Founded in 1974 and grounded in the MIT tradition of rigorous field-based research, MIT CISR helps executives meet the challenge of leading dynamic, global, and information-intensive organizations. Through research, teaching, and events, the center stimulates interaction among scholars, students, and practitioners.

2017 MIT CISR Research Projects

• What Types of Digital Business Transformations Require Organizational Surgery?

• AutoData 2.0: Answering Hard Questions About Your Customers Using Your Own Data and Comparables

• What Are the Different Types of Digital Ecosystem Drivers… and How to Get There

• Cognitive Computing: Developing the Human/Machine Partnership

• Designing Digital Organizations for Integration, Innovation, and Agility

• Exploring Blockchain• Data Wrapping: How Companies Effectively

Use Data to Create Competitive Products and Services

• Re-thinking Talent Management for Digital• Orchestrating the Digital Workplace

for Business Value • Getting Digital Innovation Right

Aetna, Inc.Akamai TechnologiesAllstate Insurance Co. ANZ Banking Group Ltd.

Founded in 1974 and grounded in the MIT tradition of rigorous field-based research, MIT CISR helps executives meet the challenge of leading dynamic, global, and information-intensive organizations. Through research, teaching, and events, the center stimulates interaction among scholars, students, and practitioners.

2017 MIT CISR Research Projects

• What Types of Digital Business Transformations Require Organizational Surgery?

• AutoData 2.0: Answering Hard Questions About Your Customers Using Your Own Data and Comparables

• What Are the Different Types of Digital Ecosystem Drivers… and How to Get There

• Cognitive Computing: Developing the Human/Machine Partnership

• Designing Digital Organizations for Integration, Innovation, and Agility

• Exploring Blockchain• Data Wrapping: How Companies Effectively

Use Data to Create Competitive Products and Services

• Re-thinking Talent Management for Digital• Orchestrating the Digital Workplace

for Business Value • Getting Digital Innovation Right

Aetna, Inc.Akamai TechnologiesAllstate Insurance Co. ANZ Banking Group Ltd.

Source: MIT CISR 2015 CIO Digital Disruption Survey (N=413 and 2016 interviews) and 2016 company interviews. Customer Experience=effectiveness on customer knowledge+omnichannel capability+customer experience projects+customer experience performance. Operational Efficiency=effectiveness on automation and employee productivity projects+% of core capabilities with APIs+cost of operations performance. Quadrants are splits at 2/3 along each axis.

Future Ready• Both innovative and low cost• Great customer experience• Modular and agile• Data is a strategic asset• Ecosystems ready

Integrated Experience• Customer gets an (simulated)

integrated experience despite complex operations

• Strong design and UX• Rich mobile experience including

purchasing products

Industrialized• Plug and play products/services • Service enabled ‘crown jewels’ • One best way to do each key task• Single source of truth

Silos and Spaghetti• Product driven • Complex landscape of processes,

systems and data• Perform via heroics

TransformedTraditional

The four pathways to Future Ready

Operational EfficiencyImproving operating margin

Cust

omer

Exp

erie

nce

Incr

easin

g N

PS Tran

sfor

med

Trad

ition

al

The lines are the transformation pathways. Explosions are major changes in decision rights and organizational surgery. Quadrants are splits at 2/3 along each axis.Customer Experience= effectiveness on customer knowledge+ omnichannel capability+customer experience projects+customer experience performance.Operational Efficiency =effectiveness on automation and employee productivity projects+% of core capabilities with APIs+cost of operations performance. Sources: Quadrants are derived from data from MIT CISR 2015 CIO Digital Disruption Survey (N=413) and 2016 company interviews.

