16

JUNE 2012 ISSUE

2

A SIMSREE FINANCE FORUM INITIATIVE

ARTHNEETI JUNE 2012 ISSUE

EDITORIAL

We have witnessed a slew of depressing data about Indian economy in the last three months. Pick any macroeconomic data and you are bound to get a negative feeling about economy and uncertain future. Fitch and S&P revised India’s credit rating outlook to negative from stable whereas Moody’s reaffirmed credit rating outlook to stable. Policy paralysis of current government is stated as primary reason for current situation where issues like subsidies, reforms, deficit and tax related issues were not addressed on time. On the positive side, decreasing crude price will ease the pressure on deficit front and recent announcement of investments by firms like Coca-Cola and Ikea will help improve investor sentiments. With a change in Finance ministry, government has started making some correct statements like clarifying GAAR, Diesel price decontrol, encouraging FII flows, FDI etc. and we can hope it would implement all these measures which would help the economy. RBI kept key policy rates unchanged in its June meeting giving a clear signal to market about its priority for inflation.

On global front, events like election of somewhat stable and pro-austerity government in Greece, injecting capital into Spanish banks, ECB rate cut helped ease some pressure on euro zone issue.

In this issue, we have interviewed Mr. Rajiv Anand, MD & CEO, Axis Asset Management Company for his views on India’s macro-economic situation, Axis AMC’s recent deal with Schroders, etc.As part of our forum activity we have an article from students on “BASEL III and Indian Banks’ ability to adhere to it”. We have an article from our alumni on“The mechanism of Crude Pricing and factors affecting it”. Lastly, an article on “GAAR and itsimplications” by the SIMSREE Finance Forum.

Happy Reading.

TEAM ARTHNEETI

Special Feature An Interview with Mr. Rajiv Anand, MD & CEO, Axis Asset Management Company BASEL III: IS THE INDIAN BANKING FRATERNITY READY?

By Jubin Mohapatra & Shikha Sharma, DoMS- IIT Roorkee The Crude story of Oil Pricing By Dinesh Agarwal, Alumni SIMSREE GAAR and Its Implications By SIMSREE FINANCE FORUM

JUNE 2012 ISSUE

3

A SIMSREE FINANCE FORUM INITIATIVE

ARTHNEETI JUNE 2012 ISSUE

1. First of all, your take on the current macro-economic situation on India.

Ans: Given the fact that growth has come off, and come off sharply over the last one year, last quarter we were at 5.3%. The fact that rupee has depreciated by almost 20-25%. Inflation continues to remain high. The Current Account Deficit (CAD) is at a perilous high of 4%. The fiscal deficit is expected to be in the vicinity if 5%. These are the indicators of a grim macro-economic situation of India, and need urgent attention.

2. Fidelity’s exit has not gone well with the Fund Management industry. Your take on this.

Ans: Fidelity sold its Mutual Fund business to L&T. I won’t be able to comment on their decision. I am sure they had their reasons to leave India. As far as its effect is concerned, I don’t think it has affected the MF industry as such.

3. After the removal of entry load by SEBI, it was said that the profit margins of the distributors will take a hit or might have taken a hit. What steps have been taken by mutual fund houses to avert this?

Ans: The removal of entry load was 3 years ago. It has become a reality now and the industry has learnt to live with it. Distributors now get a mix of income, partly from the AMCs and partly by charging the customer either an advisory or transaction fee.

4. How is the deal with Schroders expected to benefit Axis MF in the long run?

Ans: Schroders acquired 25% stake in Axis MF. It is 200 year old pure global asset manager, managing $320 billion worth of assets worldwide. In terms of the benefits, we’re planning to use the global brand and distribution of Schroders to sell Indian investment products to global investors. Further, we’ll sell their global products here in India to local investors. We expect to work closely in the areas of investment and risk management, distribution and product development.

5. What’s your message to prospective investors? What points should be kept in mind while investing in Mutual Funds, especially in such tough situations? And is this the right time to get into equities?

Ans: Patience is a great virtue in investing. My advice to all investors is to have patience in such volatile markets. They

Rajiv Anand,

Managing Director and Chief Executive Officer,

Axis Asset Management Company

INTERVIEW: MR. RAJIV ANAND

A commerce graduate and a Chartered Accountant, Mr. Rajiv Anand started off his career with HSBC in Global Markets. Before becoming the MD & CEO at Axis AMC, he has served as an Investment Head at Standard Chartered Mutual Fund and IDFC AMC. His areas of expertise include Investment Management, Building new businesses, Corporate Finance, Risk management, etc.

