30

Offshore Wind Energy – The Installation Challenge Prof. Dr. Martin Skiba Director Wind Energy Offshore RWE Innogy GmbH Nomura Offshore Wind Seminar London, 22 January 2010

Offshore Wind Energy –The Installation Challenge

Prof. Dr. Martin SkibaDirector Wind Energy OffshoreRWE Innogy GmbH

Nomura Offshore Wind SeminarLondon, 22 January 2010

RWE Innogy | Nomura Offshore Wind Seminar 22 January 2010 PAGE 2

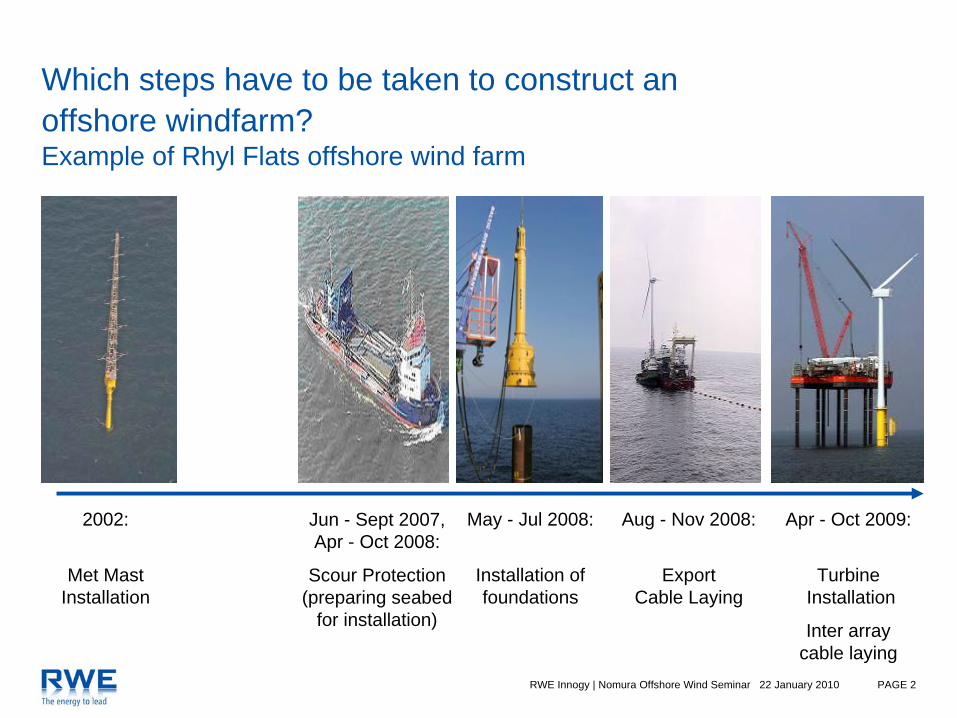

Which steps have to be taken to construct an offshore windfarm?Example of Rhyl Flats offshore wind farm

2002:

Met Mast Installation

May - Jul 2008:

Installation of foundations

Apr - Oct 2009:

TurbineInstallation

Inter arraycable laying

Aug - Nov 2008:

ExportCable Laying

Jun - Sept 2007, Apr - Oct 2008:

Scour Protection(preparing seabed

for installation)

RWE Innogy | Nomura Offshore Wind Seminar 22 January 2010 PAGE 3

Getting to the point: What are the major challenges in offshore installation?

1. Ensuring health & safety of workforce

2. Construction process is exposed to demanding weather conditions

3. All key components have to be installed in large numbers in deepwater and high altitude…

4. …and carry a substantial individual weight

5. Availability and design of installation vessels crucial, but currentlydo not meet market requirements

RWE Innogy | Nomura Offshore Wind Seminar 22 January 2010 PAGE 4

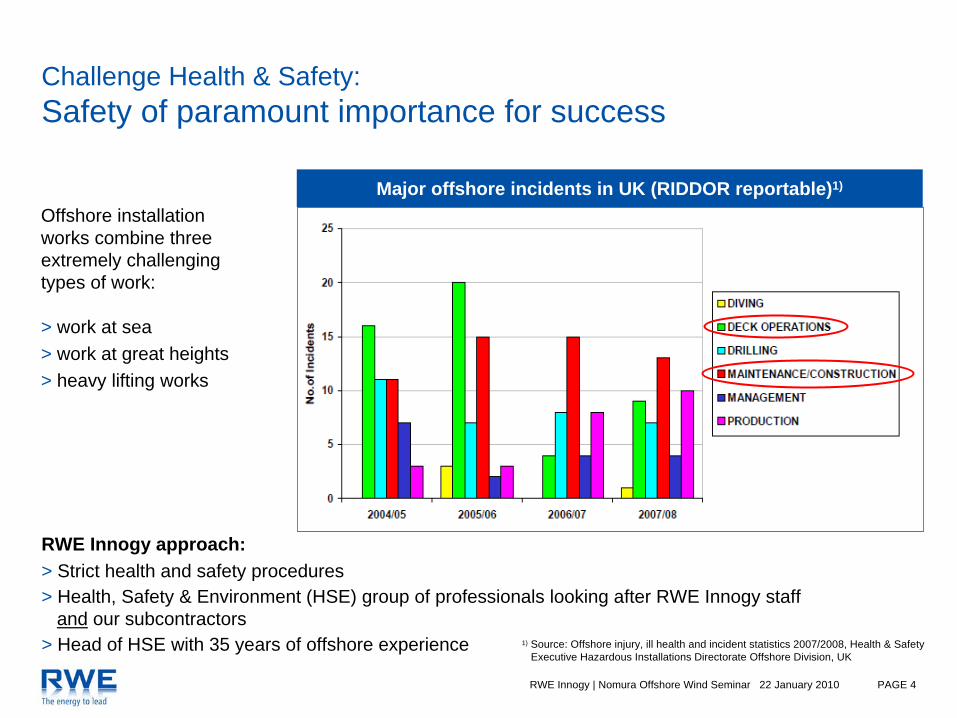

Challenge Health & Safety: Safety of paramount importance for success

Offshore installationworks combine threeextremely challengingtypes of work:

> work at sea> work at great heights> heavy lifting works

1) Source: Offshore injury, ill health and incident statistics 2007/2008, Health & SafetyExecutive Hazardous Installations Directorate Offshore Division, UK

RWE Innogy approach:> Strict health and safety procedures> Health, Safety & Environment (HSE) group of professionals looking after RWE Innogy staff

and our subcontractors> Head of HSE with 35 years of offshore experience

Major offshore incidents in UK (RIDDOR reportable)1)

RWE Innogy | Nomura Offshore Wind Seminar 22 January 2010 PAGE 5

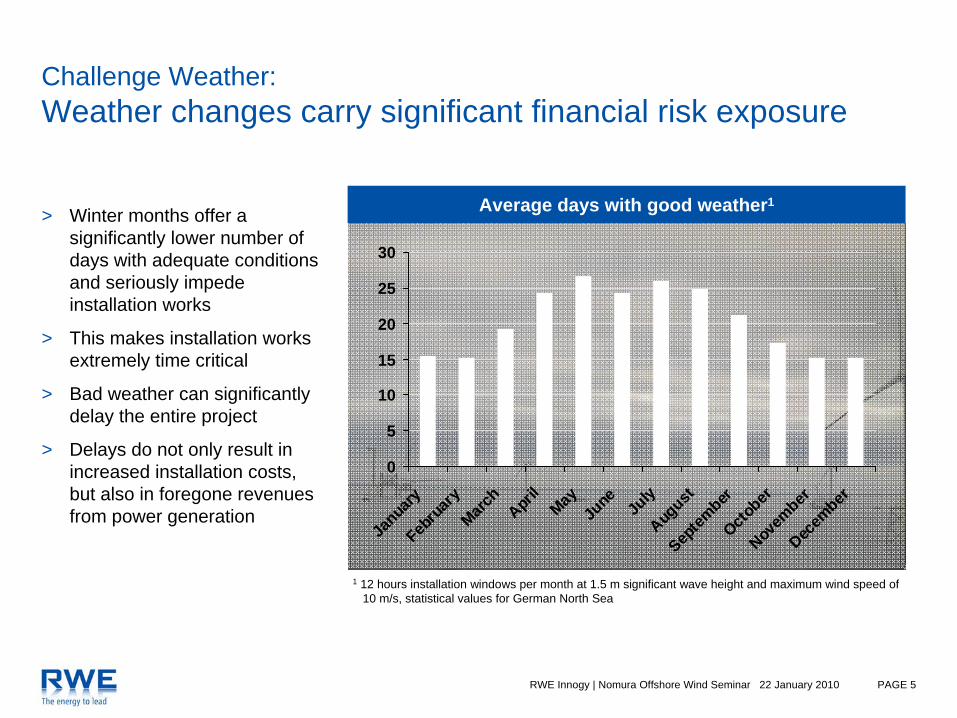

Challenge Weather: Weather changes carry significant financial risk exposure

0

5

10

15

20

25

30

Janua

ryFeb

ruar

yMarc

hApr

ilMayJu

ne July

August

Septem

berOcto

berNov

ember

Decem

ber

1 12 hours installation windows per month at 1.5 m significant wave height and maximum wind speed of 10 m/s, statistical values for German North Sea

Average days with good weather1> Winter months offer a

significantly lower number of days with adequate conditionsand seriously impedeinstallation works

> This makes installation worksextremely time critical

> Bad weather can significantly delay the entire project

> Delays do not only result in increased installation costs, but also in foregone revenues from power generation

