAV as of Dec 2015.

(2) Based on stake adjusted GAV figures as of June 2015.

Operational; 65,2%

Under Dev.; 35%

Land Bank; 0,5%

Investment

Development

Leasing

Property

Management

Asset Management

43

Dynamic shopping centre (SC) and office portfolio owner and developer; CAGR of GLA from 2008 to 2015 is %26.

Portfolio concentrated on mall assets with a

stake adjusted gross asset value of

US$509m (100%: US$509m)

Desna covers all the stages of a real estate investment including initial land and

project development, leasing, property and asset management with its specialized

teams

Stake adjusted NOI in 2015 is expected as

US$49m, it is expected to reach US$66m in

2020

GAV Breakdown

NOI US$m

Desna – General Overview

43 43 52

127

193228 228 228

2008 2009 2010 2011 2012 2013 2014 2015

GLA 000sqm

Retail; 39%

Office; 26%

Under Dev.; 34%

Land; 0,5%

11 17 1529 27

58

77

49

2008 2009 2010 2011 2012 2013 2014 2015

44

Russia Portfolio: Office Overview

Pipeline (GLA of 13k sqm)

Construction (GLA of 21k sqm)

Opening and Operation (GLA of 100k sqm)

Renaissance Plaza

CBD

Renaissance Forum

CBD

Renaissance Hall

CBD

Renaissance Centre

Vyborgsky

Renaissance House

CBD

Renaissance Pravda

CBD

Renaissance Premium

CBD

Renaissance Business Park

Vyborgsky

Renaissance Crystal

CBD

Renaissance Fontanka

CBD

1

2

3

4

5

6

7

8

9

10

St. Petersburg

123

4

5

8

9 10 6

7

Russia Portfolio: Retail Overview

Moscow

Novosibirsk

Yaroslavl2

1

-

Surgut

3

St.Petersburg

Pipeline (85k sqm)

Opening and Operation

Exited

• Leading shopping malls in regional cities under Aura brand

- Novosibirsk: First Aura mall made operational in 2010, sold in 2013

- Surgut: Operational since 2012, GLA of 66k sqm

- Yaroslavl: Operational since 2013, GLA of 61k sqm

- St. Petersburg: Under development: Marine Façade Shopping Center, GLA of 85k sqm

Yaroslavl

St. Petersburg Marine Facade

45

Surgut

Top 10 Tenants by GLA (1) - Retail Top 10 Tenants by GLA (1) - Office

46

(1) Based on leased GLA as of end of Oct’15

(2) Rent from top 10 Tenants (Retail) corresponds to 20,4% of the total rent.

Lease maturity (% of leased GLA) Lease maturity (% of leased GLA)

1

2

3

4

6

7

8

9

10

5

DESNA Tenant Base Lease Expiration Schedule (Oct’ 2015)

Tenant CategoryGLA(

sqm )

% of total

GLA(1)

# of

Assets

Hypermarket 11 050 9% 1

Clothing 10 586 9% 2

Electronics 9 007 7% 2

Enternainment 5 261 4% 2

Clothing 5 047 4% 2

Clothing 4 884 4% 2

Cinema 4 586 4% 1

Sportswear 3 409 3% 2

Sportswear 3 345 3% 2

Clothing 3 268 3% 2

TOTAL 60 443 50%

Tenant CategoryGLA(

sqm )

% of total

GLA(1)