JUNE 2012 ISSUE

4

A SIMSREE FINANCE FORUM INITIATIVE

ARTHNEETI JUNE 2012 ISSUE

should not get carried away by the market sentiments. I also think investors are too focused on market timing. Investors need to invest in a disciplined by using say SIP's such that the market volatility actually works for you. In fact, this is the right time to get into equities with a long-term horizon by picking right stocks. We (Axis AMC) are buying into equities as well.

6. What key reforms should the government make to sail through the economic slump we are into?

Ans: Working on reforms alone won’t make much of a difference. Streamlining the entire functional and regulatory process will. Hence, rather than reforms the government should focus on removing the bottlenecks to investment, hasten the process of implementation of projects and work towards containing the fiscal deficit by cutting subsidies in a phased manner. These few things itself will go a long way in improving the economic sentiment in this country.

7. What challenges do you anticipate in the Mutual Fund industry?

Ans: India is a high growth economy with high savings rates and under-penetration of mutual fund products. Our challenge really is to reach out to this huge pool of money to articulate the benefits of investing in mutual funds. And we need to do this in a cost effective manner. There is a need for investor education as well in the field of investments in Mutual Fund segment. There are various products available that cater to investors encompassing all risk profiles.

8. How hard has the recent economic slowdown hit the Mutual Fund industry? How has it affected Axis MF?

Ans: The Mutual fund industry sells various types of products across economic cycles. In good times typically investors tend to flock towards equity products. Today investors are buying the more stable fixed income funds. Hence fund houses must have a full product suite to cater to investor needs across market cycles.

Axis Mutual Fund today has funds across the entire range of money market, fixed income, hybrid and equity and all are well prepared to meet investor needs in all market conditions.

9. If you had to give a rating on the basis global competitiveness to Indian Firms, what would it be? (We have read views of some columnists and prominent economists about the value generated by Indian corporate)

Ans: It is difficult to make a generalized statement or give a rating as such, but it is fair to say that we have world-class companies in India across sectors that are able to compete with the best in the world.

“Patience is the virtue of investing”. This is the right time to get into equities with a long-term horizon by picking right stocks. We are buying into equities as well.

JUNE 2012 ISSUE

5

A SIMSREE FINANCE FORUM INITIATIVE

ARTHNEETI JUNE 2012 ISSUE

10. As per you, how can be the current political paralysis fixed? It has been the same for the past 2 decades; do you think that a coalition government causes more damage than good?

Ans: In an emerging economy such as our, you will have difficult times like these. I am very positive about the growth prospects in India. Coalition governments in India are here to stay and I am sure politicians over time will get better working within them. Again, it is a reality and we have to live with it. Of course, with coalition, there is a delay in consensus-building because of difference of opinion between various allies that form the government. How effectively the PM is able to meet the demands of the allies also matters a lot when it comes to garnering their support during an important political or economic event.

11. Any key learning that you would like to share as an advice for budding MBA students like us.

Ans: India is a growing economy and land off opportunities. My advice is- Pursue your dreams, pursue your passion.

FIN-QUIZ 1) He is the pioneer in mutual fund industry and often referred as the Father of Index Fund investing. He created the first S&P 500 Index fund. Identify this famous person?

2) Name the private sector corporate which launched the first gold fund in India.

3) In money market, what is the term used for non-convertible paper money?

4) The Reserve Bank of India provides Export Credit Refinance facility to scheduled banks at which rate?

5) Which six factors are examined under ‘CAMELS’, an International Bank Rating system to asses banks overall condition?

March 2012 Issue Answers:

1. RenukaRamnath

2. Malaysia

3. AIG 4. Fortune 5. Offer for sale (OFS) or the auction route (ONGC was the first company through this route)

“The government should focus on removing the bottlenecks to investment, hasten the process of implementation of projects and work towards containing fiscal deficit”

JUNE 2012 ISSUE

6

A SIMSREE FINANCE FORUM INITIATIVE

ARTHNEETI JUNE 2012 ISSUE

By Jubin Mohapatra & Shikha Sharma, DoMS- IIT Roorkee Before embarking on the depiction of Basel III norms and their futuristic impact on the Indian Banks and Economy at large, let's start off with a simple question- What is a Venture? It simply means an undertaking which has inherent risks and returns. When some capital is invested in a venture it is expected to yield some returns or benefits out of it. But the buck does not stop hereas along with returns also come the rabble-rousers-the different kinds of risks that plague an investment. Risks entail all potential losses which have detrimental effects on the expected output or the returns. The risks can be quantified and analyzed under many heads namely Market risk, Financial risk, Operational risk, Credit risk etc. It is to guard the banks against these risks that the Basel accords were formulated.