RWE Innogy | Nomura Offshore Wind Seminar 22 January 2010 PAGE 6

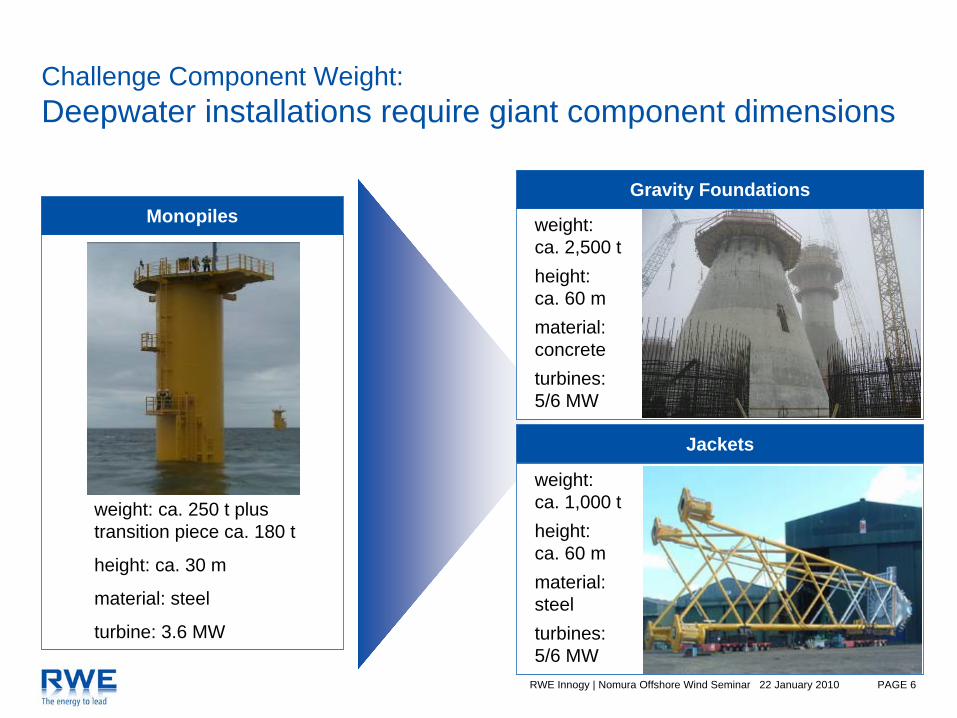

Challenge Component Weight: Deepwater installations require giant component dimensions

weight: ca. 250 t plus transition piece ca. 180 t

height: ca. 30 m

material: steel

turbine: 3.6 MW

weight: ca. 2,500 t height: ca. 60 mmaterial: concreteturbines:5/6 MW

Gravity Foundations

weight: ca. 1,000 t height: ca. 60 mmaterial: steelturbines:5/6 MW

Jackets

Monopiles

RWE Innogy | Nomura Offshore Wind Seminar 22 January 2010 PAGE 7

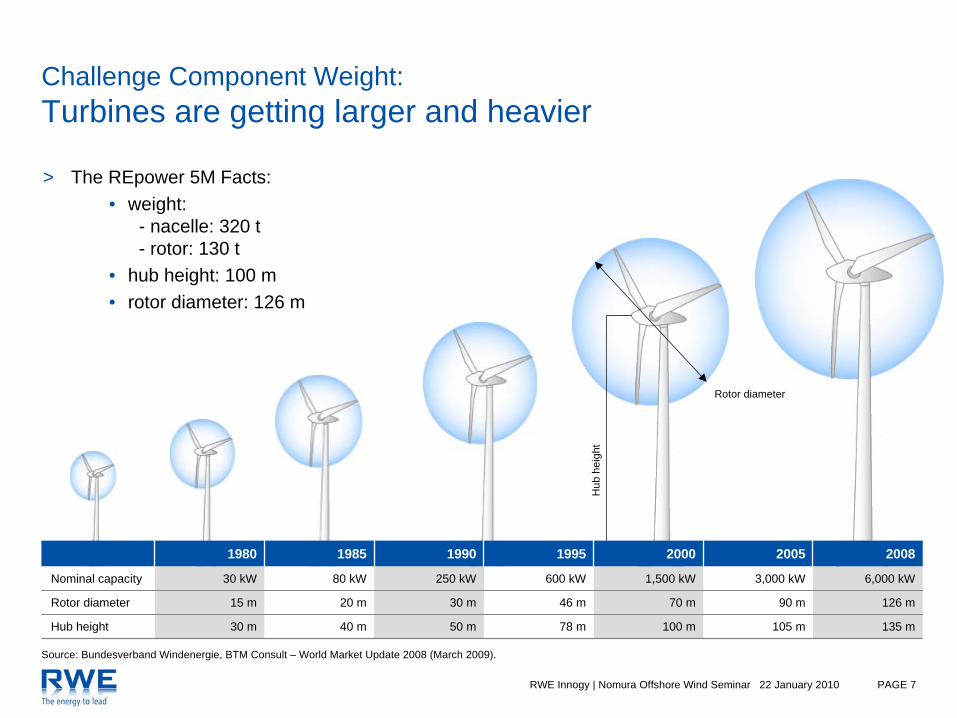

Rotor diameter

Hub

hei

ght

Source: Bundesverband Windenergie, BTM Consult – World Market Update 2008 (March 2009).

105 m

90 m

3,000 kW

2005

135 m

126 m

6,000 kW

2008

100 m

70 m

1,500 kW

2000

78 m50 m40 m30 mHub height

46 m30 m20 m15 mRotor diameter

600 kW250 kW80 kW30 kWNominal capacity

1995199019851980

Challenge Component Weight:Turbines are getting larger and heavier

> The REpower 5M Facts:• weight:

- nacelle: 320 t- rotor: 130 t

• hub height: 100 m• rotor diameter: 126 m

RWE Innogy | Nomura Offshore Wind Seminar 22 January 2010 PAGE 8

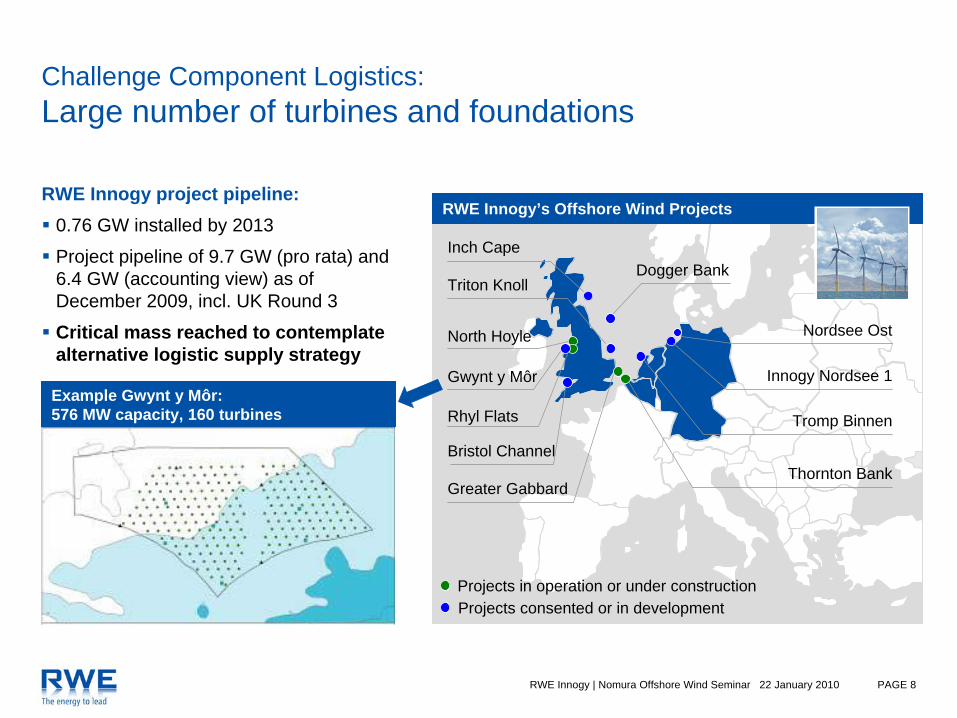

Challenge Component Logistics:Large number of turbines and foundations

RWE Innogy’s Offshore Wind Projects

Inch Cape

Triton Knoll

North Hoyle

Gwynt y Môr

Rhyl Flats

Greater Gabbard

Nordsee Ost

Innogy Nordsee 1

Tromp Binnen

Thornton Bank

Projects in operation or under constructionProjects consented or in development

Bristol Channel

Dogger Bank

RWE Innogy project pipeline:0.76 GW installed by 2013

Project pipeline of 9.7 GW (pro rata) and 6.4 GW (accounting view) as of December 2009, incl. UK Round 3

Critical mass reached to contemplate alternative logistic supply strategy

Example Gwynt y Môr: 576 MW capacity, 160 turbines

RWE Innogy | Nomura Offshore Wind Seminar 22 January 2010 PAGE 9

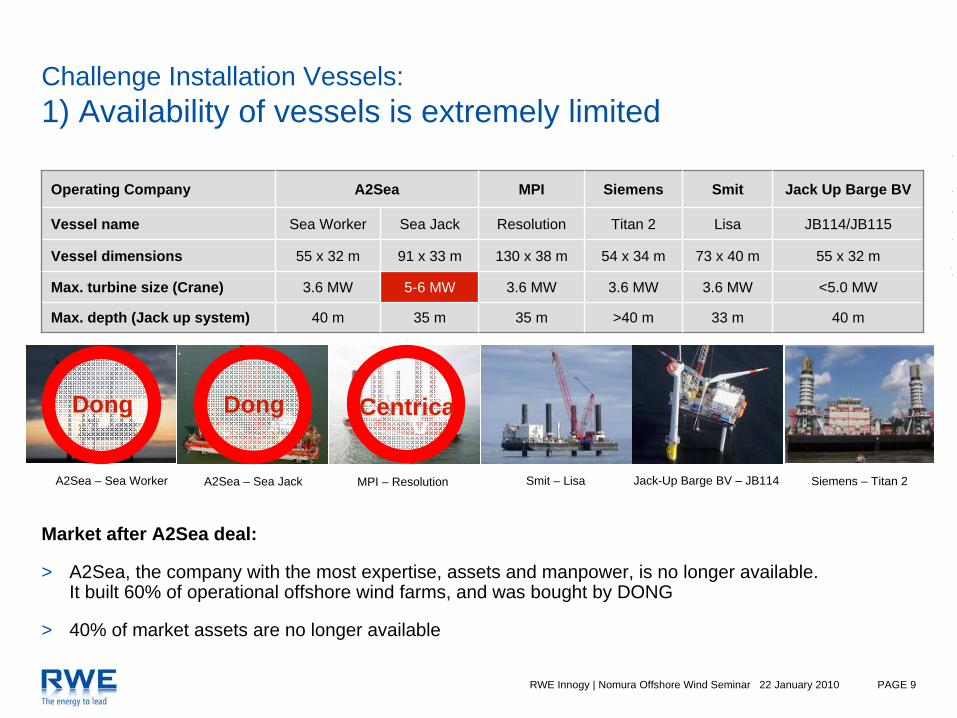

Challenge Installation Vessels:1) Availability of vessels is extremely limited

A2Sea – Sea JackA2Sea – Sea Worker MPI – Resolution Smit – Lisa Siemens – Titan 2Jack-Up Barge BV – JB114

Dong Dong

55 x 32 m73 x 40 m54 x 34 m130 x 38 m91 x 33 m55 x 32 mVessel dimensions

40 m33 m>40 m35 m35 m40 mMax. depth (Jack up system)