# of

Assets

Energy 11 364 15% 1

Construction 9 801 13% 1

Finance Ins. 5 983 8% 1

Finance Ins. 2 223 3% 1

Entertainment 2 154 3% 1

Technology 2 129 3% 1

Energy 1 477 2% 1

Transportation 1 178 2% 1

Healty 1 096 1% 1

Consulate 1 030 1% 1

TOTAL 38 435 51%

1

2

3

4

6

7

8

9

10

5

1%

10%4%

8%13%

64%

0%

10%

20%

30%

40%

50%

60%

70%

1Y 2Y 3Y 4Y 5Y +5Y

21%

7% 9%6%

23%

35%

0%

10%

20%

30%

40%

1Y 2Y 3Y 4Y 5Y +5Y

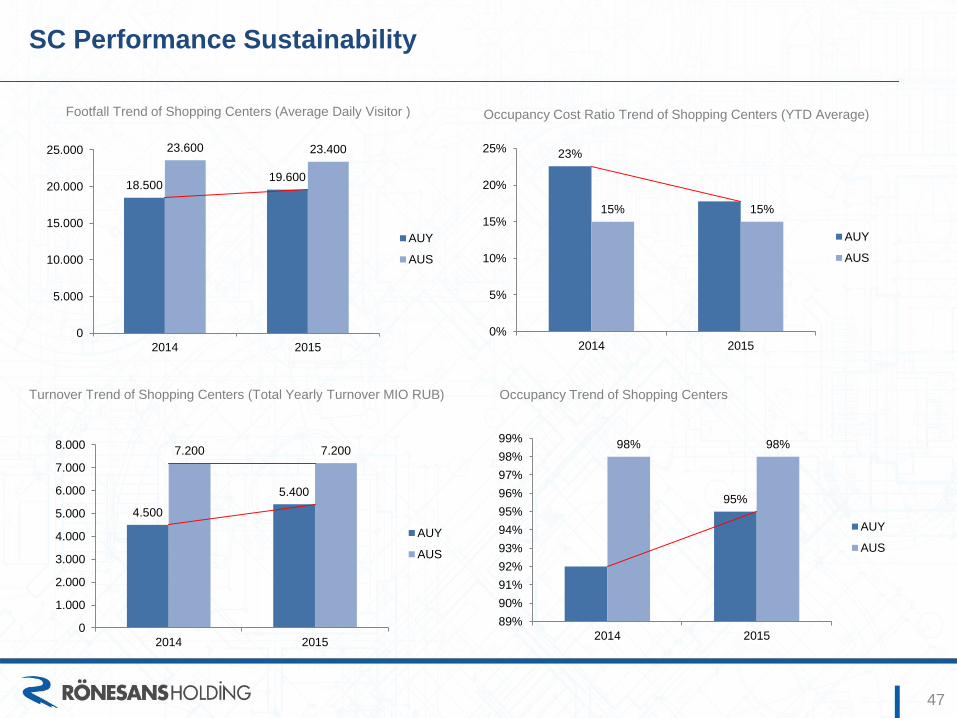

SC Performance Sustainability

47

Footfall Trend of Shopping Centers (Average Daily Visitor )

Turnover Trend of Shopping Centers (Total Yearly Turnover MIO RUB)

Occupancy Cost Ratio Trend of Shopping Centers (YTD Average)

Occupancy Trend of Shopping Centers

18.50019.600

23.600 23.400

0

5.000

10.000

15.000

20.000

25.000

2014 2015

AUY

AUS

4.500

5.400

7.200 7.200

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

2014 2015

AUY

AUS

23%

15% 15%

0%

5%

10%

15%

20%

25%

2014 2015

AUY

AUS

95%

98% 98%

89%

90%

91%

92%

93%

94%

95%

96%

97%

98%

99%

2014 2015

AUY

AUS

Contents

48

• Group Overview

• Divisions

− Construction

− Development

− Turkish Real Estate: RGY

− Russia Real Estate : Desna

− Healthcare PPPs : RSY

− Energy

• Bond Issue

• Appendix

Rönesans Healthcare Infrastructure Portfolio Overview

49

• Ministry of Health of Turkey launched its Build-Lease-Transfer program to enable private sector to build healthcare campuses and provide non-clinical services in return for yearly lease (availability) payments for an operational period of 25 years post construction term

• Close to 27,000 beds have been awarded via public tenders to pre-qualified bidders

• Ronesans Medical is the lead investor in 6 health campus projects reaching a portfolio of ~9,500 beds:

Project Name Number of beds Ronesans Share* (%)

Elazig 1,038 43.75%

Yozgat

(financial close)475

36.25%

(36.25% Meridiam Infrastructure)

Adana

(financial close)1,550

40.0%

(40% Meridiam Infrastructure)

Bursa 1,355 80.0%

Physical

Therapy Group2,400 80.0%

Ikitelli Istanbul 2,682 100.0%

Award Winning Financial Close

• Financial Close: Dec 2014

• Investment: EUR541m

• Loan: EUR433m (80/20 loan/equity ratio)