The 3 Basel Accords: Raison D’être

Basel Accords were created under the aegis of Basel Committee on banking supervision to provide various avenues of safety against the various credit, operational, market and liquidity risks vis-a-vis the liquidation of banks. The first round of deliberation was conducted in 1988 in response to the insolvency fiasco of Herstatt Bank of Cologne which was attended and ratified by the Central Banks of G10 nations. In June 2004 followed the Basel II regulationswhich broadened the horizon of Basel I to include banking laws and regulations pertaining to capital adequacy, arbitrage regulation, risk quantification, risk classification and risk

sensitive capital allocation.However, Basel II has been sporadically criticized by a section of economists for having magnified the effects of the credit bubble and ergo it has been appended and updated many times on the back of numerous financial turmoils, the sequence of reforms eventually culminating in formulation of Basel III regulations. The accord brought into existence during the year 2010-11 aims to plug the deficiencies which led to the late 2000 banking crises.

Basel III: An Overview

Apart from bank’s capital adequacy, stress tolerance and market risk pruning, the third Basel accord also sketches out well defined contours of bank leverage, capital and liquidity requirements. It tries to reconcile the banking regulations with economic robustness to safeguard against the financial frailties. The 5 salient features of the latest accord are as follows:

• It tries to better the quality, eminence, consistency, and transparency of the capital base by segregating the capital of a bank as Tier 1, 2 and 3

• It strengthens the risk coverage by trying to marginalize the credit risk

• It offers a leverage ratio based system to entrench the Basel II risk frameworks

• It requires building up capital buffers during good times for use during stress and instability

BASEL III: IS THE INDIAN BANKING FRATERNITY READY?

JUNE 2012 ISSUE

7

A SIMSREE FINANCE FORUM INITIATIVE

ARTHNEETI JUNE 2012 ISSUE

• It involves creation of a novel global liquidity standard; involving calculation of de facto liquidity coverage ratio, called Net Stable Funding ratio and it also limits the bad loans

Indian Banking Sector, Basel III and Growth Scenario

After Reserve Bank of India pronounced final guidelines for Basel III commencing 1st January, 2013and to be implemented by 31st March, 2018 speculations have been rife about its potential effects on the Indian GDP growth and whether or not the Indian Banks will be able to meet the cumbersome capital requirements. The potential trade-off between preventive safeguards and languishing economic growth has been making rounds in the economic debate mills of the country. And the cascaded effects of still to be tamed inflation, oil price hike, a free-falling Rupee and sluggish industrial expansion have only escalated the concerns.

Is the Indian Banking Fraternity ready for implementation of Basel III?

Just like every leap of faith this step also has both pros and cons. The downside begins with requirement of a massive capital raising by Indian banks in the tune of Rs 1.67

trillionover the next five years to cater to their growth necessities and boost up their held capital. This figure is churned out from the new Basel III norms requiring a minimum 5.5 per cent in common equity stock by 31st March, 2015 against 3.6 per cent as of now. Moreover creating a capital buffer by 31stMarch, 2018 entails dilution of equity up to 2.5 percent. It has also hiked the minimum overall capital adequacy to 11.5 per cent as opposed to the current level of 9 percent. For now the private sector banks like ICICI, YES Bank, Kotak Mahindra Bank etc. seem to be in a comfortable position to meet the guidelines as compared to the public sector peers like SBI who need large chunks of funding to mop up the required capital for compliance with Basel III.Because of such a massive capital structure overhaul the Indian banks will have to go for stringent loan disbursements which won’t be helpful for the Indian industrial sector which is in dire need of banking support to fortify its position. Further the banks are expected to go harsh on loan defaulters and tidy up the sectors of economy where NPAs are proliferating rapidly like the critical Power sector and MSME sector among others. Henceforth, any rate cuts expected from the chests of RBI will aid in boosting up the capital buffers of banks rather than accelerating the economic progress. All these factors might end up in a medium term reduction in growth rates of around .05 to .15 percent as per OECD studies and will most certainly have an adverse impact on the presently effervescent Indian economy. Withthat being said, let’s take a look at the vibrant side of things and the bigger picture.

As far as Capital Adequacy is concerned, Indian banks are better placed than most of

JUNE 2012 ISSUE

8

A SIMSREE FINANCE FORUM INITIATIVE

ARTHNEETI JUNE 2012 ISSUE

the foreign foils to make a transition to the stricter capital regime. The existing RBI norms are more stringent than the international Basel III standards, which mean that the equity capital ratio and capital adequacy ratio of rated Indian banks are pegged well above the required margins of 9% and 14% respectively. Moreover, recently the international credit rating agency Moody’s and its Indian subsidiary ICRA have gone on record stating that the conservative return on equity and higher cost of capital on loans adopted by Indian banks will actually be seen in a positive light after the implementation of Basel III and it will be Credit Positive for the developing economy of the subcontinent. Also the Leverage Ratio under Basel III needs to be 3% to check derivative counterfeits and takes up cudgels against off the balance sheet trading. But the same ratio for Indian banks lies between 4.3 to 4.5% thus providing a hefty cushion and making it further easier and rudimentary to implement Basel III. Moving on to the Liquidity Coverage Ratio required to provide cash flow for stress period of upto 30 days, here also Indian banks are well endowed as liquidity requirements of Basel III can be comfortably offset from two major sources namely: Cash Reserve Ratio- CRR (4.75%) and Statutory Liquidity Ratio- SLR (24%).

