25

Presented by: Md. Enamul Haque 1

| Date post: | 13-Jul-2015 |

| Category: |

Documents |

| Upload: | microcredit-summit-campaign |

| View: | 148 times |

| Download: | 1 times |

Presented by: Md. Enamul Haque

1

What is the strategic objective of Microfinance?

The principal objectives of microfinance is needed to

eradicate poverty & hunger, and chance to lift them out of poverty;

2

Clients can create productive businesses, and recover

quickly in the aftermath of natural disasters;

Microfinance is now gaining general acceptance due to

financial inclusion of Micro credit, Micro savings, Micro insurance and Remittances.

3

Microfinance targets the poor and the economically active poor in the society to assist them create wealth, accumulate assets and raise income to smooth consumption;

4

Clients can invest in better nutrition, housing, health, and education for their children;

5

Human capital is the major asset of the any company/ institutions;

Ensured better Quality, speed & maintain growth;

To learn the problem solving technique ;

To develop positive attitude and team speed;

To develop values & ethics;

Improvement of communication & motivation skills;

To build dynamic leadership; and

Maximization of products and qualitative services.

Why Invest in Human Resources Development? “Every customer is a potential reporter, and every employee is a potential spokesperson”.

6

Most of the micro finance institutions is providing credit to poor by the group guaranteed approach and collateral free services, so to development of group dynamics skilled staffs is essential;

Collateral free loan is high risk, to skill and committed staffs is essential to maintain high portfolio quality ;

Why staffs development is so important in MFI?

7

It is estimated that many millions of people around the world have unmet needs for financial services. The challenge is to scale up, skill and committed staffs is highly required;

The vast majority of people in the world do not have access to financial services. To reaching the large number of poor community skilled staffs is essential.

NGO, s/ MFI, s/ MFB, s/ Governments, public and private financial institutions, private businesses and others are recognizing the value of microfinance for poor individuals and for small and medium-sized enterprises.

8

A wrong perception has been bubbling around MFIs for long regarding behavior with clients and protection of rights; training and development on communication, client protection principle can ensure this away.

A well developed staffs are assets of the organization who can carry the corporate vision; poor remuneration structure disallow the flow intelligent breed in this sector, therefore a comprehensive training is essential.

Due to high involvement with mass population, decentralized management style is encourage which required extensive managerial skills even in bottom level.

Strong association with Corporate Strategy requires “Information Sharing”, regular conference can only ensure this.

9

Following areas get special preference on skill development to run effective operations at the bottom level:

Formation groups;

Develop leadership;

Loan processing ;

Feasibility;

Credit appraisal ;

Loan disbursement & collection;

Reporting,;

Books of accounting & record keeping;

Communication;

Use of automation & IT technology as part of Transparency.