<5.0 MW3.6 MW3.6 MW3.6 MW5-6 MW3.6 MWMax. turbine size (Crane)

JB114/JB115LisaTitan 2 ResolutionSea JackSea WorkerVessel name

Jack Up Barge BVSmitSiemensMPIA2SeaOperating Company

Market after A2Sea deal:

> A2Sea, the company with the most expertise, assets and manpower, is no longer available. It built 60% of operational offshore wind farms, and was bought by DONG

> 40% of market assets are no longer available

Centrica

RWE Innogy | Nomura Offshore Wind Seminar 22 January 2010 PAGE 10

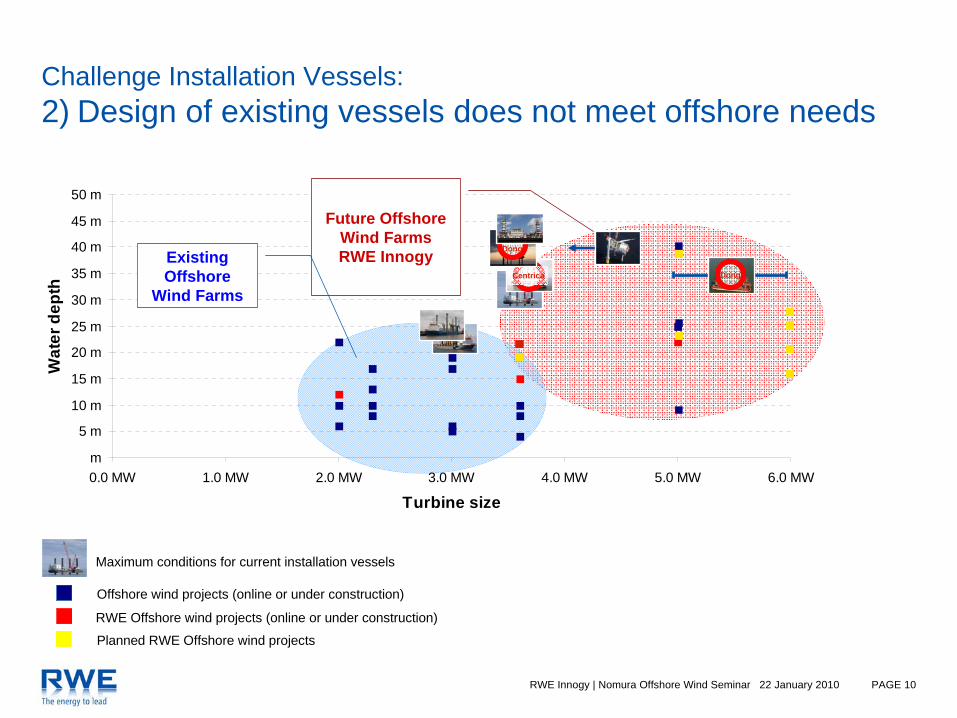

Challenge Installation Vessels:2) Design of existing vessels does not meet offshore needs

m

5 m

10 m

15 m

20 m

25 m

30 m

35 m

40 m

45 m

50 m

0.0 MW 1.0 MW 2.0 MW 3.0 MW 4.0 MW 5.0 MW 6.0 MW

Turbine size

Wat

er d

epth

Offshore wind projects (online or under construction)

RWE Offshore wind projects (online or under construction)

Planned RWE Offshore wind projects

Future Offshore Wind FarmsRWE InnogyExisting

OffshoreWind Farms

Centrica

Dong

Dong

Maximum conditions for current installation vessels

RWE Innogy | Nomura Offshore Wind Seminar 22 January 2010 PAGE 11

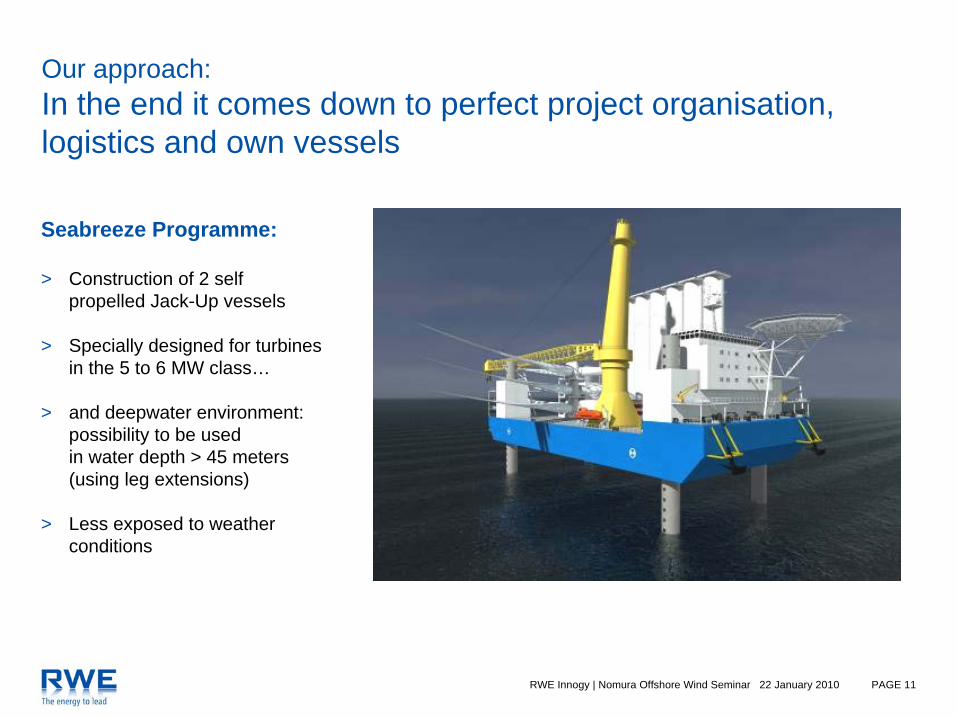

Our approach: In the end it comes down to perfect project organisation, logistics and own vessels

Seabreeze Programme:

> Construction of 2 self propelled Jack-Up vessels

> Specially designed for turbinesin the 5 to 6 MW class…

> and deepwater environment: possibility to be usedin water depth > 45 meters (using leg extensions)

> Less exposed to weather conditions

RWE Innogy | Nomura Offshore Wind Seminar 22 January 2010 PAGE 12

Back-up

RWE Innogy | Nomura Offshore Wind Seminar 22 January 2010 PAGE 13

BiomassWind Onshore Wind Offshore Hydro New Applications

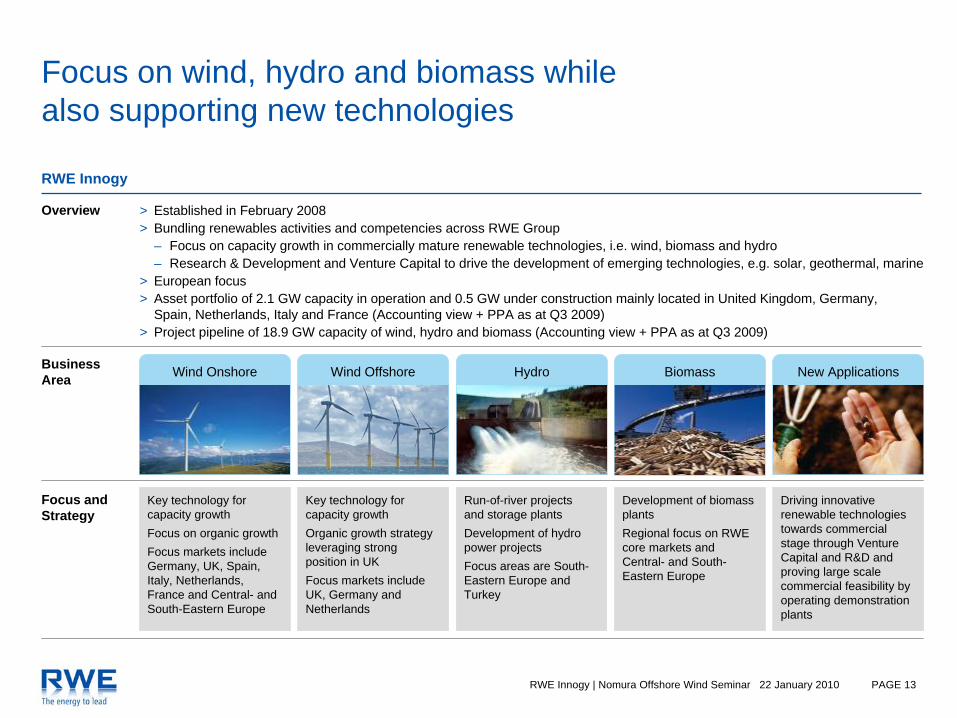

Focus on wind, hydro and biomass whilealso supporting new technologies

Overview

Business Area

Focus and Strategy

> Established in February 2008> Bundling renewables activities and competencies across RWE Group

– Focus on capacity growth in commercially mature renewable technologies, i.e. wind, biomass and hydro– Research & Development and Venture Capital to drive the development of emerging technologies, e.g. solar, geothermal, marine

> European focus > Asset portfolio of 2.1 GW capacity in operation and 0.5 GW under construction mainly located in United Kingdom, Germany,

Spain, Netherlands, Italy and France (Accounting view + PPA as at Q3 2009)> Project pipeline of 18.9 GW capacity of wind, hydro and biomass (Accounting view + PPA as at Q3 2009)

RWE Innogy

Key technology for capacity growthFocus on organic growthFocus markets include Germany, UK, Spain, Italy, Netherlands, France and Central- and South-Eastern Europe

Key technology for capacity growthOrganic growth strategy leveraging strong position in UKFocus markets include UK, Germany andNetherlands

Run-of-river projectsand storage plantsDevelopment of hydro power projectsFocus areas are South-Eastern Europe and Turkey

Development of biomass plantsRegional focus on RWE core markets andCentral- and South-Eastern Europe

Driving innovative renewable technologies towards commercial stage through Venture Capital and R&D and proving large scale commercial feasibility by operating demonstration plants

