20

UK-India cross-border residential investment, August 2008 advance

| Date post: | 18-Aug-2015 |

| Category: |

Documents |

| Upload: | neha-jindal |

| View: | 12 times |

| Download: | 1 times |

UK-India cross-border residential investment, August 2008

advance

Introduction and Executive Summary ................................................................................................. 03

The Indian Phenomenon ................................................................................................................... 04

Past, present and future

Wealth creation

Indians investing in the UK ................................................................................................................ 08

Financial matters

Why invest in the UK?

What and where to buy?

Non Resident Indians investing in India ............................................................................................. 14

Financial matters

Why invest in India?

What and where to buy?

Contents

The emergence of the world’s second most populous nation as an economic force has already had a profound global impact.

With India’s economy forecast to grow strongly in the medium-term, we expect individual wealth to balloon. This will not only be seen in greater numbers of High Net Worth Individuals (HNWIs) but also, and perhaps more significantly, in the explosion of India’s middle-classes. The implications for residential investment both in the UK and in India are potentially huge.

In this report we chart India’s recent progression and explore its prospects. We also examine the benefits of investing in residential property and look at what types of properties can be bought both in the UK and in India.

India’s growth● India is the second largest country by population. ● The Indian economy has expanded by 8.6% pa during

the past five years.● It is now the fourth largest economy in the world, up from

tenth in 1992.● Indian GDP growth is forecast to rise by 7.3% pa over

the next ten years, more than double the global average.● By 2013 India is destined to become the third largest

world economy.● By 2050 India’s population is predicted to be the largest

in the world at 1.6 billion, higher than China.

Residential investment in the UK● The UK imposes no restrictions on Indians investing in

UK residential property.● The Indian authorities, however, restrict capital outflows

to US$ 200,000 a year for resident Indians. ● To date Indian buying has been mainly in London and in

the £ 0.6 to 1.2 million price range.● There are many reasons that support strong house price

growth in the UK following the current period of uncertainty.● We forecast that Indian investment in UK housing could

exceed £ 10–15 billion over the next 10 years.

Wealth in India● The number of HNWIs in India is growing at a faster

pace than any other nation.● In 10 years there are forecast to be over 400,000

HNWIs, four times the number today.● There are expected to be 1.9 million semi-HNWIs by 2017. ● The number of middle-class Indians with the potential to

invest in UK residential property is expected to rise to 583 million by 2025.

● The number of Indians with wealth exceeding US$ 100,000 is forecast to be 29 million by 2017.

Residential investment in India● Only Persons of Indian Origin, based in India or

elsewhere, are permitted to buy residential property in India.

● Strong economic and population growth will generate increasing demand for more and better quality housing.

● India’s developing demographic profile of young, aspirational and mobile individuals will boost demand for housing in many locations.

● Indian’s are already seeking better and alternative residential growth opportunities outside of Tier I cities.

Introduction

Executive Summary

3COPYRIGHT © JONES LANG LASALLE IP, INC. 2008. All rights reserved.

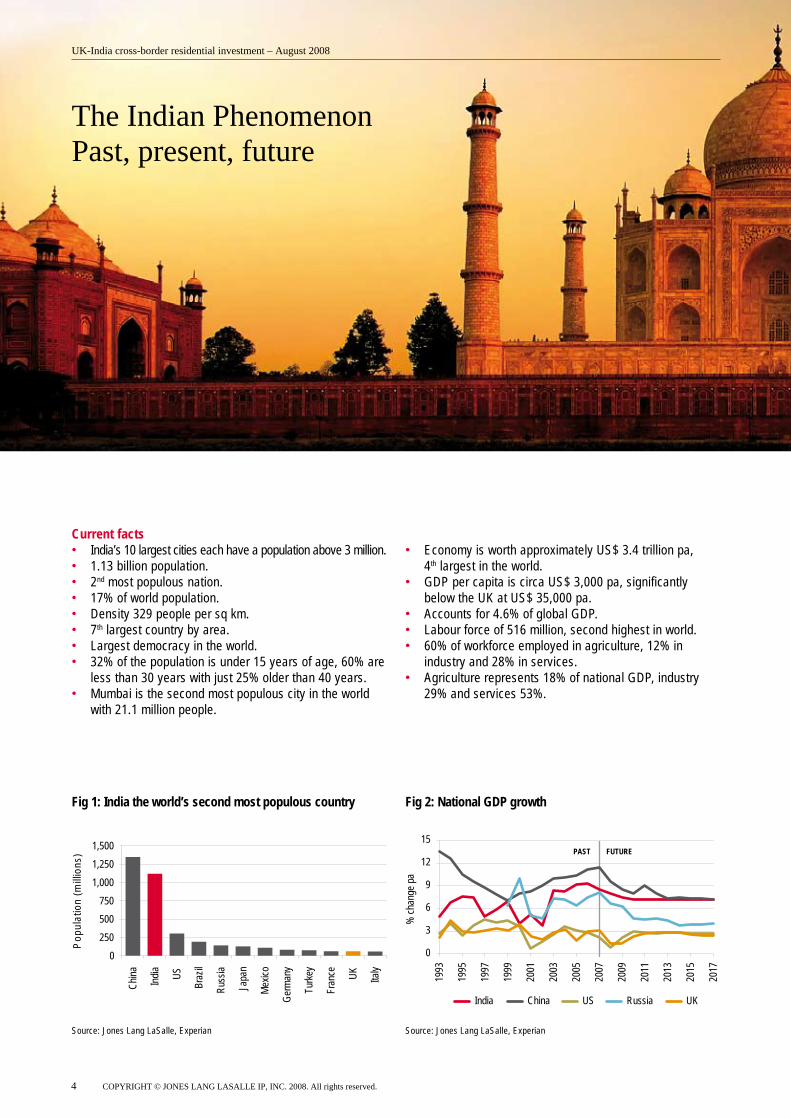

Fig 2: National GDP growth

Source: Jones Lang LaSalle, Experian

Fig 1: India the world’s second most populous country

Source: Jones Lang LaSalle, Experian

Current facts● India’s 10 largest cities each have a population above 3 million.● 1.13 billion population.● 2nd most populous nation.● 17% of world population.● Density 329 people per sq km.● 7th largest country by area.● Largest democracy in the world.● 32% of the population is under 15 years of age, 60% are

less than 30 years with just 25% older than 40 years.● Mumbai is the second most populous city in the world

with 21.1 million people.

● Economy is worth approximately US$ 3.4 trillion pa,

4th largest in the world.● GDP per capita is circa US$ 3,000 pa, significantly

below the UK at US$ 35,000 pa.● Accounts for 4.6% of global GDP.● Labour force of 516 million, second highest in world.● 60% of workforce employed in agriculture, 12% in

industry and 28% in services. ● Agriculture represents 18% of national GDP, industry

29% and services 53%.

