18

The State of Iowa: Economy and Budget Update By Randy Bauer Budget Director State of Iowa

The State of Iowa: Economy and Budget Update

By Randy BauerBudget Director

State of Iowa

Economic pressures continue for all states

• Reduced State Revenues• Corporate Tax Receipts• Personal Tax Receipts• Sales Tax Receipts• Inheritance/Estate Tax Receipts

• Reduced State Revenues• Corporate Tax Receipts• Personal Tax Receipts• Sales Tax Receipts• Inheritance/Estate Tax Receipts

• Higher Expenditures• Medicaid Costs• Homeland Security• Education• Corrections• Employee Salaries• Employee Healthcare

Costs

• Higher Expenditures• Medicaid Costs• Homeland Security• Education• Corrections• Employee Salaries• Employee Healthcare

Costs

StateBudget

States face difficult budgetary choices

• Increase Revenues

• Reduce Expenditures

• Use Reserves

Tax Revenue Decline Much Worse Than Economy Might Suggest

State Tax Rev enue Has Fallen Far More Sharply Relativ e to Ec onomyThan in 1980-82 and 1990-91 Rec es s ions

1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002

State F is cal Y ear

Sources : U .S. Bureau of Ec onom ic Analy s is , U .S. Bureau of the C ens us , Signif ic ant Features of Fis cal Federalism -1984 (AC IR ), Fis c al Survey of the States (N GA), R oc kef eller Ins t itute of Gov ernm ent

-8

-6

-4

-2

0

2

4

6

% C

hang

e

R eal GD P per capita, c alendar y ear in whic h f is c al y ear began R eal s tate tax rev enue per capita, adjus ted f or legis lat ion

-7.4

-2.0

-3.0-3.5

-1.8

-0.7

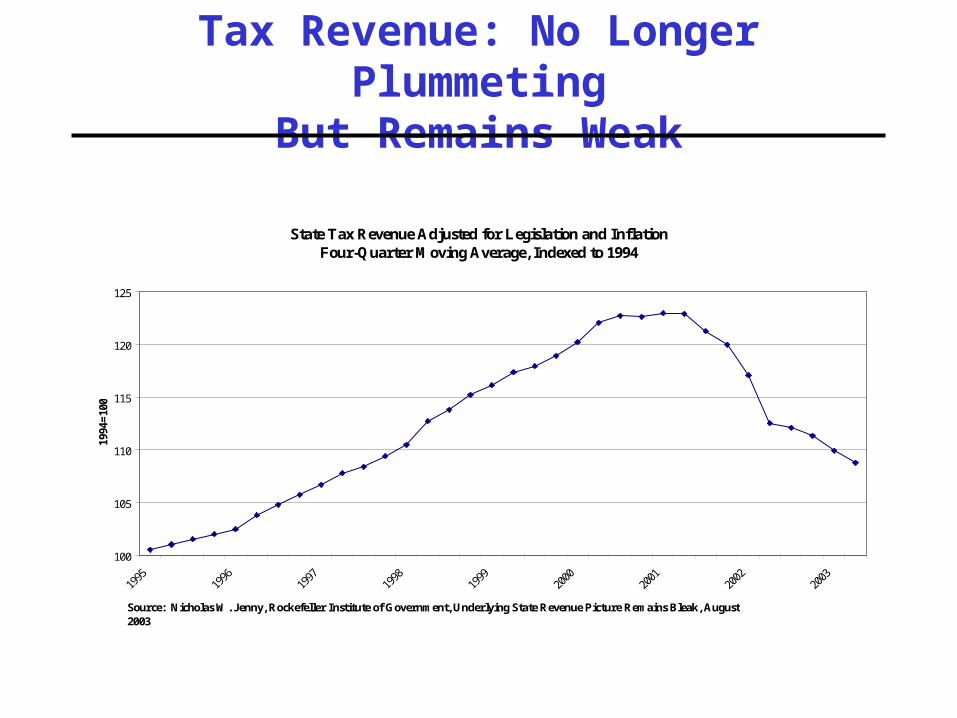

Tax Revenue: No Longer PlummetingBut Remains Weak

State Tax Revenue Adjusted for Legislation and InflationFour-Quarter Moving Average, Indexed to 1994

100

105

110

115

120

125

Source: Nicholas W. Jenny, Rockefeller Institute of Government, Underlying State Revenue Picture Remains Bleak, August 2003

1994

=10

0

Iowa – worst revenue “growth” in 50 years

State Balances are Declining

Source: National Association of State Budget Officers

Source: National Association of State Budget Officers

Only 10 States Have Adequate Balances

States Borrowing Record Amounts

• $224 billion during FY 2003

• Double the amount of two years ago

• “Follow the federal leader” tactics?

• Stall tactic?

