62

TOP TRENDS for 2012

| Date post: | 25-Dec-2015 |

| Category: |

Documents |

| Upload: | gordon-harrell |

| View: | 215 times |

| Download: | 1 times |

TOP TRENDS for 2012

©2011 Lifetime Brands, Inc.

TOP TRENDS for 2012Expert Panel

Susan YashinskyMacro Trend Forecaster & Innovation PredictorSphere Trending

Michelle LambCo-founder and Chairman; Editorial DirectorThe Trend Curve

Robin K. AlbingPresident/CEOAlbing International Marketing, LLC

TOP TRENDS for 2012

TOP TRENDS for 2012

10 New Rules for theChanging Economy6

Reinventing Customer Relationships5

The Multi-Faceted Meaning of Value4

America’s Culinary Rebirth3

The Multi-Generational Home1

The Rise of Anti-Consumerism2

THE MULTI-GENERATIONAL HOME

THE MULTI-GENERATIONAL HOME

1

THE MULTI-GENERATIONAL HOME1© 2011 GLOBAL TREND & DESIGN

Four distinct generations in the workplace, home and marketplace

Consumers taking cues from each other: Gen Y teaches the older generations about technology while Baby Boomers influence younger consumers on experiential activities (yoga, traveling, etc.)

BABY BOOMERSAge 46-6580 Million

ACTIVE SENIORSAge 66+

47 Million

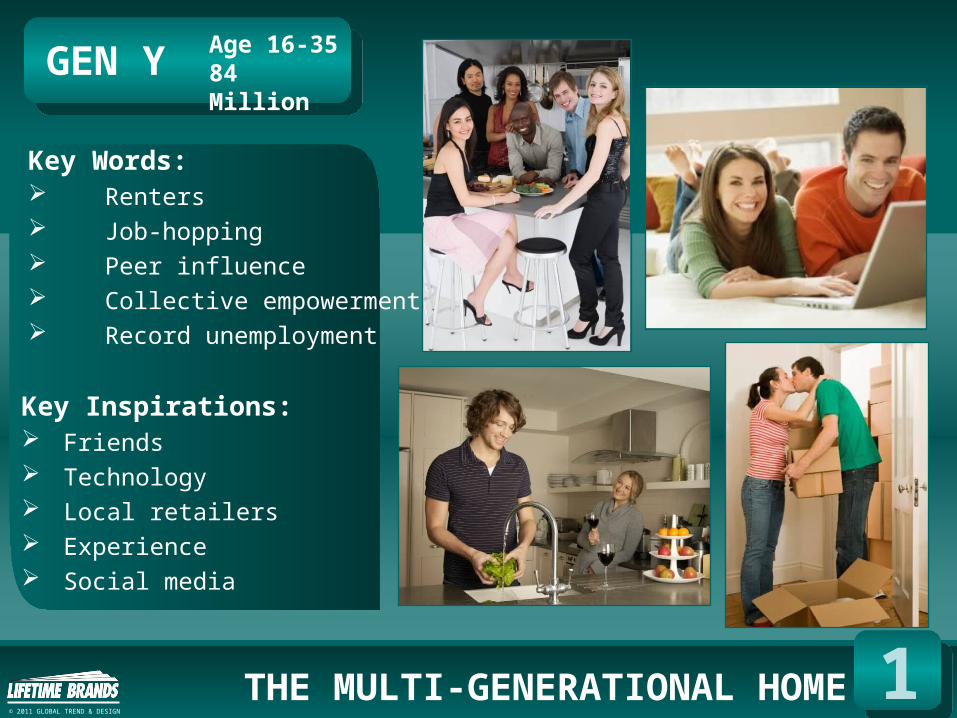

GEN YAge 16-3584 Million

GEN XAge 36-4543 Million

THE MULTI-GENERATIONAL HOME1© 2011 GLOBAL TREND & DESIGN

GEN Y Age 16-3584 Million

Key Inspirations: Friends Technology Local retailers Experience Social media

Key Words: Renters Job-hopping Peer influence Collective empowerment Record unemployment

