inadequate information to audit committee/ shareholders

5

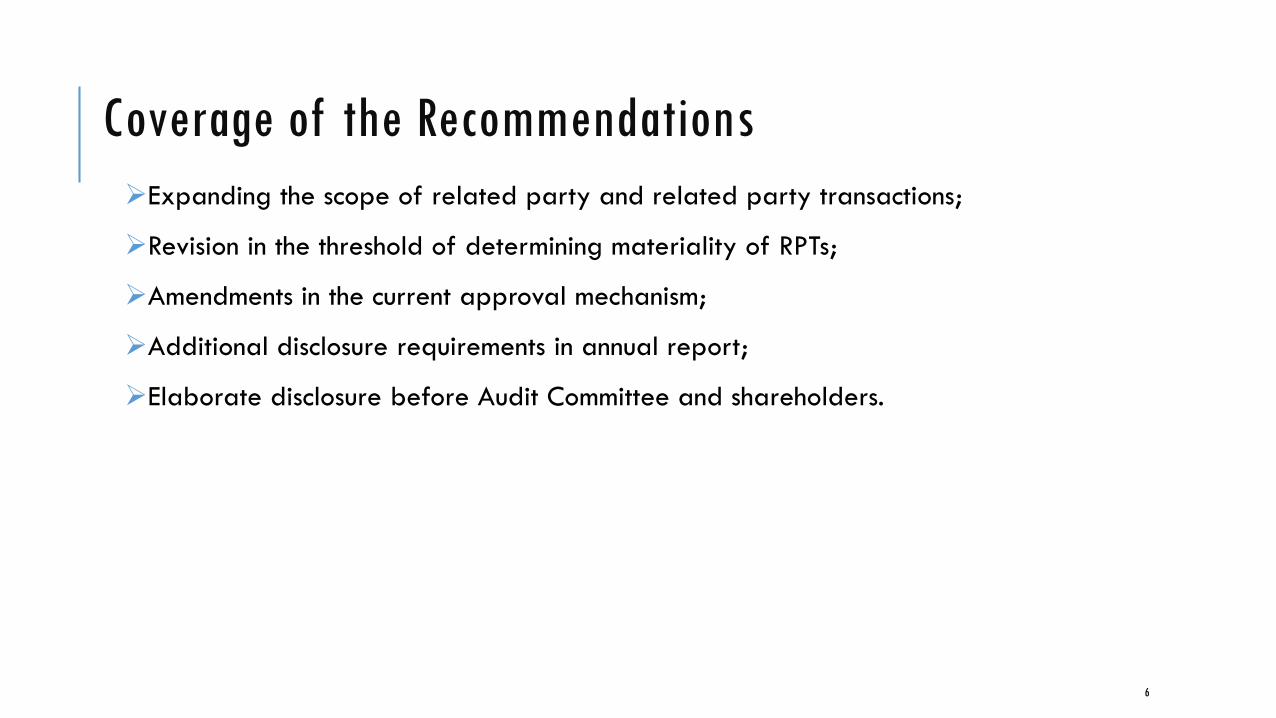

Coverage of the Recommendations

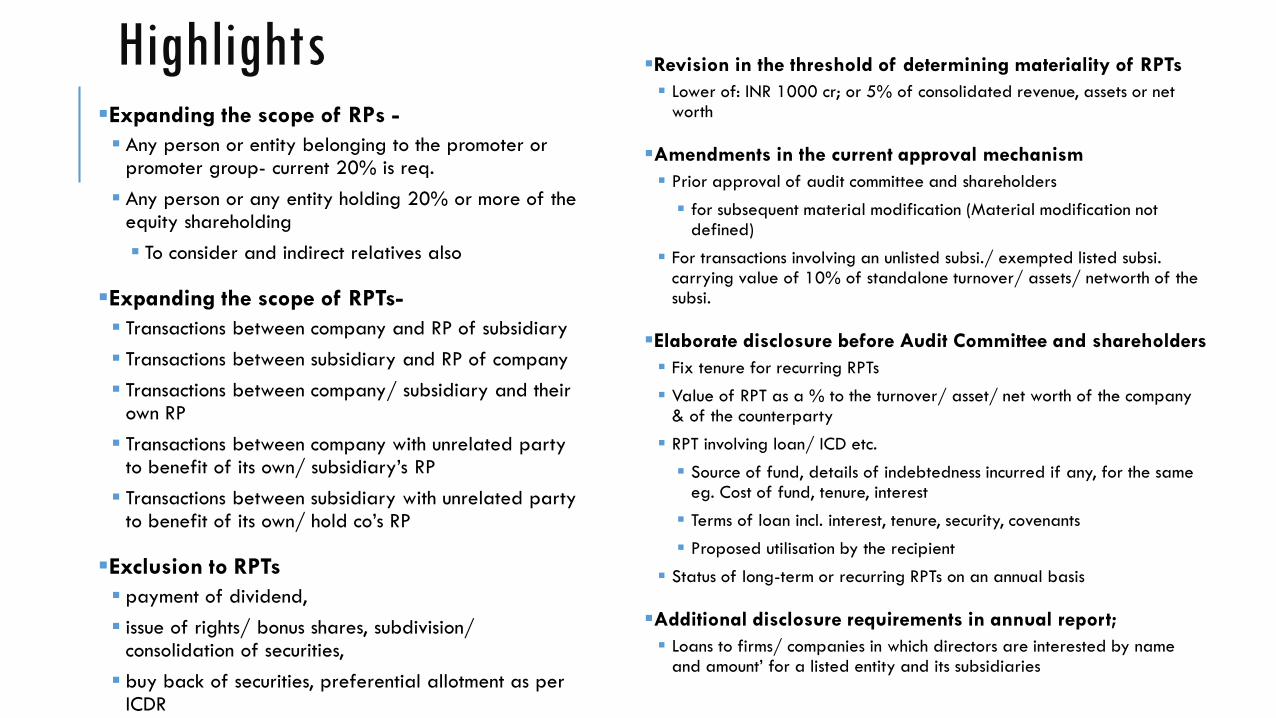

Expanding the scope of related party and related party transactions;

Revision in the threshold of determining materiality of RPTs;

Amendments in the current approval mechanism;

Additional disclosure requirements in annual report;

Elaborate disclosure before Audit Committee and shareholders.

6

DEFINITION OF RELATED PARTY

Proposed addition to the definition of related party

The following would get covered in the proposed definition

The promoters irrespective of their shareholding

Existing definition requires 20% holding also

Significant Shareholder/ Investor (holding 20%)

8

Proposed definition of related party

Related Parties

Any person or entity belonging to the

promoter or promoter group

As per IND AS

Any person or any entity holding 20% or more of the equity shareholding

As per in CA 13

Definition of Related Party TransactionsProposed Changes

Broadly to cover the following

all circular transactions