Future ReadyIntegrated Experience

IndustrializedSilos and Spaghetti

• Customer gets an (simulated) integrated experience despite complex operations

• Strong design and UX• Rich mobile experience including purchasing

products

• Both innovative and low cost• Great customer experience• Modular and agile• Data is a strategic asset• Ecosystems ready

• Product driven • Complex landscape of processes, systems

and data• Perform via heroics

• Plug and play products/services • Service enabled ‘crown jewels’ • One best way to do each key task• Single source of truth

2 4

3

1

TransformedTraditional

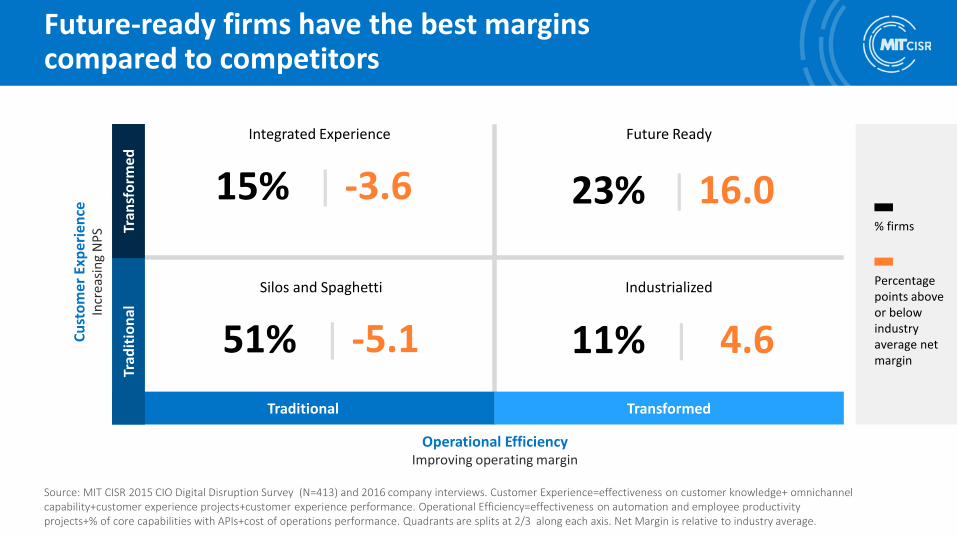

Future-ready firms have the best margins compared to competitors

Operational EfficiencyImproving operating margin

Cust

omer

Exp

erie

nce

Incr

easin

g N

PS

Tran

sfor

med

Trad

ition

al

Source: MIT CISR 2015 CIO Digital Disruption Survey (N=413) and 2016 company interviews. Customer Experience=effectiveness on customer knowledge+ omnichannelcapability+customer experience projects+customer experience performance. Operational Efficiency=effectiveness on automation and employee productivity projects+% of core capabilities with APIs+cost of operations performance. Quadrants are splits at 2/3 along each axis. Net Margin is relative to industry average.

Future ReadyIntegrated Experience

IndustrializedSilos and Spaghetti

15%% firms

Percentage points above or below industry average net margin

| -3.6 23% | 16.0

51% | -5.1 11% | 4.6

Discussion questions

Which pathway(s) are you on and what percent of your transformation is complete?

Please prepare a one-sentence summary

to share.

What is the key lesson you have learnt?

TransformedTraditional

The four pathways to Future Ready

Operational EfficiencyImproving operating margin

Cust

omer

Exp

erie

nce

Incr

easin

g N

PS

Trad

ition

al

The lines are the transformation pathways. Companies are MIT CISR researcher estimates. Source: MIT CISR 2015 & 2017 CIO Digital Disruption Survey (N=800) and 2016/7 company interviews. Customer Experience= effectiveness on customer knowledge+ omnichannel capability+customer experience projects+customer experience performance. Operational Efficiency =effectiveness on automation and employee productivity projects+% of core capabilities with APIs+cost of operations performance. Quadrants are splits at splits at 2/3 along each axis.

Future ReadyIntegrated Experience

IndustrializedSilos and Spaghetti

Tran

sfor

med

All pathways pay off

Source: Source: MIT CISR 2017 Pathways to Digital Business Transformation survey (n=400). Circles represent average performance change relative to competitors above and below 50% complete. Full circle = margin (growth) = 12.7 (15.9) percentage points improvement.

Average margin 66% higher and growth 84% higher comparing firms above and below 50% complete on transformation

Pathway Margin Growth

Employee Experience: Making it Easier to do Complex Work.