THE MULTI-GENERATIONAL HOME1© 2011 GLOBAL TREND & DESIGN

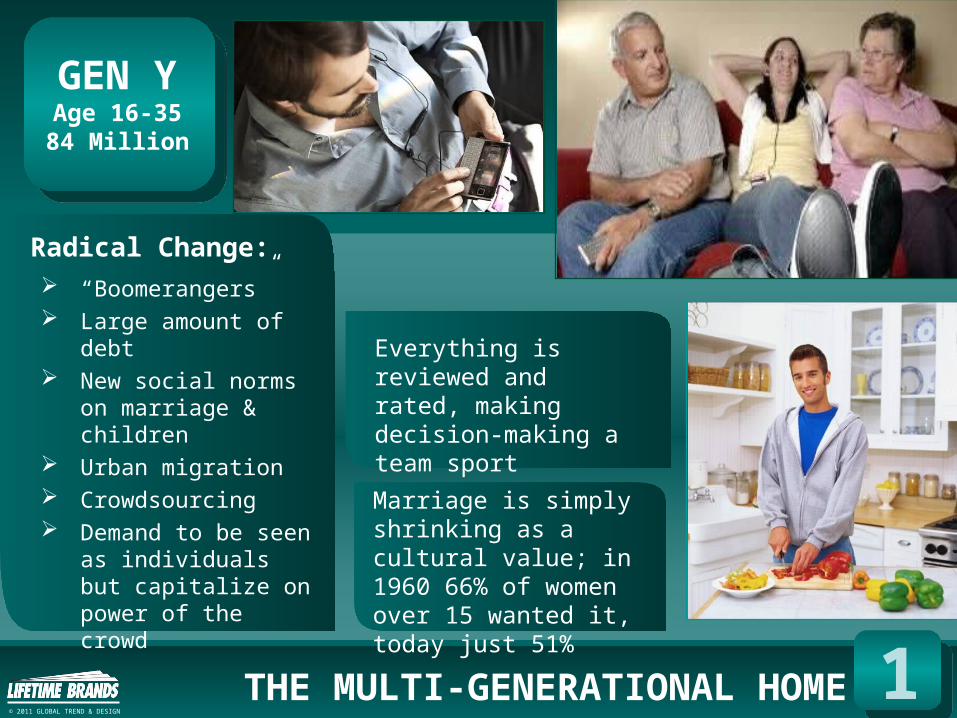

GEN YAge 16-3584 Million

Marriage is simply shrinking as a cultural value; in 1960 66% of women over 15 wanted it, today just 51%

“Boomerangers” Large amount of

debt New social norms

on marriage & children

Urban migration Crowdsourcing Demand to be seen

as individuals but capitalize on power of the crowd

Everything is reviewed and rated, making decision-making a team sport

Radical Change:

THE MULTI-GENERATIONAL HOME1© 2011 GLOBAL TREND & DESIGN

Key Words: Family Overwhelmed/ Underwater Community Entering peak

earning years

Key Inspirations: Gen Y Work / life balance Healthy living Children

GEN X Age 36-4543 Million

THE MULTI-GENERATIONAL HOME1© 2011 GLOBAL TREND & DESIGN

GEN XAge 36-4543 Million

The majority of moms (65%) utilize 5 or more forms of technology every day to stay connected

40% more households grew their own food last year than two years ago (NGA)

Radical Change: Stuck in starter homes Trading down to trade up Children’s health Hit hardest by recession Starting work later

means diminished incomes

Less ability to save Home ownership down

6% in 6 years (35-39 year olds, US Census)

THE MULTI-GENERATIONAL HOME1© 2011 GLOBAL TREND & DESIGN

THE MULTI-GENERATIONAL HOME1

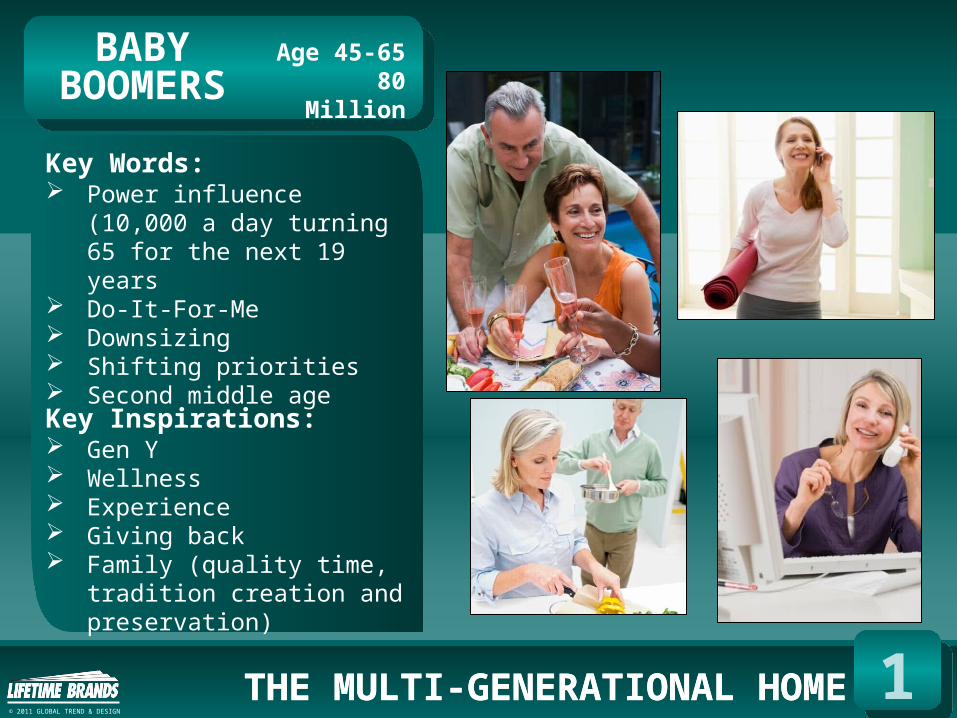

Key Words: Power influence (10,000 a

day turning 65 for the next 19 years

Do-It-For-Me Downsizing Shifting priorities Second middle age

Key Inspirations: Gen Y Wellness Experience Giving back Family (quality time,

tradition creation and preservation)