on the face of it, the transaction is with an unrelated party but actual benefits flow to arelated party

the transactions at consolidated level

swap transactions

10

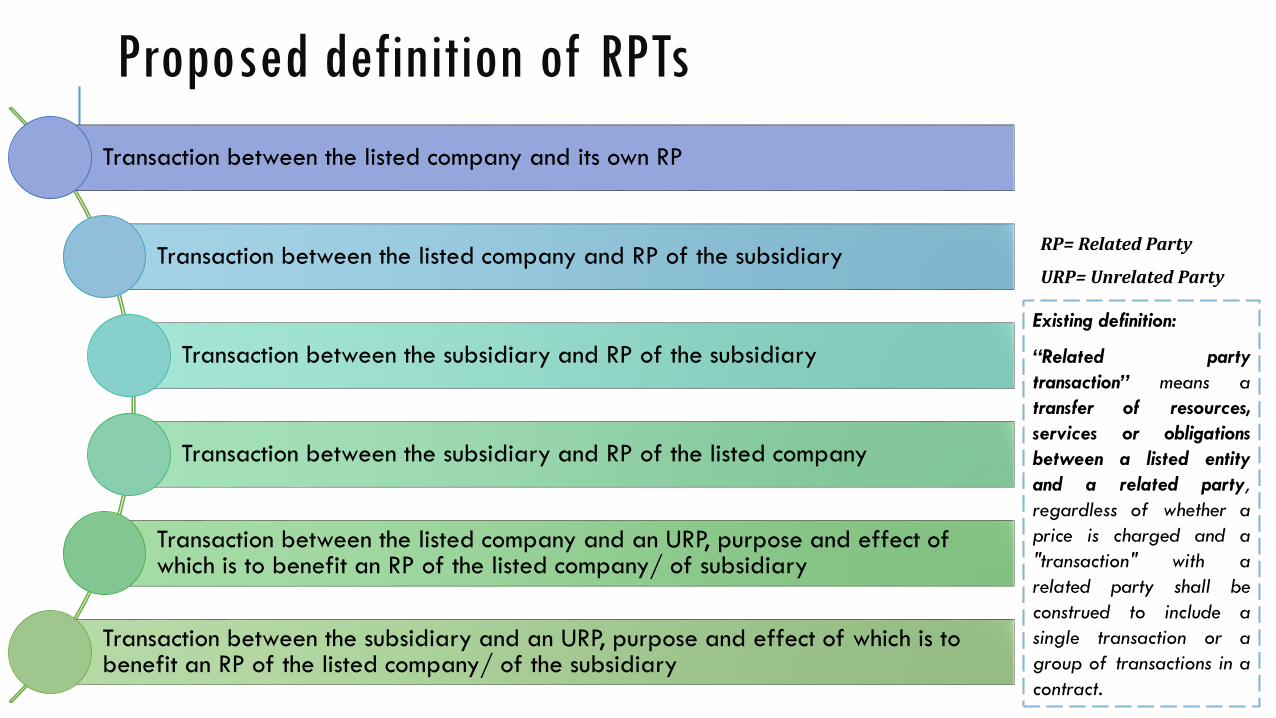

Proposed definition of RPTs

Transaction between the listed company and its own RP

Transaction between the listed company and RP of the subsidiary

Transaction between the subsidiary and RP of the subsidiary

Transaction between the subsidiary and RP of the listed company

Transaction between the listed company and an URP, purpose and effect of which is to benefit an RP of the listed company/ of subsidiary

Transaction between the subsidiary and an URP, purpose and effect of which is to benefit an RP of the listed company/ of the subsidiary

Existing definition:

“Related party

transaction” means a

transfer of resources,

services or obligations

between a listed entity

and a related party,

regardless of whether a

price is charged and a

"transaction" with a

related party shall be

construed to include a

single transaction or a

group of transactions in a

contract.