The biggest yet intangible benefit will come in form of hedging against cyclic fluctuation in business market. When the economy is zesty and rollicking, carried away by the booms, banks throw caution to the winds and disburse large amounts of loans thus accumulating unbriddled defaulting risks.During a dowturn as seen in case of housing bubble of US , these contraventions

impede the very fabric of the banking system hurtling it into a spiral of abyss. The creation of additional capital buffers under Basel III would put some shackles on the unfettered bank-lending as sufficient amount of capital has to be preserved now. This restrain will smoothen the large swings when the business cycles go berserk thus acting as a shield.

There is a famous quote: “Whatever was on the left-hand side (liabilities) was not right and whatever was on the right-hand side (assets) was not left.” This comment came in the context of Lehman Brothers who foundered so shoddily that their assets were not even worth a fraction of their book value and their entire capital base was worn out. It simply exposed the decay that had crept into the financial machinery as a result of loose lending, subprime mortgages, shadow financial institutions, speculations, large NPAs and insufficient liquidity buffers which planted the seeds of the great downturn. In this light, Basel III can prove to be an earnest and triumphant attempt to avoid crises like the late 2000s. Given their secure position in contrast with the tumultuous west, coupled with rising diplomatic and economic clout of India in world map, Indian banks are ever so ready to perk up their banking regulations by embracing Basel III. The famous adage “make hay when the sun shines” is paramount in the case of Indian Banking fraternity. Coup -de- Grace!!

CONCLUSION

JUNE 2012 ISSUE

9

A SIMSREE FINANCE FORUM INITIATIVE

ARTHNEETI JUNE 2012 ISSUE

By Dinesh Agarwal, Alumni SIMSREE The headlines of ‘sharp increase in petrol prices’ have left common people with burning holes in their individual budgets. While from time to time plausible identified reasons have been increase in global benchmark prices, increase in demand for oil, prevailing exchange rates.

A simple price conversion of WTI and NYMEX crude at prevailing foreign exchange rate reveals that we are still not a point higher than what it touched during July 2008. With almost one thousand rupees a barrel below the peak, assuming cost of refining and other things remaining constant, why there is still a need to increase the end retail product price for petrol and diesel. For sure above reasons are an input in determining final prices and are directly relevant, there are other set of reasons which make the entire pricing murky. There are

taxes including 1

globally refining cost has remained more or less stable at 12%-20% of the overall cost at refinery gate. With increasing crude oil prices,the variable cost of refining goes down and increases with lower demand. It is thus linked to the refining capacity utilization which varies directly with demand for output.

excise duty, custom duty, VAT, sales tax; local octroi is also applied in certain parts to these taxes. Even these taxes have remained more or less stable since the last peak.While gross refining margins fluctuatedepending upon crude prices, as per U.S. Energy Information Administration,

Thus in a scenario of higher crude prices on account of higher demand for products, the refining costs should go lower. Also, in a scenario of higher crude prices with supplyside issue, the refining cost would remain stable since it has very low price 1http://www.pib.nic.in/newsite/erelease.aspx?relid=61190

THE CRUDE STORY OF OIL PRICING

0

1000

2000

3000

4000

5000

6000

7000

8000

02-Jan-01 02-Jan-02 02-Jan-03 02-Jan-04 02-Jan-05 02-Jan-06 02-Jan-07 02-Jan-08 02-Jan-09 02-Jan-10 02-Jan-11 02-Jan-12

Rs. P

er B

arre

l

WTI INR Brent INR

Figure1: Calculated using the historical Western Texas Intermediate (WTI) and Europe Brent spot prices

JUNE 2012 ISSUE

10

A SIMSREE FINANCE FORUM INITIATIVE

ARTHNEETI JUNE 2012 ISSUE

elasticity. Moreover, with advanced technology and more complex integrated refining complexes being set-up by various players the cost would lower.

Even if we believe2

One of the best management practices is to determine a problem early and provide a remedy for same if prevention is not possible. Had the fuel prices hike been done moderatelyover a period of time, we would have not felt the kind of jolt we felt now.

prices at refinery gate added with transportation costs and marketing margins require current level of pricing in market, there are other reasons which are never deterministic and can be uncontrollable like subsidy, cost of subsidy etc.