• Non recourse loan

• All subscribed by international lenders

• Development bank tranche with 18-year tenor total EUR230m

• Commercial bank tranche with 15-year tenor total EUR200m

* Remaining shares belong to minority Sıla Group and Şam unless

otherwise noted for Meridiam Infrastructure Fund

Rönesans Portfolio Above 3.2m sqm of Construction Area

50

Yozgat

(475)

Elazig

(1,038)

Locations (Number of beds)

Ankara

Bursa

(1,355)

Adana

(1,550)

Istanbul

Ikitelli

(2,682)

Physical

Therapy

Physical

Therapy

Physical

Therapy

Physical

Therapy

Physical

Therapy

Physical

Therapy

Physical

Therapy

Physical

Therapy

Location

Construction

Period

Building Area

(k sqm)

Parking

Area (k sqm)

Total

Construction Area (k sqm)

Elazig 3 years 202 93 365

Yozgat 2 years 85 45 141

Adana 3 years 297 140 545

Bursa 3 years 244 122 447

Physical Therapy 2 years 484 125 752

Ikitelli Istanbul 3 years 546 271 950

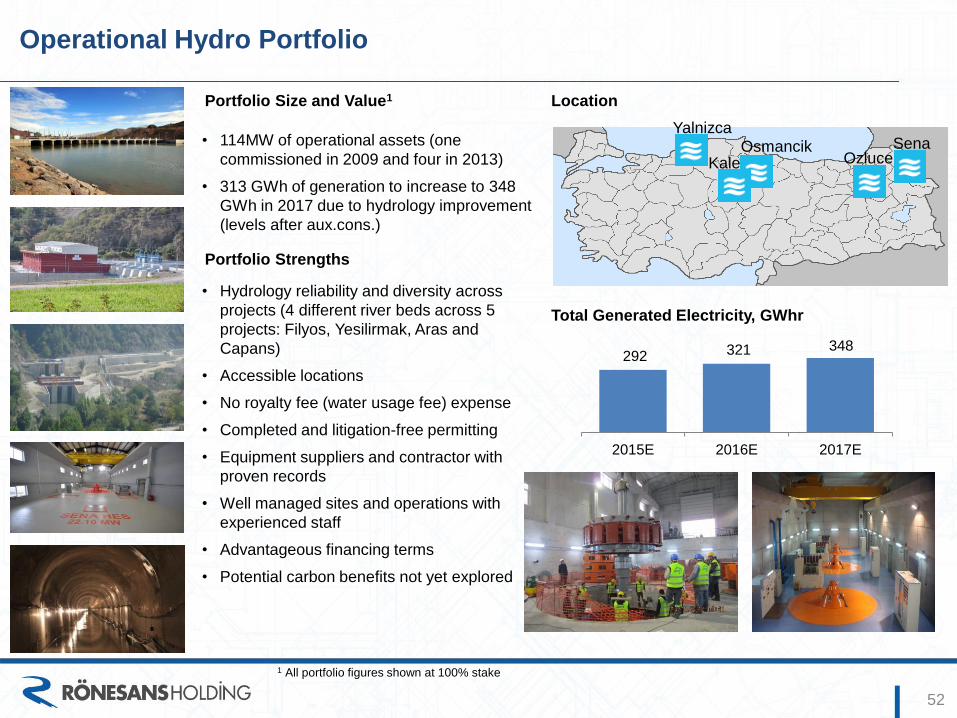

Rönesans Energy – Generation Overview

51

Rönesans Enerji, Rönesans Holding’s platform for energy, is focused on electricity generation and wholesale activities

Holds a portfolio of 2,074 MW at different stages of development (Ronesans’ stake adjusted capacity is 1,956 MW but may

increase during the course of development)

Yalnizca HEPP

16 MW

Kanyon CCGT

600 MW

Kale HEPP

30 MWOsmancik HEPP

9 MW

DC Hidro HEPP

700 MW

Sena HEPP

22 MW

Ozluce1 HEPP

37 MW

Operational 114 MW

License

Under Licensing development

1,960 MW

Klikya Impt. Coal2

660 MW

Run-off-river Dam Natural Gas Imported Coal

Rönesans Enerji

1 Ronesans stake 50% of 37 MW

2 Ronesans stake 85% of 660 MW

$2.6m

$20.8m

$2.7m

$53.2m$0.7m

$12.6m$1.3m

$29.5m

$4.0m

$42.5m2015E EBITDA :

End- 2015 Outstanding Debt :

Pre-License

Operational Hydro Portfolio

52

• 114MW of operational assets (one

commissioned in 2009 and four in 2013)

• 313 GWh of generation to increase to 348

GWh in 2017 due to hydrology improvement

(levels after aux.cons.)