RP= Related Party

URP= Unrelated Party

Threshold for determining material RPTsProposed Materiality Threshold

To be lower of the following:

INR 1000 cr; or

5% of

Total consolidated revenue

Total consolidated assets

Total consolidated net worth

to be considered only in case of positive net worth of the listed company

12

Approval of Audit Committee & ShareholdersProposed inclusion in the listPrior approval of audit committee & shareholders to be applicable

For subsequent material modifications of RPTs

What would constitute a material modification not defined

Transactions involving the following as a party

unlisted subsidiary; or

listed subsidiary which is exempted from the CG requirements

If the transaction carries a value which is lower of the following:

more than 10% of annual standalone turnover of the subsidiary or

more than 10% of total standalone assets of the subsidiary or

more than 10% of standalone net worth of the subsidiary

To be considered only where the net worth is positive

Approval of shareholders in all cases proposed to be changed to a prior approval

13

Approval of RPTs by Audit Committee & Shareholders

14

Whether the transaction is an

RPT as per definition?

Whether listed entity is a party? Prior approval is required

Whether listed subsidiary is a party and exempted from Reg. 23 & from other CG requirements u/r 15(2)?

Whether the transaction can be considered as Significant Transaction?

Whether unlisted subsidiary is a party?

Whether the transaction can be considered as Significant Transaction?

Whether listed subsidiary is a party and not exempted from Reg. 23 & from other CG requirements u/r

15(2)? Prior approval is not required

Whether none of the above applies?

Yes

Yes

Yes

Yes

Significant transaction= value of which is more than 10% of

turnover or assets or net worth, whichever is lower, of the subsidiary

on a standalone basis

ADDITIONAL DISCLOSURES

Disclosures before Audit CommitteeThe long listType, material terms and particulars of RPT;

Name of RP and its relationship with the listed entity or its subsidiary, including nature of its concern or interest (financial or otherwise);

Tenure (should not be indefinite or open ended);

Value along with an upper limit and for recurring transactions, the aggregate value and the time period within which such limit will be exhausted;

The value of the proposed transaction as the percentage of the listed entity’s annual total revenues, total assets and net worth;

If subsidiary involved, the value of the proposed transaction as a percentage of the subsidiary’s annual total revenues on a standalone basis;

Justification as to why the related party transaction is in the interest of the listed entity;

A copy of the valuation or other external report, if any such report has been relied upon;

Value of the proposed RPT as a percentage of the counter-party’s annual total revenues, total assets and net worth;

Status of long-term or recurring RPTs on an annual basis. 16

Disclosure reg. Financial Transactions

If the transaction relates to any loans, ICDs, advances or investments made or given by thelisted entity or its subsidiary:

details of the source of funds in connection with the proposed RPT;

where any financial indebtedness is incurred to make or give loans, inter-corporate deposits,advances or investments,

nature of indebtedness;

cost of funds; and

tenure;

applicable terms, including covenants, tenure, interest rate and repayment schedule, whethersecured or unsecured and if secured, the nature of security; and

the purpose for which the funds will be utilised by the ultimate beneficiary of such fundspursuant to the RPT.

17

Disclosure before shareholdersDisclosure in explanatory statementSummary of the information provided to the audit committee pursuant to paragraph B(2)ofPart C of Schedule II;

Recommendation of the audit committee w.r.t. proposed transaction, specifying justificationfor why the transaction is in the interest of the listed entity;

Where the transaction relates to any loans, inter-corporate deposits, advances or investmentsmade or given by the listed entity or its subsidiary, the details specified under paragraph B(2) (f) of Part C of Schedule II;

Whether the approval of the RPT by the audit committee was unanimous;

A statement that the valuation or other external report, if any, relied upon by the listed entityin relation to the proposed transaction will be available for inspection at the registered officeof the listed entity;

value of the proposed RPT as a percentage of the counter-party’s annual total revenues,total assets and net worth;

Any other relevant information.18

Disclosure in Annual Report

Disclosure of ‘Loans and advances in the nature of loansto firms/ companies in which directors are interested byname and amount’ for a listed entity and its subsidiaries.

19

Disclosure to Stock Exchanges

Current framework for half yearly reporting:

Disclose RPTs on consolidated basis within 30 days from the date ofpublication of its standalone and consolidated financial results in the formatspecified in the relevant accounting standards for annual results to the stockexchanges.

Proposed framework for reporting every six months:

Disclose RPTs on the date of publication of its standalone and consolidatedfinancial results in the format prescribed by SEBI.

![Related Party Transactions [Luputi]](https://static.documents.pub/doc/80x56/61afa9d10717f755d17168e3/related-party-transactions-luputi.jpg)