They say prevention is better than cure. As far as the Energy Security of this country is concerned, we have rarely taken a pro-active stand to meet it. Had it not been for brilliant leaders at the helm of private and public enterprises to have a visionary ambition, we would have been in a far worse situation. From acquiring assets in Oil producing countries to creating ventures, policy makers have left no stone unturned in creating roadblocks when these champions were trying their level best to be active participants in possible opportunities globally.

2 Since it requires further research

What it does is the fuel subsidy which is kept on hold for some period, either in form of administered prices or subsidy not being paid out, began to accumulate as arrears. And even as economists we recognize the power of compounding. On part of government, if such arrears are accumulated they balloon to become fiscal deficit first. All such arrears have interest component attached to it. The interest component starts adding to the fiscal deficit and government has to borrow. The cost of borrowing is not just absolute but an incremental one. The higher borrowing by government increases the cost of capital for private investments leading to what is known as ‘crowding-out’.

For sure there are other avenues of borrowing but come with their own attached risks like FCCB conversion issues to default on bought in derivatives contract leading to solvency issues such as those in case of Wockhardt, Ranbaxy and Suzlon. This crowding out of investments is worse for the underlying Oil and Gas sector which is hugely capital intensive and need to upgrade the infrastructure where sweet crude will become increasing difficult to avail. The same has been experienced by IOC, ONGC, HPCL and BPCL recently which have delayed their exploratory, expansion and up-gradation projects citing lack of availability of capital.

Effective Date

01.03. 2007

01.03. 2008

05.06. 2008

27.02.2010

Excise Duty (per litre)

6% plus Rs.13

Rs. 14.35

Rs. 13.35

Rs. 14.35

Customs Duty 7.5% 7.5% 2.5% 7.5%

Sales Tax/VAT 20% 20% 20% 20%

JUNE 2012 ISSUE

11

A SIMSREE FINANCE FORUM INITIATIVE

ARTHNEETI JUNE 2012 ISSUE

Needless to say further, it creates shortage of supply in a local-demand based growing economywhich has remained a perennial factor to our inflationary problem. This inflationary problem forces central bank to raise interest rates which further compounds the problem.

Figure 1 Mis-Economics of Fuel Price Management

Economics further complicates the matter when these shrinkage in demand leads to outflow of investments and capital investments from a growing economy. The outflow cause rupee to depreciate and has greatly affected the current account of trade. The current account deficit which is at 4.1% of GDP has led to a BBB- sovereign rating from S&P with a negative outlook on it. In purely economic terms, it means higher cost of borrowing and just one notch above investment grade classification for India. Any downgrade below these can have a mass exodus of investments.Thus it is not just the pricing of fuel, but the gross mismanagementof these indirect costswhich has aggravated the problem at economy wide level.

Going forward, as global economy would recover and we grow the fuel prices would increase. It is important that the Governmentand Oil Marketing companies bring more transparency to crude way of pricing these end products of black gold.

Figure2: Mis-Economics of Fuel Price Management

One of the best management

practices is to determine a

problem early and provide a

remedy for same if prevention is

not possible. Had the fuel prices

hike been done moderately over

period of time, we would have not

felt the kind of jolt we felt now.

What it does is the fuel subsidy

which is kept on hold for some

period, either in form of

administered prices or subsidy not

being paid out, began to

accumulate as arrears.

JUNE 2012 ISSUE

12

A SIMSREE FINANCE FORUM INITIATIVE

ARTHNEETI JUNE 2012 ISSUE

By SIMSREE Finance Forum

Direct Taxes Code, 2010 was tabled in the Parliament on 30 August, 2010. This code will replace the present Income Tax Act 1961. However on 7th May 2012, Finance Minister Mr.Pranab Mukherjee announced the deferment of GAAR by one year and this announcement led to a U-Turn in last hour of trade on Sensex and Nifty on that day. In this article we present the analysis of GAAR, itsimplications and recommendations.Chapter 24 of Direct Tax Code defines the need of GAAR.