The Indian Phenomenon Past, present, future

0250500750

1,0001,2501,500

China Ind

ia US

Braz

il

Russ

ia

Japa

n

Mexic

o

Germ

any

Turke

y

Fran

ce UK Italy

Popu

latio

n (m

illion

s)

% ch

ange

pa

India China US Russia UK

0

3

6

9

12

15

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

PAST FUTURE

4 COPYRIGHT © JONES LANG LASALLE IP, INC. 2008. All rights reserved.

UK-India cross-border residential investment – August 2008

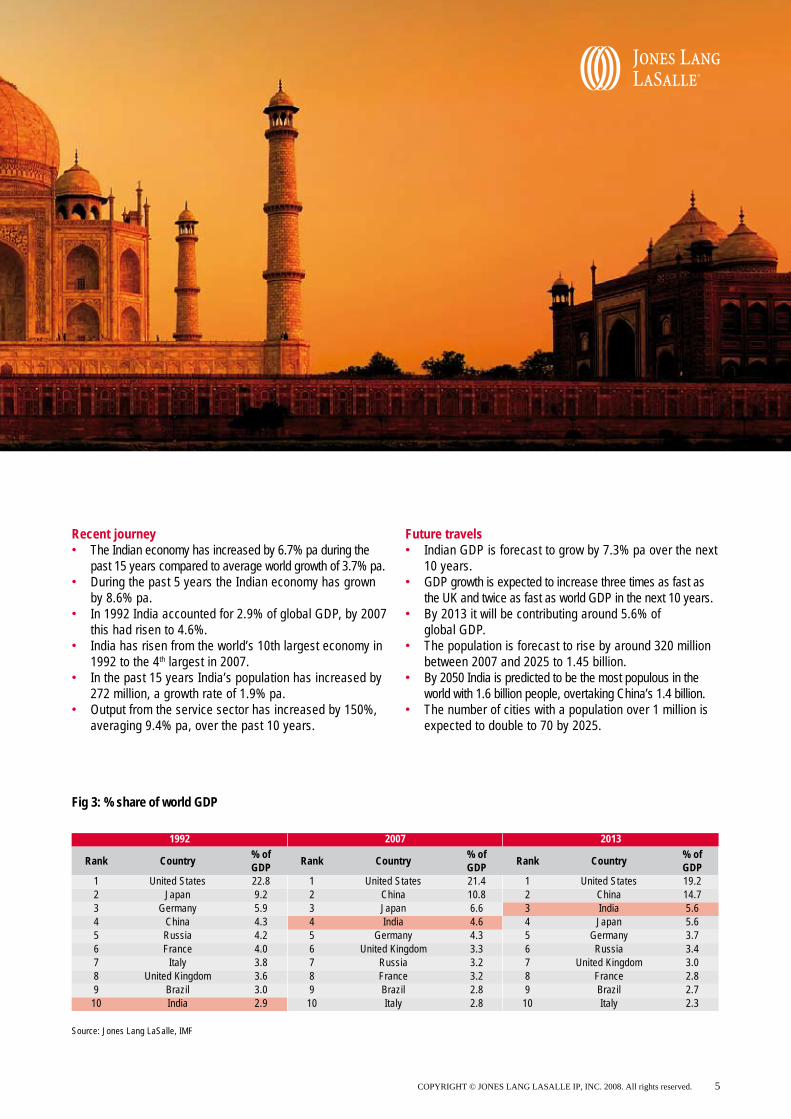

Fig 3: % share of world GDP

Source: Jones Lang LaSalle, IMF

1992 2007 2013

Rank Country % ofGDP Rank Country % of

GDP Rank Country % ofGDP

1 United States 22.8 1 United States 21.4 1 United States 19.22 Japan 9.2 2 China 10.8 2 China 14.73 Germany 5.9 3 Japan 6.6 3 India 5.64 China 4.3 4 India 4.6 4 Japan 5.65 Russia 4.2 5 Germany 4.3 5 Germany 3.76 France 4.0 6 United Kingdom 3.3 6 Russia 3.47 Italy 3.8 7 Russia 3.2 7 United Kingdom 3.08 United Kingdom 3.6 8 France 3.2 8 France 2.89 Brazil 3.0 9 Brazil 2.8 9 Brazil 2.7

10 India 2.9 10 Italy 2.8 10 Italy 2.3

Recent journey● The Indian economy has increased by 6.7% pa during the

past 15 years compared to average world growth of 3.7% pa.● During the past 5 years the Indian economy has grown

by 8.6% pa.● In 1992 India accounted for 2.9% of global GDP, by 2007

this had risen to 4.6%.● India has risen from the world’s 10th largest economy in

1992 to the 4th largest in 2007.● In the past 15 years India’s population has increased by

272 million, a growth rate of 1.9% pa.● Output from the service sector has increased by 150%,

averaging 9.4% pa, over the past 10 years.

Future travels● Indian GDP is forecast to grow by 7.3% pa over the next

10 years.● GDP growth is expected to increase three times as fast as

the UK and twice as fast as world GDP in the next 10 years.● By 2013 it will be contributing around 5.6% of

global GDP.● The population is forecast to rise by around 320 million

between 2007 and 2025 to 1.45 billion.● By 2050 India is predicted to be the most populous in the

world with 1.6 billion people, overtaking China’s 1.4 billion.● The number of cities with a population over 1 million is

expected to double to 70 by 2025.

5COPYRIGHT © JONES LANG LASALLE IP, INC. 2008. All rights reserved.