Friday, 3 November 2017

LTI@MIT CISR: Effectively Delivering on Digital Transformation

Commission (ASIC)Australian Taxation OfficeAustralianSuperB2W Companhia DigitalBanco do Brasil S.A.Bank of QueenslandBarclaysBBVA Bemis Company, Inc.

Biogen, Inc.BMW GroupBNP ParibasBNY MellonThe Boston Consulting Group, Inc.BT Group plcCanadian Imperial Bank of CommerceCardinal Health, Inc.Caterpillar, Inc.CEMEX Charles Schwab & Co., Inc.Chevron CorporationCHRISTUS HealthCochlear LimitedCommonwealth Bank of AustraliaCPPIBCSBSDBS Bank Ltd.DentaQuestEl Corte InglésEquifaxExxonMobil Global Services CompanyFairfax MediaFerrovial Corporacion, S.A.Fidelity InvestmentsFrieslandCampinaGeneral Electric

Genworth FinancialGlaxoSmithKlineHitachi, Ltd.Howden Joinery Group plcInsurance Australia GroupIron MountainJohnson & Johnson (J&J)LKK Health Products Group Ltd.LPL FinancialMcGraw-Hill EducationNational Australia Bank Ltd.National Disability Insurance SchemeNew Zealand Government—

GCIO OfficeNielsenNomura Holdings, Inc.Nomura Research Institute, Ltd.Nordea BankNorthwestern MutualOCP S.A.Orange S.A.Org. for Economic Co-operation

and Development (OECD)Origin EnergyOwens CorningPepsiCo Inc.Pioneer Natural Resources USA Inc.

Principal Financial GroupProcter & GambleQBE Raytheon CompanyReserve Bank of AustraliaRoyal Bank of CanadaRoyal PhilipsSabadell BankScentre GroupSchindler Digital Business AGSchneider Electric Industries SASStandard Bank GroupState Street Corp.Suncorp GroupSwinburne University of TechnologySydney WaterTD Bank, N.A.Teck Resources LimitedTenet HealthTetra PakTrinity HealthUSAAWestpac Banking CorporationWestRockWorld Bank

Great new CX … but how is the EX?

WORKPLACE SPEED BUMPS…

…destroy value

Employee Experience: The capabilities and behaviors that enable and constrain our people to do their jobs today, and to reimagine their jobs of tomorrow

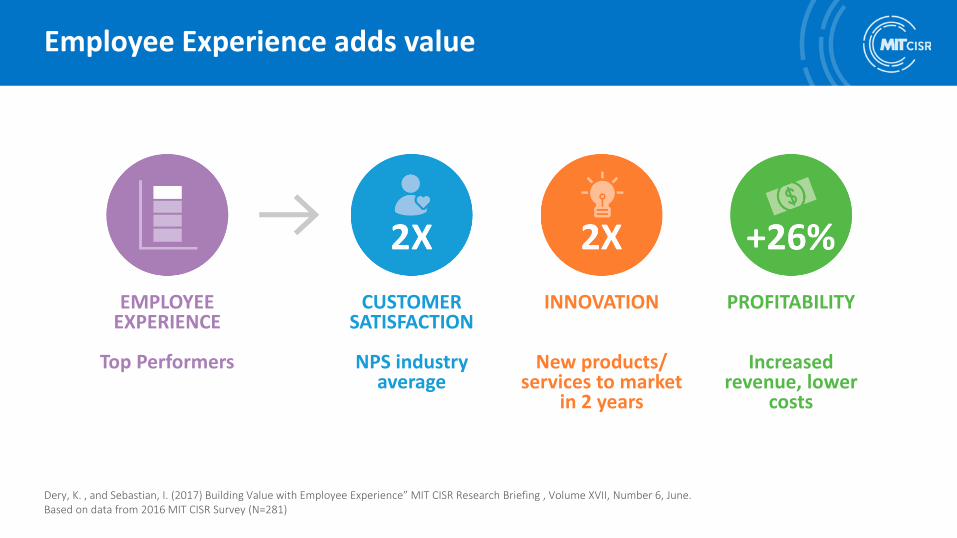

Employee Experience adds value

Dery, K. , and Sebastian, I. (2017) Building Value with Employee Experience” MIT CISR Research Briefing , Volume XVII, Number 6, June. Based on data from 2016 MIT CISR Survey (N=281)