• Even this market has limits

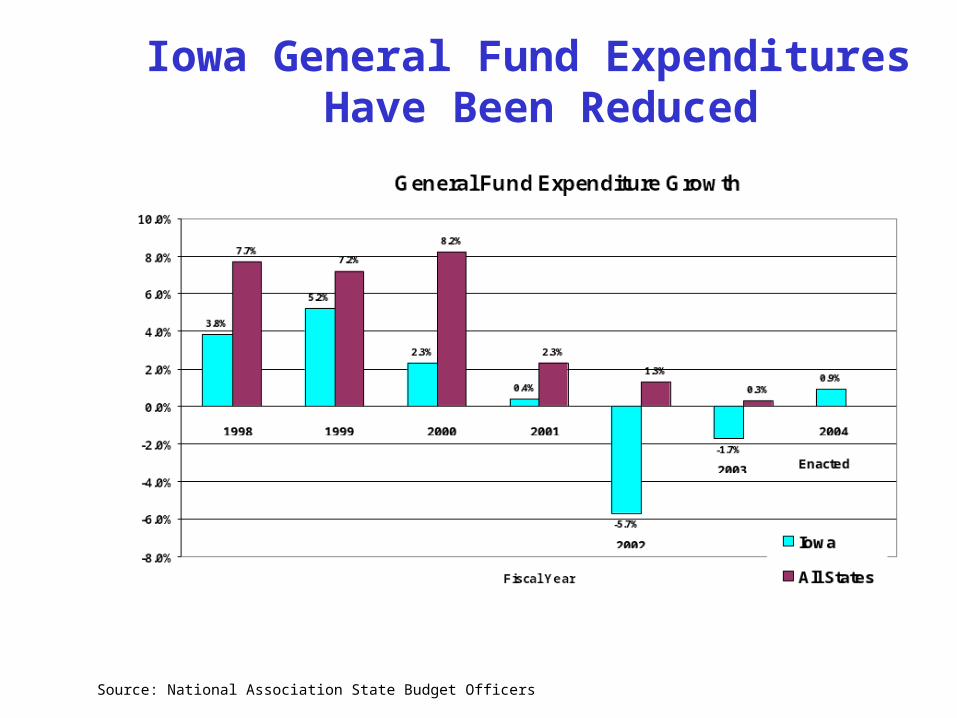

Iowa General Fund Expenditures Have Been Reduced

Source: National Association State Budget Officers

Over 60 percent of the State’s General Fund budget goes toward education

FY2003 General Fund Expenditures

Economic Development,

Ag, Other4%

Property Tax Relief

8%Safe Communities

10%

K-12 Education46%

Higher Education

15%

Health and Family Services

17%

Source: Iowa Department of Management

• Fund balances: drawn down from more than 10% of expenditures in FY 2001 to 1.3% of expenditures at end of FY 2003; 16 states now have balances of <1%

• Special funds: At least 23 states tapped capital, highway, other funds for FY 2003, and 29 for FY 2004; at least 16 have used tobacco settlement money

• Spending cuts: 31 states cut for FY 2004 in some fashion; Medicaid cost containment planned in many states (but how real?)

• Tax increases:– FY 2003: >= 1% in 16+ states, for $6.7 billion, 40% of $ was

cigarette taxes; a few large or broad-based tax increases – KS, IN, MA, NJ, TN – but these were exceptions, not the rule

– FY 2004: more income and sales tax increases, $6.9 billion tax increase in total (see next page)