The Indian Phenomenon Wealth creation

Number of global US$ billionaires

1 – 10

11 –

20

21 –

50

51 –

100

101 –

250

250+

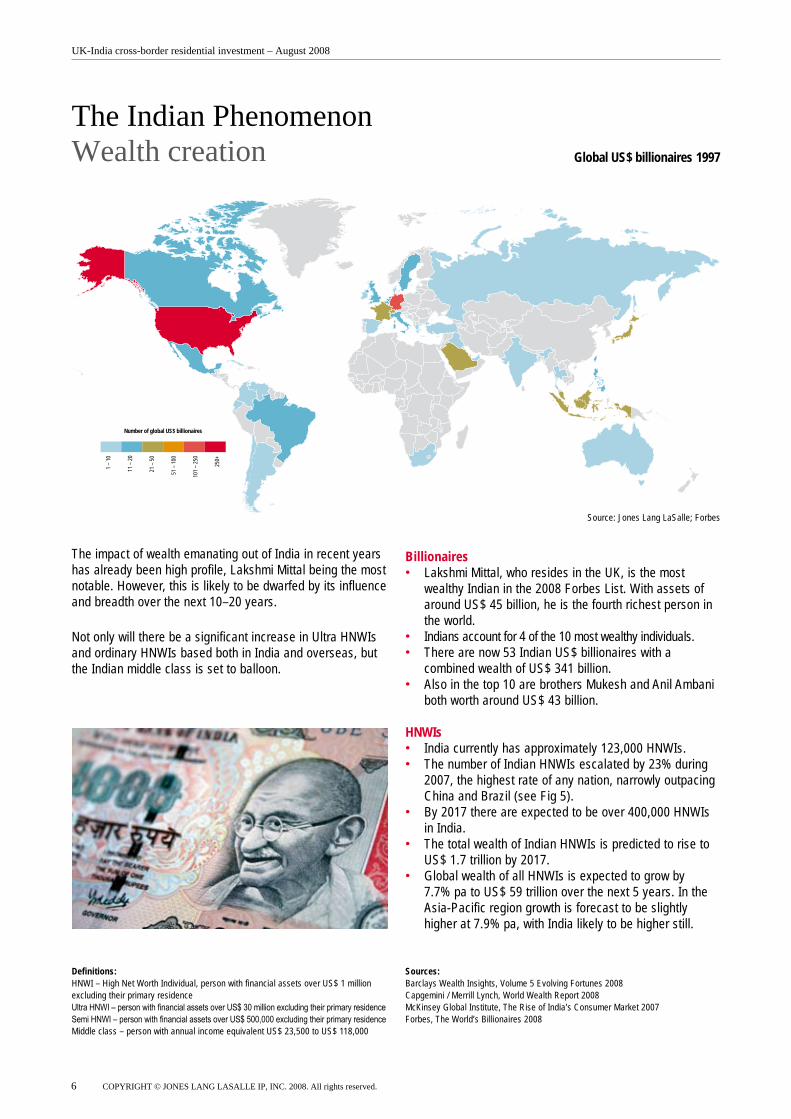

Global US$ billionaires 1997

Source: Jones Lang LaSalle; Forbes

The impact of wealth emanating out of India in recent years has already been high profile, Lakshmi Mittal being the most notable. However, this is likely to be dwarfed by its influence and breadth over the next 10–20 years.

Not only will there be a significant increase in Ultra HNWIs and ordinary HNWIs based both in India and overseas, but the Indian middle class is set to balloon.

Billionaires● Lakshmi Mittal, who resides in the UK, is the most

wealthy Indian in the 2008 Forbes List. With assets of around US$ 45 billion, he is the fourth richest person in the world.

● Indians account for 4 of the 10 most wealthy individuals.● There are now 53 Indian US$ billionaires with a

combined wealth of US$ 341 billion.● Also in the top 10 are brothers Mukesh and Anil Ambani

both worth around US$ 43 billion.

HNWIs● India currently has approximately 123,000 HNWIs.● The number of Indian HNWIs escalated by 23% during

2007, the highest rate of any nation, narrowly outpacing China and Brazil (see Fig 5).

● By 2017 there are expected to be over 400,000 HNWIs in India.

● The total wealth of Indian HNWIs is predicted to rise to US$ 1.7 trillion by 2017.

● Global wealth of all HNWIs is expected to grow by 7.7% pa to US$ 59 trillion over the next 5 years. In the Asia-Pacific region growth is forecast to be slightly higher at 7.9% pa, with India likely to be higher still.

Definitions:HNWI – High Net Worth Individual, person with financial assets over US$ 1 million excluding their primary residenceUltra HNWI – person with financial assets over US$ 30 million excluding their primary residenceSemi HNWI – person with financial assets over US$ 500,000 excluding their primary residenceMiddle class – person with annual income equivalent US$ 23,500 to US$ 118,000

Sources:Barclays Wealth Insights, Volume 5 Evolving Fortunes 2008Capgemini / Merrill Lynch, World Wealth Report 2008McKinsey Global Institute, The Rise of India’s Consumer Market 2007Forbes, The World’s Billionaires 2008

UK-India cross-border residential investment – August 2008

6 COPYRIGHT © JONES LANG LASALLE IP, INC. 2008. All rights reserved.

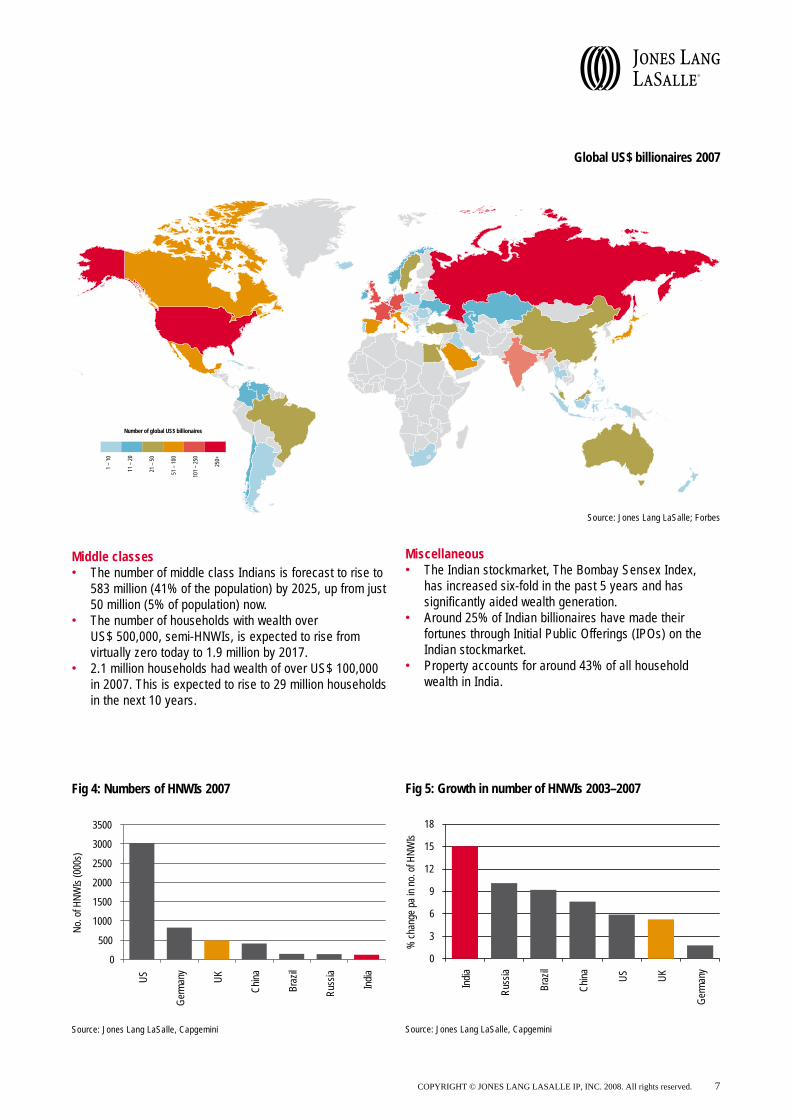

Middle classes● The number of middle class Indians is forecast to rise to

583 million (41% of the population) by 2025, up from just 50 million (5% of population) now.

● The number of households with wealth over US$ 500,000, semi-HNWIs, is expected to rise from virtually zero today to 1.9 million by 2017.

● 2.1 million households had wealth of over US$ 100,000 in 2007. This is expected to rise to 29 million households in the next 10 years.

Miscellaneous● The Indian stockmarket, The Bombay Sensex Index,

has increased six-fold in the past 5 years and has significantly aided wealth generation.

● Around 25% of Indian billionaires have made their fortunes through Initial Public Offerings (IPOs) on the Indian stockmarket.