EMPLOYEE EXPERIENCE

Top Performers

CUSTOMERSATISFACTION

NPS industry average

INNOVATION

New products/ services to market

in 2 years

PROFITABILITY

Increased revenue, lower

costs

Employee Experience: two key factors

ADAPTIVEWORK

ENVIRONMENT

COLLECTIVE WORKHABITS

Its not about Brownies in the Break Room

Image by Tastemade.co.uk

DESIGNING NEW SPACES IS

NOT THEANSWER

DIGITALCAPABILITIES

Priorities to build great Employee Experience

RESPONSIVELEADERSHIP

ADAPTIVEWORK

ENVIRONMENT

COLLECTIVE WORKHABITS

Cutting Edge Technology

StartupCulture

Great Placeto Work

DBS’ Digital Future

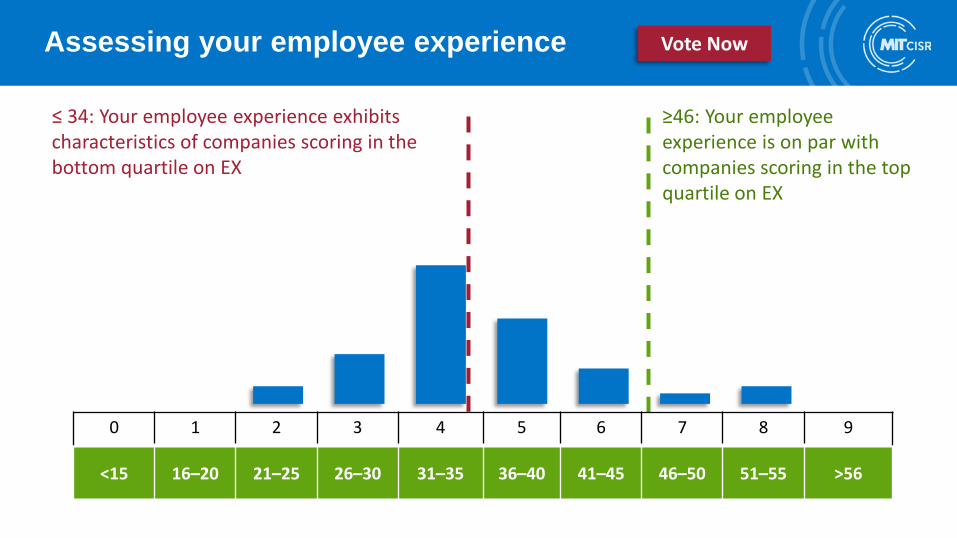

Assessing your employee experience

≥46: Your employee experience is on par with companies scoring in the top quartile on EX

≤ 34: Your employee experience exhibitscharacteristics of companies scoring in the bottom quartile on EX

Commission (ASIC)Australian Taxation OfficeAustralianSuperB2W Companhia DigitalBanco do Brasil S.A.Bank of QueenslandBarclaysBBVA

Bemis Company, Inc.Biogen, Inc.BMW GroupBNP ParibasBNY MellonThe Boston Consulting Group, Inc.BT Group plcCanadian Imperial Bank of CommerceCardinal Health, Inc.Caterpillar, Inc.CEMEX Charles Schwab & Co., Inc.Chevron CorporationCHRISTUS HealthCochlear LimitedCommonwealth Bank of AustraliaCPPIBCSBSDBS Bank Ltd.DentaQuestEl Corte InglésEquifaxExxonMobil Global Services CompanyFairfax MediaFerrovial Corporacion, S.A.Fidelity InvestmentsFrieslandCampina

General ElectricGenworth FinancialGlaxoSmithKlineHitachi, Ltd.Howden Joinery Group plcInsurance Australia GroupIron MountainJohnson & Johnson (J&J)LKK Health Products Group Ltd.LPL FinancialMcGraw-Hill EducationNational Australia Bank Ltd.National Disability Insurance SchemeNew Zealand Government—

GCIO OfficeNielsenNomura Holdings, Inc.Nomura Research Institute, Ltd.Nordea BankNorthwestern MutualOCP S.A.Orange S.A.Org. for Economic Co-operation

and Development (OECD)Origin EnergyOwens CorningPepsiCo Inc.