BABYBOOMERS

Age 45-6580 Million

THE MULTI-GENERATIONAL HOME1© 2011 GLOBAL TREND & DESIGN

THE MULTI-GENERATIONAL HOME1

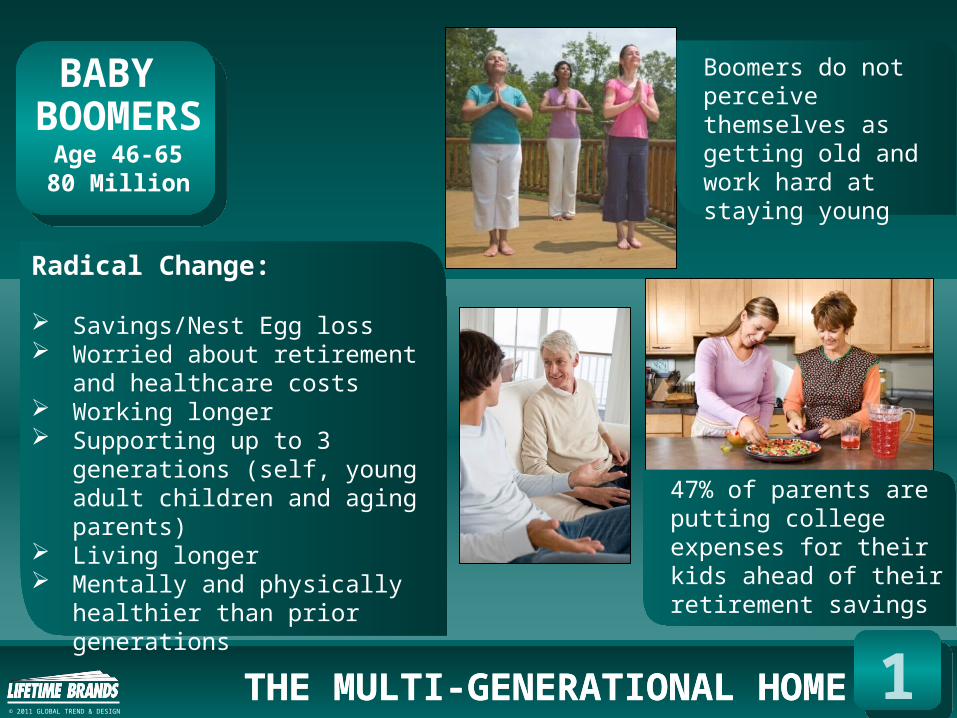

BABY BOOMERS

Age 46-6580 Million

Boomers do not perceive themselves as getting old and work hard at staying young

Radical Change:

Savings/Nest Egg loss Worried about retirement and

healthcare costs Working longer Supporting up to 3

generations (self, young adult children and aging parents)

Living longer Mentally and physically

healthier than prior generations

47% of parents are putting college expenses for their kids ahead of their retirement savings

THE MULTI-GENERATIONAL HOME1© 2011 GLOBAL TREND & DESIGN

Gen Y (ages 16-34) Globally-aware Willing to try new

things Design critical Love exotic flavors New homeowner Durability

important as an upgrade opportunity

Save me money, time and energy

Save the planet

Gen X (ages 35-44)

Rising concern about family wellness

Looking for solutions re: eating healthy

Community connections—reaching this consumer in new ways through local networks (such as Mommy blogs, Yelp, etc.)

Baby Boomers (ages 45-65)

Entering an experiential life stage

Disposable income moving to purchases that deliver experiences

New appreciation for the value of quality/family time

Know your

Customer

THE MULTI-GENERATIONAL HOME 1

PANEL DISCUSSION

THE RISE OF ANTI-CONSUMERISM

THE RISE OF ANTI-CONSUMERISM

2

THE RISE OF ANTI-CONSUMERISM2© 2011 GLOBAL TREND & DESIGN

WhatDoes It

Mean?

Anti-consumerism: refers to the socio-political movement against the equating of personal happiness with consumption and the purchase of material possessions. (Wikipedia)

Anti-consumerists believe commodities only supply short-term gratification, and detract from a sustainably happy society.