● Property accounts for around 43% of all household wealth in India.

Fig 5: Growth in number of HNWIs 2003–2007

Source: Jones Lang LaSalle, Capgemini

0

3

6

9

12

15

18

India

Russ

ia

Braz

il

China US UK

Germ

any

% ch

ange

pa in

no. o

f HNW

Is

Number of global US$ billionaires

1 – 10

11 –

20

21 –

50

51 –

100

101 –

250

250+

Fig 4: Numbers of HNWIs 2007

Source: Jones Lang LaSalle, Capgemini

0

500

1000

1500

2000

2500

3000

3500

US

Germ

any

UK

China

Braz

il

Russ

ia

India

No. o

f HNW

Is (0

00s)

Global US$ billionaires 2007

Source: Jones Lang LaSalle; Forbes

7COPYRIGHT © JONES LANG LASALLE IP, INC. 2008. All rights reserved.

In this section we consider UK residential property activity by Indians either based outside the UK or who qualify as non-domiciles in the UK. Property investment by Persons of Indian Origin (POI) who are resident in the UK are not included.

The UK residential property headlines have been grabbed by the purchases of Ultra HNWIs like Lakshmi Mittal who has bought a number of homes in the past couple of years (see page 13). However, there has also been a growing tide of lower-profile purchases by Indians. To date the bulk have been in London and have been typically in the £ 0.6 to £ 1.2 million price range but we expect this range to broaden over the next few years, both up and down.

Investment restrictions● The UK does not impose any restrictions on overseas

investment in the UK meaning that any Indian is free to buy residential property in the UK.

● However, the Reserve Bank of India (RBI) imposes a restriction on capital outflows from India of US$ 200,000 per financial year. In February 2004 the restriction was increased from US$ 25,000 to its current level and there is also some pressure on the RBI to further relax this restriction.

Financing optionsThe capital outflow restriction of US$ 200,000 per financial year is a constraint on potential investment in UK residential property as this equates to only around £ 100,000. This is well below the average house price in the UK, around £ 175,000 and significantly lower than London’s average house price of circa £ 350,000. There are, however, a number of ways to help negate this constraint.

● Join forces with other family members, colleagues or business partners. If five individuals clubbed together the potential spend in any financial year would be US$ 1m, the equivalent of around £ 500,000.

● Part-finance the property purchase via a mortgage. This can be done as an individual or as a family/group if the property is held in joint names. Finance must be obtained in the UK or via an offshore mortgage lender.

● Borrowing can be purely based on purchase but can also be taken out based on rental guarantees if the property is intended to be let to tenants.

● The options are greater still if an off-plan purchase of a new property is considered. In this case, a deposit of up to US$ 200,000 can be made in year one, perhaps before construction starts, up to US$ 200,000 in the following year, perhaps during construction, with up to US$ 200,000 on completion. This option is also attractive for UK housebuilders as deposits before completion are typically only 10% from UK buyers.

Tax implicationsTax liabilities are highly dependent on individual circumstances and how property is purchased and financed. However, the guidelines below are broadly appropriate for most investors but it is strongly recommended that personal tax advice is sought before considering residential investment in the UK.

In the UK● Non UK residents are not liable for UK capital gains tax (CGT).● For resident non-domiciles, if the UK property is the main

residence of the owner no CGT will be due on sale. If the property is not the owner’s main residence CGT, currently 18%, on the chargeable gain will be liable upon sale.

● If the property is let as an investment UK income tax will be due. ● If a property is let as an investment and the owner is not

based in the UK it is preferable for them to register under the Non Resident Landlord Scheme which enables them to receive their rents gross of tax and to obtain relief from allowable property expenditure, via the submission of an annual tax return. If the owner does not register for this scheme, basic rate income tax on rental income is withheld by their letting agent or tenant and no relief is given for property expenses and mortgage costs. The current basic rate of income tax in the UK is 20%.

In India● Persons who are resident in India for Indian tax purposes

are liable to tax on global income and global capital gains in India, including capital gains on UK residential property. This, however, is subject to the provision of the double taxation relief agreement between the governments of India and UK.

Indians investing in the UK

UK-India cross-border residential investment – August 2008

8 COPYRIGHT © JONES LANG LASALLE IP, INC. 2008. All rights reserved.

The scale of possible investmentIf we combine the growth in the Indian economy and the level of wealth creation to date with the projections made earlier in our report, it is clear that the potential spend on UK residential property investment can be huge over the next ten years.

Specific predictions are difficult but we can make some broad assumptions to give us some idea of the potential scale of investment. It has been forecast that there will be around 1.9 million Indian households with wealth exceeding US$ 500,000 by 2017. Currently, the proportion of any individual’s wealth invested in property is typically 20% of all assets. We can also make the assumption that the approximate proportion of wealth invested in the UK rather than elsewhere is 10%. By combining these numbers the following seem quite plausible over the next 10 years.

● £ 10–15 billion could be spent by Indians on UK residential property.

● Indians could own 20,000–30,000 UK residential properties.● By adding in other potential sources of UK residential

investment, such as spending by HNWIs as well as investment by some of the mass middle-class, these figures could prove quite conservative.

Other costsWith the number of middle-class Indians another potential source of UK residential investment as well as greater potential spending by HNWIs with significantly more wealth than US$ 500,000, these figures could prove quite conservative.Investors in UK residential property should also be aware of the other main costs when buying, selling and renting a property.

● When buying, these include stamp duty land tax, solicitors fees, mortgage related costs such as valuation, survey and arrangement fees and a Land Registry fee.

● When selling, the main costs include estate agent and solicitors fees.

● When renting out a property the main costs are the payment of a managing agent and furnishings.

COPYRIGHT © JONES LANG LASALLE IP, INC. 2008. All rights reserved. 9

Residential property should usually be regarded as long-term investment asset. It therefore seems wise to consider the long-term historic performance as well as the medium-term outlook of UK residential property when considering such an investment.

Past UK residential property performance● UK residential property has increased in value at an

average of 10.4% pa during the period 1970–2007, stronger than either UK equities or UK commercial property (see Fig 6).

● Residential property values in the UK have risen even faster over the last 10 years at an average of 11.5% pa growth.

● In total return terms (capital value growth plus income return) it is estimated that UK residential property has generated a return of over 16% pa since 1970, significantly stronger than UK commercial property (12% pa) and UK equities (14% pa).

● Furthermore, and unlike equities, the ability to borrow using property as collateral enables the return on equity to be even higher than the total return figures quoted here.

Short-term outlookAs a consequence of the credit crisis residential property prices are currently falling in the UK. It also remains quite uncertain how long and how deep the economic and housing slowdowns will be. At present we expect house price falls in the region of 12% this year and 7% next year before prices begin to recover.