Pioneer Natural Resources USA Inc.Principal Financial GroupProcter & GambleQBE Raytheon CompanyReserve Bank of AustraliaRoyal Bank of CanadaRoyal PhilipsSabadell BankScentre GroupSchindler Digital Business AGSchneider Electric Industries SASStandard Bank GroupState Street Corp.Suncorp GroupSwinburne University of TechnologySydney WaterTD Bank, N.A.Teck Resources LimitedTenet HealthTetra PakTrinity HealthUSAAWestpac Banking CorporationWestRockWorld Bank

Key findings: • Portfolio allocation (not total spend)

differentiates the most competitive firms• Competitive portfolios consist of four types

of digital innovation

In 5 years, Audi significantly expanded its portfolio of digital innovation1

1. A digital innovation is a new (from the point-of-view of your company) or significantly improved product, service, or process that relies in large parts on digital technologies such as social, mobile and cloud computing, analytics or internet of things technology.Source: MIT CISR Survey on Digital Innovation; data collected from Sept.-Nov. 2016 (N=201)

Digital innovation consists of four types;not all firms are in investing in all four types

Business Operations

Employee Experience

New Business Models

25%30%

25%

10%

10%

(45% do NOT invest in this type)

(25% do NOT invest in this type)

(6% do NOT invest in this type) Customer-facing- New products/services- Customer experience

(13% do NOT invest in this type)

50%

Source: MIT CISR Survey on Digital Innovation; data collected from Sept.-Nov. 2016 (N=201)

Digital innovation is inherently risky

Average Yield Rate: 42%

Average Yield Rate: 29%

Customer-facing

Business Operations

Employee Experience

New Business Models

Average Yield Rate: 49%

Average Yield Rate: 26%

Overall Yield Rate: 45%45% of total spend on digital innovation

leads to measurable positive business value

Source: MIT CISR Survey on Digital Innovation; data collected from Sept.-Nov. 2016 (N=201)

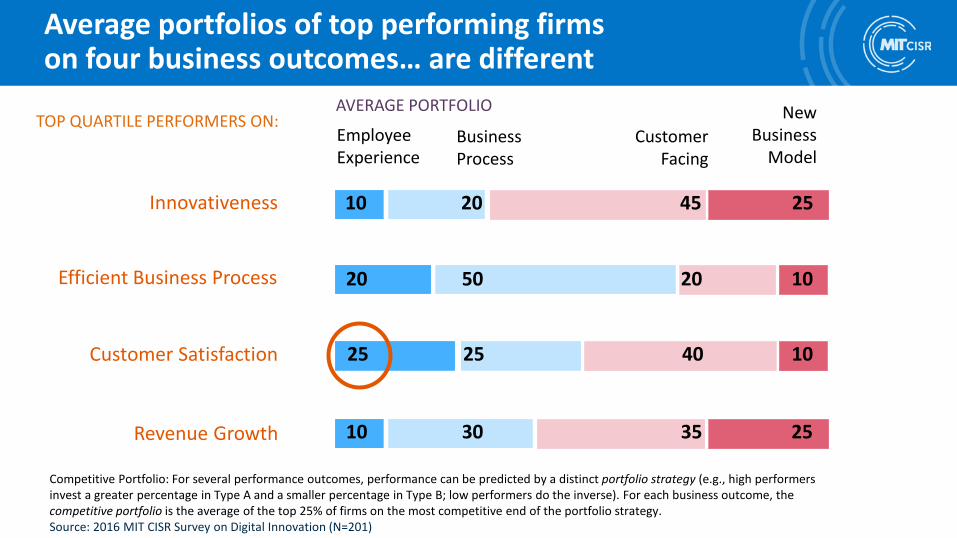

Average portfolios of top performing firms on four business outcomes… are different