292 321 348

2015E 2016E 2017E

Total Generated Electricity, GWhr

1 All portfolio figures shown at 100% stake

Portfolio Strengths

• Hydrology reliability and diversity across

projects (4 different river beds across 5

projects: Filyos, Yesilirmak, Aras and

Capans)

• Accessible locations

• No royalty fee (water usage fee) expense

• Completed and litigation-free permitting

• Equipment suppliers and contractor with

proven records

• Well managed sites and operations with

experienced staff

• Advantageous financing terms

• Potential carbon benefits not yet explored

Portfolio Size and Value1

YalnizcaSena

OzluceKaleOsmancik

Location

53

• Group Overview

• Financial Overview

• Divisions

− Construction

− Development

− Energy

• Bond Issue

• Appendix

Contents

Summary Information

Issuer Rönesans Holding A.Ş.

Total Nominal Issue Size TL 100 million (may be increased according to the demand level)

Issue Type To be sold to Qualified Investors

Interest Type Floating

Term 1091 days

Coupon Payments Every 91th day (1st coupon payment to be paid on the 90th day)

Benchmark Rate for Coupon Rates 3-month TRLIBOR

Dates for Coupon Rate Calculation 3-month TRLIBOR two business days prior to each coupon payment date

Coupon Calculation Methodology (3-month TRLIBOR + Annual Spread) * Coupon Term (days) / 365

Annual Spread To be determined between 3.25% – 3.50%

Par Value TL 100

Bookbuilding Date 27 January 2016

Issue Date 29 January 2016

Maturity Date 24 January 2019

Quotation Outright Purchases and Sales Market under Borsa Istanbul’s Debt Securities Market

Intermediary Ak Investment

54

Timetable

Bookbuilding date 27.01.2016

Finalization of Allocation 27.01.2016

Settlement 29.01.2016

Commencement of Trading on BIST (Estimated) 01.02.2016

Investors must transfer the funds on 29 January 2016 by 12pm.

55

Coupon Payment Dates

Coupon Payment Dates Dates for Coupon Rate Calculation

1.coupon 28 April 2016 26 April 2016

2. coupon 28 July 2016 26 July 2016

3. coupon 27 October 2016 25 October 2016

4. coupon 26 January 2017 24 January 2017

5. coupon 27 April 2017 25 April 2017

6. coupon 27 July 2017 25 July 2017

7. coupon 26 October 2017 24 October 2017

8. coupon 25 January 2018 23 January 2018

9. coupon 26 April 2018 24 April 2018

10. coupon 26 July 2018 24 July 2018

11. coupon 25 October 2018 23 October 2018

12. coupon ve principal payment 24 January 2019 22 January 2019

56

57

• Group Overview

• Financial Overview

• Divisions

− Construction

− Development

− Energy

• Bond Issue

• Appendix

58

• Group Overview

• Financial Overview

• Divisions

− Construction

− Development

− Energy

• Bond Issue

• Appendix

JCR Rating As of July 2015

59

RGY – Asset List

60

(1) Amstar Global Partners. Real estate investment manager headquartered in Denver, USA, manages

approximately $ 2.0bn worth assets as of June 2015.