Need for general anti-avoidance rule (GAAR) 24.1 Tax avoidance, like tax evasion, seriously undermines the achievements of the public finance objective of collecting revenues in an efficient, equitable and effective manner. Sectors that provide a greater opportunity for tax avoidance tend to cause distortions in the allocation of resources. Since the better-off sections are more endowed to resort to such practices, tax avoidance also leads to cross-subsidization of the rich. Therefore, there is a strong general presumption in the literature on tax policy that all tax avoidance, like tax evasion, is economically undesirable and inequitable. On considerations of economic efficiency and fiscal justice, a taxpayer should not be allowed to use legal constructions or transactions to violate horizontal equity. 24.2In the past, the response to tax avoidance has been the introduction of legislative amendments to deal with specific instances of tax avoidance. Since the liberalization of the

Indian economy, increasingly sophisticated forms of tax avoidance are being adopted by the taxpayers and their advisers. The problem has been further compounded by tax avoidance arrangements spanning across several tax jurisdictions. This has led to severe erosion of the tax base. Further, appellate authorities and courts have been placing a heavy onus on the revenue when dealing with matters of tax avoidance even though the relevant facts are in the exclusive knowledge of the taxpayer and he chooses not to reveal them. 24.3 In view of the above, it is necessary and desirable to introduce a general anti-avoidance rule which will serve as a deterrent against such practices. This is also consistent with the international trend. Under GAAR any arrangement is considered impermissible if its main purpose is to obtain tax benefit and it: • Creates rights or obligations which would

not be created if the transaction was implemented at arm’s length; or

• Results, directly or indirectly, in the misuse of the provisions of the Code; or

• Lacks commercial substance in whole or in part; or

• Is entered into or carried out by means or manner which would not be normally adopted for bonafide purposes

Under this rule, the Commissioner of Income-tax has been given the power to declare any

GAAR AND ITS IMPLICATIONS

JUNE 2012 ISSUE

13

A SIMSREE FINANCE FORUM INITIATIVE

ARTHNEETI JUNE 2012 ISSUE

arrangement impermissible if the main purpose of the arrangement was to get ‘tax benefit’ and there is no commercial substance in the arrangement.Secondly it will also override all the treaties India has entered into.There are two definitions that need to be specified here: • Tax avoidance • Tax evasion Tax avoidance is an arrangement of a tax payer’s affairs that is intended to reduce his liability and that although the arrangement could be strictly legal it is usually in contradiction with the intent of the law it purports to follow. Tax evasion is generally used to mean illegal arrangements where liability to tax is hidden or ignored i.e. the tax payer pays less tax than he is legally obligated to pay by hiding income or information from tax authorities. It should be noted that sometimes it is very difficult to draw a line between tax avoidance and evasion. GAAR is meant for tackling tax avoidance. It cannot deal with tax evasion since it cannot tackle what is not reported. The scope of GAAR is very wide and very vaguely defined. It covers all the arrangement which has an element of tax benefit in it and it will bring about long term retrospective tax litigation. This may create uncertainty in terms of tax implications of any kind of arrangement. So, it is very important that people working on all levels of policy making consider all the avenues before decision making. The tax implications of such decisions will play a very vital role. The negative implications can be seen in decrease in FIIs in the April-June 2012 quarter which saw a pull out of Rs 1957 Cr from equities.For this very reason Government issued a 21 point draft guidelines on GAAR on June 28 2012. Major points covered in it were:

• The rules would not apply retrospectively and would apply only to income accruing from April 1, 2013

• An income threshold has also been suggested for invoking the GAAR

This now has to be followed by different stakeholders before preparing the final draft. The task of tax collection is the responsibility of Commissioner of Income-tax and under him are assessing officers who are responsible for achieving tax collection targets given to them by the government. This again makes the tax collection very subjective and there is a possibility of tax collection or settlement in unfair manner. Once the provisions of the GAAR are invoked in respect of any arrangement, the CIT has been given wide powers to counteract the consequent tax advantages and to determine the tax consequences either by ignoring the arrangement in question or in any other manner as per the discretion of CIT. The powers awarded to Commissioner of Income Tax are: • Commissioner now gets to decide the

type and nature of transaction and to ascertain the purpose behind the transaction

• Along with misuse of power, it also brings in uncertainty in the system which the foreign investors may not like

• Also the vague definition by GAAR brings in subjectivity where the investors, other professionals and tax authorities may infer something else. The main aim of GAAR mentioned in the DTC code is ‘to remove uncertainties. However, this further adds to the confusion

JUNE 2012 ISSUE

14

A SIMSREE FINANCE FORUM INITIATIVE

ARTHNEETI JUNE 2012 ISSUE

• It also does not provide any separate

appeal mechanism for tax payers for invoking GAAR. This increases the concern of more litigations and hardship for tax payers.