Medium-term forecastsWhile there are current uncertainties and weaknesses in the UK housing market we believe that there are a number of fundamental reasons why UK residential property will appreciate strongly in value in the medium-term. Currently we forecast that UK residential prices will increase by 8–9% pa during 2010–2013 with around 6% pa likely in the medium-term. Our forecasts derive from economic and household income growth as well as restricted housing supply and strong demand factors (see opposite). In addition to capital value growth investors should be able to obtain a gross rental income return of between 4% and 6% pa.

Fig 6: UK capital value growth 1970–2007

Source: Jones Lang LaSalle; Nationwide; IPD

Residential property 10.4% paCommercial property 5.5% paEquities 9.0% pa

Index

(197

0 = 10

0)

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

0

1000

2000

3000

4000

Why invest in the UK?

“ There is a fundamental undersupply of housing in the UK and in London ”

10 COPYRIGHT © JONES LANG LASALLE IP, INC. 2008. All rights reserved.

UK-India cross-border residential investment – August 2008

● Undersupply of residential property For many years the population of England and the

demand for housing has been expanding at a faster rate than the building of new homes. In response the British Government has set targets for additions to the housing stock in England of 3 million by 2020 and a target of 240,000 a year by 2016. While additions have increased recently, they are still well below government targets (see Fig 8). Furthermore, as construction levels are likely to fall significantly over the next few years due to the weaker UK housing market, the divide between housing demand and supply will only increase further.

● Restricted land supply The amount of developable land in the UK is constrained

by a tight planning system which, in particular, restricts development on greenfield land that has not previously been built upon. As a result it is difficult for housing supply to increase to meet demand.

● Demographic demand drivers Demand for housing in the UK has increased

significantly in recent years through natural population rises, positive net inward migration and the need for more single person households. This trend is likely to continue if not accelerate over the medium-term.

● Home ownership and renting There is a strong aspiration in the UK for adults to own

their home which helps to maintain a reasonable level of housing demand over a medium-term time horizon. This

is borne out by the fact that around 70% of households own their home in the UK. Around 12% of UK households rent from private landlords, and significantly more in London, which implies there is a healthy source of potential tenants for residential investors.

● Growing importance of the family home A family’s most valuable asset has often been its home

but it has taken on even greater importance in recent years as home owners have increasingly used the value in their home as a supplement to their pension provision. Additionally, and because of the growing importance, this has led many parents to give financial assistance to their children to help them onto the property ladder. Typically this has been funded through parents taking equity out of their home or by raiding their savings rather than waiting to pass down financial support through inheritance.

● Rise in residential investors Another significant change in the UK housing market has

been the increase in buy-to-let investors. Indeed, the number of buy-to-let mortgages outstanding in the UK has risen from around 30,000 in 1998 to over 1 million today. Residential investment has been used as a real alternative to investing in shares and other asset classes especially as capital values have been rising so strongly over the last 12 years. It is also being used as a pension supplement and income generator during retirement.

Fig 7: UK residential property forecasts

Source: Jones Lang LaSalle; Nationwide

-15-10-505

101520

Dec 0

5

Dec 0

6

Dec 0

7

Dec 0

8

Dec 0

9

Dec 1

0

Dec 1

1

Dec 1

2

Dec 1

3

London Central & Northern UK

% ch

ange

pa

11COPYRIGHT © JONES LANG LASALLE IP, INC. 2008. All rights reserved.

Fig 8: Homebuilding in England

Source: Jones Lang LaSalle; DCLG

100

140

180

220

260

300

1991

/92

1992

/93

1993

/94

1994

/95

1995

/96

1996

/97

1997

/9819

98/99

1999

/0020

00/01

2001

/0220

02/03

2003

/04'20

04/05

2005

/0620

06/07

Net additions New completions Government target

Numb

er of

dwell

ings (

000s

)

City Population % Private rented sector

Average house price

London 7,410,500 15.3 £ 355,000

Birmingham 2,161,000 6.8 £ 133,000

Manchester 1,480,500 10.0 £ 116,000

Leeds 496,000 12.2 £ 155,000

Sheffield 448,000 9.2 £ 142,000

Liverpool 439,000 13.1 £ 126,000

Bristol 363,000 13.8 £ 188,000

LondonBristol

Birmingham

Sheffield

Leeds

Liverpool

Manchester

1

2

3

4

5

6

7

1

2

34

56

7

UK-India cross-border residential investment – August 2008

12 COPYRIGHT © JONES LANG LASALLE IP, INC. 2008. All rights reserved.

NORTH LONDON

WEST LONDON

EAST LONDON

SOUTH LONDON

Mayfair

Chelsea

Knightsbridge

St John’s Wood

Southwark

Camden

Regents Park

St James Park

Hampstead Heath

Canary Wharf

Houses of Parliament

London Eye

Lord’s Cricket GroundThe City

Buckingham Palace

Tower of London

Hyde Park

Fulham

Islington

River Thames

1a 1b

1c

1d

1e

1f

Central London West: KensingtonLakshmi Mittal, the fourth richest person in the world and wealthiest Indian, is said to be in negotiations to buy this mansion in Kensington for around £ 117 million.

Central London West: KnightsbridgeJones Lang LaSalle recently sold studio, one and two bedroom apartments in this new 199 Knightsbridge Ltd development in Knightsbridge.

One bedroom apartments sold for around £ 1.0 million (approx £ 1,400 per sq ft) Two bedroom apartments sold for around £ 1.9 million (approx £ 1,200 per sq ft)

Central London West: FulhamJones Lang LaSalle are currently selling studio, one and two bedroom apartments as well as three and four bedroom houses in this new Astral Homes development in Fulham.

One bedroom apartments are on the market for around £ 400,000 (approx £ 740 per sq ft)Two bedroom apartments are priced at around £ 700,000 (approx £ 850 per sq ft)Three bedroom houses are on the market for around £ 800,000 (approx £ 650 per sq ft)

Central London East: DocklandsDeveloper Ballymore has almost finished construction on a total of 736 units in two towers at Canary Wharf in London’s Docklands area. Almost all units have sold off-plan.

One bedroom apartments around £ 400,000Two bedroom apartments around £ 500,000

North London: StanmoreSt Edward Homes are developing Stanmore Place. The first phase will consist of 119 units incorporating views over a lake and landscaped gardens. Completion for this phase is due in 2010.

One bedroom apartments around £ 250,000 (approx £ 500 per sq ft)Two bedroom apartments around £ 350,000 (approx £ 450 per sq ft)Three bedroom apartments around £ 460,000 (approx £ 450 per sq ft)

BirminghamAt Park Central in central Birmingham, Crest Nicholson are marketing a selection of one to four bedroom townhouses.

One bedroom houses around £ 160,000 (approx £ 250 per sq ft) Three bedroom houses around £ 230, 000 (approx £ 230 per sq ft)

ManchesterTaylor Wimpey are currently selling one and two bedroom apartments as well as three and four bedroom townhouses in the affluent West Didsbury area of South Manchester.

One bedroom apartments around £ 150, 000 (approx £ 320 per sq ft)Two bedroom apartments around £ 180,000 (approx £ 320 per sq ft)Three and four bedroom townhouses around £ 320,000 (approx £ 260 per sq ft)

South London: CroydonBarratt Homes are developing New South Quarter, a new community in Croydon of over 700 studio, 1, 2 and 3 bedroom apartments in contemporary buildings, set around their own courtyards and gardens. Development will be phased during 2009–2012.