NewBusiness

ModelEmployee Experience

BusinessProcess

10 20 2545

Customer Facing

10 30 2535

20 50 1020

25 25 1040

AVERAGE PORTFOLIO

Competitive Portfolio: For several performance outcomes, performance can be predicted by a distinct portfolio strategy (e.g., high performers invest a greater percentage in Type A and a smaller percentage in Type B; low performers do the inverse). For each business outcome, the competitive portfolio is the average of the top 25% of firms on the most competitive end of the portfolio strategy.Source: 2016 MIT CISR Survey on Digital Innovation (N=201)

Customer Satisfaction

Efficient Business Process

Revenue Growth

Innovativeness

TOP QUARTILE PERFORMERS ON:

Top performers in customer satisfaction balancecustomer facing with employee experience

Customer FacingNew web experience

Home delivery

Business ProcessPricing engine

Upgraded platform

Employee ExperienceEmpowering product

teams to innovate smarter

New Business ModelsOnline finance

Results (2017): Sales increased 5% to $15.9BNPS of 81; 13 consecutive years on FORTUNE

magazine’s 100 Best Companies to Work For® list

Use your portfolio as a compass;Use the average portfolio of top performers as your due north

NewBusiness

ModelEmployee Experience

BusinessProcess

10 20 2545

Customer Facing

10 30 2535

20 50 1020

25 25 1040

AVERAGE PORTFOLIO

Competitive Portfolio: For several performance outcomes, performance can be predicted by a distinct portfolio strategy (e.g., high performers invest a greater percentage in Type A and a smaller percentage in Type B; low performers do the inverse). For each business outcome, the competitive portfolio is the average of the top 25% of firms on the most competitive end of the portfolio strategy.Source: 2016 MIT CISR Survey on Digital Innovation (N=201)

Customer Satisfaction

Efficient Business Process

Revenue Growth

Innovativeness

TOP QUARTILE PERFORMERS ON:

? ? ??Your organization’s portfolio

DISCUSSIONWhat is the single most important change that you would advocate for in your organization’s digital innovation portfolio?

Why?

Key findings (second pair): • For both high and low performers, 45% of

investments result in positive business impact• High performers actively manage synergies across

all four types of digital innovations

Top performers do two things differently with digital innovation

Commission (ASIC)Australian Taxation OfficeAustralianSuperB2W Companhia DigitalBanco do Brasil S.A.Bank of QueenslandBarclaysBBVA Bemis Company, Inc.

Biogen, Inc.BMW GroupBNP ParibasBNY MellonThe Boston Consulting Group, Inc.BT Group plcCanadian Imperial Bank of CommerceCardinal Health, Inc.Caterpillar, Inc.CEMEX Charles Schwab & Co., Inc.Chevron CorporationCHRISTUS HealthCochlear LimitedCommonwealth Bank of AustraliaCPPIBCSBSDBS Bank Ltd.DentaQuestEl Corte InglésEquifaxExxonMobil Global Services CompanyFairfax MediaFerrovial Corporacion, S.A.Fidelity InvestmentsFrieslandCampinaGeneral Electric

Genworth FinancialGlaxoSmithKlineHitachi, Ltd.Howden Joinery Group plcInsurance Australia GroupIron MountainJohnson & Johnson (J&J)LKK Health Products Group Ltd.LPL FinancialMcGraw-Hill EducationNational Australia Bank Ltd.National Disability Insurance SchemeNew Zealand Government—

GCIO OfficeNielsenNomura Holdings, Inc.Nomura Research Institute, Ltd.Nordea BankNorthwestern MutualOCP S.A.Orange S.A.Org. for Economic Co-operation

and Development (OECD)Origin EnergyOwens CorningPepsiCo Inc.Pioneer Natural Resources USA Inc.