GOALS:1. To increase the overall happiness and fulfillment of the

human race by encouraging simplicity

2. To save the planet from a global environmental collapse fueled by spreading hyper-consumption

THE RISE OF ANTI-CONSUMERISM2© 2011 GLOBAL TREND & DESIGN

“ I will not

overpay for

this!”

REALITY: Groupon-like sites are reimagining the coupon as a tool for dragging prices to unprecedented lows—not just a few bucks off a single product but 50 % off or moreOPPORTUNITY: While margins are compromised, consider this massive exposure for your brand and inventory leveling opportunities

“Look how much I saved!” has replaced “Look at what I bought!”

THE RISE OF ANTI-CONSUMERISM2© 2011 GLOBAL TREND & DESIGN

“Will I really use

this?”

REALITY: “The new mantra is ‘right-sized’ home amenities… Say goodbye to the industrial-grade kitchen range and the spa tub that the owners never fire up because they don’t want to clean it.” (Builder Magazine)

1 in 2 Americans will have a Smartphone by 2012, as compared to 1 in 10 in 2008 (Nielsen)

Consumer savings rate is now close to 6%, a big shift from the negative savings pre-recession

New ‘necessities’ also affect discretionary income

OPPORTUNITY: Reinventing the basics — Everyday use translates to everyday need

THE RISE OF ANTI-CONSUMERISM2© 2011 GLOBAL TREND & DESIGN

“We just don’t

have the room for

this.”

REALITIES: 57% of the 30.3 million housing units added from

2005 to 2020 will be rentals (Joint Center for Housing Studies)

Average new home size dropped 51 square feet in 2009 (Nat’l Assn. of Home Builders)

New storage needs: Cookbooks Coupons Grocery lists Medications Pet supplies Kids toys, etc.

OPPORTUNITY: Create smaller profile and smaller space solutions — the downsized home has to live larger

THE RISE OF ANTI-CONSUMERISM2© 2011 GLOBAL TREND & DESIGN

Laws ofAttractio

n

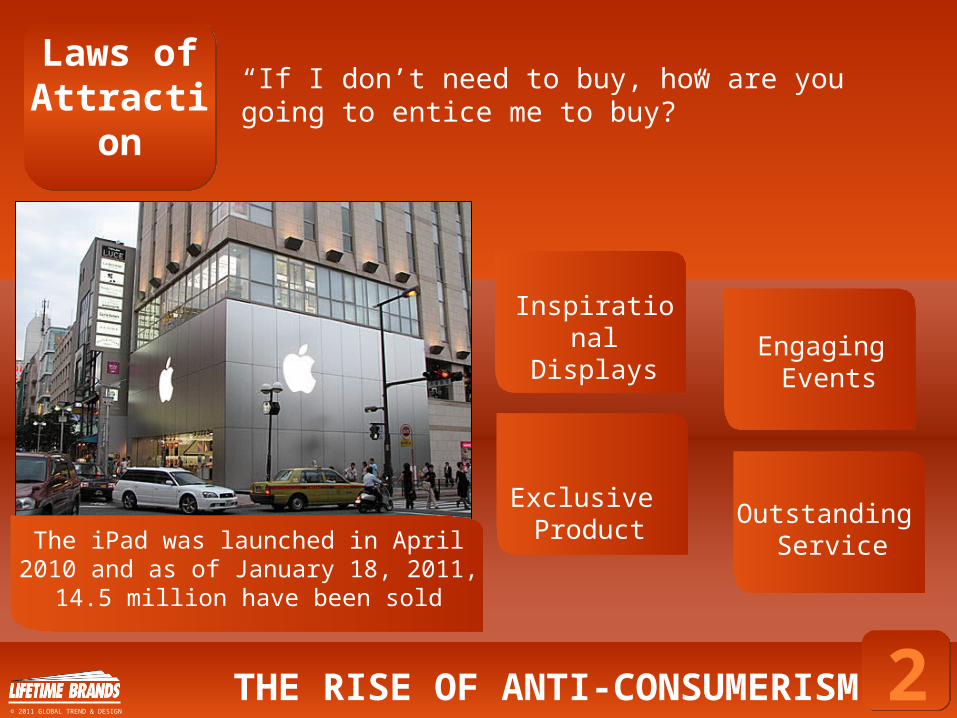

“If I don’t need to buy, how are you going to entice me to buy?”

The iPad was launched in April 2010 and as of January 18, 2011, 14.5

million have been sold

InspirationalDisplays

Exclusive Product

Outstanding Service

Engaging Events

THE RISE OF ANTI-CONSUMERISM2© 2011 GLOBAL TREND & DESIGN

Inspire Your

Consumer

People are learning to live within their means yet this doesn’t mean we have stopped being a consuming society

Understand that a new generation of coupons & discounts are enabling consumers—how do you play in this opportunity?

You’re competing for market share growth as the discretionary pie shrinks— know your competition’s strengths and weaknesses!