RWE Innogy | Nomura Offshore Wind Seminar 22 January 2010 PAGE 14

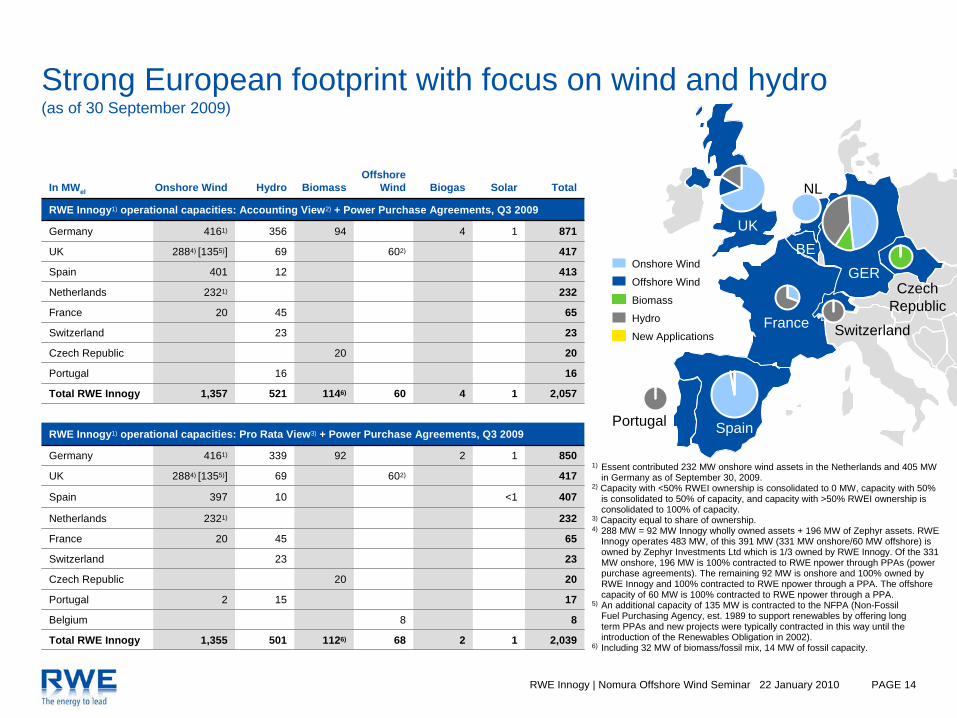

GER

UK

SpainPortugal

France Switzerland

CzechRepublic

RWE Innogy1) operational capacities: Accounting View2) + Power Purchase Agreements, Q3 2009

2020Czech Republic

2323Switzerland

41312401Spain

1

1

Solar

2322321)Netherlands

4

4

Biogas

871943564161)Germany

417602)692884) [1355)]UK

654520France

1616Portugal

2,057601146)5211,357Total RWE Innogy

TotalOffshore

WindBiomassHydroOnshore WindIn MWel NL

BE

1) Essent contributed 232 MW onshore wind assets in the Netherlands and 405 MW in Germany as of September 30, 2009.

2) Capacity with <50% RWEI ownership is consolidated to 0 MW, capacity with 50% is consolidated to 50% of capacity, and capacity with >50% RWEI ownership is consolidated to 100% of capacity.

3) Capacity equal to share of ownership. 4) 288 MW = 92 MW Innogy wholly owned assets + 196 MW of Zephyr assets. RWE

Innogy operates 483 MW, of this 391 MW (331 MW onshore/60 MW offshore) is owned by Zephyr Investments Ltd which is 1/3 owned by RWE Innogy. Of the 331 MW onshore, 196 MW is 100% contracted to RWE npower through PPAs (power purchase agreements). The remaining 92 MW is onshore and 100% owned by RWE Innogy and 100% contracted to RWE npower through a PPA. The offshore capacity of 60 MW is 100% contracted to RWE npower through a PPA.

5) An additional capacity of 135 MW is contracted to the NFPA (Non-FossilFuel Purchasing Agency, est. 1989 to support renewables by offering longterm PPAs and new projects were typically contracted in this way until the introduction of the Renewables Obligation in 2002).

6) Including 32 MW of biomass/fossil mix, 14 MW of fossil capacity.

New Applications

Hydro

Onshore Wind

Biomass

Offshore Wind

17152Portugal

RWE Innogy1) operational capacities: Pro Rata View3) + Power Purchase Agreements, Q3 2009

2020Czech Republic

2323Switzerland

407<110397Spain

1

1

2322321)Netherlands

2

2 850923394161)Germany

417602)692884) [1355)]UK

654520France

88Belgium

2,039681126)5011,355Total RWE Innogy

Strong European footprint with focus on wind and hydro(as of 30 September 2009)

RWE Innogy | Nomura Offshore Wind Seminar 22 January 2010 PAGE 15

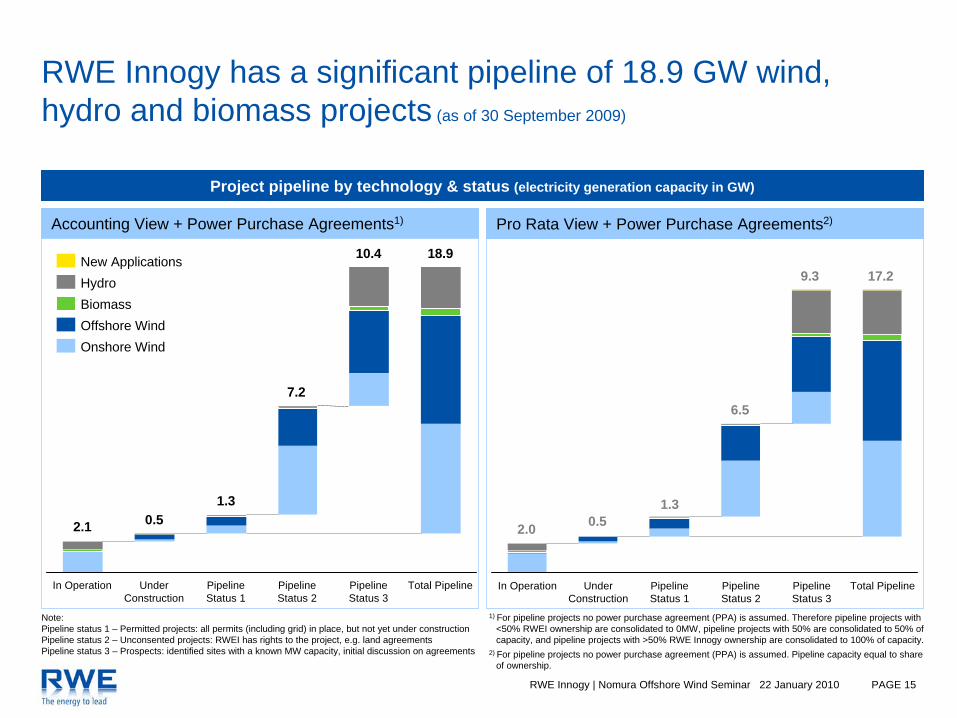

RWE Innogy has a significant pipeline of 18.9 GW wind,hydro and biomass projects (as of 30 September 2009)

Project pipeline by technology & status (electricity generation capacity in GW)

Note:Pipeline status 1 – Permitted projects: all permits (including grid) in place, but not yet under constructionPipeline status 2 – Unconsented projects: RWEI has rights to the project, e.g. land agreementsPipeline status 3 – Prospects: identified sites with a known MW capacity, initial discussion on agreements

18.9

Total PipelinePipeline Status 3

10.4

Pipeline Status 2

7.2

Pipeline Status 1

1.3

Under Construction

0.5

In Operation

2.1

Onshore WindOffshore WindBiomassHydroNew Applications

1) For pipeline projects no power purchase agreement (PPA) is assumed. Therefore pipeline projects with <50% RWEI ownership are consolidated to 0MW, pipeline projects with 50% are consolidated to 50% of capacity, and pipeline projects with >50% RWE Innogy ownership are consolidated to 100% of capacity.

2) For pipeline projects no power purchase agreement (PPA) is assumed. Pipeline capacity equal to share of ownership.

17.2

Total PipelinePipeline Status 3

9.3

Pipeline Status 2

6.5

Pipeline Status 1

1.3

Under Construction

0.5

In Operation

2.0

Accounting View + Power Purchase Agreements1) Pro Rata View + Power Purchase Agreements2)

RWE Innogy | Nomura Offshore Wind Seminar 22 January 2010 PAGE 16

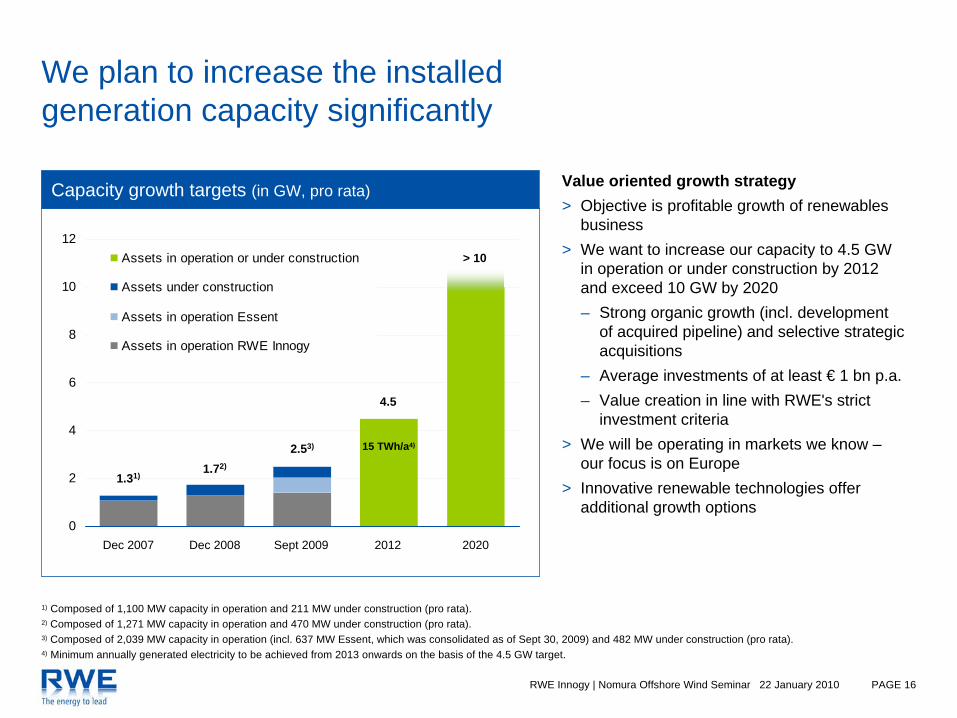

We plan to increase the installedgeneration capacity significantly

Capacity growth targets (in GW, pro rata) Value oriented growth strategy> Objective is profitable growth of renewables

business> We want to increase our capacity to 4.5 GW

in operation or under construction by 2012 and exceed 10 GW by 2020– Strong organic growth (incl. development

of acquired pipeline) and selective strategic acquisitions

– Average investments of at least € 1 bn p.a.– Value creation in line with RWE's strict

investment criteria> We will be operating in markets we know –

our focus is on Europe> Innovative renewable technologies offer

additional growth options

1) Composed of 1,100 MW capacity in operation and 211 MW under construction (pro rata).2) Composed of 1,271 MW capacity in operation and 470 MW under construction (pro rata).3) Composed of 2,039 MW capacity in operation (incl. 637 MW Essent, which was consolidated as of Sept 30, 2009) and 482 MW under construction (pro rata).4) Minimum annually generated electricity to be achieved from 2013 onwards on the basis of the 4.5 GW target.