Operational Skill Development Areas

10

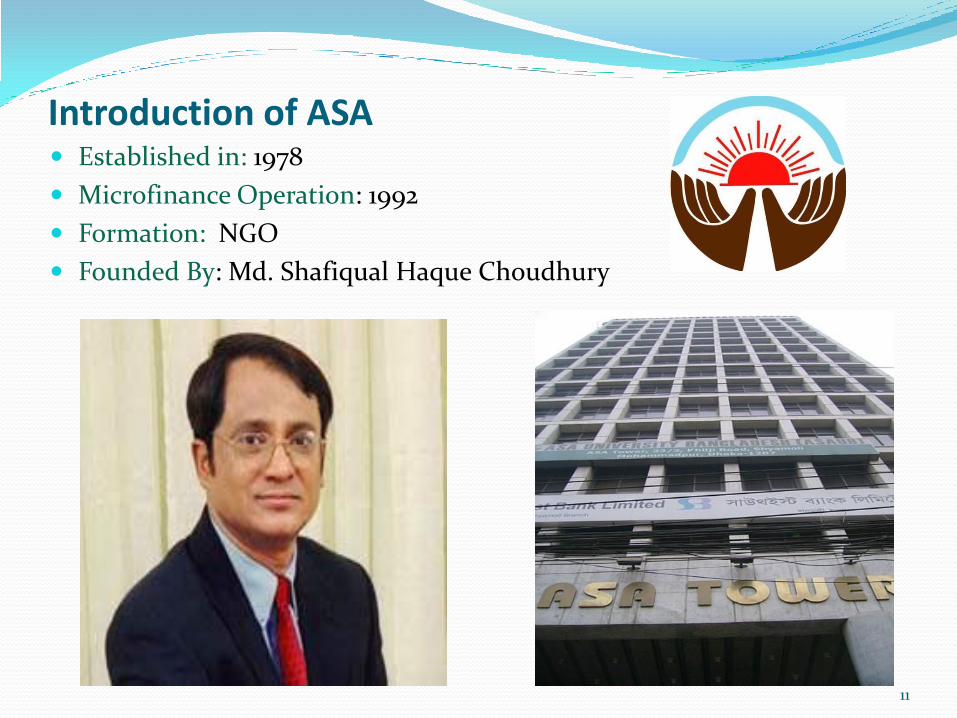

Introduction of ASA Established in: 1978

Microfinance Operation: 1992

Formation: NGO

Founded By: Md. Shafiqual Haque Choudhury

11

Key Indicators of ASA ( 1992 & June 2011)

Indicators 1992 June 2011

No. of branches 159 3,177

# of savers (millions) 0.14 5.10

Value of savings (US$ in millions) 0.73 161.65

# of active clients (millions) 0.09 4.52

Loan outstanding (US$ in millions) 2.92 608.06

# of total staff 1,239 21,795

Cost per unit of money lent 0.166 0.045

Return on equity 2.07% in 1993 6.36%

Return on assets 1.31% in 1993 3.52%

Operational sustainability 53.17% 182.48%

Financial sustainability 47.03% 118.32% 12

13

ASA International, an investment vehicle of Netherland based microfinance investor Catalyst Microfinance Investor (CMI) managed in partnership with ASA Bangladesh. Established in 2006, as Limited liability company; Total Fund is USD 125 million; Investment Location: Asia & Africa; Operation Methodology: Green field operation; Operation Strategy: ASA Cost effective and Sustainable Microfinance Model;

Country of Operations: India, Philippines, Sri Lanka, Pakistan, Ghana, Nigeria and Afghanistan; Invested equity in Seilanithih & SAMIC in Cambodia

Introduction of ASA International (ASAI)

14

At a Glance of ASAI (As of August 2011)

Particulars Total

General Information

1 No. of branches 774

2 No. of borrowers (Active) 769,148

3 No. of total staff 4,584

4 No. of borrowers per LO 259

5 Staff from ASA 70

Loan Portfolio

6 Loan outstanding (Principal) US$ in million 106.72

7 Avg. outstanding per borrower (US$) 139

Loan Security/Savings/Margin Money/LCBU

8 Total loan security (US$ in million) 17.93

Financial Performances

9 Portfolio at risk > 30 days 4.23% 15

Country-wise at a Glance of ASAI (as on August 2011)