One bedroom apartments around £ 200,000 (approx £ 420 per sq ft) Two bedroom apartments around £ 250,000 (approx £ 340 per sq ft)

13COPYRIGHT © JONES LANG LASALLE IP, INC. 2008. All rights reserved.

1a

1b

1e

1c

1d

6

1f

2

Non Resident Indians investing in India

Only a Person of Indian Origin (POI), including Non Resident Indians (NRIs), as well as all residents in India are permitted to buy residential property in India. Non POI residents in the UK are therefore not allowed to invest in Indian residential property. In this section we focus on residential investment in India by NRIs and POIs living in the UK as well as non-domiciled Indians resident in the UK. Unless otherwise stated in this section the term ‘investors’ refers to anyone meeting one of these three criteria.

In recent years the Government of India has introduced quite liberal policies to enable NRIs to invest in India. However, since property transactions and holdings count as dealing with foreign exchange, all investment must abide by the legalities set out in the Foreign Exchange Management Act (FEMA) of 1999. These and other rules and restrictions are detailed below.

Investment restrictions and conditions● Investors are permitted to acquire any form of property

in India with the exception of agriculture, plantation property or a farmhouse without the need of formal permission from the Reserve Bank of India (RBI).

● A declaration of purchase of any property must be made to the RBI.

● Residential properties can be purchased using inward remittances from anywhere outside India or through funds maintained in NRI bank accounts in India.

● There are no restrictions on the number of properties that can be owned.

● NRIs are permitted to sell a property to any person resident in India or to another NRI or to any POI.

● A POI is free to sell their property to any person resident in India or to an NRI but may only sell to another POI who is not resident in India or an NRI with the strict approval of the RBI.

● NRIs are permitted to transfer the ownership of any property to a resident Indian without any approval or restrictions.

● NRIs may inherit property owned by other NRIs provided that the property was bought within the provisions of the foreign exchange law in force at the time of the property acquisition.

● A POI may acquire any immovable property in India by way of inheritance from a person resident outside India provided that the property was bought within the provisions of foreign exchange law in force at the time of the property acquisition.

Financing optionsIn financial terms buying property in India has been made reasonably convenient since many Indian banks offer specialist home loan and mortgage schemes specifically for NRI investors. Some banks have even launched in London to further aid property investment buying.

Investors are permitted to acquire mortgages without prior approval from the RBI and can repay the loans through inward remittance via normal banking channels, via NRE or FCNR accounts (see below for explanation) or directly out of rental income. Loans can even be repaid by a borrower’s close relatives (under certain rules).

At present loans of up to 85% loan-to-value can be obtained reasonably easily although loan-to-value ratios are more typically around 60%. Fixed rate buy-to-let mortgages covering the entire duration of the loan are currently available at an interest rate of around 14% pa.

Tax implications and considerationsTax liabilities are dependent on individual circumstances and how property is purchased and financed. However, the guidelines below are broadly appropriate for most investors but it is strongly recommended that personal tax advice is sought before considering residential investment in India.

A Non Resident Ordinary Rupee Account (NRO) may be maintained by any person resident outside India. These accounts can be maintained for savings, current accounts and recurring or fixed deposits. The account can be credited with remittances received in any permitted currency from outside India or legitimate dues in India. All local payments in rupees and remittances outside India of current income are permitted to be made from a NRO account subject to the necessary compliances.

Non Resident External Rupee (NRE) accounts may be opened without any approval if the funds for the account are transferred in freely convertible foreign currency. These accounts can also be maintained for savings, current accounts and recurring or fixed deposits. Balances held in this account and any interest earned on this account are exempt from tax. NRIs may jointly open this account with another NRI.

A Foreign Currency Non Resident account (FCNR) is a deposit only account which may only be held in Pounds Sterling, US Dollars or Japanese Yen. The deposit is accepted for a period of not less than six months and not above three years. Remittance from abroad has to be made in the foreign currency in which the account is nominated to be maintained. The balances and the interest on this account are also exempt from tax.

UK-India cross-border residential investment – August 2008

14 COPYRIGHT © JONES LANG LASALLE IP, INC. 2008. All rights reserved.

● Investors must pay income tax in India on any rental income received from their Indian property holdings. However, a flat rate deduction of 30% of rental income is applicable before assessing the level of taxable rental income. If a property is purchased out of borrowed funds, the interest payable qualifies for deduction against rental income. The current rate of income tax in India varies according to income level and rises to a maximum of 30.9% on income exceeding USD 11,628 (INR 500,000). Additionally, a surcharge is applicable if income exceeds USD 23,256 when the effective rate of tax becomes 33.99%.

● If more than one property is owned, which is used for self-occupation or is vacant, an investor is liable to pay tax on the notional rental income (annual letting value) on any additional property. An investor is eligible for a 30% reduction on the notional rental income when computing the notional property income for tax purposes.

● Investors do not have to pay tax on any interest earned from the proceeds of both rental income and capital gains as long as these proceeds are placed in specialist non resident bank accounts, an NRE or a FCNR account (see below for explanation).

● Investors are also liable for wealth tax annually on certain assets including immovable properties. However, one residential house is unconditionally exempt from wealth tax while residential property which is let out for a minimum period of 300 days during the year is also not liable to wealth tax. However, other properties that are used for self-occupation or rented out for less than 300 days are liable to pay tax on their notional rental income (annual letting value). In computing the wealth, the borrowing specific to the purchase of a property which is subject to wealth tax is deductible. Wealth tax is levied on all taxable properties at 1% of the value exceeding INR 1.5 million.

● Investors are permitted to repatriate any proceeds from the sale of residential property in India although the

amount to be repatriated must not exceed that originally paid for the property either in foreign exchange by debit to a NRE or a FCNR account.

● The repatriation of sale proceeds out of foreign exchange, however, is restricted to a maximum of two properties.

● Investors are also restricted from repatriating proceeds from residential investments in the form of dividends.

● Capital gains may be credited to an NRO or FCNR account from where an investor may repatriate up to US$ 1 million per financial year.

● Investors have to pay capital gains tax in India on their capital gains from the sale of any property. Capital gains on properties held for more than 36 months is computed by indexing the cost of acquisition and is taxable at 22.66%. An exemption may be available against capital gains for any re-investment of sale proceeds of the property into another residential property or if the funds are locked into government bonds for at least three years.

● Capital gains on properties held for less than 36 months are subject to tax at 33.99%.

● As capital gains tax in India is higher than in the UK, investors would have no UK capital gains tax liability as a result of the double taxation relief agreement between the governments of India and UK.

Other costsInvesting in Indian property also attracts following main costs.

● When buying, these include stamp duty, registration charges, legal charges and mortgage related costs such as processing and valuation fees.

● When selling the main costs include brokerage and solicitors fees.

● When renting out a property the main cost is payment to a managing agent.