0

2

4

6

8

10

12Assets in operation or under construction

Assets under construction

Assets in operation Essent

Assets in operation RWE Innogy

1.72)

2.53)

4.5

> 10

Dec 2008 Sept 2009 20202012

15 TWh/a4)

Dec 2007

1.31)

RWE Innogy | Nomura Offshore Wind Seminar 22 January 2010 PAGE 17

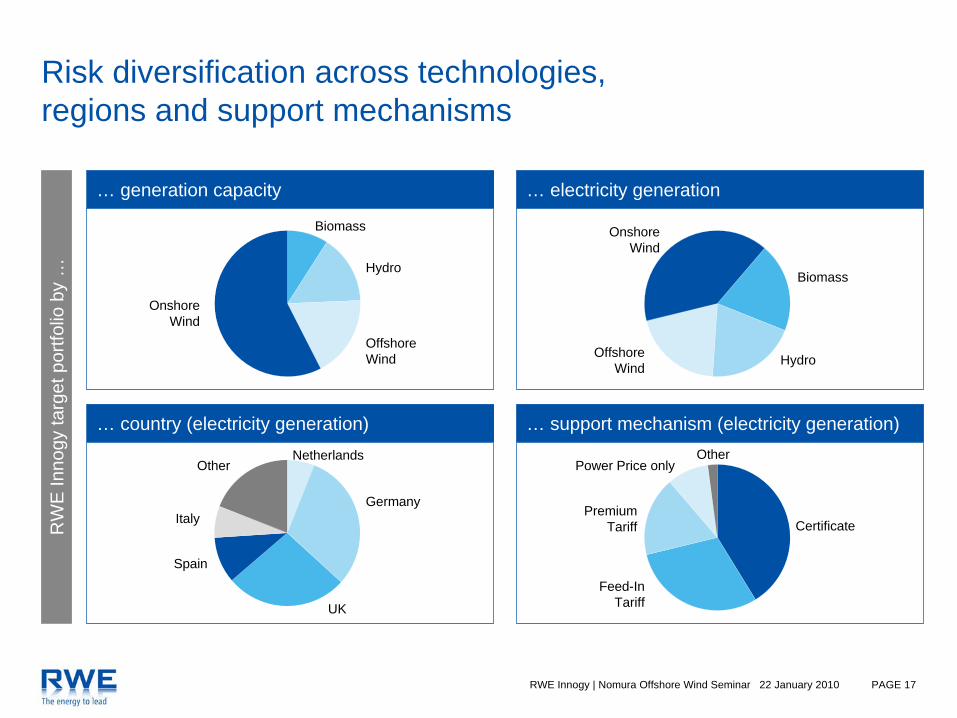

Risk diversification across technologies,regions and support mechanisms

… generation capacity … electricity generation

… country (electricity generation) … support mechanism (electricity generation)

RW

E In

nogy

targ

et p

ortfo

lio b

y … Hydro

OffshoreWind

Biomass

OnshoreWind

HydroOffshoreWind

Biomass

OnshoreWind

Germany

UK

NetherlandsOther

Certificate

OtherPower Price only

Italy

Spain

PremiumTariff

Feed-InTariff

RWE Innogy | Nomura Offshore Wind Seminar 22 January 2010 PAGE 18

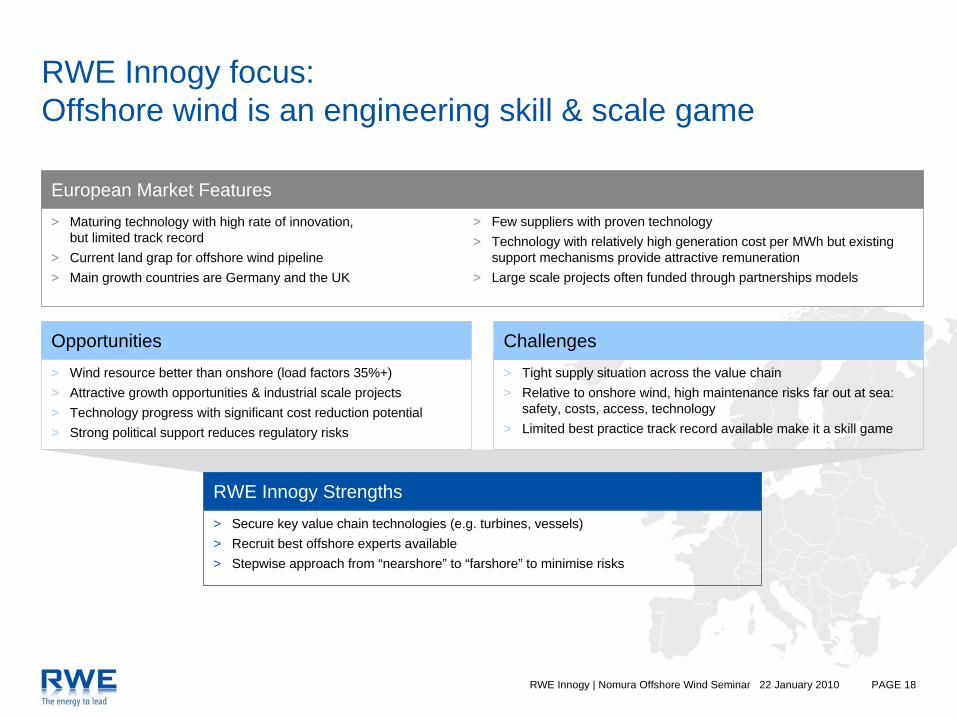

RWE Innogy focus: Offshore wind is an engineering skill & scale game

European Market Features> Maturing technology with high rate of innovation,

but limited track record> Current land grap for offshore wind pipeline> Main growth countries are Germany and the UK

> Few suppliers with proven technology> Technology with relatively high generation cost per MWh but existing

support mechanisms provide attractive remuneration> Large scale projects often funded through partnerships models

Opportunities> Wind resource better than onshore (load factors 35%+)> Attractive growth opportunities & industrial scale projects> Technology progress with significant cost reduction potential> Strong political support reduces regulatory risks

Challenges> Tight supply situation across the value chain> Relative to onshore wind, high maintenance risks far out at sea:

safety, costs, access, technology> Limited best practice track record available make it a skill game

RWE Innogy Strengths> Secure key value chain technologies (e.g. turbines, vessels)> Recruit best offshore experts available> Stepwise approach from “nearshore” to “farshore” to minimise risks

RWE Innogy | Nomura Offshore Wind Seminar 22 January 2010 PAGE 19

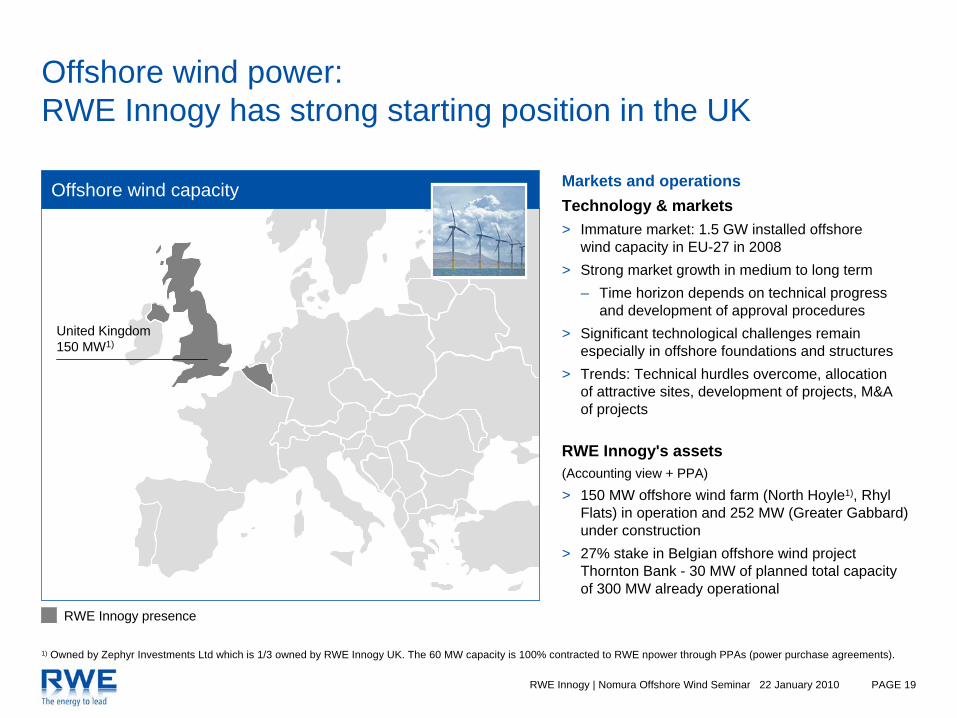

United Kingdom150 MW1)

Offshore wind power:RWE Innogy has strong starting position in the UK

Offshore wind capacity

RWE Innogy presence

1) Owned by Zephyr Investments Ltd which is 1/3 owned by RWE Innogy UK. The 60 MW capacity is 100% contracted to RWE npower through PPAs (power purchase agreements).