Project Type Location Status Ownership

# Assets RGY Stake Partner Stake

1 Optimum Ankara Shopping Centre Ankara Yielding 50% 50% (GIC)

2 Optimum Istanbul Shopping Centre İstanbul Yielding 50% 50% (GIC)

3 Optimum Izmir Shopping Centre İzmir Yielding 50% 50% (GIC)

4 Optimum Adana Shopping Centre Adana Yielding 50% 50% (AGP) (1)

5 Piazza Kahramanmaraş Shopping Centre Kahramanmaraş Yielding 50% 50% (AGP)

6 Piazza Samsun Shopping Centre Samsun Yielding 50% 50% (AGP)

7 Piazza Şanlıurfa Shopping Centre Şanlıurfa Yielding 50% 50% (AGP)

8 Kozzy Shopping Centre İstanbul Yielding 50% 50% (AGP)

9 Sankopark Shopping Centre Gaziantep Yielding 49% 51% (Sanko)

10 Mecidiyeköy Office İstanbul Yielding 100% -

11 Küçükyalı Office & School Office & School İstanbul Yielding 100% -

12 Maltepe Project Mixed-Use İstanbul Under-development 100% -

13 Küçükyalı SC & Hotel Mixed-Use İstanbul Under-development 100% -

14 Karşıyaka Shopping Centre İzmir Under-development 100% -

15 Bayraklı Project Mixed-Use İzmir Under-development 100% -

16 Konak Project Mixed-Use İzmir Under-development 50% 50% (Tekfen)

17 Ataşehir Office İstanbul Under-development 50% 50% (Acıbadem)

18 Tepeüstü Landbank İstanbul Landplot 50% 50% (Doğan)

19 Silivri Landbank İstanbul Landplot 100% -

20 Park Bravo Landbank İstanbul Landplot 100% -

21 Mamak Landbank Ankara Landplot 100% -

22 İzmit Landbank İzmit Landplot 100% -

23 Bursa Landbank Bursa Landplot 100% -

24 Antalya Landbank Antalya Landplot 100% -

RGY – Retail and Mixed Use Projects

61

Operational

Brands

Selected

New

Projects

• Leading outlet brand in major cities: Istanbul, Ankara, Izmir

and Adana

• Total number of Optimum visitors in 2015 is 42 million.

• Leading outlet brand in major cities: Samsun,

Kahramanmaraş, and Şanlıurfa

• Total number of Piazza visitors in 2015 is 40 million.

• Successful local malls prior to Piazza brands

Küçükyalı Shopping Centre &

Hotel

Maltepe İller Bankası Residence,

Office & Shopping Centre

İzmir Extension Project

RGY – Office Projects

62

• A-plus office development in Istanbul

• Mecidiyekoy project operational in 2013

• Kucukyali Office: leased to Bosch and Turkcell, operational in 2014

• Tower: Sold to Allianz in April 2015

Rönesans Tower –

sold to Allianz

RönesansBiz

Mecidiyeköy

Office

Ataşehir

Office

RönesansBiz

Küçükyalı

OfisPark

RönesansBiz

Mecidiyeköy

Office

Desna – Asset List

63

Name of Business Center Location Description of location Type Owned By Owner Company Segment

Renaissance Plaza Saint-Petersburg City Center Operating Desna Desna Development Office

Renaissance Forum Saint-Petersburg City Center Operating Desna Desna Development

Mixed Use Project (Office &

Hotel )

Renaissance Premium Saint-Petersburg Secondary Operating Desna Desna Moskovsky Office

Renaissance Pravda Saint-Petersburg City Center Operating Desna Desna Neva Office

Renaissance Center Saint-Petersburg Secondary Operating Desna Merkator Office

Renaissance House Saint-Petersburg City Center Operating Desna

Desna Gayrimenkul

Yatirim Petersburg

Branch Office

Renaissance Hall Saint-Petersburg City Center Operating Desna Desna Investment Office

Renaissance Business ParkSaint-Petersburg Secondary Under Consctruction Desna Desna Global Office

Renaissance Priyajka Saint-Petersburg Secondary Land Plot Desna Desna Real Estate Office

Renaissance Fontanka Saint-Petersburg City Center Land Plot Desna Desna Forum Office

Aura Yaroslavl Yaroslavl City Center Operating Desna YarRenInvest

Shopping and Entertainment

Center

Aura Surgut Surgut Secondary Operating Desna Rialren

Shopping and Entertainment

Center

Moscow City (Remo Towers) Moscow City Center Under Consctruction Desna ST Towers

Mixed Use Project (Office &

Residential & Commercial )

Marine Façade Saint-Petersburg Secondary Land Plot Desna YarRenPrestige

Shopping and Entertainment

Center