Implication of GAAR on Foreign Investment

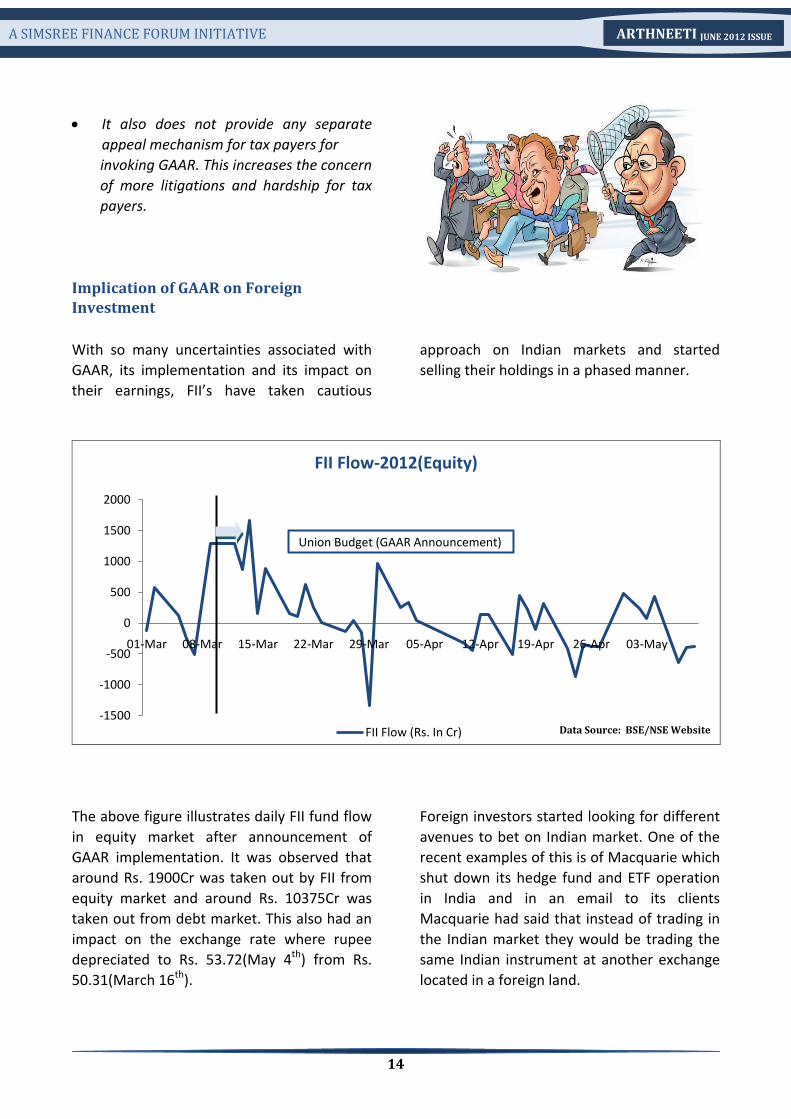

With so many uncertainties associated with GAAR, its implementation and its impact on their earnings, FII’s have taken cautious

approach on Indian markets and started selling their holdings in a phased manner.

The above figure illustrates daily FII fund flow in equity market after announcement of GAAR implementation. It was observed that around Rs. 1900Cr was taken out by FII from equity market and around Rs. 10375Cr was taken out from debt market. This also had an impact on the exchange rate where rupee depreciated to Rs. 53.72(May 4th) from Rs. 50.31(March 16th).

Foreign investors started looking for different avenues to bet on Indian market. One of the recent examples of this is of Macquarie which shut down its hedge fund and ETF operation in India and in an email to its clients Macquarie had said that instead of trading in the Indian market they would be trading the same Indian instrument at another exchange located in a foreign land.

-1500

-1000

-500

0

500

1000

1500

2000

01-Mar 08-Mar 15-Mar 22-Mar 29-Mar 05-Apr 12-Apr 19-Apr 26-Apr 03-May

FII Flow-2012(Equity)

FII Flow (Rs. In Cr)

Union Budget (GAAR Announcement)