The kitchen continues to be the hub of the home and is taking on even more responsibilities; make sure your assortments are meeting these new demands

PANEL DISCUSSION

THE RISE OF ANTI-CONSUMERISM 2

AMERICA’S CULINARY REBIRTH

AMERICA’S CULINARY REBIRTH

3

AMERICA’S CULINARY REBIRTH 3© 2011 GLOBAL TREND & DESIGN

CulturalInfluence

s

AMERICA’S CULINARY REBIRTH 3© 2011 GLOBAL TREND & DESIGN

Hub of the

Home

OPPORTUNITY: Multi-function and decorative value have never been more needed/important in this new kitchen environment

Besides cooking meals, the most common activities taking place in the kitchen are: 65% eating meals 62% planning meals 49% taking medications or

vitamins 46% talking in-person with

family & friends 43% talking on the phone 38% caring for pets 11% using computers (up from

6% in 2006)Research Institute for Cooking and Kitchen Intelligence

Male consumers now make up a $51 billion shopping industry

NPD Group

REALITY: Kitchens will continue to combine eating and

meeting spaces Bring dining, cooking, meeting, and recreation all

together in one large, open space

AMERICA’S CULINARY REBIRTH 3© 2011 GLOBAL TREND & DESIGN

StressBuster

REALITY: 79% of adults say they enjoy cooking 30% say they love it 49% say they enjoy it when they have the time (Harris Poll)

Increasingly cooking is seen as a stress reliever and a creative hobby

OPPORTUNITY: Entertaining opportunities from tasting parties to cocktails... New growth in DIY entertaining and even DIY weddings

In a survey conducted by the American

Institute of Psychologists, about

75%-90% of all visits to general physicians are

for stress-related problems

AMERICA’S CULINARY REBIRTH 3© 2011 GLOBAL TREND & DESIGN

New World

Influence

sOPPORTUNITY: Bring new culinary experiences to the mass—Williams-Sonoma has, from frittatas to stuffed pancakes (“ebelskiver”) and sous-vide cooking; all of which incidentally require new cooking appliances, prep tools, recipe books, etc.

Salsa now outsells ketchup and tortillas outsell white bread

Asian food market in the U.S. is growing 11%

Indian food market in the U.S. is growing 35%

Hispanics will account for 17% of the U.S. population by 2015, up from 14% in 2005

WILLIAMS-SONOMA

REALITY: Mass media such as television and the internet has made the American palette more sophisticated, adventurous and diverse

AMERICA’S CULINARY REBIRTH 3© 2011 GLOBAL TREND & DESIGN

Entice Your

Consumer

Address the new social aspects of cooking and baking Cooking as leisure/entertainment Cocktails, casual dinner parties, BBQ, potlucks

Consumers are looking to be creative Update traditional favorites Bring the experience and flavor of “Global Cuisine” Bring more restaurant experiences into the home

Save them more than just money Save them Time Save them Space Save them Effort

AMERICA’S CULINARY REBIRTH3

PANEL DISCUSSION

THE MULTI-FACETED MEANING OF VALUETHE MULTI-FACETED MEANING OF VALUE

4

MULTI-FACETED MEANING OF VALUE4© 2011 GLOBAL TREND & DESIGN

Value Equation

is Reweighted

Today’s marketplace that is oversaturated with brands, models and even points of purchase—no wonder their consumer expectations are so high

REALITY: The consumer has moved from ‘value = price + quality’ to a multi-dimensional equation covering a wide variety of variables

MULTI-FACETED MEANING OF VALUE4© 2011 GLOBAL TREND & DESIGN

Value of Individuality

REALITY: 27% of all households (31 million) are one-person

households Married couples are now a slight minority (49.7%)

OPPORTUNITY: Find ways to let the customer participate. Enable customization.

A market of one: with only one syrup the Starbucks latte framework offers almost 200 million variations

AD AGE AMERICAN DEMOGRPHICS

The value of the consumer as an individual increases as the mass market disappears

The value of the consumer as an individual increases as the mass market disappears

MULTI-FACETED MEANING OF VALUE4© 2011 GLOBAL TREND & DESIGN

Quality Is OnceAgain Important

OPPORTUNITY: Be best-in-class for quality. In times of recession and recovery, quality & durability to rise in importance within the value equation

The Good News: There is a lot of pent-up purchase demand from consumers who have not spent in several years

Consumers are staying in their homes longer 2-3 years pre-recession Expected average of 10+ years post-recession

REALITY: 73% of consumers say they'd rather have fewer, high quality things (Ogilvy)

MULTI-FACETED MEANING OF VALUE4© 2011 GLOBAL TREND & DESIGN

Value in theDesign/Function

Relationship

OPPORTUNITY: Embrace style as a selling point from OPP

to high end Use color and form as competitive

differentiators

The separation between function and style is vanishing as aesthetic value becomes a standard