COPYRIGHT © JONES LANG LASALLE IP, INC. 2008. All rights reserved. 15

Over the past few years there has been a steady rise in the number of NRIs investing in Indian residential property. There are several reasons behind this trend which is part motivated by investment gain but also guided by personal factors such as home town investment.

In this section we consider the driving forces behind the potential for strong house price gains as well as the preferences and trends already evident and likely to become evident in India over the medium-term.

Past Indian residential property performanceThe growth rate of residential property across major cities in India has been recorded at a high of 100% in prime locations of Tier I cities to a low of 30% in Tier III cities over a period of 2–3 years. The average rate of growth for the top 7 cities has been approximately 19% pa over the last 2–3 years.

Short-term outlookThe credit crunch and global economic slowdowns have recently decelerated the growth in house prices. The number of transactions has also declined compared to the last few years.

The residential market in India has become price sensitive and price points above INR 2,500 to INR 3,500 might face resistance from mass market consumers. The luxury or high-end housing market is expected to remain firmer as this niche sub-market caters to a smaller set of more wealthy buyers, who will remain largely unaffected by rising interest rates as many purchases will not need to depend on mortgage finance.

Medium-term forecastsWhile there are current weaknesses in the Indian market we believe that there are many reasons why residential property prices can rise strongly in the medium-term. In India these are principally demand drivers and are highlighted below. In addition to capital value growth investors should be able to obtain a gross rental income return of between 5.5% and 6.5% pa.

● Growing economy As has been mentioned earlier, the Indian economy is

expected to grow strongly over the medium-term, building further on recent performance, despite slowdowns in more developed economies. A key driver of the economy is expected to be the services industry including sectors such as IT/ITES (Information Technology Enabled Services), semi-conductors and bio-technology. This strong economic activity will lead to higher employment, income and demand for housing.

● Demographics Demand for Indian residential property is set to escalate strongly

in the medium term. India’s population is set to rise by around 320 million from 1.13 billion in 2007 to 1.45 billion by 2025. Furthermore, with 60% of the current population under the age of 30 many of these will provide an additional source of housing demand over the coming decades.

● Emergence of nuclear families Given current demographics, the recent trend towards the

emergence of nuclear families (households containing parents and immediate children only, rather than extended families that can include aunts, uncles, grandparents etc) is set to intensify further. This trend is being driven further by the wave of young adults migrating to other cities for better career opportunities. It is estimated that more than 70% of households are currently nuclear families, a figure that is expected to rise further and create additional demand for housing in the medium term future.

● Rising disposable income levels Total personal disposable income has risen from US$ 492 billion

in 2003 to US$ 876 billion in 2007 and is expected to rise to approximately US$ 1,800 billion by 2012. Rising income levels and increasing purchasing power are likely to lead to stronger consumer spending as well as potential funds for residential purchases.

● Home ownership and leasing With disposable incomes rising among young working Indians,

especially in the IT/ITES sector, many more people are aspiring to own a home. Although the migrant population across major cities, many of whom have moved for better career opportunities, prefer to live in leased houses initially, which is providing a ready source of tenants for residential investors, many of these aim to buy a home in the future. This is mainly led by the need for security, the emergence of real estate as a favoured investment asset class as well as home loan tax benefits.

● Urbanisation and infrastructure developments India’s urban areas are set for strong growth in the medium-

term. It is forecast that 41% of the population will be living in urban areas by 2011, an increase from 28% in 2001. Furthermore, the number of cities with more than one million people is expected to double from 35 in 2001 to 70 cities by 2025. The Central Government of India also recognises the dependence of economic growth on infrastructure and estimates that investment will rise to US$ 150 billion in the next five years. This urbanisation is likely to lead to significant housing demand and supply in the medium-term.

Why invest in India?

UK-India cross-border residential investment – August 2008

16 COPYRIGHT © JONES LANG LASALLE IP, INC. 2008. All rights reserved.

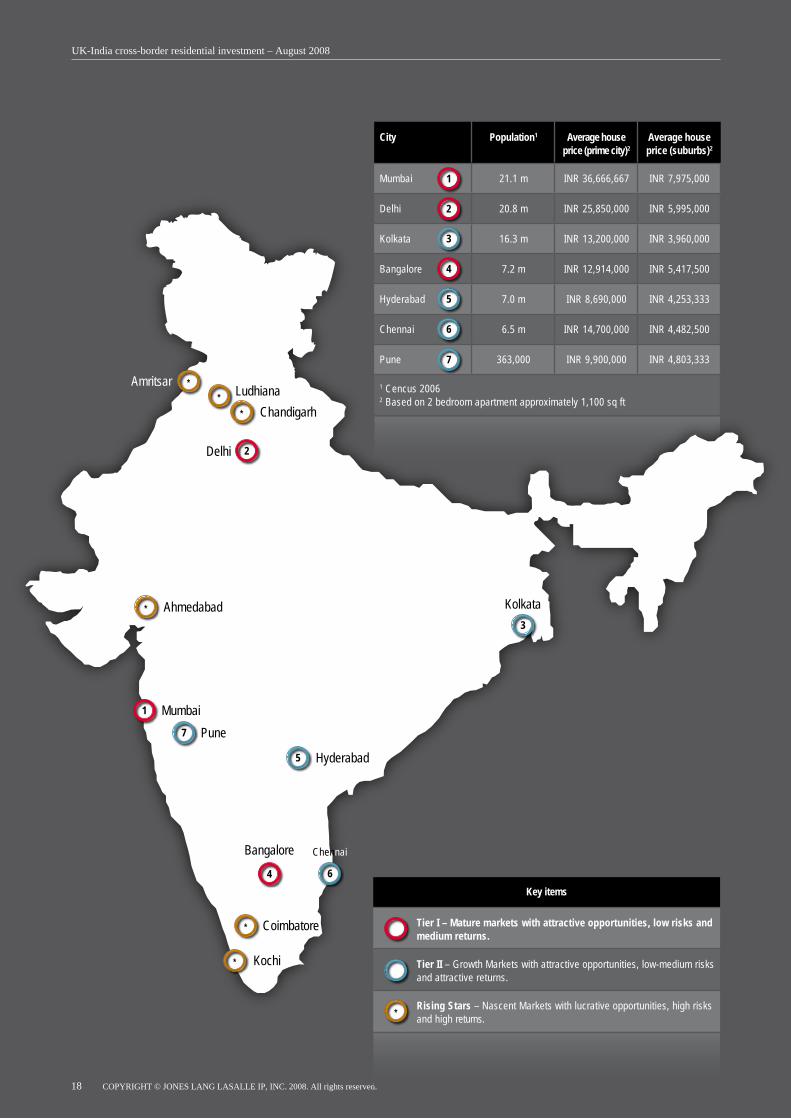

Housing preferences for NRI investorsDevelopers in India report that 15–25% of all new developments are bought by NRI investors. The source of NRIs is quite diverse with significant numbers residing in the UK, the US, Singapore, Malaysia, Dubai and the Middle-East.