Markets and operationsTechnology & markets> Immature market: 1.5 GW installed offshore

wind capacity in EU-27 in 2008> Strong market growth in medium to long term

– Time horizon depends on technical progressand development of approval procedures

> Significant technological challenges remain especially in offshore foundations and structures

> Trends: Technical hurdles overcome, allocationof attractive sites, development of projects, M&Aof projects

RWE Innogy's assets(Accounting view + PPA)

> 150 MW offshore wind farm (North Hoyle1), RhylFlats) in operation and 252 MW (Greater Gabbard) under construction

> 27% stake in Belgian offshore wind project Thornton Bank - 30 MW of planned total capacityof 300 MW already operational

RWE Innogy | Nomura Offshore Wind Seminar 22 January 2010 PAGE 20

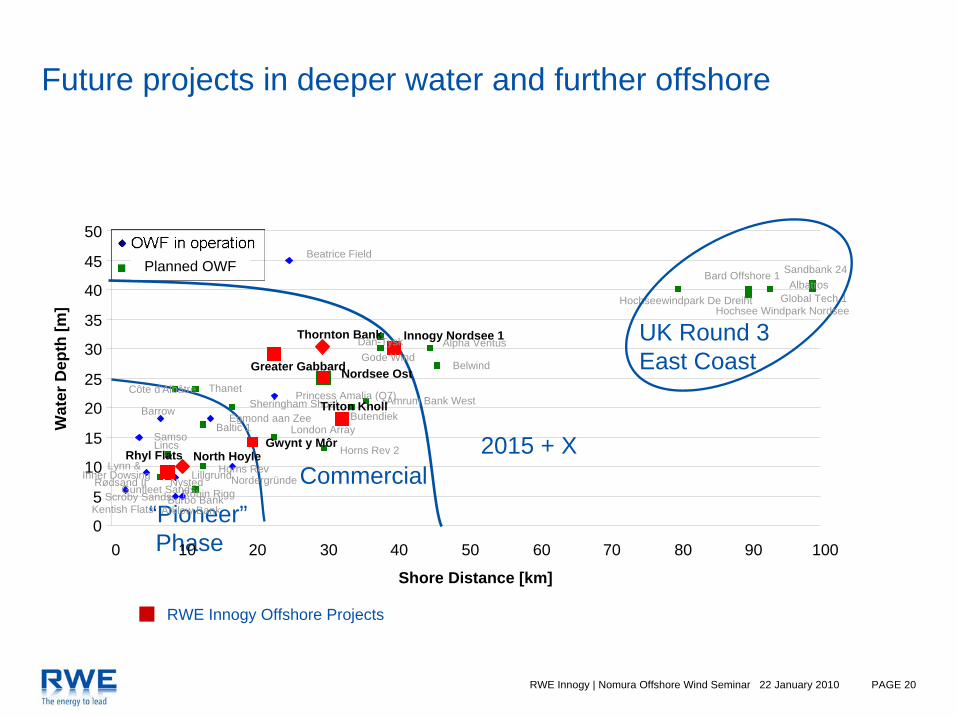

Future projects in deeper water and further offshore

“Pioneer”Phase

Commercial2015 + X

RWE Innogy Offshore Projects

Princess Amalia (Q7)

Burbo Bank

Samso

Belwind

Robin Rigg

Lynn & Inner Dowsing Lillgrund

BarrowEgmond aan Zee

Beatrice Field

Kentish FlatsScroby Sands

Arklow Bank

North Hoyle

NystedHorns Rev

Innogy Nordsee 1

London Array

Nordergründe

Nordsee Ost

Sheringham Shoal

Lincs

Rødsand II

Côte d'Albâtre

Baltic 1

Bard Offshore 1

Greater Gabbard

Thanet

Gunfleet Sands

Horns Rev 2Rhyl Flats

Alpha VentusThornton Bank

Gwynt y Môr

Global Tech 1

Amrum Bank West

Dan-Tysk

Sandbank 24

Triton Knoll

Hochseewindpark De Dreiht

Gode Wind

Butendiek

Albatros

0

5

10

15

20

25

30

35

40

45

50

0 10 20 30 40 50 60 70 80 90 100

Shore Distance [km]

Wat

er D

epth

[m]

UK Round 3East Coast

Hochsee Windpark Nordsee

Planned OWF

RWE Innogy | Nomura Offshore Wind Seminar 22 January 2010 PAGE 21

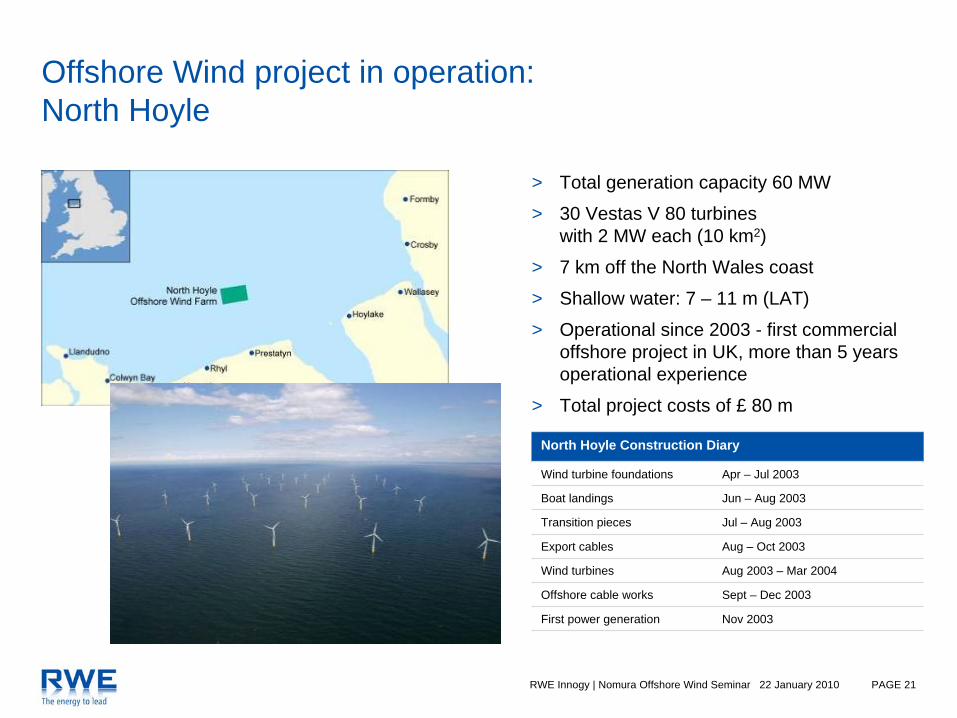

> Total generation capacity 60 MW

> 30 Vestas V 80 turbines with 2 MW each (10 km2)

> 7 km off the North Wales coast

> Shallow water: 7 – 11 m (LAT)

> Operational since 2003 - first commercial offshore project in UK, more than 5 years operational experience

> Total project costs of £ 80 m

Offshore Wind project in operation:North Hoyle

Nov 2003First power generation

Sept – Dec 2003 Offshore cable works

Aug 2003 – Mar 2004Wind turbines

Aug – Oct 2003Export cables

Jul – Aug 2003Transition pieces

Jun – Aug 2003 Boat landings

Apr – Jul 2003 Wind turbine foundations

North Hoyle Construction Diary

RWE Innogy | Nomura Offshore Wind Seminar 22 January 2010 PAGE 22

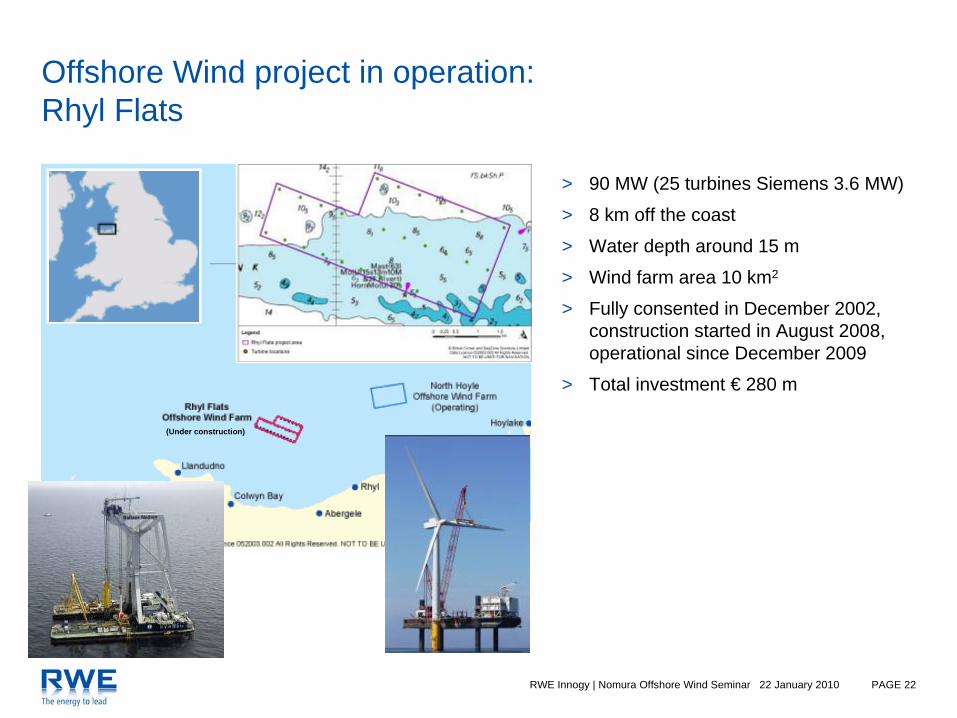

> 90 MW (25 turbines Siemens 3.6 MW)

> 8 km off the coast

> Water depth around 15 m

> Wind farm area 10 km2

> Fully consented in December 2002, construction started in August 2008, operational since December 2009

> Total investment € 280 m

(Under construction)

Offshore Wind project in operation: Rhyl Flats

RWE Innogy | Nomura Offshore Wind Seminar 22 January 2010 PAGE 23

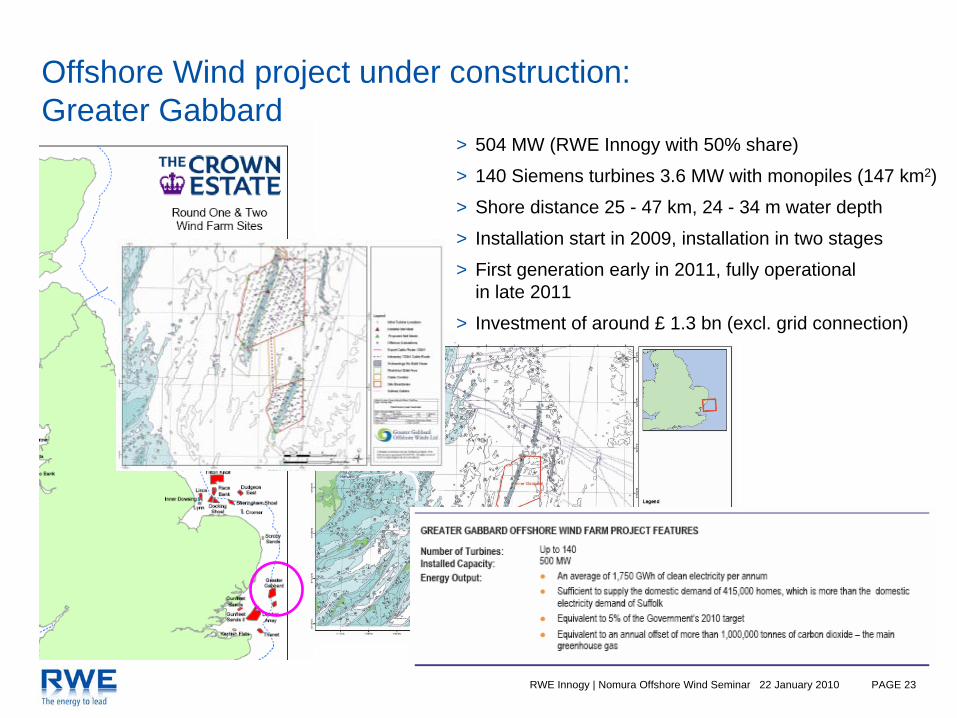

> 504 MW (RWE Innogy with 50% share)