REALITY: Decorative value weighs equally with function as the element of design rises in importance

KIZMOS

FARBERWARESABATIERMISTO

MULTI-FACETED MEANING OF VALUE4© 2011 GLOBAL TREND & DESIGN

Multi-function as a Value Multiplier

OPPORTUNITY: Multi-function adds value on all of these fronts; it means that the consumer has to buy less products, thus storing less, saving money and often even prep/clean-up time

FARBERWARE

KITCHENAID

KITCHENAID

REALITY: Regardless of consumer segmentation, the top three new value multipliers are Time Savings, Space Savings and Money Savings

MULTI-FACETED MEANING OF VALUE4© 2011 GLOBAL TREND & DESIGN

Value of Quality Time Together Growing concern over the ‘softer’ side of raising

children Parents are taking back control with regard to

play, family time and everyday habits

OPPORTUNITY: Products and services that promote “together” time (gaming, cooking, eating and sports activities)

Research by the National Center on Addiction & Substance Abuse finds that children who eat four to five meals a week with their family are 40% more likely to get higher grades in school than kids who eat two or fewer meals a week with their family

Same study finds that kids who regularly eat dinner with their families are 20% less likely to drink alcohol, smoke or use illegal drugs.

REALITY:

MULTI-FACETED MEANING OF VALUE4© 2011 GLOBAL TREND & DESIGN

Exceed Expectations

Understand that value has individual meaning—some will weigh price more in the equation, others design and others quality or some other variable Tailor your offering to exceed the value expectations of

your consumer

Speak to the consumer’s needs and lifestyle Bring all components of the value equation into your

merchandising & marketing process

“Surprise and Delight” should be part of the plan That might be color, packaging, or even humor

MULTI-FACETED MEANING OF VALUE 4

PANEL DISCUSSION

REINVENTING CUSTOMER

RELATIONSHIPS

REINVENTING CUSTOMER

RELATIONSHIPS

5

REINVENTING CUSTOMER RELATIONSHIPS

5© 2011 GLOBAL TREND & DESIGN

Technology as a Game Changer

Multi-channel strategies: Consumers who shop across a number of channels—physical stores, the Internet, and catalogs—spend about four times more annually than those who shop in just one (McKinsey Research)

The internet is playing a role in almost half of U.S. retail sales, either as a point of research and/or for point of sale

73% of mobile-powered shoppers preferred peering into their phones for basic assistance over talking to a retail clerk (Accenture Survey)

REALITY: “In five years, every Target guest will be connected to the Internet—via their iPad or phone or other device—the entire time they are in the store. If that’s the case, what can we deliver?” (Sr. VP Store Design, Target)

REINVENTING CUSTOMER RELATIONSHIPS

5© 2011 GLOBAL TREND & DESIGN

OnlineShoppingGrowth

In 2009,

154 MILLIO

Npeople in

theU.S.

boughtsomethin

g online,

or...

The total spent online on

consumer goods was

$155 BILLION

That’s an average of

$1,006.5for every person

who made an online purchase

Online population

Total U.S. population

49.8%

67%

REINVENTING CUSTOMER RELATIONSHIPS

5© 2011 GLOBAL TREND & DESIGN

OnlineShoppingGrowth

U.S. online sales will keep growing at least through 2014. Forecast sales will be nearly

$250 BILLION

20092009

$155.2 B

20102010

$172.9 B

20102010

$191.7 B

20112011

$210.0 B

20122012

$229.5 B

20132013

$248.7 B

More than 44% of online sales ($67.6 Billion) was spent on...

REINVENTING CUSTOMER RELATIONSHIPS

5© 2011 GLOBAL TREND & DESIGN

Consumer

Reasoning

What is the most important factor when buying online?

Source: Guidance/Synovate

REINVENTING CUSTOMER RELATIONSHIPS

5© 2011 GLOBAL TREND & DESIGN

Consumer Empowerme

nt

Red Laser and similar apps available on iPhone, Android and Blackberry are changing the retailers relationship with the consumer forever. (also Edocrab, Sccope, ShopSavvy and Scandit)

Scan any items bar code and get comparative information on that item both regionally and on the internet

Keep a library of scanned items, so you don’t even need to leave your house.