Country # of

branches # clients Loan outstanding Savings balance

India 252 269,291 $ 29.6 million $ 2.5 million

Philippine 185 160,397 $ 18.4 million $ 3.0 million

Ghana 54 64,795 $ 14.7 million $ 5.4 million

Pakistan 121 129,817 $ 12.5 million N/A

Sri Lanka 44 39,424 $ 4.2 million $ 1.7 million

Nigeria 63 66,403 $ 9.5 million $ 4.5 million

Afghanistan 17 13,377 $ 2.3 million $ 0.3 million 16

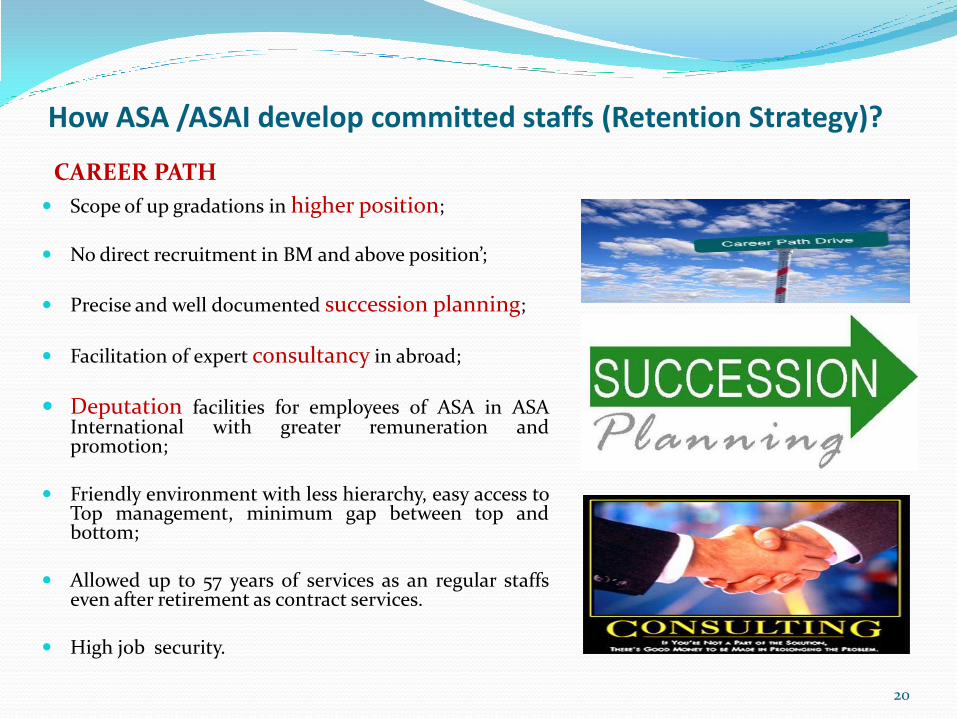

How ASA /ASAI develop skilled staffs? RECRUITMENT

Bulk recruitment in entry level position, Loan Officer in multiple screening process;

Decentralized and local recruitment;

Minimum graduation as education qualification;

17

Pre Service Orientation courses: 30% theoretical and 70% practical learning by doing methods;

Each one teach one: One skilled and experiences staffs take responsibilities to train up new comer through practical demonstrations of the daily activities;

Refreshers and up gradations’ courses after certain period in each level;

Scope of higher training/ diploma courses in abroad.

Separate HR division who have been working independently without any interference.

Separate courses, contents and curriculum on training for different level staffs.

TRAINING

18

Introduced written manual on training, operations, internal audits, accounts and finance, HR policies etc.

Monthly basis workshop and coordination meetings.

Feedback session at branch level two/three times in month ;

Written feedback at branch level on monitoring register;

By-routed responsibility for LO’s at the position of cashier and BM positions;

WRITTEN MANUALS, WORKSHOP AND FEEDBACK

19

Scope of up gradations in higher position; No direct recruitment in BM and above position’;

Precise and well documented succession planning;

Facilitation of expert consultancy in abroad;

Deputation facilities for employees of ASA in ASA International with greater remuneration and promotion;

Friendly environment with less hierarchy, easy access to Top management, minimum gap between top and bottom;

Allowed up to 57 years of services as an regular staffs

even after retirement as contract services.

High job security.

How ASA /ASAI develop committed staffs (Retention Strategy)?

CAREER PATH

20

Comparatively offered good salary including others benefits i.e.60%-70% house rent, 20% provident fund against basis, tow times gratuity of last basic for one year , medical and conveyance ,entertainment, city, cell phone, special allowances etc;

Periodical i.e. within a two years review of salary and benefits package;

Two festival allowance in a year;

Ensure proper working environment by ensuring proper work

ethics, employee conduct, open communication, security and safety etc.

100% costs of medical treatment covered by ASA if any one suffering serious disease .Employees and spouse both will be entitled.

Life insurance for all level staffs.

BENEFITS/ REMUNERATIONS

21

05 years full salary and benefits to staffs families as Employee Family Protection (EFP) if any one died on accident;

Allowed to take loses of personal belongings due to any robbery or unwanted accident.

Children of staffs allowed 100%-25 % weavers for higher study in ASA University;

Loan against provident fund and gratuity with lower rate;

Scope of housing loan with subsidies rate;

40% subsidy of Vehicle loan for BM and above level staffs in the fields.

BENEFITS/ REMUNERATIONS

22

Ensured chain of comments , discipline , justice and equality among the male female, gender, race and different geographical territories;

Multitier & Automated (MIS) reporting ensures higher transparency and accountability;

Female getting little advance of financial benefits;

Allowed to work in nearest and short distance of home to working place;

Residential facilitates in branch level; Food facilities in the branch’;

Presence of Grievance identification team ( GIT) & Performance evaluation team who are working independently;

Well written HR manual;

Essence of the growth is building “TRUST” between organization and staffs earn through mutual understanding & benefits.

TRANSPARENCY AND JUSTICE

23

ACHIEVED AWARD

2007 – Listed as Top microfinance

institute by the joint declaration of world famous magazine Forbes and MiX among the Top 50 Microfinance Institutes. Each MFI’s earned scores in the categories of scale, efficiency, portfolio risk and profitability.

2008 – Awarded as most sustainable

bank of the year by Financial Times and IFC jointly for the

category of “at the Base of the Pyramid”

24

THANK YOU!

Presented by:

Md. Enamul Haque

Executive Vice President, ASA

Chief Operating Officer, ASA International

Website: www.asa.org.bd, www.asa-international.com

25