Data Source: BSE/NSE Website

JUNE 2012 ISSUE

15

A SIMSREE FINANCE FORUM INITIATIVE

ARTHNEETI JUNE 2012 ISSUE

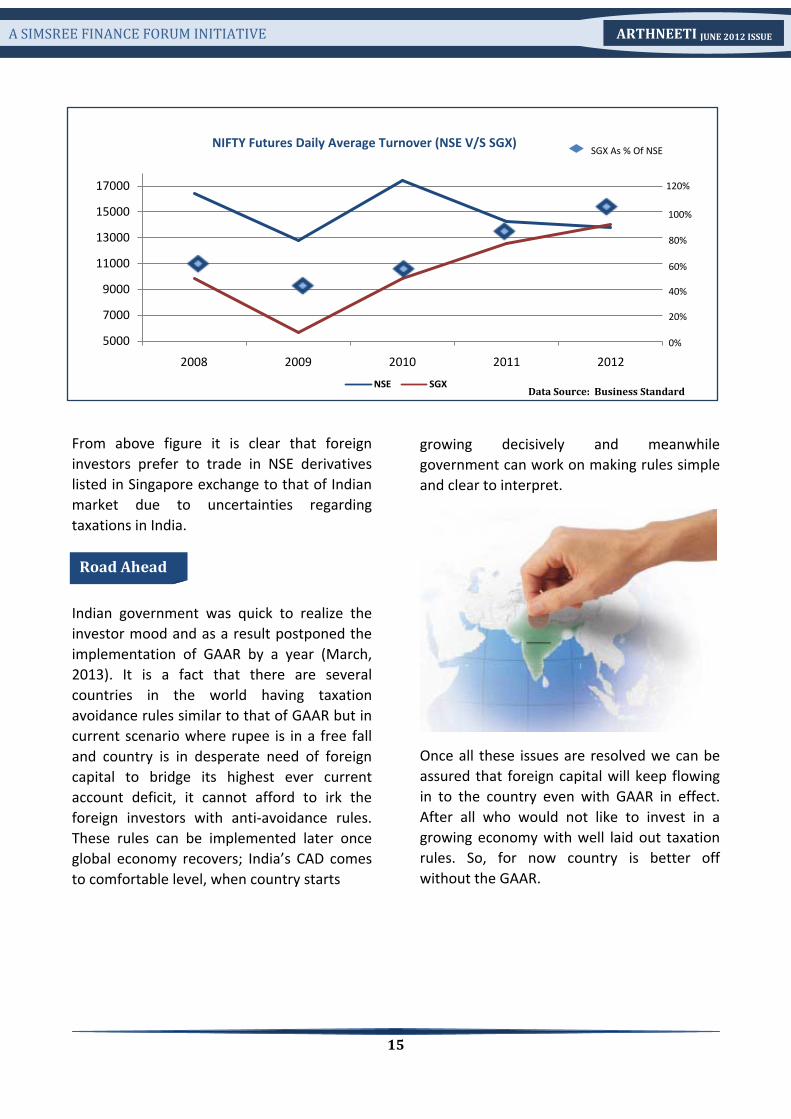

From above figure it is clear that foreign investors prefer to trade in NSE derivatives listed in Singapore exchange to that of Indian market due to uncertainties regarding taxations in India.

Indian government was quick to realize the investor mood and as a result postponed the implementation of GAAR by a year (March, 2013). It is a fact that there are several countries in the world having taxation avoidance rules similar to that of GAAR but in current scenario where rupee is in a free fall and country is in desperate need of foreign capital to bridge its highest ever current account deficit, it cannot afford to irk the foreign investors with anti-avoidance rules. These rules can be implemented later once global economy recovers; India’s CAD comes to comfortable level, when country starts

growing decisively and meanwhile government can work on making rules simple and clear to interpret.

Once all these issues are resolved we can be assured that foreign capital will keep flowing in to the country even with GAAR in effect. After all who would not like to invest in a growing economy with well laid out taxation rules. So, for now country is better off without the GAAR.

Road Ahead

5000

7000

9000

11000

13000

15000

17000

2008 2009 2010 2011 2012

NSE SGX

120%

100%

80%

60%

40%

20%

0%

NIFTY Futures Daily Average Turnover (NSE V/S SGX)SGX As % Of NSE

Data Source: Business Standard

JUNE 2012 ISSUE

16

A SIMSREE FINANCE FORUM INITIATIVE

ARTHNEETI JUNE 2012 ISSUE

SIMSREE Sydenham Institute of Management Studies Research & Entrepreneurship Education (SIMSREE) was founded in the year 1983 by Government of Maharashtra. Since then, SIMSREE has been continuously ranked as one of the Premier Institutes of our country, and it attracts the finest management minds from India. SIMSREE has been consistently ranked among Top 20 Business Schools in India. CRISIL has recently rated SIMSREE with A*** at state level (Maharashtra) and A** at National level. SIMSREE Finance Forum SFF is a student body that strives to assist the students in the development of financial acumen through collective effort. The Forum aims to bridge the gap between students and corporate leaders through various Interactive Sessions on a regular basis. Various Programs & Events form part of our Forums initiatives to provide the students with a multitude of opportunities.

SIMSREE

B Road, Churchgate Mumbai 400 020, India

[email protected] Blog:http://simsreefinanceforum.blogspot.in/

![Volume 2 Edition 6 2013 - buzzsimsree.files.wordpress.com · Volume 2 Edition 6 2013 Initiated by- BUZZ, Marketing Club Sydenham Institute of Management [SIMSREE]](https://static.documents.pub/doc/80x56/601afaa9c2599f5f5b1a2574/volume-2-edition-6-2013-volume-2-edition-6-2013-initiated-by-buzz-marketing.jpg)