The future will not just be price… Nutritional facts Allergen info Material and manufacturing info

REINVENTING CUSTOMER RELATIONSHIPS

5© 2011 GLOBAL TREND & DESIGN

Differentiate

Your Brand Work with your vendors to make certain that items

in your assortment have limited exposure on internet price comparison sites, and at your competitors

Keep an eye on the market, and stay at the right priceOPPORTUNITY: Create protection against price-only competition

Partner to create exclusive product Explore exclusive configurations for your customers

The safest competition is differentiation

RISK MANAGEMENT:

REINVENTING CUSTOMER RELATIONSHIPS

5© 2011 GLOBAL TREND & DESIGN

Beyond Products

& Services

REALITY: Consumers expect companies to go beyond being a producer of products and services…

To include helping make the world a better place Includes green products, community

involvement, charity, etc.OPPORTUNITY: Engage consumers with products or services which are more “responsible”

RECYCLE ELECTRONICS AT BEST BUY

MAKING A DIFFERENCE, SIMPLIFIED: Recyclability Minimized resource use (in

production and product lifecycle)

Fair and/or empowered labor Cause-related marketing

(Environmental, Education, Social Betterment)

Increased product lifespan

REINVENTING CUSTOMER RELATIONSHIPS

5© 2011 GLOBAL TREND & DESIGN

CreateLoyalty

REALITY: Store loyalty is eroding 43% of U.S. shoppers switched their retailer of

choice after going online for a chosen product (Nielsen)

OPPORTUNITY: Invite and engage the consumer to explore with store assortment, design and in-store experiences

Average time spent in an Anthropologie store is over one hour

ANTHROPOLOGIE

40% of customers remain open to persuasion once they enter a store (McKinsey Research)

REINVENTING CUSTOMER RELATIONSHIPS

5© 2011 GLOBAL TREND & DESIGN

Multi-Channel

Strategies

5

Physical space is still very important—but engaging the consumer has never been more difficult OR more crucial. How you leverage it must be strategic, not an afterthought

Small retailers have the advantage in creating experiential retailing

Multi-channel strategies need to be used to reinforce each other—the consumer is at a stage where single channel players seem outdated and irrelevant

Open up and get warm & fuzzy… you have to have meaning to your consumer to create loyalty, and a part of meaning is an emotional connection… show them you know their life, their needs, their aspirations

REINVENTING CUSTOMER RELATIONSHIPS 5

PANEL DISCUSSION

10 NEW RULES FOR THE CHANGING ECONOMY

10 NEW RULES FOR THE CHANGING ECONOMY

Age is a number, Not a lifestyle predictor

1

NEW RULES FOR A CHANGING ECONOMY

Meal occasions continue to blur as we eat more meals in a car or on the fly between places

Traditional kids food goes ‘up-market’ with gourmet grilled cheese and hot dog recipes

New traditions that expresses our individuality – such as the Sweet Potato Bar for Thanksgiving

© 2011 GLOBAL TREND & DESIGN

Economic recovery will be slow; success will come from taking market share from competitors… and non-competitors.

2

NEW RULES FOR A CHANGING ECONOMY

Bringing restaurant quality and excitement home will continue to create opportunities for the housewares industry

Reinventing the basics: one-pot meals, gourmet basics, tricked out snacks, crafted cocktails, embellished desserts

The economic downturn prompted consumers to buy coffee makers so that they could brew at home versus $4 lattes out

© 2011 GLOBAL TREND & DESIGN

Inspire ‘Shopping & Purchasing’ versus ‘Sharing & Trading’

3

NEW RULES FOR A CHANGING ECONOMY

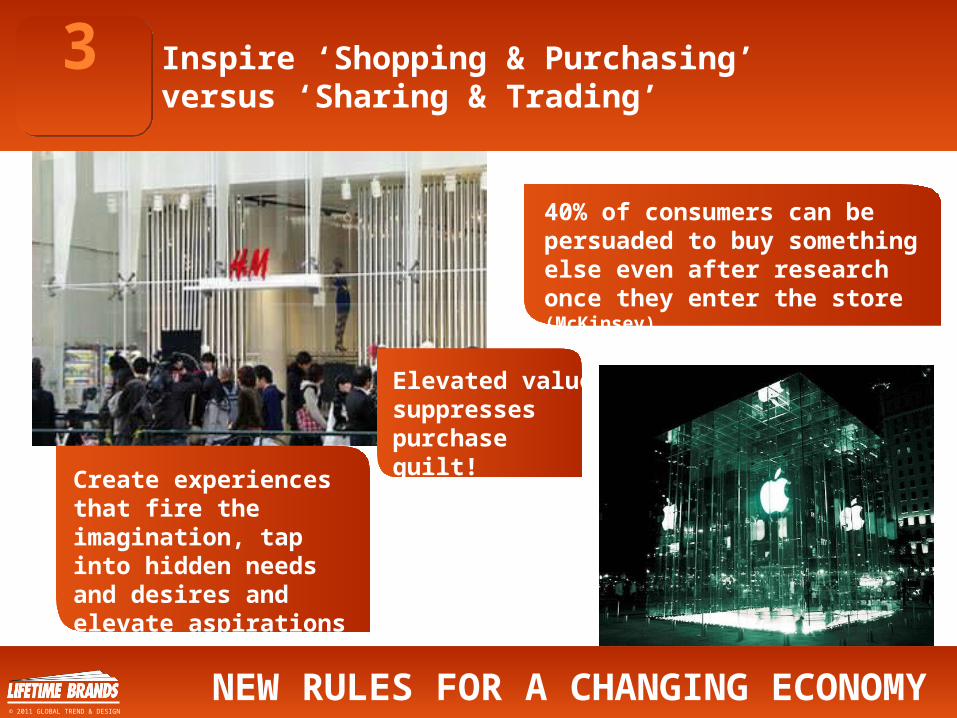

40% of consumers can be persuaded to buy something else even after research once they enter the store (McKinsey)

Create experiences that fire the imagination, tap into hidden needs and desires and elevate aspirations

Elevated value suppresses purchase guilt!