> 140 Siemens turbines 3.6 MW with monopiles (147 km2)

> Shore distance 25 - 47 km, 24 - 34 m water depth

> Installation start in 2009, installation in two stages

> First generation early in 2011, fully operational in late 2011

> Investment of around £ 1.3 bn (excl. grid connection)

Offshore Wind project under construction:Greater Gabbard

RWE Innogy | Nomura Offshore Wind Seminar 22 January 2010 PAGE 24

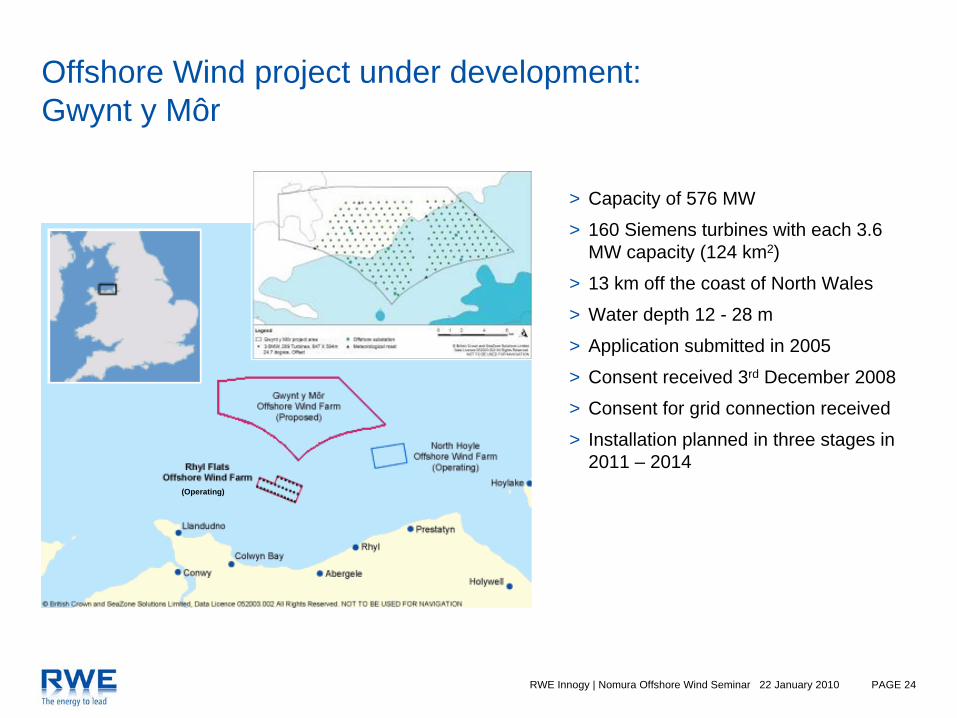

> Capacity of 576 MW

> 160 Siemens turbines with each 3.6 MW capacity (124 km2)

> 13 km off the coast of North Wales

> Water depth 12 - 28 m

> Application submitted in 2005

> Consent received 3rd December 2008

> Consent for grid connection received

> Installation planned in three stages in 2011 – 2014

(Operating)

Offshore Wind project under development:Gwynt y Môr

RWE Innogy | Nomura Offshore Wind Seminar 22 January 2010 PAGE 25

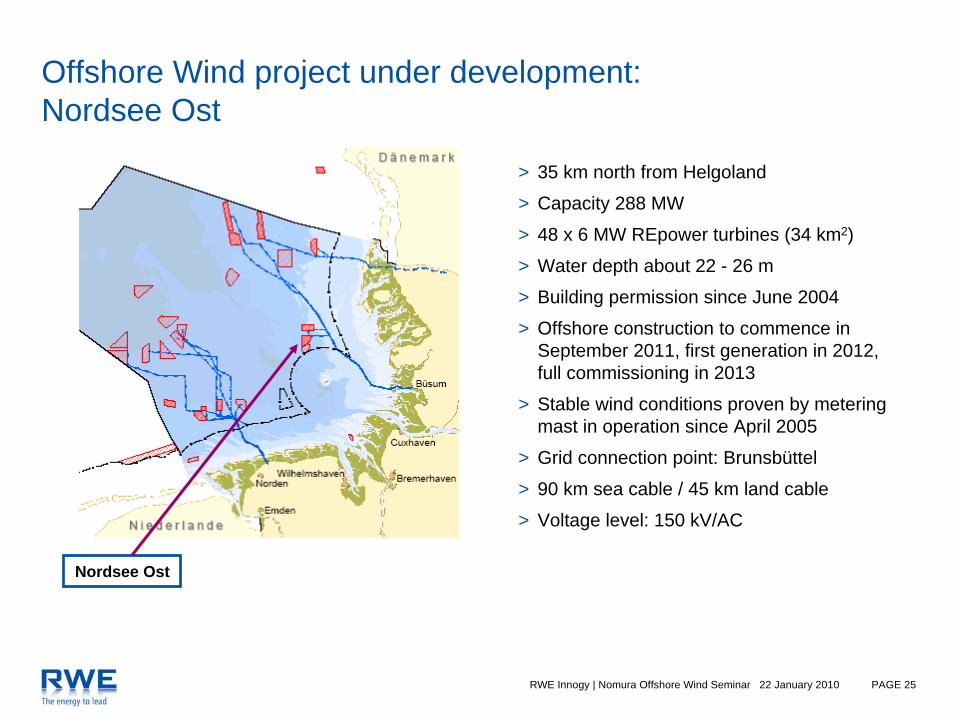

> 35 km north from Helgoland

> Capacity 288 MW

> 48 x 6 MW REpower turbines (34 km2)

> Water depth about 22 - 26 m

> Building permission since June 2004

> Offshore construction to commence in September 2011, first generation in 2012, full commissioning in 2013

> Stable wind conditions proven by metering mast in operation since April 2005

> Grid connection point: Brunsbüttel

> 90 km sea cable / 45 km land cable

> Voltage level: 150 kV/AC

Nordsee Ost

Offshore Wind project under development:Nordsee Ost

RWE Innogy | Nomura Offshore Wind Seminar 22 January 2010 PAGE 26

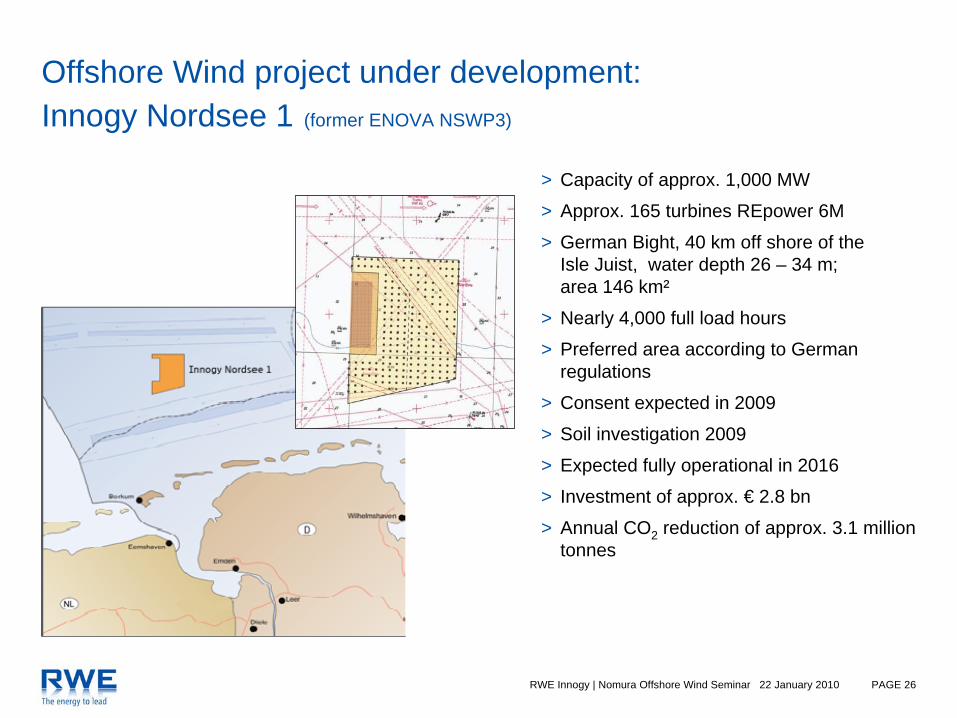

> Capacity of approx. 1,000 MW

> Approx. 165 turbines REpower 6M

> German Bight, 40 km off shore of the Isle Juist, water depth 26 – 34 m; area 146 km²

> Nearly 4,000 full load hours

> Preferred area according to German regulations

> Consent expected in 2009

> Soil investigation 2009

> Expected fully operational in 2016

> Investment of approx. € 2.8 bn

> Annual CO2 reduction of approx. 3.1 million tonnes

Offshore Wind project under development:Innogy Nordsee 1 (former ENOVA NSWP3)