Principal Financial GroupProcter & GambleQBE Raytheon CompanyReserve Bank of AustraliaRoyal Bank of CanadaSabadell BankScentre GroupSchindler Digital Business AGSchneider Electric Industries SASStandard Bank GroupState Street Corp.Suncorp GroupSwinburne University of TechnologySydney WaterTD Bank, N.A.Teck Resources LimitedTenet HealthTetra PakTrinity HealthUSAAWestpac Banking CorporationWestRockWorld Bank

IoT commitment and new business model change varies within industries

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Financial Services

Manufacturing

Retail

Percent of revenues from products and services introduced in the last 3 years

Perc

ent I

oTCo

mm

itmen

t

Source: MIT CISR 2015 CIO Digital Disruption Survey, N=352

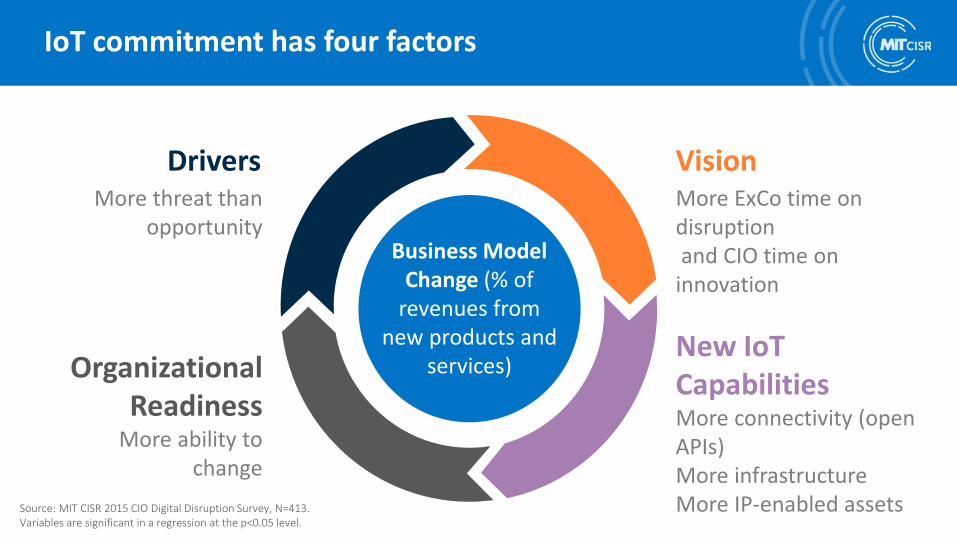

Business Model Change (% of

revenues from new products and

services)

DriversMore threat than

opportunity

Organizational Readiness

More ability to change

VisionMore ExCo time on disruptionand CIO time on

innovation

New IoTCapabilitiesMore connectivity (open APIs)More infrastructureMore IP-enabled assets

IoT commitment has four factors

Source: MIT CISR 2015 CIO Digital Disruption Survey, N=413. Variables are significant in a regression at the p<0.05 level.

Business Model Change

IoT commitment correlates with business model change

Source: MIT CISR 2015 CIO Digital Disruption Survey, N=413..

Drivers

Vision

New IoT Capabilities

Organizational Readiness

Companies in the

Top Quartile of IoTCommitment Generate

50% of their revenues from new products and services introduced in the last three years

Bottom Quartile = 16%

Schindler Holding AG

Founded in 1874 in Switzerland

Manufactures, installs, and maintains escalators, elevators and moving walks

Active in 100 countries with over 58,270 employees

Forbes Magazine lists Schindler as one of the world’s most innovative companies

DRIVERSIncreasingly price sensitive marketConstant innovation needed for growth markets in Asia (60% of new installations)Highly competitive industry with huge market opportunityMaintenance accounts for 50% of industry revenues and about 75% of operating profits

VISIONLeadership through customer service

Outperform competitors in an increasingly price-sensitive market through cost leadership

Digital systems to ensure smooth experience

ORGANIZATIONAL READINESSNew structure with two global businesses: New Installations and Supply Chain and Service Business Incubation as a separate unitIT redesigned with streamlined processesClosed loop service platform with elevators and escalators integrated using the IoT

NEW IoT CAPABILITIES

Sensors on elevators send 200 million messages a day on elevator performance

Business rules engine analyzes sensor data for insightsCustomer web portal and mySchindler app for real-time information