© 2011 GLOBAL TREND & DESIGN

Transparency is no longer optional… Manage your image like you manage your inventory

4

CRM Magazine, Lauren Mckay

NEW RULES FOR A CHANGING ECONOMY© 2011 GLOBAL TREND & DESIGN

Tracking orders. Being able to see when something has been shipped, where it is en route, estimated arrival time.

Give us your credit-card information and we will eventually give you something you paid for in return.

Our beef comes from grass-fed cows that spend a happy life in upstate Maine.

“Mystery Meat”

“Thanks for your phone call, are you calling me about the email you sent us last Monday at 2 p.m.?”

A Web site with no “contact us” page or phone number in sight.

Viewing an organization as one entity – whether it’s through a catalog, phone, Web site, or email.

“Let me transfer you to Extension 4. Hold, please.”

Leveraging customer feedback for innovation and research and developments.

“We could get some real work done is it weren’t for all these customers.”

Transparency Is Transparency Is Not

Create and enable family time, wellness and shared experiences in the home

5

NEW RULES FOR A CHANGING ECONOMY

Reevaluation of priorities means growth of:

Stand mixers & food processors Slow cookers Pressure cookers Blenders (homemade soups) Cupcake makers Cooking with kids Bring-a-dish socials

© 2011 GLOBAL TREND & DESIGN

Storage and space savings are a renewed concern in the American household

6

NEW RULES FOR A CHANGING ECONOMY

Americans buying in bulk, increase in rentals, staying longer in starter homes all point to the need for smaller footprints for everything, modularity and multifunction as important considerations for the buyer

Consumers want more storage to keep clutter under control

© 2011 GLOBAL TREND & DESIGN

Put some fun back in function.7

Functional gifting becomes more the norm

More items exposed = greater need for décor + function

Bringing joy into everyday ‘chores’

Consumers respond to little luxuries

Color and shape become the new ‘black’

Don’t be afraid to have a sense of humor

NEW RULES FOR A CHANGING ECONOMY© 2011 GLOBAL TREND & DESIGN

KIZMOS

Less ‘glam’ and more classic styling with long-term appeal.

8

The higher the ticket, the more important this becomes. We’re moving from a disposable society to one where quality and durability are again important key benefits.

NEW RULES FOR A CHANGING ECONOMY© 2011 GLOBAL TREND & DESIGN

Take “Comfort Food” and “Creature Comforts” to the next level

9

We live in a stressed society that is staying at home more, and re-discovering entertaining and loves surprising friends and family

NEW RULES FOR A CHANGING ECONOMY

Small indulgences like gourmet hot dogs and stuffed burgers

Guilty pleasures such as whoopie pies and stuffed pancakes

Taking basics “over the top”, like truffled mac and cheese and bacon cheddar popcorn

CURRY COCONUT POPCORN

© 2011 GLOBAL TREND & DESIGN

Technology increasingly changes how we shop, prepare and what we expect - don’t get left behind

10

Explore partnerships that help you capitalize on the benefits and exposure of mobile coupons, DIY blogs, online video on culinary and entertaining ideas

NEW RULES FOR A CHANGING ECONOMY

music goes digitalmovies are downloadedprint is becoming obsoleteas cookbooks become e-cookbooks

© 2011 GLOBAL TREND & DESIGN

©2011 Lifetime Brands, Inc.

TOP TRENDS for 2012

The information contained in this document provided by Lifetime Brands, Inc. is for demonstration & internal

research purposes only, to give dimension and meaning to the trends. Any reproduction of this information is a

direct violation of the Federal Copyright Law. This includes, but is not limited to, color copying, color printing, photocopying or faxing, as well as email

distribution of all content, photographs & images, or posting on the Internet. Please be careful to not copy the designs, trademarks or intellectual properties of others reported within these pages, as this may result in your

being sued or prosecuted by the owner of that content. ©2011 Lifetime Brands, Inc. Images © 2011 Sphere

Trending, LLC.

If you have any questions regarding this

presentation, please contact:

Tom MirabileSVP, Global Trend and Design

E: [email protected]: 917.864.6328

Lifetime Brands, Inc.