Source: Donald Boyd, Director, Rockefeller Institute of Government, SUNY

State Responses So Far

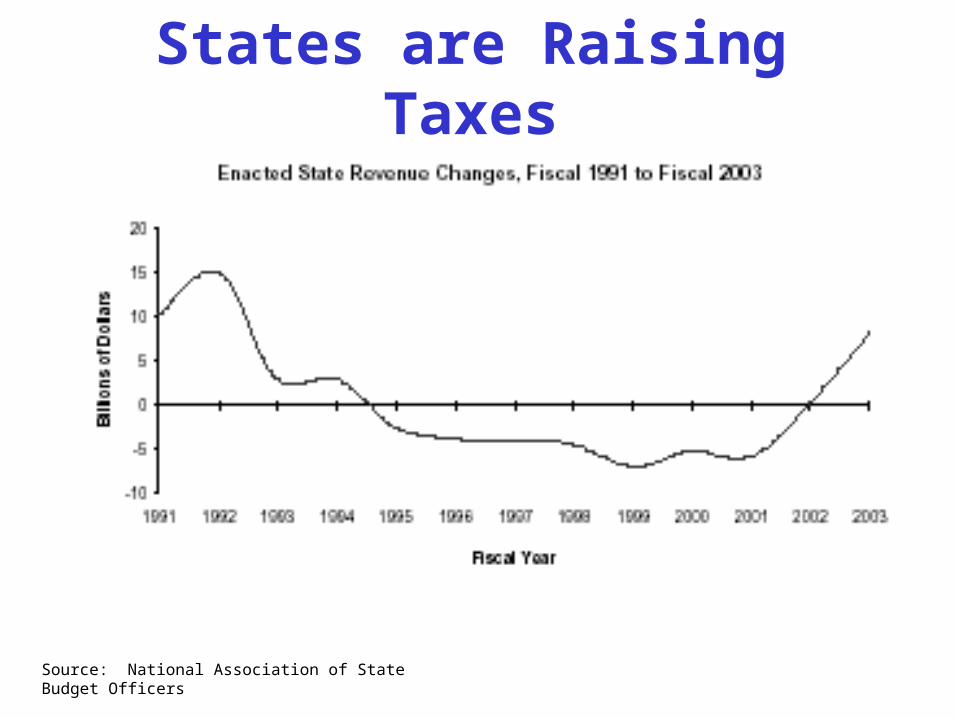

States are Raising Taxes

Source: National Association of State Budget Officers

0.10

0.11

0.12

0.13

0.14

0.15

0.16

1970 1975 1980 1985 1990 1995 2000 2005 2010

The Tax Burden: Rising Expectations?

(Ratio of personal taxes to personal income)

Source: Global Insight

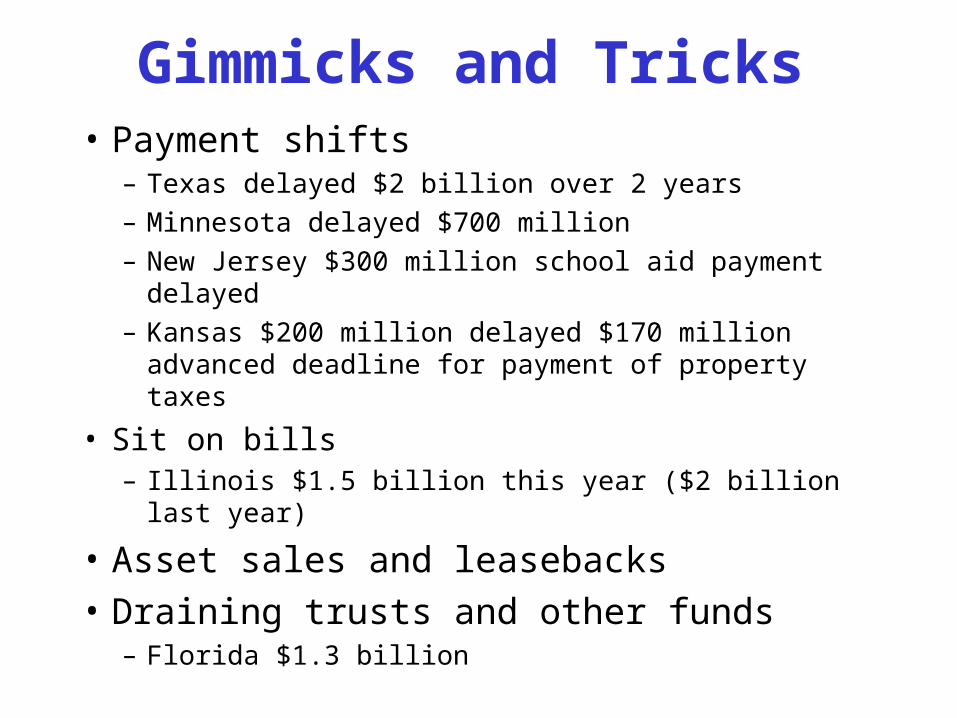

Gimmicks and Tricks• Payment shifts

– Texas delayed $2 billion over 2 years

– Minnesota delayed $700 million

– New Jersey $300 million school aid payment delayed

– Kansas $200 million delayed $170 million advanced deadline for payment of property taxes

• Sit on bills– Illinois $1.5 billion this year ($2 billion last year)

• Asset sales and leasebacks

• Draining trusts and other funds – Florida $1.3 billion

When Will Finances Of State Governments Recover?

• Economy currently at least as weak as state government forecasters expected

• Additional near-term risks for income taxes, related to financial markets

• Will be many years before markets, and associated income, recover to 2000 and 2001 levels

• Continued erosion of states’ sales taxes• Medicaid and K-12 education spending pressures• Many states solved 2003-04 problems in ways that make

2004-05 and 2005-06 much worse

Good times for most states probably at least 2-3 years away

Moody’s Outlook for StatesContinues to be Negative

• 16 states currently on negative outlook.

• More negative outlooks and rating actions likely.

• Oregon downgrade in March was 8th for states since last state upgrade in 2/01 (Connecticut).

• 4 states now on Watchlist for downgrade (Conn., Minn., Mich., Ill.)

All States:Structural Balance Will Be Elusive

• Spending is on a higher growth plane and is outstripping revenue growth.

• Budget problems will persist into FY05:– FY04 have large budget gaps due to

substantial use on non-recurring resources to balance FY03.

• Pace of economic recovery will be key, but modest recovery

forecasts will leave a difficult FY04 and FY05.• Higher rated credits will restore structural balance and

rebuild reserve funds quickly.• Further credit deterioration among states is likely. • Problems beginning to be pushed down to local governments.