RWE Innogy | Nomura Offshore Wind Seminar 22 January 2010 PAGE 27

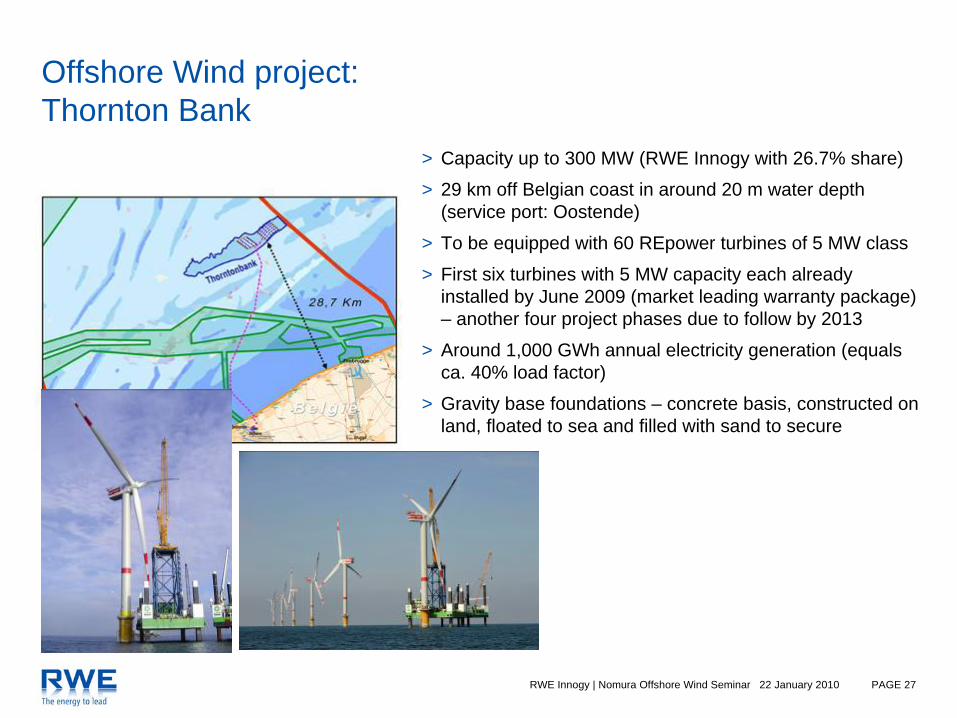

> Capacity up to 300 MW (RWE Innogy with 26.7% share)

> 29 km off Belgian coast in around 20 m water depth (service port: Oostende)

> To be equipped with 60 REpower turbines of 5 MW class

> First six turbines with 5 MW capacity each already installed by June 2009 (market leading warranty package) – another four project phases due to follow by 2013

> Around 1,000 GWh annual electricity generation (equals ca. 40% load factor)

> Gravity base foundations – concrete basis, constructed on land, floated to sea and filled with sand to secure

Offshore Wind project:Thornton Bank

RWE Innogy | Nomura Offshore Wind Seminar 22 January 2010 PAGE 28

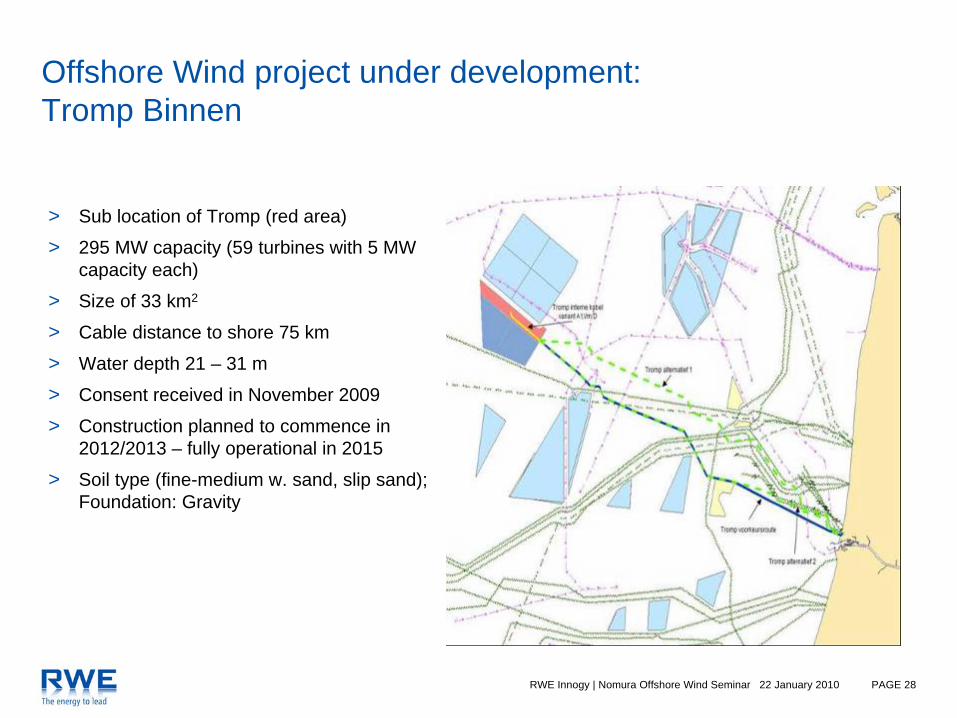

> Sub location of Tromp (red area)

> 295 MW capacity (59 turbines with 5 MW capacity each)

> Size of 33 km2

> Cable distance to shore 75 km

> Water depth 21 – 31 m

> Consent received in November 2009

> Construction planned to commence in 2012/2013 – fully operational in 2015

> Soil type (fine-medium w. sand, slip sand); Foundation: Gravity

Offshore Wind project under development:Tromp Binnen

RWE Innogy | Nomura Offshore Wind Seminar 22 January 2010 PAGE 29

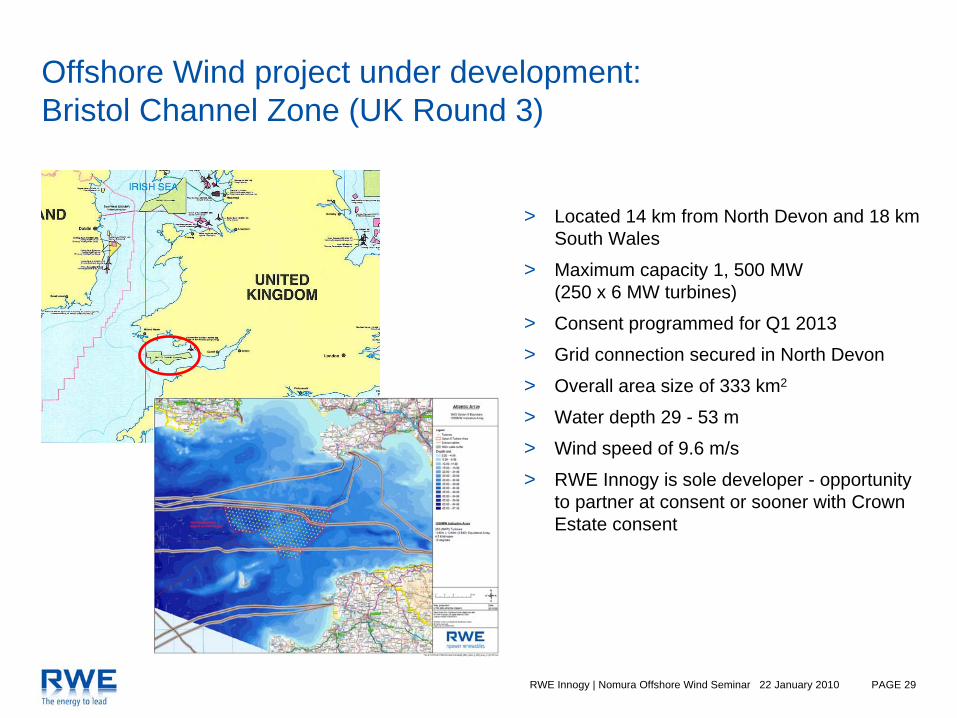

Offshore Wind project under development:Bristol Channel Zone (UK Round 3)

> Located 14 km from North Devon and 18 km South Wales

> Maximum capacity 1, 500 MW (250 x 6 MW turbines)

> Consent programmed for Q1 2013

> Grid connection secured in North Devon

> Overall area size of 333 km2

> Water depth 29 - 53 m

> Wind speed of 9.6 m/s

> RWE Innogy is sole developer - opportunity to partner at consent or sooner with Crown Estate consent

RWE Innogy | Nomura Offshore Wind Seminar 22 January 2010 PAGE 30

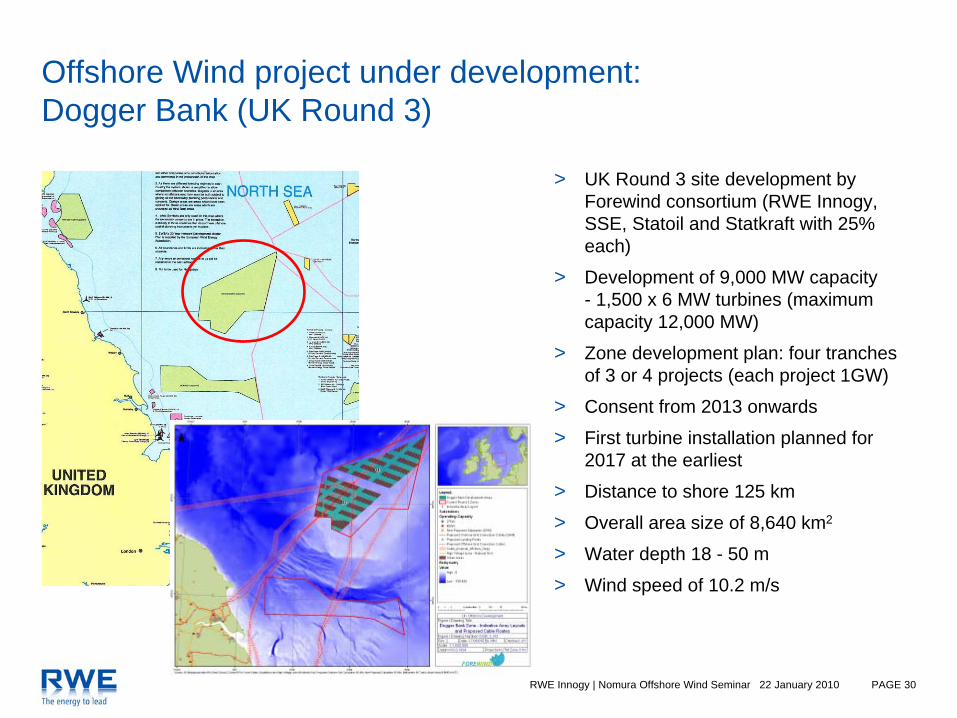

Offshore Wind project under development:Dogger Bank (UK Round 3)

> UK Round 3 site development by Forewind consortium (RWE Innogy, SSE, Statoil and Statkraft with 25% each)

> Development of 9,000 MW capacity- 1,500 x 6 MW turbines (maximum capacity 12,000 MW)

> Zone development plan: four tranches of 3 or 4 projects (each project 1GW)

> Consent from 2013 onwards

> First turbine installation planned for 2017 at the earliest

> Distance to shore 125 km

> Overall area size of 8,640 km2

> Water depth 18 - 50 m

> Wind speed of 10.2 m/s