● Evidence to date suggests that 3BHK (3 bedrooms, hall and kitchen) are the most popular size of property bought by NRI investors, with 2BHK properties following closely behind. Villas and penthouses are also proving to be as popular as apartments.

● High specification is proving a crucial factor for NRI investors. Internally this includes air-conditioning, power back-up, wi-fi capability, solar water heating and luxury entrance lobbies with CCTV. Externally, swimming pools, health and sporting facilities and quality security surveillance are also positive attributes.

● The most developed Indian cities have so far proven to be the most popular destinations for residential investment and include the Tier I cities of Delhi, Mumbai and Bangalore. Significant too is the emergence of Tier II and Tier III cities as likely residential investment locations. The key in these cities is the additional potential for growth and therefore property price growth (see Fig 9).

Emerging residential investment trends● Integrated townships are gated complexes that are

professionally managed where residents can walk to work and have important amenities such as schools and hospitals close at hand.

● Golf-centric properties, residential developments that form part of a golfing complex are proving popular amongst HNWIs.

● We expect the emergence of second or third homes that can be used as holiday homes, either by the sea or in the hills, to accelerate in the coming years as wealth spreads and deepens.

● Temple towns such as Nashik, Tirupathi and Nathdwara are likely to see the development of pilgrimage homes, probably high-end villas, catering to the regular floating pilgrims of the NRI population.

Fig 9: Most preferred cities for NRI investment

Source: Jones Lang LaSalle Meghraj

17COPYRIGHT © JONES LANG LASALLE IP, INC. 2008. All rights reserved.

City Population1 Average house price (prime city)2

Average house price (suburbs)2

Mumbai 21.1 m INR 36,666,667 INR 7,975,000

Delhi 20.8 m INR 25,850,000 INR 5,995,000

Kolkata 16.3 m INR 13,200,000 INR 3,960,000

Bangalore 7.2 m INR 12,914,000 INR 5,417,500

Hyderabad 7.0 m INR 8,690,000 INR 4,253,333

Chennai 6.5 m INR 14,700,000 INR 4,482,500

Pune 363,000 INR 9,900,000 INR 4,803,333

1 Cencus 20062 Based on 2 bedroom apartment approximately 1,100 sq ft

UK-India cross-border residential investment – August 2008

18 COPYRIGHT © JONES LANG LASALLE IP, INC. 2008. All rights reserved.

Key items

Tier I – Mature markets with attractive opportunities, low risks and medium returns.

Tier II – Growth Markets with attractive opportunities, low-medium risks and attractive returns.

Rising Stars – Nascent Markets with lucrative opportunities, high risks and high returns.

Mumbai

Delhi

Bangalore Chennai

Hyderabad

Pune

KolkataAhmedabad

Chandigarh

Kochi

Coimbatore

Ludhiana Amritsar

1

2

3

4

5

6

7

2

3

1

7

5

4 6

19COPYRIGHT © JONES LANG LASALLE IP, INC. 2008. All rights reserved.

MumbaiScheme: Lodha Solitaire, Developer: Lodha BuildersWell designed expansive bungalows with private gardens and sweeping verandas in a well designed community setting.Prices: INR 51 crores

Gurgaon, DelhiScheme: The Palm Drive, Developer: Emaar MGFVillas and apartments with international standard specifications, spacious interiors, excellent views and fine finishes.Prices: INR 2–4 crores

Noida , DelhiScheme: Unitech Grande, Developer: Unitech LimitedA project spread over large area of 347 acres, with 8 iconic towers and all apartments are luxurious facing the golf course.Prices: INR 1.5–3 crores

KolkataScheme: Rosedale Garden Complex, Developer: Rosedale Developers Pvt. Ltd.Luxurious housing project for NRIs giving them the same comforts and amenities as the west. A blend of modernism and international living.Prices: INR 1–1.5 crores

BangaloreScheme: Pebble Bay, Developer: B. Raheja Builders Pebble Bay is centrally located in up-market Dollar’ s Colony. The Project includes duplex apartment and penthouse equipped with luxury facilities.Prices: INR 1.8–2.4 crores

HyderabadScheme: Palm Meadows, Developer: Splendid Aparna Projects Private LitmitedPalm Meadows, spread over an expanse of 95 acres, offering state-of-the-art facilities and amenities with 14 acres of central park in a gated community.Prices: INR 1.5–2.5 crores

ChennaiScheme: Garden City, Developer: DLFFeaturing International standards geared to serve customer needs, the DLF Garden City is going to be a true reflection of quality living and contemporary lifestyles. The product strives to deliver the synergistic strengths of good architecture, appropriate designs, impressive aesthetics and safety features.Prices: INR 45–60 Lakh

PuneScheme: Picasso, Developer: Kumar PropertiesEach residence incorporates expertly planned layouts and is inspired by the most beautiful décor style.Prices: INR 60 Lakh – 1.5 crores

Mohali, ChandigarhScheme: The Views, Developer: Emaar MGF The Views is a gated community of premium apartments.Prices: INR 1 crores and upwards

Prices mentioned are indicative figures (exclusive of additional charges) and may vary as per size, type and developer’s norms.

1

2

2

3

4

5

6

7

Contacts

COPYRIGHT © JONES LANG LASALLE IP, INC. 2008. All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means without prior written consent of Jones Lang LaSalle. It is based on material that we believe to be reliable. Whilst every effort has been made to ensure its accuracy, we cannot offer any warranty that it contains no factual errors. No liability for negligence or otherwise is assumed by Jones Lang LaSalle for any loss or damage suffered by any party resulting from their use of this publication.

Neil ChegwiddenHead of UK Residential ResearchJones Lang LaSalleLondon+44 (0)20 3147 [email protected](Assisted by Katyayini Krishnamoorthy)

Abhishek Kiran GuptaHead of Operations, India ResearchJones Lang LaSalle Meghraj Mumbai+91 22 6658 [email protected](Assisted by Nitika Masih and Neha Gupta)

James ThomasHead of UK ResidentialJones Lang LaSalleLondon+44 (0)20 7399 [email protected]

Anuj PuriChairman and Country HeadJones Lang LaSalle Meghraj Mumbai+91 22 2482 [email protected]

Simon HalfhideHead of UK New HomesJones Lang LaSalleLondon+44 (0)20 7399 [email protected]

Vincent LottefierChief Executive OfficerJones Lang LaSalle MeghrajGurgaon +91 124 460 [email protected]

Paul M. Guest Head of EMEA Research Jones Lang LaSalleLondon +44 (0)20 3147 1925 [email protected]

Raminder GroverManaging Director Homebay Residential Delhi +91 11 4331 [email protected](A subsidiary of Jones Lang LaSalle Meghraj)

![India-UK Water Security Exchange Initiative - February ... Water Security... · India-UK Water Security Capability Exchange Initiative - February 2016 Visit [2] Introduction The UK](https://static.documents.pub/doc/80x56/5f43e84584bda74483559866/india-uk-water-security-exchange-initiative-february-water-security-india-uk.jpg)